On Robustness of Double Linear Policy

with Time-Varying Weights

Abstract

In this paper, we extend the existing double linear policy by incorporating time-varying weights instead of constant weights and study a certain robustness property, called robust positive expectation (RPE), in a discrete-time setting. We prove that the RPE property holds by employing a novel elementary symmetric polynomials characterization approach and derive an explicit expression for both the expected cumulative gain-loss function and its variance. To validate our theory, we perform extensive Monte Carlo simulations using various weighting functions. Furthermore, we demonstrate how this policy can be effectively incorporated with standard technical analysis techniques, using the moving average as a trading signal.

Index Terms:

Stochastic Systems, Finance, Robustness, Time-Varying Parameter Systems, Positive Systems.I Introduction

The Robust Positive Expectation (RPE) is a property that ensures a trading policy has a positive expected profit robustly, and it is closely related to the stochastic positivity of a dynamical system in the control area. Some early work related to robustness issues in financial systems can be found in [1]. Later, a strategy called Simultaneous Long-Short (SLS) was proposed; see [2, 3], and shown to guarantee the RPE in markets with asset prices governed by geometric Brownian motion (GBM).

Later, several extensions were proposed in the literature, including generalization for Merton’s diffusion model in [4], GBM model with time-varying parameters in [5], and any linear stochastic differential equation (SDE) in [6]. Additionally, the SLS strategy was extended to the proportional-integral (PI) controller in [7], to the latency trading in [8], and coupled SLS strategy on pair trading for two correlated assets was studied in [9, 10]. In [11], a robust design strategy for stock trading via feedback control is proposed. [12] proposed a generalized SLS with different weight settings on long and short positions. Recently, [13] considered a long-only affine feedback control with a stop-loss order.

In [14], a modified SLS strategy, called double linear policy, was proposed to solve an optimal weight selection problem using the mean-variance approach in a discrete-time setting while preserving the RPE property. Then [15] established a sufficient condition of RPE when the transaction costs are present. However, previous work including [14, 15] and many SLS literature assumed constant weight, investing the same proportion of account value in each stage. This paper extends the weight of double linear policy from constant to a broad class of time-varying functions in a discrete-time setting and proves that the RPE property still holds for this extension.

I-A Contributions of the Paper

Proving an RPE property for a policy with time-varying weights is known to be challenging.111The conventional method for proving RPE of a trading policy with constant weight often relies on a key identity that for all and . However, this approach may not apply when varies over time, as in the case of the policies with time-varying weights. This paper addresses this challenge by using a novel elementary symmetric polynomials characterization approach. We extend the existing results by showing that the RPE property holds for the double linear policy with time-varying weights. Closed-form expressions for the expected cumulative gain-loss function and its variance are provided. Additionally, we illustrate how the proposed policy can be incorporated with the common technical analysis technique. The results presented in this paper contribute to the literature on robustness in financial systems.

II Problem Formulation

For stage let be the underlying risky asset price at stage . Then the associated per-period return is given by Assume that for all with probability one, and known bounds . Additionally, assume that and are in the support of . Furthermore, assume that are independent with a common mean and common variance for all .222This setting does not assume an underlying stochastic process governing the prices of the risky asset and is less restrictive than the typical independent and identically distributed returns assumption. In the sequel, we assume that the trades incur zero transaction costs and that the underlying asset has perfect liquidity. This setting serves as a good starting point for building the model and is closely related to the frictionless market in finance; see [16].

II-A Double Linear Policy with Time-Varying Weights

In [14] and many SLS literature, the trading policy is proposed with constant weights. This paper extends the constant weights to a time-varying weighting function. With initial account value , we spilt it into two parts: Taking a fraction , define as the initial account value for long position and for short position. If , we are in a long-only position while corresponds to a pure short position.

The trading policy is given by , where and are of double linear forms:

| (1) |

The weighting function for all with and is assumed to be causal; i.e., it may depend only on the information up to stage . Any is called admissible weight. This condition is closely related to the survival trades; see Section II-B. Hence, the account values under the double linear policy and , denoted by and , can be described as the following linear time-varying stochastic difference equation:

where is a riskless rate for a bank account or a treasury bond.333In practice, when shorting an asset, the corresponding proceeds are typically held as collateral by the broker to cover any potential losses from the short position. These proceeds are generally not available for immediate reinvestment into a riskless asset, such as a bank account or treasury bond. Note that when , account profit increases. Hence, as seen later in sections to follow, when studying the robustness of the double linear policy, we assume without loss of generality . Then the account value for long position reduce to . Therefore, the overall account value for both long and short positions at stage is given by

where and .

II-B Survivability Considerations

Fix and , we ensure that the trades are survivable for all ; i.e., the -value that can potentially lead to is disallowed. To see this, for stage , fix . We observe that for the long position, we have since and . On the other hand, for the short position, we also have since . Therefore, the overall account value satisfies for all with probability one.

II-C Robust Positive Expectation Problem

The primary objective of this paper is to study the following RPE problem.

Definition 2.1 (Robust Positive Expectation).

For stage , let be the initial account value, and be the account value at stage . Define the expected cumulative gain-loss function up to stage as . A trading policy is said to have a robust positive expectation (RPE) property if it ensures that for all and under all market conditions.

III Gain-Loss Analysis

For , let and . With , consider the double linear policy with and weight for all . The cumulative trading gain-loss function up to stage is given by

and the expectation is . If the weights are constant; i.e., for all , then the RPE property is readily established when , see [15]. However, difficulties arise when the weighting function is time-varying. To address this, a set of elementary symmetric polynomials444 We say that is a symmetric polynomial if for any permutation of the subscripts , it follows that . in variables, , are considered and defined as with

for . Note that for all and , which is the sum of the th multiplication term of admissible weights. The following example illustrates the calculation of elementary symmetric polynomials.

Example 3.1 (Elementary Symmetric Polynomials).

This example illustrates the calculation of the elementary symmetric polynomials . Specifically, for , the polynomials to be calculate is which is given by For stage , the elementary symmetric polynomials are given by

Similarly, for , the elementary symmetric polynomials becomes

As seen later in this section, the representation of elementary symmetric polynomials is useful for proving the RPE property; see Lemmas 3.2 and 3.3 to follow. Define shorthand notations and . With the aid of the independence of , it follows that and .

Lemma 3.2.

Fix Let and for all , and for stage satisfies

On the other hand, for , and satisfies

Proof.

We use a shorthand notation for in the proof. Fix . Now for the case , which is an odd number, is given by

where the last equality separates terms into odd and even cases. Likewise, for is

On the other hand, for the even number case , with an almost identical argument, it is readily verified that and and the proof is complete. ∎

Lemma 3.3.

For , provided that at least two weights for some and .

Proof.

Fix . Then Proceed a proof by induction. If , which corresponds to Since we are assuming that at least two weights are strictly positive, in this case, it corresponds to . Therefore, Next, assuming that for at least two weights for some , we must show Note that

where the last inequality holds by inductive hypothesis that for at least two weights, say for some and the fact that the sum . ∎

Theorem 3.4 (RPE with Time-Varying Weights).

Let . Consider a double linear policy with and weights for all . Then, the expected cumulative gain-loss function is given by

Moreover, when and with at least two weights being strictly positive, the RPE property holds; i.e., for and all .

Proof.

To calculate the expected cumulative gain-loss function, we use the fact that per-period returns are independent with common mean for all . Thus, it is readily verified that

which is identical to the desired equality in the statement of the theorem. To complete the proof, we now show that the RPE property holds. Fix . Consider two cases by splitting into odd and even numbers. We begin by considering with , corresponding to an odd number. Then, using Lemma 3.2 for the odd case, we have

Since , we have for all and . Hence, it follows that and . In addition, for , the expected cumulative gain-loss function becomes

Since , and at least two weights are strictly positive for some with , Lemma 3.3 indicates that . It follows that . On the other hand, consider the case , which is an even number. Using the second part of Lemma 3.2, we obtain

A similar argument can be made for showing that for all and . Hence, taking , using the fact that at least two weights are strictly positive, and Lemma 3.3, we again have when , which completes the proof. ∎

Remark 3.5.

. Theorem 3.4 can be viewed as an extension of the existing RPE result using double linear policy with constant weights stated in [14]. That is, by taking for all , one readily obtains

If and , the desired strict positivity holds; i.e., for and all . . According to Theorem 3.4, it is readily verified that the expected cumulative gain-loss function satisfies for all if .

Lemma 3.6 (Variance of the Gain-Loss Function).

Let . Consider a double linear policy with and weights for all then the variance of the cumulative gain-loss function is given by

Proof.

The proof is based on straightforward calculation on . We first calculate the second moment of the gain-loss function: With the aid of the independence of , a lengthy but straightforward calculation leads to

| (2) |

Then we calculate the square of the expected cumulative gain-loss function. That is,

| (3) |

In combination with Equations (III) and (III), a lengthy but straightforward calculation again leads to the desired expression for the variance of the gain-loss function. ∎

IV Illustrative Examples

This section illustrates the robustness of the double linear policy with time-varying weights using various examples.

Example 4.1 (GBM with Jumps).

We now collect historical daily prices for Apple Inc. (Ticker: AAPL) over a one-year period from January 2022 to December 2022.555Note that this one-year period provides a good test case since 2022 is often described as a bearish market. Having estimated the volatility , we simulate the associated GBM prices with jumps, see [17], using Monte Carlo simulations. That is, for , we generate the price governed by the following stochastic differential equation:

| (4) |

where is a standard Wiener process, is the drift constant, is the volatility constant, is a Poisson process with that is independent with , is the average rate of the jump that occurs for the process, and is the magnitude of the random jump.666For 252 daily data, the drift rate and volatility constants can be approximated by using and . When , Equation (4) reduces to GBM. While it is not shown in this paper, the double linear policy (1) assures RPE for the GBM case as well.

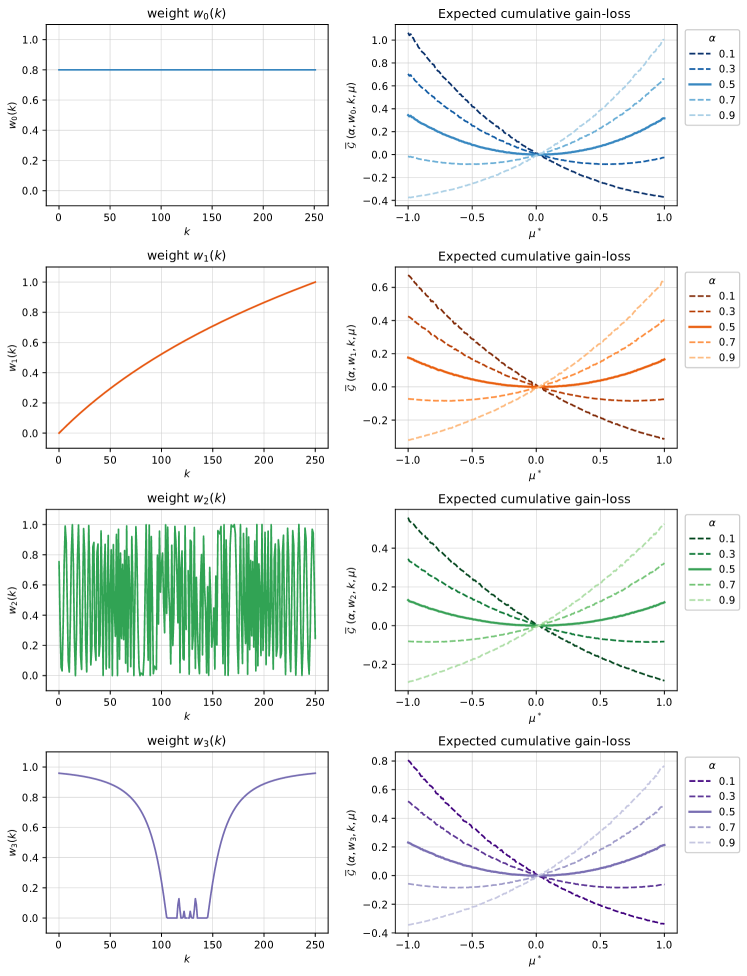

To simulate the price, we discretize the process (4) by taking a time period length of and for one year with an annualized drift rate , annualized volatility computed from historical data , jump intensity with a jump size . With initial account value , we consider four admissible weighting functions defined by for with

where and is an indicator function satisfying for and zero otherwise.

The four weighting functions above represent different investment philosophies. For example, represents a constant buy-and-hold strategy, represents an increasing investing strategy over the specified period, corresponds to a more active trading approach, and represents investing more at the beginning and end of the period, with little or no investment in the middle. Consistent with the simulations conducted in [14], we generate GBM sample paths for each and various . Then we calculate the average cumulative gain-loss; see Figure 1. For , the positive expectation gain is seen for all four weighting functions.

Example 4.2 (Minute-by-Minute Case).

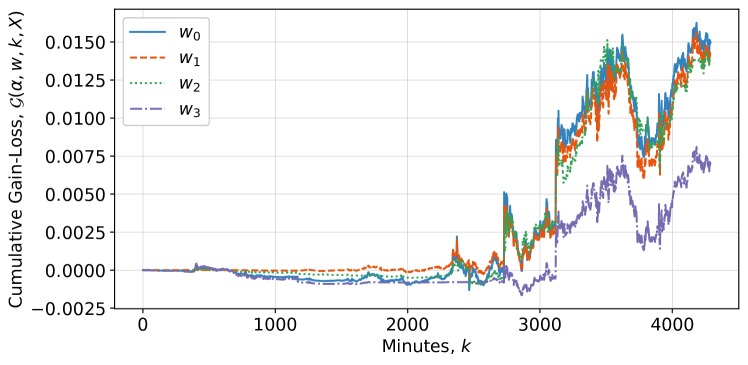

In this example, we study the performance of the double linear policy using relatively high-frequency minute-by-minute price data for Twitter Inc. (Ticker: TWTR) between May 4, 2022, and May 19, 2022.777During this period, CEO Elon Musk announced that the Twitter deal was temporarily put on hold on May 13, causing a 9.7% decreases in shares at market close. The data is retrieved using the Bloomberg Terminal. The price trajectory for the specific period is shown in Figure 2. The figure also includes a subplot with a magnified view for the interval minutes, featuring various moving average lines, which will be used in the next example.

We now examine the trading performance of the double linear policy using the same four weighting function for described in Example 4.1. Specifically, with and initial account value , the corresponding trading gain-loss trajectories are shown in Figure 3. In contrast to the negative returns obtained by the buy-and-hold (B&H) long-only strategy with constant weight , we note that all the proposed weighting functions of the double linear policy assured positive trading gains for the Twitter data. Table I also summarizes another performance metric, such as variances and Sharpe ratio. It is also worth mentioning that similar findings hold for flipped TWTR price data, indicating the robustness of double linear policy and an ability to capture underlying market dynamics in both bull and bearish markets.

| B&H | |||||

| Gain-Loss | -0.2003 | 0.0150 | 0.0142 | 0.0138 | 0.0070 |

| Variance | 0.0066 | 2.9e-05 | 2.3e-05 | 2.6e-05 | 6.2e-06 |

| Sharpe Ratio | -1.6878 | 1.2106 | 1.2308 | 1.4722 | 0.9497 |

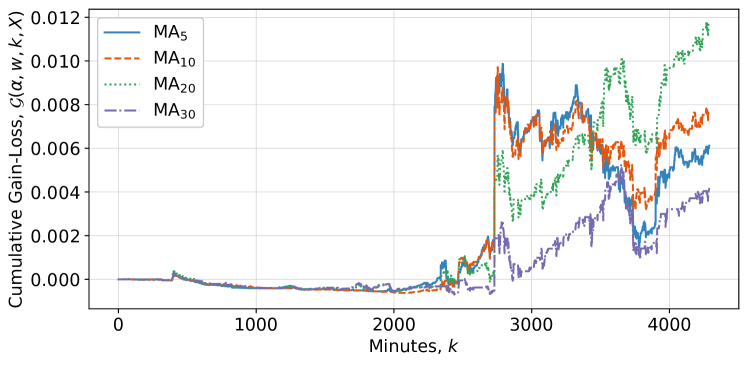

Example 4.3 (Blending Moving Average Indicator).

In this example, we blend the use of the moving average indicator, a common method in technical analysis, as a criterion for designing the weighting function into the double linear policy. This approach enables dynamic adjustment of the investment based on the indicator. The weighting function used in the double linear policy (1) is defined as

| (5) |

where and represent the last -period average stock price for . For example, in the case of minutely data, , , , represent the last 5-minute, 10-minute, 20-minute, and 30-minute average stock price, respectively. The investment philosophy is to invest only when the stock price is higher than the moving average, which signals a buying opportunity.

With , , and , we summarize the cumulative gain-loss, variance, and Sharpe ratio in Table II, and the trading trajectories are shown in Figure 4. From the table, we see that leads to the best performance in terms of the Sharpe ratio. In all cases, we see positive returns using the weighting functions incorporated with the moving average indicator. Also, while not demonstrated in this paper, the MA indicator in Equation (5) can be readily replaced by another technical analysis indicator, such as weighted moving average, moving median, moving average convergence and divergence (MACD) and so on.

| Gain-Loss | 0.0061 | 0.0076 | 0.0117 | 0.0042 |

| Variance | 9.7e-06 | 1.1e-05 | 1.4e-05 | 2.2e-06 |

| Sharpe Ratio | 0.7097 | 0.8806 | 1.6343 | 0.8651 |

V Concluding Remarks

This paper extends the double linear policy by incorporating time-varying weights in a discrete-time setting. Using a set of elementary symmetric polynomials, we prove that the RPE property is preserved in the extended policy. In addition, we derive an explicit expression for the expected cumulative gain-loss function and its variance. We conducted extensive Monte Carlo simulations using various weighting functions to validate our theory. Our results also show that the extended double linear policy with time-varying weights can be integrated with the standard technical analysis technique such as moving average.

In future research, it would be interesting to expand our analysis to a multi-asset case, where the weights can be optimized for a portfolio of assets; see [14] for an initial approach. Additionally, one valuable direction would be to investigate the impact of serial-correlated returns on the performance of the double linear policy with time-varying weights. For example, an Auto-Regressive (AR) return model might be worth pursuing. Finally, the impact of transaction costs could be considered to assess the practicality of the proposed policy in real-world applications; see [15].

References

- [1] N. Dokuchaev, Dynamic Portfolio Strategies: Quantitative Methods and Empirical Rules for Incomplete Information, vol. 47. Springer Science & Business Media, 2002.

- [2] B. R. Barmish and J. A. Primbs, “On Arbitrage Possibilities via Linear Feedback in an Idealized Brownian Motion Stock Market,” in Proceedings of the IEEE Conference on Decision and Control (CDC) and European Control Conference (ECC), pp. 2889–2894, 2011.

- [3] B. R. Barmish and J. A. Primbs, “On a New Paradigm for Stock Trading via a Model-Free Feedback Controller,” IEEE Transactions on Automatic Control, vol. 61, no. 3, pp. 662–676, 2015.

- [4] M. H. Baumann, “On Stock Trading via Feedback Control when Underlying Stock Returns Are Discontinuous,” IEEE Transactions on Automatic Control, vol. 62, no. 6, pp. 2987–2992, 2016.

- [5] J. A. Primbs and B. R. Barmish, “On Robustness of Simultaneous Long-Short Stock Trading Control with Time-Varying Price Dynamics,” IFAC-PapersOnLine, vol. 50, no. 1, pp. 12267–12272, 2017.

- [6] M. H. Baumann and L. Grüne, “Positive Expected Feedback Trading Gain for All Essentially Linearly Representable Prices,” in Proceedings of the Asian Control Conference (ASCC), pp. 150–155, 2019.

- [7] S. Malekpour, J. A. Primbs, and B. R. Barmish, “A Generalization of Simultaneous Long–Short Stock Trading to PI Controllers,” IEEE Transactions on Automatic Control, vol. 63, no. 10, pp. 3531–3536, 2018.

- [8] S. Malekpour and B. R. Barmish, “On Stock Trading Using a Controller with Delay: The Robust Positive Expectation Property,” in Proceedings of the IEEE Conference on Decision and Control (CDC), pp. 2881–2887, 2016.

- [9] A. Deshpande and B. R. Barmish, “A Generalization of the Robust Positive Expectation Theorem for Stock Trading via Feedback Control,” in Proceedings of the European Control Conference (ECC), pp. 514–520, 2018.

- [10] A. Deshpande, J. A. Gubner, and B. R. Barmish, “On Simultaneous Long-Short Stock Trading Controllers with Cross-Coupling,” IFAC-PapersOnLine, vol. 53, no. 2, pp. 16989–16995, 2020.

- [11] G. Maroni, S. Formentin, and F. Previdi, “A Robust Design Strategy for Stock Trading via Feedback Control,” in Proceedings of the European control conference (ECC), pp. 447–452, 2019.

- [12] J. D. O’Brien, M. E. Burke, and K. Burke, “A Generalized Framework for Simultaneous Long-Short Feedback Trading,” IEEE Transactions on Automatic Control, vol. 66, no. 6, pp. 2652–2663, 2020.

- [13] C.-H. Hsieh, “Generalization of Affine Feedback Stock Trading Results to Include Stop-Loss Orders,” Automatica, vol. 136, p. 110051, 2022.

- [14] C.-H. Hsieh, “On Robust Optimal Linear Feedback Stock Trading,” arXiv preprint arXiv:2202.02300, 2022.

- [15] C.-H. Hsieh, “On Robustness of Double Linear Trading with Transaction Costs,” IEEE Control Systems Letters, vol. 7, pp. 679–684, 2022.

- [16] R. C. Merton, Continuous-Time Finance. Blackwell Cambridge, MA, 1992.

- [17] A. Etheridge and M. Baxter, A Course in Financial Calculus. Cambridge University Press, 2002.