A Field Guide for Pacing Budget and ROS Constraints

Abstract

Budget pacing is a popular service that has been offered by major internet advertising platforms since their inception. Budget pacing systems seek to optimize advertiser returns subject to budget constraints through smooth spending of advertiser budgets. In the past few years, autobidding products that provide real-time bidding as a service to advertisers have seen a prominent rise in adoption. A popular autobidding stategy is value maximization subject to return-on-spend (ROS) constraints. For historical or business reasons, the systems that govern these two services, namely budget pacing and ROS pacing, are not necessarily always a single unified and coordinated entity that optimizes a global objective subject to both constraints. The purpose of this work is to theoretically and empirically compare algorithms with different degrees of coordination between these two pacing systems.

In particular, we compare (a) a fully-decoupled sequential algorithm that first constructs the advertiser’s ROS-pacing bid and then lowers that bid for budget pacing; (b) a minimally-coupled min-pacing algorithm that runs these two services independently, obtains the bid multipliers from both of them and applies the minimum of the two multipliers as the effective multiplier; and (c) a fully-coupled dual-based algorithm that optimally combines the dual variables from both the systems. Our main contribution is to theoretically analyze the min-pacing algorithm and show that it attains similar guarantees to the fully-coupled canonical dual-based algorithm. On the other hand, we show that the sequential algorithm, even though appealing by virtue of being fully decoupled, could badly violate the constraints. We validate our theoretical findings empirically by showing that the min-pacing algorithm performs almost as well as the canonical dual-based algorithm on a semi-synthetic dataset that was generated from a large online advertising platform’s auction data.

1 Introduction

Internet advertisers purchase advertising opportunities by bidding in real-time auctions, and, to control their expenditures, it is common for advertisers to set budgets for their campaigns [32, 23, 50]. Budget pacing is a popular service offered by most advertising platforms that allows advertisers to specify their budgets and then optimizes advertiser bids in real-time to maximize advertisers’ return subject to the spend being at most the budget. In the past few years, thanks to the increasing availability of ROS-related metrics, and the vastly improved conversion prediction models, autobidding products have seen a prominent rise in adoption [22, 31]. These are tools that provide value-optimizing real-time bidding subject to return-on-spend (ROS) constraints (on top of the existing budget constraints) as a service to advertisers. Autobidding takes as input high-level advertiser goals like the target cost per conversion or acquisition of an advertiser and places real-time bids on a per-query basis to optimize advertiser returns.

The algorithms that govern budget and ROS pacing, namely value-optimization subject to budget and ROS constraints, are not necessarily always a unified entity that optimizes a global objective. These services are often managed by different business units within the same organization or by different organizations altogether (many third-party demand-side platforms offer autobidding services), which results in different algorithms independently choosing/modifying advertisers’ bids. This is not surprising in light of the meaningful gap between the times at which these products gained traction, with budget pacing systems having been standard and popular much earlier. As a result, even if the objectives of both services are aligned, the presence of budget and ROS constraints can introduce inefficiencies in the bidding process when the systems are decoupled. How do the fully decoupled and fully coupled optimal pacing services compare? Is there a way to operate the pacing service that obtains the best of both worlds: i.e., (a) maintain the theoretical guarantees of the fully coupled optimal pacing service, while (b) still being only minimally coupled? Our contribution in this work is to design and analyze an algorithm that approaches the best of both worlds. We establish this fact both theoretically and empirically.

1.1 Pacing Services

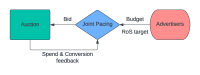

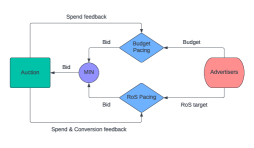

Pacing services are online algorithms that adaptivelty adjust advertisers’ bids based on auction feedback to maximize certain objectives while satisfying different constraint. Nowadays, a popular paradigm in internet advertising markets is that of value maximization [22, 31]. Unlike the usual quasilinear utility model, where the bidder seeks to maximize the difference between their value and payment, the bidder’s stated objective in autobidding/budgeting products is to maximize their overall value (e.g., the number of conversions or conversion value) while respecting their budget and ROS constraints. For example, a bidder could ask to maximize the total number of conversions they get, subject to spending at most and not paying more than per conversion. Figure Fig. 1(a) illustrates a joint optimization pacing service, which we also refer to as a dual-optimal pacing service, which takes as input the advertiser’s budget and ROS target, and then automatically bids on behalf of the advertiser in the platform’s auction. Importantly, the pacing services maintain a feedback loop that monitors the real-time spend and conversions from the auction and uses this information to adjust bids.

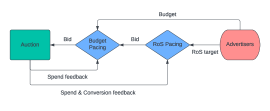

As we discussed, in many cases, the budget and pacing services maintain separate feedback loops. For historical reasons, budget pacing services are offered by platforms themselves, and ROS pacing services are built on top of them (they are either offered by the same advertising platform or third parties). In Figure Fig. 1(b) we illustrate a typical sequential pacing service in which the ROS pacing services feeds bids to the budget pacing service, which, in turn, bids in the platform’s auction. Each service consumes the spend and conversion feedback from the auction to adjust bids dynamically. The benefit of the sequential optimization architecture is its decoupled nature, i.e., it could operate separate modules for budget pacing and ROS pacing.

We also consider a third minimally coupled architecture (Figure Fig. 1(c)), which we call the min pacing service. Rather than organizing the pacing services sequentially, they are organized in parallel. For each auction, the bid is obtained by taking the minimum of the bids generated by the two systems. While more generally one can think about other reduction operations of the two pacing systems’ bids, as we show in this work, the min pacing already performs quite well and approaches the performance of the joint dual-optimal pacing service while still being only minimally coupled.

1.2 Our Results

We compare all three algorithms described above, both theoretically and empirically. We next overview the algorithmic implementations of the pacing services, the empirical evaluation, and our theoretical analysis. Our main contribution is a theoretical analysis of the min-pacing algorithm and shows that it obtains the best of both worlds, i.e., its performance approaches that of the joint dual-optimal pacing service, while still being essentially decoupled much like the sequential pacing architecture. On the other hand, we show that the sequential architecture itself is a very poor choice: it either violates constraints by or has a regret of , when there is a finite horizon of repeated auctions.

Algorithmic implementation.

In this work, we consider uniform bidding policies (which were first proposed and analyzed in [25]) that multiplicatively scale advertisers’ values, which are usually generated using advanced machine learning prediction algorithms [47, 34, 58, 37, 43]. Uniform bidding is appealing for its simplicity, can be shown to be optimal in many settings, and is extensively used in practice [1]. The bid multiplier of the uniform bidding policy is adjusted in real-time using a feedback loop. While many choices are possible for the feedback loop, in this work we consider Lagrangian dual algorithms, which are the work-horse algorithms of budget pacing [16]. At a high level, these algorithms introduce a dual variable for each constraint and then adjust these dual variables dynamically using a first-order algorithm. The final bid multiplier is calculated using these dual variables. Dual-based algorithms have strong performance guarantees and have been shown to subsume PID controllers—one of the most popular feedback controllers used in practice [51, 57, 49, 54, 55, 15]. Therefore, we believe the algorithms studied in this paper are representative of those used by pacing services in practice. We provide more details on the concrete algorithmic implementation in Section Section 2.

Theoretical evaluation.

We evaluate the three algorithms along two dimensions: ROS constraint error, and conversion value. Budget constraints are hard in practice, i.e., pacing algorithms can no longer participate in auctions when budgets are exhausted. In contrast, ROS constraints are often soft: while small violations are permitted, large violations are undesirable. Finally, the conversion value garnered before the budget runs out should be as large as possible. We benchmark algorithms by looking at their regret relative to the conversion value of an offline optimum pacing strategy satisfying budget and ROS constraints. Our results are summarized in Table Table 1.

| ROS Violation | Regret | |

|---|---|---|

| Dual-Optimal | ||

| Sequential | ||

| Min |

Technical contribution.

Our evaluation is performed in a statistical environment under uncertainty. In other words, we assume that values and competing bids are drawn independently from a distribution that is unknown to the algorithms. We consider a finite horizon with repeated auctions in which the budget is proportional to the number of auctions, i.e., for some fixed . Recently, [27] showed that joint dual-optimal algorithm scores high along three dimensions. It runs out of budget at most auctions from the end of the horizon, violates the ROS constraint by an amount , and attains a regret (conversion value relative to offline optimum) of . Our main result in this paper is to show that the min pacing algorithm also scores high along three dimensions, achieving bounds similar to those of the dual-optimal pacing algorithm. The analysis of the min pacing algorithm is challenging because we do not have access to a Lyapunov function, as in the dual-optimal pacing case. Instead, we analyze the algorithm by carefully studying the dynamics of the dual variables, which evolve according to a complex stochastic process. In particular, using the ODE technique for recursive algorithms, we first prove that the min-pacing algorithm quickly identifies which constraint binds and reaches the orbit of an optimal solution in time steps. Then, using stochastic stability tools, we argue that the algorithm never leaves the orbit of an optimal solution with high probability. We conclude by showing that the regret accumulated once the algorithm is in orbit is small using results from online convex optimization.

We finally argue that sequential pacing leads to unacceptable levels of ROS constraint violation or regret. In particular, we show any instantiation of the sequential pacing algorithm can have either linear (i.e. ) ROS violation or linear regret on some instances.

Empirical evaluation.

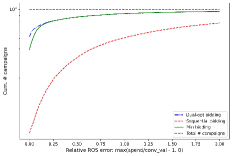

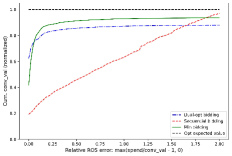

Section Section 4 explains in detail our evaluation methodology, including how we construct our semi-synthetic dataset, how we obtain the different quantities in our optimization formulation (1) based on real auction data. Here we give a high-level summary of our result. The objective of the algorithms is to maximize conversion value subject to budget and ROS constraints. In our simulations, as we explain in Section Section 4 we enforce a hard stop once the budget constraint is violated, but we do not enforce a hard stop for the ROS constraint. This is aligned with practice as budget constraints are usually enforced more strictly than ROS constraints. As a result, we cannot compare conversion values directly because some algorithms might produce solutions that are infeasible, i.e., they could violate the ROS constraints. Therefore, we evaluate the different algorithms as follows. For each algorithm, we determine for each percentual level violation of the ROS constraint, the total conversion value obtained by the algorithm over all the campaigns that violated the constraint by at most . By comparing these quantities, we can obtain the following critical insight: what percentage of ROS constraint violation does the naive sequential pacing need, to obtain the same value as the dual-optimal pacing does, at say constraint violation, or the min pacing does, at say constraint violation. Such plots are shown in Figure Fig. 2(b). Similar plots, but instead focusing on the number of campaigns that violate the ROS constraint by is portrayed in Figure Fig. 2(a).

The high level summary is quite evident from these figures: the naive sequential pacing needs to violate the ROS constraint by a very significant percentage to approach anywhere near the dual-optimal pacing, while the min pacing approaches the dual optimal pacing at a much smaller percentage of ROS constraint violation. Moreover, in sequential pacing, the feedback loops of budget and ROS can lead to unstable dynamics. Our findings suggest avoiding the sequential implementation despite its simplicity and appeal, and point towards having the two feedback loops either operating in a centralized manner, or at least minimally coupled as in the min pacing architecture. Overall, our work has implications for the design and operation of pacing services. Our findings suggest that the lack of coordination of sequential pacing can lead to suboptimal and unstable outcomes. Advertising should, whenever possible, adopt algorithms that have some level of coordination between budget and ROS pacing. If centralized architecture is not an option, then the minimally-coupled min pacing architecture is a simple, practical and high-performant option to consider.

1.3 Related Work

We discuss here the paper that is most related to ours, and due to lack of space, we discuss other related work in Appendix Appendix A. In independent work, Lucier et al. [42] studied a conceptually similar, yet different, algorithm that uses the final bid as the minimum of bid from the two pacing services. But unlike ours, the bid they use from each pacing service is different from the dual-optimal bid for that service. More importantly, they study a multi-bidder setting (unlike our single bidder setting) and their primary quantity of interest is the loss in liquid welfare, namely, the budget-capped sum of values obtained by all agents, when all of them employ this bidding algorithm. They establish that when the autobidding algorithms of agents play against each other, the resulting expected liquid welfare is at least half of the optimal expected liquid welfare achievable. But for the individual agent’s regret, even in a single bidder stochastic setting where the competing bids are drawn i.i.d. (rather than being set by other players simultaneously adopting the same algorithm), their regret bound is as opposed to the tight guarantee we prove. In general, proving a low regret guarantee when all bidders are simultaneously using the same algorithm requires strong assumptions that guarantee that the optimal dual variables of all agents converge to a unique Nash equilibrium. Such an analysis is provided by Balseiro ang Gur [11] for the case of utility-maximizing budget-constrained bidders under a strong-monotonicity assumption of the bidders expenditures. We conjecture our analysis could be extended to show similar low-regret guarantees in multi-bidder settings under similar strong assumptions, and we leave this is as an interesting research direction.

2 The setup

In this section, we define a formal model for budget and ROS constraint pacing. We consider a single bidder who participates in repeated auctions. The bidder derives a value of from getting allocated in auction . Upon submitting a bid of , the bidder gets an allocation of and an expected payment of . I.e., , and are the allocation and payment functions respectively. Note we assume without loss of generality (by scaling) that are all in . The tuple is drawn i.i.d. every round from an unknown distribution . We denote the sequence of samples by and sequences of length by where needed. At the beginning of round , the bidder has knowledge of the value and the historical information of past auctions to decide on a bid, . Denote to represent the outcome of the auction at round . At the end of round , the bidder observes . Thus the historical information at the beginning of round is .

The optimization objective

The advertiser is a value-maximizer and seeks to maximize the overall value while respecting the budget of dollars and the ROS constraint. Formally, the bidder’s optimization problem is stated as follows:

| (1) |

The first constraint is the ROS constraint, which states that for every dollar spent, there is at least a dollar of value.111More generally, one can have the constraint to state that for every dollar spent, there is at least dollars of value. But without loss of generality, one can set . The update to the bidding formula as a function of is quite straightforward, and we skip this here to avoid carrying the notational clutter of everywhere. The second constraint is the budget constraint. We define the per-round budget by . In round the bidder bids . The function could be randomized.

Truthful auctions, nontruthful auctions, uniform bidding policy.

We restrict attention to a uniform bidding policy, i.e., one computes a bid multiplier independently of the current value , and the bid submitted is . If the underlying auction is truthful 222An auction is truthful if the allocation function is weakly monotonically increasing, and the payment function satisfies In truthful auctions, quasi-linear utility maximizers are willing to report their value truthfully., Aggarwal et al. [1] showed that the optimal bidding algorithm for problem (1) is indeed a uniform bidding policy, and hence the restriction to uniform bidding is without loss of generality. If the underlying auction is non-truthful, the restriction to uniform bidding can be made without loss if the buyer has access to an optimizer that computes the optimal bid to submit in a one-shot auction for any given true value333If the bidder had access to and before placing the bid at time , the optimizer is . . In this case, bidding would be optimal for the bidder due to the revelation principle.

2.1 The Bidding Algorithms

Despite the simplicity and appeal of uniform bidding, computing the optimal multiplier requires knowledge of the entire set of , while information is only revealed in an online manner. Thus, to approach the performance of uniform bidding policy in an online setting, a standard technique is to dualize the constraints and look at the Lagrangian dual of the problem. We introduce dual variables for the budget constraint and for the ROS constraint and write Lagrangian dual of the problem (1):

| (2) |

At each time , the Lagrangian dual variables can be updated using online mirror descent, which is a generic framework such that different instantiations can lead to distinct dual update steps and theoretical guarantees. Then we compute the multiplier as a function of and set the bid of .

Dual-Optimal Pacing

We now discuss how to derive the optimal bidding multiplier when the underlying auction is truthful. Note that the Lagrangian dual problem (2) becomes separable over time after dualizing the constraints. Therefore, at time , assuming that the dual variables are and , the optimal bid by solving (2) is

| (3) |

where the second equation follows from extracting the factor and the last because the bidder’s problem is equivalent to that of bidding in a truthful auction when the value is . In other words . Note that is multiplicatively inseparable across and , therefore, we need a centralized pacing to update .

The dual variables are updated using feedback loops based on the auction result that have natural self-correcting features to prevent constraint violations (see Algorithm Algorithm 1). For example, in the case of the budget constraint, the feedback loop in (5) seeks to equate the actual spend of the auction with the per-round budget to satisfy the budget constraint (whenever this constraint is binding). Mathematically, the dual variable updates (i.e. the mirror descent step) are derived from solving a dual optimization problem, and we apply exponential updates for both budget and ROS dual variables in (4) and (5)444These exponential update rules are derived by instantiating with a particular Bregman divergence function in the mirror descent setup.. We refer the reader to [11, 27] for more details. FPW [27] show that this specific setup obtains near-optimal regret , where regret is the difference between the offline optimal total value and the bidding policy’s total value.

| (4) |

| (5) |

Sequential Pacing.

If one were to consider the problem (1) with just the budget constraint, the bidding policy (from Lagrangian duality with the ROS dual variable ) would be to bid , with the dual variable alone getting updated as in Algorithm Algorithm 1. Similarly, if one were to consider the problem (1) with just the ROS constraint, the bidding policy (from Lagrangian duality with budget dual variable ) would be to bid , with the dual variable alone updated as in Algorithm Algorithm 1. Given the historical context mentioned earlier, budget pacing systems have been around for longer than ROS pacing optimization. Therefore, it is not unexpected to have separate servers handling the feedback loops of the budget and ROS constraints and the final bid constructed in a sequential manner, namely,

| (6) |

In other words, the ROS constraint pacing service determines an intermediary bid which is fed to the budget service and, in turn, the budget pacing service operates on the scaled bid to get the final bid of (and also capped by the remaining budget ). While not optimal, this implementation has the benefit of being decentralized, i.e., it could operate separate servers for budget pacing and ROS pacing, that (a) only communicate the temporary bid and (b) could update their respective variables at different frequencies.

Min Pacing.

If the transition from sequential to dual-optimal pacing proves prohibitively expensive in the short term for organizational or engineering reasons, we propose and study another decentralized optimization, that we call the min pacing service. Rather than applying the bid-lowering operations of the two pacing systems sequentially, we take the minimum of the bids generated by the two systems:

| (7) |

The corresponding dual variables can follow the same update rules in Algorithm Algorithm 1 ((4) and (5)). The min pacing service operates in parallel instead of sequentially and also requires minimum coordination between budgeting and ROS pacing. We will show that even though is in general different from , and thus not the optimizer of the Lagrangian dual (2), bidding nonetheless achieves the same asymptotically optimal guarantees on regret and constraint violation as the dual-optimal pacing algorithm.

3 Theoretical Analysis of the Bidding Algorithms

In this section we analyze the performances of the pacing algorithms introduced in the previous section, and we use the notions of regret and constraint violation. To define the regret, we first define the reward of some pacing algorithm for a sequence of requests over a time horizon as

where ’s are the algorithm’s bids. Note the definition doesn’t require to satisfy the budget and ROS constraints. Next, we define the optimal reward for a sequence as the optimal objective of the offline optimization problem (1) given . The regret of is

We remark that we define for some specific drawn sequence, whereas is defined with respect to a distribution.

Note that itself does not fully measure the performance of since the reward of does not capture the budget and ROS constraints. All the pacing algorithms we discuss will cap the bid by the remaining budget, so the budget constraint is always satisfied. To evaluate our algorithms, we first need the following notion of stopping time.

Definition 3.1.

The stopping time of Algorithm 1, with budget is the first time at which

Intutively, is the first time step when the total payment almost exceeds the total budget. By budget endurance, we mean that is small for any or, in other words, the budget always runs out close to the end of the horizon.

In addition, we focus on the violation of the ROS constraint, i.e. . For constraint error we look at ex-post guarantees that hold for any .

In particular, both the joint pacing and min pacing algorithms achieve asymptotically nearly optimal guarantees in terms of the regret and constraint error in the stochastic i.i.d. setting. For simplicity we assume in our analysis that the allocation and payment functions are from truthful auctions. The result for the joint algorithm is already known from previous work in [14, 27].

We start with analyzing the regret of by considering a continuous-time approximation of the algorithm in which multipliers are updated using the expected gradients instead of their noisy stochastic counterparts used in the real algorithm.

Before proceeding with our analysis we provide some useful definitions. We denote by

the expected error in the budget and ROS constraints when the multiplier is . We plot some examples in Figure Fig. 3, which is located in the appendix. We require the following assumptions in our analysis.

Our first assumption is that the functions and cross zero once and from above, and that they are Lipschitz continuous.

Assumption 1.

We assume that the functions and are -Lipschitz continuous in and bounded. Moreover, the following hold:

(1) The function crosses the non-negative -axis once at and from above. That is, for any , we have and for any , we have .

(2) The function crosses the positive axis once at and from above. That is, for any , we have and for any , we have .

When the auction is truthful, it can be shown that the functions and always cross the positive axis from above. Therefore, the set of crossing points is always an interval. Assumption 1 rules out the possibility of multiple crossing points and, as we shall discuss later, implies the uniqueness of the optimal bidding strategy. This assumption is related to the so-called “general position” condition, which is pervasive in online allocation problems (see, e.g., [19, 3]). The Lipschitz continuity of the gradients is a common assumption in the analysis of online algorithms [33] and holds when either the interim allocation and payment are smooth, or the distribution of values is absolutely continuous. For example, this assumption might fail to hold in a second-price auction when values and competing bids are discrete (there, and are piecewise constant). In this case, it is possible to recover Lipschitz continuity by adding a small amount of random noise to the bids, which mollifies the functions and , without significantly impacting the performance of our algorithm. As a result, Assumption 1 is not too restrictive.

Under Assumption 1, we can upper bound the optimal performance in terms of the value collected by a uniform bidding policy that bids the minimum of the multipliers and , and provide a simple characterization of an optimal dual solution. The dual problem becomes where

is the dual function.

Lemma 3.2.

Suppose Assumption 1 holds. There exists an optimal solution with and if or and if . Moreover, we have that

where .

Assumption 2.

The problem is non-degenerate, namely, .

The non-degeneracy assumption guarantees that only one of the budget constraint or the ROS constraint can be binding for the uniform bidding policy. In practice, the data comes from a random process, and the budget and targets are given by the advertiser. Notice that the degenerate case stays in a lower dimension manifold, thus it is very likely that the non-degenerate assumption holds. Under the non-degeneracy assumption, the optimal multiplier is either or . We remark that this assumption is only imposed to simplify the analysis—we can provide a similar regret bound of for the degenerate case using techniques similar to the ones presented in this paper.

Assumption 3.

The gradients of the budget and ROS constraints have second moments bounded by .

Assumption 3 is common in the analysis of first-order algorithms for online optimization, where second moments are usually required to be bounded [33]. When the auction is truthful, a sufficient condition for this assumption to hold is that values have bounded second moments, i.e., .

Assumption 4.

There exists some and such that for all we have that either if or if .

Our final assumption requires that the spend and conversion value are locally strongly monotone around the optimal solution. In other words, we require the gradients to be locally linear around point where they cross the positive axis, for example, when the budget constraint is binding, we require that around (see Fig Fig. 3). Similarly to our Lipschtiz condition, we can guarantee this assumption holds by randomly perturbing bids. Assumption 4 is also common in the analysis of online algorithms, where it is sometimes assumed that objective functions are strongly convex, which is equivalent to gradients being strongly monotone [33].

The next theorem shows that the algorithm has an regret bound.

One can show that the optimal joint algorithm also has regret bound, which showcases that the algorithm achieves good practical performance.

Analyzing the min algorithm is challenging as we do not have access to a Lyapunov function as in the joint pacing case. We analyze the algorithm by carefully studying the dynamics of the dual variables under the min algorithm. Note that in light of Lemma Lemma 3.2, if we knew in advance which constraint is binding, then we could attain low regret by bidding using the multiplier associated with the binding constraint ( for the budget constraint and for the ROS constraint). Our proof technique is to show that with high probability the algorithm detects in steps which constraint is binding and then bids according to the optimal bidding multiplier for the binding constraint.

To do so, we consider a continuous time approximation of the multipliers in which we update them continuously according to the expected gradients, and dynamics are governed by an ODE. The ODE traces the “expected” path of the multipliers when the step-size is small. Here, we assume that step-sizes are for both constraints. The ODEs are obtained by considering the continuous approximation of multiplicative weight updates:

| (9) | ||||

where

The time in the ODE, which is denoted by can be mapped to a step in the discrete-time stochastic system by setting . In other words, the time in the ODE corresponds to the total distance traveled according to the step-size. We assume throughout that the ROS constraint binds at optimality. A similar analysis holds for the budget constraint. Our proof strategy is the following.

(1) Binding Constraint Identification. Setting the step-size to be , we show it takes order steps to be get to an orbit of size of an dual optimal solution . The orbit is chosen so that the bidding formula in this region is . We do so by first arguing that the ODE gets in a constant amount of time to the orbit of the optimal and then arguing that the actual algorithm remains close to the expected path traced by the ODE with probability using a discrete version of Gronwall’s Lemma to bound the absolute deviations and then invoking a concentration argument to bound the maximum deviation in a stochastic sense.

(2) Orbital Stability. Once the algorithm reaches an orbit of an optimal solution, we show that it never leaves the orbit with probability . We prove this result by constructing a local stochastic Lyaponuv function using the KL divergence and then invoking a classical result from stochastic stability.

(3) Regret Analysis. We conclude by showing that the regret accumulated once the algorithm is in the orbit of the optimal solution is . For this step, we first lower bound the conversion value collected by the algorithm in terms of the dual function and a complementary slackness term. Using weak duality, we can relate the first term to the optimal performance. The complementary slackness term is controlled using standard regret bounds for multiplicative weight updates. A detailed proof of Theorem 1 is presented in Appendix Appendix B.

Next, we present the constraint violation of the MinPacing algorithm. Recall that the bid is capped by the remaining budget; thus, the budget constraint will always be satisfied. Instead, we show that the budget always runs out close to the horizon’s end. On the other hand, for ROS constraint, we allow small violations throughout the horizon, and we can show that the violation is at most .

Theorem 2.

Suppose payments are at most the bid, i.e., for all . Then, satisfies the following:

(ROS constraint.) The violation of the ROS constraint is at most , i.e.,

(Budget endurance.) The budget always runs out close to the end of the horizon, i.e., stopping time satisfies .

The proof of Theorem 2 can be found in Appendix Appendix C.

Finally, we show that the sequential algorithm fails to work – it may have regret and/or constraint violation, thus it is not a sub-optimal algorithm. The proof of Proposition Proposition 3.3 is presented in Appendix Appendix D.

Proposition 3.3.

For any initial dual variables and step-sizes , there is an instance on which the algorithm either violates the ROS constraint by at least or has a regret at least .

4 Empirical Study

| Relative Constraint Violation | |||||||||||||

| Alg | |||||||||||||

| Frac. | Dual-optimal | ||||||||||||

| of | Min. | ||||||||||||

| Campaigns | Seq. | ||||||||||||

| Cum. | Dual-optimal | ||||||||||||

| Total | Min. | ||||||||||||

| Value | Seq. | ||||||||||||

We empirically evaluate the three algorithms discussed in Section Section 2.1. For confidentiality and advertiser privacy reasons, we evaluate their performance on a semi-synthetic dataset based on actual online advertising auctions. In particular, we focus on advertising campaigns from an online advertising platform that use a bidding product which is captured by our optimization formulation (1). More specifically, an advertiser bids (and therefore also pays) for clicks, i.e., submits bids for cost-per-click, and the objective is to maximize expected acquisitions (e.g. site visits, calls, conversions) with constraints on total spend being below an input budget and average cost per acquisition below an input target cost (). In our formulation (1), this corresponds to: The value is equal to , where is the probability of a conversion conditioned on a click (note both and are taken to be independent of the bid; while it is obvious for to be independent of the bid, ’s independence is supported by empirical studies [52]); The allocation is the number of clicks won by the advertiser at a bid of ; The payment is the cost of the clicks won at a bid of .

4.1 Semi-synthetic Dataset

Since we study the stochastic setting where the functions are drawn i.i.d. from some distribution, our dataset consists of a set of generative models. The parameters of the generative model for any given (actual) advertising campaign we study are derived from the performance of that campaign in the (actual) auction. We discuss the generative model itself and how we pick the parameters for each campaign in more detail in Appendix Section E.1.

4.2 Evaluation Setup

Our dataset includes randomly selected campaigns, and for each campaign, we set the budget constraint (i.e. in (1)) using its actual daily budget . We divide the day into -minute periods and use . For each campaign, we simulate an algorithm times to take the average total and total or conversion value as the result of the algorithm on that campaign. We include more details on how we simulate the algorithms as well as visualizations in Appendix Section E.2. For each algorithm, we take the pairs from all the campaigns, and arrange them into buckets based on the relative ROS constraint error555ROS constraint states that . So a constraint violation would imply , i.e., . . We look at the cumulative total value achieved by the algorithm through the ROS violation buckets. That is, for the bucket of at most relative error in the ROS constraint, we get the total value over all campaigns such that the algorithm has a relative ROS violation of at most . The cumulative total value over ROS error buckets gives us the picture of how an algorithm performs with respect to both the optimization objective and the constraints.

Benchmark.

For each campaign, our benchmark is the fluid relaxation of (1), but restricted to uniform bidding, i.e., for all . Formally, the benchmark is given by

| (10) |

We defer the details of how to calculate the benchmark value for campaigns in our semi-synthetic dataset to Appendix Section E.3.

4.3 Results

We show the performance evaluations of the three algorithms in Table Table 2, where each column is associated with a particular error bound, and we show the cumulative fraction of campaigns (top) and cumulative total value of campaigns (bottom) with relative ROS error up to the bound in each column. We normalize the quantities in the table: for value we normalize by our benchmark, i.e. sum of expected opt for all campaigns, and for number of campaigns we normalized by the total number . We look at the results both in terms of how well the algorithms respect the ROS constraint, and also the optimization objective of value maximization.

ROS constraint.

Both the dual-optimal and min pacing algorithms perform well at keeping the relative ROS error reasonably small, e.g. both have a reasonably large of campaigns finish with at most relative ROS error. The sequential pacing algorithm performs poorly in obeying the ROS constraint: only around of campaigns satisfy the ROS constraint, and in Figure Fig. 2 we see a considerable fraction of campaigns spend more than twice the conversion value.

Value maximization.

Both the dual-optimal and min pacing algorithms also do well at achieving good value. Recall our benchmark on each campaign should be fairly close to the expected optimal value of the fluid relaxation where both the ROS constraint and budget constraint are satisfied on expectation, so it is roughly an upper bound on the expected offline or hindsight optimal, and will be especially meaningful when an algorithm also obey the constraints relatively well. The dual-optimal pacing and min algorithms both achieve very large fraction of the benchmark with fairly small ROS error, e.g., for dual-optimal pacing the campaigns with relative ROS error in total get of the total benchmark conversion values over all campaigns, and for min pacing it is of the total benchmark. The sequential pacing algorithm gets much smaller total value compared to the dual-optimal and min pacing algorithms over campaigns finishing with small ROS error.

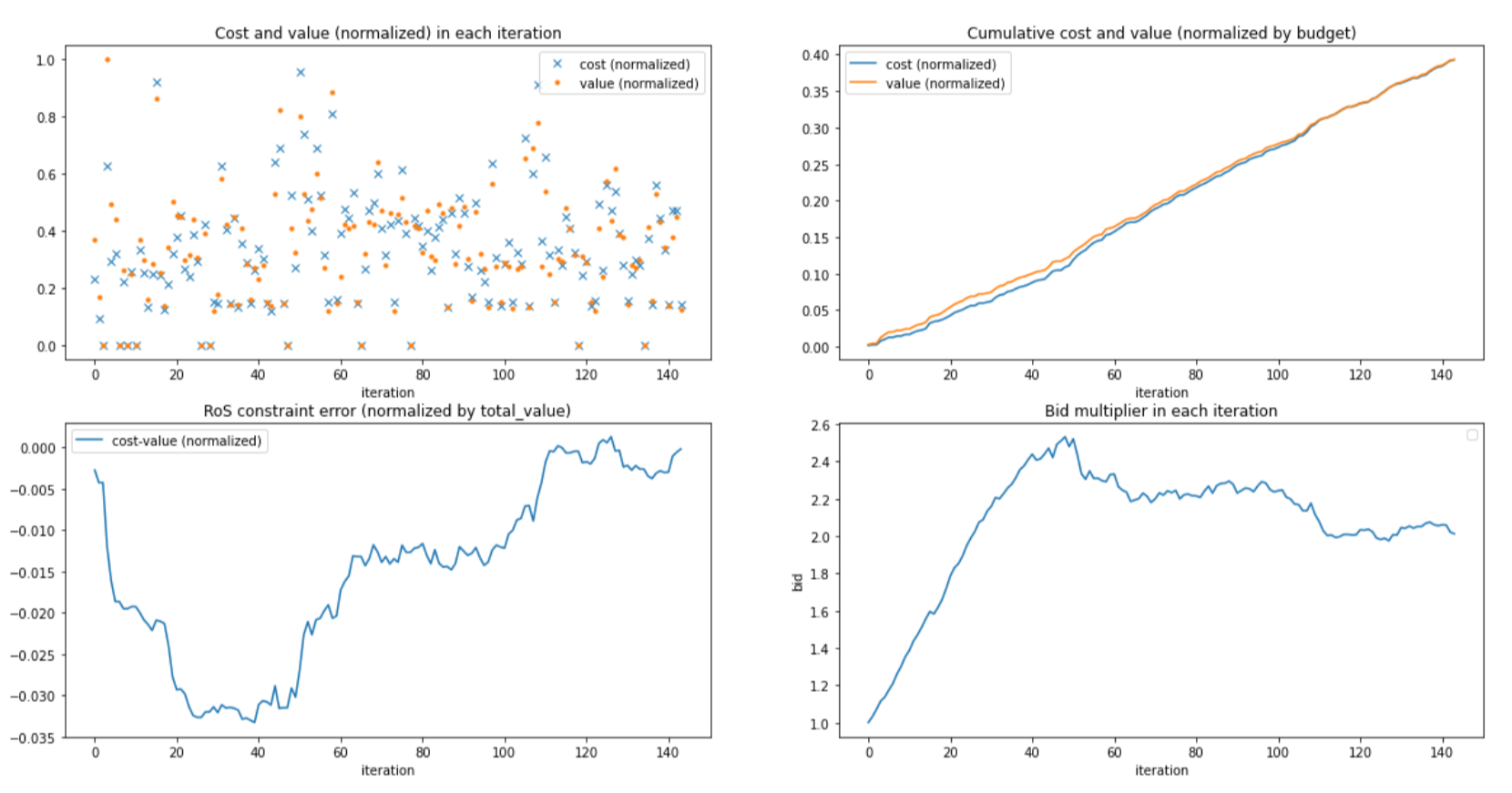

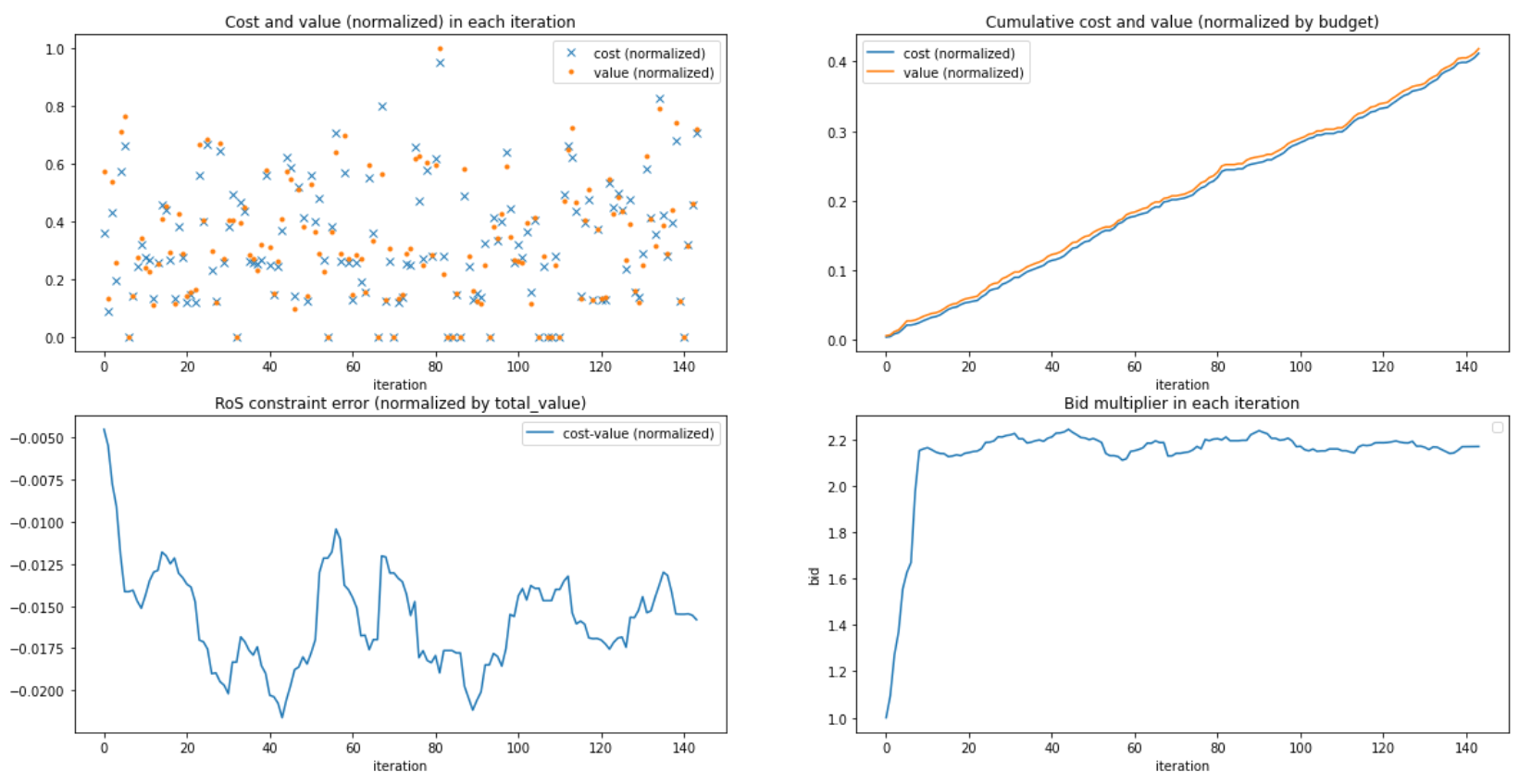

Stability and convergence

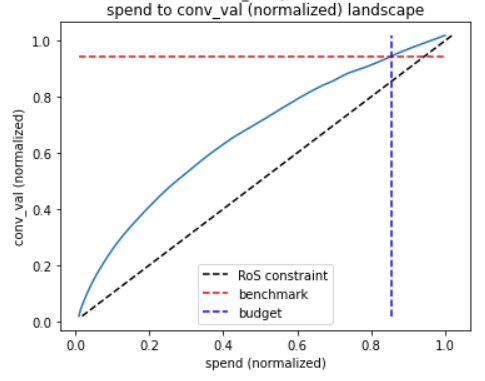

We observe that the trajectory of bidding multipliers generated by the dual-optimal and min pacing algorithms converge to the optimal solution of the benchmark (10). Figure Fig. 7 shows a representative campaign for which the ROS constraint is binding in the benchmark (but the budget constraint is not). After a small learning phase, the dual-optimal pacing algorithm converges to the optimal multiplier of around . The return-on-spend constraint is mostly obeyed and the total spend is smaller than the budget.

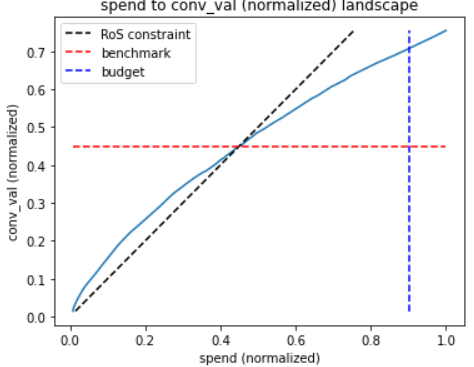

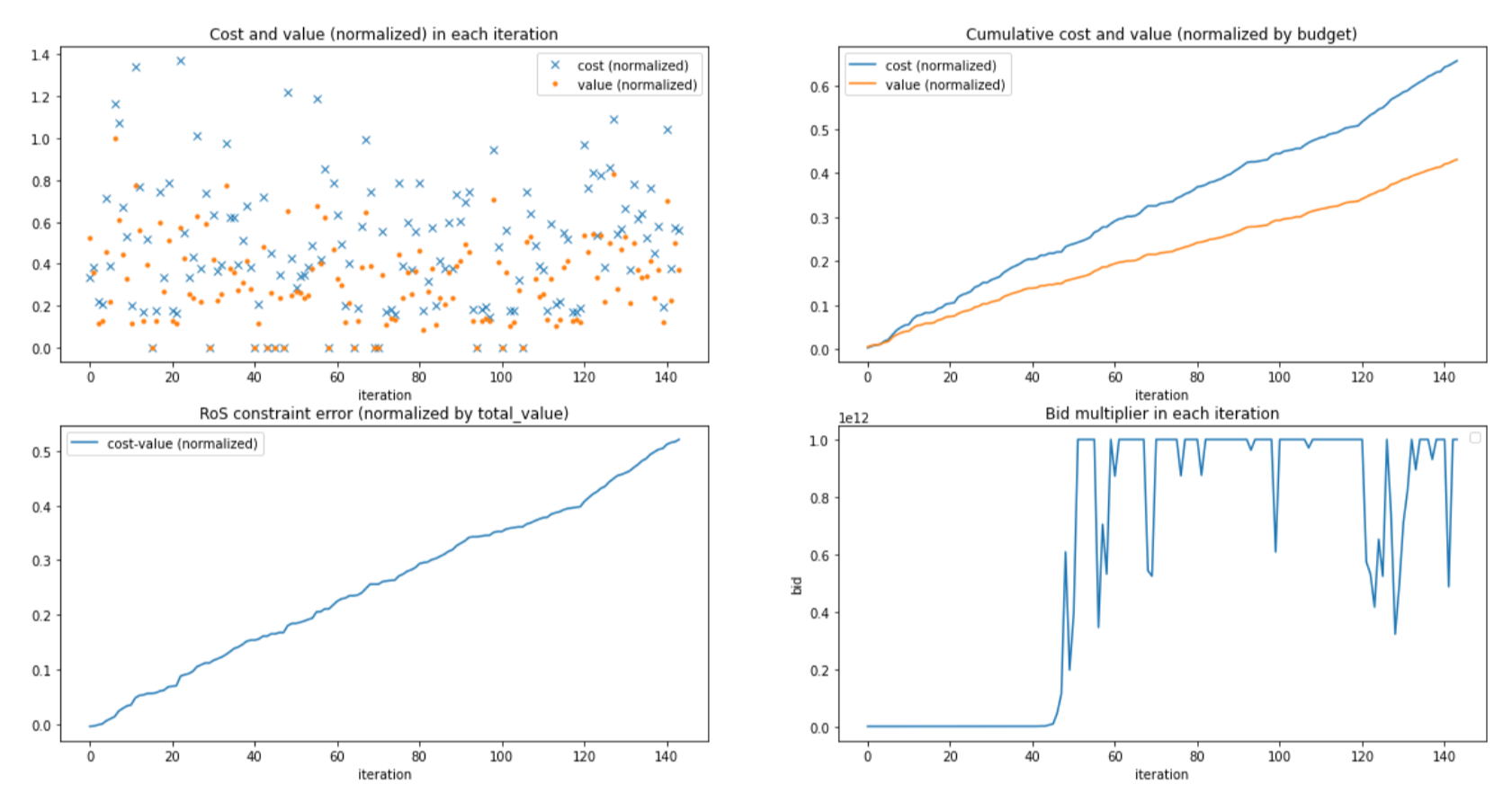

For the sequential pacing algorithm, however, we do not observe the convergence of bid multipliers. In Figure Fig. 7, it can be seen that the bid multipliers generated by the sequential pacing algorithm for the same campaign are highly unstable. Moreover, the ROS constraint is violated by a significant amount and the budget is exactly depleted by the end of the horizon. Interestingly, the behavior of the sequential pacing algorithm is driven by conflicting feedback loops between the budget and ROS pacing services. Recall that, at optimality, only the ROS constraint should bind. Initially, as the ROS pacing service detects a violation of the ROS constraint, it starts increasing its dual variable to satisfy the constraint. This results in a smaller bid multiplier and reduced spend. The budget pacing service, however, believing that the budget constraint is not binding reacts to the lower spend by decreasing its dual variable , which in turn, results in a higher multiplier. These two opposing feedback loops generate unstable dynamics and one constraint ends up being violated. Similar behaviors are observed across campaigns even when the budget constraint is binding.

References

- ABM [19] Gagan Aggarwal, Ashwinkumar Badanidiyuru, and Aranyak Mehta. Autobidding with constraints. In Web and Internet Economics - 15th International Conference, WINE 2019, New York, NY, USA, December 10-12, 2019, Proceedings, volume 11920 of Lecture Notes in Computer Science, pages 17–30. Springer, 2019.

- AD [15] Shipra Agrawal and Nikhil R. Devanur. Fast algorithms for online stochastic convex programming. In Piotr Indyk, editor, Proceedings of the Twenty-Sixth Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2015, San Diego, CA, USA, January 4-6, 2015, pages 1405–1424. SIAM, 2015.

- AWY [14] Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. A dynamic near-optimal algorithm for online linear programming. Oper. Res., 62(4):876–890, 2014.

- AZO [14] Zeyuan Allen-Zhu and Lorenzo Orecchia. Using optimization to break the epsilon barrier: A faster and simpler width-independent algorithm for solving positive linear programs in parallel. In Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms, pages 1439–1456. SIAM, 2014.

- B+ [15] Sébastien Bubeck et al. Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357, 2015.

- BBW [15] Santiago R. Balseiro, Omar Besbes, and Gabriel Y. Weintraub. Repeated auctions with budgets in ad exchanges: Approximations and design. Manag. Sci., 61(4):864–884, 2015.

- BCI+ [07] Christian Borgs, Jennifer Chayes, Nicole Immorlica, Kamal Jain, Omid Etesami, and Mohammad Mahdian. Dynamics of bid optimization in online advertisement auctions. In Proceedings of the 16th international conference on World Wide Web, pages 531–540, 2007.

- [8] Santiago R. Balseiro, Yuan Deng, Jieming Mao, Vahab S. Mirrokni, and Song Zuo. The landscape of auto-bidding auctions: Value versus utility maximization. In Péter Biró, Shuchi Chawla, and Federico Echenique, editors, EC ’21: The 22nd ACM Conference on Economics and Computation, Budapest, Hungary, July 18-23, 2021, pages 132–133. ACM, 2021.

- [9] Santiago R. Balseiro, Yuan Deng, Jieming Mao, Vahab S. Mirrokni, and Song Zuo. Robust auction design in the auto-bidding world. In Marc’Aurelio Ranzato, Alina Beygelzimer, Yann N. Dauphin, Percy Liang, and Jennifer Wortman Vaughan, editors, Advances in Neural Information Processing Systems 34: Annual Conference on Neural Information Processing Systems 2021, NeurIPS 2021, December 6-14, 2021, virtual, pages 17777–17788, 2021.

- BDM+ [22] Santiago R. Balseiro, Yuan Deng, Jieming Mao, Vahab S. Mirrokni, and Song Zuo. Optimal mechanisms for value maximizers with budget constraints via target clipping. In David M. Pennock, Ilya Segal, and Sven Seuken, editors, EC ’22: The 23rd ACM Conference on Economics and Computation, Boulder, CO, USA, July 11 - 15, 2022, page 475. ACM, 2022.

- BG [19] Santiago R. Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Manag. Sci., 65(9):3952–3968, 2019.

- BGM+ [19] Santiago Balseiro, Negin Golrezaei, Mohammad Mahdian, Vahab Mirrokni, and Jon Schneider. Contextual bandits with cross-learning. In Advances in Neural Information Processing Systems 32, pages 9679–9688. 2019.

- BKMM [17] Santiago R. Balseiro, Anthony Kim, Mohammad Mahdian, and Vahab S. Mirrokni. Budget management strategies in repeated auctions. In Rick Barrett, Rick Cummings, Eugene Agichtein, and Evgeniy Gabrilovich, editors, Proceedings of the 26th International Conference on World Wide Web, WWW 2017, Perth, Australia, April 3-7, 2017, pages 15–23. ACM, 2017.

- BLM [22] Santiago R. Balseiro, Haihao Lu, and Vahab Mirrokni. The best of many worlds: Dual mirror descent for online allocation problems. Operations Research, 2022.

- BLMS [22] Santiago R Balseiro, Haihao Lu, Vahab Mirrokni, and Balasubramanian Sivan. On dual-based pi controllers for online allocation problems. arXiv preprint arXiv:2202.06152, 2022.

- BM [22] Santiago Balseiro and Vahab Mirrokni. Robust online allocation with dual mirror descent. https://ai.googleblog.com/2022/09/robust-online-allocation-with-dual.html, 2022.

- CKK [21] Xi Chen, Christian Kroer, and Rachitesh Kumar. The complexity of pacing for second-price auctions. In Proceedings of the 22nd ACM Conference on Economics and Computation, EC ’21, page 318, New York, NY, USA, 2021. Association for Computing Machinery.

- CKSSM [22] Vincent Conitzer, Christian Kroer, Eric Sodomka, and Nicolas E. Stier-Moses. Multiplicative pacing equilibria in auction markets. Oper. Res., 70(2):963–989, mar 2022.

- DH [09] Nikhil R. Devanur and Thomas P. Hayes. The adwords problem: online keyword matching with budgeted bidders under random permutations. In John Chuang, Lance Fortnow, and Pearl Pu, editors, Proceedings 10th ACM Conference on Electronic Commerce (EC-2009), Stanford, California, USA, July 6–10, 2009, pages 71–78. ACM, 2009.

- DJSW [19] Nikhil R. Devanur, Kamal Jain, Balasubramanian Sivan, and Christopher A. Wilkens. Near optimal online algorithms and fast approximation algorithms for resource allocation problems. J. ACM, 66(1):7:1–7:41, 2019.

- DMMZ [21] Yuan Deng, Jieming Mao, Vahab S. Mirrokni, and Song Zuo. Towards efficient auctions in an auto-bidding world. In Jure Leskovec, Marko Grobelnik, Marc Najork, Jie Tang, and Leila Zia, editors, WWW ’21: The Web Conference 2021, Virtual Event / Ljubljana, Slovenia, April 19-23, 2021, pages 3965–3973. ACM / IW3C2, 2021.

- [22] Bid strategies: Meta business help center.

- Fac [23] About pacing: Meta business help center, Accessed 10/01/2023.

- FHK+ [10] Jon Feldman, Monika Henzinger, Nitish Korula, Vahab S. Mirrokni, and Clifford Stein. Online stochastic packing applied to display ad allocation. In Mark de Berg and Ulrich Meyer, editors, Algorithms - ESA 2010, 18th Annual European Symposium, Liverpool, UK, September 6-8, 2010. Proceedings, Part I, volume 6346 of Lecture Notes in Computer Science, pages 182–194. Springer, 2010.

- FMPS [07] Jon Feldman, S. Muthukrishnan, Martin Pál, and Clifford Stein. Budget optimization in search-based advertising auctions. In Jeffrey K. MacKie-Mason, David C. Parkes, and Paul Resnick, editors, Proceedings 8th ACM Conference on Electronic Commerce (EC-2007), San Diego, California, USA, June 11-15, 2007, pages 40–49. ACM, 2007.

- FPS [18] Zhe Feng, Chara Podimata, and Vasilis Syrgkanis. Learning to bid without knowing your value. In Proceedings of the 2018 ACM Conference on Economics and Computation, page 505–522, 2018.

- FPW [22] Zhe Feng, Swati Padmanabhan, and Di Wang. Online bidding algorithms for return-on-spend constrained advertisers, 2022.

- FT [22] Giannis Fikioris and Éva Tardos. Liquid welfare guarantees for no-regret learning in sequential budgeted auctions. CoRR, abs/2210.07502, 2022.

- GLL+ [22] Jason Gaitonde, Yingkai Li, Bar Light, Brendan Lucier, and Aleksandrs Slivkins. Budget pacing in repeated auctions: Regret and efficiency without convergence, 2022.

- GM [14] Anupam Gupta and Marco Molinaro. How experts can solve lps online. In Andreas S. Schulz and Dorothea Wagner, editors, Algorithms - ESA 2014 - 22th Annual European Symposium, Wroclaw, Poland, September 8-10, 2014. Proceedings, volume 8737 of Lecture Notes in Computer Science, pages 517–529. Springer, 2014.

- [31] Automated bidding strategies: Google product support.

- Goo [23] Google budget management, Accessed 10/01/2023.

- H+ [16] Elad Hazan et al. Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325, 2016.

- HPJ+ [14] Xinran He, Junfeng Pan, Ou Jin, Tianbing Xu, Bo Liu, Tao Xu, Yanxin Shi, Antoine Atallah, Ralf Herbrich, Stuart Bowers, et al. Practical lessons from predicting clicks on ads at facebook. In Proceedings of the Eighth International Workshop on Data Mining for Online Advertising, pages 1–9, 2014.

- HZF+ [20] Yanjun Han, Zhengyuan Zhou, Aaron Flores, Erik Ordentlich, and Tsachy Weissman. Learning to bid optimally and efficiently in adversarial first-price auctions. CoRR, abs/2007.04568, 2020.

- JLZ [20] Jiashuo Jiang, Xiaocheng Li, and Jiawei Zhang. Online stochastic optimization with wasserstein based non-stationarity. CoRR, abs/2012.06961, 2020.

- JZCL [16] Yuchin Juan, Yong Zhuang, Wei-Sheng Chin, and Chih-Jen Lin. Field-aware factorization machines for ctr prediction. In Proceedings of the 10th ACM conference on recommender systems, pages 43–50, 2016.

- KMS [22] Bhuvesh Kumar, Jamie Morgenstern, and Okke Schrijvers. Optimal spend rate estimation and pacing for ad campaigns with budgets. CoRR, abs/2202.05881, 2022.

- KTRV [14] Thomas Kesselheim, Andreas Tönnis, Klaus Radke, and Berthold Vöcking. Primal beats dual on online packing lps in the random-order model. In Proceedings of the Forty-Sixth Annual ACM Symposium on Theory of Computing, STOC ’14, page 303–312, New York, NY, USA, 2014. Association for Computing Machinery.

- Kus [67] Harold Joseph Kushner. Stochastic stability and control, volume 33. Academic press New York, 1967.

- LMP [22] Christopher Liaw, Aranyak Mehta, and Andrés Perlroth. Efficiency of non-truthful auctions under auto-bidding. CoRR, abs/2207.03630, 2022.

- LPSZ [23] Brendan Lucier, Sarath Pattathil, Aleksandrs Slivkins, and Mengxiao Zhang. Autobidders with budget and ROI constraints: Efficiency, regret, and pacing dynamics. CoRR, abs/2301.13306, 2023.

- LPW+ [17] Quan Lu, Shengjun Pan, Liang Wang, Junwei Pan, Fengdan Wan, and Hongxia Yang. A practical framework of conversion rate prediction for online display advertising. In Proceedings of the ADKDD’17, pages 1–9. 2017.

- LSY [20] Xiaocheng Li, Chunlin Sun, and Yinyu Ye. Simple and fast algorithm for binary integer and online linear programming. Advances in Neural Information Processing Systems, 33:9412–9421, 2020.

- LYS+ [20] Bin Li, Xiao Yang, Daren Sun, Zhi Ji, Zhen Jiang, Cong Han, and Dong Hao. Incentive mechanism design for roi-constrained auto-bidding. arXiv preprint arXiv:2012.02652, 2020.

- Meh [22] Aranyak Mehta. Auction design in an auto-bidding setting: Randomization improves efficiency beyond VCG. In Frédérique Laforest, Raphaël Troncy, Elena Simperl, Deepak Agarwal, Aristides Gionis, Ivan Herman, and Lionel Médini, editors, WWW ’22: The ACM Web Conference 2022, Virtual Event, Lyon, France, April 25 - 29, 2022, pages 173–181. ACM, 2022.

- MHS+ [13] H Brendan McMahan, Gary Holt, David Sculley, Michael Young, Dietmar Ebner, Julian Grady, Lan Nie, Todd Phillips, Eugene Davydov, Daniel Golovin, et al. Ad click prediction: a view from the trenches. In Proceedings of the 19th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1222–1230, 2013.

- Mye [81] Roger B. Myerson. Optimal auction design. Mathematics of Operations Research, 6(1):58–73, 1981.

- SLL [16] Yury Smirnov, Quan Lu, and Kuang-chih Lee. Online ad campaign tuning with pid controllers, April 21 2016. US Patent App. 14/518,601.

- Twi [23] How we built twitter’s highly reliable ads pacing service, Accessed 10/01/2023.

- TXH+ [20] Michael Tashman, Jiayi Xie, John Hoffman, Lee Winikor, and Rouzbeh Gerami. Dynamic bidding strategies with multivariate feedback control for multiple goals in display advertising. arXiv preprint arXiv:2007.00426, 2020.

- Var [09] Hal Varian. Conversion rates don’t vary much with ad position. https://adwords.googleblog.com/2009/08/conversion-rates-dont-vary-much-with-ad.html, 2009.

- WPR [16] Jonathan Weed, Vianney Perchet, and Philippe Rigollet. Online learning in repeated auctions. In Conference on Learning Theory, pages 1562–1583. PMLR, 2016.

- YLW+ [19] Xun Yang, Yasong Li, Hao Wang, Di Wu, Qing Tan, Jian Xu, and Kun Gai. Bid optimization by multivariable control in display advertising. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 1966–1974, 2019.

- YZZ+ [20] Zikun Ye, Dennis Zhang, Heng Zhang, Renyu Philip Zhang, Xin Chen, and Zhiwei Xu. Cold start to improve market thickness on online advertising platforms: Data-driven algorithms and field experiments. Available at SSRN 3702786, 2020.

- ZCL [08] Yunhong Zhou, Deeparnab Chakrabarty, and Rajan Lukose. Budget constrained bidding in keyword auctions and online knapsack problems. In Proceedings of the 17th International Conference on World Wide Web, WWW ’08, page 1243–1244, New York, NY, USA, 2008. Association for Computing Machinery.

- ZRW+ [16] Weinan Zhang, Yifei Rong, Jun Wang, Tianchi Zhu, and Xiaofan Wang. Feedback control of real-time display advertising. In Proceedings of the Ninth ACM International Conference on Web Search and Data Mining, pages 407–416, 2016.

- ZZS+ [18] Guorui Zhou, Xiaoqiang Zhu, Chenru Song, Ying Fan, Han Zhu, Xiao Ma, Yanghui Yan, Junqi Jin, Han Li, and Kun Gai. Deep interest network for click-through rate prediction. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 1059–1068, 2018.

Appendix A Related Work

Traditional auction theory in microeconomics studies maximizing objectives such as welfare, revenue and gains from trade in the presence of buyer(s) with quasilinear utility, namely, a utility of where is the value derived and be the payment. In this work, we adopt a different behavioral model, namely, one where advertisers maximize their value, subject to constraints on the return-on-spend (ROS) and total budget. As mentioned earlier, the significant rise in the adoption of autobidding algorithms in the past few years [22, 31] motivates the study of this model.

Optimal bidding algorithm for a single value-maximizing bidder with budget and/or ROS constraints.

ABM [1] initiated the study of value-maximizing bidders (value maximizers for short) subject to quite general constraints on value and cost. In particular, their model includes budget and ROS constraints. They show how the uniform bidding strategy is optimal if and only if the underlying auction is truthful (where truthfulness is defined from the point-of-view of a quasilinear bidder). Closest to our work is [27] who study the advertiser’s value maximization problem in the presence of both budget and ROS constraints in an online repeated auction setting. They show that a specific instantiation of what we call the joint pacing algorithm in this work achieves a regret while respecting both the budget and RoS constraints in the stochastic i.i.d. setting. Their algorithm computes the bid as a function of the two Lagrange multipliers exactly as in Equation (3).

Welfare in equilibrium among value maximizers.

While the description so far, and also our work, focuses on a single bidder’s optimal bidding problem, the equilibrium under the presence of multiple value maximizing bidders has also been a very active area recently. ABM [1] show how the VCG mechanism, which is welfare maximizing with quasilinear utility maximizers, can achieve, in the worst case, only a fraction of the optimal social welfare. Recent work by Meh [46] shows how randomization can improve the efficiency beyond the guaranteed by VCG, by establishing a POA of for bidders and how the POA is unimprovable beyond even with randomized mechanisms when . [41] study whether non-truthfulness can improve the POA beyond and show that this is not possible with a deterministic mechanism. But with the combined power of randomization and non-truthful mechanisms, they show how a randomized first-price auction can improve the POA to for two bidders, but again show it is unimprovable beyond when the number of bidders is large. Departing from the no information case studied by the above referenced papers, recent works by BDM+21b [9], DMMZ [21] show how to improve the efficiency under equilibrium beyond by adding boosts and reserves respectively, based on additional information from machine learned advice.

Revenue-optimal auction for value maximizers with budget and/or ROS constraints.

Much like the design of optimal auctions for utility-maximizing bidders [48], a recent line of work has focused on the design of revenue optimal mechanisms for value maximizers. BDM+21a [8], LYS+ [45] initiate this line of work, studying the revenue optimal mechanism in the presence of RoS constraints, but no budget constraints, under various information structures regarding whether or not the value is private, whether or not the advertiser specified target is private. [10] extend this work to include budget constraints for advertisers, and consider the information structure where value is public, so are advertiser budgets, but advertiser specified target is private.

Optimal bidding algorithm for a single utility maximizing bidder with & without budget constraint.

While works dealing with budget and ROS constraints in the presence of value maximizers have already been discussed, there has been a long line of work on doing the same for utility maximizers, but usually with just budget constraints. When values and competing bids are drawn from i.i.d. distributions, BG [11] show that the dual subgradient descent algorithm gives the optimal regret, and in the adversarial setting they show that it obtains the optimal asymptotic competitive ratio, namely, divided by the maximum value. ZCL [56] also study pacing in the adversarial setting and give an optimal competitive ratio, but one that is differently parameterized compared to [11]. KMS [38] study an episodic setting and show how to compute per-period target expenditures based on estimating the probability density based on samples, and ultimately pace based on these target expenditures. On similar lines JLZ [36] also show how to obtain the optimal regret in a non-stationary setting by first learning the probability distributions and then computing target expenditures based on those, using samples per distribution. Our paper is also loosely related with the rich literature about Learning to bid in repeated auctions [7, 53, 26, 12, 35], in which the existing papers usually abstract this problem as contextual bandits and do not incorporate budget or ROS constraints into them.

Equilibrium among budget-pacing strategies of utility maximizers.

There is a line of work studying equilibrium outcomes of budget pacing agents interacting with each other. We refer the reader to [29, 28, 17, 18, 6] and the references therein for more on this topic. Interestingly, these papers show that uniform bidding is also optimal in the presence of budget constraints. Also, BKMM [13] perform a comprehensive study of different common budget-pacing strategies and compare the system equilibrium in terms of their welfare, platform revenue, and advertiser utility.

Online resource allocation problems.

The budget pacing problem discussed in the preceding paragraphs is known to be a special case of online resource allocation problems, which have a long line of work. Most of the literature on this topic has focused on the i.i.d. input model or the slightly more general random permutation model. DH [19] introduce a training-based algorithm that learns the optimal dual variables from a batch of initial requests and then uses those to assign the rest of the requests. They show how to obtain a regret for the budgeted allocation problem (also known as the adwords problem) in the random permutation model. FHK+ [24] obtain a regret for more general linear packing problems in the random permutation model. AWY [3] obtain an improved regret by repeatedly solving for the optimal dual variables at geometrically increasing time lengths. The algorithm of KTRV [39] further solves a linear program at every step and apart from , also obtain the optimal dependence on the number of resources. DJSW [20] consider more general online packing and covering LPs, but in the i.i.d. model and obtain a regret with the optimal dependence on the number of resources. Their algorithm does not need to solve auxiliary linear programs if given an estimate of OPT. [30, 2, 14] make the formal connection between dual descent algorithms and online resource allocation, and show how one can use dual descent algorithms as a black box to obtain a regret. In particular, [14, 44] present simple algorithms that do not require solving auxiliary optimization problems.

Appendix B Proof of the regret bound of the algorithm

We choose the orbit to be a ball of size around the optimal solution

The value of is chosen so that

-

1.

Assumption 4 is satisfied for all ,

-

2.

The algorithm bids according to the binding constraint for all , i.e., ,

-

3.

The gradient of the budget constraint satisfies for all ,

-

4.

The gradients satisfy and if either or .

The second condition can be satisfied by Lemma Lemma 3.2 because there exists an optimal dual optimal solution with and , and the algorithm bids according to the ROS multiplier when . The third condition can be satisfied because the single-crossing property (Assumption 1) implies that for and non-degeneracy (Assumption 2) implies that for . The fourth condition holds by the single-crossing property because the gradients are negative for large enough multipliers .

B.0.1 Step 1: Binding Constraint Identification

For the first step, we show that if dual variables are positive, it takes the ODE a constant amount of time to get to the interior of the orbit.

Lemma B.1.

For any initial dual solution , there exits a finite time such that the solution of (9) satisfies and for all we have .

Proof.

It follows from Assumption 1 and 2 that for and for . Furthermore, denote , , , . We consider two cases depending on whether or is smaller.

Case 1: . In this case, we have , and the unique stationary point is given by and .

The whole space can be split into three regions (see Figure Fig. 4(a)):

Region I: . This region corresponds to . In this region, we have and , thus and .

Region II: . This region corresponds to subtracting region I. In this region, we have and , thus and .

Region III: . This region corresponds to the complementary set of region I and II. In this region, we have and , thus and .

Now, we are ready to show the result. Before proceeding, note that by definition , we have that and if and . Therefore, the ODE can never get closer to a distance from the origin.

First, we claim that for any initial solution , there exists such that it holds for all that . This is because once , would never go above due to the dynamics in regions II and III. So we just need to consider the first time . Notice that for all such that , there exists such that we have . Thus, we just need to choose .

Second, we claim there exists such that for , we have and . This is because after , . Thus, once , would never go below due to the dynamics in the regions I and II. So we just need to consider the first time . Notice that for all such that , there exists such that we have . Thus, we just need to choose .

Third, we claim there exists such that for , we have and . This is because after , . In this region, there exists such that and we just need to choose .

Fourth, we claim there exists such that for , we have that and . This is because after we have that and hence for all . The single-crossing property implies that only at , so we should reach in finite time.

Case 2: . This case is exactly symmetric to Case 1 by flipping and (see Figure Fig. 4(b)). ∎

We invoke the following result, which bounds the maximum error between a discrete-time stochastic system and its continuous-time ODE approximation.

Lemma B.2.

Consider the stochastic process with satisfying

where is a random function and is the step-size. The initial state lies in an open subset . The random functions are i.i.d. with expectation . We assume that the random functions have uniformly bounded expectation for all , uniformly bounded variance for all , and its expectation is -Lipschitz continuous in w.r.t. the max-norm, i.e., for all . Then, the following holds:

-

1.

The ODE with has a unique solution in .

-

2.

Fix . Let be such that for all and . Then,

Proof.

Denote by the corresponding time in the ODE for the discrete step . The first part follows from Picard–Lindelöf theorem because is Lipschitz continuous.

We prove the second part in two steps. In the first step, use the Lipschitz continuity of the dynamics to show that deviations of from the expected path accumulate linearly and conclude by using a discrete version of Gronwall’s Lemma to bound the absolute deviations in an almost sure sense. This first step performs a deterministic analysis of the deviations. In the second step, we use a concentration argument to bound the maximum deviation in a stochastic sense.

Step 1.

Introduce a time corresponding to the first time with such that . Consider a step under the event that , which implies that for all and for all . Using the dynamics of the stochastic process and the ODE, we obtain that

From the mean value theorem, because the solution to the ODE is absolutely continuous, we know there exists such that

Therefore, we have that

where . We refer to as a stochastic error and as the integration error. Using that is -Lipschitz continuous in , the integration error can be bounded as follows:

where the last inequality follows because from the mean value theorem there exists such that together with the fact that and .

Therefore, summing over steps and using that the initial conditions satisfy , we obtain that the following is true under the event :

where the we denote by and last inequality follows from the triangle inequality together with .

We next apply the following discrete version of Gronwall’s Lemma.

Lemma B.3 (Discrete Gronwall’s Lemma).

Let be a sequence satisfying with . Then,

Setting and choosing appropriately, we obtain that

Step 2.

Denote by the sigma-algebra generated by the random functions up to step . We have that is a martingale because and . Moreover, and is a stopping time with respect to because .

Taking expectations over the maximum of all steps up to , we obtain that

where the first inequality follows from Minkowski inequality. It is sufficient to bound each coordinate at a time because

where the first equation follows from exchanging maximums and the second since . Using that is a stopping time and is a martingale that

where the first inequality follows from Doob’s Martingale Inequality because the stopped martingale is a martingale, the second equality because martingale differences are orthogonal, and the last our bound on the variance of the random function. Putting everything together, we obtain that

| (11) |

To conclude that if is the first time win which , then we must have , which implies that (because if , we would have that because and the definition of ). The latter imples that or . Therefore, we can write the event in the statement as

where the first inequality follows from an application of Markov’s inequality and the last from (11). We conclude by noting that . ∎

We apply Lemma Lemma B.2 to and set the random function to be the gradients of the ROS and budget constraints, respectively. That is,

This choice reduces the stochastic process in the statement of the lemma to the update rule of the algorithm. Taking expectations, we obtain that

By assumption, the expected gradients are bounded and have finite variance. For Lipschitz continuity we need to show that for

The expected gradients, however, are not Lipschitz continuous for all multipliers because of the logarithmic transformation. To guarantee Lipschitz continuity, we restrict the set of dual solutions to lie in the set

For example, the gradient of the budget constraint be written as

Because the minumum and the log-sum-exp function are 1-Lipschitz continuous, we obtain that

is 1-Lipschitz continuous in . For we have that , which implies that is -Lipscthiz continuous because the exponential function is -Lipschitz continuous in .

In Lemma Lemma B.2, we set as the time it takes the ODE to reach the set and . Under the good event , we have by Lemma Lemma B.1 that and, thus, the dynamics are Lipschitz continuous. Moreover, we because the step size is we have that at time the state of the algorithm reaches the orbit with high probability. More formally, we have proved the following result.

Proposition B.4.

For every initial dual solution , there exists a time such that the probability of not hitting the orbit is bounded by

B.0.2 Step 2: Orbital Stability

We next show that once the iterates reach the orbit , they stay in the orbit for the rest of the horizon with high probability. To prove this result we show that the sum of Bregman divergence induced by the negative entropy constitutes a stochastic Lyaponuv function. The Lyaponuv function is given by

where the Bregman divergence is . Note that we can choose such that for all .

Assume that the ROS constraint is binding so that . Here, we have that . Let

be the empirical gradients at time . The multiplicative weight update implies that

where we used that second moments of the gradients are bounded by Assumption 3 and that the Bregman divergence is -local-strong-convex in by Lemma Lemma 2. Taking expectations conditional on the current iterates, we obtain that

For the budget constraint, we know that in the set there exists such that . Therefore, using that and we obtain that

For the ROS constraint, use that and for to obtain that

where the first inequality follows from the strong monotonicity condition in Assumption 4 and that dual variables are non-negative, the second inequality because for all , and the last inequality follows because the Bregman divergence of the negative entropy function satisfies for together with for all . Putting everything together, we obtain that there exists constant such that

We are now ready to invoke the following classical theorem on stochastic stability.

Theorem B.5 (Kus [40, p. 86]).

Let be a Markov process and a continuous non-negative function with

for every such that , where and . Then

Setting and , we obtain that for , which holds for large enough

where the last equation follows because , . Setting we obtain the following result.

Proposition B.6.

The algorithm is orbital stable, that is, the probability of leaving the orbit after time is bounded by

B.0.3 Step 3: Regret Analysis

As before, suppose that the ROS constraint is binding at the optimal solution. Consider an alternate algorithm that (1) behaves as the original algorithm up to time and (2) after time always uses the multiplier of the ROS constraint and projects the dual variable to . Let be the dual variable in this new algorithm and denote the multiplier used by . We denote by the event that the multipliers used by both algorithm match.

Let be a stopping time as defined in Definition 3.1 corresponding to the first time the budget is depleted for some initial budget . Because values are non-negative, we can lower bound the reward of given any by summing over the value collected only in iterations from up to and conditioning on the event

where the first equation follows from the definition of the event , and the last inequality follows because and adding back periods after . We bound each term at a time.

For the first term, use that the alternate algorithm always bid according to the ROS constraint to write

Taking expectations, we can use that is a stopping time and a martingale argument to obtain that

where is the dual function. Let be the average dual variable for the ROS constraint. Using the convexity of the dual function we obtain that

where we used that is dual feasible and weak duality together with and . Because the alternate algorithm projects dual variables to , Lemma Lemma 2 implies that the Bregman divergence of the generalized negative entropy is -strongly convex. Applying the mirror descent guarantee in Lemma Lemma 1 to the linear functions we obtain that

because the alternate algorithm updates the dual variable of the ROS constraint according to . Therefore, we have that

| (12) |

For the second term, using that values are independent of the event we obtain

| (13) |

where the first inequality follows because values are i.i.d. and for all , the second equality follows from conditioning on the event , the second inequality follows because probabilities are at most one and if for some the event is true then it must be the case that since the algorithm bids according to the ROS multiplier in the orbit of the optimal dual solution, and the last inequality follows from Proposition Proposition B.4 and Proposition Proposition B.6.

B.1 Online Mirror Descent Results

The following are some known results of Online Mirror Descent that we used in our previous analysis.

Lemma 1 ([5], Theorem ).

Let be a mirror map which is -strongly convex on with respect to a norm . Let be convex and -Lipschitz with respect to . Then, mirror descent with step size satisfies

Lemma 2 ([4]).

The Bregman divergence of the generalized negative entropy satisfies “local strong convexity”: for any ,

Proof.

The claimed inequality is equivalent to

for . Suppose . Then, choosing , Section B.1 is equivalent to

for , which holds by Taylor series. Suppose . Then Section B.1 is equivalent to

which may be checked by observing that the function is decreasing and equals zero at . This completes the proof of the claim. ∎

Appendix C Proofs of Theorem 2

To prove the result, we first show the next lemma, which bounds the constraint violations for time .

Lemma 3.

Recall and with being the dual variables for the ROS and the budget constraint respectively, and being the bid used by the algorithm. If the payment and allocation functions satisfy for any bid (e.g. truthful auctions), then we have

Proof.

Our condition only says the payment is always non-negative and at most the bid. Recall we also normalize the functions so that , and all have range . For the ROS constraint, since and , we get

Similarly, for the budget constraint because , we get

∎

The first result in Theorem 2 on ROS constraint violation can be obtained from the below lemma.

Lemma 4.

Consider a run of the min pacing algorithm starting at and , then for any outcome over the iterations, the ROS constraint violation satisfies

Proof.

The second result in Theorem 2 on stopping time can be obtained from the below lemma.

Lemma 5.

Let , and consider a run of the min pacing algorithm starting at and , then for any outcome over the iterations, we have for all , and

Proof.

The part of follows inductively. If , either , then since the step-size is chosen to be small enough we have , otherwise if , by Lemma 3 we know and thus .

The part of can be shown by contradiction. Suppose , it means and thus

Similar to the ROS case, note , which gives a contradiction. ∎

Appendix D Analysis of sequential algorithm

We prove Proposition Proposition 3.3 in this section. That is, we will show that for any initialization of the sequential pacing algorithm, i.e. choice of initial values of the dual variables and their respective step-sizes , there will always be some instance on which the algorithm performs poorly, i.e. it either violates the ROS constraint by at least or has a regret at least .

Without loss of generality, we assume and are both . All the instances we use in the proof will be deterministic, i.e. are drawn i.i.d from a point distribution. In particular, all instances we consider have fixed values , and for all . Effectively the bid ranges from to , and is equivalent to the bid multiplier as . We pick these values for notation simplicity, and it is easy to scale all quantities down to satisfy our model where are all in . Note that the payment function is the truthful pricing corresponding to the allocation function in our example. We start with the following observations for our instance.

Observation D.1.

It is straightforward to see that in each iteration, the value is a concave function on the payment, i.e. (FigureFig. 5), and thus if we fix some total spend over some iterations, the largest total value is achieved by spending evenly (i.e. ) in each of the iterations. Similarly because of concavity, if there is an additional constraint that the per-iteration spend is at least , the optimal total value is achieved by spending per-iteration (over any iterations).

Observation D.2.

In each iteration, the largest ROS slack one can achieve is at most , i.e., by bidding .

Fix any , we will consider a pair of instances. The first instance has (and the as described above). It is easy to see for that and , and it is optimal to spend per iteration and get total value. It is also easy to check that this instance satisfies all the assumptions we need for the min-pacing algorithm. Consider the sequential pacing algorithm with two cases

-

1.