Joint modelling of longitudinal and time-to-event data applied to group sequential clinical trials

Abstract

Often in Phase 3 clinical trials measuring a long-term time-to-event endpoint, such as overall survival or progression-free survival, investigators also collect repeated measures on biomarkers which may be predictive of the primary endpoint. Although these data may not be leveraged directly to support early stopping decisions, can we make greater use of these data to increase efficiency and improve interim decision making? We present a joint model for longitudinal and time-to-event data and a method which establishes the distribution of successive estimates of parameters in the joint model across interim analyses. With this in place, we can use the estimates to define both efficacy and futility stopping rules. Using simulation, we evaluate the benefits of incorporating biomarker information and the affects on interim decision making.

Keywords

Efficient designs, group sequential, joint modelling, longitudinal data, time-to-event data.

1 Introduction

Interest in joint modelling is motivated by clinical trials where the biomarker is predictive of a time-to-event (TTE) outcome. Overall survival and progression-free survival are examples of TTE endpoints. For example, Goldman et al. (1996) use CD4 lymphocyte cell counts as a surrogate endpoint for survival in a clinical trial comparing the efficacy and safety of two antiviral drugs for HIV-infected patients. Taylor et al. (2013) use joint models to predict survival times of patients with prostate cancer based on prostate specific antigen (PSA) levels measured by blood tests at multiple hospital visits.

To date, most group sequential designs for survival trials focus on a single primary endpoint. Designs which leverage repeated measurements on continuous or binary endpoints have been reported such as those by Galbraith and Marschner (2003) and this work extends this idea to survival trials with repeated measurements on a predictive biomarker. We shall focus on monitoring randomised control trials so that patients are randomised at baseline to receive either a novel treatment or control and the objective is to test for superioirity of the treatment versus control. Hence, let denote the treatment effect in a statistical model and let be the true value of , then we shall test the null hypothesis

| (1) |

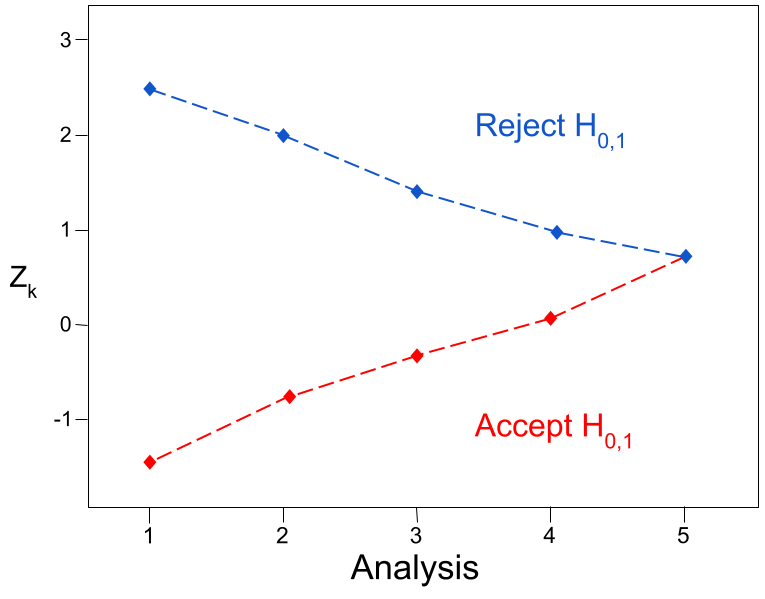

In the group sequential setting with a total of analyses, we shall test at analys by defining treatment effect estimates information levels and standardised statistics given by for The aim will then be to determine the upper boudary constants and lower boundary constants for the group sequential test as in Figure 1. These boundaries are calculated to ensure such that the Type 1 error rate is and power is when . In particular, we shall use the error spending test, also known as Gordon Lan and DeMets (1983), to calculate the boundary points.

We shall develop methods for designing and analysing a group sequential trial based on a joint model for longitudinal and TTE data. We may believe that a trend in the trajectory of the biomarker is predictive of the TTE outcome, and we would like to know whether these additional longitudinal data can be used to inform early stopping decisions. Suppose that biomarker observations are available but have not been used in the analysis. We shall assess the change in efficiency of the trial when these observations are included in the analysis. We shall focus on efficiency measured in terms of the number of patients that need be recruited to achieve a certain power, and we and show that, in some scenarios, the trial using the longitudinal data is up to 1.7 times as efficient as the trial which discards the longitudinal data.

2 Joint modelling

2.1 Joint model

The joint model that we consider is given in Equation (2) by Tsiatis and Davidian (2001). We shall refer to the authors as TD for short. There are two processes in this model which represent the survival and longitudinal parts separately, and these processes are linked through the hazard rate of the survival process. First we consider the longitudinal data. Suppose that is the true value of the biomarker at time for subject and that is the observed value of the biomarker at time for patient . Then the longitudinal model takes the form

| (2) | ||||

| (3) |

where is a vector of patient specific random effects and is the measurement error. In general, the vector can have dimension and the function need not be constrained to a linear function of We consider a random effects model where each is a random variable with density function The measurement errors are assumed to be independent and if the biomarker for patient is measured at times , then and and are independent for For now, we shall assume that is known and we later describe how can be estimated.

The model for the survival endpoint is a Cox proportional hazards model in which the underlying trajectory acts as a time-varying covariate with coefficient . Let be an indicator function that patient receives the experimental treatment and let be the corresponding treatment effect. Then the hazard function is given by

| (4) |

where is the baseline hazard function. In general, may be a column vector of coefficients and is the corresponding coefficient vector of length . In this model, is the parameter that determines the correlation between the longitudinal data and the TTE endpoint. We show in Section 4 that if then the investigator may pay a small penalty for having tried to leverage the biomarker data. However, if , then there is a large benefit from fitting this joint model to the data. Together, Equations (2), (3) and (4) define the joint model.

2.2 Conditional Score

In the fixed sample setting, TD present the “conditional score" method for fitting the joint model to the data. The method adapts the general theoretical work by Stefanski and Carroll (1987) who find unbiased score functions by conditioning on certain parameter-depedent sufficient statistics. This is a desireable method because the analysis is semi-parametric so that there are no distributional assumptions required for the random effects. Further, the authors show that the parameter estimates are normally distributed and unbiased. We shall now extend the fixed sample theory for the joint model to group sequential trials. To perform a group sequential trial with analyses, we need to know the joint distribution of the sequence of treatment effect estimates that will be obtained at analyses To determine this distribution, we shall define group sequential versions of all objects included in the single-stage conditional score, which are calculated using data obtained at that analysis. Equivalent definitions of TD’s single-stage conditional score, and associated functions, can be found by setting

The conditional score methodology builds upon the theory of counting processes. In the general definition, a counting process is a step-function increasing in integer increments and the survival counting process is a step function jumping from 0 to 1 at the failure time for an uncensored observation.

The censoring mechanism is used to keep patients in the at-risk set who have yet to experience an event. For patient with time-to-failure random variable , let be the time-to-censoring random variable at analysis . This censoring event includes “end of study" censoring for the total follow-up time of patient at analysis , then at analysis the event time random variable is The observed event time at analysis is and the observed censoring indicator is In the conditional score approach, to be included in the at-risk set at time the patient must have at least two longitudinal observations to fit the longitudinal regression model. The at-risk process at analysis is an indicator for not yet observing the event, not yet censored, or not having enough longitudinal observations. Let be the time of the second longitudinal observation for patient , then at analysis , the at-risk process and counting process for the joint model are

The function

presents us with useful notation: for any function or stochastic process the stochastic integral

| (5) |

is evaluated at the place where jumps from 0 to 1 if and , and 0 otherwise.

By analogy to survival analysis, we seek a compensated counting process with expectation zero. This property leads us to define an estimating equation from which we can obtain treatment effect estimates that are asymptotically normally distributed by Section 5.3 by Van der Vaart (2000). In the usual survival analysis setting, we can calculate the compensated counting process by subtracting the intensity process from the counting process itself. In the joint modelling setting, this is not as simple because the randomness of the nuisance parameters mean that the intensity process is unpredictable. To overcome this, TD introduce a “conditional intensity process" which is conditional on a certain “sufficient statistic". The origins of the conditional intensity process and sufficient statistic are not crucial for our purpose. What we actually use are the definitions and properties that are derived from these. In what follows, we shall present TD’s definitions of the single-stage conditional intensity process, sufficient statistic and compensated counting process and we extend these to the group sequential versions. We shall then show that the group sequential compensated counting process has expectation zero.

For patient , let be set of all time points for measurements of the biomarker, up to and including time . Let be the ordinary least squares estimate of for patient based on the set of measurements taken at times . That is, calculate and based on measurements taken at times , then . As we pass time a new observation is generated and the formula for is updated for larger values of . This seems strange since at an early time point, where , we use data in the calculation of even though there may be more data available at time points . However, this is necessary for the martingale property to hold in later results. Suppose that is the variance of the estimator at time . TD define the sufficient statistic to be the function

which is defined for all for patient . The corresponding conditional intensity process and compensated counting process are defined by

| (6) | ||||

| (7) | ||||

We show below that this compensated counting process has expectation zero conditional on and use this result to obtain the asymptotic distribution of some parameter estimates in the joint model. Specifically, we will determine the distribution of the estimates and which are unbiased estimates, at analysis , of and respectively.

Lemma 1.

The function has expectation zero conditional on the sufficient statistic, that is

Proof.

See Tsiatis and Davidian (2001). ∎

TD present the fixed sample conditional score in their Equation (6). We present some functions that are needed to define the group sequential conditional score at analysis and the derivate of such an object with respect to parameters and . Let

be a vector and matrix respectively. Now, for the following functions, we drop the dependency of all functions on the parameters and Then the functions of interest are

| (12) | ||||||

| (17) | ||||||

These functions are analogous to to those in Jennison and Turnbull (1997) for survival data. In the simple survival model, we have that and where is the vector of parameters in the hazard function of the simple survival model. In a similar manner, the superscripts and refer to the order of the differentiation for certain functions which we explain further in Section 2.3. The function has the interpretation of the expectation of the vector at analysis weighted by the conditional intensity process. Let be the maximum follow-up time at analysis , then the conditional score for analysis is

| (18) |

2.3 Differentiation of the conditional score

Another object of importance is the first derivative of the conditional score function, Equation (18), with respect to parameters and This matrix plays a key role in the definition of the covariance matrix for the estimates and and has a likeness to the Fisher information matrix which is the derivative of the score statistic for general statistical models. TD comment that the variance matrix can be found, however they do not present an equation for such an object. Details for the following calculation can be found in the supplementary materials. The first derivative the conditional score of Equation (18) with respect to and is

| (19) |

2.4 Asymptotic theory for parameter estimates and in the joint model

We shall now prove that the estimates are asymptotically multivariate normally distributed and we shall derive an explicit form for the covariance matrix of this vector of parameters. In what follows, we shall determine the limiting distribution as For clarity, we denote the objects and as dependent on .

Theorem 1.

Suppose that and are the true values of the parameters and respectively. For each , let and be the values of and which are the solution to the equation and suppose that Conditions 2 hold. Then the vector converges in distribution to a multivariate Gaussian random variable, specifically

where

| (20) |

and the matrices and are defined by

| (21) | ||||

| (22) |

Proof.

We begin this proof by considering the set of stacked equations

| (23) |

and we shall show that these equations define a multidimensional estimating equation. That is, for each , the function has expectation zero. The arguments given by TD about asymptotic normality in the fixed sample case apply for each . We present some of these arguments which are useful for the derivation of the covariance matrix in the group sequential setting. We shall write as

| (24) | ||||

| (25) |

By the same argument as TD, times Expression (25) converges in probability to zero in a neighbourhood of and we deduce that the behaviour of the estimates and will be dictated by Expression (24). Then we have that the expectation of Expression (24) is

| (26) |

for each . Therefore combined with the fact that Expression (25) converges in probability to zero, we have that Equation (23) defines a multidimensional estimating equation. Therefore, the estimates for each are asymptotically multivariate normal and unbiased for parameters and by Section 5.3 by Van der Vaart (2000). It remains to determine the covariance matrix.

In the general setting for statistical models, the sandwich estimator can be used to robustly estimate the variance matrix for estimates that are the solutions to estimating equations as in Section 2.6 by Wakefield (2013). The sandwich estimator requires deriving and where is an estimating function for parameter The similarity here is with matrices and in Equations (21) and (22) which are the sequential versions of such objects for the conditional score. Wakefield (2013) prove the asymptotic normality of estimates obtained using estimating equations and the asymptotic convergence of the sandwich estimator. The proof by Wakefield (2013) applies to scalar estimates and one-dimensional estimating functions so we shall extend this proof to derive the covariance matrix for the vector of parameters in the joint model as oppose to the scalar sandwich variance.

Following Wakefield (2013), we apply the standard Taylor expansion results to each row of Equation (23) and aggregate the results. Details of this calculation are found in the supplementary materials. Let be the block diagonal matrix whose diagonal matrix is the matrix Then we obtain

where lies on the line segment between and .

Suppose that we could show that

| (27) | ||||

| (28) |

then by an application of Slutsky’s Theorem, we have the desired result.

A simple application of the triangle inequality proves that condition (27) holds. The proof of convergence in probability closely follows the standard results for survival data seen in Theorem VII.2.2 by Andersen and Gill (1982) and the details of this step are found in the supplementary materials.

To prove condition (28) holds, first note that Expression (24) is a sum over independent and identically distributed terms. Then the multivariate Central Limit Theorem can be applied to the vector to establish asymptotic normality. It then remains to show that for

We now follow a similar structure to the partial likelihood function for survival data given by Jennison and Turnbull (1997) and we create a new counting process that allows the conditional score statistic to be written as the sum of distinct increments. This counting process is defined by for .The corresponding compensated counting process is therefore given by

for and The event for patient can only occur in one interval, and therefore we have . For consistency with Andersen and Gill (1982) and Jennison and Turnbull (1997), let Expression (24) be denoted by . Then by the definition of the difference in counting process, we have

where

and has expectation zero by a simple manipulation of Equation (26).

The main result, with details given in the supplementary materials, is as follows

| (29) |

To complete the proof, it remains to show that Equation (29) converges in probability to and we shall do so by using the definitions of the objects and for and and given in Appendix 1. We are assuming that these limits exist by Conditions 2 and we shall exploit the relationships between these terms. This working is exactly the same as for standard survival data given by Andersen and Gill (1982), with the details given in the supplementary materials, and we see that

By the argument that the behaviour of the estimates and is dictated by Expression (24), we have

which is the result. ∎

Similar to the fixed sample case, we have assumed that is known in the derivation of the distribution of and This is not generally the case but by arguments in Carroll et al. (2006) Section A.3.3, we can find a consistent estimate to replace with in the group sequential conditional score function. At analysis this estimate is given by

| (30) |

where is the residual sum of squares for the least squares fit to all observations for patient available at analysis .

2.5 A group sequential trial design based on the conditional score analysis

We shall use Theorem 1 to create a group sequential test based on the joint model. Let and be the true values of the parameters and respectively. Using the group sequential conditional score method, let be the values of the parameters and such that where the conditional score function is calculated using Equation (18). Further, let be the estimate for given in Equation (30). By Theorem 1, for each , the marginal distribution of the parameter is

where

and the matrices and are defined by Equations (21)–(22). Note that the subscript notation in the covariance matrix represents that the parameter is the second parameter in the vector . In the more general case where is a vector of dimension including other covariates appart from treatment indicator, then the information would be indexed by the corresponding dimension of the vector which relates to the treatment effect. The matrices and are estimated using

| (31) | ||||

| (32) |

The information matrix at analysis of the group sequential trial is given by

Further, a standardised test statistic at analysis is given by

3 Designing group sequential trials when the canonical joint distribution does not hold

3.1 Simulation evidence that the trial is conservative with respect to type 1 error rate

We discuss the implications for a group sequential test when the sequence of test statistics does not follow the usual canonical joint distribution and we shall show that in some scenarios, it is appropriate to make this assumption anyway and proceed with the trial as though the canonical joint distribution holds anyway. Let be the sequence of treatment effect estimates in a group sequential trial from data available at analyses respectively and are the associated observed information levels. The “canonical joint distribution" for the sequence of estimates is such that

-

1.

is multivariate normal

-

2.

-

3.

Supposing that the canonical joint distribution holds for the sequence of treatment effect estimates in the joint model, then the library of standard group sequential designs, such as Pocock (1977) and O’Brien and Fleming (1979), could be directly applied in our setting

In Section 2 we saw that asymptotically the sequence of treatment effect estimates in a group sequential trial obtained from the joint model is multivariate normally distributed. Further, each of these estimates is asymptotically unbiased. The first two conditions for the canonical distribution of the sequence of test statistics are satisfied. However, for the joint model, we have shown that

| (33) |

and

| (34) |

This implies that the third condition for the canonical joint distribution, which is the Markov property, is not satisfied. In this section, we discuss the implications of performing a group sequential trial when the assumption of a canonical joint distribution fails. We first show that there are some small differences between the matrices and the identity matrix and describe why this difference is important. Then, we discuss some alternative methods which aim to correct for this violation of the Markov property. In method 1, the trial is performed acting as though the canonical joint distribution holds, and we present some theory that this method controls the type 1 error rate conservatively.

The theory presented is for the case when a non-binding futility boundary is used which is where stopping for futility at an interim analysis is not mandatory as described in GUIDANCE (2018). FDA guidance recommends using non-binding futility rules because if binding rules are employed and not followed, then type 1 error rates are inflated. The calculation of the type 1 error rate therefore only depends on the upper boundary which is depicted in Figure 1.

The problem of not obtaining the canonical joint distribution is not unique to the conditional score method and the proof that this assumption holds is not always trivial. Slud and Wei (1982) design a group sequential test which uses the modified-Wilcoxon statistic for two-sample survival data. The authors show that the increments in test statistics are correlated and their alternative proposed method has a similar structure to our method 2. Then, Gu and Ying (1993) present a score process for the analysis of regression data under general right censorship and they implement the repeated significance method of Slud and Wei (1982) for the sequential analysis of such data. Further, Cook and Lawless (1996) discuss a modification of the error spending approach (also known as Gordon Lan and DeMets (1983)) for sequences of treatment effect estimates that do not have the independent increments structure.

If the relationship holds for each then

and the third condition holds. Therefore, we shall measure the magnitude of the violation by considering the matrix and to what extent it differs from the identity matrix. By definition, the variance of the estimate is found in the bottom right entry of the matrix and hence, the bottom row of is of interest here.

We can find estimates and from simulated data. We have done this using a large sample size of n=4800 patients to reduce noise in these estimates. This calculation is computationally expensive and takes roughly two hours to compute for this value of . This is appropriate because, although both matrices depend on the sample size , they can each be written in the form and for some functions and Therefore, in the formula , the value of cancels out, and we are left with a function that converges in distribution to as Further, to reduce simulation error, the true values of and are used in this calculation, which is appropriate because of consistency of the estimates and .

Table 1 shows the matrix for and different values of and We have chosen to investigate the properties of this matrix at the first analysis because we see empirically that the majority of problems occur at early interim analyses. We simulated a data set with parameter values and

-

•

Parameter values and in the joint model simulated with 4800 patients.

The matrices and are each of dimension The function is such that , and hence by Equations (31) and (32) it can be shown that and Further simple algebraic manipulation gives and exactly, which is shown in Table 1. The fact that is a long way from for and is therefore not a problem. As increases, the absolute value of increases, but the value of has a small impact on the value of Thus, we may expect large values of to affect the achieved type 1 error rate.

3.2 Method 1 - canonical joint distribution assumed

We consider alternative methods for creating a group sequential trial when the canonical joint distribution does not hold. In the first method, we construct the group sequential test by estimating from the data and supposing for are as specified in the canonical joint distribution. We shall prove that we have type 1 error rate less than and we also show, through simulation, that this method performs satisfactorily in practice with error rates diverging minimally from planned significance and power.

For this proof, we consider the case where and the futility boundary is non-binding. We present a sketch proof in the supplementary materials for the case and we believe that the results generalise for cases To prove that the type 1 error rates are conservative, we shall compare the probabilities of crossing the boundaries of a group sequential trial for two sequences of treatment effect estimates; one where the canonical joint distribution does not hold and one where this assumption does hold. For a group sequential trial with , suppose that are the sequence of treatment effect estimates that are calculated using the conditional score method. Let the true variance-covariance matrix for this sequence of estimates be . Proceeding using method 1, we let the information levels be calculated as and the statistic is given by for Under we have

| (35) |

where the correlation parameter is given by

| (36) |

Suppose instead, that we have a different sequence of treatment effect estimates with distribution given below. The values of and are the same as in (35) and using the same information levels given by , we define the standardised statistics for The joint distribution of the sequence and the distribution of the statistics are given by

| (37) |

with correlation parameter

| (38) |

This sequence of treatment effect estimates therefore has the canonical joint distribution and has the canonical joint distribution for a sequence of -statistics, with information levels for .

The upper boundary points are calculated under the assumption that the canonical joint distribution holds so as to give a group sequential test with the correct type 1 error rate . Hence, we have that

We consider the probability of rejecting when we apply this boundary to the sequence We aim to prove that

| (39) |

The following conditions are needed for the proof that type 1 error rate is conservative.

Conditions 1.

-

1.

The upper boundary of a group sequential trial, on the scale, is such that

-

2.

We have

Condition 1 of Conditions 1 holds under common error spending functions with increasing information sequences, which are most often used in practice. Condition 2 of Conditions 1 should be checked by simulation before proceeding with the analysis. To do so, the investigator would choose sensible values for all the parameters in the joint model, simulate a large dataset of patients using these parameter values, and calculate an estimate for the variance-covariance matrix for the sequence of estimates We have found that calculations for various examples has always lead to condition 2 being satisfied. Further, the scenarios that we have checked span a 3-dimensional grid of and values each ranging from small to large and hence, we believe that the scenarios we have checked span a suitable range of the parameter values. In the rare event that this condition does not hold, a solution is to employ method 2, which will be described later. It can also be seen by simple algebraic manipulation that condition 2 implies

The following theorem shows that Equation (39) holds.

Theorem 2.

Let be the standardised statistics of a group sequential trial with distribution given by (35) and let be the statistics with distribution given by (37). Let be the planned type 1 error rate and suppose that are the upper boundary points on the -scale such that

Suppose that Conditions 1 hold. Then the Type 1 error rate when applying the boundary for to is

Proof.

The problem is equivalent to proving that

and by another representation for the above probabilities, we aim to show that

Under , the marginal distributions of and are equivalent and are all random variables and hence the probabilities are such that for each Therefore, the problem is reduced to showing that

| (40) |

when

In the below calculations, we appeal to the fact that for two random variables which are bivariate normally distributed, the conditional distribution of one normal random variable on the other normal random variable is also normal. Specifically, we have that . Let and denote the probability density function and cumulative distribution function of a standard normal random variable respectively, then the probability on the left hand side in Equation (40) is

The corresponding calculation where and replace and yields the following

and since is strictly increasing, it suffices to show that whenever , then

| (41) |

We have by assumption that Further note that by definition and The following shows a simple algebraic manipulation of this inequality, which gives

Table 2 show estimates of type 1 error rate. This was by simulating data sets, each with a sample size This sample size was chosen because it gives power 0.9 for and for other parameter values, the power was close to 0.9. For each data set, we calculate the estimates and estimates of the covariance matrices using estimates given by Equations (31) and (32). The boundary points and are then calculated under the assumption that the canonical joint distribution holds and the type 1 error rate is calculated as the proportion of replicates that reject the null hypothesis. This simulation study is computationally expensive and with replicates, there is noise in the simulation results. Taking this into account, the simulation results support the relevance of asymptotic theory since all empirical type 1 error rates are within 2 standard deviations of 0.025.

| Method | Type 1 error | Percentage of time method fails | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.022 | 0.022 | 0.022 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 1 | 0.024 | 0.025 | 0.026 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 1 | 0.023 | 0.024 | 0.023 | 0.025 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 1 | 0.023 | 0.028 | 0.026 | 0.024 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 2 | 0.022 | 0.022 | 0.022 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 2 | 0.024 | 0.025 | 0.026 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 2 | 0.023 | 0.024 | 0.023 | 0.025 | 0.040 | 0.100 | 0.120 | 0.060 | ||

| 2 | 0.022 | 0.028 | 0.026 | 0.029 | 49.140 | 37.360 | 35.950 | 40.420 | ||

| 3 | 0.028 | 0.024 | 0.023 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 3 | 0.028 | 0.026 | 0.027 | 0.023 | 0.000 | 0.000 | 0.000 | 0.000 | ||

| 3 | 0.029 | 0.025 | 0.023 | 0.026 | 0.140 | 0.050 | 0.060 | 0.310 | ||

| 3 | 0.024 | 0.028 | 0.027 | 0.029 | 1.930 | 1.950 | 1.840 | 1.850 | ||

-

•

Calculated using a simulation study with 365 patients and replicates.

-

•

Standard error is 0.0016 when the method does not fail.

3.3 Method 2 - Use the complete structure of the covariance matrix

The second method for dealing with estimates from the joint model does not rely on the canonical joint distribution assumption. Instead, the group sequential boundaries are calculated using the complete structure of the variance-covariance matrix for the sequence of treatment effect estimates across analyses. This differs from when the canonical joint distribution is assumed because in such a case, only the variances are required and the covariances are ignored. To calculate the boundary points of the group sequential test, we are required to calculate a dimensional integral over the joint probability distribution of the sequence of test statistics. This integration calculation can be performed numerically using the R package mvtnorm by Genz et al. (2020).

However, this method poses some practical difficulties. For example, during the conditional score method, the variance-covariance matrix in Equation (20) is estimated with error which can sometimes result in a non positive-definite estimate In such a case, the boundary calculations cannot be performed. Slud and Wei (1982) allude to a similar problem in their sequential analysis of modified-Wilcoxon scores for two-sample survival data. Table 2 shows the percentage of times that this problem occurs. We see that for extremely noisey longitudinal data with this problem occurs roughly 40% of the time and for we have the problem occurring infrequently. This is not a problem for small and in such a case, the type 1 error rates are as expected. In summary, this method makes no assumption about the covariance structure of the sequence of treatment effect estimates and therefore the type 1 error rate is preserved.

3.4 Method 3 - Create an asymptotically efficient estimate

For the final method, we follow the approach of Van Lancker et al. (2022) where a new estimator is created which reaches asymptotic efficiency as it is designed in such a way to minimise the variance. The efficient estimate at analysis is a linear combination of the original estimates at analyses up to and including . We choose the weights of the linear combination using a Lagrange multiplier method in such a way that the variance is minimised. Ou rmotivation for this method follows the simple result by Jennison and Turnbull (1997), that all asymptotically efficient estimators have the canonical joint distribution. Van Lancker et al. (2022) show that this new estimator has the correct canonical distribution, and hence the group sequential methods can be used without hesitation.

Similarly to method 2, there are some limitations to this method as it relies too heavily on accurately estimating the covariance matrix of the sequence of treatment effect estimates. Van Lancker et al. (2022) do not observe these issues since their results focus on simulations with sample sizes much larger than our chosen . In some cases, because the variance-covariance matrix is estimated with error, it is possible to choose the weights of the Lagrange multiplier in such a way that the new estimate has negative variance. Table 2 shows a similar pattern to method 2, that this numerical problem occurs when the variance of the longitudinal data is extreme so that , occurs infrequently for and no problems occur for small

Given that is very close to for , there is not a lot to be gained by the more complex methods 2 and 3. The calculations are sensitive to errors in estimates of and . In some cases, the errors in these calculations lead to these methods simply not working. This raises doubts about how well they work in less extreme cases. Despite these problems, methods 2 and 3 perform adequately in simulation studies. However, this does not change our view that method 1 is preferable.

4 Results

We aim to assess the efficiency gain when longitudinal data are included in the analysis compared to when this longitudinal data is available, yet ignored. In this case, we believe that our joint model is correctly specified and therefore, we shall simulate clinical trial data from the true joint model and analyse it in two separate ways. The first way is to fit the data to the joint model using the conditional score method to find a treatment effect estimate and the second way is to ignore the longitudinal data, fitting a Cox model to the survival data and find the maximum partial likelihood estimate of the treatment effect. We are interested in comparing the sample sizes required in each method to achieve the same power. A comparison of these sample sizes reflects the efficiency of the test incorporating the longitudinal data.

We shall simulate using the joint model in Equation (4). To fit the joint model to the data, we do not need to assume a distribution for the random effects, however we must specify this for simulation purposes and we shall simulate using the following

Unless otherwise stated, throughout the simulation studies, we shall use parameter values

| (42) |

These parameter values are based on the aids dataset in the R package JM by Rizopoulos (2010).

We shall test the one-sided hypothesis

Here the subscript notation represents that the parameter is from the "joint" model. We fit the joint model using the conditional score method to find a treatment effect estimate in order to perform this hypothesis test.

Our aim is to find the sample size, , required using the conditional score method to achieve Type 1 error rate when the true treatment effect is and power when . An estimate of the sample size will be calculated by simulation. The trial is designed with 2 years recruitment and 3 years follow-up and the group sequential trial has analyses at and months. When increasing the sample size, we do so by increasing the rate of recruitment so accrual and follow-up periods in the the trial design stay fixed. This is to ensure that differences in power are purely due to the sample size and not changes in the trial design as sample size increases.

The trial uses an error spending design given by Gordon Lan and DeMets (1983). That is, the boundary constants are chosen to satisfy

where the value of is calculated to ensure that the trial has power when as described by Jennison and Turnbull (2000).

Maximum sample sizes are given in Table 3. The first analysis, at 20 months, occurs just before the end of the recruitment period which is 2 years. Trials that terminate at the first interim analysis may recruit less than patients, however this occurs with very small probability. Hence, the expected sample size will be very close to the maximum sample size for each model and therefore the maximum sample size is a useful measure to compare methods. The sample size increases as increases. This reflects that noisy longitudinal data is associated with high variance or small information levels. Sample sizes are particularly high in each case where which has been chosen as an extreme value. Further, sample sizes appear to increase slightly with and decrease slightly with .

We now consider the analysis when the longitudinal data is ignored. We believe the joint model to be true and correct, however we shall fit the data to a Cox model. To do so, we shall simulate data from the joint model and then fit this data to a misspecified Cox proportional hazards model. The Cox model is given by:

| (43) |

For this clinical trial, we test the hypothesis

| (44) |

and we find a treatment effect estimate using the maximum partial likelihood method as in Jennison and Turnbull (1997).

Although this model is misspecified, type 1 error is not affected. This is because, under we have and there is no difference between treatment groups in overall survival. When fitting the Cox model to the data, the longitudinal data trajectory is reflected in the function so that we also have that Hence, is also true.

Let be the sample size such that we achieve type 1 error when and power when when we perform the hypothesis test in (44). Values of and are given in Table 3. The values of and for simulation are varied. Notice that does not change with since this plays no role in simulating survival times, and the longitudinal data, which is affected by , is ignored. As the value of increases, the sample size increases. This represents that as the longitudinal data has more weight in the survival hazard rate, ignoring the longitudinal data results in an increasingly inefficient clinical trial. When this represents the case where longitudinal data is available yet has no influence on the survival function. In this case, and it is more efficient to fit the data to the simple Cox model. We see that the value of increasess with . This is the variance amongst patients of the slopes of the longitudinal trajectories. This indicates that the simple Cox model is unable to account for large differences between individual patients.

To compare the sample sizes obtained using the joint model and the misspecified Cox model, we define “relative efficiency" to be Using this definition, when we interpret this as the joint model analysis being the more efficient model to use and similarly when the Cox model analysis is the more efficient analysis method.

Table 3 shows the relative efficiency results. We see that RE increases with , increases with and remains constant with apart from the case where which reflects extremely noisy data. Also, we see that when and which indicates that when the longitudinal data is not correlated with the survival endpoint and the longitudinal data is noisy, the simple Cox model is a slightly more efficient method for estimating the treatment effect. Apart from the case where , it is always more efficient to analyse the data using the joint modelling approach. Even when fitting the data to the simple Cox model for survival data is only marginally more efficient than fitting the data to the joint model. In the extreme case, 2.63 times as many patients are required to analyse the data using the Cox model as when the joint modelling framework is used.

| RE | RE | RE | RE | ||||||||||

| 363 | 363 | 1.00 | 421 | 365 | 1.16 | 528 | 364 | 1.45 | 607 | 365 | 1.67 | ||

| 363 | 364 | 1.00 | 421 | 365 | 1.16 | 528 | 365 | 1.45 | 607 | 369 | 1.65 | ||

| 363 | 364 | 1.00 | 421 | 364 | 1.16 | 528 | 365 | 1.45 | 607 | 375 | 1.62 | ||

| 363 | 373 | 0.97 | 421 | 374 | 1.13 | 528 | 420 | 1.26 | 607 | 522 | 1.16 | ||

| 351 | 362 | 0.97 | 371 | 363 | 1.02 | 401 | 367 | 1.09 | 439 | 357 | 1.23 | ||

| 363 | 364 | 1.00 | 421 | 365 | 1.16 | 528 | 365 | 1.45 | 607 | 369 | 1.65 | ||

| 366 | 365 | 1.00 | 462 | 378 | 1.22 | 720 | 391 | 1.84 | 990 | 421 | 2.35 | ||

| 380 | 372 | 1.02 | 501 | 404 | 1.24 | 804 | 416 | 1.93 | 1185 | 450 | 2.63 | ||

-

•

, is the correlation parameter between the longitudinal and survival endpoints, is the measurement error of the longitudinal data and is the variance of the random effects .

5 Conclusions

The conditional score method is used to find a treatment effect estimate in the joint model of longitudinal and time to event data and we have displayed new theoretical results for the distribution of the sequence of treatment effect estimates found using the conditional score method in a group sequential trial. Although the canonical joint distribution for the sequence does not hold, we show that it is sensible and practical to proceed assuming that the canonical joint distribution holds anyway. In particular, we have proven that by assuming the canonical joint distribution holds, and using a non-binding futility boundary, the trial is conservative with respect to type 1 error rates. Finally, using simulation studies we have seen that the deviations from planned type 1 error are minimal. Other benefits of using the conditional score method are that no distributional assumptions are required for the random effects of the longitudinal data and the analysis is semi-parametric so that it is not necessary to estimate the baseline hazard function.

We have shown that by including the longitudinal data, compared to the case where the longitudinal data is observed but left out of the analysis, we can greatly improve the efficiency of the trial with respect to sample size. In some cases, 2.63 times as many patients are required to achieve the same power in the analysis where the longitudinal data is left out.

Appendix 1

Conditions for the asymptotic theory of parameter estimates

To ensure the existence of the asymptotic covariance matrix , we require the probabilistic limits of and given by (17) to exist. The limits are defined through the following conditions.

Conditions 2.

-

1.

There exist neighbourhoods of and of and for each there are functions , , , and defined on such that

-

2.

Each and is a continuous function of and uniformly in and bounded on .

-

3.

For each and are bounded away from zero on .

It is clear that the probabilistic limits of , of and of exist and can expressed in terms of and for and these are

Software

All statistical computing and analyses were performed using the software environment R version 4.0.2. Programming code for sample size calculations, is available at https://github.com/abigailburdon/Conditional-score-GST.

Acknowledgements

This research was funded by the Engineering and Physical Sciences Research Council.

References

- Andersen and Gill [1982] Per Kragh Andersen and Richard David Gill. Cox’s regression model for counting processes: a large sample study. The Annals of Statistics, pages 1100–1120, 1982.

- Carroll et al. [2006] Raymond J Carroll, David Ruppert, Ciprian M Crainiceanu, and Leonard A Stefanski. Measurement Error in Nonlinear Models: A Modern Perspective. London: Chapman and Hall/CRC, 2006.

- Cook and Lawless [1996] Richard J Cook and Jerald F Lawless. Interim monitoring of longitudinal comparative studies with recurrent event responses. Biometrics, pages 1311–1323, 1996.

- Galbraith and Marschner [2003] Sally Galbraith and Ian C Marschner. Interim analysis of continuous long-term endpoints in clinical trials with longitudinal outcomes. Statistics in Medicine, 22(11):1787–1805, 2003.

- Genz et al. [2020] Alan Genz, Frank Bretz, Tetsuhisa Miwa, Xuefei Mi, Friedrich Leisch, Fabian Scheipl, Bjoern Bornkamp, Martin Maechler, Torsten Hothorn, and Maintainer Torsten Hothorn. Package ‘mvtnorm’. Journal of Computational and Graphical Statistics, 11:950–971, 2020.

- Goldman et al. [1996] Anne I Goldman, Bradley P Carlin, Lawrence R Crane, Cynthia Launer, Joyce A Korvick, Lawrence Deyton, and Donald I Abrams. Response of CD4 lymphocytes and clinical consequences of treatment using ddI or ddC in patients with advanced HIV infection. Journal of Acquired Immune Deficiency Syndromes, 11(2):161–169, 1996.

- Gordon Lan and DeMets [1983] KK Gordon Lan and David L DeMets. Discrete sequential boundaries for clinical trials. Biometrika, 70(3):659–663, 1983.

- Gu and Ying [1993] Minggao Gu and Zhiliang Ying. Sequential analysis for censored regression data. Journal of the American Statistical Association, 88(423):890–898, 1993.

- GUIDANCE [2018] DRAFT GUIDANCE. Adaptive designs for clinical trials of drugs and biologics. Center for Biologics Evaluation and Research (CBER), 2018.

- Jennison and Turnbull [1997] Christopher Jennison and Bruce W Turnbull. Group-sequential analysis incorporating covariate information. Journal of the American Statistical Association, 92(440):1330–1341, 1997.

- Jennison and Turnbull [2000] Christopher Jennison and Bruce W Turnbull. Group Sequential Methods with Applications to Clinical Trials. London: Chapman and Hall/CRC, 2000.

- O’Brien and Fleming [1979] Peter C O’Brien and Thomas R Fleming. A multiple testing procedure for clinical trials. Biometrics, pages 549–556, 1979.

- Pocock [1977] Stuart J Pocock. Group sequential methods in the design and analysis of clinical trials. Biometrika, 64(2):191–199, 1977.

- Rizopoulos [2010] Dimitris Rizopoulos. Jm: An R package for the joint modelling of longitudinal and time-to-event data. Journal of Statistical Software, 35(9):1–33, 2010.

- Slud and Wei [1982] Eric Slud and LJ Wei. Two-sample repeated significance tests based on the modified wilcoxon statistic. Journal of the American Statistical Association, 77(380):862–868, 1982.

- Stefanski and Carroll [1987] Leonard A Stefanski and Raymond J Carroll. Conditional scores and optimal scores for generalized linear measurement-error models. Biometrika, 74(4):703–716, 1987.

- Taylor et al. [2013] Jeremy MG Taylor, Yongseok Park, Donna P Ankerst, Cecile Proust-Lima, Scott Williams, Larry Kestin, Kyoungwha Bae, Tom Pickles, and Howard Sandler. Real-time individual predictions of prostate cancer recurrence using joint models. Biometrics, 69(1):206–213, 2013.

- Tsiatis and Davidian [2001] Anastasios A Tsiatis and Marie Davidian. A semiparametric estimator for the proportional hazards model with longitudinal covariates measured with error. Biometrika, 88(2):447–458, 2001.

- Van der Vaart [2000] Aad W Van der Vaart. Asymptotic Statistics, volume 3. Cambridge: University Press, 2000.

- Van Lancker et al. [2022] Kelly Van Lancker, Joshua Betz, and Michael Rosenblum. Combining covariate adjustment with group sequential and information adaptive designs to improve randomized trial efficiency. arXiv preprint arXiv:2201.12921, 2022.

- Wakefield [2013] Jon Wakefield. Bayesian and Frequentist Regression Methods. Berlin: Springer Science & Business Media, 2013.