The Optimality of Constant Mark-Up Pricing††thanks: We acknowledge financial support from NSF grants SES-2001208 and SES-2049744, and ANID Fondecyt Iniciacion 11200365. We have benefitted from comments by Yang Cai, Jason Hartline, Yingkai Li, and Zvika Neeman. We thank Hongcheng Li for excellent research assistance.

Abstract

We consider a nonlinear pricing environment with private information. We provide profit guarantees (and associated mechanisms) that the seller can achieve across all possible distributions of willingness to pay of the buyers. With a constant elasticity cost function, constant markup pricing provides the optimal revenue guarantee across all possible distributions of willingness to pay and the lower bound is attained under a Pareto distribution. We characterize how profits and consumer surplus vary with the distribution of values and show that Pareto distributions are extremal. We also provide a revenue guarantee for general cost functions. We establish equivalent results for optimal procurement policies that support maximal surplus guarantees for the buyer given all possible cost distributions of the sellers.

Jel Classification: D44, D47, D83, D84.

Keywords: Nonlinear Pricing, Second Degree Price Discrimination, Profit Guarantees, Competitive Ratio.

1 Introduction

1.1 Motivation

The arrival of digital commerce has lead to an increasing use of personalization and differentiation strategies. With differentiated products along the quality dimension and/or the quantity dimension comes the need for nonlinear pricing policies or second degree price discrimination. The optimal pricing strategies for quality or quantity differentiated products were first investigated by \citeasnounmuro78 and \citeasnounmari84, respectively. The optimal pricing strategies were shown to depend heavily on the prior distribution of the private information regarding the types, and ultimately the willingness-to-pay of the buyers.

Yet, in many circumstances the seller has only very weak and partial information about the distribution of the types. The aim of this paper is to devise robust pricing policies that: (i) are independent of the specific distribution of the types and (ii) exhibit revenue guarantees across all possible distributions. The main results of this paper construct such robust pricing strategies and show that these pricing strategies can be expressed in term of very simple and transparent pricing policies. We establish revenue guarantees by comparing the profit under the robust pricing policy and any given distribution of private information to the social welfare attainable under the same distribution of private information. We then seek to identify the pricing policy that guarantees the highest ratio of these two measures across all feasible distributions with finite expectation. As the social welfare coincides with the profit that the seller could attain under perfect or first degree price discrimination, the ratio has two possible interpretations. In this second perspective we compare the revenue of the seller under incomplete information to the revenue that the seller could attain under complete information (and hence perfect price discrimination).

We consider two broad classes of pricing problems. First, we consider a class of quality differentiated pricing problems as first analyzed by \citeasnounmuro78. Here, the type of the buyer is the willingness-to-pay for a quality. The cost of production is an increasing and convex function of quality. We focus on iso-elastic cost function which allows to express the cost environment of the seller in terms of a constant cost elasticity. Second, we consider a class of quantity differentiated pricing as first analyzed by \citeasnounmari84. Here, the seller has a constant marginal cost of producing additional units of his good and the buyer has a concave utility for quantities. In this environment, the elasticity of demand is initially assumed to be constant across all types of the buyer.

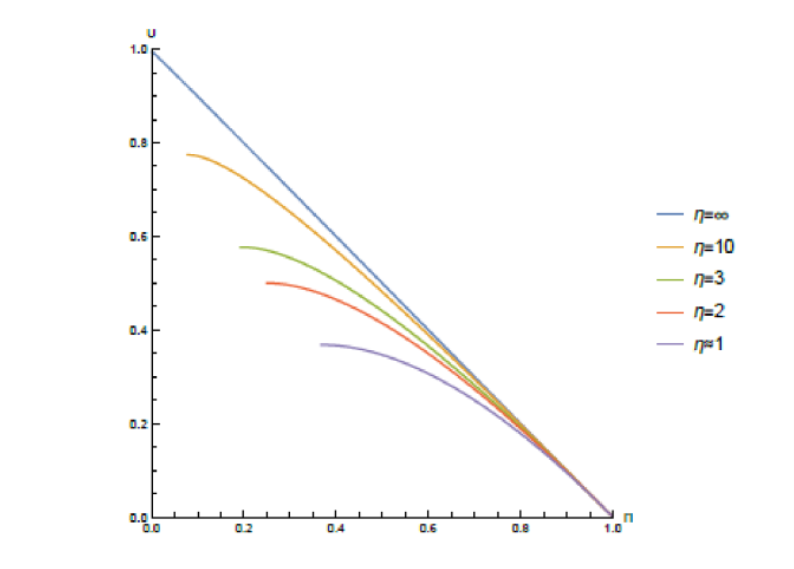

For the environment of quality differentiated products we exhibit a pricing mechanism that attains a profit guarantee that delivers at least a fraction of the social surplus across all possible prior distributions of private information. The profit guarantee that is expressed in the ratio is an expression that only depends on the cost elasticity of the quality. The ratio is described by a polynomial only in terms of the cost elasticity (Theorem 1). Interestingly, the optimal mechanism can be implemented by a pricing policy that maintains a constant mark-up for each additional unit. The mark-up is also expressed in terms of the elasticity and is given by (Corollary 2). For cost functions with an elasticity near , the ratio is the largest and is given by in the limit . As the cost function becomes more convex, the ratio decreases. With a quadratic cost function, i.e., when , the ratio is still . Eventually as the convexity of the cost becomes more pronounced, the ratio converges to as . We show that these profit guarantees are sharp and are attained by specific instances of distributions, namely Pareto distributions whose shape varies systematically with the elasticity of the cost function.

We then extend the scope of our analysis and give a complete characterization of the efficient frontier of producer surplus and consumer surplus that can be attained by optimal mechanisms across all possible distributions and all possible cost elasticities. Here we express both the ratios of the producer and consumer surplus relative to the social surplus. In fact, for every elasticity, the largest share of consumer surplus is attained by the very distribution under which the robust mechanism is the optimal revenue maximizing mechanism. While the efficient frontier is of immediate interest, we in fact obtain the entire set of pairs of attainable surplus across all distributions. Interestingly, a version of the Pareto distribution appears in all of the boundaries that form the set of attainable surplus pairs. The analysis delivers an exact upper bound on the profit guarantee when the cost function is entirely characterized by a constant elasticity . Yet, the mechanism that generates the bound, namely the constant mark-up pricing rule also generates a lower bound on the profit guarantee for arbitrary convex cost functions as long as the marginal cost is convex as well (Proposition 1).

We then turn to the model of quantity differentiation. Here the seller has a constant marginal cost to provide additional units of his product. By contrast, the buyer has a concave utility for the product and thus diminishing marginal utility for additional units of the product. The demand elasticity now summarizes the economics of the environment. The arguments developed in the setting with nonlinear cost can be largely transferred and yield equally sharp results. For every demand elasticity, we obtain a profit guarantee that is polynomial of the demand elasticity alone. Surprisingly, the robust mechanism is given by a linear pricing mechanism

1.2 Related Literature

We derive performance guarantees and robust pricing policies that secure these guarantees for large classes of second-degree price discrimination problems. We do this without imposing any restriction on the distribution of the values, such as regularity or monotonicity assumptions, or finite support conditions. We only require that the social surplus of the allocation problem has finite expectation.

The optimal monopoly pricing problem for a single object is a special limiting case of our model when the marginal cost of increasing supply becomes infinitely large. The analysis of a performance guarantee in the single-unit case is also a special case of a result of \citeasnounneem03. He investigates the performance of English auctions with and without reserve prices. The case of the optimal monopoly pricing is a special case of the auction environment with a single bidder. He establishes a tight bound for the single-bidder case that is given by a “truncated Pareto distribution” (Theorem 5). The bound that he derives is a function of a parameter that is given by the ratio of the bidder’s expected value and the bidder’s maximal value. Without the introduction of this parameter the bound is zero: as this ratio converges to zero, so does the bound. Similarly, \citeasnounharo14 establish that for distribution with support , the competitive ratio . Thus as grows, the approximation becomes arbitrarily weak (Theorem 2.1). By contrast, our results obtain a constant approximation for every convex cost function. Thus, the introduction of a convex cost function (or a concave utility function) leads to noticeable and perhaps surprising strengthening of the approximation quality.

carr17 considers a robust version of multi-item pricing problem. The buyer has an additive value for finitely many items and has private information about the value of each item. There the seller knows the marginal distribution for every item but is uncertain about the joint distribution of the valuation. \citeasnouncarr17 considers a minmax problem and shows that separate item-by-item pricing is the robustly optimal pricing policy. \citeasnoundero22 consider a related problem under informational robustness. There, the joint distribution of values is given by commonly known distribution but nature or the buyer can choose the optimal information structure. In the corresponding solution of the mechanism design problem, they show that the optimal mechanism is always one of pure bundling.

The focus of this paper is on second-degree price discrimination alone. \citeasnounbebm15 consider the limits of third-degree price discrimination. While most of their analysis is focused on the single-unit demand, they present some partial results how market segmentation can affect second-degree price discrimination. \citeasnounhasi22 present some additional results on the limits of multi-product discrimination for a given prior distribution of values.

2 Model

A seller supplies goods of varying quality to a buyer. The buyer has a willingness-to-pay (or value) for quality. The utility net of the payment is:

| (1) |

The value is distributed according to with support . The seller’s cost of providing quality is

| (2) |

Note that the cost has constant elasticity equal to .

An important benchmark is the social surplus generated by the efficient allocation:

| (3) |

This is clearly an upper bound on the profit and consumer surplus generated by any mechanism. We assume that:

This is a necessary and sufficient condition to guarantee that .

The seller chooses a menu (or direct mechanism) with qualities at prices

| (4) |

We use capital letters to denote functions and lower case letters to denote real numbers. The mechanism has to satisfy incentive compatibility and participation constraints. Thus for all

| (5) | ||||

| (6) |

The expected seller’s profit and buyer’s surplus generated by a distribution and a mechanism are respectively:

The optimal mechanism for distribution is:

With some abuse of notation, we denote by

the profit and consumer surplus evaluated at the seller-optimal mechanism.

3 A Profit-Guarantee Mechanism

3.1 A Minmax Problem

The first objective is to find the optimal profit-guarantee mechanism defined as:

| (A) |

As a direct by-product we find the distribution of values that minimizes the seller’s normalized profit:

| (B) |

In fact, we will show that the Minimax Theorem applies in our model, so (A) and (B) will be tightly connected.

As in related work on optimal pricing, the Pareto distribution and truncated versions of the Pareto distribution will play an important role. Towards this end, we define the truncated version of the Pareto distribution by:

| (7) |

That is, is the same as a Pareto distribution for values and it has a mass point at . We denote by

In other words, when we omit the parameter from the truncated Pareto distribution, it means we are taking the limit as . If then the expectation of the willingness-to-pay under the Pareto distribution is finite, and if , then the social surplus remains finite.

A mechanism is incentive compatible and meets the individual rationality constraint at if and only if the qualities are non-decreasing and the corresponding transfers are given by:

Since the optimal mechanism is uniquely defined by the qualities, we often refer to a mechanism as a set of qualities omitting the prices. The profits generated by a mechanism are:

| (8) |

We then have that the profit can be computed as a function of the qualities alone.

Under the Pareto distribution, the gross virtual values are given by:

| (9) |

and so the qualities supplied by the seller under the Bayes optimal mechanism are given by:

| (10) |

We now give the first main result, which provides the optimal profit-guarantee mechanism.

Theorem 1 (Profit Guarantee Mechanism)

The profit-guarantee mechanism is given by:

| (11) |

and generates normalized profit

| (12) |

for every .

Proof. We first prove that, for every distribution , the profits generated by qualities (11) are:

Note that we write because these are the profits generated by (11), which in general differs from the optimal mechanism under . Replacing (11) into (8), the qualities, we get:

where . Integrating by parts the second term we get:

Collecting terms, we get:

Replacing we get that:

We also note that the social surplus under distribution is:

We thus get that this strategy guarantees a fraction of the total surplus. Since (11) attains a fraction of the social surplus, the infimum cannot be smaller than this. But this fraction of the social surplus is exactly attained by the Pareto distribution with shape . Under this Pareto distribution, the above mechanism is the optimal mechanism. Hence, this gives (both) the optimal profit-guarantee mechanism and the minimum fraction of social surplus that can be generated by a Bayesian-optimal mechanism for any distribution of values.

This result establishes a mechanism that generates a profit guarantee at the level given by (12). Interestingly this mechanism generates the same normalized profit for every distribution of values!

We now establish that the profit guarantee given by (12) is indeed the optimal–the highest– profit-guarantee that can provided. For this, we first give the explicit solution to the Bayes-optimal mechanism (9) when the Pareto distribution has the shape parameter and the Bayes optimal mechanism equals the profit-guarantee established in Theorem 1.

Theorem 2 (Minimax Distribution)

The profit-guarantee mechanism is the Bayes optimal mechanism against the Pareto distribution with shape parameter:

and attains the infimum:

| (13) |

Proof. We can then compute the profit and social surplus in closed-form to conclude that, when .

This equation is valid only when because these are the Pareto distributions for which social surplus remains finite. However, by taking limit , we get (13) (and we also consider a truncated distribution as in (7) and take the limit ).

Theorem 2 then follows from Theorem 1. If the seller can guarantee herself a fraction of the social surplus, and this is in fact the best she can do for some distribution of values, then this distribution of values minimizes the fraction of the social surplus that the seller can generate as profit.

Thus the Pareto distribution with shape allows the seller to generate the least amount of normalized profit. Finally, we can analyze how the minimum normalized-profit varies with the cost elasticity. It is easy to check that the normalized profit guarantee is decreasing in We can evaluate the minimum profit for different cost elasticities:

| (14) |

Note that the limit corresponds to the case in which the seller is selling an indivisible good. The limit corresponds to the case in which the seller has nearly constant marginal cost.

We can similarly evaluate the consumer surplus at these different cost elasticities and Pareto distribution and find that:

| (15) |

The minmax solution of profit guarantee mechanism and Pareto distribution generate particular pairs of surplus sharing among seller and consumers.

Corollary 1 (Consumer Surplus in the Profit Guarantee Mechanism)

The profit-guarantee mechanism generates a constant consumer surplus

| (16) |

across all distributions .

We might have expected the uniformity of the profit guarantee across all distributions from the minmax property of the mechanism. Indeed, in \citeasnounharo14, the optimal single unit monopoly pricing policy also has the property that it generates a uniform profit guarantee across all distributions. By contrast, in the single unit monopoly pricing, the consumer surplus share is not uniform across all distribution. For a given willingness-to-pay , the net utility of a buyer is and thus the expected consumer surplus share thus depends on the distribution of . More precisely, in the profit-guarantee mechanism, each consumer receives the same share of the efficient surplus. By contrast, in the single unit monopoly pricing model, the share of the consumer surplus is increasing in the willingness to pay.

The property of a uniform consumer surplus share is interesting in its own right. But we might ask how the consumer surplus guarantee compares to levels of consumer surplus that can be attained across all Bayes optimal mechanisms. More generally, we can ask what the upper frontier of surplus sharing is among seller and buyers in the nonlinear pricing environment. This is what we pursue in the next Section 4.

3.2 A Constant Mark-Up Mechanism

It is useful to give an alternative representation of the optimal profit-guarantee mechanism as an indirect mechanism. An incentive compatible mechanism can be implemented by offering an indirect mechanism that asks for a price for a quality . Provided the indirect mechanism is sufficiently differentiable, the indirect mechanism can be represented by its marginal price for quality, the price-per-quality increment:

given by:

So that, if the buyer buys quality , the total payment is:

In other words, the transfer is the integral of the price of each additional quality increment.

Corollary 2 (Optimal Profit-Guarantee Mechanism)

The profit-guarantee mechanism can be implemented by offering quality increments at a price satisfying:

| (17) |

Following this corollary, the optimal profit-guarantee mechanism maintains a constant mark-up for each additional unit, where (17) is called the Lerner’s index. The constant mark-up here is determined by elasticity of the cost function.

It is informative to contrast the profit guarantee policy with the Bayesian optimal policy for a given prior distribution . In the Bayesian- optimal mechanism the qualities are solved by the first-order condition with respect to the virtual utility. Supposing for the moment that is regular, \citeasnounmuro78 solve:

The first-order condition is given by:

and the incentive compatible transfers in the associated direct mechanism are given by:

We thus have that:

Thus, the marginal price per unit of quality is given by:

Thus, the resulting markup is given by:

| (18) |

The right-hand-side is the negative of the reciprocal of the demand elasticity: this is the classic formula for the Lerner’s index. More precisely, the demand for quality at any given per-unit-of-quality price is:

Thus

| (19) |

We thus find the Bayes-optimal mechanism is determined entirely by the demand elasticity which can be expressed in terms of the product of the value and the hazard rate . By contrast, the profit-guarantee mechanism is determined only by elasticity of the cost function and does not refer to neither the willingness-to-pay nor the distribution of the willingness-to-pay. As the profit-guarantee is accomplished across all possible distribution of values, it does not refer to any specific distribution, but rather uses the cost information to offer a uniform menu for all possible distribution of values.

3.3 Non-Constant Cost Elasticity

In Theorem 1 and 2 we derive the optimal profit-guarantee mechanism for constant elasticity cost functions. We can then ask whether we can provide similar bounds in environment where the cost function does not satisfy the constant elasticity condition. To this end, we now consider convex costs function satisfying the curvature condition. We denote the pointwise cost elasticity by:

We assume that the cost elasticity is bounded:

We consider a mechanism in which the qualities supplied are in a linear relationship to the marginal cost of providing the quality:

| (20) |

where the linear parameter is chosen to satisfy:

| (21) |

Hence, we maintain a constant markup as in the profit-guarantee mechanism . When the cost has constant cost elasticity, we have that the quality given by , see (11), has the property that .

Proposition 1 (Profit Guarantee of Constant Markup Mechanism)

Proof. We note that when the seller charges a constant markup, the profits generated when the buyer’s value is are:

Hence, the profits generated are proportional to the production cost of the quality supplied to this type. We can write the profits in terms of the cost elasticity as follows:

Here we simply replaced the definition of the cost elasticity and we used that .

On the other hand, the efficient total surplus is given by:

We can write this as follows:

We thus get that:

We now prove that:

| (23) |

For this, we note that implies that for all :

We thus get that:

Analogously, also implies that

Taking the ratio of both inequalities, we get (23). We thus conclude that:

We can now take the reciprocal of this expression:

We clearly have that the expression is decreasing in . So,

The second equality follows from maximizing the expression with respect to , which has as a maximand

which completes the proof.

The constant mark-up mechanism given by (20)-(21) can thus provide a positive revenue guarantee in large class of convex cost functions without requiring a constant elasticity. We can verify that the guarantee is achieved by providing a larger quality than mechanism would if the cost elasticity were equal to the upper bound in the relevant range, namely as

As the seller provides a larger consumer surplus to the consumer, the revenue guarantee is weaker than in the optimal mechanism evaluated at the upper bound

Thus, the robustness against a larger class of cost functions with varying elasticity is achieved by conceding surplus to the consumer against a lower profit share.

4 Boundaries of Surplus Sharing

The profit guarantee mechanism can secure a profit guarantee for the seller as established by Theorem 1 and 2. Surprisingly, the guarantee is not only a lower bound for some distribution of values, but the mechanism enables the seller to attain this guarantee uniformly across all distributions. Corollary 1 then showed that the same mechanism also provides a uniform share of consumer surplus. But as the profit-guarantee mechanism is chosen to attain the highest possible profit level, we might be concerned that the profit guarantee mechanism is succeeding in obtaining a high profit share by depressing or even minimizing consumer surplus among all incentive compatible mechanism.

To approach this problem and answer this question, we now characterize the upper frontier of the feasible consumer surplus and profit share across all distributions:

| (24) |

We refer to the upper frontier as the surplus frontier. In other words, we seek to identify the maximum consumer surplus given that the profit is greater than or equal to some fraction of the social surplus. Of course, problem (24) is well defined when can be attained. In particular, when is the minimum profit that can be attained (i.e., equals to (B)) we will find the maximum consumer surplus across all distribution of values.

4.1 Surplus Frontier

We now provide a complete description of the surplus frontier.

Proposition 2 (Surplus Frontier)

The surplus frontier is given by:

| (25) |

The constraint is feasible if and only if .

Proof. We begin by writing and explicitly. We denote the virtual values as follows:

We denote the ironed virtual values by We can find a collection of intervals such that in and outside these intervals (i.e., in each interval of the form we have that and remains constant. The ironed-virtual values outside these intervals are given by:

The optimal quality offered by the optimal mechanism is given by (see \citeasnountoik11):

As it is standard in the literature, the quality is constant in , so to avoid confusion we write:

And types with a negative virtual value will be excluded. We then have that:

| (26) | ||||

Finally, we note that the first-best surplus is given by:

This corresponds to solving (3) explicitly.

We now note that the normalized profit can be written as follows:

| (27) |

To verify this, we note that in any regular interval we have that

Hence, we have that:

In any non-regular interval we have that

Hence, we have that:

We thus prove that (27) is satisfied and we can write the normalized profit as follows:

| (28) |

Using Hölder’s inequality we get that:

We thus have that:

Dividing by we obtain an upper bound on normalized consumer surplus:

| (29) |

We note that this function is decreasing in for all . Proposition 2 states that , so we obtain that the right-hand-side of (25) is an upper bound. We now need to show the inequality (29) is tight.

To prove the inequality is tight, consider a Pareto distribution with . We get that:

| (30) |

This proves that (29) is tight. Note that replacing in (25) we obtain:

We illustrate the frontier for different values of in Figure 1. As a direct corollary, we have the following upper bound on consumer surplus.

Corollary 3 (Maximum Consumer Suplus)

The consumer surplus is bounded above as follows,

| (31) |

and is attained by the Pareto distribution with shape parameter

Hence, we obtain that in general the buyer can capture a greater share of the social surplus when the cost is more elastic.

Surprisingly, the mechanism that guarantees the seller the highest profit guarantee across all distributional environments is also the mechanism that offers the buyer the highest expected consumer surplus across all optimal mechanism for all distributional environments. Thus, the mechanism that guarantees the seller the highest revenue does so by conceding the most consumer surplus and offering a nearly efficient mechanism. It provides an equilibrium allocation to every agent that is a constant fraction of the socially efficient allocation.

4.2 Lower Bound on Social Surplus

We now find a lower bound on the total surplus generated by a Bayesian-optimal mechanism across all distribution of values. That is, we find the minimum social surplus:

| (D) |

Note that is the social surplus generated by the efficient allocation so, in general, . We will be able to find this lower bound only when , that is, when the marginal cost is convex.

We now provide a lower bound on the distortions generated by any mechanism. Before we provide the result, we note that:

That is, when the distribution of values is the Pareto distribution with shape parameter the consumer’s surplus is 0 (in fact, it is 0 for every truncated Pareto distribution , not only in the limit), and the normalized profit is We thus have that:

| (32) |

In other words, the generated social surplus is a fraction of the efficient social surplus.

Proposition 3 (Lower Bound on Social Surplus)

When , social surplus is bounded below by:

Proof. Following expression (28) we obtain:

We first note that, , so when , we have that:

We now note that:

| (33) |

The inequality follows from the fact that, by construction of the ironed virtual values, for any increasing function we have that (see \citeasnounklms21 ). The equality follows from integrating by parts. Then the right-hand-side of (33) is exactly equal to , so we have that:

| (34) |

We can now show the inequality is tight. Using (32) we get that:

This corresponds to the lower bound (34). We thus have that:

Since and the infimum is attained at an information structure that generates 0 consumer surplus, we must also have that:

Multiplying by 2, we obtain the result.

As the cost becomes more inelastic ( grows), the lower bound becomes smaller. When the cost is quadratic, then the optimal mechanism always generates at least 1/2 of the social surplus. Note that the result obviously does not apply for every . In particular, in the limit we know that the optimal mechanism might introduce non-negligible distortions (see Proposition 2).

4.3 Complete Surplus Boundary

Finally, we might be interested in a complete characterization of the set of feasible surplus pairs. For the case of the quadratic cost function we can provide such a description. The reason that is particularly easy to analyze is that in this case we can compute all qualities in closed-form.

Beyond the quadratic case, we can also provide a general lower bound for the equilibrium surplus realized relative to the social surplus. This general bound only requires that the marginal cost is convex, thus .

The feasible normalized profit and consumer surplus are:

We consider the problem of characterizing . We will only be able to do this when , but previous results suggest that an analogous characterization applies to all

When for a fixed , we have that:

Taking the limit , we get that:

| (35) |

The curve for is the one characterized in Proposition 2; the curve for does not have a direct counter part in the results we have provided thus far (except for ).

Proposition 4 (Feasible Normalized Profits and Utilities)

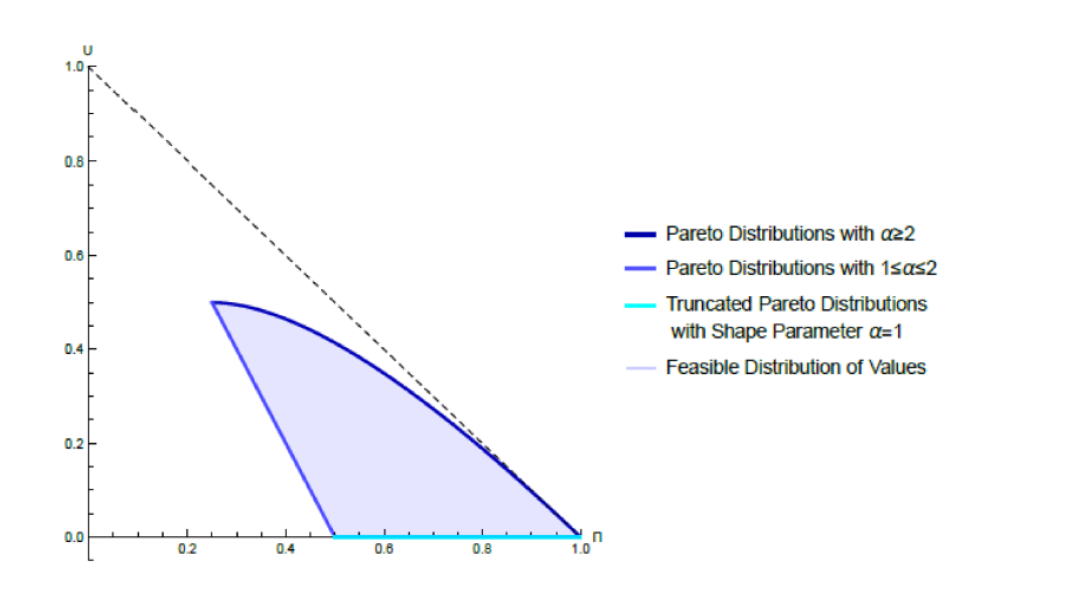

The closure of is given by the area enclosed by the curves in (35). Every point in the interior of is generated by some truncated Pareto distribution .

Proof. The upper boundary was characterized in Proposition 2. We now characterize the lower boundary of . Writing (34) for , we get:

However, the limit of Pareto distributions with parameter (see (30)) gives exactly that:

Hence, these distributions give the lower frontier of the set of feasible consumer surplus and profit.

The proposition gives a full characterization of the set of normalized profit and consumer surplus generated by any distribution of values. We provide an illustration of the result below in Figure 2. We established that the upper boundary of the surplus sharing between seller and buyers is attained by the family of Pareto distributions with . The lower bound along the segment that provides positive consumer surplus is attained by Pareto distribution with . Finally, the lower segment with zero surplus is attained by truncated Pareto distribution. Here, the seller offers the product only to the buyers with a value in the mass point of the truncated distribution. As a consequence, the seller can extract all the surplus and provides the efficient allocation for those buyers at the upper mass point. The buyers who get served receive zero net surplus.

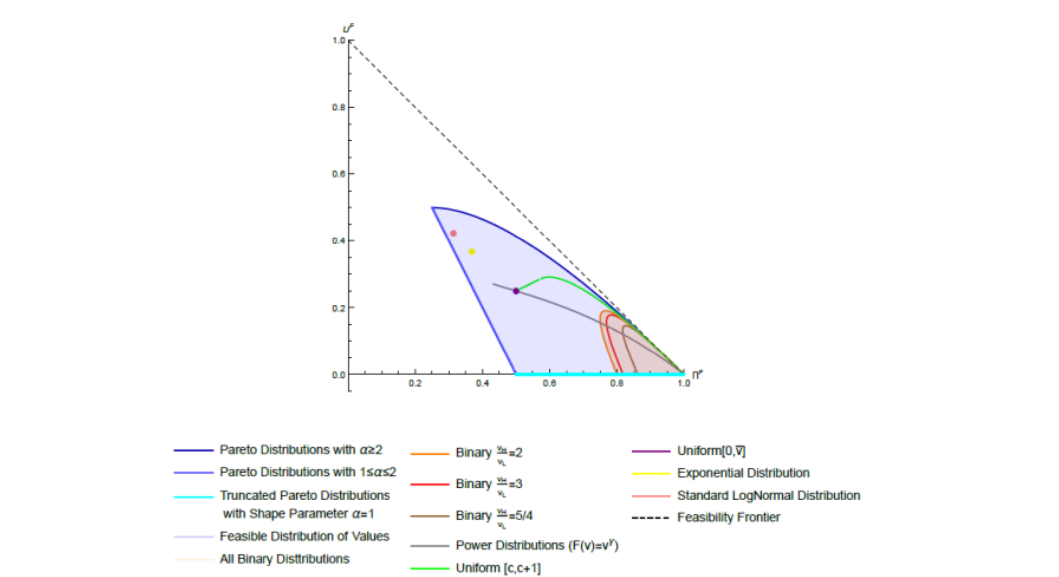

Thus, the family of truncated Pareto distribution generates all feasible surplus pairs. Yet we may be interested in how other distribution of value may affect the generation and distribution of surplus between the seller and the buyers. In Figure 3 we illustrate the range of outcomes that is generated by other families of distribution including binary, uniform and power distributions.

5 Quantity Discrimination

So far, we considered a model of quality discrimination in the spirit of \citeasnounmuro78. We now investigate corresponding results for quantity discrimination in the spirit of \citeasnounmari84. We first consider the multiplicatively separable model and then develop more general results. In the model of quality discrimination of \citeasnounmuro78, the buyer has a constant marginal willingness to pay for quality, and the cost of quality provision is increasing and convex. By contrast, in the model of quantity discrimination, there is a constant marginal cost of providing an additional unit of a given product. The diminishing returns now arise from the concavity of the utility function. Correspondingly, in the former the payoff environment is described by the cost elasticity whereas in the later the demand elasticity determines the choices of buyer and seller.

We first provide a profit guarantee for the case of multiplicatively separable utility functions and then extend it to nonlinear environments without separability conditions.

5.1 Multiplicatively Separable Utility

We now assume that the utility function is given by

for some . Thus the utility function for a higher quantity is increasing and concave. The cost of production is linear , where we normalize

The demand is defined by the inverse of the marginal utility:

where the subscript denotes the partial derivative with respect to . With the above parametrization we find that the demand elasticity is

We note that as we shift from cost elasticity to demand elasticity, we maintain as the parameter of the elasticity. However, now is a negative number .

As earlier in the case of quality discrimination, the Pareto distribution with the shape parameter is playing a critical role for the minmax problem.

Theorem 3 (Profit Guarantee with Quantity Discrimination)

The profit guarantee mechanism is a uniform-price mechanism with

| (36) |

It generates profits:

| (37) |

for every . Furthermore, The profit-guarantee mechanism is the Bayes optimal mechanism against the Pareto distribution with shape parameter and attains the infimum:

| (38) |

Proof. In the baseline model of Section 2, we have a buyer with utility function:

and a seller with a cost function:

Now consider the following change of variables

We then have that the utility functions and cost functions are given by:

and

With this change of variable we then obtain the model of this section. The profit guarantee result of Theorem 1 and 2 then follow immediately. We then establish that the uniform price mechanism is Bayes optimal against the Pareto distribution with parameter .

The social surplus is given by:

On the other hand, the profit are given by:

We then have that:

Taking the limit , we obtain the result.

Thus, in the case of concave utility functions and linear cost functions we can recover a profit guarantee mechanism. The mechanism maintains the constant mark-up property that we saw earlier, but in the presence of linear costs, we now have that a linear pricing mechanism, a uniform per unit price, generates the profit guarantee. Thus, the profit guarantee can be established with an even simpler mechanism. With the change in variable suggested in the proof of Theorem 3, it also follows immediately that the profit guarantee mechanism generates a uniform profit and consumer surplus share for all distributions . Thus, the profit guarantee mechanism maintains a uniform sharing of surplus between buyers and seller across all distributions.

5.2 Nonlinear Utility

We now consider a class of nonlinear utility functions in which willingness-to-pay and quantity can interact in a nonlinear manner and without the former multiplicative separability condition. Thus, we assume that the utility net of the payment is:

where is concave in given . The willingness-to-pay parameter remains distributed according to and the cost of production remains linear and we normalize without loss of generality.

With the nonlinearity now appearing in the utility function, we have implicitly assumed that the seller has perfect information about the exact shape of the nonlinearity while assuming incomplete information about the willingness-to-pay of the buyer. Therefore we are now asking whether we can find a profit guarantee for the seller even when the seller has imperfect information about the nonlinearity and hence the elasticity of the demand function.

The demand function is then defined by the inverse of the marginal utility:

where the subscript denotes the partial derivative with respect to . The demand elasticity is then given by:

where the demand elasticity is assumed to be negative for all . We assume that, for all ,

| (39) |

for some . We next present a robust profit guarantee that holds as long as the demand elasticity is within the range for some upper bound .

For a given demand function , the optimal uniform price is given by:

The first-order condition can be written as follows:

We then have that:

Since the upper bound will be relevant for our analysis, it is useful to denote by the profit generated by the uniform price mechanism with price :

Theorem 4 (Robust Profit-Guarantee Mechanism)

The uniform-price mechanism , where

guarantees a profit share of the social surplus:

| (40) |

Proof. The profit generated by a uniform price mechanism is given by:

The social surplus is given by:

The demand satisfies:

Since the price elasticity is non-increasing, we have that

We thus have that:

We then have that:

We then have that

We now note that the function is quasi-concave in . We also have that we assumed that and:

where . We thus have that:

Now, since the bound was established pointwise for every , it holds in aggregate across all .

Theorem 4 gives a profit guarantee for an environment where the demand elasticity may vary within a limited range across willingness-to-pay and price. Thus in contrast to the earlier results, it does not require a constant demand elasticity. The robustness of the profit guarantee is perhaps of more relevance when we consider demand rather than cost elasticity. After all, when the seller lacks information about the willingness-to-pay of the buyer, he may also lack information about the demand elasticity. Correspondingly, the bound that we obtain is somewhat weaker as it refers only to the upper bound in the demand elasticity. Similarly, we do not establish that the uniform price mechanism is Bayes optimal for arbitrary nonlinear demand functions that satisfy the above elasticity condition (39).

6 Procurement

We focused throughout on the classic problem of nonlinear pricing where the seller is uncertain about the demand of the buyers who have private information regarding their willingness-to-pay for varying quality or quantity. Alternatively, we might be interested in the robust procurement policies where a single large buyer wishes to procure from sellers who have private information about their cost condition. We can then ask what are the robust procurement policies as measured by the competitive ratio. As the selling and procurement problem are closely connected, we indeed find that a similar characterization as in Theorem 1 and 3 exists. As before, a distinction between quantity differentiation and quality differentiation proves to be useful.

6.1 Quality Differentiation

There is a buyer that procures an object with varying quality from a seller with unknown cost. The buyer has valuation for quality and the seller has a cost to provide a good of quality . The parameter is private information for the seller and described by distribution . The cost function is given by a constant elasticity

The efficient social surplus is generated by finding the optimal quality given the prevailing cost function:

The efficient quality is inversely related to the cost parameter

and generates a social surplus of:

If the buyer offers a constant price for every marginal unit of quality, then the seller will optimally offer a quality:

Corollary 4 (Surplus Guarantee Mechanism)

The optimal surplus guarantee mechanism offers a constant unit price

for incremental quality and the buyer is guaranteed a share:

of the efficient social surplus.

Thus, the robust optimal pricing policy is a uniform unit price for quality at which the seller can then deliver the optimal quality. The surplus guarantee is increasing in the elasticity of the cost function of the seller.

If follows a power function , the optimal mechanism consists of maximizing:

We get:

We thus get:

We get the same result when .

6.2 Quantity Differentiation

We can alternatively consider the case where the buyer has a declining marginal utility for quantity and the seller has a constant marginal cost of producing additional units of the product. The buyer thus has a utility function , where is the quantity of the good and

| (41) |

with a demand elasticity:

| (42) |

The utility function is increasing and concave in the above range with

(For , the above parametrization gives a negative gross utility.) The seller has cost

where the marginal cost is private information for the seller and given by a common prior distribution. The first-best surplus is:

The efficient quantity is:

and the social surplus is

Corollary 5 (Surplus Guarantee Mechanism)

The optimal surplus guarantee mechanism offers a constant mark-up

for quantity and the buyer is guaranteed a share:

of the optimal social surplus.

If the buyer sets a constant mark-up , the seller will sell

So, . So the buyer surplus will be:

We get that the optimal is:

Thus the buyer offers a constant mark-up pricing policy that the price per unit of quantity delivered is proportional to the marginal valuation.

Thus, for a large buyer, the optimal policy is not a constant unit price but a constant mark-up price that is decreasing in quantity. (This is easy to implement and offers a trade-off between commitment and insurance.)

7 Conclusion

We established robust pricing and menu policies for environments with second degree price discrimination. We showed that simple pricing policies, namely constant mark-up policies for the case of quality differentiation and linear pricing rules for the case of quantity differentiation attain the highest profit guarantee for the seller.

We established the optimality of these pricing policy for constant elasticity of cost or demand functions. But we showed that the features of the policies enable us to establish bounds even beyond the case of constant elasticity when we merely assume convexity for cost functions or concavity for demand functions.

In the analysis we focused on the classic optimal selling problem where the seller is designing a menu of choices to screen the buyers with private information regarding their willingness to pay. We showed however that the same arguments and associated mechanism allow us to establish utility guarantees in procurement settings. Here, the buyer seeks to derive optimal purchasing policies against vendors with private information regarding their cost or marginal cost of producing quantities or qualities. Thus, we derived robust profit or utility guarantees across a wide spectrum of nonlinear pricing problems.

We formulated the profit guarantee in terms of a competitive ratio relative to the socially efficient surplus. As part of the minmax problem, the Pareto distribution emerged as critical distribution that minimizes the revenue of the seller. As critical value distribution, the Pareto distribution generates a linear virtual utility. This suggests that a version of the Pareto distribution may also play an important role in related problems. For example, \citeasnounbebm15 consider the limits of third-degree price discrimination where the consumers all have unit-demand. It is an open problem how market segmentation can impact the surplus distribution in the context of nonlinear pricing problems, thus when we allow jointly for second and third-degree price discrimination. In related work, \citeasnounbehm23 we investigate the consumer surplus maximizing distribution for nonlinear pricing problems in the spirit of \citeasnounrosz17 and \citeasnoundero22 who consider single and many-item allocation problems respectively.

References

- [1] \harvarditem[Bergemann, Brooks, and Morris]Bergemann, Brooks, and Morris2015bebm15 Bergemann, D., B. Brooks, and S. Morris (2015): “The Limits of Price Discrimination,” American Economic Review, 105, 921–957.

- [2] \harvarditem[Bergemann, Heumann, and Morris]Bergemann, Heumann, and Morris2023behm23 Bergemann, D., T. Heumann, and S. Morris (2023): “The Informational Welfare Bounds of Optimal Auctions,” Discussion paper.

- [3] \harvarditem[Carroll]Carroll2017carr17 Carroll, G. (2017): “Robustness and Separation in Multidimensional Screening,” Econometrica, 85, 453–488.

- [4] \harvarditem[Deb and Roesler]Deb and Roesler2022dero22 Deb, R., and A. Roesler (2022): “Multi-dimensional Screening: Buyer-Optimal Learning and Informational Robustness,” Discussion paper, University of Toronto.

- [5] \harvarditem[Haghpanah and Siegel]Haghpanah and Siegel2022hasi22 Haghpanah, N., and R. Siegel (2022): “The Limits of Multi-Product Discrimination,” American Economic Review: Insights, 4, 443–458.

- [6] \harvarditem[Hartline and Roughgarden]Hartline and Roughgarden2014haro14 Hartline, J., and T. Roughgarden (2014): “Optimal Platform Design,” Discussion paper, Northwestern University.

- [7] \harvarditem[Kleiner, Moldovanu, and Strack]Kleiner, Moldovanu, and Strack2021klms21 Kleiner, A., B. Moldovanu, and P. Strack (2021): “Extreme Points and Majorization: Economic Applications,” Econometrica, 89, 1557–1593.

- [8] \harvarditem[Maskin and Riley]Maskin and Riley1984mari84 Maskin, E., and J. Riley (1984): “Monopoly with Incomplete Information,” RAND Journal of Economics, 15, 171–196.

- [9] \harvarditem[Mussa and Rosen]Mussa and Rosen1978muro78 Mussa, M., and S. Rosen (1978): “Monopoly and Product Quality,” Journal of Economic Theory, 18, 301–317.

- [10] \harvarditem[Neeman]Neeman2003neem03 Neeman, Z. (2003): “The Effectiveness of English Auctions,” Games and Economic Behavior, 43, 214–238.

- [11] \harvarditem[Roesler and Szentes]Roesler and Szentes2017rosz17 Roesler, A., and B. Szentes (2017): “Buyer-Optimal Learning and Monopoly Pricing,” American Economic Review, 107, 2072–2080.

- [12] \harvarditem[Toikka]Toikka2011toik11 Toikka, J. (2011): “Ironing without Control,” Journal of Economic Theory, 146(6), 2510–2526.

- [13]