Optimal investment and reinsurance policies for the Cramér-Lundberg risk model under monotone mean-variance preference

Abstract

In this paper, an optimization problem for the monotone mean-variance(MMV) criterion is considered in the perspective of the insurance company. The MMV criterion is an amended version of the classical mean-variance(MV) criterion which guarantees the monotonicity of the utility function. With this criterion we study the optimal investment and reinsurance problem which is formulated as a zero-sum game between the insurance company and an imaginary player. We apply the dynamic programming principle to obtain the corresponding Hamilton-Jacobi-Bellman-Isaacs(HJBI) equation. As the main conclusion of this paper, by solving the HJBI equation explicitly, the closed forms of the optimal strategy and the value function are obtained. Moreover, the MMV efficient frontier is also provided. At the end of the paper, a numerical example is presented.

JEL classification: C61 G11 G22

Keywords. Optimal reinsurance Monotone mean-variance preference Zero-sum game Hamilton-Jacobi-Bellman-Isaacs equation Monotone efficient frontier

1 Introduction

In the past two decades, the mean-variance(MV) optimization problem has attracted considerable attention in the financial mathematics community, especially for the terminal wealth of an investor. The MV optimization problem, first proposed by Markowitz (1952), is a multi-objective optimization problem:

| (1) |

where and are the variance and mean of the uncertain prospect controlled by the strategy under the probability measure , and is the set of admissible strategy. The goal of this problem is to find the maxima in the sense of Pareto optimality which together form the so-called efficient frontier in Markowitz (1952). The strategies for reaching these maxima are the efficient strategies. Basically, the Pareto optimality means there is no other strategy which can make either or better off without the other one being worse off.

In 2000, Li and Ng (2000) extended the MV criterion to the multi-period setting using the idea of embedding the problem in a tractable auxiliary problem. From then on, the MV criterion became a popular objective in the field of multi-period optimization. For example, Zhou and Li (2000) studied the MV optimization problem in the continuous-time market. They introduced the stochastic linear-quadratic approach and obtained the efficient strategies as well as the efficient frontier by solving a stochastic Riccati equation.

An application of the MV problem to the decision making of an insurance company is introduced by Bäuerle (2005). In this paper, the following criterion was used

This criterion aims to make the insurance company’s reserve at the terminal time remain close to a certain preassigned benchmark . If we let equal , the criterion with the benchmark becomes:

| (2) |

Since the MV problem using criterion (2) is proved to be equivalent to the multi-objective one (1), Li et al. (2002) made use of criterion (2) to solve the continuous time MV problem. Criterion (2) simplifies the multi-objective MV problem to a state constrained optimization problem which allows us to apply the dynamic programming approach (studying the Hamilton-Jacobi-Bellman(HJB) equation). In particular, in the paper Li et al. (2002), the short-selling of stocks is prohibited which means the problem has no classical solution. Fortunately, they coped with this difficulty by finding the viscosity solution. If we let vary in an appropriate interval, the set of points is exactly the efficient frontier. In addition, Bai and Guo (2008) investigated the no-shorting constrained MV problem where there are multiple risky assets. Also many other interesting aspects of MV problem are studied by some recent papers. Bielecki et al. (2005) considered the MV problem with bankruptcy prohibition, i.e., the state cannot be negative. To solve the problem, they decomposed it into two sub-problems and solved them separately. Chen and Yam (2013) studied the problem via the maximum principle approach for a regime-switching market. Also by maximum principle approach, Shen and Zeng (2014) considered the problem when there is delayed capital inflow/outflow for the wealth process. Shen et al. (2014) and Sun and Guo (2018) studied the MV problem where the price processes of the stocks follow the constant elasticity of variance (CEV) model and the Heston stochastic volatility model, respectively. They obtained the explicit solutions by the Backwards Stochastic Differential Equation (BSDE) approach. There is also much literature considering the time-inconsistency of the MV problem, see Landriault et al. (2018), Ni et al. (2019), Chen et al. (2021). Some other researchers incorporate the mean field type control theory to discuss the MV problem, see Mei and Zhu (2020) and Bensoussan et al. (2022).

By the method of Lagrange multipliers, criterion (2) can be formulated as an unconstrained utility optimization problem given by

where and is a utility function of the uncertain prospect .

Here we introduce a strategically equivalent utility function called the penalty MV utility function (or MV preference in economics literature) as follows

| (3) |

where is an index which measures the investor’s aversion to risk. Let then the utility becomes

| (4) |

which means that the investor wants to maximize the expected return regardless of risk. For large , the original problem is approximately equivalent to maximizing

| (5) |

which means the investor is absolutely risk averse and it wants to minimize the risk regardless of the expected return.

Although the MV preference (3) is successful in the field of finance and economics due to the intuitive meaning and tractability, it has an inevitable and crucial weakness in that it may fail to be monotone. This is irrational in the economic context, since it may happen that but . In practice, if an investor uses the MV preference as its objective to optimize the wealth, it may happen that the optimal strategy doesn’t actually optimize the absolute amount of the underlying wealth. To overcome this shortcoming, Maccheroni et al. (2009) introduced an amended version of the MV preference called the monotone mean-variance(MMV) preference (utility function) which is exactly monotonic with respect to the uncertain prospect . Specifically, the MMV preference is given by

| (6) |

where ranges over all the absolutely continuous probability measures whose densities are square-integrable with respect to , and is the relative Gini concentration index. The parameter in (6) is the same as that in (3). For a similar objective function, readers are referred to Hansen et al. (2006) and Elliott and Siu (2009).

It is proved that the MMV preference in (6) is the minimal monotone modification of the MV preference . Moreover, agrees with in the area where is monotonic. It follows from Lemma 2.1 of Maccheroni et al. (2009) that the domain of monotonicity of consists of that is dominated by . This is too constricted when is not small enough, and most of the meaningful variables in finance and economics fail to meet this condition. If we allow to vary in so as to get the efficient frontier, the domain of monotonicity becomes , which is especially constricted. In this paper, the uncertain prospect is the terminal wealth of the insurance company who invests in the capital market and purchases reinsurance. In this case, may not satisfy this condition under some strategies. For this reason, we use the MMV preference instead of the classical one as the criterion to optimize the insurance company’s terminal wealth. We obtain in this paper the optimal strategies for different parameters . Denote as the efficient frontier of the optimal MMV problem. A very interesting result is that the efficient frontier of MMV optimization problem is the same as that of the classical MV problem.

In the literature, there are few articles about the optimization problem of the MMV criterion. Trybula and Zawisza (2014) first investigate it in the framework of continuous time financial market and it is assumed that the interest rate is a random process driven by a Brownian motion. In Trybuła and Zawisza (2019), a continuous time portfolio choice problem is studied where the authors allow the coefficients of the stock prices process to be stochastic. They assume that is an equivalent probability measure with respect to . The optimal portfolio and the value function are obtained when the coefficients are specified. For a large class of portfolio choice problem, Strub and Li (2020) further prove that, when the risk assets are continuous semimartingale, the optimal portfolio and the value function of the classical MV preference and the MMV preference coincide.

We list the contributions of this paper as follows:

-

•

Although there is much literature in recent years for the MMV optimization problem, there is no paper studying the present problem involving jump processes. In this paper, the stock price process follows the Black-Scholes model, and the insurance surplus follows the Cramér-Lundberg model where the aggregate claims process is a jump process.

-

•

In contrast to Trybula and Zawisza (2014) and Trybuła and Zawisza (2019), where is assumed to be chosen in the set of equivalent probability measure of , in this paper, we allow to be absolutely continuous with respect to , which is more consistent with the original definition of the MMV preference in Maccheroni et al. (2009). It is difficult to consider the absolutely continuous probabilities. Since the Radon-Nikodym derivative is not necessarily positive, letting be the natural filtration, we can not simply write as an exponential martingale( which is always positive). However, we managed to resolve this problem for the continuous state process case in our former work Li and Guo (2021). And in the present jump-involving framework, the problem can be more difficult to tackle with. In the later context, we can show that the minimum point is reached at an equivalent probability measure .

-

•

It is the first time that the MMV preference is incorporated into the optimal investment and reinsurance problem for the Cramér-Lundberg risk model. The objective is to find the optimal portfolio and optimal retention level to maximize the MMV criterion of the terminal wealth of the insurance company. The explicit solutions are obtained.

The paper is organized as follows. In Section 2, we present the definition of the MMV preference proposed by Maccheroni et al. (2009) and then introduce the insurance risk model in the financial market. In Section 3, we give an auxiliary two-player zero-sum stochastic differential game(SDG). This SDG can be solved by applying the dynamic programming principle and solving the corresponding Hamilton-Jacobi-Bellman-Isaacs(HJBI) equation. The original problem is then resolved consequently. Section 4 provides the value function and the optimal strategy explicitly. The efficient frontier for MMV is presented in Section 5. In Section 6, an example is presented to show the monotonicity of the MMV criterion. Besides, a simulation of the optimal strategies in the financial and insurance market is conducted.

2 Model setup

2.1 Monotone mean-variance criterion

The following MMV preference introduced by Maccheroni et al. (2009) is used as the objective function,

| (7) |

where

and is defined as

which is called the relative Gini concentration index (or -distance) and enjoys properties similar to those of the relative entropy (see Liese and Vajda (2007)). Here is an index measuring the risk aversion of the insurance company.

Problem.

(MMVθ)

where

| (8) |

is the control process of and is the admissible set.

This is a max-min optimization problem, and is naturally relative to a zero-sum game as follows.

Problem.

(G)

Let

The player one wants to maximize with its strategy over and the player two wants to maximize with its strategy over .

To explain Problem (G) in the sense of economics, we regard it as a game between the market participant (in our paper, the insurance company) and the market (an imaginary player). is the strategy of the insurance company, is the strategy of the market. Except for the insurance company, there are many other market participants (or competitors of the insurance company) in the market. Once any new opportunity for profits appears, it will be exploited by the competitors immediately, which may cause the market probability measure to deviate from the real-world probability measure to some new absolutely continuous probability measure . For this reason, describes the deviations of the probability measure and the cost of market’s strategy (competitors’ strategy). This explains that the market is to minimize with the cost of .

The parameter here measures the difficulty for the market to take a strategy. If , the market is extremely steady such that nobody can change the probability measure of the market, in other words, the competitors cannot grab opportunities but leave them there. Hence and Problem (G) degenerates to (4). If , there is no cost to change the probability measure of the market. In this case, whatever the insurance company’s strategy is, only a riskless return can be earned, since all the opportunities are exploited immediately by other competitors once it appears. Therefore, Problem (G) degenerates to (5).

The following statement illustrates the equivalence between Problem (MMVθ) and Problem (G). We set

Definition 2.1.

If there exists and a probability measure such that

then we call the pair a Nash equilibrium( non-cooperative equilibrium) for Problem (G).

Definition 2.2.

We call an optimal strategy for Problem (MMVθ) if .

Lemma 2.1.

Given some and , the following statements are equivalent:

(a) is a Nash equilibrium of Problem (G);

(b) , ;

(c) .

Proof.

The proof is the same as that of Proposition 8.1 in Aubin (2013). ∎

Lemma 2.1 tells us that the optimal strategy of Problem (MMVθ) actually lies in the Nash equilibrium of Problem (G).

2.2 Financial market and insurance market

Let be the real world probability measure. The following standard Black-Scholes type financial market is considered.

| (9) |

where is the riskless asset, is the price of the risky stock and is a standard Brownian motion. Denote , where is the completion of under .

Assumption 2.1.

Assume that , and are all bounded positive deterministic functions such that for all and satisfies the non-degenerate condition: there exists such that for all .

On the other hand, the following controlled Cramér-Lundberg model is considered as the insurance surplus process

where is the claim process, , and are the safety loadings of the insurer and the reinsurer respectively, is the control process representing the retention level of the insurance company. Generally, . Here with a Poisson random measure counts the number of claims within the time interval whose sizes lie in the interval . is the support of . Let be the Lévy measure of the random measure and be the compensated Poisson random measure. Then . The surplus process becomes

| (10) |

Denote by , where is the completion of the -field generated by the Poisson measure under . By Proposition 2.7.7 of Karatzas and Shreve (2012), is a right-continuous filtration. Generally, the insurance market is independent of the capital market, i.e., the filtration is independent of . Denote as the combined filtration of and , where is the smallest -field containing both and .

The insurance company’s wealth process can be formulated as the following controlled process

| (11) |

with initial value . For notational convenience, let and

where . Since is the cost of risk-transfer in insurance market, and is the capital market risk premium, measures how much benefit the insurance company can derive from undertaking the risk.

3 Auxiliary SDE

To solve Problem (G) for the prospect , i.e., the terminal wealth of the insurance company, it is intuitive to characterize by some process which is more tractable than a probability measure. If the probability measure is constrained to a subset of :

( means is equivalent to ), we can take a similar procedure as that of Mataramvura and Øksendal (2008) and Elliott and Siu (2009) to characterize by the following SDE

| (12) |

where is a -predictable process and is a -adapted process. Here is the unique solution of SDE (12)(see Mataramvura and Øksendal (2008) and Elliott and Siu (2009) for the cases without jumps). Specially, we can regard and as control processes which have a one-to-one correspondence with .

In this paper, we consider the absolutely continuous probability measures . In this case, may equal zero at some . To overcome this difficulty, we take a similar procedure as shown in Li and Guo (2021) in which a continuous case is considered. By using the tools of discontinuous martingale analysis in Kabanov et al. (1979), Liptser and Shiryayev (2012) and Hansen et al. (2006), it can be proved that the martingale representation (12) still holds for all (Theorem A.1). We can then still make use of the auxiliary Problem (Psxy) to help solve the original problem. The proof is in the appendices. The original problem can be replaced by the following auxiliary problem

| (13) | |||||

| (14) |

with , and initial values , .

Problem.

(Psxy) Let

| (15) |

where represents . The player one wants to maximize with its strategy over defined below and the player two wants to maximize with its strategy over defined below.

Definition 3.1.

(admissible) The strategy of the player one is admissible for Problem (Psxy), if and are -predictable process and -adapted process, respectively, such that

moreover, we denote as the set of all admissible strategies .

The strategy of the player two is admissible for Problem (Psxy), if for any fixed , and are -predictable process and -adapted process, respectively, satisfying

such that SDE (14) has a unique solution which is a nonnegative -adapted square-integrable -martingale satisfying for . Moreover, we denote as the set of all admissible strategies .

In general, the SDE (14) admits an exponential martingale solution (positive almost everywhere) if and satisfy some additional conditions such as the Novikov’s condition. However, we do not include these additional conditions in Definition 3.1. The SDE (14) can also admit nonnegative solutions which is enough in our paper even if the Novikov’s condition does not hold.

Example 3.1.

Let and where and is a square-integrable marginale:

Then the SDE (47) becomes

| (16) |

It is easy to check that (16) admits a solution (indistinguishable). Indeed, if , then

Meanwhile, if , then

Therefore, for any . By substituting into , we have

We can notice that on the set of positive measure ,

which fails to satisfy the Novikov’s condition.

The infinitesimal generator of for any smooth function is given by

We only consider here that and are both Markov feedback control, that is, and .

4 Optimal strategies

In this section, we give the value function and the optimal strategy for Problem (MMVθ). The following lemma gives a candidate for the Nash equilibrium of Problem (Psxy).

Theorem 4.1.

Proof.

We study the following nonlinear equation

| (20) |

with the terminal condition . Inspired by the terminal condition of (20), we try a solution of the following form

| (21) |

where , and . Therefore,

| (22) |

To study the equation (23), first let be arbitrary and solve

pointwisely over the jump size . If , the minimum is attained at

| (24) |

Secondly, we try to solve

If , then the maximum is attained at

| (26) |

Substituting (26) into (25), we get the following three ordinary differential equations

with terminal conditions , and . It is easy to find that the solutions of the above equations are as follows

| (27) |

Since and are both positive functions, the above requirements are all satisfied. By plugging (27) into (26) and (24), the saddle point for the non-linear PDE (20) is proved to be (19). Moreover, it is easy to verify that (19) is indeed the saddle point of the HJBI equation (17) since it satisfies

In the end, by inserting (27) into (21), (18) is proved to be a smooth solution of (17). ∎

Define

| (28) |

where represents that , .

Theorem 4.2.

(verification theorem) in (18) is the value function of Problem (Psxy). is a Nash equilibrium of Problem (Psxy).

We first give a lemma verifying the admissibility of and before proving this theorem.

Lemma 4.1.

The strategies and defined by (28) belong to and , respectively.

Proof.

By Theorem 13 (2) and Lemma 7 (2) of Kabanov et al. (1979), SDE (14) has a unique solution in the class of nonnegative local martingales which we also denote as . Since is deterministic, bounded and satisfies

| (29) |

is a square-integrable martingale. Consequently, .

On the other hand, since

we can deduce that

which proves that . ∎

Proof of Theorem 4.2 is as follows.

Proof.

By applying Itô’s Lemma to function in (18), for any admissible strategies, we have

Let . Recall that (48) holds, therefore

By Lemma 4.1, the optimal pair given by (28) belongs to , thus is admissible. Since is the solution of the HJBI equation (17), substituting into it gives

Letting we obtain

Lemma 4.2.

Let and be the state processes under the Nash equilibrium , then

| (30) |

Proof.

Since is an Ornstein-Uhlenbeck process, it has an explicit solution as follows

∎

Theorem 4.3.

If the initial values are and , the optimal strategies of Problem (MMVθ) are given by

| (31) |

and the value function of Problem (MMVθ) is given by

| (32) |

Remark 4.1.

By taking the conditional expectation on (30), we have

Then the optimal strategies in (31) can be written as

Here and are scale factors called the market price of risk. The optimal strategies have the following economic explanation: The insurer has a benchmark which is the expected wealth plus an additional anticipated return . The larger the parameter of risk aversion , the smaller the additional anticipated return. The insurer would compare the current wealth to the benchmark, and choose its strategies according to the difference modified by the scale factors. If the current wealth is smaller than the benchmark, the insurer would take a more risky strategy and if the current wealth is large, the insurer would be more conservative.

Remark 4.2.

For the no-jump case, where the claim process is no longer a compound Poisson process but are assumed to satisfies the dynamics

| (33) |

where is a standard Brownian motion independent of , and is the Lévy measure defined in Subsection 2.2, it can be calculated that for the new problem the value functions is also (4.3) (see Li and Guo (2021))). In this case, (33) is called the diffusion approximation of the compound Poisson process .

5 Efficient frontier

We now discuss the relation between the variance and the mean of the terminal wealth process for varying . Denote as the optimal strategy for Problem (MMVθ). If we choose a strategy , then by substituting it into SDE (11), we can get the riskless wealth of the insurance company:

| (34) |

Here, we denote .

Theorem 5.1.

If we let the parameter be arbitrary, then the variance of the terminal wealth process can be written as a functional of the expectation as follows

where . The corresponding strategy is given by

Remark 5.1.

The expression in Theorem 5.1 coincides with the efficient frontier of the classical MV model (see Theorem 8 of Bi et al. (2014)), which means the optimal strategies with different in this paper also possess the property of the efficient strategies for the classical MV model. Specifically, it is well known that the efficient strategy of the classical MV model is an “optimal” strategy, which minimizes the variance while ensuring that the mean is fixed, and for our MMV problem, if we fix , its optimal strategy is (31) with

and, under this strategy, the variance indeed attains its minimum . In view of this, we call

the efficient frontier and (31) with the efficient strategies for the MMV problem.

Remark 5.2.

We first give some lemmas before proving Theorem 5.1.

Lemma 5.1.

If , , we have, for the optimal strategies , and ,

| (36) | ||||

| (37) |

Proof.

Lemma 5.2.

For any fixed , the variance of the wealth process for the optimal strategy is as follows

| (38) |

with defined by and

| (39) |

Proof of Theorem 5.1 is as follows.

Proof.

By taking expectation of (13) and comparing it with (34), we have if and only if

| (40) |

For the case , we claim that is the Nash equilibrium of Problem (P) under constraint (40). We obtain

which gives

where is deterministic that is given by (34). For any ,

For any satisfying the constraint (40),

By Lemma 2.1, for the case , the efficient strategy is . Noting that and , the efficient frontier is the point . On the other hand, since the optimal strategy , for and

we have . For this case, the efficient strategy is given by in Theorem 4.3. The efficient frontier is given by (38). ∎

Corollary 5.1.

If there is no investment in the model, i.e., , the efficient frontier is

in which

Remark 5.3.

Corollary 5.2.

If there is no insurance in the model, in other words, , the efficient frontier is

in which

6 Numerical example

Example 6.1.

Consider a company whose risk-aversion is . The company’s deterministic profit from the operation is . Assume there exists an opportunity of arbitrage in the financial market and the return is , an uniformly distributed random variable. Then, the company’s total wealth depends on whether it exploits the opportunity of arbitrage, namely, the total wealth is where or . It is obvious that , but

which is greater than

It shows that the classical MV criterion may mislead the investors in certain situation. The MMV criterion remedies this problem and we have

which is less than

The value of is calculated with the aid of Theorem 2.2 in Maccheroni et al. (2009). Let be the domain of monotonicity of the classical MV criterion . Since , we have

where

It is easy to obtain that . Then

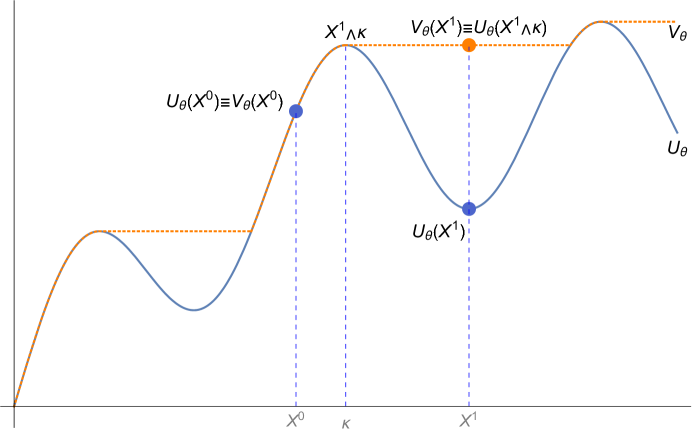

The monotonicity of the MMV criterion can be illustrated by Figure 1. The horizontal axis represents an ordering and sequencing set of random variables where the order is defined by . The vertical axis is the value of the criterion. The blue line illustrates the value of the classical MV criterion for different random variables. The orange dashed line illustrates the value of the MMV criterion. Obviously, the blue line is not always increasing and, in the domain of non-monotonicity, it is remedied by the orange dashed line.

Experiment 6.1.

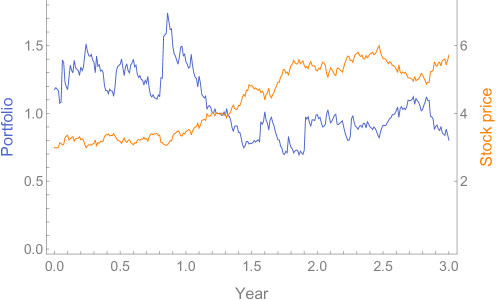

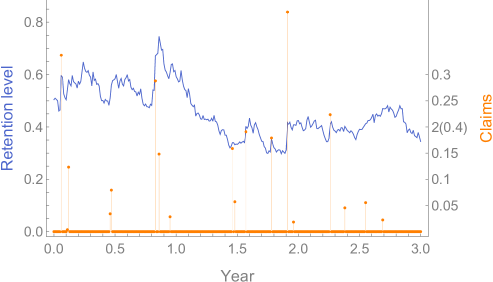

Consider an insurance company who wants to optimize its wealth in three years under the MMV criterion. For simplicity, we assume the amount of claim is exponentially distributed with intensity . The other coefficients in the model are assumed to be

In order to give an intuitive illustration, we simulate the trajectories of the optimal portfolio and the stock price in Figure 2, and the trajectories of the optimal retention level and the claims before in Figure 3. It is easy to see that the trajectory of the optimal portfolio is opposite to that of the stock price, and the trajectory of the optimal retention level rises sharply once a claim arrives. It shows the optimal strategies are ‘Buy low, Sell high’ strategies.

7 Conclusion

This paper studies the optimal monotone mean-variance problem for an insurance company in the framework of the Cramér-Lundberg risk model. The investment and the reinsurance strategies are taken into consideration. The work of this paper extends the results of Li and Guo (2021) by incorporating jumps into the surplus process of the insurance company. To investigate the MMV problem, we first give an auxiliary two-player zero-sum SDG. A generalized exponential martingale representation theorem for nonnegative martingale is proved, which is helpful for tackling with the absolutely continuity of the disturbed probability measure . The equilibrium of the SDG is found by applying the dynamic programming approach and solving the corresponding HJBI equation. The optimal solution of the original problem follows immediately from the equilibrium. It is proved that the optimal disturbed probability measure is indeed equivalent to the real measure . In the second part of the paper, we provides the efficient frontier for the MMV problem. Two numerical examples are given. To the best of our knowledge, it is the first time to study the MMV optimization problem for the model involving jump process. Possible future researches include the MMV optimization problem for more sophisticated models such as Cox process or spectral negative Lévy process. It is worth noting that, by the work of Strub and Li (2020), the optimal strategies for the MMV and the classical MV coincide in the framework of continuous semimartingale. But it is still an open problem whether the optimal strategies always coincide for a large class of jump processes. In any case, the optimal strategy for the MMV problem makes sense economically.

Appendix A From Problem (G) to Problem (Psxy)

For any market’s strategy , let

| (41) | ||||

Therefore, by virtue of properties of the Radon-Nikodym derivative, we have that . In other words, is a nonnegative martingale. In view of the fact that is right-continuous, has a RCLL version which, for simplicity, we also denote it as . Moreover, .

Lemma A.1.

Suppose that , then the process defined by (41) is a nonnegative square-integrable -martingale adapted to with . Moreover,

| (42) |

holds for any -measurable . Conversely, if is a nonnegative -adapted square-integrable -martingale with , then, for any , the probability measures defined via

| (43) |

belongs to , and satisfies the following consistency condition:

| (44) |

Moreover, for any -measurable such that , satisfies (42) .

Proof.

Suppose that . It is obvious that defined by (41) is a nonnegative martingale. By Jensen’s Inequality, we have

Thus is square-integrable. By the definition of Radon-Nikodym derivative, we have

which proves (43).

Conversely, let be a nonnegative square-integrable martingale with unit expectation. Since whenever , it follows from that defined via (43) is an absolutely continuous probability measure. The fact that is due to the square integrability of . The consistency condition is due to the martingale property of . In order to prove satisfies (42), we first prove the Bayes formula

| (45) |

By using the definition of conditional expectation, we have for any ,

The second equality and the sixth equality are due to the definition of conditional expectation. Letting proves the desired result. ∎

Lemma A.1 establishes a relationship between the mean one nonnegative square-integrable martingale and the absolutely continuous probability with square-integrable density with respect to . Let be the set of all nonnegative -adapted square-integrable -martingale with . Thus, if and only if . The MMV objective (8) can be formulated as

| (46) |

where an equivalent problem is to maximize

Therefore, Problem (G) can be changed equivalently into the following problem:

Problem.

(D) Let

The player one wants to maximize with its strategy over and the player two wants to maximize with its strategy over .

Proposition A.1.

Proof.

We first consider the case that is a Nash equilibrium of Problem (D) and , where is defined by (43) with . For any , let . It follows from Lemma A.1 that . For any , we have

which, by Lemma A.1 and the definition of Problem (G) and Problem (D), gives

For the inequality of the opposite direction, the proof is similar. ∎

So far, the strategy processes are and . However, is not a tractable strategy in the theory of dynamic programming. Here we characterize it as a state process controlled by two control processes and . The following theorem is a generalization of the exponential martingale representation theorem for the nonnegative martingale.

Theorem A.1.

There exists an -adapted process and an -predictable random field , such that admits the representation

| (47) |

where with , . Besides, and satisfy

| (48) |

for any integer , where

Proof.

See Appendix B. ∎

Remark A.1.

Let be the predictable -algebra. Let , where is the Borel -algebra of . Let be the Doléans measure associated with the random measure under the probability measure . Then and have the following representations

| (49) |

where . Given a process , it follows from Lemma 7 (2) of Kabanov et al. (1979) that SDE (47) with and defined by (49) has a unique solution which equals (indistinguishable).

Denote and for any , and are -predictable and -adapted, respectively, satisfying , such that SDE (47) has a unique solution belonging to . The following corollary provides a theoretical basis for changing the control process from to and .

Corollary A.1.

Proof.

This corollary follows immediately from Theorem A.1. ∎

The following proposition provides the equivalence of the solutions of Problem (D) and Problem (Psxy).

Appendix B Proof of Theorem A.1

We first give some lemmas before proving Theorem A.1.

Note that may hit zero at finite time, we need to consider the behavior of after that. Define

with the convention that . Then , -a.s. on the set . The following lemma shows that would stay there once it hit zero.

Lemma B.1.

On the set , it holds almost surely under probability that

Proof.

Given a fixed , note that is a nonnegative martingale, then by applying the optional stopping theorem, we have

Since is nonnegative -a.s., we obtain -a.s.. Let denote the set such that , then . Let , where is the set of all positive rational number. Then, for all , holds for all . By the right-continuity of , we have that holds for all -a.s.. ∎

Acknowledgment This work was supported by the National Natural Science Foundation of China 11931018, the Tianjin Natural Science Foundation 19JCYBJC30400, the National Natural Science Foundation of China 12201104 and the Fundamental Research Funds for the Central Universities 2232021D-29.

References

- Aubin (2013) Aubin, J.-P. (2013). Optima and Equilibria: An Introduction to Nonlinear Analysis, volume 140. Springer Science & Business Media.

- Bai and Guo (2008) Bai, L. and Guo, J. (2008). Optimal proportional reinsurance and investment with multiple risky assets and no-shorting constraint. Insurance: Mathematics and Economics, 42(3):968–975.

- Bäuerle (2005) Bäuerle, N. (2005). Benchmark and mean-variance problems for insurers. Mathematical Methods of Operations Research, 62(1):159–165.

- Bensoussan et al. (2022) Bensoussan, A., Ma, G., Siu, C. C., and Yam, S. C. P. (2022). Dynamic mean–variance problem with frictions. Finance and Stochastics, 26(2):267–300.

- Bi et al. (2014) Bi, J., Meng, Q., and Zhang, Y. (2014). Dynamic mean-variance and optimal reinsurance problems under the no-bankruptcy constraint for an insurer. Annals of Operations Research, 212(1):43–59.

- Bielecki et al. (2005) Bielecki, T. R., Jin, H., Pliska, S. R., and Zhou, X. Y. (2005). Continuous-time mean-variance portfolio selection with bankruptcy prohibition. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 15(2):213–244.

- Chen et al. (2021) Chen, L., Landriault, D., Li, B., and Li, D. (2021). Optimal dynamic risk sharing under the time-consistent mean-variance criterion. Mathematical Finance, 31(2):649–682.

- Chen and Yam (2013) Chen, P. and Yam, S. (2013). Optimal proportional reinsurance and investment with regime-switching for mean–variance insurers. Insurance: Mathematics and Economics, 53(3):871–883.

- Elliott and Siu (2009) Elliott, R. J. and Siu, T. K. (2009). Portfolio risk minimization and differential games. Nonlinear Analysis Theory Methods & Applications, 71(12):0–0.

- Hansen et al. (2006) Hansen, L. P., Sargent, T. J., Turmuhambetova, G., and Williams, N. (2006). Robust control and model misspecification. Journal of Economic Theory, 128(1):45–90.

- Kabanov et al. (1979) Kabanov, J. M., Lipcer, R. Š., and Širjaev, A. (1979). Absolute continuity and singularity of locally absolutely continuous probability distributions. I. Mathematics of the USSR-Sbornik, 35(5):631.

- Karatzas and Shreve (2012) Karatzas, I. and Shreve, S. (2012). Brownian Motion and Stochastic Calculus, volume 113. Springer Science & Business Media.

- Landriault et al. (2018) Landriault, D., Li, B., Li, D., and Young, V. R. (2018). Equilibrium strategies for the mean-variance investment problem over a random horizon. SIAM Journal on Financial Mathematics, 9(3):1046–1073.

- Li and Guo (2021) Li, B. and Guo, J. (2021). Optimal reinsurance and investment strategies for an insurer under monotone mean-variance criterion. RAIRO-Operations Research, 55(4):2469–2489.

- Li and Ng (2000) Li, D. and Ng, W.-L. (2000). Optimal dynamic portfolio selection: Multiperiod mean-variance formulation. Mathematical Finance, 10(3):387–406.

- Li et al. (2002) Li, X., Zhou, X. Y., and Lim, A. E. (2002). Dynamic mean-variance portfolio selection with no-shorting constraints. SIAM Journal on Control and Optimization, 40(5):1540–1555.

- Liese and Vajda (2007) Liese, F. and Vajda, I. (2007). Convex statistical distances.

- Liptser and Shiryayev (2012) Liptser, R. and Shiryayev, A. N. (2012). Theory of Martingales, volume 49. Springer Science & Business Media.

- Maccheroni et al. (2009) Maccheroni, F., Marinacci, M., Rustichini, A., and Taboga, M. (2009). Portfolio selection with monotone mean-variance preferences. Mathematical Finance, 19(3):487–521.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1):77–91.

- Mataramvura and Øksendal (2008) Mataramvura, S. and Øksendal, B. (2008). Risk minimizing portfolios and HJBI equations for stochastic differential games. Stochastics An International Journal of Probability and Stochastic Processes, 80(4):317–337.

- Mei and Zhu (2020) Mei, H. and Zhu, C. (2020). Closed-loop equilibrium for time-inconsistent mckean–vlasov controlled problem. SIAM Journal on Control and Optimization, 58(6):3842–3867.

- Ni et al. (2019) Ni, Y.-H., Li, X., Zhang, J.-F., and Krstic, M. (2019). Equilibrium solutions of multiperiod mean-variance portfolio selection. IEEE Transactions on Automatic Control, 65(4):1716–1723.

- Shen and Zeng (2014) Shen, Y. and Zeng, Y. (2014). Optimal investment–reinsurance with delay for mean–variance insurers: A maximum principle approach. Insurance: Mathematics and Economics, 57:1–12.

- Shen et al. (2014) Shen, Y., Zhang, X., and Siu, T. K. (2014). Mean–variance portfolio selection under a constant elasticity of variance model. Operations Research Letters, 42(5):337–342.

- Strub and Li (2020) Strub, M. S. and Li, D. (2020). A note on monotone mean-variance preferences for continuous processes. Operations Research Letters.

- Sun and Guo (2018) Sun, Z. and Guo, J. (2018). Optimal mean–variance investment and reinsurance problem for an insurer with stochastic volatility. Mathematical Methods of Operations Research, 88(1):59–79.

- Trybula and Zawisza (2014) Trybula, J. and Zawisza, D. (2014). Continuous time portfolio choice under monotone preferences with quadratic penalty - stochastic interest rate case. Quantitative Finance.

- Trybuła and Zawisza (2019) Trybuła, J. and Zawisza, D. (2019). Continuous-time portfolio choice under monotone mean-variance preferences-stochastic factor case. Mathematics of Operations Research, 44(3):966–987.

- Yeung and Petrosjan (2006) Yeung, D. W. and Petrosjan, L. A. (2006). Cooperative Stochastic Differential Games. Springer Science & Business Media.

- Zhou and Li (2000) Zhou, X. Y. and Li, D. (2000). Continuous-time mean-variance portfolio selection: A stochastic LQ framework. Applied Mathematics and Optimization, 42(1):19–33.