Towards systematic intraday news screening: a liquidity-focused approach††thanks: This work benefits from the financial support of the Chaires Machine Learning & Systematic Methods. The author would like to thank Qinkai Chen and Quentin Jacob for very useful comments.

2 Exoduspoint Capital Management, 32 Boulevard Haussmann, 75009 Paris, France

)

Abstract

News can convey bearish or bullish views on financial assets. Institutional investors need to evaluate automatically the implied news sentiment based on textual data. Given the huge amount of news articles published each day, most of which are neutral, we present a systematic news screening method to identify the “true” impactful ones, aiming for more effective development of news sentiment learning methods. Based on several liquidity-driven variables, including volatility, turnover, bid-ask spread, and book size, we associate each 5-min time bin to one of two specific liquidity modes. One represents the “calm” state at which the market stays for most of the time and the other, featured with relatively higher levels of volatility and trading volume, describes the regime driven by some exogenous events. Then we focus on the moments where the liquidity mode switches from the former to the latter and consider the news articles published nearby impactful. We apply naive Bayes on these filtered samples for news sentiment classification as an illustrative example. We show that the screened dataset leads to more effective feature capturing and thus superior performance on short-term asset return prediction compared to the original dataset.

Keywords— News screening, intraday liquidity, mode fitting, sentiment learning, jump model, exogenous events.

1 Introduction

The price of a financial asset is driven by endogenous activities, such as self-reflexive trades, and also exogenous information. A main

component of the latter comes from news releases. Nowadays, the financial market is becoming increasingly efficient, yet the embodiment of new information

transferred by news in asset price is rarely accomplished instantaneously. Quick and effective estimation of news sentiment,

i.e. whether the view given by a news article is bullish or bearish, can give profitable opportunities to investors. As said in Pedersen (\APACyear2019),

“financial markets are efficiently inefficient”, in the idea that professional investors with superior performance are compensated for their costs

and risks, and the competition among them makes markets almost efficient.

Given the large number of news publications every day, manual analysis of each piece of news is infeasible. To assess efficiently the impact of a news release on the market price of its associated financial asset, institutional investors then need to develop automatic news sentiment evaluation methods.

Numerous works using news data to predict financial assets’ price movements exist in the literature. In Chan (\APACyear2003), it is documented that the monthly returns of the stocks

associated with public news releases are less likely to reverse than those without identifiable news publication, suggesting that news can publish some information concerning the “fair” value of stocks. Jiang \BOthers. (\APACyear2021)

extend the study with intraday returns in the same spirit. A long/short trading strategy exploiting the news-driven price drifts is shown to generate abnormal profit.

In these works, the views transferred by certain news releases on the stocks of interest, whether bullish or bearish, are identified by the associated post-news market reactions. Thus to make an investment decision, investors have to wait until the emergence of some significant price drifts after news publications. To react more quickly, sentiment evaluation methods based on textual data are required. Tetlock (\APACyear2007) applies the Harvard-IV psychosocial dictionary on the articles from The Wall Street Journal to estimate the pessimistic pressure

on the Dow Jones Industrial Average index. Loughran \BBA McDonald (\APACyear2011) construct a customized dictionary more adapted to financial text using the term frequency-inverse document frequency (tf-idf) method. Stock market sentiment lexicons based on microblogging data are developed in Oliveira \BOthers. (\APACyear2016) and Renault (\APACyear2017) by computing several statistical measures. Ke \BOthers. (\APACyear2019) estimate the tone weights of sentiment-charged words via a topic modeling method, and compute the article-level

sentiment score using a regularized version of maximum likelihood estimation.

Another strand of research is using deep learning methods on news data in the same vein as current practices in natural language processing. Ding \BOthers. (\APACyear2014) transform news publications

into structural events using Open Information Extraction techniques. A novel neural tensor network is used in Ding \BOthers. (\APACyear2015)

to represent news text as dense vectors. Then the representations are put into a convolutional neural network for predicting future stock price movements. The dependence

among sequential news releases is considered in Hu \BOthers. (\APACyear2018) by proposing an attention-based recurrent neural network. Chen (\APACyear2021) develops a fine-tuned bidirectional encoder representations

from transformers, see Kenton \BBA Toutanova (\APACyear2019), to produce contextualized word embeddings, which are then fed into a recurrent neural network to output news classification results.

To develop a news sentiment learner, one needs firstly labeled samples, i.e. bullish or bearish news releases, for model training. However, the sentimental nature of a news article is not explicitly marked in real life.

In the case of Bloomberg News111https://www.bloomberg.com/professional/product/event-driven-feeds/, the first step of model development consists of manual labeling by human experts, in the idea to

isolate “true” sentiment contained in news from realized price actions. However, this method can be exposed to subjective biases. More importantly, one has to repeat the manual labeling when moving to a new training set, which can be costly. More efficient systematic news labeling methods are preferred in this case.

A common practice in the research community is to take the sign of the share price movement following a news publication as the ground truth label (Chen, \APACyear2021; Ding \BOthers., \APACyear2014, \APACyear2015; Hu \BOthers., \APACyear2018). This is understandable since news sentiments are expected to predict positively the price drifts of associated assets. However, not every news article conveys a directional view of the underlying asset price. Labeling news only based on post-publication returns would result in a non-negligible proportion of falsely labeled samples in the training set, which causes extra uncertainties for model learning. Chen (\APACyear2021) keeps only a small portion of samples with extreme market realized returns for model training to reduce the impact of neutral news. Still, we believe that relying solely on the posterior return is incomplete, given the low signal-to-noise ratio of return data.

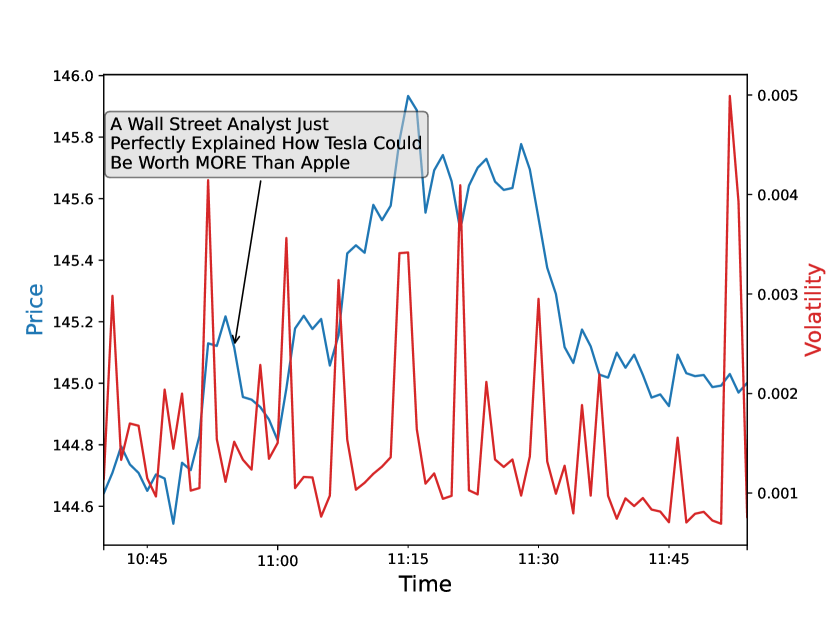

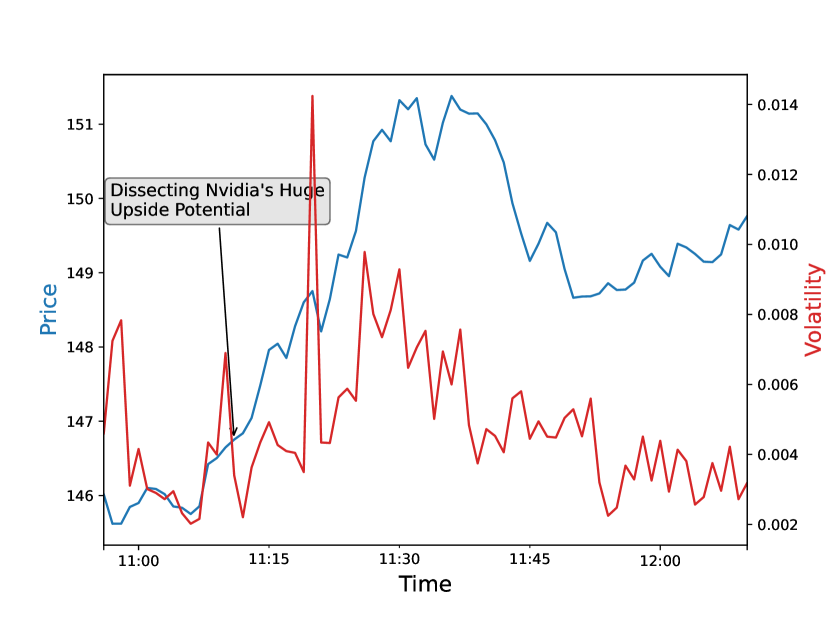

In this paper, we aim at identifying the “true” impactful news releases, i.e. those imply positive or negative views on the associated assets, with a particular focus on the liquidity states of the assets of interest. Figure 1.1 illustrates our main motivation by examining stocks’ price and volatility dynamics around

news publications with two particular examples. Both news releases would be considered positive if we look at only the short-term realized return. Yet the first one is more

likely to be a piece of neutral news for Apple, which is consistent with the mediocre volatility fluctuation. As for the case of Nvidia, we observe a more significant volatility change when the message

conveys a positive view on the company’s potential. Note that here we apply the model with uncertainty zones introduced by Robert \BBA Rosenbaum (\APACyear2011, \APACyear2012) for effective computation of

high-frequency volatility. Thus, we can conceive a two-step news screening approach. First, we divide the daily core trading session into multiple nonoverlapping time bins of equal size, and for each bin, we estimate the realized price volatility. These estimations can be sorted out using clustering methods into two clusters representing two distinct liquidity modes. We designate the one with a lower volatility level as Mode 1 and the other as Mode 2. Second, we focus on the jumps from Mode 1 to Mode 2, and consider the news articles published around these jumps impactful. That is, these jumps are thought to have caused these volatility changes.

The above method is consistent with the findings in Groß-Klußmann \BBA Hautsch (\APACyear2011). Based on news data concerning 40 stocks actively traded at the London Stock Exchange, preprocessed by the Reuters NewsScope Sentiment Engine, Groß-Klußmann \BBA Hautsch (\APACyear2011) suggests that the news with high relevance impact significantly volatilities and trading volumes.

To get a more robust liquidity mode fitting, the actual indicator set chosen in this work includes four common liquidity-driven variables, i.e. volatility, turnover, bid-ask spread, and book size (Bińkowski \BBA Lehalle, \APACyear2022). Instead of using classical clustering methods like K-means to distinguish two liquidity modes, we apply the jump model introduced in Bemporad \BOthers. (\APACyear2018) to take also the ordering of observations into account. In the jump model, we can easily penalize frequent mode switches, and thus some mode persistence is favored. This is relevant for time series describing intraday liquidity conditions.

Joulin \BOthers. (\APACyear2008); Marcaccioli \BOthers. (\APACyear2022) investigate the volatility fluctuations around the price jumps induced by news releases, suggesting that they exhibit different dynamical patterns to those arising from endogenous activities. One can thus monitor the volatility dynamics around each news publication, and then decide whether the release has impacted the market according to the observed features. However, we have to consider the following inconveniences when applying this method in practice. First, news screening one by one is very time-consuming given the large size of the news dataset. Second, when some other liquidity-driven variables in addition to volatility are considered, as in the case of our current work, the dynamical features of these variables differentiating between the exogenous and endogenous events need to be specified explicitly, and then news classification rules should be modified accordingly.

Our approach is very efficient by structuring the task into two steps: liquidity mode fitting on a time-bin basis and associating news releases with detected liquidity mode jumps. The fitting results can also be used for news data from other providers or any other exogenous events/signals in a similar manner. The jump model fits data in a nonparametric way, allowing us to be agnostic about the dynamical properties of each measured variable. Other variables can be easily tested in the same manner.

Note that only the news releases that happened during the daily core trading sessions are concerned by our screening approach.

Once the impactful releases are targeted, we mark them as positive or negative by the signs of the post-news returns of the associated assets, similarly to Chen (\APACyear2021); Ding \BOthers. (\APACyear2014, \APACyear2015); Hu \BOthers. (\APACyear2018).

Then various supervised learning methods can be applied to the labeled samples to learn sentiment-charged features. In this work, we focus on the effect of our news screening method instead of developments of alternative sentiment learning methods. To illustrate the idea, we fit two Bernoulli naive Bayes classifiers (NBCs) respectively on the original intraday news data and the dataset filtered by liquidity mode changes. Based on out-of-sample tests, the classification results given by the later classifier are more consistent with the post-news asset price movements than the former, i.e. in average the news articles with high probability to be positive (negative) assigned by the latter classifier show more significant and persistent positive (negative) post-news price drift than the ones sorted out by the former classifier. This indicates that the screened dataset includes fewer falsely labeled samples, and thus can lead to more effective sentiment learning.

The paper is organized as follows. In Section 2, we describe firstly the data involved in this study and related preprocessing procedures. The application of the jump model on liquidity mode fitting is detailed in Section 3. Numerical results with market data are presented. We then present how to use the fitted mode sequences to identify impactful news releases in Section 4. The relevance of our method for more effective news sentiment learning is then illustrated through numerical experiments. Finally, we conclude with our main findings in Section 5.

2 Data and preprocessing

In this work, we use the Daily Trade and Quote (TAQ) dataset222https://www.nyse.com/market-data/historical/daily-taq for computing the considered liquidity-driven variables. The TAQ dataset covers all stocks traded in the US market. To avoid any results biased by small-cap names, we focus on the components of S&P 500. The following variables are measured on consecutive bins of five minutes during the daily core trading session:

-

•

Average bid-ask spread in ticks . For each second, we record the last observed bid-ask spread. The average value for each 5-minute bin is computed and its ratio against the tick size is kept.

-

•

Traded value/turnover , is the total value traded during each 5-minute bin.

-

•

Volatility . Instead of using the Garman-Klass volatility as in Bińkowski \BBA Lehalle (\APACyear2022), here we take the one based on the model with uncertainty zones, whose effectiveness on high-frequency data is shown in (Robert \BBA Rosenbaum, \APACyear2011, \APACyear2012).

-

•

Average book size . We record the average volume available at the best bid and ask prices of each second inside each 5-minute bin.

After removing the data concerning the first and last 15 minutes of the daily core trading period333We recall that the regular trading hours for the US stock market are 9:30 a.m. to 4:00 p.m., for each (stock, day) pair, we get a time series of length . Intraday seasonalities of liquidity variables, induced by certain fundamental reasons, are well known (Bińkowski \BBA Lehalle, \APACyear2022; Lehalle \BBA Laruelle, \APACyear2018), and our objective is to identify the short-term impacts of news beyond these effects. For each observation of stock on day with , we use the following stationarization procedure:

where means the difference between the 75th and 25th percentiles of the data, and represents the total available days on the dataset under study.

We use IQR instead of the ordinary standard deviation to reduce the impact of outliers. In this paper, data covering 2017-01-01 2019-12-31 is selected for examining

the association between intraday liquidities and news data, i.e. . After this preprocessing, the intraday seasonalities can be mostly removed

and all the variables of all stocks have similar scales, which is essential for the fitting of intraday liquidity states, as will be detailed in the following.

Table 2.1 gives several samples of the Bloomberg News data that we used in this work. Note that we evaluate the news sentiment only based on the headlines.

The Score and Confidence fields give sentiment estimation of the news articles, which are based on Bloomberg’s proprietary classification algorithm.

The Score says whether a piece of news is bullish(1), bearish(-1), or neutral(0), with the Confidence indicating the reliability of this classification. We can thus compute an

composed score score confidence.

Naturally, we expect on average the news releases with the highest composed score are followed with significantly positive price drift and the opposite for the ones with the lowest composed score. The predictive power of this score will be compared with the sentiment score given by the NBCs, as will be shown later.

| Headline | TimeStamp | Ticker | Score | Confidence |

|---|---|---|---|---|

| 1st Source Corp: 06/20/2015 - 1st Source announces the promotion of Kim Richardson in St. Joseph | 2015-06-20T05:02:04.063 | SRCE | -1 | 39 |

| Siasat Daily: Microsoft continues rebranding of Nokia Priority stores in India opens one in Chennai | 2015-06-20T05:14:01.096 | MSFT | 1 | 98 |

| Rosneft, Eurochem to cooperate on monetization at east urengoy | 2015-06-20T08:01:53.625 | ROSN RM | 0 | 98 |

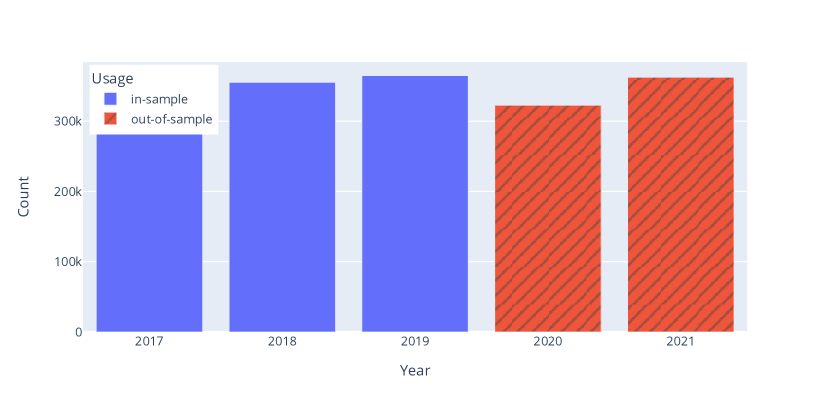

Figure 2.1 shows the number of news releases related to our work. We screen the news headlines published during the years 2017 2019 based on the liquidity-driven variables as introduced above. Thus only the ones released during the daily trading hours is concerned for this step. We then fit a news classifier to output sentiment scores capturing the sentiment-charged features based on the samples picked out. The classifier is evaluated on all the intraday news headlines published during 2020-01-01 2021-12-31, with a particular focus on the predictive power of the sentiment scores on the short-term post-publication price drifts.

3 Liquidity mode fitting

3.1 Jump model

Given a sequence of data pairs with and the number of modes , the jump model introduced in Bemporad \BOthers. (\APACyear2018) outputs a mode sequence with , and the parameter associated with each , with some positive constant. The obtained and minimize the following objective function

where , , , , and are all functions taking value on . The first two parts to the right of the equal sign represent respectively the total fitting loss of the given data and a regularization term on the model parameters. For example, when , and with , we get the standard setting for Ridge regression. The particularity of the jump model relies on the introduction of the loss taking the ordering of the mode sequence into account. It is defined as

where the loss is decomposed into three parts, the penalization on the initialization , the one linked to the fitting result of each timestamp , and the cost concerning mode transitions . As suggested in Bemporad \BOthers. (\APACyear2018), this definition generalizes popular models such as hidden Markov models. Various cost functions

can be chosen to meet the needs of different applications. We refer to Bemporad \BOthers. (\APACyear2018) for more details.

In our case, we apply the jump model in an unsupervised learning manner. For each stock-day pair with and , we have a preprocessed sequence where . The model consists in finding a mode sequence , under which the observations associated with the same mode are more similar to each other than to those linked with other modes. We denote the mode represents by . We have no prior knowledge about the initial mode , and impose no mode-specific cost, that is, . We penalize frequent mode switches, expecting some degree of persistence for the fitted mode sequence. Particularly, it leads to the same type of loss function as in Nystrup \BOthers. (\APACyear2021), which reads

| (3.1) |

where , with representing the norm, and is a hyperparameter trading off between clustering the given data and mode persistence.

In practice, it can be chosen via cross-validation. Note that when , we will get the classical K-means solution. As for the number of modes, larger can

brings better fit, while it becomes less evident to interpret and involves a higher risk of overfitting. Since we focus on the market liquidity regime

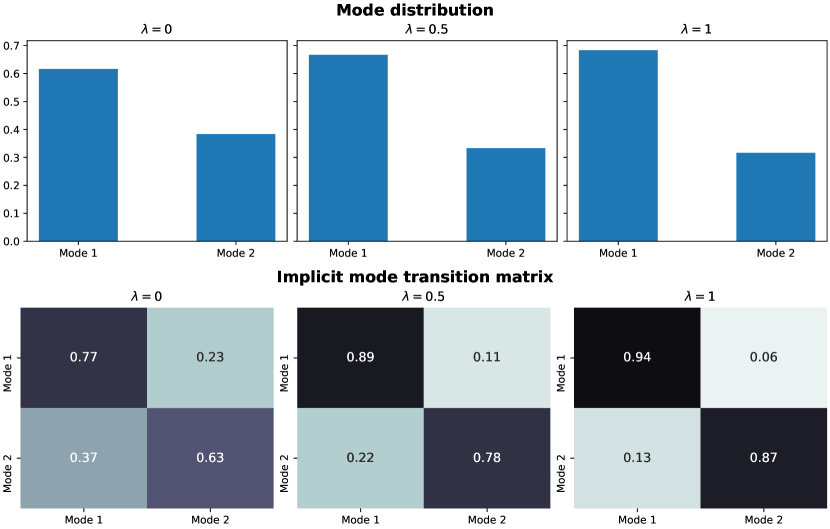

switch caused by exogenous information, we simply take in the following tests. We will see in the following that the resulting two modes are separated in terms of volatility level. We let the mode associated with lower volatility be Mode 1, and the other be Mode 2.

Therefore, the results of minimization of (3.1) are a sequence of liquidity modes associated with each time bin and two vectors of dimension four. Note that the latter are obtained based on observations, which still implies some potential risk of overfitting. To reduce this risk, we can expand the fitting on sequences of multiple days. However, as the liquidity-driven variables are not homogeneous across time, e.g. certain periods are more volatile than the others, the fitted modes will not distribute uniformly over time. For example, we expect that Mode 2 will concentrate on periods associated with relatively larger volatility. Thus in this case, the observed mode switches are mostly the results of some market-wide events such as monetary policy announcements, instead of stock-specific news releases. In this work, we expand the fitting space in the dimension of the asset. More precisely, on day the model is fitted on the pooled set of sequences . As market-wide activities impact all the stocks to a similar extent, and are unlikely to change abruptly at the intraday scale, the observations are influenced uniformly by these market-wide events across and . In this way, the fitting results can reflect the short-term liquidity fluctuations from the base level related to the market environment. Significant liquidity changes are thought to be induced by some exogenous events, i.e. news releases in our case. We ignore the superscript for ease of notation in the following. The actual fitting objective reads thus

| (3.2) |

where and . Problem (3.2) can be solved with a simple coordinate-descent optimization algorithm that alternates minimization with respect to and , which is detailed in Appendix A.

3.2 Fitting results

In this part, we give several statistics on the intraday liquidity mode fitting results for the period 2017-01-01 2019-12-31. We recall that in this study and we test several different to see its effect. Given the set of all fitted mode sequences , we count respectively the occurrences of Mode 1 and Mode 2. We also estimate a implicit transition matrix , whose entries are computed as follows:

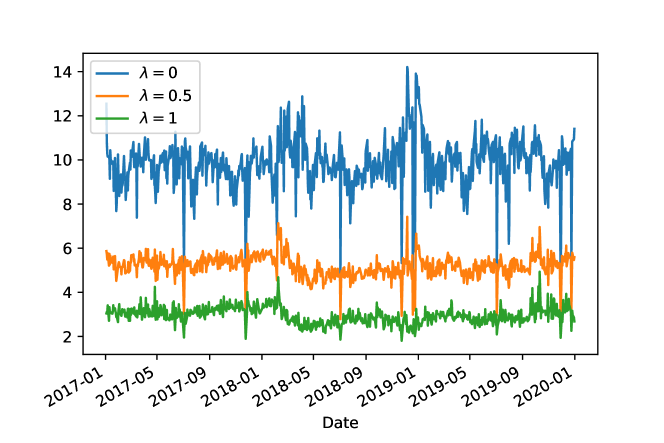

Figure 3.1 gives the results with respect to different . Most of the time the market stays at Mode 1. With larger , we get a slightly smaller assignment ratio for Mode 2 and more pronounced mode persistence. Note that even when we do not penalize the mode switch, i.e. , the diagonal elements of are significantly larger than the off-diagonal ones. This is consistent with the observations in Bińkowski \BBA Lehalle (\APACyear2022) that all the selected liquidity-driven variables are positively autocorrelated, and thus the points of adjacent time bins are likely to be classified into the same mode. Accordingly, Figure 3.2 gives the average daily count of liquidity mode switches from Mode 1 to Mode 2 per stock.

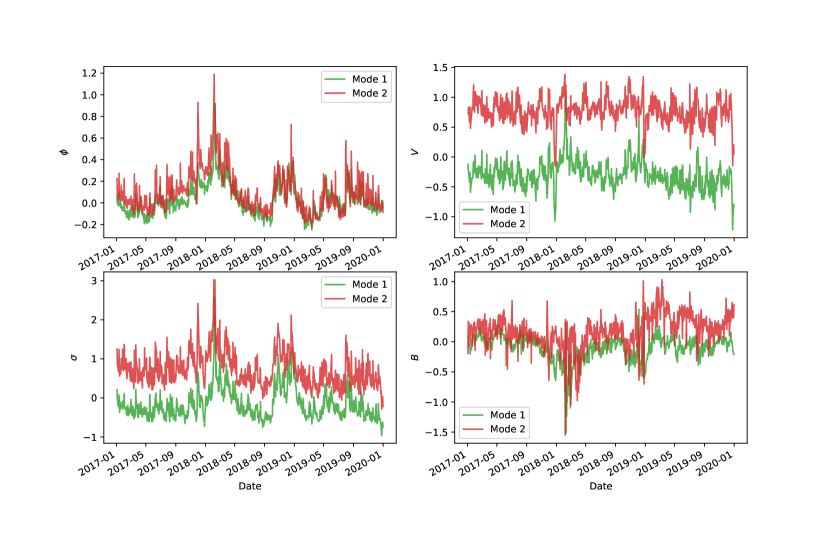

Figure 3.3 plots the dynamics of fitted mode parameters during our testing period when . As expected in Introduction, the volatility levels of the two modes are well distinct. Interestingly, it is also the case for the traded volume . The differentiation of and between the two modes are relatively less noticeable. It is unlikely that the detected Mode 2 corresponds mostly to the time slots with endogenous volatility spikes, which are usually accompanied by increased bid-ask spread as suggested, for example, in Wyart \BOthers. (\APACyear2008). Of course considering the multivariate nature in (3.2), the resulting pattern depends on the set of variables that we chose at the beginning. Developing other features and selecting the most effective ones in the context of impactful news screening is out of the scope of the current work.

4 News screening and learning

4.1 Methodology

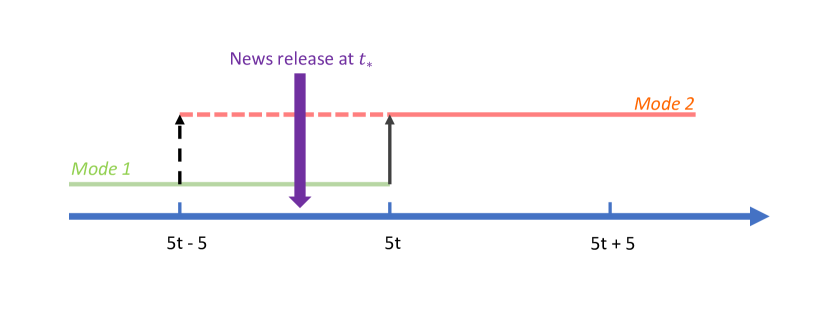

It is often suggested in the literature that exogenously driven orders can generate a larger volatility footprint than endogenously mechanical ones, see for example Huang \BOthers. (\APACyear2015); Rambaldi \BOthers. (\APACyear2019). As Mode 2 is characterized by higher volatility and increased trading volume, it is reasonable to assume that some exogenous events, news releases in this paper, evoked the mode switches. Considering a piece of news arriving inside the -th 5-minute bin as shown in Figure 4.1, with , we consider it impactful if one of the following scenarios happens:

| (4.1) |

Let the set of original intraday news releases and the impactful ones selected with the above criterion be and respectively, where is the mode switch penalization parameter defined in (3.2). Given a piece of news , released at and concerning the stock , we denote the -minute return of the stock after the publication of by , i.e. , where represents the price of stock at time . Since we are interested in the firm-specific price movements disentangled from market-wide activities, we replace with its market-detrended version defined by

where for sake of simplicity, we follow the classical capital asset pricing model with the betas fixed to be one. With , let and be the -th and -th percentile of respectively. We define the following sets

Thus, and are respectively sets of bearish and bullish news releases according to the amplitude of post-publication stock returns, which is the criterion commonly used in works such as Chen (\APACyear2021); Ding \BOthers. (\APACyear2014, \APACyear2015); Hu \BOthers. (\APACyear2018). The cases with are in the spirit that “true” impactful news releases are more likely to be followed with significant price movements. Given and , the sets of “true” bearish and bullish news in our approach are defined respectively by

Therefore, in addition to extreme post-publication return, the news publications selected by our method is also followed by noticeable changes in market liquidity conditions.

Given a set of labeled samples, such as or , we firstly inquire the dependence of news sentiment, positive or negative, on the presence or absence of each individual word through measuring the mutual information between these two random variables. Then we fit a multi-variate Bernoulli NBC as a news sentiment predictor. Some key computational rules are recalled in Appendix B. We refer to for instance Cover \BOthers. (\APACyear1991) and McCallum \BOthers. (\APACyear1998) for more details of these methods. For a piece of news , the classifier tells us the probabilities of being positive and negative. Since there is no ground truth for the news sentiment, we evaluate the classification results based on stocks’ post-news price movements, under the hypothesis that news sentiment is positively correlated with the direction of stocks’ future return. More precisely, for an NBC fitted on the training set , we define the sentiment score of news by

where and are the probabilities of being bullish and bearish respectively given by the model. We expect naturally that a significantly high (low) F is more likely to be followed by a positive (negative) price drift for the associated stock.

4.2 Numerical results

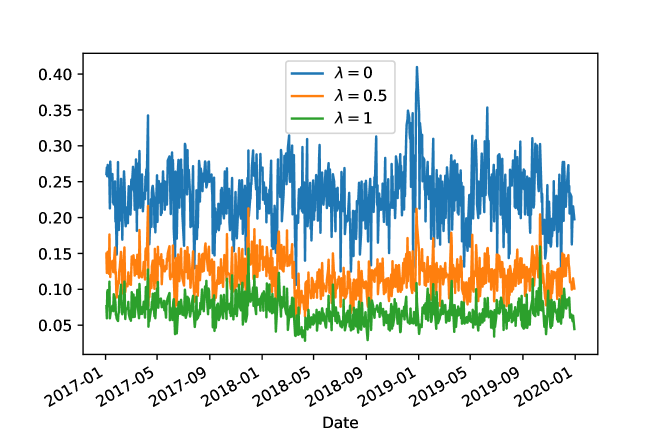

In this part, we perform news sentiment learning on the screened news dataset. Figure 4.2 gives the resulting ratio of news releases selected with the criterion (4.1). Note that with , only around of total intraday releases are thought to have impacted the market in our approach.

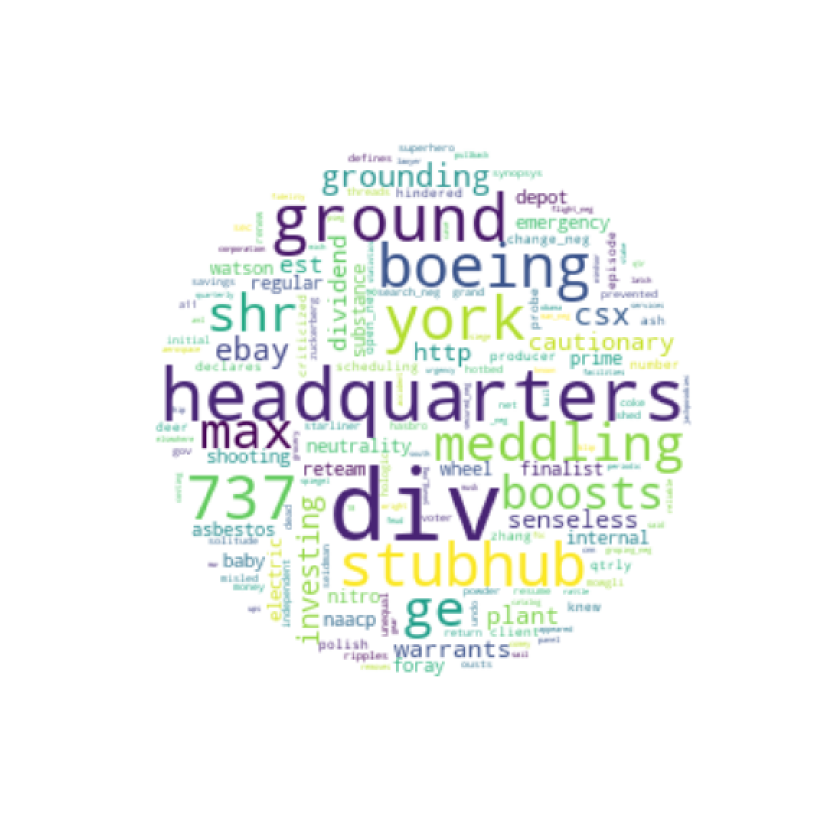

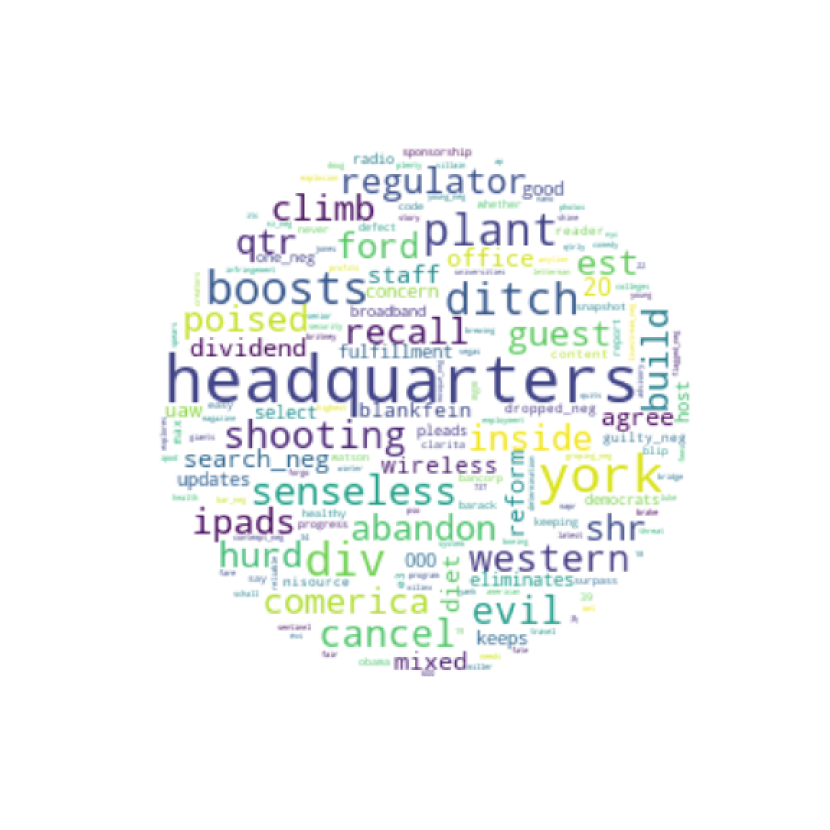

4.2.1 Most informative words

Figure 4.3 shows the words reporting the most mutual information with news sentiment, measured respectively on and . Visually, our news selection method boosted with liquidity-driven variables can reduce the weights of certain sentiment-neutral words, e.g. “boeing”, “737”, “stubhub”, “http”, etc. It also highlights some sentiment-charged words, e.g. “senseless”, “abandon”, “recall”, “poised”, “evil”, etc. Considering the limitation of uni-gram evaluation, it is not surprising that several neutral words still seem to be overvalued with our approach. For example, “headquarters” solely is not sentiment-charged, while “build new headquarters” is likely to drive some stock price movements.

4.2.2 Short-term return prediction

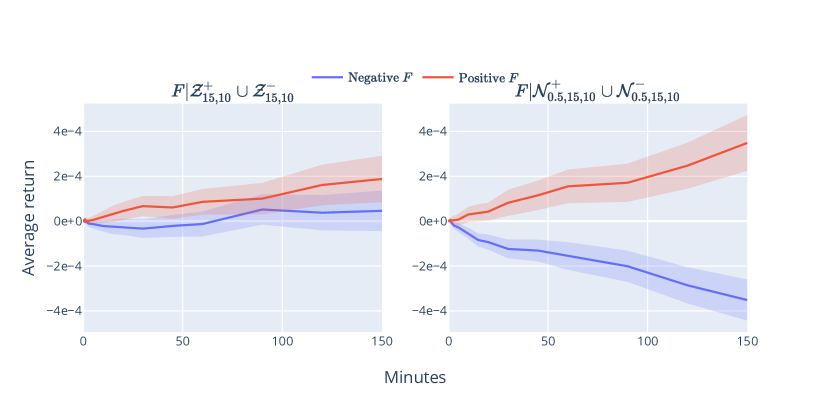

Now we evaluate the predictive power of the news sentiment scores, given by the fitted NBCs, for future price movement. Note that the following results are based on the news headlines published during the out-of-sample period, i.e. 2020-01-01 2021-12-31. We are more interested in the short-term returns following news publications since they reflect better the immediate impacts of news sentiment compared to price changes over longer horizons. We fit two NBCs on the training sets and respectively. They are then applied to the out-of-sample news data to output sentiment estimations. We plot the average post-publication price drifts of the news releases associated with distinct sentiment scores up to 150 minutes in Figure 4.4.

Clearly, after screening the news dataset with our approach, NBC can better predict the short-term stock return. The pieces of news with significantly positive sentiment scores are followed by climbing prices, while the ones with negative scores drive the inverse phenomenon.

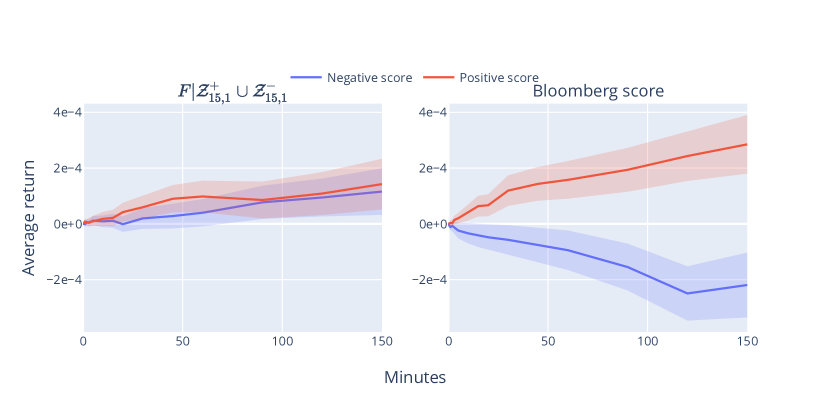

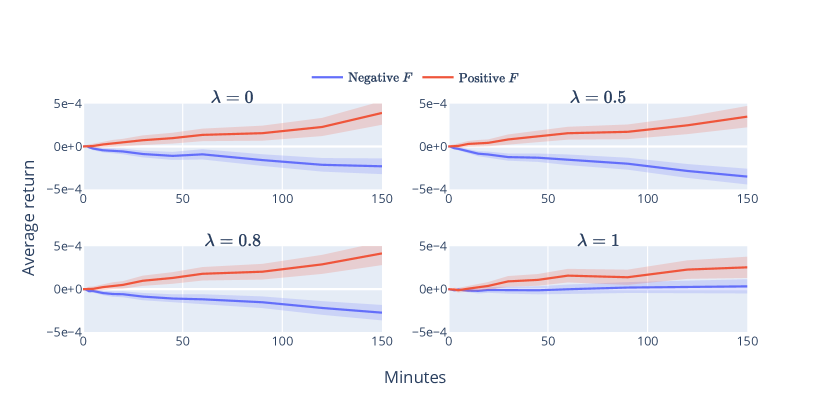

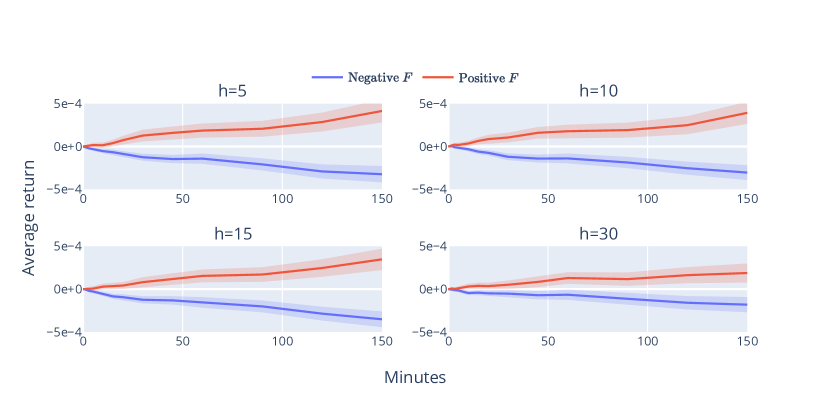

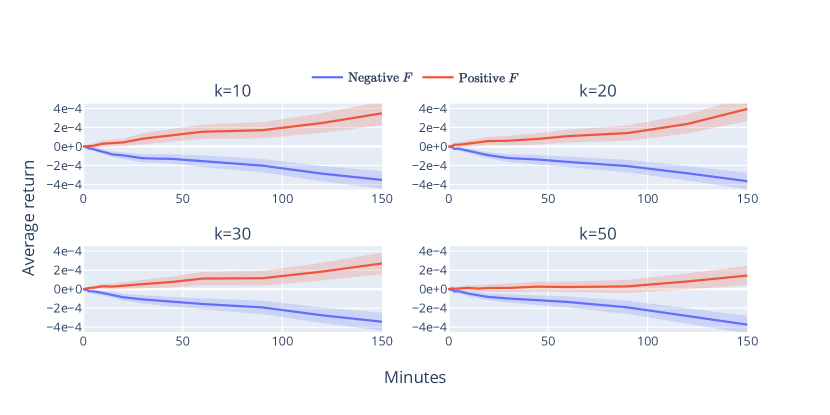

With , the size of is only about one tenth of . To verify that our selection method is not equivalent to filtering news releases by the associated post-publicaiton stock returns, we repeat the same test on . As shown in the left subfigure of Figure 4.5, with similar number of training samples to the case with , the prediction performance now is largely degraded. Keeping only the news releases with extreme post-publication stock returns can reduce the ratio of neutral samples in the training set to some extent, while it can also result in model underfitting because of data shortage. Our method presents a more efficient way to filter neutral news samples and identify the impactful ones, which helps the model learn more effectively. In Figure 4.5, we show also the results of Bloomberg composed score as defined in Section 2. Interestingly, despite its simplicity, the NBC fitted on the screened dataset performs even slightly better than the scores given by Bloomberg in terms of short-term return prediction. Moreover, we show in Appendix C that the performance of our approach is not very sensitive to the value of , and .

5 Conclusion

In this work, we introduce a systematic method for identifying “true” impactful news releases that are conceived to contain unexpected information for the financial market.

The identification method consists in associating significant changes in liquidity conditions during market open hours with nearby news publications. Four variables are used to monitor the intraday dynamics of liquidity mode, including volatility, turnover, bid-ask spread, and book size. Through numerical tests on S&P500 components, the two predetermined liquidity states are distinct from each other in terms of volatility and turnover level. We pick out the news releases with identifiable mode switch from that with lower volatility and less trading volume to the other one, and label them by the sign of post-news realized returns of the associated stocks. Experiments on news sentiment learning with NBC show that the proposed news screening method leads to more effective feature capturing and thus better model predictive performance.

The study can be extended in several directions. First, our news screening approach can be taken as a preprocessing procedure, and can be applied together with various news sentiment learning methods. Second, we focus on the Bloomberg News data in this study, while the same tests can be easily conducted on any other news dataset, or more generally on other types of exogenous events/signals. Last, it would be interesting to build some agent-based models to understand further the link between exogenous inputs and resulting dynamics of volatility/turnover.

Appendix A Jump model fitting

For each day, we run the following algorithm:

-

1.

Generate initial mode sequences through applying K-means on the pooled set of observation sequences. Initial loss .

-

2.

Iterate for until :

-

(a)

Model parameter fit: for , the optimal is given by the mean of all the samples assigned with mode , i.e.

.

-

(b)

For each , solve the optimal mode sequence with respect to :

-

i.

Compute a matrix , which is defined by:

where .

-

ii.

Reconstruct the optimal mode sequence with

-

i.

-

(c)

Update the loss by .

-

(a)

At each iteration the loss is non-increasing, so Algorithm 1 can always terminate in a finite number of steps. However, similar to other classical clustering methods such as K-means or Gaussian mixture methods, the final solution depends on the initialization and may not be the global optimal one. In practice, one can run the above algorithm multiple times with different initial model sequences and keep the one with the smallest loss.

Appendix B Mutual information and naive Bayes classifier

Mutual information

Let and be two random variables denoting respectively the category of a news release, i.e. positive or negative in this paper, and the presence or absence of word in the news text. represents the absence of the word, and represents the presence of . The mutual information between and is given by

where and are the marginal probability mass functions of and respectively, and is their joint probability mass function. In this work, for a given labeled set of news headlines, or , we estimate the above probability quantities by their classical empirical observations over all samples.

Multi-variate Bernoulli naive Bayes classifier

Let be the news class variable, indicate the presence or absence of word in the news headlines, we are interested in the classification result given by

Following Bayes’ theorem, we have

The “naive” conditional independence assumption, we have

where can be easily estimated given the Bernoulli assumption.

Appendix C Robusteness tests

Our approach involves mainly three parameters, i.e. , and . In the following we show their effects by varying their values.

- Effect of

As shown in Figure C.1, the results are relatively robust with intermediate . When , the amount of news samples taken as impactful becomes too limited to accurate model learning.

- Effect of

Figure C.2 gives the results when choosing the post-news realized return over different horizons for news sign labeling. We do not remark significant variation of performance for . Slight degradation is observed for , which is understandable given the increased volatility of realized return.

- Effect of

When using only realized return information for news labeling, we are inclined to relatively small to pick out only the news releases associated with significant post-publication price drifts. With our method, as shown in Figure C.3, the impact of on the final results is very limited. Even with , which means that the magnitude of realized return is not considered, there is no significant deterioration for the predictive performance of the resulting model.

References

- Bemporad \BOthers. (\APACyear2018) \APACinsertmetastarbemporad2018fitting{APACrefauthors}Bemporad, A., Breschi, V., Piga, D.\BCBL \BBA Boyd, S\BPBIP. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleFitting jump models Fitting jump models.\BBCQ \APACjournalVolNumPagesAutomatica9611–21. \PrintBackRefs\CurrentBib

- Bińkowski \BBA Lehalle (\APACyear2022) \APACinsertmetastarbinkowski2022endogenous{APACrefauthors}Bińkowski, M.\BCBT \BBA Lehalle, C\BHBIA. \APACrefYearMonthDay2022. \BBOQ\APACrefatitleEndogenous Dynamics of Intraday Liquidity Endogenous dynamics of intraday liquidity.\BBCQ \APACjournalVolNumPagesThe Journal of Portfolio Management486145–169. \PrintBackRefs\CurrentBib

- Chan (\APACyear2003) \APACinsertmetastarchan2003stock{APACrefauthors}Chan, W\BPBIS. \APACrefYearMonthDay2003. \BBOQ\APACrefatitleStock price reaction to news and no-news: drift and reversal after headlines Stock price reaction to news and no-news: drift and reversal after headlines.\BBCQ \APACjournalVolNumPagesJournal of Financial Economics702223–260. \PrintBackRefs\CurrentBib

- Chen (\APACyear2021) \APACinsertmetastarchen2021stock{APACrefauthors}Chen, Q. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleStock movement prediction with financial news using contextualized embedding from bert Stock movement prediction with financial news using contextualized embedding from bert.\BBCQ \APACjournalVolNumPagesarXiv preprint arXiv:2107.08721. \PrintBackRefs\CurrentBib

- Cover \BOthers. (\APACyear1991) \APACinsertmetastarcover1991entropy{APACrefauthors}Cover, T\BPBIM., Thomas, J\BPBIA.\BCBL \BOthersPeriod. \APACrefYearMonthDay1991. \BBOQ\APACrefatitleEntropy, relative entropy and mutual information Entropy, relative entropy and mutual information.\BBCQ \APACjournalVolNumPagesElements of information theory2112–13. \PrintBackRefs\CurrentBib

- Ding \BOthers. (\APACyear2014) \APACinsertmetastarding2014using{APACrefauthors}Ding, X., Zhang, Y., Liu, T.\BCBL \BBA Duan, J. \APACrefYearMonthDay2014. \BBOQ\APACrefatitleUsing structured events to predict stock price movement: An empirical investigation Using structured events to predict stock price movement: An empirical investigation.\BBCQ \BIn \APACrefbtitleProceedings of the 2014 conference on empirical methods in natural language processing (EMNLP) Proceedings of the 2014 conference on empirical methods in natural language processing (emnlp) (\BPGS 1415–1425). \PrintBackRefs\CurrentBib

- Ding \BOthers. (\APACyear2015) \APACinsertmetastarding2015deep{APACrefauthors}Ding, X., Zhang, Y., Liu, T.\BCBL \BBA Duan, J. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleDeep learning for event-driven stock prediction Deep learning for event-driven stock prediction.\BBCQ \BIn \APACrefbtitleTwenty-fourth international joint conference on artificial intelligence. Twenty-fourth international joint conference on artificial intelligence. \PrintBackRefs\CurrentBib

- Groß-Klußmann \BBA Hautsch (\APACyear2011) \APACinsertmetastargross2011machines{APACrefauthors}Groß-Klußmann, A.\BCBT \BBA Hautsch, N. \APACrefYearMonthDay2011. \BBOQ\APACrefatitleWhen machines read the news: Using automated text analytics to quantify high frequency news-implied market reactions When machines read the news: Using automated text analytics to quantify high frequency news-implied market reactions.\BBCQ \APACjournalVolNumPagesJournal of Empirical Finance182321–340. \PrintBackRefs\CurrentBib

- Hu \BOthers. (\APACyear2018) \APACinsertmetastarhu2018listening{APACrefauthors}Hu, Z., Liu, W., Bian, J., Liu, X.\BCBL \BBA Liu, T\BHBIY. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleListening to chaotic whispers: A deep learning framework for news-oriented stock trend prediction Listening to chaotic whispers: A deep learning framework for news-oriented stock trend prediction.\BBCQ \BIn \APACrefbtitleProceedings of the eleventh ACM international conference on web search and data mining Proceedings of the eleventh acm international conference on web search and data mining (\BPGS 261–269). \PrintBackRefs\CurrentBib

- Huang \BOthers. (\APACyear2015) \APACinsertmetastarhuang2015simulating{APACrefauthors}Huang, W., Lehalle, C\BHBIA.\BCBL \BBA Rosenbaum, M. \APACrefYearMonthDay2015. \BBOQ\APACrefatitleSimulating and analyzing order book data: The queue-reactive model Simulating and analyzing order book data: The queue-reactive model.\BBCQ \APACjournalVolNumPagesJournal of the American Statistical Association110509107–122. \PrintBackRefs\CurrentBib

- Jiang \BOthers. (\APACyear2021) \APACinsertmetastarjiang2021pervasive{APACrefauthors}Jiang, H., Li, S\BPBIZ.\BCBL \BBA Wang, H. \APACrefYearMonthDay2021. \BBOQ\APACrefatitlePervasive underreaction: Evidence from high-frequency data Pervasive underreaction: Evidence from high-frequency data.\BBCQ \APACjournalVolNumPagesJournal of Financial Economics1412573–599. \PrintBackRefs\CurrentBib

- Joulin \BOthers. (\APACyear2008) \APACinsertmetastarjoulin2008stock{APACrefauthors}Joulin, A., Lefevre, A., Grunberg, D.\BCBL \BBA Bouchaud, J\BHBIP. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleStock price jumps: news and volume play a minor role Stock price jumps: news and volume play a minor role.\BBCQ \APACjournalVolNumPagesWilmott Magazine46. \PrintBackRefs\CurrentBib

- Ke \BOthers. (\APACyear2019) \APACinsertmetastarke2019predicting{APACrefauthors}Ke, Z\BPBIT., Kelly, B\BPBIT.\BCBL \BBA Xiu, D. \APACrefYearMonthDay2019. \APACrefbtitlePredicting returns with text data Predicting returns with text data \APACbVolEdTR\BTR. \APACaddressInstitutionNational Bureau of Economic Research. \PrintBackRefs\CurrentBib

- Kenton \BBA Toutanova (\APACyear2019) \APACinsertmetastarkenton2019bert{APACrefauthors}Kenton, J\BPBID\BPBIM\BHBIW\BPBIC.\BCBT \BBA Toutanova, L\BPBIK. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleBert: Pre-training of deep bidirectional transformers for language understanding Bert: Pre-training of deep bidirectional transformers for language understanding.\BBCQ \BIn \APACrefbtitleProceedings of naacL-HLT Proceedings of naacl-hlt (\BPGS 4171–4186). \PrintBackRefs\CurrentBib

- Lehalle \BBA Laruelle (\APACyear2018) \APACinsertmetastarlehalle2018market{APACrefauthors}Lehalle, C\BHBIA.\BCBT \BBA Laruelle, S. \APACrefYear2018. \APACrefbtitleMarket microstructure in practice Market microstructure in practice. \APACaddressPublisherWorld Scientific. \PrintBackRefs\CurrentBib

- Loughran \BBA McDonald (\APACyear2011) \APACinsertmetastarloughran2011liability{APACrefauthors}Loughran, T.\BCBT \BBA McDonald, B. \APACrefYearMonthDay2011. \BBOQ\APACrefatitleWhen is a liability not a liability? Textual analysis, dictionaries, and 10-Ks When is a liability not a liability? textual analysis, dictionaries, and 10-ks.\BBCQ \APACjournalVolNumPagesThe Journal of finance66135–65. \PrintBackRefs\CurrentBib

- Marcaccioli \BOthers. (\APACyear2022) \APACinsertmetastarmarcaccioli2022exogenous{APACrefauthors}Marcaccioli, R., Bouchaud, J\BHBIP.\BCBL \BBA Benzaquen, M. \APACrefYearMonthDay2022. \BBOQ\APACrefatitleExogenous and endogenous price jumps belong to different dynamical classes Exogenous and endogenous price jumps belong to different dynamical classes.\BBCQ \APACjournalVolNumPagesJournal of Statistical Mechanics: Theory and Experiment20222023403. \PrintBackRefs\CurrentBib

- McCallum \BOthers. (\APACyear1998) \APACinsertmetastarmccallum1998comparison{APACrefauthors}McCallum, A., Nigam, K.\BCBL \BOthersPeriod. \APACrefYearMonthDay1998. \BBOQ\APACrefatitleA comparison of event models for naive bayes text classification A comparison of event models for naive bayes text classification.\BBCQ \BIn \APACrefbtitleAAAI-98 workshop on learning for text categorization Aaai-98 workshop on learning for text categorization (\BVOL 752, \BPGS 41–48). \PrintBackRefs\CurrentBib

- Nystrup \BOthers. (\APACyear2021) \APACinsertmetastarnystrup2021feature{APACrefauthors}Nystrup, P., Kolm, P\BPBIN.\BCBL \BBA Lindström, E. \APACrefYearMonthDay2021. \BBOQ\APACrefatitleFeature selection in jump models Feature selection in jump models.\BBCQ \APACjournalVolNumPagesExpert Systems with Applications184115558. \PrintBackRefs\CurrentBib

- Oliveira \BOthers. (\APACyear2016) \APACinsertmetastaroliveira2016stock{APACrefauthors}Oliveira, N., Cortez, P.\BCBL \BBA Areal, N. \APACrefYearMonthDay2016. \BBOQ\APACrefatitleStock market sentiment lexicon acquisition using microblogging data and statistical measures Stock market sentiment lexicon acquisition using microblogging data and statistical measures.\BBCQ \APACjournalVolNumPagesDecision Support Systems8562–73. \PrintBackRefs\CurrentBib

- Pedersen (\APACyear2019) \APACinsertmetastarpedersen2019efficiently{APACrefauthors}Pedersen, L\BPBIH. \APACrefYear2019. \APACrefbtitleEfficiently inefficient: how smart money invests and market prices are determined Efficiently inefficient: how smart money invests and market prices are determined. \APACaddressPublisherPrinceton University Press. \PrintBackRefs\CurrentBib

- Rambaldi \BOthers. (\APACyear2019) \APACinsertmetastarrambaldi2019disentangling{APACrefauthors}Rambaldi, M., Bacry, E.\BCBL \BBA Muzy, J\BHBIF. \APACrefYearMonthDay2019. \BBOQ\APACrefatitleDisentangling and quantifying market participant volatility contributions Disentangling and quantifying market participant volatility contributions.\BBCQ \APACjournalVolNumPagesQuantitative Finance19101613–1625. \PrintBackRefs\CurrentBib

- Renault (\APACyear2017) \APACinsertmetastarrenault2017intraday{APACrefauthors}Renault, T. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleIntraday online investor sentiment and return patterns in the US stock market Intraday online investor sentiment and return patterns in the us stock market.\BBCQ \APACjournalVolNumPagesJournal of Banking & Finance8425–40. \PrintBackRefs\CurrentBib

- Robert \BBA Rosenbaum (\APACyear2011) \APACinsertmetastarrobert2011new{APACrefauthors}Robert, C\BPBIY.\BCBT \BBA Rosenbaum, M. \APACrefYearMonthDay2011. \BBOQ\APACrefatitleA new approach for the dynamics of ultra-high-frequency data: The model with uncertainty zones A new approach for the dynamics of ultra-high-frequency data: The model with uncertainty zones.\BBCQ \APACjournalVolNumPagesJournal of Financial Econometrics92344–366. \PrintBackRefs\CurrentBib

- Robert \BBA Rosenbaum (\APACyear2012) \APACinsertmetastarrobert2012volatility{APACrefauthors}Robert, C\BPBIY.\BCBT \BBA Rosenbaum, M. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleVolatility and covariation estimation when microstructure noise and trading times are endogenous Volatility and covariation estimation when microstructure noise and trading times are endogenous.\BBCQ \APACjournalVolNumPagesMathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics221133–164. \PrintBackRefs\CurrentBib

- Tetlock (\APACyear2007) \APACinsertmetastartetlock2007giving{APACrefauthors}Tetlock, P\BPBIC. \APACrefYearMonthDay2007. \BBOQ\APACrefatitleGiving content to investor sentiment: The role of media in the stock market Giving content to investor sentiment: The role of media in the stock market.\BBCQ \APACjournalVolNumPagesThe Journal of finance6231139–1168. \PrintBackRefs\CurrentBib

- Wyart \BOthers. (\APACyear2008) \APACinsertmetastarwyart2008relation{APACrefauthors}Wyart, M., Bouchaud, J\BHBIP., Kockelkoren, J., Potters, M.\BCBL \BBA Vettorazzo, M. \APACrefYearMonthDay2008. \BBOQ\APACrefatitleRelation between bid–ask spread, impact and volatility in order-driven markets Relation between bid–ask spread, impact and volatility in order-driven markets.\BBCQ \APACjournalVolNumPagesQuantitative finance8141–57. \PrintBackRefs\CurrentBib