Column Subset Selection and Nyström Approximation via Continuous Optimization

Abstract

We propose a continuous optimization algorithm for the Column Subset Selection Problem (CSSP) and Nyström approximation. The CSSP and Nyström method construct low-rank approximations of matrices based on a predetermined subset of columns. It is well known that choosing the best column subset of size is a difficult combinatorial problem. In this work, we show how one can approximate the optimal solution by defining a penalized continuous loss function which is minimized via stochastic gradient descent. We show that the gradients of this loss function can be estimated efficiently using matrix-vector products with a data matrix in the case of the CSSP or a kernel matrix in the case of the Nyström approximation. We provide numerical results for a number of real datasets showing that this continuous optimization is competitive against existing methods.

1 Introduction

Recent advances in the technological ability to capture and collect data have meant that high-dimensional datasets are now ubiquitous in the fields of engineering, economics, finance, biology, and health sciences to name a few. In the case where the data collected is not labeled it is often desirable to obtain an accurate low-rank approximation for the data which is relatively low-cost to obtain and memory efficient. Such an approximation is useful to speed up downstream matrix computations that are often required in large-scale learning algorithms. The Column Subset Selection Problem (CSSP) and Nyström method are two such tools that generate low-rank approximations based on a subset of data instances or features from the dataset. The chosen subset of instances or features are commonly referred to as “landmark” points. The choice of landmark points determines how accurate the low-rank approximation is.

The challenge in the CSSP is to select the best columns of a data matrix that span its column space. That is, for any binary vector , compute

| (1) |

where is the Frobenius matrix norm, and is the projection matrix onto span ( being the -th column of ).

Solving this combinatorial problem exactly is known to be NP-complete (Shitov, 2021), and is practically infeasible even when is of moderate size. We propose a novel continuous optimization algorithm to approximate the exact solution to this problem. While an optimization approach via Group Lasso (Yuan & Lin, 2006) exists for the convex relaxation of this problem (Bien et al., 2010), to the best of our knowledge, no continuous optimization method has been developed to solve the highly non-convex combinatorial problem (1). To introduce our approach for the CSSP, instead of searching over binary vectors , we consider the hyper-cube and define for each a matrix which allows the following well-defined penalized continuous extension of the exact problem,

The parameter plays an analogous role to that of the regularization parameter in regularized linear regression methods (Tibshirani, 1996) and controls the sparsity of the solution, that is, the size of . Two aspects of this continuous extension make it useful for approximating the exact solution. Firstly, the continuous loss agrees with the discrete loss at every corner point of the hypercube , and secondly, for large datasets the gradient can be estimated via an unbiased stochastic estimate. To obtain an approximate solution to the exact problem, stochastic gradient descent (SGD) is implemented on the penalized loss. After starting at an interior point of the hyper-cube, under SGD, the vector moves towards a corner point, and some of the ’s exhibit shrinkage to zero. It is these values that indicate which columns in should not be selected as landmark points.

The Nyström approximation (Williams & Seeger, 2000; Drineas et al., 2005) is a popular variant of the CSSP for positive semi-definite kernel matrices. The Nyström method also constructs a low-rank approximation to the true kernel matrix using a subset of columns. Once the columns are selected, (in factored form) takes additional time to compute, requires space to store, and can be manipulated quickly in downstream applications, e.g., inverting takes time. In addition to the continuous extension for the CSSP, in this paper, we provide a continuous optimization algorithm that can approximate the best columns to be used to construct (Section 2.2).

The continuous algorithm for the CSSP formulated in this paper utilizes SGD where at each iteration one can estimate the gradient with a cost of . We show that the gradients of the penalized continuous loss can be estimated via linear solves with random vectors that are approximated with the conjugate gradient algorithm (CG) (Golub & Van Loan, 1996), which itself is an iterative algorithm that only requires matrix-vector multiplications (MVMs) with the matrix . Similarly, for the Nyström method we show that at each step of the gradient descent, the gradient can be estimated in time requiring only matrix-vector multiplications with the kernel matrix . This is especially useful in cases where we only have access to a black-box MVM function. The fact that both these algorithms require only matrix-vector multiplications to estimate the gradients lends itself to utilizing GPU hardware acceleration. Moreover, the computations in the proposed algorithm can exploit the sparsity that is achieved by working only with the columns of that are selected by the algorithm at any given iteration.

1.1 Related Work

There exists extensive literature on random sampling methods for the approximation of the exact CSSP and Nyström problem. Sampling techniques such as adaptive sampling (Deshpande & Vempala, 2006), ridge leverage scores (Gittens & Mahoney, 2013; Musco & Musco, 2017; Alaoui & Mahoney, 2015) attempt to sample “important” and “diverse” columns. In particular, recent attention has been paid to Determinantal Point Processes (DPPs) (Hough et al., 2006; Derezinski & Mahoney, 2021). DPPs provide strong theoretical guarantees (Derezinski et al., 2020) for the CSSP and Nyström approximation and are amenable to efficient numerical implementation (Li et al., 2016; Derezinski et al., 2019; Calandriello et al., 2020; Dereziński, 2019). Outside of sampling methods, iterative methods such as Greedy selection (Farahat et al., 2011, 2013) have been shown to perform well in practice and exhibit provable guarantees (Altschuler et al., 2016).

Column selection has been extensively studied in the supervised context of linear regression (more commonly referred to as feature or variable selection). Penalized regression methods such as the Lasso (Tibshirani, 1996) have been widely applied to select columns of a predictor matrix that best explain a response vector. The canonical -best subset or -penalized regression problem is another penalized regression method, where the goal is to find the best subset of predictors that best fit a response (Beale et al., 1967; Hocking & Leslie, 1967). The recently proposed Continuous Optimization Method Towards Best Subset Selection (COMBSS) algorithm (Moka et al., 2022) attempts to solve the -penalized regression problem by minimizing a continuous loss that approximates the exact solution. The algorithm we propose for the CSSP in this paper can be viewed as an adaptation of COMBSS to the unsupervised setting. In this setting, the goal is to find the best subset of size for a multiple multivariate regression model where both the response and predictor matrix are . Interestingly, this framework can be extended to include a continuous selection loss for the Nyström approximation.

The rest of the paper is structured as follows. In Section 2 we describe the continuous extension for the CSSP and the Nyström method. In Section 3 we provide steps for the efficient implementation of our proposed continuous algorithm on large matrices and in Section 4 we provide numerical results on a variety of real datasets.

2 Continuous Loss for Landmark Selection

In this section, we formally define the CSSP and the best size -Nyström approximation. Then, we provide the mathematical setup for the continuous extension of the exact problem.

2.1 Column Subset Selection

Let and for any binary vector , let denote the matrix of size keeping only columns of where , for . Then for every integer the CSSP finds

| (2) |

where ( denotes Moore–Penrose inverse) is the projection matrix onto and is the -th column of . By expanding the Frobenius norm it is easy to see that the discrete problem (2) can be re-formulated as,

We now define a new matrix function on which acts as a continuous generalization of .

Definition 2.1.

For , define as the diagonal matrix with diagonal elements and

where is a fixed constant.

Although not explicitly stated in (Moka et al., 2022), is used as the continuous generalization for the hat matrix to solve the -penalized regression problem.

The main difference between this definition and traditional sampling methods is that instead of multiplying by a sampling matrix to obtain we compute the matrix which weights column of by the parameter . Intuitively, the matrix can be viewed as a convex combination of the matrices and .

From an evaluation standpoint, the pseudo-inverse need not be evaluated for any interior point in this newly defined function. We remark that for any the matrix inverse in Definition 2.1 exists and therefore,

We now state two results for the function and its relationship with the projection matrix . The following Lemmas (2.2 and 2.3) are extensions of the results stated in (Moka et al., 2022).

Lemma 2.2.

For any binary vector , exists and

Lemma 2.3.

is continuous element-wise over . Moreover, for any sequence converging to , the limit exists and

We note that the proof of Lemma 2.3 follows identically to the proof of Theorem 3 in (Moka et al., 2022) where it is stated that the function is continuous over for any fixed vector .

Given is continuous on and agrees with at every corner point we can define the continuous generalization of the exact problem (2),

Instead of solving this constrained problem, for a tunable parameter , we consider minimizing the Lagrangian function,

In Section 3 we reformulate this box-constrained problem into an equivalent unconstrained problem via a nonlinear mapping for that forces to be in the hypercube . We solve this optimization via continuous gradient descent. To this end, we need to evaluate the gradient for any interior point.

Lemma 2.4.

Let , and . Then, for ,

Evaluating has a computational complexity of due to the required inversion of . In Section 3 we detail an unbiased estimate for which utilizes the CG algorithm, where the most expensive operations involved are matrix-vector multiplications with and , which reduces the computational complexity to .

2.2 Nyström Method

We now turn our attention to defining a continuous objective for the landmark points in the Nyström approximation. We consider optimizing the landmark points first with respect to the trace matrix norm and then to the Frobenius matrix norm.

In many applications, we are interested in obtaining a low-rank approximation to a kernel matrix . Consider an input space and a positive semi-definite kernel function . Given a set of input points , the kernel matrix is defined by and is positive semi-definite.

For any binary vector let be the matrix with columns indexed by and be the principal sub-matrix indexed by . The Nyström low-rank approximation for is given by,

The following observation appearing in (Derezinski et al., 2020) connects the CSSP and the Nyström approximation with respect to the trace matrix norm.

Suppose we have the decomposition of the kernel matrix where . Then, the Nyström approximation is given by and

where for is the trace matrix norm. This connection is used in (Derezinski et al., 2020) to provide shared approximation bounds for both the CSSP and Nyström approximation. Given that the kernel matrix is always positive semi-definite, the decomposition always exists and one can solve the CSSP for to obtain the best -landmark Nyström approximation with respect to the trace norm. We note that such a decomposition is not unique, e.g., it can be the Cholesky decomposition or the symmetric square-root decomposition.

The matrix does not need explicit evaluation in order to perform CSSP as one can attain with the matrix instead (see, Lemma 2.4). Therefore, finding the decomposition is not required, and one can approximately solve the CSSP by minimizing with the kernel matrix .

Suppose instead we want to use the Frobenius matrix norm to find the best choice of columns of the matrix to construct the Nyström approximation. This problem is formulated as

| (3) |

Similar to we can weight each column of by instead of sampling the columns for the Nyström approximation. We define continuous generalization for the Nyström approximation,

Definition 2.5.

For let and

where is a fixed constant. Similar to , for any the matrix is invertible.

In the following two results, we state that is a continuous function on and agrees with the exact Nyström approximation at every corner point.

Lemma 2.6.

For any corner point , exists and

Lemma 2.7.

is continuous element-wise over . Moreover, for any sequence converging to , the limit exists and

We therefore have the continuous generalization of the exact problem (3),

Instead of solving this constrained problem, for a tunable parameter , we consider minimizing the Lagrangian function,

As with the continuous extension for CSSP we use a gradient descent method to solve the above problem. The following result provides an expression for for .

Lemma 2.8.

Let , and . Then, for ,

Evaluating has a computational complexity of due to the required inversion of and evaluation of . As with we detail an unbiased estimate for in Section 3 which utilizes matrix-vector multiplications with and that helps in reducing the computational cost.

3 Implementation

In this section, we detail how to efficiently solve the continuous problems posed in Section 2. In particular, we detail a non-linear transformation that was also used in (Moka et al., 2022) to make both the CSSP and Nyström approximation optimization problems unconstrained. We then show how one can estimate the gradients using MVMs with and .

3.1 Handling Box Constraints (Moka et al., 2022)

The continuous extension of the CSSP and Nyström approximation requires minimizing the functions and over . We now consider a non-linear transformation to make both optimization problems unconstrained. Consider the mapping given by,

then if we consider the optimization of continuous CSSP,

we attain the solution to (2.1) by evaluating . This is true because for any ,

In vector form the transformation is (here denotes element-wise multiplication) and using the chain rule we obtain for ,

We can now implement a gradient descent algorithm to approximately obtain . Using this approximation we can select an appropriate binary vector as a solution to the exact problem (2). The same transformation can be applied to solve over .

3.2 Stochastic Estimate for the Gradient

As discussed in Section 2, and are problematic to compute for large due to the complexity of inverting a matrix. Here we show that we can implement a stochastic gradient descent (SGD) which has strong theoretical guarantees (Robbins & Monro, 1951) by using an unbiased estimate for and .

The method we employ is a factorized estimator for the diagonal of a square matrix. Suppose we wish to estimate the diagonal of the matrix where . Let be a random vector sampled from the Rademacher distribution, whose entries are either or , each with probability . Then an unbiased estimate for is , see (Martens et al., 2012). Further analysis of its properties including its variance can be found in (Mathur et al., 2021). We note that when and , this estimator reduces to the well-known (Bekas et al., 2007) estimator for the diagonal.

The two following results provide an unbiased estimate for and using the factorized estimator for the diagonal of a matrix.

Lemma 3.1.

Recall that in the continuous CSSP optimization for , we have the definitions for , , and .

Suppose follows a Rademacher distribution and let:

and

Then for ,

Lemma 3.2.

Recall that in the continuous Nyström optimization for a kernel matrix , we have the definitions for , and .

Suppose follows a Rademacher distribution and let:

and

Then for ,

Using these results, we can obtain for a Monte-Carlo size , the approximations and , where and are evaluated using a sample drawn from the Rademacher distribution.

These results show that to evaluate stochastic gradients one needs to solve linear systems efficiently with the matrix . These systems can be iteratively solved using the conjugate gradient (CG) algorithm (Golub & Van Loan, 1996) which uses a sequence of MVMs with . Multiplying a vector with can be reduced to a single MVM with the matrix and a sequence of element-wise vector multiplications and additions.

3.3 Obtaining a Solution

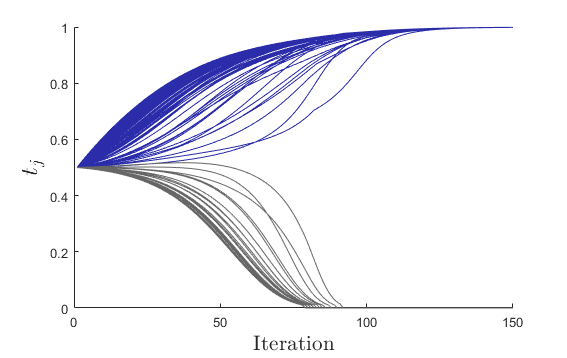

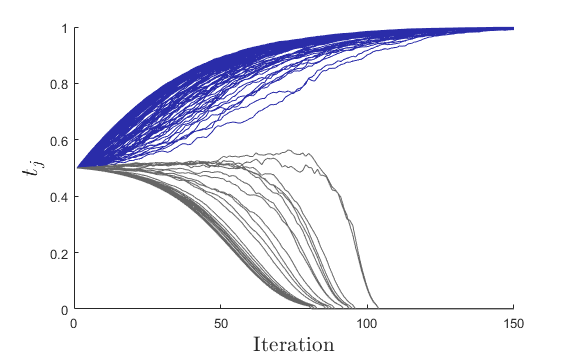

While we have re-framed both the CSSP and the Nyström problem as an optimization over , the priority remains to obtain an approximate solution to (2) and (3). To obtain such a binary vector, we first initialize SGD from a starting point and return the final value after a termination condition for SGD has been satisfied. Under SGD the iterative sequence moves towards a corner point of the hypercube. To obtain the closest corner point , we map the insignificant ’s to and all the other ’s to 1 for some tolerance parameter . This implementation is shown Algorithm 1. In Figure 1 we provide example solution paths under both batch gradient descent and SGD.

When choosing the value for it is important to consider the following true statements: if and only if and

These facts imply that if is set to zero during the course of the optimization it will remain unchanged thereafter. Therefore, it is important to choose that is away from any corner point. It is for this reason, we set in all our experiments.

3.4 Dimensionality Reduction

In Section 3.3 we stated that if is set to zero during the course of the SGD then it will remain unchanged thereafter. This opens the possibility to reduce the computational cost of estimating and by only focusing on terms where .

Let and for any let . For a vector , denote the vector of dimension (respectively ) constructed from by removing the elements with indices that are in (respectively, in ). Likewise, for a matrix , denote the principal sub-matrix (respectively, ) that is constructed by removing the rows and columns with indices that are in (respectively, in ). Then, we have the following result.

Lemma 3.3.

For any expression where and ,

where,

To incorporate this result in our algorithm, we set a small constant and during the course of SGD if , we set its value to zero. Thereafter, when solving and in either Lemma 3.1 (CSSP) or Lemma 3.2 (Nyström) the dimension of the linear system is .

3.5 Complexity Analysis

The main computational cost of our algorithm is the complexity attributed to estimating the gradients at each iteration of SGD. For simplicity of analysis, we assume the dimensionality reduction described in Section 3.4 is not carried out. The cost to solve and in either Lemma 3.1 or 3.2 via CG is flops where is the number of CG iterations and is the cost of computing a matrix-vector product with either (CSSP) or kernel matrix (Nyström). Generally, only iterations of CG are required to obtain an accurate solution to the linear system.

The cost is and via direct computation for and respectively. For kernel matrices with specific structure, this cost can be reduced. For example, for Toeplitz matrices or for matrices constructed from a kernel function that is analytic and isotropic, the cost can be reduced to quasi-linear complexity (Dietrich & Newsam, 1997; Gardner et al., 2018; Ryan et al., 2022). Utilizing GPU hardware for accelerating matrix computations has gained significant recent attention and numerous software regimes (Charlier et al., 2021; Hu et al., 2022) have been proposed to accelerate kernel MVMs. These methods can be implemented out-of-the-box and allow MVMs to be feasible on very large datasets (). Another advantage of these algorithms is that, as long as the kernel function is given, MVMs can be computed directly without ever storing the kernel matrix . This is an advantage of our method when compared to other methods such as the greedy selection method for the Nyström approximation in (Farahat et al., 2011), which has a cost of and requires the full explicit matrix to be stored in memory.

3.6 Role of parameters and

The tuning parameter controls the size of the penalty which is added to the Frobenius matrix loss. It is intuitive then that for a larger value of a stronger shrinkage is applied to during the course of the continuous optimization. In terms of curvature, as increases so does the directional slope of and in the region around . For this reason, it is likelier that more ’s will be pushed towards zero when the value for is large. This behavior is similar to that of the parameter in the COMBSS method (Moka et al., 2022) where a more formal analysis can be found. We note that the relationship between and is data dependent and it is suggested that the user apply an efficient grid search regime to obtain an appropriate for their use.

With respect to the parameter we first note that Lemma 2.2 and Lemma 2.6 remain true regardless of the choice of . Therefore, the value of affects the behavior of the penalized loss only at the interior points . We would like a choice of such that for all the interior points the functions and are well-behaved. When is very small the linear systems that require solving at may be close to singular and numerical issues can arise more frequently. Moreover, when is large we observe large shifts in the value of the objective approaching a corner point. Our simulations indicate that produces a well-behaved function.

4 Numerical Experiments and Results

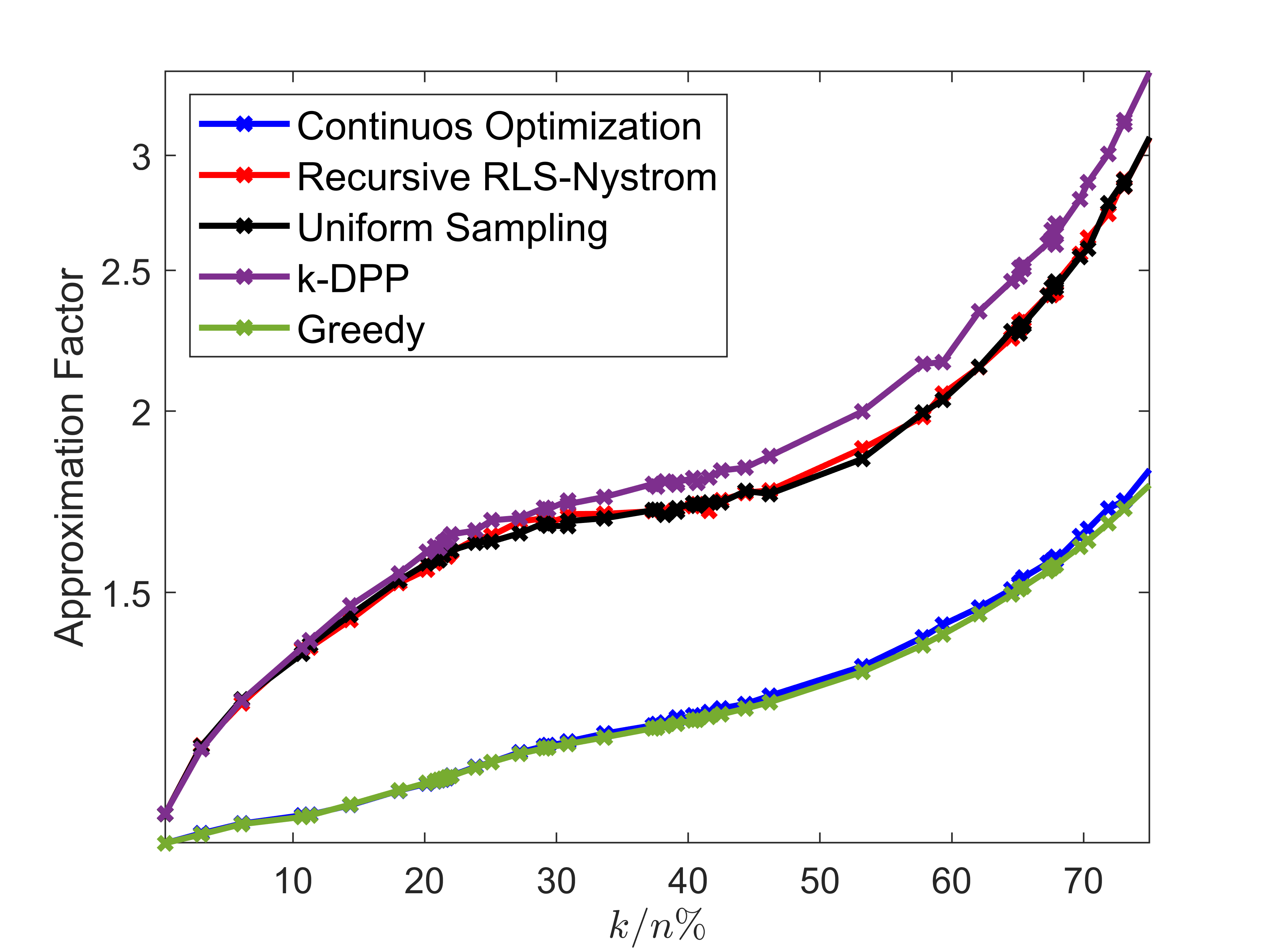

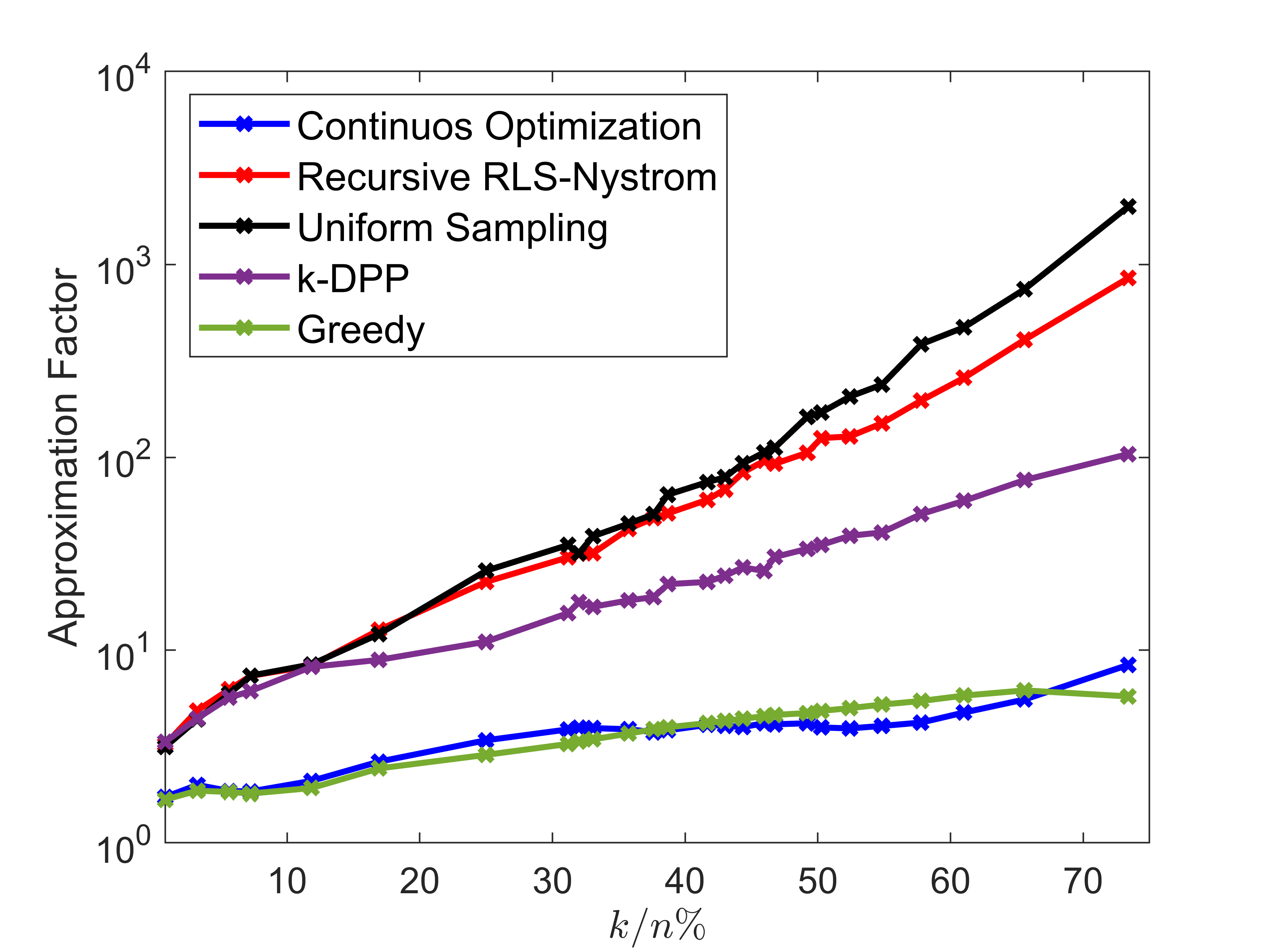

In this section, we provide numerical examples with real data designed to demonstrate that our proposed continuous optimization method outperforms well-known sampling-based methods for small and large datasets. Moreover, we demonstrate that when it is feasible to run greedy selection, our continuous method exhibits very similar performance.

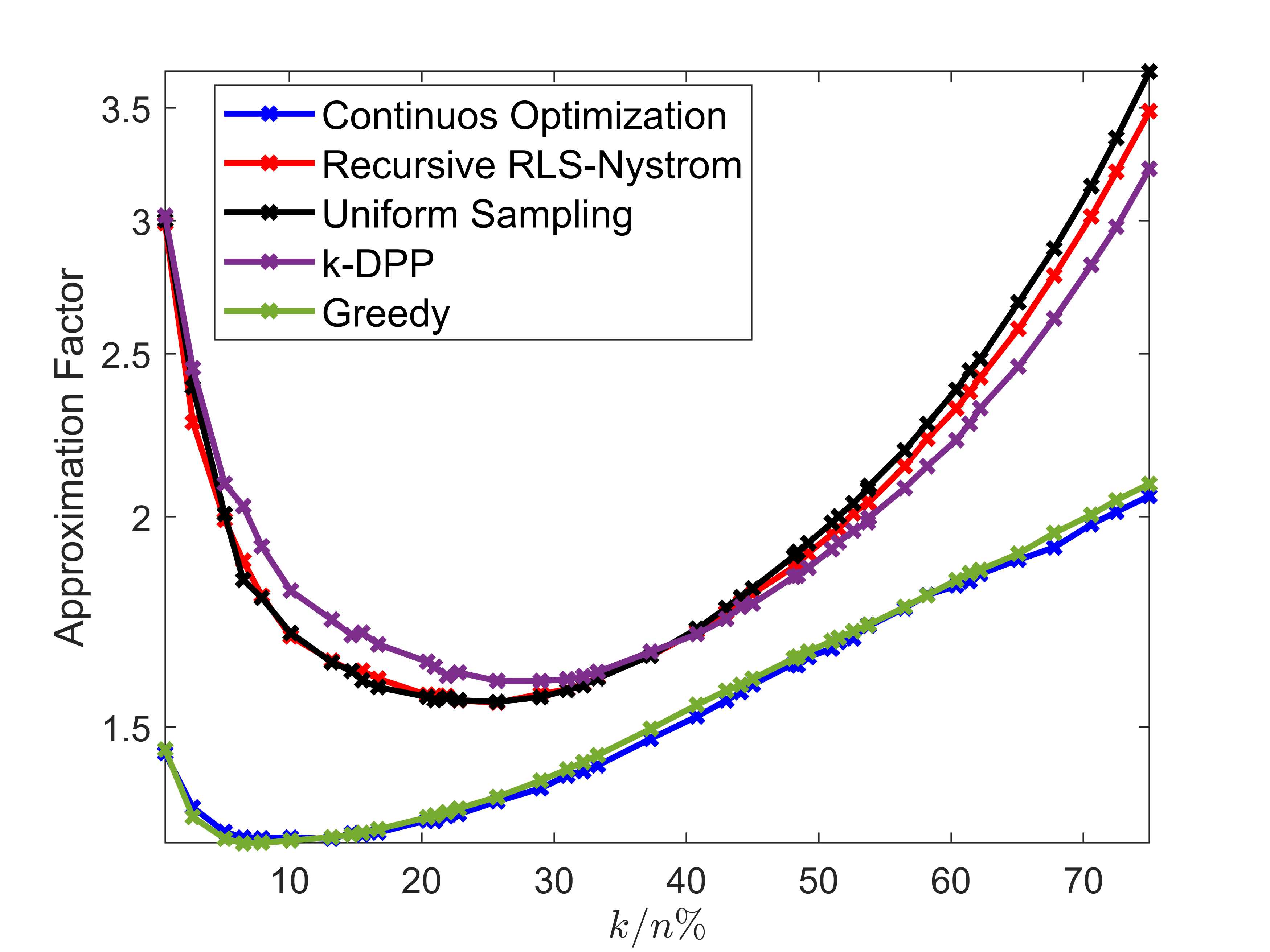

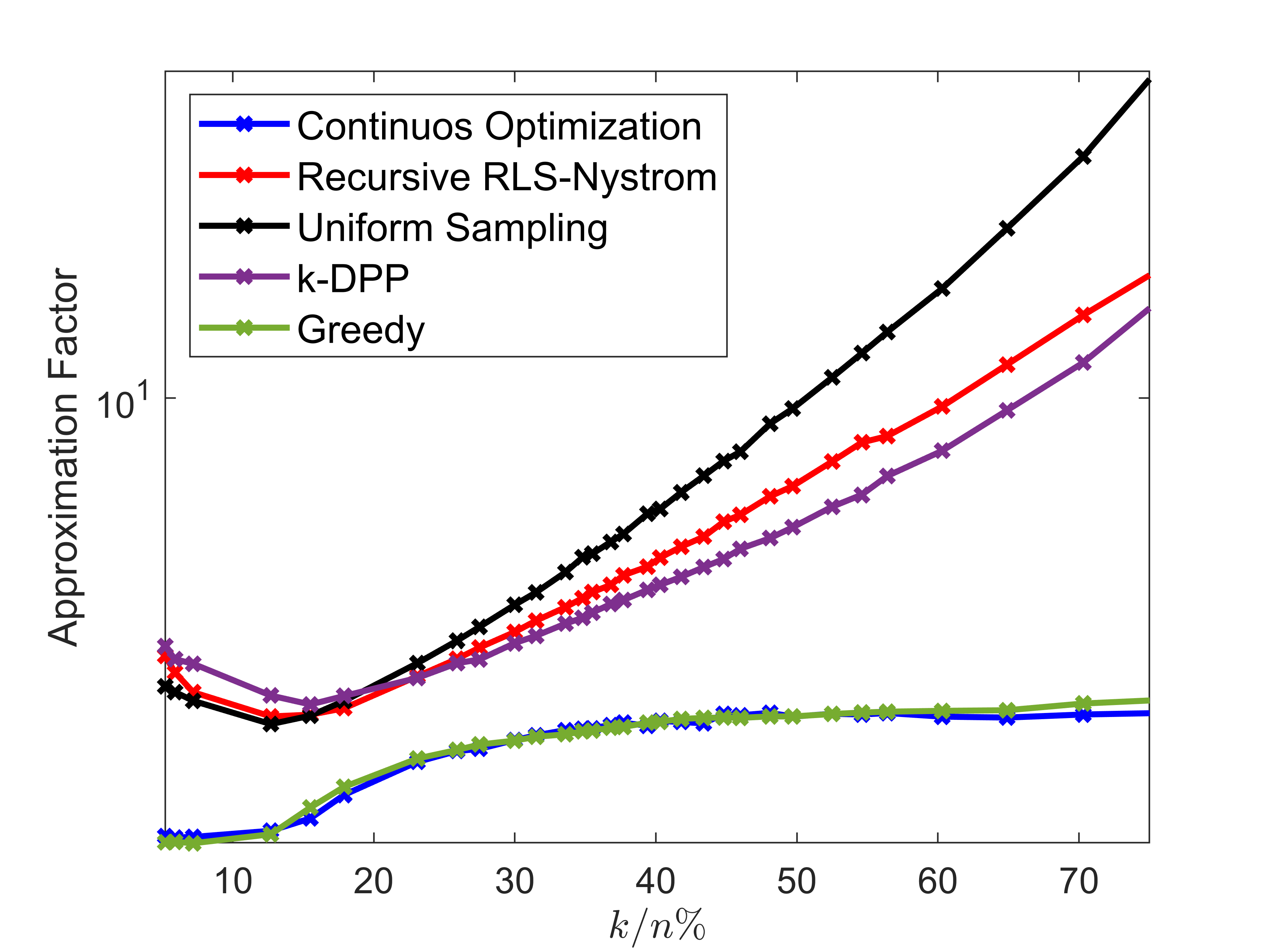

Numerical experiments were conducted on the small to medium-sized datasets: Residential and Building dataset (, ), MNIST1K (, )111https://yann.lecun.com/exdb/mnist/, Arrhythmia dataset (, ), SECOM (, ). Numerical experiments for Nyström landmark selection were also conducted on the larger datasets: Power Plant dataset (, ), HTRU2 dataset (, ) and Protein dataset (, ). All datasets except MNIST are downloaded from UCI ML Repository (Asuncion & Newman, 2007). All datasets were standardized such that all columns had mean zero and variance equal to one.

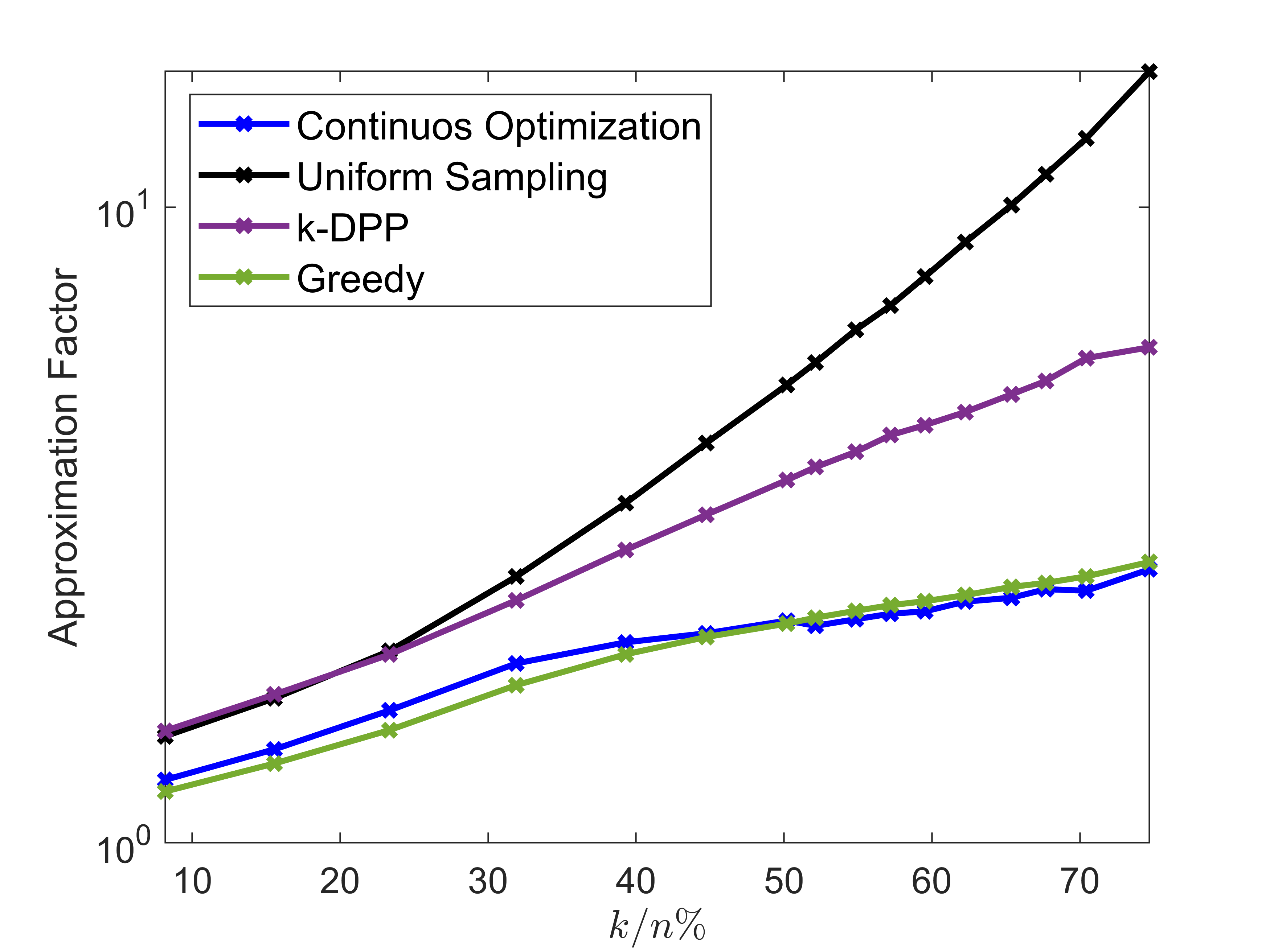

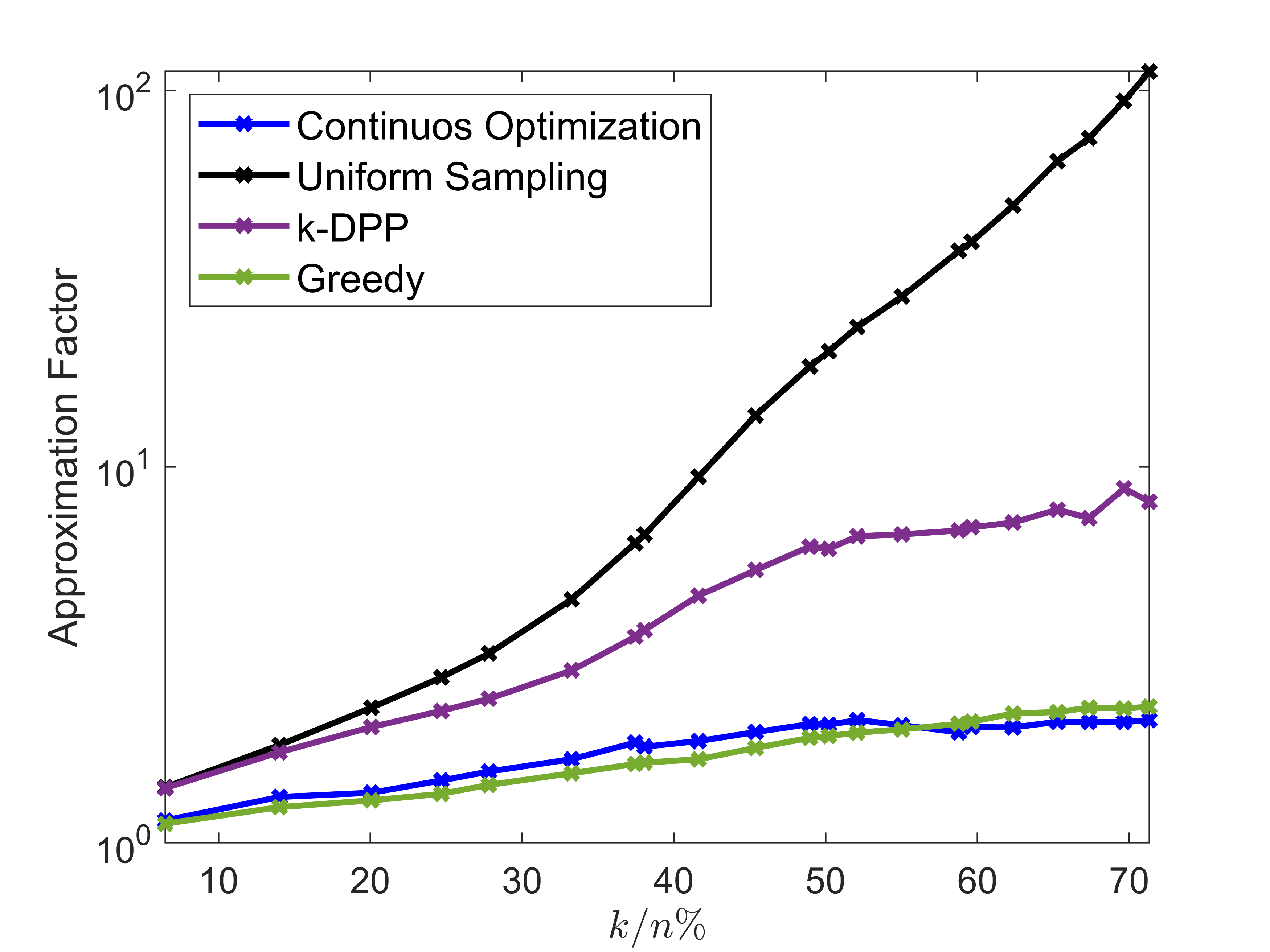

For the small to medium-sized datasets, we use the best rank-k approximation factor to compare our method to existing methods (see Figure 2 and Figure 3). The best rank-k approximation factor is given by

where is either the Nyström or CSSP low-rank matrix and is the best rank-k approximation computed using the Singular Value Decomposition (SVD) of .

In these experiments, we compare the proposed continuous landmark selection method executed with SGD () with the following four well-known methods: Uniform Sampling (Williams & Seeger, 2000), Recursive RLS (Ridge Leverage Scores) - Nyström sampling (Musco & Musco, 2017), k-DPP sampling (Derezinski & Mahoney, 2021) and Greedy selection (Farahat et al., 2011, 2013).

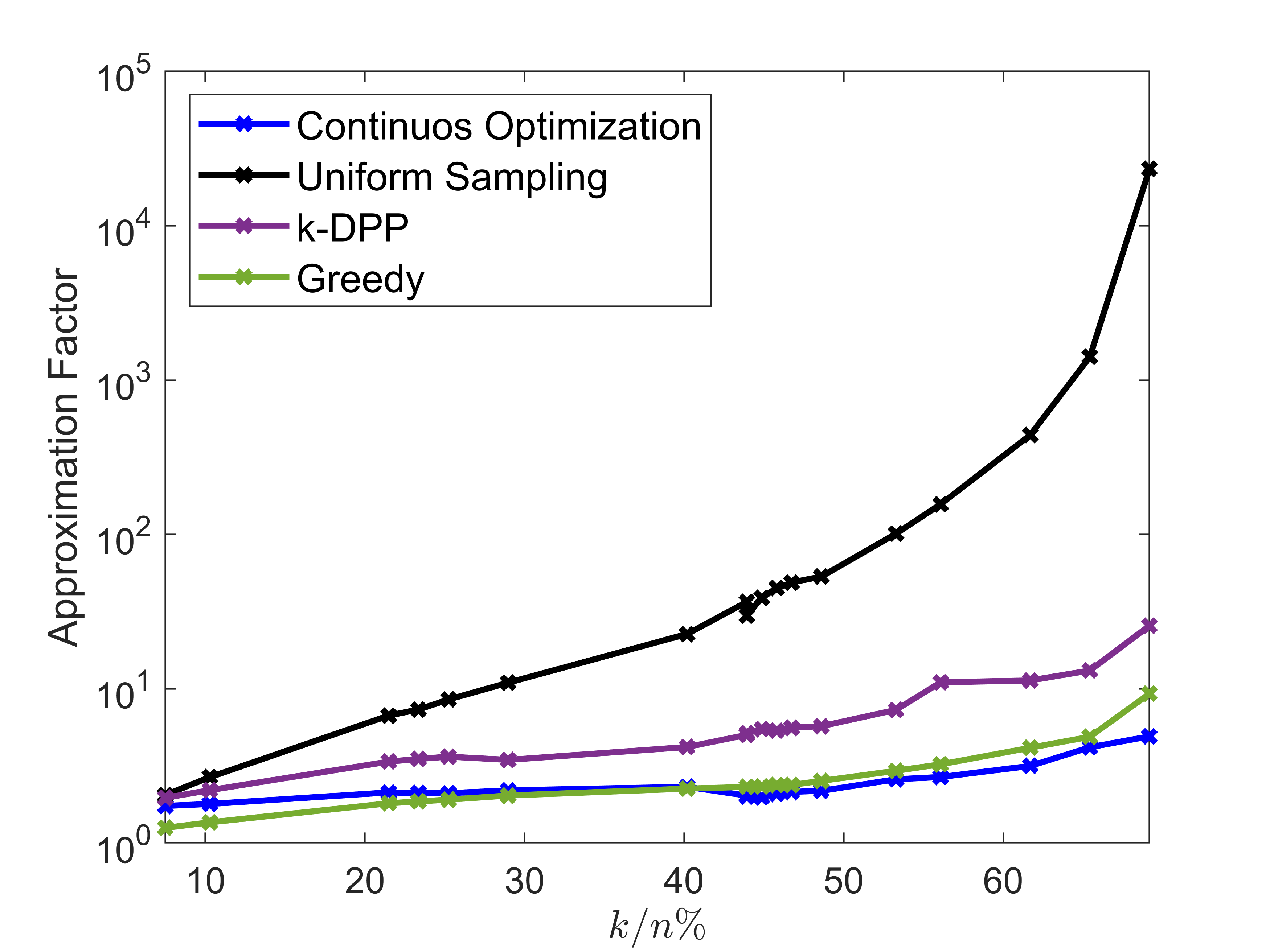

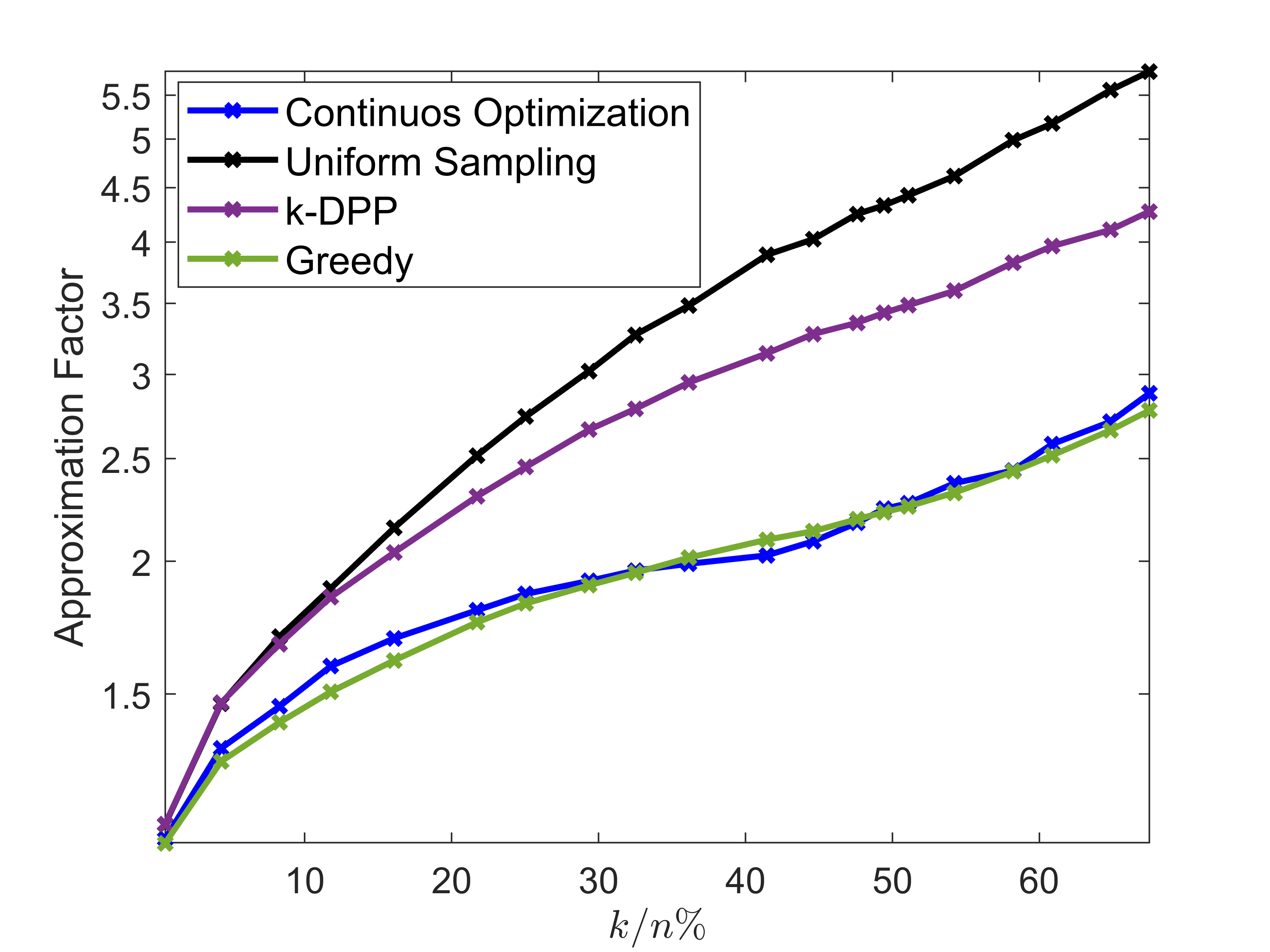

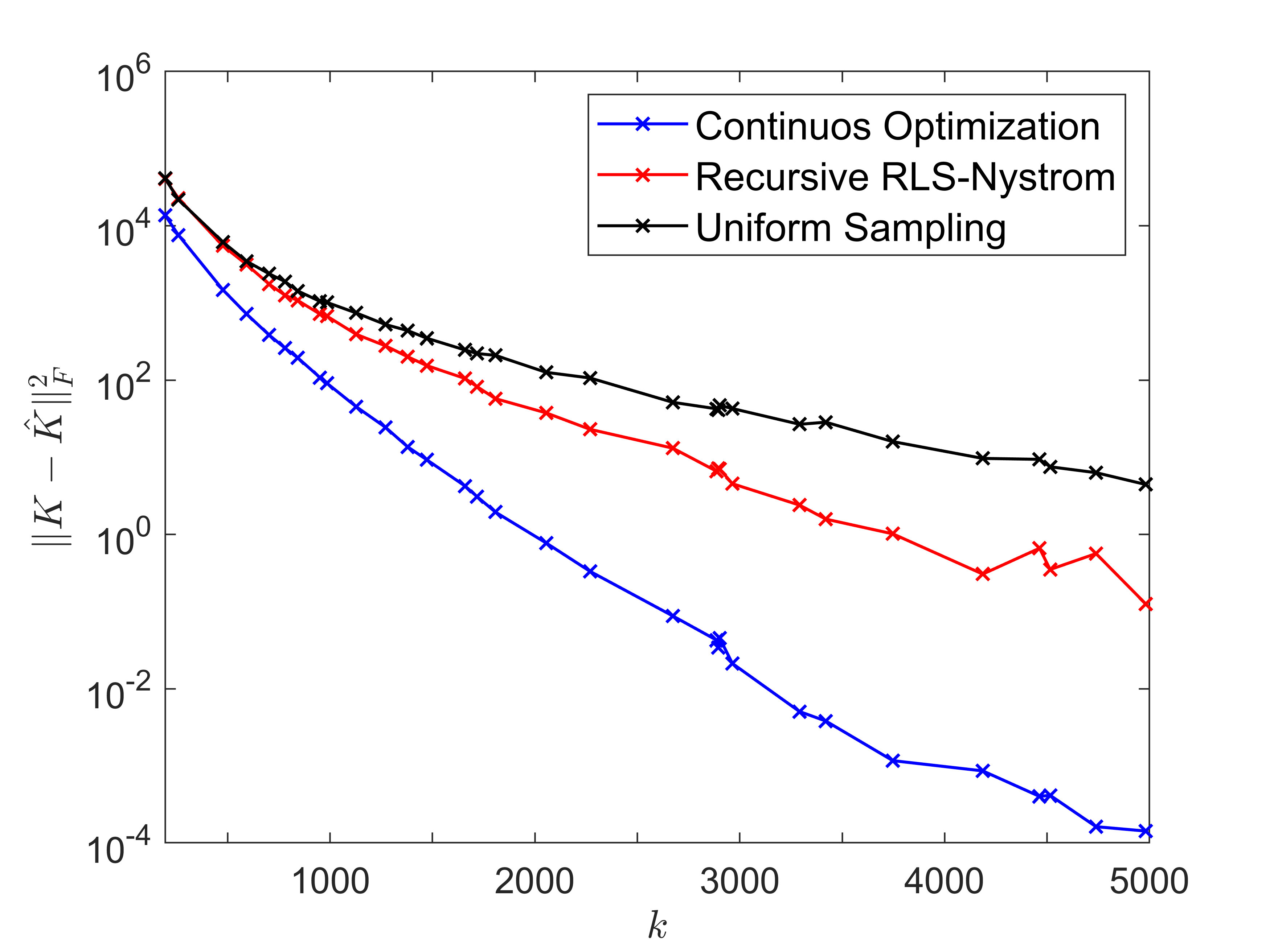

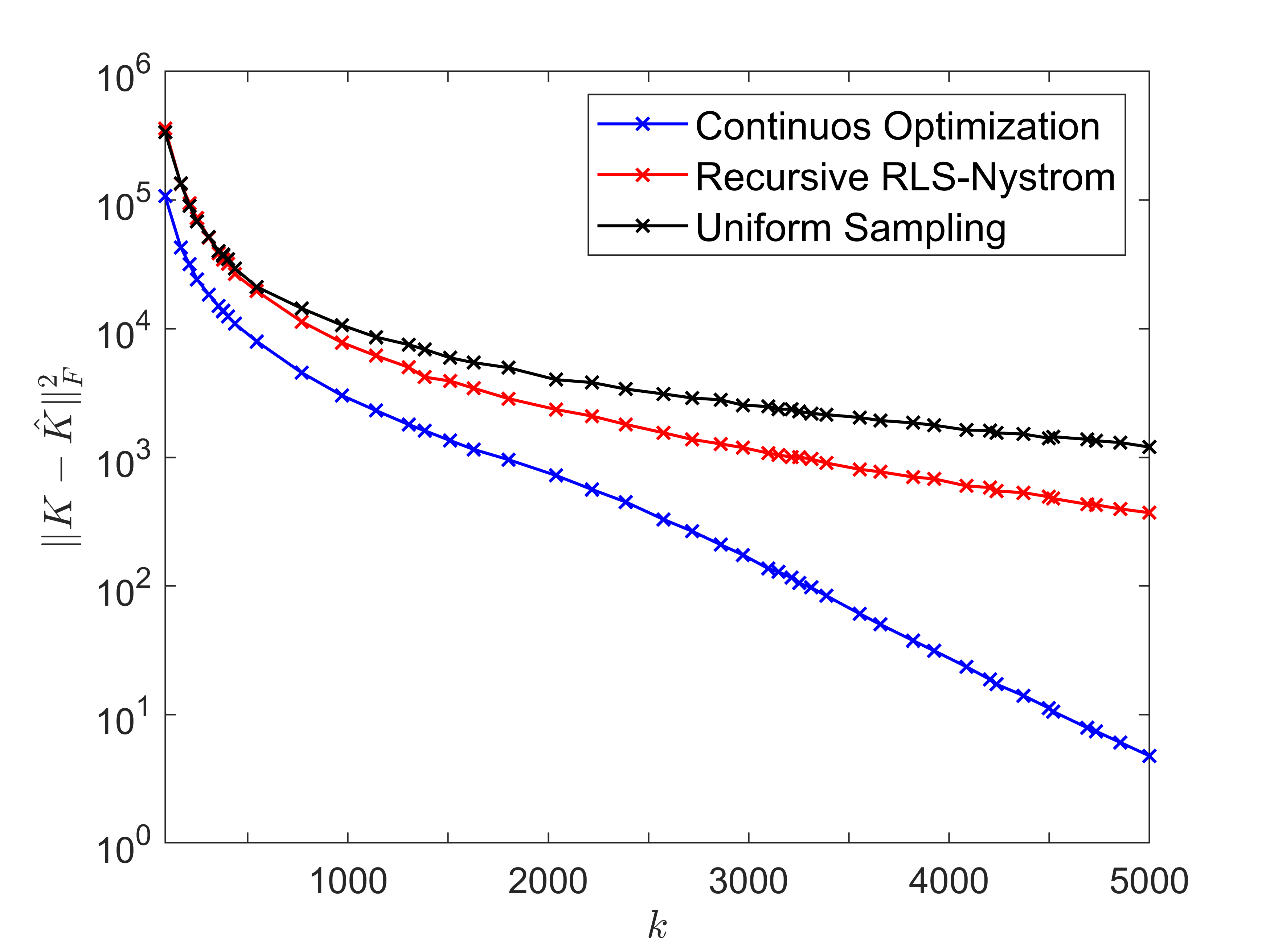

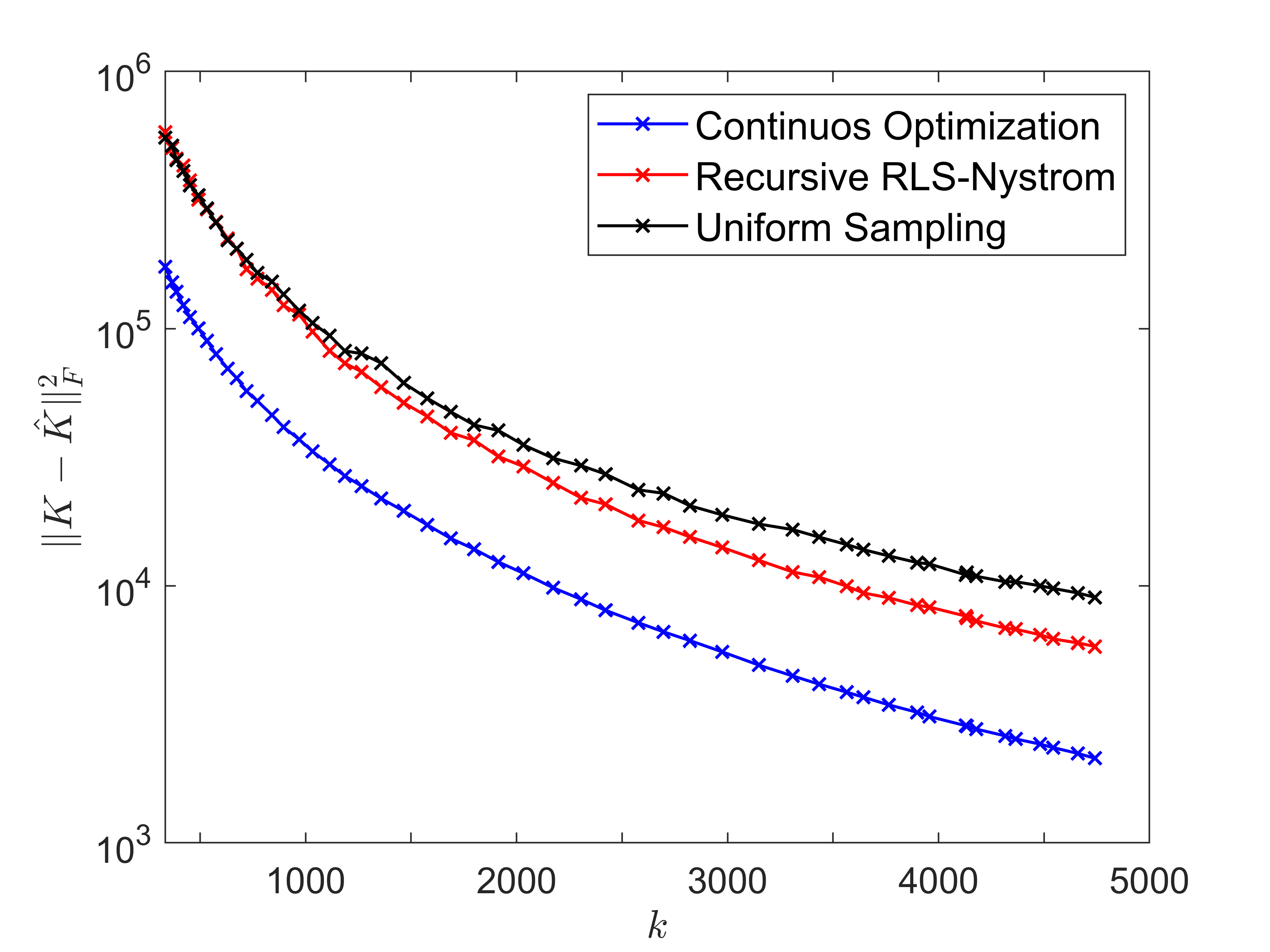

For the experiments conducted on the larger datasets (see Figure 4) we exclude the k-DPP sampling and greedy methods as it is either too costly to compute the choice of landmark points or too costly to store the full kernel matrix on a GPU. In our implementation of continuous Nyström landmark selection, we use the KeOps library (Charlier et al., 2021) to efficiently compute MVMs and linear solves on a GPU without ever storing the matrix , thus negating the need to store any objects. These experiments were run using an NVIDIA Tesla T4 GPU with 16GB memory.

In Figure 2 and Figure 3 we observe the approximation factor for Nyström and CSSP landmark selection with different subset sizes . A lower approximation factor indicates a better approximation and an approximation factor close to one implies near-best-case performance for the given subset size . The results indicate that the continuous optimization method is better than every tested sampling method and is very similar to greedy selection in performance (whenever the greedy selection is feasible). In most cases, for the CSSP, as the proportion of selected columns increases the continuous method starts to marginally outperform the greedy method.

In Figure 4, we observe for all three datasets (Power Plant, HTRU2 and Protein) that the continuous landmark selection achieves better accuracy than the Recursive RLS (Ridge Leverage Scores) - Nyström sampling and Uniform sampling methods. While Recursive RLS sampling (complexity: ) and uniform sampling are faster at selecting landmark points, for a fixed the continuous method obtains a more accurate Nyström approximation. Thus, if a memory budget for the size of the Nyström approximation is given, as is often the case, the continuous method will compute a superior approximation.

5 Conclusion

In this paper, we have introduced a novel algorithm that exploits unconstrained continuous optimization to select columns for both the CSSP and Nyström approximation. The algorithm selects columns by minimizing an extended objective which is defined over the hypercube rather than iterating over the corner points of the hypercube which correspond to all of the subsets. The extended objective for both the CSSP and Nyström approximation can be minimized via SGD where the gradients are estimated with an unbiased estimator which requires only MVMs with either (CSSP) or (Nyström). On the real-world examples that we considered in this article, the proposed method has proven to be more accurate without incurring higher computational cost.

References

- Alaoui & Mahoney (2015) Alaoui, A. and Mahoney, M. W. Fast randomized kernel ridge regression with statistical guarantees. Advances in neural information processing systems, 28, 2015.

- Altschuler et al. (2016) Altschuler, J., Bhaskara, A., Fu, G., Mirrokni, V., Rostamizadeh, A., and Zadimoghaddam, M. Greedy column subset selection: New bounds and distributed algorithms. In International conference on machine learning, pp. 2539–2548. PMLR, 2016.

- Asuncion & Newman (2007) Asuncion, A. and Newman, D. J. Uci machine learning repository, 2007, 2007.

- Beale et al. (1967) Beale, E., Kendall, M., and Mann, D. The discarding of variables in multivariate analysis. Biometrika, 54(3-4):357–366, 1967.

- Bekas et al. (2007) Bekas, C., Kokiopoulou, E., and Saad, Y. An estimator for the diagonal of a matrix. Applied numerical mathematics, 57(11-12):1214–1229, 2007.

- Bien et al. (2010) Bien, J., Xu, Y., and Mahoney, M. W. Cur from a sparse optimization viewpoint. Advances in Neural Information Processing Systems, 23, 2010.

- Calandriello et al. (2020) Calandriello, D., Derezinski, M., and Valko, M. Sampling from a k-dpp without looking at all items. Advances in Neural Information Processing Systems, 33:6889–6899, 2020.

- Charlier et al. (2021) Charlier, B., Feydy, J., Glaunes, J. A., Collin, F.-D., and Durif, G. Kernel operations on the gpu, with autodiff, without memory overflows. J. Mach. Learn. Res., 22(74):1–6, 2021.

- Dereziński (2019) Dereziński, M. Fast determinantal point processes via distortion-free intermediate sampling. In Conference on Learning Theory, pp. 1029–1049. PMLR, 2019.

- Derezinski & Mahoney (2021) Derezinski, M. and Mahoney, M. W. Determinantal point processes in randomized numerical linear algebra. Notices of the American Mathematical Society, 68(1):34–45, 2021.

- Derezinski et al. (2019) Derezinski, M., Calandriello, D., and Valko, M. Exact sampling of determinantal point processes with sublinear time preprocessing. Advances in neural information processing systems, 32, 2019.

- Derezinski et al. (2020) Derezinski, M., Khanna, R., and Mahoney, M. W. Improved guarantees and a multiple-descent curve for column subset selection and the nystrom method. Advances in Neural Information Processing Systems, 33:4953–4964, 2020.

- Deshpande & Vempala (2006) Deshpande, A. and Vempala, S. Adaptive sampling and fast low-rank matrix approximation. In Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques, pp. 292–303. Springer, 2006.

- Dietrich & Newsam (1997) Dietrich, C. R. and Newsam, G. N. Fast and exact simulation of stationary gaussian processes through circulant embedding of the covariance matrix. SIAM Journal on Scientific Computing, 18(4):1088–1107, 1997.

- Drineas et al. (2005) Drineas, P., Mahoney, M. W., and Cristianini, N. On the nyström method for approximating a gram matrix for improved kernel-based learning. journal of machine learning research, 6(12), 2005.

- Farahat et al. (2011) Farahat, A., Ghodsi, A., and Kamel, M. A novel greedy algorithm for nyström approximation. In Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, pp. 269–277. JMLR Workshop and Conference Proceedings, 2011.

- Farahat et al. (2013) Farahat, A. K., Ghodsi, A., and Kamel, M. S. Efficient greedy feature selection for unsupervised learning. Knowledge and information systems, 35(2):285–310, 2013.

- Gardner et al. (2018) Gardner, J., Pleiss, G., Wu, R., Weinberger, K., and Wilson, A. Product kernel interpolation for scalable gaussian processes. In International Conference on Artificial Intelligence and Statistics, pp. 1407–1416. PMLR, 2018.

- Gittens & Mahoney (2013) Gittens, A. and Mahoney, M. Revisiting the nystrom method for improved large-scale machine learning. In International Conference on Machine Learning, pp. 567–575. PMLR, 2013.

- Golub & Van Loan (1996) Golub, G. H. and Van Loan, C. F. Matrix computations, 1996.

- Hocking & Leslie (1967) Hocking, R. R. and Leslie, R. Selection of the best subset in regression analysis. Technometrics, 9(4):531–540, 1967.

- Hough et al. (2006) Hough, J. B., Krishnapur, M., Peres, Y., and Virág, B. Determinantal processes and independence. Probability surveys, 3:206–229, 2006.

- Hu et al. (2022) Hu, R., Sejdinovic, D., and Glaunès, J. A. Giga-scale kernel matrix vector multiplication on gpu. arXiv preprint arXiv:2202.01085, 2022.

- Li et al. (2016) Li, C., Jegelka, S., and Sra, S. Fast dpp sampling for nystrom with application to kernel methods. In International Conference on Machine Learning, pp. 2061–2070. PMLR, 2016.

- Martens et al. (2012) Martens, J., Sutskever, I., and Swersky, K. Estimating the hessian by back-propagating curvature. In Proceedings of the 29th International Coference on International Conference on Machine Learning, pp. 963–970, 2012.

- Mathur et al. (2021) Mathur, A., Moka, S., and Botev, Z. Variance reduction for matrix computations with applications to gaussian processes. In EAI International Conference on Performance Evaluation Methodologies and Tools, pp. 243–261. Springer, 2021.

- Moka et al. (2022) Moka, S., Liquet, B., Zhu, H., and Muller, S. Combss: Best subset selection via continuous optimization. arXiv preprint arXiv:2205.02617, 2022.

- Musco & Musco (2017) Musco, C. and Musco, C. Recursive sampling for the nystrom method. Advances in neural information processing systems, 30, 2017.

- Robbins & Monro (1951) Robbins, H. and Monro, S. A stochastic approximation method. The annals of mathematical statistics, pp. 400–407, 1951.

- Ryan et al. (2022) Ryan, J. P., Ament, S. E., Gomes, C. P., and Damle, A. The fast kernel transform. In International Conference on Artificial Intelligence and Statistics, pp. 11669–11690. PMLR, 2022.

- Shitov (2021) Shitov, Y. Column subset selection is np-complete. Linear Algebra and its Applications, 610:52–58, 2021.

- Tibshirani (1996) Tibshirani, R. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- Williams & Seeger (2000) Williams, C. and Seeger, M. Using the nyström method to speed up kernel machines. Advances in neural information processing systems, 13, 2000.

- Yuan & Lin (2006) Yuan, M. and Lin, Y. Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68(1):49–67, 2006.

Appendix A Proofs

Proof of Lemma 2.2. The following proof follows similar arguments to that of Theorem 1 in (Moka et al., 2022). Given that the pseudo-inverse of a matrix after a permutation of rows (respectively, columns) is identical to the matrix obtained by applying the same permutation on columns (respectively, rows) on the pseudo-inverse, we assume without loss of generality that all the zero-elements appear at the end, in the form,

where is equal to the number of non-zeros in . Then, is given by the block-wise matrix,

| (4) |

It is easy to verify, when the matrices and are square, the block-diagonal pseudo-inverse . Therefore (4) reduces to,

Proof of Lemma 2.2. To obtain the gradient for we first simplify the term by letting , and . Then, we have,

Using matrix calculus, for any , we have the partial derivative,

| (5) |

Let be the square matrix of dimension with 1 at position and 0 everywhere else. Then and we have,

| (6) |

Furthermore,

| (7) |

and using the derivative of an invertible matrix we have,

| (8) |

and,

| (9) |

Substituting we obtain the expression,

| (10) |

In order to simplify this expression we consider the following fact. If we have the matrices and then, . Using this, we obtain,

since the matrices , , and are all symmetric. Considering the partial derivative of the penalty term is we have the following expression for the gradient vector of ,

Proof of Lemma 2.6. For reasons outlined in the proof of Lemma 2.2 we assume without loss of generality that all the zero-elements in appear at the end, in the form,

where is equal to the number of non-zeros in . Then, is given by the block-wise matrix,

| (11) |

Using the block-diagonal pseudo-inverse formula we have,

Proof of Lemma 2.7. For any positive semi-definite kernel matrix , a decomposition of the form where always exists. Therefore, the function can be written as,

From Lemma 2.3 we know that the function is continuous over . Since is not a function of we conclude that is also continuous over .

Proof of Lemma 2.8. To obtain the gradient for we first simplify the term . Since and are symmetric, we have the expansion,

Therefore,

where . Factorize as and let and . Then, notice that the derivative is the same expression that we derived in the proof of Lemma 2.4, see (10). Substituting this expression in for , we obtain,

Once again, using the fact that for matrices and , we obtain,

| (12) | ||||

| (13) |

since the matrices , , and are all symmetric. Considering the partial derivative of the penalty term is we have the following expression for the gradient vector of ,

Proof of Lemma 3.1. From Lemma 2.4, we have,

where . To obtain an unbiased estimator for , we use the factorized estimator for the diagonal of a square matrix. Recall, to estimate the diagonal of the matrix where we let be a random vector sampled from the Rademacher distribution. Then the unbiased estimate for is (see (Martens et al., 2012; Mathur et al., 2021) for proof and analysis). We factorize the matrices in so that,

Then, the factorized estimator for is given by,

where and is a Rademacher random variable. If we compute the following variables: , we have,

and simplifies to,

Therefore, for we have,

Proof of Lemma 3.2. From Lemma 2.8 and Equation 12, we have,

To obtain an unbiased estimator for , we once again use the factorized estimator for the diagonal of a square matrix. We factorize the matrices in so that,

Then, the factorized estimator for is given by,

where and is a Rademacher random variable. Recall that and . Then, if we compute the following variables: , we have,

and simplifies to,

Hence, we have the expression for the gradient,

Proof of Lemma 2.3 For the same reasons outlined in the proof of Lemma 2.2 we assume without loss of generality that all the zero-elements in appear at the end, in the form,

Then is given by,

and since the matrix is invertible. Therefore,