Estimation of stability index for symmetric -stable distribution using quantile conditional variance ratios

Abstract.

The class of -stable distributions is widely used in various applications, especially for modelling heavy-tailed data. Although the -stable distributions have been used in practice for many years, new methods for identification, testing, and estimation are still being refined and new approaches are being proposed. The constant development of new statistical methods is related to the low efficiency of existing algorithms, especially when the underlying sample is small or the distribution is close to Gaussian. In this paper we propose a new estimation algorithm for stability index, for samples from the symmetric -stable distribution. The proposed approach is based on a quantile conditional variance ratio. We study the statistical properties of the proposed estimation procedure and show empirically that our methodology often outperforms other commonly used estimation algorithms. Moreover, we show that our statistic extracts unique sample characteristics that can be combined with other methods to refine existing methodologies via ensemble methods. Although our focus is set on the symmetric -stable case, we demonstrate that the considered statistic is insensitive to the skewness parameter change, so that our method could be also used in a more generic framework. For completeness, we also show how to apply our method on real data linked to plasma physics.

Keywords: stable distribution, heavy-tailed distribution, conditional variance, estimation, tail index, stability index

MSC2020: 62F10, 60E07, 62P35

1. Introduction

The -stable distributions are an important modelling tool as they constitute a domain of attraction for sums of independent random variables. That is, if the sum of independent and identically distributed (i.i.d.) random variables converges in distribution, then the limiting distribution belongs to the -stable family by the generalized Central Limit Theorem, see Lévy (1924), Khinchine and Lévy (1936), Shao and Nikias (1993), and Samorodnitsky and Taqqu (1994) for classical references. The family of -stable probability distribution is often used to describe the generalized white noise, without any assumptions imposed on the underlying moments; note that the sums of i.i.d. -stable random variables retain the shape of the original distribution, which is known as the stability property, see Feller (1966) and Jakubowski and Kobus (1989).

The first applications of the -stable distributions were related to generic financial data description and telephone line noise modelling, see Mandelbrot (1960) and Chambers et al. (1976). Since 1990s, the -stable distributions have found numerous other applications linked e.g. to financial markets, telecommunications, condition monitoring, physics, biology, medicine, and climate dynamics, see Rachev and Mittnik (2000); Bidarkota et al. (2009); Yu et al. (2013); Żak et al. (2017, 2016); Majka and Góra (2015); Kosko and Mitaim (2004); Barthelemy et al. (2008); Sokolov et al. (1997); Lomholt et al. (2005), and references therein. See also Nikias and Shao (1995); Janicki and Weron (1994); Wegman et al. (1989); Nolan (2020); Durrett et al. (2011); Lan and Toda (2013); Peng et al. (1993); Ditlevsen (1999) for classical positions on -stable distributed processes.

In general, the -stable distributions are characterized by four parameters corresponding to location, scale, tail structure, and symmetry. In this paper we consider symmetric -stable distributions and focus on the modelling of the tail index , also called the stability index, responsible for the tail power-law behavior of the -stable distribution, see Nolan (2020). For , the -stable distribution belongs to the wide class of the heavy-tailed distributions and in this case the corresponding random variable has infinite variance; the smaller the value of , the heavier the tail. On the other hand, for , the -stable distribution reduces to the Gaussian distribution. Also, it should be noted that in general the probability density function (PDF) of -stable distribution is not given in an explicit form, and the distribution structure is typically expressed via its characteristic function.

In this paper we consider the problem of statistical estimation of the stability index for the symmetric -stable distribution. The estimation problem has been studied by many authors for more than 50 years and one can find various approaches in the literature. The most recognized methods are linked to quantile methods, see e.g. Fama and Roll (1971); McCulloch (1986); Dominicy and Veredas (2013); Huixia et al. (2012); Leitch and Paulson (1975), techniques based on the characteristic functions, see e.g. Press (1972); Cizek et al. (2005); Koutrouvelis (1980); Kogon and Williams (1998); Mohammadreza et al. (2017); Arad (1980); Paulson et al. (1975), maximum likelihood, see e.g. DuMouchel (1973); Nolan (2001); Mittnik et al. (1999); Muneya and Akimichi (2006); Brorsen and Yang (1990), Hill‘s estimators, see e.g. Pictet et al. (1998); Pickands (1975); de Haan and Resnick (1980); Dekkers et al. (1990); Resnick (1997), and other techniques tailored for the -stable distributions, see e.g. Lombardi and Godsill (2006); Escobar-Bach et al. (2017); Teimouri et al. (2018); Garcia et al. (2011); Tsihrintzis and Nikias (1996); Sathe and Upadhye (2020); de Haan and Themido Pereira (1999); Matsui and Takemura (2008). Also, we refer to Akgiray and Lamoureux (1989) for a comparative study of the estimation algorithms for the -stable distribution.

While most of the considered estimators have nice theoretical properties and their asymptotic behavior is well studied, they are not very effective when applied to practical data. This is mainly due to the fact that for -stable distributed samples the estimation algorithms to be effective require a large sample sizes as well as substantial computational power. This is especially visible when the stability index is close to , i.e. when the -stable distribution tends to the Gaussian distribution. The related problem of discriminating the -stable distribution from the Gaussian one was discussed in the literature e.g. in Burnecki et al. (2012, 2015); Pitera et al. (2022); Wyłomańska et al. (2020).

To overcome the problem of small sample size, lack of the explicit form of PDF, and infinite variance of the underlying sample, the approach proposed in this paper is based on the quantile conditional variance (QCV) class of statistics. The QCV based methods have been recently proposed mainly in the context of goodness-of-fit testing or to explain empirical phenomena such as the 20/60/20 rule, see Jelito and Pitera (2021) and Jaworski and Pitera (2016). Also, this methodology has been recently applied for the local damage detection based on the signals with heavy-tailed background noise, or studies the asymptotic behavior of empirical processes see Hebda-Sobkowicz, Zimroz and Wyłomańska (2020); Hebda-Sobkowicz, Zimroz, Pitera and Wyłomańska (2020); Ghoudi (2018).

Although the theoretical variance for the -stable distribution with is infinite, the QCV always exists and can be used to characterize the -stable distribution up to the location, see Jaworski and Pitera (2020). Here, we extend the -stable distribution goodness-of-fit methodology proposed in Pitera et al. (2022) and show that it can be efficiently used for -stable tail index estimation in the symmetric case. While our approach can be generally classified as the quantile method, we show that it is more effective than the commonly used algorithms proposed in McCulloch (1986). This is mainly due to the fact that QCV gathers information about multiple quantiles at the same time and better reflects the tail structure. Moreover, the empirical QCV based ratio statistics proposed in this paper are easy to implement as they are based on sample QCV. This makes our approach effective for small samples and computationally efficient. In addition, our data study shows that the QCV approach could be successfully applied to estimate the tail index in the near-Gaussian environment, i.e. when the true stability index is close to . As already mentioned, in this paper we focus on the tail index estimation for the symmetric -stable distributions. However, we also demonstrate that the approach proposed is in fact insensitive to the skewness parameter changes and could be easily extended to a general setting. Finally, it is worth mentioning that the QCV approach extracts sample characteristics different to the ones extracted by other estimation procedures such as the regression methods. Consequently, the QCV approach could also be used to refine the existing frameworks, e.g. via ensemble learning, see Polikar (2006) and references therein.

The rest of the paper is organized as follows. In Section 2 we recall the definition of the symmetric -stable distribution as well as the main facts related to the corresponding tail behavior. Moreover, we discuss the characterization of the -stable distribution via the conditional variance. Next, in Section 3 we analyze the sample QCV for the -stable distribution and introduce the estimation technique based on the QCV approach. In Section 4 we present the simulation study where for Monte Carlo simulated samples we demonstrate the efficiency of the methodology proposed. In this section we compare the results with the benchmark methods. By simulation study we also demonstrate the robustness of the methodology in question for the skewness parameters change. Finally, in Section 5, we analyze real data obtained in experiments on the controlled thermonuclear fusion and show that the methodology proposed efficiently discriminates the -stable distributions with close to . In the last section we conclude the paper.

2. The symmetric -stable distribution

There are many ways to define the family of -stable distributions. In this paper we use the 0-parametrization and follow the characteristic function approach, see Section 1.3 in Nolan (2020) in which, other parametrizations are stated. Namely, we say that the random variable follows the -stable distribution with parameters , , , and write if its characteristic function is given by

| (1) |

The parameter is linked to the stability index, i.e. it determines the rate at which the tails of the distribution diminish; see Theorem 1 or Nolan (2020) for details. Note that for , the -stable distribution simplifies to the Gaussian distribution. The parameter is used to quantify the skewness of the heavy-tailed distribution; however, note that the classical Pearson‘s skewness coefficient is undefined for . In particular, for (, respectively) the -stable distribution is skewed to the right (left, respectively) and if , then the -stable distribution is symmetric around the location parameter . The coefficient is the scale parameter, see Samorodnitsky and Taqqu (1994); Janicki and Weron (1994).

In the following, we focus on the normalized and symmetric -stable distributions, i.e. we assume that with . For brevity, we write and say that follows the symmetric -stable distribution. For any , we use , , and , to denote the cumulative distribution function (CDF), the probability density function (PDF), and the quantile function (inverse CDF) of the symmetric -stable distribution, respectively. Note that the explicit formula for PDF of is known only for the Gaussian distribution () and the Cauchy distribution (). However, it is possible to provide an integral representation of . Namely, from Theorem 3.2 in Nolan (2020), for , we have

| (2) |

2.1. Tails of the symmetric -stable distribution

Let us now focus on the asymptotic behavior of the symmetric -stable distribution with . The tails of distribution could be characterized using power law dynamics with an additional exponent factor linked to the parameter . This is formalized in Theorem 1, where we use simplified notation whenever and to denote the Gamma function; see Theorem 1.2 in Nolan (2020) for details and the proof.

Theorem 1.

For any , , and , we get

| (3) |

Next, we show the asymptotic behavior of the quantile function of the symmetric -stable distribution. While this could be seen as a complementary result to Theorem 1, we decided to present the proof for its completeness.

Proposition 2.

For any and , we get

Proof.

Let us fix . Let , let be the survival function of , and let be the inverse of . From Theorem 1, we get . Thus, setting for , we get Now, recalling that , we know this is equivalent to . By considering the -root of the inverted limit, we know that Finally, noting that for , we get

which concludes the proof. ∎

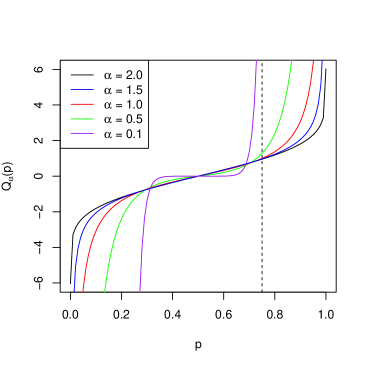

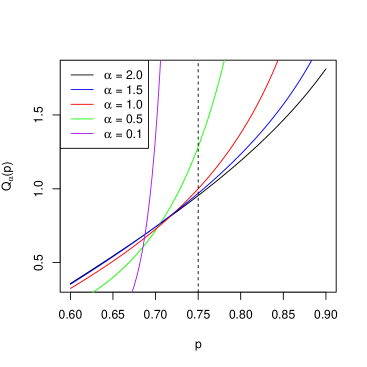

Using Proposition 2 we can show that, for quantile levels high enough, the quantiles lines are monotone with respect to the parameter ; see Proposition 3 for details and Figure 1 for a numerical illustration. This shows that the observation stated in Theorem 1, which links the parameter to the tail thickness, could be expressed in terms of the quantile functions. Note that this result could be associated with the concept of the first order tail stochastic dominance, see Zieliński (2001); Ortobelli et al. (2016); Bednorz et al. (2021) for some other results on the stochastic ordering in reference to -stable distributions.

Proposition 3.

For any satisfying there exists such that for any we get

| (4) |

Proof.

Let be such that . For brevity, we assume that ; the case could be treated using a similar logic. In order to prove (4), it is enough to show that

| (5) |

Indeed, from (5) it follows that there exists some such that for any we have , which shows (4). Let us now prove (5). Using Proposition 2, we get

Recalling that we get and consequently . Noting that , we conclude the proof. ∎

Remark 4.

From simulations, we get that the constant from Proposition 3 can be chosen independently of and , and it satisfies the inequality ; see Figure 1. The difficulty of analytical calculation of could be linked to the fact that the proof of Proposition 3 is based on the tail approximation of the quantile function; cf. Theorem 1 and Proposition 2. Since we were not able to find explicitly, we deduced it from the numerical studies. We refer to Theorem 1.2 in Nolan (2020) as well as to the following remarks for more information on technical calculation difficulties for -stable distribution tails; see also the discussion after Equation 3.2 in Fama and Roll (1971).

Remark 5.

From Proposition 3 and Remark 4 we see that the quantile functions values are monotone with respect to the tail index for sufficiently large quantile levels. This result should be compared with Zieliński (2001), where the full-domain dispersive ordering result for the stable distributions is shown. However, this result is stated in the 2-parametrization while in this paper we follow the 0-parametrization. In fact, as seen in Figure 1, the full-domain ordering does not hold for the 0-parametrization, so that the result from Zieliński (2001) cannot be extended to our setting. We refer to Proposition 3.7 in Nolan (2020) as well as to the following discussion for more details about various parametrizations of the -stable distribution family.

2.2. Quantile conditional variance for -stable distributed random variables.

In this section, we discuss the conditional variance characterization of the symmetric -stable distributions. Let us consider a generic with some . For any , we define the quantile conditioning set . The quantile conditional variance (QCV) of on is given by

| (6) |

Note that is simply the quantile trimmed variance of , i.e. the conditional variance on the quantile interval . Also, note that for any and , the quantile conditional variance is well-defined and finite. Also, the family characterizes the -stable distribution up to an additive shift, see Pitera et al. (2022) for details.

To compute the value of QCV one may use the representation based on the probability density or quantile functions. More specifically, recalling that is absolutely continuous with the density and using (6) with , we get

| (7) |

As expected, the explicit formula for could be derived only for the Gaussian () and the Cauchy () distributions, see Pitera et al. (2022). Namely, for the Gaussian case, i.e. with , we get

| (8) |

where and are standard Gaussian PDF and CDF, respectively, while for the Cauchy case, i.e. with , we get

| (9) |

where .

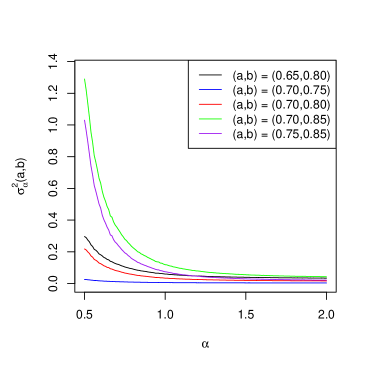

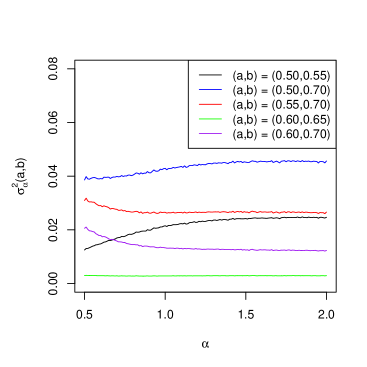

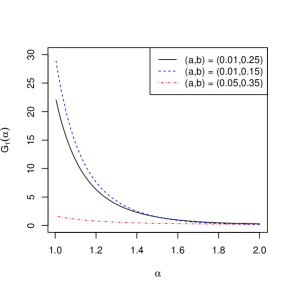

Recalling that the smaller the tail index , the heavier the tails, we expect that the quantile conditional variance on an appropriately chosen tail set should be monotone with respect to . Consequently, QCV could be used to measure the heaviness of the tail of the symmetric -stable distributions. This intuition is formalized in Theorem 6; see also Figure 2 for a numerical illustration.

Theorem 6.

Let be such that . Then, there exists such that, for any satisfying , we get

Proof.

Let us fix satisfying . Also, as in Proposition 3, assume . Note that, recalling (7), for any satisfying , we get

| (10) |

Let us define and , and note that (2.2) could be expressed as

Then, it is enough to show that and are (strictly) increasing. Indeed, using the classic Chebyshev integral inequality (see e.g. Theorem 8 in Section 2.5 of Mitrinović (1970)), from the monotonicity of and , we get , which shows . Note that is increasing as the sum of the increasing functions and . Thus, to conclude the proof it is enough to show that is increasing. Recalling that is the inverse of , we get

Thus, for any , we get if and only if . Consequently, it is enough to show that

| (11) |

Indeed, identity (11) implies that, starting from some , we get , and consequently the map is (strictly) increasing on . To show (11), we use Theorem 1 and Proposition 2. Namely, we get

Recalling that , we get , which concludes the proof. ∎

Remark 7.

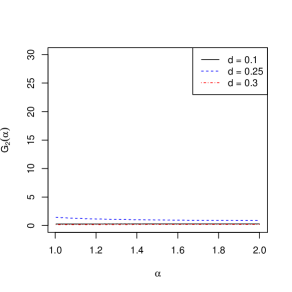

From simulations, we get that the constant from Theorem 6 can be chosen independently of and , and it satisfies the inequality . On the other hand, if the quantile level is smaller than , then the monotonicity condition from Theorem 6 may be violated. Indeed, a numerical check shows that and , while . For transparency, these observations are illustrated in Figure 2. The left panel shows exemplary choices of for which we can see that the map is decreasing while the right panel shows several other cases in which this property is violated.

2.3. Extracting the tail index using a quantile conditional variance ratio

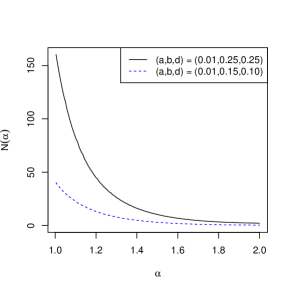

From Theorem 6 combined with Remark 7 we learn that for and adequately chosen tail quantile split values , the function should be monotone. Moreover, one would expect that for a central quantile split , where is relatively close to 0.5, the change of function is smaller when compared to in a sense that for any we get

| (12) |

Thus, given the split , we can define the variance ratio function ,

| (13) |

note that the last equality follows from the fact that for the symmetric -stable distribution we always get . The function is expected to be monotone with respect to . Moreover, noting that the is invariant with respect to the affine transformations of the underlying random variable , one could use values of to extract the value of the tail index within the class of symmetric -stable random variables .

While the direct proof of the monotonicity of (13) is challenging due to the theoretical difficulties stated in Remark 4 and Remark 7, one could numerically verify the monotonicity of (13) for an adequate choice of e.g. by approximating the related integrals by suitable numerical integration procedures. This is illustrated in Figure 3. Having the strict monotonicity of , we can easily recover the value of given the value of by using the inverse transform . This simple intuition will be used to construct a fitting statistic in Section 3.

3. Conditional variance as fitting statistics

In this section we show how to use the variance ratio function introduced in (13) for tail index parameter fitting. First, let us introduce the statistical framework and recall the basic properties of the sample QCV estimator. Given , i.i.d sample , and quantile split , the sample QCV estimator is given by

| (14) |

where denotes the conditional sample mean, corresponds to the th order statistic of the sample, and is the integer part of . It should be noted that (14) can be easily calculated as the sample variance of a sub-sample in which the conditioning is based on order statistics. Moreover, from Jelito and Pitera (2021) and Pitera et al. (2022) we know that estimator is consistent and tends to the Gaussian distribution as .

Second, we introduce and discuss properties of the variance ratio estimator. Given the split for and , we introduce a sample version of (13) by setting

| (15) |

The consistency and asymptotic normality of the statistic given in (14) imply consistency and asymptotic normality of (15), see Theorem 1 in Jelito and Pitera (2021) for the idea of the proof. Moreover, since statistic (14) is location invariant and scale proportional, we get that statistic given in (15) is both location and scale invariant. In general, the statistic (15) may be interpreted as the ratio between tail and central dispersion.

Finally, from Section 2.3 we know that for appropriate choices of , the function defined in (13) is a bijection. Thus, using consistency of , we can take to fit the tail index parameter given the value of . Namely, using the standard statistical plug-in procedure, we set

| (16) |

In the following, we propose two specific choices of the splits that guarantee the bijection property. Namely, we consider the splits and that correspond to variance ratios and , with sample estimators

| (17) |

and output estimators of the tail-index are given by

| (18) |

For brevity, we often refer to and as QCV tail index estimator and QCV tail index estimator, respectively, or simply as estimator and estimator, respectively. The first estimator is introduced to provide a generic fit for any which covers most practical application of the -stable distribution, while the second one is tailored for near-Gaussian cases, where is relatively close to 2. The choice of the split values in both cases was based on numerical experiments. Namely, we decided to choose the parameters which minimise the average root mean square error (RMSE) between true and estimated values of for different sample sizes. In the first case, the average was taken on tail index interval while in the second case we used the narrowed interval .

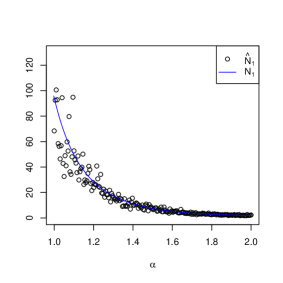

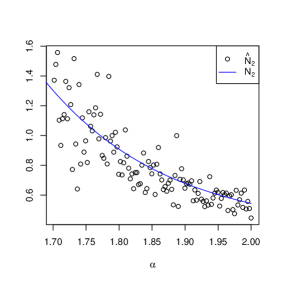

Let us now provide a more extensive comment on the estimation procedure. First, note that the specific values of and are not available in the closed-form. In fact, these quantities are defined as the ratios of the appropriate QCVs, which can be computed explicitly only in specific cases; see the discussion following (7). However, the values of and can be approximated using various numerical integration procedures. In this paper we use the standard trapezoidal rule approximation applied to the -stable distribution PDF. For completeness, in Figure 4 we compare the approximated values for and with sample-based values of and , for . The obtained results indirectly confirm reasonable accuracy of the approximation procedure.

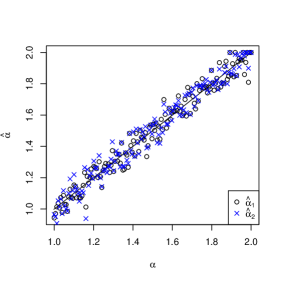

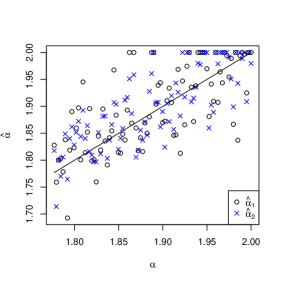

Next, in Figure 5 we compare true values of with the estimates and obtained via (18) for multiple Monte Carlo simulations with samples of size . This serves as a first sanity check indicating that the procedures proposed correctly estimate the underlying parameter. Also, the right panel in Figure 5 suggests that, for close to , the estimator outperforms as the estimates exhibit smaller dispersion. This is consistent with a the rationale behind the construction of , i.e. the fact that this estimator was intended to capture the near-Gaussian cases of the -stable distributions.

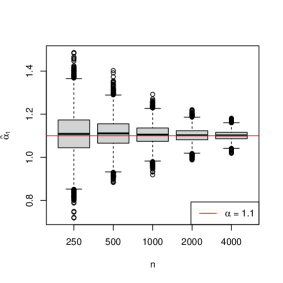

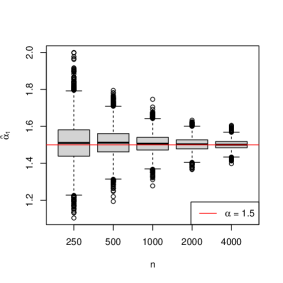

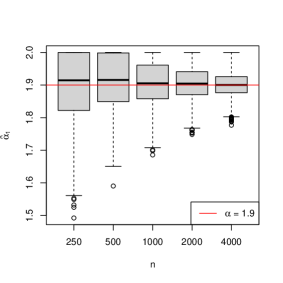

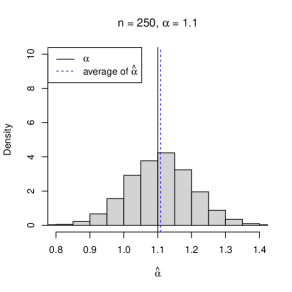

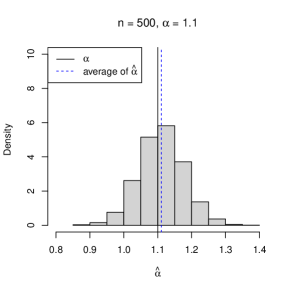

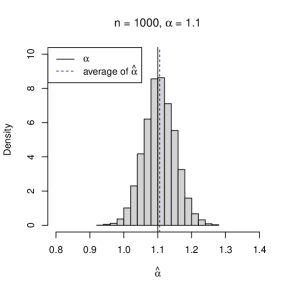

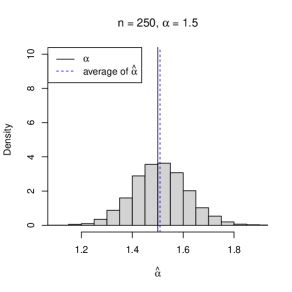

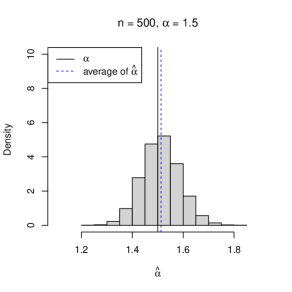

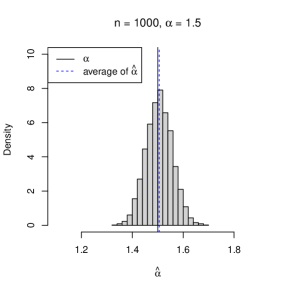

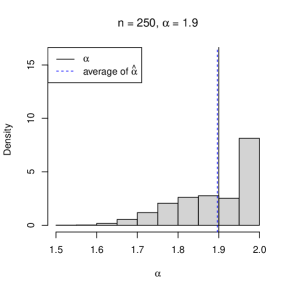

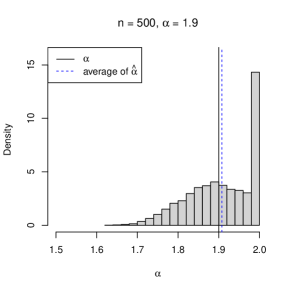

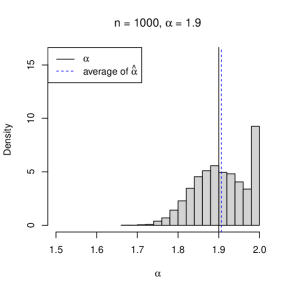

To illustrate the consistency of the proposed estimators, in Figure 6 we show Monte Carlo based box-plots for estimator for various pre-fixed values of and different sample sizes. As expected, the estimated value tends to the true value with decreasing error rate. The statistical properties of the proposed estimators are further investigated in Figure 7 in which, we present the full Monte Carlo distribution of . As expected, the plot shows that the average value of the estimate is close to the true value of and the variance of the estimator decreases as the sample size increases. Also, the distribution of for moderate values of is close to the Gaussian distribution. However, since the tail index cannot exceed 2, the distribution of for close to is naturally asymmetric; asymmetry disappears in the limit when the sample size tends to infinity. The results for are similar and are omitted for brevity.

To sum up, we conclude that the estimators proposed in (18) behave as expected and enjoy multiple useful properties, such as Gaussian-like limiting distribution and small bias. In the next section, we confront the proposed estimators with other benchmark procedures to illustrate that the framework introduced in this paper is competitive and, in many instances, outperforms some commonly used estimation methods.

4. Simulation study and performance evaluation

In this section we study the performance of the estimators and defined in (18) and confront it with the performance of various benchmark alternatives. The evaluation process is Monte Carlo based, where the estimated values for different tail indices and different sample sizes are confronted with each other. In each case, we set strong Monte Carlo size to . Given reference tail-index , the reference sample size , and the reference estimation technique, we use a performance metric given by the root mean squared error (RMSE) defined as

| (19) |

where is the true value of the parameter and is the value estimated on the th sample of size , for .

The remaining part of this section is organized as follows. In Section 4.1, we briefly describe several benchmark estimation procedures discussed in the literature and, in Section 4.2, we compare them with the estimators defined in (18). Next, in Section 4.3, we show that the estimators presented in (18) are in fact robust with respect to asymmetry, so that our estimation technique could also be efficiently applied for , which indicates asymmetry in data.

4.1. Benchmark estimation procedures

In the literature, one can find various approaches used for the estimation of the stability index for the -stable distribution. They can be classified into three main categories, i.e. quantile methods, characteristic function-based algorithms, and maximum likelihood techniques. In this section, we present the three most common approaches that can be considered as representatives of these classes. We focus on the estimation of the stability parameter as this corresponds to the main topic of this paper. However, note that some of the methods discussed could also be used for an estimation of the other parameters of generic stable distributions.

The quantile-based approach for the estimation of parameter in the symmetric case was first proposed in Fama and Roll (1971), where authors applied a simple idea based on the observation that the quantiles of an appropriate large level (e.g. ) of the symmetric -stable distribution decrease monotonically for . This idea was then extended by McCulloch (1986) for the general (non-symmetric) case. In a nutshell, to estimate , McCulloch proposes to compute the following statistic

| (20) |

where is the quantile function of the symmetric -stable distribution. Then, denoting by the sample estimator of (20), we look for the parameter which gives the same sample and theoretical values, i.e. we define the McCulloch Estimator (MCH) as

| (21) |

It should be noted that the value of cannot be determined analytically as the theoretical quantiles of the symmetric -stable distribution are not given in an explicit form. Thus, it was proposed to apply the Monte Carlo simulations and was provided the tabulated values of . In McCulloch (1986) it was proven that if the sample size is large enough, then the method gives reliable estimates of the underlying parameters, see also Chapter 4 in Nolan (2020) for further discussion. For other generalizations of the quantile-based approach see e.g.. Dominicy and Veredas (2013); Huixia et al. (2012); Maymon et al. (2000); Leitch and Paulson (1975).

The second technique is the so-called regression method based on the characteristic function. This approach is a natural choice for the estimation of -stable distribution‘s parameters. The idea of this approach was first introduced by Press (1972). In a nutshell, using (1) with , we get

Thus, the parameter can be recovered as the regression coefficient in the regression of against for from some predetermined set . In practice, given a sample , the characteristic function is estimated by its sample version , and the Regression Estimator (REG) is given as a solution to the least squares problem, i.e.

| (22) |

see e.g. Cizek et al. (2005) for details. Usually, the convergence of Press‘s method to the population values depends on the choice of estimation points, whose selection is problematic. Thus, Koutrouvelis (1980) proposed a much more accurate method which starts with an initial estimate of the parameters and proceeds iteratively until some prespecified convergence criterion is satisfied. This technique is now considered as the classical regression-type approach for the estimation of the -stable distribution‘s parameters. In the literature one can find various extensions and improved versions of this approach; see e.g. Kogon and Williams (1998); Mohammadreza et al. (2017); Arad (1980); Paulson et al. (1975) for details.

The last benchmark method presented in this paper is based on the maximum likelihood approach. For a sample , we calculate the log-likelihood function

where is the PDF of the symmetric -stable distribution. Then, the Maximum Likelihood Estimator (MLE) is given as the maximiser of , i.e.

| (23) |

It is worth highlighting that, usually, the -stable PDF is not available in the explicit form and it needs to be approximated numerically. Thus, the maximum-likelihood-based approaches discussed in the literature differ in the choice of the approximating algorithm, see e.g. DuMouchel (1973); Nolan (2001); Mittnik et al. (1999); Muneya and Akimichi (2006); Brorsen and Yang (1990).

4.2. QCV estimators performance assessment

In this section we confront the RMSE performance of , , MCH, and REG estimators defined in (18), (21), and (22). While the remaining maximum likelihood method (MLE) requires big amount of time-consuming calculations, our preliminary check indicates that this method is outperformed by all procedures in almost all instances. For completeness, in Appendix A we present the comparison of all benchmark methods, including MLE, for reduced number of Monte Carlo simulations, i.e. for . See Table 5 therein for the summary of the results.

All computations are performed in R 4.0.4 and library stabledist is used for simulations. The results for the benchmark estimators (MCH, REG, MLE) are based on our own implementation of the classical algorithms adjusted to the stable symmetric case.

The RMSE results for all considered estimators computed for 100 000 strong Monte Carlo runs for various values of and are presented in Table 1.

| MCH | REG | |||

|---|---|---|---|---|

| 1.0 | 0.091 | 0.124 | 0.092 | 0.091 |

| 1.1 | 0.096 | 0.126 | 0.098 | 0.096 |

| 1.2 | 0.100 | 0.126 | 0.104 | 0.100 |

| 1.3 | 0.103 | 0.125 | 0.112 | 0.104 |

| 1.4 | 0.104 | 0.121 | 0.121 | 0.108 |

| 1.5 | 0.107 | 0.117 | 0.134 | 0.109 |

| 1.6 | 0.110 | 0.112 | 0.149 | 0.110 |

| 1.7 | 0.115 | 0.107 | 0.157 | 0.107 |

| 1.8 | 0.116 | 0.101 | 0.152 | 0.098 |

| 1.9 | 0.104 | 0.084 | 0.139 | 0.077 |

| 2.0 | 0.103 | 0.072 | 0.143 | 0.041 |

| MCH | REG | |||

|---|---|---|---|---|

| 1.0 | 0.063 | 0.087 | 0.064 | 0.064 |

| 1.1 | 0.066 | 0.089 | 0.068 | 0.067 |

| 1.2 | 0.069 | 0.088 | 0.072 | 0.070 |

| 1.3 | 0.071 | 0.087 | 0.077 | 0.072 |

| 1.4 | 0.072 | 0.084 | 0.083 | 0.075 |

| 1.5 | 0.073 | 0.080 | 0.091 | 0.077 |

| 1.6 | 0.075 | 0.076 | 0.105 | 0.077 |

| 1.7 | 0.080 | 0.072 | 0.119 | 0.076 |

| 1.8 | 0.086 | 0.071 | 0.122 | 0.071 |

| 1.9 | 0.083 | 0.066 | 0.111 | 0.060 |

| 2.0 | 0.079 | 0.058 | 0.110 | 0.030 |

| MCH | REG | |||

|---|---|---|---|---|

| 1.0 | 0.043 | 0.058 | 0.045 | 0.045 |

| 1.1 | 0.046 | 0.060 | 0.048 | 0.047 |

| 1.2 | 0.048 | 0.060 | 0.051 | 0.049 |

| 1.3 | 0.050 | 0.059 | 0.054 | 0.051 |

| 1.4 | 0.050 | 0.058 | 0.058 | 0.053 |

| 1.5 | 0.051 | 0.055 | 0.063 | 0.054 |

| 1.6 | 0.051 | 0.052 | 0.072 | 0.054 |

| 1.7 | 0.054 | 0.049 | 0.085 | 0.053 |

| 1.8 | 0.061 | 0.048 | 0.095 | 0.051 |

| 1.9 | 0.067 | 0.052 | 0.089 | 0.044 |

| 2.0 | 0.065 | 0.054 | 0.083 | 0.022 |

We see that for any choice of and , the estimator based on outperforms the McCulloch method. Also, for in small to medium range, the method shows the best results among all compared procedures. For close to 2, the regression and methods provide the best results; the closer we are to the Gaussian case, the better the regression method performs. This shows that while is a good overall fit statistic, is good for the tail-index estimation when is close to .

Next, we want to check whether the QCV method meaningfully complements the existing benchmarks methods and brings some new statistical information. If this is the case, one might refine the existing methodology e.g. by using ensemble learning with the QCV estimator, see e.g. Polikar (2006) and references therein. We decided to focus on comparison between QCV estimators and REG estimator since they exhibited the best performance in Table 1.

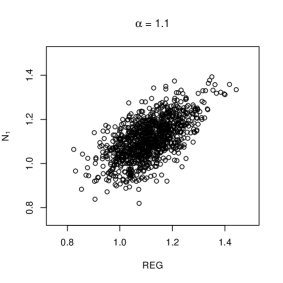

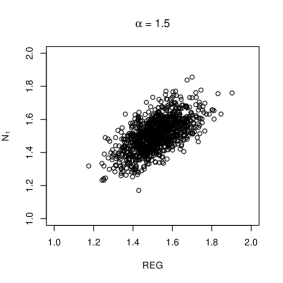

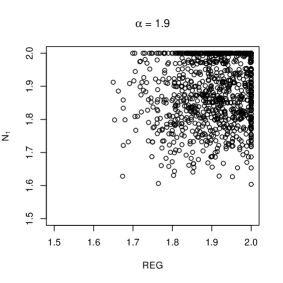

First, we decided to confront the estimated REG and values. Because is based on a different characteristics than the regression method, one would expect certain level of independence between the estimated values. This is indeed the case as shown in Figure 8, in which the results for sample size and are presented. Similar conclusions are true for other sample sizes, and for statistics.

Second, we want to sanity check whether we can refine the estimation procedure by combining the information encoded in the REG and QCV estimators. Given a sample, and estimated values , and , the simplest way to check this is to consider the averaged estimators

which we refer to simply as estimator and estimator. In particular, we can confront the performance of REG, , and method using RMSE metric in a similar way it was done in Table 1. The results of this test are presented in Table 2.

| REG | |||

|---|---|---|---|

| 1.0 | 0.091 | 0.079 | 0.089 |

| 1.1 | 0.096 | 0.085 | 0.095 |

| 1.2 | 0.100 | 0.090 | 0.099 |

| 1.3 | 0.104 | 0.094 | 0.103 |

| 1.4 | 0.108 | 0.096 | 0.104 |

| 1.5 | 0.109 | 0.097 | 0.103 |

| 1.6 | 0.110 | 0.097 | 0.100 |

| 1.7 | 0.107 | 0.094 | 0.094 |

| 1.8 | 0.098 | 0.087 | 0.084 |

| 1.9 | 0.077 | 0.069 | 0.063 |

| 2.0 | 0.041 | 0.061 | 0.047 |

| REG | |||

|---|---|---|---|

| 1.0 | 0.064 | 0.055 | 0.062 |

| 1.1 | 0.067 | 0.060 | 0.067 |

| 1.2 | 0.070 | 0.063 | 0.070 |

| 1.3 | 0.073 | 0.066 | 0.072 |

| 1.4 | 0.075 | 0.067 | 0.073 |

| 1.5 | 0.077 | 0.068 | 0.072 |

| 1.6 | 0.077 | 0.067 | 0.069 |

| 1.7 | 0.076 | 0.066 | 0.065 |

| 1.8 | 0.071 | 0.064 | 0.060 |

| 1.9 | 0.060 | 0.054 | 0.049 |

| 2.0 | 0.030 | 0.047 | 0.037 |

| REG | |||

|---|---|---|---|

| 1.0 | 0.045 | 0.039 | 0.042 |

| 1.1 | 0.047 | 0.042 | 0.046 |

| 1.2 | 0.049 | 0.044 | 0.048 |

| 1.3 | 0.051 | 0.046 | 0.050 |

| 1.4 | 0.053 | 0.047 | 0.051 |

| 1.5 | 0.054 | 0.047 | 0.050 |

| 1.6 | 0.054 | 0.047 | 0.048 |

| 1.7 | 0.054 | 0.046 | 0.045 |

| 1.8 | 0.051 | 0.045 | 0.041 |

| 1.9 | 0.044 | 0.042 | 0.037 |

| 2.0 | 0.022 | 0.037 | 0.033 |

One can note that in almost all instances the averaged estimators and outperforms the REG estimator. It confirms that the QCV estimator contains information that is not encoded in the REG estimator and could be used to refine existing approaches using e.g. ensemble learning. In fact, the simple averaging scheme already leads to a substantial reduction of RMSE.

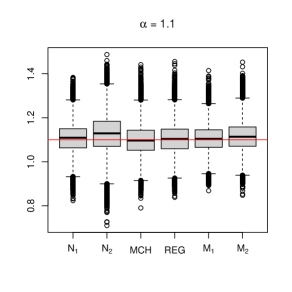

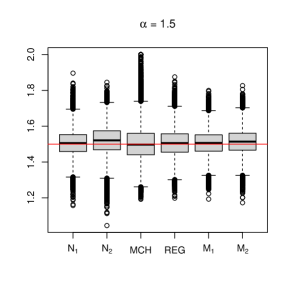

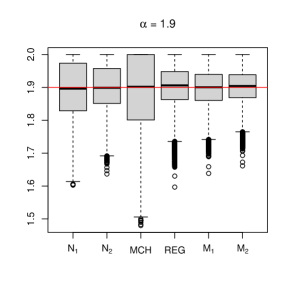

To provide a summary, in Figure 9 we present box-plots of estimated values for all considered estimators, for and . It can be seen that, in each case, the median of estimates for , MCH, and REG are close to the true value of . Next, the dispersion of the results for is smaller than for MCH and comparable with REG. Still, for and , the estimator outperforms the REG estimator in terms of RMSE as already shown in Table 1. Also, the right panel in Figure 9 confirms that the method is particularly effective for close to 2. Finally, looking at and , we see that the best results are obtained by combining REG and QCV approaches.

4.3. Asymmetry robustness

While the methodology in question is created for the symmetric -stable distribution family, in this section we demonstrate that it can also be applied for general -stable distribution, especially when the stability index is relatively close to ; recall that for , the -stable distribution is reduced to the Gaussian distribution which is independent of parameter. To demonstrate the robustness to the parameter change, in Table 3 we present the averages of the estimated parameters based on Monte Carlo simulations for sample size and various combinations of theoretical and parameters from sets and , respectively. The negative values of were not taken into account, as changing the sign of corresponds to the reflection of the random variable value across the Y axis. The results in Table 3 show that, irregardless of , the average estimates of are relatively close to the theoretical values. This suggests that both and estimators can be considered as robust in reference to .

| \ | 0.0 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.1 | 1.105 | 1.106 | 1.108 | 1.110 | 1.113 | 1.114 | 1.115 | 1.115 | 1.113 | 1.112 | 1.110 |

| 1.2 | 1.206 | 1.206 | 1.208 | 1.208 | 1.209 | 1.210 | 1.208 | 1.207 | 1.205 | 1.200 | 1.197 |

| 1.3 | 1.307 | 1.307 | 1.307 | 1.306 | 1.306 | 1.304 | 1.302 | 1.299 | 1.294 | 1.289 | 1.283 |

| 1.4 | 1.406 | 1.406 | 1.404 | 1.404 | 1.402 | 1.400 | 1.396 | 1.390 | 1.384 | 1.379 | 1.371 |

| 1.5 | 1.507 | 1.505 | 1.504 | 1.503 | 1.499 | 1.496 | 1.490 | 1.484 | 1.476 | 1.469 | 1.461 |

| 1.6 | 1.606 | 1.605 | 1.604 | 1.601 | 1.598 | 1.594 | 1.587 | 1.580 | 1.573 | 1.564 | 1.556 |

| 1.7 | 1.709 | 1.707 | 1.706 | 1.702 | 1.699 | 1.693 | 1.687 | 1.681 | 1.675 | 1.667 | 1.658 |

| 1.8 | 1.812 | 1.810 | 1.810 | 1.806 | 1.803 | 1.801 | 1.794 | 1.791 | 1.785 | 1.780 | 1.772 |

| 1.9 | 1.907 | 1.907 | 1.906 | 1.906 | 1.905 | 1.903 | 1.904 | 1.901 | 1.897 | 1.896 | 1.895 |

| 2.0 | 1.971 | 1.971 | 1.970 | 1.971 | 1.971 | 1.971 | 1.970 | 1.971 | 1.971 | 1.971 | 1.971 |

| \ | 0.0 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.1 | 1.109 | 1.112 | 1.115 | 1.119 | 1.123 | 1.124 | 1.127 | 1.129 | 1.129 | 1.129 | 1.127 |

| 1.2 | 1.210 | 1.211 | 1.215 | 1.217 | 1.219 | 1.222 | 1.223 | 1.224 | 1.224 | 1.219 | 1.217 |

| 1.3 | 1.310 | 1.312 | 1.313 | 1.314 | 1.317 | 1.318 | 1.318 | 1.317 | 1.315 | 1.310 | 1.304 |

| 1.4 | 1.409 | 1.411 | 1.411 | 1.413 | 1.414 | 1.414 | 1.412 | 1.409 | 1.404 | 1.400 | 1.393 |

| 1.5 | 1.510 | 1.510 | 1.510 | 1.511 | 1.509 | 1.509 | 1.505 | 1.502 | 1.495 | 1.489 | 1.482 |

| 1.6 | 1.609 | 1.609 | 1.609 | 1.608 | 1.607 | 1.605 | 1.600 | 1.594 | 1.589 | 1.581 | 1.574 |

| 1.7 | 1.710 | 1.709 | 1.709 | 1.707 | 1.706 | 1.701 | 1.697 | 1.691 | 1.686 | 1.679 | 1.670 |

| 1.8 | 1.812 | 1.811 | 1.812 | 1.809 | 1.807 | 1.805 | 1.799 | 1.796 | 1.789 | 1.785 | 1.778 |

| 1.9 | 1.912 | 1.912 | 1.912 | 1.911 | 1.911 | 1.909 | 1.909 | 1.906 | 1.902 | 1.901 | 1.900 |

| 2.0 | 1.981 | 1.981 | 1.981 | 1.981 | 1.981 | 1.981 | 1.980 | 1.981 | 1.981 | 1.981 | 1.982 |

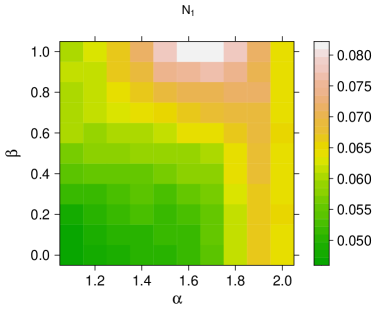

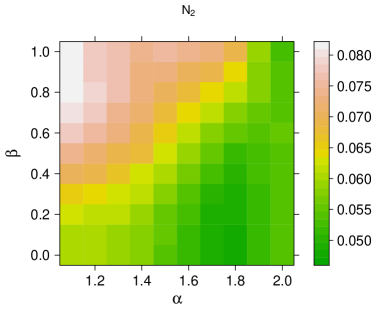

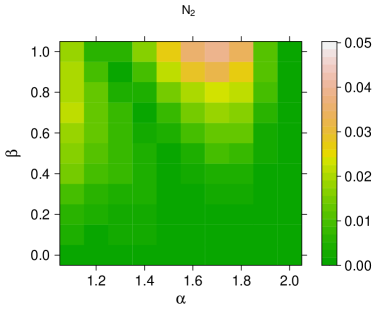

In Figure 10, we demonstrate the RMSE value of the estimated stability index for various combinations of and ; as before, the number of strong Monte Carlo simulations is equal to and sample size equals . The results presented in the level plots indicate relatively small error changes when the methodology is applied to non-symmetric data, that is, for . This effect is visible especially for the parameter close to . The vertical stripes on the level plots for the parameter close to have almost the same colors, which confirms that for this case the and estimators are robust for the parameter. Namely, we observe the same degree of error in Table 10 but from Table 3 we learn that the mean estimated value does not depend on which indicates robustness when combined together.

To further confirm the resistance of the proposed estimation methods to induced skewness, in Figure 11 we show the absolute differences between the averaged estimated values for fixed and , when confronted with symmetric alternative (). More specifically, for each and , we calculate

| (24) |

where is the number of Monte Carlo samples, is the estimate based on a sample , and , , are i.i.d. -element samples from distribution. The left panel shows the results for the estimator based on , while the right panel shows the results for . The results presented in Figure 11 demonstrate how affects the quality of the estimators. We observe that the estimated values of the stability index for the asymmetric data are relatively close to those obtained for the symmetric samples (i.e. when ), with maximal (average) difference equal to for sample size . This confirms that both and estimators are robust in reference to specification.

5. Real data analysis

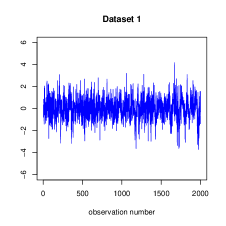

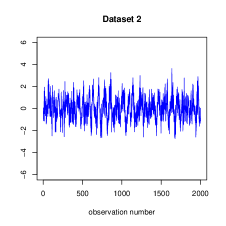

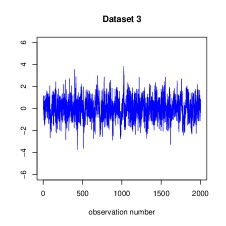

In this section we show how to apply our estimation methodology to real data. Namely, we investigate the data obtained in experiments on the controlled thermonuclear fusion from the device ’’Kharkiv Institute of Physics and Technology‘‘, Kharkiv, Ukraine. The same data set was examined in Burnecki et al. (2012, 2015); Pitera et al. (2022), where detailed description of time series was provided; see Beletskii et al. (2009) for the detailed description of the experimental set-up and the measurement procedure. Here, we only mention that the data describe the floating potential fluctuations (in volts) of plasma turbulence that is characterized by high levels of fluctuations of the electric field and particle density. In the fluctuations, the phenomenon called L-H transition has been observed. The L-H transition is a sudden transition from the low confinement mode (L mode) to a high confinement mode (H mode). During the transition, a regime shift could be observed, which might be associated with the change of the tail index.

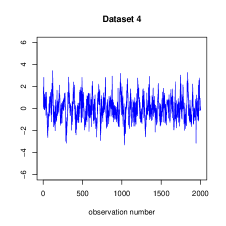

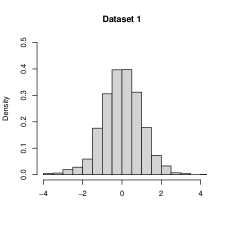

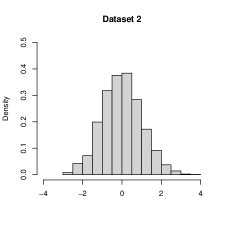

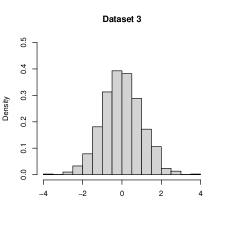

We examine four datasets denoted by Dataset 1, Dataset 2, Dataset 3, and Dataset 4. The Dataset 1 and Dataset 2 describe the floating potential fluctuations for torus radial position cm. Dataset 1 is related to the fluctuations before the transition point, Dataset 2 describes the fluctuation after the transition. Dataset 3 and Dataset 4 describe the potential fluctuations for torus radial position cm. Dataset 3 is related to prior-transition fluctuations (L mode) while Dataset 4 is linked to posterior-transition fluctuations (H mode); see Beletskii et al. (2009) for details. Each dataset contains normalized observations, see Figure 12 for the data visualization (top panels) and histograms (bottom panel).

In Burnecki et al. (2015), a visual test for discriminating between light- and heavy-tailed distributed data was proposed, which pointed out differences between a prior transition point and a posterior transition point. Namely, it was shown that the distributions of Datasets 1 and Dataset 2, or Dataset 3 and Dataset 4, respectively, are slightly different. However, the differences were not visible on the level of the PDFs or CDFs (they were relatively close) and thus, more advanced techniques were applied to distinguish the corresponding distributions. It was demonstrated that Dataset 1 can be described by the -stable distribution with (yet close to 2), Dataset 2 and Dataset 3 can be modeled by the Gaussian distribution, while Dataset 4 belongs to the domain of attraction of the Gaussian law, however, it is non-Gaussian distributed.

The results presented in Burnecki et al. (2015) were confirmed by Pitera et al. (2022), where a goodness-of-fit test for the -stable distribution based on the conditional variance methodology was proposed. It was demonstrated that all considered datasets can be described by the -stable distribution. However, for Dataset 1 and Dataset 4 the corresponding (acceptable) stability indices should lie in and , respectively. For Datasets 2 the Gaussian (or very close to the Gaussian) distribution was confirmed. Finally, for Dataset 3, the was accepted. This may also suggest the -stable distribution with the stability index very close to .

To continue this research, in this paper, we have applied the estimation methodology proposed to the datasets described above. In Table 4, we present the estimated values of together with empirical confidence intervals (CI) obtained using the bootstrap method. Namely, for each dataset, we have created re-samples and calculated empirical confidence intervals by estimating for each of re-sampled data set.

In Table 4, we also demonstrate the estimated values of using the McCulloch, regression, and maximum likelihood methods (denotes as MCH, REG and MLE, respectively). It is worth recalling that all estimation techniques discussed are dedicated for the symmetric -stable distributions, i.e. when the skewness parameter satisfies . However, as it is demonstrated in Figure 12 (bottom panel), the considered datasets exhibit non-symmetric behavior, especially see histograms of Dataset 2, Dataset 3, and Dataset 4. Thus, for comparison, in Table 4 we demonstrate also the results of modified MCH, REG, and MLE estimators, that simultaneously estimate and parameters; in this case, the methods are fitted for generic -stable distribution. For transparency, we denote them as MCH2, REG2, and MLE2, respectively. Similarly as for the symmetric case, we construct the bootstrap confidence intervals. The only exceptions are the MLE and MLE2 methods, as the construction of confidence intervals was too time-consuming. As demonstrated in Section 4.3, even though the and -based methods presented in this paper are dedicated for the symmetric -stable distributed samples, the techniques are robust to the skewness parameter , especially for the stability index close to , which is the case considered in this section.

| Estimated with confidence intervals (CI) | ||||||||

|---|---|---|---|---|---|---|---|---|

| MCH | MCH2 | REG | REG2 | MLE | MLE2 | |||

| Dataset 1 | 1.876 | 1.842 | 2.000 | 1.998 | 2.000 | 1.955 | 1.998 | 1.930 |

| Dataset 1 CI | (1.800, 2.000) | (1.798, 1.964) | (1.786, 1.997) | (1.811, 2.000) | (2.000, 2.000) | (1.876, 1.976) | ||

| Dataset 2 | 2.000 | 1.982 | 2.000 | 2.000 | 2.000 | 2.0000 | 2.000 | 1.996 |

| Dataset 2 CI | (1.917, 2.000) | (1.907, 2.000) | (1.901, 2.000) | (1.905, 2.000) | (2.000, 2.000) | (1.966, 2.000) | ||

| Dataset 3 | 1.973 | 1.997 | 1.924 | 1.922 | 2.000 | 1.985 | 1.922 | 1.990 |

| Dataset 3 CI | (1.873, 2.000) | (1.917, 2.000) | (1.781, 2.000) | (1.783, 2.000) | (2.000, 2.000) | (1.941, 2.000) | ||

| Dataset 4 | 1.952 | 1.983 | 1.970 | 1.971 | 2.000 | 1.955 | 1.971 | 1.968 |

| Dataset 4 CI | (1.848, 2.000) | (1.893, 2.000) | (1.795, 2.000) | (1.798, 2.000) | (2.000, 2.000) | (1.907, 2.000) | ||

The results obtained based on QCV approach confirm the previous conclusions. The results based on and statistics for Dataset 1 clearly indicate the stability index between and . Let us recall that if the parameter is close to , then based should be more adequate; thus, the upper limit of the CI for the -based method is not reliable here. The benchmark techniques dedicated for the symmetric -stable distribution (i.e. MCH, REG and MLE) for Dataset 1 fail, as they indicate the Gaussian distribution. The methods that simultaneously estimate the and parameters (i.e. MCH2, REG2 and MLE2) seem to overestimate the stability index. The maximum likelihood-based technique can be seen as the only exception.

For Dataset 2, identified in the previous research as the Gaussian distributed sample, all analyzed methods confirm this hypothesis and give comparable results. However, the regression-based methods brings the most precise results.

The estimated values of for Dataset 3 coincide with the previous results. The and -based techniques as well as regression-based methods confirm the Gaussianity of the data or the -stable distribution with very close to . The McCulloch-based methods (i.e. MCH and MCH2) seems to underestimate the results. The situation seems to be the same for the maximum likelihood-based approach (i.e. REG and REG2 methods).

For Dataset 4, the -based methodology as well as the REG2 algorithm confirm the previous hypothesis of -stable distribution with . The other considered techniques seem to be less efficient as they overestimate the results.

6. Summary and conclusions

In this paper we show that the quantile conditional variances can be used to construct efficient fitting statistics for the symmetric -stable distributions. The proposed estimators show good performance both on the simulated and real data, and often outperform other benchmark frameworks. The methods proposed in this paper build on the results obtained recently in Pitera et al. (2022) in the context of goodness-of-fit testing. In fact, in this paper we show that the statistical QCV based procedures could be efficiently used also for a parameter estimation. It is worth noting that while the standard moment-fit based methods cannot be directly applied in the -stable case due to the infinite variance problem, our method is based on quantile conditional variances which always exists and consequently can be directly used for fitting. In fact, the approach proposed can be seen as an extension of the method of moments to the infinite-moment framework via second moment conditioning scheme. Also, we want to highlight some form of similarity between our method and the classical McCulloch method, see (20). In a nutshell, in the McCulloch framework the fitting statistic is based on the appropriate function of tail quantiles while the procedures proposed in this paper use the quantile tail variances, see (17). As expected, the quantile conditional variances are more informative than quantiles which results in better performance of the proposed method, see Section 4.2 for details. Next, it is worth mentioning that while we focus on the symmetric case, the QCV ratio based statistic is in fact insensitive to changes in the skewness parameter and our method could be applied to a more generic framework. Finally, we have shown that the approach proposed extract sample characteristics different to the ones extracted by the other benchmark frameworks, so that our approach could be used to refine existing methodologies e.g. via ensembling.

Acknowledgements

Marcin Pitera and Agnieszka Wyłomańska acknowledge support from the National Science Centre, Poland, via project 2020/37/B/HS4/00120. Part of the work of Damian Jelito was funded by the Priority Research Area Digiworld under the program Excellence Initiative – Research University at the Jagiellonian University in Kraków.

References

- (1)

- Akgiray and Lamoureux (1989) Akgiray, V. and Lamoureux, C. G. (1989), ’Estimation of stable-law parameters: A comparative study‘, Journal of Business & Economic Statistics 7(1), 85–93.

- Arad (1980) Arad, R. W. (1980), ’Parameter estimation for symmetric stable distribution‘, International Economic Review 21(1), 209–220.

- Barthelemy et al. (2008) Barthelemy, P., Bertolotti, J. and Wiersma, D. S. (2008), ’A Lévy flight for light‘, Nature 453, 495–498.

- Bednorz et al. (2021) Bednorz, W., Łochowski, R. and Martynek, R. (2021), ’On tails of symmetric and totally asymmetric -stable distributions‘, Probability and Mathematical Statistics 41(2), 321–345.

- Beletskii et al. (2009) Beletskii, A., Grigor‘eva, L., Sorokovoy, E. L. and Romanov, V. S. (2009), ’Spectral and statistical analysis of fluctuations in the sol and diverted plasmas of the uragan-3m torsatron‘, Plasma Physics Reports 35, 818–823.

- Bidarkota et al. (2009) Bidarkota, P. V., Dupoyet, B. V. and McCulloch, J. H. (2009), ’Asset pricing with incomplete information and fat tails‘, Journal of Economic Dynamics and Control 33(6), 1314–1331.

- Brorsen and Yang (1990) Brorsen, B. W. and Yang, S. R. (1990), ’Maximum likelihood estimates of symmetric stable distribution parameters‘, Communications in Statistics - Simulation and Computation 19(4), 1459–1464.

- Burnecki et al. (2012) Burnecki, K., Wyłomańska, A., Beletskii, A., Gonchar, V. and Chechkin, A. (2012), ’Recognition of stable distribution with Lévy index close to 2‘, Phys. Rev. E 85, 056711.

- Burnecki et al. (2015) Burnecki, K., Wyłomańska, A. and Chechkin, A. (2015), ’Discriminating between light- and heavy-tailed distributions with limit theorem‘, PLOS ONE 10, e0145604.

- Chambers et al. (1976) Chambers, J. M., Mallows, C. L. and Stuck, B. W. (1976), ’A method for simulating stable random variables‘, Journal of the American Statistical Association 71(354), 340–344.

- Cizek et al. (2005) Cizek, P., Haerdle, W. and Weron, R. (2005), Statistical Tools for Finance and Insurance, Springer, Berlin.

- de Haan and Resnick (1980) de Haan, L. and Resnick, S. (1980), ’A simple asymptotic estimate for the index of a stable distribution‘, Journal of Royal Statistics Society B, 83–87.

- de Haan and Themido Pereira (1999) de Haan, L. and Themido Pereira, T. (1999), ’Estimating the index of a stable distribution‘, Statistics & Probability Letters 41(1), 39–55.

- Dekkers et al. (1990) Dekkers, A., Einmahl, J. and de Haan, L. (1990), ’A moment estimator for the index of an extreme value distribution‘, The Annals of Statistics 17, 1795–1832.

- Ditlevsen (1999) Ditlevsen, P. D. (1999), ’Observation of alpha-stable noise induced millennial climate changes from an ice-core record‘, Geophysical Research Letters 26, 1441–1444.

- Dominicy and Veredas (2013) Dominicy, Y. and Veredas, D. (2013), ’The method of simulated quantiles‘, Journal of Econometrics 172(2), 235–247.

- DuMouchel (1973) DuMouchel, W. (1973), ’On the asymptotic normality of the maximum-likelihood estimate when sampling from a stable distribution‘, The Annals of Statistics 1.

- Durrett et al. (2011) Durrett, R., Foo, J., Leder, K., Mayberry, J. and Michor, F. (2011), ’Intratumor heterogeneity in evolutionary models of tumor progression‘, Genetics 188, 1–17.

- Escobar-Bach et al. (2017) Escobar-Bach, M., Goegebeur, Y., Guillou, A. and You, A. (2017), ’Bias-corrected and robust estimation of the bivariate stable tail dependence function‘, TEST 26, 284–307.

- Fama and Roll (1971) Fama, E. F. and Roll, R. (1971), ’Parameter estimates for symmetric stable distributions‘, Journal of the American Statistical Association 66(334), 331–338.

- Feller (1966) Feller, W. (1966), An Introduction to Probability Theory and Applications, New York:John Wiley and Sons.

- Garcia et al. (2011) Garcia, R., Renault, E. and Veredas, D. (2011), ’Estimation of stable distributions by indirect inference‘, Journal of Econometrics 161(2), 325–337.

- Ghoudi (2018) Ghoudi, K. (2018), ’Serial independence tests for innovations of conditional mean and variance models‘, TEST 27, 3–26.

- Hebda-Sobkowicz, Zimroz, Pitera and Wyłomańska (2020) Hebda-Sobkowicz, J., Zimroz, R., Pitera, M. and Wyłomańska, A. (2020), ’Informative frequency band selection in the presence of non-Gaussian noise – a novel approach based on the conditional variance statistic with application to bearing fault diagnosis‘, Mechanical Systems and Signal Processing 145, 106971.

- Hebda-Sobkowicz, Zimroz and Wyłomańska (2020) Hebda-Sobkowicz, J., Zimroz, R. and Wyłomańska, A. (2020), ’Selection of the Informative Frequency Band in a Bearing Fault Diagnosis in the Presence of Non-Gaussian Noise – Comparison of Recently Developed Methods‘, Applied Science 10(8), 2657.

- Huixia et al. (2012) Huixia, J. W., Deyuan, L. and Xuming, H. (2012), ’Estimation of high conditional quantiles for heavy-tailed distributions‘, Journal of the American Statistical Association 107(500), 1453–1464.

- Jakubowski and Kobus (1989) Jakubowski, A. and Kobus, M. (1989), ’Alpha-stable limit theorems for sums of dependent random vectors‘, Journal of Multivariate Analysis 29(2), 219–251.

- Janicki and Weron (1994) Janicki, A. and Weron, A. (1994), Simulation and Chaotic Behavior of Alpha-stable Stochastic Processes, Marcel Dekker, Inc., New York.

- Jaworski and Pitera (2016) Jaworski, P. and Pitera, M. (2016), ’The 20-60-20 rule‘, Discrete & Continuous Dynamical Systems-Series B 21(4).

- Jaworski and Pitera (2020) Jaworski, P. and Pitera, M. (2020), ’A note on conditional variance and characterization of probability distributions‘, Statistics & Probability Letters 163, 108800.

- Jelito and Pitera (2021) Jelito, D. and Pitera, M. (2021), ’New fat-tail normality test based on conditional second moments with applications to finance‘, Statistical Papers 62, 2083–2108.

- Khinchine and Lévy (1936) Khinchine, A. Y. and Lévy, P. (1936), ’Sur les lois stables‘, CR Acad. Sci. Paris 202, 374–376.

- Kogon and Williams (1998) Kogon, S. M. and Williams, D. B. (1998), ’Characteristic function based estimation of stable distribution parameters‘, A practical guide to heavy tails: statistical techniques and applications pp. 311–338.

- Kosko and Mitaim (2004) Kosko, B. and Mitaim, S. (2004), ’Robust stochastic resonance for simple threshold neurons‘, Physical Review E 70, 031911.

- Koutrouvelis (1980) Koutrouvelis, I. A. (1980), ’Regression type estimation of the parameters ofstable laws‘, Journal of the Americal Statistical Association 75, 918–928.

- Lan and Toda (2013) Lan, B. L. and Toda, M. (2013), ’Fluctuations of healthy and unhealthy heartbeat intervals‘, Europhysics Letters 102(1), 18002–p1–p6.

- Leitch and Paulson (1975) Leitch, R. A. and Paulson, A. S. (1975), ’Estimation of stable law parameters: Stock price behavior application‘, Journal of the American Statistical Association 70(351a), 690–697.

- Lévy (1924) Lévy, P. (1924), ’Théorie des erreurs. la loi de Gauss et les lois exceptionnelles‘, Bulletin de la Société mathématique de France 52, 49–85.

- Lombardi and Godsill (2006) Lombardi, M. and Godsill, S. (2006), ’On-line bayesian estimation of signals in symmetric -stable noise‘, IEEE Transactions on Signal Processing 54(2), 775–779.

- Lomholt et al. (2005) Lomholt, M. A., Ambjornsson, T. and Metzler, R. (2005), ’Optimal target search on a fast-folding polymer chain with volume exchange‘, Physical Review Letter 95, 260603.

- Majka and Góra (2015) Majka, M. and Góra, P. (2015), ’Non-Gaussian polymers described by alpha-stable chain statistics: Model, effective interactions in binary mixtures, and application to on-surface separation‘, Physical Review E 91, 052602.

- Mandelbrot (1960) Mandelbrot, B. (1960), ’The Pareto-Lévy Law and the distribution of income‘, International Economic Review 1(2), 79–106.

- Matsui and Takemura (2008) Matsui, M. and Takemura, A. (2008), ’Goodness-of-fit tests for symmetric stable distributions—empirical characteristic function approach‘, TEST 17, 546–566.

- Maymon et al. (2000) Maymon, S., Friedmann, J. and Messer, H. (2000), A new method for estimating parameters of a skewed alpha-stable distribution, in ’2000 IEEE International Conference on Acoustics, Speech, and Signal Processing. Proceedings (Cat. No.00CH37100)‘, Vol. 6, pp. 3822–3825 vol.6.

- McCulloch (1986) McCulloch, J. H. (1986), ’Simple consistent estimators of stable distribution parameters‘, Communications in Statistics– Simulation and Computation 15, 1109–1136.

- Mitrinović (1970) Mitrinović, D. S. (1970), Analytic Inequalities, Springer.

- Mittnik et al. (1999) Mittnik, S., Doganoglu, T. and Chenyao, D. (1999), ’Computing the probability density function of the stable paretian distribution‘, Mathematical and Computer Modelling 29(10), 235–240.

- Mohammadreza et al. (2017) Mohammadreza, H. B., Amindavar, H. and Amirmazlaghani, M. (2017), ’Characteristic function based parameter estimation of skewed alpha-stable distribution: An analytical approach‘, Signal Processing 130, 323–336.

- Muneya and Akimichi (2006) Muneya, M. and Akimichi, T. (2006), ’Some improvements in numerical evaluation of symmetric stable density and its derivatives‘, Communications in Statistics - Theory and Methods 35(1), 149–172.

- Nikias and Shao (1995) Nikias, C. and Shao, M. (1995), Signal Processing with Alpha-Stable Distributions and Applications, John Wiley and Sons, New York.

- Nolan (2001) Nolan, J. P. (2001), Maximum Likelihood Estimation and Diagnostics for Stable Distributions, Birkhäuser Boston, Boston, MA, pp. 379–400.

- Nolan (2020) Nolan, J. P. (2020), Univariate Stable Distributions. Models for Heavy Tailed Data, Springer.

- Ortobelli et al. (2016) Ortobelli, S., Lando, T., Petronio, F. and Tichý, T. (2016), ’Asymptotic stochastic dominance rules for sums of i.i.d. random variables‘, Journal of Computational and Applied Mathematics 300, 432–448.

- Paulson et al. (1975) Paulson, A. S., Holcomb, E. W. and Leitch, R. A. (1975), ’The estimation of the parameters of the stable laws‘, Biometrika 62(1), 163–170.

- Peng et al. (1993) Peng, C. K., Mietus, J., Hausdorff, J. M., Havlin, S., Stanley, H. E. and Goldberger, A. L. (1993), ’Long-range anticorrelations and non-Gaussian behavior of the heartbeat‘, Physical Review Letters 70, 1343.

- Pickands (1975) Pickands, J. (1975), ’Statistical inference using extreme order statistics‘, The Annals of Statistics 3, 119–131.

- Pictet et al. (1998) Pictet, O., Michel, M. and Muller, U. (1998), Hill, bootstrap and jacknife estimators for heavy tails. A Practical Guide to Heavy Tails.

- Pitera et al. (2022) Pitera, M., Chechkin, A. and Wyłomanska, A. (2022), ’Goodness-of-fit test for a-stable distribution based on the quantile conditional variance statistics‘, Statistical Methods & Applications 31, 387–424.

- Polikar (2006) Polikar, R. (2006), ’Ensemble based systems in decision making‘, IEEE Circuits and systems magazine 6(3), 21–45.

- Press (1972) Press, S. J. (1972), ’Estimation in univariate and multivariate stable distributions‘, Journal of the American Statistical Association 67(340), 842–846.

- Rachev and Mittnik (2000) Rachev, S. T. and Mittnik, S. (2000), Stable Paretian Models in Finance, New York.

- Resnick (1997) Resnick, S. (1997), ’Heavy tail modeling and teletraffic data‘, The Annals of Statistics 25(5), 1805–1869.

- Samorodnitsky and Taqqu (1994) Samorodnitsky, G. and Taqqu, M. (1994), Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance, Chapman and Hall, New York.

- Sathe and Upadhye (2020) Sathe, A. M. and Upadhye, N. S. (2020), ’Estimation of the parameters of multivariate stable distributions‘, Communications in Statistics - Simulation and Computation 0(0), 1–18.

- Shao and Nikias (1993) Shao, M. and Nikias, C. (1993), ’Signal processing with fractional lower order moments: Stable processes and their application‘, Proceedings of the IEEE 81, 986–1010.

- Sokolov et al. (1997) Sokolov, I. M., Mai, J. and Blumen, A. (1997), ’Paradoxal diffusion in chemical space for nearest-neighbor walks over polymer chains‘, Physical Review Letters 79, 857.

- Teimouri et al. (2018) Teimouri, M., Rezakhah, S. and Mohammadpour, A. (2018), ’Parameter estimation using the em algorithm for symmetric stable random variables and sub-Gaussian random vectors‘, Journal of Statistical Theory and Applications 17, 439.

- Tsihrintzis and Nikias (1996) Tsihrintzis, G. and Nikias, C. (1996), ’Fast estimation of the parameters of alpha-stable impulsive interference‘, IEEE Transactions on Signal Processing 44(6), 1492–1503.

- Wegman et al. (1989) Wegman, E. J., Schwartz, S. C. and Thomas, J. B., eds (1989), Topics in Non-Gaussian Signal Processing, New York: Springer.

- Wyłomańska et al. (2020) Wyłomańska, A., Burnecki, K. and Iskander, D. R. (2020), ’Omnibus test for normality based on the edgeworth expansion‘, PLoS ONE (15(6): e0233901).

- Yu et al. (2013) Yu, G., Li, C. and Zhang, J. (2013), ’A new statistical modeling and detection method for rolling element bearing faults based on alpha-stable distribution‘, Mechanical Systems and Signal Processing 41, 155–175.

- Żak et al. (2016) Żak, G., Wyłomańska, A. and Zimroz, R. (2016), ’Data-driven vibration signal filtering procedure based on the alpha-stable distribution‘, Journal of Vibroengineering 18(2), 826–837.

- Żak et al. (2017) Żak, G., Wyłomańska, A. and Zimroz, R. (2017), ’Data driven iterative vibration signal enhancement strategy using alpha stable distribution‘, Shock and Vibration 2017, Article ID 3698370.

- Zieliński (2001) Zieliński, R. (2001), ’A reparameterization of the symmetric -stable distributions and their dispersive ordering‘, Theory of Probability & Its Applications 45(2), 357–358.

Appendix A Additional tables

In this section we present additional tables with numerical results. This complements the analysis in Section 4.2 and Section 4.3.

In Table 5 we present the RMSE metrics for , , the McCulloch method (MCH), the regression method (REG), and the maximum likelihood method (MLE). The results complements the outcomes presented in Table 1 by adding the metrics for the maximum likelihood method. As seen in Table 5, the MLE method exhibits relatively poor performance, particularly for in moderate to high range. Taking into account this observation and the fact that the results for MLE requires high number of time-consuming calculations, we decided not to include the outcomes for MLE in Section 4.2.

| N1 | N2 | MCH | REG | MLE | |

|---|---|---|---|---|---|

| 1.0 | 0.089 | 0.123 | 0.091 | 0.091 | 0.091 |

| 1.1 | 0.096 | 0.124 | 0.097 | 0.094 | 0.099 |

| 1.2 | 0.100 | 0.126 | 0.106 | 0.100 | 0.108 |

| 1.3 | 0.101 | 0.125 | 0.114 | 0.103 | 0.114 |

| 1.4 | 0.102 | 0.121 | 0.118 | 0.105 | 0.118 |

| 1.5 | 0.104 | 0.115 | 0.129 | 0.102 | 0.135 |

| 1.6 | 0.111 | 0.112 | 0.145 | 0.113 | 0.146 |

| 1.7 | 0.112 | 0.105 | 0.154 | 0.104 | 0.156 |

| 1.8 | 0.115 | 0.099 | 0.150 | 0.098 | 0.150 |

| 1.9 | 0.102 | 0.083 | 0.134 | 0.078 | 0.131 |

| 2.0 | 0.103 | 0.070 | 0.148 | 0.042 | 0.145 |

| MCH | REG | MLE | |||

|---|---|---|---|---|---|

| 1.0 | 0.061 | 0.085 | 0.063 | 0.064 | 0.063 |

| 1.1 | 0.068 | 0.088 | 0.069 | 0.067 | 0.071 |

| 1.2 | 0.067 | 0.084 | 0.070 | 0.069 | 0.070 |

| 1.3 | 0.070 | 0.084 | 0.078 | 0.071 | 0.077 |

| 1.4 | 0.074 | 0.087 | 0.083 | 0.075 | 0.083 |

| 1.5 | 0.073 | 0.080 | 0.090 | 0.076 | 0.091 |

| 1.6 | 0.074 | 0.077 | 0.103 | 0.080 | 0.103 |

| 1.7 | 0.080 | 0.070 | 0.116 | 0.076 | 0.116 |

| 1.8 | 0.084 | 0.069 | 0.121 | 0.070 | 0.120 |

| 1.9 | 0.083 | 0.067 | 0.110 | 0.061 | 0.108 |

| 2.0 | 0.075 | 0.053 | 0.108 | 0.031 | 0.105 |

| N1 | N2 | MCH | REG | MLE | |

|---|---|---|---|---|---|

| 1.0 | 0.043 | 0.060 | 0.045 | 0.045 | 0.044 |

| 1.1 | 0.046 | 0.060 | 0.049 | 0.049 | 0.050 |

| 1.2 | 0.048 | 0.059 | 0.050 | 0.049 | 0.050 |

| 1.3 | 0.050 | 0.061 | 0.055 | 0.052 | 0.054 |

| 1.4 | 0.051 | 0.060 | 0.059 | 0.054 | 0.059 |

| 1.5 | 0.052 | 0.056 | 0.062 | 0.052 | 0.063 |

| 1.6 | 0.052 | 0.053 | 0.072 | 0.056 | 0.072 |

| 1.7 | 0.054 | 0.049 | 0.086 | 0.053 | 0.085 |

| 1.8 | 0.059 | 0.046 | 0.092 | 0.050 | 0.092 |

| 1.9 | 0.067 | 0.052 | 0.090 | 0.045 | 0.089 |

| 2.0 | 0.060 | 0.050 | 0.080 | 0.023 | 0.077 |

In Table 6 we present the RMSE metrics of the estimated stability index for various combinations of and . The results are used to produce Figure 10.

| \ | 0.0 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.1 | 0.046 | 0.047 | 0.048 | 0.051 | 0.055 | 0.057 | 0.060 | 0.060 | 0.060 | 0.061 | 0.061 |

| 1.2 | 0.048 | 0.049 | 0.051 | 0.052 | 0.055 | 0.058 | 0.059 | 0.061 | 0.061 | 0.062 | 0.062 |

| 1.3 | 0.049 | 0.050 | 0.052 | 0.053 | 0.056 | 0.058 | 0.061 | 0.062 | 0.064 | 0.066 | 0.066 |

| 1.4 | 0.050 | 0.050 | 0.052 | 0.054 | 0.056 | 0.059 | 0.061 | 0.064 | 0.066 | 0.069 | 0.072 |

| 1.5 | 0.051 | 0.051 | 0.052 | 0.053 | 0.056 | 0.059 | 0.062 | 0.065 | 0.069 | 0.074 | 0.078 |

| 1.6 | 0.051 | 0.052 | 0.053 | 0.055 | 0.057 | 0.059 | 0.064 | 0.067 | 0.071 | 0.076 | 0.082 |

| 1.7 | 0.054 | 0.055 | 0.055 | 0.056 | 0.058 | 0.061 | 0.064 | 0.068 | 0.071 | 0.076 | 0.081 |

| 1.8 | 0.062 | 0.062 | 0.062 | 0.062 | 0.064 | 0.064 | 0.066 | 0.069 | 0.072 | 0.075 | 0.078 |

| 1.9 | 0.066 | 0.066 | 0.067 | 0.066 | 0.068 | 0.068 | 0.069 | 0.069 | 0.071 | 0.071 | 0.072 |

| 2.0 | 0.064 | 0.064 | 0.066 | 0.065 | 0.065 | 0.064 | 0.065 | 0.065 | 0.064 | 0.065 | 0.064 |

| \ | 0.0 | 0.1 | 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.1 | 0.060 | 0.060 | 0.063 | 0.066 | 0.070 | 0.074 | 0.078 | 0.080 | 0.081 | 0.082 | 0.081 |

| 1.2 | 0.060 | 0.060 | 0.062 | 0.064 | 0.069 | 0.072 | 0.075 | 0.078 | 0.079 | 0.078 | 0.078 |

| 1.3 | 0.059 | 0.059 | 0.061 | 0.063 | 0.066 | 0.069 | 0.072 | 0.075 | 0.076 | 0.077 | 0.076 |

| 1.4 | 0.058 | 0.057 | 0.059 | 0.061 | 0.063 | 0.067 | 0.069 | 0.071 | 0.072 | 0.073 | 0.075 |

| 1.5 | 0.054 | 0.055 | 0.056 | 0.057 | 0.060 | 0.062 | 0.065 | 0.068 | 0.070 | 0.073 | 0.075 |

| 1.6 | 0.052 | 0.052 | 0.053 | 0.054 | 0.056 | 0.059 | 0.062 | 0.064 | 0.067 | 0.071 | 0.075 |

| 1.7 | 0.049 | 0.049 | 0.049 | 0.050 | 0.052 | 0.055 | 0.058 | 0.062 | 0.064 | 0.069 | 0.073 |

| 1.8 | 0.048 | 0.048 | 0.048 | 0.049 | 0.050 | 0.052 | 0.055 | 0.057 | 0.062 | 0.064 | 0.069 |

| 1.9 | 0.052 | 0.052 | 0.052 | 0.052 | 0.053 | 0.053 | 0.054 | 0.055 | 0.058 | 0.058 | 0.059 |

| 2.0 | 0.054 | 0.054 | 0.054 | 0.054 | 0.054 | 0.054 | 0.055 | 0.054 | 0.054 | 0.054 | 0.053 |