appendixOnlyFilter segment=1 and not segment=0

The unequal effects of the health-economy tradeoff during the COVID-19 pandemic⋆

Abstract

The potential tradeoff between health outcomes and economic impact has been a major challenge in the policy making process during the COVID-19 pandemic. Epidemic-economic models designed to address this issue are either too aggregate to consider heterogeneous outcomes across socio-economic groups, or, when sufficiently fine-grained, not well grounded by empirical data. To fill this gap, we introduce a data-driven, granular, agent-based model that simulates epidemic and economic outcomes across industries, occupations, and income levels with geographic realism. The key mechanism coupling the epidemic and economic modules is the reduction in consumption demand due to fear of infection. We calibrate the model to the first wave of COVID-19 in the New York metropolitan area, showing that it reproduces key epidemic and economic statistics, and then examine counterfactual scenarios. We find that: (a) both high fear of infection and strict restrictions similarly harm the economy but reduce infections; (b) low-income workers bear the brunt of both the economic and epidemic harm; (c) closing non-customer-facing industries such as manufacturing and construction only marginally reduces the death toll while considerably increasing unemployment; and (d) delaying the start of protective measures does little to help the economy and worsens epidemic outcomes in all scenarios. We anticipate that our model will help designing effective and equitable non-pharmaceutical interventions that minimize disruptions in the face of a novel pandemic.

Since the outset of the COVID-19 pandemic, governments worldwide have successfully slowed down the transmission of SARS-CoV-2 by enacting non-pharmaceutical interventions (NPIs) [1]. These interventions include the shutdown, to different degrees and extents, of non-essential customer-facing economic activities, e.g. entertainment and restaurants, and the mandating of work-from-home policies. Such protective measures have heterogeneous outcomes across socio-economic groups (“distributional effects”): workers who work in non-essential industries or can work from home become less likely to get exposed to the pathogen while essential, in-person workers remain at a higher risk of exposure. At the same time, NPIs have different distributional economic effects depending on the industry and occupation of the workers. For example, low-income workers are more likely to work in customer-facing industries and perform in-person occupations, leading to high risk of unemployment when these industries are closed [2, 3].

Together with NPIs, the COVID-19 pandemic induced very strong behavioral change, as individuals voluntarily reduced their contacts and their consumption of customer-facing services out of fear they would get infected. How effective exactly this mechanism is compared to NPIs remains debated [4, 5, 6], and whether behavior change has distributional consequences like NPIs do, is an open problem.

Addressing the effectiveness of NPIs over behavior change, both at the aggregate and distributional level, requires building theoretical, mechanistic models that jointly simulate epidemic and economic dynamics at a fine-grained level. Most of the models that have been put forward [7, 8, 9, 10, 11], however, are quite aggregate on the epidemic and/or economic dimension, and so are not fully equipped to study distributional outcomes. There are a few Agent-Based Models (ABMs) that simulate epidemic spreading and economic decisions at the level of individual, heterogeneous agents [12, 13, 14], but these models are mostly meant to qualitatively evaluate different policies, with a basic parameter calibration that matches only a few aggregate moments of the data.

In this paper, we introduce an ABM that simulates epidemic and economic outcomes of a large synthetic population in a metropolitan area. The socio-economic characteristics of the agents and their consumption and contact patterns are initialized from detailed census, survey and mobility data, while the structure of the economy is initialized from input-output tables and national and regional accounts. Our joint epidemic-economic ABM merges and largely extends our former epidemic [15, 16] and economic [2, 17] COVID-19 models.

The epidemic-economic model.

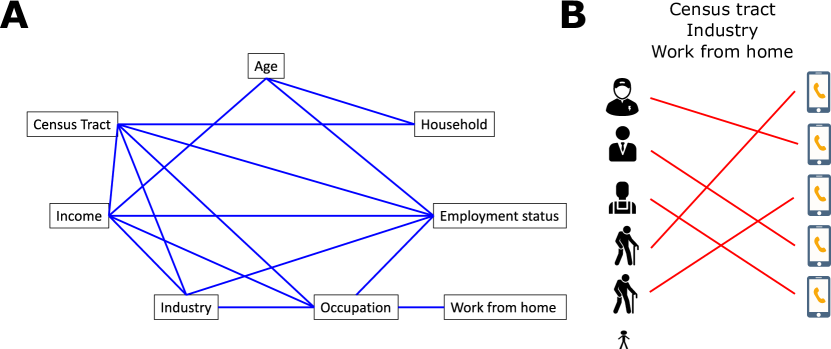

We build a data-driven, granular, ABM of the New York-Newark-Jersey City, NY-NJ-PA Metro Area. The main agents of the model are the 416,442 individuals of a synthetic population that is representative of the real population across multiple socio-economic characteristics, including household composition, age, income, occupation and possibility to work from home (see Figure 1 for a schematic representation, and Materials and Methods and Supplementary Information for a detailed description of the model).

The epidemic module of the ABM is built on the contact network that connects synthetic individuals. This network has multiple layers, where each layer captures interactions occurring (i) in the household; (ii) in school; (iii) in the workplace; (iv) in the community (during on-site consumption, such as in shops, restaurants or movie theaters). The epidemic propagates on these contact networks. We initialize contacts between individuals in the workplace and community layer by using a longitudinal database of detailed, privacy-enhanced mobility data from anonymized users who have opted-in to provide access to their (mobile phone-based) location data, through a GDPR-compliant framework provided by Cuebiq. At a daily level, we observe workplace visitation patterns among our panel of users. We are also able to estimate the probability of co-location of users in the same community places, as obtained from a dataset provided by Foursquare. On top of the contact networks and synthetic population, we run a stochastic, discrete-time transmission model in which individuals transition from one epidemic state to the other according to the distributions of key time-to-event intervals (e.g., incubation period, generation time) as per available data on SARS-CoV-2 transmission.

From an economic point of view, individuals play a role as workers and consumers. They work in one of multiple industries, producing goods and services that are either sold to other industries as intermediate products or sold to final consumers as consumption products. The economic module is particularly detailed on employment and consumption. Hiring and firing depend on industries’ workforce needs, closures of economic activities and the possibility for workers to work from home. Consumption is heterogeneous for agents with different age and income, and changes depending on the state of the pandemic as households reduce the consumption demand for customer-facing industries due to fear of infection (customer-facing industries are: entertainment, accommodation-food, other services, retail, transportation, health, education; see Supplementary Section S3.1.3). The model also considers the input-output network of intermediates that industries use to produce final goods and services [18], thus considering the propagation of COVID-19 shocks to the entire economy.

Modeling the first wave of COVID-19 in New York.

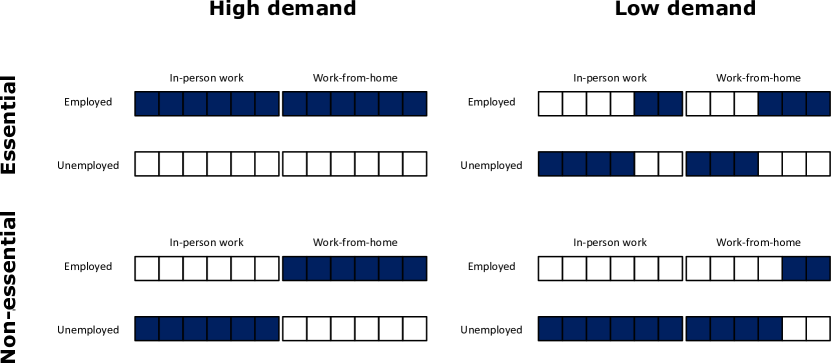

We calibrate the key parameters of the model, including the strength of behavior change, which we name fear of infection, so that the model fits some key epidemic and economic statistics of the first wave in the NY metro area (Supplementary Section S4). We also calibrate the epidemiological parameters to the ancestral SARS-CoV-2 lineages (Supplementary Table S5). We start our simulations on February 12, 2020; impose a number of protective measures on March 16; relax them on May 15; end our simulations on June 30. As protective measures, we close schools, mandate work from home, and shut down all non-essential economic activities, such as entertainment and most of the accommodation-food industry, but also large parts of manufacturing and construction. We use the official NY regulations to estimate the degree to which a given industry is essential (Supplementary Section S3.2.1) and assume that workers who can work from home are not directly affected by these closures [2]. We name this set of assumptions the empirical scenario.

Economic validation.

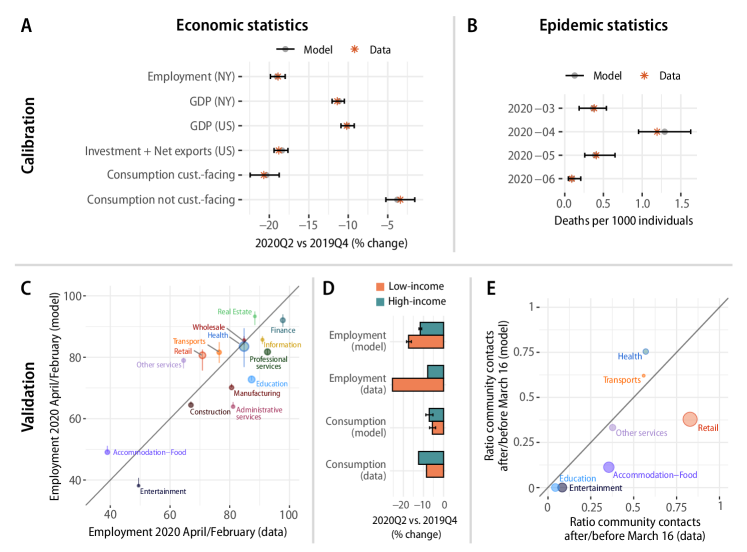

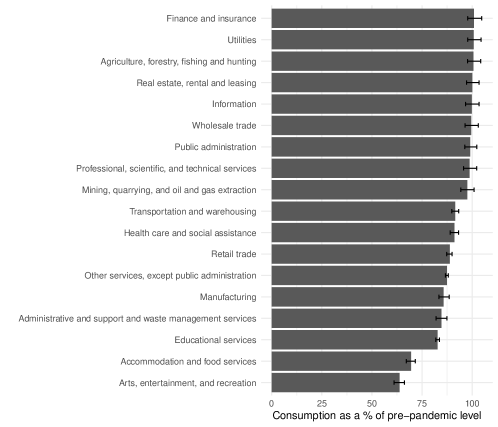

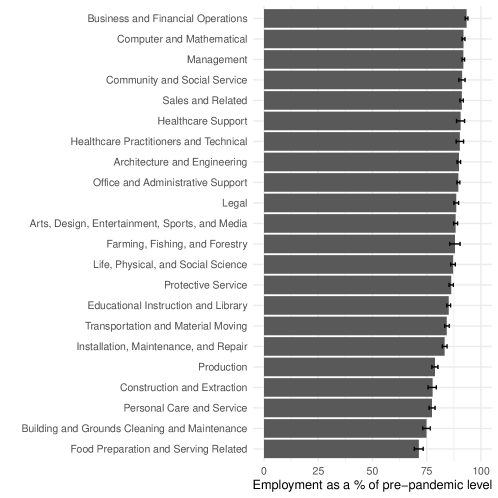

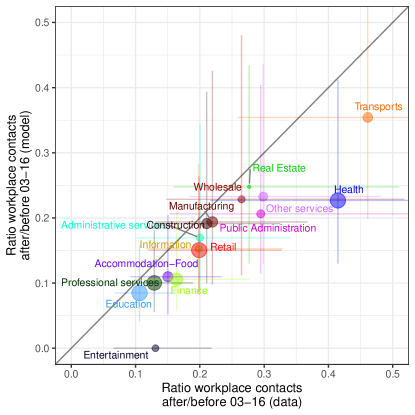

Our model accurately matches the six official economic statistics we calibrated it on (Figure 2A). It correctly reproduces the fact that employment declined more strongly than Gross Domestic Product (GDP) (this is because industries most affected by shutdown orders produce less output per worker). It also correctly reproduces the fact that consumption of goods and services produced by customer-facing industries declined more strongly than consumption of goods and services produced by industries that are not customer-facing, ranging from manufacturing products to utilities and financial services (Supplementary Figure S14). Our model also predicts some empirical properties on which it has not been calibrated (Figure 2C, D). First, thanks to our estimate of pandemic shocks [2] and shock propagation model [17], we are able to predict industry-specific changes in employment induced by the pandemic (Figure 2C), with a Pearson correlation coefficient of 0.82 (p-value: ) between model and data. Second, thanks to our granular and data-driven characterization of employment and consumption patterns (Supplementary Figures S8 and S12), we reproduce a key fact: low-income individuals were more likely to become unemployed but reduced consumption less than high-income individuals [3, 19] (Figure 2D). This happens because low-income individuals are more likely to work in the industries and occupations most affected by closures (Supplementary Figure S15), but they spend a larger share of their income on essential goods and services such as housing and utilities (we do not consider here the effect of the stimulus program, which would further increase the spending of low-income individuals).

Epidemic validation.

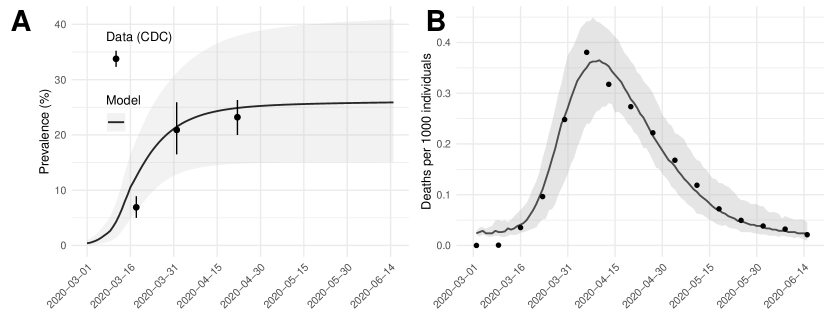

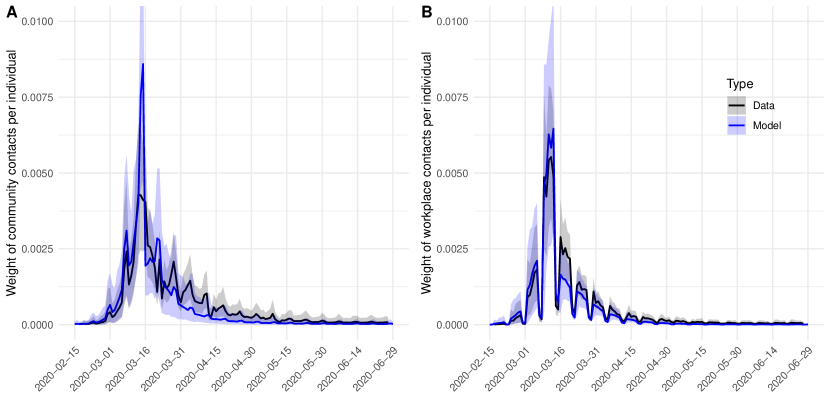

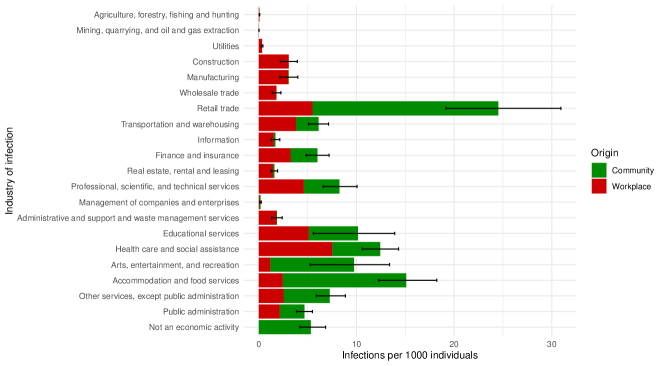

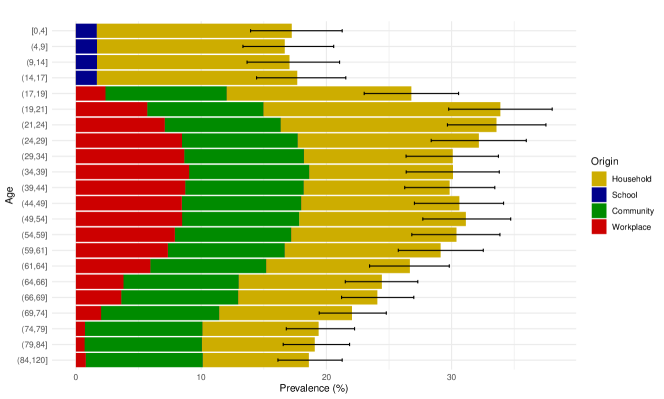

On the epidemic side, our model correctly matches the death count data on which it has been calibrated, correctly replicating the spike in the number of reported deaths in April 2020 and the strong reduction in June (Figure 2D, Supplementary Figure S17). It also correctly predicts the changes in contact patterns that occurred after protective measures were implemented, although it was not calibrated on these data (Figure 2E). Both in the model and in the data, community contacts substantially reduced (Pearson: 0.75, p-value: 0.05), more in mostly non-essential industries such as entertainment and restaurants than in mostly essential industries such as retail and health. We also accurately predict the reduction in workplace contacts across industries (Supplementary Figure S19; Pearson: 0.88, p-value: ), the temporal profile of reduction in contacts (Supplementary Figure S18) and the increase in prevalence over time (Supplementary Figure S17). Finally, the model makes a number of predictions about how many infections happen across each layer and industry over time, as well as which occupation, income and age groups are most affected (Supplementary Figures S20 to S22). While we are not able to find data to quantitatively evaluate these predictions, our literature review provides some support to these findings (Supplementary Section S5.2.1).

Counterfactual scenarios.

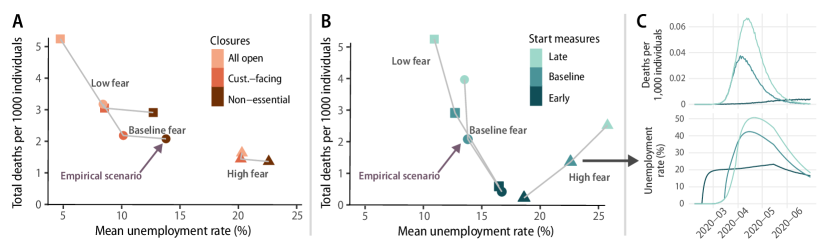

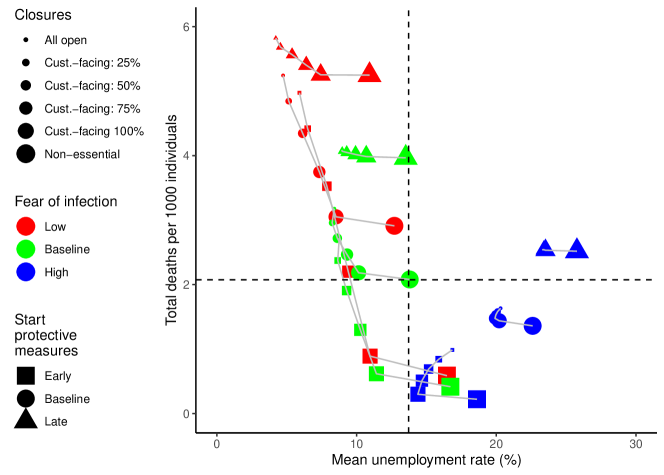

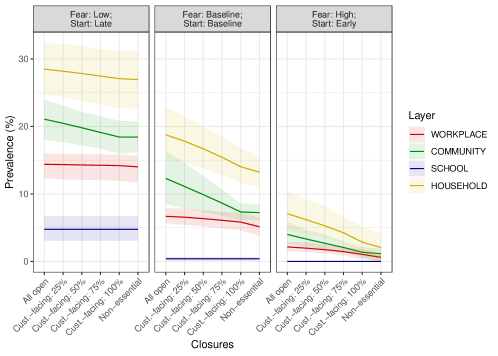

We vary three factors that characterize the behavioral and policy response to the first wave of the COVID-19 pandemic. Throughout we use the term “baseline” to refer to the estimated parameter values that match the empirical data. First, we vary the strength of behavior change, which is represented by the fear of infection parameter. Our baseline calibration gives us a distribution for this parameter (Supplementary Figure S13) that implies that consumption demand of customer-facing industries was reduced by 14% exclusively due to fear of infection at the epidemic peak. We cannot give a causal interpretation to this calibrated value, because it conflates the effect of NPIs with the effect of behavior change — if there were no NPIs, consumption demand would have needed to decline much more for the model to explain observed consumption changes. To address this issue, we examine two counterfactuals, in which we set the fear of infection parameter distribution to 0.1 (“low”) and 10 (“high”) times the baseline. These values imply that, at the epidemic peak, consumption demand was reduced respectively by 1% and 77% exclusively due to fear of infection, representing reasonable lower and upper bounds.

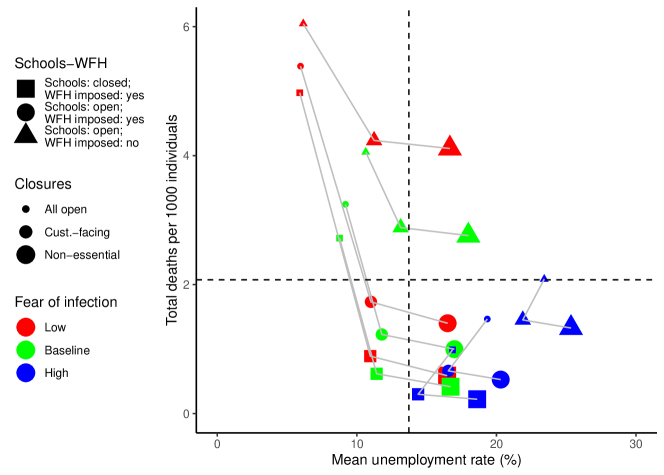

We then vary two factors related to policy. First, we explore the effect of different closures of economic activities. In addition to the closure scenario that we used in our baseline calibration, in which all non-essential industries were closed, we consider two milder closure scenarios: (i) only non-essential customer-facing industries are closed, and (ii) there are no closures, i.e. all economic activities are open. Second, we examine what would have happened if protective measures started four weeks earlier (2020-02-17) or two weeks later (2020-03-30). (In the Supplementary Information we also consider more counterfactuals that include partial closure of customer-facing industries, as well as not imposing work from home and not closing schools, see Supplementary Figures S23 and S24.)

Behavior change vs. NPIs.

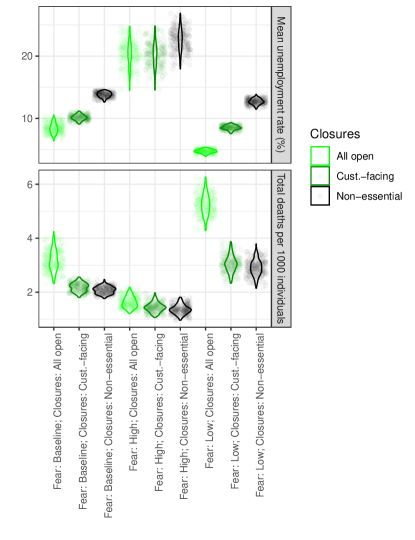

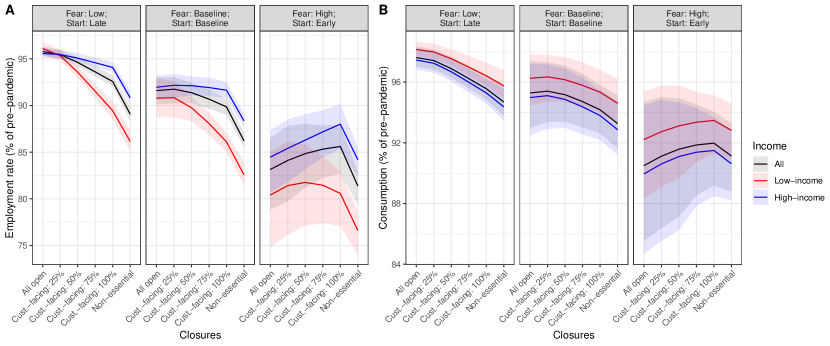

Aggregate economic and epidemic results are shown in Figure 3, while results disaggregated by income, geography and industry are shown in Figure 4 (see also Supplementary Figures S26 to S32). Figure 3A conveys our first key result: stricter closure of economic activities leads to more unemployment and fewer COVID-19 deaths, and the same effect takes place with higher fear of infection. To see this, start from the combination with baseline fear of infection and opening of all economic activities, corresponding to the light-colored circle. Holding fear of infection constant at the baseline value, closure of all non-essential economic activities (as in the baseline scenario) leads to 64% higher unemployment rate, but to a 35% lower number of deaths. At the same time, keeping the level of closures to the empirical baseline but assuming high fear of infection (dark triangle) leads to 40% higher unemployment and 50% lower deaths compared the empirical scenario. The situation across other scenarios is similar. (Variability of total deaths and mean unemployment across simulation runs can be substantial, but the relative effects of different policies are robust; see Supplementary Figure S25.)

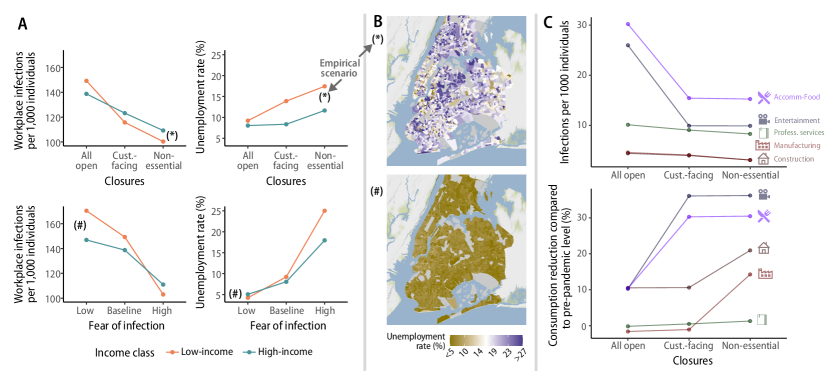

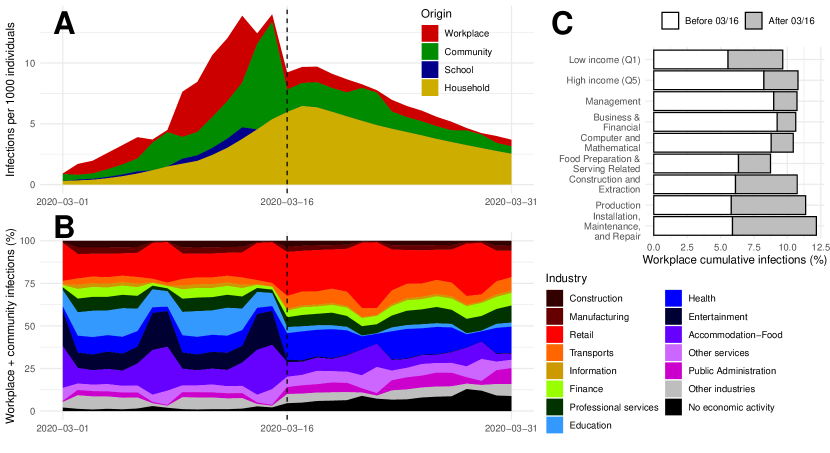

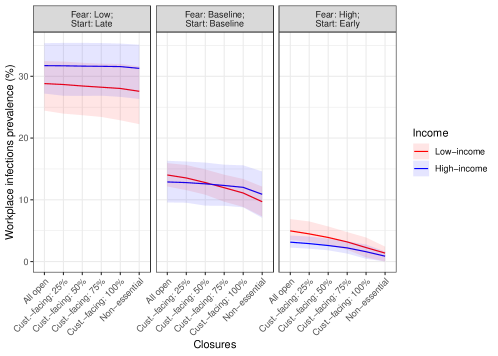

At the distributional level, both higher fear of infection and stricter closures lead to saving lives at the expense of jobs, for both low and high income workers (Figure 4A). However, for low income workers, higher fear of infection or stricter closures have a more dramatic effect, leading to more lives saved and more jobs lost, compared to high-income workers, for whom the effects of these changes are milder. As we will show later, outside the household setting, most infections occur in customer-facing industries, where most low-income workers are concentrated. Thus, mandated closure or spontaneous avoidance of these industries leads to both more unemployment and fewer workplace infections among low-income workers.

This also leads to dramatic spatial disparities. Focusing on unemployment, Figure 4B shows two maps of unemployment in Manhattan in the empirical scenario (asterisk) and in a counterfactual with low fear and no closures (hash). We see that in the counterfactual the unemployment rate is very evenly spatially distributed, while in the empirical scenario low-income areas such as the Queens and the Bronx have a high unemployment rate of more than 20%, compared to high-income areas such as Manhattan, with unemployment rates around 15%.

Overall, our work addresses the controversial debate around the effectiveness of behavior change vs. NPIs in saving both lives and the economy. Our results indicate a qualitative similarity between strong behavior change and strict closure of economic activities: spontaneously avoiding consumption of services provided by customer-facing industries, like mandated closure of these industries, increases unemployment but saves lives, and this is especially true among low-income individuals. Therefore, media campaigns aimed at increasing fear of infection are likely to have qualitatively similar effects to explicit restrictions of economic activities.

Industry-specific closures.

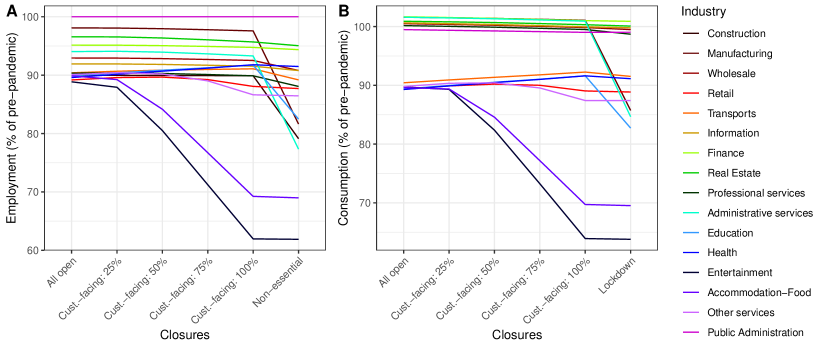

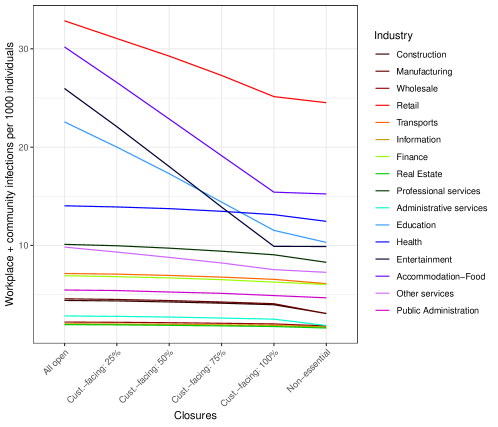

Another question that our model can address is the effectiveness of closing all non-essential economic activities (including large parts of manufacturing and construction) vs. just closing customer-facing industries. Our key finding is that closing all non-essential activities leads to marginally fewer deaths than closing only customer-facing industries, while greatly increasing unemployment. Indeed, a counterfactual with the empirical baseline fear of infection but closure of only customer-facing industries has a 4% higher death rate but a much lower 36% unemployment rate. To explain these results, consider Figure 4C. Among the five industries shown, most infections are concentrated in the customer-facing “Entertainment” and “Accommodation-Food”. When these industries are closed, infections decrease substantially at the cost of a strong decrease in consumption (and employment). Conversely, closing “Manufacturing” greatly reduces consumption of manufacturing goods, but since the share of infections in manufacturing is small, closing manufacturing only marginally decreases infections. The result is similar for “Construction”. “Professional services”, in contrast, are not much affected by different closures because they are either essential or can be largely performed from home.

From a methodological point of view, we could obtain industry-specific results because we linked each consumption venue as recorded in the mobility data to an economic activity (Supplementary Section S3.1.2), quantifying contacts across industries. This way, our granular, data-driven model leads to insights that would have been missed in more aggregate, qualitative models.

Timing of interventions.

The final question that we consider is the effectiveness of starting protective measures earlier (four weeks before) or later (two weeks later) than in the empirical scenario. As we show in Figure 3B, starting protective measures later than the empirical baseline leaves unemployment only about 2% lower while greatly increasing the number of deaths by 50%. Surprisingly, with high fear of infection, starting protective measures late leads to both 46% more deaths and 12% more unemployment than the baseline. The mechanism for these results is suggested in Figure 3C, where we show time series across the three counterfactuals with high fear of infection. We see that an early start of protective measures prevents an epidemic wave, leading to no further increase in unemployment due to fear of infection. Conversely, with a baseline or late start, strong behavior change leads to reduced consumption, and this in turn leads industries to fire their employees, increasing unemployment.

Discussion

Mitigating the health outcomes of the COVID-19 pandemic entailed immense societal and economic costs, spurring heated debates. According to some, restrictions and protective measures were essential to curb the epidemic and there was no tradeoff between economy and health, because there could be no economic recovery without reducing virus circulation to very low levels. According to others, behavioral responses could be more effective than imposed protective measures to control epidemic dynamics; letting individuals spontaneously reduce their risk of exposure when the epidemic situation worsened would have lead to optimal epidemic and economic outcomes.

Our results suggest an equivalence between behavioral response and closure of economic activities: both strong behavioral response and strict closures increase unemployment and reduce infections. This effect is more pronounced among low-income workers than among high-income workers. Our results also show that in most scenarios there is some tradeoff between health and the economy, but this tradeoff depends strongly on which economic activities are closed. Closing industries that are not customer-facing, such as manufacturing and construction, leads to a substantial increase in unemployment while marginally reducing deaths. Finally, when fear of infection is high, starting protective measures late leads to both more deaths and more unemployment, and in the other cases starting late increases deaths a lot while marginally reducing unemployment.

A huge body of scientific work has been studying the effectiveness and equitability of pandemic control policies since the outset of the COVID-19 pandemic. Our paper studies both distributional epidemic and economic outcomes while being firmly grounded in real-world data. This makes it possible to credibly address questions that other models could not consider. For instance, the result showing that high fear of infection affects low-income workers the most is possible through our data-driven mapping between the incomes, occupations and industries of workers.

Our results have the usual limitations pertaining to modeling studies. In this paper we exclusively focus on the first wave of COVID-19 in one specific metropolitan area. It could also be important to consider other aspects of the COVID-19 pandemic that became relevant after the first wave of infections such as masks, test, trace and quarantining, variants, vaccination, and waning of immunity. However, we expect our key results to hold, and we view our model as mostly applicable to the short-term management of emerging/re-emerging infectious diseases. Another important limitation is that the matching between synthetic individuals and mobility traces is probabilistic, as we do not have socio-economic information about specific Cuebiq users. Nonetheless, our privacy-preserving matching algorithm based on census tracts is likely to be accurate given the strong socio-economic disparities in different parts of the New York metro area. From the epidemiological standpoint, we assume the same per-contact risk of infection in different occupational settings. If empirical epidemiological data were collected about the contribution of these settings to SARS-CoV-2 transmission, our estimates could be further refined. Moreover, we did not consider differential risk of severe disease and death for individuals with different socio-economic status. The inclusion of this factor into the model could further exacerbate the highlighted heterogeneity in the health and economic impact of the pandemic and adopted policies on different segments of the population. From the economic standpoint, we consider industries located over the entire metro area, rather than heterogeneous firms at specific geographical locations. Although this is a limitation of our analysis, we believe that this is the right level of aggregation for the questions considered here, but we acknowledge that a more detailed representation of the production sector may be needed to address questions such as the effectiveness of spatially-targeted lockdowns. Finally, the infection transmission and economic models are combined through a “fear” mechanism that was modeled in a simple manner (i.e., as a function of the number of reported deaths on the previous day). For example, individuals may not retrieve information on a daily basis and media may amplify some information (e.g., a spike in the number of deaths) at certain times, thus altering the perception of the population [20]; different segments of the population may have a different risk perception [21]. This highlights the importance of conducting future studies to better characterize the relation between risk perception and human behavior during epidemic outbreaks.

Building on the model introduced in this paper could enrich both the epidemics literature and economic impact studies. From an epidemiological point of view, we introduce industries, occupations and possibility to work from home in a fine-grained transmission model, showing the usefulness of adding an economic dimension to models of epidemic spreading [22]. Studies on the economic impact of disasters often just focus on industries [23, 24], or consider an aggregate representative household [17]. Having a synthetic population that is a highly-detailed representation of the real population, as we do in this paper, would make it possible to address a new set of distributional questions, e.g. the distributional effects of hurricanes.

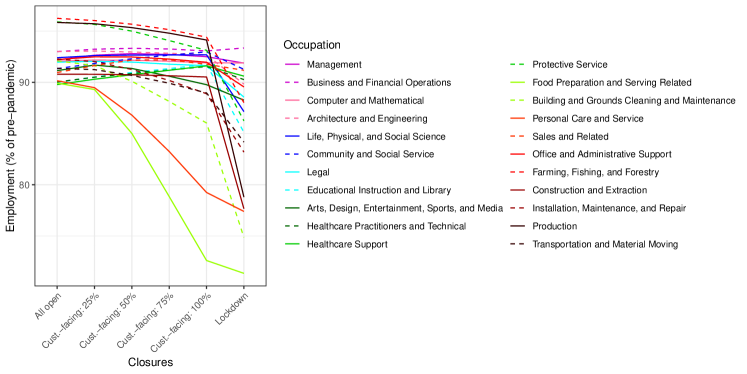

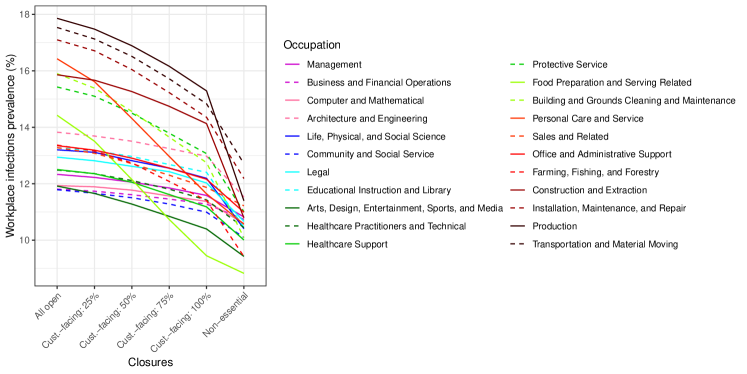

From a policy perspective, the results presented in this paper highlight the importance of targeted policies. Closure of customer-facing industries is highly effective at reducing epidemic spreading–especially when enacted early. With such a policy, income-support schemes could target specific occupational categories, such as food preparation and serving or personal care and services, rather than workers in general, such as those engaged in construction, maintenance, production, extraction and repair occupations. Enhancing surveillance and contact tracing activities in industries where these low-income workers operate could also be particularly beneficial from both the health and economic perspectives. Crucially, these policies are not only needed when customer-facing industries are closed by the government, but also when spontaneous behavior change reduces consumption of goods and services produced by these industries. Our results could be instrumental to design policies aimed at reducing the health and economic impact of pandemics and epidemics as well as reducing inequalities by protecting low-income segments of the population.

Acknowledgements.

MP, MdRC, and AP acknowledge funding from the James S. Mc Donnell Foundation Postdoctoral Fellowship Award. FL and JDF acknowledge funding from Baillie Gifford and the Institute for New Economic Thinking at the Oxford Martin School. AA acknowledges support through the grant RYC2021‐033226‐I funded by MCIN/AEI/10.13039/501100011033 and the European Union “NextGenerationEU/PRTR”. Y.M was partially supported by the Government of Aragon, Spain and “ERDF A way of making Europe” through grant E36‐20R (FENOL), by Ministerio de Ciencia e Innovación, Agencia Española de Investigación (MCIN/AEI/10.13039/501100011033) Grant No. PID2020‐115800GB‐I00,and by Soremartec S.A. and Soremartec Italia, Ferrero Group. MA, MC and AV acknowledge the support of the from the HHS/CDC 6U01IP001137, HHS/CDC 5U01IP0001137. We acknowledge the use of the computational resources of COSNET Lab at Institute BIFI, funded by Banco Santander through grant Santander‐UZ 2020/0274 and by the Government of Aragon (FONDO–COVID19-UZ-164255).

References

- [1] Seth Flaxman et al. “Estimating the effects of non-pharmaceutical interventions on COVID-19 in Europe” In Nature 584.7820 Nature Publishing Group, 2020, pp. 257–261

- [2] R Maria Rio-Chanona et al. “Supply and demand shocks in the COVID-19 pandemic: An industry and occupation perspective” In Oxford Review of Economic Policy 36.1 Oxford University Press UK, 2020, pp. 94–137 DOI: 10.1093/oxrep/graa033

- [3] Raj Chetty et al. “The economic impacts of COVID-19: Evidence from a new public database built from private sector data” In NBER, 2020

- [4] Austan Goolsbee and Chad Syverson “Fear, lockdown, and diversion: Comparing drivers of pandemic economic decline 2020” In Journal of Public Economics 193 Elsevier, 2021, pp. 104311

- [5] Maryam Farboodi, Gregor Jarosch and Robert Shimer “Internal and external effects of social distancing in a pandemic” In Journal of Economic Theory 196 Elsevier, 2021, pp. 105293

- [6] Dirk Krueger, Harald Uhlig and Taojun Xie “Macroeconomic dynamics and reallocation in an epidemic: Evaluating the “swedish solution”” In Economic Policy, 2022

- [7] Thomas Ash et al. “Disease-economy trade-offs under alternative epidemic control strategies” In Nature Communications 13.1 Nature Publishing Group, 2022, pp. 1–14

- [8] Martin S Eichenbaum, Sergio Rebelo and Mathias Trabandt “The macroeconomics of epidemics” In The Review of Financial Studies 34.11 Oxford University Press, 2021, pp. 5149–5187

- [9] Greg Kaplan, Benjamin Moll and Giovanni L Violante “The great lockdown and the big stimulus: Tracing the pandemic possibility frontier for the US” In NBER, 2020

- [10] Fernando Alvarez, David Argente and Franceso Lippi “A simple planning problem for COVID-19 lockdown, testing, and tracing” In American Economic Review: Insights 3.3, 2021, pp. 367–382

- [11] David Baqaee, Emmanuel Farhi, Michael Mina and James H Stock “Policies for a second wave” In Brookings Papers on Economic Activity 2020.2 Brookings Institution Press, 2020, pp. 385–443

- [12] Domenico Delli Gatti and Severin Reissl “Agent-Based Covid economics (ABC): Assessing non-pharmaceutical interventions and macro-stabilization policies” In Industrial and Corporate Change 31.2 Oxford University Press UK, 2022, pp. 410–447

- [13] Alessandro Basurto et al. “Economic and epidemic implications of virus containment policies: insights from agent-based simulations” In Bielefeld Working Papers in Economics and Management 05-2020, 2020

- [14] Patrick Mellacher “COVID-town: an integrated economic-epidemiological agent-based model” In arXiv preprint arXiv:2011.06289, 2020

- [15] Alberto Aleta et al. “Modelling the impact of testing, contact tracing and household quarantine on second waves of COVID-19” In Nature Human Behaviour 4.9 Nature Publishing Group, 2020, pp. 964–971

- [16] Alberto Aleta et al. “Quantifying the importance and location of SARS-CoV-2 transmission events in large metropolitan areas” In Proceedings of the National Academy of Sciences 119.26, 2022, pp. e2112182119

- [17] Anton Pichler et al. “Forecasting the propagation of pandemic shocks with a dynamic input-output model” In Journal of Economic Dynamics and Control Elsevier, 2022, pp. 104527

- [18] Ronald E Miller and Peter D Blair “Input-output analysis: Foundations and extensions” Cambridge University Press, 2009

- [19] Natalie Cox et al. “Initial impacts of the pandemic on consumer behavior: Evidence from linked income, spending, and savings data” In Brookings Papers on Economic Activity 2020.2 Brookings Institution Press, 2020, pp. 35–82

- [20] Piero Poletti, Marco Ajelli and Stefano Merler “The effect of risk perception on the 2009 H1N1 pandemic influenza dynamics” In PloS one 6.2 Public Library of Science San Francisco, USA, 2011, pp. e16460

- [21] Alexander Hodbod, Cars Hommes, Stefanie J Huber and Isabelle Salle “The COVID-19 consumption game-changer: Evidence from a large-scale multi-country survey” In European Economic Review 140 Elsevier, 2021, pp. 103953

- [22] Michele Tizzoni et al. “Addressing the socioeconomic divide in computational modeling for infectious diseases” In Nature Communications 13.1 Nature Publishing Group, 2022, pp. 1–7

- [23] Stéphane Hallegatte “An adaptive regional input-output model and its application to the assessment of the economic cost of Katrina” In Risk Analysis 28.3 Wiley Online Library, 2008, pp. 779–799 DOI: 10.1111/j.1539-6924.2008.01046.x

- [24] Dabo Guan et al. “Global supply-chain effects of COVID-19 control measures” In Nature Human Behaviour Nature Publishing Group, 2020, pp. 1–11 DOI: 10.1038/s41562-020-0896-8

- [25] Timothy W. Russell et al. “Effect of internationally imported cases on internal spread of COVID-19: a mathematical modelling study” In Lancet Public Health 6.1 Elsevier, 2021, pp. e12–e20 DOI: 10.1016/S2468-2667(20)30263-2

- [26] Anthony T Flegg and CD Webber “Regional size, regional specialization and the FLQ formula” In Regional studies 34.6 Taylor & Francis Group, 2000, pp. 563–569

- [27] Nicola Perra, Duygu Balcan, Bruno Gonçalves and Alessandro Vespignani “Towards a characterization of behavior-disease models” In PloS one 6.8 Public Library of Science San Francisco, USA, 2011, pp. e23084

- [28] “Centers for Disease Control and Prevention. Scientific Brief: SARS-CoV-2 and Potential Airborne Transmission (2020);” [Online; accessed 26. Jan. 2022], 2020 URL: http://www.cdc.gov/coronavirus/2019-ncov/more/scientific-brief-sars-cov-2.html

- [29] Kyra H. Grantz et al. “The use of mobile phone data to inform analysis of COVID-19 pandemic epidemiology” In Nat. Commun. 11.4961 Nature Publishing Group, 2020, pp. 1–8 DOI: 10.1038/s41467-020-18190-5

- [30] Forrest W. Crawford et al. “Impact of close interpersonal contact on COVID-19 incidence: Evidence from 1 year of mobile device data” In Sci. Adv. American Association for the Advancement of Science, 2022 URL: https://www.science.org/doi/10.1126/sciadv.abi5499

- [31] Dina Mistry et al. “Inferring high-resolution human mixing patterns for disease modeling” In Nature communications 12.1 Nature Publishing Group, 2021, pp. 1–12

- [32] R Maria Rio-Chanona et al. “Occupational mobility and automation: a data-driven network model” In Journal of the Royal Society Interface 18.174 The Royal Society, 2021, pp. 20200898

- [33] Christopher A Pissarides “Equilibrium in the labor market with search frictions” In American Economic Review 101.4, 2011, pp. 1092–1105 DOI: 10.1257/aer.101.4.1092

- [34] Samuel Bentolila and Giuseppe Bertola “Firing costs and labour demand: how bad is eurosclerosis?” In The Review of Economic Studies 57.3 Wiley-Blackwell, 1990, pp. 381–402 DOI: 10.2307/2298020

- [35] Eli P Fenichel et al. “Adaptive human behavior in epidemiological models” In Proceedings of the National Academy of Sciences 108.15 National Acad Sciences, 2011, pp. 6306–6311

- [36] Martin S Eichenbaum et al. “How do People Respond to Small Probability Events with Large, Negative Consequences?”, 2020

- [37] A Pichler and JD Farmer “Simultaneous supply and demand constraints in input-output networks: The case of Covid-19 in Germany, Italy, and Spain” In Economic Systems Research, 2021 DOI: 10.1080/09535314.2021.1926934

- [38] Jean-Noel Barrot, Basile Grassi and Julien Sauvagnat “Sectoral effects of social distancing” In AEA Papers and Proceedings 111, 2021, pp. 277–81

- [39] Foursquare “Foursquare Places” Accessed 16-02-2021, https://foursquare.com/products/places, 2020

- [40] Hartwig H Hochmair, Levente Juhász and Sreten Cvetojevic “Data quality of points of interest in selected mapping and social media platforms” In LBS 2018: 14th International Conference on Location Based Services, 2018, pp. 293–313 Springer

- [41] “Foursquare Venue Category Hierarchy” Accessed: 09-12-2020, https://developer.foursquare.com/docs/build-with-foursquare/categories/

- [42] U.S. Bureau of Labor Statistics “Quarterly Census of Employment and Wages” Accessed 16-02-2021, https://www.bls.gov/cew/data.htm, 2020

- [43] Maxim Pinkovskiy and Xavier Sala-i-Martin “Parametric estimations of the world distribution of income”, 2009

- [44] Adam Bee and Joshua Mitchell “Do older Americans have more income than we think?” In Proceedings. Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association 110, 2017, pp. 1–85 JSTOR

- [45] Karen J Horowitz and Mark A Planting “Concepts and Methods of the U.S. Input-Output Accounts”, 2009

- [46] Andrea Bonfiglio and Francesco Chelli “Assessing the behaviour of non-survey methods for constructing regional input–output tables through a Monte Carlo simulation” In Economic Systems Research 20.3 Taylor & Francis, 2008, pp. 243–258

- [47] Arne Geschke and Michalis Hadjikakou “Virtual laboratories and MRIO analysis – An introduction” In Economic Systems Research 29.2 Taylor & Francis, 2017, pp. 143–157

- [48] Anthony T Flegg, CD Webber and MV Elliott “On the appropriate use of location quotients in generating regional input–output tables” In Regional studies 29.6 Taylor & Francis Group, 1995, pp. 547–561

- [49] William Passero, Thesia I Garner and Clinton McCully “Understanding the Relationship: CE Survey and PCE” In Improving the measurement of consumer expenditures University of Chicago Press, 2014, pp. 181–203

- [50] “Coronavirus Disease 2019 (COVID-19) planning scenarios” [Online; accessed 15. Dec. 2020] In Centers for Disease Control and Prevention, 2020 URL: https://www.cdc.gov/coronavirus/2019-ncov/hcp/planning-scenarios.html

- [51] Shixiong Hu et al. “Infectivity, susceptibility, and risk factors associated with SARS-CoV-2 transmission under intensive contact tracing in Hunan, China” In medRxiv Cold Spring Harbor Laboratory Press, 2020, pp. 2020.07.23.20160317 URL: https://doi.org/10.1101/2020.07.23.20160317

- [52] PhD Piero Poletti “Association of Age With Likelihood of Developing Symptoms and Critical Disease Among Close Contacts Exposed to” In JAMA Netw. Open 4.3 JAMA Network, 2021, pp. e211085 DOI: 10.1001/jamanetworkopen.2021.1085

- [53] PhD Russell M. “Susceptibility to SARS-CoV-2 Infection Among Children and Adolescents Compared With Adults: A Systematic” In JAMA Pediatr. 175.2 JAMA Network, 2021, pp. 143–156 DOI: 10.1001/jamapediatrics.2020.4573

- [54] Jantien A Backer, Don Klinkenberg and Jacco Wallinga “Incubation period of 2019 novel coronavirus (2019-nCoV) infections among travellers from Wuhan, China, 20–28 January 2020” In Eurosurveillance 25.5 European Centre for Disease PreventionControl, 2020, pp. 2000062

- [55] Robert Verity et al. “Estimates of the severity of coronavirus disease 2019: a model-based analysis” In The Lancet Infectious Diseases 20.6 Elsevier, 2020, pp. 669–677

- [56] Mike Weed and Abby Foad “Rapid Scoping Review of Evidence of Outdoor Transmission of COVID-19” In medRxiv Cold Spring Harbor Laboratory Press, 2020, pp. 2020.09.04.20188417 URL: https://doi.org/10.1101/2020.09.04.20188417

- [57] Jessica T. Davis et al. “Estimating the establishment of local transmission and the cryptic phase of the COVID-19 pandemic in the USA” In medRxiv Cold Spring Harbor Laboratory Press, 2020, pp. 2020.07.06.20140285 URL: https://doi.org/10.1101/2020.07.06.20140285

- [58] István Z. Kiss, Joel C. Miller and Péter L. Simon “Mathematics of Epidemics on Networks” Cham, Switzerland: Springer, 2017 DOI: 10.1007/978-3-319-50806-1

- [59] Ensheng Dong, Hongru Du and Lauren Gardner “An interactive web-based dashboard to track COVID-19 in real time” In Lancet Infect. Dis. 20.5 Elsevier, 2020, pp. 533–534 DOI: 10.1016/S1473-3099(20)30120-1

- [60] “When is New Jersey lifting restrictions? FAQ” [Online; accessed 28. Jan. 2022], 2022 URL: https://covid19.nj.gov/faqs/nj-information/reopening-guidance-and-restrictions/when-is-new-jersey-lifting-restrictions

- [61] Tanay Warerkar “A Timeline of COVID-19’s Impact on NYC’s Restaurants and Bars” [Online; accessed 28. Jan. 2022], 2020 URL: https://ny.eater.com/2020/12/30/22203053/nyc-coronavirus-timeline-restaurants-bars-2020

- [62] Joseph Moscola et al. “Prevalence of SARS-CoV-2 antibodies in health care personnel in the New York City area” In Jama 324.9 American Medical Association, 2020, pp. 893–895

- [63] Usha Venugopal et al. “SARS-CoV-2 seroprevalence among health care workers in a New York City hospital: A cross-sectional analysis during the COVID-19 pandemic” In International Journal of Infectious Diseases 102 Elsevier, 2021, pp. 63–69

- [64] Eli S Rosenberg et al. “Cumulative incidence and diagnosis of SARS-CoV-2 infection in New York” In Annals of epidemiology 48 Elsevier, 2020, pp. 23–29

- [65] Samira Sami et al. “Prevalence of SARS-CoV-2 Antibodies in First Responders and Public Safety Personnel, New York City, New York, USA, May-July 2020.” In Emerging Infectious Diseases 27.3, 2021

- [66] Shuchi Anand et al. “Prevalence of SARS-CoV-2 antibodies in a large nationwide sample of patients on dialysis in the USA: a cross-sectional study” In The Lancet 396.10259 Elsevier, 2020, pp. 1335–1344

- [67] Marina Pollán et al. “Prevalence of SARS-CoV-2 in Spain (ENE-COVID): a nationwide, population-based seroepidemiological study” In The Lancet 396.10250 Elsevier, 2020, pp. 535–544

- [68] Karin Magnusson et al. “Occupational risk of COVID-19 in the first versus second epidemic wave in Norway, 2020” In Eurosurveillance 26.40 European Centre for Disease PreventionControl, 2021, pp. 2001875

Materials and methods

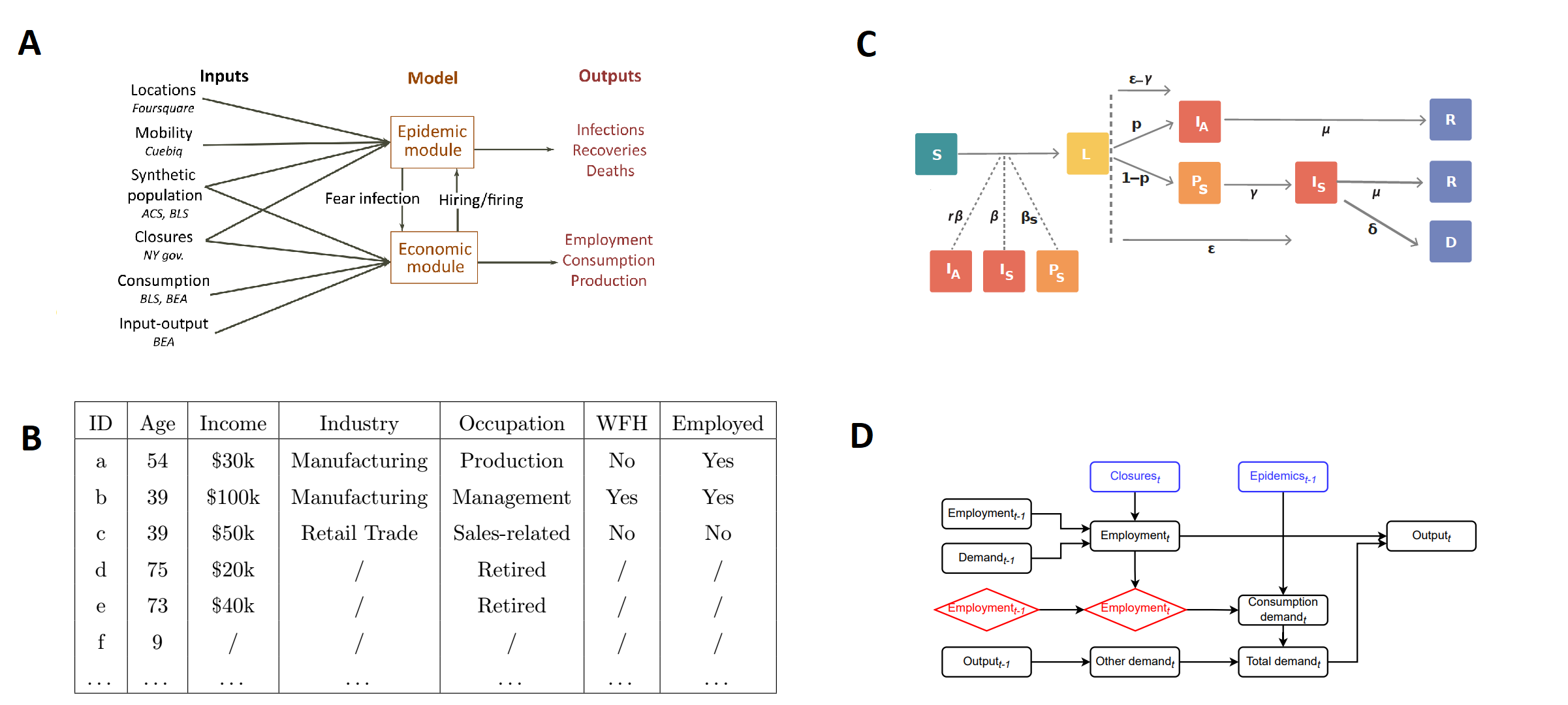

This section provides an overview of the economic and epidemic modules, how they are coupled, which data we use to initialize them, and what outputs they produce (Figure 5A). A longer description that gives all details and justifies all the assumptions can be found in the Supplementary Information.

Geography.

The epidemic-economic model focuses on the New York–Newark–Jersey City, NY–NJ–PA Metropolitan Statistical Area (FIPS code C3562), which we will often abbreviate as NY MSA. The NY MSA includes the highly urbanized area of New York City (i.e., the five boroughs of Manhattan, Bronx, Queens, Brooklyn and Staten Island), but also some rural and industrial areas. The total population, as of 2019, is 19,216,182 individuals, making up about 6% of the U.S. population. Total GDP, as of 2019, is around $1.5 trillion, a bit more than 7% of U.S. GDP. A map of the NY MSA is shown in Supplementary Figure S5. The epidemic module exclusively considers the NY MSA. This is because, while case importation from other parts of the U.S. and from abroad is an important factor in the early phase of a pandemic, it has little impact once the local incidence grows [25]. Our model is initialized in a period when local incidence was already important (see Section S4.1), and so it is a valid approximation to only consider the NY MSA. The economic module models in detail the NY MSA area and also features a simplified model of the Rest of the U.S.: The NY MSA economy is deeply integrated with that of the US, and this integration must be taken into account throughout the pandemic to properly estimate economic impacts.

Agents.

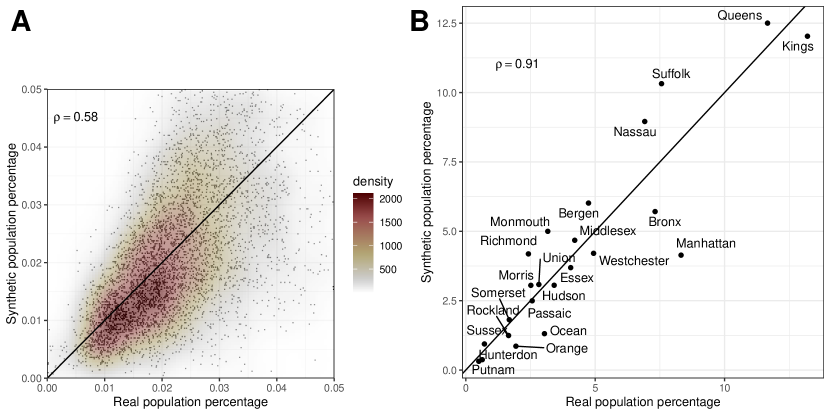

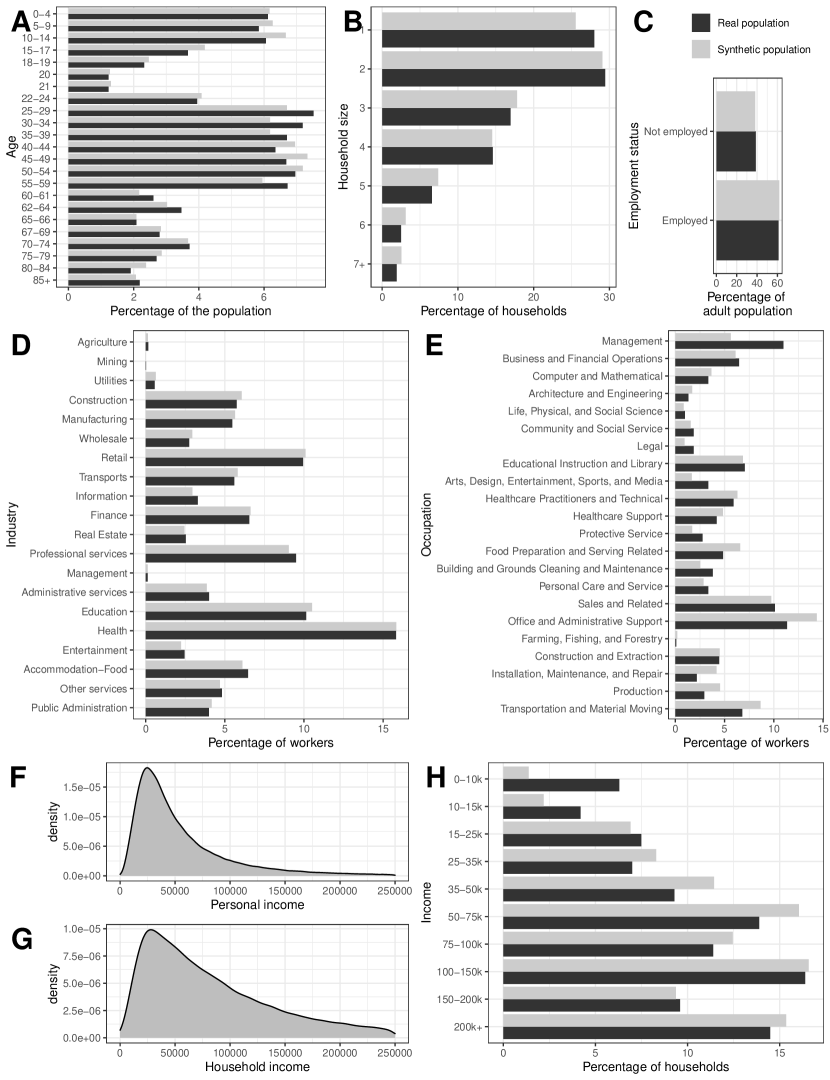

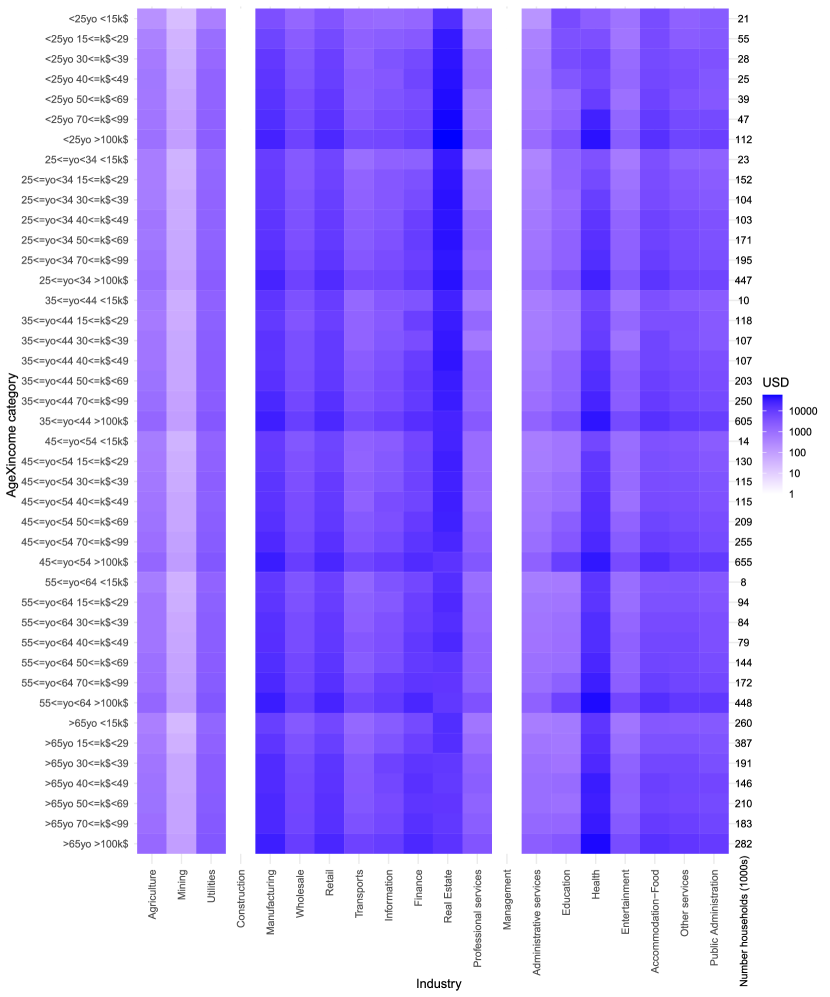

The main agents of the epidemic-economic ABM are the 416,442 individuals of a synthetic population that is representative of the NY MSA (Supplementary Section S3.3.5). The population size is determined by the availability of mobility data (see below). The agents are heterogeneous by several socio-economic characteristics (Figure 5B), including age, income, employment status, occupation, possibility to work from home, and the census tract where they live. Individuals are grouped into 153,547 households, whose composition is consistent with census microdata. We derive socio-economic characteristics of synthetic individuals from tables provided by the American Community Survey (ACS) and the Bureau of Labor Statistics (BLS), trying to get as many joint distributions of variables as we can. For instance, to study distributional outcomes, it is important that synthetic individuals have the correct joint distribution of income, occupation and industry; this is important to replicate the empirical fact that managers working in the finance industry earn high income, while food preparation workers in the restaurants industry earn low income. To achieve this objective, we combine US-level BLS tables reporting incomes by industry-occupation pair with spatially detailed ACS tables giving incomes down to the census tract level. More details on the synthetic population building algorithm and validation tests can be found in Supplementary Section S3.3.

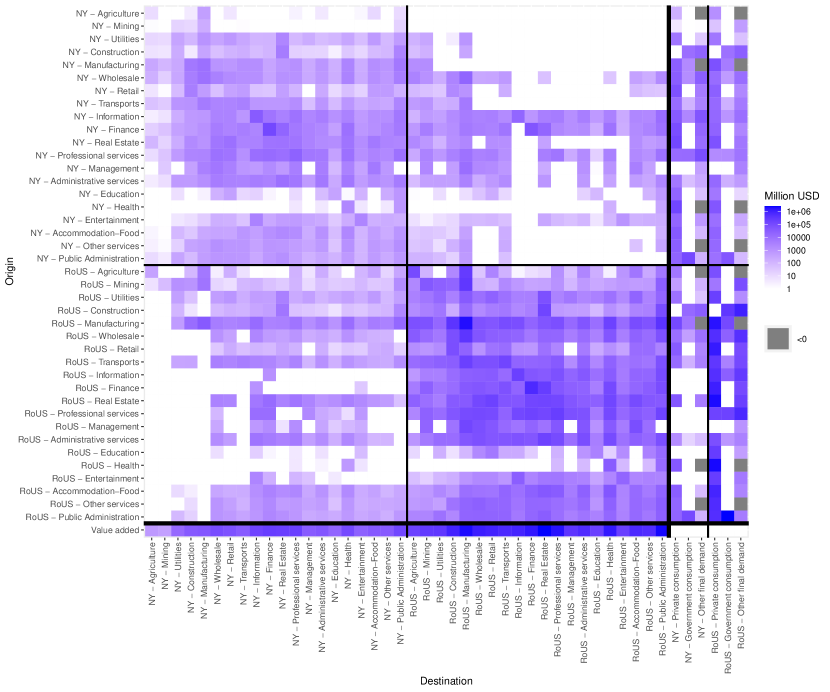

In the economic module we also treat industries as agents, considering a single representative firm per industry. We use the 2-digit NAICS level of aggregation, giving 20 different industries. Industries are mainly dependent on one another through the input-output network of consumption of intermediate goods. Since no official data for the NY MSA exist, we downloaded national data from the Bureau of Economic Analysis (BEA) and then used a regionalization method known as Flegg Location Quotient [26] to obtain an input-output table that distinguishes between the NY MSA and the Rest of the US. The main idea behind this method is that a region that is more specialized in some good or service (such as information or finance in NY) can just rely on itself to source that good or service, but if it is less specialized (as for manufacturing in NY) it is more likely to import that good or service from the other(s) region. More details on our reconstruction of the input-output table can be found in Supplementary Section S3.4.

Epidemic module.

The epidemic module is a standard epidemiological model that runs on top of a contact network extracted from GPS location data. Except for the integration with the economic module, the basic model is the same as the one described in [16]. In this model, individuals interact through a contact network composed of four layers: (i) the community layer captures occasional interactions between individuals, for instance occurring in consumption venues; (ii) the workplace layer captures interactions between workers; (iii) the household layer captures interactions between household members; (iv) the school layer captures interactions between children attending the same school. To initialize contacts in the community and workplace layers to the pre-pandemic situation, we use privacy-preserving location intelligence data provided by Cuebiq, merging information about visits to Points of Interest (POI) with a large database by Foursquare that characterizes POIs. We devised a privacy-preserving algorithm to match Cuebiq users to synthetic individuals, mainly based on the census tract where they live (Supplementary Section S3.3.6). Our approach to reconstructing contacts is probabilistic: because we cannot observe co-location of individuals reliably in the data, we use mobility data to estimate the probability that any pair of individuals is in contact in a given day and in a certain venue (Supplementary Section S1). The contact networks are initialized using data on pre-pandemic mobility, and modified over time due to exogenous interventions, feedback from the economic module and fear of infection (as explained in the sections below).

We use a stochastic, discrete-time infection transmission model coupled to the contact network (Figure 5C) that extends the classical Susceptible, Latent, Infected, Removed (SLIR) model. A susceptible individual () may become infected upon contacting an infectious individual, moving to the latent compartment (). Three states describe individuals who are potentially infectious, each of them with their corresponding transmission rate: pre-symptomatic (), with transmission rate ; infectious symptomatic, with rate ; and infectious asymptomatic (), with rate . Contacts between infectious and susceptible individuals depend on the contact network estimated for each day. Therefore, the probability that a susceptible node gets infected by an infectious node in infectious compartment and place is:

| (1) |

where day and is a weight that modulates the effectiveness of contacts in a given setting in terms of spreading. We assume that all locations within the same layer (schools, workplaces, households and community) have the same weight, except for indoor/outdoor spaces in the community layer (see Supplementary Section S4.1).

Once infected, the individual will enter the incubation compartment () for days, during which she will be infected but not infectious yet. A latent individual will become infectious days before the end of the incubation period, to account for pre-symptomatic transmission. Whether an individual becomes symptomatic or not depends on the specific age-specific symptomatic probability, . Lastly, the individual will be removed (R) from the infectious pool according to an exponential process with rate , where is the average length of the infectious period in days. Note that the removed compartment does not imply recovery, only that the individual is no longer able to infect. After days removed individuals might transition to the death compartment according to the empirical age-dependent Infection Fatality Ratio (IFR). A new death is reported days after the actual event to account for notification delays.

Economic module.

We introduce a dynamic macroeconomic model that is specifically suited to study the economic effects of COVID-19, both at the macro-level of industries and at the micro-level of individuals and households. Figure 5D shows the causal relations between the variables of the economic module. It distinguishes between variables that are exogenous to the economic module (blue rectangles), such as the epidemic trajectory or the shelter-in-place policies that lead to supply shocks, and endogenous variables. These are further distinguished into industry-level endogenous variables (black rectangles) and individual-level endogenous variables (red diamonds). Examples of industry-level variables include employment, output, consumption and total demand. The only individual-level variable that we consider is employment status, although we do consider other agent attributes (such as age) that are fixed within our simulation period. At every time step :

-

1.

Industries decide the size of the workforce they need based on their past employment, past demand, and the current levels of restrictions (we do not consider labor shortages due to illness or quarantine, as they would be difficult to model and preliminary simulations showed that they were a second-order effect). Conditional on the restrictions and on the previous employment status of individuals, industries decide which specific workers they hire or fire uniformly at random.

-

2.

Individuals, grouped into households, decide their consumption demand based both on fixed attributes such as age or income and on variable outcomes such as the situation of the epidemic, and on their employment status (workers who lose their job may cut back on spending). Aggregating over agents produces a total consumption demand for each industry.

-

3.

Total final demand for each industry is obtained by summing up consumption demand, orders of intermediate goods from other industries, and other components of final demand (including government expenditures, investments, imports and exports).

-

4.

Finally, industries produce goods and services. Industries aim to produce as much as demanded, but their production can be limited by labor shortages (for simplicity, in this paper we do not consider intermediate inputs shortages, which were not a first-order effect in the first few months of the pandemic [17]). In the case of shortages, demand is rationed on a pro-rata basis across intermediate and final consumers.

Coupling the epidemic and economic modules.

The epidemic and economic modules are strongly coupled, in the sense that at time both modules take as input the output that the other module generated at . More specifically, the economic module takes the number of deaths reported in the epidemic module, , as an input to compute reduction in consumption demand, as explained in the “Fear of infection” section below. At the same time, the epidemic module takes the employment status of each individual in the synthetic population as an input from the economic module. This information is used in the epidemic module as previously employed individuals who get fired can no longer get infected in the workplace, while previously unemployed individuals who are hired can get infected. From a technical point of view, the epidemic module is written in C, while the economic module is written in Python. To implement coupling between the two models, we use a Python-C API (https://docs.python.org/3/c-api/) that makes it possible to initialize a Python interpreter from within a C run.

Timeline.

A time step in the epidemic-economic model corresponds to one calendar day. Time effectively begins on February 12, 2020. On this date, the epidemic module starts running in calendar time (Supplementary Section S4.1) and producing epidemic outcomes at a daily scale. The economic module starts in a steady state that represents the economic situation at the beginning of 2020. All our simulations finish at the end of June 2020, giving a total of 140 time steps. In the empirical scenario, where we use our model to reproduce what happened during the first wave of COVID-19 in the NY MSA, we impose a number of exogenous interventions (see below) to both the epidemic and economic modules on March 16, 2020. We choose that date for simplicity, as several interventions were imposed at different times by the States of New York and New Jersey from March 9 to March 23, and we see an abrupt change in the social dynamics in our data around that date [16]. We remove the economic interventions on May 15, 2020, again as an approximation to the actual relaxation of protective measures that took place in the NY MSA during spring 2020. Other measures, such as the closure of schools and work from home, are kept in place until the end of the simulation. Similarly, for the modeling of counterfactuals we start protective measures at various times, ranging from February 17 to March 30, but still relax them on May 15, 2020.

Exogenous interventions.

During the COVID-19 pandemic, governments and local authorities imposed a number of non-pharmaceutical interventions with the goal of reducing epidemic spreading. In this paper, we consider three types of interventions:

-

1.

Closure of economic activities. We assume that a certain fraction of industry at time can be exogenously shut down. This implies that a fraction of the in-person workers of industry cannot work at , reducing economic output of industry . In the epidemic module, we assume the same reduction of contacts in industry . In the empirical scenario we reproduce the closures that occurred in the NY MSA in spring 2020 [2], and we name this set of closures “Non-essential”. We consider alternative closing strategies when studying counterfactuals, such as closure of customer-facing industries only.

-

2.

Imposition of work from home. All workers who can work from home must do so. We assume that this has no impact on the economic module –a worker who can work from home is as productive at home as in the workplace– but it reduces contacts and so infections in the workplace in the epidemic module.

-

3.

School closures. All contacts between children going to school are removed, effectively cutting off schools from disease transmission and thus reducing overall infections. We do not consider the impact of this policy on economic outcomes, due to the difficulty of calibrating the productivity loss related to childcare.

Fear of infection.

Further to government interventions, a distinctive hallmark of the COVID-19 pandemic has been behavior change: Due to fear of getting infected, several individuals reduced their in-person consumption and contacts in the community as the epidemic situation worsened. We follow the approach introduced in Ref. [27] and let behaviour change follow the functional form

| (2) |

where is the number of daily reported deaths in the NY MSA on day , and is a sensitivity parameter that we name fear of infection. When , , so there is no behavior change. In contrast, when grows large there is strong behavior change, as . Since , behaviour change increases with fear of infection. The exponential functional form in Eq. (2) corresponds to a non-linearity in behavioral response that gives larger weight to an initial increase in , with saturation afterwards [27], in line with the behavioral response to the first wave. (See Supplementary Section S2.4 for a comparison between our approach and other modeling efforts for fear of infection during the COVID-19 pandemic).

For parsimony, we assume that fear of infection is constant. This implies that the dynamics of the behaviour change are driven by the evolution of the death rate. We also assume that fear of infection is homogeneous across individuals. While it could be expected that old, at-risk individuals intend to reduce their consumption and contacts the most, survey evidence suggests that this is unlikely to be a first-order effect, and in some cases it may be youngest individuals that intend to reduce their consumption the most [21] (of course, whatever one’s intentions, socio-economic groups differ in their ability to actually avoid contacts, e.g. depending on whether individuals can work from home).

While behaviour change in both the epidemic and economic module is based on the functional form in Eq. (2), there are slight differences in how behaviour change affects consumption and workplace and community contacts.

-

•

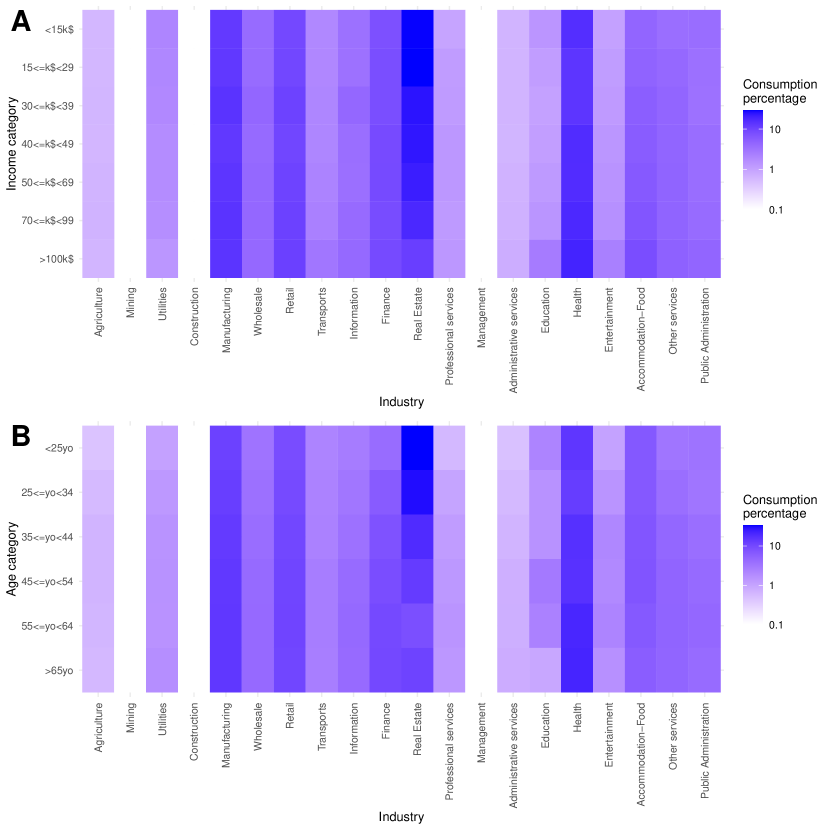

Reduction in consumption (effect in the economic module). During the COVID-19 pandemic, individuals reduced “risky” consumption of customer-facing services such as restaurants, cinemas, hairdressers, etc. However, they did not reduce consumption of financial and real estate services due to fear of infections. Most people kept paying rent, and even increased consumption of some manufacturing goods such as houseware. Therefore, we consider that fear of infection only decreased consumption in consumer facing industries. using the following functional form

(3) where is an indicator that takes value if industry is customer-facing, and if it is not. Section S3.1.3 lists which industries are customer-facing, and explains our classification. The parameter is a fear of infection parameter specific to the economic module, as we detail below.

-

•

Reduction in community contacts (effect in the epidemic module). As individuals reduce consumption of customer-facing services, they also decrease their contacts in the community, which has an effect on the epidemic module. However, the reduction in consumption is not identical to the reduction in community contacts. For instance, individuals may order take away meals from restaurants, thus reducing contacts but not consumption. We assume that reductions in consumption and community contacts are proportional, letting fear of infection in the epidemic module be given by

(4) with as a parameter giving the proportion between the two fear of infection parameters (see Section S4 for how we calibrate these parameters). The reduction in community contacts is then given by

(5) -

•

Reduction in workplace contacts (effect in the epidemic module). If work from home is not imposed by the government or local authority, individuals may nevertheless decide to work from home if they can. We assume that this is uniform across industries, so that the reduction in workplace contacts among individuals who can work from home is given by

(6) We assume no reduction in productivity from working from home –a worker who can work from home is as productive at home as in the workplace–, so this has no effect on the economic module.

Calibration and stochasticity.

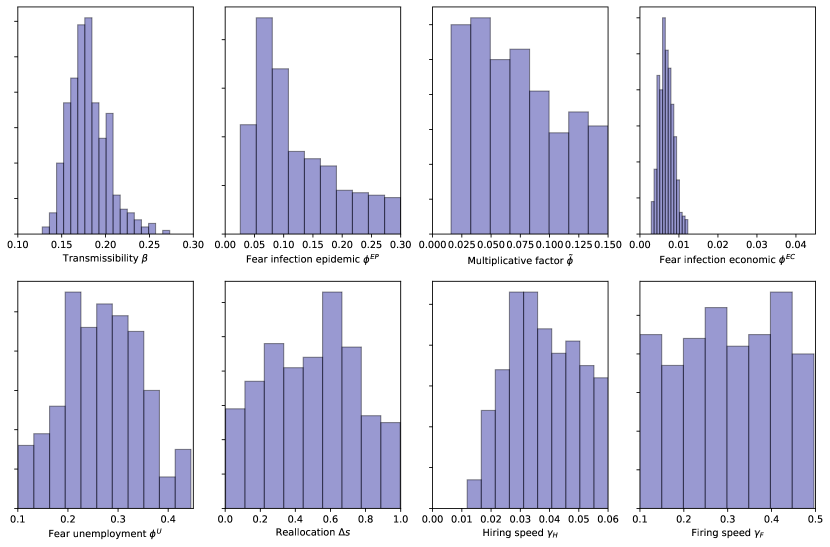

For both the epidemic and economic results, uncertainty comes from: (i) stochasticity in the simulation runs, namely inherent stochasticity of transmission in the SLIR model and inherent stochasticity in the hiring/firing process of the economic module; (ii) uncertainty over parameter values, as obtained from the Approximate Bayesian Computation (ABC) calibration algorithm that we use to calibrate the seven parameters that we cannot pin down independently (see Section S4). (This means that, in line with a Bayesian approach, we run simulations sampling from all parameter values accepted by ABC.)

Supplementary Information

-

•

Section S1 gives details on the epidemic module, which is a modified SLIR model that is simulated at the level of individuals who are heterogeneous in their contacts. Given that we have a lot of information to build the contact network on which infections take place, but not detailed enough information to build it exclusively from the data, we explain our probabilistic approach to building a multilayer contact network using all information available as well as reasonable assumptions.

-

•

Section S2 explains all details of the economic module, in particular its employment and consumption submodules. It clarifies the mechanisms that connect the macro level of industries to the micro level of individuals, as well as the reverse mechanism.

-

•

Section S3 explains how we initialize variables and agent-specific parameters. In this paper, we use the word initialization to refer to the setting of initial conditions of model quantities that change over time (variables), but also to setting individual- and industry-specific parameters.

-

•

Section S4 shows how we calibrate model-wide epidemic and economic parameters. We select some parameters directly from data or from other studies, while the remaining seven parameters are calibrated using Approximate Bayesian Computation (ABC).

-

•

Section S5 presents additional results on the empirical scenario that we cannot report in the main paper due to space constraints. These include more detailed results on infections, employment and consumption across income levels, occupations and industries.

-

•

Section S6 presents additional results on counterfactuals. These include partial closures of customer-facing industries, no school closures or imposition of work from home, and more detailed results across scenarios on infections, employment and consumption across income levels, occupations and industries.

Table S1 shows the notation that we use throughout this supplementary material. This list is not exhaustive, as it misses some minor parameters or variables of both the epidemic and economic module, but it includes all the symbols that are used repeatedly.

| Symbol | Name |

|---|---|

| Individual | |

| Household | |

| Industry | |

| Occupation | |

| Group of agents with same consumption preference | |

| Place | |

| Time (day) | |

| Links between agents and in the Community, Workplace, Household and School layers | |

| Daily reported deaths | |

| Reduction in consumption demand of customer-facing products | |

| Reduction in community and workplace contacts due to fear of infection | |

| Fraction of in-person workers of industry that cannot work due to restrictions | |

| Shocks to government demand and other (investment and export) final demand | |

| Indicator of whether industry is customer-facing | |

| Number of in-person and from-home workers employed in industry | |

| Output of industry | |

| Orders and realized intermediate consumption by industry of goods and services produced by | |

| Technical coefficients | |

| , , | Consumption, government, and other final demand for products of industry |

| Realized private consumption, government consumption and other final demand for products of industry | |

| Reproduction number | |

| , IFR,, | Other epidemic parameters |

| Fear of infection in the epidemic module | |

| Fear of infection in the economic module | |

| Factor of proportionality between and | |

| Fear of unemployment | |

| Reallocation pararameter | |

| Speed of hiring and firing |

Supplementary Information S1 Epidemic module

We use a standard stochastic, discrete-time infection model on top of a contact network extracted from GPS location data. The infection model is already described in Materials and Methods, so in this section we discuss our theoretical framework to define contact networks between individuals using available data and plausible assumptions (see also Ref. [16]).

The primary route for transmission of SARS-CoV-2 is close contacts between individuals [28]. Individual-level contacts are very hard to measure at large scale and investigators have proposed the use of aggregated mobility metrics to infer the amount of contacts in the population [29]. This, however, is not always a valid approach since it is possible for a person to travel to many distinct points of interest without actually coming into close contact with others [30]. In contrast, anonymized mobile device geolocation data has been shown to be a good proxy to estimate the real contact rates in the population [30].

In this work, we model interaction between individuals as a network in which nodes represent the agents and there is a link between them on a given day if they might have been in close contact. Furthermore, this contact can be associated to the specific place (henceforth, point of interest or POI, see Section S3.1.2) in which it took place. We distinguish four different contexts - or layers - for these contacts: households, schools, workplaces and community, which captures all connections that do not belong to the others. This last context is the one that most benefits from the use of geolocation data, since it is the one most subject to random and occasional encounters.

Ideally, one should be able to extract the links between individuals in the community directly from geolocation data. However, there are intrinsic limitations in the technology that limit this approach: information is collected asynchronously, irregularly over time, dependent on the apps being used in the device… [30]. As such, even though the mobility dataset we use is large, co-location events cannot be precisely quantified. Instead, we rely on a probabilistic approach to measure co-presence and build the contact network [30, 15, 16]. For more details on the characteristics of the data see Section S3.1.

In order to explain better our approach let us consider the homogeneous mixing approach in a contact network perspective. We assume to have individuals who are homogeneously mixed. This implies that each individual is potentially in contact with anybody else. Thus, we have a connection , among each pair of nodes. This implies that the rate of contacts for the individual is , where is an appropriate factor ensuring that the number of average effective contacts per individual unit time in the system is equal to . This implies that

| (7) |

yielding

| (8) |

This finally provides the usual expression for the rate of contact , that is multiplied by the transmissibility per contact to give the rate (or probability) of infection per contact. This finally leads to the force of infection of a susceptible as

where is the transmissibility used in homogeneous model and the last approximations are valid for very large .

In order to go beyond the homogeneous assumption, from our data we can consider that individuals who are never visiting the same places are never in contact. This is additional information of which we are certain. So for each individual we can list each of the places that they visit and assume that we can have a link between two individuals if they have the same place in their list , where if the place is on the list of visited places of individual and zero otherwise. This step improves on the homogeneous assumption as it rules out possible contacts among individuals that can never meet. Further we can consider that the potential contacts among individuals is larger for individuals that can meet in more than one place. We can then define , thus considering that some individuals have more potential contacts. It is worth remarking that we are still considering that each potential contact has the same weight as in the homogeneous assumption. In order to define properly the contact rate/probability per unit time we need to use Eq. (7) thus defining

| (9) |

where we defined as the average weighted contacts among individuals. This yields the effective rate of contact among individuals and as

| (10) |

In order to improve further on this approach we can consider that places are not visited in a deterministic way. This implies that each individual has a probability to visit a specific place that is , where is the number of places visited by the individual in a given period. We can therefore define

| (11) |

This approach still considers potential contacts only among individuals however with a weight that depends on the variability of places of each individual. As before the rate/probability of contact would be:

| (12) |

So far we did not consider at all the time spent in each location. We can therefore improve on the probability to be in a place by weighting the number of places by the time spent on average in each place. This finally leads to the expression:

| (13) |

where is the time spent by individual at location and is equal to the sum of all time spent in places in the community by individual . In this case the rate of interaction will be:

| (14) |

This is the expression we use in our work. It is important to stress that this expression is improving on the homogeneous assumption as it considers that effective contacts can occur only in places visited by both individuals, and considers that each contact is weighted by the probability for each individual to be in that place. The approach however does not account for concurrency of visits. In this respect it is still adopting an homogeneous perspective in that all places visited at any time corresponds in a potential contact.

The next steps to improve on this approach would be indeed to consider concurrency of visits. It is thus tempting to consider that each contact is weighted by , where T would be the specific amount of time of the day. One could assume the 8 hours of the working time or the 24 hours cycle of the day. This is a tempting solution but introduces a number of issues. For instance the time that should be considered in the normalization depends on the places. As an example, restaurants have specific bracket of times during the day, and concurrency should be evaluated on specific hours of the day and specific days (e.g. the weekend). The same happens for places like movie theatres, museums etc. Furthermore, during the lockdown the concurrency normalization should all be re-evaluated to be consistent in their definition as the number of hours in the community of the population drastically changed. In other words, we are not sure if the simple normalization by a fixed number of hours although trying to capture the concurrency of contacts is actually introducing unwanted and uncontrolled biases. For this reason we decided to work with the approach of Eq. (14), for which all the assumptions can be clearly stated and provides an obvious improvement with respect to the fully homogeneous assumption.

Using our probabilistic approach to detect contacts, we build our contact network in each of the layers:

-

•

Community weighted contact network. In the community layer contacts are built by estimating co-location of two individuals in the same POI. Specifically, the weight, , of a link between individuals and within the community layer at day is computed according to the expression:

(15) where is the total time that individual was observed at place in day and is the total time that individual has been observed at any place set within the community layer that day .

For robustness and computational reasons, we have included only links for which , removing 2.88% of the original links. For other values of the threshold like and we would remove 1.19% and 6.19% of the links respectively. Note however that since those links have very small weights, our results for the epidemic spreading do not depend significantly of the threshold chosen provided that it is small.

-

•

Workplace weighted contact network. For privacy reasons, our data is obfuscated around home and workplaces to the level of Census Block Groups (CBGs). To get a proxy of contacts at the workplace, we assume that all workers in the same Census Block Groups have a probability to interact. To account for the potential number of working places in that area, we weight that probability by the number of POIs at the same census block group. Therefore, the contact weight, , of a link between individuals and in the workplace layer at day is given by:

(16) where is the set of POIs in the census block group , is the number of POIs in , is the binary variable of observing or not an individual at her workplace within census block group at day . As before, we have included only links for which .

-

•

Household weighted contact network. We first identify individuals’ approximate home place as their most likely visited census block group at night. Then we assign a synthetic representative household and demographic traits as documented in Ref. [31]. To assign weights, we assume that the probability of interaction within a household is proportional to the number of people living in the same household (well-mixing). Therefore, the weight, , of a link between individuals and within the same household is given by:

(17) where is the number of household members. This fraction is assumed to be the same for all individuals in the population. We assume this layer is static throughout our period.

-

•

School weighted contact network. To calculate the weights of the links at the school layer, we mix together all children that live in the same census tract. Interactions are considered well-mixed, hence, the probability of interaction at a school is proportional to the number of children at the same school. Therefore, the weight, , of a link between children and within the same school is given by:

(18) where is the number of school members. This layer is removed on March 16 to account for the imposed school closure.

Supplementary Information S2 Economic module

We introduce a dynamic macroeconomic model that is specifically suited to study the economic effects of COVID-19, both at the macro-level of industries and at the micro-level of individuals and households. The model is particularly focused on employment and consumption, but also considers the input-output network of intermediates that industries use to produce final goods and services. The model is built so that its key variables can be mapped to quantities defined in national and regional accounts.

As a general modeling principle, we keep our model as simple as possible, with a minimal number of free parameters. We focus instead on a very detailed initialization of the state variables of the model, both at the micro- and macro-level, using multiple datasets coming from various sources (see Section S3).

S2.1 Geography

Our model is set up for detailed modeling of a relatively small “local region” and coarse modeling of a “large area” that is strongly interconnected with the local region (but does not include it) and sufficiently isolated from the Rest of the World. In the following, we also call the inhabitants of the region the “locals” and the inhabitants of the large area the “outsiders”. As described in Materials and Methods, in our application the local region modelled in detail is the New York-Newark-Jersey City, NY-NJ-PA, Metro Area, and the large area being modeled at a more coarse level is the Rest of the United States. Nonetheless, our model is general and, in principle, the region could represent a country and the large area could be the Rest of the World.

S2.2 Agents

S2.2.1 Individuals

Individuals (or persons) play a role in the economic module as workers and consumers. We model individuals in the large area coarsely and in the local area more granularly. In the large area, individuals can be thought of as a “continuum”, so that the only state variable is the fraction of employed and unemployed individuals for each industry. All individuals in the large area have the same consumption patterns.

In contrast, in the local region, individuals are discrete units, composing a synthetic population that is representative of the real population. (Typically, the synthetic population is a downscaled version of the real population, but it does not need to be.) Individuals are denoted by or and grouped in households . As described in more details in Section S3.3, individuals are characterized by the following attributes: id , household id , age, income, employment status, industry where they work, occupation, possibility to work from home. Individuals are located spatially, as we also consider the smaller geographical unit where they live. In our application to New York, this is the census tract, but one could consider finer or coarser geographical units.

Economically active individuals (i.e. those who receive an income) play a direct role in the economic module by working and taking consumption decisions for their household. Economically inactive individuals (e.g. individuals younger than 18 years old) may play an indirect role as they participate in the epidemic module which feeds back into the economic module, but do not work nor take household consumption decisions. Note that we do consider retirees, who are out of the labor force but receive an income, and thus participate in the consumption market.

S2.2.2 Industries

We consider a representative firm for each industry i.e. we do not differentiate between different firms/establishments within the same industry. We denote the representative firm of each industry with subindexes or . Industries participate in the labor and consumption markets. Additionally, industries are connected by input-output linkages quantifying the flows of intermediates that they use to produce final goods and services.

Industries are modeled at the same level of detail in the region than in the large area. We consider flows of intermediate and final goods and services both within and across the region and the large area. In our application, this means that we consider flows of intermediate goods between pairs of industries that are both located in New York, between an industry in New York and an industry in the Rest of the US, etc. We also consider final demand by New Yorkers for goods and services produced locally, but also final demand of inhabitants from the Rest of the US for goods/services produced in New York, final demand by New Yorkers for goods/services produced in the Rest of US, etc.

Differently from individuals, industries are not assigned a specific geographical location other than belonging to the region or to the large area. In our application, this means that from an economic point of view the location of workers within the New York metro area does not matter. However, as we detail in Section S1, from an epidemiological point of view we do consider the specific location where individuals work.

S2.3 Hiring and firing