Identification of time-varying counterfactual parameters in nonlinear panel models

Abstract

We develop a general framework for the identification of counterfactual

parameters in a class of nonlinear semiparametric panel models with

fixed effects and time effects. Our method applies to models for discrete

outcomes (e.g., two-way fixed effects binary choice) or continuous

outcomes (e.g., censored regression), with discrete or continuous

regressors. Our results do not require parametric assumptions on the

error terms or time-homogeneity on the outcome equation. Our main

results focus on static models, with a set of results applying to

models without any exogeneity conditions. We show that the survival

distribution of counterfactual outcomes is identified (point or partial)

in this class of models. This parameter is a building block for most

partial and marginal effects of interest in applied practice that

are based on the average structural function as defined by Blundell and Powell (2003, 2004).

To the best of our knowledge, ours are the first results on average

partial and marginal effects for binary choice and ordered choice

models with two-way fixed effects and non-logistic errors.

JEL classification: C14; C23; C41.

Keywords: index model; panel data; fixed effects; average

structural function; semiparametric; binary choice; discrete choice;

censored regression.

1 Introduction

We study counterfactual or policy parameters for nonlinear panel models with structural equation

| (1) |

where indexes individual units, indexes time, is a weakly-monotone transformation function that can vary over in an unrestricted way, is a vector of regression coefficients, is an individual-specific effect, and is a stochastic error term.111There is a large literature on the identification and estimation of structural parameters in the cross-sectional version of this model, e.g., see the work on single index models by Han (1987), Powell et al. (1989), Ichimura (1993), Ahn et al. (2018), and references therein. For each unit , we observe covariates , . The dependence between and is left unrestricted, so that is a fixed effect, c.f., e.g., Graham and Powell (2012). The class of models with outcome equation as in (1) includes the binary choice model with two-way fixed effects, the ordered choice model with fixed effects and time-varying cut-offs, the censored regression model with time-varying censoring, and various transformation models for continuous dependent variables.222For example, letting , the structural equation for the binary choice model with two-way fixed effects is , for the ordered choice model with time-varying cutoffs it is , , and for censored regression with time-varying censoring it is .

For a subpopulation of individuals defined by their sequence of regressor values , our parameter of interest is the counterfactual survival probability:333The counterfactual survival probability answers the question “For a subpopulation defined by their sequence of regressor values , what is the ceteris paribus probability that their period- outcome exceeds if their period- regressor values were exogenously set to ?”

| (2) |

where is given by (1), is a fixed counterfactual value of the period- regressors, and is a fixed cut-off value, where denotes the support of the observed .444Conditioning on the sequence allows us to identify the same parameter across different exogeneity and time-stationarity assumptions. The parameter in (2) is a building block for most partial and marginal effects of interest in applied practice that are based on the average structural function (ASF) as defined in the pioneering work of Blundell and Powell (2003, 2004). For example, when is non-negative , the ASF at time can be obtained as:555See, for example, Song and Wang (2021) for the integrated tail probability expectation formula that uses a survival function as defined in (2).

| (3) |

The ASF can then be used to define partial effects based on partial derivatives or marginal effects based on discrete differences, see, e.g., Lin and Wooldridge (2015).

The challenge is to identify (2) in nonlinear panel models with structural equation as in (1) when are fixed effects and . To see that this is challenging, consider the special case of the binary choice model with two-way fixed effects. A recent literature has made progress in identifying certain counterfactual parameters for this model provided that the error terms follow a standard logistic distribution, see e.g. Aguirregabiria and Carro (2021), Davezies et al. (2022), Dobronyi et al. (2021).666Earlier work by Honoré and Tamer (2006) provides partial identification of marginal effects under a more general structure with dynamics and arbitrary but known error term distributions. See also Pakel and Weidner (2023) for an approach that applies to parametric models covered by the results in Bonhomme (2012). Finally, see Honore (2008) for results on marginal effects for the censored regression model.

A separate literature provides identification results under time-homogeneity assumptions that do not allow for arbitrary time-effects, see the benchmark results in Hoderlein and White (2012), Chernozhukov et al. (2013), and Chernozhukov et al. (2015).777There, the authors consider a nonseparable structural function and impose no parametric assumptions on the error terms. When , the class we models we study here is nested in their analysis. To the best of our knowledge, nothing is known about the identification of the ASF for the binary choice model with two way fixed effects without logistic errors.888We do not consider here the case of correlated random effects or the case of large-. Progress on counterfactual parameters for the former case has been made by, e.g., Arellano and Carrasco (2003), Altonji and Matzkin (2005), Bester and Hansen (2009), Chen et al. (2019), Liu et al. (2023), while for the latter by, e.g., Fernández-Val (2009), Fernández-Val and Weidner (2018), and Bartolucci et al. (2023).

We derive (partial) identification results for (2) without parametric restrictions on the distribution of for panel models with outcome equation as in (1). Our results are for short-. Relevant examples of models to which our results apply are (i) binary choice with two-way fixed effects and nonlogistic errors, (ii) ordered choice with time-varying thresholds, (iii) censored regression with time-varying censoring. Additionally, since (2) varies over time whenever is time-varying, policy parameters that are functionals of (2) are also time-varying.

For nonseparable panel models with fixed effects, the results in benchmark work such as Hoderlein and White (2012), Chernozhukov et al. (2013), and Chernozhukov et al. (2015) establish limitations on what can be learned from panel data in terms of counterfactual parameters. By imposing additional structure on the latent outcome, such as additivity in a linear index and the fixed effects, we show that (partial) identification of counterfactual parameters can be obtained without time-homogeneity assumptions on the outcome equation and no parametric assumptions on the distribution of the error terms. Because we make no time-homogeneity assumptions on , the counterfactual parameters can vary over time in an arbitrary way. To the best of our knowledge, it is the combination of time-varyingness of the outcome equation (hence, of the counterfactual parameters) and no parametric distributional assumptions on the error terms that constitutes our contribution relative to the literature on partial effects in nonlinear panel models with fixed effects.

For our results, we treat and as given, i.e. either known or previously point- or partially-identified.999Sufficient conditions for the identification of and time-varying for models with structural equation as in (1) are provided in Botosaru and Muris (2017) and Botosaru et al. (2021) under strict exogeneity and weak monotonicity of , and Botosaru et al. (2022) under endogeneity and strict invertibility of . With a parametric structure on both and the distribution of the stochastic errors, one may use the results in Bonhomme (2012). Consistent estimators for or/and time-invariant transformation in nonlinear panel models without parametric assumptions on the error terms have been derived by, e.g., Abrevaya (1999), Chen (2010), Chen and Wang (2018), Wang and Chen (2020), Chen et al. (2022) and references therein. For specific panel models, such as binary choice, ordered choice, linear models, duration models, censored regression, see, e.g., Manski (1987), Honoré (1992), Honoré (1993), Horowitz and Lee (2004), Chen et al. (2005), Lee (2008), Muris (2017). Recent work on sharp identification regions for structural parameters includes Khan et al. (2011), Khan et al. (2016), Honoré and Hu (2020), Khan et al. (2023), and Aristodemou (2021). See also Ghanem (2017) on testing identifying assumptions in the class of models we consider here. Our key insight is that the linear index structure allows us to classify each observed probability at time ,

| (4) |

as either an upper bound on , a lower bound on , or both. We show that (4) is an upper bound only if the observed index at time , , is at least the counterfactual index at time , ; and a lower bound only if the observed index at time is at most the counterfactual index at time . Without any additional time-stationarity or exogeneity assumptions, bounds on the period- counterfactual probability can be constructed from the period- observed probabilities , . Under a conditional time-stationarity assumption on the errors, outcomes from all periods are informative for the period- counterfactual probability. The bounds under conditional time-stationarity are tighter than those without exogeneity assumptions. Point identification is obtained when the transformation function is invertible or when the counterfactual index equals one of the observed indices.

The remainder of this paper is organized as follows. Section 2 presents our main results: Section 2.1 constructs bounds without any additional time-stationarity or exogeneity assumptions, while Section 2.2 constructs bounds under a conditional time-stationarity assumption on the error terms. Section 3 applies our results to a few examples: binary choice model, ordered choice model, and censored regression. We present a numerical experiment for the binary choice model in Section 4.1 and one for the ordered choice model in Section 4.2. All proofs and an additional numerical experiment can be found in the Appendix.

2 Main results

We provide two results on the identification of defined in (2). Our first result in Theorem 1 provides bounds on without imposing any exogeneity assumptions or time-stationarity assumptions on . Our second result in Theorem 2 uses a conditional time-stationarity assumption on to tighten those bounds. Conditioning on the sequence allows us to identify the same parameter, , across different exogeneity and time-stationarity assumptions.

The following two assumptions are maintained throughout the paper:

Assumption 1.

Footnote 9 lists work that provides sufficient assumptions for either the point- or the partial-identification of and .

Assumption 2.

For each , is weakly-monotone and right-continuous.

Assumption 2 does not restrict the way that can vary over . Our results apply to the case of time-invariant , in which case parameters such as (2) and (3) are also time-invariant. This assumption allows to have flat parts and jumps, or to be continuous. Hence, our setting accommodates both discrete and continuous outcomes.

Given Assumption 2, we define the generalized inverse of as:101010Existence of is ensured by Assumption 2.

| (5) |

i.e. it is the smallest value of the latent variable that yields a value of the observed outcome .

For what follows we fix and we fix .

2.1 No additional exogeneity or time-stationarity assumptions

For our first set of results, we define the following sets:

| (6) | ||||

| (7) |

The set collects the values for which the counterfactual index at time , , is greater than the observed index at time , , while collects the values for which the counterfactual index at time is smaller than the observed index at time . Note that .

Theorem 1.

Theorem 1 uses the linear-index structure of (1) and knowledge of and to classify as a lower (upper) bound on for any value of . By varying we obtain the sets ( of values that provide lower (upper) bounds. Equation (8) intersects these bounds. Since , every value of provides an upper bound, a lower bound, or both. Note that since either or can be empty, the trivial lower (upper) bound is selected by the intersection with .

Section 3 applies Theorem 1 to binary choice, ordered choice, and censored regression. In the case of binary choice, the bounds of Theorem 1 simplify significantly. In that case, provides an upper bound for if , and a lower bound if . When , point-identifies .

Remark 1.

The result in Theorem 1 is stated for a given value of . Thus, the bounds are directly applicable in case where are point-identified. If are partially identified, bounds on can be obtained by taking the worst-case bounds across parameter values in the identified set.

Remark 2.

The bounds in Theorem 1 do not require any additional exogeneity conditions on beyond those that may be needed for Assumption (1)(ii). In particular, the bounds are valid for models with strictly or weakly exogenous regressors, with lagged dependent variables, and with endogenous regressors. Likewise, the bounds do not require any time-stationarity assumptions on the distribution of the error terms. In this sense, the bounds are valid for models with errors with time-varying distributions. Finally, separability in and is not necessary for identification of the counterfactual survival probability, suggesting that our argument can be applied to a more general class of models.

Remark 3.

Point identification occurs in a number of settings. First, when is invertible, see Section (3.1). Second, when there exists a such that

This can happen, among others, when and (or ). In this case, and the upper and lower bounds coincide.

Remark 4.

The bounds in Theorem 1 shrink with the cardinality of , so that the worst case for our bounds is when the outcomes are binary (worst case here means that, provided failure of point-identification, one of the bounds is always trivial), while the best case is when the outcomes are continuous (best case in the sense that the parameter of interest is always point-identified).

2.2 Conditional time-stationarity

The bounds in Theorem 1 can be wide, for example when the dependent variable has few points of support (see Remark 4). The following assumption obtains tighter bounds by using information across all time periods rather than information from period only.

Assumption 3.

Conditional time-stationarity: , for all .

Conditional time-stationarity requires that the conditional distribution of the error terms conditional on be the same in each time period. In Chernozhukov et al. (2013, 2015) and Hoderlein and White (2012)111111See, e.g., Manski (1987), Honoré (1992), Abrevaya (2000), Hoderlein and White (2012), Graham and Powell (2012), Chernozhukov et al. (2013), Chernozhukov et al. (2015), Khan et al. (2016), Chen et al. (2019), Khan et al. (2023). the authors refer to this assumption as both “strict exogeneity” and time-homogeneity of the error terms.121212For a discussion of strict exogeneity, as well as other notions of exogeneity, in the context of linear models, see Chamberlain (1984), Arellano and Honoré (2001), Arellano and Bonhomme (2011). Note that the error terms are required to have a time-stationary (“time-homogeneous”) distribution conditional on and the entire sequence . The assumption allows for serial correlation in the errors and in some components of , and it leaves the distribution of conditional on unrestricted. Note that, in our set-up with time-varying structural equation, the conditional distribution of given can still vary over time.

Fix and define the sets:

Theorem 2.

As in the case of in Theorem 1, the result above applies directly to point-identified and . If are partially identified, bounds on can be obtained by taking the worst-case bounds across parameter values in the identified set.

According to Theorem 2, we can use information from any period to construct bounds on the counterfactual survival distribution in period . The resulting bounds can be much more informative than those in Theorem 1 without time-stationarity and exogeneity assumptions; this can be seen from the expressions for binary and ordered choice in Section 3, and from the numerical experiments in Section 4. The gains can be substantial, especially if the number of time periods is large, if there is variation in the values of the sequence , and if there is a large degree of variation over time in .131313Although, we do not prove sharpness of the bounds in Theorem 2, we were unable to construct a situation where they were not. As we show in the numerical exercises, the bounds are (very) informative.

Remark 5.

That variation in can improve identification is particularly interesting. In related settings, time-homogeneity of the outcome equation, i.e. , has been used for identification of partial effects in panel models. In our setting, time-variation in the structural function can aid identification of partial effects in monotone single-index models. For an example, see our analysis of binary choice models in Section 3.2.

Remark 6.

The best upper and lower bounds can be thought of as, first, choosing the best for each time period (as in Theorem 1) and then choosing the best time period. Letting

we obtain a bound for each time period,

and, because this bound applies for each period , we obtain

or

We illustrate this for the binary and ordered choice models in Section 3.

Remark 7.

Remark 8.

Theorem 2 updates and replaces the results in Section 3.2 in Botosaru and Muris (2017).

3 Examples

In this section, we apply our results to a number of empirically relevant choices for . These examples are helpful in understanding how informative our bounds are, and help relate them to existing bounds in the literature derived under related but different conditions.

Let . We start by applying our results to the fixed effects linear transformation model with invertible . We then study binary choice models with two-way fixed effects , ordered choice models with time-varying thresholds , and censored regression with .

3.1 Continuous outcomes and invertible

Let be invertible, so that . Examples include linear regression with two-way fixed effects, i.e. ; transformation models used in duration analysis; and the Box-Cox transformation model.141414Such models have been studied extensively in the cross-sectional setting, see, e.g., Amemiya and Powell (1981); Powell (1991, 1996).

Let be defined on or There always exists a such that

Theorem 1 applies and the counterfactual survival probability (2) is point-identified. To see this, consider the argument below:151515See also Remark 2 in Botosaru and Muris (2017), and Botosaru et al. (2021).

where invertibility of was used in the second equality.

3.2 Binary choice

The link function

obtains the panel binary choice model with two-way fixed effects with structural function

| (9) |

Our results yield bounds on (2), hence on partial effects, without parametric assumptions on the distribution of the error terms and for a variety of exogeneity conditions. The only existing results without parametric assumptions on the error term that we are aware of are those in Chernozhukov et al. (2013), but those require that regressors be discrete and that for all .

In what follows, we fix the time period for the counterfactual to and use the abbreviated notation

| (10) |

For this model, and .

Remark 9.

By removing inf, we remove . This is useful, since, e.g., Theorem 1 asks us to compare to for all values of and fixed . For the particular case that , this obtains and . Note that we could allow for fixed , but this would lead to obtaining trivial bounds, i.e. for and , . Hence, we restrict both .

3.2.1 Theorem 1 bounds

For Theorem 1 leads to three different cases depending on the sign of . These cases are:

-

1.

, in which case (10) is point-identified;

-

2.

, in which case the observed index exceeds the counterfactual one, so that and the observed probability provides an upper bound for (10);

-

3.

, in which case the observed index is lower than the counterfactual one, so that and the observed probability provides a lower bound for (10).

The results of Theorem 1 can be summarized as follows:

To see that these bounds are valid, we adapt the key derivation underlying Theorem 1 to this specific case:

| (11) |

where the third line denotes that the direction of the inequality depends on the sign of the difference between the observed index and the counterfactual index .

3.2.2 Theorem 2 bounds

Under Assumption 3, Theorem 2 implies that any period can be used to construct counterfactuals for period . Instead of stating the bounds as implied by Theorem 2, we show how to construct them from first principles.

Suppose that there exists a time period such that

| (12) |

Then (10) is point identified with

where the second equality follows by Assumption (3) and the third equality follows by (12).161616As a special case, in a model without time dummies and with a binary treatment indicator, e.g., , we can point-identify the distribution under treatment for any subpopulation that is treated at some point, .

If there does not exist a time period such that (12) holds, Theorem 2 can be operationalized as follows. Fix and, for each period , compare to , and group the time periods according to whether they provide an upper bound or a lower bound :

These sets correspond to and in Theorem 2 with , counterfactual period , and

These bounds have a few interesting properties. First, they can be informative for stayers, i.e. even when for all , nontrivial bounds can be derived as long as there are time effects for some . Second, under Assumption 3, the bounds tighten as compared to the bounds without this assumption. In Section 4, we investigate these and other properties through a numerical experiment.

3.3 Ordered choice

The link function

obtains an ordered choice model with fixed effects and time-varying thresholds:171717Das and van Soest (1999); Johnson (2004); Baetschmann (2012a, b); Muris (2017); Botosaru et al. (2021) discuss identification of the under various conditions. With logistic errors, the parameters can be estimated via composite conditional maximum likelihood estimation. Without logistic errors, the parameters can be estimated using maximum score methods. In the logistic case, the results in Davezies et al. (2022) can then be used to bound average marginal effects.

| (15) |

For this model, and

We fix the time period for the counterfactual to . The parameter of interest is then

| (16) |

3.3.1 Theorem 1 bounds

Fix . To bound in (16), for each we compare the observed index to the counterfactual index , and construct the sets

These sets can be used to form lower/upper bounds on according to Theorem 1.

Note that for the ordered choice model, for a fixed , there may be multiple s yielding nontrivial bounds. This is different from the binary choice case where has one element, that provides either a non-trivial lower bound or a non-trivial upper bound. For the ordered choice model, has at least two elements, so there may be nontrivial upper and lower bounds. To see this, let (so that ) and assume . Then , so that the observed probability provides a nontrivial upper bound:

However, there may be other values in , call them for which . This would happen if, e.g., and are such that . In this case, the observed probability is a nontrivial lower bound:

The bounds given by Theorem 1 are the best bounds across and , i.e.

| (17) |

setting and to deal with the case when all of provides an upper (lower) bound.

3.3.2 Theorem 2 bounds

Fix . For each , compare to , and compute the sets:

The bounds under time-stationary errors are then the intersection of the bounds in (17) across all time periods:

| (18) |

3.4 Censored regression

The structural function

corresponds to a censored regression model.181818For ease of exposition, we do not consider here extensions covered by our setup such as with time-varying censoring cutoff, and unknown time-varying function. For the identification and estimation of the common parameters in censored regression models, see e.g. Honoré (1992); Honoré and Powell (1994); Honoré et al. (2000); Charlier et al. (2000); Abrevaya and Muris (2020). For the cross-sectional case, see e.g. Powell (1984); Honoré and Powell (1994). For this model, Honore (2008) shows that one can point-identify a meaningful marginal effect using knowledge of . Because this model is encompassed by our framework, with and

we can use our Theorems 1 and 2 to generate additional point and partial identification results for partial effects in this model.

The object of interest is

The case is not informative because . Thus, we restrict attention to and use that . If there exists a such that

i.e. if

then

so that Theorem 1 implies point identification

If then

because , which yields the trivial upper bound

Each provides a lower bound, since

Then

so that

Hence, Theorem 2 obtains

With time-stationary errors, point identification occurs if there exists a time period and a such that

because then

This only requires the existence of one time period for which we can find such a .

Partial identification thus only results if, for each time period,

in which case the resulting bound is

This partial identification result only applies when the subpopulation is such that for each , .

4 Numerical experiments

We report on two numerical experiments that explore the bounds in Theorem 1 and Theorem 2 for the two-way binary choice and ordered choice models. We show that our bounds are informative without exogeneity or time-homogeneity assumptions on the error terms. The bounds tighten as grows, and they are more informative for ordered choice models than for binary choice since the bounds tighten as the cardinality of grows. Section 4.1 presents results for a two-way binary choice probit model with continuous regressors. Section 4.2 presents results for a staggered adoption design with both binary and ordered outcomes.

4.1 Two-way binary choice probit with a continuous regressor

Consider the following data generating process for a binary choice model with two-way fixed effects:

with and . The former parameter controls the cross-sectional heterogeneity in , while the latter controls the degree of variation in the sequence . The smaller each parameter is, the tighter the bounds are expected to be.

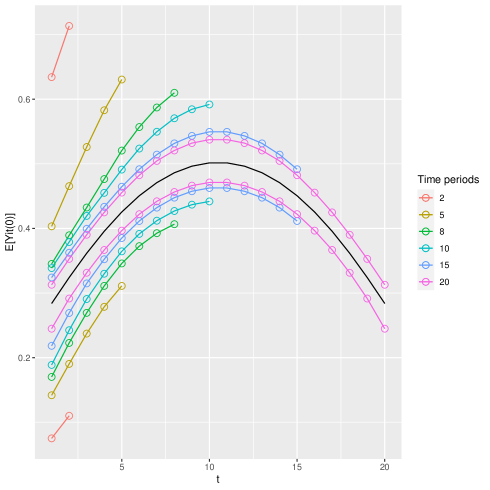

Figure 1 plots the bounds on the sequence , . The bounds are computed according to Theorem 2. We find that the bounds get tighter as the number of periods increases. For example, the width of the interval is when computed with up to 5 periods, when using all periods. In a separate experiment with (not reported), the width shrinks to when using all periods. The identified region may not collapse to a point as , since its width depends on the distribution of , the stationary distribution of , and the shape of .

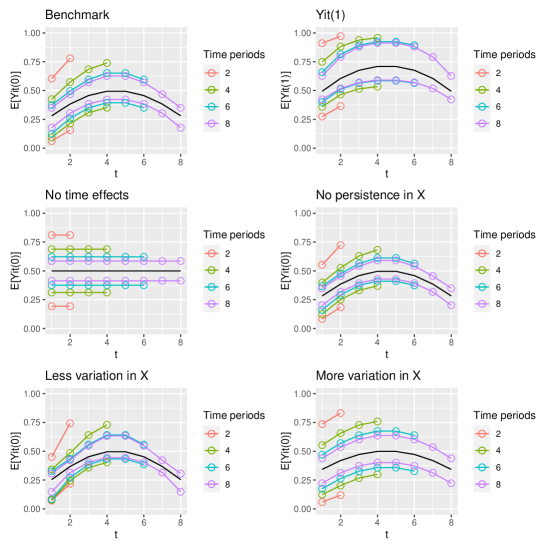

Figure 2 presents results for the sequence for some variations on the model above. The first row, left column shows results for , keeping the other design parameters unchanged. Note that, because , this changes the evolution of the expectation. All subpanels of Figure 2 display results for a deviation from the top left panel. All results in Figure 2 are for the sequence , except for the top right panel, which shows the bounds for the sequence , under the same model as that for the top left panel. The bounds are wider because has less mass around than around . The second row reports bounds on the sequence , when there are no time-effects (left column) and when there is no persistence in , i.e. (right column). The bounds are slightly wider when the transformation function is time-invariant, and they are tighter when there is no persistence in . The third row shows the bounds when is (left column; compare to in the benchmark case) and (right column). The bounds when there is smaller cross-sectional variation in at a given time period are tighter than when there is greater cross-sectional variation.

For the specification consider in this section – binary probit with two way fixed-effects and short – there are no other results in the literature. In Appendix B, we present another numerical exercise for binary probit with discrete regressors. That DGP is the same as the one in Section 8 of Chernozhukov et al. (2013) when there are no time-effects, i.e. for all . In that case, we recover the bounds in Chernozhukov et al. (2013).

4.2 Staggered adoption with binary and ordered outcomes

In this section, we consider a staggered adoption design with both binary and ordered outcomes.

The population consists of groups and individuals in each group are observed over periods. Individuals are untreated up to and including period ; they are treated at period , and then stay treated for , i.e.

where is individual ’s group. Here, and .

The latent outcome is given by

and is standard logistic. The observed outcome is generated as

where 191919For , the outcome is binary, while for , the outcome is ordered., and the threshold is generated as follows. Set , so that are the lowest outcomes, and are the top outcomes. Set , then draw and construct

We draw one set of and condition our results on them. This allows us to compare the same parameter across different values of and .

The parameter of interest is

This parameter gives the probability of being in the upper half of possible outcomes.202020A two-period version of this setup resembles the nonlinear difference-in-difference setup in Athey and Imbens (2006). The results in this section differ from theirs because we allow for the combination of fixed effects and discrete outcomes, which is not covered by their results.

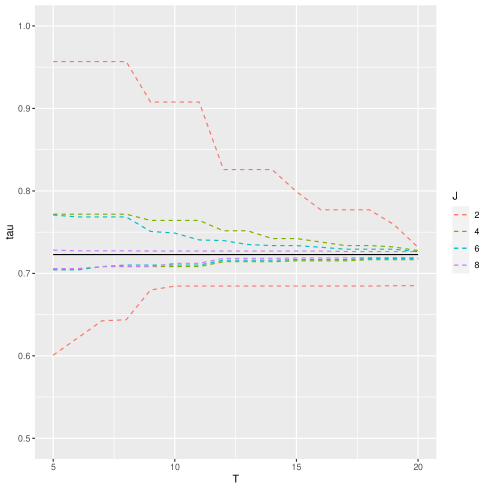

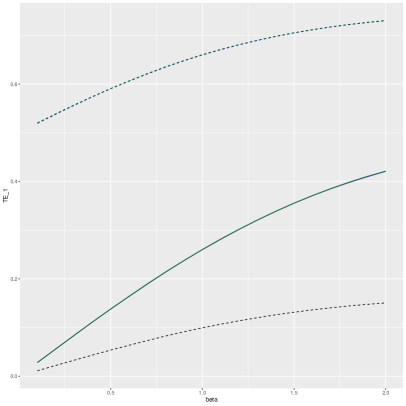

Our results for this design are presented in Figure 3. The solid black line is . Bounds for different values of are in colored, dashed lines. Binary choice is in red. At , the width of the bounds for are approximately , and become as narrow as when . As increases, the bounds narrow substantially. This is especially evident when is small. For example, at , the width of the bounds for is , and for it is .

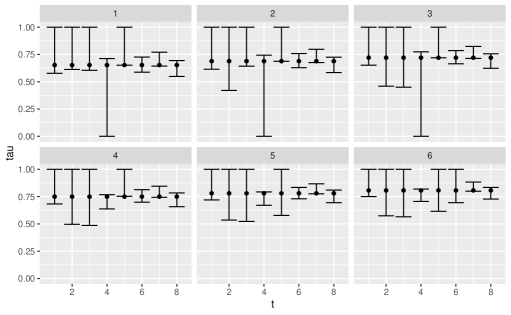

Figure 4 provides further insight, and further clarifies the construction of the bounds in Theorem 2. Consider , and . Each panel corresponds to a group , so that panel “3” corresponds to the population of individuals treated in periods . The vertical error bars, at each , correspond to the best bounds that can be constructed for the period- counterfactual using period- data, see Remark 6:

with

From Figure 4, it is clear that is not sufficient to provide non-trivial bounds in each period, see for example periods 1-3. The bounds in period 4 are also trivial, but in a way that complements the period 1-3 bounds. Furthermore, the thresholds in periods 6-8 are such that these periods supply non-trivial bounds. By using Assumption 3, and taking the best bounds in each panel over the time periods as in Theorem 2, relatively narrow bounds are obtained on , see Figure 3.

5 Conclusion

This paper discusses identification of counterfactual parameters in a class of nonlinear semiparametric panel models with fixed effects and arbitrary time effects. We derive bounds on the counterfactual survival probability and related functionals that depend on either outcomes from the same time period as the counterfactual (without exogeneity assumptions) or outcomes from across all available time periods (under a “strict exogeneity” or conditional time-stationarity assumption on the errors). The bounds tighten as the cardinality of the support of the dependent variable increases, and, under a time-stationarity assumption on the errors, as increases. The bounds need not collapse to a point as grows, rather they collapse to a point under particular assumptions on the time effects and the observed regressors, i.e. when the counterfactual index equals one of the observed indexes. Our bounds are valid for continuous and discrete outcomes and covariates, for both movers and stayers.

Although our focus is on identification, we describe here a potential way of addressing the issue of inference. Note that the bounds in Theorem 2 can be written as a set of conditional moment inequalities: for fixed and for all :

When are partially identified via a set of moment inequalities, these moment inequalities can be added to the program. For either pointwise or uniform in inference, one could implement the full vector approach of Cox and Shi (2022) if the regressors have finite support, or Andrews and Shi (2017) if the regressors are continuously distributed.

The bounds of Theorem 1 are valid for dynamic panel models. However, the bounds may be wider than those obtained by studying specific models, where the dynamic structure is known, e.g., binary choice with lagged outcomes as covariates. In ongoing work, we are studying how to extend our approach to such models. It is an open question as to whether our approach could be extended to nonseparable models.

References

- Abrevaya (1999) Abrevaya, J. (1999). Leapfrog Estimation of a Fixed-Effects Model with Unknown Transformation of the Dependent Variable. Journal of Econometrics 93, 203–228.

- Abrevaya (2000) Abrevaya, J. (2000). Rank Estimation of a Generalized Fixed-Effects Regression Model. Journal of Econometrics 95(1), 1–23.

- Abrevaya and Muris (2020) Abrevaya, J. and C. Muris (2020). Interval Censored Regression with Fixed Effects. Journal of Applied Econometrics 35(2), 198–216.

- Aguirregabiria and Carro (2021) Aguirregabiria, V. and J. M. Carro (2021). Identification of Average Marginal Effects in Fixed Effects Dynamic Discrete Choice Models. Technical report. Available at https://doi.org/10.48550/arXiv.2107.06141.

- Ahn et al. (2018) Ahn, H., H. Ichimura, J. Powell, and P. Ruud (2018). Simple Estimators for Invertible Index Models. Journal of Business and Economic Statistics 36(1), 1–10.

- Altonji and Matzkin (2005) Altonji, J. G. and R. L. Matzkin (2005). Cross Section and Panel Data Estimators for Nonseparable Models with Endogenous Regressors. Econometrica 73(4), 1053–1102.

- Amemiya and Powell (1981) Amemiya, T. and J. L. Powell (1981, December). A comparison of the Box-Cox maximum likelihood estimator and the non-linear two-stage least squares estimator. Journal of Econometrics 17(3), 351–381.

- Andrews and Shi (2017) Andrews, D. and X. Shi (2017). Inference Based on Many Conditional Moment Inequalities. Journal of Econometrics 196, 274–287.

- Arellano and Bonhomme (2011) Arellano, M. and S. Bonhomme (2011). Nonlinear Panel Data Analysis. Annual Review of Economics 3, 395–424.

- Arellano and Carrasco (2003) Arellano, M. and R. Carrasco (2003). Binary Choice Panel Data Models with Predetermined Variables. Journal of Econometrics 115, 125–157.

- Arellano and Honoré (2001) Arellano, M. and Honoré (2001). Panel Data Models: Some Recent Developments. Handbook of econometrics, Volume 5, 3229–3296.

- Aristodemou (2021) Aristodemou, E. (2021). Semiparametric Identification in Panel Data Discrete Response Models. Journal of Econometrics 220(2), 253–271.

- Athey and Imbens (2006) Athey, S. and G. W. Imbens (2006). Identification and Inference in Nonlinear Difference-in-Differences Model. Econometrica 74(2), 431–497.

- Baetschmann (2012a) Baetschmann, G. (2012a). Identification and Estimation of Thresholds in the Fixed Effects Ordered Logit Model. Economics Letters 115(3), 416–418.

- Baetschmann (2012b) Baetschmann, G. (2012b). Identification and Estimation of Thresholds in the Fixed Effects Ordered Logit Model. Economics Letters 115(3), 416–418.

- Bartolucci et al. (2023) Bartolucci, F., C. Pigini, and F. Valentini (2023). Conditional inference and bias reduction for partial effects estimation of fixed-effects logit models. Empirical Economics 64, 2257–2290.

- Bester and Hansen (2009) Bester, C. A. and C. B. Hansen (2009). Identification of Marginal Effects in a Nonparametric Correlated Random Effects Model. Journal of Business and Economic Statistics 27(2), 235–250.

- Blundell and Powell (2003) Blundell, R. W. and J. L. Powell (2003). Endogeneity in Nonparametric and Semiparametric Regression Models. In M. Dewatripont, L. Hansen, and S. Turnovsky (Eds.), Advances in Economics and Econometrics: Theory and Applications, Volume Eighth World Congress, Vol. II. Oxford: Cambridge University Press.

- Blundell and Powell (2004) Blundell, R. W. and J. L. Powell (2004). Endogeneity in Semiparametric Binary Response Models. Review of Economic Studies 71(3), 655–679.

- Bonhomme (2012) Bonhomme, S. (2012). Functional Differencing. Econometrica 80(4), 1337–1385.

- Botosaru and Muris (2017) Botosaru, I. and C. Muris (2017). Binarization for Panel Models with Fixed Effects. Technical report. cemmap Working paper CWP31/17, available at https://www.cemmap.ac.uk/publication/binarization-for-panel-models-with-fixed-effects/.

- Botosaru et al. (2021) Botosaru, I., C. Muris, and K. Pendakur (2021). Identification of Time-Varying Transformation Models with Fixed Effects, with an Application to Unobserved Heterogeneity in Resource Shares. Journal of Econometrics.

- Botosaru et al. (2022) Botosaru, I., C. Muris, and S. Sokullu (2022). Partial Effects in Time-Varying Linear Transformation Panel Models with Endogeneity. Technical report. University of Bristol, School of Economics Discussion Paper 22/756.

- Chamberlain (1984) Chamberlain, G. (1984). Panel Data. In Z. Griliches and M. Intriligator (Eds.), Handbook of Econometrics, Volume 2, Chapter 22, pp. 1247–1315. Elsevier.

- Charlier et al. (2000) Charlier, E., B. Melenberg, and A. van Soest (2000). Estimation of a Censored Regression Panel Data Model Using Conditional Moment Restrictions Efficiently. Journal of Econometrics 95(1), 25–56.

- Chen (2010) Chen, S. (2010). An Integrated Maximum Score Estimator for a Generalized Censored Quantile Regression Model. Journal of Econometrics 155(1), 90–98.

- Chen et al. (2005) Chen, S., G. Dahl, and S. Khan (2005). Nonparametric Identification and Estimation of a Censored Location-Scale Regression Model. Journal of the American Statistical Association 100(469), 212–221.

- Chen et al. (2019) Chen, S., S. Khan, and X. Tang (2019). Exclusion Restrictions in Dynamic Binary Choice Panel Data Models: Comment on Semiparametric Binary Choice Panel Data Models Without Strictly Exogenous Regressors. Econometrica 87, 1781–1785.

- Chen et al. (2022) Chen, S., X. Lu, and X. Wang (2022). Nonparametric Estimation of Generalized Transformation Models with Fixed Effects. Econometric Theory, 1–32.

- Chen and Wang (2018) Chen, S. and X. Wang (2018). Semiparametric Estimation of Panel Data Models without Monotonicity or Separability. Journal of Econometrics 206, 515–530.

- Chernozhukov et al. (2013) Chernozhukov, V., I. Fernández-Val, J. Hahn, and W. K. Newey (2013). Average and Quantile Effects in Nonseparable Panel Models. Econometrica 81(2), 535–580.

- Chernozhukov et al. (2015) Chernozhukov, V., I. Fernández-Val, S. Hoderlein, H. Holzmann, and W. K. Newey (2015). Nonparametric Identification in Panels Using Quantiles. Journal of Econometrics 188(2), 378–392.

- Cox and Shi (2022) Cox, G. and X. Shi (2022). Simple Adaptive Size-Exact Testing for Full-Vector and Subvector Inference in Moment Inequality Models. The Review of Economic Studies.

- Das and van Soest (1999) Das, M. and A. van Soest (1999). A Panel Data Model for Subjective Information on Household Income Growth. Journal of Economic Behavior & Organization 40(4), 409–426.

- Davezies et al. (2022) Davezies, L., X. D’Haultfoeuille, and L. Laage (2022). Identification and Estimation of Average Marginal Effects in Fixed Effects Logit Models. Technical report. Available at https://doi.org/10.48550/arXiv.2105.00879.

- Dobronyi et al. (2021) Dobronyi, C., J. Gu, and K. i. Kim (2021). Identification of Dynamic Panel Logit Models with Fixed Effects. Technical report. Available at https://doi.org/10.48550/arXiv.2104.04590.

- Fernández-Val (2009) Fernández-Val, I. (2009). Fixed Effects Estimation of Structural Parameters and Marginal Effects in Panel Probit Models. Journal of Econometrics 150, 71–85.

- Fernández-Val and Weidner (2018) Fernández-Val, I. and M. Weidner (2018). Fixed Effects Estimation of Large-T Panel Data Models. Annual Review of Economics 10, 109–138.

- Ghanem (2017) Ghanem, D. (2017). Testing Identifying Assumptions in Nonseparable Panel Data Models. Journal of Econometrics 197, 202–217.

- Graham and Powell (2012) Graham, B. and J. Powell (2012). Identification and Estimation of Average Partial Effects in "Irregular" Correlated Random Coefficient Panel Data Models. Econometrica 80(5), 2105–2152.

- Han (1987) Han, A. K. (1987). Non-Parametric Analysis of a Generalized Regression Model: The Maximum Rank Correlation Estimator. Journal of Econometrics 35, 303–316.

- Hoderlein and White (2012) Hoderlein, S. and H. White (2012). Nonparametric Identification in Nonseparable Panel Data Models with Generalized Fixed Effects. Journal of Econometrics 168(2), 300–314.

- Honoré (1992) Honoré, B. (1992). Trimmed LAD and Least Squares Estimation of Truncated and Censored Regression Models with Fixed Effects. Econometrica 60(3), 533–565.

- Honoré (1993) Honoré, B. (1993). Orthogonality Conditions for Tobit Models with Fixed Effects and Lagged Dependent Variables. Journal of Econometrics 59, 35–61.

- Honoré and Hu (2020) Honoré, B. and L. Hu (2020). Selection Without Exclusion. Econometrica 88, 1007–1029.

- Honoré and Powell (1994) Honoré, B. and J. Powell (1994). Pairwise difference estimators of censored and truncated regression models. Journal of Econometrics 64(1-2), 241–278.

- Honoré and Tamer (2006) Honoré, B. and E. Tamer (2006). Bounds on Parameters in Panel Dynamic Discrete Choice Models. Econometrica 74(3), 611–629.

- Honore (2008) Honore, B. E. (2008). On marginal effects in semiparametric censored regression models. Technical report. Available at SSRN: https://ssrn.com/abstract=1394384 or http://dx.doi.org/10.2139/ssrn.1394384.

- Honoré et al. (2000) Honoré, B. E., E. Kyriazidou, and J. L. Powell (2000, January). Estimation of tobit-type models with individual specific effects. Econometric Reviews 19(3), 341–366.

- Horowitz and Lee (2004) Horowitz, J. and S. Lee (2004). Semiparametric Estimation of a Panel Data Proportional Hazards Model with Fixed Effects. Journal of Econometrics 119, 155–198.

- Ichimura (1993) Ichimura, H. (1993). Semiparametric Least Squares (SLS) and Weighted SLS Estimation of Single-Index Models. Journal of Econometrics 58, 71–120.

- Johnson (2004) Johnson, E. G. (2004). Panel Data Models With Discrete Dependent Variables. Phd thesis, stanford university.

- Khan et al. (2011) Khan, S., M. Ponomareva, and E. Tamer (2011). Sharpness in Randomly Censored Linear Models. Economic Letters 113, 23–25.

- Khan et al. (2016) Khan, S., M. Ponomareva, and E. Tamer (2016). Identification of Panel Data Models with Endogenous Censoring. Journal of Econometrics 94, 57–75.

- Khan et al. (2023) Khan, S., M. Ponomareva, and E. Tamer (2023). Identification of Dynamic Binary Response Models. Journal of Econometrics 237.

- Lee (2008) Lee, S. (2008). Estimating Panel Data Duration Models with Censored Data. Econometric Theory 24, 1254–1276.

- Lin and Wooldridge (2015) Lin, W. and J. M. Wooldridge (2015). On Different Approaches to Obtaining Partial Effects in Binary Response Models with Endogenous Regressors. Economics Letters 134, 58–61.

- Liu et al. (2023) Liu, L., A. Poirier, and J.-L. Shiu (2023). Identification and Estimation of Average Partial Effects in Semiparametric Binary Response Panel Models. Technical report. Available at https://doi.org/10.48550/arXiv.2105.12891.

- Manski (1987) Manski, C. (1987). Semiparametric Analysis of Random Effects Linear Models From Binary Panel Data. Econometrica 55(2), 357–362.

- Muris (2017) Muris, C. (2017). Estimation in the Fixed-Effects Ordered Logit Model. Review of Economics and Statistics 99(3), 465–477.

- Pakel and Weidner (2023) Pakel, C. and M. Weidner (2023). Bounds on Average Effects in Discrete Choice Panel Data Models. Technical report. Available at https://doi.org/10.48550/arXiv.2309.09299.

- Powell (1991) Powell, J. (1991). Monotonic Regression Models under Quantile Restrictions. In W. A. Barnett, J. Powell, and G. E. Tauchen (Eds.), Nonparametric and Semiparametric Methods in Econometrics and Statistics: Proceedings of the Fifth International Symposium in Economic Theory and Econometrics, Chapter 14, pp. 357–384. Cambridge University Press.

- Powell et al. (1989) Powell, J., J. Stock, and T. Stoker (1989). Semiparametric estimation of index coefficients. Econometrica 57(6), 1403–1430.

- Powell (1984) Powell, J. L. (1984, July). Least absolute deviations estimation for the censored regression model. Journal of Econometrics 25(3), 303–325.

- Powell (1996) Powell, J. L. (1996, June). Rescaled methods-of-moments estimation for the Box-Cox regression model. Economics Letters 51(3), 259–265.

- Song and Wang (2021) Song, P. and S. Wang (2021). A Further Remark on the Alternative Expectation Formula. Communications in Statistics - Theory and Methods 50(11), 2586–2591.

- Wang and Chen (2020) Wang, X. and S. Chen (2020). Semiparametric Estimation of Generalized Transformation Panel Data Models with Non-Stationary Error. The Econometrics Journal 23(3), 386–402.

Appendix A Proofs

Proof of Theorem 1..

Define the (potential) latent variables

| (19) | ||||

Assumption 2 obtains the following equivalent relationships:

| (20) | |||

| (21) |

that is, the counterfactual outcome being greater than a fixed value is equivalent to the random variable being smaller than the counterfactual index evaluated at .

Then, for any value , the following are equivalent:

To see this, suppose that there exists a such that

Then:

where the inequality follows by weak monotonicity of CDFs. ∎

Proof of Theorem 2.

Appendix B Numerical experiment with discrete regressors

We consider here a numerical exercise inspired by Section 8 in Chernozhukov et al. (2013): a probit model with discrete regressors. When the structural equation is time-invariant, the data generating process corresponds to that in Chernozhukov et al. (2013). We present results for, first, the time-invariant case – for which our bounds correspond to those in Chernozhukov et al. (2013), and then for a time-varying case.

The data generating process is:

| (23) | ||||

We consider the ATE at , defined as:

Recall that refers to the counterfactual probability that in period (first index), the probability that the counterfactual outcome under (second index) for the the subpopulation with equals or exceeds (third index). For simplicity, we set , so that the counterfactual index for the analysis that follows is:

| (24) |

According to Theorem 2, if the observed index is smaller (greater) than the counterfactual index (24), the observed probability associated with the observed index provides a lower (upper) bound on the counterfactual probability, while if the observed index equals the counterfactual index, the observed probability point identifies the counterfactual probability.

First, in order to compare our results to those in Chernozhukov et al. (2013), we set .212121In this case, there are no time effects, so the outcome equation is time-homogeneous, as required by the results of Chernozhukov et al. (2013). Theorem 2 then obtains the following results for and . Note that is point-identified for the subpopulations with

because for the listed subpopulations, the value is observed in at least one of the periods. Thus:

For the subpopulation of stayers with , the value is not observed in either time period, so the counterfactual probability is partially identified unless :

This is because the observed index for this subpopulation is in both time periods.

The analysis for is similar and omitted. Figure 5 plots the bounds for . Note that our bounds for this particular example coincide with those in Chernozhukov et al. (2013) that the authors call “NPM.”

Consider now the specification with positive time effects, . Theorem 2 then obtains the following results for and .

First, is point-identified for the subpopulations with : the stayers with and the movers with . This is because at for those subpopulations, so that the observed index for these subpopulations equals the counterfactual index. Thus,

Second, for the subpopulation of movers with , the period observed probability provides a lower bound on because the observed index for this subpopulation is , which is smaller than the counterfactual index since we assumed that , so:

Whether the observed probabilities point or partially identify for this subpopulation depends on how the observed index compares to the counterfactual index in (24):

Third, for the subpopulation of stayers with , the observed index at is , so that comparing it to the counterfactual index in (24) obtains:

while the observed index at for this subpopulation is , which compared to the same counterfactual index in (24) obtains:

We have now described all the restrictions underlying Theorem 2 for for all in our example. The bounds now follow by selecting the best bounds for each case and for each as in Theorem 2. The same analysis can be done for and for period 2 counterfactuals.

Figure 6 plots the bounds for ATEt=1 (left panel) and ATEt=2 (right panel). The solid lines correspond to the true ATEs, while the dashed lines correspond to their respective bounds, grouped by color. The colors correspond to different values of . For example, in both panels, the red lines correspond to the true ATE and its bounds when (no time-effects). In the left panel, all true ATEs have the same value since there are no time-effects, , while in the right panel the true ATEs have different values because they correspond to different time effects.