Easily Computed Marginal Likelihoods from Posterior Simulation Using the THAMES Estimator

Abstract

We propose an easily computed estimator of marginal likelihoods from posterior simulation output, via reciprocal importance sampling, combining earlier proposals of DiCiccio et al (1997) and Robert and Wraith (2009). This involves only the unnormalized posterior densities from the sampled parameter values, and does not involve additional simulations beyond the main posterior simulation, or additional complicated calculations. It is unbiased for the reciprocal of the marginal likelihood, consistent, has finite variance, and is asymptotically normal. It involves one user-specified control parameter, and we derive an optimal way of specifying this. We illustrate it with several numerical examples.

1 Introduction

A key quantity in Bayesian model selection is the marginal likelihood, also known as the evidence, the normalizing constant of the posterior density, or the integrated likelihood. Consider a statistical model with parameter vector and data . Let be the usual likelihood, and be the prior distribution of . Then is the marginal likelihood.

The marginal likelihood plays a key role in defining Bayes factors. Consider two models and with marginal likelihoods and . Then the Bayes factor (or ratio of posterior to prior odds) for model against is .

The marginal likelihood is also a critical quantity for Bayesian model averaging (BMA). Consider models, , with prior model probabilities (which add up to 1), and marginal likelihoods . Suppose is a quantity of interest, such as a parameter or a future observation to be predicted. Then the BMA posterior distribution of is

| (1) |

where is the posterior model probability of , which satisfies and . So .

Finally, the most likely model a posteriori is the one that maximizes . Choosing it minimizes the model selection error rate on average over the prior (Jeffreys, 1961). Often the prior over the model space is chosen to be uniform, in which case . In this case, Bayesian model selection by choosing the most likely model a posteriori boils down to choosing the model with the largest , and hence involves only the marginal likelihoods.

Bayesian models are often estimated using Monte Carlo methods in which a sample of values of is simulated from the posterior distribution. The most common class of such methods is Markov chain Monte Carlo (MCMC). Perhaps surprisingly, estimating the marginal likelihood from the output of MCMC and other posterior simulation methods has turned out not to be straightforward. Many different methods have been proposed, and none of them is widely considered to be generally the best. Llorente et al. (2023) provide a comprehensive review of such methods, describing 16 different methods and, remarkably, cite over 20 other review articles!

We seek a method that is accurate, generic and simple for estimating the marginal likelihood from posterior simulation output. We take this to mean that it gives accurate estimates of the marginal likelihood, uses posterior simulation output for just the one model being analyzed, uses only likelihoods and prior densities of the sampled values of , and does not need additional simulations or complicated calculations.

Some well-known methods do not satisfy our desiderata. These include Chib’s method (Chib, 1995), which requires complicated additional calculations, bridge sampling (Meng and Wong, 1996), which requires simulations from two models, importance sampling, which requires additional simulations, and nested sampling (Skilling, 2006), which involves other simulations. They also include the harmonic mean of the likelihoods (Newton and Raftery, 1994), which is unbiased and consistent, but has infinite variance and is unstable, as pointed out by the original authors.

Arguably, the only methods that are accurate, generic and simple for estimating the marginal likelihood from MCMC by our definition are versions of reciprocal importance sampling (RIS) (Gelfand and Dey, 1994). These are based on the identity:

| (2) |

where is a (normalized) probability density function (pdf) over the posterior support. Remarkably, this holds for any pdf . This leads to the estimator

| (3) |

where are simulated from the posterior using MCMC or another method. This estimator has good properties in general, provided that the tails of the distribution are thin enough in all directions. It can be hard to choose so that it both overlaps substantially with the posterior distribution (needed for efficiency) and has thin enough tails, especially in higher dimensions. We propose a choice of that leads to easily computed estimates and is optimal or near optimal in a certain sense.

The paper is organized as follows. In Section 2 we discuss reciprocal importance sampling and its properties. In Section 3 we describe our proposed choice of and derive some of its properties. In Section 4 we give several numerical examples, including a multivariate Gaussian example, a Bayesian regression example, a non-Gaussian case, and a Bayesian hierarchical model. We conclude in Section 5 with a discussion.

2 Reciprocal Importance Sampling

In general, the RIS estimator of the marginal likelihood is defined by Equation (3). This has several good properties. It is unbiased, in the sense that , where the expectation is over the posterior distribution of . It is also strongly simulation-consistent, in the sense that almost surely as .

In addition, the RIS estimator of the reciprocal marginal likelihood, , has finite variance and is asymptotically normally distributed as if the tails of are thin enough. Specifically, this requires that

| (4) |

It is hard to choose so that it both overlaps substantially with the area of the parameter space with high posterior density, which is needed for efficiency, and so that it also has thin enough tails, which is needed for finite variance. The difficulty grows as the dimension increases.

Two choices of in the literature deserve attention. DiCiccio et al. (1997) proposed , where is the posterior mean or mode, and is an estimate of the posterior covariance matrix. This overlaps nicely with , but its tails may not be thin enough when the posterior is asymmetric or the parameter is high-dimensional.

To remedy the problem of the tails possibly being too thick, DiCiccio et al. (1997) proposed truncating it, using instead , a multivariate normal distribution truncated to the set , where

| (5) |

Thus is an ellipsoid with radius and volume

| (6) |

Truncating the distribution ensures that the estimator has finite variance. They found that the truncation improved the performance of the RIS estimator. However, with high-dimensional parameters, the result might be sensitive to the specification of .

Robert and Wraith (2009) proposed setting to be a uniform distribution on the convex hull of simulated MCMC parameters values in the -HPD region, namely the highest posterior density region containing a proportion of the sampled parameter values. They considered the values and 0.25. They applied it to a two-dimensional toy example where it performed well.

However, as far as we know, the method has not yet been fully developed for realistic, higher-dimensional situations. For example, we know of no simple way to compute the volume of the convex hull of a set of points in higher dimensions, which is required for the method in general. It is also not clear how best to choose nor how sensitive the method would be to in higher dimensions. It has been used in a higher-dimensions application by Durmus et al. (2018), but this involved comparing competing models defined on the same parameter space, thus avoiding the need to calculate the volume of , which canceled out in Bayesian model comparisons. Calculating the volume of may be the most difficult part of this method in general.

3 Estimating the marginal likelihood

3.1 Estimating the marginal likelihood with THAMES

We propose combining the proposals of DiCiccio et al. (1997) and Robert and Wraith (2009) to obtain a method that we believe satisfies all our desiderata. We propose specifying to be a uniform distribution, but to be uniform over the set defined in Equation (5), rather than over a convex hull of points. This resolves the problem of computing the volume of , since this is given analytically by Equation (6). If is not a subset of the posterior support, for example if the posterior support is constrained, we adjust the volume of by a simple Monte Carlo approximation.

This yields the estimator

| (7) |

Thus is a truncated harmonic mean of the unnormalized posterior densities, .111Recall that the unstable harmonic mean estimator described by (Newton and Raftery, 1994) was quite different, not being truncated, and being a harmonic mean of the likelihoods rather than the unnormalized posterior density values. We call it the Truncated HArmonic Mean EStimator, or THAMES.

The THAMES, , has several desirable properties. It is simple to compute, involving only the prior and likelihood values of the sampled parameter values. In fact it involves only the product of the prior and likelihood values, namely the unnormalized posterior densities of the sampled parameter values. It is unbiased as an estimator of . It is also simulation-consistent, in the sense that almost surely as , by the strong law of large numbers. Its variance (over simulation from the posterior given the data ) is finite provided that

| (8) |

which will usually hold since is a bounded set in . In fact, it suffices that the likelihood and the prior are continuous with respect to and strictly positive on the closure of . If Equation (8) holds, is asymptotically normal (again as the number of parameter values simulated increases), by the Lindeberg central limit theorem. Note that asymptotic normality holds on the scale of , and not exactly on other scales such as or .

If the posterior simulation method yields independent draws, then Var() can be estimated directly as the empirical variance of the values of , divided by . If MCMC is used, successive simulations from the posterior will in general not be independent. A central limit theorem will still hold, but the variance needs to take account of the serial dependence. This can be done approximately by computing the variance based on serial independence and multiplying it by an estimate of the spectral density of the sequence at zero. For example, if the sequence of values of can be approximated by a first-order autoregressive model with parameter , then this would be approximately . An alternative would be to thin the sequence enough that the resulting subsequence is approximately uncorrelated and then use the variance based on assuming independence. A different approach was taken by Frühwirth-Schnatter (2004).

Note that an approximate normal confidence interval can be obtained for , because that is the scale on which a central limit theorem holds. This could be turned into a confidence interval for by taking the reciprocals of the ends of the normal confidence intervals for ; the resulting confidence interval would not be symmetric. The same could be done for in a similar manner.

3.2 Optimal choice of control parameter,

We now address the question of how to choose the radius of the ellipse that specifies the THAMES in Equation (5). Ignoring serial correlation between simulated values of the parameters, we suggest choosing to minimize the estimated variance of . This could be done empirically by computing for a range of values of , estimating Var() for each value of , and optimizing it over by a grid search or a one-dimensional numerical optimization method.

It is possible to obtain analytic results in the case where the posterior distribution is normal. This is of considerable interest as the posterior distribution is asymptotically normal in many common situations, including some where standard regularity conditions do not hold (Heyde and Johnstone, 1979; Ghosal, 2000; Shen, 2002; Miller, 2021). In this case the THAMES has finite variance since the posterior density, and thus the product of the likelihood and the prior, is continuous with respect to and strictly positive everywhere.

We want to minimize the variance of the THAMES. Due to our assumption of independence of all of the successive MCMC simulations, this variance can be simplified to

| (9) |

Here denotes

| (10) |

the squared coefficient of variation of the first term of the THAMES. Since the variance is a product of and , minimizing with respect to is equivalent to minimizing the variance of the THAMES.

We derive a statement about the optimal choice of by assuming that the posterior covariance matrix and the posterior mean can be provided by a stochastic oracle. The THAMES can then be defined using

| (11) |

Interestingly, in this case the depends neither on the data, , nor on the number of samples from the posterior, . Of course, this is rarely the case in practice. However, plugging in consistent estimators of approximately gives the same results if the number of samples from the posterior is large enough. This is due to the continuous mapping theorem.

The proofs of these results are given in Appendix 1.

Assumption 1

For the following theorems it is assumed that we can ignore serial correlation (i.e. we assume independence of all of the successive MCMC simulations) and that the posterior distribution is normal with mean and a positive definite covariance matrix

. We further assume that the THAMES is defined on .

Theorem 1

There exists a unique radius such that the ellipse with radius minimizes the variance of the THAMES. This value does not depend on the posterior mean or covariance matrix. It satisfies , where the optimal shifting parameter is a sequence for which holds.

Remark 1.

Theorem 2

The following statements hold for the :

-

1.

For any choice of the shifting parameter there exists an such that

(12) for all but finitely many . Thus choosing the radius results in an that is both asymptotically at most twice as large as the optimal and is of order .

-

2.

The following inequality for the can be given for choosing the radius :

(13) (14) This inequality holds for all .

Remark 2.

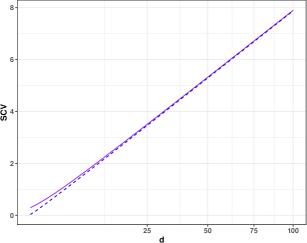

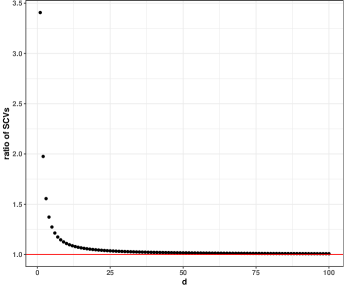

Statement 1 of Theorem 2 shows that is increasing with order as , both in our choice and the optimal choice . This is strongly supported numerically by Figure 2. This also shows that is extremely close to the theoretical lower bound of . Further, any choice of the shifting parameter used to define the radius is asymptotically at most twice as bad as any optimal solution in terms of the . This suggests some robustness of our estimator with respect to the choice of .

Also note that is asymptotically normal. However, it is usually the case that we want to estimate the logarithm of the marginal likelihood. We can do this by using the estimator . The asymptotic behavior of this estimator can be determined by a delta-method approximation:

| (15) |

Thus the roughly reflects the variance of our estimator on the log likelihood scale.

Remark 3.

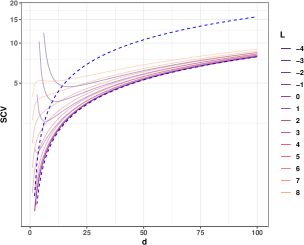

Statement 2 of Theorem 2 gives a very rough theoretical guarantee: For any dimension , the obtained by choosing our recommendation for the radius, , and the obtained by choosing the optimal radius, , can be bounded by an affine transform of . However, our calculations suggest that the in the point has an asymptotically optimal performance.

This is well illustrated numerically by Figure 3, in which is plotted against for several values of . The lower bound from Remark 2 is added. The of our estimator (purple) seems to approach the lower bound, while the resulting from other choices of is larger, but not more than twice as large as this bound, even for small .

So far, we have given results for the idealized situation where the posterior distribution is exactly normal. We now give a result for the much more common and realistic situation where the posterior distribution is only asymptotically normal.

Theorem 3

Let be a sequence of posterior densities with data , posterior covariance matrix , posterior mean and as denoted by . Then, if

| (16) |

uniformly in on all compact subsets of , it is the case that

| (17) |

uniformly in on all compact subsets of . In particular, for any ,

| (18) |

Remark 4.

We have already stated that the normal case is important because the posterior distribution is often asymptotically normal when the size of the data, , is large. Theorem 3 assures that our results still hold in this limiting case, under some assumptions:

If the convergence of the normalized posterior pdf is uniform in (Equation (16)), our statements about the limiting behaviour of the (Theorem 2 and Remarks 2-3) still hold approximately when is large (Equation (17)). If additionally any optimal radius does not converge to zero or infinity, any result about (Theorem 1 and Remark 1) also holds approximately when is large (Equation (18)).

Let denote the Fisher information matrix. Reformulating Equation (16) by replacing by , to which it is asymptotically equivalent, , gives a statement that has been proven under a variety of assumptions (e.g., (Miller, 2021, Theorem 4)), except that in these results the type of convergence is usually not uniform convergence, but a weaker type of convergence, such as convergence in distribution or convergence in total variation.

Additional assumptions can be placed on the pdfs of the sequence of distributions such that convergence in distribution implies uniform convergence of the pdfs. For example, if the pdfs are asymptotically equicontinuous and we have convergence in distribution, the convergence of the pdfs is uniform (Sweeting, 1996, Theorem 1). Note that in this case there is no problem if the parameter space is constrained: Uniform convergence of the pdfs implies that is a subset of the posterior support if is large enough.

Remark 5.

Due to the assumption of normality it is the case that when choosing the optimal radius , the probability of a term of the THAMES in not being set to 0 is equal to

| (19) |

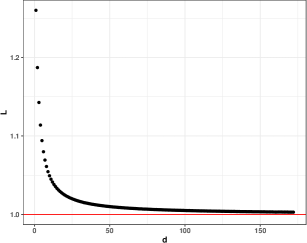

the CDF of the -distribution with degrees of freedom evaluated at . It approaches due to Theorem 1 (compare Figure 4). Thus the algorithm sets about of the highest terms in Equation (7) to 0. This means that for a large number of samples and given the normality assumption, our algorithm is similar to the following method:

Instead of checking whether directly, one can set roughly of the highest terms of the THAMES, the terms not included in the Heighest Posterior Density (HPD) region of size , to 0.

We can check how this method performs in the normal case by setting

| (20) |

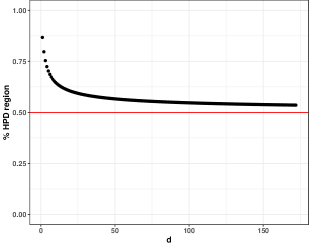

the -quantile of the -distribution with degrees of freedom. This corresponds to setting roughly of the highest terms of the THAMES to 0 and dividing by the volume of the ellipse with radius defined in Equation (20). Figure 5 shows the ratio between the when taking this approach and the SCV when using the optimal radius. The ratio is decreasing to 1, so the heuristic performs quite well, even for small .

Note that the calculations in Equation (19) still hold asymptotically for large even if is not normal, but its elements satisfy a central limit theorem, e.g., if the entries of are independent given the data. This could justify using the heuristic in the case when asymptotic posterior normality does not hold, though the estimator is also necessarily biased in this case, with the bias vanishing as increases.

Remark 6.

It is assumed that the covariance matrix of the posterior distribution is positive definite. This assumption is necessary since otherwise a posterior density with respect to the Lebesgue-measure on would not exist. On the other hand this assumption is not restrictive, since the same estimation procedure can be applied to the lower dimensional subspace of on which a density is defined.

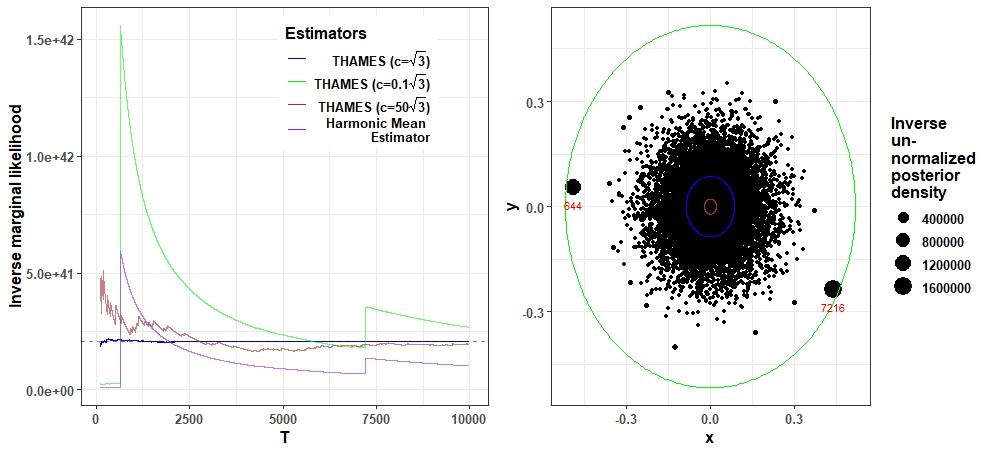

We can illustrate the relationship between the THAMES and the harmonic mean estimator defined by Newton and Raftery (1994) using the toy example from Figure 6. It was calculated using the same model as the one introduced in Section 4.1 with the dimensions of the parameter space , but by setting the data set to to ensure stability of the estimator on the inverse likelihood scale.

The pdf of the Uniform distribution on the ellipse is essentially used as a rejection rule: Values with a very low posterior (and therefore high inverse posterior) are rejected, while high-density values are accepted. A balance between the volume of the ellipse and the percentage of the rejected posterior sample needs to be found to ensure optimal performance. The harmonic mean estimator does not have this rejection rule, so sample points with a high posterior can lead to massive jumps.

3.3 THAMES algorithm

Below is an algorithm for the implementation of THAMES. Procedures for sample splitting, as well as the truncated ellipsoid correction used in the case that the parameter space is constrained have been included. These additions are described in Section 3.3.1 and Section 3.3.2, respectively.

We recommend these additions, but we have also found that in some cases they make almost no difference. For example, sample splitting does not appear to have an impact when the dimension of the parameter space, , is small (Section 4.1 and Section 4.2), while the truncated ellipsoid correction is negligible when the posterior mean is not close to the edge of the posterior support (Section 4.4 and Section 4.3).

3.3.1 Sample splitting

The theoretical guarantees established in Section 3.2 operate under the assumption of an oracle ellipsoid . In particular, this means that the ellipsoid determining the THAMES estimator is defined independently of the posterior samples . In practice, we find that estimating and simultaneously using the same posterior sample can induce bias in when the parameter space is high-dimensional. As such, we implement a sample splitting procedure that involves estimating and using separate posterior draws. Specifically, we first estimate the posterior mean and covariance matrix via the empirical mean and sample covariance using the first posterior samples . Defining as in Equation (5) based on and , we then calculate the THAMES estimator using the last posterior samples .

3.3.2 Correcting for the presence of constrained parameters

Whenever the posterior support of the parameters is not equal to , for example when the parameters are variances or probabilities, it is possible that our choice of in Equation (3), the pdf of the uniform distribution on , is not correctly normalized. This is due to the fact that is not necessarily a subset of the posterior support and thus is not a pdf over this space.

In this case, the expectation of the THAMES is distorted by a multiplicative constant:

| (21) |

where denotes the volume of the intersection between and the posterior support. One way to deal with this problem is to transform the parameter space, e.g., by setting if is a variance parameter. One can then continue with marginal likelihood estimation on , using the transformed prior distribution. In this case, it is of course important to include the Jacobian of the transformation when computing the prior density.

Another way is to adjust for the bias by calculating the ratio of these volumes, , using a simple Monte Carlo approximation: We simulate and calculate

| (22) |

Given , this is an unbiased and consistent estimator of by the law of large numbers. The bias-adjusted THAMES is then

| (23) |

The problem of the parameter space being constrained is common not only for the THAMES, but for reciprocal sampling estimators in general. It has for example been addressed by Hajargasht and Wo’zniak (2018) and Sims et al. (2008). Hajargasht and Wo’zniak (2018) used variational Bayes techniques and showed that these ensure that the support of the chosen is a subset of the posterior support, under mild conditions. Sims et al. (2008) used an ellipsoidal density truncated on a subset of the joint support, , where . Since the support of is equal to the posterior support, our truncation set is similar to the one chosen in Sims et al. (2008), except that we set .

The adjustment is usually very small: The problem arises only when the posterior mean is close enough to the edge of the parameter space. The edge of the parameter space often inherently indicates a priori unlikely values. For this reason it is also rare that the data indicates posterior parameters being close to the edge. Thus the ratio between the volumes is close to one and the variance of is small. In fact, the adjustment did not have any sizeable impact on any of the examples simulated in Section 4. This may not be the case, however, if the actual data generating mechanism are very different from the model being considered. In this case, it can in practice happen that the posterior mean is indeed very close to the edge. We show one example of this in Section 4.3.

In either case we have found that a small number of simulations, around , is usually enough. Confidence intervals obtained from the fact that is asymptotically normal can be used to check whether the variance of is large. In this case should be increased to yield a more precise approximation.

4 Examples

We now describe several simulated and real data examples to assess the THAMES estimator. In Sections 4.1, 4.2, and 4.3, three statistical models, for which exact expressions of the marginal likelihood are derived, are considered. This allows us to compare the THAMES estimated values to the exact ones for evaluation. In Section 4.4, we consider a real data example with models for which no analytical expressions for the marginal likelihood are available and where there is a need for reliable estimators. We compare our estimator to bridge sampling, which is more complicated than THAMES but is known to have perform well (Meng and Wong, 1996; Gronau et al., 2020).

4.1 Multivariate Gaussian data

We first consider the case where data are drawn independently from a multivariate normal distribution:

along with a prior distribution on the mean vector :

with . As shown in the Appendix, the posterior distribution of the mean vector given the data is given by:

| (24) |

where , , and .

Interestingly, while the observations are independent given the vector , they are not independent marginally, and the marginal likelihood does not take a product form over marginal terms in . Conversely, thanks to the isotropic Gaussian prior distribution which is considered for , where the are all iid, not only are the vectors independent given , they are also independent marginally. From such a key property, we prove in Proposition 2 of the Appendix that the marginal likelihood of the model can be written analytically as:

| (25) |

where is the vector of all observations for variable such that and is the vector of 1 in .

4.1.1 Assessing the precision of the THAMES estimator as a function of

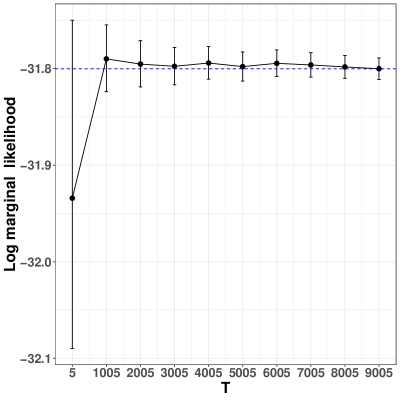

We first considered the univariate case . Thus, we simulated a unique sample of size with . Moreover, we set , for illustration. Note that other choices for led to similar conclusions regarding the quality of the estimation. Figure 8 shows the THAMES estimated values for the log marginal likelihood, for samples of the posterior distribution (Equation (24)). Confidence intervals as well as the exact value of the log marginal likelihood computed using Equation (25) are also reported. It can be seen that the estimate converges to the correct value and that the confidence intervals contain the true value in all cases, even for only.

4.1.2 Assessing the precision of the THAMES estimator as a function of

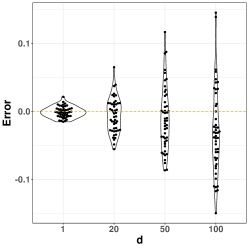

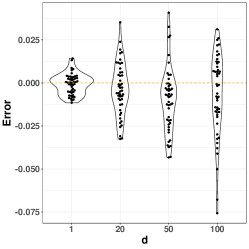

For this second set of experiments, we considered different values of , and aimed at testing the robustness of the THAMES approach on multiple data sets, with increasing dimensionality. Thus, for each , we generated 50 different data sets of size using the multivariate Gaussian model. In practice, we set the true value of to , for all its components. Again, the prior parameter was set to and similar conclusions were drawn for other values. Moreover, the value of was set to for all the experiments.

We also used this example to assess sample splitting procedure for the posterior samples, as proposed in Section 3.3.1. The results are given in Figure 8. On the figure on the left, where no sample splitting of the posterior samples is employed to compute THAMES, we observe that a bias appears as the dimensionality of the model considered increases, and the log marginal likelihood tends to be slightly underestimated. As illustrated by the figure on the right hand side, this bias is primarily related to the estimation of the posterior covariance matrix, and not to the THAMES estimation itself. Indeed, focusing on this figure on the right, we note that if the exact expression of the posterior covariance matrix given in Equation (24) is used to compute THAMES, then while the variance of the estimator increases with , we do not observe any bias. Crucially, if the sample splitting of the posterior samples is employed to compute THAMES, then again, we do not observe any bias.

Overall, we found that the sample splitting procedure of the posterior samples was not necessary to compute THAMES for low values of . The estimated values are indeed particularly close to the exact ones. However, for large values of , we recommend using the sample splitting procedure to remove the bias.

|

|

|

4.2 Bayesian Regression

We consider a data set to train a linear regression model of the form

Note that we assume the noise variance to be known for the sake of the illustration. Indeed, as the goal in this section is to assess the quality of the estimator we propose, an exact expression for the marginal likelihood is needed, for comparison. If a prior distribution such as a gamma distribution for instance is chosen for , then, while the methodology we propose in this paper can be used directly for estimation, no analytical expression for is not available, making the assessment infeasible.

Denoting , the vector of target variables , and the design matrix where the input vectors are stacked as row vectors, the linear regression model becomes:

We rely on a centered isotropic Gaussian prior distribution for the regression vector :

with . This framework was largely covered by the PhD thesis of D. MacKay through the development of the so called evidence procedure (MacKay, 1992). In this context, the posterior distribution over , given the training data set is tractable:

with

and

where the observed vector of target variables associated to . Moreover, the marginal likelihood also has an analytical expression:

The two corresponding proofs are given in Proposition 3 of the Appendix.

The data for this example are described by Hastie et al. (2009) and come from a study by Stamey et al. (1989). They examined the correlation between the level of prostate-specific antigen (lpsa) and eight clinical measures in men who were about to receive a radical prostatectomy. The variables are log cancer volume (lcavol), log prostate weight (lweight), age, log of the amount of benign prostatic hyperplasia (lbph), seminal vesicle invasion (svi), log of capsular penetration (lcp), Gleason score (gleason), and percent of Gleason scores 4 or 5 (pgg45). The target variable is the level of prostate-specific antigen (lpsa). Note that in our experiments, we set , but could also be estimated with the evidence procedure. Other choices for led to similar conclusions regarding the quality of the estimation.

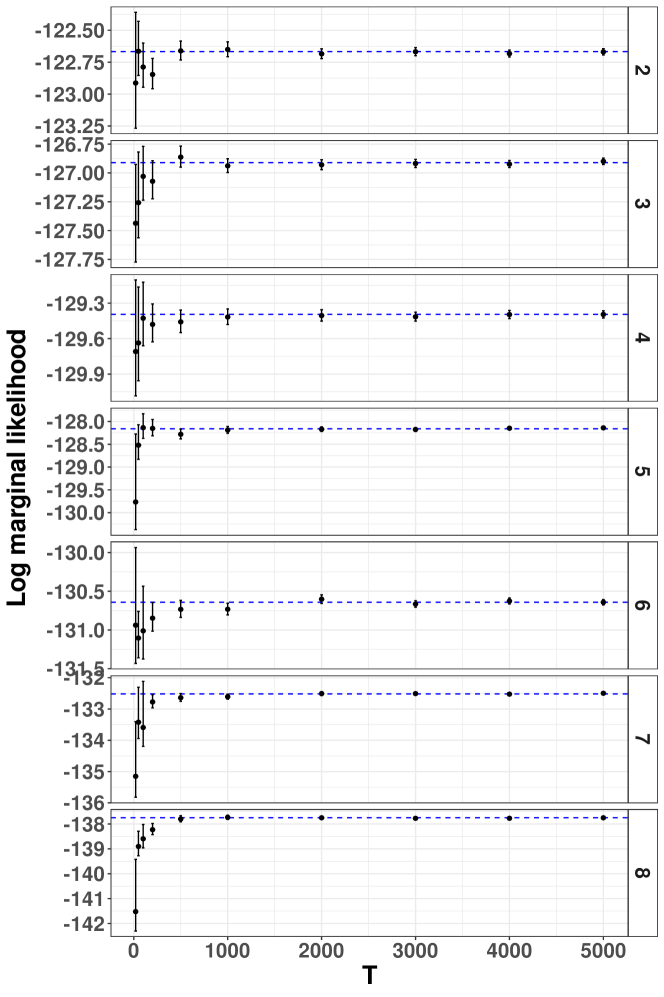

Seven different regression models , , , , each with a different number of selected variables, ranging from 2 to 8, are considered for illustration. The variables are added in the order given above. Thus, is made of variables lcavol and lweight, while Model considers the variables lcavol, lweight, as well as age for prediction. Finally, model takes all input variables into account. Figure 9 shows the THAMES of the log marginal likelihood for different number of samples from the posterior distribution in , for the different models, as well as the approximate confidence intervals. We did not use sample splitting to estimate in this example, as the dimension of the parameter vector was relatively low.

There was no noticeable bias in the results. Indeed, it can be seen that the estimators converge rapidly to the correct value and that the intervals cover the correct values in most cases, even when the number of samples used is small, for all models investigated. For all models, the THAMES estimator is particularly accurate for 1000 samples of the posterior only. While the main goal of this section is to illustrate the precision of our estimation strategy for a series of models, we can also report that the model with the highest marginal likelihood, for this data set, is Model . In other words, the variables lcavol and lweight are seen as key for the prediction of the level of prostate-specific antigen.

4.3 Dirichlet-multinomial model

Extensions of the Dirichlet-multinomial model are widely used in the context of topic modelling (see, e.g., Blei et al. (2003)) The expression for the marginal likelihood in this model is known, as in the previous two sections. This allows us to assess the performance of our estimator in another simulation study, in a non-Gaussian context.

A simulation study in this setting is useful for two reasons: First, this is a high-dimensional setting in which the posterior distribution of the parameters is highly non-Gaussian. In fact the parameter space is bounded. This allows us to assess how well the THAMES performs in a very different setting and also lets us assess how much of an impact the correction for a bounded parameter space from Section 3.3.2 has.

Second, there do exist similar models to this one for which the marginal likelihood is not tractable, e.g. Blei and Lafferty (2007)). These models are therefore a possible application of the THAMES. The simulation study might give an idea of how well the THAMES would perform in these applications.

The Dirichlet-multinomial model is defined as follows: Each data point is drawn from a multinomial distribution given a Dirichlet-distributed random variable :

Here, is positive and -dimensional with components summing to 1. The covariance matrix of is thus necessarily singular. As noted in Remark 6, the THAMES needs to be used on posterior simulations from the subspace of on which a density is defined. In this case, this is . The prior density is thus

The posterior support is the -dimensional simplex

The posterior distrib ution given the data is tractable:

The marginal likelihood is thus also tractable, using Bayes’s theorem.

4.3.1 Results

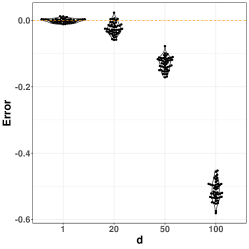

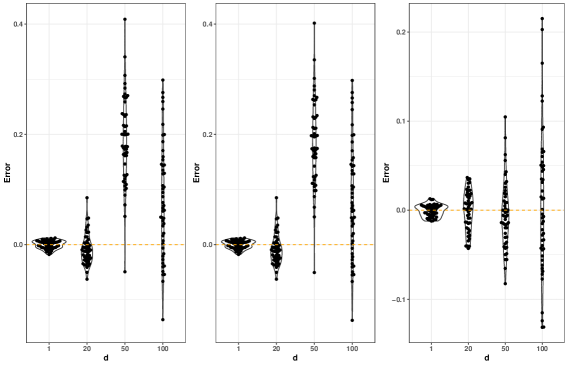

The marginal likelihood was estimated in the setting with varying between 1,20, 50 and 100. The quantities and were intentionally chosen to be large, since this model has very high dimensional applications. For example, Blei et al. (2003) used a data set with 8000 documents, words and used up to different topics.

We considered two different approaches for the simulation procedure. In the first, a fixed value of was determined using the Dirichlet distribution with parameters for each value of . For each , 50 data sets were simulated using the multinomial distribution with parameters and . The second approach was to not simulate , but fix it to be the probability vector of the uniform distribution, i.e. and repeat the same simulation procedure just described. The results of both of these approaches are shown in Figure 10. The posterior sample was split: the first parameter values simulated from the posterior were used to estimate the covariance matrix and mean, while the remaining values were used to calculate the THAMES.

Overall, the THAMES performed well in all the experiments, and the impact of the bounded parameter correction was small in this case. The performance of the THAMES in the second setting, with fixed , was noticeably better than its performance in the first, with stochastic . In fact, the third plot in Figure 10 is quite similar to the third plot in Figure 8, which shows the Gaussian case. Presumably this can be explained by Theorem 3: it seems that the size of the data set is large enough that the posterior is well approximated by a multivariate Gaussian, for which the parameter of the THAMES is optimal.

The results from the approach in which was simulated from the Dirichlet (the left plot in Figure 10) are less symmetric and show larger errors on average than the results obtained in which was fixed to be the probability vector of the discrete uniform. This is probably because probability vectors simulated from the Dirichlet are more skewed, with some of their elements being close to the edge of the parameter space. For this reason convergence of the posterior to the multivariate Gaussian presumably takes longer. The results are still similar to those the baseline setting in which was fixed: the errors increase with the number of dimensions, roughly at rate , as predicted by Theorem 2.

As mentioned, probability vectors simulated from the Dirichlet can often have elements close to the edge of the parameter space. The bias correction from Section 3.3.2 was thus used in the first approach, although this correction only had a small impact: The values of the log marginal likelihood estimation where changed by at most 0.007 (plot 2 in Figure 10). The Bias-correction was 0 each time for the base-line approach. This makes sense, as none of the elements of the probability vector of the discrete uniform are close to the boundary of the simplex.

We have simulated the THAMES in a high dimensional, non-Gaussian setting. Still, the results obtained showed similarity to those obtained in another setting in which the posterior was exactly Gaussian. This shows a real strength of the THAMES: While a large sample size hugely increases the size of the marginal likelihood and could thus be thought to increase the difficulty of the estimation procedure, it has in our experience improved the performance of the THAMES. The THAMES could thus be a candidate for very high dimensional estimation procedures in which both the dimension of the parameter space and the sample size are large.

4.4 Mixed effects model

4.4.1 Netherlands schools data

To demonstrate the performance of THAMES on a random effects model, we consider the Netherlands (NL) schools dataset of Snijders and Bosker (1999). For our purposes, the data consist of language test scores of 2,287 eighth-grade pupils from 133 classes (in 131 schools) in the Netherlands. We denote by the language test score of pupil in class , where with and with the size of class . Let denote the full sample size.

We aim to determine if there is clustering of language test scores by class, with some classes performing significantly better than others on average. To do this, we fit both a simple mean model (which treats test scores of students in the same class as independent) and a random intercept model (which accounts for correlation of test scores within each class) to the data. The former (null) model posits that all classes perform the same, on average, while the latter (alternative) model allows for variation in performance at the class level. We estimate the log marginal likelihoods for the two models, and , respectively, using THAMES and bridge sampling (Gronau et al., 2020) for comparison. With estimates of and , we estimate the log Bayes factor to conduct a Bayesian hypothesis test of versus . Note that posterior simulation and marginal likelihood calculation are not analytically tractable for this model. As such, the use of approximate posterior sampling (e.g., via MCMC) and marginal likelihood estimation (e.g., via THAMES) is required.

4.4.2 Linear model (LM)

We first consider a simple mean model (denoted LM), which posits that

The fixed hyperparameters are specified so as to ensure that the prior distribution is dispersed relative to the likelihood, but on the same scale, as

The hyperparameters are chosen so that the prior mean of the precision equals . The set of parameters to be estimated in this model has dimension .

4.4.3 Full linear mixed model (full LMM)

We consider the random intercept model (denoted full LMM):

Here are as above and we specify

where is the sample mean for class . The hyperparameters are chosen so that the prior mean of the precision equals . The set of parameters to be estimated in this model has dimension .

4.4.4 Reduced linear mixed model (reduced LMM)

Note that the intercept parameters of the full LMM are not identifiable, as there is give-and-take in estimating the grand mean and the random intercepts . By absorbing into the error term structure , we can specify an equivalent model (having the same marginal likelihood) with identifiable parameters . Mathematically, this amounts to marginalizing out of the model. The model (denoted reduced LMM) is given by

Here are as above.

4.4.5 Results

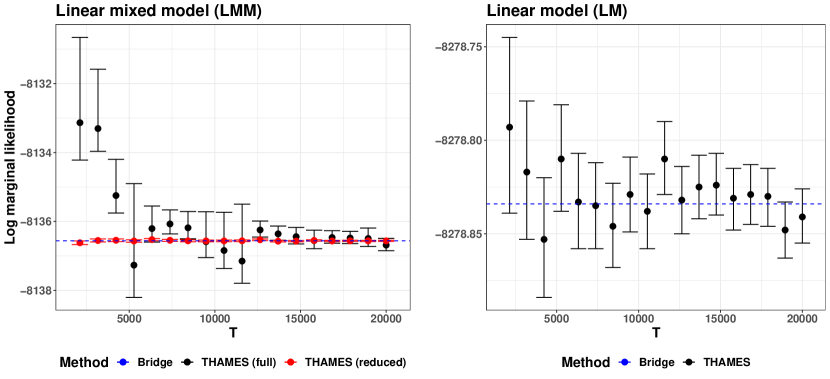

Figure 11 shows the log marginal likelihood of the NL schools data for each model as estimated by THAMES with approximate 95% confidence intervals, as a function of the number of posterior MCMC draws. In the left panel, the bridge sampling estimate of the log marginal likelihood for the reduced LMM based on 20,000 posterior samples is plotted in black (Gronau et al., 2020). In the right panel, the bridge sampling estimate for the LM with 20,000 posterior samples is shown. Bridge sampling is a popular state-of-the-art method to estimate log marginal likelihoods from posterior MCMC samples, which is substantially more complicated computationally than the THAMES. MCMC sampling is carried out in R using Stan (R Core Team, 2023; Stan Development Team, 2022). We use values of the posterior sample size evenly spaced between 2,000 and 20,000. For each , we run 4 chains in parallel for iterations and burn the first , yielding MCMC samples from each of the 4 chains.

THAMES provides unbiased estimates of the log marginal likelihood with greater precision as the posterior sample size grows. As we would expect, THAMES converges much faster for the LM (with ) and the reduced LMM (with ) as compared to the full LMM (with ), although the estimates of the reduced and full LMM converge to the same value. While the posterior support of this model is constrained due to the variance parameters , we found that the truncation correction defined in Section 3.3.2 had no impact on the results. For a given posterior sample size, we find that bridge sampling generally produces more precise estimates than THAMES. However, THAMES has the advantage of being much simpler to implement in practice.

Using the THAMES estimates of the log marginal likelihoods for the LM () and the (reduced) LMM () with 20,000 posterior draws, the log Bayes factor () is estimated as

which indicates decisive evidence in favor of the random intercept model (Kass and Raftery, 1995).

5 Discussion

We have proposed an estimator of the reciprocal of the marginal likelihood, called THAMES, which is simple to compute, unbiased, consistent, has finite variance and is asymptotically normal, with available confidence intervals. It is a version of reciprocal importance sampling. The estimator has one user-specified control parameter, and we have derived an optimal value for this in the situation where the posterior distribution is normal, which is of great interest because posterior distributions are asymptotically normal in many situations. We have carried out several numerical experiments in which the estimator performs well.

The THAMES relies on estimating the posterior covariance matrix and mean. In our experience it is important that the estimator chosen for the covariance matrix be accurate for estimating each matrix entry. Elementwise accuracy appears to be important because the covariance matrix is used to precisely define a quadratic inequality. For example, using a Shrinkage estimator for the covariance matrix, which can produce large errors in a small proportion of its elements, has in our experience degraded the performance of the THAMES in some situations.

One possible alternative to covariance matrix estimation would be to select a minimum-volume covering ellipse which includes a certain percentage of those points of the posterior sample which have the largest value with respect to the (unnormalized) posterior density evaluated at those points. This would ensure that an HPD-region is well approximated, independent of the underlying posterior distribution. Determining a minimum-volume covering ellipse given a set of points can be difficult computationally, but this problem has been addressed by a vast amount of literature in many different settings and could possibly be adapted to the THAMES.

Acknowledgements:

Irons’s research was supported by a Shanahan Endowment Fellowship and a Eunice Kennedy Shriver National Institute of Child Health and Human Development training grant, T32 HD101442-01, to the Center for Studies in Demography & Ecology at the University of Washington. Raftery’s research was supported by NIH grant R01 HD070936 from the Eunice Kennedy Shriver National Institute of Child Health and Human Development (NICHD), by the Fondation des Sciences Mathématiques de Paris (FSMP), and by Université Paris-Cité.

References

- Blei and Lafferty (2007) Blei, D. M. and J. D. Lafferty (2007). A correlated topic model of science. Annals of Applied Statistics 1(1), 17–35.

- Blei et al. (2003) Blei, D. M., A. Y. Ng, and M. I. Jordan (2003). Latent dirichlet allocation. Journal of Machine Learning Research 3, 993–1022.

- Chib (1995) Chib, S. (1995). Marginal likelihood from the Gibbs output. Journal of the American Statistical Association 90, 1313–1321.

- DiCiccio et al. (1997) DiCiccio, T. J., R. E. Kass, A. E. Raftery, and L. Wasserman (1997). Computing Bayes factors by combining simulation and asymptotic approximations. Journal of the American Statistical Association 92, 903–915.

- Durmus et al. (2018) Durmus, A., E. Moulines, and M. Pereyra (2018). Efficient Bayesian computation by proximal Markov chain Monte Carlo: when Langevin meets Moreau. SIAM Journal on Imaging Sciences 11, 473–506.

- Frühwirth-Schnatter (2004) Frühwirth-Schnatter, S. (2004). Estimating marginal likelihoods for mixture and Markov switching models using bridge sampling techniques. Econometrics Journal 7, 143–167.

- Gelfand and Dey (1994) Gelfand, A. E. and D. K. Dey (1994). Bayesian model choice: asymptotics and exact calculations. Journal of the Royal Statistical Society: Series B (Methodological) 56, 501–514.

- Ghosal (2000) Ghosal, S. (2000). Asymptotic normality of posterior distributions for exponential families when the number of parameters tends to infinity. Journal of Multivariate Analysis 74, 49–68.

- Gronau et al. (2020) Gronau, Q. F., H. Singmann, and E.-J. Wagenmakers (2020). bridgesampling: An R package for estimating normalizing constants. Journal of Statistical Software 92(10), 1–29.

- Hajargasht and Wo’zniak (2018) Hajargasht, G. and T. Wo’zniak (2018). Accurate computation of marginal data densities using variational bayes. arXiv: Applications. https://arxiv.org/pdf/1805.10036.pdf.

- Hastie et al. (2009) Hastie, T., R. Tibshirani, and J. H. Friedman (2009). The Elements of Statistical Learning: Data Mining, Inference, and Prediction (2nd ed.). Springer.

- Heyde and Johnstone (1979) Heyde, C. C. and I. M. Johnstone (1979). On asymptotic posterior normality for stochastic processes. Journal of the Royal Statistical Society: Series B (Methodological) 41, 184–189.

- Jeffreys (1961) Jeffreys, H. (1961). Theory of Probability (3rd ed.). Oxford, U.K.: Oxford University Press.

- Kass and Raftery (1995) Kass, R. E. and A. E. Raftery (1995). Bayes factors. Journal of the American Statistical Association 90(430), 773–795.

- Llorente et al. (2023) Llorente, F., L. Martino, D. Delgado, and J. Lopez-Santiago (2023). Marginal likelihood computation for model selection and hypothesis testing: An extensive review. SIAM Review 65, 3–58.

- MacKay (1992) MacKay, D. J. (1992). Bayesian interpolation. Neural computation 4, 415–447.

- Meng and Wong (1996) Meng, X.-L. and W. H. Wong (1996). Simulating ratios of normalizing constants via a simple identity: A theoretical exploration. Statistica Sinica 6, 831–860.

- Miller (2021) Miller, J. W. (2021). Asymptotic normality, concentration, and coverage of generalized posteriors. The Journal of Machine Learning Research 22, 7598–7650.

- Newton and Raftery (1994) Newton, M. A. and A. E. Raftery (1994). Approximate Bayesian inference with the weighted likelihood bootstrap. Journal of the Royal Statistical Society: Series B (Methodological) 56, 3–26.

- (20) Olver, F. W. J., A. B. Olde Daalhuis, D. W. Lozier, B. I. Schneider, R. F. Boisvert, C. W. Clark, B. R. Miller, B. V. Saunders, H. S. Cohl, M. A. McClain, and eds. NIST digital library of mathematical functions. https://dlmf.nist.gov/, Release 1.1.9 of 2023-03-15.

- R Core Team (2023) R Core Team (2023). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing.

- Robert and Wraith (2009) Robert, C. P. and D. Wraith (2009). Computational methods for Bayesian model choice. In AIP conference proceedings, Volume 1193, pp. 251–262. American Institute of Physics.

- Shen (2002) Shen, X. (2002). Asymptotic normality of semiparametric and nonparametric posterior distributions. Journal of the American Statistical Association 97, 222–235.

- Sims et al. (2008) Sims, C. A., D. F. Waggoner, and T. Zha (2008). Methods for inference in large multiple-equation Markov-switching models. Journal of Econometrics 146(2), 255–274.

- Skilling (2006) Skilling, J. (2006). Nested sampling for general Bayesian computation. Bayesian Analysis 1, 833–859.

- Snijders and Bosker (1999) Snijders, T. A. B. and R. J. Bosker (1999). Multilevel Analysis. An Introduction to Basic and Advanced Multilevel Modelling. Sage.

- Stamey et al. (1989) Stamey, T., J. Kabalin, J. McNeal, I. Johnstone, F. Freiha, E. Redwine, and N. Yang (1989). Prostate specific antigen in the diagnosis and treatment of adenocarcinoma of the prostate II radical prostatectomy treated patients. Journal of Urology 16, 1076––1083.

- Stan Development Team (2022) Stan Development Team (2022). RStan: the R interface to Stan. R package version 2.21.7.

- Sweeting (1996) Sweeting, T. (1996). On a Converse to Scheffe’s Theorem. The Annals of Statistics 14, 1252–1256.

Appendix 1: Proofs of Theorems 1, 2 and 3

The first two theorems will be proven using two lemmas and one proposition. Theorem 3 is proven using Theorem 1, while Theorem 1 is proven using Theorem 2 and Lemma 1. Theorem 2 is proven using Proposition 1, while Proposition 1 is proven using Lemma 1 and Lemma 2.

Lemma 1 gives the first basic results and an explicit expression of the . Lemma 2 can be used to simplify this expression and give an exact upper and an exact lower bound on the . This is shown in Proposition 1. These exact bounds are simplified to their limiting solutions to prove Theorem 2. It is further shown that these bounds lead to a contradiction if the limit of is not 1, proving Theorem 1. Finally, the fact that is unique (Theorem 1) is used to prove Theorem 3.

Lemma 1

Let denote the mean and the covariance matrix of the posterior distribution, which is multivariate normal. There exists a sphere centered in with radius such that minimizes the variance of the THAMES, i.e. any other measurable set results in a larger or equal variance. Choosing the set for the THAMES gives the corresponding

| (26) |

It has a unique minimal point and its first derivative with respect to is

| (27) |

where an explicit expression of is given by

| (28) |

with the double factorial denoting

for any and

Note that does not depend on the posterior mean or the posterior covariance matrix . Thus any optimal choice of is going to be optimal for any normal posterior distribution with positive definite covariance matrix.

Proof.

Let us calculate the following quantity in order to minimize it according to the shape of :

Since is the density of a normal distribution with mean an positive definite covariance matrix it follows that

where denotes the translate of by and the rescaling of by . From this it immediately follows that there exists a such that is optimal.

Proving that is optimal

Let be a measurable set with volume . We can choose such that

This directly implies . It follows that

This is due to the fact that Using this and the fact that one can similarly conclude

It follows that for any measurable set a exists such that the (and thus the variance) of the THAMES is strictly lower when choosing to be the uniform distribution on instead of .

Calculating an exact expression for the SCV

Let us remind that the area of a -sphere of radius is and its volume is . Using the spherical coordinates, we get that defined as follows for :

First, the limiting behaviour of w.r.t. can be observed by applying l’Hôpital’s rule. We have

and

Since is continuous w.r.t. it follows that a global minimum exists and that this minimum can be found by setting the first derivative of w.r.t. to 0.

Let us now take the derivative of w.r.t. :

The first order condition is thus

| (29) |

or equivalently

| (30) |

Let be a point that fulfills Equation (30). We plug into the second order condition:

This is the case if, and only if . Further any local maximum point needs to fulfill . Since any two local minima need to have at least 1 local maximum in between them, it follows that there exists only one minimum point, . Still, the explicit solution of needs to be verified.

For ,

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) |

with and .

To verify the explicit solution of , it suffices to show that it fulfills the recursive relation (34) for and that the initial value conditions for hold.

This is indeed the case, as this expression for fulfills the initial value conditions by definition and

∎

Lemma 2

The analytical solution of (Equation (28)) can be simplified to

| (35) |

Lemma 2 provides a closed form expression of for both the even and uneven case, but is likely only of theoretical interest, as it is not clear how this sum should be implemented numerically.

Proof.

We are trying to show that

This simplification is a consequence of the fact that the sum is a Taylor series of in both the even and the uneven case.

Case 1: is even

We make use of the following identity:

Thus for even

Case 2: is uneven

We make use of the following identity:

Thus for odd

where we used the Cauchy product rule and a specific solution for the gaussian hypergeometric function evaluated at . By (Olver et al.,§15.4(i), Equation 15.2.4)

Further by (Olver et al., §15.4(i), Equation 15.4.20)

∎

It turns out that we can use this lemma to construct exact upper and lower bounds on the .

Proposition 1

For any which can depend on

| (36) |

and for

| (37) |

For , there exists a function such that

and inequality (37) holds for in .

Proof.

We know that the minimum point fulfills the first order condition (Equation (29)):

This information can immediately be used to get a lower bound on in . Let . By Equation (30)

It follows that

For this we used the fact that the function

is minimized w.r.t. if, and only if

Note that this is really a global minimum as the derivative changes signs at . Since is a minimal point, this gives a real lower bound for any choice of .

Determining the upper bound is similar, only that we now want to show that in the point the ratio which we used is bounded:

Due to Lemma 2 this is equivalent to

The sum is absolutely convergent, as it is a power series with infinite convergence radius (see the proof of Lemma 2: Taylor series are power series, and in our case we know that these specific Taylor series converge everywhere). It follows that we are allowed to change the order of summation. It follows that, if ,

as this implies that any component of the sum is non-negative. No restrictions on are necessary in the limiting case, since for the first finitely many negative expressions

is then defined as the , but with these first finitely many components set to 0.

This gives

if , so in particular if . On the other hand the inequality holds for for any . ∎

Calculating the asymptotic behaviour of these bounds gives the proof of Theorem 2:

Proof of Theorem 2.

We are first going to prove the limiting behaviour of the w.r.t. and then use this result to provide a proof of the limiting behaviour of the optimal value .

Applying Stirling’s formula gives

The derivative of the logarithm of the function

is

and its second derivative is

Thus the first derivative is decreasing towards its limit, 0, which implies that the first derivative is strictly greater than 0. It follows that this function is strictly increasing in with supremum and minimum

An exact inequality is thus given by

Analogously, applying the other direction of Stirling’s formula

with an exact inequality given by

One can analogously apply the asymptotic Stirling’s formula for :

| (38) | ||||

| (39) | ||||

| (40) |

Proof of Theorem 1.

First of all, the fact that with radius minimizes the and is a result of Lemma 1.

To prove that , we show that

and

Note that

so any for which this expression diverges can be excluded. Further the function

is decreasing if and increasing if . Both of these facts follow from previous statements.

Suppose that there exists an such that

This implies that

for infinitely many . For these it holds that

This sequence diverges because of the well known inequality if . It follows that

If on the other hand

we have that

for infinitely many and by the same argument

we have a contradiction. So

In total

∎

Proof of Theorem 3.

Let

be the set used for the THAMES when applying it to estimate the marginal corresponding to . The corresponding is then defined by

Rescaling and shifting to the sphere

gives

Let denote the supremum norm on the set . By uniform convergence on the compact set

since uniform convergence means convergence in the supremum norm and since the two reciprocals are uniformly bounded away from 0 on by the same reason.

Let be compact. is maximized by and the supremum is maximized by . Denoting the resulting spheres by respectively, gives

for all . Thus the convergence is uniform on all compact subsets of .

Let us fix and restrict to an interval . Then converges uniformly in on . Further, is continuous in since an integral over an absolutely continuous function is continuous. Uniform convergence of continuous functions implies epigraphical convergence (Rockafellar&2009, Proposition 7.15).

is the unique minimal point of the limiting function and the level sets are bounded by definition. The statement in Theorem 3 follows by (Rockafellar&2009, Theorem 7.33).

∎

Appendix 2: Derivations of Analytical Expressions for the Examples

After the following proposition, all proofs for the multivariate Gaussian model of Section 4.1 are provided.

Proposition 2

If , are drawn independently from the multivariate normal distribution:

and if the following prior distribution is considered for the mean vector :

with , then the posterior distribution of the mean vector given the data is given by:

where , , and . Moreover, the marginal likelihood of the model can be written analytically as:

where is the vector of all observations for variable such that and is the vector of 1 in .

Proof.

Let us first derive the analytical expression for the posterior distribution of the mean vector :

Taking the log of the expression and focusing on the terms in :

By identification, we recognize the functional form of a Gaussian distribution:

where

and

To compute the marginal likelihood of the model, we first introduce the notation which corresponds to the vector of all observations for variable such that . By construction:

where is the component of the vector and is the vector of 1 in . Note that the covariance matrix comes for the fact that all observations are independent with unit variance, given . Interestingly, while the observations are independent given the vector , they are not marginally, and the marginal likelihood does not take a product form over marginal terms in . Conversely, thanks to the isotropic Gaussian prior distribution which is considered for , where the are all iid, not only are the vectors independent given , they are also independent marginally:

Finally, to compute, , can be written as:

where

Thus, by construction, is defined as a product and sum over and , which are independent from one another. Therefore, from Gaussian property:

Finally

∎

After the following proposition, all proofs for the Bayesian linear regression model of Section 4.2 are provided.

Proposition 3

If a linear regression model of the form

is considered where , with the variance known, and if the following prior distribution is considered for the regression vector :

with , then the posterior distribution of the regression vector given the training data set is given by:

with

and

| (41) |

where is the vector of observed target variables , and is the design matrix where the input vectors are stacked as row vectors. Moreover, the marginal likelihood of the model can also be written analytically as:

Proof.

Relying on matrix notations, the linear regression model can be written as:

| (42) |

where is the random vector of target variables , and is the design matrix where the input vectors are stacked as row vectors. In such a supervised context, the training data set is made of all pairs and can be denoted . The posterior distribution of the regression vector is then given by:

Now, denoting the observed vector of target variables associated to , taking the log of the expression, and focusing on the terms in :

By identification, we recognize the functional form of a Gaussian distribution:

where

and

Then, the marginal likelihood of the model can easily be obtained simply by writing:

where

and

Thus, by construction, is defined as a product and sum over the Gaussian random vectors and , which are independent. Therefore, from Gaussian property:

and so the marginal likelihood is given by:

∎