Explicit Caplet Implied Volatilities for Quadratic Term-Structure Models

Abstract

We derive an explicit asymptotic approximation for implied volatilities of caplets under the assumption that the short-rate is described by a generic quadratic term-structure model. In addition to providing an asymptotic accuracy result, we perform experiments in order to gauge the numerical accuracy of our approximation.

Keywords: quadratic term-structure, simple forward rate, implied volatility, caplet.

MSC Codes: 60G99, 35C20, 91-08.

JEL Classification: C600 , C630 , C650, G190, G100.

1 Introduction

In a general term-structure framework, the instantaneous short-rate of interest is given by an explicit function of time and some auxiliary factors, which are typically modeled as the solution of a (multi-dimensional) stochastic differential equation. By far the most well-known class of term-structure models are the affine term-structure (ATS) models which, as the name suggests, model the short rate as an affine function of the auxiliary factor process. Notable ATS models include the Vasicek Vasicek [1977], Cox-Ingersoll-Ross (CIR) Cox et al. [2005] and Hull-White Hull and White [1990] models. ATS models have enjoyed widespread popularity because they allow for zero-coupon bond prices to be written explicitly as exponential affine functions of the auxiliary factors.

A somewhat lesser-known class of term-structure models are the quadratic term-structure (QTS) models, which, as the name suggests, model the short rate as an quadratic function of the auxiliary factor process.

QTS models include some ATS models as special cases and also offer some additional modeling flexibility due to the fact that the zero-coupon bond price can be written as exponential quadratic functions of the auxiliary factors. Moreover, empirical results from Ahn et al. [2002] indicate that QTS better capture historical bond price than ATS models.

The purpose of this paper is to derive an explicit approximation for implied volatilities of options written on simple forward rates, assuming the underlying short-rate is given by a general QTS model. The implied volatility approximation we obtain is based on the coefficient polynomial expansion method that was introduced by Pagliarani and Pascucci [2012] in order to derive approximate option prices in a scalar setting and later extended in Lorig et al. [2017] in order to derive approximate implied volatilities in a multi-factor local-stochastic volatility (LSV) setting. Our work is similar in some senses to Lorig and Suaysom [2022], who also employ the polynomial expansion method to derive approximate implied volatilities. But, there are two important differences between that work and ours: (i) Lorig and Suaysom [2022] derived implied volatilities for options on bonds rather than on simple-forward rates and (ii) Lorig and Suaysom [2022] focus on ATS rather than QTS models. For related work on implied volatility in a Heath-Jarrow-Morton (HJM) setting, we refer the reader to Angelini and Herzel [2006].

The rest of the paper proceeds as follows:

in Section 2 we introduce a financial market in which the short-rate of interest is described by the class of QTS models. In Section 3 we provide a concise review of how to explicitly price options on bonds and simple forward rates (including caplets) in a QTS setting using Fourier transforms.

In Section 4 we provide a precise link (see Proposition 4 and Remark 5) between simple forward rates and classical multi-factor LSV models. We use this result in Section 5

to develop an explicit approximation for caplet prices.

In Section 6, we translate the price approximation into a corresponding approximation of implied volatility.

Lastly, in Section 7, we perform experiments to gauge the numerical accuracy of our implied volatility approximation.

2 Quadratic term-structure models

We fix a time horizon and consider a continuous-time financial market, defined on a filtered probability space with no arbitrages and no transaction costs. The probability measure represents the market’s chosen pricing measure taking the money market account as numéraire. The filtration represents the history of the market.

We suppose that the money market account is strictly positive, continuous and non-decreasing. As such, there exists a non-negative -adapted short-rate process such that

| (1) |

We will focus on the case in which the dynamics of the short-rate are described by a QTS model. Specifically, let , be the unique strong solution of a stochastic differential equation (SDE) of the following form

| (2) |

where is a column vector, the matrix is diagonalizable and has negative real components of eigenvalues, the matrix and is a -dimensional -Brownian motion. Then, following [Ahn et al., 2002, Section 2], every equivalence class of QTS models has a unique canonical representation of the form

| (3) |

for some constant and some matrix that is positive semidefinite and satisfies for . Note that the restrictions on and guarantee that the short-rate is non-negative.

3 Pricing options on bonds and simple forward rates in a QTS setting

In this section we provide a formal review of how to explicitly price options on bonds and simple forward rates in the QTS setting. For a rigorous treatment of the results presented below, we refer the reader to [Chen et al., 2004, Section 4.3]. To begin, for any , column vector and matrix , let us define by

| (4) |

where denotes the -conditional expectation under . The existence of the function follows from the Markov property of . Formally, the function satisfies the Kolmogorov backward partial differential equation (PDE)

| (5) |

where the operator is the generator of under . Explicitly, the generator is given by

| (6) |

where , and “Tr” denotes the trace operator. The solution to (5) is given by

| (7) |

where, from [Chen et al., 2004, Theorem 3.6], the scalar-valued function , the vector-valued function and the matrix-valued function solve the following system of ordinary differential equations (ODEs)

| (8) | ||||

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) |

The solution to the system (9),(11) and (13) exists and is unique.

As , and will appear frequently throughout this paper, it will be convenient to define

| (14) |

Now, for any , let us denote by the value of a zero-coupon bond that pays one unit of currency at time . In the absence of arbitrage, the process must be a -martingale. As such, we have

| (15) |

where we have used . Solving for , we obtain

| (16) | ||||

| (17) |

where the third equality follows from (4) and the fourth equality follows from (7) and (14).

3.1 Pricing options on zero-coupon bonds

Let denote the value of a European option that pays at time for some function . With the aim of finding , let denote the generalized Fourier transform of , which is defined as follows

| (18) |

We can recover from using the inverse Fourier transform

| (19) |

Now, noting that, in the absence of arbitrage, the process must be a -martingale, we have

| (20) |

Solving for , we obtain

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) | ||||

| (25) | ||||

| (26) |

In general, the inverse Fourier integral (25) that defines must be computed numerically.

Remark 1.

As -a.s., values of for do not affect the conditional expectation (21) and thus do not affect the value of the option. The values of for do, however, affect convergence properties of the Fourier transform (18) and inverse Fourier transform (19). As such, it makes sense to choose values of for so that these integrals converge for some value of .

3.2 Pricing options on simple forward rates

The simple forward rate from to is a process , which is defined as follows

| (27) |

Let denotes the value of a European forward rate option with reset date and settlement date that pays at time for some function . Because the payoff to be made at time is known at time we have

| (28) |

To see this, simply note that . Using (27) and , we can express as a function of as follows

| (29) |

Thus, we can view a forward rate option on with reset date , settlement date and payoff as a European option on with expiration date and payoff , where is defined in (29). It follows that

| where | (30) |

with given by (26).

Example 2.

An important example of a European forward rate option is a caplet, which has a payoff

| (31) |

Here, is the strike of the caplet. We have from (30) that

| (32) |

and thus, from (18), the generalized Fourier transform of is given by

| (33) |

The caplet price can now be computed by inserting the expression (33) for into (25) and evaluating the integral numerically.

4 Relation between QTS models and LSV models

While (26) and (30) in conjunction with (33) can be used to compute caplet prices explicitly, the resulting expression tells us very little about the corresponding implied volatilities. In this section, we will establish a precise relation between QTS models and LSV models. This relation will be used in subsequent sections to find an explicit approximation for caplet prices and implied volatilities.

We begin by deriving the dynamics of . Using (1) and (17), we have by Itô’s Lemma that

| (34) |

where we have introduced the vector-valued function , which is defined as follows

| (35) | ||||

| (36) |

Now, let us denote by the -forward probability measure, whose relation to is given by the following Radon-Nikodym derivative

| (37) |

where . Observe that the last equality follows from (34). By Girsanov’s theorem and (37), the process , defined as follows

| (38) |

is a -dimensional -Brownian motion. The following lemma will be useful.

Lemma 3.

Let denotes the value of a self-financing portfolio and let , defined by , be the -forward price of . Then the process is a -martingale.

Proof.

Define the Radon-Nikodym derivative process by . Using the fact that is a -martingale as well as [Shreve, 2004, Lemma 5.2.2] we have for any that

| (39) |

where denotes the -conditional expectation under . Dividing both sides of equation (39) by and canceling common factors of and , we obtain

| (40) |

which establishes that is a -martingale, as claimed. ∎

Note from (27) that is the -forward price of a static portfolio consisting of shares of and shares of . As such, we have from Lemma 3 that is a -martingale.

It will be helpful to write the dynamics of under the -forward measure .

Using Itô’s Lemma, (27), (34) and (38), we obtain

| (41) | ||||

| (42) | ||||

| (43) |

Now, let us denote by the of the simple forward rate from to , that is

| (44) |

We are now in a position to state the main result of this section.

Proposition 4.

As in Section 3.2, let denote the value of a European forward rate option with reset date and settlement date that pays at time for some function . Let denote the -forward price of . Then, there exists a function such that

| (45) |

Moreover, the function satisfies the following PDE

| (46) |

where the operator is given by

| (47) | ||||

| (48) | ||||

| (49) |

Proof.

We begin by writing the dynamics of and under the -forward probability measure . First, using Itô’s Lemma and (43), we obtain

| (50) | ||||

| (51) |

Next, using (2) and (38), we find

| (52) |

The pair is a Markov process whose generator under is given by (49). Now, using the fact that -forward prices are -martingales and the fact that the process is Markov, there exists a function such that

| (53) |

where, in the third equality, we have used (28). We have from (53) that the function satisfies the Kolmogorov backward PDE (46). ∎

A few important remarks are in order.

Remark 5.

As is a positive -martingale, the process can be seen as a classical LSV model, where represents non-local factors of volatility. For example, when we have from (49) that

| (54) |

where the functions , , and are given by

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) |

Remark 6.

The instantaneous covariance matrix of the process is singular due to the fact that can be written as an explicit function of and . Indeed, using (17), (27) and (44), we have

| (59) |

As a result, the generator defined in (49) is not uniformly elliptic. The setting here is similar to the settings in Leung et al. [2017] and Barletta et al. [2019] where the authors use the approximation methods described in Sections 5 and 6 of this paper to find explicit approximations of implied volatility for options on leveraged exchange traded funds and the VIX, respectively. As the authors of those papers point out, the lack of a uniformly elliptic generator does not complicate the construction of a formal implied volatility approximation.

Remark 7.

Let . Had the function defined in (59) been invertible with respect to for some , we could have written where is the inverse of with respect to . The process would have been a -dimensional Markov process with a non-singular instantaneous covariance matrix and thus, a uniformly elliptic generator. This was the approach taken in Lorig and Suaysom [2022], where the authors found explicit approximations of implied volatilities for options on bonds in an affine (as opposed to quadratic) term-structure setting.

5 Option price asymptotics

Let . We have from (46) that the function satisfies a parabolic PDE of the form

| (61) |

where, for brevity, we have omitted the dependence on and . Note that we have introduced standard multi-index notation

| (62) |

In general, there is no explicit solution to PDEs of the form (61). In this section, we will show in a formal manner how an explicit approximation of can be obtained by using a simple Taylor series expansion of the coefficients of . The method described below was introduced for scalar diffusions in Pagliarani and Pascucci [2012] and subsequently extended to -dimensional diffusions in Lorig et al. [2017, 2015].

To begin, for any and , let be the unique classical solution to

| (63) |

where the operator is defined as follows

| with | (64) |

Observe that and thus . We will seek an approximate solution of (63) by expanding and in powers of . Our approximation for will be obtained by setting in our approximation for . We have

| (65) |

where the functions are, at the moment, unknown, and the operators are given by

| (66) |

Note that is the sum of the th order terms in the Taylor series expansion of about the point . Inserting the expansions from (65) for and into PDE (63) and collecting terms of like order in we obtain

| (67) | |||||||

| (68) |

Now, observe that the coefficients of do not depend on . Thus, is the generator of a -dimensional Brownian motion with a time-dependent drift vector and covariance matrix. As such, is given by

| (69) |

where is the semigroup generated by and is the associated transition density (i.e., the solution to (67) with ). Explicitly, we have

| (70) |

where m and are given by

| (71) |

and and are, respectively, the instantaneous drift vector and covariance matrices

| (72) |

By Duhamel’s principle, the solution of (68) is

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |

While the expression (75) for is explicit, it is not easy to compute as written because operating on a function with requires performing a -dimensional integral. The following proposition establishes that can be expressed as a differential operator acting on .

Proposition 9.

Proof.

Having obtained expressions for the functions as differential operators acting on , we define , the th order approximation of , as follows

| (85) |

Note that depends on the choice of . In general, if one is interested in the value of a good choice for is .

6 Implied volatility asymptotics

In this section, we show how to translate the price approximation developed in Section 5 into an approximation of Black implied volatilities associated with caplets. The derivation below closely follows the derivation in Lorig et al. [2017], where the authors develop an approximation for Black-Scholes implied volatilities associated with call options on equity.

Throughout this section, we fix a QTS model (2)-(3), an initial date , a reset date , a settlement date , the initial values and a caplet payoff . Our goal is to find an approximation of implied volatility for this particular caplet. To ease notation, we will sometimes hide the dependence on . However, the reader should keep in mind that the implied volatility of the caplet under consideration does depend on , even if this is not explicitly indicated. Below, we remind the reader of the Black model and provide definitions of the Black price and Black implied volatility, which will be used throughout this section.

In the Black model, the dynamics of the simple forward rate are given by

| and thus | (86) |

where is the Black volatility and is a scalar -Brownian motion. Equation (86) leads to the following definitions.

Definition 10.

The -forward Black price of a caplet, denoted , is defined as follows

| (87) |

where the dynamics of are given by (86) and

| (88) |

Definition 11.

The Black implied volatility corresponding to the -forward price of a caplet is the unique positive solution of the equation

| (89) |

where the Black price is given by (87).

Now, suppose that is the -forward price of a caplet corresponding to a QTS model, where we have now indicated the dependence on the strike explicitly. As in Section 5, we will seek an approximation of the implied volatility corresponding to by expanding in power of . Our approximation of will then be obtained by setting . We have

| (90) |

where are, at the moment, unknown. Expanding the Black price in powers of we obtain

| (91) | ||||

| (92) | ||||

| (93) | ||||

| (94) | ||||

| (95) |

where is given by (76). Inserting the expansions for and into the equation and collecting terms of like order in we obtain

| (96) | |||||

| (97) |

Now, from (69) and (87) we have

| (98) |

where is defined in (71). Thus, it follows from (96) that

| (99) |

Having identified , we can use (97) to obtain recursively for every . We have

| (100) |

Using the expression given in (77) for , one can show that is an th order polynomial in -moneyness with coefficients that depend on ; see [Lorig et al., 2017, Section 3] for details. We provide explicit expressions for , , and for in Appendix A.

We now define our th order approximation of implied volatility as

| (101) |

where is given by (100). If we set in the price approximation, then the corresponding implied volatility approximation (101) satisfies the following asymptotic accuracy result

| as | (102) |

within the parabolic region for some . The proof of (102) is a direct consequence of [Barletta et al., 2019, Theorem 3.10].

7 Numerical example: Quadratic Ornstein-Uhlenbeck model

Throughout this section, we consider a QTS model, whose dynamics are as follows

| (103) |

where the constants are positive and are nonnegative. Noting that is an Ornstein-Uhlenbeck process, we refer to the model (103) as the Quadratic Ornstein-Uhlenbeck (QOU) model.

Remark 12.

If we consider the special case . then we have by Itô’s lemma that

| (104) |

Note that (104) is a Cox-Ingersoll-Ross (CIR) process with a mean , rate of mean-reversion and volatility . Thus, the QOU model contains as a special case, some (but not all) CIR short-rate models.

Comparing (103) with (2) and (3) we obtain

| (105) |

Next, we can obtain from (9), (11), and (13) that satisfies the following system of ODEs

| (106) |

Solving (106), we obtain

| (107) |

| (108) |

where the functions for are given by

| (109) | ||||||

| (110) | ||||||

| (111) | ||||||

| (112) |

Next, from (54) we have the form of the generator

| (113) |

where the functions , , and are given by

| (114) | ||||

| (115) | ||||

| (116) | ||||

| (117) |

Introducing the notation

| where | (118) |

the explicit implied volatility approximation can now be computed up to order using the formulas in Appendix A. We have

| (119) | ||||

| (120) | ||||

| (121) |

where we have omitted the 2nd order term due to its considerable length.

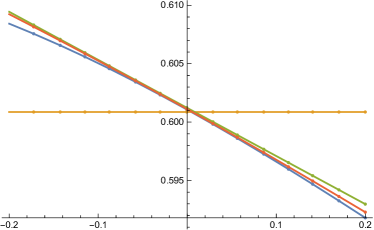

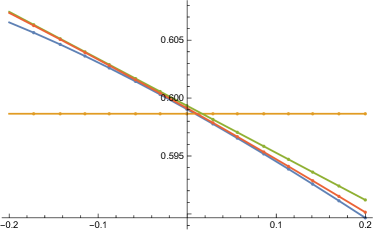

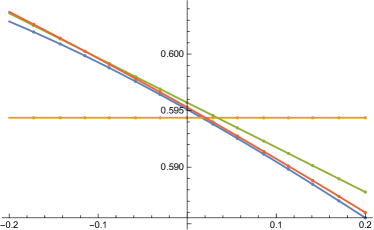

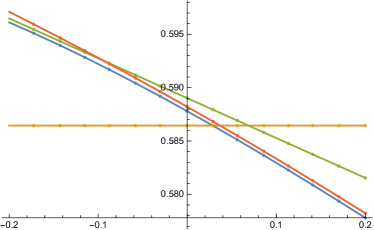

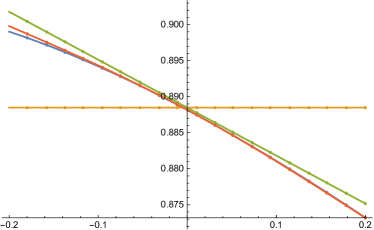

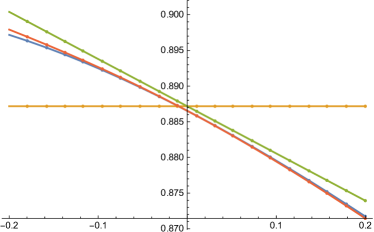

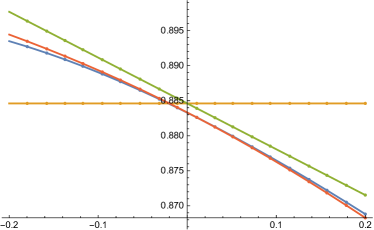

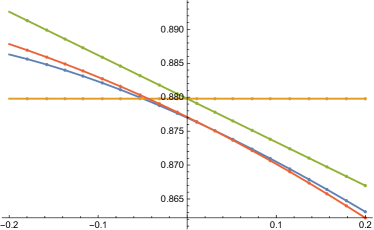

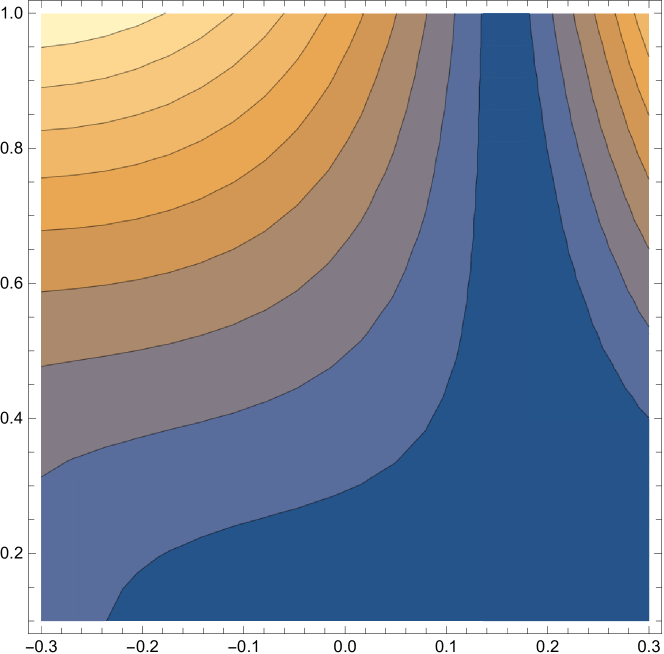

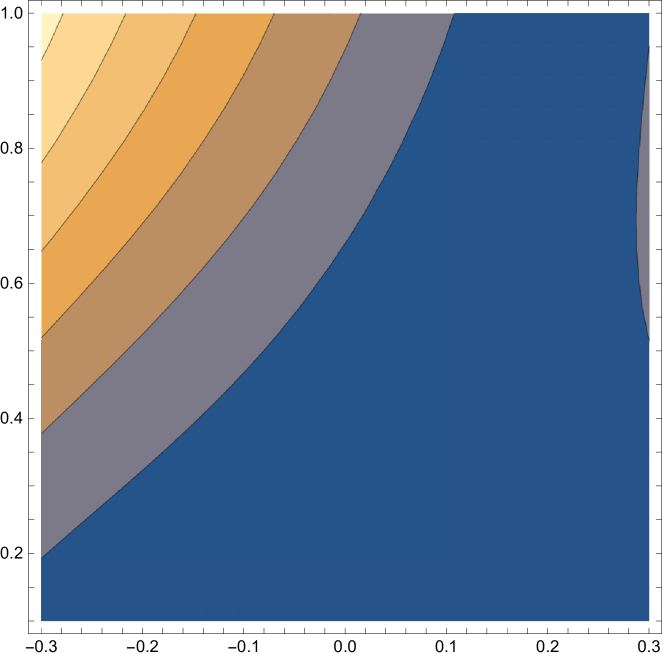

In Figures 1 and 2, using different parameters for , we plot our explicit approximation of implied volatility up to order as a function of -moneyness with and fixed and with reset date ranging over .

For comparison, we also plot the “exact” implied volatility , which can be computed using -forward caplet prices using (60) and inverting the Black formula (87) numerically.

In both figures, we observe that the second order approximation accurately matches the level, slope, and convexity of the exact implied volatility near-the-money for all four reset dates.

In Figures 3 and 4, using the same values for as in Figures 1 and 2, respectively, we plot the absolute value of the relative error of our second order approximation as a function of -moneyness and reset date .

Consistent with the asymptotic accuracy results (102), we observe that the errors decrease as we approach the origin in both directions of and .

Appendix A Explicit expressions for , and

In this appendix we give the expressions for the implied volatility approximation using (99) and (100) explicitly up to second order for in terms of the coefficients ,,, and of , given in (54), by performing Taylor’s series expansion of the coefficients around . To ease the notation, we define

| (122) |

The zeroth order term is given by

| (123) |

Next, let us define

| (124) |

where is the th-order Hermite polynomial. Then the first order term is given by

| (125) |

where and are given by

| (126) | ||||

| (127) |

Lastly, the second order term is given by

| (128) |

where the terms , , are given by

| (129) | ||||

| (130) | ||||

| (131) | ||||

| (132) | ||||

| (133) | ||||

| (134) | ||||

| (135) | ||||

| (136) | ||||

| (137) | ||||

| (138) | ||||

| (139) | ||||

| (140) | ||||

| (141) | ||||

| (142) | ||||

| (143) | ||||

| (144) | ||||

| (145) | ||||

| (146) | ||||

| (147) | ||||

| (148) | ||||

| (149) | ||||

| (150) | ||||

| (151) | ||||

| (152) | ||||

| (153) | ||||

| (154) | ||||

| (155) | ||||

| (156) | ||||

| (157) |

Note that, although and appear in the expressions for and , the 3rd and 4th order terms in cancel the 3rd and 4th order terms resulting from , , and , respectively, resulting in a second order implied volatility expansion that is quadratic in .

References

- Ahn et al. [2002] D.-H. Ahn, R. F. Dittmar, and A. R. Gallant. Quadratic term structure models: Theory and evidence. The Review of financial studies, 15(1):243–288, 2002.

- Angelini and Herzel [2006] F. Angelini and S. Herzel. Notes and comments: An approximation of caplet implied volatilities in gaussian models. Decisions in Economics and Finance, 28(2):113–127, 2006.

- Barletta et al. [2019] A. Barletta, E. Nicolato, and S. Pagliarani. The short-time behavior of vix-implied volatilities in a multifactor stochastic volatility framework. Mathematical Finance, 29(3):928–966, 2019.

- Chen et al. [2004] L. Chen, D. Filipović, and H. V. Poor. Quadratic term structure models for risk-free and defaultable rates. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 14(4):515–536, 2004.

- Cox et al. [2005] J. C. Cox, J. E. Ingersoll Jr, and S. A. Ross. A theory of the term structure of interest rates. In Theory of valuation, pages 129–164. World Scientific, 2005.

- Hull and White [1990] J. Hull and A. White. Pricing interest-rate-derivative securities. The review of financial studies, 3(4):573–592, 1990.

- Leung et al. [2017] T. Leung, M. Lorig, and A. Pascucci. Leveraged etf implied volatilities from etf dynamics. Mathematical Finance, 27(4):1035–1068, 2017.

- Lorig and Suaysom [2022] M. Lorig and N. Suaysom. Options on bonds: implied volatilities from affine short-rate dynamics. Annals of Finance, pages 1–34, 2022.

- Lorig et al. [2015] M. Lorig, S. Pagliarani, and A. Pascucci. Analytical expansions for parabolic equations. SIAM Journal on Applied Mathematics, 75:468–491, 2015.

- Lorig et al. [2017] M. Lorig, S. Pagliarani, and A. Pascucci. Explicit implied volatilities for multifactor local-stochastic volatility models. Mathematical Finance, 27(3):926–960, 2017. ISSN 1467-9965. doi: 10.1111/mafi.12105. URL http://dx.doi.org/10.1111/mafi.12105.

- Pagliarani and Pascucci [2012] S. Pagliarani and A. Pascucci. Analytical approximation of the transition density in a local volatility model. Cent. Eur. J. Math., 10(1):250–270, 2012. ISSN 1895-1074. doi: 10.2478/s11533-011-0115-y. URL http://dx.doi.org/10.2478/s11533-011-0115-y.

- Shreve [2004] S. E. Shreve. Stochastic calculus for finance II: Continuous-time models, volume 11. Springer Science & Business Media, 2004.

- Vasicek [1977] O. Vasicek. An equilibrium characterization of the term structure. Journal of financial economics, 5(2):177–188, 1977.

|

|

|

|

|

|

|

|

|

|