Ruin probability for the quota share model with phase-type distributed claims

Abstract

In this paper, we generalise the results presented in the literature for the ruin probability for the insurer–reinsurer model under a pro-rata reinsurance contract. We consider claim amounts that are described by a phase-type distribution that includes exponential, mixture of exponential, Erlang, and mixture of Erlang distributions. We derive the ruin probability formulas with the use of change-of-measure technique and present important special cases. We illustrate the usefulness of the introduced model by fitting it to the real-world loss data. With the use of statistical tests and graphical tools, we show that the mixture of Erlangs is well-fitted to the data and is superior to other considered distributions. This justifies the fact that the presented results can be useful in the context of risk assessment of co-operating insurance companies.

keywords:

multidimensional risk process , ruin probability , change of measure , phase-type distribution , mixture of Erlang distributions1 Introduction

Risk theory in general and ruin probabilities in particular have been an active area of research since the classical Cramér-Lundberg model, introduced in 1903 by the Swedish actuary Filip Lundberg [19] and then generalised in the 1930’s by Harald Cramér [17].

The Cramér-Lundberg model describes the surplus of an insurance company that experiences two opposing cash flows: incoming premiums and outgoing claims. The traditional approach in risk theory is to study the probability of ruin, that is, the probability that the risk process will ever go below zero [2]. Ruin is considered a technical term. It does not mean that the company becomes bankrupt. If ruin occurs, this is interpreted to mean that the company has to take action to make the business profitable. For solvency purposes, the probability of ruin can be used as a rough approximation of the insolvency. Moreover, setting it to an acceptably low level, the needed initial capital and the rate of premiums can be estimated. It can also serve as a useful tool in long-range planning for the use of insurer’s funds. In addition, ruin theory has deep methodological links and applications to other fields of applied probability, such as queueing theory and mathematical finance [2].

The ruin probabilities in infinite and finite time, even for the classical risk process, can only be calculated for a few special cases of the claim amount distribution. For the infinite horizon case, there are well-known elementary results for zero initial capital, and the exponential and mixture of two exponential claim amount distributions, see [22, 16]. For the results for general phase-type distributions, in particular for mixture of exponential distributions, see [2]. For the finite-horizon case, the only convenient ”semi-elementary” formula (involving only a simple integral) exists for the exponential distribution [23, 16]. However, this case can always be approximated by the Monte Carlo method.

Recently, multidimensional risk processes have been introduced in the literature to account for multiple lines of business of an insurance company and collaborating insurance companies. The ruin probability can be now defined in several ways, e.g. when all lines or all companies are ruined or at least one. The multidimensional ruin problem for light-tailed claims and general ruin sets was studied for the first time in [10] and multidimensional heavy-tailed processes in [18]. They mainly concentrated on multivariate regularly varying random walks and calculated sharp boundaries for the asymptotic ruin probability.

Since different risks usually have an effect on a few lines of business at the same time, the statistical dependence among claims in these lines should be taken into account. The multidimensional risk process was specialised to the two-dimensional case with claims shared with a predetermined proportion in [3, 4]. This case is usually referred to as the insurer–reinsurer model, as it well describes the quota share proportional treaty. It can also be used to model two branches of the same insurance company. The ruin occurs here if one or both companies go bankrupt. The former case, which is more interesting from a practical point of view, is usually analysed, and the latter can be obtained from the former in a straightforward way. The only simple ruin probability formulas for the insurer–reinsurer model were provided for exponentially distributed claims in [4] (by explicitly inverting the Laplace transform) and later in [9] (by means of a change-of-measure technique). Another type of dependence was studied in [6], where the link was established by a random bipartite network. An extension to a system of two insurers, where the first insurer is experiences claims arising from two independent compound Poisson processes and the second insurer covers a proportion of the claims was introduced in [5]. In [20], a model driven by a general spectrally positive or negative Lévy process was investigated, see also [3].

In this paper, we derive the results for the infinite-time ruin probability for the general phase-type distributions. The article is organised as follows. In Section 2, the model is presented and ruin probabilities are defined. In Section 3 the results for phase-type claims for the classical Cramér-Lundberg model are recalled. The main results are presented in Section 4. For the insurer–reinsurer model driven by the renewal process, we derive a ruin probability formula for the infinite-time horizon. The special cases of mixture of exponential and Erlang distributions are presented. In order to illustrate the usefulness of phase-type distributions in the context of ruin probability, in Section 5 we analyze loss data from a Polish insurance company. We identify and validate the aggregate non-homogeneous Poisson by means of rigorous statistical tests and visual techniques. We show that the mixture of two Erlang distributions outperforms other considered distributions. This justifies the usefulness of the obtained results and importance of the mixture of two Erlang distributions in modelling the loss data. Section 6 summarises our results.

2 Insurer–reinsurer model

We consider here an insurance network that describes capitals of insurer and reinsurer companies that share a quota-share reinsurance contract. We assume that both the insurer and reinsurer participate in settling claims that have common origin. Formally, we can define the network on the usual probability space as a system of two Cramér-Lundberg models in the following form:

| (9) |

Here, and denote the initial capitals of the first and second reinsurer, and are their premium income rates, is a claim counting Poisson processes with intensity that is independent of claim amount sequence . Parameter defines the split proportions for the insurer and reinsurer, respectively.

Usually, we assume that

| (10) |

where are the relative safety loadings. Due to higher acquisition and administration costs of the insurer, it is natural to assume that the premium rate for the insurer is higher than for the reinsurer and therefore the following relation holds: .

Our main goal is to obtain an analytical expression for the ruin probability for at least one of considered insurance companies in the infinite time horizon, which is formally defined as follows

| (11) |

where is the ruin time:

| (12) |

One can also be interested in the ruin probability for both companies at the same time in the infinite time horizon:

| (13) |

Here, the ruin time is defined as follows:

| (14) |

3 Ruin probability for phase-type claims

We recall that in [3] we find that for (ii) the following holds:

| (22) |

where is the ruin probability in infinite time for with initial capital and

| (23) |

with the specific time point T such that

| (24) |

In this section we assume that the distribution of the generic claim size appearing in (9) is given by

where is a column vector with all its entries equal to , is an initial distribution of a continuous-time Markov chain on states with a transition sub-rate matrix of dimension . We assume that this Markov chain is transient, that is, has a positive entry. Then describes the lifetime of our Markov chain and its density equals

| (25) |

where for any matrix . If for example has exponential distribution with parameter then and , and .

From Cor. 3.1 on p. 264 of [1] we have the following lemma that defines the ruin probability for one-dimensional risk process with claims being a phase-type distributed .

Lemma 3.1.

| (26) |

where

| (27) |

for Poisson intensity of the claims arrival process111In the case when we have perturbed by the Brownian motion risk process, that is, , then by [24, Eq. (19)] where are distinct roots with strictly negative real part of the Cramér-Lundberg equation for a Laplace exponent of and .

Note that for the exponential distribution with parameter , we have222See also Thm. 8.3.1, p. 340 of [23], see also Cor. 6.5.3, p. 252 of [23]

| (28) |

and

| (29) |

Hence, the main identity (22) will give the expression for the two-dimension ruin probability as long as we identify .

4 Two-dimensional ruin for phase-type claims

Now, the numerical analysis of finding two-dimensional ruin probability can be done for general phase-type distributions. The matrix exponent appearing in (26) can be found by classical Jordan-type decomposition methods.

For some particular sub-families of phase-type distributions the whole analysis can be further simplified. We will now consider two such families of distributions based on [7].

For both families we assume the key condition that all solutions of a Lundberg equation are real, hence the equation

| (30) |

(with possible multiplicity, that is some of might be equal). We denote by the multiplicity of . By Theorem 4.5 on p. 264 of [1] we know that this assumption is equivalent to requirement that all eigenvalues of the matrix defined in (27) are real. In other words this means that in the Jordan decomposition of this matrix given by

| (31) |

for matrix with columns being right eigenvectors corresponding to , there are no complex conjugate pairs in the set of solution of (30). In (31) is a Jordan block of size equal to

| (32) |

Note that if all eigenvalues are different, then and . In particular, if has the exponential distribution with parameter then and .

The first class corresponds to mixtures of independent exponentially distributed random variables satisfying above condition (30). More precisely, for a given ,

where with . The class is suitable for representing random variables with a squared coefficient of variation (scov) strictly larger than one as one can find a distribution in with the same moments; see [26, p. 359] when for details.

Second class corresponds to sums of independent exponentially distributed random variables with parameters for satisfying the condition (30). For this class one can match all finite moments for any distribution with scov strictly less than one. Note that when all intensities of exponential distributions are equal than resulting distribution has Erlang distribution with phases. The estimation of all the parameters of the distributions from class can be done via EM algorithm.

From (26) and (31) we can conclude that

| (33) |

for

Moreover, by safety loading condition and by considering large initial reserves it follows that all . Let be number of different solution of Lundberg equation (30). Then from (33) it follows that

| (34) |

for some ( and ). We recall that assumption that there are not conjugate solutions of Lundberg equation (30) is not always satisfied. As Dickson and Hipp [14] show if one takes symmetric mixture od Erlang and Erlang, and then and then and

Moreover, we have then

and . Thus

and it is not of the form of (34). In this case additionally may appear for being a radial part of the constant in front of .

Still, if one take the Erlang of claim size distribution, then for and we have , and

| (35) |

Moreover, then

and . Thus

| (36) |

and it is the form of (34).

Since is a Lévy process, hence by [21] we can introduce now the following exponential change of measure:

| (37) |

for a natural filtration of the process and

| (38) |

By we will denote the expectation with respect to . Moreover, by Prop. 5.6 of [21], under probability measure , process equals with being the Poisson process with intensity

| (39) |

and generic claim size has new density function

| (40) |

for

Note that from the representation (25) it follows that is again phase-type with generators . In particular, if has the exponential distribution with parameter then, under probability measure , the generic claim size has the exponential distribution with parameter for defined in (28). Moreover, in this case . Finally,

| (41) |

Similarly, if has the Erlang distribution then, under probability measure , the generic claim size has Erlang distribution with .

The main results of this section is given by the following theorem.

Theorem 4.1.

Proof.

We denote by the th component of a vector .

Corollary 4.1.

Note that and can be calculated by using numerical procedures, see e.g. [25]. Another approach is related with the power series expansion which is done the claim size distributions of mixed Erlang type in [15] and [13]; see also [12, 27]. An alternative very accurate numerical method is to randomize the time horizon . The detailed numerical analysis in some special cases of phase-type distribution of claim sizes and other comments will be subject of next section.

4.1 Ruin probability for the mixture of two exponentials

Example 4.1.

In this part we establish a ruin probability for the model (9) assuming that the claims follows a mixture of exponential distributions. For the simplicity in presentation of results we investigate a mixture of two exponential distributions given by positive weights that and means and , respectively. Our result can be easily extended to the case where the mixture consists of finite number of exponential distributions.

4.2 Ruin probability for the Erlang

Example 4.2.

If has Erlang law then from (36) and (34) it follows that , . Then in the next step from (38) we find () where , and matrix is given in (35). Then from Corollary 4.1 we can conclude that in this case

| (47) | ||||

| (48) |

where under measures , , the risk process has premium and claim size Erlang distributed with parameters , , , respectively. Note that and () for the ruin time for the risk process and given in (24). To find this quantity, it is enough to find the density of the ruin time . This can be done using [13, page 58].

5 Numerical analysis for phase-type distributions

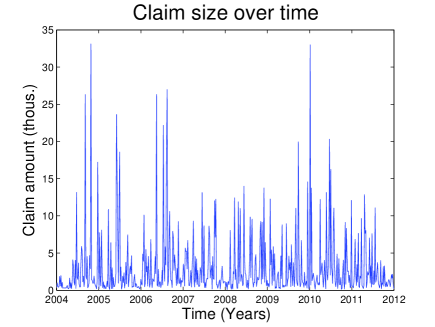

We analyse now real-world loss data describing liability insurance claims obtained from a Polish insurance company in the years 2004-2012. The first step is to prepare the data so that the claim amounts are discounted at the same moment and aggregated on the single claim basis. Analysis of the empirical claim amount distribution reveals two claims that deviate from the rest of the sample. These two claims constitute 5.31% of all claims. For the purpose of this study they were excluded as outliers. The final sample consists of 542 payments and is shown in Figure 1.

The following distributions were taken into account to describe the claim amounts: exponential, mixture of exponentials, Erlang and mixture of Erlangs. To check the goodness of fit we consider four test statistics based on the distance between the empirical and fitted distribution function.

The first considered test statistic is the classical Kolmogorov–Smirnov statistic based on the supremum norm defined as:

A similar statistic is the Kuiper :

where and .

We will also use statistics calculated on the basis of quadratic norm, namely Cramer—von Mises and Anderson and Darling statistics:

and

The former statistic puts more weight on observations in the tails of the distribution and is one of the most powerful statistical tests for detecting most departures from normality, cf. [11].

In order to estimate the parameters of the distributions we apply the estimation method based on minimising statistics. To calculate -values for the studied tests we follow the Monte Carlo simulation algorithm described in [8]. The results of parameter estimation and hypothesis testing for the data are presented in Table 1.

To calculate -values for the studied tests we follow the Monte Carlo simulation algorithm described in [8]. The results of the parameter estimation and hypothesis testing for the third-party liability insurance claims amount are presented in Table 1. We decided not to include exponential distribution in the table since for the Erlang distribution the coefficient , which means that Erlang distribution simplifies to the exponential.

| Distribution | Mixture of exps | Erlang | Mixture of Erlangs |

|---|---|---|---|

| Parameters | |||

| Test results | |||

Unfortunately, neither of the proposed distributions passes the tests. However, we can see that the mixture of Erlang distributions with parameters and has the best results in terms of test statistics (the statistic values are the lowest).

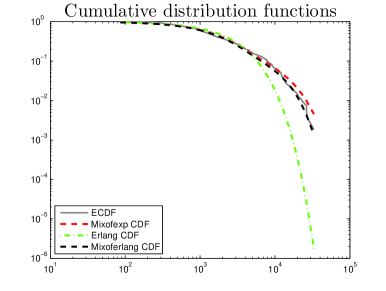

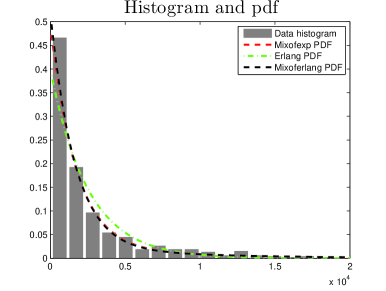

We also check the quality of fit graphically by comparing the cumulative empirical and fitted distribution functions, see Figure 2. In addition, a histogram is plotted with theoretical probability functions corresponding to the fitted distributions. The illustrations suggest that mixtures of exponential and Erlang distributions are best fitted to the data.

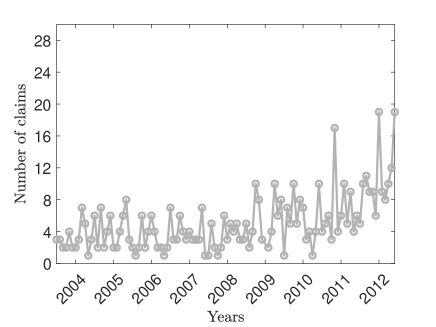

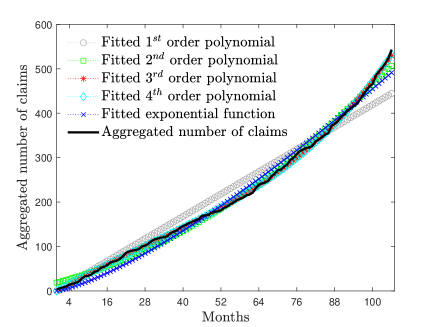

Now, we identify the claim counting process. Firstly, we determine the number of claims in subsequent months. They are depicted in Figure 3.

We do not observe seasonality, however, one can observe an increase in the number of claims in subsequent years. That is why we decided to apply a non-homogeneous Poisson process with being polynomial or exponential function. To find a proper intensity function, we fit polynomial or exponential functions to the aggregated number of claims. Parameters of the functions are estimated by minimisation of mean-squared error (the error is calculated with respect to the mean value function of the non-homogeneous Poisson process). In Figure 4 we present the graphical comparison of the aggregate number of claims with the mean value function for analysed forms of intensity function.

We notice that a first-degree polynomial is clearly worse suited to the aggregate number of claims. To verify the quality of fit of the intensity functions which are higher order polynomials or exponential functions, we determine the mean-squared error of the considered functions and present the results in Table 2.

| Order of the polynomial | |||||

| Exp. function | |||||

| MSE | 22.23 | 8.52 | 3.16 | 3.09 | 13.20 |

Based on the mean-square errors, we choose the order polynomial. For the higher order, the gain is negligible, and for the exponential function it even increases. Therefore, for the considered data, we select the non-homogeneous Poisson process with the intensity function:

5.1 Probability of ruin for different scenarios

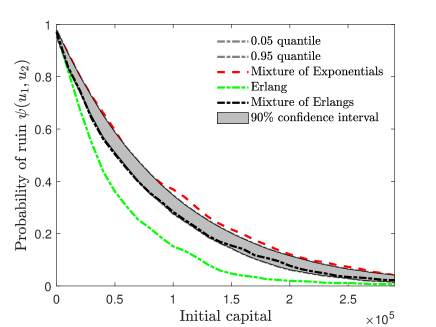

We now calculate the ruin probability values using the formulas derived in Section 4. The obtained results are compared to the probability of ruin calculated with the use of empirical distribution function (non-parametric bootstrap). In Figure 5 we can see the results for the fitted mixture of exponentials, Erlang and mixture of Erlangs, and the confidence interval obtained by the non-parametric bootstrap.

We can clearly observe that only for the mixture of Erlang distributions the obtained values lie in the area between the quantiles of order 0.05 and 0.95, which proves the goodness of fit for this distribution. The probability of ruin calculated for the mixture of exponential distributions seems overestimated and for Erlang it is heavily underestimated. The analysis carried out leads to the conclusion that the Erlang mixture is the best suited for the data.

6 Conclusions

In this paper, the problem of ruin probability in the case of a two-dimensional risk process for general phase-type claim amounts is investigated. The considered risk process assumes that both premiums and claims are divided between two lines in the same fixed proportions. Such a system can describe the capitals of the insurer and reinsurer under the quota share contract or two lines of business of the insurance company where the claims split on a pro rata basis.

Our main findings are based on the purely stochastic arguments. Our main technique is the change of the measure that allows us to express the Laplace transform as the ruin probability of some modified risk process. We derived infinite-time ruin probability formulas for general phase-type distributions and present specialised results for the mixture of exponential, Erlang and mixture of Erlang distributions.

In order to illustrate presented results, we considered loss data from a Polish insurance company. The data contained claim amounts resulting from third-party liability insurance between 2004 and 2012. We fitted a non-homogeneous Poisson process to the claim counting process and considered exponential, mixture of exponential, Erlang and mixture of Erlang distributions as candidates to describe the claim amount sequence. We performed statistical tests based on empirical cumulative distribution function and analysed the right tails of the fitted distribution. Finally, we calculate the ruin probability values for the considered distributions and compared them with the ruin probabilities obtained from the empirical distribution function. The analyses show that the model based on the mixture of two Erlang distributions is the best fitted to the data which illustrates the usefulness of phase type distributions in the context of the risk assessment.

References

- Asmussen [2000] Asmussen, S., 2000. Ruin Probabilities. Advanced Series in Dynamical Systems, World Scientific, Singapore.

- Asmussen and Albrecher [2010] Asmussen, S., Albrecher, H., 2010. Ruin Probabilities. Advanced Series on Statistical Science and Applied Probability. World Scientific Publishing Co. Inc., Singapore.

- Avram et al. [2008a] Avram, F., Palmowski, Z., Pistorius, M., 2008a. A two-dimensional ruin problem on the positive quadrant. Insurance: Mathematics and Economics 42, 227 – 234. doi:10.1016/j.insmatheco.2007.02.004.

- Avram et al. [2008b] Avram, F., Palmowski, Z., Pistorius, M.R., 2008b. Exit problem of a two-dimensional risk process from the quadrant: Exact and asymptotic results. Ann. Appl. Probab. 18, 2421–2449. doi:10.1214/08-AAP529.

- Badescu et al. [2011] Badescu, A.L., Cheung, E.C.K., Rabehasaina, L., 2011. A two-dimensional risk model with proportional reinsurance. J. Appl. Prob. 48, 749–765. doi:10.1239/jap/1316796912.

- Behme et al. [2020] Behme, A., Klüppelberg, C., Reinert, G., 2020. Ruin probabilities for risk processes in a bipartite network. Stochastic Models 36, 548–573. doi:10.1080/15326349.2020.1760109.

- Boxma and Mandjes [2019] Boxma, O., Mandjes, M., 2019. Affine storage and insurance risk models. Preprint.

- Burnecki et al. [2011] Burnecki, K., Janczura, J., Weron, R., 2011. Building loss models, in: Statistical Tools for Finance and Insurance, 2nd ed.. Springer, Berlin, pp. 293–328.

- Burnecki et al. [2021] Burnecki, K., Teuerle, M.A., Wilkowska, A., 2021. Ruin probability for the insurer-reinsurer model for exponential claims: A probabilistic approach. Risks 9. URL: https://www.mdpi.com/2227-9091/9/5/86, doi:10.3390/risks9050086.

- Collamore [1996] Collamore, J.F., 1996. Hitting probabilities and large deviations. The Annals of Probability 24, 2065 – 2078. URL: https://doi.org/10.1214/aop/1041903218, doi:10.1214/aop/1041903218.

- D’Agostino and Stephens [1986] D’Agostino, R., Stephens, M., 1986. Goodness-of-Fit Techniques. Marcel Dekker, Inc., New York.

- Dickson [2008] Dickson, D., 2008. Some explicit solutions for the joint density of the time of ruin and the deficit at ruin. Astin Bulletin 38, 259–276.

- Dickson and Willmot [2005] Dickson, D., Willmot, G., 2005. The density of the time to ruin in the classical poisson risk model. Astin Bulletin 35, 45–60.

- Dickson and Hipp [1998] Dickson, D.C., Hipp, C., 1998. Ruin probabilities for Erlang(2) risk processes. Insurance: Mathematics and Economics 21, 251–262.

- Garcia [2005] Garcia, J., 2005. Explicit solutions for the survival probabilities in the classical risk models. Astin Bulletin 35, 113–130.

- Grandell [1991] Grandell, J., 1991. Aspects of Risk Theory. Springer, Berlin.

- Grenander [1995] Grenander, U., 1995. A survey of the life and works of Harald Cramér. Scandinavian Actuarial Journal 1995, 2–5. doi:10.1080/03461238.1995.10413944.

- Hult et al. [2005] Hult, H., Lindskog, F., Mikosch, T., Samorodnitsky, G., 2005. Functional large deviations for multivariate regularly varying random walks. The Annals of Applied Probability 15, 2651 – 2680. URL: https://doi.org/10.1214/105051605000000502, doi:10.1214/105051605000000502.

- Lundberg [1903] Lundberg, F., 1903. I. Approximerad framstallning af sannolikhetsfunktionen ; ii. Aterforsakring af kollektivrisker. Uppsala.

- Michna [2020] Michna, Z., 2020. Ruin probabilities for two collaborating insurance companies. Probab. Math. Statist. 40, 369–386.

- Palmowski and Rolski [2002] Palmowski, Z., Rolski, T., 2002. A technique for the exponential change of measure for Markov processes. Bernoulli 8, 767–785.

- Panjer and Willmot [1992] Panjer, H., Willmot, G., 1992. Insurance risk models. Society of Acturaries, Schaumburg.

- Rolski et al. [1999] Rolski, T., Schmidli, H., Schmidt, V., Teugels, J., 1999. Stochastic Processes for Insurance and Finance. Wiley Series in Probability and Statistics, Wiley, New York.

- S. Asmussen and Pistorius [2004] S. Asmussen, F.A., Pistorius, M., 2004. Russian and American put options under exponential phase-type Lévy models. Stoch. Proc. Appl. 109(1), 79–111.

- Stanford and Stroiński [1994] Stanford, D., Stroiński, K., 1994. Recursive method for computing finite– time ruin probabilities for phase–distributed claim sizes. Astin Bulletin 24, 235–254.

- Tijms [1994] Tijms, H., 1994. Stochastic Models: an Algorithmic Approach. Wiley, Chichester.

- Willmot and Woo [2007] Willmot, G., Woo, J., 2007. On the class of Erlang mixtures with risk theoretic applications. North American Actuarial J. 11, 99–115.