Empirical Bayes When Estimation Precision Predicts Parameters

Abstract.

Empirical Bayes shrinkage methods usually maintain a prior independence assumption: The unknown parameters of interest are independent from the known precision of the estimates. This assumption is theoretically questionable and empirically rejected, and imposing it inappropriately may harm the performance of empirical Bayes methods. We instead model the conditional distribution of the parameter given the standard errors as a location-scale family, leading to a family of methods that we call close. We establish that (i) close is rate-optimal for squared error Bayes regret, (ii) squared error regret control is sufficient for an important class of economic decision problems, and (iii) close is worst-case robust. We use our method to select high-mobility Census tracts targeting a variety of economic mobility measures in the Opportunity Atlas (Chetty et al., 2020; Bergman et al., 2023). Census tracts selected by close are more mobile on average than those selected by the standard shrinkage method. For 6 out of 15 mobility measures considered, the gain of close over the standard shrinkage method is larger than the gain of the standard method over selecting Census tracts uniformly at random.

JEL codes. C10, C11, C44

Keywords. Empirical Bayes, regret, heteroskedasticity, nonparametric maximum likelihood, Opportunity Atlas, Creating Moves to Opportunity

1. Introduction

After obtaining noisy estimates for many parameters of interest, applied economists increasingly use empirical Bayes methods to shrink these estimates, in hopes to improve subsequent policy decisions.111Empirical Bayes methods are appropriate whenever many parameters for heterogeneous populations are estimated in tandem. For instance, value-added modeling, where the parameters are latent qualities for different service providers (e.g. teachers, schools, colleges, insurance providers, etc.), is a common thread in several literatures (Angrist et al., 2017; Mountjoy and Hickman, 2021; Chandra et al., 2016; Doyle et al., 2017; Hull, 2018; Einav et al., 2022; Abaluck et al., 2021; Dimick et al., 2010). Our application (Bergman et al., 2023) is in a literature on place-based effects, where the unknown parameters are latent features of places (Chyn and Katz, 2021; Finkelstein et al., 2021; Chetty et al., 2020; Chetty and Hendren, 2018; Diamond and Moretti, 2021; Baum-Snow and Han, 2019). Empirical Bayes methods are also applicable in studies of discrimination (Kline et al., 2022; Rambachan, 2021; Egan et al., 2022; Arnold et al., 2022; Montiel Olea et al., 2021), meta-analysis (Azevedo et al., 2020; Meager, 2022; Andrews and Kasy, 2019; Elliott et al., 2022; Wernerfelt et al., 2022; DellaVigna and Linos, 2022; Abadie et al., 2023), and correlated random effects in panel data (Chamberlain, 1984; Arellano and Bonhomme, 2009; Bonhomme et al., 2020; Bonhomme and Manresa, 2015; Liu et al., 2020). In terms of policy decisions driven by empirical Bayes posterior means, Gilraine et al. (2022) report that by the end of 2017, 39 states require that teacher value-added measures—typically, empirical Bayes posterior means of teacher performance—be incorporated into the teacher evaluation process. The textbook empirical Bayes method assumes prior independence—that the precisions of the noisy estimates do not predict the underlying unknown parameters. However, prior independence is theoretically questionable and empirically rejected in many contexts,222To see this, take value-added modeling as an example. The precision of value-added estimates is usually a function of the number of customers associated with a service provider (e.g. number of students for a teacher). It is possible that customers select into higher quality providers. It is also possible that congestion effects render more popular service providers worse. These channels predict that the sample sizes for a provider are associated with latent value-added, and the direction of association depends on the interplay of the selection and congestion effects. Section A.5 outlines a formal discrete choice model to illustrate these effects. and inappropriately imposing it can harm empirical Bayes decisions. Motivated by these concerns, this paper introduces empirical Bayes methods that relax prior independence.

To be concrete, our primary empirical example (Bergman et al., 2023) computes empirical Bayes posterior means for economic mobility estimates published in the Opportunity Atlas (Chetty et al., 2020). Throughout this paper, measures of economic mobility are defined as certain average outcomes of children from low-income households.333There are various definitions of economic mobility provided by Chetty et al. (2020), discussed later in the paper. They are all measures of economic outcomes for children from low-income households (households at the 25th percentile of the national income distribution). One example is the probability that a Black person have incomes in the top 20 percentiles, whose parents have household incomes at the 25th percentile. Here, prior independence is the assumption that the standard errors of these noisy mobility estimates do not predict true economic mobility. However, Census tracts with more low-income households naturally have more precise estimates for outcomes of low-income children—and hence more precise estimates of economic mobility. These tracts also tend to have lower underlying economic mobility due to, for one, residential segregation (Chyn and Katz, 2021). Consequently, the standard errors of the estimates and true economic mobility are positively correlated.

Bergman et al. (2023) aim to select high mobility Census tracts by screening on empirical Bayes posterior mean estimates. Inappropriately imposing prior independence may lead to poor selections: Using a validation procedure that we develop, for several measures of economic mobility where prior independence is severely violated, we find that screening on conventional empirical Bayes posterior means selects less economically mobile tracts, on average, than screening on the unshrunk estimates.444Fortunately, for the measure of economic mobility (mean income rank pooling over all demographic groups whose parents are at the 25th percentile of household income) used in Bergman et al. (2023), screening on these empirical Bayes posterior means still outperforms screening on the raw estimates. In contrast, screening on empirical Bayes posterior means computed by our method selects substantially more mobile tracts.

Section 2 introduces our method in detail. To describe our method, let be some noisy estimates for some parameters , with standard errors , over heterogeneous populations . In our empirical application, are published in the Opportunity Atlas for each Census tract and are designed to measure true economic mobility . Motivated by the central limit theorem applied to the underlying micro-data, is approximately Gaussian:

If is random, then oracle Bayes decisions based on the posterior distribution are optimal. Empirical Bayes emulates such optimal decisions by estimating the oracle prior distribution of . Assuming prior independence—that is, —simplifies this estimation problem. However, empirical Bayes methods based on this assumption have poor performance when it fails to hold.

We relax prior independence by modeling the prior distribution flexibly. We model as a conditional location-scale family, controlled by -dependent location and scale hyperparameters and a -independent shape hyperparameter. Under this assumption, different values of the standard errors translate, compress, or dilate the distribution of the parameters , but the underlying shape of does not vary. This model generalizes prior independence: Prior independence is the special case where the unknown location and scale parameters are constant functions of .

This conditional location-scale assumption leads naturally to a family of empirical Bayes methods that we call close. Since the unknown prior distribution is fully described by its location, scale, and shape hyperparameters, close estimates these parameters flexibly and plugs the estimated parameters into downstream decision rules. There are different choices of estimators for these hyperparameters. Our preferred specification of close uses nonparametric maximum likelihood (npmle, Kiefer and Wolfowitz, 1956; Koenker and Mizera, 2014) to estimate the unknown shape of the prior distribution . We find that close-npmle inherits the favorable computational and theoretical properties for npmle (Soloff et al., 2021; Jiang, 2020; Polyanskiy and Wu, 2020).

There are four theoretical contributions in this paper. Section 3 contains the first three, which are statistical guarantees on close-npmle. First and foremost, 1 and 2 establish that close-npmle is minimax rate-optimal, up to logarithmic factors and under the conditional location-scale assumptions, for Bayes regret in squared error. Bayes regret is the gap between the expected loss of decision rules from close-npmle and that from an oracle Bayesian who knows the true distribution of . Squared error Bayes regret is a standard performance metric for empirical Bayes (Jiang and Zhang, 2009). This result thus shows that close-npmle emulates the oracle as well as possible, at least in terms of squared error loss.

Second, to connect squared error regret to policy problems in economics, Theorem 3 shows that the Bayes regret in squared error dominates the Bayes regret for two ranking-related decision problems, including the problem of selecting high-mobility tracts encountered by Bergman et al. (2023). Thus, regret guarantees for squared error imply guarantees for these decision problems, since these latter problems are easier than estimation in squared error. Third, to assess robustness of close to the location-scale modeling assumption, 2 establishes that close-npmle is worst-case robust: We show that a population version of the procedure has bounded worst-case Bayes risk as a multiple of the minimax risk, when the true distribution of is adversarially chosen, without imposing the conditional location-scale assumption.

Fourth, to provide an honest assessment of close-npmle in a given dataset, Section 4.3 extends the coupled bootstrap in Oliveira et al. (2021) to produce a simple validation procedure. If one had access to the micro-data, one could split the data into training and testing samples, compute decision rules on the training sample, and use the testing sample to evaluate performance. This validation procedure emulates this sample-splitting without needing access to the underlying micro-data and provides unbiased loss estimates for any decision rules over a class of loss functions. In particular, this procedure allows practitioners to evaluate whether close provides improvements for their setting by comparing loss estimates for close and those for the standard shrinkage procedure.

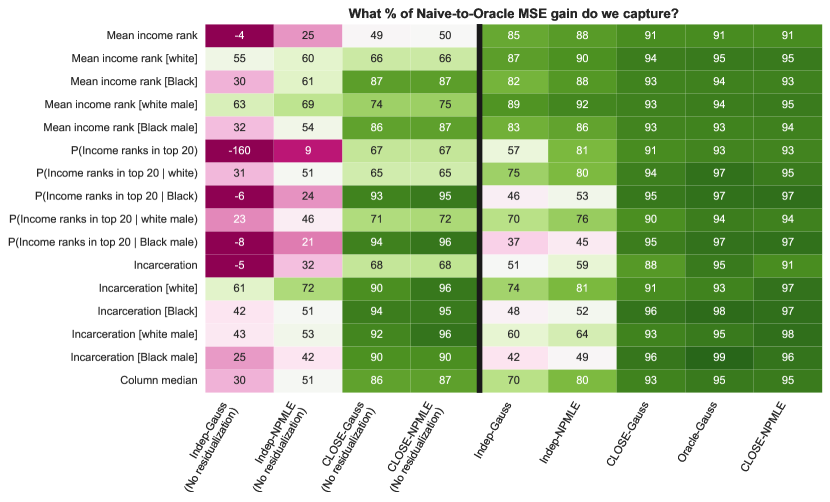

Section 4 also provides a practitioner-oriented discussion of our methods. To illustrate our method, Section 5 applies close to two empirical exercises, building on Chetty et al. (2020) and Bergman et al. (2023). The first exercise is a calibrated Monte Carlo simulation, in which we have access to the true distribution of . We find that close-npmle has mean-squared error (MSE) performance close to that of the oracle posterior, uniformly across the 15 measures of economic mobility that we include. For all 15 measures, close-npmle captures over 90% of possible MSE gains relative to no shrinkage, whereas conventional shrinkage captures only 70% on average.

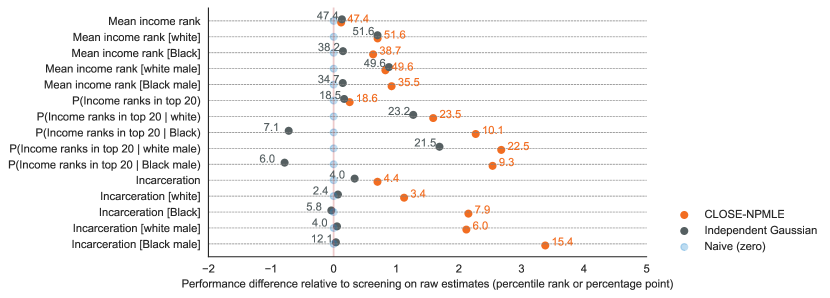

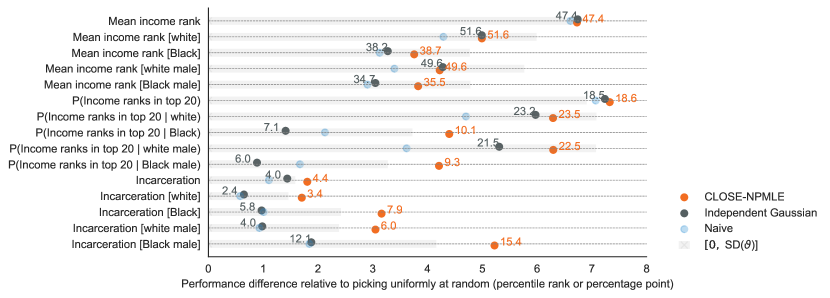

The second exercise uses the coupled bootstrap procedure to evaluate the performance of various procedures for selecting high-mobility Census tracts. In a hypothetical version of Bergman et al. (2023), we find that close-npmle selects more economically mobile tracts than the conventional shrinkage method, in terms of the average mobility of selected tracts. These improvements of close-npmle over the standard method are comparable to or larger than the value of basic empirical Bayes—that is, the improvements the standard method delivers over screening on the raw estimates directly. Therefore, if one finds using the standard empirical Bayes method a worthwhile methodological investment, then the additional gain of using close is likewise meaningful. For 6 out of 15 measures of mobility, close even improves over the standard method by a larger amount than the value of data—that is, the amount by which the standard method improves over selecting Census tracts completely at random. These improvements are substantial since the value of data is likely economically significant if the mobility estimates are at all useful for the policy problem.

2. Model and proposed method

We observe estimates and their standard errors for parameters , over populations . We maintain throughout that the estimates are conditionally Gaussian and independent across :

The Normality in (2) is motivated by the central limit theorem applied to the underlying micro-data that generate the estimates . That is, let denote the underlying sample size in the micro-data which generate . Standard large-sample approximation implies

as .555Since is estimated as well, one might object to treating as a known population quantity in (2). Note that the approximation (2) holds for both the estimated and its population counterpart; thus, we can motivate the approximation (2) using the estimated standard error . Alternatively, note that the estimation error in is typically of order , which is smaller than that in , which is of order .

We also assume that the population parameters are themselves sampled from some joint distribution. Throughout this paper, we treat as fixed or conditioned upon. We assume that are independently and identically drawn,666Combined with the independence assumption of across , we assume that are independently drawn unconditionally. The independence assumption for the estimates conditional on holds when the underlying micro-data for different estimates are sampled independently. This assumption does not precisely hold for the Opportunity Atlas, but the correlation between and , which arises from individuals who move between tracts, is likely small. In any case, the widely applied standard empirical Bayes method maintains such an assumption, as do recent papers by Mogstad et al. (2020) and Andrews et al. (2023). The independence assumption for the parameters is perhaps controversial, especially for spatial contexts (Müller and Watson, 2022). We discuss an interpretation of the procedure when we erroneously assume that and/or are independent across in Section A.6. but the conditional distribution may be different across :

We use to denote the marginal distribution of and we use to denote the joint distribution of the ’s conditional on the ’s, , which is fully described by . We refer to as the oracle Bayes prior.

Popular empirical Bayes methods impose more structure than (2).777The literature in empirical Bayes methods is vast. For theoretical and applied results of particular interest to economists, see the recent lecture by Gu and Walters (2022) and references therein. Efron (2019) and its discussions and rejoinders are excellent introductions to the statistics literature on empirical Bayes. The standard parametric empirical Bayes method additionally models as identical across and Gaussian (Morris, 1983): i.e., for all , . Henceforth, we shall refer to this method as independent-gauss. On the other hand, state-of-the-art empirical Bayes methods (Jiang, 2020; Soloff et al., 2021; Jiang and Zhang, 2009; Koenker and Gu, 2019; Gilraine et al., 2022), where priors are estimated by npmle, assume that the marginal distributions are equal to some common, unknown distribution , not necessarily Gaussian: i.e., for all , . We refer to this method as independent-npmle. The “independent” here emphasizes that these methods assume prior independence: , under the prior .

We relax prior independence by instead modeling as a location-scale family,888We explore alternatives to the location-scale model in Section A.7. We find that no alternative provides a free-lunch improvement over our assumptions. indexed by unknown hyperparameters :

| (2.4) |

where is normalized to have zero mean and unit variance. Under (2.4), different values of may translate, compress, or dilate the conditional distribution of via the location parameter and the scale parameter , but the conditional distributions can be normalized to take the same shape . As a preview, since the oracle prior distribution is fully described by the hyperparameters , our method, close, proposes to estimate with the estimate , derived from estimated hyperparameters . close then produces empirical Bayes decision rules with respect to the estimated prior . Since Bayes decisions rules with respect to the oracle prior are optimal, we expect Bayes decisions with respect to the estimated prior are approximately optimal.

Before describing close in detail in Section 2.3, it is useful to first define a few decision-theoretic primitives, describe empirical Bayes in generality, introduce some decision problems, and discuss the plausibility and consequences of the prior independence assumption. We do so in Sections 2.1 and 2.2.

2.1. Oracle Bayes and empirical Bayes decisions

Under the sampling model (2) and (2), empirical Bayes offers a general recipe for decision-making. Let be a decision rule mapping the data to actions. Let denote a loss function mapping actions and parameters to a scalar. Let denote the frequentist risk associated with the loss function , which integrates over the randomness in , keeping fixed. Finally, let be the Bayes risk of under , which additionally integrates over the conditional distribution .999Since is kept fixed throughout, we suppress their appearances in .

The decision rule that minimizes is the Bayes rule with respect to the oracle Bayes prior (Lehmann and Casella, 2006). At each realization of , this oracle Bayes rule picks an action that minimizes the posterior expected loss:

Empirical Bayesians seek to approximate the oracle Bayes rule , most commonly by learning relevant features of from the data (Efron, 2014). With an estimate for , it is natural to construct an empirical Bayes decision rule by plugging into (2.1):101010To emphasize the distinction between the true expectation with respect to the data-generating process (2) and a posterior mean taken with respect to some possibly estimated measure , we shall use to refer to the former and to refer to the latter. Subscripts typically make the distinction clear as well. Specifically, where is the probability density function of a standard Gaussian.

A natural metric of success for the empirical Bayesian is thus the gap between the Bayes risks of and . We refer to this quantity as Bayes regret:

where the right-hand side integrates over the randomness in , and, by extension, . If an empirical Bayes method achieves low Bayes regret, then it successfully imitates the decisions of the oracle Bayesian, and its decisions are thus approximately optimal. Our theoretical results focus on bounding Bayes regret for close.111111Bayes regret is likewise the focus of the literature in empirical Bayes that we build on (Jiang, 2020; Soloff et al., 2021). On the other hand, other optimality criteria are also considered. For instance, Kwon (2021), Xie et al. (2012), Abadie and Kasy (2019), and Jing et al. (2016) propose methods that use Stein’s Unbiased Risk Estimate (SURE) to select hyperparameters for a class of shrinkage procedures. A common thread of these approaches is that they seek optimality in terms of the frequentist risk —which is stronger than controlling the Bayes risk —but limit attention to squared error and to a restricted class of methods.

Next, we introduce a few concrete decision problems by specifying the actions and loss functions and state the corresponding oracle Bayes and empirical Bayes decision rules.

Decision Problem 1 (Squared-error estimation of ).

The canonical statistical problem (Robbins, 1956) is estimating the parameters under mean-squared error (MSE). That is, the action collects estimates for parameters , evaluated with MSE:

The oracle Bayes decision rule here is simply the posterior mean under , denoted by :

Next, we describe two problems that are likely more relevant for policy-making, such as replacing low value-added teachers and recommending high economic mobility tracts (Gilraine et al., 2022; Bergman et al., 2023).121212We analyze these problems from a decision-theoretic perspective, under the sampling assumption (2). For a different and complementary perspective in terms of conditional-on- frequentist inference on ranks, see Mogstad et al. (2020, 2023). For additional ranking-related decision problems, see Gu and Koenker (2023).

Decision Problem 2 (Utility maximization by selection).

We refer to the following problem as utility maximization by selection. Suppose , where is a selection decision for population . For each population, selecting that population has benefit and known cost . The decision maker wishes to maximize utility (i.e., negative loss):

The oracle Bayes rule selects all populations whose posterior mean benefit exceeds the selection cost :

One natural empirical Bayes decision rule replaces with , following (2.1).

In a context where the parameters are conditional average treatment effects for a particular covariate cell, , and are treatment decisions, this problem is an instance of welfare maximization by treatment choice (Manski, 2004; Stoye, 2009; Kitagawa and Tetenov, 2018; Athey and Wager, 2021). In this setting, is a decision to treat individuals with covariate values in the th cell. The average benefit of treating these individuals is their conditional average treatment effect , and the cost of treatment is .131313The literature on treatment choice uses a different notion of regret compared to this paper (based on rather than ).

Decision Problem 3 (Top- selection).

We refer to the following problem as top- selection. Similar to utility maximization by selection, suppose consists of binary selection decisions, with the additional constraint that exactly populations are chosen: . The decision maker’s utility is the average of the selected set:

Oracle Bayes selects the populations corresponding to the largest posterior means (breaking ties arbitrarily):

Again, the empirical Bayes recipe (2.1) suggests replacing with the estimate .

The utility function (3) rationalizes the widespread practice of screening based on empirical Bayes posterior means. For instance, this objective may be reasonable for rewarding the top 5% of teachers or replacing the bottom 5%, according to value-added (Gilraine et al., 2020; Chetty et al., 2014; Kane and Staiger, 2008; Hanushek, 2011). In Bergman et al. (2023), where housing voucher holders are incentivized to move to Census tracts selected according to economic mobility, (3) represents the expected economic mobility of a mover if they move randomly to one of the selected tracts.141414Our theoretical results in Section 3.2 can accommodate a slightly more general decision problem, which allows for an expected mobility interpretation for movers who do not move uniformly randomly.

To estimate and implement the empirical Bayes decision (2.1), it is often convenient to assume prior independence. We turn to its plausibility next.

2.2. Plausibility of prior independence

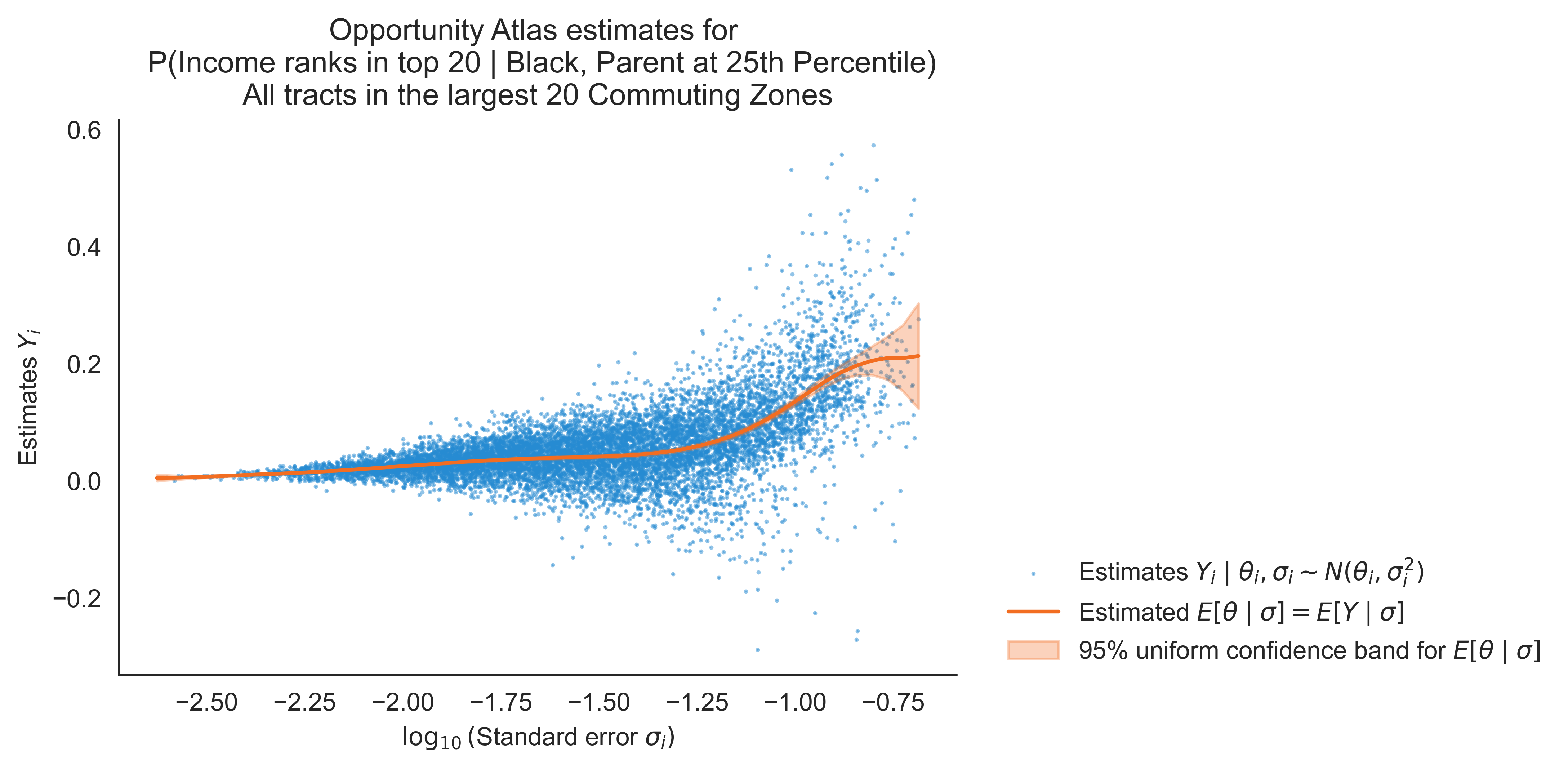

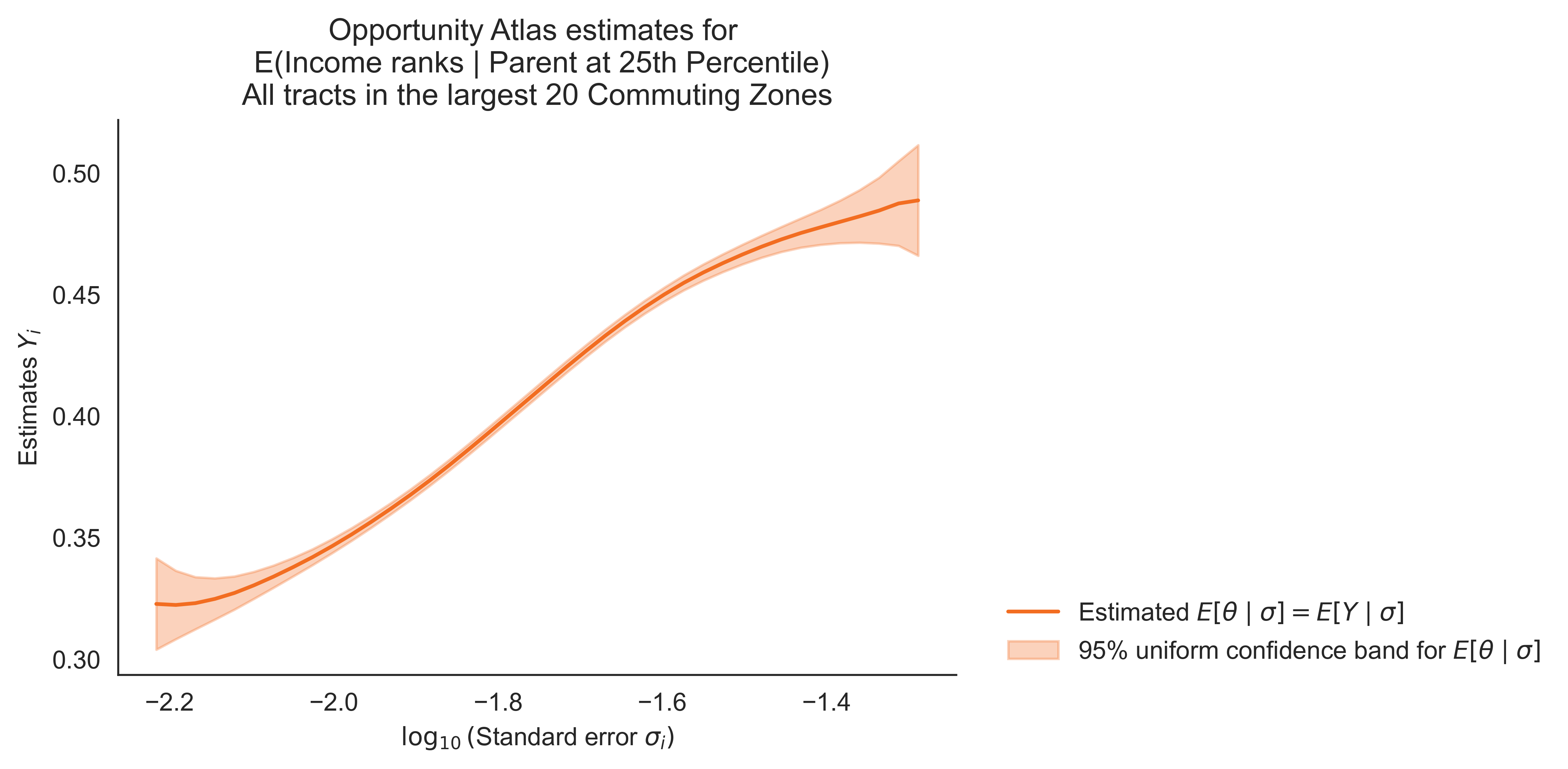

To be concrete, we start by considering prior independence in the context of estimating tract-level economic mobility (Chetty et al., 2020). As a running example, let us define economic mobility as the probability of family income ranking in the top 20 percentiles of the national income distribution, for a Black individual growing up in tract whose parents are at the 25th national family income percentile. Note that the standard error for an estimate of is then related to the implicit sample size—the number of Black households at the 25th income percentile in tract .

Notes.

All tracts within the largest 20 Commuting Zones (CZs) are shown. Due to the regression specification in Chetty et al. (2020), point estimates of do not always lie within . The orange line plots nonparametric regression estimates of the conditional mean , estimated via local linear regression with automatic bandwidth selection implemented in Calonico et al. (2019). The orange shading shows a 95% uniform confidence band, constructed by the max- confidence set over 50 equally spaced evaluation points. The confidence band excludes any constant function. See Appendix G for details on estimating conditional moments of given . ∎

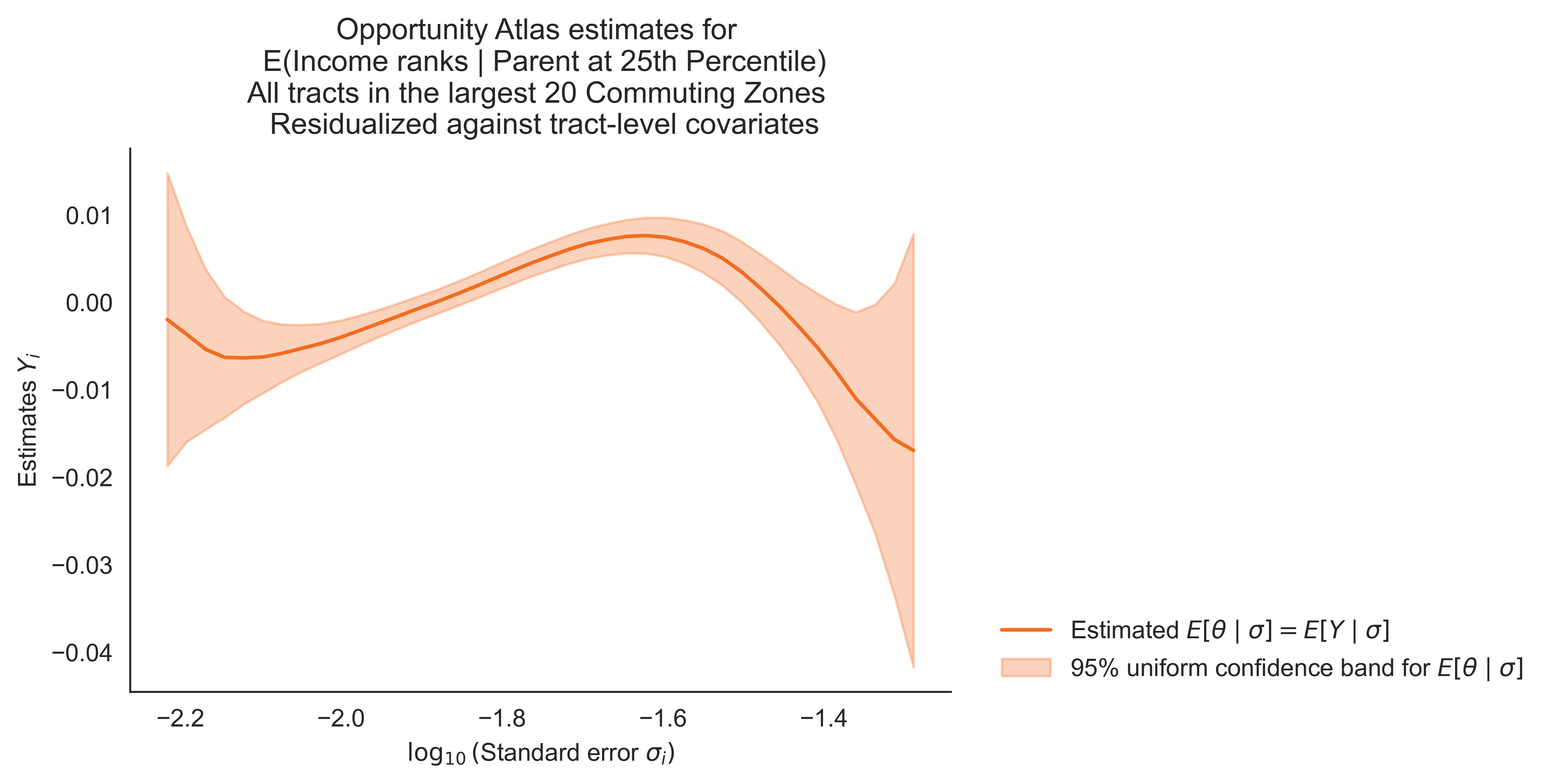

As an empirical matter, prior independence is readily rejected for this measure of economic mobility. Figure 1 plots against , as well as a nonparametric regression estimate of . If were independent of , then the true conditional mean function, , should be constant. Figure 1 shows the contrary—tracts with more imprecisely estimated tend to have higher economic mobility.151515Moreover, remains predictive of even if we residualize against a vector of tract-level covariates (Figure B.9). Prior independence is also readily rejected for the mobility measure used in Bergman et al. (2023), but its violation is not as severe once adjusted for tract-level covariates (Section 5 and Figure B.8). This correlation is in part through the following channel. Since is an average outcome for children from poor Black families, tracts with more poor Black families tend to have more precise estimates of .161616Since is also the mean of a binary outcome, the asymptotic variance of its estimators also depend on mechanically on . However, they also tend to have lower economic mobility due to the pernicious effects of residential segregation.

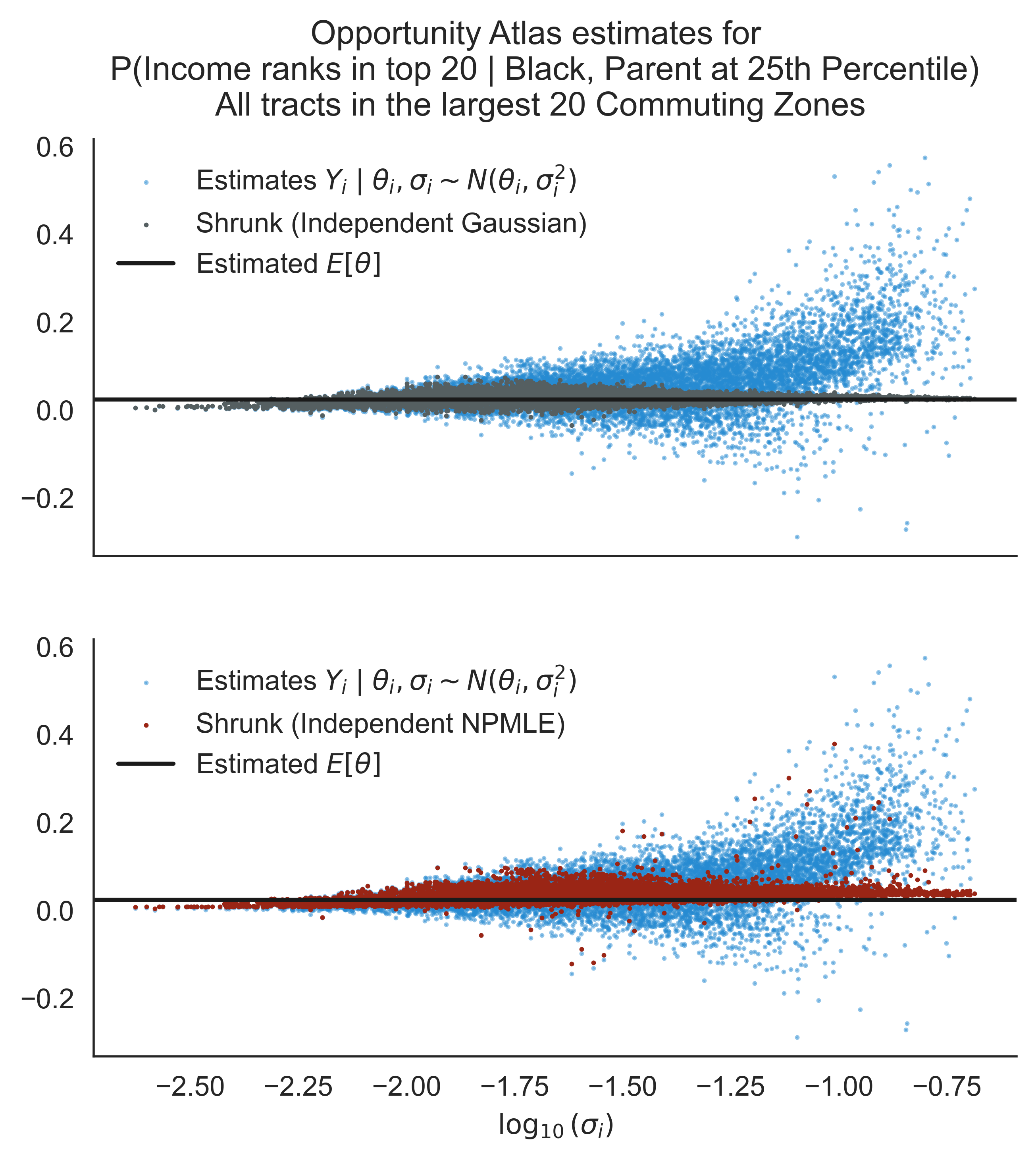

Notes.

The top panel shows posterior mean estimates with independent-gauss shrinkage. The bottom panel shows the same with independent-npmle shrinkage. In the top panel, the estimates for are weighted by the precision (as in Bergman et al., 2023). Under , this weighting scheme improves efficiency of the -estimates by underweighting noisier . ∎

What happens if we apply empirical Bayes methods that assume prior independence here? Figure 2 overlays the empirical Bayes posterior means, computed from independent-gauss and independent-npmle, on the -against- scatterplot. independent-gauss (1) shrinks estimates towards a common estimated mean , depicted as the black line in Figure 2(a), and shrinks noisier estimates more aggressively. When and are positively correlated—as is the case in Figure 2, estimated posterior means under independent-gauss systematically undershoot for populations with imprecise estimates. Similarly, independent-npmle suffers from the same undershooting, though less so.

This undershooting is particularly problematic for Decision Problem 2 and Decision Problem 3. In these problems, the tracts one would like to select are exactly those with high imprecision , owing to the positive correlation between and . By shrinking these tracts severely towards the estimated common mean, empirical Bayes under prior independence makes suboptimal selections that may underperform screening directly based on .171717This latter point is similarly made in Mehta (2019), though for different loss functions.

We end this section with a discussion on the plausibility of prior independence in other economic contexts.

Remark 1 (Plausibility of prior independence).

To describe the general channels underlying the potential failure of prior independence, let us write (2) in a different form

Expression (1) decomposes the (estimated) standard error into the underlying sample size in the micro-data and the asymptotic variance of the (properly scaled) estimator. Both and may predict in a variety of empirical contexts.

Let us start with the implicit sample sizes . It is possible that is in part determined by , which we loosely term selection. In value-added modeling, is the number of observations associated with a provider. It is possible that selects on the latent quality of that provider. For instance, Chandra et al. (2016) find “higher quality hospitals have higher market shares and grow more over time.” If market share and hospital size relate to the underlying sample size (e.g. number of patient observations) for estimating hospital value-added, then this suggests non-independence between and . As another example, in meta-analysis, suppose represents the treatment effect of some intervention . If researchers power studies based on informative priors for , then we should observe that interventions with larger conjectured effect sizes have smaller sample sizes .

Another channel driving the correlation between and can be loosely termed congestion, where affects the latent feature . For our primary application, represents the number of poor and minority households in a Census tract, and represents underlying economic or social mobility. Places with more poor and minority households experience white flight and residential segregation (Cutler et al., 1999; Agan and Starr, 2020; Kain, 1968), develop oppressive institutions (Derenoncourt, 2022; Alesina et al., 2001), and worse public goods provision (Laliberté, 2021; Jackson and Mackevicius, 2021; Colmer et al., 2020). These factors contribute to lower economic mobility . Section A.5 contains more examples of violation of prior independence and outlines a model in which selection and congestion effects drive correlation between and .

There are also cases where the asymptotic variance is correlated with . In the context of intergenerational mobility, a parallel literature on the Great Gatsby curve (reviewed by Durlauf et al., 2022) seeks to explain a negative relationship between inequality—which contributes to —and intergenerational mobility. For instance, Becker et al. (2018) posit that parental investment and parental human capital are complements in a child’s skill formation. As a result, parents with higher human capital—and more wealth—invest disproportionately more in their children’s education than parents with lower human capital. This process then produces both inequality and low economic mobility. In other words, places that are more unequal (higher ) have lower mobility .

2.3. Conditional location-scale relaxation of prior independence

Having argued that (i) prior independence is theoretically suspect and empirically rejected and that (ii) inappropriately imposing it can harm empirical Bayes decision rules, we propose the conditional location-scale model (2.4) as a relaxation.181818In the presence of covariates —which do not predict the noise in , —the assumption (2.4) can be modified to accommodate additional covariates as well. We provide additional discussion of covariates in Section A.6.2. Here, we state (2.4) equivalently as

| (2.11) |

To estimate under this assumption, it suffices to estimate the unknown hyperparameters . Expression (2.11) makes clear that, under the location-scale model, the transformed parameter is independent from with distribution . Applying the same transformation to the data yields transformed estimates and its standard errors , which obey an analogue of the Gaussian location model (2) in which prior independence holds:

Thus, it is natural to use empirical Bayes methods that assume prior independence on these transformed quantities to estimate .

This strategy is still infeasible, since the transformation depends on unknown location and scale parameters . Fortunately, these are readily estimable from the data , as they only require conditional expectations and variances of given :

We then form the estimated transformed data as

We apply empirical Bayes methods assuming prior independence on . This leads to a family of empirical Bayes strategies that we refer to as conditional location-scale empirical Bayes, or close:

-

Nonparametrically estimate .191919Both are feasible with nonparametric regression methods. For instance, in our empirical exercises, we find that local polynomial regression with the automatic bandwidth selection procedure in Calonico et al. (2019) works well. We give a more detailed walkthrough of these steps in Section 4. We also detail a local linear regression estimator in Appendix G.

-

With the estimates , transform the data according to (2.3). Apply empirical Bayes methods with prior independence to estimate with some on the transformed data .

This procedure produces a family of strategies since can take different forms. We consider two flavors of close.

2.3.1. close-npmle

To leverage theoretical and computational advances, we will focus on—and recommend—using nonparametric maximum likelihood (npmle) to estimate .202020The nonparamtric maximum likelihood has a long history in econometrics and statistics (Kiefer and Wolfowitz, 1956; Lindsay, 1995; Heckman and Singer, 1984). There is recent renewed interest. See, among others, Koenker and Gu (2019); Koenker and Mizera (2014); Jiang and Zhang (2009); Jiang (2020); Soloff et al. (2021); Saha and Guntuboyina (2020); Polyanskiy and Wu (2020); Shen and Wu (2022); Polyanskiy and Wu (2021). That is, we maximize the log-likelihood of (an estimated version of) the transformed data , whose marginal distribution is the convolution :212121We use to denote convolution and to denote the Gaussian probability density function.

The maximization is over the set of all probability measures on , . We note that when the estimated moments are constant functions of , close-npmle estimates the same prior as independent-npmle. In the theoretical literature, under prior independence, independent-npmle is state-of-the-art in terms of computational ease and regret properties.222222Empirical Bayes methods via npmle have computational and theoretical advantages, though much of the favorable theoretical results are proven in a homoskedastic setting. Its computational ease (Koenker and Mizera, 2014; Koenker and Gu, 2017) and lack of tuning parameters are advocated in Koenker and Gu (2019). Polyanskiy and Wu (2020) find that, with high probability, npmle recovers a distribution with only support points despite searching over the set of all distributions; they refer to this property as self-regularization. For regret control in the homoskedastic Gaussian model, Jiang and Zhang (2009)’s result is the best known and matches a lower bound up to log factors (Polyanskiy and Wu, 2021). Our results in Section 3 extend some of these favorable properties to close-npmle under the conditional location-scale model.

A simple alternative, which we call close-gauss and think of as a “lite” version of close-npmle, additionally models the shape as (standard) Gaussian. We briefly discuss its properties in the following section.

2.3.2. close-gauss

Under , the oracle Bayes posterior means are simply

Equation (2.3.2) is the analogue of the standard shrinkage formula (1), where unconditional means and variances are replaced with their conditional counterparts. As an empirical Bayes strategy, close-gauss then replaces the unknown conditional moments with their estimated counterparts.232323(2.3.2) is first proposed by Weinstein et al. (2018). Weinstein et al. (2018) propose estimating in a particular manner to ensure the resulting empirical Bayes posterior means dominate the naive estimates in frequentist risk , uniformly over . Its properties depend on those of the oracle (2.3.2) it mimics, which we turn to now.

Despite being rationalized under the restrictive assumption , (2.3.2) enjoys strong robustness properties: It is optimal over a restricted class of decision rules and minimax over all decision rules—without imposing (2.4). First, (2.3.2) is the optimal decision rule for estimating in squared error—solely under the sampling assumption (2)—among the class of decision rules that are linear in : . Second, (2.3.2) is minimax in the sense that it minimizes the worst-case squared error Bayes risk, where an adversary chooses , subjected to the constraint that ’s first two moments are .242424Formally, where the supremum is taken over having moments . To wit, note that the Bayes risk of (2.3.2) is the same regardless of choices of under the moment constraint, and it is equal to the optimal Bayes risk when . We conclude that (2.3.2) is minimax by observing that the minimax Bayes risk is at least the risk of (2.3.2).

However, the Normality assumption does imply that (2.3.2), unlike close-npmle, fails to achieve optimality—in the sense of vanishing regret (2.1)—when the location-scale assumption (2.4) does hold. Since we also show that close-npmle is worst-case robust—though with higher worst-case risk than close-gauss, we recommend close-npmle over close-gauss, unless the researcher is extremely concerned about the misspecification of the location-scale model.

3. Regret results for close-npmle

Recall that we observe , where satisfies the location-scale assumption (2.4) and obeys the Gaussian location model (2). Our recommended procedure, close-npmle, transforms the data into , with estimated nuisance parameters for in . It then estimates the unknown shape parameter via npmle (2.3.1) on .

Our leading result shows that close-npmle mimics the oracle Bayesian as well as possible, for the problem of estimation under squared error loss, in the sense that its Bayes regret vanishes at the minimax optimal rate. Our second result connects squared error estimation to Decision Problems 2 and 3 by showing that if an empirical Bayesian has low regret in squared error loss, then they likewise have low regret for Decision Problems 2 and 3.

Since our main result assumes the location-scale model, one may be concerned about potential misspecification of the location-scale model. The last result in this section, 2, bounds the worst-case Bayes risk of an idealized version of close-npmle (i.e. with known and fixed but misspecified ) as a multiple of the minimax risk without assuming (2.4). Thus, even under misspecification, close-npmle does not perform arbitrarily badly relative to the minimax procedure.

The rest of this section states and discusses these results formally. Practitioners who are less interested in the theoretical details are free to skip to Section 4, where we discuss a number of practical considerations.

Remark 2 (Notation).

In what follows, we use the symbol to denote a generic positive and finite constant which does not depend on . We use the symbol to denote a generic positive and finite constant that depends only on , some parameter(s) that describe the problem. Occurrences of the same symbol may not refer to the same constants. Similarly, for , generally functions of , we use to mean that some universal exists such that for all , and we use to mean that some universal exists such that for all . In logical statements, appearances of implicitly prepend “there exists a universal constant” to the statement. For instance, statements like “under certain assumptions, ” should be read as “under certain assumptions, there exists a constant such that for all , .”

Since all expectation or probability statements are with respect to the conditional distribution of , going forward, we treat as fixed and simply write to denote the expectation and probability over . We omit the subscript and the conditioning on .

3.1. Regret rate in squared error

Since we consider close-npmle in mean-squared error, we specialize and define

as the excess loss of the empirical Bayes posterior means—obtained by prior and nuisance parameter estimate for —relative to that of the oracle Bayes posterior means. The Bayes regret for close-npmle in squared error is then the -expectation of :

Equation (3.1) additionally notes that expected is equal to the expected mean-squared difference between the empirical Bayesian posterior means and the oracle Bayes posterior means.

We assume that belongs to some restricted class. Informally speaking, our first main result shows that for some constants that depend solely on , the Bayes regret in squared error decays at the same rate as the maximum estimation error for squared:

where we define for This result continues a recent statistics literature on empirical Bayes methods via npmle by characterizing the effect of an estimated nuisance parameter in a first step.252525Our theory hews closely to—and extends—the results in Jiang (2020) and Soloff et al. (2021), which themselves are extensions of earlier results in the homoskedastic setting (Jiang and Zhang, 2009; Saha and Guntuboyina, 2020). These results, under either homoskedasticity or prior independence, show that empirical Bayes derived from estimating the prior via npmle achieves fast regret rates. In particular, Saha and Guntuboyina (2020) show that the regret rate is of the form under prior independence and assumptions similar to ours.

Moreover, we show that controlling the Bayes regret is no easier than estimating in , which is a corresponding lower bound on regret. There exists such that for any estimator of , its worst-case regret is bounded below

Since the minimax estimation rates of and of are the same up to logarithmic factors, we conclude that our regret upper bound is rate-optimal up to logarithmic factors. We now introduce the assumptions on needed for these results, state the upper and lower bounds, and provide a technical discussion.

3.1.1. Assumptions for regret upper bound

We first assume that is an approximate maximizer of the log-likelihood on the transformed data and satisfying some support restrictions. This is not a restrictive assumption, as the actual maximizers of the log-likelihood function satisfy it.262626In particular, the support restriction for is satisfied by all maximizers of the likelihood function satisfy this constraint (see Corollary 3 in Soloff et al., 2021).

Assumption 1.

Let be the objective function in (2.3.1), ignoring a constant factor . We assume that satisfies

for tolerance

Moreover, we require that has support points within . To ensure that is positive, we assume that .272727The constants also feature in Jiang (2020) to ensure that the fitted likelihood is bounded away from zero. The particular constants in are chosen to simplify expressions and are not material to the result.

We now state further assumptions on the data-generating processes beyond (2.4). First, we assume that is exponential-tailed with parameter that controls the thickness of its tails. We state the restriction in an equivalent form of simultaneous moment control.282828An equivalent statement to Assumption 2 is that there exists such that for all . Note that when , is subgaussian, and when , is subexponential (see the definitions in Vershynin, 2018), as commonly assumed in high-dimensional statistics. Assumption 2 is slightly stronger than requiring that all moments exist for , and weaker than requiring to have a moment-generating function. Similar tail assumptions feature in the theoretical literature on empirical Bayes (Soloff et al., 2021; Jiang and Zhang, 2009; Jiang, 2020).

Assumption 2.

The distribution is has zero mean, unit variance, and admits simultaneous moment control with parameter : There exists a constant such that for all ,

Next, Assumption 3 bounds the variance parameters away from zero and infinity. This is a standard assumption in the literature, maintained likewise by Jiang (2020) and Soloff et al. (2021).

Assumption 3.

The variances admit lower and upper bounds:

where . This implies that for some .

Lastly, we require that satisfies some smoothness restrictions. We also require that satisfy some corresponding regularity conditions.

Assumption 4.

Let be the Hölder class of order

with maximal Hölder norm supported on .292929We recall the

definition of a Hölder class from van der Vaart and Wellner (1996), Section 2.7.1. We specialize

its definition to functions of one real variable. For an integer , Hölder-

functions are -times differentiable, with a Lipschitz continuous st derivative.

Definition 1.

For some set and constant , , let be the set of continuous functions with . The norm is defined as follows. Let be the

greatest integer strictly smaller than . Define

We refer to as a Hölder class of order and as the Hölder norm.

We assume that

-

(1)

The true conditional moments are Hölder-smooth: .

Additionally, let be a constant. Let be a set of bounded functions supported on that (i) admits the uniform bound and (ii) admits the metric entropy bound

We assume that the estimators for and , , satisfy the following assumptions.

-

(2)

For any , there exists a sufficiently large , independently of , such that for all ,

-

(3)

The nuisance estimators take values in almost surely: .

-

(4)

The conditional variance estimator respects the conditional variance bounds in Assumption 3: .

Assumption 4 is a Hölder smoothness assumption on the nuisance parameters and , which is a standard regularity condition in nonparametric regression; our subsequent minimax rate optimality statements are relative to this class. Moreover, it is also a high-level assumption on the quality of the estimation procedure for . Specifically, Assumption 4 expects that the nuisance parameter estimates and are rate-optimal up to logarithmic factors (Stone, 1980). Assumption 4 also expects that the nuisance parameter estimates belong to a class with the same metric entropy behavior as the Hölder class .303030If the nuisance parameters are -Hölder smooth almost surely, we can simply take for some potentially different . This can be achieved in practice by, say, projecting estimated nuisance parameters to in . Assumption 4(4) also expects the nuisance parameter estimates to respect the boundedness constraints for . This is mainly so that our results are easier to state; we discuss this assumption in C.1.

Assumptions 2, 4, and 3 specify a class of distributions and nuisance estimators indexed by a set of hyperparameters Our subsequent theoretical results are finite sample, with implicit constants dependent on these hyperparameters . To review, are bounds on the variances ; control the tails of ; and control the smoothness of ; and is the power of the log factor in the estimation rate for .

3.1.2. Regret results

Consider the following “good event,” indexed by ,

indicates that the nuisance parameter estimates satisfy some rate in . Our main result derives a convergence rate for the expected MSE regret conditional on this good event

Theorem 1.

Assume Assumptions 4, 2, 3, and 1 hold. Then, for any , there exists universal constants and such that (i) and that (ii) the expected regret conditional on is dominated by the rate function

If the event is sufficiently likely, we can control expected regret on the bad event as well. In Appendix G, we verify that local linear regression satisfies a weakening of these assumptions that are also sufficient for the conclusion of 1.

Corollary 1.

Assume the same setting as Theorem 1. Suppose, additionally, for all sufficiently large , Then, there exists a constant such that the expected regret is dominated by the rate function

We can show a corresponding lower bound on the Bayes regret—i.e., a lower bound on the worst-case Bayes regret when an adversary picks —by showing that any good posterior mean estimate implies a good estimate for . Minimax lower bounds for estimation of then imply lower bounds for estimation of the oracle posterior means .313131A similar argument is considered in Ignatiadis and Wager (2019) for related but distinct setting. See Section A.6.2.

Theorem 2.

Fix a set of valid hyperparameters for Assumptions 2, 4, and 3. Let be the set of distributions on support points which satisfy (2.4) and Assumptions 2, 4, and 3 corresponding to . For a given , let denote the oracle posterior means. Then there exists a constant such that the worst-case Bayes regret of any estimator exceeds :

where the infimum is taken over all (possibly randomized) estimators of .

As a result, the rate (1) is optimal up to logarithmic factors. The additional logarithmic factors are partly the price of having to estimate via npmle and partly deficiencies in the proof of Theorem 1. In any case, this cost is not substantial.

The regret upper bounds Theorems 1 and 1 are finite-sample statements. As a result, they hold uniformly over all distributions satisfying Assumptions 4, 2, and 3 delineated by the problem parameters . However, the usefulness of Theorems 1 and 1 still lies in the convergence rate, as the constants implied by the proofs are not sharp.

These regret upper bounds readily extend to the case where covariates are present and the location-scale assumption is with respect to the additional covariates :

under assumption on analogous to Assumption 4. Of course, the resulting convergence rate would suffer from the curse of dimensionality, and the term would be replaced with , where is the dimension of .

Taken together, 1 and 2 are strong statistical optimality guarantees for close-npmle in the canonical problem of estimation with squared error loss. That is, the worst-case performance gap of close-npmle relative to the oracle contracts at the best possible rate, meaning that close-npmle mimics the oracle as well as possible.

For interested readers, we provide an overview of the proof of our main result Theorem 1 in the following remark. A more detailed walkthrough is in Section C.3.

Remark 3 (Informal discussion of the proof for Theorem 1).

Regret results assuming prior independence are established by Soloff et al. (2021) and Jiang (2020), and we build on these results for Theorem 1. Applied to , these results state that (i) approximate maximizers of the (infeasible) log-likelihood are close to in terms of the average Hellinger distance of the induced densities of

and (ii) if is small, then posterior means for under are close to posterior means under in squared error.

Our results extend this argument by accommodating the fact that is unknown and must be estimated with .323232We also translate the resulting regret guarantee on estimating to regret guarantees on estimating . In doing so, we identify an apparent gap in the arguments of Jiang (2020) and Soloff et al. (2021). We show a modified argument avoids the gap in our setting, which applies to the setting in Soloff et al. (2021) as well. See F.1 for details. To apply (ii) in the literature, we would like to show that (i’) —an approximate maximizer of the feasible log-likelihood —is close to in terms of . This is not a straightforward task and is the most intricate part of our argument. To show (i’), we prove a lower bound for the likelihood (Theorem D.1) and modify (i) suitably to accommodate our likelihood lower bound (Theorem E.1).

To lower bound , we relate the two likelihoods by linearization (formally, see (D.4)):

Since approximately maximizes the feasible likelihood , is large by construction. Thus, if we can show that the right-hand side is small, then the infeasible likelihood would also be large. To obtain the rate (1), it is important to show that the right-hand side vanishes strictly faster than . To do so, we additionally need to show that the average derivative is small. Without it, we would obtain a worse squared error regret rate of the form .

In particular, we manage to relate this term to the average Hellinger distance (see Lemmas D.1 and D.2)

Loosely, this is because the population score in is mean-zero, . Thus if is close to , then the sample score evaluated at should also be approximately zero. This is a key step in Appendix D.

This bound for creates an additional complication when attempting to apply the claim (i). The claim (i) upper bounds the Hellinger distance using a lower bound for . However, now our lower bound for the likelihood itself depends on , and so we cannot apply (i) directly. The proof for (i’) additionally modifies the argument for (i) to accommodate our likelihood bound (Appendix E).

So far, our regret guarantees are only about estimation in squared error (Decision Problem 1). In the next subsection, we analyze regret for empirical Bayes decision rules targeted to the ranking-related problems (Decision Problems 2 and 3), and relate their performances to those for Decision Problem 1.

3.2. Other decision objectives and relation to squared-error loss

Notably, the oracle Bayes decision rules in Decision Problems 2 and 3 depend solely on the vector of oracle Bayes posterior means .333333 In principle, one could consider many other policy problems with a ranking flavor (Koenker and Gu, 2019). Among these problems, utility maximization by selection and top- selection are special in that optimal decisions are simple functions of the posterior means. We caution that the worst-case regret rate for ranking-type problems without this property can be unfavorable—as Gu and Koenker (2023) put it, “inherently futile”—since their optimal decisions depend on functionals that are known to be difficult to estimate (i.e., they have logarithmic minimax rates of estimation, Pensky, 2017; Dedecker and Michel, 2013; Cai and Low, 2011). In general, the minimax squared error rate of estimating is logarithmic, unless is an analytic function, by an extension of the argument in Cai and Low (2011). Ranking-type problems often involve of the form or , which are not smooth. This observation suggests that these ranking-type problems may also suffer from logarithmic regret rates—though, this observation alone does not prove so, as difficulties in estimating in squared error might not preclude a polynomial regret rate for these ranking-type problems. Therefore, for these problems, the natural empirical Bayes decision rules simply replace oracle Bayes posterior means, , with empirical Bayes ones, , in the oracle decision rules.343434Theorem 3 applies to any estimators of the oracle Bayes posterior means—not necessarily derived through an empirical Bayes procedure and does not impose the location-scale assumption. As a result, it may be of independent interest. For instance, if one is comfortable with the prior estimated by close-npmle, then the corresponding decision rules for Decision Problems 2 and 3 threshold based on estimated posterior means under close-npmle.

In these problems, (2.1) is equal to the expected risk gap between using the feasible decision rules and the oracle decision rules . To specialize, we let denote for Decision Problem 2 and we let denote for Decision Problem 3. The following result relates and to .

Theorem 3.

Suppose (2) holds, but (2.4) may or may not hold. Let be the plug-in decisions with any vector of estimates , not necessarily from close-npmle. We have the following inequalities on the expected regret corresponding to the decision rules :

-

(1)

For utility maximization by selection,

-

(2)

For top- selection,

Theorem 3 shows that the two decision problems utility maximization by selection and top- selection are easier than estimating the oracle Bayesian posterior means. As a result, our convergence rates from Theorems 1 and 1 also upper bound regret rates for these two decision problems, rendering the regret rates more immediately useful for policy problems. In particular, for , both regret rates (1) and (2) are of the form under 1. Thus, the performance of the empirical Bayes decision rule approximates that of the oracle at approximately the rate . However, the actual performance of close-npmle for Decision Problems 2 and 3 may be better than predicted by Theorem 3. The speed at which regret converges, as implied by Theorem 3, might not be tight, though it is competitive with recent results.353535Regarding potential looseness of Theorem 3, as would be clear from the proof, the bound (1) holds even when the ’s are adversarially chosen such that the empirical Bayesian makes every mistake: for every . However, for a fixed vector , we expect that only for a vanishing fraction of populations. On the other hand, though, if the ’s are adversarially chosen to be , then the regret is equal to . In the proof, the upper bound (1) can be replaced by . Thus, in this adversarial case, we would have matching upper and lower bounds. That said, Theorem 3 is competitive with recent results. top- selection is recently studied by Coey and Hung (2022), who show that under prior independence, if are -modeling posterior means, i.e., posterior means for some estimate for the prior , then where is the Wasserstein-1 distance between two distributions. Theorem 3 attains a worse rate in parametric settings, when the prior can be estimated at fast rates. However, in nonparametric settings, is often only estimable at logarithmic rates (Dedecker and Michel, 2013), and thus the rate in Theorem 3 is much more favorable in those settings.

Recall that we can think of top- selection as the decision problem in Bergman et al. (2023). The utility function represents the expected mobility of a mover, assuming that the mover moves randomly into one of the high mobility Census tracts. Our proof of Theorem 3 in Section A.2 allows for a slightly more general decision problem. Suppose the decision now is to provide a full ranking of Census tracts for potential movers and maximize the expected mobility for a mover. Suppose that the probability that a mover moves to a tract depends decreasingly and solely on the tract’s rank. To be more concrete, suppose the mover has probability of moving to the highest-ranked tract, to the second-highest, and so forth. Then, with the same argument, the corresponding regret is dominated by , which generalizes (2).

3.3. Robustness to the location-scale assumption (2.4)

We prove our regret upper and lower bounds imposing the location-scale model (2.4). This is an optimistic assessment of the performance of close-npmle. While (2.4) nests prior independence, it may still be misspecified. We now consider the worst-case behavior of close-npmle without the location-scale assumption. Section A.7.3 additionally discusses an interpretation of close-npmle under misspecification of (2.4).

We will do so by considering an idealized version of the procedure. So long as has two moments, are well-defined as conditional moments of without imposing the location-scale assumption. We will assume that are known. Without the location-scale model, is ill-defined, but we will assume that we obtain some pseudo-true value that has zero mean and unit variance. This is a reasonable condition to impose, since every conditional prior distribution obeys this moment constraint.363636We do not know if the maximizer of the population analogue to (2.3.1) respects the moment constraints. In any case, imposing these moment constraints computationally in npmle is feasible, as they are simply linear constraints over the optimizing variables. Projecting the estimated to these moment constraints make little difference in our empirical exercise (Section B.2). Thus, for estimating , whose true prior is , this idealized procedure uses some misspecified prior , which does have the correct first two moments. Chen (2023) shows that the worst-case risk for estimating is uniformly bounded, over arbitrary choices of and with zero mean and unit variance: Let be the set of mean-zero, variance-one distributions, then

Hence, the misspecification of does not cause unbounded risk. Translating this result to the problem of estimating in squared error, we arrive at the following corollary.

Corollary 2.

Under (2) but not (2.4), assume the conditional distribution has mean and variance . Denote the set of distributions of which obey these restrictions as . Let denote the posterior mean estimates with a pseudo-true prior which obeys a location-scale model Assume has zero mean and unit variance. Assume that is non-random. Then, for any ,

Let be some (possibly randomized) estimator of , which may depend on the data and . Suppose additionally that and . Then, the worst-case risk of is at least

2 shows that an oracle version of close-npmle has finite worst-case risk, scaling like . It also shows that any procedure must incur worst-case risk at least for some . We thus interpret 2 as a robustness guarantee on close-npmle, as it shows that close-npmle approximates some ideal procedure whose worst-case behavior is within a constant multiple of the minimax procedure.373737On the other hand, unlike this idealized version of close-npmle, the oracle version of independent-gauss, (1), has unbounded worst-case risk as a multiple of that of the minimax procedure (2.3.2).

4. Practical considerations when (not) applying close

4.1. A detailed recipe

We now describe the implementation of close-npmle in more detail, following our previous outline in , , and . We emphasize that, in practice, these are implemented in accompanying software; our discussion here is just an overview of what goes on under the hood.

The first step estimates the conditional moments nonparametrically. Since the two conditional moments can be written as conditional expectations

| (4.1) |

we can estimate them accordingly with off-the-shelf methods (e.g., local polynomial kernel smoothing methods implemented by Calonico et al., 2019). Specifically, estimating with is directly a nonparametric regression of on .383838We take in our empirical implementation since the distribution of tends to be right-skewed, and thus we suspect regressing on has a better fit. Estimating can be operationalized by first nonparametrically regressing on , and then subtracting off . This is a plug-in estimator for , as it replaces quantities in (4.1) with their empirical counterparts.393939Since (4.1) can be written in different forms, there are other reasonable plug-in estimators for . We investigate one such alternative estimator in Section B.2 and find very similar performance in our empirical exercise.

A wrinkle is that the plug-in estimate may be negative.404040The negative estimated variance phenomenon similarly may occur with estimating the prior variance with independent-gauss and with conditional variance estimation in Armstrong et al. (2022). This is in part caused by estimation noise in . However, there is some evidence that observations with large estimated ’s are underdispersed for the measures of economic mobility in the Opportunity Atlas. See Section B.1. Truncating at zero results in observations whose estimated prior variances . These observations also have implied . For these observations, an empirical Bayesian taking at face value has degenerate priors at . Since observations with do not contribute to the likelihood objective for npmle, dropping observations with from the npmle estimation and setting the estimated posterior mean for those observations to is consistent with what close-npmle instructs. In our experience, this simple approach does not appear to affect performance. Nevertheless, in Appendix G, we propose a heuristic but data-driven truncation rule, borrowing from a statistics literature on estimating non-centrality parameters for non-central distributions (Kubokawa et al., 1993). Appendix G also discusses tuning parameter selection for estimating and verifies that our local linear regression estimators satisfy the regularity conditions in Section 3.

Next, in the second step , we form the transformed estimates and the transformed standard errors . We then estimate the npmle on the data by maximizing (2.3.1). In practice, we approximate the infinite-dimensional optimization problem (2.3.1) with a finite-dimensional one, by discretizing distributions on a grid. To be precise, let be a pre-specified grid of points, not necessarily equally spaced, and denote it by .414141Since the gridding is a computational approximation to the infinite dimensional optimization problem, the sole downside of a finer grid is computational burden (cf. bias-variance tradeoffs with typical tuning parameter selection problems). Ideally, adjacent grid points should have a sufficiently small and economically insignificant gap between them. Since the true prior for have zero mean and unit variance, we find that a fine grid within (e.g., 400 equally spaced grid points), with a coarse grid on (e.g., 100 equally spaced grid points), performs well. Also see recommendations in Koenker and Gu (2017) and Koenker and Mizera (2014). The feasible version of (2.3.1) maximizes the concave program The estimated npmle is a discrete distribution with support points and corresponding masses .

Finally, given the estimate , we can compute empirical Bayes decision rules by minimizing posterior expected loss to implement . Since is a discrete distribution, the posterior for is given by the probability mass function

normalized so that the probabilities sum to 1. This probability mass function can be plugged into (2.1) to compute the empirical Bayes decision rule for any loss function .424242In the leading use-case, the posterior means for are simply . In practice, REBayes::GLmix (Koenker and Gu, 2017) in R implements estimation of the npmle and computation of the posterior means .

4.2. When does relaxing prior independence matter?

When prior independence holds, close-npmle is the same as independent-npmle, up to the estimation of the constant conditional moments . Since close-npmle has to estimate the conditional moments, we expect it to underperform independent-npmle. Though, since the location-scale assumption (2.4) strictly generalizes prior independence, we do not expect close-npmle to underperform by much in large samples.

When prior independence does not hold, but when the conditional location-scale model (2.4) approximately holds, we expect close to outperform methods that assume prior independence. Qualitatively speaking, if are not constant, we expect the improvement of close-methods to be large when large portions of the unconditional signal variance is attributable to the conditional expectation. Since we can decompose

we expect the improvement of close-methods to be large when the variance of the conditional expectation is large compared to . Intuitively, this is the case when is highly predictive of . Whether this is the case can be easily checked by plotting against , as in Figure 1, and inspecting the estimated conditional moments.

Finally, when the conditional distributions are non-Gaussian, and in particular when they are discrete, skewed, or thick-tailed, we expect close-npmle to additionally outperform independent-gauss due to not assuming Normality. When the conditional priors are Gaussian, estimating it via the npmle pays a statistical price, but we theoretically and empirically observe that the price is not large. Admittedly, it is often difficult to diagnose whether the underlying conditional distributions have these properties, since we only observe . Likewise, so far the discussion in this subsection is heuristic. To be more certain of the extent of improvement of close-npmle over other empirical Bayes methods, it is helpful to have out-of-sample validation. The next subsection proposes a minor extension of Oliveira et al. (2021), which allows for an unbiased estimate of loss and serves as a validation procedure.

4.3. A formal validation procedure via coupled bootstrap

Consider where . For some and a random independent Gaussian noise , consider adding to and subtracting from some scaled version of :

Oliveira et al. (2021) call the coupled bootstrap draws. Observe that the two couple bootstrap draws are conditionally independent:

The conditional independence allows us to use as an out-of-sample validation for decision rules computed based on . We will denote their marginal variances by and .

It is helpful to think of as training data and as testing data. In fact, the coupled bootstrap precisely emulates sample-splitting on the micro-data. To see that, suppose is a sample mean of i.i.d. micro-data . Suppose we split the micro-data into a training set and a testing set, with proportions and , respectively. Let and be the training and testing set sample means, respectively. Then the central limit theorem implies that, approximately,

independently. Note that the two representations (4.3) and (4.3) are equivalent, and hence coupled bootstrap emulates sample-splitting. For instance, coupled bootstrap with a value of is statistically equivalent to splitting the micro-data with a 90-10 train-test split.

Just as we can perform out-of-sample validation with sample-splitting on the micro-data, we can also do so with the coupled bootstrap emulation of sample-splitting. The following proposition formalizes this and states unbiased estimators for the loss of these decision rules, as well as their accompanying standard errors.434343Oliveira et al. (2021) state the unbiased estimation result for the mean-squared error estimation problem. They develop the result further by connecting the coupled bootstrap estimator to Stein’s unbiased risk estimate. Our analogous calculation for other loss functions and for the standard errors is a minor extension of their results. Lemma 1 can also be easily generalized to other loss functions that admit unbiased estimators (effectively, the loss is a function of a Gaussian location . For unbiased estimation of functions of Gaussian parameters, see Table A1 in Voinov and Nikulin, 2012).

| Problem | Unbiased estimator of loss, | |

|---|---|---|

| Decision Problem 1 | ||

| Decision Problem 2 | ||

| Decision Problem 3 |

Lemma 1.

Suppose obey the Gaussian heteroskedastic location model, assumed to be independent across (2). Fix some and let be the coupled bootstrap draws. For some decision problem, let be some decision rule using only data . Let , for Decision Problems 1, 2, and 3, the estimators displayed in Table 1 are unbiased for the corresponding loss:

Moreover, their conditional variances are equal to those expressions displayed in the third column of Table 1.

Lemma 1 allows for an honest, out-of-sample evaluation of decision rules, as well as uncertainty quantification around the estimate of loss, solely imposing the heteroskedastic Gaussian model. This is a useful property in practice for comparing different empirical Bayes methods. The alternative is to take some estimated prior—say the one learned by close-npmle—as the oracle prior, and evaluate performance of competing methods. Doing so likely tips the scale in favor of a particular method, and we advocate for the coupled bootstrap instead.

5. Empirical illustration

How does close-npmle perform in the field? We now consider two empirical exercises related to the Opportunity Atlas (Chetty et al., 2020) and Creating Moves to Opportunity (Bergman et al., 2023). We first summarize these papers.

5.1. The Opportunity Atlas and Creating Moves to Opportunity

Using longitudinal Census micro-data, Chetty et al. (2020) estimate tract-level children’s outcomes in adulthood and publish the estimates in a collection of datasets called the Opportunity Atlas. Each dataset contains estimates and standard errors for some particular definition of the economic parameter of interest, at the Census tract level. Taking these estimates from the Opportunity Atlas, Bergman et al. (2023) conducted a program in Seattle called Creating Moves to Opportunity. They provided assistance to treated low-income individuals444444They are families with a child below age 15 who are issued Section 8 vouchers between April 2018 and April 2019, with median household income of $19,000. About half of the sampled households are Black and about a quarter are white (Table 1, Bergman et al., 2023). to move to “Opportunity Areas”—Census tracts with empirical Bayes posterior means in the top third.454545There are also adjustments to make the selected tracts geographically contiguous. See Bergman et al. (2023) for details. We view \NAT@swafalse\NAT@partrue\NAT@fullfalse\NAT@citetpbergman2019creating objectives as top- selection (Decision Problem 3), for equal to one third of the number of tracts in King County, Washington (Seattle).

Before proceeding further, we discuss how we handle tract-level covariates for these datasets.

Remark 4 (Covariates).

The Opportunity Atlas also includes tract-level covariates, a complication that we have so far abstracted away from. In the ensuing empirical exercises—as well as in Bergman et al. (2023)—the estimates and parameters are residualized against the covariates as a preprocessing step. We now let denote the raw Opportunity Atlas estimates for a pre-residualized parameter and let be their residualized counterparts against a vector of tract-level covariates , with regression coefficient .464646Precisely speaking, let be a vector of tract-level covariates. Let be the raw Opportunity Atlas estimates of a parameter , with accompanying standard errors . Let be some vector of coefficients, typically estimated by weighted least-squares of on . Let and be the residuals. We assume that the tract-level covariates do not predict the estimation noise in : i.e., . Since is precisely estimated, we ignore its estimation noise. Then, the residualized objects obey the Gaussian location model See additional discussion on covariates in Section A.6.2. Figure B.6 contains empirical results without residualizing against covariates. We can apply the empirical Bayes procedures in this paper to and obtain an estimated posterior for . This estimated posterior for the residualized parameter then implies an estimated posterior for the original parameter , by adding back the fitted values (Fay and Herriot, 1979). When there are no covariates, and .

We consider more measures of economic mobility than our example in Section 2. For our purposes, these definitions of take the following form: is the population mean of some outcome for individuals of some demographic subgroup growing up in tract , whose parents are at the 25th income percentile. We will consider three types of outcomes:

-

(1)

Percentile rank of adult income

-

(2)

An indicator for whether the individual has incomes in the top 20 percentiles

-

(3)

An indicator for whether the individual is incarcerated

for the following demographic subgroups:474747We focus on men as a subgroup since incarceration rates for women are extremely low. (1) all individuals (pooled), (2) white individuals, (3) white men, (4) Black individuals, and (5) Black men. As shorthands, we refer to the three types of outcomes as mean rank, top-20 probability, and incarceration, respectively. The outcome we use in Section 2 corresponds to top-20 probability for Black individuals.484848In each Opportunity Atlas dataset, the estimates are computed from the fitted value of a semiparametric regression procedure on the Census micro-data. The regression procedure implicitly pools observation with similar parent income ranks and is not fully nonparametric. As a result of this extrapolation, the estimates need not respect support conditions for Bernoulli means. For instance, some estimates for top-20 probability and for incarceration are negative. Similarly, the standard errors for estimates for binarized are typically not precisely of the form . We refer interested readers to Chetty et al. (2020) for details of their regression specification.

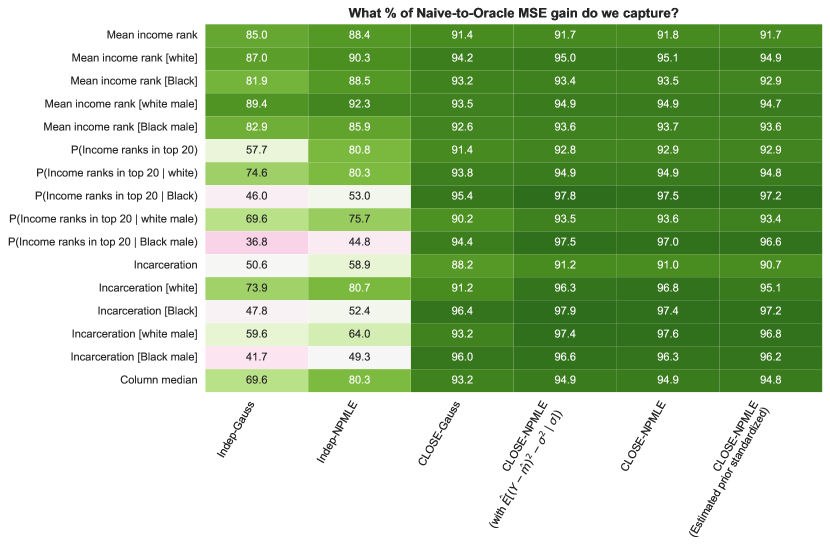

The remainder of this section compares several empirical Bayes approaches on two exercises. The first exercise is a calibrated simulation. In the simulation, we compare performance in MSE of various methods to the that of the oracle posterior. We find that close-npmle has near-oracle performance in terms of MSE, and substantially outperforms independent-gauss. The second exercise is an empirical application to a scale-up of the exercise in Bergman et al. (2023). It uses the coupled bootstrap to evaluate whether close-npmle selects more economically mobile tracts—in terms of the objective in Decision Problem 3—than independent-gauss. We find that it does, and the magnitude of improvement is substantial compared to the value of basic empirical Bayes methods and even the value of data.

5.2. Calibrated simulation

Our first empirical exercise is a calibrated simulation. To devise a data-generating process that does not impose the location-scale assumption, we partition into vingtiles, fit a location-scale model within each vingtile, and draw from the estimated model (see Section B.3 for details). Since the location-scale model is only imposed within each vingtile, this data-generating process does not impose (2.4) on the entire dataset. Figure 3 shows an overlay of real and simulated data for one of the variables we consider. Visually, at least, the simulated data resemble the real estimates.

On the simulated data, we then put various empirical Bayes strategies to test. We consider the feasible procedures naive, independent-gauss, independent-npmle, close-gauss, and close-npmle, where naive sets .494949We note that none of the feasible procedures (naive, independent-gauss, independent-npmle, close-gauss, and close-npmle) have access to the true projection coefficient of onto , which they must estimate by residualizing against covariates on the data. Additionally, we weight the estimation of and in independent-gauss by the precision , following Bergman et al. (2023). Because we have the ground truth data-generating process, we additionally have two infeasible benchmarks:

-

•

oracle: A Bayesian who has access to the distribution of and uses the true posterior means for .505050These posterior means are computed by approximating the true prior with the empirical distribution of a large sample drawn from the true prior.

-

•

oracle-gauss: A Bayesian who knows and uses (2.3.2).

For this exercise, we focus on estimating the parameters in MSE (Decision Problem 1).

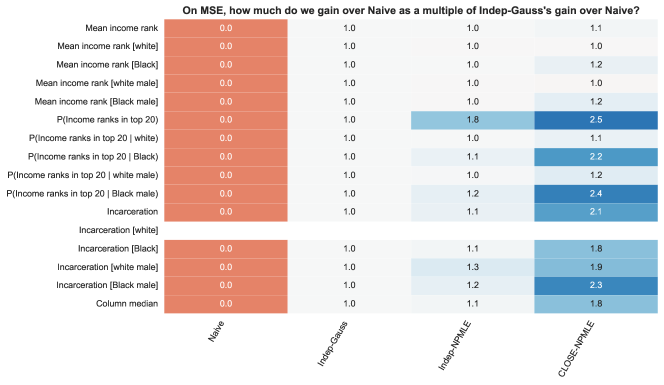

Notes.

Each column is an empirical Bayes strategy that we consider, and each row is a different definition of . The table shows relative performance, defined as the squared error improvement over naive, normalized as a percentage of the improvement of oracle over naive. That is, if we think of going to oracle from naive as the total extent of risk gains via empirical Bayes methods, this relative performance denotes how much of those gains each method captures. The last row shows the column median. Since we rely on Monte Carlo approximations of oracle, the resulting Monte Carlo error causes close-npmle to outperform oracle in the top right. Results are averaged over 1,000 Monte Carlo draws.