Uncertainty Quantification of MLE for Entity Ranking with Covariates

Abstract

This paper concerns with statistial estimation and inference for the ranking problems based on pairwise comparisons with additional covariate information such as the attributes of the compared items. Despite extensive studies, few prior literatures investigate this problem under the more realistic setting where covariate information exists. To tackle this issue, we propose a novel model, Covariate-Assisted Ranking Estimation (CARE) model, that extends the well-known Bradley-Terry-Luce (BTL) model, by incorporating the covariate information. Specifically, instead of assuming every compared item has a fixed latent score , we assume the underlying scores are given by , where and represent latent baseline and covariate score of the -th item, respectively. We impose natural identifiability conditions and derive the - and -optimal rates for the maximum likelihood estimator of and under a sparse comparison graph, using a novel ‘leave-one-out’ technique (Chen et al., 2019) . To conduct statistical inferences, we further derive asymptotic distributions for the MLE of and with minimal sample complexity. This allows us to answer the question whether some covariates have any explanation power for latent scores and to threshold some sparse parameters to improve the ranking performance. We improve the approximation method used in Gao et al. (2021) for the BLT model and generalize it to the CARE model. Moreover, we validate our theoretical results through large-scale numerical studies and an application to the mutual fund stock holding dataset.

1 Introduction

Ranking plays an essential role in many real-world applications. For example, it is crucial in individual choice (Luce, 2012), psychology (Thurstone, 1927, 2017), recommendation systems (Baltrunas et al., 2010; Li et al., 2019), and many others. The ranked items such as sports teams (Massey, 1997; Turner and Firth, 2012), scientific journals (Stigler, 1994), web pages (Dwork et al., 2001), election candidates (Plackett, 1975), or even movies (Harper and Konstan, 2015) will not only illustrate their qualities but also affect people’s future choices. Thus, the ranking problem has been extensively studied in statistics, machine learning, and operations research, etc.; see for example (Hunter, 2004; Richardson et al., 2006; Jang et al., 2018; Chen et al., 2019, 2022b, 2022a; Liu et al., 2022; Gao et al., 2021) for more details.

Among various models for the ranking problem, the most well-known one is the Bradley-Terry-Luce (BTL) model (Bradley and Terry, 1952; Luce, 2012), which assumes the existence of scores of compared items such that the preference between item and item is given by

The underlying assumption of this BTL model is the scores of compared items are fixed and do not explicitly use their attributes. However, in many real-world applications, covariate information often exists and this heterogeneity needs to be incorporated. For example, US News and Times Higher Education consider many characteristics of universities, such as international research reputation, teaching quality, the ratio between students and professors, and citations to conduct global university rankings. In addition, in NBA basketball competitions, the final rank of a team is also affected by its underlying attributes, such as the ability to defend, make a three-point shot, etc. Thus, a crucial question still remains open:

“Can one design a provably efficient mechanism for ranking by incorporating features of compared items and conduct associated high-dimensional statistical inference?”

To this end, we introduce a new model that incorporates feature information of items into the BTL model, called the Covariate-Assisted Ranking Estimation (CARE) model. Specifically, we address covariate heterogeneity by assuming the underlying score (ability) of the -th item is given by where captures the covariate effect and is the intrinsic score that can not be explained by the covariate. In this case, the outcome of pairwise comparison is modeled as

We do not assume that all pairs are compared. Rather, each pair is selected at random for comparison. In specific, we let the underlying comparison graph be the Erdős-Rényi random graph with edge probability . In addition, once a pair is selected, they are compared times. In this work, we consider the fixed design in the sense that the randomness only comes from results of comparisons.

There are several challenges in studying statistical inference for our CARE model. First, our model incorporates feature information into the original BTL model, not only the underlying scores but also shall be estimated and analyzed in a novel way. This also gives rise to the issue of identifiability. Second, given consistent estimators, it remains open to quantify these key components’ uncertainty. Most existing work focuses more on deriving statistical rates of covergence for those underlying scores via various estimators in the BLT model to achieve specific rank recoveries such as top-K and partial recovery (Chen et al., 2019, 2022b, 2022a). There are few results established for the inference of the BTL model (Gao et al., 2021; Liu et al., 2022), letting alone the uncertainty quantification for the more general BTL model with covariates (CARE model).

In our work, we resolve the first challenge by designing a novel constrained maximum likelihood estimator (MLE) which efficiently estimates the underlying scores and . With some proper initialization, the MLE can be solved by simply running the projected gradient descent algorithm. By leveraging the ‘leave-one-out’ technique (Chen et al., 2019), we prove that the statistical rate of convergence of the MLE of the intrinsic scores and overall scores in -norm are of order in which is the dimension of the observed covariates. These statistical rates reduce to the standard minimax rates for estimating the BTL model when no covariate exists, namely, (Chen et al., 2019, 2022b, 2022a).

To take on the second challenge, namely, depicting the asymptotic distribution of the MLE, we first approximate the MLE by the minimizer of the quadratic approximation of our joint likelihood function, whose uncertainty is easier to depict. The critical difficulty lies in quantifying this approximation error. To tackle this issue, we then utilize the ‘leave-one-out’ technique to derive novel proof frameworks, which is valid under the minimal sample complexity up to logarithm terms. In a more specific BLT model, the seminal work by Gao et al. (2021) leverages the minimizers of the more restricted diagnonal quadratic approximations of their marginal likelihoods to approximate the MLE. They capture the approximation errors based on a ‘leave-two-out’ technique. In contrast, in this work, we utilize the minimizer of the quadratic approximation of the joint likelihood to approximate the MLE and achieve a tighter approximation error compared with Gao et al. (2021).

Finally, we conduct numerical experiments to corroborate our theory. The performance of the model is also convincingly illustrated by analysis of the multual fund holding data. From the perspective of stock selection and return prediction, our proposed covariate-assisted BTL model (CARE) outperforms the original BTL model in many aspects.

To summarize, contributions of this work are of multiple folds. First, we propose a new CARE model that is able to incorporate the feature information into the classical BTL model. Second, we design a novel technical device to analyze the MLE of parameters in CARE. Specifically, we derive - and - optimal statistical rates for the MLE of and , respectively. Moreover, we also conduct uncertainty quantification for our MLE, where we improve the approximation errors given in Gao et al. (2021) and derive more general asymptotic results. Furthermore, our results hold even on the sparse comparison graph, i.e. the probability of pairwise comparison up to logarithm terms, with minimal sample complexity. Finally, we illustrate our methods via large-scale numerical studies on synthetic and real data. Numerical results lends further support of our proposed CARE model over the original BTL model.

1.1 Prior Arts

Ranking problems based on pairwise comparison for parametric and non-parametric models have received much attention. For the BTL model, Hunter (2004) studies its variants and establishes theoretical properties using a minorization-maximization algorithm. Chen and Suh (2015) use a two-step method to study the BTL model which is provably optimal in terms of sample complexity. Jang et al. (2016) leverage the spectral method to recover the top-K items with only minimal samples. In addition, Negahban et al. (2012) propose an iterative rank aggregation algorithm named Rank Centrality to recover the underlying scores of the BTL model in optimal - statistical rate. In the sequel, Chen et al. (2019) derive both - and - optimal statistical rates of those underlying scores and prove that the regularzied MLE and spectral method are both optimal for recovering top-K items when the conditional number is a constant. Furthermore, Chen et al. (2022b) prove that for partial recovery, MLE is optimal but the spectral method is not when we have a general conditional number. They further extend their frameworks to study the full ranking problem (Chen et al., 2022a). It is worth noting that the aforementioned prior arts mostly focus on studying the parametric BTL model. There is also a series of work that studies certain non-parametric variants of the BTL model. For instance, Shah and Wainwright (2017) develop a counting-based algorithm to recover top- ranked items under the nonparametric stochastically transitive model. For more details on the non-parametric comparison models, see Shah et al. (2016); Shah and Wainwright (2017); Chen et al. (2017); Pananjady et al. (2017) and the references therein.

Going beyond the pairwise comparison, there also exist other works which study ranking problems using -way comparisons . The first well known model is the Plackett-Luce model and its variants (Plackett, 1975; Guiver and Snelson, 2009; Cheng et al., 2010; Hajek et al., 2014; Maystre and Grossglauser, 2015; Szörényi et al., 2015; Jang et al., 2018; Fan et al., 2022). For instance, a closely related work is Jang et al. (2018), who study the Plackett-Luce model under a uniform hyper-graph. They divide -way compared data into pairs and utilize the spectral method to derive the - statistical rate of underlying scores. They further provide a lower bound for sample complexity to recover top-K items in the Plackett-Luce model. Another well known model is the Thurstone model (Thurstone, 1927), which admits the Plackett-Luce model as a special case; see Thurstone (1927); Guiver and Snelson (2009); Hajek et al. (2014); Vojnovic and Yun (2016); Jin et al. (2020) for more details.

The aforementioned literature mainly focuses on non-asymptotic statistical consistentcy results for the underlying scores of compared items through various ranking frameworks. However, the limiting distributional results for ranking models still remain highly under-explored. There are several results on the asymptotic distributions for the ranking scores in the BTL model. For instance, Simons and Yao (1999) derive the asymptotic normality of the MLE of the BTL model in the scenario where all pairs of comparison are fully conducted (i.e, ). Han et al. (2020) further extend the results to the regime where the comparison graph (Erdős-Rényi random graph) is dense but not fully connected, i.e. . In addition, recently, Liu et al. (2022) propose a Lagrangian debiasing method to derive asymptotic distribution for ranking scores, where they allow sparse comparison graph but require comparison times to be larger than Moreover, Gao et al. (2021) utilize a ‘leave-two-out’ trick to derive asymptotic distributions for ranking scores with optimal sample complexity in the regime where the comparison graph is sparse, i.e. up to logarithm terms.

All afforementioned models and methods mainly study the estimation and uncertainty quantification for ranking models without considering any individual feature information. Yet, covariate data exist in most applications and this results in additional challenges in technical derivations and computation. This paper takes up this challenge by conducting estimation and uncertainty quantification for our CARE model in a sparse comparison graph with minimal requirements of the sample complexity.

1.2 Notation

We introduce some useful notations before proceeding. We denote by for any positive integer . For any vector and , we use to represent the vector norm of . In addition, the inner product between any pair of vectors and is defined as the Euclidean inner product . For vector and index , we denote by the vector we get by deleting the -th element in . For any given matrix , we use , , and to represent the operator norm, Frobenius norm, nuclear norm and two-to-infinity norm of matrix respectively. Moreover, we use or to denote positive semidefinite or negative semidefinite of matrix . Moreover, we use the notation or for non-negative sequences and if there exists a constant such that . We use the notation for non-negative sequences and if there is a constant such that . For simplicity, we define function . We write if and . For matrix , we denote by its pseudoinverse (Banerjee, 1973).

1.3 Roadmap

The remaining paper is organized as follows. We describe the problem formulation for our BTL model with covariate and derive the corresponding maximum likelihood estimators for its involved parameters in §2. In §3, we establish the statistical estimation results for our MLE. In §4, we further conduct uncertainty quantification for the obtained MLE. In §5, we corroborate our theoretical results by conducting large-scale numerical studies via both synthetic and real dataset.

2 Model Formulation

In this section, we introduce the Covariate-Assisted Ranking Estimation (CARE) model which incorporates covariate information into the BTL model. In the tranditional BLT model (Bradley and Terry, 1952; Luce, 2012), it is assumed that each item has a latent score and the outcomes of comparisons are modeled as the realizations of the Bernoulli trials:

| (2.1) |

It is worth mentioning that the function in (2.1) can be replaced by any increasing differentiable functions.

In many applications, one observes individual features and would like to incomporate them for conducting more accurate ranking. As an extension of the parameterization (Chen et al., 2019, 2022b, 2022a), we model the scores as for . The linear term captures the part of the scores explained by the variables and represents the intrinsic score that can not be explained by the covariate . This leads to model the outcomes of comparisons as the Bernoulli trials with probabilities

| (2.2) |

We call this model as Covariate Assisted Ranking Estimation (CARE) model.

We do not assume that all pairs are compared, but only those in the comparison graph . Here and represent the collections of vertexes ( items) and edges, respectively. More specifically, if and only if item and item are compared. Throughout our paper, the comparison graph is assumed to follow the Erdős-Rényi random graph (Erdos et al., 1960) where each edge appears independently with probability . In short, items i and j with are compared at random with probability .

In addition, for any , we observe independent and identically distributed realizations from the Bernoulli random variables

Let and , where stand for the canonical basis vectors in and Then, the log-likelihood function conditioned on is given by

where is a sufficient statistic. The identifiability question arises naturally since we overparametrize the problem. To remedy this issue, we restrict the parameter space of onto some constrained set that has a natural interpretation. In specific, we denote let and consider the constrained set . Under these identifiability constraints, if the true parameter vector , the identifiability condition implies that and with . It admits clear interpretation: represents the scores that be captured by the covariates whereas and the represents the residual scores (or equivalently intrinsic scores) that can not be explained by the involved features. We denote by a matrix by padding matrix to , i.e. and . As a result, can be also written as . Denote by the projection matrix onto space .

Given the aforementioned identifiable condition, we consider the following constrained maximum likelihood estimator (MLE)

| (2.3) |

where

| (2.4) |

Note that when there is no covariate , we have and the scores are identifiable up to a constant shift. Therefore, our formulation includes those studies of BTL model without covariate information as special cases (Chen et al., 2019, 2022b, 2022a; Gao et al., 2021).

The inference question arises naturally if some covariates can explain the underlying scores, namely if some or all components of are statistically significant. Similarly, one might ask if the covariates are adequate for determining the underlying scores by testing whether some or all components of are zero. In general, we would expect the variations among the components of is much smaller than the original scores . This enables us to improve data predictions by shrinking or regularizing the estimate of

3 Rate of Convergence of Maximum Likelihood Estimator

In this section, we show the statistical consistency results for the maximum likelihood estimator in (2.3). Before proceeding to the main results, we begin with introducing several key assumptions on the design matrix. First, we assume the projected matrix satisfies the following incoherence condition.

Assumption 3.1.

[Incoherence Condition] Assume that there exists a positive constant such that

To demonstrate the rationality behind Assumption 3.1, we first note that the . Therefore, a sufficient condition for this assumption to hold is when the rows of are nearly balanced, with row sum of squares all of order or smaller. When there does not exist the covariate (i.e. ), we have In this scenario, this assumption holds automatically with The following results of this paper are established under this incoherence condition.

We next introduce a key assumption on the covariates which guarantees a well-behaved landscape of the loss function as well as good statistical properties of the MLE estimator. In specific, we put the following assumption on .

Assumption 3.2.

Assume that there exists positive constants and such that

where is the operator norm of and

In this Assumption 3.2, we assume that is well-behaved in all directions inside our parameter space , namely, both of its largest and smallest eigenvalues are of order . When there is no covariate (i.e., ), then and Assumption 3.2 holds naturally with (Chen et al., 2019).

Assumption 3.2 is made implicitly based on the rescaled as it concatenated with vector . In order to meet the requirements, we rescale to , where is a positive number such that for all after the transformation. The likelihood function and prediction are not affected by the scaling but this normalization facilitates us with scaling issue in the technical derivations. Content that follows will be based on the scaled data and parameters.

We introduce the condition number of this problem as

where , which extends the condition number in Chen et al. (2019) when there does not exist covariate. With all aforementioned assumptions in hand, we next present our first main theorem on the statistical rates of convergence of the MLE . Recall that we assume that the true parameter vector , without loss of generality.

Theorem 3.1.

(Rate of convergence) Suppose for some and . Consider for any absolute constants . Let be the solution of the MLE given in (2.3). Then with probability at least , we have

where .

Recall that we rescaled the covariates such that . This scaling has an impact on the definition of and influences its rate. This explains why converges slower. However, as explained above, this does not impact on the estimation of the individual score, as shown in Theorem 3.1.

Remark 3.1.

Theorem 3.1 asserts that the statistical errors of the maximum likelihood estimators for and the ranking scores are of the order . This is the best rate one can hope if one ignores the logarithmic term. To understand this, we note that the expected number of the comparisons involving item is for all . Besides, the parameter only appears in the model of the comparisons when item is involved. Thus, if we ignore the logarithmic term and consider the case with a finite , the best estimation error of is for , which matches the obtained bound for . Similar reasoning applies to estimating ranking scores . When there is no covariates (i.e., ), our results in Theorem 3.1 reduces to the minimax optimal statistical error bound for MLE in -norm (Chen et al., 2019, 2022b, 2022a).

Remark 3.2.

Following a similar proof, it holds that

which are the relative -statistical rates of the intrinsic scores and overall scores , respectively. Combining this relative statistical rate in -norm with that in -norm mentioned in Theorem 3.1, we conclude that the estimation errors of latent scores and overall scores spread out across all items.

We finally discuss our assumption on the sparseness of our comparison graph. Note that when the comparison graph is disconnected, there are at least two groups that have no cross-group comparisons and consistent ranking is impossible. It is well-known that the Erdős-Rényi random graph is disconnected when and connected when with high probability for any In our work, we only require the sampling probability to satisfy , which meets the minimal requirements for the connectivity of the Erdős-Rényi random graph. Therefore, the statistical rate results given in Theorem 3.1 hold even under the sparse regime of the comparison graph.

4 Uncertainty Quantification of MLE

Most existing works on ranking mainly study the first order asymptotic behavior of their estimators (Hunter, 2004; Chen and Suh, 2015; Jang et al., 2016; Shah and Wainwright, 2017; Chen et al., 2019, 2022a). Deriving limiting distributional results in ranking models is important for uncertainty quantification but rarely conducted, especially when covariate information is incorporated into the ranking problem.

This section devotes to understanding the sampling variability of the MLE under the CARE model. Directly studying the asymptotic behavior of is very challenging. To address this issue, we approximate by considering

| (4.1) |

here is the quadratic expansion of the loss function around given by

| (4.2) |

According to this definition, can also be given by the following linear equations

Observe that serves as an candidate approximator of whose uncertainty is easier to quantify according to Berry-Esseen theorem (Berry, 1941; Esseen, 1942). It is not a statistical estimator but an auxillary random variable that we used for the technical proof. The critical difficulty falls in proving that the difference is negligible compared to under certain conditions. To accommodate this, we derive novel proof frameworks by leveraging the ‘leave-one-out’ (Chen et al., 2019, 2021) technique to control the approximation error in -norm and in -norm. The upper bounds are summarized in the following Theorem 4.1.

Theorem 4.1.

(Approximation error) Under the assumptions of Theorem 3.1, if and for some fixed constant , then with probability at least we have

Remark 4.1.

The assumptions and for some fixed constant are mild. When and are bounded, they hold when . This matches the lower bound of the sampling probability to ensure the connectivity of the Erdős-Rényi random graph, which is a necessary requirement for item ranking. Besides, is also required by the consistency results of our estimator according to Theorem 3.1.

Next, we utilize Berry-Essen theorem (Berry, 1941; Esseen, 1942) to derive the asymptotic distribution of the linear conbinaitons of , respectively. Since it holds for any linear combinations, the result applies to any finite dimensional distribution of .

Theorem 4.2.

(Asymptotic normality of MLE) Given , let be the projection of onto linear space . Under the assumptions of Theorem 4.1, we have the following decomposition

where

with probability exceeding (randomness comes from and ) and

with probability exceeding (randomness comes from ). Combining the approximation error and asymptotic distribution together, and by taking all randomness into consideration, we further obtain

In Theorem 4.2, we first obtain the distributional guarantee of , conditioned on the comparison graph , in the sense that we only take the randomness of into consideration. These results are stronger than the distributional guranttees which make use of all the randomness from and , by the dominated convergence theorem. Besides, combining with the approximation results, we further derive distributional guarantees for linear combinations of by taking all the randomness of into consideration.

Moreover, recall that we have scaled the covariates to satisfy in the data preprocessing step. Then, if and are bounded, the asymptotic normality holds when

| (4.3) |

in the sense that it allows the comparison graph to be sparse, ( up to logarithmic terms), and only requires minimal sample complexity.

Finally, we comment on the condition . This is only a mild requirement. For instance, when and is sparse (the original BTL model), this inequality holds naturally. In addition, the comparison of preference ratings is another significant illustration that meets the requirement. In specific, for testing , we choose . In this scenario, the the condition is met since and .

An important corollary of Theorem 4.2 is the limiting distribution of , which could be directly utilized to derive confidence interval for intrinsic score The corresponding theoretical property is summarized in the following Corollary 4.1.

Corollary 4.1.

(Asymptotic normality of intercepts) Under the assumptions of Theorem 4.1, if , for , we have

Although our results are established under more general setting than the existing literature on the BTL model, which does not involve the covariates, our specific result given in Corollary 4.1 with can still compare favorably. Compared with Liu et al. (2022), we need much smaller sample complexity to establish the asymptotic normality. Specifically, they require to derive the asymptotic normality. This condition requires . In contrast, we allow and our requirement for the sample complexity is minimax optimal up to logarithm terms (Negahban et al., 2012; Chen et al., 2019). Moreover, Liu et al. (2022) use Lagrangian debiasing method to derive the estimators, which involves an additional tuning parameter. Compared with Han et al. (2020), we allow sparse compare graphs ( by ignoring logarithm terms), whereas they require a much denser comparison graph () than ours.

We now compare our results with Gao et al. (2021). As the analysis in Gao et al. (2021) does not incorporate the condition number or covariate, we will consider the regime and in our theorems for comparison. First of all, both papers show that the asymptotic normality holds even for the sparse regime , up to a logarithmic order. However, the choice of approximators and approximation errors are very different. Instead of using the Taylor expansion given by Eq. (4.2), Gao et al. (2021) consider the following quadratic approximation:

which only keeps the diagonal part of , and define the approximator . In terms of the approximation errors, Gao et al. (2021) show that with high probability

| (4.4) |

while we prove that for our approximation , with high probability for it holds that

| (4.5) |

When , the term dominates the right hand side of (4.4) and hence also dominates the error rate given by (4.5) as long as . In other words, our approximation error is an order of magnitude smaller than that in Gao et al. (2021). This holds true for the common case where .

Besides investigating the asymptotic behavior of studying the asymptotic property for is another crucial task as it depicts whether some covariates have any power for explaining latent scores. We deduce these from the Theorem 4.1 and Theorem 4.2, and summarize them together with a refined -upper bound of in Corollary 4.2.

Corollary 4.2.

In Corollary 4.2, we first obtain a refined upper bound of , and we next explain the rationality behind this. In Theorem 3.1, a rough upper bound for is obtained via concentration since no precise distributional results are involved in that stage. Given the statistical rates derived in Theorem 3.1, we then analyze the non-asymptotic approximation and distribution of in Theorems 4.1 and 4.2, respectively. Finally, based on these distributional results, a refined upper bound for is achieved.

If we let , one observes that the final upper bound of involves both rates and by ignoring logarithm terms. We conjecture the term which comes from the approximation error () in Theorem 4.1, can be improved to . In this case, should be bounded by the rate of (the same order as the variance of ). The numerical studies in §5.1 validates this conjecture by showing that the rates of is proporation to after we fix and . However, improving the approximation error is highly non-trivial and needs more complex theoretical analysis. Therefore, we will leave this as our future work.

Besides the refined -bounds, the asymptotic distribution for each and the - confidence interval for are also derived in Corollary 4.2. This will enable us to determine each covariate’s significance in real data studies.

5 Numerical Results

In this section, we conduct numerical experiments using synthetic and real data to validate our theories. In §5.1 and §5.2, we leverage synthetic data to corroborate the statistical rates given in §3 and distributional results given in §4, respectively. In addition, in §5.3, we illustrate further our model and methods by using the multual funds holding data.

5.1 Rate of Convergence

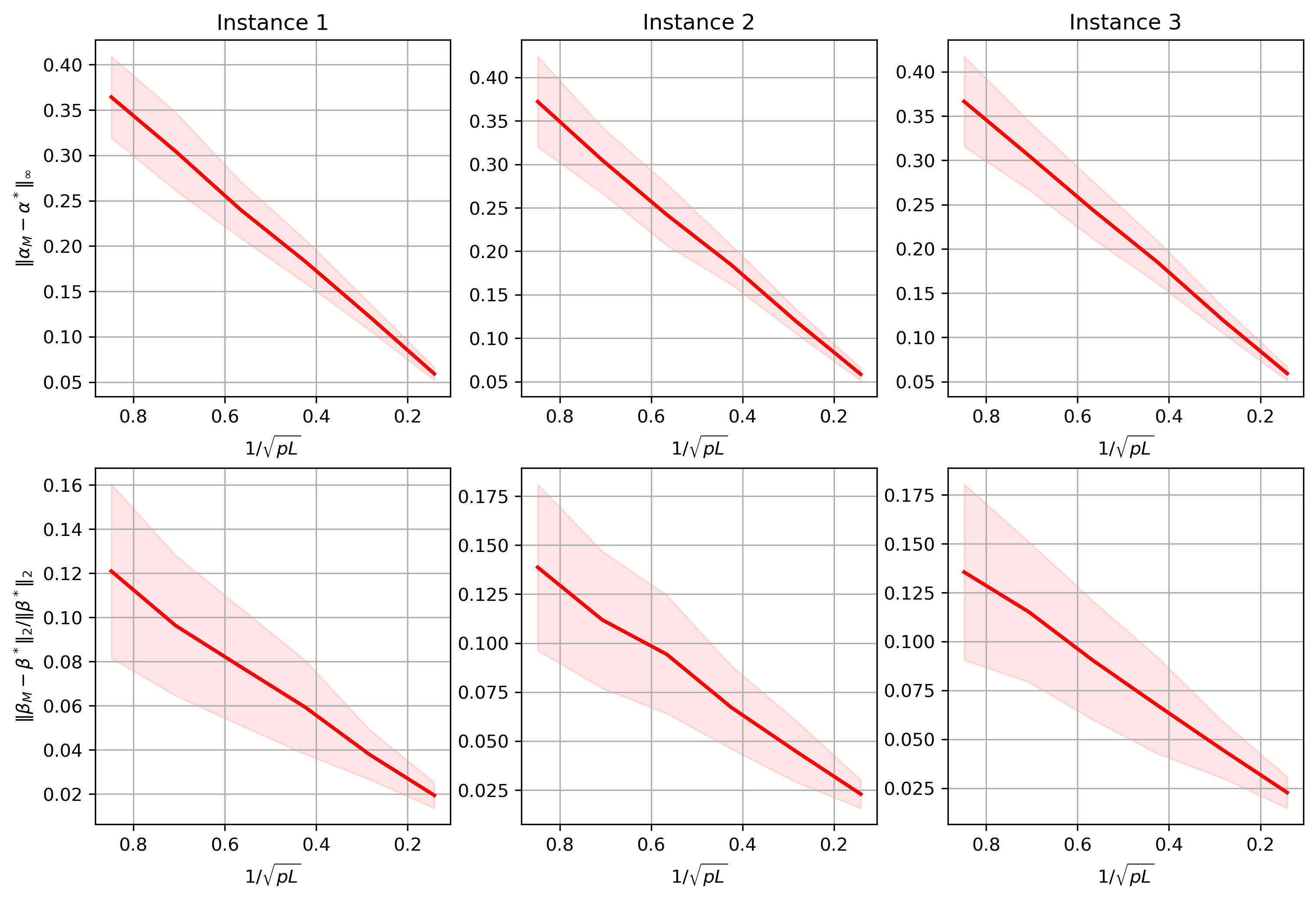

We begin with the data generation process. Throughout the synthetic data experiments, we set to be and to be . The covariates are generated independently with for all . For matrix , its columns are then normalized such that they have mean and standard deviation . Next, we scale by so that . For , its entries are generated independently from . For , it is generated uniformly from the hypersphere . In this way, we ensure . Then we project onto linear space .

To validate the statistical rates in Theorem 3.1, we use the above method to generate the covariates and for three times. This gives us three different instances of the covariates and the parameter . For each given instance, we consider different pairs, which are list below.

| 1 | 0.5 | 0.222 | 0.625 | 0.4 | 0.278 | |

| 50 | 25 | 25 | 5 | 5 | 5 |

For each pair, comparion graph , is generated and the MLE is calculated based on the available data. This process is repeated times and the averaged , as well as their associated standard deviations are recorded. The results are depictd in Figure 1 for each of three instances. Note that and are nearly proportional to , lending further support of the results in Theorem 3.1. The results are insensitive to three different instance, as expected.

5.2 Distributional Results

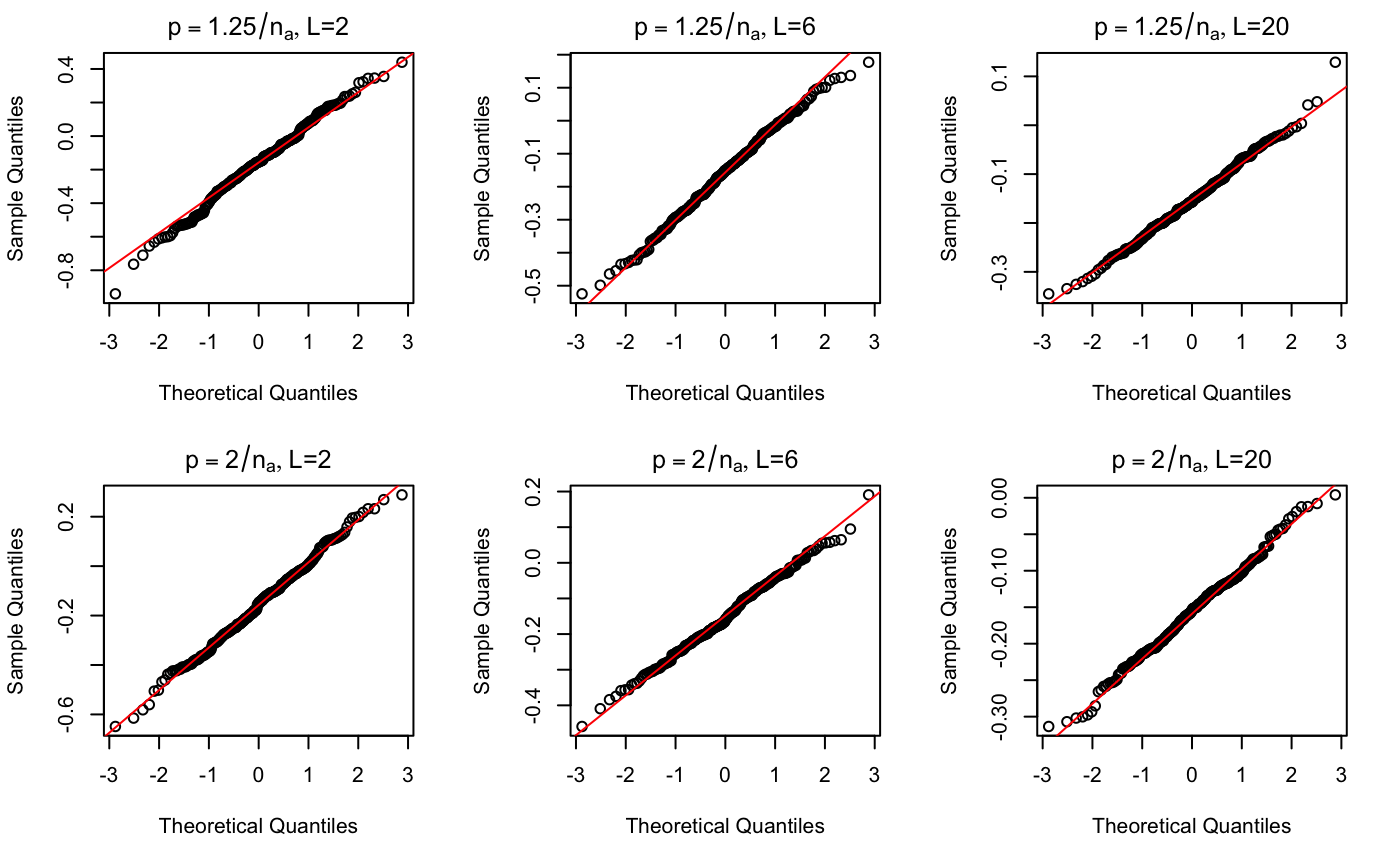

We employ the same method given in §5.1 to generate the covariates and once and fix them throughout the simulation. Letting the effective sample size , we choose the pairs with or and . For each pair, the graph and data are generated times and the MLEs for all simulations are recorded. Figure 2 presents the Q-Q plots for checking the normality of , the first component of . The results show that follows closely the normal distribution.

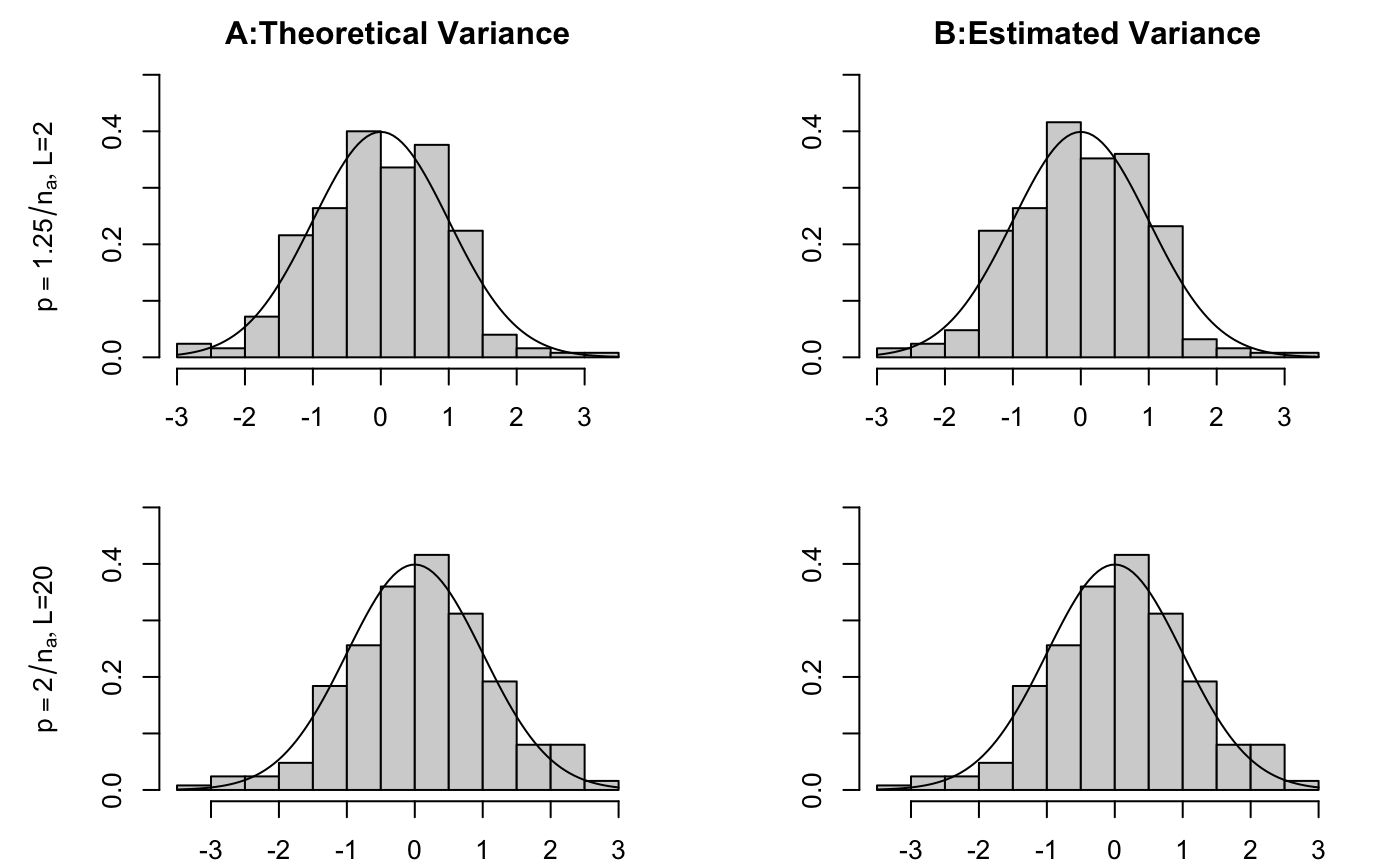

In addition to checking the asymptotic normality, we now verify the asymptotic variance of our estimator. As an illustration, we consider the linear combination , where and is the -th vector from the standard basis of . Based on 250 simulations with and , the histograms of the following two standardized random variables are plotted:

| (5.1) |

This uses the asymptotic theory with plug-in asymptotic variance using the true and estimated parameters, where is the projection of onto linear space . Figure 3 shows that the histograms follow closely the standard Gaussian density. The first row of Figure 3 is presented in the regime with . It holds that, even when the sample size is very small, the two density plots are still very close to the standard Gaussian density. The second row of Figure 3 is drawn based on the setting where . In this case, the density plots of and are more stable and close to the standard Gaussian curve. These results in turn support our theoretical results in Theorem 4.2.

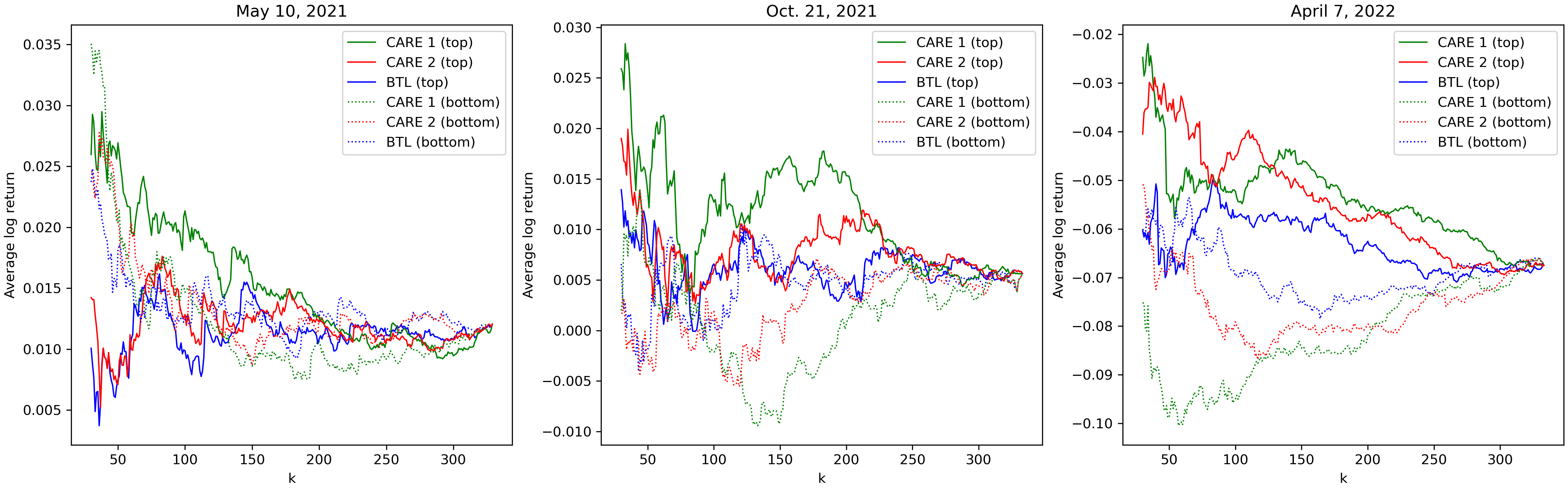

5.3 An Application to Ranking of Stocks

In this subsection, we apply our methods to mutual fund holding data collected from the CRSP Mutual Funds database and the stock prices from Yahoo Finance in 2021 and 2022. Most mutual funds have a variety of stocks and derivatives in their portfolios. The percentage of total net assets allocated to the stocks in a portfolio shows the fund manager’s views on their expected future returns. If the percentage of asset A is higher than asset B in a portfolio, it is an indicatation that the fund manager ranks asset A higher than asset B. As a result, similar to Chen et al. (2022a), the holding information of the mutual funds provides us with pairwise comparisons between the two assets. Although there are a lot of financial assets such as stocks and derivatives on the market, we concentrate on the stocks in the S&P500 list.

Since the returns of the portfolios reflect the quality of the comparisons, we only consider those portfolios that outperform their peers. At any time , we look at the returns of all the funds over the past two years. Those funds with the top returns among all the funds are selected. This selection reflects fund managers actually have stock picking ability (we selected top 25% and got similar results). Then we focus on the holding information of the portfolios corresponding to these funds (approximately, 1400 funds). In other words, we only consider the portfolios that have performed well over the last two years since they are more likely to produce more accurate comparison results. We then collect the pairwise comparisons results for the S&P500 stocks in these selected portfolios. In specific, if the percentage of stock A is higher than stock B in a portfolio, stock A is preferred, and the comparison result is discarded if their percentages are the same. Moreover, among all constituents in the S&P500, only stocks that are compared for at least times are kept. We consider the following three covariates: the log-returns over the past month and the log-returns over the past year, which quantify the short-term and long-term performances of this stock, respectively. The third covariate is the weighted percentage of holdings of the stock, calculated from all the selected portfolios that contain this stock. In specific, letting Portfolios(i) be the set of selected portfolios that contain stock , the third covariate of stock is calculated as the weighted percentage defined by

where is the total number of assets in portfolio q.

Since each portfolio’s holdings do not change much in a short period (such as one or two months), we select three time points in the past two years as representatives to analyze, and the intervals between these time points are roughly half a year apart. Specifically, we focus on the portfolio holdings recorded on May 10, 2021, October 21, 2021, and April 7, 2022, with 1415, 1417, and 1422 funds respectively chosen for these three time points. Based on the information in these funds, there are 332, 334, and 334 S&P500 stocks, respectively, that were compared at least 5 times. At each time point given above, we calculate the MLE estimator in (2.3), and the implementation details are deferred to Appendix D.

We first investigate the statistical significance of these variables at each time point. This amounts to testing the following hypothesis testing problems for each feature:

The test statistics are given by for all and the corresponding -values are calculated via the asymptotic normality results in §4. The results are depicted in Table 1, where most of these three variables are statistically significant at each given time point.

| one month return | one year return | weighted percentage | |

| May 10, 2021 | 1e-5 | 1e-5 | 1e-5 |

| Oct. 21, 2021 | 1e-5 | 1e-5 | 4.49e-3 |

| April 7, 2022 | 3.76e-3 | 2.49e-3 | 5.82e-1 |

We next turn to compare our model with the original BTL model in terms of predicting the future returns. We consider the following two estimators as the representatives of ranking scores derived from our model:

In specific, in we simply set the part to as if the scores were completely captured by the covariates, which corresponds to with . In we apply a soft-thresholding to the part with and for each item . This corresponds to set those estimates that are statistically indifferent from zero to zero. The use of significant level is to control the familywise false positive rates for hundreds of stocks. We then generate the ranking results and for the stocks according to and . In addition, we also let be the ranking result given by the ranking scores of the original BTL model.

To see if the preference ranking of stocks has better performance, we compute the average log-returns of the top stocks and bottom stocks for the subsequent month for each ranking method. The average log-returns of the top stocks and bottom stocks for different ranging from to is presented in Figure 4. It is observed that, the ranking results and given by our method achieve higher log-returns for the top stocks and lower log-returns for the bottom stocks. This implies that our model predicts the future returns better than the original BTL model.

6 Conclusion and Discussion

In this paper, we study the ranking problem by proposing a new model, namely, the covariate assisted ranking estimation (CARE) model. This allows us to incorporate the covariate information of compared items into the ranking framework, which includes the standard BTL model as a particular case. We derive the minimal sample complexity required for statistical consistency and uncertainty quantification for MLE based on novel proof techniques and illustrate the theory and methods using the mutual fund holding dataset. The empirical results lend further support of the CARE model over the classical BTL model in selecting stocks in mutual fund portfolios.

There are a few future directions worth exploring. First, it is worth extending the idea of incorporating covariates into a more general ranking framework such as the Plackett-Luce model or nonparametric model under a more general comparison graph. In contrast, our work only studies the BTL model with the Erdős-Rényi comparison graph. Second, it would be interesting if some structure assumptions exist on the parameters and such as sparsity. In this scenario, one shall leverage certain regularizers on and in the likelihood function to achieve a solution that generalizes well. Third, except for the covariate, one may also incorporate time information into the ranking framework as in many real applications, the underlying scores of compared items change over time. Lastly, in our paper, we consider the scenario where the underlying score of the -th item is given by in the sense that the overall score of the -th item is the summation of its intrinsic score and its covariate times one specific evaluation criterion . It would be interesting if we do ranking based on data evaluated from multiple sources. In specific, suppose that we have users and items and the score of the -th item, evaluated by the -th person, is . It would be interesting to derive novel statistical estimation and uncertainty quantification principles for ranking models under this setting. We will leave these open problems for future research.

References

- Baltrunas et al. (2010) Baltrunas, L., Makcinskas, T. and Ricci, F. (2010). Group recommendations with rank aggregation and collaborative filtering. In Proceedings of the fourth ACM conference on Recommender systems.

- Banerjee (1973) Banerjee, K. (1973). Generalized inverse of matrices and its applications.

- Berry (1941) Berry, A. C. (1941). The accuracy of the gaussian approximation to the sum of independent variates. Transactions of the american mathematical society, 49 122–136.

- Bradley and Terry (1952) Bradley, R. A. and Terry, M. E. (1952). Rank analysis of incomplete block designs: I. the method of paired comparisons. Biometrika, 39 324–345.

- Chen et al. (2022a) Chen, P., Gao, C. and Zhang, A. Y. (2022a). Optimal full ranking from pairwise comparisons. The Annals of Statistics, 50 1775–1805.

- Chen et al. (2022b) Chen, P., Gao, C. and Zhang, A. Y. (2022b). Partial recovery for top-k ranking: Optimality of mle and suboptimality of the spectral method. The Annals of Statistics, 50 1618–1652.

- Chen et al. (2017) Chen, X., Gopi, S., Mao, J. and Schneider, J. (2017). Competitive analysis of the top-k ranking problem. In Proceedings of the Twenty-Eighth Annual ACM-SIAM Symposium on Discrete Algorithms. SIAM.

- Chen et al. (2020) Chen, Y., Chi, Y., Fan, J., Ma, C. and Yan, Y. (2020). Noisy matrix completion: Understanding statistical guarantees for convex relaxation via nonconvex optimization. SIAM journal on optimization, 30 3098–3121.

- Chen et al. (2021) Chen, Y., Chi, Y., Fan, J., Ma, C. et al. (2021). Spectral methods for data science: A statistical perspective. Foundations and Trends® in Machine Learning, 14 566–806.

- Chen et al. (2019) Chen, Y., Fan, J., Ma, C. and Wang, K. (2019). Spectral method and regularized mle are both optimal for top-k ranking. Annals of statistics, 47 2204.

- Chen and Suh (2015) Chen, Y. and Suh, C. (2015). Spectral mle: Top-k rank aggregation from pairwise comparisons. In International Conference on Machine Learning. PMLR.

- Cheng et al. (2010) Cheng, W., Dembczynski, K. and Hüllermeier, E. (2010). Label ranking methods based on the plackett-luce model. In ICML.

- Dwork et al. (2001) Dwork, C., Kumar, R., Naor, M. and Sivakumar, D. (2001). Rank aggregation methods for the web. In Proceedings of the 10th international conference on World Wide Web.

- Erdos et al. (1960) Erdos, P., Rényi, A. et al. (1960). On the evolution of random graphs. Publ. Math. Inst. Hung. Acad. Sci, 5 17–60.

- Esseen (1942) Esseen, C.-G. (1942). On the liapunov limit error in the theory of probability. Ark. Mat. Astr. Fys., 28 1–19.

- Fan et al. (2022) Fan, J., Lou, Z., Wang, W. and Yu, M. (2022). Ranking inferences based on the top choice of multiway comparisons. arXiv preprint arXiv:2211.11957.

- Gao et al. (2021) Gao, C., Shen, Y. and Zhang, A. Y. (2021). Uncertainty quantification in the bradley-terry-luce model. arXiv preprint arXiv:2110.03874.

- Guiver and Snelson (2009) Guiver, J. and Snelson, E. (2009). Bayesian inference for plackett-luce ranking models. In proceedings of the 26th annual international conference on machine learning.

- Hajek et al. (2014) Hajek, B., Oh, S. and Xu, J. (2014). Minimax-optimal inference from partial rankings. Advances in Neural Information Processing Systems, 27.

- Han et al. (2020) Han, R., Ye, R., Tan, C. and Chen, K. (2020). Asymptotic theory of sparse bradley–terry model. The Annals of Applied Probability, 30 2491–2515.

- Harper and Konstan (2015) Harper, F. M. and Konstan, J. A. (2015). The movielens datasets: History and context. Acm transactions on interactive intelligent systems (tiis), 5 1–19.

- Hunter (2004) Hunter, D. R. (2004). Mm algorithms for generalized bradley-terry models. The annals of statistics, 32 384–406.

- Jang et al. (2018) Jang, M., Kim, S. and Suh, C. (2018). Top- rank aggregation from -wise comparisons. IEEE Journal of Selected Topics in Signal Processing, 12 989–1004.

- Jang et al. (2016) Jang, M., Kim, S., Suh, C. and Oh, S. (2016). Top- ranking from pairwise comparisons: When spectral ranking is optimal. arXiv preprint arXiv:1603.04153.

- Jin et al. (2020) Jin, T., Xu, P., Gu, Q. and Farnoud, F. (2020). Rank aggregation via heterogeneous thurstone preference models. In Proceedings of the AAAI Conference on Artificial Intelligence, vol. 34.

- Li et al. (2019) Li, H., Simchi-Levi, D., Wu, M. X. and Zhu, W. (2019). Estimating and exploiting the impact of photo layout: A structural approach. Available at SSRN 3470877.

- Liu et al. (2022) Liu, Y., Fang, E. X. and Lu, J. (2022). Lagrangian inference for ranking problems. Operations Research.

- Luce (2012) Luce, R. D. (2012). Individual choice behavior: A theoretical analysis. Courier Corporation.

- Ma et al. (2018) Ma, C., Wang, K., Chi, Y. and Chen, Y. (2018). Implicit regularization in nonconvex statistical estimation: Gradient descent converges linearly for phase retrieval and matrix completion. In International Conference on Machine Learning. PMLR.

- Massey (1997) Massey, K. (1997). Statistical models applied to the rating of sports teams. Bluefield College.

- Maystre and Grossglauser (2015) Maystre, L. and Grossglauser, M. (2015). Fast and accurate inference of plackett–luce models. Advances in neural information processing systems, 28.

- Negahban et al. (2012) Negahban, S., Oh, S. and Shah, D. (2012). Iterative ranking from pair-wise comparisons. Advances in neural information processing systems, 25.

- Pananjady et al. (2017) Pananjady, A., Mao, C., Muthukumar, V., Wainwright, M. J. and Courtade, T. A. (2017). Worst-case vs average-case design for estimation from fixed pairwise comparisons. arXiv preprint arXiv:1707.06217.

- Plackett (1975) Plackett, R. L. (1975). The analysis of permutations. Journal of the Royal Statistical Society: Series C (Applied Statistics), 24 193–202.

- Richardson et al. (2006) Richardson, M., Prakash, A. and Brill, E. (2006). Beyond pagerank: machine learning for static ranking. In Proceedings of the 15th international conference on World Wide Web.

- Shah et al. (2016) Shah, N., Balakrishnan, S., Guntuboyina, A. and Wainwright, M. (2016). Stochastically transitive models for pairwise comparisons: Statistical and computational issues. In International Conference on Machine Learning. PMLR.

- Shah and Wainwright (2017) Shah, N. B. and Wainwright, M. J. (2017). Simple, robust and optimal ranking from pairwise comparisons. The Journal of Machine Learning Research, 18 7246–7283.

- Simons and Yao (1999) Simons, G. and Yao, Y.-C. (1999). Asymptotics when the number of parameters tends to infinity in the bradley-terry model for paired comparisons. The Annals of Statistics, 27 1041–1060.

- Stigler (1994) Stigler, S. M. (1994). Citation patterns in the journals of statistics and probability. Statistical Science 94–108.

- Szörényi et al. (2015) Szörényi, B., Busa-Fekete, R., Paul, A. and Hüllermeier, E. (2015). Online rank elicitation for plackett-luce: A dueling bandits approach. Advances in Neural Information Processing Systems, 28.

- Thurstone (1927) Thurstone, L. L. (1927). The method of paired comparisons for social values. Journal of Abnormal Psychology, 21.

- Thurstone (2017) Thurstone, L. L. (2017). A law of comparative judgment. In Scaling. Routledge, 81–92.

- Tropp (2012) Tropp, J. A. (2012). User-friendly tail bounds for sums of random matrices. Foundations of computational mathematics, 12 389–434.

- Tropp (2015) Tropp, J. A. (2015). An introduction to matrix concentration inequalities. arXiv preprint arXiv:1501.01571.

- Turner and Firth (2012) Turner, H. and Firth, D. (2012). Bradley-terry models in r: the bradleyterry2 package. Journal of Statistical Software, 48 1–21.

- Vojnovic and Yun (2016) Vojnovic, M. and Yun, S. (2016). Parameter estimation for generalized thurstone choice models. In International Conference on Machine Learning. PMLR.

Appendix A Proof Outline of Estimation Results

In this section, we present the proof outline for Theorem 3.1. The detailed proof of Theorem 3.1 is presented in §C.12.

To understand statistical error of , we begin with analyzing the regularized MLE

| (A.1) |

where for and then make connections with by a properly chosen . Before proceeding, we introduce the following two quantities and indicating the difficulty of recovering

The regularized MLE solves a strong convex problem whose estimation error bounds are derived in Theorem A.1 below.

Theorem A.1.

Suppose for some and . We consider for any absolute constants and

for some . Let be the solution of the regularized MLE Eq. (A.1). Then with probability at least , we have

where .

Theorem A.1 presents the statistical rates of the regularized MLE in (A.1). Before presenting the formal proof for Theorem A.1, in the folllowing several subsections A.1, A.2 and A.3 , we focus on establishing its associated building blocks. Moreover, in §C.12, we provide the formal proof of Theorem 3.1 with the help of Theorem A.1.

A.1 Preliminaries and Basic Results

In this subsection, we study the theoretical properties of the gradient and Hessian of the loss function in (A.1). Their expressions are given by

| (A.2) | ||||

| (A.3) |

The gradient of at is controlled by the following lemma.

Lemma A.1.

With given by Theorem A.1, the following event

happens with probability exceeding for some which only depend on .

Next, we proceed to analyzing the Hessian matrix . First, we consider and study its eigenvalues in Lemma A.2.

Lemma A.2.

Suppose for some . The following event

happens with probability exceeding when is large enough.

Proof.

See §C.2 for a detailed proof. ∎

In the rest of the content, without loss of generality, we assume the conditions stated in Lemma A.2 hold. Moreover, with the help of Lemma A.2, we next analyze the Hessian and summarize its theoretical properties in Lemma A.3 and Lemma A.4, respectively.

Lemma A.3.

Suppose event holds, we obtain

Proof.

Since , we have

∎

Lemma A.4.

Suppose event happens. Then for all such that , , we have

where .

A.2 Convergence of Projected Gradient Descent

In this subection, we consider a sequence of iterates which is generated by the following gradient descent algorithm with stepsize and the number of iterations .

We initialize at and the target loss given in (A.1) is strongly convex, and we show that the iterates has geometric convergence rate to . We summarize the theoretical findings in the following Lemma A.5, Lemma A.6 and Lemma A.7, respectively.

Lemma A.5.

Under event , we have

where .

Next, we prove that the initial point is not far from .

Lemma A.6.

On the event happens, it follows that

Proof.

See §C.5 for a detailed proof. ∎

Lemma A.7.

On event , there exists some constant such that

Proof.

See §C.6 for a detailed proof. ∎

In this subsection, we prove that the iterate converges to geometrically and enjoys a good optimization error after iterations. In order to prove the distance between and , i.e. the statistical error of , in the next subsection, we leverage the leave-one-out technique and use induction to prove that the iterate stays close to our initial point , even after iterations.

A.3 Analysis of Leave-one-out Sequences

In this section, we construct the leave-one-out sequences (Ma et al., 2018; Chen et al., 2019, 2020) and bound the statistical error by induction. To construct the leave-one-out sequence, we consider the following loss function for any .

Then for any , we construct the leave-one-out sequence in the way of Algorithm 2.

With the help of the leave-one-out sequences, we do induction to demonstrate that the iterate will not be far away from when In specific, we take again and . With the leave-one-out sequences in hand, we prove the following bounds by induction for .

| (A) | ||||

| (B) | ||||

| (C) | ||||

| (D) |

For , since , the (A) (D) hold automatically. In the following lemmas, we prove the conclusions of (A)-(D) for the -th iteration are true when the results hold for the -th iteration.

Lemma A.8.

Proof.

See §C.7 for a detailed proof. ∎

Lemma A.9.

Proof.

See §C.8 for a detailed proof. ∎

Lemma A.10.

Proof.

See §C.9 for a detailed proof. ∎

Lemma A.11.

Proof.

See §C.10 for a detailed proof. ∎

Appendix B Proof Outline of Inference Results

In this section we provide the proof outlines for Theorem 4.1, Theorem 4.2, respectively. The details of proofs in this section is deferred to Section C. We first introduce some building blocks for the proof of main theorems.

Lemma B.1.

For , with probability at least we have

-

•

;

-

•

, , .

-

•

, for any .

Proof.

See §C.13 for a detailed proof. ∎

Recall that we define the norm as

Then for any and , we have .

B.1 Proof Outline of Theorem 4.1

In this subsection, we provide the proof outline for Theorem 4.1. The following lemma gives a bound for , which validates the first part of Theorem 4.1.

Theorem B.1.

Under the assumptions of Theorem 3.1, with probability at least we have

Proof.

See §C.14 for a detailed proof. ∎

Next, we consider controlling the magnitude of for in order to prove the second part of Theorem 4.1.

Recall that we define the quadratic approximation to in (4.2), which is also given as below:

We adopt the following notation for a given vector ,

which acts as a marginal likelihood function for the -th coordinate given the other coordinates fixed. Accroding to this definition, we have the following proposition. The proof of Proposition B.1 is included in §C.15.

Proposition B.1.

For , is the minimizer of the univariate function .

By changing the coordinates that we fix, we define as the minimizer of . Here we fix and optimize based on this fixed parameter. Explicitly, the minimizer is calculated as

In order to bound we bound and separately.

In terms of , we provide an upper bound for this quantity in Lemma B.2.

Lemma B.2.

Under the assumptions of Theorem 3.1, as long as , for , with probability at least we have

On the other hand, for a given we let

| (B.1) |

Here we consider the marginal loss of in the -th coordinate given other coordinates fixed. Similar to Proposition B.1, we have the following proposition for . The proof of Proposition B.2 is also included in §C.15.

Proposition B.2.

For , is the minimizer of the univariate function .

We now describe the intuition of bounding . Since is the minimizer of and is the minimizer of . Therefore, as long as and are close enough, the difference between their minimizers and is small. We summarize this finding in the following lemma B.3.

Lemma B.3.

Under the assumptions of Theorem 3.1, for , with probability at least we have

Theorem B.2.

Under the assumptions of Theorem 3.1, as long as and for some fixed constant , with probability at least , for we have

If we further assume , then with probability at least , for we have

Proof.

See §C.19 for a detailed proof. ∎

Appendix C Proof Details

In this section, we prove detailed proof of aforementioned building blocks.

C.1 Proof of Lemma A.1 and Its Corollary

In this subsection, we provide the proof of Lemma A.1 in the sense that we provide an upper bound for the gradient vector in -norm.

Proof.

The gradient is calculated as

Since , we have

| and |

as long as is large enough. Thus, with high probability (with respect to the randomness of ), we have

and

Let and . By matrix Bernstein inequality (Tropp, 2015), we have

with probability exceeding as long as and . On the other hand, we have

To summarize, we have

with probability exceeding . ∎

Once Lemma A.1 is established, we have the following lemma which can be viewed as a direct corollary of Lemma A.1.

Lemma C.1.

With given by Theorem A.1, the following event

is contained by the event . As a result, happens with probability exceeding .

Proof.

By the fundamental theorem of calculus we know that

where . So for all such that , we have

Under event , we have

And, under event , we have . As a result, is contained by . ∎

C.2 Proof of Lemma A.2

Proof.

Let be any matrix with orthonormal rows such that the row space of is , where is the dimension of . Then, it holds that

Let for . Then we have and

as long as is large enough. Furthermore,

By the matrix Chernoff inequality (Tropp, 2012), we have

As a result, if for some , we have

This concludes the proof of Lemma A.2. ∎

C.3 Proof of Lemma A.4

In this subsection, we provide the proof of Lemma A.4 by providing a lower bound for

Proof.

For pair , without loss of generality we assume , we then obtain

One the other hand, it holds that

Therefore, we obtain

where . As a result, for the Hessian we have

This completes the proof of Lemma A.4. ∎

C.4 Proof of Lemma A.5

Proof.

Since is -strongly convex and -smooth on the event , we know that

As a result, when event happens, we have

Therefore, under event , we have

∎

C.5 Proof of Lemma A.6

In this section, we prove is not far from the initial point .

Proof.

Since is the minimizer, we have that . By the mean value theorem, for some between and , we have

As a result, we have

Therefore, we get

As a result, on event we have

We conclude the proof of Lemma A.6. ∎

C.6 Proof of Lemma A.7

C.7 Proof of Lemma A.8

Proof.

By definition we know that

Consider . By the fundamental theorem of calculus we have

Let be large enough such that

In addition, by the assumption of induction, we have

Then by Lemma A.4, we have

On the other hand, by Lemma A.3, we have

Let , then we have

Since , it holds that

Therefore, on the event , we have

as long as . ∎

C.8 Proof of Lemma A.9

Proof.

For any , by definition we have

We consider . By the fundamental theorem of calculus we have

| (C.1) | ||||

| (C.2) | ||||

| (C.3) |

Consider which is large enough such that

Then we also have

Use the same approach derived in §C.7, we have

| (C.4) |

as long as .

On the other hand, since , it remains to bound By definition, we have

By definition, we also have

Consider random variable . By Chernoff bound (Tropp, 2012), we know that

as long as for some . As long as , we have for . Since , by Hoeffding’s inequality and union bound, we get

with probability exceeding conditioning on as long as . On the other hand, since with probability exceeding , we have

with probability exceeding .

On the other hand, for we have

where

Consider . Since , we have that

By Bernstein inequality we know that

As a result, for we have

In summary, there exists constants which are independent of such that

| (C.5) |

with probability exceeding . Combining Eq. (C.3), Eq. (C.4) and Eq. (C.5) we have

as long as and is large enough such that .

∎

C.9 Proof of Lemma A.10

Proof.

For , we have

For , we have

By Lemma C.1, with probability at least we have

as long as

In this case, for we have

| (C.6) |

On the other hand, for we have

| (C.7) | ||||

| (C.8) |

Normalizing the numerators below to 1 and by the mean value theorem, there exists some between and such that

| (C.9) |

Combining Eq. (C.8) and Eq. (C.9), we have

By taking absolute value on both side, we get

Since , we have

By the defintion of we have

Consider which is large enough such that

Then we have

Then it holds that,

Using for , we have

Combine this result with Eq. (C.6), we get

as long as , and . This concludes our proof for Lemma A.10. ∎

C.10 Proof of Lemma A.11

Proof.

For any , we have

As a result, we have

as long as . ∎

C.11 Proof of Theorem A.1

In this subsection, we aim at providing proof for Theorem A.1 by combining the results established above.

For any , by Talor expansion, one obtains

where is some real number between and . As a result, it holds that

By the Cauchy-Schwartz inequality, we have

where and is large enough. The last inequlity holds from the results derived in §A.2 and §A.3. Then for and such that , we have

Similarly, we also obtain

C.12 Proof of Theorem 3.1

With all necessary building blocks at hand, in this subsection, we provide the formal proof for Theorem 3.1. In specific, we assume in the following proof and it is easy to extend the proof to the regime . The way to solve this is changing the power in Lemma A.1 and Lemma A.2 to a larger number.

Proof.

Consider the following MLE

| (C.10) |

We choose in the definition of such that

for some . As long as for some absolute constants , the proof of Lemma A.7 is still valid and Theorem A.1 still holds for this . For large enough such that satisfies the constraints in Eq. (C.10), by the optimality of we know that . On the other hand, by Taylor’s expansion

where for some .

This leads to

| (C.11) |

Next, we first define the norm as

Therefore, we have

as long as

As a result, by Lemma A.4 we have

| (C.12) |

Combine Eq. (C.11) and Eq. (C.12) we have

Therefore, after some simple calculations, it holds that

And, when is large enough, we have

| (C.13) | |||

| (C.14) |

where and . As a result, falls in the interior of the inequality constraints in Eq. (C.10). By the convexity of and its strong convexity in , we have . Therefore, by Eq. (C.13) and Eq. (C.14) we have

| (C.15) | |||

| (C.16) |

The result of and hold based on the same derivations in Section C.11 and we omit the corresponding details. ∎

C.13 Proof of Lemma B.1 and Two Propositions

Proof.

(1) By definition for we have

Since , by Bernstein inequality we have

with probability exceeding , as long as . On the other hand, since , we know that . As a result, we have

(2) By definition we have

with probability at least . Similarly, we have

and

with probability at least .

(3) For , by definition we know that is the average of independent Bernoulli random variables. By Hoeffding’s inequality we know that

with probability at least . As a result, by union bound we know that

holds for all with probability at least . ∎

We also include here two propositions which are also involved in the later proofs.

Proposition C.1.

is the solution of the following linear equations

Proposition C.2.

Under event , we have

Proposition C.1 follows from Eq. (4.1), which gives the definition of , we next provide the proof of Proposition C.2 here.

Proof of Proposition C.2.

Since , by taking variance (conditioned on ) on the both sides we have

| (C.17) |

On the other hand, by considering the covariance (conditioned on ) of and we get

As a result, we know that

| (C.18) |

Combine Eq. (C.17) and Eq. (C.18) we get

| (C.19) |

By taking variance on the both sides of , we have . This also implies . As a result, Eq. (C.19) can be also written as

This immediately implies . Under event , we have . As a result, for any , we have

As a result, we have for all . Combine this fact with , we know that

∎

C.14 Proof of Theorem B.1

Proof.

We know that

Let

we have

| (C.20) |

On the other hand, we know that

| (C.21) |

Combine Eq. (C.20) and Eq. (C.21) we have

| (C.22) |

For we have

By definition we have

By Lemma A.2 we know that

holds uniformly for all with probability at least . As a result, we get

| (C.23) |

with probability exceeding . Since , we know that

As a result, we get

| (C.24) |

By Lemma A.4 we know that

| (C.25) |

with probability exceeding . Therefore, combine Eq. (C.23), Eq. (C.24) and Eq. (C.25) we get

with probability exceeding . ∎

C.15 Proof of Proposition B.1 and Proposition B.2

We denote by . By the definition of and we know that for any and , we have

On the other hand, under Assumption 3.2 we have the following lemma.

Lemma C.2.

For any , there exists a such that .

Proof.

We only have to show that for any , . Assume there exists a such that . First of all, we must have . Since , we must have as . Since , we know that there exists a non-zero vector such that . By the definition of , we know that . Recall the definition of and Assumption 3.2 in §3. Since , we know that , so we must have . As a result, this contradicts to Assumption 3.2 since . ∎

Proof of Proposition B.1 and B.2.

Assume there exists a such that . Then we let be the vector such that and . And, let be the vector in such that . Then we have

This contradicts to the definition of Eq. (4.1).

Similarly, if we assume that there exists a such that . Then we let be the vector such that and . And, let be the vector in such that . Then we have

This contradicts to the definition of Eq. (2.3). ∎

C.16 Auxiliary Results

In this section we include two results which are helpful to the proof of Lemma B.2 in §C.17. These two results are analogies of Theorem 3.1 and Theorem B.1 which we have proven before. The main difference is we replace with . As a result, the following two results can be viewed as the leave-one-out version of Theorem 3.1 and Theorem B.1. To be more specific, we define as

and let be the solution of the following equations

Lemma C.3.

Suppose for some and . We consider for any absolute constants . Then for every and , with probability at least we have

Lemma C.4.

Under the assumptions of Theorem C.3, for every , with probability at least we have

C.17 Proof of Lemma B.2

Proof.

Next, we bound - one by one. Before proceeding, the denominator can be bounded as

with probability at least .

For , by Lemma C.3 we have

So the numerator of can be bounded as

with probability at least . As a result, can be bounded as

| (C.27) |

with probability at least .

When it comes to , by definition we know that is independent with for all . As a result, by Bernstein’s inequality and Lemma C.4 we know that

| (C.28) | ||||

| (C.29) | ||||

| (C.30) | ||||

| (C.31) |

with probability at least . On the other hand, by Lemma C.4 we have

| (C.32) | ||||

| (C.33) |

and

| (C.34) |

with probability exceeding . Combine Eq. (C.31), Eq. (C.33) and Eq. (C.34) we finally bound the numerator of as

with probability at least . As a result, we have

| (C.35) |

with probability at least .

We finally consider bounding . By definition, we know that

Combine the two equations we get

| (C.36) |

For , it is easy to see . By definition we have

For , by Hoeffding inequality, we have

conditioned on with probability at least . On the other hand, since with probability at least , we have

with probability at least . Furthermore, by Lemma B.1 we have

with probability at least . For , we have

with probability at least . Therefore, for we have

| (C.37) | ||||

| (C.38) |

with probability exceeding .

For , since , it holds that

As a result, it follows that

with probability exceeding . On the other hand, we obtain

with probability at least . That is to say, we have

| (C.39) |

with probability at least .

Combine Eq. (C.38) and Eq. (C.39) with Eq. (C.36), we know that

with probability at least . Since , we have

As a result, we know that

| (C.40) |

with probability at least . Therefore, for we finally achieve

| (C.41) | ||||

| (C.42) |

with probability at least .

And, by Eq. (C.40) we know that

with probability exceeding . Combine with Eq. (C.35) we have

| (C.43) |

with probability exceeding . Combine Eq. (C.27), Eq. (C.43) and Eq. (C.42) we know that

with probability at least .

∎

C.18 Proof of Lemma B.3

Proof.

Since is the minimizer of , we know that . By the mean value theorem we know that

where is some real number between and . As a result, we have

By the definition Eq. (2.4) and Eq. (B.1), we have

We first estimate the difference . We have

with probability at least . On the other hand, we have

| (C.44) | ||||

| (C.45) | ||||

| (C.46) | ||||

| (C.47) | ||||

| (C.48) | ||||

| (C.49) |

where

By Taylor expansion we know that

where is some real number between and . As a result, we have

| (C.50) |

Combine Eq. (C.49) and Eq. (C.50) we have

with probability exceeding . As a result, we have

where

and

with probability exceeding . On the other hand, we know that

with probability at least . To sum up, we have

with probability at least . ∎

C.19 Proof of Theorem B.2

C.20 Proof of Theorem 4.2

This subsection aims at deriving theoretical proof for Theorem 4.2.

Proof.

The following content is conditioned on the event . Recall that is the projection of onto linear space . Therefore, we obtain

By Proposition C.1 we have . Since , we also have . Let . Then we have

As a result, we have

For such that and , we define

Then we have

with probability exceeding (randomness comes from ). As a result, by Berry (1941) we have

with probability exceeding (randomness comes from ). And, we know that and

with probability exceeding . Therefore,

with probability exceeding (randomness comes from ). On the other hand, by Theorem 4.1 we have

with probability at least . Therefore, we conclude the first part of Theorem 4.2.

We next take all randomness into consideration. For simplicity we denote by

To begin with, for fixed we have

As a result, we have

| (C.51) |

Consider event , where is some constant such that . Then we consider the following three events

Then we have

| (C.52) | ||||

| (C.53) |

On the other hand, for we have

As a result, we know that

| (C.54) |

By Eq. (C.51) we have

On the other hand, we have

Therefore, we have

| (C.55) |

For we also have

| (C.56) |

By definition we have

By Eq. (C.51) we have

On the other hand, we have

Therefore, we have

| (C.57) |

Combine Eq. (C.53), Eq. (C.54) and Eq. (C.56) we know that

Therefore, by Eq. (C.55), Eq. (C.57) we have

Since the above inequality holds for every , we prove the desired result.

Thus, we finally conclude our proof of Theorem 4.2.

∎

C.21 Proof of Corollary 4.1

Proof of Corollary 4.1.

Let be canonical basis vectors of . By taking for in Theorem 4.2, we only have to show that , and this is also equivalent to . By the definition of we have

As a result, the first part of Corollary 4.1 is proved by Theorem 4.2.

For simplicity we denote by . To begin with, for fixed we have

As a result, we have

| (C.58) |

Consider event , where is some constant such that . Then we consider the following three events

Then we have

| (C.59) | ||||

| (C.60) |

On the other hand, for we have

As a result, we know that

| (C.61) |

By Eq. (C.58) we have

On the other hand, we have

Therefore, we have

| (C.62) |

For we also have

| (C.63) |

By definition we have

By Eq. (C.58) we have

On the other hand, we have

Therefore, we have

| (C.64) |

Combine Eq. (C.60), Eq. (C.61) and Eq. (C.63) we know that

Therefore, by Eq. (C.62), Eq. (C.64) we have

Since the above inequality holds for every , we prove the desired result.

∎

C.22 Proof of Corollary 4.2

The proof of Corollary 4.2 except the refined bound Eq. (4.6) follows directly from the proof of Theorem 4.2. Therefore, we omit the details and only prove Eq. (4.6) here. We prove the following lemma first.

Lemma C.5.

Consider some fixed constants for , and random variable

| (C.65) |

Conditioned on the comparison graph , with probability exceeding we have

Proof.

Let . Then we know that and . As a result, by Hoeffding inequality, with probability at least , we have

| (C.66) |

On the other hand, since are independent random variables, we know that

As a result, we have . Therefore, by Eq. (C.66) we know that

with probability exceeding . ∎

Proof of Eq. (4.6).

Conditioned on the comparison graph , the entries of can be written as the form Eq. (C.65). By Lemma C.5 and union bound, conditioned on the comparison graph , we know that

| (C.67) |

with probability at least . By Proposition C.1 we know that

By the definition of we know that

under event . As a result, we have

| (C.68) | ||||

| (C.69) |

with probability at least . Combine Eq. (C.67) and Eq. (C.69) we know that

with probability at least . On the other hand, by Theorem 4.1, we have

with probability at least . We know that

with probability at least . ∎

Appendix D Details of Real Data Experiments

In this section, we provide the detains in computing the maximum likelihood estimator . We first generated the variables and comparisons as described in §5.3. We standardized each columns to make sure they have mean and standard deviation . In real world data the numbers of comparisons between each compared pair are not the same, so we denote by the number of comparisons betweern pair . Let be all the comparisons we have, then the negative log-likelihood can be written as

We then scaled this log-likelihood by the total number of portfolios selected at this time point. In addition, we added a small regularization term to ensure the algorithm converges. For the same reason we state in §5.3, that is, we expect the residule scores to be close to , we only imposed the regularization term to the part. As a result, the objective that we minimized is

with being . We ran projected gradient descent with step size and stopped the algorithm when the difference before and after updating has norm not greater that .