Fast exact simulation of the first passage of a tempered stable subordinator across a non-increasing function

Abstract

We construct a fast exact algorithm for the simulation of the first-passage time, jointly with the undershoot and overshoot, of a tempered stable subordinator over an arbitrary non-increasing absolutely continuous function. We prove that the running time of our algorithm has finite exponential moments and provide bounds on its expected running time with explicit dependence on the characteristics of the process and the initial value of the function. The expected running time grows at most cubically in the stability parameter (as it approaches either or ) and is linear in the tempering parameter and the initial value of the function. Numerical performance, based on the implementation in the dedicated GitHub repository, exhibits a good agreement with our theoretical bounds. We provide numerical examples to illustrate the performance of our algorithm in Monte Carlo estimation.

Key words: exact simulation; subordinator; first passage of subordinator; overshoot and undershoot of a subordinator; complexity.

AMS Subject Classification 2020: 60G51, 65C05 (Primary); 62E15, 60E07 (Secondary).

1 Introduction

The study of the first-passage event across a barrier is a classical subject that has long been of interest for many stochastic processes, including Lévy processes. For instance, first-passage events describe the ruin event (i.e. the ruin time and penalty function) in risk theory [doi:10.1142/7431, Ch. 12], are used to describe the law of the steady-state waiting time and workload in queuing theory [MR1978607] and arise in the probabilistic representation of the solutions to fractional partial differential equations (FPDEs) (see e.g. [hernandez2017generalised] and the references therein), as well as in financial mathematics (in payoffs of barrier-type derivative securities). In all such areas, simulation algorithms and Monte Carlo methods are of great interest and widely used (see [MR2331321, Ex. 5.15]). However, direct biased Monte Carlo methods, based on random walk approximations of the crossing time, may lead to errors that are often difficult and computationally expensive to control, see e.g. Subsection 3.3.1 below. Fast exact simulation of the crossing time of a level by a subordinator is thus needed for a stable Monte Carlo algorithm in these contexts. For example, in [MR4219829], exact simulation of the first-passage time of a stable subordinator was used to solve numerically an FPDE with a Caputo fractional derivative [MR2854867]. Generalising [MR2854867] beyond Caputo fractional derivatives requires an exact simulation algorithm for more general subordinators, along with an a priori bound on its expected running time. The exact simulation algorithm in [chi2016exact], applicable to a broad class of subordinators, typically turns out to have an infinite expected running time (see Subsection 2.7 below), making it hard to exploit the general algorithm in [chi2016exact] in this context.

The present paper develops an exact simulation algorithm for the first-passage event of a tempered stable subordinator across a non-increasing function, such that its random running time has finite exponential moments with explicit (in terms of model parameters) control over the expected running time. While our algorithm is widely applicable to problems in applied probability discussed above when the underlying model is a finite variation tempered stable process (cf. [MR3500619] for examples in financial mathematics), our main interest in this algorithm stems from our aim to generalise [MR4219829] to tempered fractional derivatives and possibly, in future work, to more general non-local operators using ideas from [chi2016exact, MR4122822].

1.1 The complexity of the main exact simulation algorithm

A subordinator (where ) is a non-decreasing process with independent and stationary increments and right-continuous paths, started at zero . It is well known that , where is a non-negative drift parameter and the (positive) jumps form a Poisson point process with mean measure on , where is the Lévy measure of , satisfying (see details in [ken1999levy, Def. 8.2]). In this work we consider a driftless tempered stable subordinator : and for some (fixed) , and . The first-passage event of is described by the random element

is the first crossing time of over a non-increasing absolutely continuous function , with . Since , we have almost surely and the variable , referred to as the undershoot in this paper, gives the position of the subordinator just before it crosses the function . The position of the subordinator at first crossing time over is given by . TSFFP-Alg below, which is the main simulation algorithm of this paper, samples from the law of the vector .

Denote by the (random) running time of our main algorithm TSFFP-Alg. Here and throughout we assume that elementary operations such as addition, multiplication and evaluation of elementary functions , , all have constant computational cost. Further, we assume all operations use floating point precision and denote by the desired number of precision bits of the output. Then has finite exponential moments (up to some order) and its mean is bounded above by

where the constant does not depend on , or (see Corollary 2.2 below). Moreover, can be made explicit in terms of the costs of elementary operations listed above.

Since the law of the vector degenerates in any of the limiting regimes, , , or , the deterioration in the performance of the algorithm in these regimes is expected. Indeed, the subordinator converges weakly to a linear drift as (see the stable characteristic function in (2.1) below), making the law of the undershoot increasingly harder to simulate from. If instead or , then the subordinator converges weakly to the trivial process for which the first-passage time is infinite. Finally, if increases, then the crossing time increases, extending the running time of several loops in the algorithm. The main point of the formula in the display above is that it provides an explicit insight into the deterioration of the performance of the algorithm in any of the limiting regimes. There is a good match between this theoretical upper bound on the performance and what we observe through the implementation found in the repository [repository], see Subsection 3.1 below for details.

The key step in the exact simulation of the first-passage triplet for a general tempering parameter (TSFFP-Alg below) is the stable case , given in SFP-Alg below. The general case in TSFFP-Alg requires only an additional accept-reject step based on the Esscher transform described below. In turn, the simulation of the first-passage event of a stable process in SFP-Alg is essentially reduced to the simulation of the undershoot on the event when the first passage did not occur continuously (i.e. by creeping444Note that creeping occurs with positive probability when the boundary function is not constant, even though the tempered stable subordinator has no drift, see [https://doi.org/10.48550/arxiv.2205.06865, chi2016exact]., which occurs on the event , cf. Subsection 4.1 below). Sampling the undershoot efficiently, which turns out to be deceivingly hard (see Subsection 2.5 below), is the main technical contribution of this paper. Although the density of the undershoot , conditional on , admits a semi-analytic explicit form (see (4.5) below), it is unbounded and does not lend itself well to direct accept-reject methods. Our main strategy to circumvent this issue is to break up the state space of into subintervals, depending on the values of the (possibly random) parameters, and on each subinterval use an appropriate accept-reject algorithm. The algorithm in [devroye2012note], see LC-Alg in Appendix LABEL:sec:devroye below, plays a key role precisely in the subinterval where the density of decreases sharply from a very high value to super-exponentially small values, making the standard accept-reject bounds hard to find.

Most algorithms developed and used in this paper are based on a combination of two components: (I) a numerical search step in the form of binary search (also known as the bisection method), possibly followed by an application of the Newton–Raphson method (rigorous care is taken to verify the assumptions that guarantee quadratic convergence of the Newton–Raphson algorithm) and (II) rejection (or accept-reject) sampling. For both components, we do a careful complexity analysis accounting for all computational operations. This is crucial because parameter values themselves are often random, requiring control over their distribution as well as the impact on the computational complexity when these random parameters take extreme values. Note that the infinite expected running time of the algorithm in [chi2016exact] arises essentially due to an accept-reject step having a random acceptance probability with large mass close to zero, see Subsection 2.7 below for details.

1.2 Comparison with the literature

Exact simulation of the first-passage event of a tempered stable subordinator is a central topic of two articles: [chi2016exact] and [MR4122822]. [chi2016exact] was the first to develop a simulation algorithm for the first-passage event for a wide class of subordinators over a general non-decreasing absolutely continuous boundary functions . The case of the tempered stable subordinator plays a prominent role in [chi2016exact], because the entire general class of subordinators considered in [chi2016exact] can be viewed as a modification of the tempered stable case. Indeed, the main algorithm in [chi2016exact] relies on this structure. As discussed above, the algorithm for the tempered stable first-passage event in [chi2016exact] typically has infinite expected running time (see Subsection 2.7), making it hard to use in Monte Carlo estimation.

[MR4122822] consider a tempered stable subordinator and a constant function . They develop an exact simulation algorithm [MR4122822, Alg. 4.1] for the pair . In this case, the problem is first reduced to the stable case via the Esscher transform. Then the constant barrier makes the density of explicit with a stable scaling property. The scaling property in turn allows for a change of variables (in the form of the variable in [MR4122822, l.11, §4.2]) that makes it easy to sample from the resulting density. This technique, which depends on the explicit density of the random vector , does not generalise easily to a non-constant function , including a linear function with . Part of the difficulty in generalising such methodology is that a new possibility arises: the subordinator may creep (i.e. cross continuously [https://doi.org/10.48550/arxiv.2205.06865, chi2016exact]) through the curve , in which case . Moreover, the probability of creeping is not uniform in time even for linear functions (see Proposition 4.1(b) below), making it hard to compute even the mass of the absolutely continuous component of the joint law.

1.3 Organisation of the paper

The main algorithms and the results on their respective computational complexities are provided in Section 2. In Section 3 we present numerical evidence for the theoretical bounds on the computational complexities of our algorithms. We also present two numerical applications of our simulation algorithms, using Monte Carlo estimation, to solve fractional partial differential equations and to price barrier options. The GitHub repository [repository] contains the implementation (in Julia) of the algorithms in this paper, used in Section 3. Finally, the proofs of all our results on the validity and computational complexities of our algorithms are given in Section 4. See [Presentation_Jorge] for a short YouTube presentation on Prob-AM channel discussing the algorithm.

2 Sampling the first passage of a tempered stable subordinator

For any stability index , intensity and tempering parameter , let be, under (with expectation operator ), a driftless tempered stable subordinator started at with Laplace transform and Lévy measure

| (2.1) |

Note that, under , is a stable subordinator with Lévy measure .

2.1 Dependence of the algorithms for the simulation of under

Figure 2.1 above summarises the dependence between the algorithms used to simulate the triplet for the tempered stable subordinator . Algorithm TSFFP-Alg essentially reduces the problem to the same problem in the stable case, dealt with by SFP-Alg. The hardest step of the stable first-passage algorithm SFP-Alg consists of the simulation of the undershoot , performed by SU-Alg, which in turn relies on -Alg and -Alg. These two rejection-sampling algorithms are tailored to the specific densities and that arise in our problem (see Proposition 4.2 for the definition). Upon noting that a certain function (related to ) is log-concave, -Alg essentially only calls LC-Alg, a very fast rejection-sampling procedure for log-concave densities. -Alg requires a partitioning of the state space, which relies on numerical inversion of elementary functions, and finely tuned rejection sampling. The details are given in the remainder of this section.

2.2 Sampling the first passage of a tempered stable subordinator

Before presenting our simulation algorithm TSFP-Alg, we give a brief intuitive account. The measures (for ) are known to be equivalent to each other (see Appendix LABEL:app:temper). In fact, the law of the trajectory (for any ) under is equal to the law under weighted by the change-of-measure . Since this change-of-measure is bounded, it can be used for rejection sampling of under : propose a path on under and accept it with probability , which is on average equal to , see Lemma LABEL:lem:tempered_law in Appendix LABEL:app:temper below for details. Thus, it is natural to expect that the simulation of the first-passage triplet under can essentially be reduced to the case on the stochastic interval . However, since may have unbounded support, the change-of-measure may also be unbounded, making a direct rejection-sampling algorithm for infeasible. TSFP-Alg makes use of the change-of-measure idea by introducing a time grid and sampling on the grid until the compact interval in which lies is identified.

TSFP-Alg makes use of S-Alg and TS-Alg, well-known simple and fast procedures for sampling stable and tempered stable marginals, respectively (see Appendix LABEL:app:temp_stable_marginal below). In lines 2–7, TSFP-Alg consecutively samples (and stores the value in ) over the grid (i.e., the variable keeps track of time) under the tempered stable law until the interval containing is identified, i.e., the smallest with . When the interval containing under is identified, in lines 8–11, TSFP-Alg samples under via rejection sampling: it proposes and under , and accepts the sample (under ) with probability . The parameter affects the following three components of TSFP-Alg: the number of iterations of the loop in lines 2–7, the complexity of SFP-Alg called in line 9 (cf. Theorem 2.3 below) and the acceptance probability in line 11. The choice of in line 1 of TSFP-Alg is made to control the overall complexity of the algorithm, see details in (4.28) of Section 4 below.

Stable First-Passage algorithm SFP-Alg and its analysis constitute the main technical contribution of this paper. The complexity of TSFP-Alg is given in the following theorem. Proofs of all the results in this paper are in Section 4 below.

Theorem 2.1.

The upper bound on the running time of TSFP-Alg has a term of order , which may be quite large if either , or are large. However, the exponential dependence on these parameters of the complexity of TSFP-Alg can be easily turned into a linear dependence (see Corollary 2.2) by picking a constant and applying TSFP-Alg successively with the boundary function until the initial boundary is crossed. Our main algorithm TSFFP-Alg, which we now describe, does precisely this. Indeed, variables and , introduced in line 1 of TSFFP-Alg keep track of time and the value of at this time. Line 3 of TSFFP-Alg, samples under via TSFP-Alg, where . The algorithm updates and in line 4. If (line 5), then , the algorithm stops and returns the triplet in line 6; otherwise (i.e., if ), it repeats from line 2. The choice of in TSFFP-Alg is fixed in line 1 and is chosen to minimise an upper bound on the expected running time of the algorithm, see details in Section 4 below.

2.3 Sampling the first passage of a stable subordinator

The algorithm SFP-Alg for sampling under the stable law is based on the formulae in Proposition 4.1 below, describing the law of under . Before presenting SFP-Alg, we give a brief account of its contents. First, SFP-Alg samples the crossing time of the stable subordinator, conditional on , in line 1 and stores its value in the variable . The algorithm then determines in lines 2 & 3 whether the crossing occurred via a jump of positive size or continuously (i.e., by creeping, with ). In the latter case, the algorithm simply returns the crossing triple (line 4) and, in the former, the algorithm samples the undershoot and the overshoot and returns the triplet (lines 6–8).

Theorem 2.3.

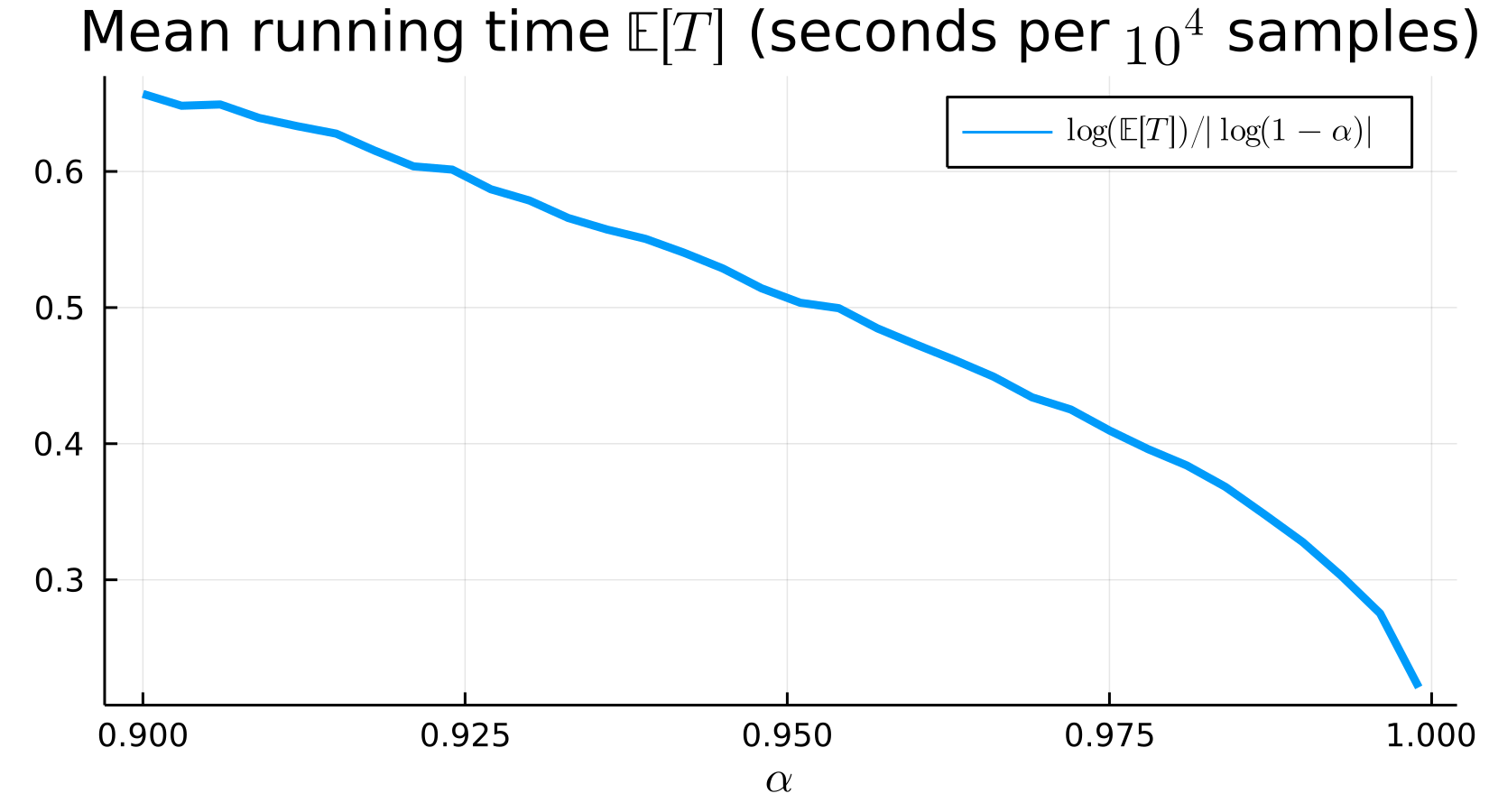

The proof of Theorem 2.3 is in Section 4.4 below. If , then , and Theorem 2.3 implies that the expected running time of SFP-Alg may increase as fast as as . A deterioration in the limit as is expected since, in this limit, the stable subordinator converges to a pure-drift subordinator , for which the distribution of the triplet degenerates to a delta distribution. Similarly, the expected running time of SFP-Alg may increase as fast as as . This is expected as well since the stable subordinator converges to the trivial process as . Numerical evidence for these increases in complexity and the theoretical bounds in Theorem 2.3 can be found in Section 3.1 below. We stress that existing algorithms for the simulation of the triplet have infinite expected running time for any , see Subsection 2.5 below for more details.

As we said before, SFP-Alg has three main steps. First, the algorithm generates the first-passage time in line 1. This requires evaluating, up to bits of precision, the inverse of the function , which is defined on where . This step may require a numerical inversion of (or, equivalently, numerically finding the root of ). Such algorithms are standard in the literature (see Appendix LABEL:sec:NewtonRaphson), making this a simple step. Second, the algorithm determines if the first passage occurred continuously (i.e., by creeping) in line 3. If the process crept, the triple equals , but, if it did not, then we must sample the undershoot and overshoot of the process conditional on the crossing time. The third main step is precisely the simulation of the undershoot and overshoot in lines 7 and 8. By Proposition 4.1, the conditional law of the overshoot is a power law and hence easy to sample from, while the law of the undershoot, although expressible in terms of the stable law and Lévy measure, is complicated and hard to sample from. For this reason, the focus of the remainder of this section is to construct SU-Alg, which samples from the law of the undershoot.

2.4 Simulation of the stable undershoot via domination by a mixture of densities

Our main objective now is to present a simulation algorithm from the undershoot law , , that is, the law of under , conditional on . Our main tool is the general rejection-sampling principle. Unlike before, the tools and algorithms used here have little probabilistic interpretation and are mostly based on analytical properties and inequalities. The derivation of these inequalities, which validate SU-Alg, will be developed and explained in Section 4 below. For now, we only present the algorithms with a brief description of how it works. The algorithm has several nontrivial components that we will slowly introduce and explain. The reason for this is that the task of simulating from the undershoot law comes with multiple pitfalls, with several tempting approaches having severe problems, see Subsection 2.5 for an account of these pitfalls.

First, the density of involves the density of the stable law, which can be written as a non-elementary integral of elementary functions (see Proposition 4.1). Thus, by extending the state space and applying an elementary transformation, the problem is converted into producing samples from a density proportional to on , where , and is the convex function defined in terms of trigonometric functions in (4.2). The density is difficult to sample from directly, so we first bound it with (and propose from) the mixture of two simpler densities and on , which are respectively proportional to and (see details in Subsection 4.3 below).

SU-Alg proposes from the mixture in lines 2–8 and accepts the sample with probability proportional to . Lines 3 & 4 of SU-Alg decide whether the sample from the mixture will come from (sampled in line 5) or (sampled in line 7). The simulation algorithms corresponding to the simpler densities and will be discussed later.

Remark 2.1.

The proportion (and hence ) can be efficiently evaluated to arbitrary precision using Gauss–Legendre quadrature. In fact, the numerator in the formula in (4.9) equals the distribution function of a stable law while the integrand in the denominator is a convex geometric combination of the integrands of the density and distribution functions of a stable law. The computation time for is thus assumed to be constant for any , and to only depend on the number of precision digits , see fast algorithms in e.g. [nolan1997numerical, ament2018accurate]. The error of the quadrature is known to decay exponentially fast in the number of nodes but may also be sensitive to large values of the high order derivatives of the integrand [4272861]. In our case, the derivatives of the integrand also grow quickly in the order of differentiation, implying a locally large relative error in the numerical integral. Since, however, these derivatives are large precisely when the function is nearly vanishing, the overall relative error appears to be small, resulting in a complexity that is only a function of the precision , as has been confirmed many times in the literature and by our own simulation times, see Section 3.1 below.

Remark 2.2.

Line 7 of SFP-Alg calls SU-Alg on random input, making the parameter in SU-Alg equal to (where is as in SFP-Alg), which follows the stable law of conditioned on . In particular, the density of is proportional to the restriction to of , defined in (4.3), making heavy tailed and its law dependent only on and .

For any , define .

Proposition 2.4.

The proof of Proposition 2.4 is given in Subsection 4.3.4 below. In the following two subsections we describe how to sample from the laws given by the densities and .

2.4.1 Simulation from the density .

The density is proportional to

The first factor (the marginal of the second component) is proportional to a log-concave density and can be sampled easily via LC-Alg by virtue of being log-concave (by Lemma 4.3 established below). The second factor (the conditional density of the first component given the second) is a shifted exponential with shift and scale , which is also easy to sample.

Proposition 2.5.

The proof of Proposition 2.5 is given in Subsection 4.3.1 below. -Alg does not rely on numerical inversion (cf. NR-Alg). Its expected running time does therefore not depend on the number of precision bits . In fact, the computational complexity of -Alg primarily comes from the pre-processing step (line LABEL:line_find_a_1 of LC-Alg), which depends on the values of the parameters in -Alg.

2.4.2 Simulation from the density .

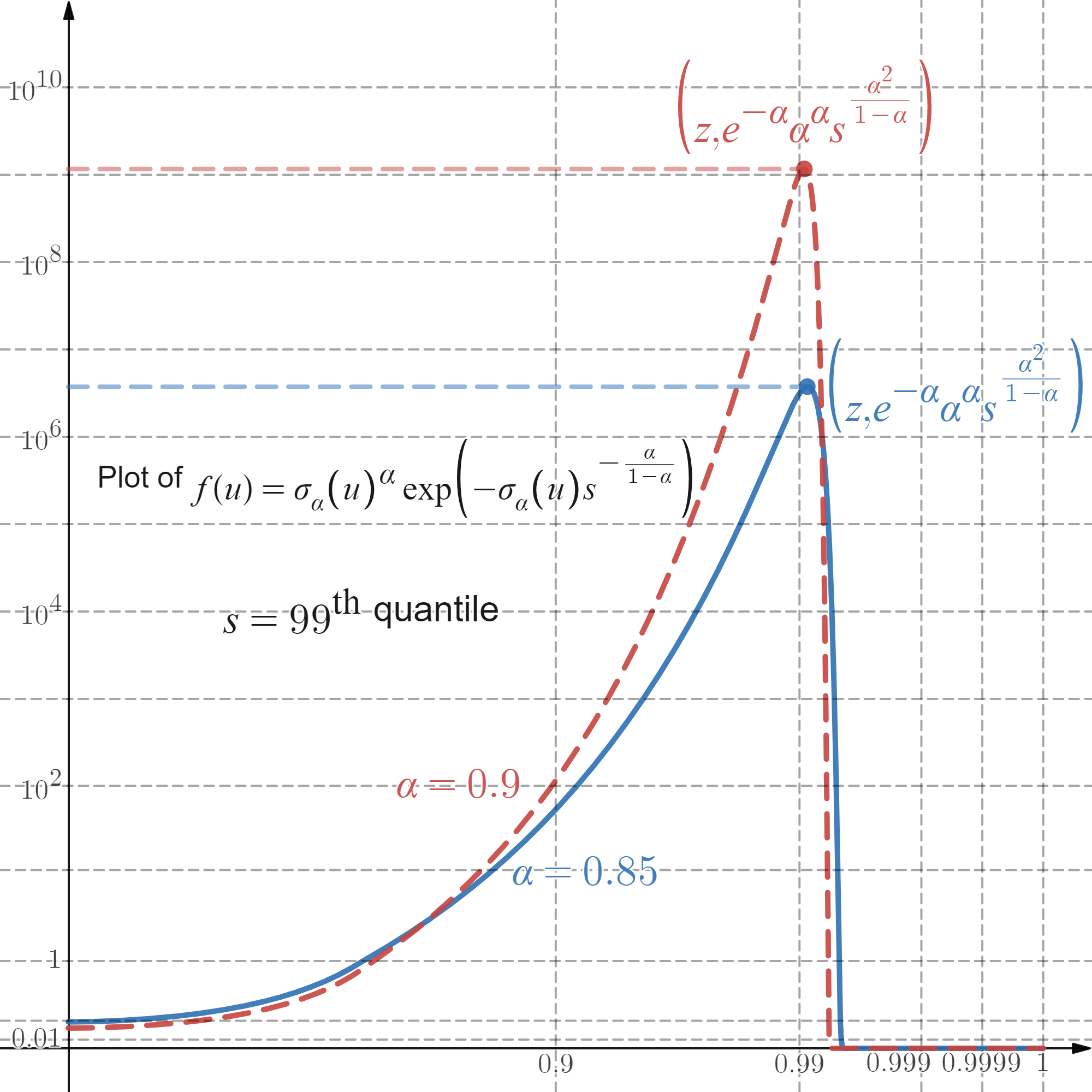

Simulating from the density is a delicate matter, particularly because of the sensitivity of the function on and on , which is heavy-tailed in line 7 of SFP-Alg (see Remark 2.2 above). -Alg below samples from the density , proportional to , in two steps. The algorithm first samples, in lines 1–25, the second marginal of , with density proportional to on . Then, the algorithm samples, in line 26, the first marginal conditionally given the second, with conditional density proportional to on , which is simply a translated (by ) gamma random variable with shape and scale and hence easy to sample from. The simulation from the second marginal density is done by breaking up the support depending on the parameters and and using rejection sampling with respect to various dominating (proposal) densities on each subinterval. Finding appropriate dominating functions, from which we can sample, is hard since the function may have a very large peak at level followed by a extremely steep descent to , even for reasonable values of , if the parameter (recall is heavy-tailed, see Remark 2.2 above) takes moderately large values. Figure 2.2 below illustrates how peaked the corresponding density may be in such cases.

The figure shows the graphs of the density of the second marginal of , in a custom logarithmic-style scale, for two processes with and , where the parameter is at its quantile. Thus, on average in one of every runs of SFP-Alg, -Alg is called to sample from a density which, at the mode , takes extremely large value followed by a steep drop towards zero. Moreover, in this case the density is strictly increasing on the interval and strictly positive on . But since its derivatives of all orders are equal to zero at , the graphs appear to be equal to zero on most of the interval . Furthermore, the behaviour of the density on either side of the mode is markedly different. Taking a uniform upper bound would result in an extremely inefficient algorithm with infinite expected running time (in fact, such a bound was used to sample from this type of function in [chi2016exact], see Subsection 2.7 below). For parameter values as in the graph above, -Alg sets , splits the interval and uses appropriate proposal densities on each subinterval.

-Alg needs to numerically invert several twice differentiable functions to produce samples of certain dominating (proposal) densities. This inversion is achieved via the Newton–Raphson root-finding method given in NR-Alg. Each call of NR-Alg requires the input of a specific target function and an auxiliary function satisfying (LABEL:eq:newton_raphson_auxiliary) (see Appendix LABEL:sec:NewtonRaphson).

Remark 2.3.

Proposition 2.6.

-Alg samples from the law given by the density . Moreover, the running time of -Alg is bounded above by a constant multiple of

where specifies the number of precision bits of the output and is a geometric random variable with probability of success bounded below by a multiple of . In particular, the running time of -Alg has exponential moments and its mean is bounded by

where the constant depends neither on nor .

The proof of Proposition 2.6 is given in Subsection 4.3.3 below. The computational cost in -Alg comes from various sources: (I) applications of the inversion NR-Alg, which may depend on the parameters and (recall that the parameter is in fact random in SU-Alg, which calls -Alg); (II) in the cases and , we also perform an accept-reject step where the acceptence probability depends on the parameters and ; (III) in the case , the pre-processing (line LABEL:line_find_a_1 in LC-Alg) also adds to the final computational complexity since the function LC-Alg is applied to in line 6 of -Alg depends both on and . We note that the accept-reject step in the case is embedded in LC-Alg and has uniformly bounded (in parameter values) expected running time.

2.5 How not to sample the stable undershoot

At a glance, there are several apparently feasible ways to produce a sample from the undershoot law of , under , conditional on . However, most of these simulation methods are either infeasible altogether or their computational complexity grows rapidly as either or . In this section, we will briefly discuss some of these “approaches”.

First recall that sampling from the undershoot law is, by Proposition 4.1(c), essentially reduced to producing samples from the density proportional to where and is the density of and given in (4.3). A first guess would be to employ rejection sampling on this density. Indeed, since the function is unbounded, we cannot propose from the density . However, the density is bounded and hence we may propose from the density proportional to and accept the sample with probability proportional to . For a fixed , this algorithm has a running time with finite mean; however, we require an algorithm that performs well for . Since puts most of its mass close to (which is stable distributed and thus heavy tailed), the acceptance probability of such an algorithm is asymptotically equivalent to as for some . In turn, this means that the running time is bounded below by , for some , which does not have a finite mean (in fact, it has a finite moment if and only if ).

Another possibility would be to perform a numerical inversion of the distribution function proportional to . Since

where can be computed to arbitrary precision using numerical quadrature, one may expect Newton–Raphson’s method to perform well in inverting numerically. It is, however, computationally intensive. Every step in Newton–Raphson method and in the binary search required prior to the quadratic convergence of Newton–Raphson’s method evaluates the double integral in (recall that is itself given in terms of an integral). If the numerical quadrature for computing accurately requires nodes, the corresponding quadrature for needs approximately nodes. Since we typically have for double-precision floating-point numbers, each numerical evaluation of requires evaluating at least functions (sums, products, exponentiation and trigonometric functions). This makes this approach infeasible despite the good properties of Newton–Raphson method and the boundedness and smoothness of the function .

A third option is to maintain parts of our current methodology and modify the parts of the algorithm that sample from a density of the form for some . For instance, one may attempt a rejection-sampling algorithm via elementary bounds on , such as those found in Lemma 4.9 below. Such algorithms are feasible and, in fact, we use some of them for certain parameter combinations. The drawback of those approaches is that the acceptance probability becomes tiny as , which is why we introduce the auxiliary parameter and other simulation algorithms for certain parameter combinations. Indeed, the acceptance probability is often upper bounded by for some where we recall that . This probability is incredibly small even for moderate values of . For instance, the quotient between the lower and upper bounds on in Lemma 4.9 is proportional to , as , which is approximately (resp. ) when (resp. ).

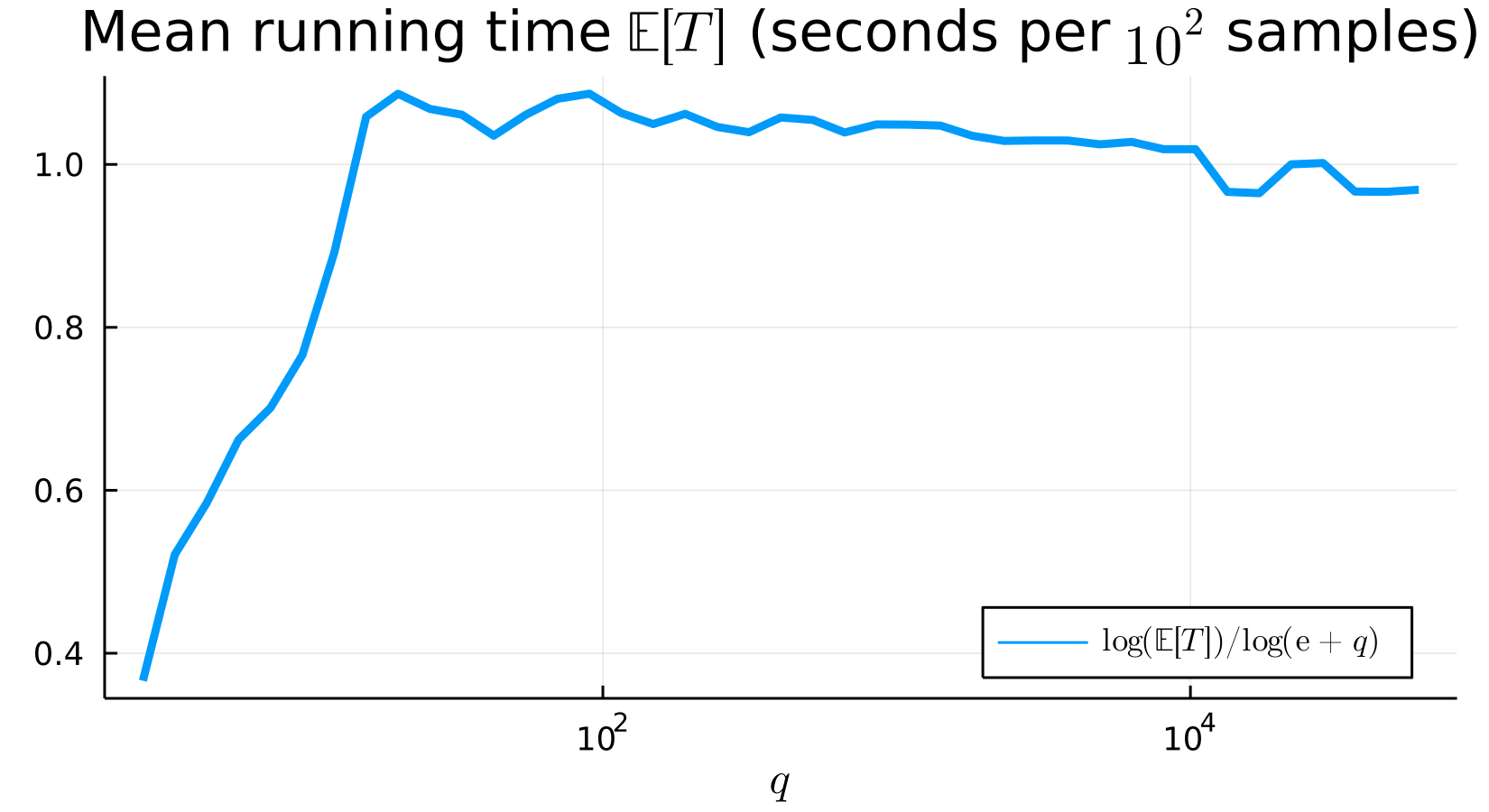

Our SU-Alg (and its subalgorithms) are in fact informed by the pitfalls described above. In particular, the choices made in -Alg may appear arbitrary but are, in fact, designed to control the computational complexity. It remains an open problem to design an exact simulation algorithm with uniformly bounded expected running time on the entire parameter space . Figure 1(b) below appears to suggest that the complexity of our algorithm grows as as , which is much smaller than , as suggested by our theoretical bounds.

2.6 Simulation of and via numerical inversion with numerical integrals

It is natural to enquire555We thank an anonymous referee for drawing our attention to this questions. about the performance of a simulation method based on a direct numerical inversion of the distribution functions corresponding to the marginals and . Using direct numerical inversion via Householder’s method with (see H-Alg in Appendix LABEL:sec:NewtonRaphson below), we can sample from these marginals of and .

Recall that -Alg requires no numerical integration, while -Alg uses 3 such integrations (see line 4), each over an interval where the integrand is monotone. In contrast, since every step of H-Alg evaluates the distribution function, the numerical integration is used much more extensively over regions where the integrands are not monotone. Thus the direct inversion method is more sensitive to large values of the number of precision digits and to instabilities in the numerical integration appearing for such large .

We compared numerically the outputs of -Alg and -Alg with the outputs of their direct inversion counterparts: Figure 2.3 shows that our algorithms and the direct inversion alternatives sample from the same laws. We found that algorithms -Alg and -Alg were on average approximately and times faster, respectively than the direct inversion alternatives over the range of .

The graph on the left (resp. right) show the function where and are the empirical distribution functions of the samples produced using -Alg (resp. -Alg) and direct numerical inversion, respectively, for . Such functions indeed resemble Brownian bridges time-changed by the corresponding distribution functions. All samples pass the two-sample Kolmogorov-Smirnov test, confirming that our algorithms and direct numerical inversion produce samples from the same laws.

2.7 Infinite expected running time of the algorithm in [chi2016exact, §7]

In [chi2016exact, §7], an algorithm that produces a sample of the first-passage triplet of a tempered stable process is given. Such an algorithm has almost surely finite running time. However, it can be seen as follows, that its expected running time is infinite.

Suppose for simplicity that and is bounded by the variable denoted by in the algorithm in [chi2016exact, §7]. Consider Step 3 of the algorithm in [chi2016exact, §7], which uses rejection sampling to simulate the pair given (recall from Proposition 4.1 that , where is the inverse of ). The proposal for is for some , with acceptance probability , where is an auxiliary variable, and is a global bound on . Thus, the expected runnig time of this step equals , where and the variables , and are independent. Hence, recalling that , we have

| (2.2) | ||||

However, if and only if by (4.26) below. Since for all , the expected running time of the algorithm in [chi2016exact, §7] is indeed infinite.

We note that, similarly, Step 5 of the algorithm in [chi2016exact, §7] also has infinite expected running time. Since Step 5 is more complex than Step 3, we made the phenomenon above explicit only for Step 3.

2.8 Can an implemented simulation algorithm be exact?

The answer depends on the definition of exact simulation. Since our algorithms are implemented inside computers with finite resources, the output of any algorithm cannot have the same law as the variable it is simulating if the variable has a density. However, we may consider an algorithm to be practically exact if a chosen distance between the law of the ideal variable and the algorithm’s output can be controlled within a given multiple of machine precision (see Appendix LABEL:app:exact for further discussion of this question and various natural suggestions for the distance). Our algorithms are practically exact with respect to the Prokhorov metric (which metrises weak convergence) because we can create a coupling under which, with high probability, the distance is bounded by a constant multiple of machine precision, and this multiplicative constant is only dependent on the parameters and , see details in Appendix LABEL:app:exact below.

3 Applications

The main objective of this section is to present some applications of our algorithms. First, we present some numerical evidence for the theoretical bounds on the expected running time of TSFFP-Alg and SFP-Alg. We then show how TSFFP-Alg can be used to sample the first-passage event of a two-sided tempered stable process, which in turn can be used to price barrier options via Monte Carlo. Next, we use the probabilistic representation of the solution of a fractional partial differential equation (FPDE) [hernandez2017generalised] along with TSFFP-Alg to produce Monte Carlo estimators of the solution of such a FPDE.

3.1 Implementation

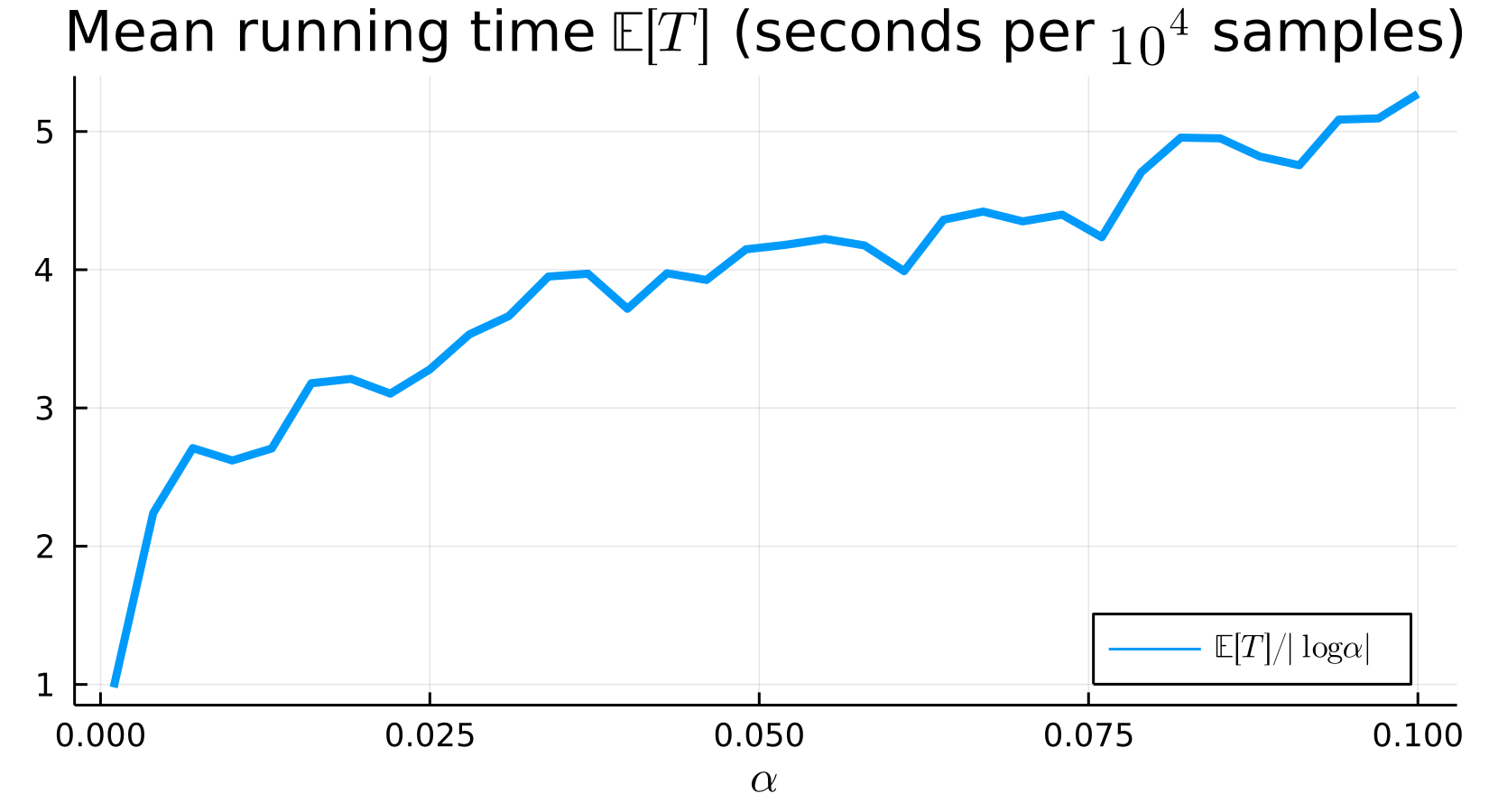

In this section, we showcase an implementation of our algorithms in Julia computing language. Our first goal is to show that such an implementation makes the simulation of the first-passage event feasible and fast in practice. Our second goal is to show that, in practice, our bounds on the expected running time of TSFFP-Alg and SFP-Alg overestimate the true complexity.

The average time is measured in seconds taken for every samples.

Observe that the expected running time in Figure 1(b) appears to be smaller for (close to ) than for (close to ). Although this is surprising since our upper bounds are of order for large and of order for small , it is important to consider a few things. First, our key -Alg, used to simulate the stable undershoot, uses a very different simulation method for and for . In particular, the multiplicative constants in the notation can be significantly different. Second, the bounds in Theorem 2.3 are only bounds, and need not be sharp. In particular, this does not necessarily mean that the asymptotic cost as is truly smaller than the asymptotic cost as .

The behaviour of the expected running time of TSFFP-Alg, as a function of , is in good agreement with our upper bound in Theorem 2.1, see Figure 3.2 for details.

3.2 Extensions to Lévy processes of bounded variation

We start by recalling the algorithm in [chi2016exact, §5.1]. Let be a Lévy process with non-positive drift, such that its Lévy measure satisfies

Decompose as , where and are independent subordinators with Levy measures and , respectively, and where is driftless. Fix some and let . The following algorithm provides a method to simulate under the assumption that the first-passage triplets , where , as well as the increments and can be sampled for any and . Further consider some . According to [chi2016exact, Proposition 5.1], if either a.s. (which can be determined, e.g., via Rogozin’s criterion [MR4448688, Thm 2.7]) or , then BVFP-Alg below stops a.s. and it samples the triplet .

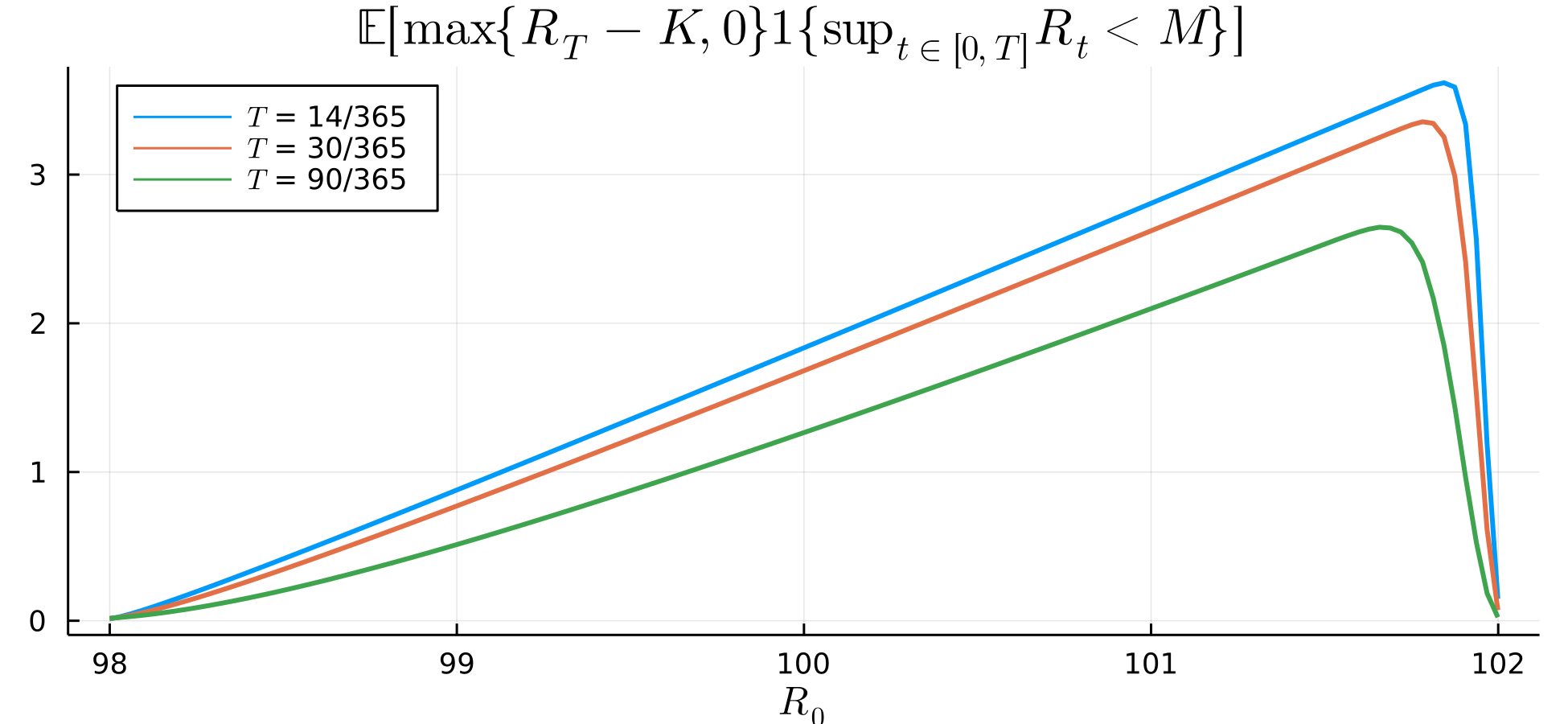

3.2.1 Pricing barrier options.

Let be a Lévy process of bounded variation started from and let , , model the risky asset for some initial value . The simulation of the first-passage event can be used to obtain Monte Carlo estimators of the price of a barrier option. Indeed, fix and consider the payoff of the up-and-out barrier call option with payoff

where and . Then the price of the option is given by , where is the discount rate.

Let , , be iid samples with the law of generated via BVFP-Alg. Then, for every , we consider the Monte Carlo estimator

of . Figure 3.3 shows such an implementation for the case where is the difference of two tempered stable subordinators. To obtain smoother graphs, we apply BVFP-Alg to successive values of the barrier level (i.e., by decreasing values of ), obtaining strongly correlated samples. This is a well-known procedure in Monte Carlo estimation that retains the accuracy of each estimate as if we had used independent samples for each value of , but reduces the random fluctuations between any two estimated values, see [MR1999614, §4.2].

We considered the time horizons and parameters , and . We assume where and are both driftless tempered stable subordinators with parameters and , respectively, as calibrated from the USD/JPY currency pair, see [MR3038608, Table 3].

3.3 Solution of fractional partial differential equations

Let be a continuous function that vanishes at infinity and . For , consider the following fractional partial differential equation (FPDE):

| (3.1) |

where is a generator of a Feller semigroup on acting on , , the operator is a generalised differential operator of Caputo type of order less than acting on the time variable . The solution of the FPDE problem in (3.1) exists and its stochastic representation is given by (see [hernandez2017generalised]):

where is the stochastic process generated by and where is the decreasing -valued process started at generated by . Note that is the first-passage time of the subordinator over the constant level .

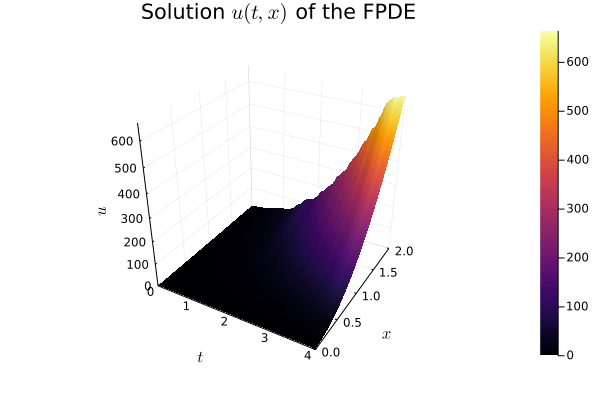

In the special case , , (where is the Laplacian on ) and the subordinator is tempered stable, we can simulate the Monte Carlo estimator

| (3.2) |

of the solution of the FPDE in (3.1). In particular, the variables are an iid samples of , obtained by TSFFP-Alg, while

where are iid standard normal random variables. Since is a geometric Brownian motion and TSFFP-Alg is exact, the variables in the estimator in (3.2) have the same law as . A plot of , based on samples, is presented in Figure 3.4. In this case, the dependence of the estimator for fixed (as a function of ) is explicit. The section of as a function of (for fixed ) is obtained by sampling consecutive crossing times for increasing barriers. This is a well-know procedure in Monte Carlo estimation that retains the accuracy of each estimate but reduces random fluctuations between the values of at consecutive time points and a given level by introducing correlation [MR1999614, Sec.4.2]. The spacing between values of (resp. ) where is evaluated in Figure 3.4 is (resp. ).

3.3.1 Comparison with a biased approximation.

We stress that being able to simulate exactly from the law of is essential for the stability of the estimator . It is tempting to simulate a random walk approximation (i.e. the skeleton) of the subordinator on a time grid with mesh and approximate the law of with the first time the random walk crosses level . Unlike , the estimator

is biased. Thus, in order for the -error to be at most , its bias and variance need to be of order and , respectively. In the specific case considered here, it is easy to see that, for fixed , the bias of is proportional to . In particular, the computational complexity of evaluating is proportional to , making the total complexity of proportional to . In contrast, the computational complexity of evaluating based on our exact simulation algorithm is proportional to . This yields an improvement in computational complexity proportional to .

The analysis outlined in the previous paragraph can be made precise for all Lipschitz functions . We note that, if is only locally Lipschitz (as is the case in the example above), the error of the naive random walk algorithm may deteriorate significantly as a function of . For instance, in the example above, the bias is proportional to , where (because stable paths dominate tempered stable paths) and, by Proposition 4.1(a) and (4.26),

Thus, the bias of the naive approximation is proportional to . This would require to be proportional to if the -error is to be smaller than . Thus, the improvement in computational complexity of over is proportional to .

We chose . Note has the law of the first-passage time of a tempered stable subordinator with parameters , , crossing level and is geometric Brownian motion with .

4 Analyses of the algorithms

For any and , let (where ) be the stable subordinator (for background on Lévy, including stable, processes see monograph [MR1406564]) with Laplace transform and Lévy measure

| (4.1) |

respectively, where ( denotes the Gamma function). The constant factor in the Lévy measure is chosen so that the Lévy-Khinchin formula for the Laplace exponent yields the desired Laplace exponent . Let be the tail function of the Lévy measure :

In particular, starts at zero, has zero drift and satisfies for all . Denote by the density of (for ). Introduce the functions

| (4.2) |

where . Note and hence . The density of can be expressed as follows [uchaikin2011chance, §4.4]: for any ,

| (4.3) |

In particular, the -th derivative exists on for any and satisfies .

4.1 Distribution of the first-passage event of a stable subordinator

The paths of are assumed to be right-continuous with left limits, where for we define . The jump at time is given by . The first-passage event for over a non-increasing, absolutely continuous function , with , is described by the random vector

| (4.4) |

is the crossing time of over the function and is the left limit of at the crossing time of . The size of the jump of at the crossing time may be zero with positive probability (i.e. it does not jump at time ) if is not constant. In this case we say that the subordinator creeps over .

Theorem LABEL:thm:joint_law, stated and proved in Appendix LABEL:app:proof_of_Thm_Joint_law below for completeness but originally established in [chi2016exact] (see also [https://doi.org/10.48550/arxiv.2205.06865]), describes the law of the triplet (and hence of (4.4), since ) for a general class of subordinators. In particular, as a consequence of (LABEL:subeq:joint_undershoot_law), the stable subordinator does not jump onto or out of the function at :

Note that, since is monotone and absolutely continuous, it is differentiable Lebesgue-a.e. on and its derivative is a version of its density. We denote its derivative by and, on the Lebesgue zero measure set where it is not defined, we set it equal to (arbitrary choice, without ramifications). The next proposition is key for the sampling of .

Proposition 4.1.

Let be a stable subordinator and a non-increasing absolutely continuous function with . Define (with convention ). The following statements hold.

-

(a)

, where is a strictly decreasing continuous function , with inverse . Hence, .

-

(b)

The probability of creeping at , conditional on at time , equals

-

(c)

Conditional on not creeping at the crossing time , we have

(4.5) (4.6)

Remark 4.1.

-

(i)

The representation of the law of in Proposition 4.1(a) is based on the scaling property of the stable subordinator . In particular, Proposition 4.1(a) implies that, at the crossing time of a stable subordinator over a boundary function , the law of the variable is stable for any non-increasing absolutely continuous function .

- (ii)

- (iii)

Proposition 4.1.

(a) By the scaling property of , note

for any .

(b) We claim that is absolutely continuous with density given by the function ,

| (4.7) |

In fact, , which is absolutely continuous since (and hence ) is absolutely continuous. Differentiating this identity in and applying the scaling property to the density yields

Since ,

the representation in (4.7) and (LABEL:subeq:creep_b) imply .

(c) By (LABEL:subeq:joint_undershoot_law) in Theorem LABEL:thm:joint_law, for and , we have

Thus, and

To evaluate the denominator, let us recall that is the density of . Together with (LABEL:subeq:creep_b) we have

Combining (4.7) we get and (4.5) follows. Also from (LABEL:subeq:joint_undershoot_law) we know that

and (4.6) follows. ∎

4.2 Simulation of the first-passage event of a stable process

The task is to justify the validity of SFP-Alg, which samples the triplet of the stable subordinator under . The analysis of its expected computational complexity has some technical prerequisites and will thus be deferred to Subsection 4.4.

By Proposition 4.1(a), has the same law as and can be sampled exactly in constant time (i.e. not requiring a random number of steps) via the widely used S-Alg given in Appendix LABEL:app:temp_stable_marginal below. Moreover, by Proposition 4.1(b), the probability of the stable subordinator creeping over the function (i.e. ), given , equals . SFP-Alg samples a Bernoulli variable taking the value with probability . If the Bernoulli equals , then, since the probability of jumping onto the function is zero , SFP-Alg returns . If, conditional on , creeping does not occur, SFP-Alg samples the undershoot from the law , given in (4.5) of Proposition 4.1(c), using SU-Alg given below. Then, conditional on , the jump size has by (4.6) the same law as , where is an independent uniform on . Thus, SU-Alg returns .

By the previous paragraph, for SFP-Alg to be valid, it suffices to justify that SU-Alg produces samples from the law of , which is described analytically in (4.5) of Proposition 4.1(c). Note that the simulation from the law via SU-Alg is the only step in SFP-Alg that has random running time. In fact, the design of SU-Alg is one of the main contributions of this paper and will be discussed in detail in the following subsection.

4.3 Simulation from the law of the stable undershoot

We now describe and justify SU-Alg and analyse its computational complexity. Recall from Subsection 4.1 above that the function is absolutely continuous and non-decreasing and hence almost everywhere differentiable with derivative almost everywhere equal to the density of and set to be equal to at the points of non-differentiability of . Further recall that , and the definition , as well as that of the functions and defined in (4.2) and (4.3), respectively.

By (4.5) in Proposition 4.1(c) and the representation of the stable density in (4.3), the density of is given by

while the density of equals

Clearly, for . Thus, . It suffices to sample from the law with density , and . Sampling efficiently from a density on , proportional to , is hard to do directly, see Section 2.5. We use the integral representation of in (4.3) to extend the state space: consider with density

Define a random variable . Note that , and hence . Moreover, the law of the random vector is given by the density

| (4.8) |

Fast exact simulation from the law given by the density is non-trivial but possible, see SU-Alg. The first step, given in Proposition 4.2, is to dominate the density by a mixture of densities that can both be simulated using rejection sampling.

Proposition 4.2.

Fix any . Let (resp. ) be the density on proportional to (resp. ). Define the mixture density

where and

| (4.9) |

Then there exists a constant such that, for all , we have

| (4.10) |

Remark 4.2.

The numerical value of the constant in Proposition 4.2 is not required in SU-Alg, which samples from the density in (4.8). The inequalities in (4.10) enable us to apply rejection sampling to a proposal from to obtain an exact sample from the law given by the density . The first inequality in (4.10) explicitly states a decay of the acceptance probability as . Sampling from requires a mixture of samples from and . The respective algorithms are constructed and analysed in Subsections 4.3.1 and 4.3.3 below, respectively.

Proposition 4.2.

Denote the total masses of the positive functions and by

Then, and . Moreover,

Note that , making proportional to

Let be the normalizing constant, such that for ,

| (4.11) |

Thus in (4.10) follows.

4.3.1 Simulation from the density : proof of Proposition 2.5

The proof of Proposition 2.5 requires the following two elementary lemmas about certain properties of the function defined in (4.2).

Lemma 4.3.

The derivative of any order of , and hence of , is positive on .

Proof.

Clearly, by definition (4.2), , where for . Recall that for where is the Riemann zeta function. Thus, for any , we have

This shows that and all its derivatives are positive on , implying the same is true of . Thus, , making convex on . Similarly, a derivative of of any order is a linear combination with non-negative coefficients of derivatives of , multiplied with , and thus non-negative itself on the interval . ∎

Lemma 4.4.

For , we have .

Proof.

Proposition 2.5.

Recall that is convex by Lemma 4.3. To sample from , we first sample from the marginal log-concave density proportional to on via LC-Alg. Then, conditional on , we sample from the law whose density is proportional to the function on . Note that this makes , conditional on , into a shifted exponential random variable.

As explained in Section LABEL:sec:devroye below, the computational cost of LC-Alg has two parts: (I) the cost of finding the value of in line LABEL:line_find_a_1 of LC-Alg and (II) the expected cost of the accept-reject step in LC-Alg. By [devroye2012note, §4], the expected cost of (II) is bounded above by .

Note that cost (I) of finding within -Alg is not constant in the variable , which is itself random in SFP-Alg. Thus we need to analyse the cost of finding in LC-Alg as a function of . By Lemma 4.4, for , we have . Thus we set and note that the following inequality holds: . Therefore the number of steps in the binary search in Step LABEL:step_binary of LC-Alg is bounded above by

where the constant in depends neither on nor , implying the claim. ∎

4.3.2 Time cost of applying the Newton–Raphson method in -Alg.

Inverting is equivalent to inverting the convex increasing function

Equivalently, for any , we must find the root of the convex increasing function where

| (4.13) |

Proposition 4.5.

Define the auxiliary function

| (4.14) |

For any , the computational cost of finding the root of via NR-Alg with auxiliary function is where is the solution and specifies the number of precision bits.

Proof.

Since is convex, if our initial estimate (obtained via binary search) of the root is larger than the true root, then the Newton–Raphson sequence

decreases and has quadratic convergence to the root . Using the power series of the cotangent function (as in the proof of Lemma 4.3) and the inequality , for satisfying , we have

Since , by the stopping condition of the binary search of line LABEL:alg:inversion_newton_raphson_bisection_stop in NR-Alg, we only need

implying . Thus, the binary search for this requires steps. ∎

Proposition 4.6.

Define the auxiliary function

| (4.15) |

The total cost of numerical inversion of the function on the interval via NR-Alg with auxiliary function is where specifies the number of precision bits.

Proof.

On , the function is convex and increasing with derivative . Thus, given , if our initial estimate (obtained via binary search) of the root of the function is larger than and sufficiently close to , then the Newton–Raphson sequence

is decreasing and has quadratic convergence to the root . Note that and are increasing, and thus

Since ,

has uniform upperbound for and

By the stopping condition of the binary search of line LABEL:alg:inversion_newton_raphson_bisection_stop in NR-Alg, we only need the final expression in the previous display to be smaller than , implying . Thus, the binary search for requires iterations. ∎

For , define the function

| (4.16) |

Proposition 4.7.

Define auxiliary function

| (4.17) |

For , the total cost of numerical inversion of the function via NR-Alg with auxiliary function is where specifies the number of precision bits.

Proof.

Note that for . Given , if our initial estimate (obtained via binary search) of the root of the function is larger than and sufficiently close to , then the Newton–Raphson sequence

has quadratic convergence to the root . Note that

By the stopping condition of the binary search of line LABEL:alg:inversion_newton_raphson_bisection_stop in NR-Alg, we only need

implying . Thus the binary search for requires iterations. ∎

4.3.3 Simulation from the density : proof of Proposition 2.6.

Before proving Proposition 2.6, we need following lemmas, describing the properties of functions and .

Lemma 4.8.

The function , where is defined in (4.2), is concave on .

Proof.

Clearly, by definition (4.2), , where for . Recall that for where is the Riemann zeta function. Thus, for any ,

This shows that and all its derivatives are positive on , implying the same is true of . Thus, , making convex on . Similarly, a derivative of of any order is a linear combination with non-negative coefficients of derivatives of , multiplied with , and thus non-negative itself on the interval .

To prove that is concave, let and note that it suffices to show that . If , then is constant since and the double angle formula imply that , and

To prove the general case , denote , then we have , , implying that

We will show that termwise. When , we have so all the coefficients of and of for agree:

To establish the termwise inequality for general , it thus suffices to show that

Since the equality is attained when , it suffices to show that attains its maximum at . Since , it suffices to show that is the only critical point of . This will follow once we show that the derivative

is positive and decreasing (resp. negative and increasing) in for any (resp. ). Indeed, so the only solution to is (where for any ).

For , the inequality for is equivalent to

This inequality is further equivalent to

It is easy to see that the positive and negative coefficients of the powers of are the same (with different corresponding powers of ). An elementary but tedious calculation shows that can be rewritten as

Since and for and for , we deduce that completing the proof. ∎

Lemma 4.9.

For , we have

In particular, if satisfies for some (recall ), we have

| (4.18) |

Proof.

By the concavity of function , we have and for . Moreover, we have and . ∎

Lemma 4.10.

For , .

Proof.

Note that . By Lemma 4.9, we only need to show that

The power series expansion of shows that the left-hand side is equivalent to

where is Riemann zeta function. Note that attains its maximum value when , so it suffices to establish the following inequality

In fact, let , then

Now we can complete the proof of Proposition 2.6.

Proposition 2.6.

In line 2, -Alg sets when . Otherwise the equation , , has a unique solution by Lemma 4.3 and we may define to be that solution. This inversion is carried out by the Newton–Raphson method, converging quadratically fast since is log-convex, see Section LABEL:sec:NewtonRaphson below for details. By Proposition 4.5 the computational cost of finding is bounded above by . Since , if , Lemma 4.4 implies . Hence, by (4.18) in Lemma 4.9, we obtain

where the second inequality follows from , which holds since for every we have . Thus, the computational cost of finding is bounded above by

The simulation from can be decomposed into two steps: first sample from the marginal density proportional to and then from the conditional law proportional to (which is a gamma with shape and rate and translated by ). Now let us establish a simulation algorithm from the density .

To sample from , we first toss (at most two) coins to determine on which of the following (possibly degenerate) intervals lies the sample: on , or , where . The time cost of this step is constant, see Remark 2.3.

-

a)

Case (the sample lies in ). Recall that by Lemma 4.3 we have on and that is the unique solution to . By definition of , the following equalities

hold on the interval . Since is strictly increasing and , log-concave on with mode at . Thus we may apply LC-Alg to obtain a sample in the interval .

Again, the computational cost of LC-Alg has two parts: (I) the cost to finding the value of and (II) the expected cost of the accept-reject step. By [devroye2012note, §4], the expected cost of (II) is bounded above by .

To analyse the cost of finding in LC-Alg, our idea is to find such that since is the first number we check in the binary search. And then we only need to estimate the upperbound of . Recall that and . In fact, for satisfying , we have

By Lemma 4.10 and the fact that is convex, we have

Together with (4.18) in Lemma 4.9, we have

Therefore the steps of binary search in Devroye’s algorithm is bounded by

-

b)

Case (the sample lies in , where ). We propose a sample from the distribution function

(4.19) on via the inversion method. By Proposition 4.6, the computation cost of inversion is bounded above by . Since has a strictly positive (by Lemma 4.3) density, proportional to , we accept the sample with probability , where

(4.20) The first inequality in (4.20) holds since both and on . The second inequality follows from Lemma 4.3 because is increasing on and . A direct calculation using the definition of in (4.2) yields the final expression in (4.20), which is decreasing in and approaching its infimum as .

-

c)

The case (where and the sample lies in ), is split in two subcases:

-

(i)

Case . We propose from the density proportional to

(4.21) When , the density is proportional to . We can sample from this via inversion directly and the time cost is a constant. When , we can sample from the density via inversion via Newton–Raphson method: the CDF of our target density equals

(4.22) with defined in (4.16). So to get a sample from the target density we only need to solve where . By Proposition 4.7 and Lemma 4.9, the time cost of inversion is bounded above by

Then we accept the sample with probability , where is given by

(4.23) We now prove the second inequality in (4.23). By concavity, for , we have

Moreover, again by concavity, the quotient satisfies

Using the elementary inequalities for , we have

-

(ii)

Case . We propose from the distribution function

(4.24) which can be sampled from via the inversion method. Note that now the solution in the inversion method, by Proposition 4.5 and Lemma 4.9, the time cost of inversion method is bounded above by

Then accept the proposal with probability

(4.25) where

By Lemma 4.8, is decreasing, so and

This shows that is uniformly bounded away from for and .

-

(i)

All in all, the expected running time is bounded above by

where the constant depends on neither nor . ∎

4.3.4 Proof of Proposition 2.4.

In this subsection we prove Proposition 2.4 using Propositions 2.5, 2.6 and 4.2. Let and be as in the statement of Proposition 2.4 and recall that is the “intensity” in the Lévy measure (4.1) of the stable subordinator . Recall also that . As explained in the beginning of Section 4.3, if we sample with density given in (4.8), then the random variable follows the law of . By the inequalities in (4.10) of Proposition 4.2, SU-Alg samples from (defined in Proposition 4.2) and performs an accept-reject step to obtain a sample from the density . This implies that SU-Alg indeed samples from the law .

It remains to prove that the expected running time of SU-Alg is bounded as stated. As explained in Remark 2.1 above, the computation of is assumed to take a constant amount of time. By (4.10), the acceptance probability in line 10 of SU-Alg equals and is bounded below by , uniformly in (and all other parameters except ). Thus the accept-reject step in SU-Alg on average takes no more than steps. Since is mixture of densities and (see Proposition 2.4), we sample a Bernoulli variable taking value with probability . If we get , then sample from and otherwise from . Thus, the computational complexities of Algorithms -Alg and -Alg, given in Propositions 2.5 and 2.6), imply the bound in Proposition 2.4.∎

4.4 Proofs of Theorem 2.3

We begin by recalling a well-known property of the moments (or Mellin transform) of stable random variables, see [ken1999levy, Example 25.10]. For and , we have

| (4.26) |

Since and by Proposition 4.1, where is the value of the stable subordinator at time and is the inverse of the decreasing function , we have

and hence . Note that the density of is , which does not depend on the value of (see the representation of density of in (4.3)).

Lemma 4.11.

The following limit holds: as .

Proof.

Note from (4.1) and the Lévy–Khintchine formula that the Fourier transform of is, for any , given by

where is the sign of . Recall that for any . Thus,

where as by dominated convergence and as . ∎

Lemma 4.12.

Denote .

- (a)

-

(b)

Note that the function attains its maximum when , implying for all . Thus

The expectation in part (b) of the lemma can now be bounded as follows:

By substituting we get

Theorem 2.3.

Case . SFP-Alg samples under by Proposition 4.1. By Proposition 2.4, to find an upper bound on the average running time, we only need to take expectation of the average running time of SU-Alg in . In other words, upper bound , and .

By (4.26) (with equal to either or ), the inequality for all and the fact that , we have

Together with Lemma 4.12, the average running time of SFP-Alg is bounded above by

where the constant does not depend on .

To show the running time of SFP-Alg has exponential moments, we only need to verify that the running times of Algorithms -Alg and -Alg, with random parameter , have exponential moments. By Propositions 2.5 and 2.6, we only need to show that , and have exponential moments. Note from (4.26) that for any , for any , and

for any , where we recall that . Thus, these steps indeed have running times with exponential moments, completing the proof.

Case . Again by Proposition 4.1, SFP-Alg samples under conditional on since we keep sampling until . Indeed, note that is equivalent to being larger or equal to , where is specified in Proposition 4.1, and has acceptance probability equal to . The other steps are the same as in the case .

The running time of SFP-Alg in the case consists of two parts: (I) the naive sampling of until in Line 2 of SFP-Alg and (II) the running time of SU-Alg with random input in Line 8 of SFP-Alg, where is conditioned to be smaller or equal to . Let be the expected runtime of SU-Alg with parameter . Then the running time of SFP-Alg in the case is bounded by

where by Theorem 2.3. It remains to lower bound the probability .

Pick and note that

Suppose , then the elementary inequality for gives

Since attains its maximum when , it is optimal to let be the ‘solution’ to . This solution, however, need not exist if is small. Note that is increasing and continuous on and decreasing thereafter, with maximal value . Thus, we may take to be the solution of

This leads to the lower bound

implying the claim and completing the proof. ∎

4.5 Proofs of Theorem 2.1 and Corollary 2.2

We begin by introducing a construction of the probability measures given the base probability measure via the Esscher transform. Fix any and and let be a driftless stable subordinator under the probability measure with Lévy measure . Denote by the right-continuous filtration generated by . Given , the probability measure can be constructed via its Radon–Nikodym derivative

Indeed, by [Sato, Thm 33.2], is subordinator under with Lévy measure , making it a tempered stable process as desired.

Recall , fix some and recall that . For any measurable we have and hence

where is independent of under . In particular, we have

| (4.27) |

Theorem 2.1.

For a fixed time , TSFP-Alg first samples the event under . Indeed, this is done by sampling under and noting that the event is equivalent to the corresponding tempered stable process, of which is the final value, to not cross the boundary on the time horizon . Thus, if , by the Markov property of , we may simply start a new iteration from the initial time-space point . If instead , we need to sample under . Moreover, in that case, by (4.27), we need only repeatedly sample under conditional on and an independent , until . For that, SFP-Alg samples under conditional on . By the strong Markov property, to check if , we need only sample independently (and conditionally given ) via S-Alg and set . This justifies the validity of TSFP-Alg.

Now let us consider the computational complexity of TSFP-Alg. The expected number of iterations in Line 3 of TSFP-Alg is

In each iteration we use TS-Alg with expected complexity uniformly bounded by according to [TemperedStableDassios, Thm 3.1]. After that, we sample the triplet conditional on via SFP-Alg. By Theorem 2.3, the expected running time of SFP-Alg is bounded by

The acceptance probability in Line 12 of TSFP-Alg is

All in all, the expected running time of TSFP-Alg is bounded by

| (4.28) |

It remains to upper bound and lower bound .

Recall that

Note that, by concavity, . Thus, by Lemma LABEL:lem:exp_moment with , we have

On the other hand, note that

Hence, if satisfies , then the elementary inequality for gives

Denote , and set and note that . Then the expected running time of TSFP-Alg is bounded by

where is a constant that depends neither on , nor . ∎