Mixture Quantiles Estimated by Constrained Linear Regression

Abstract

The paper considers the problem of modeling a univariate random variable. Main contributions: (i) Suggested a new family of distributions with quantile defined by a linear combination of some basis quantiles. This family of distributions has a high shape flexibility and covers commonly used distributions. (ii) Proposed an efficient estimation method by constrained linear regression (linearity with respect to the parameters). Various types of constraints and regularizations are readily available to reduce model flexibility and improve out-of-sample performance for small datasets . (iii) Proved that the estimator is asymptotically a minimum Wasserstein distance estimator and is asymptotically normal. The estimation method can also be viewed as the best fit in quantile-quantile plot. (iv) Case study demonstrated numerical efficiency of the approach (estimated distribution of historical drawdowns of SP500 Index).

1 Introduction

Building a model for univariate distribution involves a trade-off between interpretability, flexibility and tractability. This paper studies a family of distributions that is sufficiently flexible to accommodate most distributions considered in practice, while being straightforward to interpret and estimate.

The suggested family of distributions is similar to the mixture of probability densities constructed by a weighted sum of basis density functions (i.e., cumulative probability function (CDF) is a weighted sum of the basis CDFs). We consider a new family of distributions with quantile (inverse CDF) defined by a weighted sum of some basis quantiles. The idea of quantile aggregation dates back to Vincent (1912). The reader is referred to Ratcliff (1979) for a detailed review and further development. Their motivation is to estimate the population distribution by averaging some known distributions obtained from individuals with equal weights, while we aim to approximate quantiles with a linear combination of basis quantiles. Various types of basis quantile functions have been earlier considered: orthogonal polynomials (Sillitto, 1969), quantiles of normal and Cauchy distribution mixed with linear and quadratic terms (Karvanen, 2006), and quantile of modified logistic distribution (Keelin and Powley, 2011).

Earlier considered approaches are limited in the choice of basis functions and do not guarantee nondecreasingness of the resultant quantile function. Our approach addresses these two issues. The type and number of basis functions in the weighed sum are arbitrary, as long as they are valid quantile functions. We propose to use quantiles of common distributions such as normal and exponential, especially when prior knowledge on the shape of the distribution is available. For more complicated cases, such as multimodal distributions, we can use, for example, the monotone I-spline basis (Ramsay, 1988). Moreover, Papp (2011), Papp and Alizadeh (2014) show that piecewise I-spline with non-negative coefficients can approximate any bounded continuous nondecreasing function. Quantiles of known distributions and the I-spline basis are both continuous and nondecreasing. Therefore, the nondecreasingness of the estimated function is guaranteed by nonnegativity of the weights (sum of nondecreasing functions with non-negative weights is nondecreasing). While Gaussian mixture densities is considered a parametric model, the mixture splines (estimating quantile) is considered a nonparametric model. However, the mixture of splines still has a simple closed-form expression and great flexibility. Monte Carlo simulation can be easily conducted by inverse transform sampling.

To fit the model, we propose to minimize the distance between the sample quantile function and the model at sample probabilities (confidence levels111Both terms are used in this paper.). The distance is determined by the type of error function we choose. We formulate the estimation problem as a constrained linear regression. This approach differs from existing ones. The minimum quantile distance estimation (LaRiccia, 1982; Millar, 1984; Gilchrist, 2007) minimizes the difference between the sample quantile function and the model. Such approach is also widely studied in the literature of minimum Wasserstein distance (Kantorovich–Rubinstein distance) estimator (Bassetti and Regazzini, 2006; Bassetti et al., 2006; Bernton et al., 2019). However, the difference is an integral in the unit interval rather than at sample probabilities. Maximum likelihood estimation (MLE) is inconvenient to use for our model since it requires the derivative of the inverse of sum of quantile functions. Moreover, the optimization problems of mentioned approaches are nonconvex. In contrast, our formulation of linear regression with linear constraints is a convex optimization problem allowing for efficient computation with powerful convex programming solvers. One more method having efficient optimization, Lariccia and Wehrly (1985), uses only a fixed number of quantiles. Moment fitting and the analogous L-moment fitting (Hosking, 1990; Karvanen, 2006) requires calculating unstable high-order moments of the data. We show that L-moment fitting can be incorporated into our framework as a linear constraint. The quantile regression approach in Peng and Uryasev (2023) considers a different objective function which is equivalent to the sum of continuous ranked probability score (Matheson and Winkler, 1976). If there is only one basis function in the model, our proposed estimation method reduces to estimating the location and scale parameters of a distribution by weighted least squares regression (Ogawa, 1951; Lloyd, 1952). Using a similar method, Kratz and Resnick (1996) estimates the tail index of Pareto distribution with logarithm-transformed data.

We studied asymptotic properties of the estimator and demonstrated that the estimator is asymptotically minimum -Wasserstein (Kantorovich–Rubinstein) distance estimator, when the error function is norm222To avoid confusion between in probability and in norm, we use for the norm.. This is proved by viewing the objective function of the optimization as a Monte Carlo integration of the difference between two quantile functions. Different from Bassetti and Regazzini (2006); Bassetti et al. (2006); Bernton et al. (2019), the objective function in our approach is not the -Wasserstein distance between the empirical quantile function and the model in the nonasymptotic case. The convergence of the objective value to the Wasserstein distance allows for the parameter estimation and the goodness-of-fit test in one shot, since the Wasserstein distance can be used for goodness-of-fit test (Barrio et al., 2005; Panaretos and Zemel, 2019). We also prove the consistency of the estimator using theorems developed for minimum distance estimator in Newey and McFadden (1994). We proved the asymptotic normality of the estimator with a fixed number of quantiles using order statistics (Balakrishnan and Rao, 2000). This is a special case of the result in Lariccia and Wehrly (1985).

Alternatively, the distance between the model and the empirical quantile function at sample probabilities can be viewed as the sum of horizontal distances of sample points to the straight line in a quantile-quantile plot (Q-Q plot). Thus the fitted model makes the sample points as close to as possible. Loy et al. (2016) uses Q-Q plots for hypothesis testing.

We use constraints and regularization in regression to improve out-of-sample performance for small datasets. Cardinality constraint limits the maximum number of basis functions selected from a large number of candidates. Mixed integer linear programming (MILP) solvers are very effective for such problems. We compare numerical performance of the suggested algorithm with LASSO regression (Santosa and Symes, 1986; Tibshirani, 1996).

The paper is organized as follows. Section 2 describes the mixture quantiles model and section 3 defines the regression optimization problem. Section 4 proves the relation to minimum Wasserstein estimator. Section 5 proves the asymptotic normality of the estimator. Section 6 discusses some properties of the estimator obtained by weighted least squares regression. Section 7 discusses various constraints, penalties and error functions in the optimization problem. Section 8 contains two numerical experiments. Section 9 concludes the paper.

2 Mixture Quantiles Model

Notations:

-

•

number of basis quantile functions in the mixture quantiles model;

-

•

confidence level;

-

•

= vector of (unknown) non-negative coefficients;

-

•

= basis quantile functions, where ;

-

•

quantile model with confidence level and parameter ;

-

•

inverse function of with respect to .

This section introduces the mixture quantiles model (linear combination of quantiles) and formulates a linear regression problem for parameter estimation. We consider real-valued continuous random variables defined on a probability space with a distribution function . The -quantile is defined by . If consists of random samples from , is called the sample -quantile.

A location-scale family of distributions is obtained by scaling and translation a random variable with a fixed distribution. Consider an arbitrary quantile function . The quantile function of the location-scale family generated by quantile function is defined by

| (1) |

where is the location parameter and is the non-negative scale parameter. We construct a new family of quantile functions obtained by linearly combining quantile functions from different location-scale families. This new family differs from the mixture densities constructed with these selected distributions.

Model formulation

The mixture quantiles model is defined by

| (2) |

where . The functions can be any monotone non-decreasing function defined on the unit interval. are linearly independent functions, i.e., any function cannot be represented by a linear combination of . We propose two types of basis functions: quantile functions of common distributions and monotone I-spline basis (Ramsay, 1988). When prior knowledge on the shape of the distribution is available, the common quantile functions such as those of normal and exponential distributions are preferred, while the splines are needed for more complicated case such as multimodal distribution. Papp (2011); Papp and Alizadeh (2014) show that piecewise I-spline with non-negative coefficients can approximate any bounded continuous nondecreasing function. We focus on common quantile functions in this study.

The density corresponding to is given by . While all distributions in one location-scale family have equal skewness, the sknewness of the distribution with quantile function is dependent on nonlinearly if there are more than one quantile function in the mixture.

The quantile functions , considered in this paper, are standardized in the following way. For two-tailed distribution, is standardized to have zero 0.5-quantile and unit interquartile range, i.e., , . For one-tailed distribution, is standardized to have zero zero-quantile and unit interquartile range, i.e., , . We do not standardize by mean and variance since they may not exist for some fat-tailed distributions.

3 Parameter Estimation by Constrained Linear Regression

Notations:

-

•

sample size;

-

•

number of selected confidence levels;

-

•

= selected confidence levels in ascending order;

-

•

sample -quantiles of observations;

-

•

vector of sample quantiles of observations in ascending order;

-

•

;

-

•

matrix of regression factors.

We want to find a quantile function parametrized by , which is closest to the sample data. The distance is measured between the sample quantile function and at some selected confidence levels . The estimation problem is formulated as a linear regression problem. We can describe the setting in a matrix form

| (3) |

are the differences between the sample and the -quantile of the model. are not independent or identical. Note that is not necessarily the total number of observations. When , is the vector of all samples in ascending order. Sections 4 and 5 discuss two cases. The first case uses all available observations as , i.e., . The second case uses a fixed number of the observations as .

Optimization Problem Statement

Distance minimization problem is

| (4) |

where is a feasible set, is an error measure. Various errors, , can be considered, but this paper focuses on weighted norm. In particular, we consider the weighted least absolute deviation regression and weighted least squares regression corresponding to the weighted and norms. Other possible choices are the regular measures of error axiomatically defined in Rockafellar and Uryasev (2013). It is possible to add penalty terms to the objective function. Section 7 discusses constraints, penalties and error measures in the optimization problem.

Estimation of Probabilities

Consider the case where . Observe that if are exactly the true probabilities where is the true parameter, then is an optimal solution, regardless of the choice of the error , since the error equals its minimum zero value. In such case, we have , . Since the true probabilities are not known, we select a reasonable estimator

| (5) |

Note that the -th sample in ascending order is an asymptotically unbiased estimator of the -quantile of the random variable with quantile function . There is no consensus on how to best define the sample quantiles (Hosseini and Takemura, 2016). With a finite sample size, we need to analyze bias introduced in the procedure. The sample set can be regarded as being generated by where are i.i.d. samples from uniform distribution on in ascending order. Taylor’s Theorem implies

| (6) | ||||

Since follows a Beta distribution , see (Balakrishnan and Rao, 2000), we have . When the small term can be ignored, the sign of the bias is determined by the sign of the second derivative , while the scale is determine the variance . For quantile functions that are concave on the left end and convex on the right end, using has a positive bias for close to and a negative bias for close to . Hence, the heaviness of the tail tends to be underestimated.

Since if is the true probability , the residual can be viewed as the consequence of an estimation error of . Alternatively, we can view as a random residual of sampling the -quantile. In the asymptotic theory of order statistics applied in Section 5, is proved to asymptotically follows a normal distribution with mean equal to the -quantile. That is, asymptotically follows a normal distribution with mean zero.

The two interpretations lead to different approach to dealing with outliers in the estimation. If we view the residual as the consequence of an estimation error of , we should find better estimate on for the outliers. It could be beneficial to partly correct the bias by shrinking the probabilities toward , e.g., using for close to and for close to . Since the true distribution is not known in practice, it is difficult to find an optimal modification method. Ogawa (1951) treats as free variables and minimizes the variance of the estimator. The procedure, called optimal spacing in related literature (Pyke, 1965, 1972; From, 1989) involves non-linear non-convex optimization problems that are difficult to solve. On the other hand, if are regarded as noise from sampling, we can assign small weights to the outliers as is commonly done in linear regression to mitigate the impact.

Q-Q Plot

In a Q-Q plot, the horizontal distance between a data point and the straight line is . Thus the estimation problem 4 can be viewed as obtaining the best Q-Q plot by minimizing the average distance between the data points and the straight line. It is known from empirical evidence that the Q-Q plot of samples against true quantiles often exhibits a noticeable deviation from the straight line at both ends, where extreme values reside. This finding provides additional support for the proposed downweighting approach suggested in eariler discussion of the sample probabilities.

4 Minimum Wasserstein Distance Estimator

Notations:

-

•

non-negative weights;

-

•

non-negative integrable weight function;

-

•

;

-

•

feasible set;

-

•

-th row of matrix with dimension

-

•

weighted variant of objective function in (4);

-

•

;

-

•

estimator with sample size ;

-

•

;

-

•

true parameter vector;

-

•

The weighted Wasserstein distance between two distributions with quantile functions and is defined by

(7)

This section considers the case where the number of selected confidence levels is equal to the sample size . We have , . We prove that the estimator is asymptotically the minimum Wasserstein distance estimator. The model is said to be correctly specified if the true quantile function is in the form of (2) and the true parameter is in the interior of the feasible set .

Proposition 1

If (i) is a unique minimizer of ; (ii) is an element in the interior of a convex set , then . If the model is correctly specified, then is a consistent estimator.

Proof. is a convex function with respect to . , due to (8). The rest is proved by applying Theorem 2.7 of Newey and McFadden (1994). If the model is correctly specified, we have .

Since are linearly independent, if and only if for . Thus if the model is correctly specified, there exists a unique minimizer , i.e., the assumption (i) is automatically satisfied. Proposition 1 is a general result that holds for convex error functions .

Proposition 2

For , converges in probability to the weighted -Wasserstein distance between the model and true quantile function .

Proof. We can view the function in the limit as a Monte Carlo integration. The convergence is derived by standard argument (Robert et al., 1999)

| (8) |

Note that although the estimator converges to the one that minimizes the -Wasserstein distance between the model and true quantile function, the objective function is not the -Wasserstein distance.

Furthermore, with the linear formulation with respect to , we can bound the -Wasserstein distance by the scaled distance between the estimator and true parameters.

Proposition 3

Suppose (i) the conditions in Proposition 1 are satisfied; (ii) the model is correctly specified; (iii) , where is a constant. Then the -Wasserstein distance between the model and true distribution is bounded by the scaled distance between the estimator and true parameters.

Proof. Since the model is correctly specified, we have . Thus . We have

| (9) | ||||

The inequality is due to subadditivity of . By Proposition 1, we have that .

Proposition 3 holds for any convex and positively homogeneous error function. For a random variable with quantile function , the lower and upper partial -moments with a reference confidence level are defined by and , respectively (for definition and application in finance, see Bawa and Lindenberg (1977)). When , the condition is equivalent to that the random variables with quantile function have finite lower and upper partial moments.

5 Asymptotic Normality

Notations:

-

•

inverse function of with respect to ;

-

•

weight matrix;

-

•

asymptotic covariance matrix of difference between sample quantile and true quantile, ;

-

•

;

-

•

;

-

•

vector of true quantiles of confidence levels .

We study an estimator that selects a fixed number of confidence levels in this section. This is in contrast to Section 4 where . The estimator is more robust to outliers since only the sample -quantiles are used in the regression. Here we consider the weighted norm as the error measure in (4). The proof of the following proposition is similar to Ogawa (1951) but presented in matrix form.

Proposition 4

If (i) is differentiable w.r.t. ; (ii) the density function is positive and bounded; (iii) is invertible, then

-

•

The estimator converges in distribution to the normal distribution

(10) -

•

The optimal weight for the best linear unbiased estimator (BLUE) that minimizes the variance is

(11) -

•

The optimal estimator obtained with the optimal weight converges in distribution to a normal distribution

(12) where .

Proof. The difference between the sample quantiles and true quantiles asymptotically follows the normal distribution (Arnold et al., 2008),

| (13) |

The solution to the estimation problem (4) has a closed-form expression

| (14) |

Let . Substituting with leads to

| (15) |

Thus

| (16) |

With (13), we have

| (17) |

where

| (18) |

By the generalized Gauss-Markov Theorem (Aitken, 1936), the best linear unbiased estimator is obtained by the following weight matrix

| (19) |

Substituting with in (18) gives the optimal estimator in (12).

Lariccia and Wehrly (1985) studies a general case where is not linear with respect to . The asymptotic normality is proved directly with the inverse function theorem and Taylor series expansion. The resultant optimal weight matrix is the same as what we obtain in (19).

The weight matrix obtained in (11) is not directly applicable, since it requires knowing the covariance matrix, which is a function of the unknown density. The feasible weighted least squares regression uses an estimated covariance matrix to replace matrix in the regression. It can be obtained by calculating the covariance matrix of the residuals of ordinary least squares regression, or by plugging point density estimation in matrix . Though these estimators may result in suboptimal weight, empirical results in Ergashev (2008) show that the impact is insignificant as long as the extreme tail observations are assigned with small weights.

6 Discussion of Estimation with Weighted Least Squares Regression

This section discusses some properties of the estimator obtained by weighted least squares regression. Since the sample size does not play a role in the conclusion of this section, we omit the superscripts and subscripts . The objective function equals

| (20) |

where is a symmetric positive-definite weight matrix. The estimator has a closed form solution

| (21) |

Notice that are linear combinations of the observations . Thus, it can be regarded as an L-estimator (David and Nagaraja, 2004). The results in this section all hold for symmetric matrix .

6.1 Equivariance

We introduce the following notations:

-

•

the estimator;

-

•

the estimator with scaled standard distributions and scaled and shifted ;

-

•

= diagonal matrix of scale parameters of ;

-

•

= location shift vector of data ;

-

•

;

-

•

scale parameter of data .

The estimator obtained by weighted least squares regression possesses nice properties such as location-scale equivariance (Lehmann and Casella, 2006). In addition, we can study the impact of nonnormalized basis quantile function. If we replace a quantile function in the mixture with a scaled one , the scale estimator becomes while the other scale parameters and the location parameter do not vary. These properties can be obtained by the following direct matrix calculation using the closed form solution (21)

| (22) |

6.2 Model with Single Basis Function

We consider the simplest case where there is only one component in the mixture and the error function is norm. We estimate the location and scale parameters , in a location-scale family with ordinary least squares regression. Using identity matrix as in (21), we obtain

| (23) |

where , . Both the location and the scale estimator are a weighted sum of the observations . If the true distribution is symmetric, we have . We have that is the sample mean . If the observations equal exactly the -quantiles of the true distribution, i.e., , we recover the true parameters , .

7 Constraints, Penalties and Error Function in Optimization

Linear regression can be combined with various standard techniques. Imposing constraints and using robust error functions can improve the estimator especially when the sample size is small. When there is a large number of quantile functions in the mixture, we can select a few most important ones by imposing a cardinality constraint. Alternatively, a penalty on non-zero parameters can be added to the objective function.

7.1 Constraints

This subsection lists some important constraints to be used in the regression.

Non-negativity Constraint

The non-negativity constraint

| (24) |

which we denote by , ensures that the function is monotone increasing, and thus a valid quantile function. It is found in preliminary numerical experiments that frequently contains negative elements without the non-negativity constraint when the sample size is small.

Cardinality Constraint

The cardinality constraint controls the maximum number of non-zero values in to mitigate overfitting. The constraint is defined with the cardinality function,

| (25) |

where is the indicator function that equals 0 when the statement in the bracket is true and 0, if false. The cardinality constraint can be transformed to a mixed integer linear systemn of constraints one by introducing auxiliary integer variables

| (26) | ||||

where and are upper and lower bounds for . Mixed integer linear programming can be effectively solved using powerful solvers, such as GUROBI. The caridinality constraint allows for including a large number of quantile functions in the initial mixture.

VaR and CVaR Constraints

Since we assign tiny weights to tail observations, the fitted distribution could underestimate the heaviness of tail. By imposing constraints on the tail behavior, we can better encode the tail risk demonstrated by the data or obtained from expert knowledge.

The quantile is also called Value-at-Risk (VaR) in finance. CVaR is a popular risk measure in finance and engineering that accounts for the average of the tail of a distribution (Rockafellar and Uryasev, 2000, 2002). The -CVaR of a random variable with quantile function is defined by . Equivalently, CVaR for a continuous distribution is the average outcome exceeding the -quantile and thus contains more information on the tail than -quantile. From the definition we observe that the -CVaR of is linear with respect to parameters .

The -quantile constraint is defined by

| (27) |

and the -CVaR constraint is defined by

| (28) |

where are constants. The direction of the inequality sign indicates that we do not want to underestimate the upper tail risk, but similar we can control the lower tail as well.

L-moment Constraints

The L-moments are defined by a linear combination of order statistics. These moments can characterize a distribution (Hosking, 1990), similar to the moments of a distribution, but are more robust to outliers. With an abuse of notation, denote by the -th L-moment of a sample set of a random variable whose quantile function is , and by the vector of L-moments .

Hosking (1990) gives the analytical expression of L-moment where is a polynomial. We observe that the L-moment of a sum of quantile function of is linear with respect to

| (29) |

where .

L-moment fitting in Karvanen (2006), analogous to method of moments, matches the L-moments of data and the model. For our estimation problem, we propose a constraint that bounds the error of L-moments of fitted distribution from the empirical -moments as follows

| (30) |

L-moment fitting is a special case of this procedure, since the feasible set shrinks to the optimal solution of L-moment fitting as . The constraint (30) is equivalent to the following system of linear constraints with auxiliary variables ,

| (31) | ||||

7.2 Error Function and Penalty

While this paper mainly considers weighted mean squared error and mean absolute error, other error functions for can be chosen, as well. For example, the robust Huber error (Huber, 1964) combining mean squared and mean absolute errors can be useful for handling outliers.

There is numerous research on regularized optimization in statistics. For example, LASSO regression achieves sparsity in the parameters by adding an penalty to the objective function. The optimization problems can be reduced to linear or convex programming and serve as a good heuristic for optimization with a cardinality constraint. We compare the performance of LASSO regression with regression imposed with a cardinality constraint in the numerical study.

8 Case Study

This section includes two numerical experiments demonstrating effectiveness of our approach. Wee consider the case where the number of selected confidence levels is equal to the sample size in both experiments. The first experiment fits the model to the data sampled from a known distribution. By increasing the sample size, we observe that both the objective value and the distance between the fitted model and the true model converge to zero. This provides empirical support for Propositions 1 and 2 in the setting of correctly specified model. The second experiment applies our method to real-world data. We fit the mixture of generalized beta distributions of the second kind to historical drawdowns of SP500 stock market index. We compare performance of minimizing and norm with the cardinality constraint and penalty. Maximum likelihood estimator is also included as a benchmark. The non-negativity constraints for coefficients were imposed in all problems. We test with different cardinality constraint and penalty. The optimization was done with the optimization package Portfolio Safeguard (Zabarankin et al., 2016).

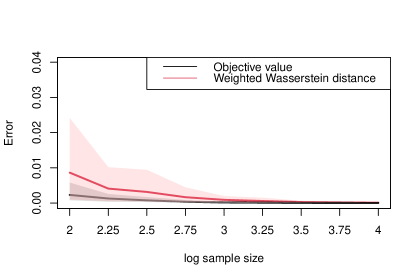

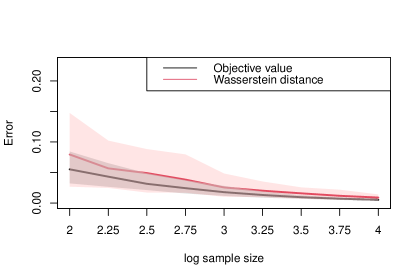

8.1 Simulation and Analysis of Convergence

We fit the model to the sample data-set generated by a mixture of skewed distributions. We calculated distance between the quantile functions of the underlying data-generating model and of the fitted model. Section 4 shows that the objective value of (4) converges to the -Wasserstein distance. We show with graphs that as the sample size increases, the distance between the model quantile function and the true quantile function tends to zero, and that the objective value tends to zero.

Fernandez and Steel (1998) modifies skewed distribution by scaling the two sides of the density function differently. Similarly, we modify skewed distribution by scaling differently the positive and negative sides of the quantile function. The quantile function of the skewed distribution is defined by

| (32) |

where , , are the probability, skewness parameter and degrees of freedom, is the quantile function of standard distribution with degrees of freedom , is an normalizer to obtain unit quartile range. The median of the skewed distribution is zero.

Consider the model

| (33) |

where , . The true parameter is set as , i.e., besides intercept , with have coefficient while the rest have . We fit the model to the samples generated from the true model with inverse transform sampling. We use the integer part of as the sample size . For each sample size, the experiment is conducted for times to obtain the mean and confidence band.

In this case study, the weights of observations are the diagonal elements of the optimal weight matrix (11). Since the density function in (11) is not known apriori in practice, we plug in normal distribution to obtain the weights. The weights are , where , and are the density and quantile of a standard normal distribution. Numerical experiments in Ergashev (2008) show that the impact of the weights is insignificant as long as the extreme tail observations are assigned with small weights.

Figures 1 and Figure 2 show that the Wasserstein distance between the estimated quantile function and the true quantile function converges to zero as the sample size increases.

8.2 Estimation of Mixture Quantiles of Generalized Beta Distributions with Financial Market Drawdowns

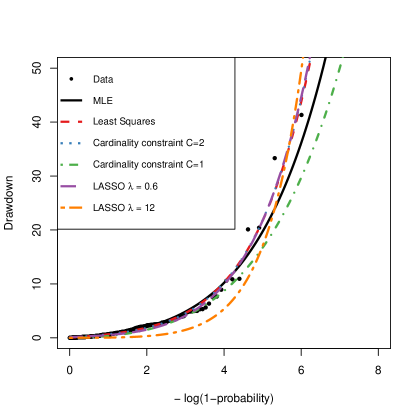

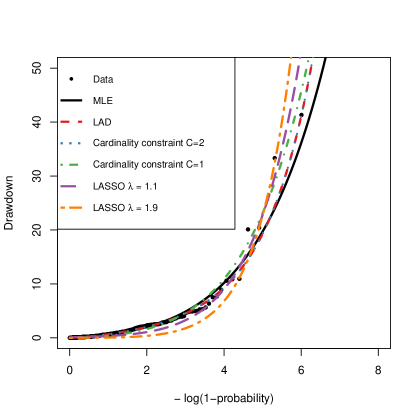

This section applies the model to a real-life data set. We fit the mixture quantiles of generalized beta distributions of the second kind to the log market drawdowns. This case study is inspired by Frey (2021) which finds that the lomax distribution has a good fit for market drawdowns. Drawdowns are calculated with 40-year historical adjusted close price of the SP500 Index from 01/01/1982 to 01/01/2022.

Financial Market Drawdowns

Drawdown financial characteristics is the the security price drop from the previous highest value in percentage. Suppose we have a time series of security price, , . The drawdown at time is defined by . The security is in a drawdown at time , if . We call period a drawdown period if for and . We take the maximum drawdown in each drawdown period. SP500 Index has a total of drawdown periods from 01/01/1982 to 01/01/2022. Then, we fit a model to 406 maximum log-tranformed drawdowns.

Generalized Beta Distribution of the Second Kind

The generalized beta distribution of the second kind is defined by the following density function . It nests many common distributions such as the generalized gamma (GG), Burr type 3, lognormal, Weibull, Lomax, half-Student’s , exponential, power function, etc. Our approach can be regarded as estimating mixture quantiles of these distributions. We first use the following grid to populate the design matrix. , , . The scale parameter is fixed at . The quantile functions are then standardized as described in Section 3. Then, to improve stability of optimization, we remove extreme values: quantile functions that either have -quantile smaller than or -quantile larger than . This is a reasonable choice since the scale of drawdowns varies from to . Those removed components is unlikely to be selected by the algorithm as a good fit, anyway. A total of quantile functions are included in the initial mixture.

Optimization Setting

We minimize the error (see (4)), with non-negativity constants (see Section 7). Additionally, we impose the cardinality constraints ( see Section 7). The value of the cardinality constraint is . As a comparison, we also use LASSO regression to select the quantile functions. The coefficient in LASSO regression is determined as follows: is increased with step until the cardinality (number of non-zero variables) equals and . The smallest that achieves the cardinality is reported. We do not use the optimal weights formula (11) in this case study, because it assigns too small weights to extreme observations. Equal weights are assigned to all observations, as we are concerned about the tail risk.

Goodness-of-fit

Table 1 presents the goodness-of-fit test statistics. We report the weighted mean squared error (WMSE), mean absolute error (MAE), Kolmogorov–Smirnov distance (KS) and log likelihood (LLK). Maximum likelihood estimate (MLE) of generalized beta distribution of the second kind is included for comparison.

| Least squares regression | Least absolute deviation regression | MLE | |||||||||

| N/A | 2 | 1 | N/A | N/A | N/A | 2 | 1 | N/A | N/A | N/A | |

| N/A | N/A | N/A | 0.6 | 1.2 | N/A | N/A | N/A | 1.1 | 1.9 | N/A | |

| WMSE | |||||||||||

| MAE | |||||||||||

| KS | |||||||||||

| LLK | - | - | - | - | - | - | - | - | - | - | - |

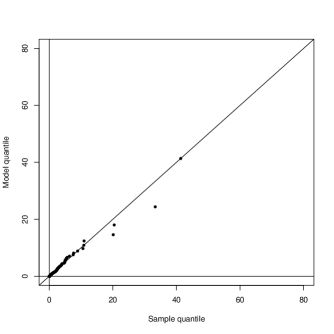

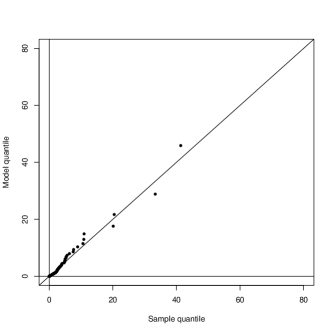

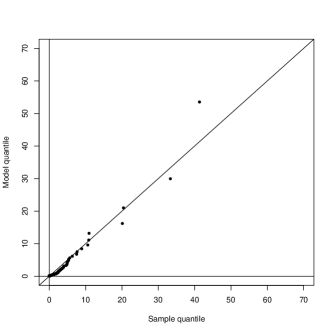

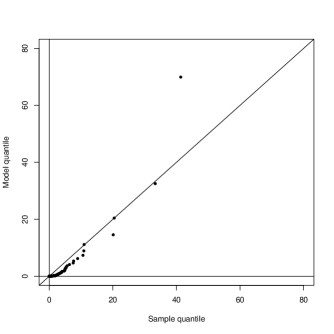

When the cardinality of the model is at least 2, regressions outperform MLE in terms of WMSE and MAE. The error of the optimization with cardinality constraint 2 is only slightly higher compared to the optimization without cardinality constraint. The test statistics are significantly worse with cardinality 1. MLE outperforms other models in terms of KS and LLK. In most cases, the model fitted with cardinality constraint outperforms the model fitted with penalty.

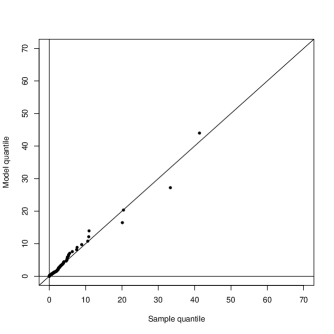

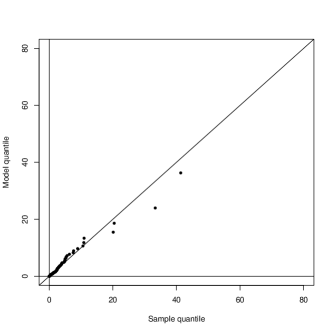

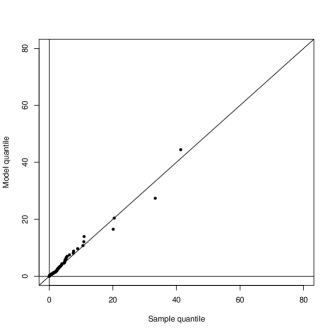

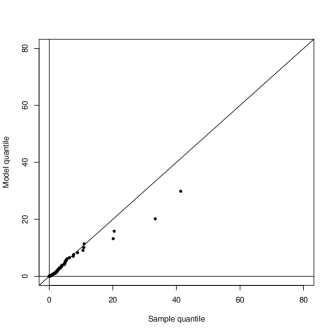

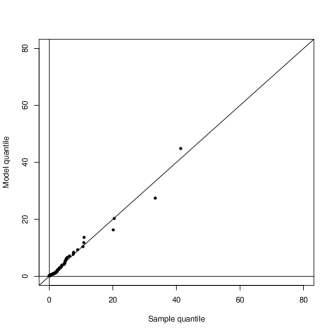

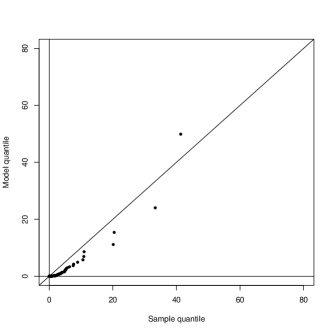

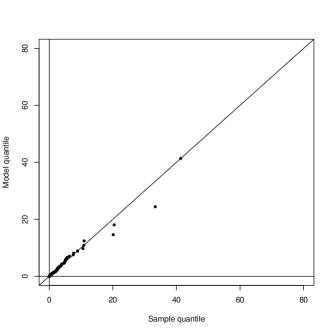

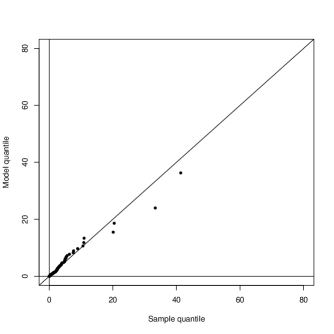

Figure 3 and 4 present the Q-Q plot of models fitted with different errors, constraints and penalties. MLE is included for comparison. The following three regressions provide close results and have good fit: 1) weighted least squares regression; 2) weighted least squares regression with cardinality constraint ; 3) weighted least squares regression with Lasso penalty coefficient . These models have a better fit to the tail observations than MLE. Figures 3b, 4b for MLE show that extreme tail observations are all below the straight line , i.e., MLE underestimates the tail risk. When cardinality equals , neither of the regression with cardinality constraint or with penalty has a good fit. For least absolute deviation regression, except for the regression with coefficient of penalty , all models are close and have good fit. They have better fit to the tail observations than MLE. Log probability plot in Appendix A directly compares the models in one graph.

9 Conclusion

We proposed a flexible parametric model for the quantile function. The model can be efficiently fitted using constrained linear regression. We studied various properties of the estimator. We proved that the estimator is asymptotically the minimum Wasserstein estimator. Also, we proved the asymptotical normality of the estimator. We suggested constraints and penalties for the regression optimization problem to improve performance of the estimator. Numerical experiments demonstrated that the suggested models have a good fit to tail observations. Also, experiments demonstrated that test statistics of weighed mean squared error and mean absolute error outperformed maximum likelihood estimation. We observe, that the model with cardinality constraint outperforms the model with penalty. The proposed model can be generalized to other risk functions, such as Conditional Value-at-Risk (CVaR, Rockafellar and Uryasev (2000, 2002)) and expectile (Newey and Powell, 1987), which are popular in finance and engineering.

References

- Vincent (1912) Stella Burnham Vincent. The Functions of the Vibrissae in the Behavior of the White Rat…, volume 1. University of Chicago, 1912.

- Ratcliff (1979) Roger Ratcliff. Group reaction time distributions and an analysis of distribution statistics. Psychological bulletin, 86(3):446, 1979.

- Sillitto (1969) G. P. Sillitto. Derivation of approximants to the inverse distribution function of a continuous univariate population from the order statistics of a sample. Biometrika, 56(3):641–650, 1969. ISSN 00063444. URL http://www.jstor.org/stable/2334672.

- Karvanen (2006) Juha Karvanen. Estimation of quantile mixtures via l-moments and trimmed l-moments. Computational Statistics & Data Analysis, 51(2):947–959, 2006. ISSN 0167-9473. doi: https://doi.org/10.1016/j.csda.2005.09.014. URL https://www.sciencedirect.com/science/article/pii/S0167947305002513.

- Keelin and Powley (2011) Thomas W. Keelin and Bradford W. Powley. Quantile-parameterized distributions. Decision Analysis, 8(3):206–219, 2011. doi: 10.1287/deca.1110.0213. URL https://doi.org/10.1287/deca.1110.0213.

- Ramsay (1988) J. O. Ramsay. Monotone regression splines in action. Statistical Science, 3(4):425–441, 1988. ISSN 08834237. URL http://www.jstor.org/stable/2245395.

- Papp (2011) Dávid Papp. Optimization models for shape-constrained function estimation problems involving nonnegative polynomials and their restrictions. 2011.

- Papp and Alizadeh (2014) Dávid Papp and Farid Alizadeh. Shape-constrained estimation using nonnegative splines. Journal of Computational and Graphical Statistics, 23(1):211–231, 2014. doi: 10.1080/10618600.2012.707343. URL https://doi.org/10.1080/10618600.2012.707343.

- LaRiccia (1982) Vincent N. LaRiccia. Asymptotic properties of weighted quantile distance estimators. The Annals of Statistics, 10(2):621 – 624, 1982. doi: 10.1214/aos/1176345803. URL https://doi.org/10.1214/aos/1176345803.

- Millar (1984) P. Warwick Millar. A general approach to the optimality of minimum distance estimators. Transactions of the American Mathematical Society, 286:377–418, 1984.

- Gilchrist (2007) Warren G. Gilchrist. Modeling and fitting quantile distributions and regressions. American Journal of Mathematical and Management Sciences, 27(3-4):401–439, 2007. doi: 10.1080/01966324.2007.10737707. URL https://doi.org/10.1080/01966324.2007.10737707.

- Bassetti and Regazzini (2006) Federico Bassetti and Eugenio Regazzini. Asymptotic properties and robustness of minimum dissimilarity estimators of location-scale parameters. Theory of Probability and Its Applications, 50:171–186, 2006.

- Bassetti et al. (2006) Federico Bassetti, Antonella Bodini, and Eugenio Regazzini. On minimum kantorovich distance estimators. Statistics & Probability Letters, 76(12):1298–1302, 2006. ISSN 0167-7152. doi: https://doi.org/10.1016/j.spl.2006.02.001. URL https://www.sciencedirect.com/science/article/pii/S0167715206000381.

- Bernton et al. (2019) Espen Bernton, Pierre E Jacob, Mathieu Gerber, and Christian P Robert. On parameter estimation with the Wasserstein distance. Information and Inference: A Journal of the IMA, 8(4):657–676, 10 2019. ISSN 2049-8772. doi: 10.1093/imaiai/iaz003. URL https://doi.org/10.1093/imaiai/iaz003.

- Lariccia and Wehrly (1985) Vincent N. Lariccia and Thomas E. Wehrly. Asymptotic properties of a family of minimum quantile distance estimators. Journal of the American Statistical Association, 80(391):742–747, 1985. doi: 10.1080/01621459.1985.10478178. URL https://www.tandfonline.com/doi/abs/10.1080/01621459.1985.10478178.

- Hosking (1990) J. R. M. Hosking. L-moments: analysis and estimation of distributions using linear combinations of order statistics. Journal of the Royal Statistical Society. Series B (Methodological), 52(1):105–124, 1990. ISSN 00359246. URL http://www.jstor.org/stable/2345653.

- Peng and Uryasev (2023) Cheng Peng and Stanislav Uryasev. Factor model of mixtures, 2023. URL https://arxiv.org/abs/2301.13843.

- Matheson and Winkler (1976) James E. Matheson and Robert L. Winkler. Scoring rules for continuous probability distributions. Management Science, 22(10):1087–1096, 1976. doi: 10.1287/mnsc.22.10.1087. URL https://doi.org/10.1287/mnsc.22.10.1087.

- Ogawa (1951) Junjiro Ogawa. Contributions to the theory of systematic statistics. I. Osaka Mathematical Journal, 3(2):175 – 213, 1951. doi: ojm/1200929248. URL https://doi.org/.

- Lloyd (1952) E. H. Lloyd. Least-squares estimation of location and scale parameters using order statistics. Biometrika, 39(1-2):88–95, 05 1952. ISSN 0006-3444. doi: 10.1093/biomet/39.1-2.88. URL https://doi.org/10.1093/biomet/39.1-2.88.

- Kratz and Resnick (1996) Marie Kratz and Sidney I. Resnick. The qq-estimator and heavy tails. Communications in Statistics. Stochastic Models, 12(4):699–724, 1996. doi: 10.1080/15326349608807407. URL https://doi.org/10.1080/15326349608807407.

- Barrio et al. (2005) Eustasio Del Barrio, Evarist Giné, and Frederic Utzet. Asymptotics for L2 functionals of the empirical quantile process, with applications to tests of fit based on weighted Wasserstein distances. Bernoulli, 11(1):131 – 189, 2005. doi: 10.3150/bj/1110228245. URL https://doi.org/10.3150/bj/1110228245.

- Panaretos and Zemel (2019) Victor M. Panaretos and Yoav Zemel. Statistical aspects of wasserstein distances. Annual Review of Statistics and Its Application, 6(1):405–431, 2019. doi: 10.1146/annurev-statistics-030718-104938. URL https://doi.org/10.1146/annurev-statistics-030718-104938.

- Newey and McFadden (1994) Whitney K. Newey and Daniel McFadden. Chapter 36 large sample estimation and hypothesis testing. volume 4 of Handbook of Econometrics, pages 2111–2245. Elsevier, 1994. doi: https://doi.org/10.1016/S1573-4412(05)80005-4. URL https://www.sciencedirect.com/science/article/pii/S1573441205800054.

- Balakrishnan and Rao (2000) N. Balakrishnan and C. R. Rao. Handbook of statistics 16: order statistics-theory and methods. Technometrics, 42(4):445–445, 2000. doi: 10.1080/00401706.2000.10485750. URL https://doi.org/10.1080/00401706.2000.10485750.

- Loy et al. (2016) Adam Loy, Lendie Follett, and Heike Hofmann. Variations of q–q plots: The power of our eyes! The American Statistician, 70(2):202–214, 2016. doi: 10.1080/00031305.2015.1077728. URL https://doi.org/10.1080/00031305.2015.1077728.

- Santosa and Symes (1986) Fadil Santosa and William W. Symes. Linear inversion of band-limited reflection seismograms. SIAM Journal on Scientific and Statistical Computing, 7(4):1307–1330, 1986. doi: 10.1137/0907087. URL https://doi.org/10.1137/0907087.

- Tibshirani (1996) Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996. doi: https://doi.org/10.1111/j.2517-6161.1996.tb02080.x. URL https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/j.2517-6161.1996.tb02080.x.

- Rockafellar and Uryasev (2013) R. Tyrrell Rockafellar and Stan Uryasev. The fundamental risk quadrangle in Risk Management, Optimization and Statistical Estimation. Surveys in Operations Research and Management Science 18, 2013.

- Hosseini and Takemura (2016) Reza Hosseini and Akimichi Takemura. An objective look at obtaining the plotting positions for qq-plots. Communications in Statistics - Theory and Methods, 45(16):4716–4728, 2016. doi: 10.1080/03610926.2014.927498. URL https://doi.org/10.1080/03610926.2014.927498.

- Pyke (1965) R. Pyke. Spacings. Journal of the Royal Statistical Society: Series B (Methodological), 27(3):395–436, 1965. doi: https://doi.org/10.1111/j.2517-6161.1965.tb00602.x.

- Pyke (1972) Ronald Pyke. Spacings revisited, pages 417–428. University of California Press, 1972. doi: doi:10.1525/9780520325883-022. URL https://doi.org/10.1525/9780520325883-022.

- From (1989) Steven G. From. Optimal spacing of quantiles for the estimation of the mixing parameters in a mixture of two exponential distributions. Communications in Statistics - Theory and Methods, 18(6):2201–2223, 1989. doi: 10.1080/03610928908830031. URL https://doi.org/10.1080/03610928908830031.

- Robert et al. (1999) Christian P Robert, George Casella, and George Casella. Monte Carlo statistical methods, volume 2. Springer, 1999.

- Bawa and Lindenberg (1977) Vijay S. Bawa and Eric B. Lindenberg. Capital market equilibrium in a mean-lower partial moment framework. Journal of Financial Economics, 5(2):189–200, 1977. ISSN 0304-405X. doi: https://doi.org/10.1016/0304-405X(77)90017-4. URL https://www.sciencedirect.com/science/article/pii/0304405X77900174.

- Arnold et al. (2008) Barry C Arnold, Narayanaswamy Balakrishnan, and Haikady Navada Nagaraja. A first course in order statistics. SIAM, 2008.

- Aitken (1936) A. C. Aitken. Iv.—on least squares and linear combination of observations. Proceedings of the Royal Society of Edinburgh, 55:42–48, 1936. doi: 10.1017/S0370164600014346.

- Ergashev (2008) Bakhodir A Ergashev. Should risk managers rely on maximum likelihood estimation method while quantifying operational risk? Journal of Risk, 2008.

- David and Nagaraja (2004) Herbert A David and Haikady N Nagaraja. Order statistics. John Wiley & Sons, 2004.

- Lehmann and Casella (2006) Erich L Lehmann and George Casella. Theory of point estimation. Springer Science & Business Media, 2006.

- Rockafellar and Uryasev (2000) R. Tyrrell Rockafellar and Stanislav Uryasev. Optimization of Conditional Value-at-Risk. Journal of Risk, 2:21–41, 2000.

- Rockafellar and Uryasev (2002) R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional Value-at-Risk for general loss distributions. Journal of Banking and Finance, pages 1443–1471, 2002.

- Huber (1964) Peter J. Huber. Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics, 35(1):73 – 101, 1964. doi: 10.1214/aoms/1177703732. URL https://doi.org/10.1214/aoms/1177703732.

- Zabarankin et al. (2016) Michael Zabarankin, Stan Uryasev, et al. Statistical decision problems. Springer, 2016.

- Fernandez and Steel (1998) Carmen Fernandez and Mark F. J. Steel. On bayesian modeling of fat tails and skewness. Journal of the American Statistical Association, 93(441):359–371, 1998. ISSN 01621459. URL http://www.jstor.org/stable/2669632.

- Frey (2021) Robert Frey. 180 Years of Market Drawdowns. http://www.ams.sunysb.edu/~frey/, 2021. Online Presentation.

- Newey and Powell (1987) Whitney K. Newey and James L. Powell. Asymmetric least squares estimation and testing. Econometrica, 55(4):819–847, 1987. ISSN 00129682, 14680262. URL http://www.jstor.org/stable/1911031.

Appendix A Comparison of Scaled Quantile Functions of Fitted Models

The Appendix presents two log probability plots summarizing numerical case study in Section 8.2. The quantile functions of different models fitted by minimizing the same error are compared in one graph. The x-axis is log-transformed for better visualization of tail behavior.