LEAP: The latent exchangeability prior for borrowing information from historical data

Department of Biostatistics

University of North Carolina

Chapel Hill, NC 27516

ethanalt@live.unc.edu

& Xiuya Chang

Department of Biostatistics

University of North Carolina

Chapel Hill, NC 27516

coco.xyc@unc.edu

&Xun Jiang

Amgen

Thousand Oaks, CA 91320

xunj@amgen.com

&Qing Liu

Amgen

Thousand Oaks, CA 91320

qliu02@amgen.com

&May Mo

Amgen

Thousand Oaks, CA 91320

mm0@amgen.com

&H. Amy Xia

Amgen

Thousand Oaks, CA 91320

mm0@amgen.com

&Joseph G. Ibrahim

University of North Carolina

Chapel Hill, NC 27516

ibrahim@bios.unc.edu

Abstract

It is becoming increasingly popular to elicit informative priors on the basis of historical data. Popular existing priors, including the power prior, commensurate prior, and robust meta-analytic prior provide blanket discounting. Thus, if only a subset of participants in the historical data are exchangeable with the current data, these priors may not be appropriate. In order to combat this issue, propensity score (PS) approaches have been proposed. However, PS approaches are only concerned with the covariate distribution, whereas exchangeability is typically assessed with parameters pertaining to the outcome. In this paper, we introduce the latent exchangeability prior (LEAP), where observations in the historical data are classified into exchangeable and non-exchangeable groups. The LEAP discounts the historical data by identifying the most relevant subjects from the historical data. We compare our proposed approach against alternative approaches in simulations and present a case study using our proposed prior to augment a control arm in a phase 3 clinical trial in plaque psoriasis with an unbalanced randomization scheme.

Keywords Bayesian dynamic borrowing External data Historical data, Clinical trials

1 Introduction

It is becoming increasingly common to utilize statistical methods that incorporate prior information. Such prior information, such as historical data, is naturally integrated in the Bayesian paradigm, where analysts may specify a prior distribution for what evidence they possess prior to the analysis of the data. Bayesian methods for incorporating historical data have been used or proposed in wide a variety of statistical applications including, but not limited to, epidemiology (Warasi et al., 2016), political science (Isakov and Kuriwaki, 2020), engineering (Lorencin and Pantoš, 2017), spatial applications (Louzada et al., 2021), small area estimation (Young and Chen, 2022), and psychology (König et al., 2021).

In the areas of medical device and drug development, where historical data from clinical studies are abundant, it is of interest to incorporate historical data to improve a current trial’s efficiency. For example, in pediatric studies, it can be difficult to recruit an appropriate number of patients, necessitating the use of incorporating prior information (Azzolina et al., 2021). In rare diseases, prevalence is low by definition, and some have recommended Bayesian methods to borrow information from controls to reduce recruitment burden (e.g., Chow and Huang (2020)). In disease areas with unmet need, the incorporation of historical data can make clinical trials more ethical by assigning fewer patients to the control arm. Conversely, in disease areas where an established standard of care exists with a wealth of historical data, conducting balanced randomization can add to the time and cost of patient recruitment, delaying the drug approval process and potentially costing lives. However, some or all subjects in the historical data might be different than the current data set, necessitating so-called dynamic borrowing techniques.

The literature on informative priors on the basis of historical data is rich. One of the earliest and most popular methods for leveraging historical data is the power prior (PP) of Ibrahim and Chen (2000). The PP involves raising the likelihood of the historical data to a power , which is sometimes referred to as the discounting parameter. The PP assumes that the parameters of the current and historical data sets are the same and allows the user to elicit a value to reflect the degree to which they may be different. A second option is the commensurate prior (CP) of Hobbs et al. (2012). Unlike the PP, the CP assumes that the parameters between the data sets could possibly be different, but that the parameters for the current data set are normally distributed with mean equal to the parameters of the historical data set. While the PP only permits blanket discounting, the CP allows parameter-specific discounting. A third popular approach is the robust meta-analytic predictive prior (RMAPP) of Schmidli et al. (2014). The RMAPP is essentially a mixture prior whose first component is an informative prior consisting of a meta-analytic predictive prior for the current data parameter and whose second component is a noninformative (vague) prior. Although the RMAPP is conceptually simple, it has only been developed for single parameter settings, limiting its applicability. Also, the RMAPP is not available in closed-form in general, so that approximations to the prior must be used in practice.

While the PP, CP, and RMAPP allow analysts to flexibly specify the amount of borrowing, they do not directly handle the case where perhaps only a subset of individuals in the historical data set are exchangeable. To this end, propensity score (PS) methods have been developed, where the probability of being enrolled in the current study is modeled as a function of baseline covariates to construct a PS. The PS serves as a measure of similarity between participants in the current and external data sets such that individuals with similar PSs are considered to be exchangeable. The end goal of PS methods is to end up with balance in baseline covariates. However, covariate balance does not ensure that individuals are exchangeable, as the outcome model could be different between the historical and current data sources, particularly when there is heterogeneity in study design.

In this paper, we introduce the latent exchangeability prior (LEAP). The LEAP is a simple, dynamic borrowing prior for historical data that is based on the assumption that possibly only a fraction of individuals in the historical data set are exchangeable with the current data set. The LEAP is a fully Bayesian characterization of exchangeability, providing an advantage over PS based approaches, for which the amount of borrowing necessarily depends on the baseline covariates of the current study. Moreover, the LEAP provides discounting at the individual level, permitting efficiency gains when a subset of patients in the historical data are exchangeable with subjects in the current data. This contrasts with the PP, CP, and RMAPP approaches, which only permit blanket discounting.

This paper proceeds as follows. In Section 2, we motivate our prior with a placebo-controlled clinical trial with an unbalanced randomization scheme, where we wish to augment the control arm for efficiency gains. Section 3 includes the development of the LEAP in full generality. We compare the LEAP to other approaches in Section 4. Section 5 reports results from extensive simulations for the normal linear model, comparing with other suggested priors. Section 6 provides results from data analysis using a real clinical trial. We conclude our results in Section 7.

2 The ESTEEM Trials

Our proposed method is motivated by the ESTEEM trials for patients with moderate-to-severe plaque psoriasis. There was an unmet medical need for this patients population because many of them discontinued the conventional treatments due to safety issues and lack of tolerability. Apremilast, an oral phosphodiesterase 4 inhibitor regulates immune response associated with psoriasis, provided a novel therapeutic option for this population.

The ESTEEM I trial (Papp et al., 2015) was the first phase 3 study evaluating the efficacy and safety of Apremilast for patients with moderate-to-severe plaque psoriasis, which was a double-blinded, placebo controlled randomized trial with 562 subjects randomized to Apremilast group and 282 subjects to placebo group. The ESTEEM II trial (Paul et al., 2015) was another phase 3 placebo controlled clinical study evaluating Apremilast for the same population but with smaller sample size. A total of 411 patients enrolled in the trial, and 274 subjects were randomized to Apremilast arm and 137 were assigned to placebo. We discuss the ESTEEM trials in more detail in Section 5.

Due to the unbalanced randomization, there is a potential for efficiency loss in the ESTEEM II trial. Since the ESTEEM I trial was a larger study with similar design, precision can be increased by borrowing information from the ESTEEM I study. To avoid bias and inflation of the type I error rate, only the most relevant patients from the study should be included. Thus, the goal is to improve the precision of treatment effect estimate for the ESTEEM II study by augmenting its control arm through a dynamic borrowing procedure.

3 The latent exchangeabilty prior

In this section, we develop the LEAP as motivated by the ESTEEM trials. We discuss prior elicitation and posterior propriety. We also introduce a concept called sample size contribution (SSC), which can be used to tune the amount of information borrowing.

3.1 The general methodology

Suppose that we possess historical data with observations. The LEAP assumes that the historical data come from independent observations of a mixture model with components, where the component is parameterized by . Let . In this article, we use the term “density” to refer generally to probability density functions (PDFs) for continuous random variables or probability mass functions (PMFs) for discrete random variables. The joint density for the historical data is given by

| (1) |

where is the observation of the historical data, , and . Throughout this paper, we assume without loss of generality that the first component of the mixture in (1) is the same density function as the current data . Thus, the parameter quantifies the marginal probability that an individual in the historical data set is exchangeable with the current data set.

It is more convenient to work with the density in (1) using a latent variable representation. Specifically, let denote the class to which the subject of the historical data set belongs, where we assume are i.i.d., i.e., the joint mass function of is given by where is an indicator that equals 1 if subject in the historical data belongs to class and 0 otherwise. Then the joint density of is given by

| (2) |

Note that when , the individual in the historical data set is exchangeable with the current data set. This motivates the namesake for the LEAP, namely, that latent variables indicate whether a given individual in the historical data set is exchangeable.

Let denote a prior for and that, adopting the terminology of Ibrahim and Chen (2000) we refer to as the “initial prior.” The LEAP is defined as the prior induced by the density in (2) and the initial prior. Mathematically, we may write the joint LEAP as

| (3) |

The prior in (3) may be interpreted as the posterior density of the historical data, which is modeled as a finite mixture, with prior . The marginal LEAP is given by

| (4) |

Note that the marginal prior in (4) marginalizes over our uncertainty about to which class each observation in the historical data belongs. The LEAP is thus a “dynamic borrowing” prior. Perhaps more importantly, the LEAP is applicable even if only a proportion of individuals in the historical data set are exchangeable.

Let denote the marginal prior of induced by the mixture model, which depends only on hyperparameters. Switching the order of the summation and integration in (4) and normalizing, we can write the marginal LEAP as

| (5) |

The equation in (5) indicates that the LEAP is a mixture prior consisting of components, with the mixture weights being the marginal prior of induced by the mixture model. In Section 4, we show that this characterization of the LEAP is closely related to robust mixture priors and Bayesian model averaging (BMA).

The joint posterior density under the LEAP is given by

| (6) |

where, contains the indices for the historical data classified to be exchangeable and is the number of subjects in class . We provide conditions under which the posterior in (6) is proper in Section 3.2. Note that the posterior in (6), for a particular value of , essentially pools the subjects from the current data set and those from the historical data that are classified to be exchangeable. Hence, has a nice interpretation, namely, the contribution of the historical data set to the posterior of . We refer to the number of observations contributing to as “sample size contribution” (SSC), which is formally introduced in Section 3.3 in the context of limiting the informativeness of the LEAP.

3.2 Prior elicitation

In this section, we discuss prior elicitation for the initial prior for the LEAP. We provide conditions for which the LEAP and the posterior density under the LEAP are proprer.

Recall that the LEAP is essentially the prior induced by the posterior of a finite mixture model for the historical data set. Thus, in the case of unbounded parameters, a proper initial prior is required for the LEAP to be proper. This is most easily observed using the data augmentation scheme in (3). If a component of the finite mixture is unoccupied (i.e., for some ), then the LEAP for the component is the marginal prior .

Conversely, the posterior density in (6) may be proper even if the initial prior is improper. We provide conditions for posterior propriety in Theorem 1.

Theorem 1.

The first condition of Theorem 1 says that each partition of the historical data set must yield a proper posterior based on the marginal initial prior for . In general, the worst case scenario would be when all subjects in the historical data set are assigned to classes other than the first class. A simplified version of the first condition in Theorem 1 is that the posterior density is proper under initial prior without using the historical data.

The second condition of Theorem 1 essentially says that the initial prior must be proper for all components other than the first, which is analogous to the conditions for propriety in finite mixture models. This is intuitive since the likelihood of the current data does not involve the parameters of the other components. For the remainder of this paper, we assume initial priors of the form

In general, it is desirable to elicit a prior on that is noninformative over the -dimensional simplex so that the data can decide how best to allocate the components of the mixture. In Section 3.5, we argue that noninformative Dirichlet priors with small concentration parameters play a fundamental role in the posterior consistency of .

3.3 Sample size contribution

We now develop a stochastic definition of SSC that is intuitive and simple. Under a conditionally conjugate (i.e., Dirichlet) prior for , the prior SSC is available in closed form. Even if a conjugate prior is not used, the prior and posterior SSC is easily computable using numerical and/or Monte Carlo integration. It is clear from the joint posterior in (6) that, for a fixed , the contribution from the historical data to the posterior of is given by . Thus, can be thought of as a “sample size contribution” (SSC). In the sequel, we show that this stochastic concept of the SSC is useful for prior elicitation.

Let denote the -dimensional vector giving the size of each class for a fixed value of . Since are i.i.d., we have that and can write the PMF as The conditional distribution of is thus binomial, i.e., Let denote the marginal prior for . Then the marginal prior for the SSC is given by

| (7) |

As a special case, if is a beta prior with shape parameters , such as when is a Dirichlet prior (in which case and ), then we have i.e., is a beta-binomial random variable.

This characterization of the prior SSC facilitates prior elicitation. For example, suppose and the analyst, after studying the historical data and considering the inclusion-exclusion criteria of the current study, believes with probability that the true number of exchangeable individuals in the historical data set is between and . Then, under a beta prior for , the analyst may use the quantile function of the beta-binomial distribution to find values of hyperparameters and that reflect this belief. Under a non-conjugate prior for , then the PMF in (7) is easily obtainable using numerical integration and it is straightforward to find hyperparameters that satisfy such criteria.

3.4 Larger historical data sets

Occasionally, the historical data sample size exceeds the current data sample size . For example, the ESTEEM I trial is much larger than the ESTEEM II trial. It would be inappropriate to utilize the LEAP as currently developed since it is feasible for the historical data to dominate the posterior. To combat this, we derive a new density over the -dimensional simplex where one of the components is truncated.

Consider the density

| (8) |

where , , and is a normalizing constant. We call the distribution corresponding to the density in (8) a partially truncated Dirichlet (PTD) distribution with concentration parameter and truncation parameters and , and we write

Let and decompose . Let . The following properties of the PTD distribution hold:

-

1.

.

-

2.

.

-

3.

If where is known, then

We formally prove statements (1)-(3) in Section 3 of the Supplementary Appendix. Since the marginal prior on is a truncated beta prior, we may elicit and to guarantee that the historical data do not dominate the posterior. Using (1), (2), and (3), it is straightforward to sample from the PTD density in a Gibbs sampling algorithm.

3.5 Asymptotic properties of the LEAP

In this section, we discuss the LEAP’s asymptotic properties. The asymptotic distribution is crucial to understanding the borrowing properties of the LEAP. We argue that the LEAP can asymptotically pool the current and historical data sets under full exchangeability while being robust to prior-data conflict.

Suppose that the true number of components in the historical data is , but we elicit . Suppose without loss of generality that we may decompose . Under some mild regularity conditions, (e.g., the prior for being noninformative relative to the dimension of the ), Rousseau and Mengersen (2011) show that Hence, extra components will, asymptotically, be given no weight in the resulting posterior density of the historical data. For mixtures of location-scale families, Rousseau and Mengersen (2011) recommend eliciting with for every .

For example, suppose that the current data set and historical data sets are completely exchangeable. Then we have and . It follows that Thus, if the prior for the mixture weights is noninformative, the LEAP asymptotically pools the current and historical data.

Conversely, if no one in the historical data set is exchangeable with the current data set, then . By an analogous argument, under this case, the marginal prior for under the LEAP will converge to the initial prior for . That is,

The facts that the data are pooled under full exchangeability and the historical data are given no weight under a lack of exchangeability illustrate the potential versatility and robustness of the LEAP. Namely, type I error rates should be relatively low when using the LEAP, while efficiency gains can be made even if only a subset of the historical data is exchangeable. This conjecture is verified via simulation studies presented in Section 5.

4 Comparison to other methods

In this section, we compare the LEAP with Bayesian model averaging, the power prior, and PS approaches. We discuss situations under which the LEAP can be competitive in comparison to the other priors.

4.1 Relationship with Bayesian model averaging

Bayesian model averaging (BMA) is considered a gold standard in model uncertainty. In this application, our uncertainty is regarding who from the historical data set is exchangeable with the current data set. It is an ideal, then, that we would set a prior probability for each partition, pool the current data and the historical data assigned to the first class, and average over posterior results. In this section, we show that the LEAP induces a prior probability on the space of partitions, and develop the notion of a posterior partition probability.

Note that we may write the joint LEAP as , where

| (9) |

is the conditional prior for based on a particular classification and

| (10) |

is the marginal PMF of induced by the historical data and initial priors. The denominator in (10) may be interpreted as a marginal likelihood for the mixture model of the historical data, and the numerator may be interpreted as a “partitional marginal likelihood,” i.e., the marginal likelihood based on a particular partition of .

Let the “partition space”, defined as set of all possible partitions of , be denoted by where is the data partition, is the set of indices in belonging to class , and . Let denote the probability from the PMF corresponding with the partition and let be the prior in (9) corresponding to partition . We refer to the ’s as “prior partition probabilities.” The prior for may then be expressed as

| (11) |

where is the likelihood function of based on data . Note that the prior in (11) is equivalent to fitting the posterior for all data partitions and averaging over the prior partition probabilities, which is conceptually equivalent to BMA.

Using the LEAP in (11), the posterior density for is given by

where

is the posterior probability of based on historical data partition and where is the posterior partition probability (marginal likelihood) of the historical data partition, which mimics the posterior model probability in BMA. Hence, the posterior distribution of the LEAP may be interpreted as a “partition averaged” posterior density, i.e., the posterior distribution is a weighted average of partitions of the historical data set. The partitions are weighted based on its prior and how well the partition fits the current data (i.e., the “posterior partition probabilities”).

For example, consider an i.i.d. Poisson model with components for the LEAP. Let the initial prior for be a product of Gamma densities, and that for be a Dirichlet density, where . Let denote the number of subjects assigned to class and let denote the sample mean for the particular partition, where we take if . It can be shown that the posterior partition PMF is given by where is the multivariate beta function, , , and . Table 1 shows the prior and posterior partition probabilities and means for each partition assuming , , , , and .

Recall that the prior PMFs are induced by the mixture model of the historical data set. Since is closer to than , for a fixed value of , the prior PMFs that cluster the first and second observations together are given higher weight than those that cluster the first and third or second and third observations together. Thus, the LEAP has the attractive feature that, for a fixed value of , historical data observations that fit locally to a parametric distribution are given higher prior weight. Table 1 also shows that the posterior partition probabilities are influenced by the observe data via a Bayesian update. For example, since are closer to the mean of the observed data, higher posterior weight is given for than for even though the prior partition probabilities are equal, illustrating the LEAP’s dynamic borrowing properties.

The overall posterior mean is given as , which is identical to the estimated posterior mean using MCMC. An attractive feature of the MCMC approach is that it is computationally feasible in higher dimensions and does not spend time sampling from partitions with low posterior probability.

In Section 4 of the Supplementary Appendix, we provide analytical results of the LEAP for the normal linear model. We show that prior partition probabilities are higher for partitions yielding lower mean squared errors, agreeing with the Poisson example. Furthermore, we show that, all else equal, the posterior model probabilities decrease in , where is the MLE of the current data set and is the MLE for a particular partition of the historical data set assigned to the first component. Thus, posterior partition probabilities will be larger for (and, hence, more posterior weight will be given to) partitions of the historical data set whose MLE is similar to that of the current data set.

We note that the partition averaging representation is closely related to robust mixture priors, which take the form , where , is an informative prior density, and is a vague (i.e., noninformative) prior density. For the LEAP, partitions yielding small values of will be noninformative priors (e.g., if , the prior for is simply the initial prior ).

4.2 Comparison to power priors

The power prior (PP) is a popular prior for historical data sets. The PP is simple, and its interpretation as a discounted likelihood is attractive. Given a historical data set , the PP is given by where is an initial prior for the parameters (which is usually taken to be noninformative and, in some cases, can be improper), is a discounting parameter, and is a normalizing constant.

Note that if is fixed, then the LEAP and the PP are equivalent. A fundamental difference between the PP and the LEAP is that the PP conducts blanket discounting on all individuals in the historical data set. By contrast, the LEAP searches for the most relevant individuals in the historical data set pertaining to the outcome model, so that the most relevant individuals have a higher weight on the posterior density. Thus, in settings where the exchangeability assumption holds, the PP may be more appropriate. If exchangeability does not hold, then the PP can lead to large bias and type I error rates.

While the LEAP is a dynamic prior, the PP is not when is taken as fixed. To solve this issue, the normalized power prior (NPP) has been proposed (Duan et al., 2006). The NPP extends the PP by putting a prior on . Specifically, the NPP is given by where is a prior on . The NPP avoids having to specify a single value for and allows the value of to be data driven. Hobbs et al. (2012) point out that the posterior of under the NPP closely resembles the prior. Thus, even under full exchangeability and a large sample, the posterior mean of will not approach under a flat prior for . However, the posterior mean of will typically approach 0 for flat priors on under incompatibility between the current and historical data sets. If a proportion of individuals in the historical data set are exchangeable, it is unclear how the NPP will behave, but these limiting cases shed some light. If the posterior of is close to zero, then bias (in terms of the posterior expectation of the parameters) will be minimized but efficiency gains are limited. Conversely, if the posterior of resembles the prior, then point estimates under the NPP may have substantial bias.

By contrast, we argued in Section 3.5 that when the samples size for the historical data is large enough, the LEAP has the effect of pooling the historical data and current data sets together when the data sets are completely exchangeable, while being completely uninformative asymptotically if there is complete incompatibility between the two data sets. We numerically examine this property of the LEAP via simulation in Section 5.

In general, there is a computational and implementation advantage for the LEAP over the NPP. Namely, the NPP requires the evaluation of in every iteration of the MCMC scheme in general, and is only analytically tractable under certain special cases (e.g., a normal linear model with a conjugate prior). By contrast, the LEAP simply specifies a mixture model for the historical data set, allowing for non-conjugate priors and avoiding having to compute a normalizing constant under those contexts. In general, it is quite easy to implement the LEAP for any MCMC software that supports mixture models.

4.3 Comparison to propensity score approaches

More recently, so-called “propensity score integrated” priors have been developed, which expand upon existing priors under the assumption that balance in baseline characteristics yields exchangeability. Specifically, let denote the historical data and let denote the current data, where, for the historical and current data sets, respectively, and are responses, and are treatment indicators (equaling 1 if the individual was treated; 0 if the individual received control), and and are vectors of covariates, each of which may include an intercept term.

PS integrated approaches are two-step approaches. The first step, which we refer to as the “design stage,” involves estimating the probability of being in the current study as a function of covariates (i.e., the PS). Note that this PS is different than that in the causal inference literature, which models the probability of receiving treatment as a function of covariates. Let for and let for all denote the indicator to which study each individual belongs. Let and denote the estimated PSs for the current and historical data sets, respectively, that are obtained from a logistic regression model after pooling the two data sets. Then, PS approaches (e.g., matching, weighting, stratification) are conducted in attempt to balance the baseline covariates.

The second step, which we call the “analysis stage,” is to analyze the data obtained from step 1 (excluding the covariates). The underlying assumption is that the PS approach in the design stage balances baseline covariates, so that there is nothing further to control for.

For example, Lu et al. (2022) propose the PS integrated power prior (PSIPP), where observations are stratified by the PS in the design stage and strata-specific PPs are elicited in the analysis stage. Their prior may be represented as where is the mean for individuals receiving treatment in the stratum, contains the historical data assigned to treatment and the stratum, is a stratum-specific discounting parameter, and is an initial prior. A treatment effect, , is then obtained via an average of the stratum-specific treatment effects, i.e.,

There are several disadvantages with PS integrated approaches. First, these approaches are not fully Bayesian. Note that the PS is estimated, but it does not take into account uncertainty surrounding the parameter values of the PS. As a result, each individual is placed into a single stratum during the analysis stage, and uncertainty regarding exchangeability is not incorporated in these approaches. By contrast, in Section 4.1, we showed that the LEAP can be conceptualized as a mixture prior over partitions of exchangeable individuals, directly incorporating this uncertainty.

While it may seem desirable to incorporate a fully Bayesian approach, allowing the PS and outcome parameters to be jointly estimated, it has been shown that these approaches generally lead to increased bias in the Bayesian causal inference literature (Zigler et al., 2013). A quasi-Bayesian approach that cuts the dependence from the PS to the outcome model could alternatively be used, but that approach is also not fully Bayesian.

Perhaps most critically, these approaches implicitly assume that individuals are exchangeable if and only if their covariates are similar. In most regression settings, we condition on covariates, e.g., we model . When adjusting for covariates, we do not require covariate balance for inference to be valid. If there is a discrepancy between the covariate distributions of the historical and current data set but the distribution of the outcome conditional on the covariates is the same, PS approaches can be inefficient since exchangeable individuals may be discarded.

5 Simulations

In this section, we present extensive simulation results comparing the LEAP with several competing priors, including a normalized version of the partial borrowing power prior (Ibrahim et al., 2015a), which we refer to as the NPBPP, the PS integrated power prior (PSIPP), and a reference prior. The simulations are based off of the ESTEEM I and ESTEEM II trials described in Section 2. To compare the borrowing properties of the priors, we generate current data sets that are at least as large as the historical data sets.

5.1 Simulation setup

For the ESTEEM trials, the primary outcome measure was the percentage of participants who achieved an improvement of at least 75 percent in the Psoriasis Area Severity Index (PASI) at week 16 from baseline. A PASI score can range from 0 to 72 with higher scores indicating more severe psoriasis. We consider the percent reduction in the PASI score as the outcome of interest as opposed to the dichotomization of it.

Let denote the current data, where is a treatment indicator ( if subject received treatment; if subject received control) and is a -dimensional vector of covariates, which may contain an intercept term. We generate the data from a linear regression model of the form where is a vector of regression coefficients associated with the intercept and the centered and scaled covariates (age, age2, and baseline PASI score), is the treatment effect, and is an error term. Let the historical control data be denoted by , where is the percent change in PASI score for subject , is a -dimensional vector of covariates, and denotes the number of historical controls. The treatment indicators for the current and historical data sets are generated via for , . We consider current data sample sizes as for . Note that we omit the treatment indicator since each subject in the historical data receives control. The logarithms of age and baseline PASI were generated from a multivariate normal distribution using the sample mean and covariance matrix from the ESTEEM II study, given by with variances and covariance given respectively by , , and .

We consider several cases of exchangeability for our simulation, which we refer to fully exchangeable (i.e., the historical data participants have the same outcome and covariate parameters), half exchangeable (i.e., half of the historical data participants have the same outcome and covariate parameters), and fully unexchangeable (i.e., the historical data participants have different outcome and covariate parameters). We assume all individuals in the current data set are exchangeable, and any sources of heterogeneity arise only in the historical data sets. We let and , defined above, denote the regression coefficients and covariate parameters for the exchangeable group.

For the half exchangeable and fully unexchangeable settings, we define a parameter that enters as a scalar multiple, namely, and , where and are the regression coefficients and the mean for the continuous covariates, respectively, for the unexchangeable group. Taking scalar multiples to both the outcome and covariate parameters puts the LEAP and PSIPP on a level playing field. A total of 20,000 posterior samples were obtained after a burn-in period of 2,000 via the Stan programming language Carpenter et al. (2017).

5.2 Prior elicitation for the simulation study

The NPBPP is given by where is a normalizing constant and is an initial prior. We assume the initial prior takes the form where , , , and are elicited hyperparameters. This choice of initial prior allows the normalizing constant for the NPBPP to be analytically tractable (Ibrahim et al., 2015b), which facilitates MCMC sampling. We elicited , , , and .

A second comparator is PSIPP, which is described in detail in Section 4.3. For our simulations, we stratified by quintiles of the PS. While this selection is somewhat arbitrary, in the causal inference literature, Rosenbaum and Rubin (1984) note that stratification based on quintiles can reduce up to 90% of the bias due to confounding. As suggested by Lu et al. (2022), the elicitation of depends on the degree of overlap in the PS distributions of the strata. Stratification was implemented using the psrwe R package (Wang and Chen, 2022).

Finally, we compare the posterior under the LEAP with a reference prior, where we assume and , where denotes the positive half-normal distribution with mean and variance . We may write this prior as In order to showcase the broad computational feasibility of the LEAP, we do not use conjugate priors or Gibbs sampling. Instead, we take the initial prior in (3) as where we set and .

5.3 Simulation results

For each simulation scenario, we compute percent absolute bias (PAB), mean squared error (MSE), and 95% symmetric credible interval (CI) coverage. The PAB is computed as , where is the posterior mean of the treatment effect for the data set. The MSE is computed as . The CI coverage is computed as the proportion of the samples with CI intervals containing .

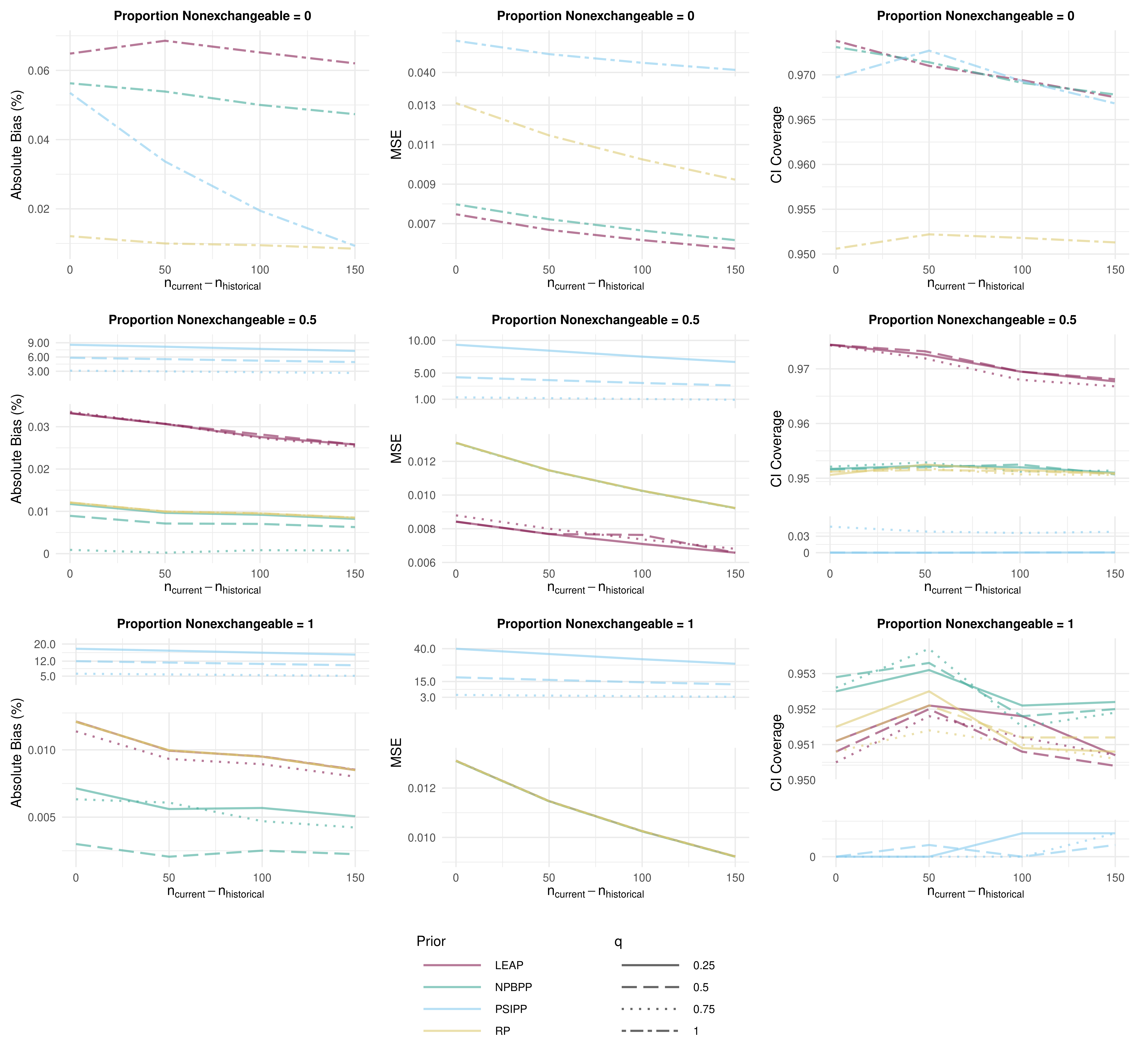

The results of the simulation are presented in Figure 1. The three rows of Figure 1 correspond to the fully exchangeable, half exchangeable, and fully unexchangeable settings, respectively. The three columns of the figure correspond to PAB, MSE, and CI coverage respectively, which are measured on the vertical axis. The different priors are represented as colors and the different values of are represented as line types.

For the fully exchangeable setting (i.e., the first row), the LEAP has the highest PAB and the lowest MSE, which can be attributed to a bias-variance tradeoff. The bias between the priors, however, is negligible, as the maximum observed PAB for the LEAP is less than 0.08%. The LEAP and NPBPP have similar MSEs, while the MSE under the PSIPP is over times that of the LEAP. All three historical data priors had comparable CI coverage.

The PSIPP has poor performance under partial exchangeability and full unexchangeability, where it must be represented as a separate axis. The CI coverage is near 0 for all simulation scenarios and the bias is inflated up to 20%. This may be because the PSIPP is a static borrowing prior, where the amount of borrowing is taken to be fixed based on the PS (which is treated as known and fixed).

Under full unexchangeability (i.e., the third row), the LEAP and the NPBPP are again similar in terms of PAB, MSE, and CI coverage, where they essentially have the same features as a reference prior. Where they differ the most is under half exchangeability (i.e., the second row). We see that the LEAP has slightly inflated bias compared to the reference prior and the PBNPP, with an MSE that is about 33% less than the reference prior across the sample sizes. The LEAP also is the only prior to have higher than nominal CI coverage. This validates the conjecture in Section 3 that efficiency gains can be achieved even if only a fraction of individuals in the historical data are exchangeable.

Overall, it appears that the LEAP is the best performer among these three priors. Having CI coverage at the nominal level under a fully unexchangeable setting is similar to type I error control, which suggests that the LEAP may be a good option when borrowing from external controls. Only the LEAP exhibited efficiency gains under partial exchangeability whereas the performance of the information borrowing priors was similar under full exchangeability.

6 Data analysis example

In this section, we analyze data from ESTEEM II study, augmenting the control arm using the placebo data from the ESTEEM I study. Key summary statistics for the ESTEEM II trial and the placebo arm in ESTEEM I trial are provided in Table 1 in the Supplementary Appendix. Posterior samples were taken using two variations of the LEAP (i.e., and ). We compare posterior summary statistics under the LEAP with the PSIPP, PBNPP, and reference priors described in Section 5.2.

We constrain all information borrowing priors so that a maximum of subjects are borrowed from the historical controls, where is the number of subjects enrolled in arm of study , for , where denotes the control arm and denotes the historical study. Translated to a proportion, this results in a constraint of for in the LEAP and in the NPBPP. The DIC (Spiegelhalter et al., 2002), historical SSC, and the estimated treatment effect on percent change in total PASI Score at Week 16 are evaluated. We report posterior means, standard deviations, and 95% credible intervals of the treatment effect for each prior.

Using the Stan programming language, 250,000 posterior samples were obtained for each prior after a burn-in period of 2,000. Results for the treatment effect from the data analysis are presented in Table 2. Posterior means and standard deviations are provided for all model parameters in Section 5 of the Supplementary Appendix. All priors provided overwhelming evidence that Apremilast results in a lower percent change in PASI scores compared to individuals receiving placebo.

| Prior | DIC | Post. Mean | Post. SD | CI | |

|---|---|---|---|---|---|

| LEAP | ( , | ) | |||

| LEAP | ( , | ) | |||

| PBNPP | ( , | ) | |||

| PSIPP | ( , | ) | |||

| Reference | ( , | ) | |||

As expected, all information borrowing priors resulted in a lower posterior variance for the treatment effect compared to the reference prior, illustrating the benefit of utilizing the historical data. The posterior variance for the treatment effect is lower for the PBNPP than those for the LEAPs. As the study design (e.g., inclusion/exclusion criteria) was very similar for the ESTEEM I and ESTEEM II studies, it is conceivable that all patients in the historical data set are exchangeable with those in the current data set. As discussed in Section 3, PPs can be preferable to the LEAP under fully exchangeable settings since they provide discounting on the entire historical data set, while the LEAP averages over partitions subject to the probability of being exchangeable.

The DIC is the lowest for the PBNPP, indicating that the PBNPP is the best fitting prior, while the two LEAPs resulted in slightly higher DIC. The DIC was lower for these priors than the reference prior, indicating a low degree of prior-data conflict. The PSIPP resulted in a substantially larger DIC compared to the reference prior, which may indicate some model misspecification. The fact that the posterior mean under the PSIPP is quite different than those under the other priors provides support of this conjecture. Moreover, there were large differences between the stratum-specific means for the PSIPP (see Section 5 of the Supplementary Appendix). The posterior variance is lowest for the PSIPP, indicating that the PSIPP is the most aggressive prior in terms of information borrowing.

The posterior means and 95% CIs (in parentheses) for for the LEAP priors were and for and , respectively, and those for in the PBNPP was and , respectively. Thus, the LEAPs and the PBNPP provide a moderate degree of borrowing from the historical data with moderate uncertianty about how much to be borrowed. Since these values are similar but the posterior under the NPBPP resulted in increased precision, the LEAP may discount more aggressively than the NPBPP.

7 Conclusion

In this paper, we developed a novel prior we refer to as the LEAP. The LEAP is a dynamic borrowing prior that is suitable when only a fraction of individuals in a historical data set can be considered to be exchangeable. It may be particularly attractive under situations in which there is a large amount of historical data, and we only wish to borrow from the most relevant individuals in the historical data sets.

One limitation of the LEAP is that it cannot be used for i.i.d. Bernoulli proportion models. This is because the parameters for the mass function for a mixture of Bernoulli random variables are not identifiable. However, the LEAP could be applied to logistic regression models with at least one continuous covariate (e.g., age).

The LEAP opens up several avenues for future research. First is the development of the LEAP for other outcome models. For example, a LEAP could be developed for time-to-event data, where censoring precludes using the LEAP as developed in this paper. Second, a LEAP could be developed to borrow information from real-world data (RWD), where confounding is of paramount concern. Although our results indicate that PS approaches should be used with caution, a LEAP that incorporates the PS to formulate individual-specific probabilities of being exchangeable via a hierarchical scheme could be highly relevant since the amount of borrowing would still be outcome-adaptive.

References

- Warasi et al. [2016] Md S. Warasi, Joshua M. Tebbs, Christopher S. McMahan, and Christopher R. Bilder. Estimating the prevalence of multiple diseases from two-stage hierarchical pooling. Statistics in Medicine, 35(21):3851–3864, 2016. ISSN 1097-0258. doi:10.1002/sim.6964. URL http://onlinelibrary.wiley.com/doi/abs/10.1002/sim.6964.

- Isakov and Kuriwaki [2020] Michael Isakov and Shiro Kuriwaki. Towards principled unskewing: Viewing 2020 election polls through a corrective lens from 2016. Harvard Data Science Review, 2(4):69, 2020.

- Lorencin and Pantoš [2017] Ivan Lorencin and Miloš Pantoš. Evaluating Generating Unit Unavailability Using Bayesian Power Priors. IEEE Transactions on Power Systems, 32(3):2315–2323, May 2017. ISSN 1558-0679. doi:10.1109/TPWRS.2016.2603469. Conference Name: IEEE Transactions on Power Systems.

- Louzada et al. [2021] Francisco Louzada, Diego Carvalho do Nascimento, and Osafu Augustine Egbon. Spatial Statistical Models: An Overview under the Bayesian Approach. Axioms, 10(4):307, December 2021. ISSN 2075-1680. doi:10.3390/axioms10040307. URL https://www.mdpi.com/2075-1680/10/4/307.

- Young and Chen [2022] Linda J. Young and Lu Chen. Using Small Area Estimation to Produce Official Statistics. Stats, 5(3):881–897, September 2022. ISSN 2571-905X. doi:10.3390/stats5030051. URL https://www.mdpi.com/2571-905X/5/3/51. Number: 3 Publisher: Multidisciplinary Digital Publishing Institute.

- König et al. [2021] Christoph König, Sarah Depaoli, Haiyan Liu, and Rens van de Schoot. Moving Beyond Non-informative Prior Distributions: Achieving the Full Potential of Bayesian Methods for Psychological Research. Frontiers in Psychology, 12:809719, December 2021. ISSN 1664-1078. doi:10.3389/fpsyg.2021.809719. URL https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8695424/.

- Azzolina et al. [2021] Danila Azzolina, Giulia Lorenzoni, Silvia Bressan, Liviana Da Dalt, Ileana Baldi, and Dario Gregori. Handling Poor Accrual in Pediatric Trials: A Simulation Study Using a Bayesian Approach. International Journal of Environmental Research and Public Health, 18(4):2095, February 2021. ISSN 1661-7827. doi:10.3390/ijerph18042095. URL https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7924849/.

- Chow and Huang [2020] Shein-Chung Chow and Zhipeng Huang. Innovative design and analysis for rare disease drug development. Journal of Biopharmaceutical Statistics, 30(3):537–549, May 2020. ISSN 1054-3406. doi:10.1080/10543406.2020.1726371. URL https://doi.org/10.1080/10543406.2020.1726371.

- Ibrahim and Chen [2000] Joseph G. Ibrahim and Ming-Hui Chen. Power prior distributions for regression models. Statistical Science, 15(1):46–60, February 2000. ISSN 0883-4237, 2168-8745. doi:10.1214/ss/1009212673. URL http://projecteuclid.org/euclid.ss/1009212673.

- Hobbs et al. [2012] Brian P. Hobbs, Daniel J. Sargent, and Bradley P. Carlin. Commensurate Priors for Incorporating Historical Information in Clinical Trials Using General and Generalized Linear Models. Bayesian Analysis, 7(3):639–674, August 2012. ISSN 1931-6690. doi:10.1214/12-BA722. URL https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4007051/.

- Schmidli et al. [2014] Heinz Schmidli, Sandro Gsteiger, Satrajit Roychoudhury, Anthony O’Hagan, David Spiegelhalter, and Beat Neuenschwander. Robust meta-analytic-predictive priors in clinical trials with historical control information. Biometrics, 70(4):1023–1032, 2014. ISSN 1541-0420. doi:10.1111/biom.12242. URL http://onlinelibrary.wiley.com/doi/abs/10.1111/biom.12242.

- Papp et al. [2015] Kim Papp, Kristian Reich, Craig L. Leonardi, Leon Kircik, Sergio Chimenti, Richard G. B. Langley, ChiaChi Hu, Randall M. Stevens, Robert M. Day, Kenneth B. Gordon, Neil J. Korman, and Christopher E. M. Griffiths. Apremilast, an oral phosphodiesterase 4 (PDE4) inhibitor, in patients with moderate to severe plaque psoriasis: Results of a phase III, randomized, controlled trial (Efficacy and Safety Trial Evaluating the Effects of Apremilast in Psoriasis [ESTEEM] 1). Journal of the American Academy of Dermatology, 73(1):37–49, July 2015. ISSN 0190-9622. doi:10.1016/j.jaad.2015.03.049. URL https://www.sciencedirect.com/science/article/pii/S0190962215014942.

- Paul et al. [2015] C. Paul, J. Cather, M. Gooderham, Y. Poulin, U. Mrowietz, C. Ferrandiz, J. Crowley, C. Hu, R.m. Stevens, K. Shah, R.m. Day, G. Girolomoni, and A.b. Gottlieb. Efficacy and safety of apremilast, an oral phosphodiesterase 4 inhibitor, in patients with moderate-to-severe plaque psoriasis over 52 weeks: a phase III, randomized controlled trial (ESTEEM 2). British Journal of Dermatology, 173(6):1387–1399, 2015. ISSN 1365-2133. doi:10.1111/bjd.14164. URL http://onlinelibrary.wiley.com/doi/abs/10.1111/bjd.14164.

- Rousseau and Mengersen [2011] Judith Rousseau and Kerrie Mengersen. Asymptotic behaviour of the posterior distribution in overfitted mixture models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(5):689–710, 2011. ISSN 1467-9868. doi:10.1111/j.1467-9868.2011.00781.x. URL http://onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-9868.2011.00781.x.

- Duan et al. [2006] Yuyan Duan, Keying Ye, and Eric P. Smith. Evaluating water quality using power priors to incorporate historical information. Environmetrics, 17(1):95–106, 2006. ISSN 1099-095X. doi:10.1002/env.752. URL https://onlinelibrary.wiley.com/doi/abs/10.1002/env.752.

- Lu et al. [2022] Nelson Lu, Chenguang Wang, Wei-Chen Chen, Heng Li, Changhong Song, Ram Tiwari, Yunling Xu, and Lilly Q. Yue. Propensity score-integrated power prior approach for augmenting the control arm of a randomized controlled trial by incorporating multiple external data sources. Journal of Biopharmaceutical Statistics, 32(1):158–169, 2022. ISSN 1054-3406.

- Zigler et al. [2013] Corwin M. Zigler, Krista Watts, Robert W. Yeh, Yun Wang, Brent A. Coull, and Francesca Dominici. Model Feedback in Bayesian Propensity Score Estimation. Biometrics, 69(1):263–273, 2013. ISSN 1541-0420. doi:10.1111/j.1541-0420.2012.01830.x. URL http://onlinelibrary.wiley.com/doi/abs/10.1111/j.1541-0420.2012.01830.x.

- Ibrahim et al. [2015a] Joseph G. Ibrahim, Ming-Hui Chen, Mani Lakshminarayanan, Guanghan F. Liu, and Joseph F. Heyse. Bayesian probability of success for clinical trials using historical data. Statistics in Medicine, 34(2):249–264, January 2015a. ISSN 02776715. doi:10.1002/sim.6339. URL http://doi.wiley.com/10.1002/sim.6339.

- Carpenter et al. [2017] Bob Carpenter, Andrew Gelman, Matthew D Hoffman, Daniel Lee, Ben Goodrich, Michael Betancourt, Marcus Brubaker, Jiqiang Guo, Peter Li, and Allen Riddell. Stan: A probabilistic programming language. Journal of Statistical Software, 76(1), 2017.

- Ibrahim et al. [2015b] Joseph G. Ibrahim, Ming-Hui Chen, Yeongjin Gwon, and Fang Chen. The power prior: theory and applications. Statistics in Medicine, 34(28):3724–3749, 2015b. ISSN 1097-0258. doi:10.1002/sim.6728. URL http://onlinelibrary.wiley.com/doi/abs/10.1002/sim.6728.

- Rosenbaum and Rubin [1984] Paul R. Rosenbaum and Donald B. Rubin. Reducing Bias in Observational Studies Using Subclassification on the Propensity Score. Journal of the American Statistical Association, 79(387):516–524, 1984. ISSN 0162-1459. doi:10.2307/2288398. URL http://www.jstor.org/stable/2288398.

- Wang and Chen [2022] Chenguang Wang and Wei-Chen Chen. psrwe: PS-Integrated Methods for Incorporating RWE in Clinical Studies. 2022. URL https://CRAN.R-project.org/package=psrwe.

- Spiegelhalter et al. [2002] David J. Spiegelhalter, Nicola G. Best, Bradley P. Carlin, and Angelika Van Der Linde. Bayesian measures of model complexity and fit. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(4):583–639, 2002. ISSN 1467-9868. doi:10.1111/1467-9868.00353. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/1467-9868.00353.