Cascading Waves of Fluctuation in Time-delay Multi-agent Rendezvous

Abstract

We develop a framework to assess the risk of cascading failures when a team of agents aims to rendezvous in time in the presence of exogenous noise and communication time-delay. The notion of value-at-risk (VaR) measure is used to evaluate the risk of cascading failures (i.e., waves of large fluctuations) when agents have failed to rendezvous. Furthermore, an efficient explicit formula is obtained to calculate the risk of higher-order cascading failures recursively. Finally, from a risk-aware design perspective, we report an evaluation of the most vulnerable sequence of agents in various communication graphs.

I Introduction

In the past decades, consensus networks have shown spectacular advantages in coordinating the networked control systems, e.g., [6, 4]. However, like “every coin has two sides”, consensus networks or cyber-physical systems also show their vulnerability to large-scale failures [3, 18, 7]. Given that most consensus networks suffer from communication or other physically induced limitations (e.g., time-delay), as well as external disturbances (e.g., biased opinion or noisy sensor measurements), individuals within the network will be inevitably driven away from the consensus and enter failure states. These failures are prone to cascade in the system and cause new failures to emerge [8, 9]; then, one needs to investigate how the existing failures are going to impact the rest of the system, i.e., the cascading (domino) effect, as well as developing systemic techniques to quantify such effects.

The domino effects in the systemic failure navigate our interests towards the cascading failures [14, 25, 26], and how their emergence will impact the system’s safety. In other words, we aim to investigate how resilient the system is while multiple failures have already occurred in the system, as well as how likely the failure will cascade. Probing into the cascading failures and their emergence have many practical meanings from the system design perspective: It is essential to evaluate the performance of the networked control system under the impact of the existing failures, or, in other words, the ability to isolate the propagation of existing failures and keep the rest of the system safe.

In this paper, we will develop a theoretical framework based on systemic risk analysis [16, 17] to evaluate the possibility of cascading failures in the consensus network. Our objective is to utilize the risk quantification regime, e.g., the value-at-risk measure, to assess how likely the existing failures in the consensus network can trigger future failures throughout the system. Providing the quantification of such effects will give valuable insights into the networked control systems design and highlight the potential of a networked system to suffer from cascading systemic failures.

We consider the motivational scenario as a network of autonomous agents that aim to achieve rendezvous in time [21]. It is assumed that agents communicate over a time-invariant network with lagged transmission and processing of information from other agents. The network is also perturbed by statistical noise applied to each agent independently. The noise models the effect of external perturbations and turns the system into a stochastic dynamical network. We will focus on studying the event of a large fluctuation, i.e., failing to reach the rendezvous in time, given that some agents have already deviated from the consensus.

Our Contributions: As a natural outgrowth of our recent works on first-order linear consensus networks [22, 19, 21, 9], this paper generalizes the concept of the cascading failures of two agents [8, 9] into the situation when there exists an arbitrary number of failures [10]. First, we examine the value-at-risk measure of cascading failures in the steady-state distribution of observables for a time-delayed linear consensus network. In particular, explicit formulas are obtained for the risk of large fluctuation, given that other agents have failed to reach the consensus. Then, with extensive simulations, we evaluate the most vulnerable sequence of agents in a network, which is exclusively obtained with the generalized cascading risk for multiple existing failures.

II Mathematical Notation

We denote the non-negative orthant of the Euclidean space by , its set of standard Euclidean basis by , and the vector of all ones by . The absolute value operation for vectors is defined element-wise, i.e., .

Algebraic Graph Theory: A weighted graph is defined by , where is the set of nodes, is the set of edges (feedback links), and is the weight function that assigns a non-negative number (feedback gain) to every link. Two nodes are directly connected if and only if .

Assumption 1.

Every graph in this paper is connected. In addition, for every , the following properties hold:

-

•

if and only if .

-

•

, i.e., links are undirected.

-

•

, i.e., links are simple.

The Laplacian matrix of is a matrix with elements

where . The Laplacian matrix of a graph is symmetric and positive semi-definite [24]. Assumption 1 implies the smallest Laplacian eigenvalue is zero with algebraic multiplicity one. The spectrum of can be ordered as The eigenvector of corresponding to is denoted by . By letting , it follows that with . We normalize the Laplacian eigenvectors such that becomes an orthogonal matrix, i.e., with .

Probability Theory: Let be the set of all valued random vectors of a probability space with finite second moments. A normal random variable with mean and covariance matrix is represented by . The error function is which is invertible on its range as . We employ standard notation for the formulation of stochastic differential equations.

III Problem Statement

We consider the class of time-delay linear consensus networks that have found wide applications in engineering, such as clock synchronization in sensor networks, rendezvous in space or time, and heading alignment in swarm robotics; we refer to [15, 11] for more details. As a motivational application, we consider the rendezvous problem in time where the group objective is to meet simultaneously at a prespecified location known to all agents.111Rendezvous in space is very similar to rendezvous in time by switching the role of time and location. Agents do not have a priori knowledge of the meeting time as it may have to be adjusted in response to unexpected emergencies or exogenous uncertainties [15]. Thus, all agents should agree on a rendezvous time by achieving consensus. The consensus can be accomplished by each agent creating a state variable, say , representing its belief of the rendezvous time. Each agent’s initial belief is set to its preferred time that it can rendezvous with others. Then, the rendezvous dynamics for each agent evolve in time according to the following stochastic differential equations:

| (1) |

for all . Each agent’s control input is . The source of uncertainty is diffused in the network as additive stochastic noise, and its magnitude is uniformly scaled by the diffusion coefficient . The impact of uncertain environments on the dynamics of agents is modeled by independent Brownian motions . In most real-world situations, agents experience a time-delay accessing, computing, or sharing their own and neighboring agents’ state information [15]. Hence, all agents are assumed to experience an identical time-delay . The control inputs are determined via a negotiation process by forming a linear consensus network over a communication graph using feedback law

| (2) |

where are non-negative feedback gains. Let us denote the state vector by , and the vector of exogenous disturbance by . The dynamics of the resulting closed-loop network can be cast as a linear consensus network that is governed by the time-delayed stochastic differential equation

| (3) |

for all , where the initial function is deterministically given for and . The underlying coupling structure of the consensus network (3) is a graph that satisfies Assumption 1 with Laplacian matrix . It is considered that the communication graph is time-invariant such that the network of agents aim to reach a consensus on a rendezvous time before they perform motion planning to get to the meeting location. Upon reaching a consensus, a properly designed internal feedback control mechanism steers each agent toward the rendezvous time.

Assumption 2.

The time-delay satisfies .

When there is no noise, i.e., , it is known [12] that under Assumption 1 and 2, states of all agents converge to the average of all initial states ; whereas in the presence of input noise, state variables fluctuate around the average value . To quantify the quality of rendezvous and its fragility features, we consider the vector of observables

| (4) |

in which is the centering matrix and the observable measures the agents’ deviations from consensus. Assumption 1 implies that one of the modes of network (3) is marginally stable. The marginally stable mode, which corresponds to the zero eigenvalue of , is unobservable from the output (4), which keeps bounded in the steady-state. When the noise is absent, we have as . Consequently, the exogenous noise excites the observable modes of the network, and the output fluctuates around zero. This implies that agents will not agree upon an exact rendezvous time. A practical resolution is to allow a tolerance interval for agents to concur.

Definition 1.

For a given tolerance level , the consensus network (3) reaches -consensus if it can tolerate some degrees of disagreement such that

| (5) |

holds with high probability222The high probability means a probability larger than a predefined cut-off number close to one..

The notion of -consensus means that all agents have agreement on all points in . Suppose that event (5) holds, then the network of agents will achieve a -consensus over the rendezvous time in the following sense. In steady-state, the ’th agent is assured that by units of time, all other agents will arrive and meet each other in that time interval with high probability. At the same time, some undesirable situations that we refer to as systemic failures may also happen.

Definition 2.

For a given tolerance level , an agent with observable is prone to systemic failure, i.e., the large fluctuation, if the probability of the stochastic event

| (6) |

is nonzero as .

The problem is to quantify the risk of large fluctuations conditioned on the knowledge that a subset of agents has already deviated from the consensus. We refer to this quantity as the cascading risk of large fluctuations, and our goal is to characterize its value as a function of the underlying communication graph topology, time-delay, and statistics of noise. To this end, we will develop a general framework to assess the cascading risk of large fluctuations using the steady-state statistics of the closed-loop system (3).

The rest of the paper is organized as follows. First, in §IV, we present a few key preliminary results on the steady-state behavior and statistics of the noisy consensus network. These results help us shape the closed-form risk formula of cascading failures in §V, which constitutes the main contribution of this work. Finally, in §VI, we also present an update law that reveals the evolution of the cascading risk when new failures are discovered in the system. All proofs of theoretical results are shown in the appendix of this paper.

IV Preliminary Results

In this section, we present the steady-state statistics of network observables under external disturbances and time-delay. Such statistics form the foundation for the latter results on the value-at-risk measure.

IV-A Steady-State Statistics of Observables

Let us denote the steady-state value of the observable by whenever it exists. It is known from [21] that if Assumption 1 and 2 are satisfied, as , the statistics of steady-state observables (4) follows a normal distribution , where is a covariance matrix .

Lemma 1.

The elements of are given by

| (7) |

where denotes the ’th column of for all .

For simplicity, we write the diagonal elements as . One can also find out that the cross-correlation is independent of , the magnitude of external noises. This observation implies that the probabilistic interrelation between two agents originates from the time-delay and the communication graph but not the magnitude of the stochastic perturbation.

IV-B Value-at-Risk Measure

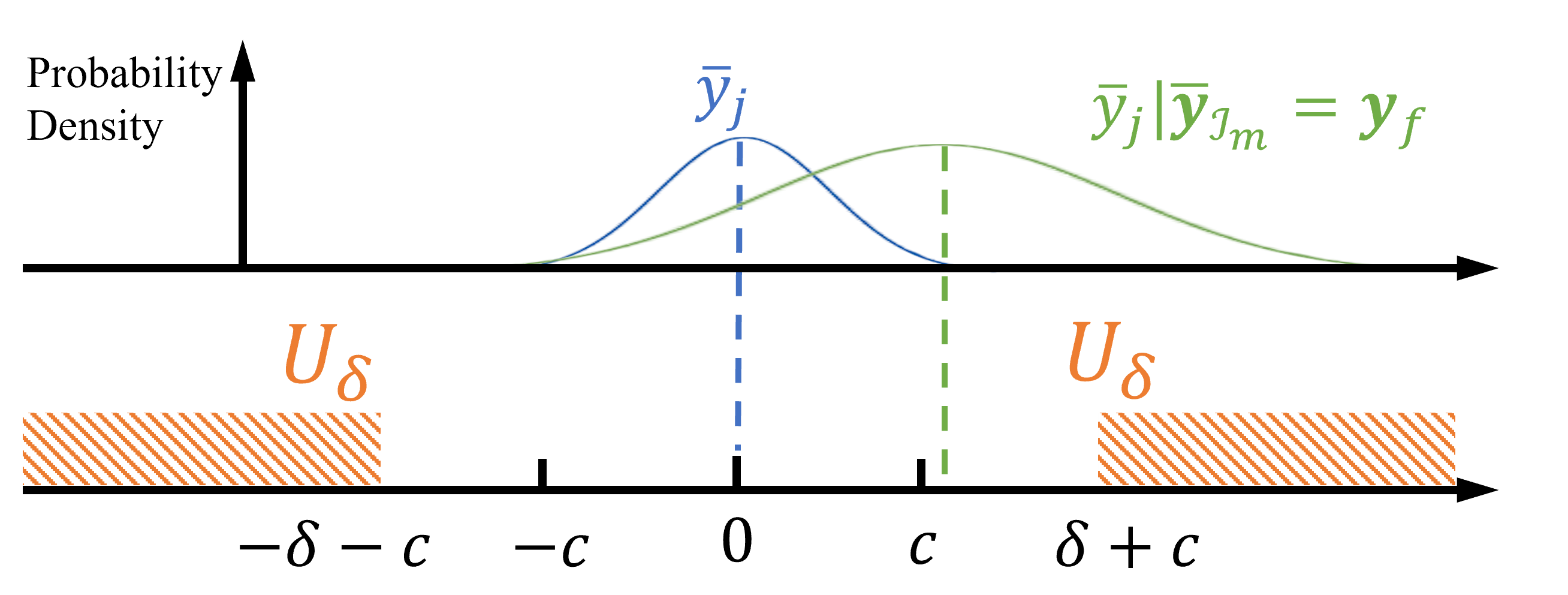

To quantify the uncertainty level encapsulated in agents’ observables, we employ the notion of Value-at-Risk (VaR) measure [5, 16, 22, 20]. The VaR indicates the chance of a random variable landing inside an undesirable set of values that characterizes a systemic failure. The set of such undesirable values is referred to as a systemic set and denoted by . In probability space , the set of systemic events of random variable is defined as . We define a collections of supersets of that satisfy the following conditions for any sequence with property

-

•

when

-

•

.

In practice, one can tailor the super-sets to cover a suitable neighborhood of to characterize alarm zones as a random variable approaches . For a given , the chance of indicates how close can get to in probability. For a given design parameter , the VaR measure is defined by

where a smaller indicates a higher level of confidence on random variable to stay away from . Let us elaborate and interpret what typical values of imply. The case signifies that the probability of observing dangerously close to is less than . We have if and only if for with probability less than . In addition to several interesting properties (see for instance [1, 2, 20]), the risk measure is non-increasing with . We refer to Fig. 1 for an example.

V Risk of Cascading Failures

As a natural outgrowth of our previous work [9], we generalize the definition of the “cascading failures” from assuming only one existing failure into an arbitrary number of existing failures [10]. To this end, let us consider the risk of cascading large fluctuation for the ’th agent, assuming that agents with ordered indices for some have failed to reach the consensus, where and . To evaluate the effect of the prior large fluctuations on the ’th agent, let us form a block covariance matrix

| (8) |

where , and . The values of s are computed using the result from (7).

We also denote that observables of the failed agent are represented by vector . For instance, when the ’th agent failed to each the consensus, one may set the value of to satisfy . To obtain the statistics of the observable when multiple failures occur, one should calculate the steady-state conditional probability distribution of given within a multivariate normal distribution, where .

Lemma 2.

The above lemma reveals the statistics of the observables when there exist multiple large fluctuations (failures) in the consensus network. In this scenario, we aim to evaluate the risk of cascading failure on the ’th agent. The corresponding event is shown by

where the family of risk set333It should be noted that in our definition of for -consensus, the family of supersets obviously depends on but its dependency to this parameter is omitted from for notational simplicity. of cascading failure for the ’th agent is given by

with and . Then, the value-at-risk measure for the cascading failure on the ’th agent is defined as

| (10) |

where takes value in . The cascading risk takes value in , and it measures the chance of an agent failing to reach the consensus given that other agents have failed to rendezvous.

For the exposition of the next result, we introduce the following notation:

| (11) |

with and defined in Lemma 2. The notation below is also introduced for simplicity,

| (12) |

Theorem 1.

The two cases of the cascading risk value are self-explanatory. The case indicates the scenario when the probability of the ’th agent failing to reach consensus is always less than , which commonly corresponds to a low confidence level or the conditional distribution that lands away from the undesired set of the observable values. In the other case, the risk obtains a positive value based on the solution of (12). A higher value of usually indicates a higher chance that the cascading failure will occur in the system. The value of will also play the role as a design parameter when since the system will reach the consensus with the confidence level .

When the existing failures are not correlated to the ’th agent, i.e., , the cascading risk expression boils down to the risk of large fluctuation for a single agent to rendezvous,

where . This formula expands the risk of large fluctuations expression derived in [21], which considers deviations on -consensus state for .

Given that agents have failed to reach the -consensus, one can formulate the risk profile of the network by stacking up all the cascading risk among remaining agents with a systemic risk profile vector as follows

where if .

VI The Update Law for the Cascading Risk Computation

In this section, let us consider the scenario where agents with labels are found in failure states, and we aim to update the statistics of the agent of interest, i.e., , when a new failure at agent is discovered. For the exposition of the next result, let us introduce the following notations

| (13) | ||||

where the value of are computed using (7), the values of are given by (8) in the view of the agent 444The values of are obtained with agent , respectively., and the matrix is computed using (8).

Theorem 2.

Suppose that follows when agents have already failed with labels . The updated conditional distribution of when a new agent fails, i.e., agent with observable , is given by , such that

| (14) |

where

and the value of are computed using (13).

The above result provides a good insight into the change in the conditional mean and covariance of an agent when the number of failed agents increase from to . Interestingly, the conditional covariance of the agent is independent of the value of the deviation of the failed agent . However, the conditional mean of the agent depends on the difference between the conditional mean of the failed agent , when failures have occurred, and its current value of the failed observable, . In the unlikely case of , the conditional mean of the agent remains unchanged.

In addition, the above result can be applied to find the sequence of agents with maximum risk after each additional failure. This information can be very helpful in designing an optimal communication network to protect a sequence of agents that is most vulnerable to cascading systemic failures.

VII Case Studies

We discuss the case studies for the rendezvous problem with the consensus dynamics governed by (3) among the complete, path, and the p-cycle communication graphs [24]. In all case studies, we consider agents with labels cannot achieve the -consensus and have been found with large fluctuations . Let us consider for all simulations.

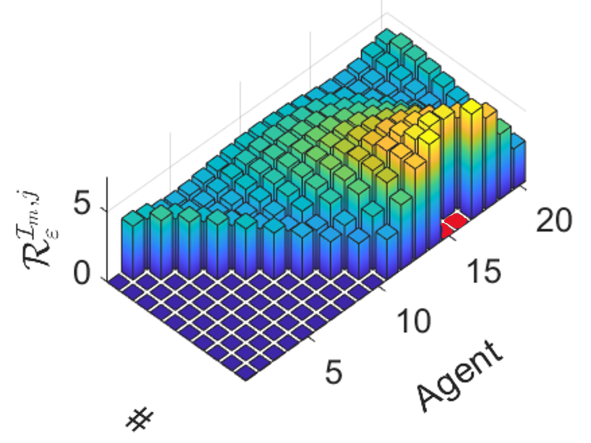

VII-A Risk of Cascading Large Fluctuation

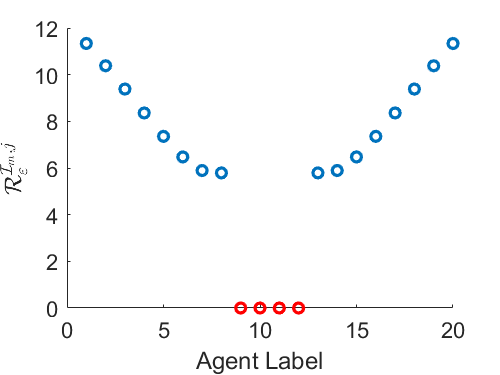

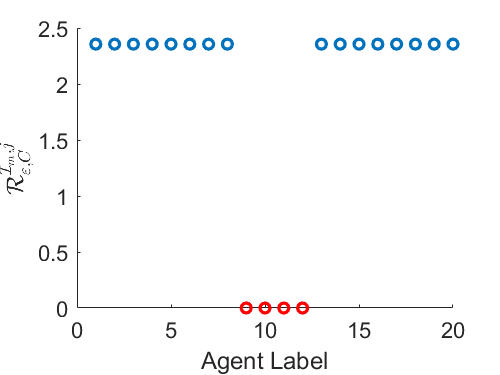

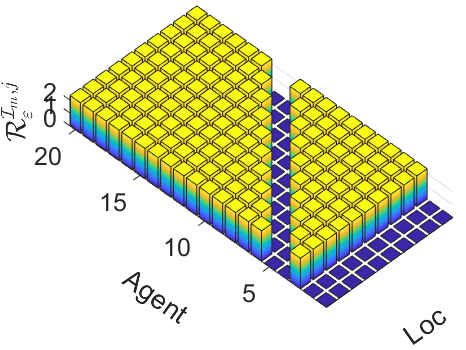

The risk profile of the cascading failure to reach -consensus is computed using the closed-form expression derived in Theorem 1 for various unweighted communication graph topologies, which is shown in Fig. 2. There are a few interesting results worth reporting: In path graph [24], it is shown that the riskiest agent is found at both ends of the graph when there exist multiple failures in the system; In cycle graphs [24], one can observe that the risk profile pattern converges to the complete graph as increases. Finally, the complete graph shows that the risk value remains unchanged regardless of the agent of the interest.

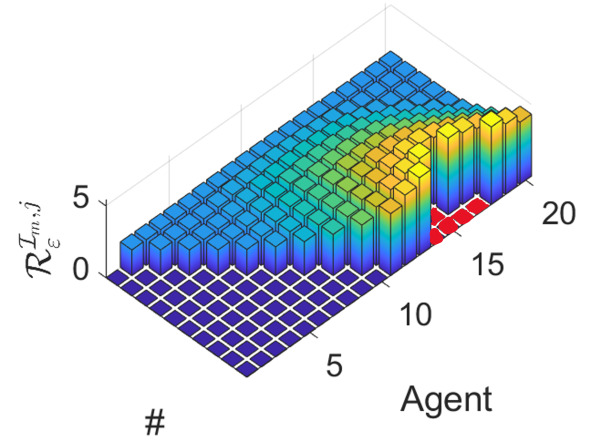

VII-B Characteristics of Existing Failures

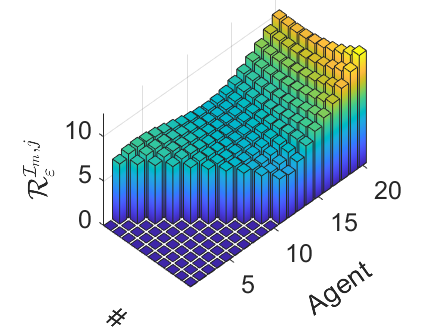

In the cascading risk, the characteristics of the existing failures will profoundly affect the cascading risk profile. For instance, the number of existing failures and their spatial distribution in the network reshapes the cascading risk profile in various networks. This phenomenon is examined in Fig. 3, in which a different number of failures and various failures distribution are considered. Some of these results can be validated with our theoretical findings, e.g., in a complete graph, the risk profile obtains a constant value with a fixed number of existing failures, regardless of their spatial distribution in the communication graph.

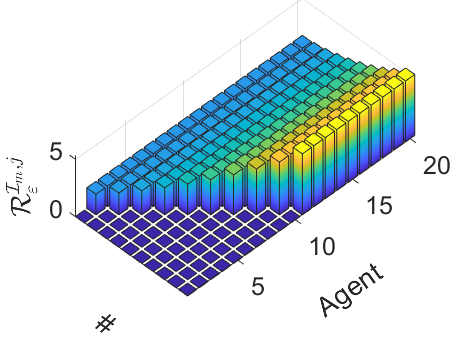

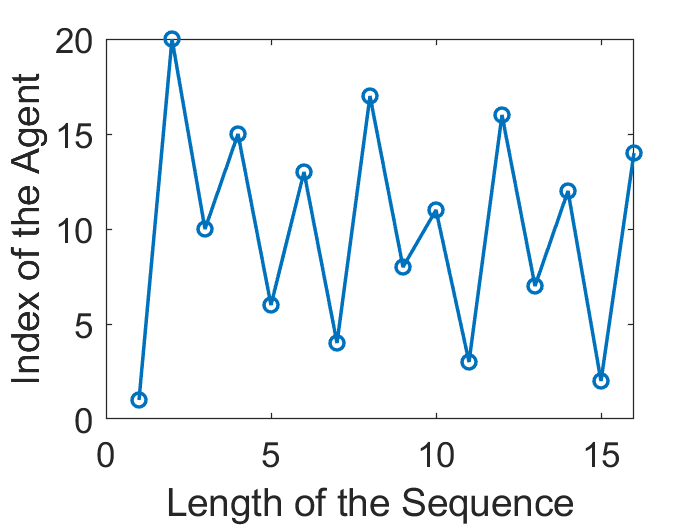

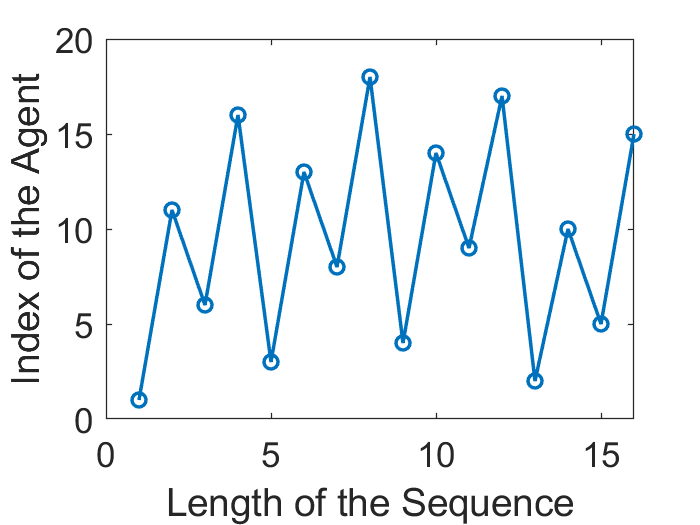

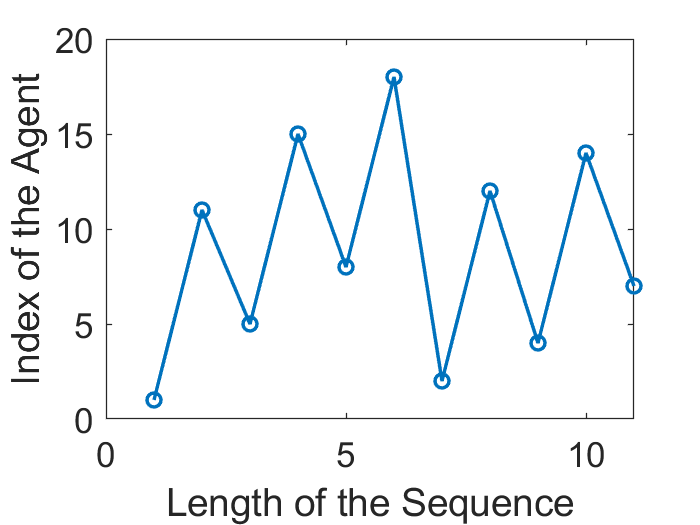

VII-C Most Vulnerable Sequence

We also explore the emergence of the most vulnerable sequence of agents prone to cascading failures (Fig. 4). The most vulnerable sequence can be assessed by first finding the agent that obtains the highest risk and then finding the next most vulnerable agent by evaluating the cascading risk with the assumption that the previously found agents have failed to reach the consensus. The result in the complete graph indicates that any arbitrary sequence of agents is identically vulnerable since the agents will always obtain the same value of cascading risk in a complete graph. The investigation of the most vulnerable sequence provides information from the network design perspective such that one can adjust the systemic design based on the priority of the agents in the network.

VIII Conclusion

To investigate the emergence of the cascading waves of fluctuations in the time-delay multi-agent systems, we develop a methodology to evaluate the risk of cascading failures using the notion of value-at-risk measure. The proposed cascading risk framework is a natural outgrowth of single event risk measure [9], and it shows a significant advantage compared to the previous works as it can explore the scenarios when multiple system failures exist. In addition, to provide insights from the design perspective, we explore the time-delay induced hard limits on the best achievable levels of cascading risk as well as the update law for risk computation. Furthermore, the cascading risk framework reveals its advantages in the design of networks as it enables the designer to assess the sequence of the most vulnerable agents in a given network.

-1 Proof of Lemma 1

The result is an immediate extension of the steady-state statistics of the observables in [21] by considering a centering matrix .

-2 Proof of Lemma 2

-3 Proof of Theorem 1

Considering Lemma 2, one can rewrite the RHS of (10) as

The result follows by taking cases on the risk value. More specifically, the case when is equivalent to

and the first branch condition follows from the definition of the error function.

For the second branch, when , the monotonicity condition on and implies there is a unique such that

the result follows by solving the above equation for .

-4 Proof of Theorem 2

To characterize the effect of the failures of agents, let us consider the block covariance matrix

where , and is obtained from (8). Since is invertible, we have

where is the Schur complement [13] of block of the matrix . Let us consider the vector of failed observables of agents as where is the vector of failed observables of agents and is the failed observable of agent k, i.e., agent. Consider the following vectors, and the conditional cross-covariance of agents and after agents have failed , the result then follows directly by applying Lemma 2.

References

- [1] P. Artzner “Thinking coherently” In Risk, 1997, pp. 68–71

- [2] P. Artzner, F. Delbaen, J. Eber and D. Heath “Coherent measures of risk” In Mathematical finance 9.3 Wiley Online Library, 1999, pp. 203–228

- [3] Marcos Cesar Bragagnolo, Nadhir Messai and Noureddine Manamanni “Attack detection in a cluster divided consensus network” In 2019 18th European Control Conference (ECC), 2019, pp. 1091–1096 IEEE

- [4] A. Fagiolini, Marco Pellinacci, Gianni Valenti, Gianluca Dini and Antonio Bicchi “Consensus-based distributed intrusion detection for multi-robot systems” In 2008 IEEE International Conference on Robotics and Automation, 2008, pp. 120–127 IEEE

- [5] H. Föllmer and A. Schied “Stochastic Finance” In Stochastic Finance De Gruyter, 2016

- [6] J. Krueger “On the perception of social consensus” In Advances in experimental social psychology 30 Elsevier, 1998, pp. 163–240

- [7] David Kushner “The real story of stuxnet” In ieee Spectrum 50.3 Institute of ElectricalElectronics Engineers, Inc., 345 E. 47 th St. NY …, 2013, pp. 48–53

- [8] G. Liu, C. Somarakis and N. Motee “Risk of Cascading Failures in Time-Delayed Vehicle Platooning” In IEEE Conference on Decision and Control, 2021

- [9] Guangyi Liu, Vivek Pandey, Christoforos Somarakis and Nader Motee “Risk of Cascading Failures in Multi-agent Rendezvous with Communication Time Delay” In 2022 American Control Conference (ACC), 2022, pp. 2172–2177 IEEE

- [10] Guangyi Liu, Christoforos Somarakis and Nader Motee “Emergence of Cascading Risk and Role of Spatial Locations of Collisions in Time-Delayed Platoon of Vehicles” In 2022 IEEE 61st Conference on Decision and Control (CDC), 2022, pp. 6460–6465 IEEE

- [11] R. Olfati-Saber, J.. Fax and R.. Murray “Consensus and cooperation in networked multi-agent systems” In Proceedings of the IEEE 95.1 IEEE, 2007, pp. 215–233

- [12] R. Olfati-Saber and R.. Murray “Consensus problems in networks of agents with switching topology and time-delays” In IEEE Transactions on automatic control 49.9 IEEE, 2004, pp. 1520–1533

- [13] Diane Valerie Ouellette “Schur Complements and Statistics” In Linear Algebra and Its Applications 36.9 Elsevier, 1981, pp. 187–295

- [14] M. Rahnamay-Naeini and M.. Hayat “Cascading Failures in Interdependent Infrastructures: An Interdependent Markov-Chain Approach” In IEEE Transactions on Smart Grid 7.4, 2016, pp. 1997–2006

- [15] W. Ren, R.. Beard and E.. Atkins “Information consensus in multivehicle cooperative control” In IEEE Control systems magazine 27.2 IEEE, 2007, pp. 71–82

- [16] R.. Rockafellar and S. Uryasev “Optimization of Conditional Value-at-Risk” In Portfolio The Magazine Of The Fine Arts 2, 1999, pp. 1–26

- [17] R. Rockafellar and Stanislav Uryasev “Conditional value-at-risk for general loss distributions” In Journal of Banking and Finance 26.7, 2002, pp. 1443–1471

- [18] Jill Slay and Michael Miller “Lessons learned from the maroochy water breach” In International conference on critical infrastructure protection, 2007, pp. 73–82 Springer

- [19] C. Somarakis, Y. Ghaedsharaf and N. Motee “Aggregate fluctuations in time-delay linear consensus networks: A systemic risk perspective” In Proceedings of the American Control Conference, 2017

- [20] C. Somarakis, Y. Ghaedsharaf and N. Motee “Risk of Collision and Detachment in Vehicle Platooning: Time-Delay-Induced Limitations and Tradeoffs” In IEEE Transactions on Automatic Control 65.8, 2020

- [21] C. Somarakis, Y. Ghaedsharaf and N. Motee “Time-delay origins of fundamental tradeoffs between risk of large fluctuations and network connectivity” In IEEE Transactions on Automatic Control 64.9, 2019

- [22] C. Somarakis, M. Siami and N. Motee “Interplays Between Systemic Risk and Network Topology in Consensus Networks” In IFAC-PapersOnLine 49.22, 2016

- [23] Y.. Tong “The multivariate normal distribution” Springer Science & Business Media, 2012

- [24] P. Van Mieghem “Graph spectra for complex networks” Cambridge University Press, 2010

- [25] Y. Zhang, A. Arenas and O. Yağan “Cascading failures in interdependent systems under a flow redistribution model” In Physical Review E 97.2 APS, 2018, pp. 022307

- [26] Y. Zhang and O. Yağan “Robustness of interdependent cyber-physical systems against cascading failures” In IEEE Transactions on Automatic Control 65.2 IEEE, 2019, pp. 711–726