The Elasticity of Quantitative Investment††thanks: I thank Michael Weber, Joachim Freyberger, and Andreas Neuhierl for providing excellent data. I thank Lubos Pastor, Stefan Nagel, Ralph Koijen, and Niels Gormsen, Doug Diamond, Lars Hansen, John Heaton, Anthony Zhang, Bryan Kelly, Toby Moskowitz, Stefano Giglio, James Choi, Christopher Clayton, Paul Goldsmith-Pinkham, Gary Gorton, Song Ma, Elena Asparouhova, Jonathan Brogaard, Davidson Heath, Mark Jansen, Avner Kalay, Yihui Pan, Jiacui Li, Philip Bond, Stephan Siegel, Léa Stern, Christopher Hrdlicka, Yang Song, Adem Atmaz, Huseyin Gulen, Svetlana Bryzgalova, Roberto Gomez Cram, Marco Grotteria, Christopher Hennessy, Victor DeMiguel, Steven Kou, Andrew Lyasoff, Max Reppen, Scott Robertson, Lucy White, Hao Xing, Fernando Zapatero, Christian Heyerdahl-Larsen, Fotis Grigoris, Preetesh Kantak, Fahiz Baba Yara, Craig Holden, Noah Stoffman, Daniel Carvalho, James H. Cardon, Brigham Frandsen, Lars Lefgren, Olga Stoddard, Mark Showalter, Riley Wilson, Brian Boyer, Tyler Shumway, Karl Diether, Ryan Pratt, Craig Merrill, Darren Aiello, Taylor Nadauld and seminar participants at University of Utah, University of Washington, Yale, Purdue, London Business School, Boston University, Brigham Young University Economics Department, Brigham Young University Finance Department and Indiana University for their helpful comments and input. This paper was earlier circulated with the title "Machine Learning, Quantitative Portfolio Choice, and Mispricing."

Abstract

What is the price elasticity of demand for canonical portfolio choice methods in financial economics? Twelve models from the literature exhibit strikingly inelastic demand, in contrast to classical models. This is due to the difficulty of trading against price changes in practice, and is consistent with demand elasticity estimates. This provides a novel answer to the inelastic markets hypothesis, raises important concerns for the use of strongly elastic investors in theory models, and quantifies the difficulty of trading against potential mispricing aside from the standard limits to arbitrage frictions. Counterfactual experiments with these demand functions exhibit large and persistent alpha.

Keywords: price elasticity, demand-based asset pricing, machine learning.

JEL Classification: G11, G12, G17.

How investors react to price changes—the price elasticity of demand—is a central quantity of interest in financial economics (Koijen and Yogo, 2019). Indeed, the elasticity of demand is considered a measure of the degree of aggressiveness in trading against mispricing (Haddad et al., 2022). The elasticity is the inverse of price impact from flows and supply shocks, which means that inelastic demand corresponds to large price impacts of trading flows (Gabaix and Koijen, 2021). Interestingly, since the elasticity is in terms of percentage changes, an investor who doubles their leverage does not necessarily double their elasticity of demand. Indeed, an investor who doubles their leverage for reasons unrelated to prices does not change their elasticity at all. Thus the elasticity of demand is a measure of aggressive trading separate from leverage.

Recent work has estimated an average elasticity for individual stocks is in the approximate range of 0.3 to 1.6, implying a price impact from about 0.6% to 3.3% from trading flows equal to 1% of shares outstanding (Gabaix and Koijen, 2021). This stands in stark contrast to calibrations of classic models resulting in much higher elasticity values, e.g. 6,000 in Petajisto (2009) and the cited 5,000 in Gabaix and Koijen (2021). Even the demand of hedge fund and mutual funds, which include classic statistical arbitrage and smart beta funds (Khandani and Lo, 2011; Ahmed and Nanda, 2005) that are perhaps most like the high-elasticity investors in these models, is strikingly inelastic compared to these calibrations (Koijen and Yogo, 2019). What accounts for this difference?

The purpose of this paper is to measure the elasticity of reasonable statistical arbitrage strategies based on canonical portfolio choice methods from the academic literature. I consider twelve different canonical portfolio choice models from the literature (e.g., Fama and French (1993); Brandt et al. (2009); Kelly et al. (2019); Kozak et al. (2020)). I calculate not only the portfolio weights that come from these models, but also how these models react to changing prices. The main finding of the paper is that these methods have strikingly inelastic demand. Why is this? In classic models, the only uncertainty comes from not knowing the future realizations of well-known and understood random variables. Many variables in models are often fixed, known, and exogenous to prices, e.g. the covariance matrix of returns, the set of state variables that matter, the structure of equilibrium, and expected asset payouts. For example, Berk and van Binsbergen (2021), Martin and Nagel (2022), Heaton (1995), Pavlova and Sikorskaya (2022), Haddad and Muir (2021), Kyle (1985) have assets with expected payouts that are exogenous to prices. Thus when price of the asset changes, there is strong incentive to trade aggressively against the price change since a 1% decrease in prices represents a 1% increase in expected returns. These models are then applied the stock market, where stock payouts are the sum of future dividends and prices, and future prices are likely not exogenous to today’s prices. Vuolteenaho (2002) and Gonçalves (2021) show that much of the price movements in individual stocks is associated with long-term discount rates and cash flow news, rather than only next-period returns. Thus most price movements have much less than one-for-one predictability for next-period returns. This helps explain the so-called inelastic markets hypothesis, as coined by Gabaix and Koijen (2021).

The reason that demand for these methods is inelastic can be summarized succinctly: trading against stock-level mispricing is risky and hard.111If statistical arbitrage is risky, perhaps it should not be called arbitrage. Also, the term statistical arbitrageur is perhaps overly broad, as it includes investment strategies apart from classic factor bets, e.g. pairs trading. However, in the spirit of the literature, e.g. Stein (2009), I refer to as a hypothetical investor who invests according to these methods as a statistical arbitrageur. While this concept is not new, quantification of using methods from the literature is novel. In contrast to many classical models, canonical portfolio choice strategies invest according to some method that maximizes an objective function based on some concept of historical performance. While there are certainly fixed inputs into these models, fewer components of the model tend to be exogenous, fixed, and known. In many cases, nearly all components of the investment rules are modeled with uncertainty (e.g. Kozak et al., 2020). Thus in many classical models with so much held constant, a 1% price change represents near arbitrage opportunities. With canonical portfolio choice strategies, a 1% price change is far less predictive of trading profits. Thus these methods have much less elastic demand.

These demand functions are relatively inelastic because there is so much noise in the time series and cross-section, making it difficult to create a factor model that strongly depends on prices. I document how a 1% price change effects the standard predictors (often valuation ratios) used in these models. These changes tend to be relatively small, making the portfolio weights relatively insensitive to prices, because it is difficult to construct reliable valuation ratios in the cross-section that are sensitive to prices. Indeed, most portfolio choice models heavily rely on predictors that are not even a function of prices, such as investment and profitability, which makes the models’ demand more inelastic. Finally, noise in the time series means that estimates of alpha today are made from historical data, making model-implied demand relatively inelastic. Updating a factor’s alpha frequently as a function of prices is difficult since long time periods are needed to estimate this alpha given this time series noise.

There are two lenses with which to view linear factor models that price the cross-section222I use the typical definition of a factor model that prices the cross-section: all test assets have zero alpha relative to this model. and their corresponding linear SDFs:333Certainly an arbitrary SDF does not necessarily deliver a linear factor model. However, a linear factor model that prices the cross sectional corresponds to a linear SDF (Kozak et al., 2018). (1) models that describe the cross-section of returns or (2) investment advice for mean-variance investors.444A factor model only prices the cross section if and only if it delivers the highest possible Sharpe ratio. See the “agnostic interpretation” of factor models in Fama (2014) that comes from the logic in Huberman and Kandel (1987). The first lens is typically used in academic papers, but certainly the second lens is well-known and understood (e.g., Pástor (2000); Kozak et al. (2018); Brandt et al. (2009); DeMiguel et al. (2009)).

There is a rich literature that views these models through this second lens. For example, Pástor (2000), Brandt et al. (2009), and DeMiguel et al. (2009) consider various methods of computing weights on a set of factors from an optimal portfolio choice perspective. Kozak et al. (2018) think of arbitrageurs who essentially use a factor model to trade against mispricing. Indeed, this is so common in the literature that I refer to these as canonical portfolio choice models. Given this second lens equivalence, these statistical arbitrageur models should produce mean-variance demand functions, meaning that the elasticity should be identical.

Take for example an investor who believes the Fama and French (1993) three-factor model prices the cross-section of returns and wants to invest in a portfolio with the highest possible Sharpe ratio (i.e., mean-variance preferences). In this case, the investor believes that instead of diving into the complicated work of investing in many individual assets, the highest Sharpe ratio can be achieved by investing by only using three predictors: (1) market equity, (2) book-to-market ratio, and (3) relative size. These three predictors from this model—in combination with some method such as Pástor (2000), DeMiguel et al. (2009), or Kozak et al. (2020) to choose how much to weight each predictor—generates a demand function for individual assets.

The asset pricing literature has produced a large set of return predictors, also known as asset characteristics. The large set of portfolios formed based on these predictors is often known as the factor zoo and has been discussed at length in the literature (Cochrane, 2011; Harvey et al., 2015; Feng et al., 2020). There are two types of predictors, those that are a direct function of price (e.g. price ratio variables like book-to-market and earnings-to-market) and those that are not a function of price (e.g. Fama and French (2015) profitability and investment are functions of only accounting variables). In order to calculate the elasticity of a statistical arbitrageur, one must calculate how a 1% price change affects predictors, and then how changes in those predictors affect the ultimate portfolio weights. I use the Freyberger et al. (2020) 62 predictors, although some models like Fama and French (2015) and Hou et al. (2014) use only a small subset of these predictors. In the literature, often portfolio weights are formed based on discontinuous functions of predictors (e.g. Fama and French, 2015), but to measure these price pass-throughs with derivatives, differentiable approximations of Kelly et al. (2019) and Kozak et al. (2020) portfolio weight functions are used.

While the very purpose of linear factor models is to describe why different assets earn different returns (Kelly et al., 2019), the discussion of how these models react to changes in prices is strangely sparse in the factor model literature.555A notable exception is van Binsbergen and Opp (2019), who show that price wedges and short-term alpha do not have a one-for-one relationship. The factor model literature is no small niche of the literature either, it is the “greatest collective endeavor of the asset pricing field in the past 40 years" (Kelly et al., 2019). If a factor model is perfectly inelastic in an extreme case, then the model only describes differences in returns unrelated to prices. A model with a large positive elasticity value implies that the model shifts optimal weights strongly when prices shift, implying the the model is potentially able to describe differences in the cross section that are actually due to prices. A model with a negative elasticity value implies that the model corresponds to momentum-style upward sloping demand. Across the twelve models, there are relatively large quantitative differences. For example, the modified version of the Bryzgalova et al. (2020) model is the most elastic model with an elasticity of about 16, while the Kelly et al. (2019) model has an elasticity of about -8. The average elasticity value is across models is 3.4. Importantly, this means this paper introduces a novel and important new concept to the literature: the elasticity of a factor model.

The elasticity of these factor models is for the most part more elastic than the average elasticity of about 0.3 in Koijen and Yogo (2019), hereafter just KY, which is perhaps the most commonly referenced estimate of elasticity estimates. However, I show that KY have a relatively restricted functional form. I estimate the demand elasticity using a functional form similar to the flexible factor model demand presented in the paper to determine if this restriction explains the difference in elasticity values. I find that indeed, when demand is estimated with an unrestricted model, the elasticity is higher and comparable to factor model demand. Importantly, the unrestricted demand function aggregates well, meaning that multiple funds with different investment strategies within the same 13F institution have a combined demand function with the same functional form. In KY, the demand is exponential linear in predictors, but the demand function of multiple funds combined is not also exponential linear. Gabaix and Koijen (2021) estimate a macroeconomic demand function with similarly good aggregation properties, and this paper contributes to the microeconomics (stock-level) asset demand estimation literature with a demand function with good aggregation properties.

Once one realizes that (1) many predictors are not a function of stock prices, (2) time-series noise makes predicting real-time alphas difficult, and (3) cross sectional noise makes it difficult to create valuation ratios that move strongly with prices, it is not surprising that these statistical arbitrageurs are inelastic. In an extreme case, an investor who invests according to the CAPM as a market indexer has perfectly inelastic demand, which is well-known (Koijen and Yogo, 2019). If the result is not surprising, why does this matter? One can interpret this inelastic demand in one of two ways. First, to the degree to which these statistical arbitrageurs represent actual hedge funds and mutual funds who use smart beta or other statistical arbitrage techniques in practice, this shows that these investors cannot actually invest aggressively against mispricing as many models imply. This exercise quantifies an important limit to arbitrage apart from the fear of losing investments under management (Shleifer and Vishny, 1997), correlated arbitrage capital (Cho, 2020), or a host of other limits (Stein, 2009). To be clear, many other limits to arbitrage translate into lower price elasticity values, but the model-implied elasticity values are low for reasons separate than this broad literature. These are essentially friction-free models, but the fundamental risk still implies low elasticity values.

Second, to the degree that these models do not represent actual statistical arbitrage investors in practice, this result is still an important contribution to the factor model and cross sectional asset pricing literature. Given recent the elasticity estimates in this paper, KY, and the rest of the literature surveyed in Gabaix and Koijen (2021), actual statistical arbitrageurs likely do not have more elastic demand than these models. Thus these models provide an upper bound on a reasonable degree to which statistical arbitrageurs have the capacity to trade against price movements, even before imposing common literature frictions (e.g. Shleifer and Vishny, 1997). Note that the framework of these models is relatively general: the models simply use a broad set of predictors, many based on prices, to produce optimal portfolio weights. This is much more general than just showing that market indexers are inelastic, this shows that by leveraging the vast set of return predictors from the literature using twelve models honed to combine these predictors optimally, even the most price-sensitive models fall far short of classical elasticity values of 5,000. While it is perhaps unsurprising that these models deliver inelastic demand, it is striking how well these elasticity values line up with estimated elasticity values than for example, the midpoint of this vast range between 5,000 and the estimated values. The elasticity provides a useful metric for factor models that answers the question: how sensitive is this model to asset prices? This provides an important contribution to the large cross sectional asset pricing literature (e.g. Harvey et al., 2015; Feng et al., 2020; Cochrane, 2011; Kozak et al., 2020). This paper also provides a critique for theoretical models that contain highly elastic investors, and rely on these investors to rule out mispricing or create small price impacts from flows. Thus this paper contributes to the literature on limits to arbitrage, (e.g. Shleifer and Vishny, 1997; Cho, 2020; Kozak et al., 2018; Martin and Nagel, 2022; Fama and French, 2007; Hart and Kreps, 1986; Stein, 2009; Hong and Stein, 1999).

At the end of the paper, I show counterfactual experiments with the statistical arbitrage demand from these models combined with estimated demand. Following KY, the counterfactual experiments hold fixed shares outstanding and accounting variables, and determine what the historical price of all individual stocks in the sample with counterfactual insertions of the statistical arbitrageur models in this paper. Interestingly, CAPM alpha in some cases increases in magnitude and is never eliminated. This is unsurprising given the levered but inelastic demand of these models, but lends some credence to the idea that trading against prices and statistical arbitrage in the stock market is difficult.

1 Elasticity of Theoretical Statistical Arbitrageurs

In order to discuss the elasticity of statistical arbitrage, we first have to explore the elasticity of standard theoretical model-based investors.

Consider a set of assets. Suppose an arbitrageur has assets under management.666If this is a household instead, then would denote the wealth of the household. Let denote the share price of asset , and denote the portfolio weight of the fund for the asset. Then denotes the number of shares of the asset that the fund owns. The elasticity is defined as:

| (1) |

where in calculating the second equation, I follow KY by assuming the assets under management are exogenous.777In other words, the assumption is This assumption is problematic in a macroeconomics setting where the market-level return is being examined. This paper focuses on the microeconomics cross-sectional setting, where this assumption is less problematic. For example, an elasticity of 3.5 implies that a 1% increase in the price would lead to a 3.5% decrease in the shares demanded for the asset.

As KY point out, value-weighted index funds are designed to avoid rebalancing for price fluctuations, and are thus perfectly inelastic. This can be seen using equation (1), since a 1% price rise leads to a 1% increase in the asset’s portfolio weights. Thus, , and ().888As shown below, static models with classic mean-variance demand have very elastic demand. It is this type of model that is typically used to derive the CAPM. However, if one believes the CAPM and then because of this just invests in the market without paying attention to prices, then this investor has completely inelastic demand. As this becomes more widespread, aggregate demand strikingly becomes more inelastic. This is analogous to the famous Grossman and Stiglitz (1980) paradox, rephrased in terms of elasticity.

The price elasticity is a key quantity in asset pricing models, because it describes how investors react to price changes. If investor demand strongly reacts to price changes, then the effect of many behavioral biases can be either dampened or entirely offset (see Gabaix and Koijen (2021) for a discussion on the importance of demand elasticity). Demand elasticity is also the inverse of the price impact of investment flows. Thus, inelastic demand implies a large price impact.

The point of this section is not to convince the reader that statistical arbitrageurs produce inelastic demand. This is shown empirically below for the twelve models in this paper. This section simply (1) points out that these elasticity values are quite low relative to their theoretical counterpart and (2) gives some basic reasoning with a simple model for why statistical arbitrageur demand is inelastic.

1.1 Elasticity of Classic Models: A Simple Calibration Exercise

Consider an investor with CARA utility that chooses a vector of portfolio weights at time of the risky assets. Let be the vector of returns in excess of the risk-free rate, with the gross risk-free rate . The investor chooses to maximize utility:

| (2) |

where is the CARA risk-aversion coefficient and is a vector of ones. The classic demand, with multivariate normal returns, is then:

| (3) |

where is the covariance matrix, is the vector of expected excess returns.

Alternatively, consider the case of Epstein-Zin multivariate demand for the risky assets from Campbell et al. (2003). Let be the dimensional vector of log returns minus the log risk-free return. They show, after log-linearization, portfolio weights are given by the approximation:

| (4) |

where , is the conditional covariance matrix of , is the dimensional vector containing the diagonal elements of , is the dimensional vector of conditional covariance of the log consumption to wealth ratio and , is the relative risk aversion coefficient, is the elasticity of intertemporal substitution, and .999See equation (20) of Campbell et al. (2003). Note that in their equation, there are some additional terms because they also consider to be log return of the asset minus a benchmark with potential covariance terms. We consider just the risk-free rate, which eliminates some of these extra terms. Recall that Epstein-Zin demand nests CRRA demand.

It is common to have a covariance matrix that is exogenous to prices. It is also quite common, across a large variety of models, to model assets with expected payouts that are exogenous to prices (e.g. Berk and van Binsbergen, 2021; Martin and Nagel, 2022; Heaton, 1995; Pavlova and Sikorskaya, 2022; Haddad and Muir, 2021; Kyle, 1985).101010For example, Berk and van Binsbergen (2021) have a “liquidating dividend” at the end of the single period, and it is easy to see that this expected payoff is exogenous to prices. This is extremely common in asset pricing models, but then the model-implied price impact (inverse of demand elasticity) is sometimes used to assess the actual impact of investment flows (e.g. ESG investment in this example).111111One may argue that in equilibrium, prices cannot move independently from payoffs in some of these models. This argument misses the definition of the elasticity of demand, which is calculated based on the demand function before prices are solved for in equilibrium. Indeed, in many models prices can move very little precisely because demand is elastic and therefore price impact from flows is small. Price elasticity is not defined by trades, it is defined as the sensitivity of a demand function to price movements, even if those price movements are off-equilibrium price movements. Indeed there is a demand price elasticity even in a model with a representative investor. Many of these models are applied to stock markets. Given the two demand functions above, with exogenous covariance matrices and expected asset payouts, the only other way that prices can affect demand other than through expected returns ( or ), is through the consumption-to-wealth covariance term in Epstein-Zin demand. Davis et al. (2023) show that empirically, this consumption-to-wealth component affects elasticity values only slightly.121212This is sensible economically as well, since the consumption to wealth ratio is an aggregate quantity, and thus a 1% price change does not appear to affect the covariance of individual asset returns and the consumption to wealth ratio. In Davis et al. (2023), at the largest, this term decreases the elasticity value by at most 6% of the total elasticity value. Even 94% of the calibrated elasticity value is orders of magnitude above literature estimates. Thus ignoring this hedging component in calculating the elasticity, we can use the chain rule to expand equation (1):

| (5) |

where we can write this same equation, but replace with as well.

Let be the exogenous payoff. With this payoff, we can calculate:

| (6) |

| (7) |

Assuming , then we can use as a conservative approximation for both of these derivatives in the elasticity equation. Davis et al. (2023) criticize this feature of many models (i.e. ), in particular static models, and how this is often used to generate unrealistically small price impacts and high elasticity values. Plugging this into equation (5) yields:

| (8) |

which we can again write as a function of for the Epstein-Zin case.

Note that any increase (decrease) in or decreases (increases) or respectively by the exactly the same amount that increases (decreases) by. Thus elasticity values are independent of any positively chosen or , and thus without loss of generality with regard to elasticity calculations, we can set these parameters such that the weights of risky assets sum to one in equilibrium.131313This is consistent with a zero net supply of the risk-free asset, which is again assumed without loss of generality in regards to elasticity value calculations. Given the parameter values below, this is set at .

To show the magnitude of this elasticity, I plug in a set of parameters. I consider 1,000 assets, and consider an asset with an average portfolio weights, i.e. .141414This does not mean this calibration only holds for equally weighted portfolios. It simply means we consider an asset with an average portfolio weight. I set the correlation between all stocks to be 0.3,151515Pollet and Wilson (2010) report average daily correlations to be 0.237, and longer-horizon correlations are higher due to autocorrelations across days. Thus, I use 0.3 as a reasonable parameter value a volatility of 30% per annum, an expected excess return of individual stocks to be 6%. This implies in the case of CARA demand. This delivers an elasticity of about 7,000 (). This is comparable to the elasticity value of 6,000 from Petajisto (2009), and similar to Gabaix and Koijen (2021), which cites an elasticity of 5,000 or above in classical models. To calibrate the Epstein-Zin demand elasticity, with a similar covariance structure and assuming the term is about 6%, then this of course delivers the same demand elasticity.

When the elasticity is written in this form, as , with many assets and reasonable values of expected returns and covariances, it is clear that the elasticity is likely to be at least three orders of magnitude larger than unity (similar to Petajisto (2009)). This exercise also reveals how standard multivariate utility yields much higher elasticity values than in settings with only a single or a few assets. This is intuitive, since many assets naturally means that assets will be better substitutes for each other and thus have a higher price elasticity, while a setting with only a single or a few risky assets naturally provides only limited substitutability and thus a lower elasticity.

An elasticity of 7,000 implies that a 1% drop in prices leads to an 7,000% increase in shares demanded. This sensitivity to prices is an important component of many asset pricing models. An investor with highly elastic demand has a strong sense of the "right" price. When prices deviate from this price, highly elastic investors trade aggressively against these price deviations. This strong sense of the right price is fundamental to the logic that if there were mispricing, investors would act dramatically in this highly elastic fashion to correct the mispricing.

What causes this difference in demand elasticity values? What is wrong with this calibration? The logic is simple: it is hard to know what the true alpha is and therefore it is hard to know the right price. Alpha is typically assessed using historical data, and thus as prices move, it may be difficult to update the contemporaneous alpha and thus the current mispricing. The calibration holds all else equal (e.g., holding risks and expectations of future payoffs equal) and just varies prices, but in practice this is quite hard to do. Empirical canonical portfolio choice models by design try to limit risk while achieving high Sharpe ratios. This risk-return optimization means these models are less inclined to make large bets about the right price—meaning they are relatively inelastic—than their theoretical counterparts that hold all else equal.

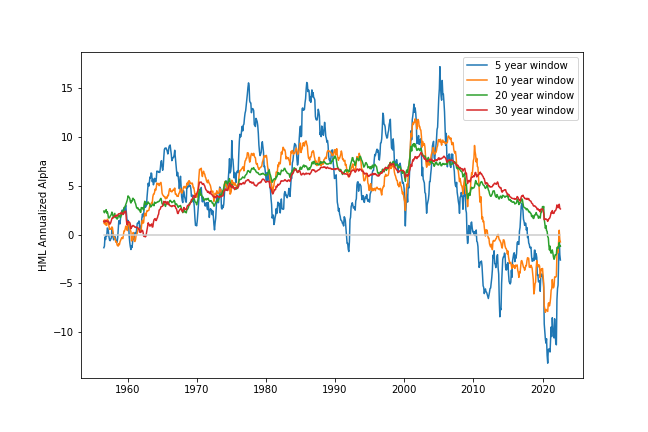

For example, it is difficult to determine the alpha of value stocks. Over a two year period (April 2020 - March 2022),161616When the data were downloaded, this was the most recent two-year period. the long-short portfolio from the Fama and French (1993) three-factor model beat the market, after a decade (April 2010 - March 2020) of underperformance. Calculating the CAPM alpha with 5-, 10-, 20-, and 30-year rolling windows yields very different results about the sign and magnitude of the alpha.171717This is well-known, but is also shown in Figure A.1 in the Appendix. It of course gets more complicated if standard errors are calculated with different assumptions. Is the true value alpha positive, negative, or zero? If the price of value stocks changes quickly, what is the alpha going forward? These questions are inherently challenging. If this was easy, then there likely would not be so much debate over the right factor model.

Due to the difficulty of determining the right price, a statistical arbitrageur that takes a strong stand on the "right" price may make strong levered bets in the wrong direction, which is unlikely to yield a high Sharpe ratio. Thus, the statistical arbitrageurs are actually fairly insensitive to current mispricing. In other words, the statistical arbitrageurs are relatively price inelastic compared to the calibration. In conclusion, this inelasticity is a feature of these statistical arbitrageurs and not a bug.

2 Why is Statistical Arbitrageur Investment Inelastic?

To understand why canonical portfolio choice demand may be relatively inelastic, it is important to first understand the structure of demand from these models. Figure 1 shows how these demand functions work. The price of a share of stock in period is . Various predictors, , are a function of this price term. In this example, book-to-market and earnings-to-price ratios are a function of the stock price. However, Fama and French (2015) profitability is not a function of the price. The raw predictors are transformed into normalized predictors, , as described below. Finally, the portfolio weight for stock is a function of the normalized predictors. This is the general form for KY demand, as well as canonical portfolio methods.

There are two ways these functions can be modified to create more elastic demand:

-

1.

First, the portfolio weights on the factors themselves could be modified to vary substantially with the overall price of the value portfolio. However, as discussed above, it is difficult to determine the current alpha of these factors in real time. In other words, this is difficult because the time series of factor returns is noisy.

-

2.

Second, the portfolio weights of individual component assets could be modified to vary more with prices. This is difficult as well, because these predictors are only weak signals about future returns on average, and much less so at the individual stock level. In other words, this is difficult because there is so much noise in the cross-section of individual stock returns.

This does not imply that modifying demand to be more elastic is impossible, just difficult.

2.1 Stylized Model

I consider the case where a mean-variance investor believes that the market and value factor from the Fama and French (1993) model price the cross-section of returns, and are thus mean-variance efficient. I exclude the size factor from Fama and French (1993) for simplicity. The purpose of this subsection is not to present a general model, but to transparently reveal the key economic reason why the canonical statistical arbitrageurs in this paper are inelastic with as simple a model as possible.

What is the economic reason that this model produces inelastic demand? In other words, why is this model unsure of the "right" price? This is because book-to-market ratios are noisy unreliable signals about what price should be. The aggregate value premium has at times been historically high (see Figure A.1), but has fluctuated much through time. Critically, there is even more noise at the individual stock level, meaning that the model is designed such that only relatively large price movements are needed to switch a stock from a value stock to a growth stock, or vice versa. Thus, since large price movements are needed to change asset demand substantially, this statistical arbitrageur has inelastic demand.

I consider a single asset , which is contained in both the market fund and the value fund. In other words, I consider a market portfolio (composed of many assets), a long-short value portfolio (composed of many assets), and one asset in particular that is potentially in both the market and value portfolios. I will discuss two kinds of portfolio weights: (1) portfolio weights of the factors themselves and (2) portfolio weights of assets within those factors.

The number of shares outstanding has no economic significance, and thus I assume that there is one share outstanding for the asset considered here181818Investors can invest with fractional shares.. Let denote the price of this asset, which is the same as market equity if this asset is a stock because there is only one share outstanding.

Importantly, in this example, each statistical arbitrageur invests a fixed fraction of her money into the value fund and into the market. The variable is chosen by considering optimal portfolio weights in the data and critically does not vary as prices change. Brandt et al. (2009) and Kozak et al. (2020) are portfolio optimization methods where the investment weights for each portfolio do not vary as prices change.

The weight of the asset in the market portfolio is , where is the value of the market—i.e. is the sum of the prices of all assets. Assume that the statistical arbitrageur has dollars to invest. Both and are exogenous. Assume that the asset’s weight in the value fund is , where is a function that equals either 1, 0, or depending on whether the asset is in the long portion of the portfolio sort (i.e. ), the asset has no weight in the portfolio (i.e. ), or the asset is in the short portion of the portfolio sort (i.e. ). Notice that this portfolio is a difference of value-weighted portfolios. In other words, this is a standard valued-weighted long-short portfolio.

In this case, this statistical arbitrageur invests the following amount of dollars into the asset:

where the first term represents the dollar amount invested in this asset because the asset is in the market portfolio and the second term represents the dollar amount investment in this asset because the asset is in the value portfolio.

Thus, shares demanded of this asset are:

and the elasticity is

Notice that except for a few portfolio sort break points where the derivative is not defined, . Thus, except for these break points, demand is complete inelastic—i.e. . This is perhaps not fair to traditional discontinuous portfolio sort methods because demand does change with changes in the price at these break-points. I consider a continuous version of this below.

It is important to note that if this strategy instead was a combination of investing in the market and a profitability portfolio for example, then would not vary with prices, because market equity does not affect profitability portfolio sorts. In other words, in this example, this demand function is perfectly inelastic everywhere.

Thus, this key result, that the classic quantitative portfolio choice strategies results in relatively inelastic demand almost everywhere holds for any combination of the market portfolio and long-short value-weight portfolios where two conditions hold: (1) portfolio weights of the factors are determined with historical data and not a function of today’s fluctuations and (2) large price changes are needed to substantially change the individual asset portfolio weights within the long-short value fund.

2.1.1 Continuous Predictors Weighting Instead of Discontinuous Jumps

The above function is characterized by a few discontinuous jumps. Suppose instead, that this function is linearized. Assume that is known to fall between some small price —a low price that makes the asset an extreme value stock—and some large price —a high price that makes the asset an extreme growth stock. Assume is large, which means that the plausible range for is large and the difference between a large growth price and a small value price is large. Define to be

This linearized version of represents a portfolio that is predictor-weighted, like Brandt et al. (2009) and Kozak et al. (2020). In other words, the asset in the portfolio is weighted by the degree to which the asset is a value stock or a growth stock.

In this case the elasticity is given by

Since the growth price is much larger than the value price , this quantity is small. Thus, even in this linearized case, statistical arbitrageur demand is still relatively price inelastic. This also nicely shows that if only small changes in prices are needed to move an asset from the long end to the short end of the portfolio—i.e. is small—then demand can be much more elastic.

Thus, the key intuition of this subsection is not the fact that discontinuous portfolio sorts generate inelastic demand, but rather that statistical arbitrageur demand even with continuous portfolio weights is by design, relatively inelastic.

3 Data

I describe the data in this section. First, I describe the Center for Research in Security Prices (CRSP) fund flows data. Then I describe the holdings data, followed by the returns and predictors data.

The CRSP monthly fund flows data start January 1960 and end March of 2022. I merge these data with the standard market portfolio excess return and risk-free rate data from Kenneth French’s website. The risk-free rate is the standard one-month Treasury bill rate.

I also use quarterly institutional long-only holdings data from the SEC 13F filings dataset. See KY for more details about these data. My sample period is from 1984 to 2020. Across many assets, the 13F holdings often do not account for the entire set of shares outstanding, and I follow KY by creating an additional "household" investor that holds the residual shares.191919This residual investor is labeled ”households” by KY.

I use the monthly equity returns and stock predictors data from Freyberger et al. (2020), which contains 62 predictors (i.e. asset characteristics). A thorough description of the variables can be found at Freyberger et al. (2020). This data was extended from 2014 to the end of 2020 by Baba-Yara (2022). The sample starts in July of 1967. The 13F filing data are are merged with the predictors data. This data is merged to the CRSP monthly returns data which contains changes in shares outstanding, returns, and dividends.

4 Measuring the Elasticity of Quantitative Investment

4.1 Notation and Data Preparation

Let denote the market equity of stock at time , while denotes the share price of the asset. Therefore, where denotes the number of shares outstanding.

I take the raw predictor for stock at time , denoted , and normalize them as shown in Figure 1. For example, could be the book-to-market or profitability ratio in Freyberger et al. (2020). As Kozak et al. (2020) and Kelly et al. (2019) discuss, it is important to normalize the predictor into a well-behaved predictor, , for statistical arbitrageurs.

The main type of normalized predictor is used for the factor models, denoted as . I use a continuous version of the normalization that Kozak et al. (2020) and Kelly et al. (2019) use, among others. Their normalization is the raw predictor, , mapped into cross-sectional percentiles (between 0 and 1) minus one half (with a resulting range between and ). For example, if an asset has a book-to-market ratio in the twentieth percentile in the cross-section of assets, then the resulting normalized value would be (). A slightly modified version of these normalized predictors are used in the demand estimation section, which is discussed below.

I use a continuous version of this percentile transformation, as defined and discussed below. I use a continuous transformation to be able to calculate the elasticity of demand of these statistical arbitrageurs. In other words, every step between prices and portfolio weights in Figure 1 should be continuous, including having be a continuous function of . This allows the calculation of for each predictor (see Appendix B.1 for the closed-form formula for these derivatives).

The transformation of the raw predictors, , into the normalized predictors, , allows me to form predictor-weighted portfolios. As Kozak et al. (2020) and Kelly et al. (2019) discuss, using portfolios weighted with these cross-sectional percentiles produces clean long-short portfolios with a long tradition in asset pricing, while using portfolios based on raw predictors, , is full of noise.

4.2 Continuous Transformation Into Normalized Predictors

This subsection explains the statistical arbitrageur predictors, denoted as . I consider the standard predictor-weighted portfolios, like Kozak et al. (2020) and Kelly et al. (2019), among others. These are portfolios which are weighted, in the long and short tails of the portfolio, by the cross-sectional deviation of a specific predictor, such as book-to-market or investment values. When using predictors in this way, predictor normalization is critical to producing relatively reliable statistical arbitrageurs (see Kozak et al., 2020). This alleviates issues with outliers and noise in the data. I discuss the normalization immediately below.

Let be the -dimensional vector of the raw predictor known at time that is filled with the raw predictor values. Let and be the corresponding normalized predictors. The standard normalization, used for example in Kozak et al. (2020) and Kelly et al. (2019), is to transform the raw predictors to be

| (9) |

where is a function that reads in a vector and outputs a vector of values through corresponding to the relative rank of the input values ( is assigned the largest value, the smallest), and is the element of this output vector. This transforms predictors to be in the range of .

This is a discontinuous function of the predictor . If is the book-to-market ratio for example, then any demand function that is a function of is then a discontinuous function of the price. This complicates elasticity estimations. Thus, I create a continuous version of this normalization defined as

| (10) |

where is the standard inverse hyperbolic sine function and is the cumulative distribution function (cdf) of a standard kernel density function. Similar to above, is the element of . I use the standard well-known normal cdf kernel function, described in detail in Appendix B.1 below.

This transformation above yields very similar results to its discontinuous version, but this function is of course continuous. The function is used because it is similar to the log function in that it shrinks extreme values towards zero, but is defined at zero and negative input values.202020In fact, the approximation holds for large values of . Since many predictors can assume negative values, this is necessary. The final kernel minus one half function is necessary to transform the value into the interval.

4.3 Forming Linear Predictor-Based Factor Portfolios

The BPZL, BSV, DGU, and the KNS models use linear predictor-weighted portfolios, defined here. Following Kozak et al. (2020), I rescale these predictors in every period to avoid leverage in the predictor-weighted portfolios from fluctuating across time with the number of assets available. Note that the sum of the absolute value of the predictors in any given period is about (i.e., ).212121Note that could be notated as , since the number of available stocks varies across months. However, to avoid conflicts with standard notation used in Kelly et al. (2019) and Kozak et al. (2020), among many others, I use the simpler term. For any , I define and . Thus, I can write . This allows me to define predictor-weighted portfolio returns. Let be the zero-cost portfolio return associated with predictor :222222Note that these are zero-cost portfolios even if the weights were all positive because are excess returns, not just returns. However, since the weights, before being scaled down, fall evenly between and (i.e., weights sum to zero), these are classic long-short predictor weighted portfolios (see Kozak et al. (2020)).

| (11) |

Factor models, such as Fama and French (1993), require a market portfolio return as well. Let be the AUM of institution , and .232323Note that by this definition, . As in KY and discussed below, a residual institution is added so that institutions collectively hold all assets in the data. I let the first predictor, , be a market portfolio return weight: . Note that this is defined in terms of and not , so that , which matches the other portfolios.

4.4 Two Types of Predictors

Following KY, I separate predictors into two categories: (1) those that are a function of price and (2) those where price is not needed or used to calculate the predictor. I follow KY by assuming this latter type of predictors are exogenous to prices, such as historical beta, book values, asset values, investment, and profitability. Fifteen out of the 62 predictors are a function of price. In Appendix B.2, I describe the classification of the predictors into these two types in more detail.

Some of the predictors from the Freyberger et al. (2020) data use historical prices, instead of contemporaneous prices, to create price ratio variables. For example, the book-to-market ratio is computed with stale market capitalization values in order to better match the period when when the accounting book values were released. I follow KY by instead using the most recent prices to calculate these standard valuation ratios. Using historical prices instead of current prices of course would make the statistical arbitrageurs in this paper even less price elastic. However, this seems to violate the spirit of standard valuation ratios. Basing investment decisions on valuation ratios should make investors sensitive to prices, which is why I use contemporaneous prices. As is standard with the CRSP data, the monthly price is the closing price on the last trading day of the month.

The most difficult predictors to sort into these two categories is the maximum daily return over the previous month and momentum. The maximum daily return is sometimes a function of today’s price if the maximum daily return was the most recent day. However, if this is classified into the category of being a function of price, then this is a discontinuous function. Since this is a historical daily flow and not a stock, this classification has little effect on the measured elasticity. Similarly, short term reversals are classified as being a function of price, but momentum is not. Momentum is defined as the return over the past year excluding the most recent month. This means it is not a function of price, while short term reversals are a function of price given that it is the return over the previous month. If these variables are dropped from the dataset, I have similar measured elasticity results. I keep these variables in the data because it is simple, does not change the elasticity results significantly, and keeps the set of predictors the same as Freyberger et al. (2020).

4.5 Price Sensitivity of Individual Factor Investment

Table 1 shows the 15 endogenous predictors, and importantly the median derivatives values for each predictor across assets and months. Some predictors with the price in the numerator, like Tobin’s q, tend to have a positive derivative. Other predictors, like the book-to-market ratio, have a price term in the denominator; thus, when the price increases, the predictor tends to decline (negative derivative). A derivative of , for example, means that a 1% rise in the price implies the predictor decreases by a quarter of its full range (recall the full range of these predictors is between and ). The 47 exogenous predictors of course have zero derivatives.

Note that many of these values are less than one in absolute value. For example, the median book-to-market (beme) derivative is . This is because the log book to market ratio has a relatively large range of values, and it thus needs to be compressed to be in the standard percentile range. The return over the past month (cum_return_1_0) and relative price to high price ratio (rel_to_high_price) values tend to have a relatively small range, and thus need to be expanded in some sense to be transformed into a percentile. This means these values tend to be larger than one in absolute value.

| Covariates | Gradient | Covariates | Gradient | Covariates | Gradient | ||

| a2me | e2p | o2p | |||||

| (, ) | (, ) | (, ) | |||||

| beme | ldp | q | |||||

| (, ) | (, ) | (, ) | |||||

| beme_adj | lme | rel_to_high_price | |||||

| (, ) | (, ) | (, ) | |||||

| cum_return_1_0 | lme_adj | roc | |||||

| (, ) | (, ) | (, ) | |||||

| debt2p | nop | s2p | |||||

| (, ) | (, ) | (, ) | |||||

| Obs. | 1,869,963 | 1,869,963 | 1,869,963 | ||||

| Months | 703 | 703 | 703 |

4.6 Factor Models

In this section, I describe the general framework for the twelve asset pricing models. These models are described in Appendix A and of course in their original papers, but I describe the basics here. I refer to these models by the initialisms which are summarized in Table 2. Baba-Yara et al. (2022) have a similar set of models with additional details.

| Initialism | Factor Method | MVE Collapse Method |

| BPZF | Bryzgalova et al. (2020) forest | Bryzgalova et al. (2020) |

| BPZL | linear characteristic-weighted portfolios | Bryzgalova et al. (2020) |

| BSV | linear characteristic-weighted portfolios | Brandt et al. (2009) |

| DGU | linear characteristic-weighted portfolios | DeMiguel et al. (2009) |

| FF3 | Fama and French (1993) | Kozak et al. (2020) |

| FF6 | Fama and French (2015) with Carhart (1997) momentum | Kozak et al. (2020) |

| GKX | Gu et al. (2021) | Bryzgalova et al. (2020) |

| HXZ | Hou et al. (2014) | Kozak et al. (2020) |

| KNS | linear characteristic-weighted portfolios | Kozak et al. (2020) |

| KPS | Kelly et al. (2019) | Bryzgalova et al. (2020) |

| NN | neural network | |

| RF | random forest |

I assume a sample of dates , which are used to form portfolio weights at time . Let be the matrix filled with values. Every model has portfolio weights that equal , where is a function that reads in predictors and outputs an matrix of factor portfolio weights and is an vector that collapses the factor weights down to a single (attempted) MVE portfolio. Let denote this row of factor weights specific to asset . Then portfolio weights for asset can be written as:

| (12) |

Various models use different functions and methods of estimating . Some factor models do not specify . For example, the Fama and French (1993) three-factor model does not specify the fractions of capital (portfolio weights) that should be invested in the market, value, and size portfolios in order to achieve mean-variance efficiency. In these cases, I use canonical methods from the literature, such as Bryzgalova et al. (2020) or Kozak et al. (2020) to collapse these factors down to a single set of portfolio weights.

Each model has three steps:

-

1.

First, I form the factor model weights, .

-

2.

Second, I form factor excess returns from weights: . Then compute the mean vector and covariance matrix using these returns:

(13) -

3.

Third, I estimate as a function of and using one of the methods discussed below. I refer to this as the "collapse" step, since it collapses the factors down to a single portfolio and demand function. Portfolio weights are set such that .

I show returns and elasticity values with these factor models with and without the market level factor (), but the results for the statistical arbitrageurs without the level term are shown only in the Appendix. Many of these models, including Kelly et al. (2019) and Kozak et al. (2020) for example, were originally estimated without a market factor. However, I follow Kelly et al. (2019) by including an additional intercept in .

Most models have a set of hyperparameters. Tables A.3 and A.4 in the Appendix show the hyperparameters for the models with and without the market level term. While some hyperparameters are just chosen using a standard rule-of-thumb, most are chosen with a four fold cross-validation design using the sample before 1990.

The scaling of the weights is arbitrary in many of these models. In other words, the models are designed to maximize the Sharpe ratio, but not to necessarily pick the level of risk and return. Thus, to create comparable returns results, the amount of leverage and risk needs to be chosen.242424As shown above, the amount of chosen leverage does not change the elasticity values. I simply follow Kozak et al. (2020), who scale portfolio weights so that the portfolio volatility matches the market volatility.

Let denote the derivative with respect to . Then the elasticity, defined only for assets with positive weights following KY, can be written as:

| (14) |

For the 47 exogenous predictors, such as investment and profitability that are not a function of price, . The other predictors affect the demand elasticity, because the portfolio weights change as prices change, as discussed in Section 1. In other words, every asset’s elasticity is a function of how much portfolio weights change as prices change (e.g., a valuation ratio like book-to-market changing as prices change) and how much the statistical arbitrageur invests according to that predictor (e.g., how much they invest in value stocks).

In the Appendices B.5 - B.10, I show the closed form solution for the elasticity of each model. For the two random forest based models, is discontinuous, and I describe in the Appendix how the derivatives are numerically calculated.

For the BPZL, BSV, DGU, and the KNS portfolios, linear predictor portfolios are used as the function, which are defined as . This scales the portfolio weights such that the relevant factor returns are . The models are described in detail in Appendix A. I describe both the portfolio collapse methods used to create , and as well as the portfolio weight functions .

4.7 Returns and Elasticity of Factor Investment

In Table 3, I show the annualized CAPM alphas, betas, and annualized Sharpe ratios of the twelve factor models during the out-of-sample period—which are the three decades from February 1990 to January 2020 inclusive. I follow Kozak et al. (2020) by scaling the portfolios so that their volatility matches the volatility of the market during the same period. The model parameters are estimated once using the data up until December 1989.252525Although not shown for brevity, the elasticity results are similar if parameters in each model are re-estimated every year instead of just once.

| BPZF | BPZL | BSV | DGU | FF3 | FF6 | GKX | HXZ | KNS | KPS | NN | RF | |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| 14.718∗∗∗ | 27.091∗∗∗ | 26.287∗∗∗ | 21.762∗∗∗ | 10.531∗∗∗ | 26.219∗∗∗ | 2.608∗ | 12.097∗∗∗ | 34.895∗∗∗ | 5.286∗∗ | 14.351∗∗∗ | 10.977∗∗∗ | |

| (1.980) | (2.548) | (2.642) | (2.699) | (2.514) | (2.702) | (1.476) | (2.416) | (2.598) | (2.248) | (2.408) | (1.872) | |

| 0.681∗∗∗ | -0.333∗∗∗ | -0.210∗∗∗ | 0.052 | 0.366∗∗∗ | 0.006 | 0.838∗∗∗ | 0.448∗∗∗ | -0.275∗∗∗ | -0.555∗∗∗ | 0.454∗∗∗ | 0.721∗∗∗ | |

| (0.039) | (0.050) | (0.052) | (0.053) | (0.049) | (0.053) | (0.029) | (0.047) | (0.051) | (0.044) | (0.047) | (0.037) | |

| Sharpe | 1.398 | 1.671 | 1.686 | 1.524 | 0.932 | 1.804 | 0.656 | 1.085 | 2.24 | 0.047 | 1.244 | 1.164 |

| Observations | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 | 360 |

| 0.463 | 0.111 | 0.044 | 0.003 | 0.134 | 0.000 | 0.701 | 0.200 | 0.075 | 0.308 | 0.206 | 0.520 | |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |||||||||||

Table 3 shows that many of these models have Sharpe ratios well above one out-of-sample. For some of the models, the annualized alphas are around 30%. Thus, as a whole, these models perform very well during this out-of-sample period.

Note that because of the in the denominator of the elasticity term, assets with values close to zero are extremely elastic (i.e. in the limit as goes to zero, they are infinite). This is sensible, since an investor who initially has a very small position in the asset then purchased much more due to a drop in prices appears extremely elastic since an elasticity is in percentage terms. In order to look at the average elasticity value across stocks and time in the bulk of the distribution instead of this extreme tails, the elasticity values are winsorized at the 5th and 95th percentiles. Table 4 shows the average elasticity values of these statistical arbitrageurs during this same period across stocks and time. Standard errors are shown in parentheses below the estimates, which are double clustered by month and stock. Note that by construction of the cross sectional predictors which are between -0.5 and 0.5, these elasticity values are quite stable across time. Mechanically, it is primarily cross sectional variation, which can be seen in Table 1, that generates variation in these results.

Across models, the average elasticity is 3.4. This is over ten-fold higher than the 0.3 value from KY, and I show below that this difference can be explained by a relatively restrictive function form used in KY versus the flexible functional form these models use. Interestingly, there is also a fairly large dispersion, with a average elasticity above 15 for the BPZL model, and the average elasticity of -8 for the KPS model. The KPS model is the only model with upward sloping demand, which is similar to a momentum trader in Stein (2009) that has upward sloping demand.262626(Stein, 2009, emphasis in original) stated: “Arbitrageurs do not base their demand on an independent estimate of fundamental value. As a result, their demand for an asset may be a nondecreasing function of the asset’s price.” For most models, the valuation ratios are enough to generate downward sloping demand, but the KPS model is a notable exception. It is also striking that the only difference between the BPZL model and the KNS model is the inclusion of a hyperparameter that is intended to shrink away noise in the estimates of past average returns, and the inclusion of this parameter almost doubles the elasticity. These models are all created to price the cross section of assets, but have strikingly different sensitivity to prices.

| Model | Elasticity | Model | Elasticity | Model | Elasticity | Model | Elasticity | |||

| BPZF | 0.544∗∗∗ | DGU | 5.839∗∗∗ | GKX | 1.000∗∗∗ | KPS | -8.023∗∗∗ | |||

| (0.016) | (0.055) | (0.001) | (0.136) | |||||||

| BPZL | 15.551∗∗∗ | FF3 | 4.119∗∗∗ | HXZ | 1.158∗∗∗ | NN | 1.742∗∗∗ | |||

| (0.157) | (0.032) | (0.008) | (0.068) | |||||||

| BSV | 4.541∗∗∗ | FF6 | 2.644∗∗∗ | KNS | 8.589∗∗∗ | RF | 3.051∗∗∗ | |||

| (0.031) | (0.015) | (0.067) | (0.025) | |||||||

| Obs. | 1,253,175 | 1,253,175 | 1,253,175 | 1,253,175 | ||||||

| Months | 360 | 360 | 360 | 360 | ||||||

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |||||||||

5 Demand Estimation

5.1 Demand Estimation Overview

As I show below, the KY demand function is similar to a restricted version of the flexible demand function that statistical arbitrageurs have as shown above. The key question of this section is to determine whether it is this restriction which, if relaxed, empirically explains the difference in elasticity values estimated from data versus those of the statistical arbitrageurs shown above. I find that when this restriction is relaxed, estimated elasticity values from holdings data are indeed higher and more comparable.

Note that this is a separate but related question to whether the restriction should or should not be imposed. This section uses a similar functional form for demand estimation to create an apples to apples comparison with the above elasticity results. There are some good economic reasons to relax these restrictions as discussed below, but KY likewise have compelling reasons to impose these restrictions.

My demand system methodology largely follows KY, with some important distinctions. For each investment institution in every month, I have the following demand function:

| (15) |

where is the portfolio weight of institution in asset at time . Note that is asset-specific while and are not. There are three important terms in the equation: the intercept, the price level term, and the log price term as labeled above.

Following KY, this demand function is specified only for the assets in the fund’s investment universe, which is the investment mandate or the set of assets a fund considers. Let equal one if asset is in the investment universe of fund at time , and zero otherwise. The dollar holdings of the asset for this institution are .

It follows that aggregate demand for the asset, in terms of portfolio weights, is:

| (16) |

where the , , and coefficients are defined as the terms in parentheses. Thus, all that is needed to fully describe the demand function for the aggregate market is these three parameters for each stock in each period.

I next describe the estimated demand function predictors. Then, I describe the motivation and justification for this demand function, which comes from KY. Following this, I discuss the estimation procedure and summarize the elasticity results from the estimation.

5.2 Demand Function Predictors

For the demand function estimation, it is useful to separate linearly into two components:

where is an exogenous component of the predictor and is constant across assets in a given period. A first order approximation in a given period would make the intercept term clearly an endogenous function of the asset’s own price. It is useful to use these demand function predictors, , because this allows us to separately instrument for the endogenous component using standard linear regression models. The results of the paper, including the counterfactual experiment results below, can be shown with similar results with these predictors as well. At times these can result with predictors that are outside of -0.5 and 0.5, potentially causing concerns that the models are not using properly normalized predictors and are thus disadvantaged. Thus we use different predictors for demand estimation than for the statistical arbitrage models.

For , I simply set equal to the median value of for each month and each predictor . In Appendix B.1, I show the closed-form solution for these derivatives. It should be obvious that

| (17) |

I simply use a regression to estimate the other two parameters. In particular, in every month for every predictor, I run the following cross-sectional regression:

| (18) |

where and are OLS regression estimates, and is described as follows. It can be thought of as the predictor with the market equity stripped out with only the exogenous component remaining. I calculate where is the very same as the raw predictor , except instead of using the market equity of the asset at time , the median market equity across stocks that month is used. Following KY, where aggregate parameters across assets are exogenous,272727See equation (9) of KY, which has aggregate values that are assumed exogenous. This essentially corresponds to a model where the market-wide parameters are endogenous, and cross-sectional differences are the endogenized components of the model. This paper of course similarly investigates cross-sectional pricing as well. In this sense it is a partial equilibrium model, which is standard in cross-sectional theory and empirical papers. this essentially strips out the endogenous price component and leaves to be the exogenous predictors component of . This calculation is only done for the 15 endogenous predictors.

These regression estimates are then plugged to give the log-linearized predictor . Importantly, this procedure is only done for the 15 predictors that are a function of price. For the other 47 predictors, excluding the market weights predictor (), I simply set , where trivially and . For the market weight predictor, I just define .

Why is not estimated with the regression (i.e., put the on right-hand side of the regression)? This is for two reasons. First, the very point of calculating with the continuous function above is so that the marginal impact of a change in prices on is known. Thus, I do not need to do this again—the marginal effect is known. Second, this would create an endogenous regressor problem since prices are endogenous.

5.3 Motivation and Justification of the Demand Function

In this subsection, I briefly motivate this demand function written above. KY prove that with log utility and their functional form assumption for expected returns and the covariance matrix, portfolio weights are linear in an asset’s own predictors. This can be trivially extended to CARA utility (see Appendix B.3). While the details and assumptions of this demand function in Appendix B.3 largely follows KY, I just discuss the key points here.

KY go one step further beyond the linear demand that they derive and assume a specific parameterization of their parameters that transforms their demand function from linear to exponential-linear in predictors.282828KY have an exponential-linear demand function, except with an extra term that allows portfolio weights to be exactly zero for some assets. This means that ignoring these zero-weight cases, the log of portfolio weights is linear in predictors. I ignore this term just to simplify the notation. This is useful because 13F institutions only have to report long positions. An exponential-linear demand function mandates positive weights. I do not take this extra step, which keeps the demand function as a simple linear function of predictors with a great deal of flexibility.

To see this flexibility, note that the KY exponential-linear demand function can be written as:

| (19) |

where captures their exogenous predictors including their latent demand term, denotes their exponential-linear price coefficient, and . Comparing this to equation (15), it is clear that the demand function has a similar price level term, , as the KY demand function. However, the demand function includes the intercept term, , and log price term, , which allows the demand function to potentially capture higher elasticity values due to this increased flexibility.

Are there good reasons to use this more flexible demand function? I list the reasons below, however, these reasons should be carefully weighed against the discussion that KY provide for their restrictions.

The first reason that having this flexible functional form is beneficial is that having portfolio weights that are linear in predictors allows aggregation, which is useful for many applications, including modeling a representative investor and estimating demand from institutional data (e.g. 13F data) that aggregates multiple funds pursuing different strategies.292929For example, two institutions with exponential-linear demand functions do not together have an exponential-linear demand function unless some fairly strong assumptions are imposed.

Second, the 13F data are aggregated up to the institution level, and this demand function allows institutions to take short positions and have leverage. For example, Blackrock’s positions are reported across all funds in the 13F data. While Blackrock has many long-only funds, it also has long-short mutual funds. A linear demand function gives this flexibility.

The full demand function can be written as:

| (20) |

where the terms are regression coefficients and represents the error term or latent demand.

Connecting this back to equation (15), I can write:

| (21) |

I address one last important question: why should the demand function have both a coefficient on price and log price? The simple reason is that the statistical arbitrageurs have both terms, and thus we include both terms in these demand functions to determine how comparable estimated demand results are when a similar flexible functional form is used. Also, note that the linear term allows the demand function to fit index fund demand. If and , then fund is a market-weighted index fund. The parameter captures institution ’s proclivity to market-weight index. Also, the log term ensures that equilibrium prices in counterfactual experiments, as shown below, has non-negative prices. This captures the limited-liability positive-price aspect of stock markets that is necessary for reasonable counterfactual experiments.

5.4 Estimation

As KY discuss, there is some cause for concern that correlated demand shocks across investors will cause price impact, making endogenous. I follow their approach and use their same instrument for price. In order to calculate this instrument, I follow KY and calculate the investment universe in the same way: all stocks ever held in the previous 11 quarters.303030See KY for more details. Then the instrument for the price of institution is:

where is what the log market equity of asset would be if all other funds with asset in their investment universe held equal weighted portfolios.313131I can also define: as KY do, but I get very similar results. The extra one accounts for the ”outside asset” in their setting, they need to include because of their different function form. This simpler functional form does not require this. Following KY, I exclude households from the calculation of the instrument for the institutions in the data.

Thus, the first stage regression, which is estimated with standard OLS for every institution in every quarter, is

where the terms are regression coefficients and is the error term. The predicted value is used in the second stage regression.

KY have an exponential linear demand function estimated using GMM. Given this simpler functional form than KY, I can also estimate the first and second stage regression with OLS, which gives a two-stage least squares (2SLS) estimate of the betas. The second stage regression is given by equation (5.3) above, except that is replaced by and is replaced by . Note that the regression can also be estimated such that there are two first stage regressions to instrument and with the instruments and , but this yields similar results, is slightly more complicated, and deviates a bit more from KY.

Second, like KY, who constrain the coefficients on the log of prices to have well-behaved demand functions and equilibrium prices, I have similar constraints. In particular, I constrain and . This ensures that and for all assets, which when combined with a similar restriction on statistical arbitrageur demand is sufficient to ensure that a unique closed-form positive equilibrium price exists in the counterfactual experiments and investors have downward sloping demand. Like KY, this can be estimated with generalized method of moments (GMM). However, since this is just a standard linear regression with constraints, this is the same as just estimating a constrained OLS regression for the second stage regression, which is what I estimate.

Similar to KY, funds are grouped together if they have too few strictly positive holdings and the aggregate demand across the funds is estimated. KY groups firms together if there are less than 1,000 observations. My estimation procedure does not have the same convergence issues, so I group funds together if they have less than 500 strictly positive holdings. I group firms together with similar predictors, using the same procedure as KY.

The 13F data only has strictly positive holdings. I estimate the model with only these holdings for each institution, which means that the sample is truncated. In other words, the short and zero asset positions that a fund has are not in the sample. Data truncation is not a problem unless there are sample selection issues between the truncated and non-truncated sample. However, even if there are sample selection issues, the short and zero asset positions are grouped into "household" demand. Like in KY, this household demand captures short positions. However, the model aggregates nicely, and it is fine to estimate a demand function of investors with very different beliefs and preferences as long as demand can be captured with this more flexible functional form.323232Note that there are some assets that were held by a fund in the previous three years, but are no longer held by the fund. These assets in the investment fund could be included as zeros in the institution-level regressions. This would require an assumption that the true asset position is actually zero or negative and that the investment universe is measured correctly for these assets. While the investment universe is not measured perfectly as KY discuss, it is more problematic for these assets than for the instrument calculation. The instrument calculation should average some of the error out. Including these extra zeros in the regression also requires a censored data approach, such as a Tobit regression. A second stage estimated with a Tobit model or Censored Least Absolute Deviations (CLAD) model from Powell (1984) yield similar results. I present the simpler version here where these zero asset positions are not added to the regression.

In conclusion, I highlight the major two ways this demand estimation differs from KY. First, I have a simple and flexible linear-in-predictors functional form for the portfolio weights, rather than exponential-linear. Second, I use a broader set of predictors from the Freyberger et al. (2020) data.

Note from equation (5.1) that differences in price elasticity for any asset are driven by the differences in what funds have that asset in their investment universe. KY note "that institutions hold a small set of stocks and that the set of stocks that they have held in the recent past (e.g., over the past 3 years) hardly changes over time." The calculation of the investment universe and instrument relies on this fact. Thus, it is relatively mild to impute the investment universe, price level coefficient, and log price coefficients to funds for the two months following the quarterly 13F holdings data.333333The price level coefficient is while the log price coefficient is . The aggregate intercept term, , is pinned down by the equilibrium condition, , combined with equation (5.1). Thus, only the investment universe, the price level coefficients, and the log price coefficients need to be imputed. I impute these values, which allows analysis of portfolio returns at the standard monthly frequency with the counterfactual experiments below. This is very different from the problematic assumption that institutions hold the same portfolio weights for the following two months, which I do not assume.

5.5 Results

I first define the elasticity values with the above demand functions, and then summarize the estimated elasticity values.

The elasticity of institution for any asset with a positive portfolio weight,343434KY also define elasticity only for assets with strictly positive weights. using equation (1), can be calculated as:

| (22) |

If and , then the elasticity is zero. Just as there is a level term and log term in equation (15), this equation has the corresponding elasticity effects of these two terms. Note that the inclusion of the log term allows potentially higher elasticity values than assuming that .

The elasticity of the aggregate market for any asset can be written as:

| (23) |

This aggregate elasticity is guaranteed to be positive.353535To see this, just note that in equilibrium, , and the estimation constraints guarantee that and .

| Row | Covariates () | Elasticity | Level term | Log term |

| (1) | All | 11.131∗∗∗ | 0.574∗∗∗ | -10.705∗∗∗ |

| (0.401) | (0.003) | (0.401) | ||

| (2) | Only Level | 0.345∗∗∗ | 0.655∗∗∗ | |

| (0.002) | (0.002) | |||

| (3) | Level & KY | 4.314∗∗∗ | 0.347∗∗∗ | -3.661∗∗∗ |

| (0.159) | (0.005) | (0.158) | ||

| (4) | Level, KY, & Exog | 8.265∗∗∗ | 0.616∗∗∗ | -7.882∗∗∗ |

| (0.323) | (0.002) | (0.322) | ||

| (5) | Level, KY, & Endog | 49.563∗∗∗ | 0.514∗∗∗ | -49.078∗∗∗ |

| (2.638) | (0.004) | (2.637) | ||

| Obs. | 1,620,817 | 1,620,817 | 1,620,817 | |

| Months | 489 | 489 | 489 | |

| Note: | ∗p0.1; ∗∗p0.05; ∗∗∗p0.01 | |||