Asymptototic Expected Utility of Dividend Payments in a Classical Collective Risk Process

Abstract.

We find the asymptotics of the value function maximizing the expected utility of discounted dividend payments of an insurance company whose reserves are modeled as a classical Cramér risk process, with exponentially distributed claims, when the initial reserves tend to infinity. We focus on the power and logarithmic utility functions. We perform some numerical analysis as well.

1. Introduction

The problem of identifying the optimal dividend strategy of an insurance company was introduced in the seminal paper of [14] and mathematically formalized by [17]. Since then, many authors have analyzed various scenarios for which they proposed optimal dividend strategies.

[17] assumed that the reserve process of an insurance company follows a classical Cramér-Lundberg risk process given by

| (1) |

where are i.i.d positive random variables with an absolutely continuous distribution function representing the claims; is an independent Poisson process, with intensity modeling the times at which the claims occur; denotes the initial surplus; and is the premium intensity. We further consider the dividend payments, defined via an adapted and nondecreasing process , representing all the accumulated dividend payments up to time . Then, the regulated process is given by

| (2) |

We observe this regulated process until the time of ruin

The time of ruin of an insurance company depends on the chosen dividend strategy. We assume that the usual net profit condition, , for the underlying Cramér-Lundberg risk process, is fulfilled. Another natural assumption is that no dividends are paid after the ruin.

[21] and [18] consider the optimal dividend problem in a Brownian setting. [31] study the constant barrier under the Cramér-Lundberg model and [4] under the Lévy model. For related works considering the dividend problem, we refer to [2]; [6]; [12]; [16]; [20]; [25]; [27]; [24]; [29]; [1]; [3]; [30]; [13]; [5] and references therein.

Inspired by [23], we consider, instead of the classical maximization of the expected value of the discounted dividend payments, the maximization of the expected value of the utility of these payments, for some utility function [23] consider the asymptotic of the expected discounted utility of dividend payments for a Brownian risk process with drift under the assumption that is absolutely continuous with respect to the Lebesgue measure. Under the same assumption of , we perform the asymptotic analysis of the expected utility in a classical compound Poisson risk model, which, due to its jumps, brings an extra level of complexity. As in [23], we solve some ’peculiar’ non-homogenous differential equations.

Assuming that the process admits, almost surely, a density, denoted by namely for each ,

we define the target value function as

| (3) |

where is a discount factor, is a fixed differentiable utility function, which equals on the negative half-line, and represents the expectation with respect to . Here, the density models the intensity of the dividend payments in continuous time, and thus we will be maximizing the value function over all admissible dividend strategies . We assume that the dividend density process is admissible, whenever it is a nonnegative, adapted and cádlág process, and there are no dividends after the ruin, namely , for all . We denote by the set of all admissible strategies .

Moreover, we restrict ourselves to Markov strategies, meaning that, for every , the strategy depends only on the amount of the present reserves. We introduce a non-decreasing function such that

The non-decreasing assumption is justified by the fact that the company should be willing to pay more dividends whenever it has larger reserves. Finally, we assume that the ruin cannot be caused by the dividend payment alone and we choose such that the value function given in (3) is well-defined and finite for all .

The above dividend problem can be used to monitor the financial state of the company. In particular, it can be considered as a signalling device of future prospects. In this paper, we assume that the company has large reserves and therefore by taking the initial value to infinity we can produce a very transparent optimal strategy and hence a very clear and simple value function, which, we believe, is crucial from a management point of view.

For the above dividend problem, one can formulate the Hamilton-Jacobi-Bellman (HJB) equation of the optimal value function (see Section 2). Although impossible to solve this HJB equation explicitly (see, e.g., [2]), one can analyze the asymptotic properties of its solutions for large initial reserves. We focus on the asymptotic analysis of such value functions when the claim sizes are exponentially distributed, with utility functions that are either powers or logarithms (see Section 3). We also introduce a numerical algorithm for identifying such value functions (see Section 4).

2. Hamilton–Jacobi–Bellman Equation

From now on, we assume that is increasing and strictly concave, such that , and where denotes the derivative of a function with respect to . We denote by the set of all admissible strategies bounded above by and let

| (4) |

Using the verification theorem, one can prove the following theorem.

Theorem 1.

If then the value function is differentiable and fulfills the Hamilton–Jacobi–Bellman equation:

| (5) |

The proof of the above theorem follows the same steps as the proof of Theorem 3.3 of [7] and therefore we simply refer to them. Since the set of all possible strategies over which we take the supremum in is smaller than the one for , then one has . We note also that depends on . The goal of the next corollary is to prove that .

Corollary 1.

The optimal value function is differentiable and fulfills the Hamilton–Jacobi–Bellman equation:

| (6) |

Proof.

Note that increases monotonically to , for any fixed as unless

| (7) |

where when and when (in this way the ruin is not caused by the dividend payments). The reason for that is that the supremum on the left hand side of (5) is a monotone function and thus converges to the supremum given in (6). To exclude (7), it is sufficient to demonstrate that for sufficiently large , for a fixed , the function tends to zero. Observe that the regulated risk process equals either , or equals until the nearest jump moment, otherwise, at the time of the first jump, after . Further, if the first jump happens before , then either the company becomes ruined by this jump/loss or, it continues, but from an initial position/reserve smaller than , hence collecting a smaller amount of dividends than . We recall that . Thus

where . Therefore, for any , we can find a sufficiently small , such that which tends to zero as , since we assumed that and that This completes the proof. ∎

Note that the supremum in (6) is attained for the function

| (8) |

We end this section by adding two crucial observations. By considering the fix strategy and the first jump epoch we have

where the function describes the deterministic trajectory of the risk process (1) up to the first jump time , that is, From the assumption that , it follows that

| (9) |

Moreover, we have the following lemma.

Lemma 1.

Proof.

Firstly, we demonstrate that . Recall that, from the definition of an admissible strategy, is a nondecreasing function and hence it is enough to prove that is unbounded. Assuming the contrary, that there exists , such that, for all , we have , it implies that for all . Hence

However, this means that is bounded, which contradicts (9). Thus, indeed as . Then

where the last equality in this equation comes from the Inada condition required for the utility function. ∎

3. Asymptotic Analysis

From now on, we assume that the claims follow an exponential distribution with parameter , that is for all . This section is dedicated to the asymptotic analysis of the expected utility of dividend payments, for large initial reserves

3.1. Classical Risk Process (1) and Power Utility Function

In this subsection, we consider the classical risk process (1) paired with the power utility function

| (10) |

The supremum in (6) is attained at

| (11) |

and thus, after an integration by parts, the Equation (6) simplifies to

| (12) |

where is the second derivative of . This is a nonlinear second order ODE. Peano Theorem, see [11, Chp. 1] guarantees the existence of a solution. For uniqueness, we need two boundary conditions. Evaluating in Equation (6), we have a first initial condition,

| (13) |

The derivation of the second condition is described later, in Remark 2. In order to asymptotically analyze the solutions of Equation (12), we transform it into a nonlinear first order ODE, via a Riccati type substitution, namely

Lemma 2.

As ,

Proof.

Let , then using Lemma 1 concludes the proof. ∎

From , we have that . Substituting into Equation (12), it produces the following equation

| (14) |

which is equivalent with

| (15) |

This is a nonlinear first order ODE without known explicit solutions. We focus on the asymptotic behaviour of the solutions and derive the asymptotic optimal strategy of paying dividends , for a function of the initial reserve.

Note that throughout the paper, .

Theorem 2.

Let , where . Then, as ,

| (16) | |||

| (17) | |||

| (18) |

Remark 1.

The assumption that is rational is not restrictive, because the set of all rational numbers is sufficiently large to model various shapes of the power utility function.

3.2. Classical Risk Process (1) and Logarithmic Utility Function

We consider the classical risk process (1) and the logarithmic utility function

| (19) |

The supremum in the Equation (6) is attained for

| (20) |

and this equation simplifies to

| (21) |

This is a nonlinear second order ODE with the initial condition

| (22) |

For the existence of solutions, see [11, Chp. 1]. Apart from the initial condition above, one more initial condition is required to ensure the uniqueness of solutions. Similarly to the case of the power utility function, the choice of this condition is postponed to Section 4. By a Riccati substitution, we transform Equation (21) into the following nonlinear first order ODE

| (23) |

Theorem 3.

As , we have,

| (24) | |||

| (25) | |||

| (26) |

4. Numerical Analysis

In this section, we provide a numerical algorithm for calculating the value function for the classical risk process (1) with exponentially distributed claims and power utility function (10). To do this, we first find . Then, based on the boundary condition (13), we determine and numerically solve Equation (12). Obviously, we could propose a similar algorithm for the logarithmic utility function. The considerations regarding the second boundary condition which we formulate in Remark 2 remain true when considering the logarithmic utility functions.

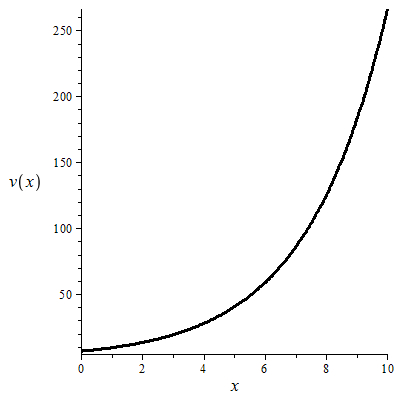

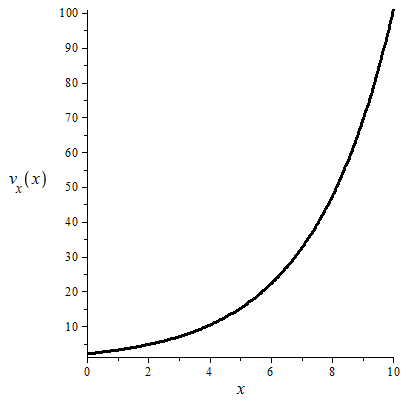

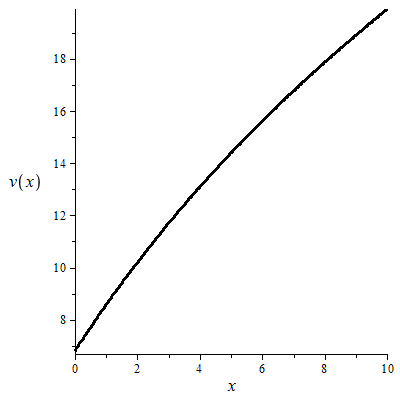

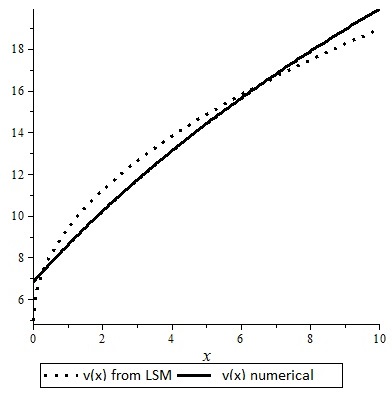

Note that a similar analysis is presented in [Baran and Palmowski (2013)], from which we retrieve some numerical considerations in the case of the power utility, see Table 1 and Figures 1 and 2. Note that [Baran and Palmowski (2013)] does not present the derivation of the HJB equation nor the analysis of the logarithmic utility function.

| 0 | 6,8021 | 1,9000 | 0,2770 |

|---|---|---|---|

| 1 | 8,5790 | 1,6929 | 0,3489 |

| 2 | 10,2022 | 1,5575 | 0,4122 |

| 3 | 11,7010 | 1,4431 | 0,4802 |

| 4 | 13,0940 | 1,3454 | 0,5525 |

| 5 | 14,3963 | 1,2613 | 0,6286 |

| 6 | 15,6203 | 1,1884 | 0,7081 |

| 7 | 16,7762 | 1,1247 | 0,7905 |

| 8 | 17,8723 | 1,0687 | 0,8755 |

| 9 | 18,9158 | 1,0192 | 0,9626 |

| 10 | 19,9126 | 0,9752 | 1,0515 |

Remark 2.

The choice of is crucial in the context of the optimality of the solution of the HJB equation. Indeed, if we choose and it is too big, then and go to infinity as . In fact, by (11) the discounted cumulative dividends go to (see Table 2). This situation corresponds to a bubble, meaning that the value of the company is not increased by the dividend payments and we cannot derive an optimal solution.

| 0 | 6,8000 | 2,0000 | 0,2500 |

|---|---|---|---|

| 1 | 9,4022 | 3,1941 | 0,0980 |

| 2 | 13,3275 | 4,7502 | 0,0443 |

| 3 | 19,1343 | 7,0039 | 0,0204 |

| 4 | 27,6771 | 10,2878 | 0,0094 |

| 5 | 40,2103 | 15,0801 | 0,0044 |

| 6 | 58,5692 | 22,0787 | 0,0021 |

| 7 | 85,4378 | 32,3029 | 0,0010 |

| 8 | 124,7394 | 47,2425 | 0,0004 |

| 9 | 182,2094 | 69,0750 | 0,0002 |

| 10 | 266,2320 | 100,9833 | 0,0001 |

When is sufficiently large like Figure 2 shows, the function is concave and tends to as , allowing the cumulative discounted dividend payments to increase (see Table 1).

To find we propose the following algorithm.

-

•

Set initial value ,

-

•

From the equality (13) derive initial value ;

-

•

Solve numerically the differential Equation (12) with the initial condition ;

-

•

Calculate using ;

-

•

Using the least squares method, approximate be the linear function . Because of our results from Theorem 2, we assume that is a linear function;

-

•

Let be a trajectory of the regulated process starting from until the first time claim arrival . Hence

(27) i.e.,

-

•

Using the least squares method, approximate by a function of the form . Because of our results from Theorem 2, we assume that is a power function;

-

•

Calculate

(28) where .

-

•

Calculate the value ;

-

•

Repeat until for fixed .

If we choose hence also correctly, then observing the regulated process right after the first jump occurs, the left hand side of (28) gives the true estimator of . Hence, will approximate . In practice, we should look for the correct changing by some small fixed value until for a prescribed precision .

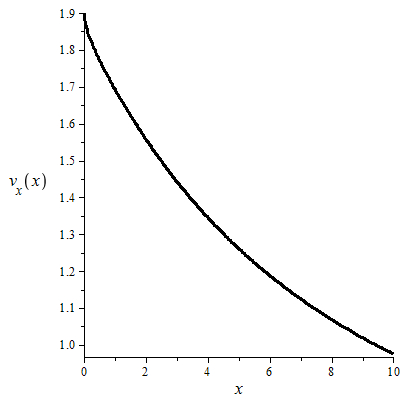

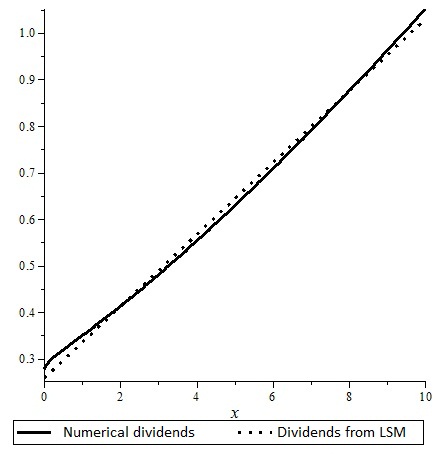

We apply the above procedure in a ten points least square algorithm to the data given in Figure 2. The results are described in the Figures 3 and 4 and the Table 3. At the beginning, we chose . We notice that for , we have a bubble. As per Remark 2, we cannot derive an optimal solution. Thus, the values of are not greater than .

We start from the value for and observe the difference . Then, we reduce by . We noticed that the difference is getting smaller as we are decreasing . We stop the above procedure when because then for . Similarly, we can check that all the values of less that are too small. Then, successively, we decrease to and then to . By repeating the above procedure, we can find the ”correct” . For example, if we choose then . Table 3 explains how the algorithm works. It contains the results of each step of the loop of this algorithm until . Thus, the ”correct” value of is .

Let us recall that our main goal was to derive the asymptotic behavious of the value function for large initial reserves and to identify its corresponding optimal strategy. The methodology was based on comparing the asymptototic behaviours of components of the HJB equation. This approach produces a very simple solution that can be used instead of numerically solving the HJB equation.

| correctness | value | |||

|---|---|---|---|---|

| t.b. | 1,97 | - | - | - |

| c. | 1,96 | 6,798693877 | 6,783185889 | 0,015507988 |

| c. | 1,95 | 6,798803418 | 6,784849201 | 0,013954217 |

| c. | 1,94 | 6,799092783 | 6,786580941 | 0,012511842 |

| c. | 1,93 | 6,799564767 | 6,788388955 | 0,011175812 |

| c. | 1,92 | 6,800222221 | 6,790283409 | 0,009938812 |

| c. | 1,91 | 6,801068062 | 6,792277924 | 0,008790138 |

| c. | 1,90 | 6,802105263 | 6,794392618 | 0,007712645 |

| c. | 1,89 | 6,803336861 | 6,796662198 | 0,006674663 |

| t.s. | 1,88 | - | - | - |

| t.s. | 1,881 | - | - | - |

| c. | 1,882 | 6,804464186 | 6,798652236 | 0,005811950 |

| c. | 1,8819 | 6,804479085 | 6,798679195 | 0,005799890 |

| t.s. | 1,8818 | - | - | - |

| t.s. | - | - | - | |

| t.s. | 1,88185 | - | - | - |

| c. | 1,88186 | 6,804485051 | 6,798690050 | 0,005795001 |

| c. | 1,881859 | 6,804485199 | 6,798690322 | 0,005794877 |

| c. | 1,881858 | 6,804485348 | 6,798690594 | 0,005794754 |

| c. | 1,881857 | 6,804485498 | 6,798690867 | 0,005794631 |

| c. | 1,881856 | 6,804485647 | 6,798691139 | 0,005794508 |

| c. | 1,881855 | 6,804485795 | 6,798691412 | 0,005794383 |

| c. | 1,881854 | 6,804485945 | 6,798691685 | 0,005794260 |

| c. | 1,881853 | 6,804486095 | 6,798691958 | 0,005794137 |

| c. | 1,881852 | 6,804486243 | 6,798692231 | 0,005794012 |

| c. | 1,881851 | 6,804486392 | 6,798692504 | 0,005793888 |

| t.s. | 1,881850 | - | - | - |

| t.s. | - | - | - | |

| t.s. | 1,8818503 | - | - | - |

| c. | 1,8818504 | 6,804486482 | 6,798692667 | 0,005793815 |

| c. | 1,88185039 | 6,804486484 | 6,798692671 | 0,005793813 |

| c. | 1,88185038 | 6,804486485 | 6,798692673 | 0,005793812 |

| c. | 1,88185037 | 6,804486486 | 6,798692675 | 0,005793811 |

| c. | 1,88185036 | 6,804486488 | 6,798692679 | 0,005793809 |

| c. | 1,88185035 | 6,804486489 | 6,798692681 | 0,005793808 |

| t.s. | 1,88185034 | - | - | - |

| t.s. | 1,881850341 | - | - | - |

| c. | 1,881850342 | 6,804486491 | 6,798692684 | 0,005793807 |

Still, to compare the asymptotics with the exact values of the value function, we propose a numerical algorithm for solving HJB equations. Using it, we can observe that the asymptotic values are very close to the true ones. In particular, Figure 3 shows that the optimal strategy of paying dividends with intensity in the case of the power-type utility function is asymptotically linear as (18) suggests. What is interesting, it that this is true even for small values of reserves (starting from ). We have observed that this is true for other sets of parameters, which is very promising.

Appendix A Proof of Theorem 2

Proof.

When , the Equation (14) has the following form:

If we make the substitution , then , and furthermore

If we multiply both sides of the equation by , we obtain

| (29) |

specifically, an equation of the form

| (30) |

where are polynomials in and . Recall that, from (9), . Any term on the left-hand side of (30) is of the form or . [26] proved that if two functions (where denote the class of Hardy functions) then the set of all terms on the left-hand side of Equation (30) is totally ordered with respect to the relation , where , for means that either or as . In other words, heuristically, we can order all terms (which are functions of ) according to the speed that they tends to infinity as . [26, p. 195] shows that in this set exist two terms of the same order; namely, their quotient tends to a finite limit for . Using this result, we can derive the asymptotic behaviour of the solutions of Equation (30).

Firstly, note that . Because of that, we note that in the Equation (29), the term is of a smaller order than the other terms, which contain . Similarly, the term has a smaller order than the other terms of Equation (29), which do not contain . Since we know that there exists two terms of the Equation (29) of the same order, we have three possibilities to produce the asymptotic behaviour of a solution of the Equation (29):

-

(a)

and ;

-

(b)

and ;

-

(c)

and .

Lemma 3.

Only the case (a) above produces a feasible asymptotic behaviour.

Proof.

Note that in case (a), both terms have the same order. Indeed, let

Denote

where , which reduces to

Since , this becomes

Placing the above asymptotics into Equation (29) and dividing by gives . Finally, we obtain the following asymptotics of :

| (31) |

Obviously, in this case for , as required.

Similarly, in case (b), we have

Following the same steps as in case (a), let

where This reduces to

which after integration becomes

From Karamata Theorem (see [19, Prop. 1.5.8]) , leading to

for . However, for , we have as , which contradicts the assumption that for . Thus, this is not acceptable.

In case (c), we have

Introducing

as , this simplifies into

| (32) |

We will distinguish two cases. Using the same arguments as before, with respect to Karamata arguments given in [19], for , we encounter two possible asymptotics:

-

I.

If , then, via the separation of variables, we have

-

II.

If , then a simple integration leads to

In both of the above cases, is a constant and its appearance is a consequence of the lack of uniqueness of the solutions of Equation (32) due to the lack of sufficient boundary conditions for .

Note that in the first case, the asymptotics of makes sense only if because otherwise for , leading to a contradiction. In both cases, after substituting the above asymptotics into Equation (29), the term including dominates any other term. Dividing both sides of Equation (29) by this asymptotically dominant element leads to the false identity . ∎

We continue the proof of Theorem 2. From Lemma 3, the asymptotic solution of is given by (31). When substituting , the asymptotic behavior of is given by

which, for , is equivalent to

Recall that . Hence

We can now solve (via a separation of variables) the equation

deriving for any constant . Applying classical Karamata’s arguments leads to as This produces (16). Using (11) completes the proof. ∎

Appendix B Proof of Theorem 3

Proof.

We use similar arguments as in the proof of Theorem 2. In fact, one can derive (30), with the main difference that terms of the form and will appear in the expressions of and To satisfy the eliminating procedure given by [26, Eq. (3.3)]), we mimic all the arguments from [26] . Thus, one can conclude that also in the case of the logarithmic utility function there exists two of the terms of the equation (23) of the same order. Now, note that in the Equation (23), the term is of a smaller order than . Similarly, the term is of a smaller order than the other elements, which do not contain . We then have three possibilities:

-

(a)

and ;

-

(b)

and ;

-

(c)

and .

In case (b) we have

Let

with This is equivalent to

which after integration from to , leads to

namely

Using the direct half of Karamata Theorem (see [19, Prop. 1.5.8]), we have that as ,

equivalent to

| (33) |

Thus, we obtain a contradiction, since the right hand side converges to zero as , whereas the left hand side converges to .

In case (c), we have

leading to

| (34) |

The above asymptotic behaviour makes sense only for , because otherwise when . Substituting (34) into (23) gives . Hence

Recall that . Thus, with solving the equation

References

- [1] Albrecher, Hansjőrg, and Stefan Thonhauser. 2009. Optimality results for dividend problems in insurance. RACSAM Revista de la Real Academia de Ciencias, Serie A, Matematicas 103: 295–320.

- [2] Asmussen, Søren, and Michael Taksar. 1997. Controlled diffusion models for optimal dividend pay-out. Insurance: Mathematics and Economics 20: 1–15.

- [3] Asmussen, Soren, and Hansjorg Albrecher. 2010. Ruin Probabilities. Singapore: World Scientific Singapore.

- [4] Avram, Florin, Zbigniew Palmowski, and Martijn R. Pistorius. 2007. On the optimal dividend problem for a spectrally negative Lévy process. Annals of Applied Probability 17: 156–80.

- [5] Avram, Florin, Zbigniew Palmowski, and Martijn R. Pistorius. 2015. On Gerber-Shiu functions and optimal dividend distribution for a Lévy risk-process in the presence of a penalty function. Annals of Applied Probability 25: 1868–1935.

- [6] Azcue, Pablo, and Nora Muler. 2005. Optimal reinsurance and dividend distribution policies in the Cramér-Lundberg model. Mathematical Finance 15: 261–308.

- [Baran and Palmowski (2013)] Baran, Sebastian, and Zbigniew Palmowski. 2013. Problem optymalizacji oczekiwanej uĹĽyteczności wypłat dywidend w modelu Craméra-Lundberga. Roczniki Kolegium Analiz Ekonomicznych 31: 27–43.

- [7] Baran, Sebastian, and Zbigniew Palmowski. 2017. Optimal utility of dividends for Cramér-Lundberg risk process. Applicationes Mathematicae 44: 247–65.

- [8] Bellman, Richard. 1953. Stability Theory of Differential Equations. New York: McGraw-Hill.

- [9] Bertoin, J. 1996. Lévy Processes. Cambridge: Cambridge University Press.

- [10] Doob, Joseph L. 2004. Measure Theory. New York: Springer.

- [11] Coddington, E. A., and N. Levinson. 1987. Theory of Differential Equations. New Delhi: McGraw-Hill.

- [12] Eisenberg, Julia, and Zbigniew Palmowski. 2021. Optimal dividends paid in a foreign currency for a Lévy insurance risk model. North American Actuarial Journal 25: 417–37.

- [13] Eisenberg, Julia, and Hanspeter Schmidli. 2011. Minimising expected discounted capital injections by reinsurance in a classical risk model. Scandinavian Actuarial Journal 3: 155–76.

- [14] De Finetti, B. 1957. Su un’impostazione alternativa dell teoria colletiva del rischio. Trans. XV Intern. Congress Act. 2: 433–43.

- [15] Fleming, Wendell H., and Halil Mete Soner. 2006. Controlled Markov Processes and Viscosity Solutions. Berlin: Springer.

- [16] Gao, Hui, and Chuancun Yin. 2023. A Lévy risk model with ratcheting and barrier dividend strategies. Mathematical Foundations of Computing 6: 268–79.

- [17] Gerber, Hans U. 1979. Introduction to Mathematical Risk Theory. Richard D Irwin.

- [18] Gerber, Hans U., and Elias S. W. Shiu. 2004. Optimal dividends: Analysis with Brownian motion, North American Actuarial Journal 8: 1–20.

- [19] Goldie, C., N. Bingham, and J. Teugels. 1989. Regular Variation. Cambridge: Cambridge University Press.

- [20] Grandits, Peter, Friedrich Hubalek, Walter Schachermayer, and Mislav Žigo. 2007. Optimal expected exponential utility of dividend payments in Brownian risk model. Scandinavian Actuarial Journal 2: 73–107.

- [21] Jeanblanc-Picqué, Monique, and Albert Nikolaevich Shiryaev. 1995. Optimization of the flow of dividends. Russian Math. Surveys 50: 257–77.

- [22] Hardy, Godfrey H. 1912. Some results concerning the behaviour at infinity of a real and continuous solution of an algebraic differential equation of the first order. Proceedings of the London Mathematical Society 10: 451–68.

- [23] Hubalek, Friedrich, and Walter Schachermayer. 2004. Optimizing expected utility of dividend payments for a Brownian risk process and a peculiar nonlinear ODE. Insurance: Mathematics and Economics 34: 193–225.

- [24] Loeffen, Ronnie L. 2008. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. The Annals of Applied Probability 18: 1669–80.

- [25] Noba, Kei. 2021. On the optimality of double barrier strategies for Lévy processes. Stochastic Processes and their Applications 131: 73–102.

- [26] Marić, Vojislav. 1972. Asymptotic behavior of solutions of nonlinear differential equation of the first order. Journal of Mathematical Analysis and Applications 38: 187–92.

- [27] Paulsen, Jostein. 2007. Optimal dividend payments until ruin of diffusion processes when payments are subject to both fixed and proportional costs. Advances in Applied Probability 39: 669–89.

- [28] Rolski, Tomasz, Hanspeter Schmidli, Volker Schmidt, and Jozef L. Teugels. 1999. Stochastic processes for insurance and finance. New York: John Wiley and Sons, Inc.

- [29] Schmidli, Hanspeter. 2008. Stochastic Control in Insurance. Berlin: Springer.

- [30] Thonhauser, Stefan, and Hansjőrg Albrecher. 2011. Optimal dividend strategies for a compound Poisson risk process under transaction costs and power utility. Stochastic Models 27: 120–40.

- [31] Zhou, Xiaowen. 2005. On a classical risk model with a constant dividend barrier. North American Actuarial Journal 9: 1–14.

- [32] Zhu, Hang. 1991. Dynamic Programming and Variational Inequalities in Singular Stochastic Control. Doctoral dissertation, Brown University, Providence, RI, USA.