Probabilistic Overview of Probabilities of Default for Low Default Portfolios by K. Pluto and D. Tasche

Abstract

This article gives a probabilistic overview of the widely used method of default probability estimation proposed by K. Pluto and D. Tasche. There are listed detailed assumptions and derivation of the inequality where the probability of default is involved under the influence of systematic factor. The author anticipates adding more clarity, especially for early career analysts or scholars, regarding the assumption of borrowers’ independence, conditional independence and interaction between the probability distributions such as binomial, beta, normal and others. There is also shown the relation between the probability of default and the joint distribution of , where , including but not limiting, is the standard normal, admits, including but not limiting, the beta-normal distribution and are independent.

keywords:

probability of default, binomial distribution, beta-normal distribution, Vasicek distribution, independence, Pluto-Tasche methodMSC:

60-02, 60E05, 62-02, 26D10[inst1]organization=Institute of Mathematics,addressline=Naugarduko 24, city=Vilnius, postcode=LT-03225, country=Lithuania

1 Introduction

The probability of default is actually the most important metric in credit risk management. Roughly, this probability provides the likelihood for a certain obligor not to follow the taken financial commitments properly within a certain period of time, typically one year. The number of defaulted borrowers divided by the number of total borrowers within a certain portfolio is known as the observed default rate, while the predicted one is called the expected default rate. Any model tasked to predict , should ensure the alignment between the observed and expected default rates. However, in some instances, such as low default portfolios, there is not possible to have any robust observations for the observed default rate. In such instances, the famous work [14] suggests applying the Bernoulli trials to estimate the experiment’s success probability . This work is a survey of two models: (a) the estimation of when obligors in the portfolio are treated independently of each other and there is no side influence for such a portfolio, (b) the estimation of when obligors in the portfolio are treated conditionally independent of each other when each obligor is influenced by some systematic factor. We aim to reflect on the detailed steps and assumptions used in deriving the two mentioned models.

Let us recall several well-known probability distributions.

-

1.

We say that the random variable is binomial distributed with parameters and (denoted ) if the probability mass function is

where

We denote the cumulative distribution function of the binomial random variable by

-

2.

We say that the random variable is beta distributed with parameters and (denoted ) if its probability density function is

where

and the gamma function for the complex number is

We denote the cumulative distribution function of the beta random variable by

and its inverse by .

-

3.

We say that the random variable is normally distributed with parameters and (denoted by ) if its probability density function is

We denote the cumulative distribution function of the normal distribution by

and its inverse by . We recall the symmetry and write , and respectively if .

The other distributions met in this paper, are introduced in the proper places where they are used.

2 Binomial and mixture binomial distributions for the probability of default estimation

In this section, in the subsections 2.1 and 2.2 respectively, we review the derivation of two methods used to estimate the probability of default . As mentioned in Introduction 1, the first method is just the Bernoulli trials assuming the obligors’ independence, while the second method provides the estimation of under the assumption of obligors’ conditional independence of each other under the influence of a certain systematic factor.

2.1 Binomial distribution

Let be independent copies of Bernoulli random variable which distribution is . In risk management, the random variables are treated as independent obligors and the attained value , means that the ’th obligor defaults within some observation period (typically one year), while , means that the ’th obligor does not default within the same observation period. Then, the sum may attain any value form the set with probability

| (1) |

The probability mass function of the binomial distribution (1) means the probability to default out of total obligors in the portfolio, while the distribution function (2)

| (2) |

is the probability to default no more than obligors out of total . Obviously,

for any .

In many examples, e.g., tossing a coin or a die, the experiment’s success probability is known beforehand. However, in real-life problems, such as default probability estimation, the probability is desired to know. In order to get out of (1) or (2) we need an expert judgment first. Let us suppose that the probability of the amount of defaulted obligors does not exceed out of is at least . Then,

| (3) |

and, in view of Proposition 1, the upper bound of default probability is

| (4) |

where is an inverse of beta distribution function. In particular, if , i.e., we are certain with probability that there be no defaulted obligors at all, then

The probability can be introduced as the probability of type I error, also known as the false positive instance classification, which in our context means that the actual probability of default does not belong to the predicted interval ; see [4]. Moreover, the confidence interval of the binomial distribution is known as the Clopper–Pearson interval; see [5], [3].

2.2 Mixture of Binomial and Normal distributions

Let be an annual return rate and the increment of the invested amount when the return rate is compounded times per year. It is well known that when . Thus,

assuming the continuously compounded return, where denotes the final value and the initial one. Based on the previous thoughts, we define

| (5) |

The return derived in (5) is called the logarithmic return or just log-return. We now assume the logarithmic return to be a random variable. More precisely, we assume

| (6) |

where , , , the random variables and are independent and both non-degenerate. Also, is known as systematic risk factor, while as idiosyncratic; see [9]. The origin of return’s definition (6) has similarities with the capital asset pricing model which states that every expected return under certain assumptions satisfies

where is the risk-free return rate, the return of systemic portfolio and , see, for example, [8] and observe that (6) implies .

Let us now standardize the log-return (6). It is easy to check that

Thus, it is equivalent to define as

| (7) |

where

| (8) |

and , are independent standard normal random variables. Indeed, is quivalent to .

We note that

and the coefficient in (8) is called the asset correlation (see [19]); it expresses the correlation between and :

We now define the default event by

| (9) |

Of course, is Bernoulli random variable and since the random variable is standard normal. We now are interested in that particular which causes . Conditioning on , i.e., assuming that the systematic factor attains some particular value , for , we have

| (10) |

and

| (11) |

The random variable

| (12) |

where , is known as Vasicek distribution, see [17].

Let be the conditionally independent copies of the random variable when the systematic factor . Then, is binomial random variable and the conditional probability that if is

| (13) |

where . Thus, being certain with probability at least , that there default up to obligors out of total , by the law of total probability we get

| (14) |

Notice that if , then the inequality (2.2) is satisfied with any when . Also, in (2.2) implies the inequality (2.1). Equally, the integral in (2.2) is nothing but the mixture of the binomial and Vasicek distributions: it is the cumulative binomial distribution function when the parameter is Vasicek distributed (12). See [13] for the mixture distribution models.

According to Proposition 2, the upper bound of in (2.2) is

| (15) |

where is the inverse of the cumulative distribution function

| (16) |

It is not easy to get a more convenient expression of the cumulative distribution function in (16). Thus, we should search for the quantiles of the underlying distribution, described by , numerically; see Section 5. Of course, the function is defined in view of Proposition 2 by replacing

in (19) and there is equivalent to search for such that

or

| (17) |

where is the continuous cumulative distribution function with respect to .

Let us mention that the probability distribution, described by its cumulative distribution function

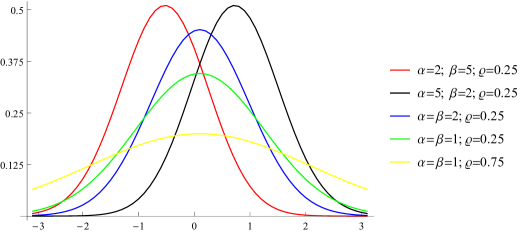

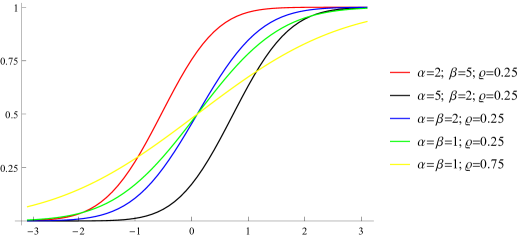

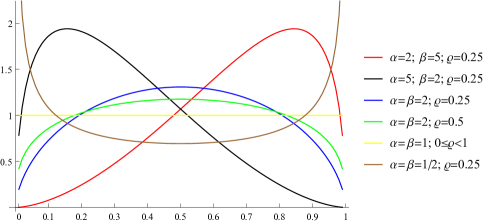

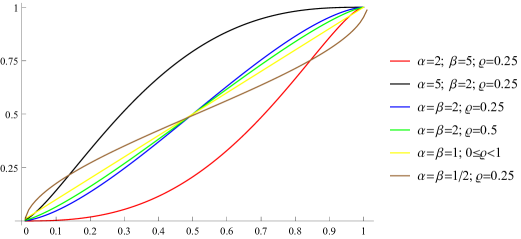

is known as beta-normal. We write if is the beta-normal random variable and , denotes its density. See [6], [7], [15] and [10] for the beta-normal distribution. Thus, in (16) can be easily described in terms of the beta-normal distribution. See also [2] as the good initial source on credit risk management and some other insights deriving inequality (2.2). Equally, in view of (16), we depict the probability density function

for some chosen parameters in Figure 1 and the cumulative distribution function itself correspondingly in Figure 2 below.

The derivative of in (17) and the cumulative distribution function itself for some chosen parameters are depicted in Figure 3 and Figure 4 below respectively.

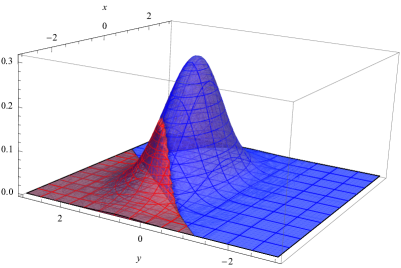

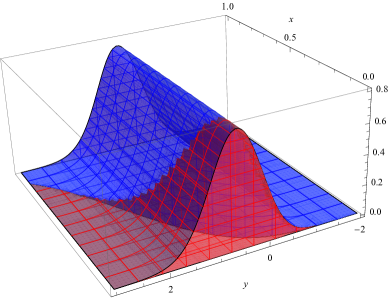

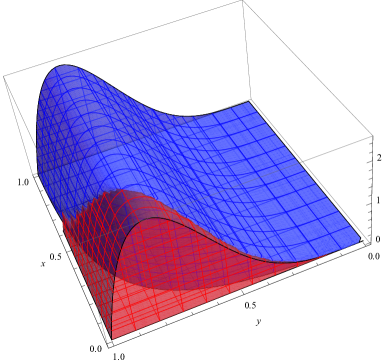

The depicted functions in Figures 1-4 relate the search of the upper bound of with the quantile function of under the underlying distribution. According to Propositions 2 and 3, in Figures 5, 6 and 7 below we illustrate the search of the upper bound of relation with the partial volume of the unit given by (the blue colored volume in Figures 5, 6 and 7) under the joint density surface.

To estimate the probability of default by (4) or (15) among the portfolio sub-classes , where represents the lowest risk borrowers and the highest respectively, there was proposed a method of conservatism; see [14]. The method of conservatism states the following. Let , and be the number of obligors, the number of expected defaults and default probabilities over the portfolio sub-classes respectively. Then , and the probability of defaults should be estimated using the parameters in (4) or (15), should be estimated using , with and so on up to which should be estimated using .

3 Statements

In this section, we recall the connection between the binomial and beta distributions, provide several equivalent forms of inequality (2.2) and its connection to the normal multivariate distribution when there are no expected defaults, i.e. .

Proposition 1.

Let , be fixed and . Then the cumulative distribution function of binomial and beta random variables are related as

Note 1: Let us emphasize that the function in Proposition 1 is understood as the function of , when and are fixed.

Proposition 2.

Let , be fixed and . Then the inequality (2.2) admits the following equivalent representations:

| (18) | |||

| (19) |

where is the cumulative distribution function of the beta random variable.

Note 2: The same way as Proposition 1 relates the cumulative distribution functions of binomial and beta distributions, Proposition 2 relates the cumulative distribution function , from (2.2) to the ones in (18) or (19) when . Of course, in (18) and (19) can be easily replaced by due to the argument .

We denote the uniform distribution over the interval . Then, the following proposition is correct.

Proposition 3.

Note 3: Of course, there can be given some other joint distributions’ expressions than those provided in (20), (21), (22).

Corollary 4.

If , and , then the left hand-side of the inequality (2.2) is

| (23) | |||

| (24) |

where is the Gaussian copula with the correlation matrix

On top of that, the multivariate density of in (24) is

| (25) |

Corollary 4 and its proof (see Section 4) implies

where , and these moments of Vasicek distribution (12) are connected to the moments of the probability distribution given by

| (26) |

where and , see (2.2). Indeed, due to the well-known moment-generating function of the binomial distribution, the moment-generating function of (3) is

where . Notice that is the probability-generating function of the underlying distribution.

4 Proofs

This section provides the proofs for three formulated statements in Section 3. Majority of the given proofs are commonly known among researchers or scholars and there is difficult to give any initial source.

Proof of Proposition 1.

Let us first show that

Indeed,

We now aim to prove

where is considered as a function of when and are fixed. Let us rewrite

One may observe that , and the derivative

is positive for all . Thus, is the cumulative distribution function over the interval and its derivative is nothing but the density of the beta distribution with parameters , i.e.,

∎

Proof of Proposition 2.

Proof of Proposition 3.

Proof of Corollary 4.

Let . Assume the random variables are independent and identically distributed by . If and are conditionally independent of , then

The equality (23) follows by choosing

while the equality (24) is implied observing that

where

because

and

The determinant of is

and the inverse matrix of admits the following representation

5 Examples of computation

In this section, we give two examples that illustrate the discussed estimation of default probability . The required computations are performed with program [12].

Example 5.

Suppose there are up to defaults expected with probability out of obligors which are split into three risk classes: and , where represents the lowest risk and the highest. Assume the numbers of obligors are and the numbers of expected defaults are up to in risk classes , and respectively. We apply Propositions 1, 2 and the method of conservatism introduced in [14] to estimate the probabilities of default , and in risk classes , and .

The method of conservatism (see [14] and the description by end of Section 2) states that should be estimated for the entire portfolio, i.e., and in the considered case. The probability should be estimated for the entire portfolio excluding the class , i.e., and in the considered case. Then, the probability is estimated using and as per the riskiest class .

Using Proposition 1, the underlying logic stated in subsection 2.1 and the method of conservatism, we obtain Table 1.

Note that the numbers in Table 1 are given in [14] too and we replicate them for comparison purposes, especially calculating the quantiles of the underlying distribution given by .

Suppose the asset correlation in Example 5. Then, using Proposition 2, the underlying logic stated in subsection 2.2, the method of conservatism and the function ”FindRoot” in progam [12] we obtain Table 2 and Table 3.

The provided numbers in Table 3 match the corresponding ones in [14] except few cases caused by rounding errors in the fourth decimal place.

Example 6.

Suppose there are up to defaults expected with probability out of obligors which are split in four risk classes: , and where represents the lowest risk and the highest. Assume the numbers of obligors are and the numbers of expected defaults are up to in risk classes , , and respectively. We apply Propositions 1, 2 and the method of conservatism introduced in [14] to estimate the probabilities of default , and in risk classes , , and .

Using Proposition 1, the underlying logic stated in subsection 2.1 and the method of conservatism, we obtain Table 4.

Notice that in Table 4 and (see [14, Footnote 6]) ”… this is not a desirable effect, a possible – conservative – work-around could be to increment the number of defaults in grade up to the point where would take on a greater value than …”.

Suppose the asset correlation in Example 6. Then, using Proposition 2, the underlying logic stated in subsection 2.2, the method of conservatism and the function ”FindRoot” in progam [12] we obtain Table 5 and Table 6.

| 2.57 | ||||||

6 Concluding remarks

As stated, this survey article gives a detailed probabilistic overview of two methods for the upper bound of default probability. The provided insights reveal the important role played by the beta-normal distribution. However, the beta-normal distribution appears to be little studied, compared to the voluminous literature for the separate normal or beta distributions. It would be of interest to get any closed-form of the inverse of (see (16)) in terms of a superposition of and , which possibly would include studying the cumulative distribution function when and .

7 Acknowledgments

The author is thankful to Arvydas Karbonskis for his feedback on the draft version of this article and also to Dirk Tasche for pointing to the reference [16] and giving several other valuable comments.

References

- Arbenz [2013] Arbenz, P., 2013. Bayesian copulae distributions, with application to operational risk management — some comments. Methodology and Computing in Applied Probability 15, 105–108. doi:10.1007/s11009-011-9224-0.

- Bluhm et al. [2003] Bluhm, C., Overbeck, L., Wagner, C., 2003. An introduction to credit risk modeling. Chapman & Hall/CRC.

- Brown et al. [2001] Brown, L.D., Cai, T.T., DasGupta, A., 2001. Interval estimation for a binomial proportion. Statistical Science 16, 101 – 133. doi:10.1214/ss/1009213286.

- Casella and Berger [2002] Casella, G., Berger, R.L., 2002. Statistical Inference. Duxbury Press, Pacific Grove. Second edition.

- Clopper and Pearson [1934] Clopper, C.J., Pearson, E.S., 1934. The use of confidence or fiducial limits illustrated in the case of the binomial. Biometrika 26, 404–413. doi:10.1093/biomet/26.4.404.

- Eugene et al. [2002] Eugene, N., Famoye, F., Lee, C., 2002. Beta-normal distribution and its applications. Communications in Statistics - Theory and Methods 31, 497–512. doi:10.1081/STA-120003130.

- Eugene et al. [2004] Eugene, N., Famoye, F., Lee, C., 2004. Beta-normal distribution: bimodality properties and application. Journal of Modern Applied Statistical Methods 3. doi:10.22237/jmasm/1083370200.

- French [2003] French, C.W., 2003. The Treynor capital asset pricing model. Journal of Investment Management 1, 60–72.

- Gatfaoui [2007] Gatfaoui, H., 2007. Idiosyncratic risk, systematic risk and stochastic volatility: an implementation of Merton’s credit risk valuation. Palgrave Macmillan UK, London. pp. 107–131. doi:10.1057/9780230625846_6.

- Gupta and Nadarajah [2005] Gupta, A.K., Nadarajah, S., 2005. On the moments of the beta normal distribution. Communications in Statistics - Theory and Methods 33, 1–13. doi:10.1081/STA-120026573.

- Gut [2009] Gut, A., 2009. An intermediate course in probability. Springer. doi:10.1007/978-1-4419-0162-0.

- [12] Inc., W.R., . Mathematica online, Version 13.2. URL: https://www.wolfram.com/mathematica. Champaign, IL, 2022.

- Lindsay [1995] Lindsay, B.G., 1995. Mixture models: Theory, geometry and applications. NSF-CBMS Regional Conference Series in Probability and Statistics 5, 1–163.

- Pluto and Tasche [2006] Pluto, K., Tasche, D., 2006. Estimating probabilities of default for low default portfolios. Springer Berlin Heidelberg, Berlin, Heidelberg. pp. 79–103. doi:10.1007/3-540-33087-9_5.

- Rêgo et al. [2012] Rêgo, L.C., Cintra, R.J., Cordeiro, G.M., 2012. On some properties of the beta normal distribution. Communications in Statistics - Theory and Methods 41, 3722–3738. doi:10.1080/03610926.2011.568156.

- Tasche [2013] Tasche, D., 2013. Bayesian estimation of probabilities of default for low default portfolios. Journal of Risk Management in Financial Institutions 6, 302–326.

- Vasicek [1987] Vasicek, O.A., 1987. Probability of loss on loan portfolio. San Francisco: KMV Corporation.

- Xue-Kun Song [2000] Xue-Kun Song, P., 2000. Multivariate dispersion models generated from Gaussian copula. Scandinavian Journal of Statistics 27, 305–320. doi:https://doi.org/10.1111/1467-9469.00191.

- Zhang et al. [2008] Zhang, J., Zhu, F., Lee, J., 2008. Asset correlation, realized default correlation, and portfolio credit risk. Moody’s KMV Company .

Andrius Grigutis

Institute of Mathematics

Faculty of Mathematics and Informatics, Vilnius University

Naugarduko 24, LT-03225 Vilnius, Lithuania

andrius.grigutis@mif.vu.lt