[caption,subcaption]

Liu, Grigas, Liu, and Shen \RUNTITLEActive Learning in the Predict-then-Optimize Framework: A Margin-Based Approach

Active Learning in the Predict-then-Optimize Framework: A Margin-Based Approach

Mo Liu \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA, 94720, \EMAILmo_liu@berkeley.edu \AUTHORPaul Grigas \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA, 94720, \EMAILpgrigas@berkeley.edu \AUTHORHeyuan Liu \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA, 94720, \EMAILheyuan_liu@berkeley.edu \AUTHORZuo-Jun Max Shen \AFFDepartment of Industrial Engineering and Operations Research, University of California, Berkeley, Berkeley, CA, 94720, \EMAILmaxshen@berkeley.edu

We develop the first active learning method in the predict-then-optimize framework. Specifically, we develop a learning method that sequentially decides whether to request the “labels” of feature samples from an unlabeled data stream, where the labels correspond to the parameters of an optimization model for decision-making. Our active learning method is the first to be directly informed by the decision error induced by the predicted parameters, which is referred to as the Smart Predict-then-Optimize (SPO) loss. Motivated by the structure of the SPO loss, our algorithm adopts a margin-based criterion utilizing the concept of distance to degeneracy and minimizes a tractable surrogate of the SPO loss on the collected data. In particular, we develop an efficient active learning algorithm with both hard and soft rejection variants, each with theoretical excess risk (i.e., generalization) guarantees. We further derive bounds on the label complexity, which refers to the number of samples whose labels are acquired to achieve a desired small level of SPO risk. Under some natural low-noise conditions, we show that these bounds can be better than the naive supervised learning approach that labels all samples. Furthermore, when using the SPO+ loss function, a specialized surrogate of the SPO loss, we derive a significantly smaller label complexity under separability conditions. We also present numerical evidence showing the practical value of our proposed algorithms in the settings of personalized pricing and the shortest path problem.

active learning, predict-then-optimize, prescriptive analytics, data-driven optimization

1 Introduction

In many applications of operations research, decisions are made by solving optimization problems that involve some unknown parameters. Typically, machine learning tools are used to predict these unknown parameters, and then an optimization model is used to generate the decisions based on the predictions. For example, in the shortest path problem, we need to predict the cost of each edge in the network and then find the optimal path to route users. Another example is the personalized pricing problem, where we need to predict the purchase probability of a given customer at each possible price and then decide the optimal price. In this predict-then-optimize paradigm, when generating the prediction models, it is natural to consider the final decision error as a loss function to measure the quality of a model instead of standard notions of prediction error. The loss function that directly considers the cost of the decisions induced by the predicted parameters, in contrast to the prediction error of the parameters, is called the Smart Predict-then-Optimize (SPO) loss as proposed by Elmachtoub and Grigas (2022). Naturally, prediction models designed based on the SPO loss have the potential to achieve a lower cost with respect to the ultimate decision error.

In general, for a given feature vector , calculating the SPO loss requires knowing the correct (in hindsight) optimal decision associated with the unknown parameters. However, a full observation of these parameters, also known as a label associated with , is not always available. For example, we may not observe the cost of all edges in the graph in the shortest path problem. In practice, acquiring the label of one feature vector instance could be costly, and thus acquiring the labels of all feature vectors in a given dataset would be prohibitively expensive and time-consuming. In such settings, it is essential to actively select the samples for which label acquisition is worthwhile.

Algorithms that make decisions about label acquisition lie in the area of active learning. The goal of active learning is to learn a good predictor while requesting a small number of labels of the samples, whereby the labels are requested actively and sequentially from unlabeled samples. Intuitively, if we are very confident about the label of an unlabeled sample based on our current predictor, then we do not have to request the label of it. Active learning is most applicable when the cost of acquiring labels is very expensive. Traditionally in active learning, the selection rules for deciding which samples to acquire labels for are based on measures of prediction error that ignore the cost of the decisions in the downstream optimization problem. Considering the SPO loss in active learning can hopefully reduce the number of labels required while achieving the same cost of decisions, compared to standard active learning methods that only consider measures of prediction error.

Considering active learning in the predict-then-optimize framework can bridge the gap between active learning and operational decisions, but there are two major challenges when designing algorithms to select samples. One is the computational issue due to the non-convexity and non-Lipschitzness of the SPO loss. When one is concerned with minimizing the SPO loss, existing active learning algorithms are computationally intractable. For example, the general importance weighted active learning (IWAL) algorithm proposed by Beygelzimer et al. (2009) is impractical to implement, since calculating the “weights” of samples requires a large enumeration of all pairs of predictors. Other active learning algorithms that are designed for the classification problem cannot be extended to minimize the SPO loss directly. Another challenge is to derive bounds for the label complexity of the algorithms and to demonstrate the advantages over supervised learning. Label complexity refers to the number of labels that must be acquired to ensure that the risk of predictor is not greater than a desired threshold. To demonstrate the savings from active learning, label complexity should be smaller than the sample complexity of supervised learning, when achieving the same risk level with respect to the loss function of interest (in our case SPO). Kääriäinen (2006) shows that, without additional assumptions on the distributions of features and noise, active learning algorithms have the same label complexity as supervised learning. Thus, deriving smaller label complexity for an active learning algorithm under some natural conditions on the noise and feature distributions is a critical but nontrivial challenge.

In this paper, we develop the first active learning method in the predict-then-optimize framework. We consider the standard setting of a downstream linear optimization problem where the parameters/label correspond to an unknown cost vector that is potentially related to some feature information. Our proposed algorithm, inspired by margin-based algorithms in active learning, uses a measure of “confidence” associated with the cost vector prediction of the current model to decide whether or not to acquire a label for a given feature. Specifically, the label acquisition decision is based on the notion of distance to degeneracy introduced by El Balghiti et al. (2022), which precisely measures the distance from the prediction of the current model to the set of cost vectors that have multiple optimal solutions. Intuitively, the further away the prediction is from degeneracy, the more confident we are that the associated decision is actually optimal. Our proposed margin-based active learning (MBAL-SPO) algorithm has two versions depending on the precise rejection criterion: soft rejection and hard rejection. Hard rejection generally has a smaller label complexity, whereas soft rejection is computationally easier. In any case, when building prediction models based on the actively selected training set, our algorithm will minimize a generic surrogate of the SPO loss over a given hypothesis class. For each version, we demonstrate theoretical guarantees by providing non-asymptotic excess surrogate risk bounds, as well as excess SPO risk bounds, that hold under a natural consistency assumption.

To analyze the label complexity of our proposed algorithm, we define the near-degeneracy function, which characterizes the distribution of optimal predictions near the regions of degeneracy. Based on this definition, we derive upper bounds on the label complexity. We consider a natural low-noise condition, which intuitively says that the distribution of features for a given problem is far enough from degeneracy. Indeed, for most practical problems, the data are expected to be somewhat bounded away from degeneracy. Under these conditions, we show that the label complexity bounds are smaller than those of the standard supervised learning approach. In addition to the results for a general surrogate loss, we also demonstrate improved label complexity results for the SPO+ surrogate loss, proposed by Elmachtoub and Grigas (2022) to account for the downstream problem, when the distribution satisfies a separability condition. We also conduct some numerical experiments on instances of shortest path problems and personalized pricing problems, demonstrating the practical value of our proposed algorithm above the standard supervised learning approach. Our contributions are summarized below.

-

•

We are the first work to consider active learning algorithms in the predict-then-optimize framework. To efficiently acquire labels to train a machine learning model to minimize the decision cost (SPO loss), we propose a margin-based active learning algorithm that utilizes a surrogate loss function.

-

•

We analyze the label complexity and derive non-asymptotic surrogate and SPO risk bounds for our algorithm, under both soft-rejection and hard-rejection settings. Our analysis applies even when the hypothesis class is misspecified, and we demonstrate that our algorithms can still achieve a smaller label complexity than supervised learning. In particular, under some natural consistency assumptions, we develop the following guarantees.

-

–

In the hard rejection case with general surrogate loss functions, we provide generic bounds on the label complexity and the non-asymptotic surrogate and SPO risks in Theorem 4.5.

-

–

In the hard rejection case with the SPO+ surrogate loss, we provide a much smaller non-asymptotic surrogate (and, correspondingly, SPO) risk bound in Theorem 4.11 under a separability condition. This demonstrates the advantage of the SPO+ surrogate loss over general surrogate losses.

-

–

In the soft rejection case with a general surrogate loss, which is computationally easier, we provide generic bounds on the label complexity and the non-asymptotic surrogate and SPO risks in Theorem 4.13.

-

–

For each case above, we characterize sufficient conditions for which we can specialize the above generic guarantees and demonstrate that the margin-based algorithm achieves sublinear or even finite label complexity. We provide concrete examples of these conditions, and we provide different non-asymptotic bounds in cases where the feasible region of the downstream optimization problem is either a polyhedron or a strongly convex region. In these situations, and under natural low-noise conditions, we demonstrate that our algorithm can achieve much smaller label complexity than the sample complexity of supervised learning.

-

–

-

•

We demonstrate the practical value of our algorithm by conducting comprehensive numerical experiments in two settings. One is the personalized pricing problem, and the other is the shortest path problem. Both sets of experiments show that our algorithm achieves a smaller SPO risk than the standard supervised learning algorithm given the same number of acquired labels.

1.1 Example: Personalized Pricing Problem

To further illustrate and motivate the integration of active learning into the predict-then-optimize setting, we present the following personalized pricing problem as an example.

Example 1.1 (Personalized pricing via customer surveys)

Suppose that a retailer needs to decide the prices of items for each customer, after observing the features (personalized information) of the customers. The feature vector of a generic customer is , and the purchase probability of that customer for item is , which is a function of the price . This purchase probability is unknown and corrupted with some noise for each customer. Suppose the price for each item is selected from a candidate list , which is sorted in ascending order. Then, the pricing problem can be formulated as

| (1) | |||

Here, encodes the decision variables with indices in the set , where is a binary variable indicating which price for item is selected. Namely, if item is priced at , and otherwise . The objective (1) is to maximize the expected total revenue of items by offering price for item . Constraints (LABEL:con:1price) require each item to have one price selected. In constraint (LABEL:con:sum1), is a matrix with rows, and is a vector with dimensions. Each row of constraints (LABEL:con:sum1) characterizes one rule for setting prices. For example, if the first row of is and the first entry in is zero, then this constraint further requires that if item is priced at , then the price for the item must be no smaller than . For another example, if the second row of is , and the second entry of is 1, then it means that at most one item can be priced below the price . Thus, constraints (LABEL:con:sum1) can characterize different rules for setting prices for items.

Traditionally, the conditional expectation of revenue must be estimated from the purchasing behavior of the customers. In this example, we consider the possibility that the retailer can give the customers surveys to investigate their purchase probabilities. By analyzing the results of the surveys, the retailer can infer the purchase probability for each price point and each item for this customer. Therefore, whenever a survey is conducted, the retailer acquires a noisy estimate of the revenue, denoted by , at each price point and item .

In personalized pricing, first, the retailer would like to build a prediction model to predict given the customer’s feature vector . Then, given the prediction model, the retailer solves the problem (1) to obtain the optimal prices. In practice, when evaluating the quality of the prediction results of , the retailer cares more about the expected revenue from the optimal prices based on this prediction, rather than the direct prediction error. Therefore, when building the prediction model for , retailers are expected to be concerned with minimizing SPO loss, rather than minimizing prediction error.

One property of (1) is that the objective is linear and can be further written as . By the linearity of the objective, the revenue loss induced by the prediction errors can be written in the form of the SPO loss considered in Elmachtoub and Grigas (2022). In general, considering the prediction errors when selecting customers may be inefficient, since smaller prediction errors do not always necessarily lead to smaller revenue losses, because of the properties of the SPO loss examined by Elmachtoub and Grigas (2022). \Halmos

In Example 1.1, in practice, there exists a considerable cost to investigate all customers, for example, the labor cost to collect the answers and incentives given to customers to fill out the surveys. Therefore, the retailer would rather intelligently select a limited subset of customers to investigate. This subset of customers should be ideally selected so that the retailer can build a prediction model with small SPO loss, using a small number of surveys.

Active learning is essential to help retailers select representative customers and reduce the number of surveys. Traditional active learning algorithms would select customers to survey based on model prediction errors, which are different from the final revenue of the retailer. On the contrary, when considering the SPO loss, the final revenue is integrated into the learning and survey distribution processes.

1.2 Literature Review

In this section, we review existing work in active learning and the predict-then-optimize framework. To the best of our knowledge, our work is the first work to bridge these two streams.

Active learning.

There has been substantial prior work in the area of active learning, focusing essentially exclusively on measures of prediction error. Please refer to Settles (2009) for a comprehensive review of many active learning algorithms. Cohn et al. (1994) shows that in the noiseless binary classification problem, active learning can achieve a large improvement in label complexity, compared to supervised learning. It is worth noting that in the general case, Kääriäinen (2006) provides a lower bound of the label complexity which matches supervised learning. Therefore, to demonstrate the advantages of active learning, some further assumptions on the noise and distribution of samples are required. For the agnostic case where the noise is not zero, many algorithms have also been proposed in the past few decades, for example, Hanneke (2007), Dasgupta et al. (2007),Hanneke (2011), Balcan et al. (2009), and Balcan et al. (2007). These papers focus on binary or multiclass classification problems. Balcan et al. (2007) proposed a margin-based active learning algorithm, which is used in the noiseless binary classification problem with a perfect linear separator. Balcan et al. (2007) achieves the label complexity under uniform distribution, where is a parameter defined for the low noise condition and is the desired error rate. Krishnamurthy et al. (2017) and Gao and Saar-Tsechansky (2020) consider cost-sensitive classification problems in active learning, where the misclassification cost depends on the true labels of the sample.

The above active learning algorithms in the classification problem do not extend naturally to real-valued prediction problems. However, the SPO loss is a real-valued function. When considering real-valued loss functions, Castro et al. (2005) prove convergence rates in the regression problem, and Sugiyama and Nakajima (2009) and Cai et al. (2016) also consider squared loss as the loss function. Beygelzimer et al. (2009) propose an importance-weighted algorithm (IWAL) that extends disagreement-based methods to real-valued loss functions. However, it is intractable to directly use the IWAL algorithm in the SPO framework. Specifically, it requires solving a non-convex problem at each iteration, which may have to enumerate all pairs of predictor candidates even when the hypothesis set is finite.

Predict-then-optimize framework.

In recent years, there has been a growing interest in developing machine learning models that incorporate the downstream optimization problem. For example, Bertsimas and Kallus (2020), Kao et al. (2009), Elmachtoub and Grigas (2022), Zhu et al. (2022), Donti et al. (2017) and Ho and Hanasusanto (2019) propose frameworks that somehow relate the learning problem to the downstream optimization problem. In our work, we consider the Smart Predict-then-Optimize (SPO) framework proposed by Elmachtoub and Grigas (2022). Because the SPO loss function is nonconvex and non-Lipschitz, the computational and statistical properties of the SPO loss in the fully supervised learning setting have been studied in several recent works. Elmachtoub and Grigas (2022) provide a surrogate loss function called SPO+ and show the consistency of this loss function. Elmachtoub et al. (2020), Loke et al. (2022), Demirovic et al. (2020), Demirović et al. (2019), Mandi and Guns (2020), Mandi et al. (2020), and Tang and Khalil (2022) all develop new applications and computational frameworks for minimizing the SPO loss in various settings. El Balghiti et al. (2022) consider generalization error bounds of the SPO loss function. Ho-Nguyen and Kılınç-Karzan (2022), Liu and Grigas (2021), and Hu et al. (2022) further consider risk bounds of different surrogate loss functions in the SPO setting. There is also a large body of work more broadly in the area of decision-focused learning, which is largely concerened with differentiating through the parameters of the optimization problem, as well as other techniques, for training. See, for example, Amos and Kolter (2017), Wilder et al. (2019), Berthet et al. (2020), Chung et al. (2022), the survey paper Kotary et al. (2021), and the references therein. Recently there has been growing attention on problems with nonlinear objectives, where estimating the conditional distribution of parameters is often needed; see, for example, Kallus and Mao (2023), Grigas et al. (2021) and Elmachtoub et al. (2023).

1.3 Organization

The remainder of the paper is organized as follows. In Section 2, we introduce preliminary knowledge on the predict-then-optimize framework and active learning, including the SPO loss function, label complexity, and the SPO+ surrogate loss function. Then, we present our active learning algorithm, margin-based active learning (MBAL-SPO), in Section 3. We first present an illustration to motivate the incorporation of the distance to degeneracy in the active learning algorithm in 3.1. Next, we analyze the risk bounds and label complexities for both hard and soft rejection in Section 4. To demonstrate the strength of our algorithm over supervised learning, we consider natural low-noise conditions and derive sublinear label complexity in Section 5. We demonstrate the advantage of using SPO+ as the surrogate loss in some cases by providing a smaller label complexity. We further provide concrete examples of these low-noise conditions. In Section 6, we test our algorithm using synthetic data in two problem settings: the shortest path problem and the personalized pricing problem. Lastly, we point out some future research directions in Section 7. The omitted proofs, sensitivity analysis of the numerical experiments, and additional numerical results are provided in the Appendices.

2 Preliminaries

We first introduce some preliminaries about active learning and the predict-then-optimize framework. In particular, we introduce the SPO loss function, we discuss the goals of active learning in the predict-then-optimize framework, and we review the SPO+ surrogate loss.

2.1 Predict-then-Optimize Framework and Active Learning

Let us begin by formally describing the “predict-then-optimize” framework and the “Smart Predict-then-Optimize (SPO)” loss function. We assume that the downstream optimization problem has a linear objective, but the cost vector of the objective, , is unknown when the problem is solved to make a decision. Instead, we observe a feature vector, , which provides auxiliary information that can be used to predict the cost vector. The feature space and cost vector space are assumed to be bounded. We assume there is a fixed but unknown distribution over pairs living in . The marginal distribution of is denoted by . Let denote the decision variable of the downstream optimization problem, where the feasible region is a convex and compact set that is assumed to be fully known to the decision-maker. To avoid trivialities, we also assume throughout that the set is not a singleton. Given an observed feature vector , the ultimate goal is to solve the contextual stochastic optimization problem:

| (2) |

From the equivalence in (2), observe that the downstream optimization problem in the predict-then-optimize framework relies on a prediction (otherwise referred to as estimation) of the conditional expectation . Given such a prediction , a decision is made by then solving the deterministic version of the downstream optimization problem:

| (3) |

For simplicity, we assume is an oracle for solving (3), whereby is an optimal solution of .

Our goal is to learn a cost vector predictor function , so that for any newly observed feature vector , we first make prediction and then solve the optimization problem in order to make a decision. This predict-then-optimize paradigm is prevalent in applications of machine learning to problems in operations research. We assume the predictor function is within a compact hypothesis class of functions on . We say the hypothesis class is well-specified if . In our analysis, the well-specification is not required. The active learning methods we consider herein rely on using a variant of empirical risk minimization to select by minimizing an appropriately defined loss function. Our primary loss function of interest in the predict-then-optimize setting is the SPO loss, introduced by Elmachtoub and Grigas (2022), which characterizes the regret in decision error due to an incorrect prediction and is formally defined as

for any cost vector prediction and realized cost vector . We further define the SPO risk of a prediction function as , and the excess risk of as . (Throughout, we typically remove the subscript notation from the expectation operator when it is clear from the context.) Notice that a guarantee on the excess SPO risk implies a guarantee that holds “on average” with respect to for the contextual stochastic optimization problem (2).

As previously described, in many situations acquiring cost vector data may be costly and time-consuming. The aim of active learning is to choose which feature samples to label sequentially and interactively, in contrast to standard supervised learning which acquires the labels of all the samples before training the model. In the predict-then-optimize setting, acquiring a “label” corresponds to collecting the cost vector data that corresponds to a given feature vector . An active learner aims to use a small number of labeled samples to achieve a small prediction error. In the agnostic case, the noise is nonzero and the smallest prediction error is the Bayes risk, which is . The goal of an active learning method is to then find a predictor trained on the data with the minimal number of labeled samples, such that , with high probability and where is a given risk error level. The number of labels acquired to achieve this goal is referred to as the label complexity.

2.2 Surrogate Loss Functions and SPO+

Due to the potential non-convexity and even non-continuity of the SPO loss, a common approach is to consider surrogate loss functions that have better computational properties and are still (ideally) aligned with the original SPO loss. In our work, the surrogate loss function is assumed to be continuous. The surrogate risk of a predictor is denote by , and the corresponding minimum risk is denoted by .

As a special case of the surrogate loss function , Elmachtoub and Grigas (2022) proposed a convex surrogate loss function, called the SPO+ loss, which is defined by

and is an upper bound on the SPO loss, i.e., for any and . Elmachtoub and Grigas (2022) demonstrate the computational tractability of the SPO+ surrogate loss, conditions for Fisher consistency of the SPO+ risk with respect to the true SPO risk, as well as strong numerical evidence of its good performance with respect to the downstream optimization task. Liu and Grigas (2021) further demonstrate sufficient conditions that imply that when the excess surrogate SPO+ risk of a prediction function is small, the excess true SPO risk of a prediction function is also small. This property not only holds for the SPO+ loss, but also for other surrogate loss functions, such as the squared loss (see, for details, Ho-Nguyen and Kılınç-Karzan (2022)). Importantly, the SPO+ loss still accounts for the downstream optimization problem and the structure of the feasible region , in contrast to losses like the loss that focus only on prediction error. As will be shown in Theorem 4.11, compared to the general surrogate loss functions that satisfy Assumption 3.1.1 in our analysis, the SPO+ loss function achieves a smaller label complexity by utilizing the structure of the downstream optimization problem.

Notations. Let on be a generic norm. Its dual norm is denoted by , which is defined by . We denote the set of extreme points in the feasible region by , and the diameter of the set by . The “linear optimization gap” of with respect to cost vector is defined as . We further define and , where again is the domain of possible realizations of cost vectors under the distribution . We denote the cost vector space of the prediction range by , i.e., . For the surrogate loss function , we define . We also denote for the general norm. We use to denote the multivariate normal distribution with center and covariance matrix . We use to denote . When conducting the asymptotic analysis, we adopt the standard notations and . We further use to suppress the logarithmic dependence. We use to refer to the indicator function, which outputs 1 if the argument is true and 0 otherwise.

3 Margin-Based Algorithm

In this section, we develop and present the margin-based algorithm in the predict-then-optimize framework (MBAL-SPO). We first illustrate and motivate the algorithm in the polyhedral case. Then, we provide some conditions for the noise distribution and surrogate loss functions for our MBAL-SPO.

3.1 Illustration and Algorithm

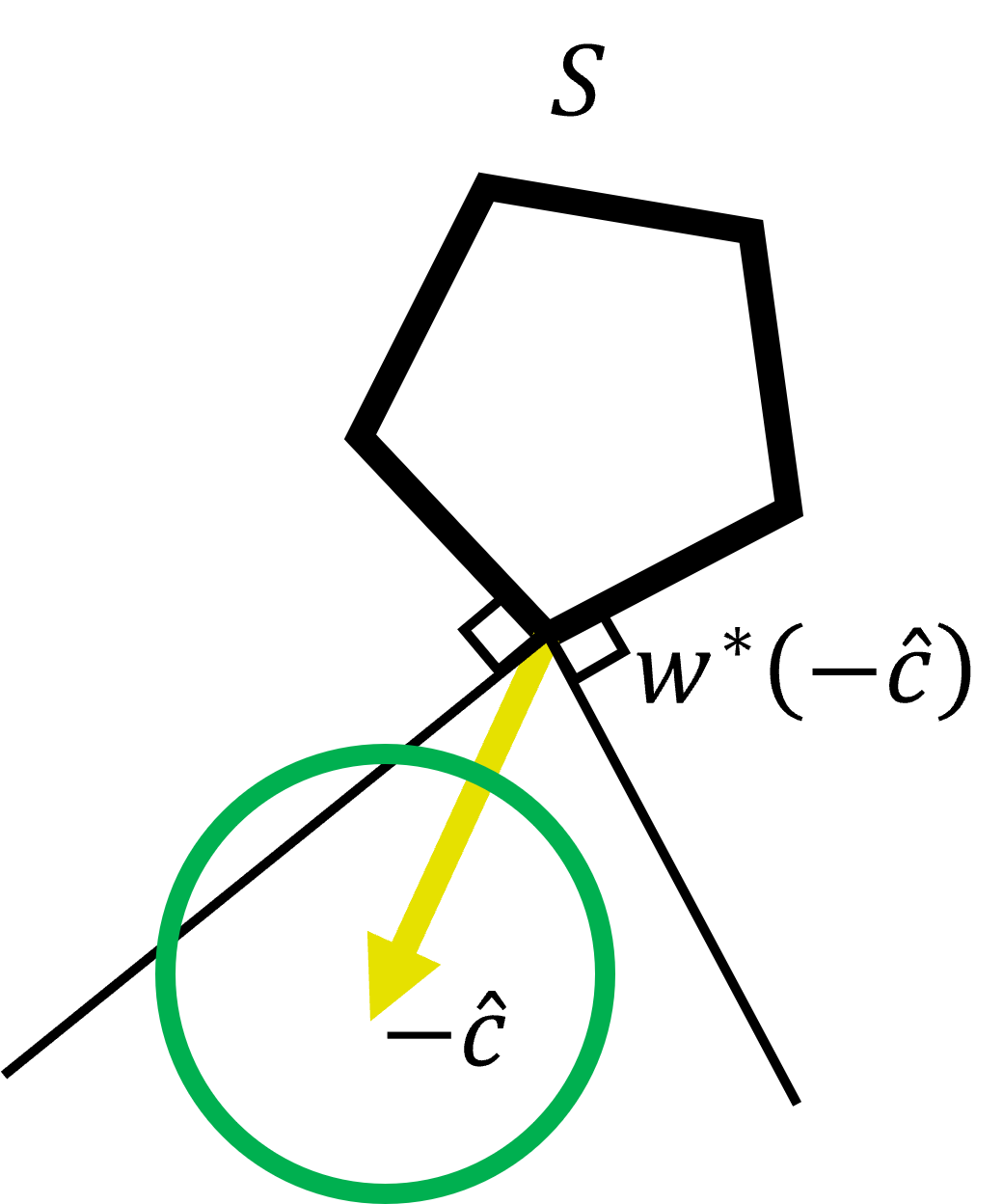

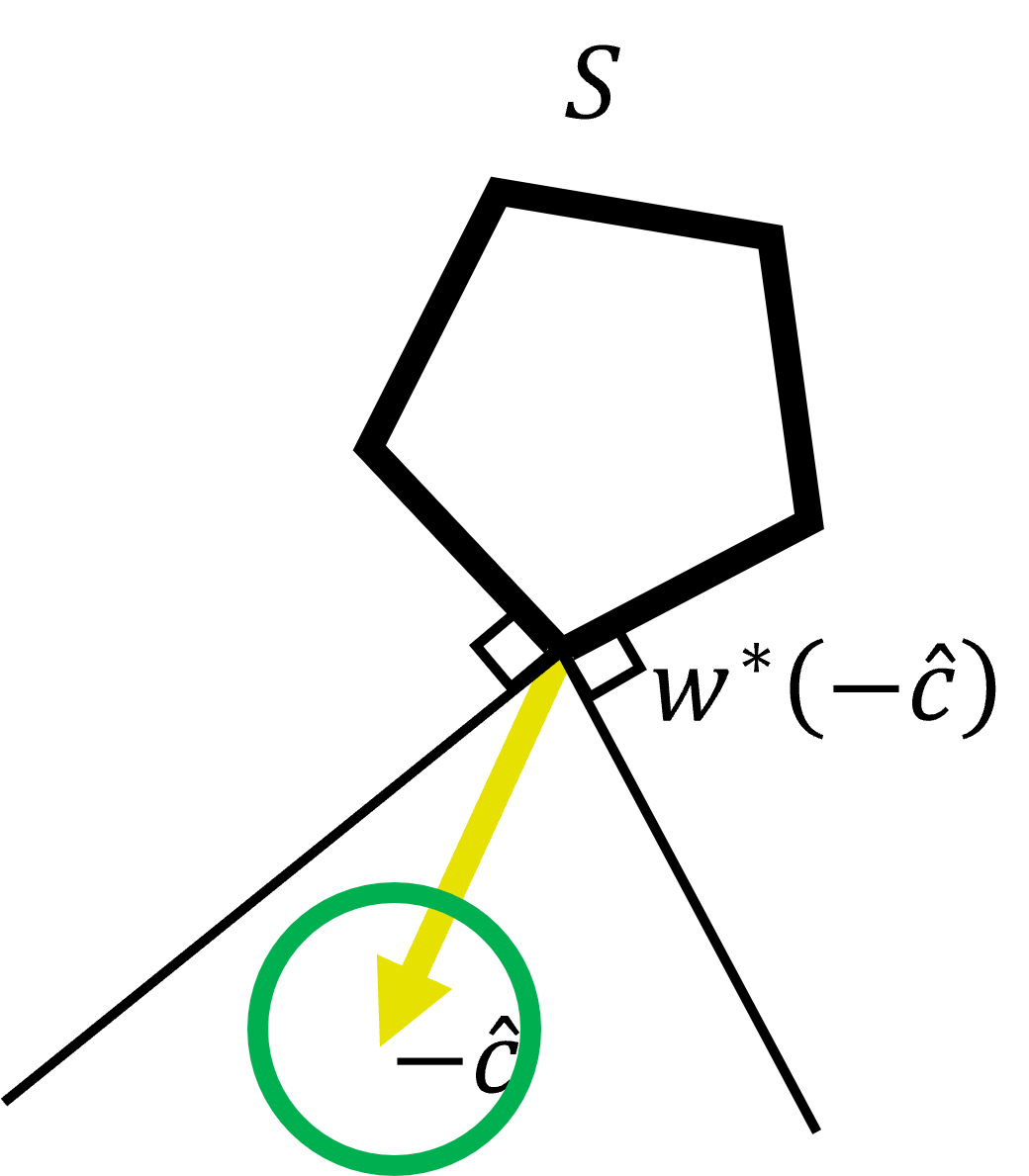

Let us introduce the idea of the margin-based algorithm with the following two examples, which illustrate the value of integrating the SPO loss into active learning. Particularly, given the current training set and predictor, it is very likely that some features will be more informative and thus more valuable to label than others. In general, the “value” of labeling a feature depends on the associated prediction error (Figure 1) and the location of the prediction relative to the structure of the feasible region (Figure 2). In Figure 1, the feasible region is polyhedral and the yellow arrow represents . Within this example, for the purpose of illustration, let us assume the hypothesis class is well-specified. Our goal then is to find a good predictor from the hypothesis class , such that is close to . However, because is random, the empirical best predictor in the training set may not exactly equal the true predictor , where . Given one feature , the prediction is , the negative of which is shown in Figures 1(a) and 1(b). Intuitively, when the training set gets larger, the empirical best predictor should get closer to , and should get closer to . Thus, we can construct a confidence region around , such that is within this confidence region with some high probability. Examples of confidence regions for the estimation of given the current training set are shown in the green circles in Figure 1. The optimal solution is the extreme point indicated in Figure 1, and the normal cone at illustrates the set of all cost vectors whose optimal solution is also . In addition, those cost vectors that lie on the boundary of the normal cone are the cost vectors that can lead to multiple optimal decisions (they will be defined as degenerate cost vectors in Definition 3.1 later). In cases when the confidence region is large (e.g., because the training set is small), as indicated in Figure 1(a), the green circle intersects with the degenerate cost vectors, which means that some vectors within the confidence region for estimating could lead to multiple optimal decisions. When the confidence region is smaller (e.g., because the training set is larger), as indicated in Figure 1(b), the green circle does not intersect with the degenerate cost vectors, which means the optimal decision of is the same as the optimal decision of , , with high probability. Thus, when the confidence region of does not intersect with the degenerate cost vectors, the optimal decision based on the current estimated cost vector will lead to the correct optimal decision with high probability, and the SPO loss will be zero. This in turn suggests that the label corresponding to is not informative (and we do not have to acquire it), when the confidence region centered at the prediction is small enough to not intersect those degenerate cost vectors.

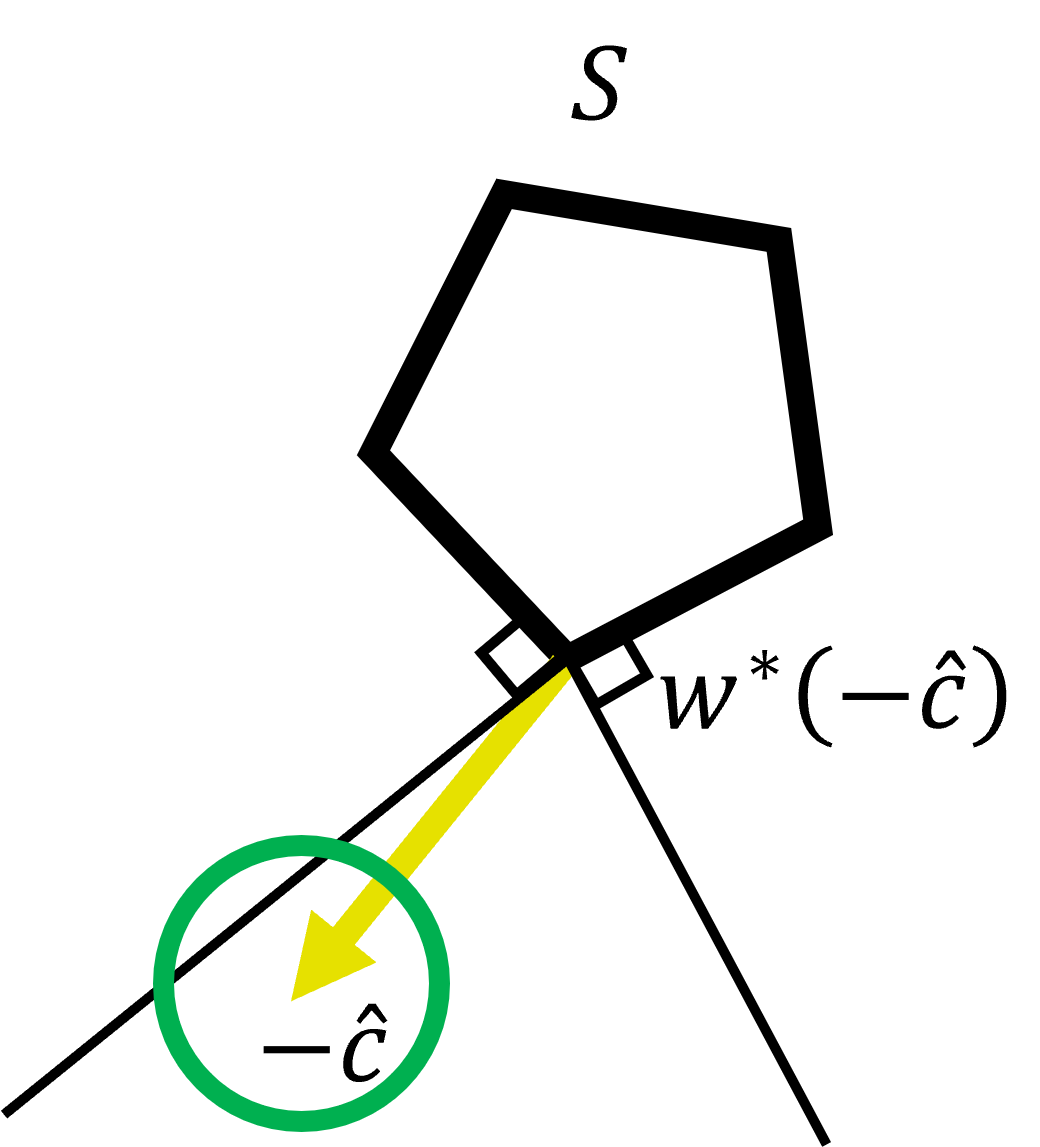

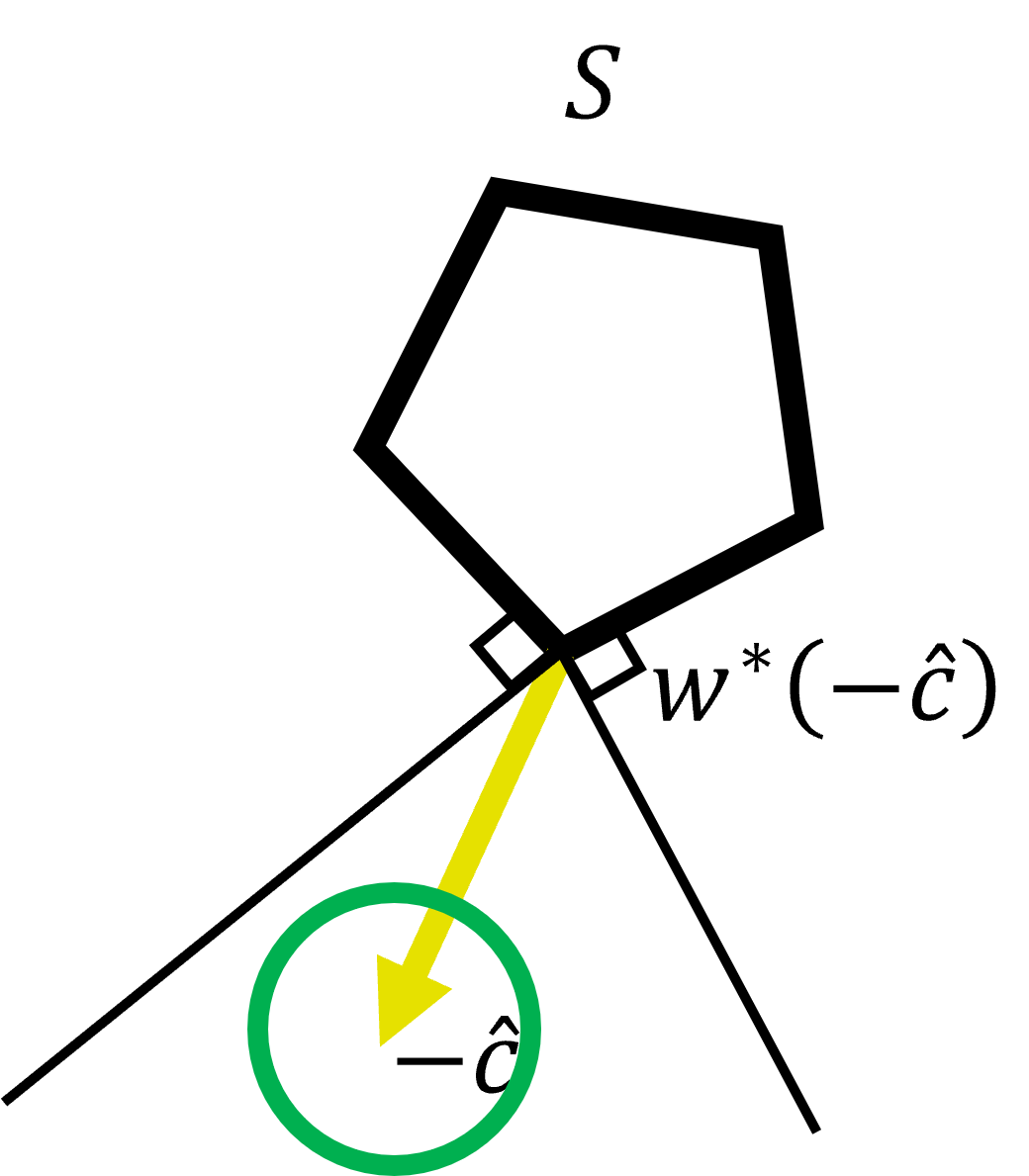

Figure 2 further shows that considering the SPO loss function reduces the label complexity when the confidence regions of the cost vector are the same size. In Figure 2, both green circles have the same radius but their locations are different. In Figure 2(a), the confidence region for is close to the degenerate cost vectors, and thus the cost vectors within the confidence region will lead to multiple optimal decisions. In Figure 2(b), the confidence region for is far from the degenerate cost vectors, and therefore acquiring a label for is less informative, as we are more confident that leads to the correct optimal decision due to the more central location of the confidence region.

The above two examples highlight that the confidence associated with a prediction is crucial to determine whether it is valuable to acquire a true label associated with . Furthermore, confidence is related to both the size of the confidence region (which is often dictated by the number of labeled samples we have acquired) and the location of the prediction relative to the structure of . El Balghiti et al. (2022) introduced the notion of “distance to degeneracy,” which precisely measures the distance of a prediction to those degenerate cost vectors with multiple optimal solutions and thus provides the correct way to measure confidence about the location of a prediction. In fact, El Balghiti et al. (2022) argue that the distance to degeneracy provides a notion of confidence associated with a prediction that generalizes the notion of “margin” in binary and multiclass classification problems. El Balghiti et al. (2022) use the distance to degeneracy to provide tighter generalization guarantees for the SPO loss and its associated margin loss. In our context, we adopt the distance to degeneracy in order to determine whether or not to acquire labels. It is motivated by our intuition from the previously discussed examples wherein the labels of samples should be more informative if their predicted cost vectors are closer to degeneracy. In turn, we develop a generalization of margin-based active learning algorithms that utilize the distance to degeneracy as a confidence measure to determine those samples whose labels should (or should not) be acquired. Definition 3.1 reviews the notion of distance to degeneracy as defined by El Balghiti et al. (2022).

Definition 3.1

(Distance to Degeneracy, El Balghiti et al. (2022)). The set of degenerate cost vector predictions is has multiple optimal solutions. Given a norm on , the distance to degeneracy of the prediction is . \Halmos

The distance to degeneracy can be easily computed in some special cases, for example, when the feasible region is strongly convex or in the case of a polyhedral feasible region with known extreme point representations. El Balghiti et al. (2022) provide the exact formulas of the distance to degeneracy function in these two special cases. In particular, in the case of a polyhedral feasible region with extreme points , that is, , Theorem 8 of El Balghiti et al. (2022) says that the distance to degeneracy of any vector satisfies the following equation:

| (4) |

Theorem 7 of El Balghiti et al. (2022), on the other hand, says that whenever is a strongly convex set. As mentioned, the distance to degeneracy provides a measure of “confidence” regarding the cost vector prediction and its implied decision . This observation motivates us to design a margin-based active learning algorithm, whereby if the distance to degeneracy is greater than some threshold (depending on the number of iterations and samples acquired so far), then we are confident enough to label it using our current model without asking for the true label.

Our margin-based method is proposed in Algorithm 1. The idea of the margin-based algorithm can be explained as follows. At iteration , we first observe an unlabeled feature vector , which follows distribution . Given the current predictor , we calculate the distance to the degeneracy of this unlabeled sample . If the distance to degeneracy is greater than the threshold , then we reject with some probability . If , this rejection is referred to as a hard rejection; when , this rejection is referred to as a soft rejection. If a soft-rejected sample is not ultimately rejected, we acquire a label (cost vector) associated with and add the sample to the set . On the other hand, if , then we acquire a label (cost vector) associated with and add the sample to the working training set . At each iteration, we update the predictor by computing the best predictor within a subset of the hypothesis class that minimizes the empirical surrogate risk measured on the labeled samples. Note that Algorithm 1 maintains two working sets, and , due to the two different types of labeling criteria. To ensure that the expectation of empirical loss is equal to the expectation of the true loss, we need to assign weight to the soft-rejection samples in the set . It is assumed throughout that the sequence is an i.i.d. sequence from the distribution .

Two versions of the MBAL-SPO have their own advantages. When using hard rejection, we update the set of predictors according to Line 20 in Algorithm 1, and the value of is set to zero. In contrast, in the soft rejection case, we keep as the entire hypothesis class for all iterations, and the value of is non-zero. In comparison, hard rejection can result in a smaller label complexity because , while soft rejection can reduce computational complexity by keeping as the whole hypothesis class . Please see the discussion in Sections 4.2 and 4.4 for further details.

In Algorithm 1, the case where intuitively corresponds to the case where the confidence region of does not intersect with the degenerate cost vectors. Hence, we are sufficiently confident that the optimal decision is equal to , where is a model that minimizes the SPO risk. Thus, we do not have to ask for the label of . Lemma 3.2 further characterizes the conditions when two predictions lead to the same decision when the feasible region is polyhedral.

Lemma 3.2 (Conditions for identical decisions in polyhedral feasible regions.)

Suppose that the feasible region is polyhedral. Given two cost vectors , if , then it holds that . In other words, the optimal decisions for and are the same.

Lemma 3.2 implies that given one prediction of the cost vector, when its distance to degeneracy is larger than the radius of its confidence region, then all the predictions within this confidence region will lead to the same decision. Moreover, if the optimal prediction is also within this confidence region, the SPO loss of this prediction is zero.

The computational complexity of Algorithm 1 depends on the choice of the surrogate loss we use. As discussed earlier, calculating the distance to degeneracy is efficient in some special cases. In general, in the polyhedral case when a convex hull representation is not available, a reasonable heuristic is to only compute the minimum in (4) with respect to the neighboring extreme points of . Alternatively, we observe that the objective inside the minimum in (4) is quasiconcave. Therefore, we can relax the condition that be an extreme point and still recover an extreme point solution. One can solve the resulting problem with a Frank-Wolfe type method, for example, see Yurtsever and Sra (2022). The computational complexity of updating in Line 19 depends on the choice of hypothesis class . In the case of soft rejection, we maintain for all and the update is the same as performing empirical risk minimization in , which can be efficiently computed exactly or approximately for most common choices of , including linear and nonlinear models. In the case of hard rejections, is now the intersection of different level sets. Thus, is a minimization problem with level set constraints. The complexity of solving this problem again depends on the choice of and can often be solved efficiently. For example, in the case of linear models or nonlinear models such as neural networks, a viable approach would be to apply stochastic gradient descent to a penalized version of the problem or to apply a Lagrangian dual-type algorithm. In practice, since the constraints may be somewhat loose, we may simply ignore them and still obtain good results. Finally, we note that in both cases of hard rejection and soft rejection, although we have to solve a different optimization problem at every iteration, these optimization problems do not change much from one iteration to the next, and therefore using a warm-start strategy that uses as the initialization for calculating will be very effective.

3.1.1 Surrogate Loss Function and Noise Distribution

Without further assumptions on the distribution of noise and features, the label complexity of an active learning algorithm can be the same as the sample complexity of supervised learning, as shown in Kääriäinen (2006). Therefore, we make several natural assumptions in order to analyze the convergence and label complexity of our algorithm. Recall that the optimal SPO and surrogate risk values are defined as:

We define as the set of all optimal predictors for the SPO risk, i.e., for all and as the set of all optimal predictors for the risk of the surrogate loss, i.e., for all . We also use the notation and when the surrogate loss is SPO+. We define the essential sup norm of a function as , with respect to the marginal distribution of and where is the norm defining the distance to degeneracy (Definition 3.1). Given a set , we further define the distance between a fixed predictor function and as . Assumption 3.1.1 states our main assumptions on the surrogate loss function that we work with.

[Consistency and error bound condition] The hypothesis class is a nonempty compact set w.r.t. to the sup norm, and the surrogate loss function is continuous and satisfies:

-

(1)

, i.e., the minimizers of the surrogate risk are also minimizers of the SPO risk.

-

(2)

There exists a non-decreasing function with such that for any , for any ,

Assumption \theassumption.(1) states the consistency of the surrogate loss function. Note that since is a nonempty compact set and is a continuous function, is also a nonempty compact set. On the other hand, the SPO loss is generally discontinuous so is not necessarily compact, although the consistency assumption ensures that is nonempty. Assumption \theassumption.(2) is a type of error bound condition on the risk of the surrogate loss, wherein the function provides an upper bound of the sup norm between the predictor and the set of optimal predictors whenever the surrogate risk of is close to the minimum surrogate risk value. By Assumption \theassumption.(2), when the excess surrogate risk of becomes smaller, becomes closer to the set , which implies that the prediction also gets closer to an optimal prediction for any given . As a consequence, the distance to degeneracy also converges to for almost all . This property enables us to analyze the performance of MBAL-SPO under SPO+ and surrogate loss function respectively in the next two sections. Assumption 3.1.1 is related to the uniform calibration property studied in Ho-Nguyen and Kılınç-Karzan (2022) in the SPO context. Next, to measure how the density of the distribution is allocated near the points of degeneracy, we define the near-degeneracy function in Definition 3.3.

Definition 3.3 (Near-degeneracy function)

The near-degeneracy function with respect to the distribution of is defined as:

The near-degeneracy function measures the probability that the distance to degeneracy of is smaller than , when follows the marginal distribution of in . If contains more than one optimal predictor, the near-degeneracy function considers the distribution of the smallest distance to degeneracy of all optimal predictors . Intuitively, when is smaller, the density allocated near the points of degeneracy becomes smaller, which means Algorithm 1 has a larger probability to reject samples, and achieves smaller label complexity. This intuition is characterized in Lemma 3.4.

Lemma 3.4 (Upper bound on the expected number of acquired labels)

Lemma 3.4 provides an upper bound for the expected number of acquired labels up to time , by utilizing the near-degeneracy function . Note that in the soft rejection case, if and is independent of , Lemma 3.4 implies that this upper bound grows linearly in . However, if we know the value of before running the algorithm, then this upper bound can be reduced to a sublinear order by setting as a function of . On the other hand, if we can set , i.e., in the hard rejection case, the upper bound in Lemma 3.4 is sublinear if is sublinear. As will be shown later in Proposition 5.1, in the hard rejection case, we achieve a sublinear and sometimes even finite label complexity when the near-degeneracy function satisfies certain conditions.

4 Guarantees and Analysis for the Margin-Based Algorithm

In this section, we analyze the convergence and label complexity of MBAL-SPO in various settings. We first review some preliminary information about sequential complexity and covering numbers in Section 4.1. Next, we analyze the label complexity under hard rejections and soft rejections in Sections 4.2 and 4.4, respectively. In both sections, we develop non-asymptotic surrogate and SPO risk error bounds. We also develop bounds for the label complexity that, under certain conditions, can be much smaller than supervised learning. In Section 4.3, we further provide tighter SPO+ and SPO risk bounds when using the SPO+ surrogate under a separability condition. At the end of this section, we discuss how to set the values of the parameters in practice in MBAL-SPO. All missing proofs are provided in the appendix.

4.1 Preliminaries About Sequential Complexity

In Algorithm 1, the samples in the training set are not i.i.d., instead, whether to acquire the label at iteration depends on the historical label results. One of the challenges in analyzing the convergence and label complexity of the margin-based algorithm stems from the non i.i.d. samples. In this section, we review some techniques that characterize the convergence of non i.i.d. random sequences.

In Algorithm 1, the random variables in one iteration can be written as , where represents whether the sample is near degeneracy or not, i.e. if then , otherwise . The random variable represents the outcome of the coin flip that determines if we acquire the label of this sample or not, in the case when . For simplicity, we use random variable to denote the tuple of random variables . Thus, depends on and the classical convergence results for i.i.d. samples do not apply in the margin-based algorithm. We define as the -field of all random variables until the end of iteration (i.e., ). In Algorithm 1, the re-weighted loss function at iteration is . It is easy to see that is upper bounded by .

Then, to analyze the convergence of to , we adopt the sequential covering number defined in Rakhlin et al. (2015b). This notion generalizes the classical Rademacher complexity by defining a stochastic process on a binary tree. Let us briefly review the relevant results from Rakhlin et al. (2015b). A -valued tree of depth is a rooted complete binary tree with nodes labeled by elements of . A path in the tree is denoted by , where , for all , with representing the left child node, and representing the right child node. The tree is identified with the sequence of labeling functions which provide the labels for each node. Therefore, is the label for the root of the tree, while for is the label of the node obtained by following the path of length from the root. In a slight abuse of notation, we use to refer to the label of the node along the path defined by . Similar to a -valued tree , a real-valued tree of depth is a tree identified by the real-valued labeling functions . Thus, given any loss function , the composition is a real-valued tree given by the labeling functions for any fixed .

Definition 4.1 (Sequential covering number)

(Rakhlin et al. (2015b), Kuznetsov and Mohri (2015)) Let denote the loss of predictor given the random variable . Given a -valued tree of depth , a set of real-valued trees of depth is a sequential -cover, with respect to the norm, of a function class with respect to the loss if for all and for all paths , there exists a real-valued tree such that

The sequential covering number of a function class with respect to the loss is defined to be the cardinality of the minimal sequential cover. The maximal covering number is then taken to be , where the supremum is over all -valued trees of depth . \Halmos

In Definition 4.1, the loss function can be either the reweighted loss or the surrogate loss. In comparison, the standard covering number for i.i.d. observations is defined as

Utilizing the sequential covering number, Kuznetsov and Mohri (2015) provides a data-dependent generalization error bound for non i.i.d. sequences. As a relaxed version of their results, the data-independent error bound is stated in Proposition 4.2. This proposition is from the last line of proof of Theorem 1 in Kuznetsov and Mohri (2015), and we apply it to the reweighted loss.

Proposition 4.2 (Non i.i.d. generalization error bound)

(Theorem 1 in Kuznetsov and Mohri (2015)) Let be a (non i.i.d.) sequence of random variables. Fix . Then, the following holds:

Proposition 4.3 further provides an upper bound for when is a smoothly-parameterized class.

Proposition 4.3 (Bound for the sequential covering number)

Suppose is a class of functions smoothly-parameterized by with respect to the norm, i.e., there exists such that for any and any , . Let be the diameter of in the norm. Suppose the surrogate loss function is -Lipschitz with respect to the norm for any fixed . Then, given , for any , for any , we have that

The smoothly-parameterized hypothesis class is a common assumption when analyzing the covering number for parameterized class, e.g., see Assumption 3 in Gao (2022) and their examples. When hypothesis class is smoothly parameterized, for example, a bounded class of linear functions, Proposition 4.3 implies that is upper bounded by , which is independent of . Together with Proposition 4.2, it shows that converges to at rate .

4.2 MBAL-SPO with Hard Rejections

In this section, we develop excess risk bounds for the surrogate risk and the SPO risk, and present label complexity results, for MBAL-SPO with hard rejections. Our excess risk bounds for the surrogate risk hold for general feasible regions . To develop risk bounds for the SPO risk, we consider two additional assumptions on : (i) the case where satisfies the strength property, and (ii) the case where is polyhedral. The strength property, as defined in El Balghiti et al. (2022), is reviewed below in Definition 4.4.

Definition 4.4 (Strength Property for the Feasible Region )

The feasible region satisfies the strength property with constant if, for all and , it holds that

| (5) |

where is the distance to degeneracy function. We refer to as the strength parameter. \Halmos

The strength property can be interpreted as a variant of strong convexity that bounds the distance to the optimal solution based on the parameter as well as the distance to degeneracy . El Balghiti et al. (2022) demonstrate that the strength property holds when is polyhedral or a strongly convex set. In addition, for some of the results herein, we make the following assumption concerning the surrogate loss function, which states the uniqueness of the surrogate risk minimizer and a relaxation of Hölder continuity. {assumption}[Unique minimizer and Hölder-like property] There is a unique minimizer of the surrogate risk, i.e., the set is a singleton, and there exists a constant such that the surrogate loss function satisfies

It is easy to verify that the common squared loss satisfies Assumption 4.4 with when the hypothesis class is well-specified. In Lemma 8.6 in Appendix 8, we further show that the SPO+ loss satisfies Assumption 4.4 under some noise conditions.

Theorem 4.5 is our main theorem concerning MBAL-SPO with hard rejections and with general surrogate losses satisfying Assumption 4.4. Theorem 4.5 presents bounds on the excess surrogate and SPO risks as well as the expected label complexity after iterations.

Theorem 4.5 (General surrogate loss, hard rejection)

Suppose that Assumptions 3.1.1 and 4.4 hold, and that Algorithm 1 sets and updates the set of predictors according to the optional update rule in Line 20 with . Furthermore in Algorithm 1, for a given , let , for , , and for . Then, the following guarantees hold simultaneously with probability at least for all :

-

•

(a) The excess surrogate risk satisfies ,

-

•

(b) If the feasible region satisfies the strength property with parameter , then the excess SPO risk satisfies

-

•

(c) If the feasible region is polyhedral, then the excess SPO risk satisfies ,

-

•

(d) The expectation of the number of labels acquired, , deterministically satisfies .

In the polyhedral case, Theorem 4.5 indicates that the excess SPO risk of Algorithm 4.5 converges to zero at rate , and the expectation of the number of acquired labels grows at rate for small . (Usually, .) Note that Theorem 4.5 is generic in that the excess risk and label complexity bounds depend on the functions and . In Appendix 8, we give the explicit forms of these functions in some special cases of interest.

Remark 4.6 (Updates of )

In Theorem 4.5, the set of predictors is updated according to Line 20 in Algorithm 1. This is a technical requirement for the convergence when setting . This update process means that . By constructing these shrinking sets of predictors, we are able to utilize the information from previous iterations. Particularly, Lemma 4.9 below shows that these shrinking sets always contain the true optimal predictor under certain conditions. \Halmos

Remark 4.7 (Value of )

In Theorem 4.5, to find the best value of the parameter in part (b) that minimizes the excess SPO risk for sets satisfying the strength property, we observe that the choice of depends on , and . If satisfies that (1) , when , and (2) , when , then the excess SPO risk will converge to zero. For example, we can set , where . \Halmos

Auxiliary Results for the Proof of Theorem 4.5.

To achieve the risk bound in part (a) of Theorem 4.5, we decompose the excess surrogate risk into three parts. First, we denote the re-weighted surrogate risk for the features that are far away from degeneracy by , defined by:

where we use to denote and the expectation above is with respect to . Since and are i.i.d. random variables, and only depends on , can further be written as . Note also that, since , the re-weighted loss function can be written as , for a given . Next, for given and , we denote the discrepancy between the conditional expectation and the realized excess re-weighted loss of predictor at time by , i.e., . Lemma 4.8 shows that the excess surrogate risk can be decomposed into three parts.

Lemma 4.8 (Decomposition of the excess surrogate risk)

In the case of hard rejections, i.e., in Algorithm 1, for any given and , the excess surrogate risk of any predictor can be decomposed as follows:

The first part in Lemma 4.8 is the averaged excess surrogate risk for the hard rejected features at each iteration. Lemma 4.9 below further shows that is close to zero when .

Lemma 4.9

Suppose that Assumptions 3.1.1 and 4.4 hold where denotes the unique minimizer of the surrogate risk, and that Algorithm 1 sets and updates the set of predictors according to the optional update rule in Line 20 with . Furthermore, suppose that that , for , , and for . Then, for all , it holds that (a) , and (b) .

With Lemma 4.9, we can appropriately bound the first average of terms in Lemma 4.8, involving the expected surrogate risk when far from degeneracy. Thus, Lemmas 4.8 and 4.9 enable us to prove the excess surrogate risk bound in part (a). The proofs of the remaining parts follow by translating the excess surrogate risk bound to guarantees on the excess SPO risk and the label complexity.

4.3 Refined Bounds for SPO+ Under Separability

Next, we provide a smaller excess risk bound when using SPO+ as the surrogate loss, again in the case of hard rejections. The SPO+ loss function incorporates the structure of the downstream optimization problem and, intuitively, the excess SPO+ risk when far away from degeneracy will be close to zero when the distance is small and the distribution satisfies a separability condition, which we define below.

[Strong separability condition] There exist constants and such that, for all , with probability one over , it holds that:

-

•

(1) , and

-

•

(2) .

The following proposition shows that the separability condition leads to zero SPO+ and SPO risk in the polyhedral case. Indeed, the SPO+ loss is a generalization of the hinge loss and the structured hinge loss in binary and multi-class classification problems and is expected to achieve zero loss when there is a predictor function that strictly separates the cost vectors into different classes corresponding to the extreme points of (Elmachtoub and Grigas 2022). Assumption 4.3 and Proposition 4.10 formally define the notion of separability, wherein the distance between the prediction and the realized cost vector , relative to the distance to degeneracy of , is controlled.

Proposition 4.10 (Zero SPO+ risk in the polyhedral and separable case)

Assume that there exists and a constant such that with probability one over . When the feasible region S is polyhedral, it holds that and is a minimizer for both and .

As compared to Theorem 4.5, Theorem 4.11 below presents improved surrogate risk convergence guarantees for SPO+ under separability in the polyhedral case.

Theorem 4.11 (SPO+ surrogate loss, hard rejection, polyhedral and separable case)

Suppose that the feasible region is polyhedral, Assumptions 3.1.1 and 4.3 hold, and the surrogate loss function is SPO+. Suppose that Algorithm 1 sets and for all . Furthermore in Algorithm 1, for a given , let , for , , and for . Then, the following guarantees hold simultaneously with probability at least for all :

-

•

(a) The excess SPO+ risk satisfies ,

-

•

(b) The excess SPO risk satisfies ,

-

•

(c) The expectation of the number of labels acquired, , deterministically satisfies .

Remark 4.12 (Benefits of SPO+ Under Separability)

When using SPO+ in the separable case, the bound in part (a) of Theorem 4.11 is substantially improved as compared to Theorem 4.5. Intuitively, when an optimal predictor is far away from degeneracy and and are close, then the excess SPO+ risk of can be shown to be zero. As a result, the rejection criterion – which compares to a quantity that is related to the distance between and – is “safe” in the sense that whenever we can demonstrate that leads to a correct optimal decision with high probability. Thus, when using the SPO+ loss function, we can obtain a smaller excess SPO+ risk bound. Indeed, in Theorem 4.11, the value of is determined by the i.i.d. covering number, which implies that this risk bound is the same as the risk bound of supervised learning that labels all the samples. Furthermore, another benefit of SPO+ under the separability assumption is that we do not need to update at each iteration, which simplifies the computation substantially. Finally, Assumption 4.4 which assumes the minimizer is unique is not needed. \Halmos

Theorem 4.11 shows that the excess SPO+ risk converges to zero at rate , which equals the typical learning rate for the excess SPO+ risk in supervised learning. As Algorithm 1 requires much fewer labels, this demonstrates the advantage of active learning. In fact, the main idea of the proof of Theorem 4.11 is to show that actually, with high probability, achieves zero empirical SPO+ risk over all samples – including the cases where the label is not acquired. Indeed, in the separable case, the rejection criterion is “safe” and we are able to demonstrate that when . This of course implies that is an empirical risk minimizer for SPO+ across i.i.d. samples and we are able to conclude part (a).

4.4 MBAL-SPO with Soft Rejections

In this section, we analyze the convergence and label complexity of MBAL-SPO with soft rejection. We return to the setting of a generic surrogate loss function . Compared to the hard rejection case in Theorem 4.5, this positive will lead to a larger label complexity than Theorem 4.5. On the other hand, when is positive, we do not have to construct the confidence set of the predictors at each iteration. In other words, can be set as , for all as in Theorem 4.11. Thus, we do not have to consider additional constraints when minimizing the empirical re-weighted risk, which will reduce the computational complexity significantly. Theorem 4.13 is our main theorem for the MBAL-SPO under a general surrogate loss, which again provides upper bounds for the excess surrogate and SPO risk and label complexity of the algorithm.

Theorem 4.13 (General surrogate loss, soft rejection)

Suppose that Assumption 3.1.1 holds, and let and be given. In Algorithm 1, set for all , , for , for . Then, the following guarantees hold simultaneously with probability at least for all :

-

•

(a) The excess surrogate risk satisfies ,

-

•

(b) If the feasible region satisfies the strength property with parameter , then the excess SPO risk satisfies

-

•

(c) If the feasible region is polyhedral, then the excess SPO risk satisfies ,

-

•

(d) The expectation of the number of labels acquired, , deterministically satisfies .

Remark 4.14 (Value of and )

In part (d) of Theorem 4.13, depends on both and . When the exploration probability is large, in part (d) of Theorem 4.13 is large. On the other hand, in Theorem 4.13, the value of depends on , and furthermore is in the order of . It implies that when the exploration probability is small, is large, and in part (d) of Theorem 4.13 is large. Hence, to minimize the label complexity, there is a trade-off when choosing the value of . In Proposition 5.3, we will specify the value of and provide an upper bound for which is sublinear in . \Halmos

Although Theorem 4.13 does not require Assumptions 4.4 or 4.3, as will be shown later, to demonstrate the advantage of the supervised learning algorithm, another assumption, (Assumption 5.2), on the noise distribution is needed. We elaborate this in Section 5.2.

Setting Parameters in MBAL-SPO.

To conclude this section, we discuss the issue of setting the parameters for MBAL-SPO in practice. Although Theorems 4.5 and 4.13 provide the theoretical settings for the parameters and in the MBAL-SPO algorithm, how to set the scale of these parameters is an important question in practice. The complexity of the hypothesis class, the noise level and the distribution of features all impact the settings of these parameters. When the noise level is larger, or the cost vector is further away from the degeneracy, the scale of for the algorithms should be larger. In addition, to set a proper scale of the parameters in practice, we need to consider the tradeoff between the budget of the labels (or the cost to acquire each label) and the efficiency of the learning process. A reasonable practical approach is to set a “burn in” period of iterations where MBAL-SPO acquires all labels during the first iterations. One can then use the distribution of values for all previous features to inform the value of . For example, we can set the scale of as some order statistics of the past values for , e.g., the mean or other quantile depending on the practical cost of acquiring labels versus the rate at which feature vectors are collected. Then, the value of for can be updated according to the value of .

5 Risk Guarantees and Small Label Complexity Under Low Noise Conditions

To demonstrate the advantage of MBAL-SPO over supervised learning in Theorems 4.5 and 4.13, we need to analyze the functions and . In Appendix 8, we present some natural low-noise conditions such that we can provide concrete examples of under the SPO+ loss. In these examples, satisfies that . In Appendix 8, we further show that Assumption 4.4 holds for SPO+ and derive the upper bound for under some noise conditions. Given these results, in this section, we analyze the exact order of the label complexity and the risk bounds. These results demonstrate the advantages of MBAL-SPO.

5.1 Small Label Complexities

In this section, we analyze the order of the label complexity for both hard rejection and soft rejection. First, we characterize the noise as the level of near degeneracy in Assumption 5.1, which is similar in spirit to the low noise condition assumption in Hu et al. (2022).

[Near-degeneracy condition] There exist constants such that

Assumption 5.1 controls the rate at which – which measures the probability mass of features with small distance to degeneracy – approaches 0 as approaches 0. In other words, for small enough so that , when the parameter is larger the probability near the degeneracy is smaller at a faster rate. When the above near-degeneracy condition in Assumption 5.1 holds and satisfies that , we have the sublinear label complexity for the hard rejection in the polyhedral cases in Proposition 5.1.

Proposition 5.1 (Small label complexity for hard rejections)

Suppose that Assumptions 3.1.1, 4.4, 5.1 and the conditions in Proposition 4.3 hold. Suppose there exists a constant such that Assumption \theassumption.(2) holds with . Under the same setting of Algorithm 1 in Theorem 4.5, for a fixed , the following guarantees hold simultaneously with probability at least for all :

-

•

The excess surrogate risk satisfies .

-

•

The excess SPO risk satisfies .

-

•

The expectation of the number of labels acquired, conditional on the above guarantee on the excess surrogate risk, is at most for , and for .

The last claim in Propositon 5.1 indicates that the label complexity is sublinear. Notice that, as compared to Theorem 4.5, for simplicity, we state the bound on the label complexity conditional on the excess SPO+ risk guarantee that holds with probability at least . When , the label complexity is even finite. To compare this label complexity with supervised learning, we consider the excess SPO risk with respect to the number of labels . Let be a fixed value. Under the same assumptions and similar proof procedures, we can show that the excess SPO risk of the supervised learning is at most . In comparison, Proposition 5.1 indicates that the expected excess SPO risk of MBAL-SPO is at most . Thus, when , MBAL-SPO acquires much fewer labels than the supervised learning to achieve the same level of SPO risk. This demonstrates the advantage of MBAL-SPO over supervised learning.

Remark 5.2 (Small label complexity under separability condition with SPO+ loss)

Similar to the case of MBAL-SPO with hard rejections, when Assumption 5.1 and the condition that hold, we obtain sublinear label complexity of Algorithm 1 with soft rejections in Proposition 5.3.

Proposition 5.3 (Small label complexity for soft rejections)

Suppose Assumptions 3.1.1, 5.1 and the conditions in Proposition 4.3 hold. Suppose there exists a constant such that Assumption \theassumption.(2) holds with . Set and for all , and the same values as Theorem 4.13. For a fixed , the following guarantees hold simultaneously with probability at least for all :

-

•

The excess surrogate risk satisfies .

-

•

The excess SPO risk satisfies .

-

•

The expectation of the number of labels acquired, conditional on the above guarantee on the excess surrogate risk, is at most for .

In Proposition 5.3, the larger the parameter in near-degeneracy condition is, the smaller the label complexity will be. We observe that in Proposition 5.3, when , the excess surrogate risk converges to zero at rate , which is slower than the typical learning rate of supervised learning, which is . In the next section, we demonstrate that the excess surrogate risk can be reduced to under some further conditions.

5.2 Small Label Complexity with Soft Rejections.

In this section, we show that under certain conditions, the convergence rate of excess surrogate risk under soft rejection is , which is the same as standard supervised learning (except for logarithmic factors). To achieve this rate, we assume the near-degeneracy function satisfies Assumption 5.2.

[Lower bound for ] There exists , such that the near-degeneracy function satisfies , for all .

Remark 5.4

Assumption 5.2 says that the near-degeneracy function is at least in the order of . Here is the intuitive illustration of why we need a lower bound for the near-degeneracy function . If there is no lower bound for , then the features could be distributed far away from the degeneracy and could converge to zero at a very fast rate. In that case, the probability to have a near-degeneracy feature could be very small, and thus the probability to acquire the labels would be very small as well. That means the algorithm would have a slower speed to collect labels, and thus its learning rate would be slow. Therefore, a lower bound for in Assumption 5.2 is in need. This lower bound also implies that can not be great than 1, which is consistent with the common Tsybakov’s noise condition in the active learning literature, where the parameter of the Tsybakov’s noise condition (inverse of ), should be larger than 1. See Hanneke (2011) as an example. \Halmos

Proposition 5.5 shows that under Assumption 5.2 and other assumptions, the excess surrogate risk of active learning, converges to zero at rate , when .

Proposition 5.5

Suppose that Assumption 5.2 holds and there exists a constant such that Assumption 3.1.1 holds with . Suppose Assumption 5.1 holds with . Suppose that the surrogate loss function is Lipschitz for any given . Let for some . For a fixed , consider Algorithm 1 under the same settings as Theorem 4.13. Then, with probability at least .

In Proposition 5.5, Assumptions 5.1 and 5.2 mean that the near-degeneracy function is in the order of , i.e., . Proposition 5.5 implies that the excess surrogate risk converges to zero at rate , which is the same as the typical generalization error bound in the supervised learning except for the small logarithmic term. Thus, Proposition 5.5 implies that for the excess risk of the surrogate function, our active learning algorithm achieves the same order as the supervised learning. However, compared to supervised learning, active learning algorithms acquire much fewer labels. In illustration, when the near-degeneracy condition holds with , the label complexity of MBAL-SPO is in Proposition 5.3. Therefore, the MBAL-SPO can achieve the same order of surrogate risk with a smaller number of acquired labels.

6 Numerical Experiments

In this section, we present the results of numerical experiments in which we empirically examine the performance of our proposed margin-based algorithm (Algorithm 1) under the SPO+ surrogate loss. We use the shortest path problem and personalized pricing problem as our exemplary problem classes. For both problems, we use (sub)gradient descent to minimize the SPO+ loss function in the MBAL-SPO algorithm. We set and set according to Theorem 4.13. The norm is set as the norm. In both problems, to calculate the distance to the degeneracy, we use the result of Theorem 8 in El Balghiti et al. (2022), which was stated in Equation (4). We set the function as the square root function, which is used directly in the setting of the sequence . The numerical experiments were conducted on a Windows 10 Pro for Workstations system, with an Intel(R) Xeon(R) Silver 4114 CPU @ 2.20GHz 20 cores.

6.1 Shortest Path Problem

We first present the numerical results for the shortest path problem. We consider a (later also a ) grid network, where the goal is to go from the southwest corner to the northeast corner, and the edges only go north or east. In this case, the feasible region is composed of network flow constraints, and the cost vector encodes the cost of each edge.

Data generation process.

Let us now describe the process used to generate the synthetic experimental data. The dimension of the cost vector is 12, corresponding to the number of edges in the grid network. The number of features is set to 5. The number of distinct paths is 6. Given a coefficient matrix , the training data set and the test data set are generated according to the following model.

1. First, we identify six vectors , , such that the corresponding cost vector is far from degeneracy, that is, the distance to the closest degenerate cost vector is greater than some threshold, and the optimal path under the cost vector is the path .

2. Each feature vector is generated from a mixed distribution of six multivariate Gaussian distributions with equal weights. Each multivariate Gaussian distribution follows , where the variance is set as .

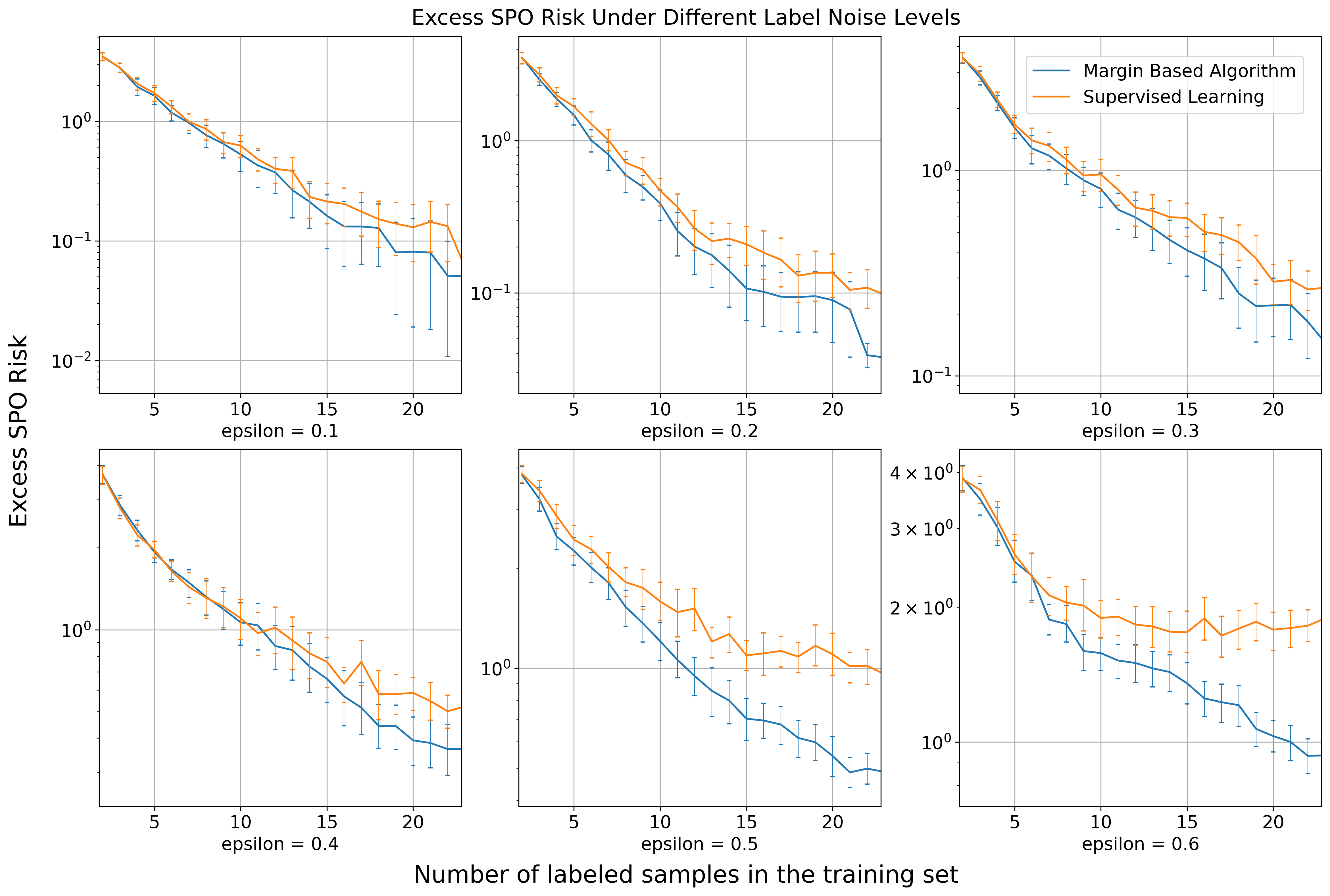

3. Then, the cost vector is generated according to , for , where is the row of the matrix . The degree parameter is set as 1 in our setting and is a multiplicative noise term, which is generated independently from a uniform distribution . Here, is called the noise level of the labels.

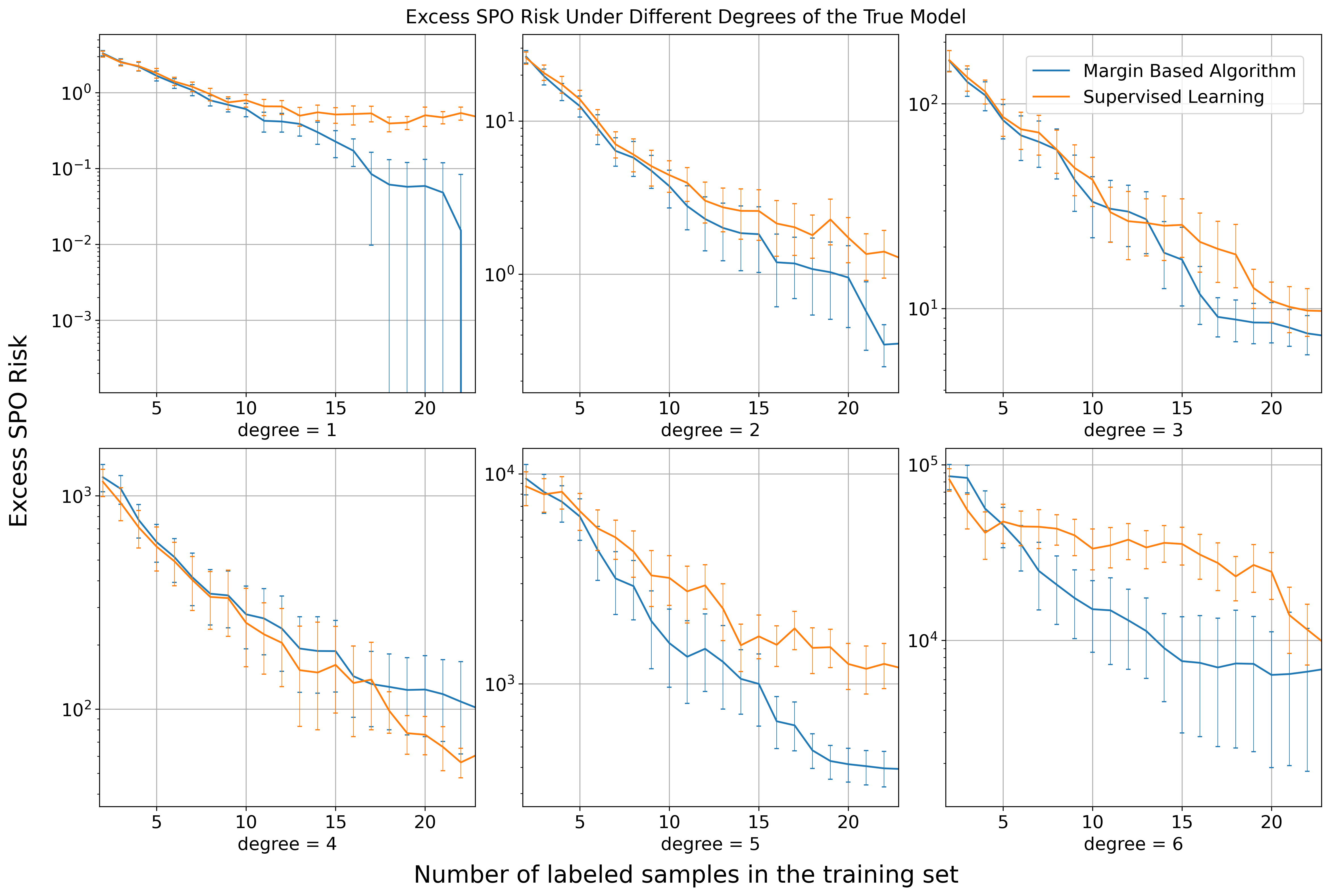

To determine the coefficient matrix , we generate a random candidate matrix multiple times, whose entries follow the Bernoulli distribution (0.5), and pick the first such that exists in Step 1 for each . The size of the test data set is 1000 sample points. In the context of our margin-based algorithm, we set , where is the iteration counter, is the dimension of the cost vector, and is set as . According to Proposition 5.3, we set . The running time for one single run on a grid to acquire 25 labels is about 10 minutes for the margin-based algorithm.

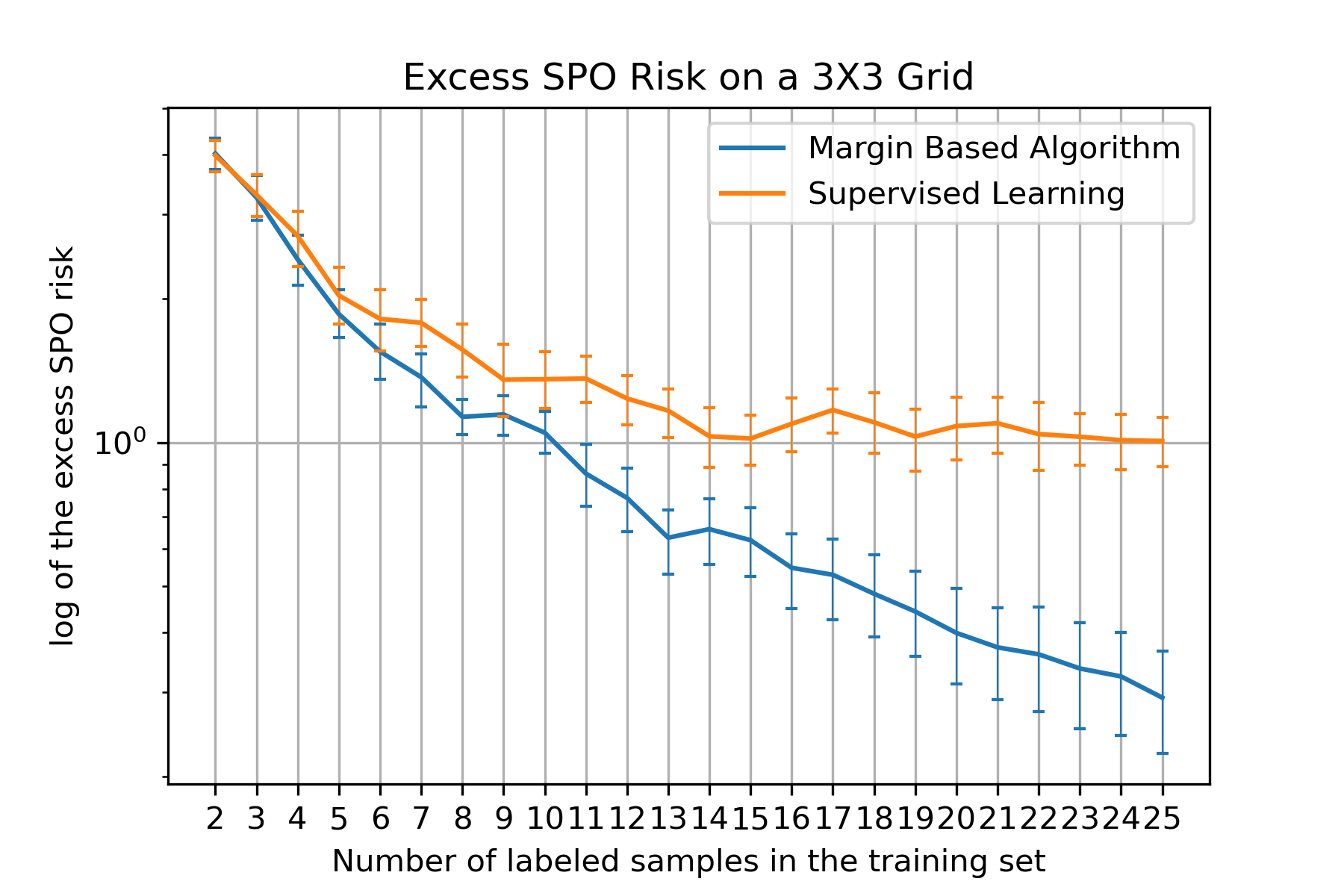

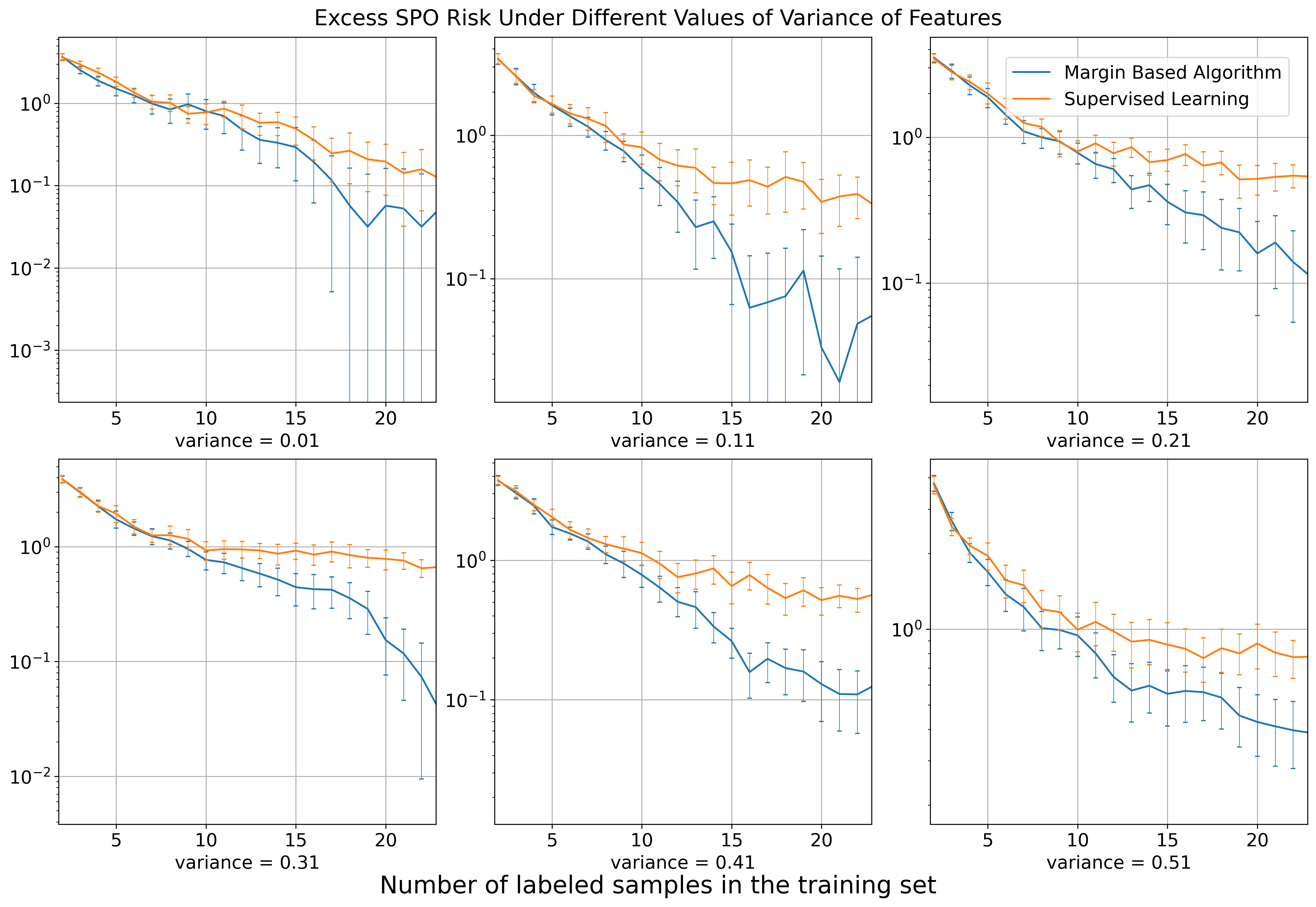

Figure 3 shows our results for this experiment. Excess SPO risks during the training process for MBAL-SPO and supervised learning are shown in the left plot of Fig. 3. The x-axis shows the number of labeled samples and the y-axis shows the log-scaled excess SPO risk on the test set. The results are from 25 trials, and the error bar in Figure 3 is an 85% confidence interval. We observe that as more samples are labeled, the margin-based algorithm performs better than supervised learning, as expected. Compared to supervised learning, the margin-based algorithm achieves a significantly lower excess SPO risk when the number of labeled samples is around 25.

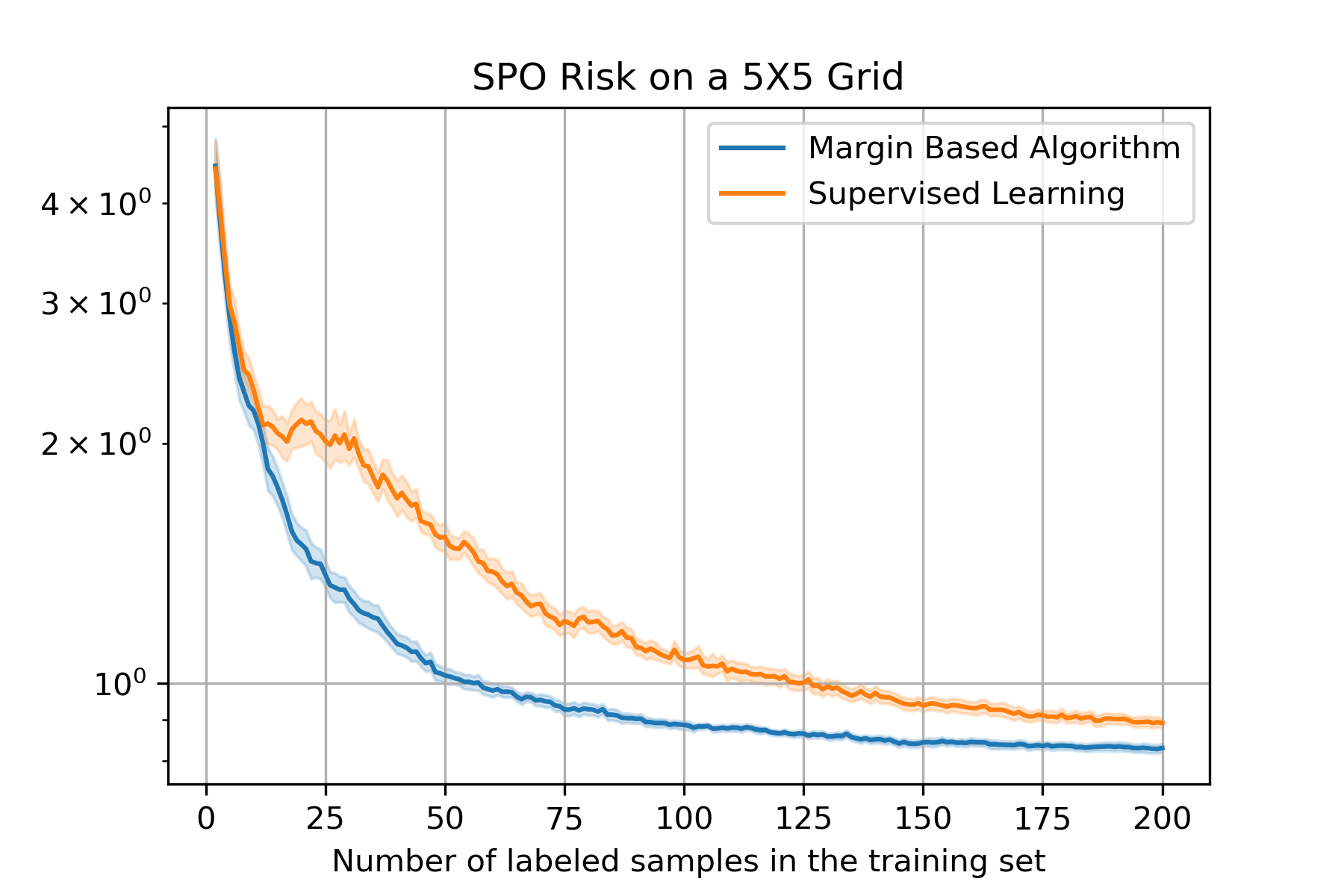

The margin-based algorithm has good scalability as long as the calculation of the distance to the degeneracy is fast, for example, in the case of relatively simple polyhedral sets. To further examine the performance of the margin-based algorithm on a larger-scale problem, we conduct a numerical experiment in a grid network in the right plot of Figure 3, again shown with an 85 % confidence interval. We see that although both algorithms converge to the same optimal SPO risk level, the margin-based algorithm has a much faster learning rate than supervised learning and can achieve a lower SPO risk even after 200 labeled samples.

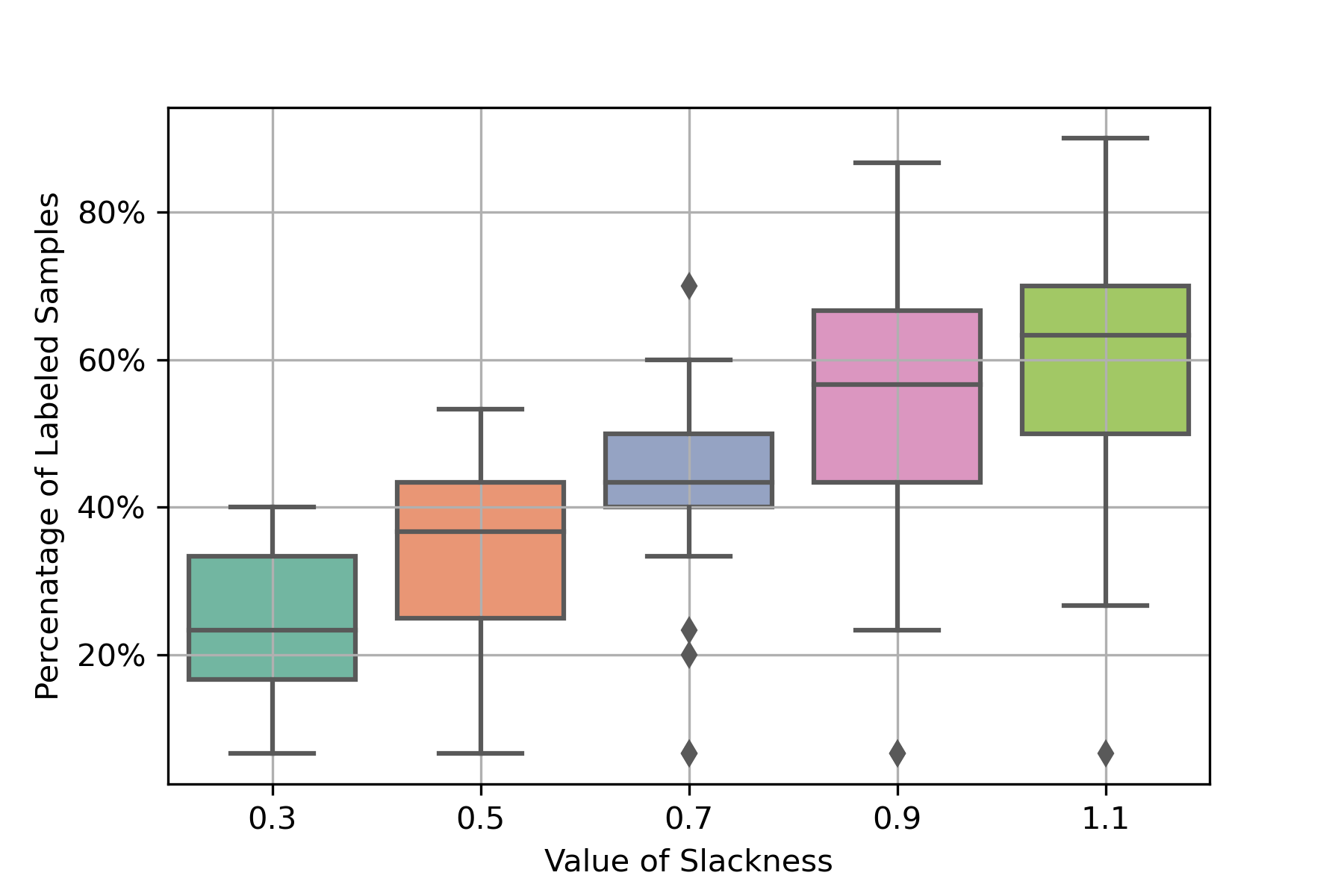

In Appendix 10.1, we further examine the impacts of the scale of parameters, and , on the number of labels and the SPO risk during the training process, which demonstrates the robustness of the SPO risk with respect to the scales of these parameters. In Appendix 10.2, we include more results in which we change the noise levels and variance of the features when generating the data. This verifies the advantages of our algorithms under various conditions.

6.2 Personalized Pricing Problem

In this section, we present numerical results for the personalized pricing problem. Suppose that we have three types of items, indexed by . We have three candidate prices for these three items, which are , and . Therefore, in total, we have possible combinations of prices. Suppose that the dimension of the features of the customers is . When a customer is selected to survey, their answers will reveal the purchase probability for all three items at all possible prices. These purchase probabilities are generated on the basis of an exponential function of the form . We add additional price constraints between products, such that the first item has the highest price, and the third item has the lowest price. Please see the details in Appendix 10.3.

Because there are three items and three candidate prices, the dimension of the cost vector is . Therefore, our predictor is a mapping from the feature space to the label space . We assume that the predictor is a linear function, so the coefficient of is a matrix, including the intercept. Unlike the shortest path problem which can be solved efficiently, the personalized pricing problem is NP-hard in general due to the binary constraints. In our case, since the dimensions of products and prices are only three, we enumerate all the possible solutions to determine the prices with the highest revenue.

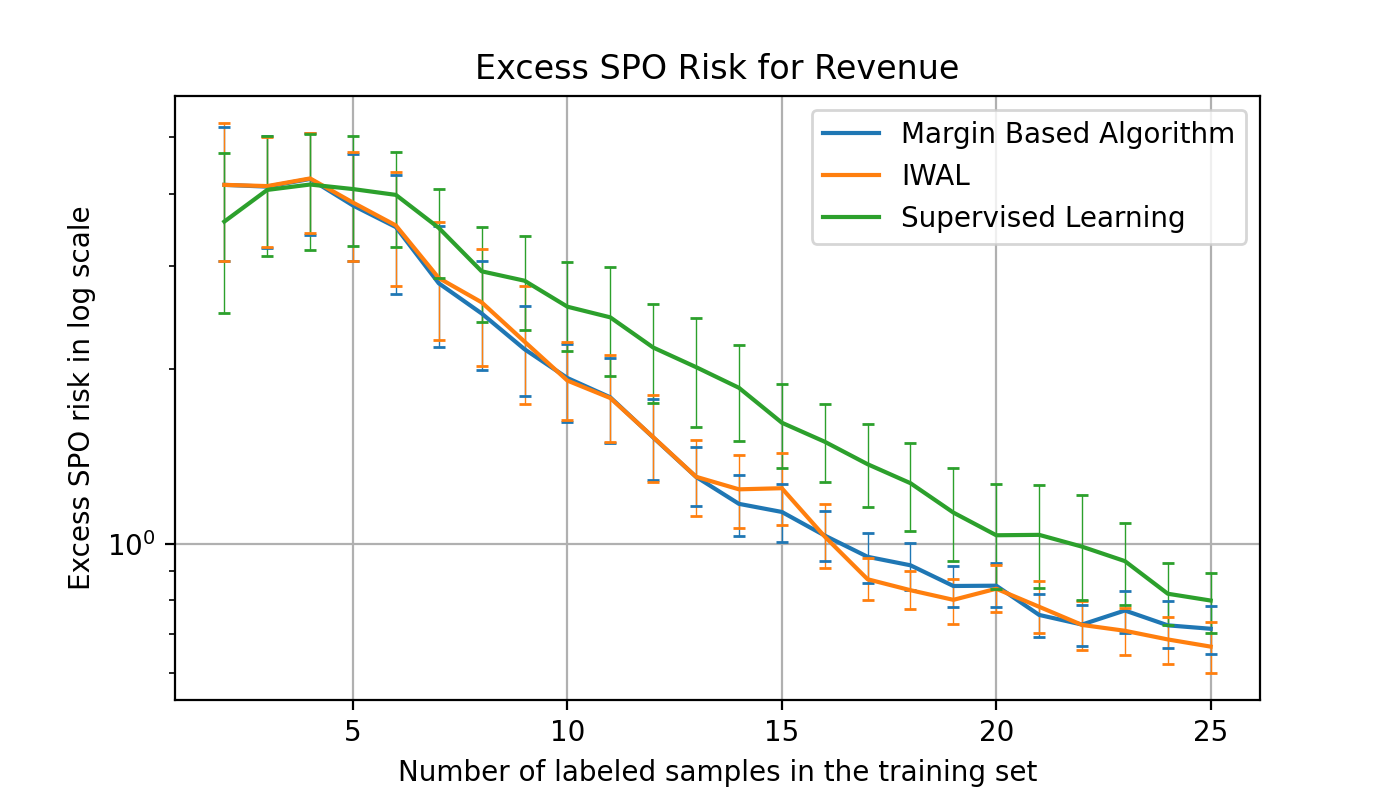

The test set performance is calculated on samples. In MBAL-SPO, we set , where is the iteration counter, is the dimension of the cost vector, which is 9, and is set as . According to Proposition 5.3, we set . The scales of and are selected by the rules discussed at the end of Section 4.4. The excess SPO risks of MBAL-SPO and supervised learning on the test set as the number of acquired labels increases are shown in Figure 4. The results are from 25 simulations, and the error bars in Figure 4 represent an 85% confidence interval. Notice that the demand function is in an exponential form but our hypothesis class is linear, so the hypothesis class is misspecified. The results in Figure 4 show that MBAL-SPO achieves a smaller excess SPO risk than supervised learning even when the hypothesis class is misspecified.

7 Conclusions and Future Directions