11email: borreynoso@ciencias.unam.mx 22institutetext: IIMAS, UNAM

Maximum Likelihood Estimation for a Markov-Modulated Jump-Diffusion Model

Abstract

We propose a method for obtaining maximum likelihood estimates (MLEs) of a Markov-Modulated Jump-Diffusion Model (MMJDM) when the data is a discrete time sample of the diffusion process, the jumps follow a Laplace distribution, and the parameters of the diffusion are controlled by a Markov Jump Process (MJP). The data can be viewed as incomplete observation of a model with a tractable likelihood function. Therefore we use the EM-algorithm to obtain MLEs of the parameters. We validate our method with simulated data.

The motivation for obtaining estimates of this model is that stock prices have distinct drift and volatility at distinct periods of time. The assumption is that these phases are modulated by macroeconomic environments whose changes are given by discontinuities or jumps in prices. This model improves on the stock prices representation of classical models such as the model of Black and Scholes or Merton’s Jump-Diffusion Model (JDM). We fit the model to the stock prices of Amazon and Netflix during a 15-years period and use our method to estimate the MLEs.

keywords:

Diffusion Processes, Markov Jump Processes, Maximum Likelihood Estimator, EM-Algorithm, Mathematical Finance1 Introduction

Modelling the stock market is a central topic of mathematical finance due to the importance of predicting values to help investors identify investments with better returns. It is generally assumed that the stock prices may be represented by a continuous-time stochastic process and that we may observe its values at discrete times. From these historical data, we may estimate uncertainties and predict stock market trends to help investors when making decisions.

One of the earliest model for is the Geometric Brownian Motion (GBM) introduced by Black and Scholes in 1973 [4]. This process is defined by its initial value, drift and volatility; see equation (1) for a detailed definition.

The GBM is central to describe the behavior of a stock price in option pricing models. However, since the works in [5], [13], and [14], it is recognized that the market dynamics can not be modelled by GBM with constant parameters of drift and volatility. One of its main drawbacks is that large and abrupt changes in the prices may not be accounted for without assuming that the process has an artificially large volatility. The source of these abrupt changes may be macroeconomic events such as changes in the rate of economic growth, gross domestic product, unemployment rates, and inflation.

In 1976, Merton [16] proposed a JDM for asset pricing to incorporate rare and abrupt changes in the values of . The JDM adds, to the GBM, a compound Poisson process where jumps are independent and identically distributed; see equation (2) for a detailed definition. In Merton’s model the logarithm of a jump is normally distributed [16], which renders some computations relatively easier. On the other hand, Kou [12] modifies Merton’s JDM by replacing the normal distribution with the Laplace distribution, this becomes computational more stable since the latter distribution is determined by one parameter only. Nevertheless, the continuous term of these models have constant drift and volatility which does not completely reflect the behavior of real data; see, e.g., Figure 1.

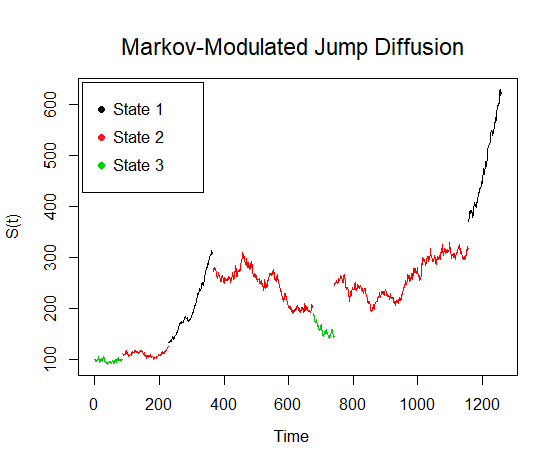

Later models introduce random drift and random volatility parameters. e.g., in [10] and [11], the authors introduced the MMJDM which seeks to incorporate more variables that may influence the values of the stock prices; see Figure 2 for an example. In the MMJDM there is an underlying MJP that modulates both the drift and volatility of . The heuristic for this mechanism is that, abrupt jumps in the prices correspond to changes in the macroeconomic state of the market, therefore, not only a discontinuity occurs but also the process enters a distinct phase that determines distinct drift and volatility. We assume that the state space of the MJP represents the different environments of the financial market and so it influences the drift and volatility of the diffusion. MMJDMs for asset dynamics have been investigated in many works including [6], [7] and [9].

In this paper, we are concerned with the estimation of parameters of a MMJDM. Inference, when there are two states in the underlying MJP, was presented in [8]. Likelihood based estimation (including Bayesian) for MMJDM in risk theory has been investigated by [1] and [2]. Our main contribution is Section 3, where we present a methodology for the inference of the MMJDM for the general case with states and Laplace distribution for the logarithm of each jump; see Section 2 for a detailed definition. We deal with maximum likelihood estimation in the situation where we observe the diffusion process (at discrete times) and no direct observations of the MJP are given. Therefore, the data can be viewed as incomplete observations from a model with a tractable likelihood function where the full data set consists of a continuous time record of both the diffusion process and the MJP. We therefore use the EM-algorithm (see, e.g. [15], [18]) to tackle the difficulties that arise from using incomplete information in finding the MLEs. Another natural methodology used to estimate the parameters is through Markov chain Monte Carlo (MCMC) algorithms (see, e.g, [1]). Although the MCMC method allows us to obtain more information on the parameters from their distribution, in general, EM algorithms have two advantages: the speed of convergence and precision of the parameters are better and the estimation does not depend on the choice of the prior distribution.

2 Markov-Modulated Jump- Diffusion Model

Before introducing the MMJDM, we present the definitions of both the GBM and the JDM. The GBM is the stochastic process solution of the stochastic differential equation (SDE)

| (1) |

where , , and is a standard Brownian motion.

The process is a JDM if it is given by the SDE

| (2) |

where, in addition to the initial value , parameters and we also have a compound Poisson process with intensity and i.i.d. jump sizes . We recall, as a warm up, that the solution for the JDM (2) is

For the MMJDM, we assume that, for some positive integer , the financial market undergoes a macroeconomic environment that evolves among distinct states. The financial environment is then given by a MJP with state space and intensity matrix . Let and be, respectively, the jump times and the counting process that records the number of jumps of .

Each of the jumps of the MJP represents the occurrence of abrupt events that cause changes in the environment and we assume that state represents the -th most favourable and stable environment; from good growth and confidence to crisis in the business sector.

For the stock prices , we assume to have an initial state and vectors and corresponding to the drift and volatility of the stock prices at each state . In addition, let be a succession of independent random variables with Laplace distribution ; these variables will determine the jumps of the stock prices. The MMJDM associated to the stock prices is the solution to the SDE given by

| (3) |

where , and is independent of . Note that the parameters of the MMDJM are given by .

3 Methodology for the Maximum Likelihood Estimators

We deal with the situation where we do not have full observation of the MMJDM. The data are observations of the stock prices at discrete times , where for . Our aim is to find the MLE of when we only observe ; we consider this data as an incomplete observation of a full data set consisting of both sample paths and .

First, we find the likelihood function for the full data set and then estimate conditional expectation of this full log-likelihood function given the observations . Assume that we count with ; that is, a continuous observation of the MJP and historical data of the stock prices. Then the likelihood function is given by

which may be expressed as

| (4) |

where

-

•

is the number of jumps from state to ,

-

•

is the number of visits to state , i.e.,

-

•

is the total time spent at state ,

-

•

is the number of jumps ,

-

•

is the number of observations of on the -th visit of at state ,

-

•

where is the -th observation of stock prices on the -th visit of at state ,

-

•

is the size of the -th jump,

-

•

.

In the case where the MMJDM is continuously observed, which is not a realistic assumption, finding the MLE is straightforward. For the case of incomplete data, the overall methodology is summarize in Algorithm 1; we detail each of its steps in the subsequent sections.

3.1 Identify the jumps of the MJP

We will transfer the analysis of to the log-yields which are defined by , for .

Observe that if there are no jumps in we may write for and some and so the process may be regarded as a GBM process with parameters and ; see (1).

Thus, conditional on not having jumps in and using that and are independent, we can solve the SDE in (3) and obtain, for ,

| (5) |

Consequently, for , assuming that for (i.e., there are no jumps in such interval), we infer that ; that is,

| (6) |

Heuristically, the logarithm of each jump should be significantly larger than the fluctuations of the diffusion over intervals of length , at any of the MJP states. Namely, we assume that is significantly larger than . Consequently, we choose a suitable constant and define ; we determine that has (at least) a jump in the time interval whenever .

3.2 Estimate the distribution of the jumps

Write . By assuming that there is at most one jump in each of the intervals , we may associate to the -th jump of the process; in fact, we heuristically argue below that . Since we have that the MLE of is given by

| (7) |

Indeed, assume that the -th jump is contained in . We may assume that , for some distinct . Hence, is the sum of and two perturbations; that is

where . Note that is independent of both and . The variability of the distribution of is assumed to be significantly larger than the fluctuations of the continuous part of the process in an interval of length . We have that

which implies that the perturbations may be ignored, equivalently, .

3.3 Estimate the coefficients of the GBM

Let us analyse now the yields that correspond to intervals with no jumps. If then for some and . Therefore, (6) implies that . Hence, we may regard as an observation of a mixture of normal distributions, and so we estimate the parameters and from the observations .

For ease of writing, let and let be an enumeration of the yields that preserves the original order in . In what follows we introduce a latent discrete variable such that whenever ; in this case we say that belong to group . Observe that, conditioned to having no jumps in the interval corresponding to , the latent variable coincides with , for all in such interval.

For classifying , we can view each element , with , as an observation of a random variable with a -component finite mixture density given by

| (8) |

where and are the mixing proportions; that is, and for , . We have that

| (9) |

where and is the probability density function of a normal distribution of parameters .

We shall call the complete data set and refer to the actual observed data as incomplete. We apply the EM algorithm to classify and, simultaneously, approximate the MLE of both and . We have that the log-likelihood of the complete data (see [19]) is given by

| (10) |

Since the increments of the Wiener process are conditionally independent (on MJP), so are their corresponding log-returns and we can use the EM Algorithm 2 to estimate and .

3.4 MLE of

Finally, it remains to estimate the parameter of the MJP process . To do so, we need to estimate the time the process spends at each state and the frequency of jumps from state to state , for distinct . First, we classify the clusters of yields between jumps, thus recovering the bulk of time spent at each state . The inference from the yields in which a jump is involved is more delicate and is performed in Algorithm 3.

Let us decompose into clusters,

where are the yields between -th and -th jumps for and, similarly, and are the yields before the first jump and after the -th jump, respectively.

We again refer to the latent variables to classify each cluster in one of the groups , . For and , we have that the probability that the block comes from the -th density is

| (11) |

Thus, we partially reconstruct a path of the MJP for the time intervals , where is the time of observation and is the time of observation . We classify each cluster using for . If the -th cluster is in state then for .

The values of are still undetermined in the missing intervals, i.e., we can only observe at the endpoints of interval for . Hence, we use Algorithm 3 to , iteratively, simulate such missing paths and estimate the MLE of each of the entries in the intensity matrix . Algorithm 3 is a Stochastic EM (SEM) algorithm (see, e.g. [17]); the E-step and M-step of each of these algorithms are repeated until convergence, i.e., when the estimators are observed to arrive at the stationary distribution. An advantage of using the stochastic version of EM algorithm is that, by having the distribution of the estimator, we can calculate confidence intervals for the MLE’s obtained.

4 Simulation Study

In this section, we present the results of a simulation study that calibrates the method presented in Section 3. We test the model with ; that is, we consider three states going from a stable economy to an unstable economy to crisis in the sector. Hence, we may consider in the test that drifts are decreasing (possibly ) while volatilities are increasing in .

We consider a MMJDM with the following parameters. Let

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) |

We generate a sample path where , , and . Observe that if represents one-day periods, then represents, for example, the daily observations of the stock prices during a 7-year period of time if . In fact, the parameters may be proposed on a time scale of 1 year (252 business days) and then rescaled to (12)–(15) which then may be interpreted as daily rates of the process.

Figure 2 shows a path of MMJDM with the aforementioned parameters in the time interval . The MLEs of are presented in Table 1. The MLEs of and for 1000 iterations are given in Table 2 and, Table 3 respectively; Algorithm 2 was run with . We tried several seeds for Algorithms 2 and 3. In this study, no dependence was observed in the estimations except for the number of iterations, so we report the results using the seeds that best represent the model.

| Value | Error | |

|---|---|---|

| 7.575757 | ||

| 5.897666 | 1.678092 | |

| 6.241154 | 1.334603 | |

| 7.756247 | 0.1804897 | |

| 7.352301 | 0.2234567 | |

| 7.144313 | 0.4314449 | |

| 6.994469 | 0.5812881 | |

| 7.175147 | 0.4006109 |

| Error | ||||

|---|---|---|---|---|

| 0.0059523810 | 0.0011904762 | -0.0009920635 | ||

| 0.0059469097 | 0.0027668870 | 0.0019743179 | 0.00001128 | |

| 0.0066422130 | 0.0034594822 | 0.0025009336 | 0.00001782 | |

| 0.0066102728 | 0.0032372128 | 0.0020031847 | 0.00001359 | |

| 0.0063053813 | 0.0028402039 | 0.0020858060 | 0.00001231 | |

| 0.0059171341 | 0.0031332369 | 0.0017120427 | 0.00001108 | |

| 0.0060495312 | 0.0030009829 | 0.0013917915 | 0.00000897 | |

| 0.0060614045 | 0.0029881755 | 0.0008520252 | 0.00000664 |

| Error | ||||

|---|---|---|---|---|

| 0.009449112 | 0.017817415 | 0.022047928 | ||

| 0.012769167 | 0.015921710 | 0.017703704 | 0.00003348 | |

| 0.009535770 | 0.015774837 | 0.017788880 | 0.00002231 | |

| 0.009327915 | 0.015878260 | 0.018081729 | 0.00001950 | |

| 0.009104289 | 0.015999326 | 0.017911584 | 0.00002053 | |

| 0.009154862 | 0.015454727 | 0.018728368 | 0.00001668 | |

| 0.009237009 | 0.014904877 | 0.014904877 | 0.00001700 | |

| 0.014904877 | 0.014492026 | 0.019310947 | 0.00001854 |

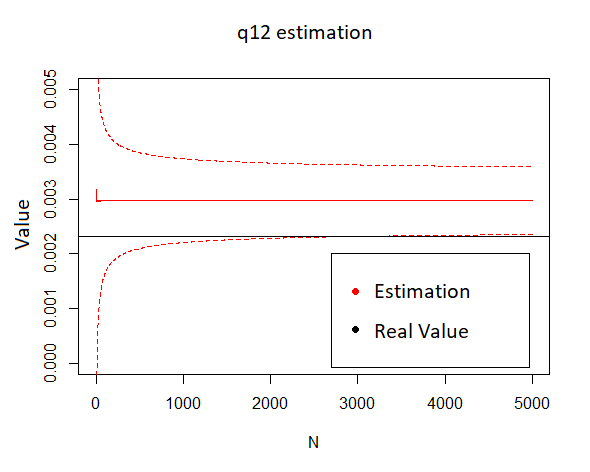

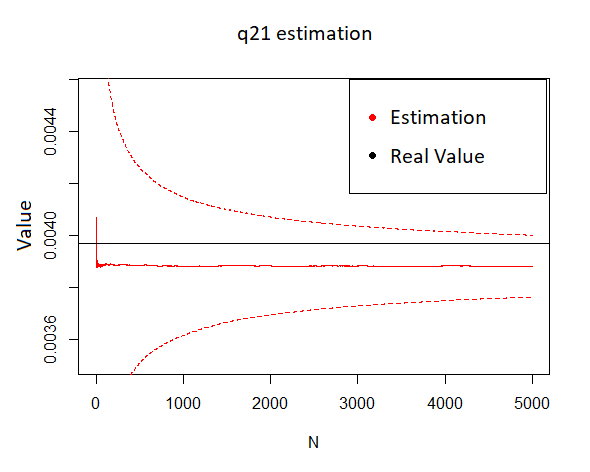

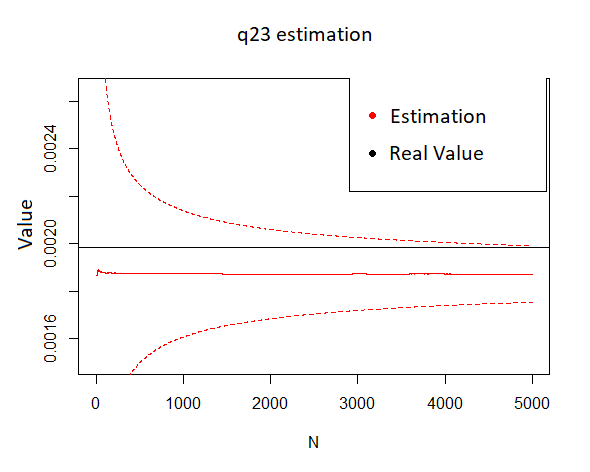

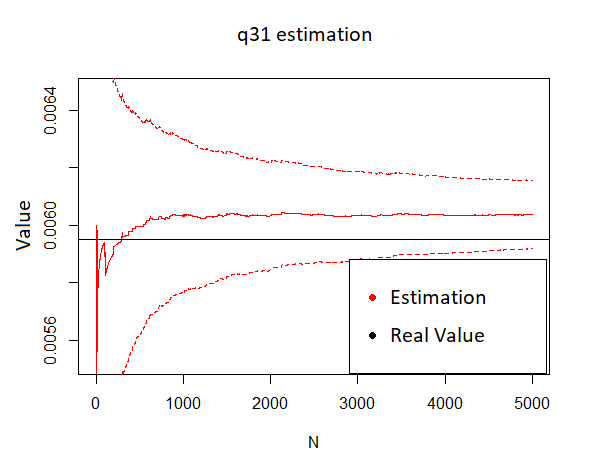

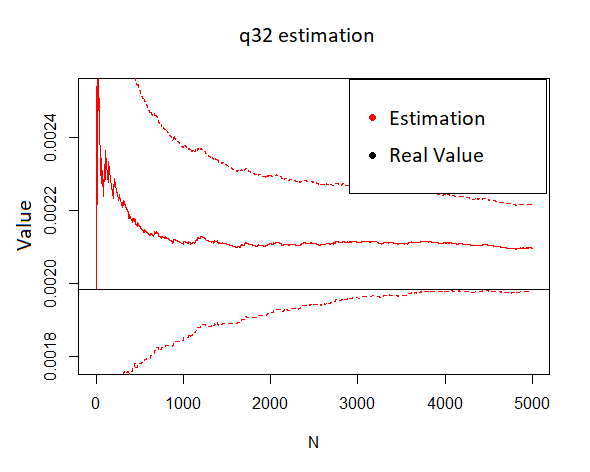

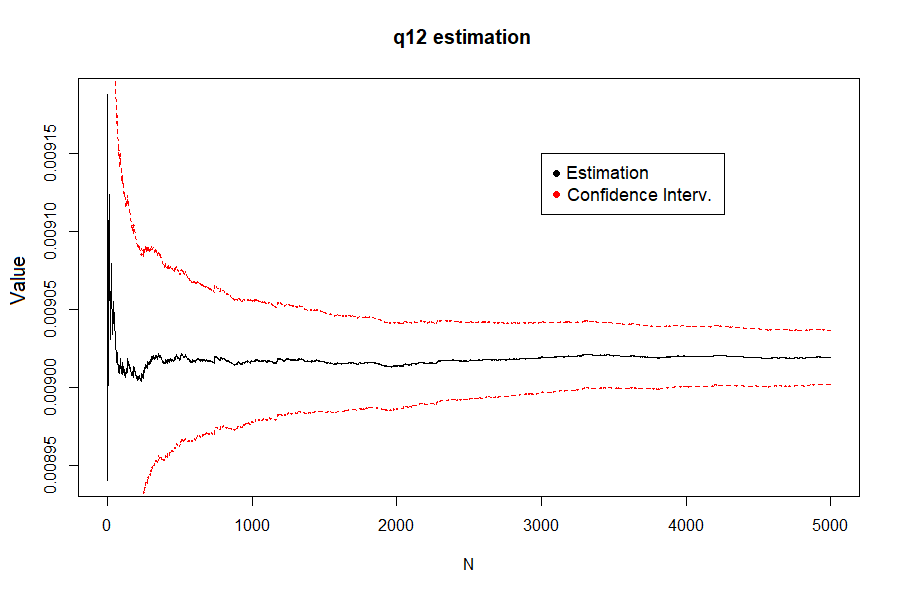

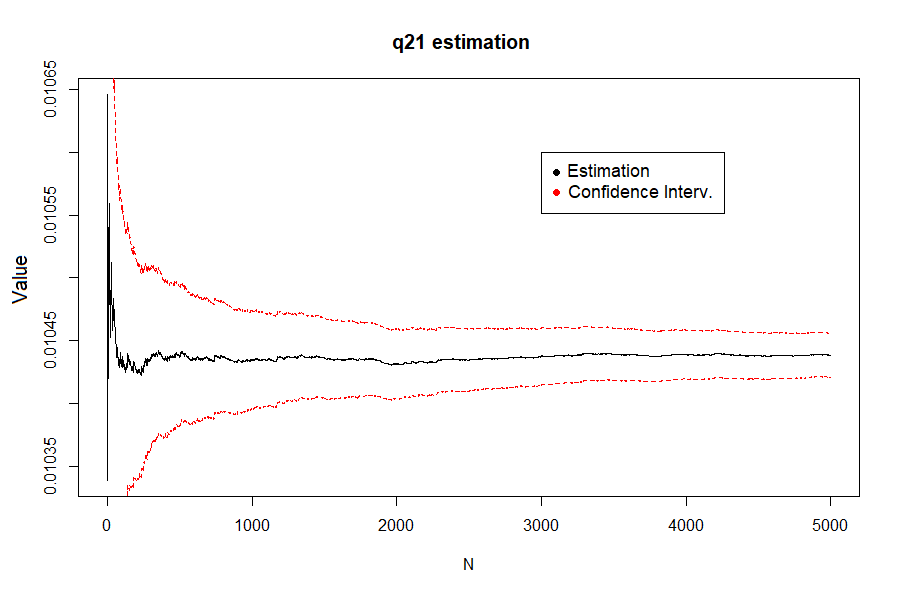

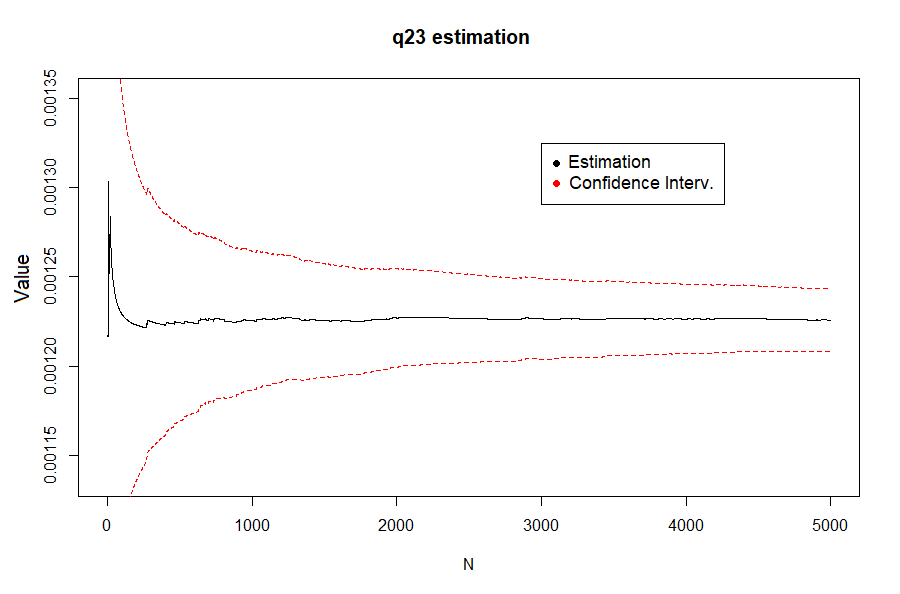

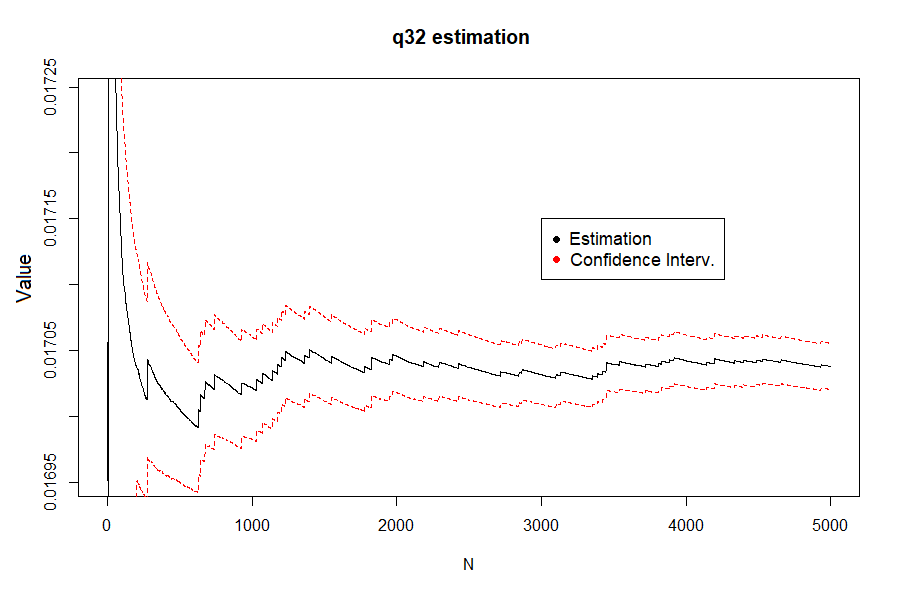

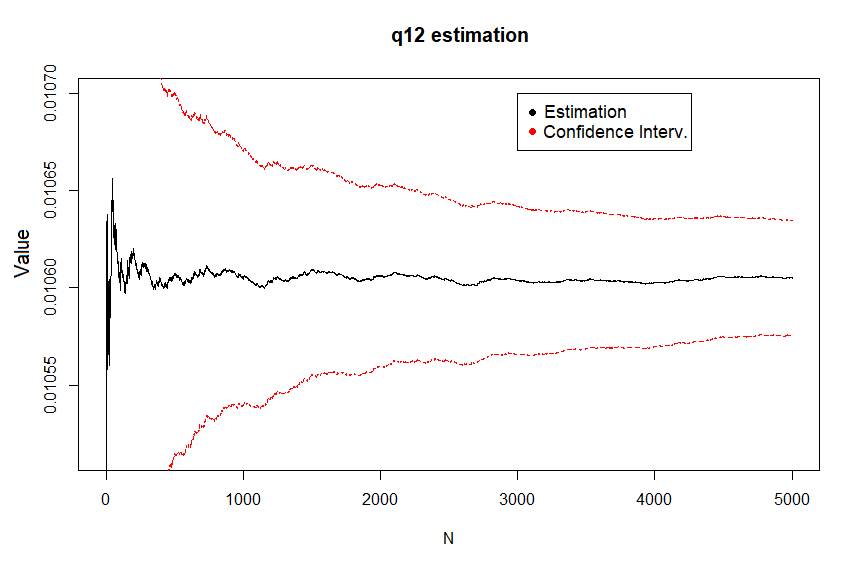

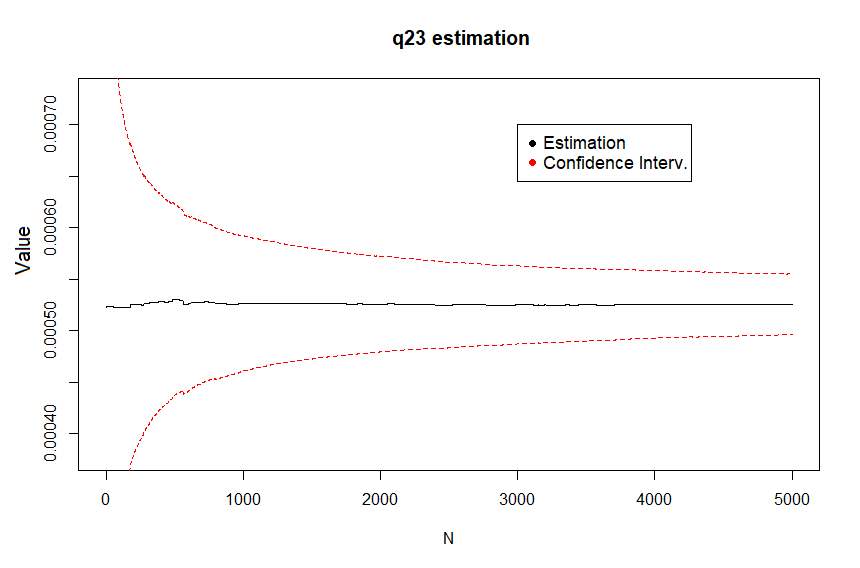

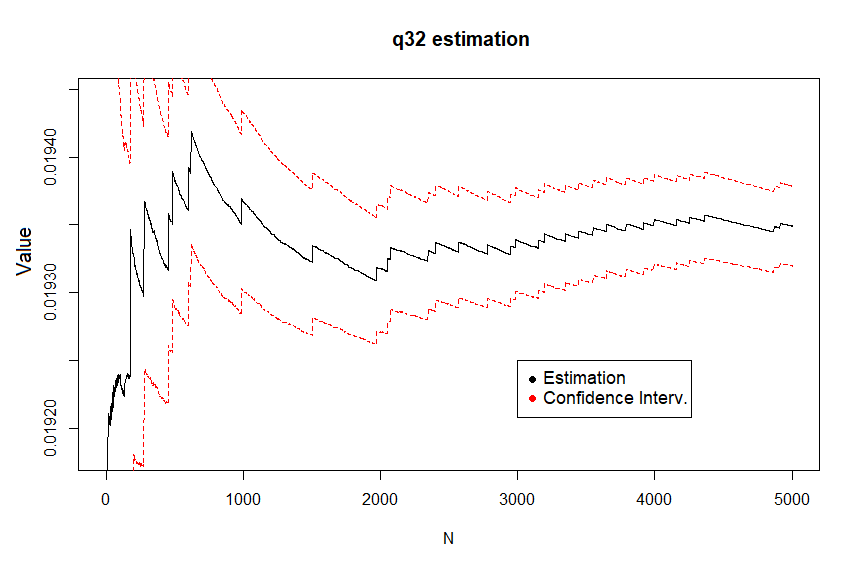

Finally, the MLE of the intensity matrix (after 1000 iterations) when is given in equation (16). Figure 3 plots the iterations of the Algorithm 1 to find the MLE of and 95% confidence intervals; we estimate the standard deviation of the MLEs through the Fisher information matrix (see [3]). We obtain

| (16) |

5 Real Data

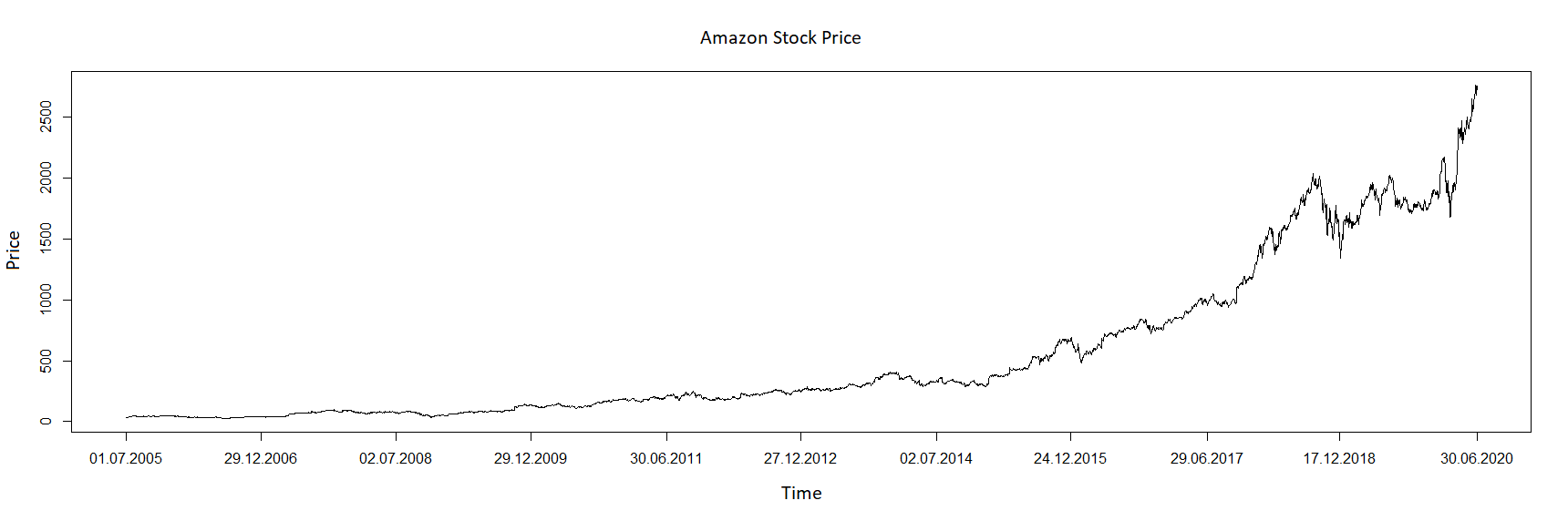

In this section, we fit the MMJDM for two sets of stock prices real data using the method presented in Section 3. Each data set corresponds to Amazon and Netflix daily stock prices from July 1st, 2005 to June 30, 2020; see Figure 1. Thus, it is natural to consider a day as the unit of time; that is . This historical data presents abrupt changes and these do not occur homogeneously in time and so we may use the MMJDM model to fit the data; based on the graphical evidence, we assume that the underlying MJP has three states.111 Estimating the number of states is a classification problem is more complex and beyond the scope of this paper.

Following our method, the first step is to identify the jumps. We can observe in the final prices of Netflix’s stock that the price suffers a change in its behavior after March 20, 2020. This can be explained because in March many countries introduced lockdown measures due to COVID 19 pandemic. In order to catch this change in this behaviour the threshold for the jumps was set to for the squared log-returns. Similarly, the tolerance level for Amazon was set to . As we do not consider jumps in consecutive days, we have 39 jumps for Netflix and 41 jumps for Amazon. These were used to obtain the jump parameter estimations for Netflix and for Amazon.

Algorithm 2 was run considering 1000 iterations; we use and initial values as in (13) and (14). The MLEs obtained for the drift and volatility parameters for both Netflix and Amazon are shown in Table 4.

| j | |||

|---|---|---|---|

| 1 | |||

| 2 | |||

| 3 |

Once the drifts and volatilities are estimated, we classified each cluster using (11) and partially constructed the path of the MJP for each stock. The initial value for both and estimation was (12) and we set the EM algorithm to 1000 initial iterations. The MLE for and is shown in equation (17) and (18); respectively. Finally, the graphs of the estimations of and are shown in Figures 4 and 5, respectively.

| (17) |

| (18) |

6 Conclusions

We propose a methodology based on Maximum Likelihood Estimators to estimate the parameters of the MMJDM process; this process models stock prices whose drift and volatility are shaped by macroeconomic states.

There are two key properties of the stock market that the MMJDM describes. First, changes in the macroeconomic states may lead to discontinuities or jumps in the prices (disguised in the sample paths as abrupt fluctuations). Second, when these changes occur they also modify the overall diffusion properties of the prices. Although previous Jump-Diffusion Models incorporate the eventual jumps in the process, the MMJDM also takes into account the changes in drift and volatility that fortuitous events or news in the sector may entail.

Among the challenges faced in this work are identifying the jumps, classifying the clusters of the log yields and optimizing the EM algorithms. We highlight that, as the simulation study in Section 3 shows, the methodology is robust since we are able to recover the parameters of the synthetic MMJDM.

The study with the real data on both Amazon and Netflix’ prices qualitatively reflects the same macroeconomic fluctuations. It is natural to conjecture that if the states are ordered according to the degree of stability in the market then the transitions between the stability and crisis will be sequential (e.g. before a crisis hit, there is a period of increased volatility). It is remarkable to note that, although this heuristic is not built into the model, there is no transition from the stable to the crisis state (that is; ).

Therefore we consider that the MMJDM more accurately represents the nature of fluctuations in the stock market. Moreover, the methodology proposed in this work to estimate the parameters of the process allows us to make inferences about the financial environments that favor a stock, which a useful tool in stock value speculation.

As future work, one may generalize this method by replacing the JMP to an underlying process where the length of stay in each stage follows a Phase Type distribution. One may also fit the distribution of the jump sizes according to the observed data. Finally, one may also consider methodologies that test for a suitable number of macroeconomic states since, at the moment, we assume the number of states is given.

Acknowledgements

We would like to thank the anonymous referee for their thorough comments. This work has been supported by PAPIIT TA100820.

References

- [1] Baltazar-Larios F., Esparza L.J.R. (2019) Bayesian Estimation for the Markov-Modulated Diffusion Risk Model. In: Antoniano-Villalobos I., Mena R., Mendoza M., Naranjo L., Nieto-Barajas L. (eds) Selected Contributions on Statistics and Data Science in Latin America. FNE 2018. Springer Proceedings in Mathematics Statistics, vol 301. Springer, Cham. 10.1007/978-3-030-31551-1_2

- [2] Baltazar-Larios, F. and Esparza, Luz Judith R. (2022). Statistical inference for partially observed Markov-Modulated Diffusion Risk Model. Methodology and Computing in Applied Probability. Version on line. 10.1007/s11009-022-09932-7.

- [3] Bladt, M., Esparza, L.J.R. Friis, B.F. (2011). Fisher information and statistical inference for phase-type distributions. Journal of Applied Probability, 48(A): 277–293. :10.1239/jap/1318940471.

- [4] Black, F. and Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy 81(3): 637-654. 10.1086/260062

- [5] Clark, P. K. (1973). A subordinated stochastic process model with finite variance for speculative prices. Econometrica 41(1): 135–155. 10.2307/1913889

- [6] Costabile, M. Leccadito, A., Massabó, I. and Russo E. (2014). Option pricing under regime-switching jump–diffusion models. Journal of Computational and Applied Mathematics 256: 152-167. 10.1016/j.cam.2013.07.046

- [7] Das, M. K., Goswami, A. and Rana, N.(2018). Risk sensitive portfolio optimization in a jump diffusion model with regimes. SIAM Journal on Control and Optimization 56(2): 1550-1576. 10.1137/17M1121809

- [8] Das, M. K., Goswami, A. N., and Rajani, S. (2021). Inference of binary regime models with jump discontinuities. Preprint. arXiv:1910.10606

- [9] Elliott, R. J., Siu, T. K., Chan, L. and Lau, J. W. (2007). Pricing options under a generalized Markov-modulated jump-diffusion model. Stochastic Analysis and Applications 25(4): 821-843. 10.1080/07362990701420118

- [10] Guo, X. (2001). Information and option pricings. Quantitative Finance 1: 38–44. 10.1080/713665550

- [11] Jobert, A. and Rogers, L. C. G. (2006). Option pricing with Markov-modulated dynamics. SIAM Journal on Control and Optimization 44(6): 2063–2078. 10.1137/050623279

- [12] Kou, S. G. and Wang, H. (2004). Option pricing under a Double Exponential Jump Diffusion Model. Management Science 50(9): 1178-1192. 10.1287/mnsc.1030.0163

- [13] Mandelbrot, B. (1963). The variation of certain speculative prices. The Journal of Business 36(4): 394–419. 10.1086/294632

- [14] Mandelbrot, B. and Taylor, H. M. (1967). On the distribution of stock price differences. Operations Research 15(6): 1057–1062. 10.1287/opre.15.6.1057

- [15] McLachlan, G.J. and Krishnan, T. (2007). The EM Algorithm and Extensions. Wiley, New York. 10.1002/9780470191613

- [16] Merton, R.C. (1976). Option pricing when underlying stock returns are discontinuous. J. Financial Economics 3(1-2): 125–144. 10.1016/0304-405X(76)90022-2

- [17] Nielsen, S.F. (2000). The Stochastic EM Algorithm: Estimation and Asymptotic Results. Bernoulli. 6(3): 457-489. 132.248.181.19

- [18] Tanner, M.A. (1996). Tools for Statistical Inference: Methods for the Exploration of Posterior Distributions and Likelihood Functions. Springer-Verlag.

- [19] Guzman Solis, C. (2018). Algoritmo EM: Implementación y Aplicaciones. Facultad de Ciencias UNAM.