Prediction-Powered Inference

Abstract

Prediction-powered inference is a framework for performing valid statistical inference when an experimental dataset is supplemented with predictions from a machine-learning system. The framework yields simple algorithms for computing provably valid confidence intervals for quantities such as means, quantiles, and linear and logistic regression coefficients, without making any assumptions on the machine-learning algorithm that supplies the predictions. Furthermore, more accurate predictions translate to smaller confidence intervals. Prediction-powered inference could enable researchers to draw valid and more data-efficient conclusions using machine learning. The benefits of prediction-powered inference are demonstrated with datasets from proteomics, astronomy, genomics, remote sensing, census analysis, and ecology.

1 Introduction

Imagine a scientist has a machine-learning system that can supply accurate predictions about a phenomenon far more cheaply than any gold-standard experimental technique. The scientist may wish to use these predictions as evidence in drawing scientific conclusions. For example, accurate predictions of three-dimensional structures have been made for a vast catalog of known protein sequences [1, 2] and are now being used in proteomics studies [3, 4]. Such machine-learning systems are increasingly common in modern scientific inquiry, in domains ranging from cancer prognosis to microclimate modeling. Predictions are not perfect, however, which may lead to incorrect conclusions. Moreover, as predictions beget other predictions, these imperfections may cumulatively amplify. How can modern science leverage machine-learning predictions in a statistically principled way?

One way to use predictions is to follow the imputation approach: proceed as if they are gold-standard measurements. Although this lets the scientist draw conclusions cheaply and quickly due to the high-throughput nature of the machine-learning system, the conclusions may be invalid because the predictions may have biases.

Another approach is to apply the classical approach: ignore the machine-learning predictions and only use the available gold-standard measurements, which are typically far less abundant than predictions. The resulting discoveries will be statistically valid, but the smaller amount of data will limit the scope of possible discoveries.

This manuscript presents prediction-powered inference, a framework that achieves the best of both worlds: extracting information from the predictions of a high-throughput machine-learning system, while guaranteeing statistical validity of the resulting conclusions. Prediction-powered inference provides a protocol for combining predictions, which are abundant but not always trustworthy, with gold-standard data, which is trusted but scarce, to compute confidence intervals and p-values. The resulting confidence intervals and p-values are statistically valid, as in the classical approach, but also leverage the information contained in the predictions, as in the imputation approach, to make the confidence intervals smaller and the p-values more powerful.

Prediction-powered inference can be used with any machine-learning system. As such, it absolves the need for case-by-case analyses dependent on the machine-learning algorithm on hand. The proposed protocol thereby enables researchers to report and assess the evidence for their conclusions in a fully standardized way.

1.1 General principle

We now overview prediction-powered inference. The goal is to estimate a quantity , such as the mean or median value of a random outcome over a population of interest. Towards this goal, we have access to a small gold-standard dataset of paired features and outcomes, , as well as the features from a large unlabeled dataset, , where we do not observe the true outcomes . We care about the case where . For both datasets, we have predictions of the outcome made by a machine-learning algorithm , denoted and .

Prediction-powered inference builds confidence intervals that are guaranteed to contain . Imagine we have an estimator of . One feasible but naive way to estimate , which we call the imputation approach, is to treat the predictions as gold-standard outcomes and compute . If the predictions are accurate, meaning , then is close to . However, will generally be biased due to errors in the predictions. Instead, our key idea is to use the gold-standard dataset to quantify how the prediction errors affect the imputed estimate, and then construct a confidence set for by adjusting for this effect.

More systematically, the first step is to introduce a problem-specific measure of prediction error called the rectifier, denoted as . The rectifier captures how errors in the predictions lead to bias in . Intuitively, recovers by “rectifying” . The appropriate rectifier depends on the estimand of interest , and we show how to derive it for a broad class of estimands. Next, we use the gold-standard data to construct a confidence set for the rectifier, . Finally, we form a confidence set for by taking and rectifying it with each possible value in the set . The collection of these rectified values is the prediction-powered confidence set, , which is guaranteed to contain with high probability.

![[Uncaptioned image]](/html/2301.09633/assets/figures/ppi-art.jpg) 1. Define rectifier

Define the rectifier, , a measure of prediction error.

2. Rectifier confidence set

With labeled data, create , a confidence set for the rectifier.

3. Prediction-powered confidence set

Construct confidence set by

rectifying with each value in .

1. Define rectifier

Define the rectifier, , a measure of prediction error.

2. Rectifier confidence set

With labeled data, create , a confidence set for the rectifier.

3. Prediction-powered confidence set

Construct confidence set by

rectifying with each value in .

Prediction-powered inference leads to powerful and provably valid confidence intervals and p-values for a broad class of statistical problems, enabling researchers to reliably incorporate machine learning into their analyses. We provide practical algorithms for constructing prediction-powered confidence intervals for means, quantiles, modes, linear and logistic regression coefficients, as well as other inferential targets. For conciseness, our technical statements and algorithms will focus on constructing confidence intervals; however, note that through the duality between confidence intervals and hypothesis tests, our intervals directly imply valid prediction-powered p-values and hypothesis tests as well.

1.2 Further preliminaries

We use to denote the labeled dataset, where and . We use the terms “labeled” and “gold-standard” interchangeably. We use analogous notation for the unlabeled dataset, , where the outcomes are not observed. For now we assume that and are independently and identically distributed samples from a common distribution, . We generalize our results to settings with distribution shift and finite populations in Section 4.2 and Appendix B, respectively. By we denote the estimand of interest, which will typically be an underlying property of , such as the mean outcome.

Next, we have a prediction rule, , that is independent of the observed data. For example, it may have been trained on other data independent from both the labeled and the unlabeled data. Thus, denote the predictions for the labeled data and denote the predictions for the unlabeled data. We let and . We will treat as vectors and matrices where appropriate.

Our key conceptual innovation is the rectifier : a measure of the prediction rule’s error. We formally define the rectifier in Section 2. We use to denote an estimate of the rectifier based on labeled data, which we call the empirical rectifier.

1.3 Warmup: Mean estimation

Before presenting our main results, we use the example of mean estimation to build intuition. Our goal is to give a valid confidence interval for the average outcome, . The classical estimate of is the sample average of the outcomes on the labeled dataset, . We construct a prediction-powered estimate, , and show that it leads to tighter confidence intervals than if the prediction rule is accurate. Consider

| (1) |

The key idea is that if the predictions are accurate, we have and , which has a much lower variance than since .

Notice is unbiased for and it is a sum of two independent terms. Thus, we can construct 95% confidence intervals for as

| (2) |

where , , and are the estimated variances of the , , and , respectively. The prediction-powered confidence interval is smaller than the classical interval when the model is good. Because , the width of the prediction-powered interval is primarily determined by the term . Furthermore, when the model has small errors, we have . Thus, the width of the prediction-powered interval will be smaller than the width of the classical interval. This estimator exists in many forms in the literature—see Section 1.4. This variance reduction is why prediction-powered confidence intervals are smaller than their classical counterparts in a broad range of settings beyond mean estimation.

1.4 Related work

Our technical results generalize tools from the model-assisted survey sampling literature [[, e.g.,]]sarndal2003model, which provides methods to improve inference from surveys in the presence of auxiliary information. In particular, the mean estimator in Section 1.3 is the difference estimator, closely related to generalized regression estimators [6]. It has long been recognized that model predictions can be leveraged as auxiliary data [7], and much work has gone into producing asymptotically valid confidence intervals when the predictive model is fit on the same data that is used for inference—see [8] for a recent overview. Our work is also related to the statistical literature on semiparametric inference, missing data, and multiple imputation [9, e.g.,]. In particular, Robins et al. [10], Robins and Rotnitzky [11], Chen and Breslow [12], Yu and Nan [13] study regression with missing data. The rectifier resembles debiasing strategies that are pervasive in this literature, an example being the AIPW estimator [11]. Likewise, our setting is related to measurement error [14, e.g.,], particularly to Chen et al. [15], who study the estimation of parameters defined as solutions to many estimating equations, as we will in this work. Prediction-powered inference aims to provide simple, broadly applicable algorithms using similar debiasing tricks, while allowing the use of state-of-the-art black-box machine-learning systems.

Recently, a body of work on estimation with many unlabeled data points and few labeled data points has been developed [16, 17, 18, 19, 20, 21], focusing on efficiency in semiparametric or high-dimensional regimes. In particular, Chakrabortty and Cai [22] study efficient estimation of linear regression parameters, Chakrabortty et al. [23, 24] study efficient quantile estimation and quantile treatment effect estimation with high-dimensional covariates, Zhang and Bradic [25] study mean estimation in a high-dimensional setting, Deng et al. [26] study linear regression parameters in a high-dimensional setting, and Hou et al. [27] study an imputation approach to improving generalized linear models. Finally, Song et al. [21] study M-estimation, using a projection-based correction to the classical M-estimator loss based on simple statistics (e.g. low-order polynomials) of the features. Prediction-powered inference continues in this vein but focuses on the setting where the scientist has access to a good predictive model fit on separate data and makes no assumptions about the model (such as consistency). The confidence intervals and resulting p-values from previous work rely on asymptotic approximations, while prediction-powered inference has both asymptotic and nonasymptotic variants. Furthermore, prediction-powered inference goes beyond random sampling and considers certain forms of distribution shift.

More distantly, our setting, in which we have access to some labeled data alongside unlabeled data, also appears in semisupervised learning [28, 29, e.g.,], which studies the question of how to improve prediction accuracy with unlabeled data. We also refer the reader to the related literatures on transfer learning [30, 31, 32, 33, e.g.,] and surrogates in causal inference [34, e.g.,]. Thematically, our work is most similar to the work of Wang et al. [35], who also introduce a method to correct machine-learning predictions for the purpose of subsequent inference. However, our work provides confidence intervals that are provably valid under minimal assumptions about the data-generating distribution, whereas Wang et al. require certain parametric assumptions about the relationship between the prediction model and the true response. We compare against this baseline in Appendix F.

2 Main theory: Convex estimation

Our main contribution is a technique for inference on estimands that can be expressed as the solution to a convex optimization problem. In addition to means, this includes medians, other quantiles, linear and logistic regression coefficients, and many other quantities. Formally, we consider estimands of the form

| (3) |

for a loss function that is convex in , for some . Throughout, we take the existence of as given. If the minimizer is not unique, our method will return a confidence set guaranteed to contain all minimizers. Under mild conditions, convexity ensures that can also be expressed as the value solving

| (4) |

where is a subgradient of with respect to . We will call convex estimation problems where satisfies (4) nondegenerate, and we will later discuss mild conditions that ensure this regularity.

Defining the rectifier.

Following the outline in Section 1.1, the first step in prediction-powered inference is to define a rectifier. As in the mean estimation case, the rectifier captures a notion of prediction error. In the general setting of convex estimation problems, the relevant notion of error is the bias of the subgradient computed using the predictions:

| (5) |

Rectifier confidence set.

The second step is to create a confidence set for the rectifier, , satisfying

| (6) |

Because the rectifier is an expectation for each , can be constructed using standard, off-the-shelf confidence intervals for the mean, which we review in Appendix E.

Prediction-powered confidence set.

The final step is to form a confidence set for . We do so by combining with a term that accounts for finite-sample fluctuations due to having unlabeled data points. In particular, for every , we want a confidence set for , satisfying

Again, since is a mean, constructing is easy and can be done with off-the-shelf tools.

We put all the steps together in Theorem 2.1.

Theorem 2.1 (Convex estimation).

Suppose that the convex estimation problem is nondegenerate as in (4). Fix and . Suppose that, for any , we can construct and satisfying

Let , where denotes the Minkowski sum.111The Minkowski sum of two sets and is equal to . Then,

| (7) |

This result means that we can construct a valid confidence set for , without assumptions about the data distribution or the machine-learning model, for any nondegenerate convex estimation problem. We also present an asymptotic counterpart of Theorem 2.1 in Appendix C.1.

Most practical problems are nondegenerate (4). For example, if the loss is differentiable for all , then the problem is immediately nondegenerate. Furthermore, if the data distribution does not have point masses and, for every , is nondifferentiable only for a measure-zero set of pairs, then the problem is again nondegenerate.

We have focused on convex estimation problems, since this is a broad class of estimands addressed by prediction-powered inference. Nonetheless, we highlight that the general principles for prediction-powered inference from Section 1.1 are applicable more broadly, and lead to additional results and algorithms for other estimands and some forms of distribution shift; see Section 4 for such extensions.

2.1 Algorithms

In this section we present prediction-powered algorithms for several canonical inference problems. We defer the proofs of their validity to Appendix D. The algorithms rely on confidence intervals derived from the central limit theorem. We implicitly assume the standard, mild regularity conditions required for the asymptotic validity of such intervals, which we overview in Appendix C.3. We also present a parallel set of algorithms that are obtained via nonasymptotic constructions in Appendix C.2. In the algorithms we use to denote the quantile of the standard normal distribution, for . All algorithms are technically simplified versions of Algorithm 5 with different choices of gradients and rectifiers; see Table 1 for the correspondence.

Mean estimation.

We begin by returning to the problem of mean estimation:

| (8) |

The mean can alternatively be expressed as the solution to a convex optimization problem by writing it as the minimizer of the average squared loss:

The squared loss is differentiable, with gradient equal to . Applying this in the definition of the rectifier (5), we get . Note that this rectifier has no dependence on . We provide an explicit algorithm for prediction-powered mean estimation and its guarantee in Algorithm 1 and Proposition 2.1, respectively.

Quantile estimation.

We now turn to quantile estimation. For a pre-specified level , we wish to estimate the -quantile of the outcome distribution:

| (9) |

To simplify the exposition, we assume that the distribution of does not have point masses; this ensures that the problem is nondegenerate (4), though it is possible to generalize beyond this setting with a standard construction. It is well known [36] that the -quantile can be expressed in variational form as

| (10) |

where is called the quantile loss (or “pinball” loss). The quantile loss has subgradient . Plugging the expression for into the definition (5), we get the relevant rectifier: . In Algorithm 2 we state an algorithm for prediction-powered quantile estimation; see Proposition 2.2 for a statement of validity.

Logistic regression.

In logistic regression, the target of inference is defined by

| (11) |

where . The logistic loss is differentiable and hence the optimality condition (4) is ensured. Its gradient is equal to , where is the predicted mean for point based on parameter vector . Other generalized linear models (GLMs) have the same gradient form, and thus also optimality condition (4), but for a different mean predictor (see Chapter 3 of Efron [37]). For example, Poisson regression uses . In view of our general solution for convex estimation, the rectifier is constant for all and equal to . In Algorithm 3 we state a method for prediction-powered logistic regression and in Proposition 2.3 we provide its guarantee. We use to denote the -th coordinate of point . Poisson regression is handled in essentially the same way: concretely, in Algorithm 3 we simply change the choice of defined in line 5.

Linear regression.

Finally, we consider inference for linear regression:

| (12) |

While it is possible to obtain an algorithm for linear regression based on Theorem 2.1, one can derive a more powerful solution by using the fact that the natural estimator for problem (12) is linear in . We exploit these further properties in Algorithm 4 and Proposition 2.4, where we state a method for prediction-powered linear regression and establish its validity, respectively.

Proposition 2.4 (Linear regression).

| Estimand | Prediction-based gradient | Rectifier | Procedure |

|---|---|---|---|

| Mean | Alg. 1 | ||

| Median | Alg. 2 | ||

| -quantile | Alg. 2 | ||

| Logistic regression | Alg. 3 | ||

| Linear regression | Alg. 4 | ||

| Convex minimizer | Alg. 5 |

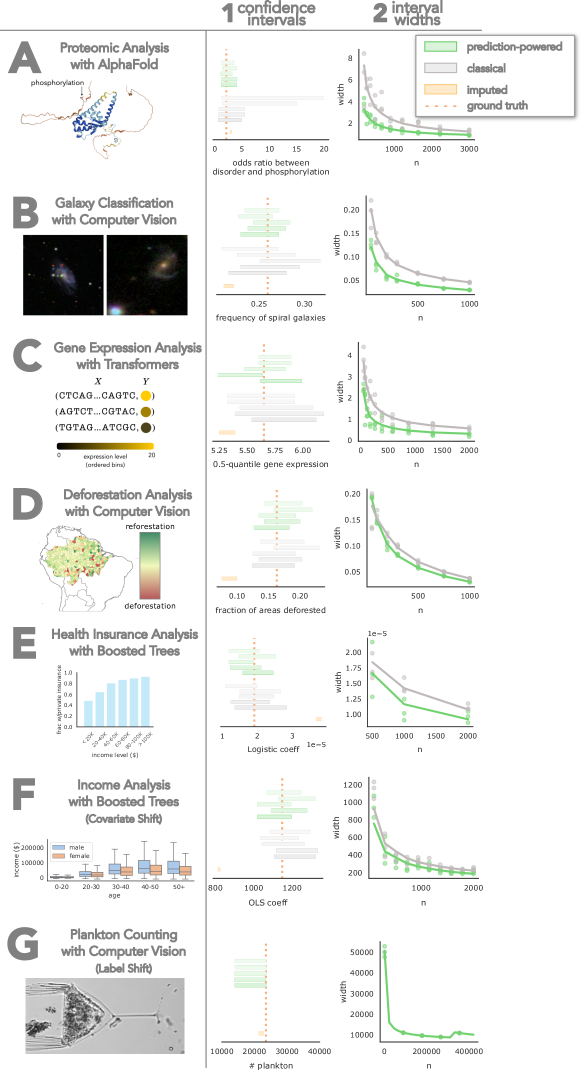

3 Applications

| Problem | Prediction-powered | Classical |

|---|---|---|

| A Proteomic analysis with AlphaFold | ||

| B Galaxy classification with computer vision | ||

| C Gene expression analysis with transformers | ||

| D Deforestation analysis with computer vision | ||

| E Health insurance analysis with boosted trees | ||

| F Income analysis with boosted trees |

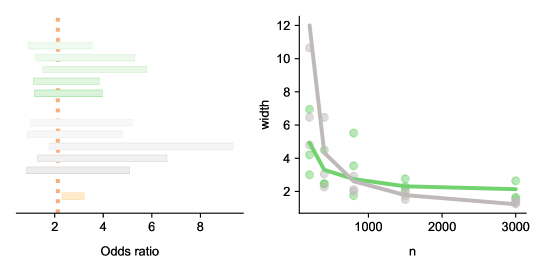

We demonstrate prediction-powered inference on real tasks. In each, we compute a prediction-powered confidence interval for an estimand and compare it to intervals obtained through the classical approach and the imputation approach. In all cases, we show that the imputation approach, which uses machine-learning predictions without accounting for prediction errors, does not contain the true value of the estimand. We compare the widths of the two valid approaches, prediction-powered and classical, as a function of the amount of labeled data used. In addition, we compare the number of labeled examples needed to reject a null hypothesis at level with high probability. Each trial randomly splits the data into a labeled dataset and an unlabeled dataset. The results are given in Figure 1 and Table 2.

See [38] for a Python package implementing prediction-powered inference, which contains code for reproducing the experiments. Each application below comes with a corresponding Jupyter notebook that can be accessed by clicking these icons:

![]() .

We packaged the data in such a way that the reader can run the notebooks on their local machine without downloading large datasets.

.

We packaged the data in such a way that the reader can run the notebooks on their local machine without downloading large datasets.

3.1 Relating protein structure and post-translational modifications

![[Uncaptioned image]](/html/2301.09633/assets/x3.png)

The goal is to characterize whether various types of post-translational modifications (PTMs) occur more frequently in intrinsically disordered regions (IDRs) of proteins [39]. Recently, Bludau et al. [3] studied this relationship on an unprecedented proteome-wide scale by using structures predicted by AlphaFold [1] to predict IDRs, in contrast to previous work which was limited to far fewer experimentally derived structures.

To quantify the association between PTMs and IDRs, the authors applied the imputation approach: they computed the odds ratio between AlphaFold-based IDR predictions and PTMs on a dataset of hundreds of thousands of protein sequence residues [40]. Using prediction-powered inference, we can combine AlphaFold-based predictions together with gold-standard IDR labels to give a confidence interval for the true odds ratio that is statistically valid, in contrast with the interval constructed with the imputation approach, and smaller than the interval constructed using the classical approach.

We use the fact that the odds ratio, , between whether or not a protein residue is part of an IDR, , and whether or not it has a PTM, , can be written as a function of two means:

| (13) |

where and . We therefore proceed by constructing prediction-powered confidence intervals for and , denoted and , respectively. We then propagate and through the odds-ratio formula (13) to get the following confidence interval:

| (14) |

By a union bound, contains with probability at least .

We have 10803 data points from Bludau et al. [3]. For each of 100 trials, we randomly sample points to serve as the labeled dataset and treated the remaining points as the unlabeled dataset for which we do not observe the IDR labels. For all values of , the prediction-powered confidence intervals were smaller than classical intervals; see row A in Figure 1. Often, the classical intervals were large enough that they contained the odds ratio value of one, which means the direction of the association could not be determined from the confidence interval. On the other hand, the imputed confidence interval was far too small and significantly overestimated the true odds ratio. To reject the null hypothesis that the odds ratio is no greater than one, prediction-powered inference required labeled observations, and the classical approach required labeled observations; see row A in Table 2.

3.2 Galaxy classification

![[Uncaptioned image]](/html/2301.09633/assets/x4.png)

The goal is to determine the demographics of galaxies with spiral arms, which are correlated with star formation in the discs of low-redshift galaxies, and therefore, contribute to the understanding of star formation in the Local Universe. A large citizen science initiative called Galaxy Zoo 2 [41] has collected human annotations of roughly 300000 images of galaxies from the Sloan Digital Sky Survey [42] with the goal of measuring these demographics. We seek to explore the use of machine learning to improve the effective sample size and decrease the requisite number of human-annotated galaxies.

We focus on estimating the fraction of galaxies with spiral arms. We have 1364122 labeled galaxy images from Galaxy Zoo 2, from which we simulate labeled and unlabeled datasets as follows. For each of 100 trials, we randomly sample points to serve as the labeled dataset and use the remaining points as the unlabeled dataset. We then use the algorithm for prediction-powered mean estimation to construct intervals. The prediction-powered confidence intervals for the mean are consistently much smaller than the classical intervals while retaining validity, and the imputation strategy fails to cover; see Figure 1, row B. To reject the null hypothesis that the fraction of galaxies with spiral arms is at most 0.2, prediction-powered inference requires labeled examples, and classical inference requires examples; see Table 2, row B.

3.3 Distribution of gene expression levels

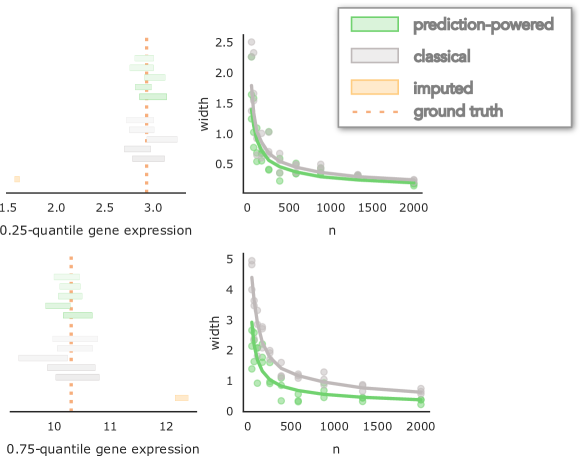

![[Uncaptioned image]](/html/2301.09633/assets/x5.png)

Next, we construct prediction-powered confidence intervals on quantiles that characterize how a population of promoter sequences affects gene expression. Recently, Vaishnav et al. [43] trained a state-of-the-art transformer model to predict the expression level of a particular gene induced by a promoter sequence. They used the model’s predictions to study the effects of promoters—for example, by assessing how quantiles of predicted expression levels differ between different populations of promoters.

Here we focus on estimating different quantiles of gene expression levels induced by native yeast promoters. We have 61150 labeled native yeast promoter sequences from Vaishnav et al. [43], from which we simulate labeled and unlabeled datasets as follows. For each of 100 trials, we randomly sample points to serve as the labeled dataset and use the remaining points as the unlabeled dataset. We then use the second and third row of Table 1 to construct prediction-powered intervals for the median, as well as the 25%- and 75%-quantiles, of the expression levels. The prediction-powered confidence intervals for all three quantiles are much smaller than the classical intervals for all values of . See row C in Figure 1 for the results for the median, and Figure 7 in Appendix H.3 for the other two quantiles. We also evaluate the number of labeled examples required by prediction-powered inference and classical inference, respectively, to reject the null hypothesis that the median gene expression level is at most five. Prediction-powered inference requires examples and classical inference requires examples; see row C in Table 2.

3.4 Estimating deforestation in the Amazon

![[Uncaptioned image]](/html/2301.09633/assets/x6.png)

The goal is to estimate the fraction of the Amazon rainforest lost between 2000 and 2015. Gold-standard deforestation labels for parcels of land are scarce, having been collected largely through field visits, an expensive process impractical for large areas [44]. However, machine-learning predictions of forest cover based on satellite imagery are readily available for the entire Amazon [45].

We begin with 1596 gold-standard deforestation labels for parcels of land in the Amazon. For each of 100 trials, we randomly sample data points to serve as the labeled dataset and use the remaining data points as the unlabeled dataset. We use the first row of Table 1 to construct the prediction-powered intervals. The imputation approach yields a small confidence interval that fails to cover the true deforestation fraction. The classical approach does cover the truth at the expense of a wider interval and, accordingly, diminished inferential power. The prediction-powered intervals are smaller than the classical intervals and retain validity; see row D in Figure1. We also compare the number of gold-standard deforestation labels required by prediction-powered inference and the classical approach to reject the null hypothesis that there is no deforestation. We obtain labels for prediction-powered inference and labels for the classical approach; see row D in Table 2.

3.5 Relationship between income and private health insurance

![[Uncaptioned image]](/html/2301.09633/assets/x7.png)

The goal is to investigate the quantitative effect of income on the procurement of private health insurance using US census data. Concretely, we use the Folktables interface [46] to download census data from California in the year 2019 (378817 individuals).

As the labeled dataset with the health insurance indicator, we randomly sample census entries. The remaining data is used as the unlabeled dataset. We use a gradient-boosted tree [47] trained on the previous year’s data to predict the health insurance indicator in 2019. We construct a prediction-powered confidence interval on the logistic regression coefficient using the fifth row of Table 1. Results in row E in Figure1 show that prediction-powered inference covers the ground truth, the classical interval is wider, and the imputation strategy fails to cover. We also compare the number of gold-standard labels required by prediction-powered inference and the classical approach to reject the null hypothesis that the logistic regression coefficient is no greater than . We observe a significant sample size reduction with prediction-powered inference, which requires labels, whereas classical inference requires labels.

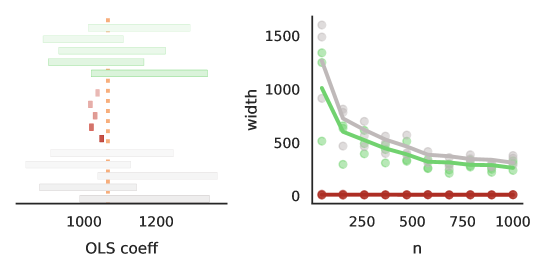

3.6 Relationship between age and income in a covariate-shifted population

![[Uncaptioned image]](/html/2301.09633/assets/x8.png)

The goal is to investigate the relationship between age and income using US census data. We use the same dataset as in the previous experiment, but the features are age and sex, and the target is yearly income in dollars. Furthermore, we introduce a shift in the distribution of the covariates between the gold-standard and unlabeled datasets by randomly sampling the unlabeled dataset with sampling weights 0.8 for females and 0.2 for males.

We used a gradient-boosted tree [47] trained on the previous year’s raw data to predict the income in 2019. We construct a prediction-powered confidence interval on the ordinary least squares regression coefficient using the covariate-shift-robust version of prediction-powered inference from Corollary 4.1. Results in row F in Figure1 show that prediction-powered inference covers the ground truth, the classical interval is wider, and the imputation strategy fails to cover. We also compare the number of gold-standard labels required by prediction-powered inference and the classical approach to reject the null hypothesis that the OLS regression coefficient is no greater than 800. We observe a significant sample size reduction with prediction-powered inference, which requires labels, whereas classical inference requires labels.

3.7 Counting plankton

![[Uncaptioned image]](/html/2301.09633/assets/x9.png)

Assessment of the increases in phytoplankton growth during springtime warming is important for the study of global biogeochemical cycling in response to climate change. We counted the number of plankton observed by the Imaging FlowCytobot [48, 49], an automated, submersible flow cytometry system, at Woods Hole Oceanographic Institution in the year 2014. We have access to data from 2013, which are labeled, and we impute the 2014 data with machine-learning predictions from a state-of-the-art ResNet fine-tuned on all data up to and including 2012. The are images of organic matter taken by the FlowCytobot and the are one of {detritus, plankton}, where detritus represents unspecified organic matter. The labeled dataset consist of 421238 image–label pairs from 2013 and we receive 329832 labeled images from 2014. We use the data from 2014 as our unlabeled data and confirm our results against those that were hand-labeled. The years 2013 and 2014 have a distribution shift, primarily caused by the change in the base frequency of plankton observations with respect to detritus. To apply prediction-powered inference to count the number of plankton recorded in 2014, we use the label-shift-robust technique described in Theorem 4.2. The results in row G in Figure 1 show that prediction-powered inference covers the ground truth and the imputation strategy fails to cover.

4 Extensions

We demonstrate that the framework of prediction-powered inference is applicable beyond inference under i.i.d. observations and convex losses studied in Section 2. First, we provide a strategy for prediction-powered inference when can be expressed as the optimum of any optimization problem, not necessarily a convex one. Then, we discuss prediction-powered inference under certain forms of distribution shift. We end with a brief discussion of a natural estimation strategy suggested by prediction-powered inference.

4.1 Beyond convex estimation

The tools developed in Section 2 were tailored to unconstrained convex optimization problems. In general, however, inferential targets can be defined in terms of nonconvex losses or they may have (possibly even nonconvex) constraints. For such general optimization problems, we cannot expect the condition (4) to hold. In this section we generalize our approach to a broad class of risk minimizers:

| (15) |

where is a possibly nonconvex loss function and is an arbitrary set of admissible parameters. As before, if is not a unique minimizer, our method will return a set that contains all minimizers.

The problem (15) subsumes all previously studied settings. Indeed, when the loss is convex and subdifferentiable and for some —which is the case for all problems previously studied— can be equivalently characterized via the condition (4). In this section we provide a solution that can handle problems of the form (15) in full generality. We note, however, that the solution does not reduce to the one in Section 2 for convex estimation problems, and we expect the method from Section 2 to be more powerful for convex estimation problems with low-dimensional rectifiers.

To correct the imputation approach, we rely on the following rectifier:

| (16) |

Notice that the rectifier (16) is always one-dimensional, while the rectifier (5) was -dimensional.

One key difference relative to the approach of Section 2 is that we have an additional step of data splitting. We need the additional step because, unlike in convex estimation where we know , for general problems we do not know the value of . To circumvent this issue, we estimate by approximating with an imputed estimate on the first unlabeled data points (for simplicity, take to be even). To state the main result, we define

Theorem 4.1 (General risk minimization).

Fix and . Suppose that, for any , we can construct and such that

Let

Then, we have

For example, if the loss takes values in for all , then we can set . The validity of this choice follows by Hoeffding’s inequality.

Mode estimation.

A commonplace inference task that does not fall under convex estimation is the problem of estimating the mode of the outcome distribution. When the outcome takes values in a discrete set , this can be done by using the loss function . A generalization of this approach to continuous outcome distributions is obtained by defining the loss , for some width parameter . The target of inference is thus the point that has the most probability mass in its -neighborhood, . Theorem 4.1 applies directly in both the discrete and continuous cases.

Tukey’s biweight robust mean.

The Tukey biweight loss function is a commonly used loss in robust statistics that results in an outlier-robust mean estimate. It behaves approximately like a quadratic near the origin and is constant far away from the origin. Formally, Tukey’s biweight loss function is given by

where is a user-specified tuning parameter. It is not hard to see that the function is nonconvex and hence not amenable to the analysis in Section 2; however, Theorem 4.1 applies.

Model selection.

Nonconvex risk minimization problems are ubiquitous in model selection. For example, a common model selection strategy is best subset selection, which optimizes the squared loss, , subject to the constraint . Here, is the space of all -sparse vectors for a user-chosen parameter . Even though the loss function is convex, is a nonconvex constraint set and hence we cannot rely on the condition (4) to find the minimizer. However, Theorem 4.1 still applies.

4.2 Inference under distribution shift

In Section 2 we focused on forming prediction-powered confidence intervals when the labeled and unlabeled data come from the same distribution. Herein, we extend our tools to the case where the labeled data comes from and the unlabeled data —which defines the target of inference —comes from , and these are related by either a label shift or a covariate shift. For covariate shift, we handle all estimation problems previously studied; for label shift, we handle certain types of linear problems.

We will write , etc to indicate which distribution the data inside the expectation is sampled from.

4.2.1 Covariate shift

First, we assume that is a known covariate shift of . That is, if we denote by and the relevant marginal and conditional distributions, we assume that . As in previous sections, we consider estimands of the form

| (17) |

Estimands of the form (17) can be related to risk minimizers on using the Radon-Nikodym derivative. In particular, suppose that is dominated by and assume that the Radon-Nikodym derivative is known. Then, we can rewrite (17) as

where . In words, risk minimizers on can simply be written as risk minimizers on , but with a reweighted loss function. This permits inference on the rectifier to be based on data sampled from as before. For concreteness, we explain the approach in detail for convex risk minimizers. Let

| (18) |

where and is a subgradient of as before. A confidence set for the above rectifier suffices for prediction-powered inference on .

Corollary 4.1 (Covariate shift).

Suppose that the problem (17) is a nondegenerate convex estimation problem. Fix and . Suppose that, for any , we can construct and satisfying

Let , where denotes the Minkowski sum. Then,

| (19) |

The same reweighting principle can be used to handle nonconvex risk minimizers as in Section 4.1.

4.2.2 Label shift

Next, we analyze classification problems where the proportions of the classes in the labeled data is different from those in the unlabeled data. This problem has been studied before in the literature on domain adaptation, e.g. by Lipton et al. [50], but our treatment focuses on the formation of confidence intervals. Formally, let be the label space and assume that . We consider estimands of the form

where is a fixed function. For example, choosing for some asks for inference on the proportion of instances that belong to class .

Using an analogous decomposition to the one for mean estimation, we can write

where denotes the distribution of . The quantity can be estimated using the unlabeled data from and the model. Estimating the quantity using observations from will require leveraging the structure of the distribution shift. Central to our analysis will be the confusion matrix

| (20) |

The label-shift assumption implies that , which can be estimated from labeled data sampled from . In particular, we estimate from the labeled data as

| (21) |

Similarly, we can estimate as

Treating and as vectors, notice that we can write , and hence . This leads to a natural estimate of , . Below, we use these quantities to construct a prediction-powered confidence interval for .

Theorem 4.2 (Label shift).

Fix and . Let

where

and denotes the Binomial CDF. Then,

Naturally, the confidence interval becomes more conservative as the number of classes grows. Also, the power of the bound depends on the smallest number of instances observed for a particular class.

4.3 Prediction-powered point estimate

Prediction-powered inference suggests a natural approach to constructing point estimates as well. Define the rectified loss function as

| (22) |

The expected value of the rectified loss is equal to the true population loss that minimizes: . We define the prediction-powered point estimate as the minimizer of the rectified loss:

| (23) |

The confidence intervals formed in Algorithms 1- 5 were implicitly based on the gradient of the rectified loss, . More precisely, they all used as a statistic for testing whether . Notice that the prediction-powered point estimate is always contained in the constructed confidence intervals, since it satisfies .

5 Acknowledgments

We would like to thank Amit Kohli for suggesting the term “rectifier,” Eric Orenstein for helpful discussions related to the WHO-I Plankton dataset, Philip Stark and the San Francisco Department of Elections for helping us find the ballot dataset, and Sherrie Wang for help with the remote sensing experiment. This work was supported in part by the Mathematical Data Science program of the Office of Naval Research under grant number N00014-21-1-2840 and the National Science Foundation Graduate Research Fellowship.

References

- [1] John Jumper, Richard Evans, Alexander Pritzel, Tim Green, Michael Figurnov, Olaf Ronneberger, Kathryn Tunyasuvunakool, Russ Bates, Augustin Žídek and Anna Potapenko “Highly accurate protein structure prediction with AlphaFold” In Nature 596.7873 Nature Publishing Group, 2021, pp. 583–589

- [2] Kathryn Tunyasuvunakool, Jonas Adler, Zachary Wu, Tim Green, Michal Zielinski, Augustin Žídek, Alex Bridgland, Andrew Cowie, Clemens Meyer and Agata Laydon “Highly accurate protein structure prediction for the human proteome” In Nature 596.7873 Nature Publishing Group, 2021, pp. 590–596

- [3] Isabell Bludau, Sander Willems, Wen-Feng Zeng, Maximilian T Strauss, Fynn M Hansen, Maria C Tanzer, Ozge Karayel, Brenda A Schulman and Matthias Mann “The structural context of posttranslational modifications at a proteome-wide scale” In PLoS Biology 20.5 Public Library of Science San Francisco, CA USA, 2022, pp. e3001636

- [4] Inigo Barrio-Hernandez, Jingi Yeo, Jürgen Jänes, Tanita Wein, Mihaly Varadi, Sameer Velankar, Pedro Beltrao and Martin Steinegger “Clustering predicted structures at the scale of the known protein universe” In bioRxiv Cold Spring Harbor Laboratory, 2023, pp. 2023–03

- [5] Carl-Erik Särndal, Bengt Swensson and Jan Wretman “Model Assisted Survey Sampling” Springer Science & Business Media, 1992

- [6] Claes M Cassel, Carl E Särndal and Jan H Wretman “Some results on generalized difference estimation and generalized regression estimation for finite populations” In Biometrika 63.3 Oxford University Press, 1976, pp. 615–620

- [7] Changbao Wu and Randy R Sitter “A Model-Calibration Approach to Using Complete Auxiliary Information From Survey Data” In Journal of the American Statistical Association 96.453 Taylor & Francis, 2001, pp. 185–193 DOI: 10.1198/016214501750333054

- [8] F Jay Breidt and Jean D Opsomer “Model-assisted survey estimation with modern prediction techniques” In Statistical Science 32.2 Institute of Mathematical Statistics, 2017, pp. 190–205

- [9] Roderick JA Little and Donald B Rubin “Statistical Analysis with Missing Data” John Wiley & Sons, 2019

- [10] James M Robins, Andrea Rotnitzky and Lue Ping Zhao “Estimation of regression coefficients when some regressors are not always observed” In Journal of the American Statistical Association 89.427 Taylor & Francis, 1994, pp. 846–866

- [11] James M Robins and Andrea Rotnitzky “Semiparametric efficiency in multivariate regression models with missing data” In Journal of the American Statistical Association 90.429 Taylor & Francis, 1995, pp. 122–129

- [12] Jinbo Chen and Norman E Breslow “Semiparametric efficient estimation for the auxiliary outcome problem with the conditional mean model” In Canadian Journal of Statistics 32.4 Wiley Online Library, 2004, pp. 359–372

- [13] Menggang Yu and Bin Nan “A revisit of semiparametric regression models with missing data” In Statistica Sinica JSTOR, 2006, pp. 1193–1212

- [14] Raymond J Carroll, David Ruppert, Leonard A Stefanski and Ciprian M Crainiceanu “Measurement Error in Nonlinear Models: A Modern Perspective” ChapmanHall/CRC, 2006

- [15] Xiaohong Chen, Han Hong and Elie Tamer “Measurement error models with auxiliary data” In The Review of Economic Studies 72.2 Wiley-Blackwell, 2005, pp. 343–366

- [16] Margaret Sullivan Pepe “Inference using surrogate outcome data and a validation sample” In Biometrika 79.2 Oxford University Press, 1992, pp. 355–365

- [17] Song Xi Chen, Denis H Y Leung and Jing Qin “Information recovery in a study with surrogate endpoints” In Journal of the American Statistical Association 98.464 Taylor & Francis, 2003, pp. 1052–1062

- [18] Larry Wasserman and John Lafferty “Statistical Analysis of Semi-Supervised Regression” In Advances in Neural Information Processing Systems 20 Curran Associates, Inc., 2007 URL: https://proceedings.neurips.cc/paper/2007/file/53c3bce66e43be4f209556518c2fcb54-Paper.pdf

- [19] Anru Zhang, Lawrence D. Brown and T. Cai “Semi-supervised inference: General theory and estimation of means” In The Annals of Statistics 47.5 Institute of Mathematical Statistics, 2019, pp. 2538–2566

- [20] David Azriel, Lawrence D. Brown, Michael Sklar, Richard Berk, Andreas Buja and Linda Zhao “Semi-Supervised Linear Regression” In Journal of the American Statistical Association 117.540 Taylor & Francis, 2022, pp. 2238–2251 DOI: 10.1080/01621459.2021.1915320

- [21] Shanshan Song, Yuanyuan Lin and Yong Zhou “A General M-estimation Theory in Semi-Supervised Framework” In Journal of the American Statistical Association Taylor & Francis, 2023, pp. 1–11

- [22] Abhishek Chakrabortty and Tianxi Cai “Efficient and adaptive linear regression in semi-supervised settings” In Annals of Statistics 46.4, 2018, pp. 1541–1572 DOI: 10.1214/17-AOS1594

- [23] Abhishek Chakrabortty, Guorong Dai and Raymond J Carroll “Semi-Supervised Quantile Estimation: Robust and Efficient Inference in High Dimensional Settings” In arXiv preprint arXiv:2201.10208, 2022

- [24] Abhishek Chakrabortty, Guorong Dai and Eric Tchetgen Tchetgen “A general framework for treatment effect estimation in semi-supervised and high dimensional settings” In arXiv preprint arXiv:2201.00468, 2022

- [25] Yuqian Zhang and Jelena Bradic “High-dimensional semi-supervised learning: in search of optimal inference of the mean” In Biometrika 109.2 Oxford University Press, 2022, pp. 387–403

- [26] Siyi Deng, Yang Ning, Jiwei Zhao and Heping Zhang “Optimal and Safe Estimation for High-Dimensional Semi-Supervised Learning” In arXiv prepring arXiv:2011.14185, 2020

- [27] Jue Hou, Zijian Guo and Tianxi Cai “Surrogate assisted semi-supervised inference for high dimensional risk prediction” In arXiv preprint arXiv:2105.01264, 2021

- [28] Xiaojin Jerry Zhu “Semi-supervised learning literature survey” University of Wisconsin-Madison Department of Computer Sciences, 2005

- [29] Xiaojin Zhu and Andrew B Goldberg “Introduction to semi-supervised learning” In Synthesis Lectures on Artificial Intelligence and Machine Learning 3.1 Morgan & Claypool Publishers, 2009, pp. 1–130

- [30] Hamsa Bastani “Predicting with proxies: Transfer learning in high dimension” In Management Science 67.5 INFORMS, 2021, pp. 2964–2984

- [31] Kan Xu and Hamsa Bastani “Learning across bandits in high dimension via robust statistics” In arXiv preprint arXiv:2112.14233, 2021

- [32] Ye Tian and Yang Feng “Transfer learning under high-dimensional generalized linear models” In Journal of the American Statistical Association Taylor & Francis, 2022, pp. 1–14

- [33] Haotian Lin and Matthew Reimherr “On transfer learning in functional linear regression” In arXiv preprint arXiv:2206.04277, 2022

- [34] Nathan Kallus and Xiaojie Mao “On the role of surrogates in the efficient estimation of treatment effects with limited outcome data” In arXiv preprint arXiv:2003.12408, 2020

- [35] Siruo Wang, Tyler H McCormick and Jeffrey T Leek “Methods for correcting inference based on outcomes predicted by machine learning” In Proceedings of the National Academy of Sciences 117.48 National Acad Sciences, 2020, pp. 30266–30275

- [36] Roger Koenker and Gilbert Bassett Jr “Regression quantiles” In Econometrica: Journal of the Econometric Society JSTOR, 1978, pp. 33–50

- [37] Bradley Efron “Exponential Families in Theory and Practice” Cambridge University Press, 2022

- [38] Anastasios N Angelopoulos, Stephen Bates, Clara Fannjiang, Michael I Jordan and Tijana Zrnic “ppi-py: A Python package for scientific discovery using machine learning”, 2023 URL: https://github.com/aangelopoulos/ppi_py

- [39] Lilia M Iakoucheva, Predrag Radivojac, Celeste J Brown, Timothy R O’Connor, Jason G Sikes, Zoran Obradovic and A Keith Dunker “The importance of intrinsic disorder for protein phosphorylation” In Nucleic acids research 32.3 Oxford University Press, 2004, pp. 1037–1049

- [40] UniProt Consortium “UniProt: a hub for protein information” In Nucleic acids research 43.D1 Oxford University Press, 2015, pp. D204–D212

- [41] Kyle W Willett, Chris J Lintott, Steven P Bamford, Karen L Masters, Brooke D Simmons, Kevin RV Casteels, Edward M Edmondson, Lucy F Fortson, Sugata Kaviraj and William C Keel “Galaxy Zoo 2: detailed morphological classifications for 304 122 galaxies from the Sloan Digital Sky Survey” In Monthly Notices of the Royal Astronomical Society 435.4 Oxford University Press, 2013, pp. 2835–2860

- [42] Donald G York, J Adelman, John E Anderson Jr, Scott F Anderson, James Annis, Neta A Bahcall, JA Bakken, Robert Barkhouser, Steven Bastian and Eileen Berman “The sloan digital sky survey: Technical summary” In The Astronomical Journal 120.3 IOP Publishing, 2000, pp. 1579

- [43] Eeshit Dhaval Vaishnav, Carl G Boer, Jennifer Molinet, Moran Yassour, Lin Fan, Xian Adiconis, Dawn A Thompson, Joshua Z Levin, Francisco A Cubillos and Aviv Regev “The evolution, evolvability and engineering of gene regulatory DNA” In Nature 603.7901, 2022, pp. 455–463

- [44] Eric L Bullock, Curtis E Woodcock, Carlos Souza Jr and Pontus Olofsson “Satellite-based estimates reveal widespread forest degradation in the Amazon” In Global Change Biology 26.5 Wiley Online Library, 2020, pp. 2956–2969

- [45] Joseph O Sexton, Xiao-Peng Song, Min Feng, Praveen Noojipady, Anupam Anand, Chengquan Huang, Do-Hyung Kim, Kathrine M Collins, Saurabh Channan and Charlene DiMiceli “Global, 30-m resolution continuous fields of tree cover: Landsat-based rescaling of MODIS vegetation continuous fields with lidar-based estimates of error” In International Journal of Digital Earth 6.5 Taylor & Francis, 2013, pp. 427–448

- [46] Frances Ding, Moritz Hardt, John Miller and Ludwig Schmidt “Retiring adult: New datasets for fair machine learning” In Advances in Neural Information Processing Systems 34, 2021, pp. 6478–6490

- [47] Tianqi Chen and Carlos Guestrin “Xgboost: A scalable tree boosting system” In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, 2016, pp. 785–794

- [48] Robert J Olson, Alexi Shalapyonok and Heidi M Sosik “An automated submersible flow cytometer for analyzing pico-and nanophytoplankton: FlowCytobot” In Deep Sea Research Part I: Oceanographic Research Papers 50.2 Elsevier, 2003, pp. 301–315

- [49] Eric C Orenstein, Oscar Beijbom, Emily E Peacock and Heidi M Sosik “WHOI-Plankton-a large scale fine grained visual recognition benchmark dataset for plankton classification” In arXiv preprint arXiv:1510.00745, 2015

- [50] Zachary Lipton, Yu-Xiang Wang and Alexander Smola “Detecting and correcting for label shift with black box predictors” In International Conference on Machine Learning, 2018, pp. 3122–3130 PMLR

- [51] Ian Waudby-Smith and Aaditya Ramdas “Estimating means of bounded random variables by betting” In arXiv preprint arXiv:2010.09686, 2020

- [52] Andreas Buja, Lawrence Brown, Richard Berk, Edward George, Emil Pitkin, Mikhail Traskin, Kai Zhang and Linda Zhao “Models as approximations I: Consequences illustrated with linear regression” In Statistical Science 34.4 Institute of Mathematical Statistics, 2019, pp. 523–544

- [53] Halbert White “Using least squares to approximate unknown regression functions” In International Economic Review JSTOR, 1980, pp. 149–170

- [54] Halbert White “A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity” In Econometrica: Journal of the Econometric Society JSTOR, 1980, pp. 817–838

- [55] Aryeh Dvoretzky, Jack Kiefer and Jacob Wolfowitz “Asymptotic minimax character of the sample distribution function and of the classical multinomial estimator” In The Annals of Mathematical Statistics JSTOR, 1956, pp. 642–669

- [56] Pascal Massart “The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality” In The Annals of Probability JSTOR, 1990, pp. 1269–1283

- [57] Clément L Canonne “A short note on learning discrete distributions” In arXiv preprint arXiv:2002.11457, 2020

- [58] Paul Erdős “On the central limit theorem for samples from a finite population” In Publications of the Mathematical Institute of the Hungarian Academy of Sciences 4, 1959, pp. 49–61

- [59] Thomas Höglund “Sampling from a finite population. A remainder term estimate” In Scandinavian Journal of Statistics JSTOR, 1978, pp. 69–71

- [60] Thomas Hamelryck and Bernard Manderick “PDB file parser and structure class implemented in Python” In Bioinformatics 19.17, 2003, pp. 2308–2310

- [61] Kaiming He, Xiangyu Zhang, Shaoqing Ren and Jian Sun “Deep residual learning for image recognition” In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition (CVPR), 2016, pp. 770–778 DOI: 10.1109/CVPR.2016.90

- [62] Diederik P Kingma and Jimmy Ba “Adam: A method for stochastic optimization” In International Conference on Learning Representations, 2014

- [63] Ilya Loshchilov and Frank Hutter “Decoupled weight decay regularization” In arXiv preprint arXiv:1711.05101, 2017

Appendix A Prediction-powered p-values

By relying on the standard duality between confidence intervals and p-values, we can immediately repurpose the presented theory to compute valid prediction-powered p-values.

To formalize this, suppose that we want to test the hull hypothesis , for some set (for example, a common choice when is ). Let be a valid confidence interval. Then, we can construct a valid p-value as

A p-value is valid if it is super-uniform under the null, meaning for all . This is indeed the case for the p-value defined above, because when , we have

The first inequality follows by the definition of and the fact that , and the second inequality follows by the validity of at level . We are implicitly using the fact that when .

The above derivation is a general recipe for deriving p-values from confidence intervals. For the prediction-powered confidence intervals stated in Algorithms 1-5 (derived from Theorem C.1), the corresponding prediction-powered p-value is given by:

Below we state analogues of Algorithms 1-4 when the goal is to compute a prediction-powered p-value.

Corollary A.1 (Mean p-value).

Let be the mean outcome:

Then, the prediction-powered p-value in Algorithm 6 is valid: under the null, .

Corollary A.2 (Quantile p-value).

Let be the -quantile:

Then, the prediction-powered p-value in Algorithm 7 is valid: under the null, .

Corollary A.3 (Logistic regression p-value).

Let be the logistic regression solution:

Then, the prediction-powered p-value in Algorithm 8 is valid: under the null, .

Corollary A.4 (Linear regression p-value).

Fix . Let be the linear regression solution:

Then, the prediction-powered p-value in Algorithm 9 is valid: under the null, .

Appendix B Inference on a finite population

The techniques developed in this paper directly translate to the finite-population setting. Here, we treat as a fixed finite population consisting of feature-outcome pairs, without imposing any distributional assumptions on the data points. Analogously to the i.i.d. setting, we observe all features and a small set of outcomes. Specifically, we assume that we observe , where is a uniformly sampled subset of of size . In this section we adapt all our main results to the finite-population context.

Given a loss function and parameter space , the target estimand is the risk minimizer we would compute if we could observe the whole population:

| (24) |

The following two subsections mirror the results for convex and nonconvex estimation from the main body of the paper. All results in this section are proved essentially identically as their i.i.d. counterparts.

In what follows, we construct prediction-powered confidence sets assuming a valid confidence set around the rectifier (defined below for the finite-population context). The confidence set for the rectifier can be constructed from via a direct application of off-the-shelf results outlined in Appendix E. In particular, in Proposition E.4 we state an asymptotically valid interval for the mean based on a finite-population version of the central limit theorem, and in Proposition E.3 we state a nonasymptotically valid interval for the mean for finite populations due to Waudby-Smith and Ramdas [51]. The only assumption required to apply the latter is that has a known bound valid for all .

B.1 Convex estimation

In the finite-population setting, the mild nondegeneracy condition ensured by convexity takes the form

| (25) |

where is a subgradient of . The rectifier is thus:

| (26) |

Theorem B.1 (Convex estimation, finite population).

Suppose that the convex estimation problem is nondegenerate (25). Fix . Suppose that, for any , we can construct satisfying

Let . Then,

| (27) |

We apply Theorem B.1 in the context of mean estimation, quantile estimation, logistic regression, and linear regression. The target estimand is defined as in (24) with the loss function chosen appropriately, as discussed in Section 2.1. We remark that, just like in the i.i.d. case, the analysis for linear regression follows a more refined approach, as in the proof of Proposition 2.4.

Corollary B.1 (Mean estimation, finite population).

Let be the mean outcome. Fix . Suppose that, for any , we can construct an interval such that , where

Let

Then,

Corollary B.2 (Quantile estimation, finite population).

Let be the -quantile. Fix . Suppose that, for any , we can construct an interval such that , where

Let

Then,

Corollary B.3 (Logistic regression, finite population).

Let be the logistic regression solution. Fix . Suppose that we can construct such that , where

Let

Then,

| (28) |

Corollary B.4 (Linear regression, finite population).

Let be the linear regression solution. Fix . Suppose that we can construct such that , where

Let

Then,

| (29) |

B.2 Beyond convex estimation

We now consider general risk minimizers in the finite-population context. The rectifier is equal to:

| (30) |

Unlike in the i.i.d. setting, there is no need for data splitting because the imputed estimate is deterministic. We let:

Theorem B.2 (General risk minimization, finite population).

Fix . Suppose that, for any , we can construct such that

Let

Then, we have

Appendix C Deferred theoretical details

We state an asymptotic counterpart of Theorem 2.1 that is used to prove the propositions in Section 2.1. Then, we provide nonasymptotically-valid counterparts of the algorithms in Section 2.1. Finally, we state the regularity conditions necessary for the guarantees presented in Section 2.1.

C.1 Asymptotic counterpart of Theorem 2.1

The following is an asymptotic counterpart of Theorem 2.1 that uses the central limit theorem in the confidence set construction. We note the error budget splitting used in Theorem 2.1 is in fact not necessary, but we believe that it facilitates exposition when presenting nonasymptotic guarantees. The asymptotic result below is stated without the splitting of the error budget. The proof is stated in Appendix D.

Theorem C.1 (Convex estimation: asymptotic version).

Suppose that the convex estimation problem is nondegenerate as in (4) and that , for some . Fix . For all , define

Further, denoting by the -th coordinate of , let

for all . Let and . Then,

| (31) |

C.2 Algorithms with nonasymptotic validity

We state nonasymptotically-valid algorithms for prediction-powered mean estimation, quantile estimation, and logistic regression. Like the methods in Section 2.1, the algorithms rely on the abstract recipe from Theorem 2.1. The proofs of validity are included in Appendix D.

The following algorithms rely on any off-the-shelf method for computing confidence intervals for the mean. We choose a variance-adaptive confidence interval for the mean due to Waudby-Smith and Ramdas [51], which we state in Algorithm 13. We opt to present this construction as the default nonasymptotic confidence interval for the mean because of its strong practical performance. The only assumption required to apply Algorithm 13 is that the observations are almost surely bounded within a known interval.

Corollary C.1 (Mean estimation).

Corollary C.2 (Quantile estimation).

Corollary C.3 (Logistic regression).

We note that there exists an analogous nonasymptotic algorithm for linear regression, however we do not recommend it in practice. The reason is that the refined (but asymptotic) analysis used to prove Proposition 2.4 shows that it is sufficient to analyze a one-dimensional rectifier, while directly invoking Theorem 2.1 would require analyzing a -dimensional rectifier and thus yields more conservative intervals.

C.3 Regularity conditions

All algorithms stated in Section 2 rely on confidence intervals derived from the central limit theorem. For such intervals to be asymptotically valid, we require that the two quantities whose mean is being estimated, namely and , have at least the first two moments (see Proposition E.2).

For Proposition 2.4 to hold, we need the same conditions as those required for classical linear regression intervals to cover the target. We note that these conditions are very weak; in particular, it is not required that the true data-generating process be linear or the errors be homoskedastic. See Buja et al. [52] for a detailed discussion. The following are the required conditions, as stated in Theorem 3 of Halbert White’s seminal paper [53]. The data is generated as , , where are mean-zero i.i.d. random draws from some distribution such that and are finite and nonsingular, and , , and are all finite. In addition, we assume that and are measurable. Under these conditions,

where , , , . Moreover, and almost surely.

Appendix D Proofs

D.1 Proof of Theorem 2.1

We show that with probability at least ; that is, with probability at least it holds that

Consider the event . By a union bound, . On the event , we have that

| (32) | ||||

| (33) |

The theorem finally follows by invoking the nondegeneracy condition, which ensures , so we have shown .

D.2 Proof of Theorem C.1

We show that with probability at most in the limit; that is,

For each , the central limit theorem implies that

where is the variance of and is the variance of . Therefore, by Slutsky’s theorem, we get

This in turn implies

| (34) |

where is a consistent estimate of the variance . We take ; this estimate is consistent since the two terms are individually consistent estimates of the respective variances. Now notice that

| (35) |

where the last step follows by the nondegeneracy condition. Putting together (34), (35), and the choice of derived above, and applying a union bound, we get

D.3 Proof of Proposition 2.1

D.4 Proof of Proposition 2.2

D.5 Proof of Proposition 2.3

D.6 Proof of Proposition 2.4

For linear regression, we can derive more powerful prediction-powered confidence intervals than those implied by Theorem 2.1 by exploiting the linearity of the least-squares estimator.

Recall that Theorem C.1 assumes that , for some fraction .

Theorem 3 of White [54] implies that

for appropriately defined coviariance matrices and , where and . With this, we can write the target estimand as .

Combining Theorem 3 of White with Slutsky’s theorem, we get

White also shows that and , as defined in Algorithm 4, are consistent estimates of and , respectively. Therefore, is asymptotically normal and consistent, and we have a consistent estimate of its covariance. In particular,

This means that we can construct asymptotically valid confidence intervals via a normal approximation by choosing width , and this is precisely what Algorithm 4 accomplishes.

D.7 Proof of Theorem 4.1

Define

By the definition of , we have

By applying the validity of the confidence bounds, a union bound implies that with probability we have

Therefore, with probability we have that , as desired.

D.8 Proof of Theorem 4.2

Notice that we can write , where on the right-hand side we are treating and as vectors of length . We can write similar expressions for , etc. Using this notation, by triangle inequality we have

| (36) |

We bound the first term using Hölder’s inequality,

| (37) |

For the second term, we write

| (38) |

In the above equation, the factor on the right, , is exactly equal to , and thus lives on the simplex, which we denote by . Using this fact and Hölder’s inequality,

| (39) |

Next, we have

| (40) |

where indexes the -th column of . This yields the expression

| (41) |

Putting everything together and going back to (36), we have

| (42) |

Since can be evaluated empirically, it remains to bound the distributional distances and .

For the first term, we can simply apply the DKWM inequality [55, 56], which gives

| (43) |

with probability . See [57] for details.

For the second term, , since we only have observations for estimation, we use a more adaptive concentration result. In particular, for each , (conditional on the -th column) follows a binomial distribution with draws and success probability . Therefore, if we let

where denotes the Binomial CDF, then by a union bound:

| (44) |

Combining equations (42), (43) and (44) yields the final result.

D.9 Proof of Corollary C.1

D.10 Proof of Corollary C.2

D.11 Proof of Corollary C.3

Appendix E Confidence intervals for the mean

We give an overview of off-the-shelf confidence intervals for the mean. We state the results for two observation models: first for the i.i.d. sampling model considered in the main body and then for the finite-population setting discussed in Appendix B. In both cases, we provide a construction with nonasymptotic guarantees and one with asymptotic guarantees.

For the nonasymptotic confidence intervals, we rely on the results of Waudby-Smith and Ramdas [51], specifically their Theorem 3 and Theorem 4. We opt for these results because of their strong practical performance, which is primarily driven by variance adaptivity. These results assume that the observed random variables are bounded within a known interval. Without loss of generality we assume that the observations are bounded in (otherwise we can always normalize the observations to ).

For the asymptotic confidence intervals, we rely on the central limit theorem (CLT) and its variant for sampling without replacement; see [58, 59] for classical references.

E.1 Inference with i.i.d. samples

In the following two results, assume that we observe and let .

Proposition E.1 (Nonasymptotic CI: Theorem 3 in [51]).

Assume . Let

| (45) |

For every , define the supermartingale:

| (46) |

Let

| (47) |

Then,

Intuitively, the supermartingale should be thought of as the amount of evidence against being the true mean. That is, being big suggests that is unlikely to be the true mean, so the final confidence set is the collection of all for which the amount of such evidence is small.

For large , computing the intersection in the definition of can be intractable, so we conservatively choose a subsequence of for the computation.

Proposition E.2 (Asymptotic CI: CLT interval).

Assume has a finite second moment. Let

where . Then,

E.2 Inference on a finite population

In the following two results, we assume that there exists a fixed sequence , and we observe , where is a uniform random subset of with cardinality . We let . For the asymptotic result, we assume that is the first entries of an infinite underlying sequence .

Proposition E.3 (Nonasymptotic CI: Theorem 4 in [51]).

Assume . Let

| (48) |

For every , define the supermartingale:

| (49) |

where is the putative mean. Let

| (50) |

Then,

Proposition E.4 (Asymptotic CI: CLT for sampling without replacement).

Let , and . Assume that and have a limit and that for some . Let

Then,

| (51) |

Appendix F Comparison to baseline procedures

We compare prediction-powered inference with two baseline procedures that also combine labeled and unlabeled data in performing statistical inference. The baselines are:

-

1.

Post-prediction inference. We use the post-prediction inference procedure of Wang et al. [35] to estimate ordinary least-squares (OLS) coefficients. The procedure first fits a regression to predict from on the gold-standard dataset. Subsequently, the regression function is used to correct the imputed labels on the unlabeled dataset. Confidence intervals are formed using the as if they were gold-standard data. This procedure has no theoretical guarantees in general and requires strong distributional assumptions on the relationship between and to provide coverage. Our experiments indicate that this approach fails to cover in realistic conditions.

-

2.

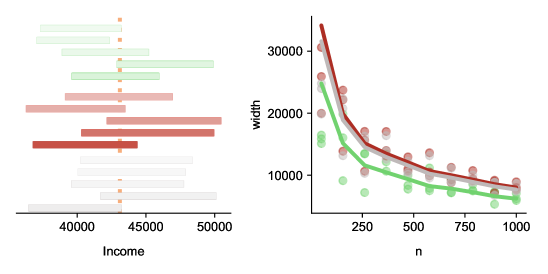

Semi-supervised mean estimation. The semi-supervised mean estimation procedure of Zhang and Bradic [25] involves cross-fitting a (possibly-regularized) linear model on distinct folds of the gold-standard dataset. The average of the model predictions on each unlabeled data point is taken as its corresponding prediction , and the average bias of the models is also computed and used to debias the resulting mean estimate. The formal validity of this approach applies to mean estimation and requires the cross-fitting of linear models; it does not have formal guarantees for more flexible model classes. For this reason, it provides little improvement over the classical confidence interval in our experiments, since the variance reduction possible with linear models is typically limited.

F.1 Experimental protocol

We evaluate the methods on an income prediction task on the same census dataset used for the logistic regression experiments in the main text. In the case of the semi-supervised baseline, the goal is to estimate the mean income in California in the year 2019 among employed individuals using a small amount of labeled data and a large amount of covariates. In the case of the post-prediction inference baseline, the target of inference is the OLS coefficient between age and income. The setup is the same as the logistic regression experiment described in the main text (including the use of the Folktables [46] interface and the gradient-boosted tree [47] as the predictor).

F.2 Comparison to post-prediction inference

Results of the post-prediction inference protocol as compared to the classical and prediction-powered approaches are shown in Figure 2 for the previously-described OLS coefficient between age and income. The procedure does not cover at the proper rate and the intervals are biased.

F.3 Comparison to semi-supervised mean estimation

Results of the semi-supervised mean estimation protocol as compared to the classical and prediction-powered approaches are shown in Figure 3 for the previously described mean income estimation task. The prediction-powered intervals dominate both the semi-supervised intervals and the classical ones in the experiment for all values of .

Appendix G Cases where prediction-powered inference is underpowered

Since standard confidence intervals scale with the standard error of the estimator, prediction-powered inference is powerful when a machine-learning model can provide a reduction in the estimator variance. At a high level, this happens when is large enough relative to and the model is accurate enough. This was the case in all the experiments shown in the main text. This section precisely quantifies what it means to have an accurate enough model and large enough . Corroborating the theory, we present two cases where classical inference outperforms prediction-powered inference: one where the model is not good enough and another where is too small.

G.1 Mathematical derivation

Consider the case of mean estimation, . The widths of the classical confidence interval based on the central limit theorem and the prediction-powered confidence interval based on Algorithm 1 scale with and , respectively, where and are defined in Section 1.3. The classical estimator has variance equal to

The variance of the prediction-powered estimator equals

Therefore, the prediction-powered confidence interval will be tighter when

Since the predictions will typically have a variance that is of the same order as the variance of , if one should not expect prediction-powered inference to help. Gains are expected when . In that case, , and thus prediction-powered inference helps when

In other words, prediction-powered inference gives tighter confidence intervals when the predictions explain away some of the outcome variance.

To gain further intuition, suppose that the outcomes are binary, , where denotes the Bernoulli distribution with parameter . In this case, . For simplicity, suppose that . Then, a direct variance calculation gives and . This allows for a direct comparison of the variances in terms of the outcome bias and model error . For example, when , the model error has to be smaller than for prediction-powered inference to yield smaller intervals; when , meaning the outcomes themselves have low variance, the model error has to be smaller than about . In general, the lower the variance of the outcome, the lower the model error has to be for prediction-powered inference to be helpful.

Putting everything together, the main takeaway is as follows: prediction-powered inference should only be applied when is (preferably substantially) larger than , and when the model has a high enough predictive accuracy to explain away some of the outcome variance. While this derivation focused on mean estimation, a similar intuition holds for other estimation problems.

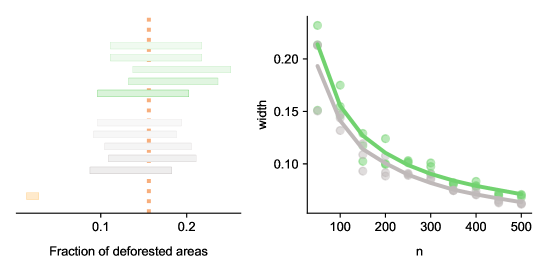

G.2 Inaccurate machine-learning model

We repeat the deforestation analysis experiment from the main text. However, instead of a gradient-boosted tree, we use a linear regression model for prediction. This degrades predictive performance enough that the classical baseline outperforms the prediction-powered approach. See Figure 4 for the results. Due to the reduction of power, for the same null hypothesis tested in the main text, the prediction-powered approach requires data points to reject, while the classical baseline requires .

G.3 Unlabeled dataset is too small

We repeat the AlphaFold-based proteomic analysis from the main text. However, data points are randomly chosen as the unlabeled dataset. The rest of the procedure is performed exactly the same way as described in the main text. The decrease in the unlabeled sample size leads to a reduction in power, and in the regime , the classical baseline outperforms the prediction-powered approach. See Figure 5 for the results. For the same null hypothesis as in the main text, the prediction-powered approach requires data points to reject, while the classical baseline requires .

Appendix H Experimental particulars

H.1 Relating protein structure and post-translational modifications

The predictive model of whether a sequence position is in an intrinsically disordered region (IDR), , is a logistic regression model that maps the relative solvent-accessible surface area (RSA) of each position, computed based on the AlphaFold-predicted structure using Bio.PDB [60], to a probability that the position is in an IDR. Following Bludau et al. [3], the RSA was locally smoothed with a window of , or amino acids, and a sigmoid function was used to predict disorder from this smoothed RSA quantity. To fit the sigmoid, we used the data in [3] that had IDR labels but no PTM labels. The smoothing window size used for the final model was the value that resulted in the lowest variance of the bias, , on this data.