Equalised Odds is not Equal Individual Odds:

Post-processing for Group and Individual Fairness

Abstract

Group fairness is achieved by equalising prediction distributions between protected sub-populations; individual fairness requires treating similar individuals alike. These two objectives, however, are incompatible when a scoring model is calibrated through discontinuous probability functions, where individuals can be randomly assigned an outcome determined by a fixed probability. This procedure may provide two similar individuals from the same protected group with classification odds that are disparately different – a clear violation of individual fairness. Assigning unique odds to each protected sub-population may also prevent members of one sub-population from ever receiving equal chances of a positive outcome to another, which we argue is another type of unfairness called individual odds. We reconcile all this by constructing continuous probability functions between group thresholds that are constrained by their Lipschitz constant. Our solution preserves the model’s predictive power, individual fairness and robustness while ensuring group fairness.

1 Introduction

Predictive models that output a score or probability for a multi-dimensional input, i.e., scoring functions, are a common tool in automated decision-making [1, 2]. Binary classification is a popular realisation of this paradigm, where the score is thresholded to produce a decision; among others it can be found in school examinations where individual answers are condensed into a grade that translates to a pass/fail mark [3], or banking where the history of personal finances is compressed into a credit score that captures one’s likelihood of defaulting on a loan [4]. Many such applications, especially in high-stake domains like healthcare and finance, are coming under increased scrutiny given their potential harm to society – predictive models deployed in these scenarios are expected to be accurate, robust, fair and explainable. These four desiderata, however, are often at odds. Improving utility (i.e., predictive power) of a model may entail increasing its complexity at the expense of interpretability and robustness (e.g., due to over-fitting) [5, 6]. Similarly, equalising errors between protected groups to ensure fairness may require sacrificing utility and impairing other notions of fairness [7, 8].

In this paper we focus on the latter scenario, where (protected) sub-populations are treated differently, thus unfairly, due to persistent historical biases [9], training data under-representation [10] and greedy optimisation of an objective function. Correcting for these biases is often challenging as it requires detailed knowledge of the data domain and the input space. One popular solution to this problem, which we study here, is threshold optimisation under fairness constraints when dealing with multiple protected groups. The method relies on calculating unique decision functions based on scores for each protected group in order to satisfy a given fairness constraint (such as demographic parity) [11].

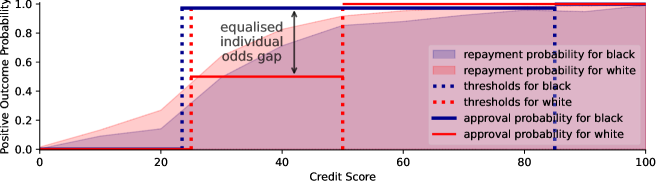

We re-examine this approach, as finding a set of thresholds for a given score function that satisfy multiple fairness constraints (such as equalised odds [12]) is often impossible if only using a collection of single thresholds. Instead, a decision function that is optimal with respect to an owner-selected definition of group fairness is derived directly from the scoring function using a pair of thresholds for each group. Outputs that fall between the thresholds are allocated a random decision based on a fixed probability parameter – a procedure called fixed randomisation – which, while effective, exhibits a number of shortcomings as shown by Figure 1 and discussed later in Section 3. Using a fixed randomisation parameter is sub-optimal for both the entities that create the model (owners) and those whose case is being decided by the model (users) because: (1) if the scoring function is accurate, the decision function cannot leverage this in the intervals between the thresholds; (2) even if the scoring function is individually fair, the step-based decision function is not, e.g., users whose scores are just under a threshold are treated very differently to users who are barely above it, despite their scores being similar; and (3) users from one protected group may be unable to access the odds of positive classification offered to another group (equalised individual odds unfairness).

Consider the fixed randomisation solution shown in Figure 1 which satisfies equalised odds. For example, a white user with a credit score of is assigned the same odds (%) of receiving a loan as a white user whose credit score is despite the latter being times more likely to default than the former. This stands in stark contrast to a white user with a credit score of who has no chance of getting a loan despite being only times more likely to default than the aforementioned white user with a credit score of (for more examples, see Figure 9 in Appendix H). This case study illustrates that an increase in credit score – and therefore an increase in the likelihood of repaying a loan – is not reflected in the final decision for all scores except at the thresholds. In addition, while some white users have a % chance of receiving a loan and some black users have a % chance, these success odds are never offered to the other group; therefore, a white user will never be given a % chance of receiving a loan and vice versa. This disparity motivates a new notion of fairness – called equalised individual odds – which we define in Section 3 (Definition 3.2).

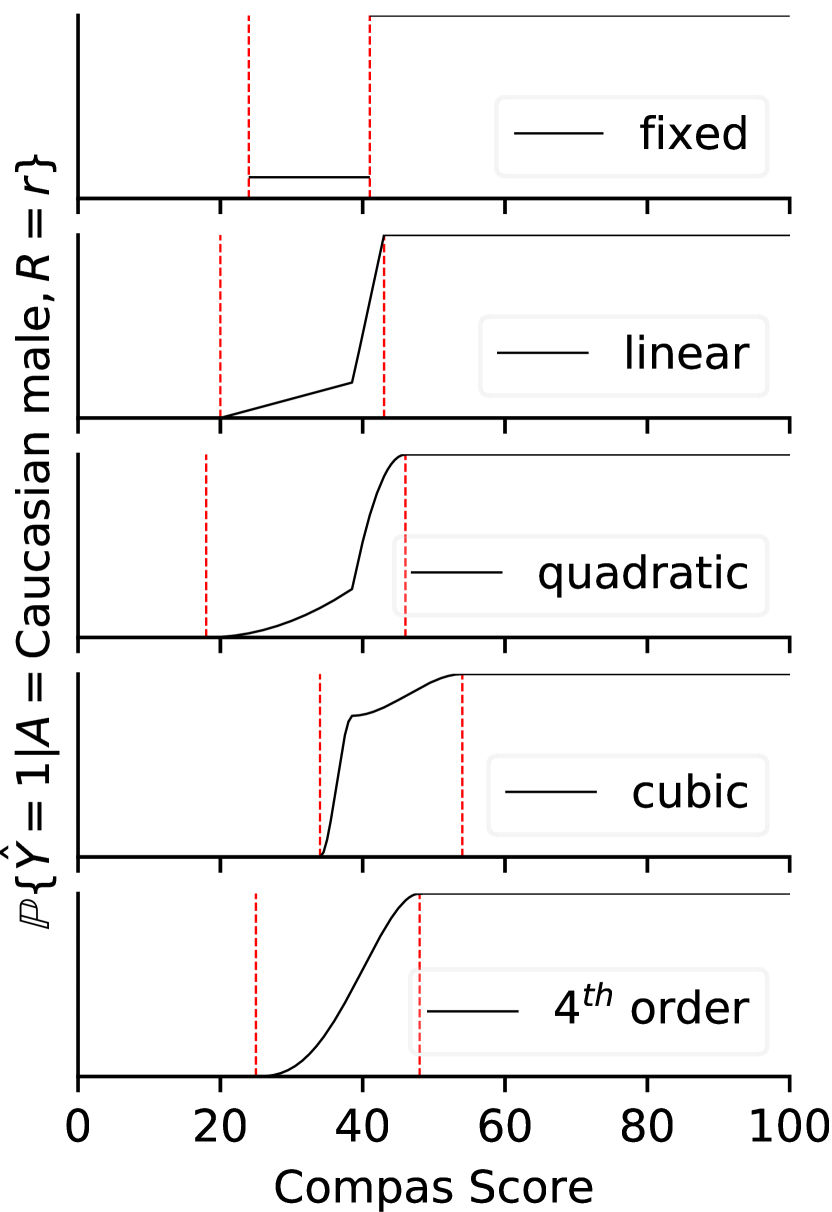

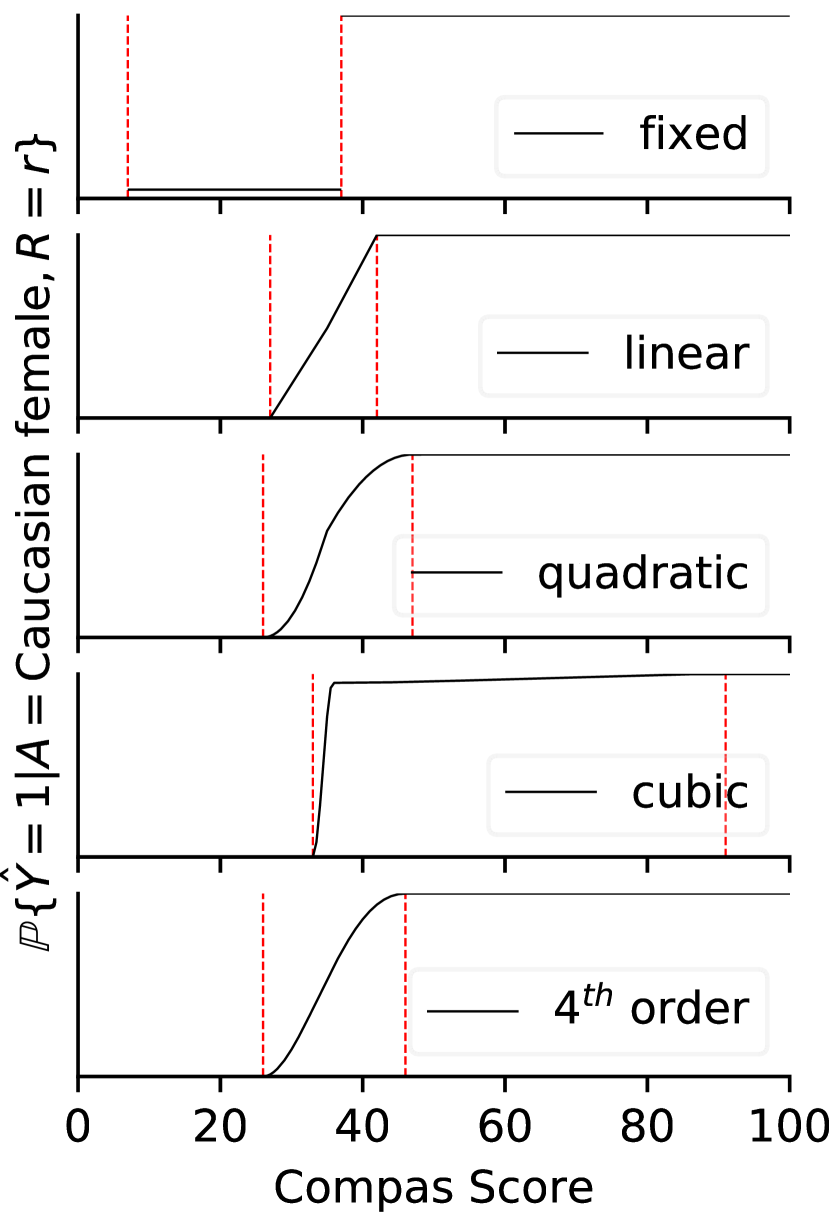

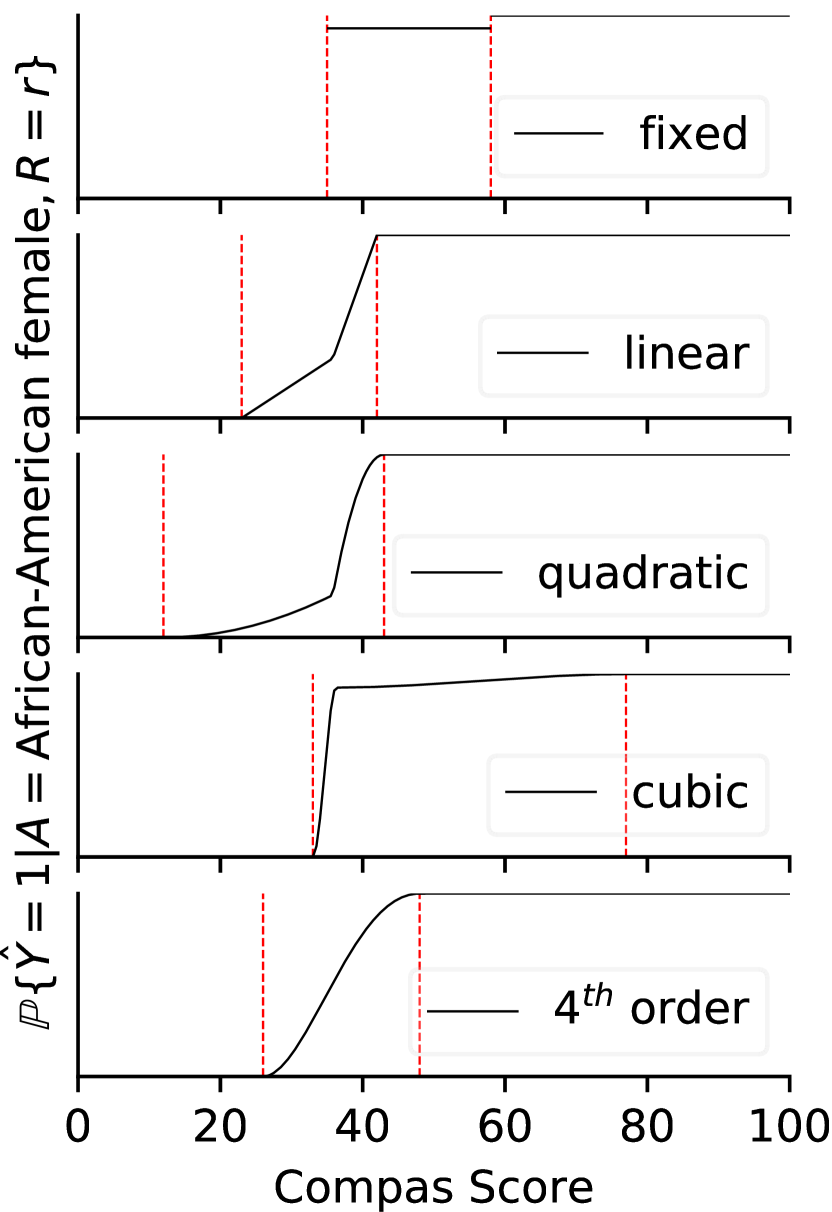

We address these shortcomings by deriving a set of closed-form, continuous, monotonic functions – see Figure 4 and Appendix D – parameterised only by the thresholds and a probability parameter, making them easy to compute (Section 4.2). We show that these functions are constrained via a maximum derivative, thus preventing a change in score leading to a large shift in classification odds and maintaining individual fairness (Section 4.3). Our approach enables the model owners to prioritise users with higher scores, thus better honouring the underlying score distribution as well as improving the transparency of the process. These properties incentivise users to increase their score as such an action improves their odds of a positive outcome – see Figure 3 for a direct comparison to Figure 1. We analyse our method through the lens of credit scoring for loan allocation (Section 5). Specifically, we seek equalised odds across the four values of the race attribute – non-Hispanic white (white), black, Hispanic and Asian – found in the 2003 TransUnion TransRisks Scores [14] (CreditRisk) data set, and show that individual fairness is improved while group fairness and accuracy are preserved. In Appendix A we report an additional set of experiments for the COMPAS data set, which is used for recidivism prediction [15]. In summary, our contribution is threefold: (1) we demonstrate that fixed randomisation for group fairness violates individual fairness; (2) we derive a set of closed-form, continuous and monotonic probability functions; and (3) we show that these continuous curves preserve group fairness and improve performance while adhering to the constraint imposed by individual fairness.

2 Preliminaries

Notation

We assume that the scalar scoring function takes individual instances and outputs a score ; , where , is an arbitrary, possibly stochastic, binary decision function on that maps the scores to predicted classes according to a predetermined probability distribution . Lower case letters denote an individual instance from a sample, e.g., is an instance in . Functions denoted by Greek letters, such as where , parameterise this probability based on scores, e.g., according to the Bernoulli distribution . Effectively, is the probability that for . Alternatively, for deterministic behaviour can be defined by a single threshold , where a score yields and yields ; this behaviour can be captured by the indicator function:

One common realisation of this thresholding function is a binary probabilistic classifier, where and . We therefore define the final decision function as the composition , where the subscript on indicates the composition function on the scoring function . Additionally, capital letters refer to samples from spaces, such that is a sample from the space ; are the corresponding scores calculated by from the sample ; are classes predicted for all instances in the sample ; and captures their ground truth labels. We denote the protected attribute as , and consider the joint distribution . We make no assumptions on the type or shape of , nor on the construction of (the behaviour of which is discussed in Section 3).

Related Work

A large portion of fairness research in machine learning (ML) focuses on equalising outcomes and errors between users who belong to different protected groups, such as race or sex [16]. There are three distinct areas where fairness can be injected into a data modelling pipeline: pre-processing transforms the underlying training data such that signals and cross-correlations causing bias and discrimination are weakened [17]; in-processing incorporates fairness constraints directly into the optimisation objective [18]; and post-processing alters the output of a decision-making process to mitigate bias of the underlying (fixed) model [19]. A variety of methods is needed as even when the scoring function is trained as “unaware” [20], and as such has no knowledge of the value of the protected class , can still become unfair. For example, the ground truth may be correlated with due to historical biases, some features in may act as a proxy, or the distribution/behaviour of some features in may be different between sub-populations, causing a predictive model to under-perform for underrepresented groups. A different strand of work looks into fair data collection [21] and feature selection [22] as well as fair learning procedures, e.g., adversarial learning [23]. Here, we focus on a popular class of post-processing methods known as threshold optimisation. Our work builds directly upon the foundational method introduced by Hardt et al. [13] by expanding and improving it along multiple dimensions.

Group and Individual Fairness

Group and individual fairness are two commonly considered categories [24]. Group fairness focuses on the statistical difference in outcomes between sub-populations determined by the values of a protected attribute [25]. The type of statistical outcome that a model-maker may want to focus on is domain-specific, but measures closer to are more desirable as this indicates no statistical difference between two groups. For a simple case of a binary protected feature where , we can further differentiate two types of group fairness [26]:

- Outcome

-

Predictions are equalised in a set way across groups, e.g., demographic parity [27]:

An example of demographic parity may be in school admissions [28], where the distribution of admitted students should represent the distribution of the applicants for each value of (i.e., if applicants are male and female, admissions should reflect this pattern).

- Error Distribution

-

(In)correct classifications should be equalised in a predetermined way, e.g., using false negative rate:

An example of equalising false negative rate may be in the medical field, where false negatives could have dire consequences for a patient. Erring on the side of caution equally for all groups is therefore more preferable, up to a certain cost [29].

There are many ways in which group fairness can be operationalised, with different tasks and domains requiring a specific constraint or a mixture thereof. In this paper, we mainly consider a strong fairness constraint called equalised odds [30], which is outlined in Definition 2.1.

Definition 2.1 (Equalised Odds)

A decision function satisfies equalised odds with respect to a protected attribute if false positives and true positives are independent of the protected attribute:

| (1) |

A slightly more nuanced view on fairness is the notion of “treating similar individuals similarly”, known as individual fairness [31]. In short, we look to impose a constraint on the distance between any two points (individuals) in the input space against their distance in the output space [20]. We measure distance or similarity using distance functions on the input () and output () spaces:

| (2) |

where and is a Lipschitz constant – see Appendix B for a discussion on distance metrics. The Lipschitz constant describes the maximal difference of the distance between two values in the input space with their corresponding distance in the output space. Limiting is usually done with a smoothing process, e.g., manifold regularisation [32], or by constraining the optimisation of subject to a condition on the size of . The concept is to assume that individuals with similar features (small ) should appear close together in the output space (small ). Therefore, limiting the rate at which can change (i.e., its differential) in densely populated areas of the feature space can force to be smoother, hence more fair. can be as simple as Gower’s distance for mixed categorical and numerical features (see Appendix B), but ideally should be chosen appropriately to the problem at hand; since is scalar, we can define .

3 Post-processing for Fairness with Fixed Randomisation

In general, we expect that the higher the score output by a scoring function used for a predictive task, the “better” the outcome – a property known as positive orientation [33] (negative orientation describes the opposite behaviour). For example, if and are randomly drawn instances from used to calculate credit scores, and has a higher credit score than (i.e., ), this relation implies that is more likely to have healthier spending habits, thus making them more likely to repay a loan (see Figure 8 in Appendix H). This does not need to be strictly true for all values, but should hold in general. In other words, we expect the receiver operating characteristic (ROC) curve, which expresses the (false positive, true positive) rates at different thresholds on , to at least be above the diagonal line from to [34] (which denotes a scoring function that is completely independent of , i.e., trivial scoring function) and monotonic (never decreasing).

Optimising a scoring function with respect to complex definitions of fairness (such as equalised odds given by Definition 2.1) for multiple protected groups is more challenging than optimising for less strict fairness notions (e.g., demographic parity). With post-processing, we assume that is fixed and inaccessible, i.e., a black box. We cannot therefore know or alter how scores are calculated from the input space, nor do we have access to the input space. This may be due to trade secrets or privacy concerns [35], and applies to credit scoring [36] among other domains. To achieve the desired notion(s) of fairness we therefore need to build an unbiased decision function upon by finding optimal thresholds for using only the joint distributions of , and .

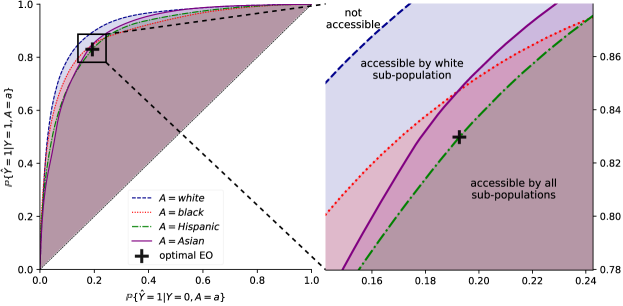

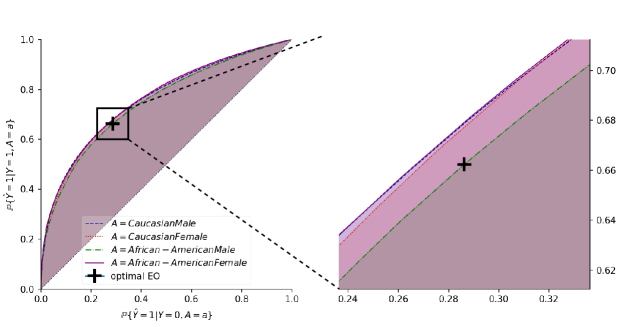

When cardinality of is 2, optimal equalised odds can be achieved by fixing a single threshold at any point where the ROC curves are equal. If there are multiple points where the curves meet, the optimal solution (lowest false positive and highest true positive rates) is the intersection closest to , i.e., the perfect model. Figure 2 shows the ROC curves stratified by a protected attribute (race) for a loan repayment prediction based on credit scores from the CreditRisk data set.

The challenge arises when the ROC curves do not touch or if . If the curves do not touch in , we can only satisfy equalised odds with a single threshold at the trivial points or , i.e., assign the same outcome to all the scores. For – e.g., where may be a Cartesian product of protected characteristics – it is highly unlikely for all the ROC curves to intersect at the same point (except for the trivial points). When using a single threshold, each group can only access false and true positive values that are on their respective ROC curve (shown in Figure 2 as the coloured line). Using multiple thresholds and randomisation, however, allows each group to access all points that are below their respective ROC curve and above the trivial scoring function (shown in Figure 2 as the coloured region). The optimal point for equalised odds therefore becomes the point under all ROC curves that is closest to .

Hardt et al. [13] achieve equalised odds by setting group-specific thresholds – where , so – that are applied to the scoring function . If a score falls between the thresholds designated for the protected group , it is assigned a class at random with a probability given by the parameter . Since thresholds are group-specific, we define a threshold-based classification function , where the probability of is given by:

| (3) |

for each protected sub-population . In other words, . We therefore define the final decision function as , and Equation 3 gives us:

We call this fixed randomisation, as yields probability of . Setting , or is synonymous to using a single threshold. A visual example of fixed randomisation is provided in Figure 1.

Fixed randomisation is an effective approach to build a classifier based on a scoring function that satisfies group fairness such as equalised odds. This strategy, however, exhibits a number of undesired properties; most notably: (i) it does not follow the general behaviour expected of a scoring function since all users who are subject to randomisation receive the same classification odds, no matter their score, but users whose scores are similar and near the thresholds are treated differently (see Figure 1); (ii) even if is individually fair with well-defined , the discontinuities introduced by at prevent from complying with individual fairness; and (iii) if then users from group cannot access the random classification odds offered to group and vice versa.

Section 1 has thoroughly demonstrated the adverse consequences of point (i). While users are made to believe that a higher score is better, e.g., their credit rating, fixed randomisation only exhibits this behaviour at the thresholds. Refer back to Figure 1, which shows that despite there being clear evidence of white users with a credit score of being more likely to repay their loan than white candidates whose credit score is , both are equally likely (but not guaranteed) to receive a loan.

Definition 3.1 (Classification Odds Distance)

Given a decision function such that , we define the corresponding distance metric such that:

Using Equation 3, the distance is the difference in odds of positive classification between two scores.

Point (ii) concerns the classification behaviour around the thresholds and fixed randomisation parameter , which create discontinuities in odds for the final decision function . To demonstrate this we use Definition 3.1, which specifies a distance metric on the classification odds. Lipschitz conditions scale across compositions [37], such that:

Issues arise around the thresholds. Take:

In such a case, from Equation 3, we have that is either or and . Therefore:

| (4) |

and thus must be very large. As approaches from one side and from the other, is clearly not locally Lipschitz continuous since but or , one of which is always above . In theory, could be crafted such that it cannot map individuals to values around the thresholds, however this would introduce discontinuities to and thus invalidate the Lipschitz condition. In this scenario, assuming satisfies the individual fairness constraint defined in Equation 2, must ultimately violate such an individual fairness constraint at the thresholds when fixed randomisation is employed. Fixed randomisation can therefore be seen as a step function – see Figure 1 – which is not uniformly continuous on any interval that contains [38].

Definition 3.2 (Equalised Individual Odds)

Given a probabilistic classifier , where , defined by the probability curve such that and , satisfies individual odds iff:

Therefore, all sub-populations in must be capable of attaining classification odds available to all the other groups.

Point (iii) highlights an interesting behaviour that gives rise to a novel, relatively weak, notion of fairness, which we call individual odds – see Definition 3.2. To satisfy this fairness criterion does not necessarily need to be continuous but every point that it can reach must also be available to , so effectively we require . Violating this constraint implies that there exists a subset of users from the sub-population that can never be treated the same as a portion of individuals from the group and vice versa. Whenever , the individual odds criterion is clearly not satisfied for fixed randomisation. This definition of fairness bridges the, thus far somewhat separate, concepts of individual and group fairness as it considers the treatment of individual users in view of their assignment to distinct sub-populations determined by the protected attribute .

4 Constructing Curves for Preferential Randomisation

Under these conditions, assuring group and individual fairness is equivalent to searching for solutions that are continuous and smooth, with a well-defined limit on , which also satisfy Definition 2.1. We therefore must find a combination of the group thresholds ( and ) and a curve between them that satisfies individual as well as group fairness.

4.1 Defining Solution Behaviour

There are potentially infinite curves that satisfy the aforementioned conditions. In order to decrease the size of the solution space, we can impose further restrictions on the expected behaviour of the solution and parameterisation thereof. Where follows fixed randomisation, we define preferential randomisation as to distinguish between the two; therefore, and:

We expect preferential randomisation to behave as follows:

- Monotonicity

- Continuity at boundaries

-

The solution should avoid sudden jumps in probability at the thresholds to satisfy point (ii), i.e.:

- Continuity for interval space

-

The curve that maps to the classification probability must be well-defined at all points in in compliance with point (iii). If is any fixed point in :

where is approaching from above and is approaching from below.

Monotonicity between the thresholds guarantees that higher scores are treated better; continuity within the interval ensures that the Lipschitz constant does not explode at the thresholds – see Figure 3 for an example. Because no score can be outside of the range, the output of does not need to span the entire probability range if the thresholds are fixed at the extremes, i.e., or . This is especially important when we can only access the final decisions as opposed to the scores , i.e., is a crisp classifier , in which case we require the ability to randomise the crisp predictions. With these constraints we can satisfy the requirements outlined in Section 3.

4.2 Viable Solutions from Linear Systems

Even with these constraints, the number of curves between each combination of thresholds that constitute viable solutions is still infinite. We therefore further constrict the solution space to piece-wise polynomials parameterised only by and . We assume each solution takes the form:

and so for :

| (5) |

We choose this particular point of connection () because it ensures that all solutions (including ) follow:

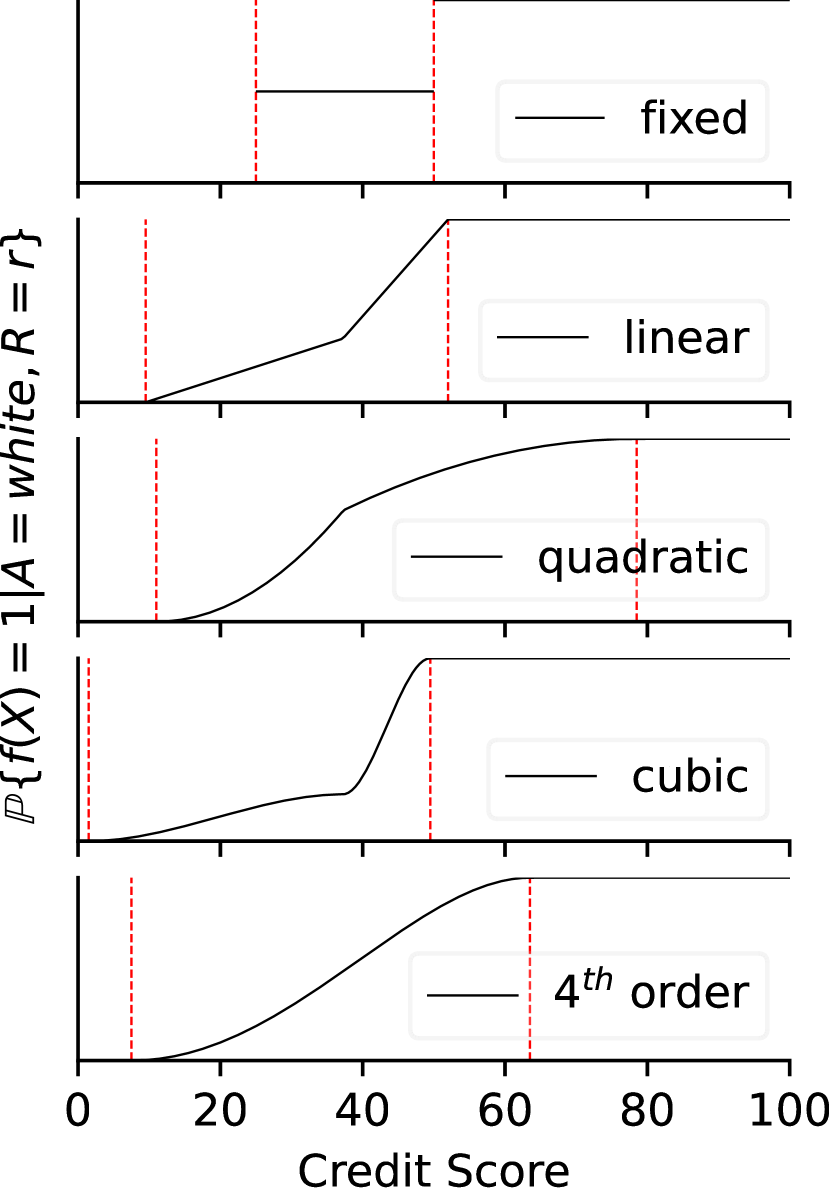

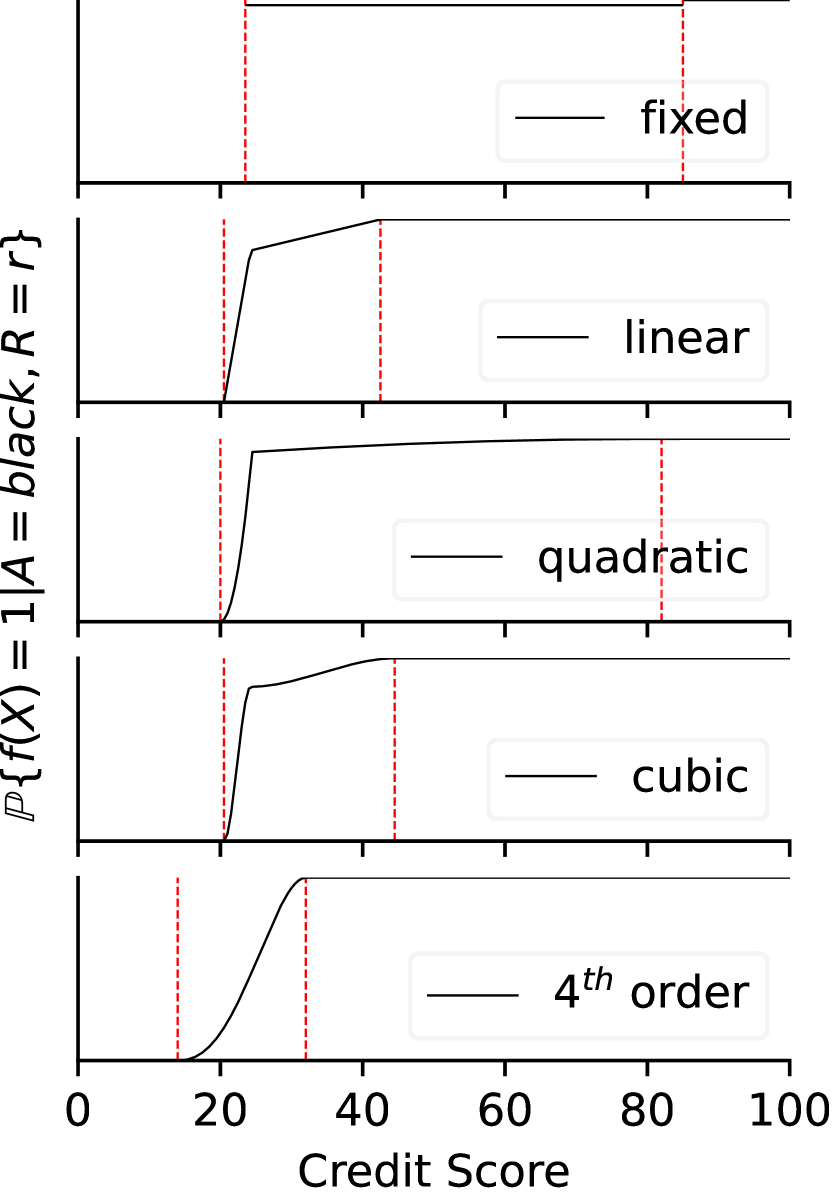

This property guarantees that curves parameterised by the same thresholds and probabilities are comparable as they yield the same average probability between and . The only difference between such solutions is their smoothness and continuity – see Appendix C for the proof. Finding families of closed-form solutions is achieved by using the continuity and monotonic constraints, with the addition of smoothness constraints as the order of the polynomial increases, and solving a full-rank linear system – refer to Appendix D for details. For example, one could consider four candidate curves: (i) linear (Equation 18); (ii) quadratic (Equation 19); (iii) cubic (Equation 20); and (iv) 4th order (Equation 21). Their closed-form definitions are given in Appendix E.

4.3 Validating Individual Fairness

If is individually fair from the outset, validating that a given solution satisfies the individual fairness constraint is straight forward. From Definition 3.1 and Equation 4:

Taking the limit , we get the definition of a derivative. Therefore, we can calculate by considering the maximum derivative:

Due to the definitions of each , the maximum value of on is always either at the thresholds or at the connection point, with the exception of the 4th order polynomial for which is where for , thus is always known. Finding an optimal solution is therefore a case of identifying values of and for that satisfy Definition 2.1 such that is well-defined. While is not guaranteed to be small, it is guaranteed to be finite. Taking the limit:

which is synonymous with using a single threshold, hence invalidating equalised odds.

5 CreditRisk Case Study

To facilitate a direct comparison, we apply our method to the case study conducted by Hardt et al. [13]111Source code available at: https://github.com/Teddyzander/McGIF.. Credit scores are often used to determine whether an individual should receive a loan or mortgage, to calculate interest rates and credit limits, and even to conduct background check on tenants [39, 40]. The scoring function – which calculates credit scores on input space – operates as a black box (see Section 3), therefore we only observe the scores and cannot access or . The input space may contain attributes influenced by cultural background (i.e., related to race), possibly causing the joint distribution of and to differ between sub-populations . The CreditRisk data set captures the credit score’s ability to predict defaulting on a loan (i.e., failing to repay it) for 90 days or more. The data show that as credit score increases, the number of defaults decreases. The rate of these changes, however, depends on race. Therefore, when a single threshold for each sub-population is optimised for maximum accuracy, the equalised odds (Definition 2.1) becomes ; we should strive for this fairness metric to be as close to as possible.

We overcome this by using different thresholds and probabilities (specified in Table 3 in Appendix F) achieved with a set of curves with differing smoothness constraints. These curves honour the “higher credit score leads to higher repayment probability” dependency encoded in the underlying data. Referring back to the example introduced in Section 1, we can see from Figures 3 and 4 that the white user with a credit score of is now – times more likely to receive a loan than the white user with a credit score of , depending on which continuous solution is chosen. The results – reported in Table 1 – show that the difference in accuracy and equalised odds between fixed randomisation and preferential randomisation is negligible. The method additionally improves individual fairness by the Lipschitz constant on and through satisfying Definition 3.2 (individual odds). Preferential randomisation can therefore be used to guarantee group and individual fairness through the notions of equalised odds and individual odds, and this encourages users to engage with the scoring model.

| white | black | Asian | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| acc (%) | EO | acc (%) | EO | acc (%) | EO | ||||||

| fixed [13] | |||||||||||

| linear | |||||||||||

| quadratic | |||||||||||

| cubic | |||||||||||

| 4th order | |||||||||||

6 Conclusion and Future Work

In this work we demonstrated how using fixed randomisation to guarantee group fairness may be detrimental to both the owners and users of a predictive model. Users with higher scores should be more likely to receive a better outcome – a property that may be lost when enforcing group fairness. Ensuring this behaviour also allows the owners to preserve predictive performance and transparency of the automated decision-making process. By using the method proposed in this paper – which relies on monotonic and continuous curves – we can guarantee these properties. Our approach rewards building accurate scoring functions and adheres to the notion of individual fairness from the perspective of function composition. Importantly, the burden of accurate classification remains the sole responsibility of the model-maker since our method forces all individuals to rely on the equalised odds measure of the worst-performing sub-population. This allocation of responsibility is desirable as owners can choose to invest in better predictors, data or scoring functions, whereas users in under-performing groups lack this agency.

Notably, our case study shows that there can exist multiple solutions that simultaneously satisfy equalised odds and individual fairness (model multiplicity) [41]. When equalised odds, individual fairness and accuracy are comparable between groups, we can choose to discriminate the solutions based on other criteria. Future work will explore this aspect of our curves; specifically, we will consider: (1) the most robust curve for each group [42]; (2) curves such that is closest between groups; (3) the smoothest curves; (4) curves that subject the fewest individuals to random outcomes, for example, ; and (5) curves that subject equal number of individuals to random outcomes between groups, e.g., where .

Acknowledgements

This research was conducted by the ARC Centre of Excellence for Automated Decision-Making and Society (project number CE200100005) funded by the Australian Government through the Australian Research Council.

References

- Dembczyński et al. [2010] Krzysztof Dembczyński, Weiwei Cheng, and Eyke Hüllermeier. Bayes optimal multilabel classification via probabilistic classifier chains. In Proceedings of the 27th International Conference on International Conference on Machine Learning, ICML’10, page 279–286, Madison, WI, USA, 2010. Omnipress. ISBN 9781605589077.

- Cimpoeşu et al. [2013] Mihai Cimpoeşu, Andrei Sucilă, and Henri Luchian. A statistical binary classifier: Probabilistic vector machine. In Luís Correia, Luís Paulo Reis, and José Cascalho, editors, Progress in Artificial Intelligence, pages 211–222, Berlin, Heidelberg, 2013. Springer Berlin Heidelberg. ISBN 978-3-642-40669-0.

- Spring et al. [2011] Laura Spring, Diana Robillard, Lorrie Gehlbach, and Tiffany A Moore Simas. Impact of pass/fail grading on medical students’ well-being and academic outcomes. Medical Education, 45(9):867–877, 2011. doi: https://doi.org/10.1111/j.1365-2923.2011.03989.x.

- Markov et al. [2022] Anton Markov, Zinaida Seleznyova, and Victor Lapshin. Credit scoring methods: Latest trends and points to consider. The Journal of Finance and Data Science, 8:180–201, 2022. ISSN 2405-9188. doi: https://doi.org/10.1016/j.jfds.2022.07.002. URL https://www.sciencedirect.com/science/article/pii/S2405918822000095.

- Yu et al. [2022] Chaojian Yu, Bo Han, Li Shen, Jun Yu, Chen Gong, Mingming Gong, and Tongliang Liu. Understanding robust overfitting of adversarial training and beyond. In Kamalika Chaudhuri, Stefanie Jegelka, Le Song, Csaba Szepesvari, Gang Niu, and Sivan Sabato, editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 25595–25610. PMLR, 17–23 Jul 2022. URL https://proceedings.mlr.press/v162/yu22b.html.

- Barceló et al. [2020] Pablo Barceló, Mikaël Monet, Jorge Pérez, and Bernardo Subercaseaux. Model interpretability through the lens of computational complexity. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 15487–15498. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/b1adda14824f50ef24ff1c05bb66faf3-Paper.pdf.

- Dutta et al. [2020] Sanghamitra Dutta, Dennis Wei, Hazar Yueksel, Pin-Yu Chen, Sijia Liu, and Kush Varshney. Is there a trade-off between fairness and accuracy? A perspective using mismatched hypothesis testing. In Hal Daumé III and Aarti Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 2803–2813. PMLR, 13–18 Jul 2020. URL https://proceedings.mlr.press/v119/dutta20a.html.

- Wang et al. [2021] Yuyan Wang, Xuezhi Wang, Alex Beutel, Flavien Prost, Jilin Chen, and Ed H. Chi. Understanding and improving fairness-accuracy trade-offs in multi-task learning. Proceedings of the 27th ACM SIGKDD Conference on Knowledge Discovery & Data Mining, 2021.

- Chen et al. [2018] Irene Chen, Fredrik D Johansson, and David Sontag. Why is my classifier discriminatory? In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018. URL https://proceedings.neurips.cc/paper/2018/file/1f1baa5b8edac74eb4eaa329f14a0361-Paper.pdf.

- Chen et al. [2021] Yan Chen, Christopher Mahoney, Isabella Grasso, Esma Wali, Abigail Matthews, Thomas Middleton, Mariama Njie, and Jeanna Matthews. Gender bias and under-representation in natural language processing across human languages. In Proceedings of the 2021 AAAI/ACM Conference on AI, Ethics, and Society, AIES ’21, page 24–34, New York, NY, USA, 2021. Association for Computing Machinery. ISBN 9781450384735. doi: 10.1145/3461702.3462530. URL https://doi.org/10.1145/3461702.3462530.

- Vogel et al. [2021] Robin Vogel, Aurélien Bellet, and Stephan Clémençon. Learning fair scoring functions: Bipartite ranking under ROC-based fairness constraints, 2021.

- Awasthi et al. [2020] Pranjal Awasthi, Matthäus Kleindessner, and Jamie Morgenstern. Equalized odds postprocessing under imperfect group information. In Silvia Chiappa and Roberto Calandra, editors, Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 1770–1780. PMLR, 26–28 Aug 2020. URL https://proceedings.mlr.press/v108/awasthi20a.html.

- Hardt et al. [2016] Moritz Hardt, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. In D. Lee, M. Sugiyama, U. Luxburg, I. Guyon, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 29. Curran Associates, Inc., 2016. URL https://proceedings.neurips.cc/paper/2016/file/9d2682367c3935defcb1f9e247a97c0d-Paper.pdf.

- U.S. Federal Reserve [2007] U.S. Federal Reserve. Report to the congress on credit scoring and its effects on the availability and affordability of credit. Board of Governors of the Federal Reserve System, 2007. URL https://github.com/fairmlbook/fairmlbook.github.io/tree/master/code/creditscore/data.

- Angwin et al. [2016] Julia Angwin, Jeff Larson, Surya Mattu, and Lauren Kirchner. Machine bias. ProPublica, 23, May 2016.

- Mehrabi et al. [2021] Ninareh Mehrabi, Fred Morstatter, Nripsuta Saxena, Kristina Lerman, and Aram Galstyan. A survey on bias and fairness in machine learning. ACM Comput. Surv., 54(6), jul 2021. ISSN 0360-0300. doi: 10.1145/3457607. URL https://doi.org/10.1145/3457607.

- Biswas and Rajan [2021] Sumon Biswas and Hridesh Rajan. Fair preprocessing: Towards understanding compositional fairness of data transformers in machine learning pipeline. In Proceedings of the 29th ACM Joint Meeting on European Software Engineering Conference and Symposium on the Foundations of Software Engineering, ESEC/FSE 2021, page 981–993, New York, NY, USA, 2021. Association for Computing Machinery. ISBN 9781450385626. doi: 10.1145/3468264.3468536. URL https://doi.org/10.1145/3468264.3468536.

- Wan et al. [2022] Mingyang Wan, Daochen Zha, Ninghao Liu, and Na Zou. In-processing modeling techniques for machine learning fairness: A survey. ACM Trans. Knowl. Discov. Data, jul 2022. ISSN 1556-4681. doi: 10.1145/3551390. URL https://doi.org/10.1145/3551390. Just Accepted.

- Lohia et al. [2019] Pranay K. Lohia, Karthikeyan Natesan Ramamurthy, Manish Bhide, Diptikalyan Saha, Kush R. Varshney, and Ruchir Puri. Bias mitigation post-processing for individual and group fairness. In ICASSP 2019 - 2019 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 2847–2851, 2019. doi: 10.1109/ICASSP.2019.8682620.

- Dwork et al. [2012] Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. Fairness through awareness. In Proceedings of the 3rd Innovations in Theoretical Computer Science Conference, ITCS ’12, page 214–226, New York, NY, USA, 2012. Association for Computing Machinery. ISBN 9781450311151. doi: 10.1145/2090236.2090255. URL https://doi.org/10.1145/2090236.2090255.

- Wilkinson et al. [2016] Mark Wilkinson, Michel Dumontier, IJsbrand Jan Aalbersberg, Gaby Appleton, Myles Axton, Arie Baak, Niklas Blomberg, Jan-Willem Boiten, Luiz Olavo Bonino da Silva Santos, Philip Bourne, Jildau Bouwman, Anthony Brookes, Tim Clark, Merce Crosas, Ingrid Dillo, Olivier Dumon, Scott Edmunds, Chris Evelo, Richard Finkers, and Barend Mons. The fair guiding principles for scientific data management and stewardship. Scientific Data, 3, 03 2016. doi: 10.1038/sdata.2016.18.

- Grgić-Hlača et al. [2016] N. Grgić-Hlača, M. B. Zafar, K. P. Gummadi, and A. Weller. The case for process fairness in learning: Feature selection for fair decision making. Symposium on Machine Learning and the Law at the 29th Conference on Neural Information Processing Systems, 3, 03 2016.

- Xu et al. [2021] Han Xu, Xiaorui Liu, Yaxin Li, Anil Jain, and Jiliang Tang. To be robust or to be fair: Towards fairness in adversarial training. In Marina Meila and Tong Zhang, editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 11492–11501. PMLR, 18–24 Jul 2021. URL https://proceedings.mlr.press/v139/xu21b.html.

- Binns [2020] Reuben Binns. On the apparent conflict between individual and group fairness. In Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, FAT ’20, page 514–524, New York, NY, USA, 2020. Association for Computing Machinery. ISBN 9781450369367. doi: 10.1145/3351095.3372864. URL https://doi.org/10.1145/3351095.3372864.

- Baumann et al. [2022] Joachim Baumann, Anikó Hannák, and Christoph Heitz. Enforcing group fairness in algorithmic decision making: Utility maximization under sufficiency. In 2022 ACM Conference on Fairness, Accountability, and Transparency, FAccT ’22, page 2315–2326, New York, NY, USA, 2022. Association for Computing Machinery. ISBN 9781450393522. doi: 10.1145/3531146.3534645. URL https://doi.org/10.1145/3531146.3534645.

- Castelnovo et al. [2022] Alessandro Castelnovo, Riccardo Crupi, Greta Greco, Daniele Regoli, Ilaria Penco, and Andrea Cosentini. A clarification of the nuances in the fairness metrics landscape. Scientific Reports, 12, 03 2022. doi: 10.1038/s41598-022-07939-1.

- Agarwal et al. [2018] Alekh Agarwal, Alina Beygelzimer, Miroslav Dudik, John Langford, and Hanna Wallach. A reductions approach to fair classification. In FATML’17. Association for Computing Machinery, March 2018. URL https://www.microsoft.com/en-us/research/publication/a-reductions-approach-to-fair-classification/.

- Woo et al. [2023] Sang Eun Woo, James M. LeBreton, Melissa G. Keith, and Louis Tay. Bias, fairness, and validity in graduate-school admissions: A psychometric perspective. Perspectives on Psychological Science, 18(1):3–31, 2023. doi: 10.1177/17456916211055374. URL https://doi.org/10.1177/17456916211055374. PMID: 35687736.

- Rajkomar et al. [2018] Alvin Rajkomar, Michaela Hardt, Michael D Howell, Greg Corrado, and Marshall H Chin. Ensuring fairness in machine learning to advance health equity. Annals of Internal Medicine, 169(12):866–872, 2018. doi: 10.7326/M18-1990. URL https://www.acpjournals.org/doi/abs/10.7326/M18-1990. PMID: 30508424.

- Romano et al. [2020] Yaniv Romano, Stephen Bates, and Emmanuel Candes. Achieving equalized odds by resampling sensitive attributes. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 361–371. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/03593ce517feac573fdaafa6dcedef61-Paper.pdf.

- Petersen et al. [2021] Felix Petersen, Debarghya Mukherjee, Yuekai Sun, and Mikhail Yurochkin. Post-processing for individual fairness. In M. Ranzato, A. Beygelzimer, Y. Dauphin, P.S. Liang, and J. Wortman Vaughan, editors, Advances in Neural Information Processing Systems, volume 34, pages 25944–25955. Curran Associates, Inc., 2021. URL https://proceedings.neurips.cc/paper/2021/file/d9fea4ca7e4a74c318ec27c1deb0796c-Paper.pdf.

- Belkin et al. [2006] Mikhail Belkin, Partha Niyogi, and Vikas Sindhwani. Manifold regularization: A geometric framework for learning from labeled and unlabeled examples. Journal of Machine Learning Research, 7(85):2399–2434, 2006. URL http://jmlr.org/papers/v7/belkin06a.html.

- Gneiting and Raftery [2007] Tilmann Gneiting and Adrian E Raftery. Strictly proper scoring rules, prediction, and estimation. Journal of the American Statistical Association, 102(477):359–378, 2007. doi: 10.1198/016214506000001437. URL https://doi.org/10.1198/016214506000001437.

- Gneiting [2011] Tilmann Gneiting. Making and evaluating point forecasts. Journal of the American Statistical Association, 106(494):746–762, 2011. ISSN 01621459. URL http://www.jstor.org/stable/41416407.

- Kil et al. [2021] Krzysztof Kil, Radosław Ciukaj, and Justyna Chrzanowska. Scoring models and credit risk: The case of cooperative banks in poland. Risks, 9(7), 2021. ISSN 2227-9091. doi: 10.3390/risks9070132. URL https://www.mdpi.com/2227-9091/9/7/132.

- Homonoff et al. [2021] Tatiana Homonoff, Rourke O’Brien, and Abigail B. Sussman. Does knowing your FICO score change financial behavior? Evidence from a field experiment with student loan borrowers. The Review of Economics and Statistics, 103(2):236–250, 05 2021. ISSN 0034-6535. doi: 10.1162/rest_a_00888. URL https://doi.org/10.1162/rest_a_00888.

- Federer [1996] H. Federer. Geometric Measure Theory. Classics in Mathematics. Springer Berlin Heidelberg, 1996. ISBN 9783540606567. URL https://books.google.com.au/books?id=8uOHQgAACAAJ.

- Estep [2002] Donald Estep. Practical analysis in one variable. Undergraduate Texts in Mathematics, page 83–87. Springer, 2002. ISBN 978-0387954844.

- Pennington-Cross [2003] A Pennington-Cross. Credit history and the performance of prime and nonprime mortgages. In The Journal of Real Estate Finance and Economics, pages 279–301. Curran Associates, Inc., 2003. URL https://doi.org/10.1023/A:1025891223226.

- Hanson et al. [2016] Andrew Hanson, Zackary Hawley, Hal Martin, and Bo Liu. Discrimination in mortgage lending: Evidence from a correspondence experiment. Journal of Urban Economics, 92:48–65, 2016. ISSN 0094-1190. doi: https://doi.org/10.1016/j.jue.2015.12.004. URL https://www.sciencedirect.com/science/article/pii/S0094119015000868.

- Sokol et al. [2022] Kacper Sokol, Meelis Kull, Jeffrey Chan, and Flora Dilys Salim. Fairness and ethics under model multiplicity in machine learning. arXiv preprint arXiv:2203.07139, 2022.

- Ma et al. [2022] Xinsong Ma, Zekai Wang, and Weiwei Liu. On the tradeoff between robustness and fairness. In Alice H. Oh, Alekh Agarwal, Danielle Belgrave, and Kyunghyun Cho, editors, Advances in Neural Information Processing Systems, 2022. URL https://openreview.net/forum?id=LqGA2JMLwBw.

Appendix A COMPAS Case Study

The COMPAS software222COMPAS guide: https://www.equivant.com/practitioners-guide-to-compas-core/; COMPAS documentation: https://doc.wi.gov/Pages/AboutDOC/COMPAS.aspx. (Correctional Offender Management Profiling for Alternative Sanctions) is a commercial tool used across multiple U.S. states to analyse and predict a defendant’s behaviour if released on bail. The software output can be considered by judges during sentencing, albeit such a practice must be disclosed. Specifically, COMPAS offers three insights:

-

1.

likelihood of general recidivism (re-offending);

-

2.

likelihood of violent recidivism (committing a violent crime); and

-

3.

likelihood of failing to appear in court (pretrial flight risk).

Here, we focus on the risk of re-offending using the raw COMPAS scores available in the ProPublica data set333https://github.com/propublica/compas-analysis [15]. The COMPAS algorithm uses characteristics such as criminal history, known associates, drug involvement and indicators of juvenile delinquency in order to calculate a score , where a higher score corresponds to a higher likelihood of recidivism. As is the case with CreditRisk (Section 5), the scoring algorithm used by the COMPAS software is proprietary. Given its high-stakes nature, it is important to understand the predictive behaviour of this tool since its social situatedness captured by the (protected) data features – which are translated into the score – may yield biased results.

To this end, we define as the Cartesian product of two sensitive attributes, sex and race , found in the COMPAS data set, such that and . Additionally, normalised COMPAS scores for a population of interest are denoted with ; the ground truth label for each score in is given by , where corresponds to individuals who committed an offence in a two-year time window; and captures crisp predictions, with indicating high risk (of recidivism). Studying the link between the scores and labels provided by the COMPAS data set – refer to Figure 9 in Appendix H – indicates that for most values of across all groups encoded by , if , then:

| (6) |

Therefore, we are in a good position to use the monotonic probability functions proposed by this paper to build the final classifier.

Given the aforementioned relationship, it is in the public’s (and judicial system’s) best interest to always increase the probability of classifying an individual as high-risk when the score increases. However, fixed randomisation does not allow for this. For example, under fixed randomisation a Caucasian male with a COMPAS score in the range has an chance of being classified as high-risk (see Table 4); nevertheless, a Caucasian male at the top of this score range is almost twice as likely to commit an offence as a Caucasian male with a score at the low end of this range. Therefore, fixed randomisation is unfair on three fronts:

-

1.

Caucasian males with scores in the lower range of are treated the same as Caucasian males with scores in the higher range of this interval;

-

2.

higher risk individuals are not labeled as such despite their score indicating so; and

-

3.

individuals whose outcome is randomised are never offered the same odds as members of other protected groups (in violation of Definition 3.2).

Notably, these arguments apply to all groups in the protected attribute and not only Caucasian males.

| Caucasian male | Caucasian female | African-American female | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| acc (%) | EO | acc (%) | EO | acc (%) | EO | ||||||

| fixed [13] | |||||||||||

| linear | |||||||||||

| quadratic | |||||||||||

| cubic | |||||||||||

| 4th order | |||||||||||

The between-group equalised odds measure when we maximise accuracy separately for each group is . Mirroring Section 5, we apply our method to the COMPAS model in order to reduce the equalised odds disparity without breaking individual fairness. We therefore seek to calibrate the model with a combination of thresholds and probabilities that parameterise the continuous curves defined in Appendix E using nothing but the joint distributions of . We then compare the continuous solutions to the step function solution (fixed randomisation) defined in Equation 3.

The results reported in Table 2 and Figure 6 show that continuous curves can be used to simultaneously satisfy equalised odds, individual fairness and individual odds. Since low-scoring individuals are less likely to be classified as high-risk, defendants have an incentive to engage in behaviours that actively lower their COMPAS score. Furthermore, public safety is prioritised more effectively since individuals with a measurably higher probability of recidivism are given higher odds of being classified as high-risk.

Appendix B Similarity Measures

As discussed in Section 2, distance on metric spaces, regardless of its definition, must follow a set of axioms. If is a metric space and , then :

-

•

– the distance between a point and itself is ;

-

•

if , – the distance between two different points is strictly greater than ;

-

•

– the distance between two different points and is equal to the distance between and ; and

-

•

– the distance between any two points is equal to or less than the distance given by visiting another point on a journey between the original two points (triangle inequality).

Defining “similar individuals” can be quite challenging, and is deeply rooted in the landscape and shape of the input space, the complexity of the problem, and the density and distribution of the training data within the space. This problem is also not strictly mathematical and depends highly on context. Additionally, discrete or categorical data can be difficult to quantify and compare; for example, in a feature space of size , how different is an unmarried individual from a married person, all other things being equal? One could argue that its importance depends on the size of – a large value of can dilute the importance of each individual feature. If we are trying to predict whether an individual has any children, however, this feature is of high importance regardless of the size of . To best capture such dependencies, we can employ similarity graphs or bespoke distance metrics chosen based on the problem definition and data set that we work with.

Using tailor-made definitions of similarity, nevertheless, poses two issues:

-

1.

it makes it difficult to compare results between experiments; and

-

2.

the results are subject to the quality of the metric and its suitability for the problem at hand.

As stated in the paper, model inputs are inaccessible; we are only given scores, values of the protected attribute and the label (ground truth). For our work we therefore rely on generic distance metrics such as Euclidean, Hamming, and Gower’s distances. Note that we assume that changing the protected class for an individual is too large of a change to label the two instances as similar since this alteration entails using a different set of thresholds and probabilities in the final decision function.

Euclidean Distance (Comparison of Continuous Features)

The -norm is defined as:

and is the foundation of Euclidean distance defined as:

and so:

Hamming Distance (Comparison of Discrete Features)

The -norm is defined as:

| (7) |

and is the foundation of Hamming distance , which counts the number of features that differ between two inputs and , and is defined as:

where is the XOR operation. Therefore, is simply a vector of ’s and ’s such that:

| (8) |

For example:

Gower’s Distance (Mixed Continuous and Discrete Features)

Take that contain both continuous (numerical) variables and discrete (categorical) variables. We then consider each variable for . If is continuous:

where is the range of th feature. Fundamentally, the second term is the normalised -norm, defined in Equation 7, on the differences between two vectors. However, if is discrete, we use the Iverson operation:

As such, a value of for both continuous and discrete features implies that , and implies that and are maximally different. We put this together to get Gower’s Similarity Coefficient:

| (9) |

which is bounded within . However, this coefficient does not follow the axioms laid out at the beginning of this section as . Therefore, we define Gower’s distance using Equation 9, giving:

which offers the behaviour expected of a distance metric.

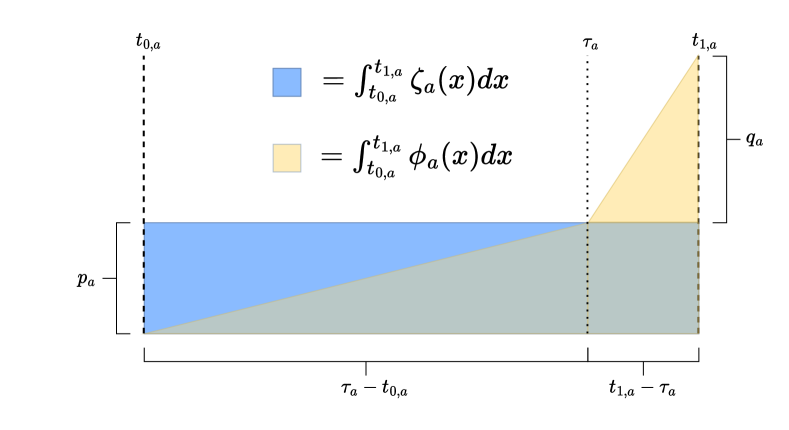

Appendix C Geometric Motivation for the Average Probability (Linear Case)

We can parameterise each set of potential solutions for each value of (i.e., protected sub-population) by only 3 parameters – , and – by constraining the area under each curve as equal to . This forces all potential solutions with the same set of parameters to have the same average probability between the thresholds.

C.1 Proof (Point of Intersection)

Here, we discuss the details of bounding the piece-wise linear solution such that the two lines join at . We present a proof that this value can be easily found, and is defined only through , and .

We begin by assuming that the solution is linear in nature and, as outlined in the paper (Section 4.1), they preserve the average probability of the step function within the interval . As such, we can generate a geometric interpretation of the solution as shown in Figure 7. From here, we can see that finding is straight forward. By combining the area of a triangle equation, area of a rectangle equation, and forming an equality between equations, we get:

which can be interpreted as Rectangle = Triangle 1 + Triangle 2 + Small Rectangle. We can then rearrange the notation as follows:

Since we know that :

We therefore define to get the final result from Section 4.2:

| (10) |

C.2 and Proof (Piece-wise Linear Solution)

We define the linear form of the interpolant:

| (11) |

where each is linear, so:

In order to derive the final form, we must assume the following conditions (continuity):

-

1.

;

-

2.

; and

-

3.

.

From the difference of these equations, we get:

From the proof in Appendix C.1, we know that (Equation 10), giving:

Similarly, from conditions 2 and 3:

The difference yields:

From the definition of and :

Substituting these values back into the equations yields the final parameters:

Putting it all back into the piece-wise equation and factorising then gives:

| (12) |

C.3 Preservation of Average Probability Proof

We previously stated that solutions with the same set of parameters should always have the same average probability. For example, the linear solution preserves group fairness introduced by the step function by maintaining the same predictive behaviour (on average) in the interval. This follows directly from how we defined: (1) the linear solution; and (2) the point of intersection. Nonetheless, we can also prove this property directly. If is the step function for , we follow by stating that we require:

The first thing to observe is that, from Equations 3 and 5:

and so:

We know that the integral in the interval for the step function is:

| (13) | ||||

From Equation 11 in Appendix C.2 we know that:

| (14) |

We can decompose the integral of the piece-wise linear solution into two integrals over the interval, so using Equation 14:

| (15) |

Therefore, from Equation 12:

From definition of and in Appendix C.1:

| (16) |

Also from Equation 12, we have:

and again, from definition of and in Appendix C.1:

| (17) |

Then, from Equations 15, 16 and 17, and recalling that , we get:

and therefore:

which means:

(Proofs for other curves follow the same logic.)

Appendix D Obtaining Full-rank Linear Systems to Find Closed-form Piece-wise Solutions of Differing Smoothness

D.1 Linear System

We search for a family of possible solutions for each group , satisfying equalised odds (Definition 2.1), that adhere to the following constraints:

- Continuity

-

- Monotonicity

-

- Preservation of Probability

-

By assuming that each , we can use these constraints (as well as other, more strict constraints) to find solutions to this problem of varying smoothness by solving the linear system:

where . (Continuous, non-smooth solutions to this linear problem are given in Appendix C.)

D.2 Closed-form Smoothness for

Here, we search for a smooth closed-form solution to the above problem. For simplicity, we assume that and , however the solution can be generalised to arbitrary thresholds by applying shift and stretch operations.

We have the following constraints:

-

1.

;

-

2.

;

-

3.

;

-

4.

; and

-

5.

.

Having five constraints requires five coefficients, and so we assume that:

We know that:

and so we have the following well-defined, full-rank linear system:

After solving the system, we get:

If the scoring function and , then this gives the final solution:

This function, however, is only monotonic for .

D.3 Piece-wise Cubic Interpolant

The closed-form, 4th order solution satisfies the smoothness and boundary constraints, but violates the monotonic constraint for any probability outside of the range. We can address this issue by constructing a piece-wise spline based on cubic polynomials:

However, we need to add two additional constraints to the optimisation problem: an agreed meeting point and an agreed derivative at the meeting point. Again, assuming that and – recall that we can shift and rescale the solution later – we get:

-

1.

;

-

2.

;

-

3.

;

-

4.

;

-

5.

;

-

6.

;

-

7.

; and

-

8.

.

Since:

and

we get the following linear system:

Solving yields:

We then take the solution to be:

Appendix E Closed-form Equations for Probability Curves in Figure 4

The general form is:

We use smoothness and continuity constraints from Appendix D to find the definitions of .

Linear Form

| (18) |

Quadratic Form

| (19) |

Cubic Form

| (20) | ||||

4th Order Polynomial Form

| (21) |

(Note that the 4th order polynomial is not monotonic if .)

Appendix F Optimal Parameters for Equalised Odds

All possible solutions, including that of fixed randomisation, are defined using a single probability parameter and a pair of thresholds . The parameters used to find a decision-making function – for fixed randomisation and for preferential randomisation – are given in Tables 3 and 4 respectively for the CreditRisk and COMPAS data sets.

Appendix G Maximum for Different Curves

As discussed in Section 4.2, we know that:

Since these curves are specified through closed-form solutions parameterised by and on a known interval , can be found analytically for each curve. Here we show the derivation procedure for the linear and 4th order solutions. The other curves (cubic and quadratic) follow the same protocol.

The linear solution is defined in Equation 12. As such, we know that:

Thus, the value of is related to the value of and the distance between the thresholds with:

The 4th order is define in Equation 21, and takes the form:

where

| (22) |

Since the definition of is always constrained such that it is monotonic and , the maximum derivative always occurs at the point of inflexion, or:

From Equation 22:

and so from the quadratic formula for :

where we ignore the second root, as it takes out of range. We can use this to find , which assumes and are fixed at and respectively, and apply a re-scaling such that:

This method works for all valid values of , except when where is reduced to a cubic equation, and thus the point of inflexion is perfectly between the two thresholds:

Then:

Appendix H Probability Functions

In our case studies, we look at functions capturing the probability of for an individual with a score . Figure 8 shows this for CreditRisk, where is the credit score and is not defaulting on a loan in the last days. Figure 9 displays this information for COMPAS, where is the COMPAS score and is re-offending in the last years. Ideally, we should see the probability of increase as increases, and this is the general behaviour we observe for both case studies.