Convex scalarizations of the mean-variance-skewness-kurtosis problem in portfolio selection

Andries Steenkamp \thanksCentrum Wiskunde & Informatica (CWI), Amsterdam. \urlandries.steenkamp@cwi.nl \newlineThis work is supported by the European Union’s Framework Programme for Research and Innovation Horizon 2020 under the Marie Skłodowska-Curie Actions Grant Agreement No. 813211 (POEMA).

Abstract

We consider the multi-objective mean-variance-skewness-kurtosis (MVSK) problem in portfolio selection, with and without shorting and leverage. Additionally, we define a sparse variant of MVSK where feasible portfolios have supports contained in a chosen class of sets. To find the MVSK problem’s Pareto front, we linearly scalarize the four objectives of MVSK into a scalar-valued degree four polynomial depending on some hyper-parameter . As one of our main results, we identify a set of hyper-parameters for which is convex over the probability simplex (or over the cube). By exploiting the convexity and neatness of the scalarization, we can compute part of the Pareto front. We compute an optimizer of the scalarization for each in a grid sampling of . To see each optimizer’s quality, we plot scaled portfolio objective values against hyper-parameters. Doing so, we reveal a sub-set of optimizers that provide a superior trade-off among the four objectives in MVSK.

1 Introduction

We gently introduce the reader to the well-studied portfolio selection problem in finance. We progressively extend the model to include higher-order moments, shorting and leveraged positions, and sparsity. We explore some results of multi-objective optimization to apply the results later in Section 2.

1.1 The portfolio selection problem

In finance, portfolio selection is the task of selecting from a pool of available assets a weighted subset, called a portfolio, in such a way that the portfolio maximizes return on investment while minimizing the risk of loss of capital. In 1952 Harry Markowitz [21] systematized portfolio selection by phrasing it as a constrained quadratic optimization problem involving data on past returns. Markowitz modeled the portfolio’s profitability by the mean returns, and he modeled risk by using the variance as a proxy. Hence the model is a bi-objective optimization problem over the simplex:

| (1) |

where is the standard simplex, is a covariance matrix, and is the vector of means. Here denotes the number of assets that are available for selection and, for each , denotes the weight of the ith asset in the portfolio . Problem (1) can be converted into a single-objective optimization problem of the following form

| (2) |

for some hyper-parameter modelling the investors risk tolerance. Hence, there are two conflicting objectives, maximizing the mean returns and minimizing the variance in the returns. Though the model may seem crude by modern standards, it began the field of portfolio optimization, see [5]. Variants of this model are still used and studied, see, for example, [17, 20, 14]. We will consider an extension of (1) before stating our contribution to the field.

1.2 Extending to higher order moments

The Markowitz model is often called the mean-variance framework, as it only uses the mean and the variance in describing the problem. In statistics, the mean and variance are, respectively, called the first and second moments of the data. Using only the first two moments, the Markowitz model implicitly assumes that the data comes from a Gaussian distribution, however, this is not the case in practice, see [26, 28]. Assuming the data is Gaussian, one underestimates the frequency of extreme events, like rare but significant losses. To account for this underestimation, several authors propose extending the model to include higher order moments like skewness and kurtosis, see [16, 31, 23, 14, 27].

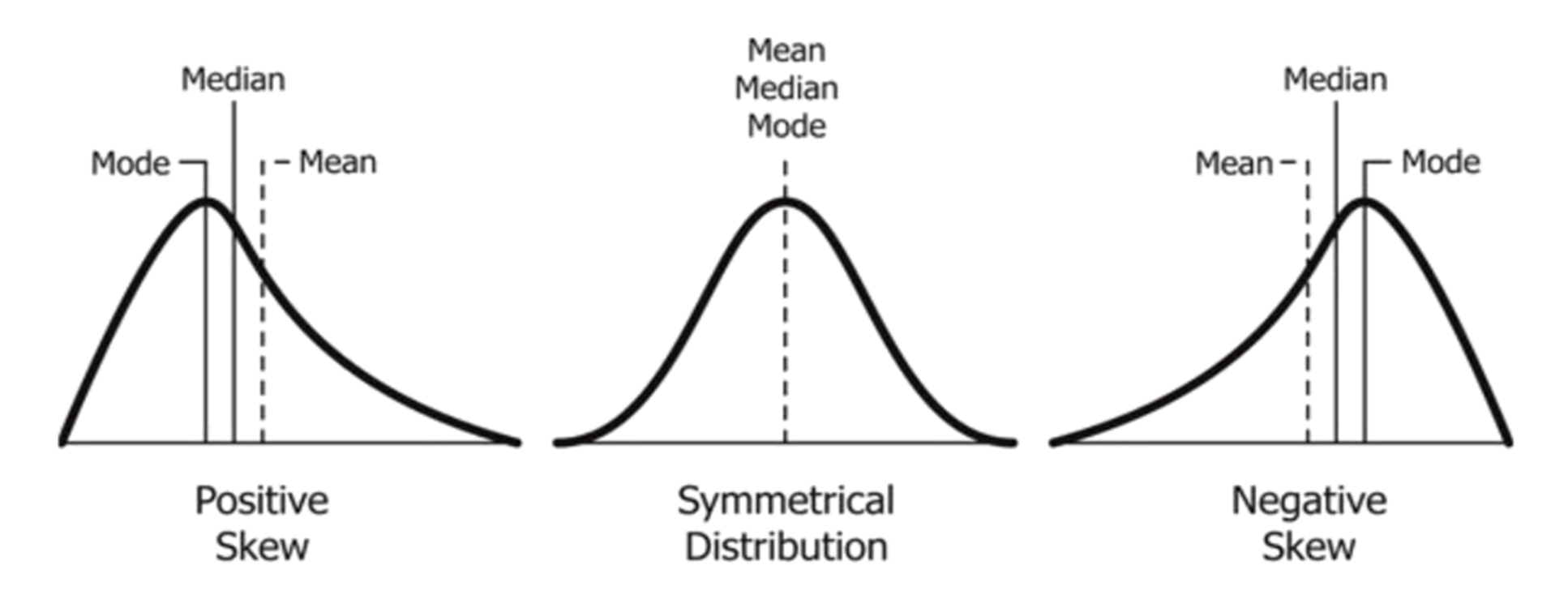

Skewness, the third data moment, represents the asymmetric characteristics of a distribution. One can think of a Gaussian leaning in a particular direction, the skewness quantifying the direction and intensity of the leaning.

Positive skewness implies higher chances of occasional rare high returns, while

negative skewness implies the potential risk of occasional significant losses, see Fig. 1.

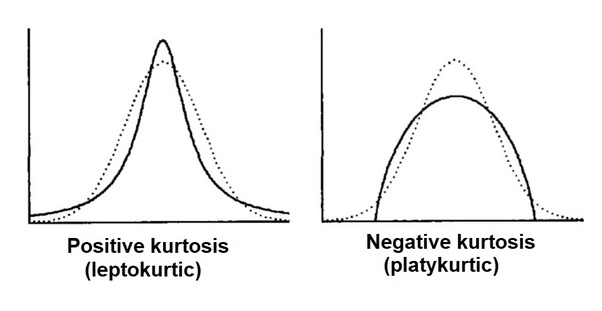

Kurtosis, the fourth data moment, is similar to variance in that larger values correspond to a sharper peak and fatter tails, i.e., more extreme returns on either side of the mean, compared with the normal distribution, see Fig. 2.

Alternatively, some researchers use notions of entropy and mutual information instead of correlation to quantify risk [12].

Most investors would prefer a large positive skewness and a small kurtosis if given a choice. Adding these new terms improves the model’s expressiveness at the cost of adding more complexity. Skewness, in particular, is likely non-convex. We will elaborate more on the objective functions in Section 2.3.

This extended model is called the mean-variance-skewness-kurtosis (MVSK) problem. We give the mathematical description in Section 2.3. It is a multi-objective optimization problem (MOOP) with the first four moment functions as objectives, see (13) and (15) for the formal definitions. Solving the MVSK and some of its variants will be our primary task in this paper. We mention extensions to even higher-order moments in Section 5.

1.3 Including leverage and shorting

The MVSK model, though an improvement on the mean-variance model, does not fully capture the richness of portfolio selection in the financial industry. We consider two further extensions to the model. Note that each extension is stand-alone and complementary to the rest. Hence they can be studied separately and used in combination. The first extension we consider is the option to hold shorted and leveraged positions, this means that the portfolio can consist of borrowed assets. Financial details aside, we allow some of the assets in the portfolio to have negative weights or weights exceeding one. Mathematically, we no longer optimize over the simplex but rather over a bounded cube. Secondly, we consider sparsity. A portfolio is sparse if it supports fewer assets than the selection pool allows. Given two equally well-performing portfolios, one often prefers the sparser portfolio to dense portfolios (where all weights are non-zero) because having fewer assets to manage leads to fewer transaction costs when rebalancing, see for example [5]. Alternatively, some authors explicitly model transaction costs directly, as done in [19].

1.4 Multi-objective optimization problems

In addition to inheriting the difficulties of single-objective optimization problems, MOOPs have new challenges to address, see, e.g., [11] for background. Consider the general MOOP:

| (3) |

where are some scalar valued functions acting on , and .

How one defines optimality is the first change from single to multiple objectives. Real numbers are well ordered by , and as such, it is clear when one solution gives a better objective value than another. In contradistinction, the values of MOOPs are real-valued vectors, and thus they are only partially ordered by , applied entry-wise between two vectors (of equal size). Optimal solutions to MOOPs are hence only optimal in the sense of not being strictly worse than any other solution vector. Formally we define a partial order on vectors :

| (4) |

A point is said to be Pareto optimal for (3) if there exists no such that

| (5) |

Similarly, a point is said to be locally Pareto optimal for (3) if it is Pareto optimal in some open neighborhood of . The Pareto front of (3) is defined as the set of all Pareto optimal solutions of (3). The following is a well-known fact.

Lemma 1.

Proof.

Suppose by way of contradiction that is not globally Pareto and let be a point such that . Take any and observe that via convexity we have

Since this holds for arbitrarily small positive values of it holds that is not locally Pareto optimal, contradicting our initial assumption. ∎

Among the several approaches to optimizing a MOOP, we will be looking for optimizers via scalarizations of the MOOP. Scalarization is a well-known approach that converts a MOOP into a single objective optimization problem called the scalarized problem. Several authors have done this for MVSK by encoding some objectives as constraints, see, e.g., [20]. One downside of this approach is that one must make an a priori estimate of these objectives. Alternatively, one can scalarize by combining the multiple objectives into a single scalar-valued objective function. We follow this approach. For the MVSK problem, the literature predominantly considers two scalarizations. The first is the Minkowski scalarization, as seen in [17, 23, 1]. Here one first computes the optimal values for each of the objectives independent of the others

Using these independent optima one constructs, for some positive user-defined hyper-parameter , the Minkowski distance scalarization is as follows:

| (6) |

The second scalarization is simply a linear combination of the objectives with the linear weights being some choice of hyper-parameter , see [14, 13]. The resulting scalarized optimization problem is hence

| (7) |

where

| (8) |

Note that this scalarization has a linear dependence on hyper-parameters and is also conceptually simple to interpret. We will be using this linear scalarization throughout this paper. Optimizers of the scalarized problem are not guaranteed to be Pareto optimal for the MOOP, but for neat scalarizations, this is the case. A scalarization is said to be neat if any optimal solution of the scalarized problem is also a Pareto optimal solution of the original MOOP.

Lemma 2 (Proposition 3.9 [11]).

Proof.

Consider now the case when the feasible set is defined as

| (9) |

for some functions . Let denote the index set of active constraints. The following result holds for the MOOP (3).

Theorem 3 (Theorem 3.25 [11]).

Let be a set as defined in (9). Let , be scalar-valued functions that are continuously differentiable at . Assume that is a Pareto optimal point of (3) and that there is no vector such that

| (10) |

Then there exist vectors and such that , , and

Therefore, is a KKT point of the following scalarization of problem (3):

| (11) |

A point that is Pareto optimal and satisfies the system (10) is also known in the literature as being properly efficient in the Kuhn-Tucker sense (see Definition 2.49 in [11]).

Proposition 4.

Proof.

The claim follows from the fact that any KKT point of a convex problem must be a global optimizer. ∎

Let us again consider the scalarized problem (7) where for some . Depending on the functions , the hyper-parameter , and the domain , problem (7) can still be extremely difficult to solve. However, in the special case when the objective and the domain are convex (strictly convex), there are efficient methods to find the (unique) minimizer [2]. Having found an optimizer to the scalarized problem, Lemma 2 relates said optimizer back to a Pareto point of the MOOP.

The core theme of this paper is to partially recover the Pareto set of the MVSK problem by solving different linear scalarizations of the MVSK problem. In order to achieve this we identify classes of hyper-parameters that ensure the resulting scalarization is convex over the domain of optimization, which is either the standard simplex or the cube.

1.5 Structure of the paper

In Section 2 we formally derive the MVSK problem using a random variable to model asset price data, see (16).

Applying the linear scalarization, we get a problem of the form (7). If we take , then becomes a quartic polynomial.

For our purposes, the domain can be either the simplex or the cube.

Polynomial optimization is an active field of research, for a general reference on this topic we refer to [18].

For general polynomial optimization, quadratic polynomials are already hard to optimize over the simplex, see [24].

However, in our particular setting, we will show that for some ’s, the problem is convex and can be efficiently solved.

The section ends with a suggested sparse variant of MVSK.

In Section 3 we characterize the parameters for which is convex. Thus we obtain, for some scalarizations, a differentiable convex problem of the form (7). We can apply first-order optimization methods to this problem and obtain good approximations of optimizers. The particular algorithm we use is called FISTA, described in more detail in Section 4.1. For the scalarizations that are not convex, we still apply FISTA, though we only have that the returned optimizer is locally optimal. Regardless, a local optimizer of (7) is still a locally Pareto optimal solution to (7), provided for all .

We partially recover the Pareto set of MVSK by solving different scalarized MVSK problems. In Section 4, we demonstrate the efficacy of our approach by conducting a numerical experiment on real-world data. We explain the well-known optimization algorithm FISTA that we use, and we list its beneficial properties. Four optimization domains are considered: the simplex, the cube, and their respective sparse analogs. We visualize and compare the resulting approximate Pareto sets. A striking feature of our numerical results is that although each Pareto point obtained in this way is not strictly worse than any other in the sense of the partial order described in (4), there are some points that provide a better trade-off among the four objectives. We call such points solutions of superior trade-off. These solutions of superior trade-off are described in Section 4.3 and visualized in Section 4.4.

Finally we conclude with some remarks on even higher order models and alternative scalarizations in Section 5.

Hence, our contributions in this paper are three-fold. We characterize some scalarizations of the MVSK problem that result in a convex problem; we propose a sparse MVSK problem; we show that some Pareto optimizers give a better trade-off among the different objectives.

2 The MVSK model

This section gives the mathematical formulation of the MVSK optimization problem. We start with a random variable representing asset prices and then define the four objectives that constitute the MVSK MOOP. Finally, we conclude with a proposed sparse variant of MVSK and a list of some motivations why this model is of practical interest.

2.1 The domain of optimization

A portfolio consists of a weighted selection of assets, represented by . We will consider two choices of the domain for portfolios.

The first is the standard simplex. In this setting, investors cannot “short sell” assets nor take “leveraged” positions. We write , where .

Short selling is the act of selling a borrowed asset with the hope that it will depreciate over time. After the asset has lowered in price, one repurchases the asset to return to the original owner. Mathematically, negative portfolio weights can model this, i.e., . In finance, leverage is buying additional assets on credit, and the investor then aims to make an additional profit using the extra assets before repaying the debt. Mathematically this means that the portfolio weights can sum up to more than one.

The second setting is the cube, where we allow short selling and leverage.

There is a bound on how leveraged a position can be.

Mathematically we write , where we set for simplicity.

For a general overview of financial terms, we refer the reader to any standard text like [22].

To distinguish the general results of Section 1 from the particular setting of MVSK, we change the notation from to . With this, we intend the reader to not think of a general vector anymore but rather a vector of weights, or .

2.2 Computing the objective functions

In portfolio optimization, the underlying assets are usually paper assets like stock in publicly traded companies. We do not restrict ourselves to this setting, but it is a useful example of the model. For asset let denote the relative return, a random variable taking values in . Hence, is the fractional change in value relative to the initial cost of purchasing the asset . Let

| (12) |

denote the vector of expected returns. Now define the following random variable:

which we call the centralized relative returns.

We can now begin to build the multi-objective MVSK problem. To start, we define the statistical moments as functions of the weights and the data . Let

| (13) |

represent the expected returns of the portfolio. We do not use as it has a zero mean. Similarly, we can define for the functions

| (14) |

These functions are related to the second, third, and fourth moments of as follows:

| (15) |

where is the covariance matrix, is the skewness matrix, and is the kurtosis matrix, all w.r.t. the data . With slight abuse of terminology, we refer to as the variance of portfolio , and similarly, and are called its skewness and kurtosis.

Let us examine these functions. Firstly we note that , and are convex. Indeed is linear and therefore convex. The functions and are convex and nonnegative for all by virtue of and being positive semidefinite. To see why is PSD observe that is the expectation of a random variable taking PSD matrices as values. Hence, the Hessian of , , is PSD, and thus is convex. The convexity and nonnegativity of the kurtosis function follows for a similar reason.

2.3 MVSK optimization problem

With the individual objective functions defined in (13) and (15), we can define the MVSK MOOP:

| (16) |

Interpret this program as follows: one wishes to maximize returns while minimizing extreme events like rare but significant losses. The “odd” functions and correspond, in expectation, to increased returns when positive and to losses when negative. While the “even” functions and describe the spread of returns, with larger values corresponding to more significant fluctuations at the extremes. Note that variance and kurtosis are symmetric, which means they treat extreme profits and losses with equal prejudice. As a rule of thumb, investors prefer consistently high returns and dislike volatility.

In contradistinction to scalar optimization problems with a single scalar optimal value, a MOOP has a set of Pareto optimal points, sometimes called its efficient frontiers or Pareto front. From the investor’s perspective, one need only choose from this frontier to be sure that no strictly better choice exists. Some Pareto solutions provide a better spread among the multiple objectives than others, more on this in Section 4. However, it still falls to the investor to decide how to choose among these solutions. Hence our task is to find this efficient frontier of (16), but first, let us consider some extensions.

2.3.1 A sparse variant of MVSK

In selecting a portfolio, we prefer sparse weights, that is, portfolios with most weights equal to zero. Sparse should be understood in contradistinction to dense (portfolios), where almost all of the possible asset choices have a non-zero weight assigned. Having more assets beyond a point of “reasonable diversification” could increase management fees and transaction costs, as rebalancing the portfolio requires adjusting more weights. The additional costs will then counteract the profitability of the portfolio. A second reason a portfolio can become sparse is by disallowing certain asset combinations. When one knows that two assets are causally linked, the portfolio gains little diversification by holding both. One of the core ideas in portfolio selection, diversification, is the principle that buying causally unrelated stocks will protect the portfolio from the possibility of significant losses. The idea is that one expects the depreciation of a single stock to be unrelated (or inversely related) to the value of other stocks. Of course, this only holds outside of systemic events like economic crises, see [29]. Diversification is the motivation for why one does not simply invest all one’s capital in the single asset showing the largest return. We reformulate a general sparse version of the problem (16) as follows:

| (17) |

where is some set of subsets of .

There are two motivating instances for the above form of sparsity.

Reducing transaction costs and management fees by bounding the number of stocks in the portfolio. We do this by setting

for some integer . This is equivalent to saying that the solution must not have more than non-zero entries, i.e., , where . In terms of the portfolio, this is equivalent to holding at most assets at any given time.

Accounting for causally linked stocks. To factor in the notion of diversification into the above model, we set

for some , where is the Pearson correlation coefficient, see [30], but other notions of mutual information or expert opinion could also be used in constructing .

3 Scalarizing MVSK

In this section, we will consider a linear scalarization (18) of the MOOP (16) and analyse the conditions under which the resulting objective is convex. In particular we characterize the coefficients for which is convex over the simplex (resp., cube) in terms of the data . In general, it is highly desirable for objective functions to be (strict) convex as it ensures that any local optimizer is also a (unique) global optimizer. Convex functions are well studied and efficiently optimized if the gradient is known, see, for example, the standard textbook [6].

For any choice of , consider the following scalarization of (16):

| (18) |

This linear formulation is often called the “weighted sum method”. Recall that we are looking for the optimizers of and not for the optimal value. Since for any scalar we have

we can without loss of generality scale to lie in the simplex .

Our ambition is hence as follows: Via Lemma 2, we can find Pareto optimal solutions of (16) by solving (18) for such that is convex. By doing this for various appropriate , we hope to recover part of the Pareto front. Later we also apply the same process for that are neither strictly positive nor resulting in convex , this still yields a local optimizer of (18) but we have no guarantees of it being Pareto optimal for the MOOP (16).

It is not necessarily true that all Pareto optimizers of (16) are also optimizers for some scalarization of the form (18). It is true, however, that each Pareto point of (16) satisfying (10) corresponds to a Karush–Kuhn–Tucker (KKT) point of some scalarization with , as was seen in Theorem 3. Applying Theorem 3 to our setting, we have the following result.

Corollary 5 (KKT).

We now shift to finding for which is convex over the simplex, the cube, or the whole space .

3.1 Convex scalarization of MVSK

In general, optimizing a quadratic polynomial over the simplex is already hard. Indeed, recall the Motzkin-Straus [24] formulation of the stability number of an undirected graph. Problem (18) has a quartic objective and is expected to contain the difficulty of the quadratic case. However, we can solve some convex problems efficiently using gradient methods [6]. We now give several characterizations of for which is convex. Begin by considering the gradient of at a point

The Hessian of at is given by

| (19) |

where we define

| (20) |

Define the quadratic polynomial

| (21) |

and observe that under the change of variables .

Lemma 6.

Let , . Then for all if and only if one of the following conditions is satisfied:

-

(i)

and ,

-

(ii)

and ,

-

(iii)

, , , and ,

-

(iv)

, , , and .

Proof.

If , then if and only if . Requiring that this hold for all is equivalent to requiring . So we find case (i).

Suppose and consider the discriminant of .

If then has no real roots, meaning that for all . The condition is equivalent to requiring . In the case that then has double root at and for all . So we find case (ii).

Assume . Then has two roots

Hence there are only two cases when for all . The first is when all values of are below , i.e.,

Hence, we have shown case (iii). The second case is when all values of are above , i.e.,

With this case (iv) is proved and the proof is concluded. ∎

Observation 7.

Note that condition (iv) in Lemma 6 implies . In numerical experiments with real-world data, we often have , and thus condition (iv) seldom holds.

Corollary 8.

Proof.

These results follow directly from the fact that the Hessian is PSD when , i.e.,

∎

The results of Lemma 6 can be extended to strict convexity by making a timid assumption on the random variable .

Corollary 9.

Consider the Hessian given in (19) for some . Assume that and that, for all , a.e.111The abbreviation a.e. stands for almost everywhere and is used to indicate that the accompanying statement may fail, but only on a set of measure zero.. Then is strictly convex on .

Proof.

Since a.e. for all , we have that on . Assume by way of contradiction that is not positive definite, then there exists a nonzero such that By linearity of the expectation this implies that Since each argument is a.e. nonnegative we have that and thus by virtue of a.e.. Taking the expectation we get contradicting our assumption that . ∎

Observation 10.

The scalarization is convex on the standard simplex if and only if the hyper-parameter satisfies

| (22) |

When , is convex, so is the limiting factor to PSDness of the Hessian of . Hence, we seek the largest for which for all . The parameter plays no role in the convexity of . The Hessian is linear in but quadratic in . The expression in problem (22) is not simply a linear matrix inequality, and to the best of our knowledge, it cannot be solved efficiently [4].

Thus far, we have considered convexity over the simplex domain. Analogous results hold for the cube. To generalize Lemma 6 to the cube simply modify the bounds and by defining

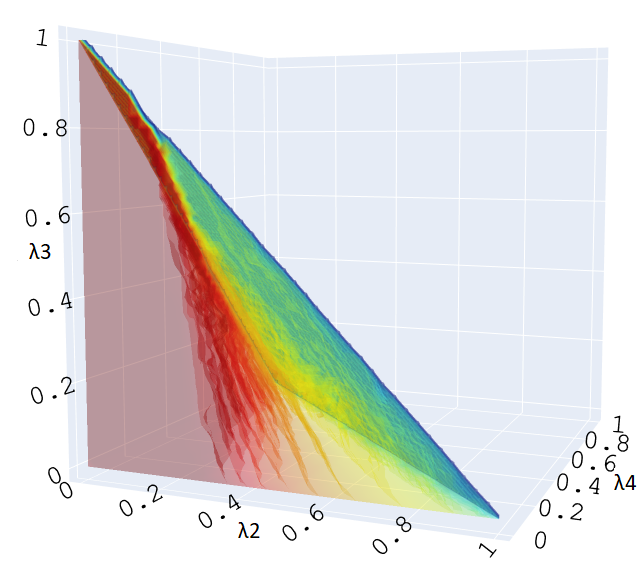

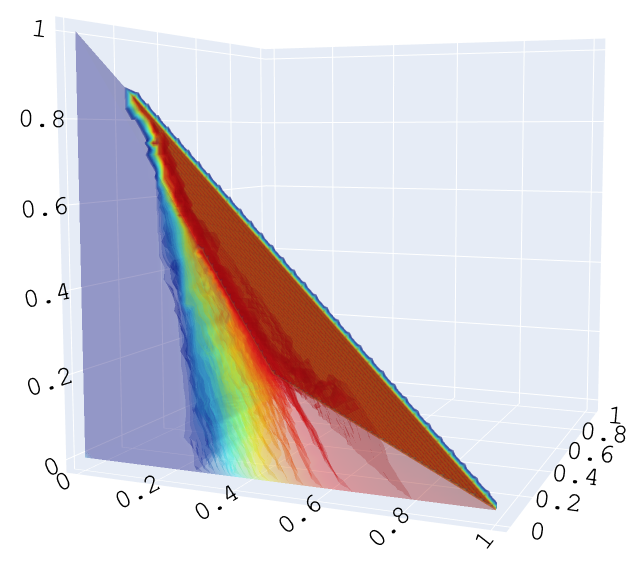

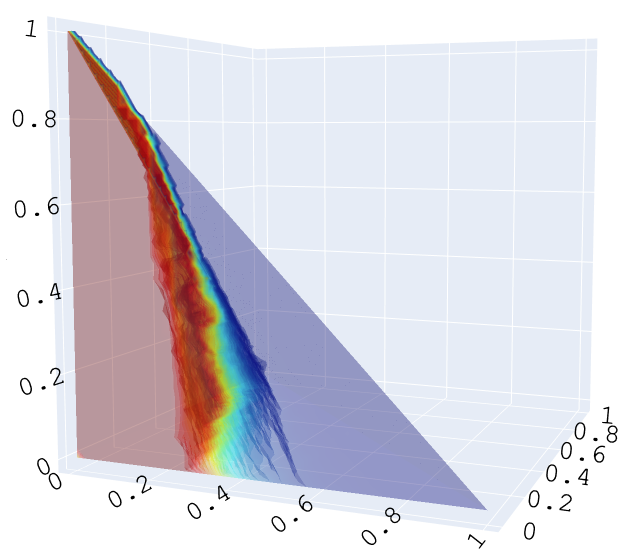

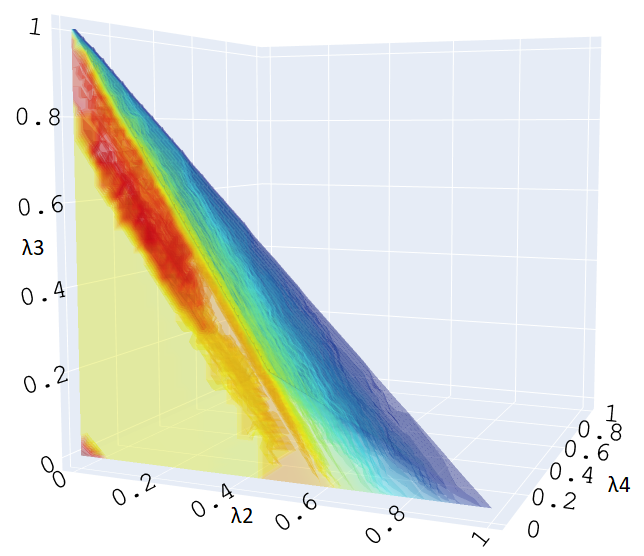

3.1.1 Regions of hyper-parameters for which is convex

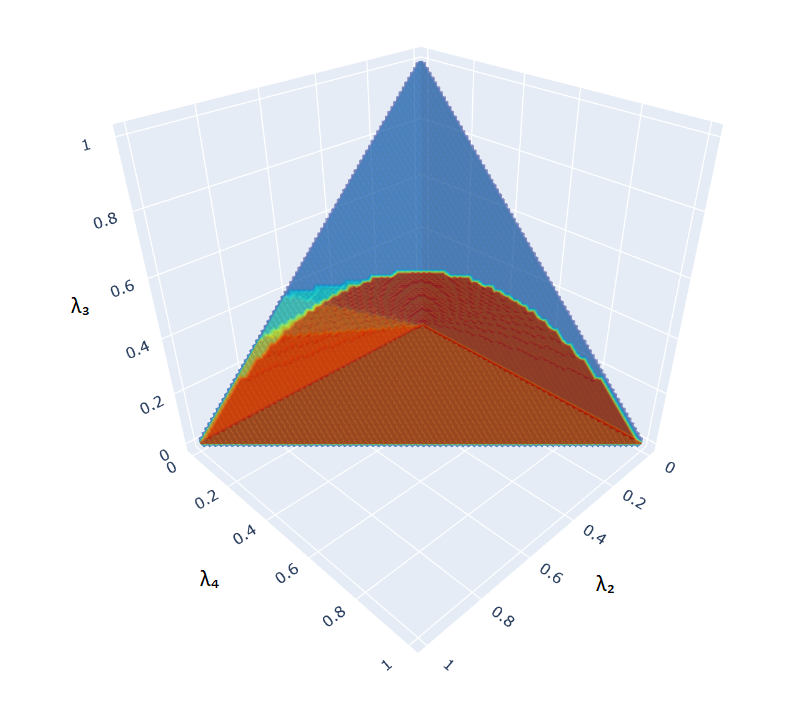

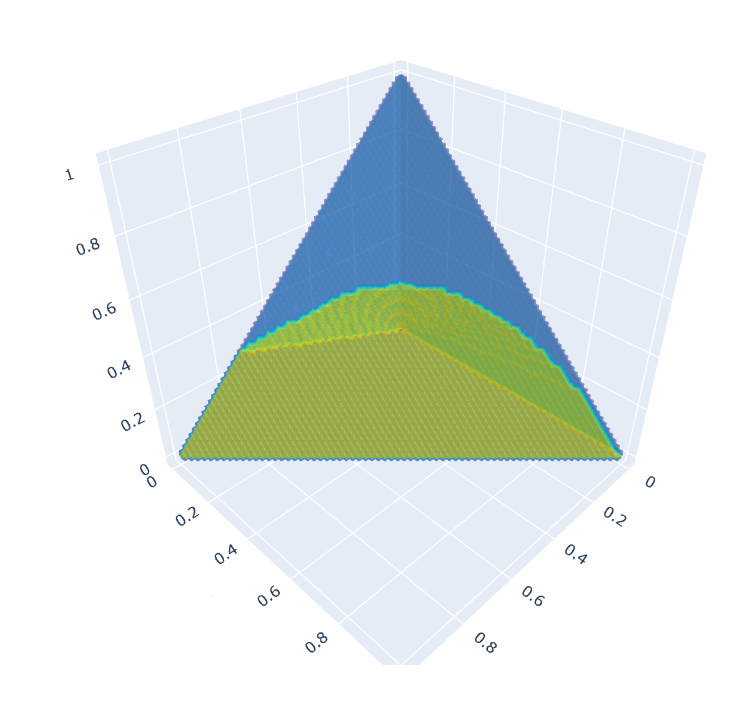

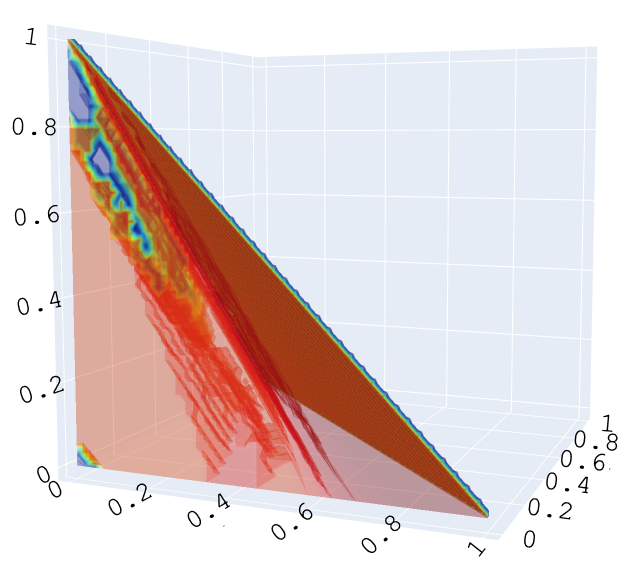

We define the following nested sets of hyper-parameters

where

| (23) |

Via Lemma 6, it now follows that if then is convex over . Similarly if (resp., ) then is convex over the simplex (resp., the cube ). The benefit of eliminating a variable ( in this case) is that the hyper-parameter sets , and can now be plotted, see Fig. 3. Keep in mind that the set is a conservative estimate for the set of all for which is convex over the simplex, i.e.,

Hence, the region shown in Fig. 3 should be thought of as pessimistic, and similarly for . Furthermore, even if is non-convex, one can still optimize (18) and hope that the local optimum attained is sufficiently good.

The function of these sets is as follows. By optimizing for different , we recover local optimizers . If then, by Corollary 8, we know that the optimizer is globally optimal for problem (18). If additionally we know that , then by Lemma 2 we know that is a Pareto optimal point of problem (16). Later in Section 4, we will visualize the quality of solutions by plotting objective values against , for . Hence, the sets , are useful in showing where we certainly have Pareto optimality.

3.2 Scalarized sparse MVSK

Analogous to the above discussion, one can associate a linear scalarization to the sparse MOOP in (17) as follows:

| (24) |

We now show that optimization problems of the form (24) can be decomposed into a collection of several independent sub-problems of the form (18). The motivation for doing this is that the sub-problems could possibly be solved independently using parallelization or other forms of distributed computing.

For any set and vector denote by the lifting of into , defined entrywise by

Similarly, for , let denote the restriction of to . For a function define the restricted function .

Lemma 11.

Let be all the maximal subsets of not containing any set . Then we have

where

| (25) |

Proof.

The above result is reminiscent of Proposition 6 [15]. In [15], the concept of ideal-sparsity was introduced in the context of the generalized moment problem (GMP), when one restricts the support of the involved measure. This GMP with a single measure with restricted support can be shown to be equivalent to another GMP involving several measures, each having smaller support than the measure in the original GMP. In Lemma 11, we show that a polynomial optimization problem with support constraints is equivalent to optimizing over a set of smaller restricted polynomial optimization problems. In both settings, the critical insight is that the restricted support constraint decomposes into a collection of smaller restrictions.

3.2.1 Convexity of the scalarized sparse MVSK

Similar to the dense case in Section 3.1, the objective function in (24) is convex if satisfies any of the conditions (i)-(iv) of Lemma 6. The result of Lemma 6 transfers to the sparse case because on implies that on

| (26) |

Hence Lemma 6 and its consequences continue to hold in the sparse setting. Note that the domain is not convex, so the problem (24) is not convex. However, if denote all the maximal subsets of not containing any set , then for any the sub-problem

does have a convex domain, i.e., . Moreover, on this sub-problem, Lemma 6 can be adapted by using the following bounds

Observe that for all . Furthermore, any that satisfies at least one of the conditions (i)-(iv) of Lemma 6 using the bounds and will necessarily again satisfy one of the conditions using instead now the bounds and , for any . Intuitively one can think of using these new bounds and as relaxing the condition for all to the weaker condition for all with . This mirrors the fact that there are potentially more hyper-parameters for which is convex over for each than there are for which is convex over .

The sparse problem (24) could have combinatorially many sub-problems to solve, but each sub-problem is smaller than the original problem and can be solved independently of the other sub-problems. If we set to be the collection of all sets of size , then there are sub-problems to solve, each involving variables.

4 Numerical experiments

In this section, we apply the theory from the preceding sections to real-world data. We discuss the optimization algorithm FISTA, by Beck and Teboulle [3], that we use to solve the scalarized problem (18), and we motivate its use by listing some of FISTA’s desirable properties. We explain our methodology for acquiring a grid approximation for the Pareto set of MVSK problem (16). Having obtained a set of optimizers of the scalarized problem (18) for different choices of hyper-parameters, we compare and visualize the objective values of the MOOP (16) at said optimizers. We observe that some optimizers give a better overall balance among the four objectives. This procedure is performed for the simplex and cube settings as well as their sparse analogs.

4.1 Optimization algorithm for the scalarized problem

Fast iterative shrinkage-thresholding algorithm (FISTA), also known as fast proximal gradient method, is a well-studied first-order iterative optimization algorithm first devised and analyzed by Beck and Teboulle [3]. Consider the scalar optimization problem (18) and assume that is convex. Then under some mild smoothness assumptions, the details of which we omit to mention here for the sake of brevity, there is the following performance guarantee for the kth iteration of FISTA applied to (18), see Theorem 10.34 [2]:

Here is the Lipschitz constant of , is the initial point, is an optimizer, and is the point obtained from FISTA at the kth iteration. For all our application of FISTA we used iterations.

For more details on FISTA, we refer to Chapter 10 of the monograph by Beck [2]. We now proceed to mention some of the properties of FISTA that make it well suited for our problem.

Like many gradient descent algorithms, FISTA makes use of a projection operator in order to maintain the simplex (resp., cube) constraints. The operator that projects to the simplex defined by

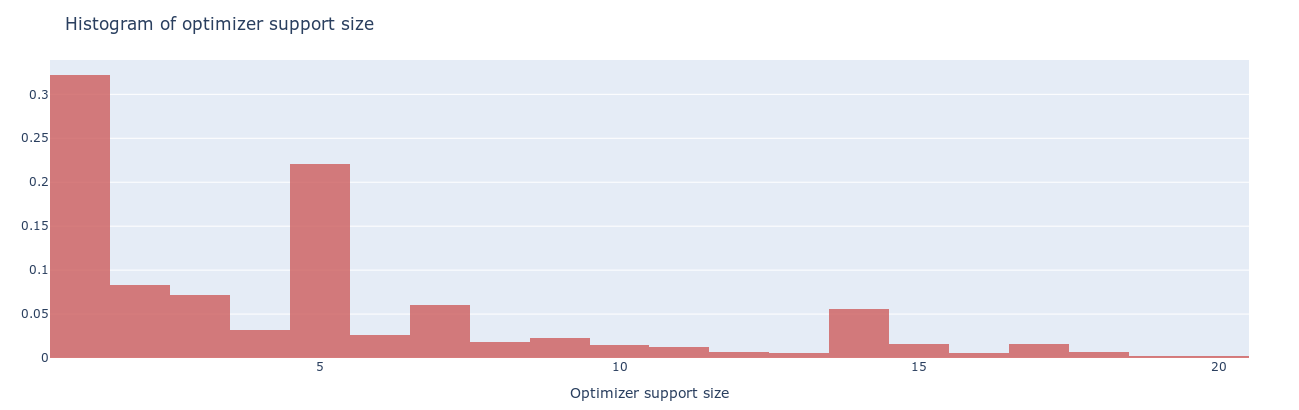

If the nearest unconstrained optimizer lies outside of the simplex, then most gradient steps will leave the domain. Projecting back to the simplex results in a sparse vector, i.e., without full support. The sparsity seems to be due to the fact that projections are often on a face of the simplex. Hence, most optimizers obtained from FISTA will be sparse. We provide a histogram of the supports of optimizers from the set (defined in Section 4.1.2) for our particular problem in Fig. 4. This sparsity does not occur in the case of the cube domain, i.e., the supports of (defined in Section 4.1.2) are all full. One possible reason for this is that the unconstrained optimizer lies within the cube, and, as such, the projection operator does nothing. Note that the cube is full-dimensional in contradistinction to the simplex, which lies in the hyperplane .

FISTA is an iterative algorithm that starts from an initial guess and then incrementally improves a proposed optimizer until a certain number of iterations have been completed. In the convex problem, the algorithm will converge to the global optimum regardless of where one starts, but a closer start does imply faster convergence. Furthermore, if the problem is not convex, and one starts sufficiently close to the global optimizer, then one can be sure that FISTA will converge to the true optimum. An initial guess that is close to the global optimizer is called a warm start. We now propose to use the optimizer from an already solved problem (18), with a fixed , as a warm start for solving (18) with a different hyper-parameter . In other words, fix . If

then take as a warm start for FISTA when solving

| (27) |

Our intuition here is as follows: if is close to , then we expect should be close to an optimizer of (27). Note that this is a heuristic and we provide no proof of the validity of this intuition. The same idea can be applied to computing sparse optimizers via FISTA. We elaborate more on this in the following sub-section.

4.1.1 Optimization algorithm for the sparse scalarized problem

We saw above that the optimizers of problem (18) are sometimes sparse for the simplex setting, but not always. So we propose a simple scheme for finding optimizers with support not exceeding some fixed integer . We do this starting from a set of possibly dense solutions . Let be the optimizer of the (dense) problem (18). If then we are done. So suppose that . Keeping with the notation of Section 3.2 we let and define the set

of all maximal subsets of that do not contain any set . The sparse problem (24) can be rewritten as follows:

| (28) |

For a fixed we can solve the sub-problem

| (29) |

using FISTA with as a warm start, where is assumed to be an optimizer from the dense problem (18) with the same hyper-parameter .

Removing sub-problems based on proximity to the dense optimizer.

In order to not consider all -many sets of , we propose the following two heuristics to remove sets for which the resulting sub-problem (29) could have a poor optimum value. The two heuristics we introduce can be used independently of each other. However, we will use them together in the sequence we introduce them.

The first heuristic consists of discarding all sets that do not satisfy . Doing so yields only sets to optimize over in (28). The second heuristic is to look at the elements of the set

obtained by projecting onto and then lifting the projection to a vector in by padding entries not supported by with zeros, for all appropriate sets . To use the second heuristic independently of the first simply drop the constraint in the definition of . We can then choose to solve problem (29) only over sets for which is close to in the Euclidean norm. For our implementation we take the sets corresponding to the closest to . Though we provide no guarantee that choosing a such that is closest to would result in an optimum value of problem (29) being any better than another choice of , we still find that this a helpful heuristic for removing poor choices of .

4.1.2 The set of obtained optimizers

Whether is convex or not, we can apply FISTA to obtain at least a local optimizer for problem (18). Construct the following sets of optimizers, obtained by applying FISTA to various scalarizations:

| (30) |

Here, denotes the local minimizers obtained via the algorithm FISTA, not to be confused with the true (unknown) global minimizers. In Section 4.4.1 we will visualize the values of the objectives , and for (resp., ) using colors. Similarly, we construct the sets of sparse FISTA local optimizers

obtained by following the procedure described in Section 4.1.1. As mentioned before, projecting onto the simplex often produces a sparse vector. Hence, it makes sense to use as a starting point for computing , as many of the vectors of may already be sparse enough. Regardless of whether the elements of (resp., ) are sparse we can use the ideas of Section 4.1.1 to prune computations and generate warm starts for the problems associated with (resp., ).

4.2 Defining objective functions from empirical data

For the sake of generality, we have worked with a vector-valued random variable (resp., ) taking values in . Practically, the data will arise from a table of results, taking the form of an matrix , where is the number of outcomes observed over time. We introduce new notation for the empirical data and the subsequent derived quantities. The entry (resp., ) is interpreted as the empirical (resp., centralized) relative returns of asset at time . In this context, the expectation is taken over the outcomes. The mean becomes the empirical mean, i.e.,

Hence, the empirical centralized relative returns is defined for each and by

Similar to the mean, the formulation of the other empirical moments is as follows:

| (31) |

Observe that we use the unbiased estimator of the variance in (31); for a general reference on statistical estimators, we refer to [30].

The objective functions , , , and defined in (13) and (15) can henceforth be redefined in terms of the above , , , or .

Using , the bounds and in Lemma 6 now become

For the cube the bounds are and . The sparse analogs , , , and are defined, mutatis mutandis, in the same manner. The bounds we gave in Fig. 3 are also used for all computation we show. We only compute and use the dense bounds (, , , and ), even for the sparse settings.

In the next section we sub-sample the sets , , , and , described in the preceding section.

Our empirical data will be a selection of stocks from the well-known Standard and Poor’s 500 (S&P500) stock market index, see [10]. We will consider stocks, each measured in increments of a day over a timespan of days starting in January 1990. We have chosen this dataset because it is well known and publicly available. However, everything we describe in this paper could also be applied to any other time series data of asset prices. For the reader’s convenience we list some papers [23, 1] that investigate the MVSK model on markets different from the S&P500. Using we can generate , , , and as described above. From here we can define problem (18) and its sparse analog (24). Solving these problems, using the procedure described in Section 4.1, we obtain elements from the sets , , , and .

4.3 A grid approximation of the Pareto set

Recall that the ultimate goal is to obtain Pareto optimizers of the MVSK problem (16). Via Lemma 2, solving the scalarization (18) for gives a Pareto optimizer of (16). However, we can still recover an optimizer from solving the scalarization (18) for , we simply have no guarantee of them being Pareto optimal in (16). Because contains uncountably many elements we resort to sub-sampling with a uniform mesh. Fix , and consider the following sets:

that are clearly in bijection. For our computations we take , resulting in choices of hyper-parameter to consider. For each , we solve the associated scalarization (18) using FISTA to obtain a set of local optimizers , denoted by

Observe that the set is not necessarily contained in the Pareto front, but the following subset is:

Here we use the claims from Section 3.1 and Lemma 2 that if and then is a Pareto optimizer of problem (16). The reason we consider the bigger set is that we get a more complete picture, see the figures of Section 4.4. Although some points of are not guaranteed to be a Pareto optimizer of (16), they are nonetheless quite comparable to the points that are Pareto optimal for (16). We illustrate this claim with visualization in the subsequent sub-sections of Section 4.4.

In order to compare points , we rank them in terms of their values for the objective functions , , , and in (16). For each we compute the values , , , and . For the sake of clarity, since there is a scale difference between the different functions, we linearly rescale the values to be in the interval . Formally, for each define

to be the set of linearly scaled values for , where

| (32) |

with

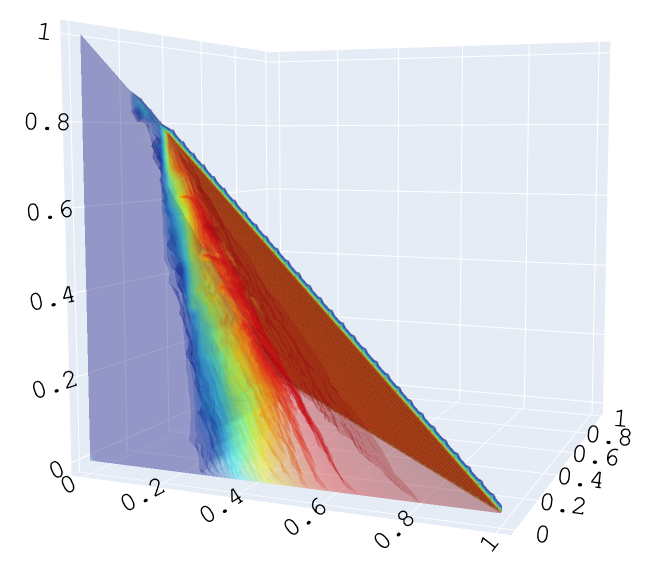

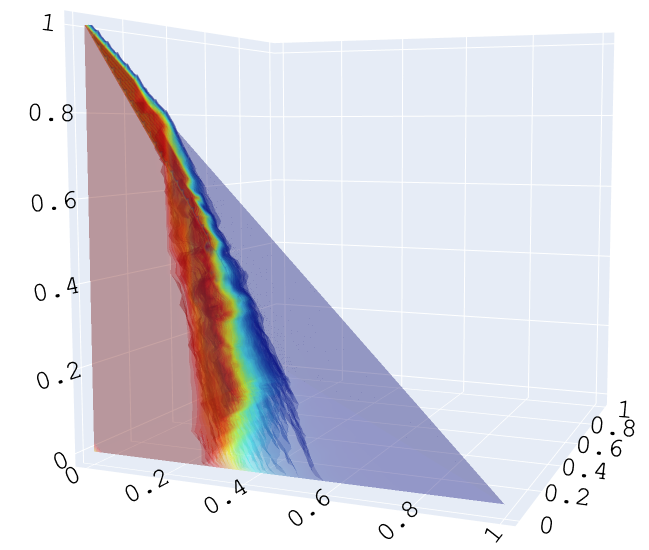

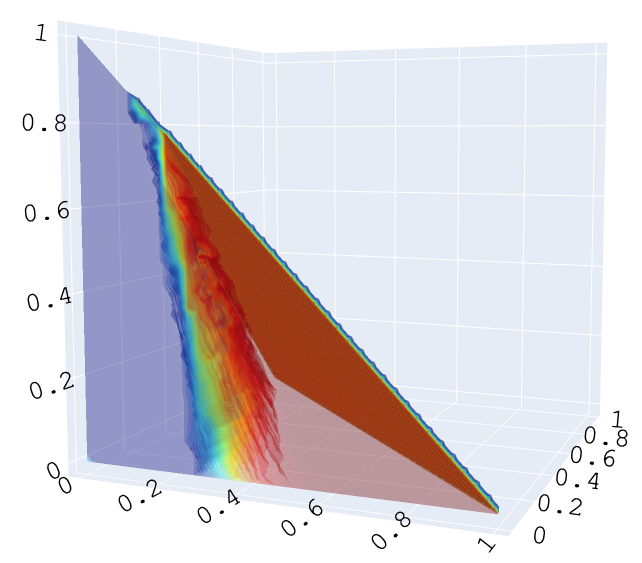

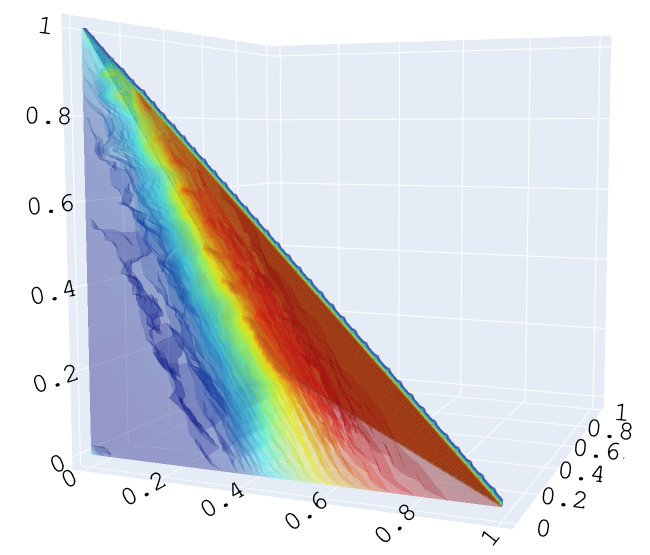

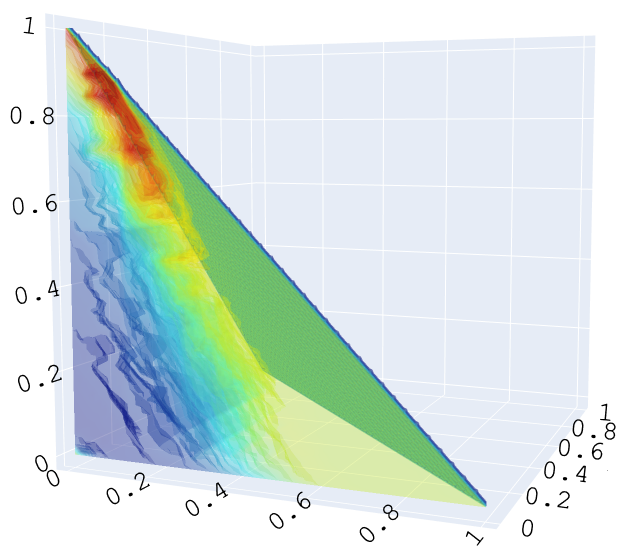

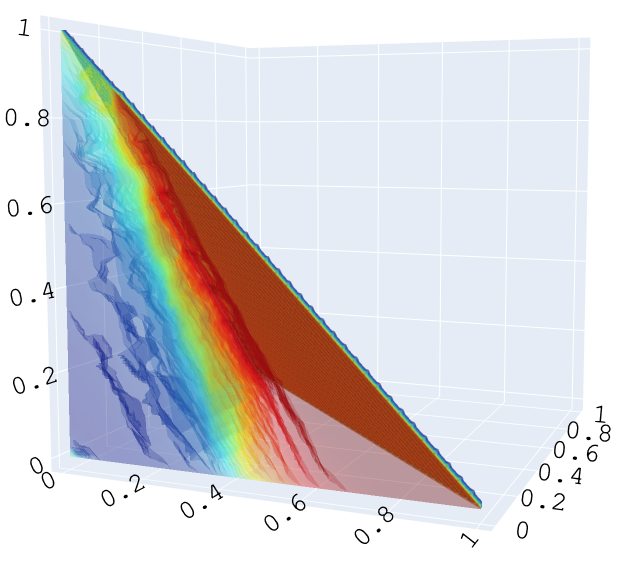

Hence, for any , the set is contained in the unit interval , with “less desirable” values close to zero and “more desirable” values close to one. Note that the scaling considers the fact that we want to maximize and , and to minimize and . Hence, the set gives us a way to compare the performance of each portfolio with respect to the objective function , for all . For each , we plot (in color) against (in ), see Fig. 5.

In order to aggregate the quality of an optimizer over all of the objectives , , , and , we propose looking at the value

The intuition behind this value is that if has a value close to four, then it does well among many of the objectives and is hence a superior choice to another solution for which for some but . We refer to the following set

where , as the set of portfolios with -superior trade-off, and we define the set of associated scores

We plot in color against in Fig. 6. Our plots should not be compared to figures as those in [20] where three of four objective are plotted against each other with two independent and the third dependent. We give a separate plot for each objective and we scale for comprehensibility.

Handling the cube and sparse cases.

Above, we have described the process for the simplex (), but the treatment is analogous for the cube domain () and sparse domains (, ) and (, ). Notation-wise, the sets , , and are all defined analogously to the simplex case, now using the domain instead of . Similarly the sparse simplex sets are denoted by , , and , where is an upper bound on the support size of the elements as described in Section 4.1.1. The sparse cube sets, denoted , , and , are defined, mutatis mutandis, in the same manner.

4.4 Numerical results

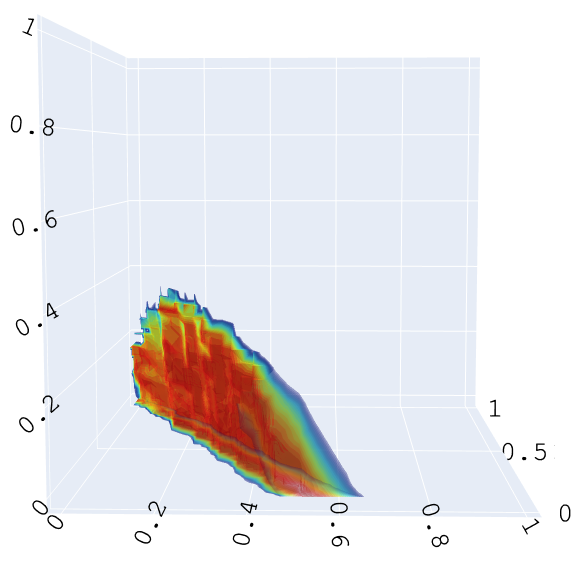

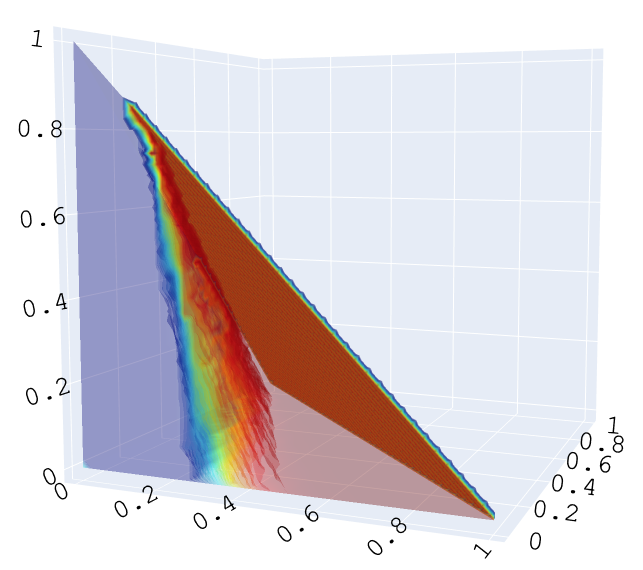

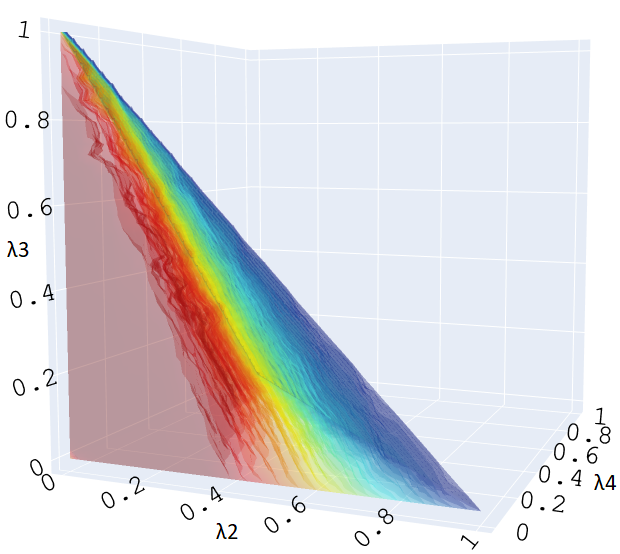

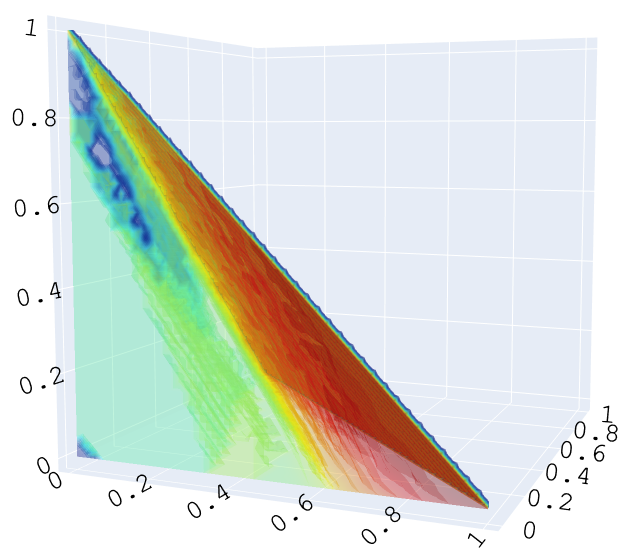

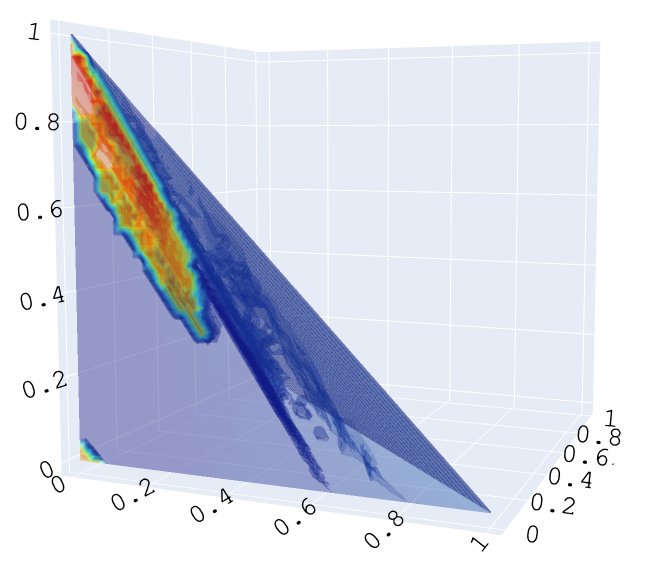

This final subsection is the culmination of the preceding subsections. For the S&P500 data considered at the end of Section 4.2 we compute , , , and . For each we plot (in color) against the hyper-parameter set . Doing so, we observe how each portfolio makes a trade-off between the objectives , , , and . Which of the objectives are favoured by is influenced by the choice of . For example, for the portfolios tend to have values close to one, see Fig. 5a. Observations like these are useful to investors who can now visually navigate the in Fig. 5 to find a portfolio that matches their risk preferences.

To see which correspond to portfolios with a good balance of all four objectives we plot (in color) against (resp., ) in Fig. 6. Note that the hyper-parameters for which are not displayed so as not to clutter the plot.

Above, we explained the process for the (dense) simplex setting, but the same treatment applies to the cube and sparse settings, resulting in analogous figures and similar observations.

4.4.1 Numerical results in the simplex setting:

| [0.154, 0.256, 0.077, 0.513 ] | 0.623 | 0.81 | 0.058 | 0.978 | 5 |

| [0.026, 0.077, 0.256, 0.641 ] | 0.601 | 0.825 | 0.05 | 0.98 | 10 |

| [0.231, 0.41 , 0.308, 0.051 ] | 0.581 | 0.854 | 0.034 | 0.989 | 5 |

| [0.462, 0.513, 0.026, 0.0 ] | 0.691 | 0.724 | 0.118 | 0.942 | 5 |

| [0.051, 0.051, 0.205, 0.692 ] | 0.677 | 0.741 | 0.104 | 0.95 | 5 |

| [0.179, 0.359, 0.308, 0.154 ] | 0.562 | 0.872 | 0.026 | 0.992 | 5 |

| [0.462, 0.41 , 0.128, 0.0 ] | 0.774 | 0.586 | 0.241 | 0.85 | 3 |

| [0.282, 0.333, 0.385, 0.0 ] | 0.752 | 0.625 | 0.203 | 0.881 | 5 |

| [0.154, 0.231, 0.487, 0.128 ] | 0.676 | 0.742 | 0.104 | 0.95 | 5 |

| [0.256, 0.256, 0.077, 0.41 ] | 0.715 | 0.686 | 0.148 | 0.922 | 5 |

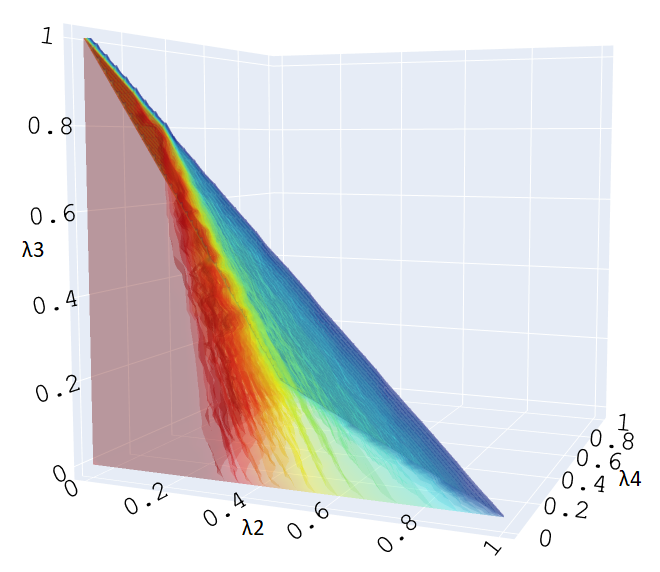

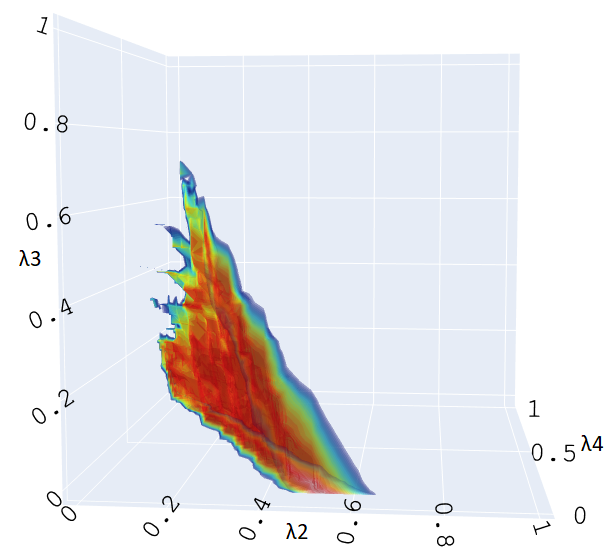

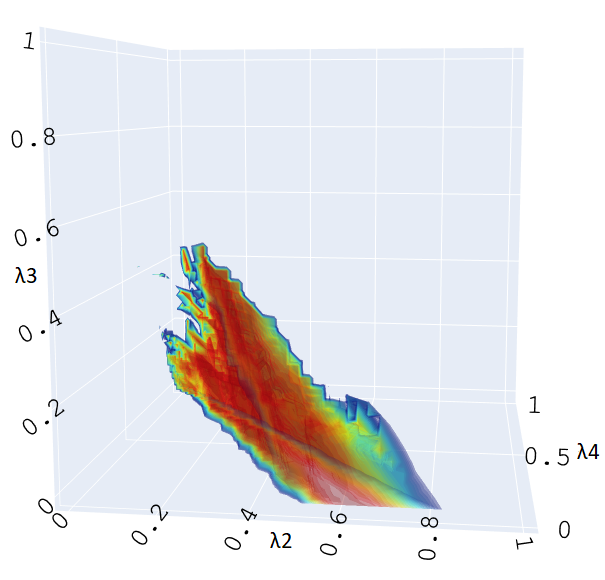

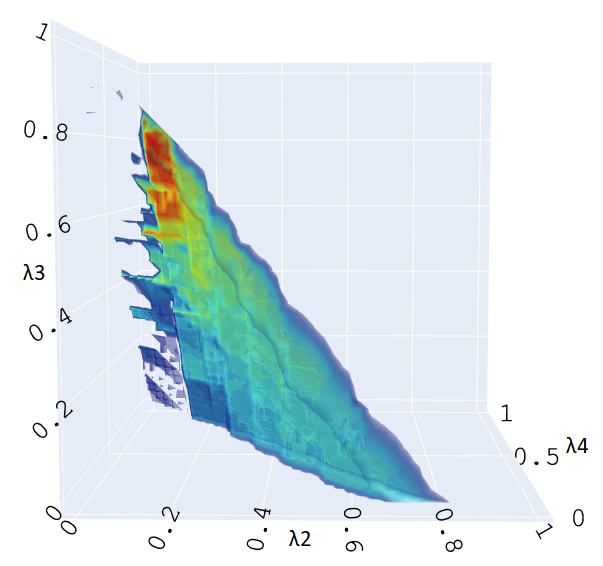

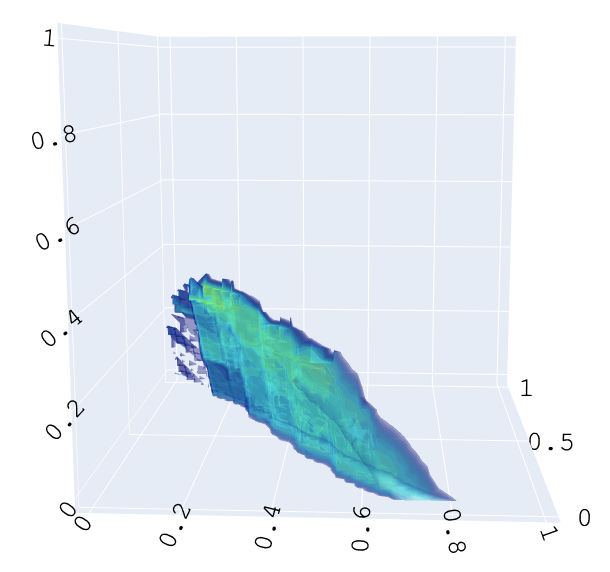

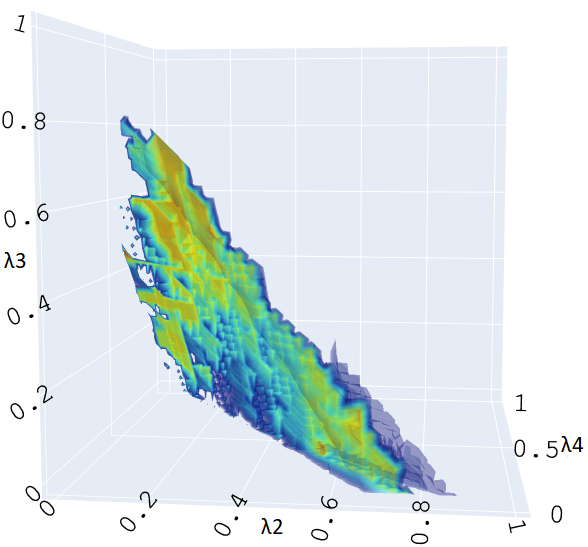

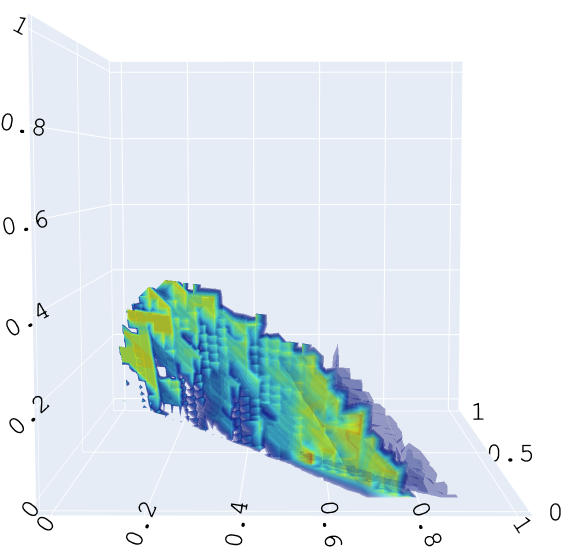

In Fig. 5, regions where the objectives and perform well (are red) overlap heavily, see Fig. 5a and Fig. 5c. Furthermore, these regions overlap with the regions where the objectives and do poorly (are blue), namely the rear slice of the simplex where either or is small, see Fig. 5b and Fig. 5d. The central wedge, such that , where the objectives seem to balance out is shown in Fig. 6a along with the same wedge restricted to , shown in Fig. 6b.

Recall from definition (23) that is a set of hyper-parameters for which is convex over the simplex . Further recall that FISTA converges to a global minimizer when applied to a convex problem. With this in mind one would expect the quality of optimizers produced by FISTA to decline as leaves and (possibly) ceases to be convex. However, this is not apparent from our plots. Observe how there does not seem to be a change in color in the plots of Figs. 5 and 6 as the hyper-parameters move out of the region . This hints at the possibility that the local optima obtained by FISTA for hyper-parameters in are not much worse than the global optima.

Lastly, observe how the set

of hyper-parameters corresponding to solutions of superior trade-off overlap with the respective sets and , see Fig. 3c and Fig. 6b. In fact, the approximate volumes of these two sets and their intersection relative to are as follows:

Hence, by virtue of Lemma 2 and Corollary 8, we have that approximately of the optimizers with superior trade-off in are guaranteed to be Pareto optimizers of the MVSK problem (16).

For concreteness we show in Table 1 the numerical values for ten randomly selected hyper-parameters . We make the following observations. First, the skewness, i.e., , seems to be the weakest performing objective relative to the others. Second, variance and kurtosis, i.e., and , seem to be positively correlated. Third, the associated portfolios are all sparse with at least half of their entries zero. Eight of the ten portfolios in Table 1 have support size , this corroborates the data in the histogram shown in Fig. 4.

In the literature computational results are often represented in tabular from as we did in Table 1, see for example[17, 14]. Presenting results in this way for a large selection of hyper-parameters soon becomes cumbersome, especially in our case where we have (recall Section 4.3). Moreover the overall patterns are often obscured by the detail of each specific entry. In contradistinction, by representing the results as we did in Fig. 5 and Fig. 6 we see larger trends across the various choices of hyper-parameters . Hence, via the grid sampling approach of Section 4.3 and the visualizations of this section we believe we get a better overall understanding of the relationship between , , and the objective values than by simply looking at a few specific values of .

We now proceed with the other settings (sparse simplex, cube, and sparse cube), which follow in a similar manner. Because the subsequent sub-sections follow the same format as this one, we omit describing the figures and focus instead on the differences and new observations.

4.4.2 Numerical results in the sparse simplex setting: ,

The similarity between Fig. 7 and its dense analog Fig. 5 is because at least half of the portfolios are from . Recall the histogram in Fig. 4, in which more than half of the points are shown to have support size five or less. Following the procedure of Section 4.1.1, these portfolios are taken as they are when constructing .

Between Fig. 8 and Fig. 6, there is again much similarity. The reader may wonder why the range of values in the sparse setting Fig. 8 (from 2.57 to 2.59) exceeds that of dense setting Fig. 6 (from 2.455 to 2.475). There is no contradiction here because the scaling (32) is different in each setting (simplex, cube, sparse, and dense). Hence, the values and are incomparable, similarly for the forthcoming cube setting.

4.4.3 Numerical results in the cube setting:

The cube setting differs significantly from the simplex setting. Portfolios are now in and have full support (at least for all examples we have computed). Except for skewness, Fig. 9c, the figures of Fig. 9 follow roughly the same pattern as in Figs. 5 and 7. In the cube setting, portfolios now require a large to attain good values for the skewness objective, see Fig. 9c.

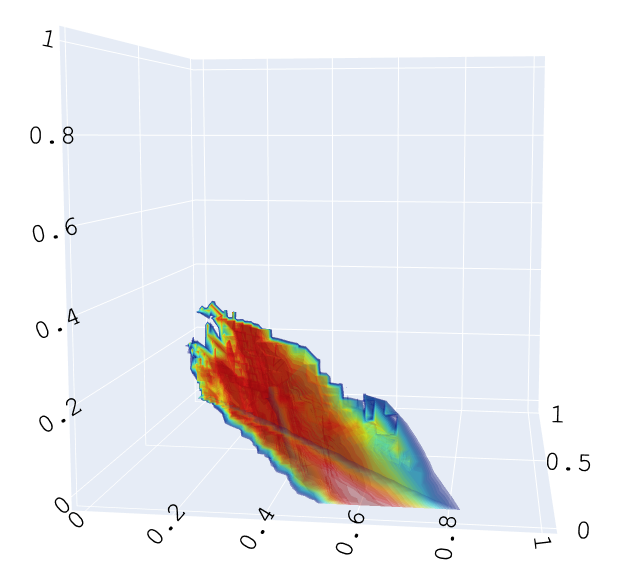

We observe that the portfolios of superior trade-off are more scarce in the cube setting than in the simplex counterpart. Hence, in Fig. 10, we now take because the set (of hyper-parameters corresponding to solutions of superior trade-off) gives a fuller and more informative plot than . Secondly, we observe the same “wedge” of superior portfolios we saw in Figs. 6 and 8. Lastly, the portfolios that do the best in Fig. 10 have , with the concentration lying outside of .

4.4.4 Numerical results in the sparse cube setting: ,

The results for the sparse cube setting differ vastly from the dense cube setting. The difference in results is primarily due to the portfolios having full support and thus differing greatly from the portfolios . In particular, we see concentrations forming in the same places as in Fig. 9c, namely the upper tip of where is large. We also see a tinny concentration near . Despite the changes we still have that the odd objectives (mean and skewness) perform better in regions where the even objectives (variance and kurtosis) do poorly and vice versa, see Fig. 11. Surprisingly, in Fig. 12 is again the same “wedge”-like shape we have seen in Figs. 6, 8 and 10. There are now hardly any red regions, indicating that very few points reach the higher value range.

5 Conclusion

In this paper, we considered the multi-objective optimization problem MVSK that models the portfolio selection problem in finance.

We considered two settings.

The first was the simplex (), which represents portfolios that do not allow short selling and leverage.

The second setting was the cube (), where we allow leverage and short selling.

Refer to Section 1.3 to refresh the notions of leverage and short selling.

Furthermore, we introduced a sparse variant of MVSK, where one can set an upper bound on the support size of portfolios.

In order to (partially) recover the Pareto front of MVSK (for the different settings), we proposed the following three-step process. First, we considered the linear scalarization of MVSK and identified a set of hyper-parameters for which the resulting scalar-objective problems are convex. Second, we used the fast iterative shrinkage-thresholding algorithm (FISTA) (which converges to a global optimizer when applied to convex problems) to recover optimizers of the scalarized problems. Third, we used the fact that the (global) optimizers of neat scalarizations are Pareto optimizers of the original multi-objective problem, hence, showing that many of the optimizers computed by FISTA are Pareto optimal for MVSK.

Additionally, we demonstrate that gradient-descent algorithms like FISTA have three desirable properties in this setting: the ability to benefit from warm starts, the tendency to generate sparse solutions (due to the projection step, in the case of the simplex), and guaranteed convergence to the global optimizer (for convex problems).

We hope the visualizations accompanying our computations will further intuition and understanding within this exciting field.

In the introduction, we hinted at extending the model to include even higher moments, i.e., beyond kurtosis.

The formulation of the objective functions in (14) is well-defined for any integer .

Hence, one can define objectives with in addition to those already present in (16) and thereby extend the model. With an extended model, one can again scalarize linearly, now using more hyper-parameters than before. Again one can characterize the Hessian of this new scalarization and possibly recover results similar to Lemmas 6 and 8.

However, one must first justify adding these higher moments, considering the additional computational and complexity costs involved.

There is not much motivation in the literature for this further extension.

Some authors even advocate against relying on correlation-based risk measures [29].

Alternative to the linear scalarization (8) some authors propose the Minkowski distance scalarization (6). The Minkowski distance formulation lends itself to a signomial optimization interpretation [7]. Indeed, the scalarization (6) applied to the MVSK problem with simplex domain has the following form:

where with given in (15) and (13) for each . Under the change of variable , the above problem can be written as a signomial optimization program

Problems of this type have been studied before and have mature methods to solve them, see [25]. Approaching the MVSK problem from the signomial programming direction opens a new and unexplored line of inquiry into the MVSK problem. As before, one can try to characterize the convexity of such a scalarization in the hopes of getting similar results to Lemma 6, but we do not attempt it here. The appeal of solving these scalarizations is that they are also neat for and could reveal Pareto points that the linear scalarization approach cannot. However, the benefits of the Minkowski distance scalarization must be weighed against the fact that it is much harder to interpret than linear scalarization. Moreover, one has to compute the independent optima for , which can already be challenging in the case of .

References

- [1] B. Aracıoğlu, F. Demircan Keskin, and H. Uçak. Mean–variance–skewness–kurtosis approach to portfolio optimization: An application in Istanbul stock exchange. Ege Academic Review, 11:9–17, 2011.

- [2] A. Beck. First-Order Methods in Optimization. Society for Industrial and Applied Mathematics, Philadelphia, PA, 2017.

- [3] A. Beck and M. Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- [4] A. Ben-Tal and A. Nemirovski. Lectures on Modern Convex Optimization. Society for Industrial and Applied Mathematics, Philadelphia, PA, 2001.

- [5] M. J. Best. Portfolio Optimization. Chapman and Hall, New York, first edition, 2010.

- [6] S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, Cambridge, 2004.

- [7] V. Chandrasekaran and P. Shah. Relative entropy relaxations for signomial optimization. SIAM Journal on Optimization, 26(2):1147–1173, 2016.

- [8] L. T. DeCarlo. On the meaning and use of kurtosis. Psychological Methods, 2:292–307, 1997.

- [9] D. P. Doane and L. E. Seward. Measuring Skewness: A Forgotten Statistic? Journal of Statistics Education, 19(2):1–18, 2011.

- [10] Britannica, T. Editors of Encyclopaedia. S&P 500. Encyclopedia Britannica, 2023. https://www.britannica.com/topic/SandP-500

- [11] M. Ehrgott. Multicriteria Optimization. Springer Berlin, Heidelberg, second edition, 2005.

- [12] G. Gonçalves, P. Wanke, and Y. Tan. A higher order portfolio optimization model incorporating information entropy. Intelligent Systems with Applications, 15:200101, 2022.

- [13] P.-M. Kleniati, P. Parpas, and B. Rustem. Partitioning procedure for polynomial optimization. Journal of Global Optimization, 48(4):549–567, 2010.

- [14] P.-M. Kleniati and B. Rustem. Portfolio decisions with higher order moments. Working Papers 021, COMISEF, 2009. https://ideas.repec.org/p/com/wpaper/021.html

- [15] M. Korda, M. Laurent, V. Magron, and A. Steenkamp. Exploiting ideal-sparsity in the generalized moment problem with application to matrix factorization ranks, arXiv:2209.09573, 2022.

- [16] A. Kraus and R. H. Litzenberger. Skewness preference and the valuation of risk assets. The Journal of Finance, 31(4):1085–1100, 1976.

- [17] K. Lai, L. Yu, and S. Wang. Mean-variance-skewness-kurtosis-based portfolio optimization. First International Multi-Symposiums on Computer and Computational Sciences (IMSCCS’06), 2:292–297, 2006.

- [18] J. B. Lasserre. Moments, Positive Polynomials and Their Applications. Imperial College Press, 2009.

- [19] X. Li and P. Zhang. High order portfolio optimization problem with transaction costs. Modern Economy, 10(6):1507–1525, 2019.

- [20] D. Maringer and P. Parpas. Global optimization of higher order moments in portfolio selection. Journal of Global Optimization, 43(2):219–230, 2009.

- [21] H. Markowitz. Portfolio Selection. The Journal of Finance, 7(1):77–91, 1952.

- [22] R. W. Melicher and E. Norton. Introduction to Finance: Markets, Investments, and Financial Management, John Wiley & Sons, Inc., Hoboken, NJ, sixteenth edition, 2016.

- [23] M. Mhiri and J.-L. Prigent. International portfolio optimization with higher moments. International journal of economics and finance, 2:157–169, 2010.

- [24] T. S. Motzkin and E. G. Straus. Maxima for graphs and a new proof of a theorem of Turán. Canadian Journal of Mathematics, 17:533–540, 1965.

- [25] R. Murray, V. Chandrasekaran, and A. Wierman. Signomial and polynomial optimization via relative entropy and partial dualization. Mathematical Programming Computation, 13(2):257–295, 2021.

- [26] P. A. Samuelson. The Fundamental Approximation Theorem of Portfolio Analysis in terms of Means, Variances and Higher Moments. In W. Ziemba and R. Vickson, editors, Stochastic Optimization Models in Finance, pages 215–220. Academic Press, 1975.

- [27] P. Sheng-zhi and W. Fu-sheng. Semidefinite programming relaxation for portfolio selection with higher order moments. 2011 International Conference on Management Science & Engineering 18th Annual Conference Proceedings, pages 99–104, 2011.

- [28] J. C. Singleton and J. Wingender. Skewness persistence in common stock returns. The Journal of Financial and Quantitative Analysis, 21(3):335–341, 1986.

- [29] N. Taleb. Statistical Consequences of Fat Tails: Real World Preasymptotics, Epistemology, and Applications. STEM Academic Press, 2020.

- [30] D. Wackerly, W. Mendenhall, and R. Scheaffer. Mathematical Statistics with Applications. Cengage Learning, 2014.

- [31] R. Zhou and D. P. Palomar. Solving high-order portfolios via successive convex approximation algorithms. IEEE Transactions on Signal Processing, 69:892–904, 2021.