Chance Constrained Program with Quadratic Randomness: A Unified Approach Based on Gaussian Mixture Distribution

Abstract

This paper investigates the stochastic program with the chance constraint on a quadratic form of random variables following multivariate Gaussian mixture distribution (GMD). Under some mild conditions, it is proved that the asymptotic distribution of this kind of quadratic randomness is a univariate GMD. This finding helps to translate the chance constrained program into a more tractable one, based on which an effective branch-and-bound algorithm that takes advantage of the special structure of the problem is introduced to search the global optimal solution. Furthermore, it is shown that the error resulting from approximating the quadratic randomness with its associated asymptotic distribution can be reduced by restricting the condition numbers of covariance matrices of the multivariate GMD’s components. In addition, some numerical simulations are also carried out to verify the effectiveness of this flexible and unified approach.

Keywords: Chance constrained program, Gaussian mixture distribution, Quadratic randomness, Asymptotic distribution, Branch-and-bound

1 Introduction

Chance constrained program (CCP) is a typical stochastic program for dealing with random uncertainty in decision making. Initial from Charnes et al. (1958), Miller and Wagner (1965) and Prékopa (1970), CCP has been widely applied in engineering, finance, and other fields. For instance, in finance, the widely encountered problem of maximizing the portfolio return subject to the constraint on value-at-risk (VaR) is actually a special case of CCP, where VaR is the risk measure characterized by a quantile of the loss distribution (see, e.g., Jorion (2007)). However, as Nemirovski and Shapiro (2006) point out, even with the linear structure on the chance constraint, the problem may still be non-convex. Thus CCP is generally computationally intractable, which hinders the applications of the model in practice.

Generally, CCP considers the probabilistic constraint on a randomness that is a function of some random variables and decision variables. Due to the difficulty in solving CCP, previous literature mainly considers the randomness taking a linear form of the random variables. Shapiro et al. (2009) discuss the conditions on the form of randomness and the distribution of random variables under which the CCP is a convex program. Henrion and Moller (2012) provide the gradient formula for linear chance constraints under a possibly singular multivariate Gaussian distribution. There is a branch of literature on linear distributionally robust CCP or its variant VaR optimization via defining the uncertain set of the distribution of random variables with different approaches, such as the known first- and second-moment information of El Ghaoui et al. (2003), the radially symmetric distribution set of Calafiore and El Ghaoui (2006), and the known expectation and dispersion function of Hanasusanto et al. (2017).

In this paper, we consider the general form of quadratic randomness in CCP. More specifically, let us introduce the following quadratic randomness:

| (1) |

where is a random vector with probability distribution , is the decision vector, is a real symmetric matrix, and . We consider the following CCP:

where is a nonempty convex set, , , and denotes the probability that is taken with respect to .

In the literature, there exist some related works on some special cases of QCCP. Zymler et al. (2013) consider a worst-case chance constraint where is in a set of all probability distributions with the same first- and second-moment. They prove that if is a quadratic function of , the worst-case QCCP is equivalent to the worst-case CVaR problem. Cui et al. (2013) study the optioned portfolio selection problem under the mean-VaR framework, which is a special case of QCCP. In their model, is supposed to be normally distributed. Based on the widely used Delta-Gamma-Normal method which can be referred to Hull (2009), they further assume that follows a normal distribution and then the problem can be reformulated as a second-order cone program (SOCP). Zhu et al. (2020) prove that the asymptotic distribution of remains normal distribution if is normally distributed under some mild conditions, which provides the theoretical basis for the Delta-Gamma-Normal method. Kishida and Nagahara (2023) study a system control problem with a similar structure to QCCP. They assume that the distribution of lies in a probability set with known mean and variance, and consider the worst-case chance constraint, which is further approximated by worst-case CVaR for tractability. It is evident that how to specify the distribution of is crucial for solving QCCP.

The procedure of specifying the distribution of underlying random factors is usually called input modeling, which not only affects the choice of solution methods, but also directly affects the rationality of practical application. Therefore, it is meaningful and necessary to develop a unified approach that combines the input modeling with CCP, so that it can be applied to as many cases as possible. In addition, in many application fields, there usually exist substantial observations of the random factors, and thus it is important to estimate the true distribution by learning the data. The mixture distribution model, which is first used by Pearson (1894) in the biological field, is a flexible approach for learning the data. The most attractive characteristic of the mixture distribution is its fitting capacity. The density function of mixture distribution, which is the weighted sum of a finite number of density functions, can approximate many density functions within sufficient precision. More properties about the mixture model can be referred to McLachlan and Peel (2000). Theoretically, Wilson (2000) proves that any univariate integrable distribution function can be approximated by Gaussian mixture distribution (GMD) within any precision. Distributions with some common and even unusual features, such as skewness, fat tail, and multimodality can be well modeled by GMD (Marron and Wand (1992)).

Recently, the combination of CCP and GMD has already been studied in both theory and application. Chen et al. (2018) propose a convex approximation approach to solve the robust CCP where the random parameters are modeled by GMD and the weights on components lie in an uncertainty set based on moment estimation. Hu et al. (2022) consider some typical forms of joint and single CCPs where the random parameters are modeled by GMD. They derive the first-order method and spatial branch-and-bound approach to search the local and the global solutions, respectively. In the field of distributed generation, Chen et al. (2022) assume that the wind output follows GMD and solve a CCP to determine the optimal power scheduling of generators. Ren et al. (2022) use GMD to model the multimodal behaviors of obstacles’ uncertain states and use CCP to guarantee the safety of the trajectory planning.

There are some general scenario approximation methods that can be used to solve QCCP. Calafiore and Campi (2005) and Campi and Garatti (2008) prove the lower bound on the number of samples that guarantees the optimal solution of the scenario approach satisfies the chance constraint with a high confidence level. Campi and Garatti (2011) consider sample discarding and further study the lower bound on the number of samples. Luedtke and Ahmed (2008) replace the violation probability of the chance constraint with the empirical violation probability, which can be reformulated as a mixed integer program. In this paper, different from these approaches, we derive a unified approach for QCCP based on GMD. More specifically, we use multivariate GMD to model the distribution of the random variables and show that the asymptotic distribution of the quadratic form of those random variables follows a univariate GMD under some mild conditions. And this result is further used to reformulate QCCP as a deterministic program with analytical form and then the branch-and-bound algorithm or the first-order method proposed by Hu et al. (2022) can be applied to derive the optimal solution. Furthermore, we show the relationship between the convergence rate and other factors, among which the condition numbers of covariance matrices of GMD’s components are highlighted. To reduce the asymptotic approximation error, we suggest to use condition number constrained GMD to model the distribution of random variables. In addition, we show that this condition number constrained GMD can still approximate any integrable density function within any precision. The main contributions of this paper are as follows:

This paper proposes a unified approach for solving CCP with quadratic randomness based on GMD. Although the true distribution of the quadratic randomness has no analytic form, an approximated global solution can be obtained by combining the asymptotic distribution approximation and the branch-and-bound algorithm.

This paper uncovers the factors that affect the convergence rate of the asymptotic distribution of the quadratic randomness. It is proved that a condition number constrained GMD leads to a faster convergence for the quadratic randomness without loss of fitting capability and flexibility.

The proposed approach can be applied to a wide range of areas where data are available. Unlike other commonly used distributions, GMD can learn the characteristics of distribution from the data, e.g., skewness, fat tail, and multimodal shape. Therefore, our model is especially beneficial to those areas where the data are hard to depict.

The rest of this paper is organized as follows. In Section 2, we discuss the asymptotic distribution of the quadratic form of random variables following GMD. We also explore the associated factors that affect the convergence rate, based on which we investigate how to reduce the approximation errors while using the asymptotic distribution as a proxy of the real one. In Section 3, we reformulate the QCCP and apply the branch-and-bound algorithm to solve the optimization problem globally under the assumption that is a linear function of . In Section 4, numerical experiments are executed to verify the theoretical findings and test the effectiveness of the proposed method. The concluding remark is provided in Section 5.

2 Asymptotic Properties of Quadratic Randomness under GMD

Due to the universal approximation ability of GMD, we suppose in this paper that follows a GMD with Gaussian components. More specifically, the density function of is given by

| (2) |

where the mixture weight , and (abbreviated as ) denotes the Gaussian density function with mean and covariance matrix . Under this setting, we first discuss the asymptotic distribution of the quadratic form of . Then we analyze the convergence rate of the asymptotic distribution. Finally, we discuss the factors that affect the error between the asymptotic distribution and the true distribution, based on which we further explore how to reduce the approximation errors.

2.1 Asymptotic Distribution of Quadratic Randomness

It will be shown that, under some mild conditions, the asymptotic distribution of the quadratic form of random vector following a GMD remains a GMD. We start the analysis from the first- and second-moment of the quadratic form of a random vector following a GMD in the sequel.

Proposition 1.

Proof.

See Appendix A. ∎

Now we turn to the asymptotic distribution of where follows GMD. For simplicity of reformulation, we omit the decision vector and denote , and as , and , respectively.

Without loss of generality, we assume that each , is non-singular. Then we decompose as , and as where is a diagonal matrix with diagonal elements being and is the associated orthogonal matrix. Assume only the first diagonal elements of are nonzero, i.e., . Then we have

| (3) | |||||

If follows the normal distribution , then both the covariance matrices of and are identity matrix. Thus () and () are independent normal random variables with unit variances and means ( and (), respectively. Here, is the th element of . Notice that if is singular, we can also decompose into the form of (3), but a more complicated process of reformulation is required.

According to the Lévy’s continuity lemma (Van der Vaart (1998)) which is summarized in Appendix B, the convergence of characteristic function is equivalent to the convergence in distribution. Noting that the above reformulation is the same for each probability distribution , by investigating the characteristic function of , we have the following results on the asymptotic distribution of while follows a GMD.

Theorem 1.

Suppose that follows a GMD defined by (2), and as , . Then

where , and , if

| (4) |

uniformly holds for any and for .

Proof.

First, we show that

Since the proof of the above equation is the same for each , we consider the case without loss of generality and simplify the notations as , , , , , and .

Denote . According to (3) and the characteristic function of the normally distributed random variable, if , we have

| (5) |

where and . Otherwise, for , there is no linear term in , i.e., , and the proof is a special case of the following one.

Let us first focus on only in the sequel. Since is normally distributed with density , is a non-central Chi-square random variable and its characteristic function is . Thus we have

Denote . Taking logarithm on both sides of the above equation derives

| (6) |

Before taking Taylor’s expansion of the equation (6) with respect to for further analysis, we need to prove is small enough. To this end, in the following we first show . For simplicity, we further denote

Notice that for and for . Then according to some algebraic operations, we have

where . The second equality holds since and are the th element of and . Now we can reformulate as a product of three terms

where the second term is obviously bounded. In addition, according to Proposition 1, , which further implies that is also bounded. For the first term, since , according to assumption (4), we have

which implies that . Thus .

Let us return to equation (6). For any given , there exists sufficiently large such that since . According to Taylor’s expansion, for , and . Then for sufficiently large , equation (6) can be reformulated as

| (7) |

Recalling that , and , we have

According to the assumption (4), for any given and sufficiently small , there exists sufficiently large irrelavent to such that for each . Therefore,

which implies that

| (8) |

According to equations (5) and (7) and the fact that , we have

| (9) | |||||

where the last equality holds due to

and the fact .

Finally, notice that , we have

| (10) |

The proof is completed. ∎

As shown in the following corollary, the conditions in Theorem 1 are very mild.

Corollary 1.

If for each , as , and , , then equation (10) holds.

Proof.

The conditions in Theorem 1 are the same for each . Again, to simplify the analysis, we consider the case for and omit the related subscripts. Notice that and are only determined by parameters of GMD so that they are naturally bounded. Therefore, there exist finite positive constants and such that for . Then, for , we have

where is a constant irrelevant to . Notice that is bounded for so can be any number larger than this bound. Then for any , there exists irrelevant to such that while ,

which implies that uniformly holds for if as . This verifies the conditions in Theorem 1. The proof is completed. ∎

In plain language, Theorem 1 and Corollary 1 conclude that if the number of non-zero eigenvalues of for each are sufficiently large, then the distribution of can be approximated with the following univariate GMD

| (11) |

Recall that and are the mean and variance of with respect to probability distribution .

Specially, when , the distribution of the random variables turns to a multivariate Gaussian distribution and the asymptotic distribution of is a Gaussian distribution, which is consistent with the results of Zhu et al. (2020). If , then becomes a linear function of and this case has already been investigated by Hu et al. (2022).

2.2 Error Analysis of Asymptotic Approximation

Now we explore the factors that cause errors when using asymptotic distribution (11) as an approximation of the true distribution of with finite . Let us start from the conditions proposed in Theorem 1. Notice that the conditions are the same in form for each with respect to . Thus we only analyze the case when for simplicity, and the results can be parallelly generalized to the case of .

For , by dropping subscript again, equation (3) can be simplified as

| (12) |

which is constituted by three terms: weighted sum of the square of independent Gaussian random variables, weighted sum of independent Gaussian random variables, and a constant. Furthermore, the first term and the second term are independent of each other and the asymptotic distribution of is the Gaussian distribution. It is clear that the error of asymptotic approximation is due to the first term. Therefore, we investigate the asymptotic behaviour of the following general weighted sum of non-central Chi-square variables

| (13) |

where for each , is an independent Gaussian random variable with mean and variance 1, i.e., . We provide its convergence rate of the characteristic function of in the following theorem.

Theorem 2.

Suppose is a non-zero decreasing sequence. If , where , then

for sufficient large , where .

Proof.

According to Proposition 2 of Zhu et al. (2020), the logarithm of characteristic function of is

| (14) |

where . We have

| (15) | |||||

Denote . We further have

| (16) |

Notice that and if . Then we have for any and , which implies that uniformly converges to 0 for .

Furthermore, the assumption implies that for sufficient large . Therefore, given , for any and any small enough , there exists a sufficiently large which is irrelevant to such that

Consequently,

which implies that converges to zero as increases to infinity, i.e.,

| (17) |

Theorem 2 indicates that, for given and , the distribution of the weighted sum of non-central Chi-square random variables converges to a Gaussian distribution as the number of random variables increases to infinity, and the convergence rate is . It also says that the difference between the characteristic functions of and its asymptotic distribution also depends on the weight vector and the mean vector . The smaller the differences among the absolute values of weights ’s and the larger the absolute values of means ’s, the faster the convergence. Since this conclusion holds for each probability distribution , these results remain true for the case of GMD with .

2.3 Error Reduction of Asymptotic Approximation

There are two types of errors arising from the asymptotic approximation: underlying fitness error and asymptotic approximation error. Specifically, the underlying fitness error is the one generated by the approximation of the distribution of with a GMD, while the asymptotic approximation error denotes the one caused by the approximation of the distribution of with the associated asymptotic distribution based on the underlying GMD.

Comparing equations (12) and (13) yields

where and are the th elements of and . By Theorem 2, the larger the absolute values of ’s and the smaller the ratio of the largest to the smallest absolute value of non-zero eigenvalues of matrix , the smaller the asymptotic approximation error. Essentially, the error is determined by distribution parameters and of , and . Given the decision vector , and are two constants, and the error is only determined by parameters and . Thus we mainly discuss why and how one can reduce the error of asymptotic approximation by properly setting parameters and in the sequel.

Suppose and . Then , which implies the lowest convergence rate associated with by Theorem 2. Thus a larger deviation between the mean vector and the origin is more likely to lead to faster convergence. However, given different values of and , has different effects on the asymptotic approximation error. Therefore, error reduction may not be achieved by manipulating the mean vector , and we focus on the discussion of in the following.

Since the number of non-zero eigenvalues of matrix instead of its singularity affects our analysis, for simplicity we assume that is non-singular, or equivalently, both and are non-singular, in the following analysis. As to the ratio of the maximum to the minimum of the absolute values of non-zero eigenvalues of matrix , we have the following proposition where we denote by the th largest absolute value of eigenvalues of an -dimensional non-singular matrix for simplicity.

Proposition 2.

Suppose both and are non-singular. Then

Proof.

Notice that is a definite matrix satisfying . Referring to Theorem 8.1.17 of Golub and Van Loan (2013), we have

for , which indicates that

The proof is completed. ∎

By comparison of equation (13) and the first term of equation (12), Theorem 2 and Proposition 2 imply that when the ratio of the largest to the smallest absolute value of eigenvalues of matrix and/or are relatively small, the distribution of can converge to the associated asymptotic distribution relatively easily.

An intuition derived from the aforementioned analysis is that we can constrain ’s, the condition numbers of covariance matrices of Gaussian distributions that constitute the GMD to reduce asymptotic approximation error. Remind that our original motivation for selecting GMD is because it has strong fitting capacity to the real distribution of which can reduce the underlying fitness error. We show in the following that this purpose can also be achieved even if the condition numbers of covariance matrices are restricted.

Theorem 3.

Suppose is a non-negative Riemann integrable function that satisfies . Then for any given and , there exists a Gaussian mixture density function

| (19) |

where , , and , , such that

Proof.

According to the assumption , can be approximated by the finite sum of some simple functions:

where , , are mutually disjoint cubes, and is the indicator function. Without considering those small cubes containing points whose function values are equal to zeros, we further assume . Here, is chosen to be sufficiently large such that

| (20) |

In the following, we show that given the number of cubes and the partition , can be approximated by a Gaussian mixture density function with an error smaller than . And this is done by approximating each simple function with a convolution, and then approximating the convolution with a Gaussian mixture density function.

For simplicity, we denote the simple function as

and a Gaussian density function with zero mean vector and covariance matrix as . Consider the convolution of with which is defined by

| (22) |

There are two properties of this convolution. First,

| (23) |

where is the volume of . The order of integration in (23) is reversed since the integral domains of and are irrelevant. Second, for any ,

| (24) |

Combing with (23)-(24), we can derive the integral absolute error between the simple function and the corresponding convolution

| (25) |

where is the set of interior point with respect to . This absolute error depends on the integral of the convolution on . In the following we show the condition on which the integral absolute error converges to zero, or equivalently, the integral of the convolution converges to .

Recalling (22), the convolution can be rewritten as

where , is the corresponding Jacobi matrix, i.e., the derivative matrix of with respect to , which is equal to the identity matrix here, and . Decompose as , where is a diagonal matrix with entries and is an orthogonal matrix, and further denote . For any , we have that . Note that is the orthogonal transformation of . Thus . Therefore, there exists a subset and with sufficiently small , . Then we have that for any ,

where , and . Given , , if all the eigenvalues , , are small enough, then converges to . Therefore, there exists a sufficiently small and a covariance matrix such that if

then

Note that the above inequality holds for . Integrating both side of the above inequality on and combining with (23) we have

Combining the above inequality with (2.3) further derives

| (26) |

We have proved that any simple function can be approximated by a corresponding convolution function. In the following we prove that the convolution function can be approximated by a Gaussian mixture density function.

According to (23), the convolution is integrable in . Therefore, there exists a compact set with sufficiently large volume such that

According to Lemma 4 in the Appendix C, given , there exists a partition and a function

where , such that

In addition, the above inequality also implies that

Finally we have

| (27) |

We have proved that the convolution can be approximated by a Gaussian mixture density function. In the following we combine all of the above to complete the final step of the proof.

Theorem 3 shows that condition number constrained GMD still has the fitting capacity. It is worth mentioning that although it is possible to reduce the underlying fitness error and the asymptotic approximation error, the cost is that it may increase the number of components.

3 Reformulation and Algorithm for QCCP under GMD

In this section, we develop the solution methodology by reformulating the original problem to a tractable one under the condition that the distribution of can be well approximated by the associated asymptotic GMD. More specifically, according to Theorem 1, the density function of is approximated as

where and .

Following Hu et al. (2022), problem can be equivalently formulated as

where is the cumulative distribution function of standard normal distribution. By introducing auxiliary vector , the above problem can be further equivalently reformulated as

where .

To derive a local optimal solution, some first-order algorithms can be used to solve . In the following we consider a linear form of , and and investigate its global optimal solution, i.e.,

| (30) |

Then a lemma from Zhu et al. (2020) is introduced to reformulate .

Lemma 1.

According to Lemma 1, problem is equivalent to

In general, problem is a non-convex program. For problems with this structure, Hu et al. (2022) propose a spatial branch-and-bound (BB) algorithm to derive the global optimal solution which is placed in Appendix D. Roughly speaking, the BB algorithm relaxes the constraint over the divided sub-domain of cube to solve an easier problem and generate a lower bound for the sub-domain in each iteration. Once the optimal value of the relaxed problem is smaller than the current global optimal value and the optimal solution to the relaxed problem is also feasible to the original problem, the global solution of the original problem is updated and those branches with local lower bounds that are larger than the global one will be pruned. This iterative process generates a sequence of non-increasing values that converges to the global optimal value by solving a sequence of relaxed problems on the subdivided cubes, which is discussed in detail in the sequel.

Suppose that is a subdivided cube. A relaxed problem shown in the following is solved to derive a lower bound for the primary problem over .

Hu et al. (2022) point out that if holds for , then the is a convex program.

In the real implementation, we can only achieve an -optimal solution with the algorithm due to the termination criterion in the code. Suppose is a feasible solution to problem . If , , where

then we call an -feasible solution to . If is the optimal solution and satisfy , , we call it -optimal solution. It is worth mentioning that the if the solution is -feasible, it indicates that , . Otherwise, if , , which contradicts the condition of -feasible. If , both and are equal to . It remains inconvenient to deal with the subtraction of two infinities in implementation. Therefore, in the real implementation, we replace the feasible set with an approximated set as the input of the algorithm, where , and and are sufficiently small numbers.

Proposition 3.

Assume that is compact and the initial cube of the Algorithm 1 satisfies , . To generate an -optimal solution to or verify its infeasibility, the number of relaxed sub-problem needed to be solved is at most

where is the maximum integer smaller than or equal to the given number, , , , is the standard normal density function, , , and is the maximum eigenvalue among , .

Proof.

For any and ,

where . The last inequality hold since the derivative of is and is positive semi-definite and thus .

Suppose that a cube satisfies

If problem is feasible over the , denote the optimal solution as . Since , The solution is an -optimal solution over . If problem is infeasible over , problem must be infeasible over . In both cases, will not be divided into two smaller cubes.

According to the algorithm, the initial cube will be divided into two smaller cubes from the middle point of the longest edge if the longest edge is larger than . Now consider the th edge of the cube with the length of . According to the rule cutting in the middle, to generate all instances with the length of this edge equal to , it is only required time of division. If all instances on this edge are equal to , it is required times of division. It is not difficult to conclude that times of division can obtain all instances that the length of this edge is equal to .

Let . Then the instances with the length of the th edge are equal to

Therefore this edge is no longer divided and the corresponding number of partition is

Note that each division corresponds to one computation of problem . This implies that the number of division is equal to the number of computation of . Therefore, the number of problem solved is at most

The proof is completed. ∎

Proposition 3 provides a worst-case estimation of the number of sub-problems solved in the BB algorithm. The complexity of the algorithm is exponential with respect to the number of components . Fortunately, is usually a small number. Furthermore, as only the sub-cubes that are interacted with the hyperplane are considered in the algorithm, the number of sub-problems needed to be solved is far fewer than the worst-case estimation in proposition 3.

4 Numerical Simulation

In this section we first conduct numerical experiments to verify the theoretical results. Then we test the efficiency of the BB algorithm.

4.1 Test of Conditions for Asymptotic Distribution

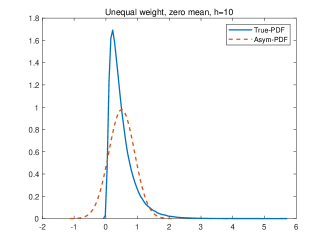

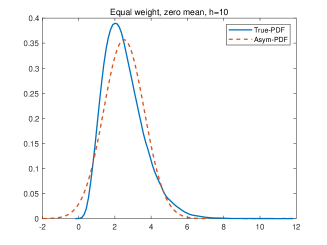

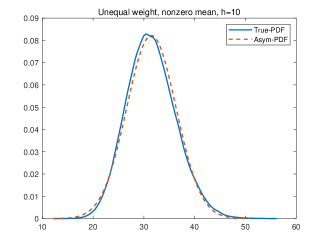

We start from equation (13) to test how the mean ’s and the weight ’s affect the asymptotic errors by directly comparing the density function of with the corresponding theoretical asymptotic density function.

We simulate 20000 samples from independent normal distributed variables with unit variance and different mean settings, and then calculate the weighted sum of the square of these samples to obtain samples of . The sample histogram of is approximated by a smooth curve, which is a representation of the density function of . The asymptotic distribution is directly derived from Theorem 1 by setting . In Figure 1, three sub-figures are displayed with different settings of mean and weight: , and , for the left sub-figure; , and , for the middle sub-figure; , are uniformly sampled from (0,10) and , for the right sub-figure. As we can see, when the means are non-zeros, the asymptotic approximation error is small even though the weights of all random variables are not even. When the weights are equal, the asymptotic approximation error decreases as compared with the unequal case. These findings are consistent with the result of Theorem 2.

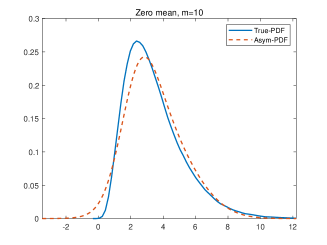

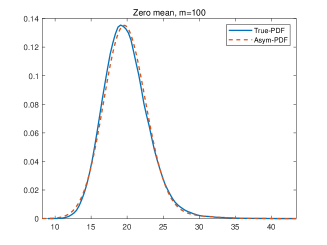

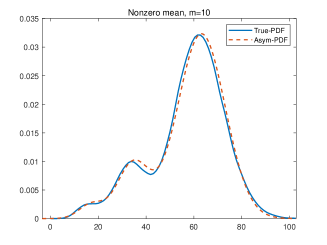

Then we use other numerical experiments to directly verify the result of Theorem 1, again by comparing the density functions. We set , , and . The covariance matrix of each component is generated by , where is an orthogonal matrix that is randomly generated, and is a diagonal matrix whose elements are uniformly generated from (0,1). The mixture weights , , are uniformly generated and then regularized.

The results are displayed in Figure 2. By comparing the left and the middle sub-figures, we can see that as increases, the true distribution of converges to its asymptotic distribution. In the right sub-figure, we set the means of GMD components to be nonzero. Specifically, each is uniformly generated from (0,10). It shows that the asymptotic approximation error of the case with nonzero means is smaller than that of the case with zero means.

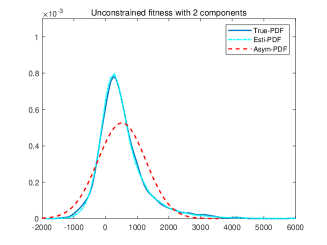

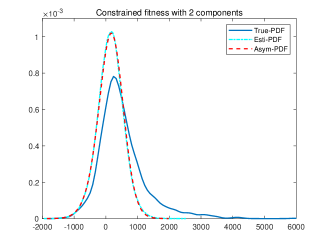

Finally, we provide simulations to verify the implications of Theorem 2, Proposition 2 and Theorem 3, which indicate that the restriction of the condition number of , can reduce the underlying fitness error and asymptotic approximation error simultaneously. The simulation procedures are as follows. First, randomly generate 20000 samples from a 30-dimensional random vector that follows a specified distribution as the benchmark for comparison, which is usually unknown in reality. Then, estimate a GMD or a GMD with condition number constraints with the samples. Denote by the random vector following the estimated GMD. Next, use the Monte Carlo method to draw the density function of and the density function of . By comparing these two density functions we can check the underlying fitness error. Finally, draw the asymptotic density function of according to Theorem 1, and evaluate the asymptotic approximation error by comparing it with the density function of .

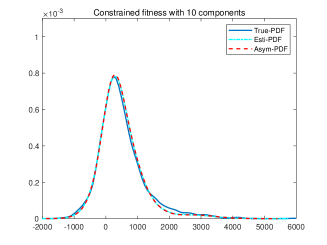

More specifically, in the first step, we specify the distribution of as a GMD with the number of components . For the th component, is uniformly generated from (0,1), , where the elements of are uniformly generated from (0.5,1.5), and the mixture weight is randomly generated. In the simulating results shown in Figure 3, the condition number of the covariance matrices are 436510 and 1742000, respectively. In the second step, the EM algorithm that can be referred to McLachlan and Krishnan (1997) is used to estimate the parameters of GMD. In addition, , is randomly generated from (-100,100) and .

In Figure 3, “True-PDF”, “Esti-PDF”, and “Asym-PDF” represent the density function of , , and the theoretical asymptotic distribution of , respectively. In the left sub-figure, we use the unconstrained GMD in the second step. The estimated density with two components can fit the true density well but the asymptotic density is far away from the estimated density. It implies that the underlying fitness error is small but the asymptotic approximation error is large. When we impose constraints on the condition number, as shown in the middle sub-figure, the estimated density is quite different from the true density but is close to its asymptotic density, indicating that the underlying fitness error is large but the asymptotic approximation error is small. The right sub-figure shows that as the number of components increases, the asymptotic distribution based on the GMD with constraints on condition number can approximate well to the true distribution, implying that the underlying fitness error and asymptotic approximation error simultaneously decrease.

4.2 Test of BB Algorithm

In this subsection, we use some numerical examples to test the efficiency of the BB algorithm. We set the objective function as a linear function , where , , are uniformly generated from (-5,5). To construct a non-convex , for the th component, the entries of are randomly generated from , and the covariance matrix is calculated by , where the entries of are randomly generated from . In addition, we set , , , the th entry of is -1 and otherwise 0, , , and , . For the decision vector , let and other entries vary from [-100,100]. The confidence level is set at .

We compare the efficiency of the BB algorithm and the optimization function “fmincon” from MATLAB. In the options of “fmincon”, the algorithm is set as “SQP” and the maximal function evaluation and maximal iteration are both set at 30000. For the BB algorithm, if the relative error between the lower bound and the current optimal value is smaller than , the algorithm is terminated. If a branch with lower bound and upper bound for satisfies , this branch will not be further divided. We use the optimal solution from “fmincon” as the initial point of the BB algorithm.

Table 1 and Table 2 display the optimal value and computational time of simulated problems with different problem size settings. In this simulation, the mixture weights are randomly generated and satisfy , so that the sub-problems are convex. For each problem size the experiments are executed 5 times and “Max”, “Ave”, and “Min” represent the maximum, average, and minimum values in the five experiments, respectively. Since the sub-problems of the BB algorithm are all convex, the BB algorithm can obtain the global optimal solution in a short time. In addition, as we can see, compared with the BB algorithm, we find that “fmincon” spend less time but only obtain a local optimal solution.

| BB | Fmincon | ||||||

|---|---|---|---|---|---|---|---|

| Max | Ave | Min | Max | Ave | Min | ||

| 50 | |||||||

| 2 | 100 | ||||||

| 200 | |||||||

| 50 | |||||||

| 3 | 100 | ||||||

| 200 | |||||||

| 50 | |||||||

| 4 | 100 | ||||||

| 200 | |||||||

| BB | Fmincon | ||||||

|---|---|---|---|---|---|---|---|

| Max | Ave | Min | Max | Ave | Min | ||

| 50 | |||||||

| 2 | 100 | ||||||

| 200 | |||||||

| 50 | |||||||

| 3 | 100 | ||||||

| 200 | |||||||

| 50 | |||||||

| 4 | 100 | ||||||

| 200 | |||||||

Then we execute other experiments with the same parameter setting except for , , which are randomly generated such that there is at least one satisfies . In this case, the sub-problems of the BB algorithm are non-convex. Table 3 and Table 4 display the optimal value and the corresponding computational time. We can see that the computational time of BB algorithm is much larger than that when sub-problems are convex, even though the problem size is smaller.

| BB | Fmincon | ||||||

|---|---|---|---|---|---|---|---|

| Max | Ave | Min | Max | Ave | Min | ||

| 10 | |||||||

| 2 | 20 | ||||||

| 30 | |||||||

| 10 | |||||||

| 3 | 20 | ||||||

| 30 | |||||||

| 10 | |||||||

| 4 | 20 | ||||||

| 30 | |||||||

| BB | Fmincon | ||||||

|---|---|---|---|---|---|---|---|

| Max | Ave | Min | Max | Ave | Min | ||

| 10 | |||||||

| 2 | 20 | ||||||

| 30 | |||||||

| 10 | |||||||

| 3 | 20 | ||||||

| 30 | |||||||

| 10 | |||||||

| 4 | 20 | ||||||

| 30 | |||||||

5 Conclusion

In this paper, we study the chance constrained program with quadratic randomness, where random variables that constitute the quadratic randomness are supposed to follow GMD. The key finding for solving this problem is that under some mild conditions, the asymptotic distribution of the quadratic randomness is a univariate GMD, which is employed to approximate the distribution of the quadratic randomness and thus an effective BB method can be used to find the global solution. Furthermore, due to the fitting capability of GMD, the proposed method is a unified approach that could be applied in many different situations.

An interesting finding of this paper is that using condition number constrained GMD in the real application can not only reduce the asymptotic approximation error, but also learn the characteristics of the data very well. However, the cost of this constrained GMD is that more components are needed, which leads to more computational times for the BB algorithm. Although we have proved the density function of condition number constrained GMD can approximate any density function to any precision, it is still unclear how many components are exactly needed given the approximation precision. In addition, the algorithm to efficiently estimate the parameters of the constrained GMD is also needed to be investigated. We believe that these issues are worth exploring in the future.

Appendix

Appendix A: Proof of Proposition 1

We first introduce a relevant lemma from Zhu et al. (2020).

Lemma 2.

Given the decision vector ,

respectively. Here, is the trace of a matrix.

Proof.

For then mean, we have

For the variance, we have

Notice that

Therefore, we have

The proof is completed. ∎

Appendix B: Lévy’s continuity Lemma

Lemma 3.

For a sequence of random variables and , if and only if for every . Here, means convergence in distribution.

Appendix C: Introduction of a Lemma for Theorem 3

Before the introduction of the lemma, we recall some notations. Since the conclusion of this lemma holds for any , , without loss of generality, we rewrite , and as , and . The corresponding notations are

Let be a partition of , that is, any entry of belongs to one and only one of , . Denote a function , where , . Denote . By the definition of Riemann integral, the relation between and is that for any given ,

The following lemma indicates that this convergence is a uniform convergence.

Lemma 4.

If is a compact set, then for any given , there exists a partition of such that

Proof.

First we show that for any given , there exists a that is only related to such that if , , where represents the maximal absolute value among the entries of a vector, then .

If is given, is a Gaussian density function with mean vector , which is uniformly continuous, so by definition there exists a such that if , , then

Consider another point and let . If , then

and then

which implies that given , there exists a that is invariant with respect to and such that if , ,

Then let the partition satisfy that for any , , . Then we have

Finally, we have

The proof is completed. ∎

Appendix D: Branch-and-bound algorithm proposed by Hu et al. (2022)

References

- Calafiore and Campi (2005) Calafiore, G., M. C. Campi. 2005. Uncertain convex programs: Randomized solutions and confidence levels. Mathematical Programming 102(1) 25–46.

- Calafiore and El Ghaoui (2006) Calafiore, G. C., L. El Ghaoui. 2006. On distributionally robust chance-constrained linear programs. Journal of Optimization Theory and Applications 130(1) 1–22.

- Campi and Garatti (2008) Campi, M. C., S. Garatti. 2008. The exact feasibility of randomized solutions of uncertain convex programs. SIAM Journal on Optimization 19 1211–1230.

- Campi and Garatti (2011) Campi, M. C., S. Garatti. 2011. A sampling-and-discarding approach to chance-constrained optimization: Feasibility and optimality. Journal of Optimization Theory and Applications 148 257–280.

- Charnes et al. (1958) Charnes, A., W. W. Cooper, G. H. Symonds. 1958. Cost horizons and certainty equivalents: An approach to stochastic programming of heating oil. Management Science 4 235–263.

- Chen et al. (2022) Chen, G., H. C. Zhang, Y. H. Song. 2022. Chance-constrained DC optimal power flow with non-gaussian distributed uncertainties. 2022 IEEE Power Energy Society General Meeting. 1–5. doi:10.1109/PESGM48719.2022.9916658.

- Chen et al. (2018) Chen, Z. P., S. Peng, J Liu. 2018. Data-driven robust chance constrained problems: A mixture model approach. Journal of Optimization Theory and Applications 179 1065–1085.

- Cui et al. (2013) Cui, X. T., S. S. Zhu, X. L. Sun, D. Li. 2013. Nonlinear portfolio selection using approximating parametric value-at-risk. Journal of Banking and Finance 37(6) 2124–2139.

- El Ghaoui et al. (2003) El Ghaoui, L., M. Oks, F. Oustry. 2003. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research 51(4) 543–556.

- Golub and Van Loan (2013) Golub, G. H., C. F. Van Loan. 2013. Matrix Computations. 4th ed. The Johns Hopkins University, Baltimore.

- Hanasusanto et al. (2017) Hanasusanto, G. A., V. Roitch, D. Kuhn, W. Wiesemann. 2017. Ambiguous joint chance constraints under mean and dispersion information. Operations Research 65(3) 751–767.

- Henrion and Moller (2012) Henrion, R., A. Moller. 2012. A gradient formula for linear chance constraints under gaussian distribution. Mathematics of Operations Research 37(3) 475–488.

- Hu et al. (2022) Hu, Z. L., W. J. Sun, S. S. Zhu. 2022. Chance constrained programs with gaussian mixture models. IISE Transactions 54(12) 1117–1130.

- Hull (2009) Hull, J. 2009. Options, Futures and Other Derivatives. Pearson Prentice Hall, New Jersey.

- Jorion (2007) Jorion, P. 2007. Value at Risk: The New Benchmark for Managing Financial Risk. McGraw-Hill Companies, New York.

- Kishida and Nagahara (2023) Kishida, M., M. Nagahara. 2023. Risk-aware maximum hands-off control using worst-case conditional value-at-risk. IEEE Transactions on Automatic Control doi:10.1109/TAC.2023.3235246.

- Luedtke and Ahmed (2008) Luedtke, J., S. Ahmed. 2008. A sample approximation approach for optimization with probabilistic constraints. SIAM Journal on Optimization 19 674–699.

- Marron and Wand (1992) Marron, J. S., M. P. Wand. 1992. Exact mean integrated squared error. Annals of Statistics 20 712–736.

- McLachlan and Peel (2000) McLachlan, G., D Peel. 2000. Finite Mixture Models. Wiley, New York.

- McLachlan and Krishnan (1997) McLachlan, G. J., T. Krishnan. 1997. The EM algorithm and Extensions. John Wiley & Sons, New York.

- Miller and Wagner (1965) Miller, L. B., H. Wagner. 1965. Chance-constrained programming with joint constraints. Operations Research 13 930–945.

- Nemirovski and Shapiro (2006) Nemirovski, A., A. Shapiro. 2006. Convex approximation of chance constrained programs. SIAM Journal on Optimization 17(4) 969–996.

- Pearson (1894) Pearson, K. 1894. Contributions to the mathematical theory of evolution. Philosophical Transactions of the Royal Society of London 54 326–330.

- Prékopa (1970) Prékopa, A. 1970. On probabilistic programming. In proceedings of the Princeton Symposium on Mathematical Programming, Princeton University Press, Princeton, NJ, 113–138.

- Ren et al. (2022) Ren, K., H. Ahn, M. Kamgarpour. 2022. Chance-constrained trajectory planning with multimodal environmental uncertainty. IEEE Control Systems Letters 7 13–18.

- Shapiro et al. (2009) Shapiro, A., D. Dentcheva, A. Ruszczynski. 2009. Lectures on Stochastic Programming: Modeling and Theory. Society for Industrial and Applied Mathematics, Philadelphia, PA.

- Van der Vaart (1998) Van der Vaart, A. W. 1998. Asymptotic Statistics. Cambridge University Press.

- Wilson (2000) Wilson, R. 2000. MGMM: multiresolution Gaussian mixture models for computer vision. Proceedings 15th International Conference on Pattern Recognition. ICPR-2000, vol. 1. 212–215. doi:10.1109/ICPR.2000.905305.

- Zhu et al. (2020) Zhu, S. S., W. Zhu, X. Pei, X. T. Cui. 2020. Hedging crash risk in optimal portfolio selection. Journal of Banking and Finance 119 105905.

- Zymler et al. (2013) Zymler, S., D. Kuhn, B. Rustem. 2013. Distributionally robust joint chance constraints with second-order moment information. Mathematical Programming 137 167–198.