Simultaneous Best Subset Selection and Dimension Reduction via Primal-Dual Iterations

Abstract

Sparse reduced rank regression is an essential statistical learning method. In the contemporary literature, estimation is typically formulated as a nonconvex optimization that often yields to a local optimum in numerical computation. Yet, their theoretical analysis is always centered on the global optimum, resulting in a discrepancy between the statistical guarantee and the numerical computation. In this research, we offer a new algorithm to address the problem and establish an almost optimal rate for the algorithmic solution. We also demonstrate that the algorithm achieves the estimation with a polynomial number of iterations. In addition, we present a generalized information criterion to simultaneously ensure the consistency of support set recovery and rank estimation. Under the proposed criterion, we show that our algorithm can achieve the oracle reduced rank estimation with a significant probability. The numerical studies and an application in the ovarian cancer genetic data demonstrate the effectiveness and scalability of our approach.

Keywords: High-dimensional data; Multivariate response; Primal-dual active selection algorithm; Reduced rank regression; Variable selection.

1 Introduction

Sparse reduced rank regression is an indispensable tool for many contemporary applications, such as bi-clustering (Lee et al., 2010; Zhong and Huang, 2022), microeconomics (Uematsu and Tanaka, 2019), pattern recognition (Zheng, 2014) and others. For the estimate of underlying coefficients, the classical framework for the pursuit of the sparse reduced rank regression has been “optimization + regularization,” and many approaches using the regularization technique have been proposed in recent years, including Chen and Huang (2012); Bunea et al. (2012); She (2017); Uematsu et al. (2019); Ma et al. (2020). In the aforementioned works, estimation is characterized as a nonconvex optimization subject to sparsity and low-rank constraints. Scientists then establish a good statistical convergence rate, sometimes even the minimax optimal rate, by concentrating on the optimization’s global optimum.

Unfortunately, the nonconvexity that causes the gap between the statistical guarantee and the numerical computation means that the numerical methods in the existing literature usually only achieve a local optimum. There is some published work that makes an attempt to close this gap by imposing the KKT-type condition and the sparsity assumption on the numerical solution (see, for example, Zhang and Zhang (2012); Fan and Lv (2014); Chen et al. (2022)). The question of whether the obtained numerical solution holds up to these assumptions remains open. It’s also not easy to tell if the solution actually matches the goal in their theory, as there’s more than one local optimum. As such, it only rephrases the original question and does nothing to bridge the theoretical gap that the numerical algorithm suffers from. Although the sparse reduced rank regression has been numerically solved, the theoretical guarantee for these solutions remains unknown.

The computational complexity of massive data sets is another obstacle. In order to address the original optimization problem, researchers break it down into a series of unit-rank estimations using regularization (see, for example, Chen et al. (2012); Ahn et al. (2015); Mishra et al. (2017)) and then use alternating coordinate descent to find solutions. He et al. (2018) and Chen et al. (2022) have recently argued that alternating coordinate descent is still slow when there are a lot of predictors. Therefore, they employ the stagewise algorithm to decompose sparse matrices. However, the stagewise approach mainly relies on an empirical choice of step size. A slow computation will arise from too small a step size, whereas a reckless estimation will follow from too large a step size. Importantly, the iteration complexity for achieving the statistical convergence rate is unanswered by either the alternating coordinate descent or the stagewise algorithm. Concerning large-scale computing, this is an extremely important issue.

Taking inspiration from the primal-dual algorithm, we offer a new approach to estimating the parameters in sparse reduced rank regressions that fixes the aforementioned problems. In order to find the best subset of covariates, the suggested method iteratively updates the primal and dual variables. Every iteration of the algorithm, which can be interpreted as a local second-order algorithm, implements a typical reduced rank estimation based on the given covariates. Consequently, it benefits from a rapid computation without having to decide on a suitable step size in advance. Additionally, the statistical guarantee for the numerical solution is established. Our contributions are multifold. First, the nearly minimax optimal rate for the algorithmic solution is determined, bridging the gap between theoretical analysis and numerical computation. Second, our approach can produce the nearly optimal estimation in a polynomial iteration complexity, which permits a fast computing in practice. Third, a generalized information criteria (GIC) is introduced to simultaneously ensure the consistency of support set recovery and rank estimation. Last but not least, owing to the proposed GIC, the algorithmic solution achieves the oracle reduced rank estimation with a significant probability.

The remainder of the paper is structured as follows: The proposed method, together with its justification and derivatives, are described in Section 2. The theoretical results for the proposed method are provided in Section 3. Numerical studies are presented in Section 4 to demonstrate the advantages of the proposed method. In Section 5, we show how this can be used in genetics. Future work is discussed in Section 6. All technical proofs are provided in the appendix.

Notations. We use the boldface uppercase or lowercase to denote the matrix or column vector, respectively. For an arbitrary vector , define the norm with . For an arbitrary matrix , we denote the th row of by , and the th column of by . That is . Throughout the paper, we use and to denote the Frobenius norm and the number of nonzero rows of , respectively. Moreover, denote the operator norm of by . For an arbitrary index set , is the submatrix consisting of the rows of indexed by . Similarly, is the submatrix consisting of the columns indexed by in the original matrix. In addition, denotes the cardinality of .

2 Methodology and Algorithm

2.1 Model setting

Denote the response vector and the covariate vector by and , respectively. We consider the reduced-rank regression model as follows,

where is the noise vector and is the coefficient matrix with . Assume that a random sample of i.i.d. observations is drawn from the above model, then we have

where , and denote the matrices of stacked response, covariate and noise vectors, respectively. We denote the th row and the th column of the coefficient matrix by and , respectively. Moreover, we assume the norm of the each column of is normalized to without loss of generality.

In this paper, we consider the row-sparsity structure and denote the number of the nonzero rows of by . Then let the index set of nonzero rows be

Our main target is to recover the row-sparse and low-rank coefficient matrix and its corresponding support set .

Formally, with the user-specified rank and sparsity , we consider the best subset selection problem in reduced-rank regression as follows

| (2.1) |

where the -norm constraint not only enables the variable selection but also reduces the bias in the estimation. Henceforth, we call the problem (2.1) as Multi-response Best Subset Selection (MrBeSS) problem and its minimum as MrBeSS estimator.

2.2 MrBeSS with fixed rank and sparsity level

We next consider the following optimization problem:

| (2.2) |

The two constraints are intertwined, making the optimization extremely nonconvex to solve. To address this issue, we disentangle these two restrictions through a reparameterization of , i.e., , with and satisfying . Then (2.2) can be rewritten as

| (2.3) |

Note that the solution to the optimization problem (2.3) is not unique. For example, suppose is a solution of (2.3), then is also a solution of (2.3), if there is an orthogonal matrix such that and . Nonetheless, the fact that assures that both solutions give the same estimation of .

Initialize and assume that we have an initial support set . Therefore, restricted in the , the optimization (2.3) is an ordinary reduced rank regression that has a closed form (Reinsel and Velu, 1998). It motivates us to update right singular vectors, where the -th column of is the -th eigenvector of

and the eigenvectors are listed in descending order by eigenvalues. Then with the given , the optimization (2.3) is simplified as

| (2.4) |

which is a typical multi-response regression. For the best subset selection of predictors, we consider the following primal-dual formulation

| (2.9) |

where and are submatrices of and , respectively, and they consist of rows indexed by corresponding support sets. Let and be the -th rows of and , respectively. With the given , the optimization (2.4) is reduced to a group Lasso, thereby, which is similar to Zhu et al. (2020). can be seen as a measure of the importance of the -th predictor, and is equal to the difference of the optimal value of the loss function in (2.4) when we add/knockout the -th covariate for the current support set. A more significant -th covariate is indicated by a bigger value of . But the proposed method includes the low rank restriction that distinguishes the problem from Zhu et al. (2020).

Based on the above formulation, we develop an algorithm to iteratively update the triple until the convergence and the outline of the proposed algorithm is presented in Algorithm 1. Here we need to specify an initial active set . A naive argument is to implement the screening for the rows of that selects the indices of top- rows in term of the norm, where is the top- right singular vectors of . In details, there is , where is the th column of and is the descending sort of with . That is equivalent to update the active set by the formula with the given and .

Input: response matrix , predictor matrix , rank and row sparsity .

Output: .

The existing methods, e.g. She (2017); Bunea et al. (2012); Chen and Huang (2012); Uematsu et al. (2019), usually formulate the sparse reduced rank regression as a nonconvex optimization by “loss function + regularization”. Then they use the block relaxation algorithm to solve the nonconvex optimization that only attains a local optimum and is difficult to ensure the statistical convergence of the numerical output. Different from these approaches, MrBeSS iteratively updates the primal variable and the dual variable and then updates the support set by a hard thresholding rule, which is an “implicit regularization”. Owing to this framework, it enables us to analyze the statistical properties in the view of the algorithm. Recently, we notice that there have be some literature to analyze the statistical convergence in the view of the algorithm, e.g. Qiu et al. (2022) and Zhao et al. (2022). But MrBeSS is the first to solve the sparse reduced rank regression. In addition, different from the gradient descent method (Qiu et al., 2022; Zhao et al., 2022), MrBeSS needs not to choose the step size for the algorithm. In the following theoretical analysis, we reveals that the numerical solution of MrBeSS enjoys the nearly optimal convergence rate, which bridges the gap between the statistical guarantee and numerical computation. Moreover, we will show that the iteration complexity is polynomial to attain the nearly optimal estimation. As far as we know, this is the first to the sparse reduced rank regression.

2.3 MrBeSS with adaptive parameter tuning

In practice, the rank and the row-sparsity are unknown, and some data-driven procedure is needed to tune them. One approach is to select parameters by the -fold cross validation technique (Hastie et al., 2009) based on a two-dimensional grid of and . Nevertheless, it is time-consuming especially with a large grid. Alternatively, we propose a generalized-type information criterion (GIC) to tune parameters. For any coefficient matrix , we define GIC as follows:

| (2.10) |

where is the number of non-zero rows of and . The GIC attempts to trade off between the prediction error and the complexity of the model, and smaller GIC represents a more balanced choice.

A naive approach is to minimize GIC among all candidate parameters over a grid of and . However, simultaneous search for optimal pair of tuning parameters over a two-dimensional grid is still computationally expensive. For instance, if the numbers of the candidates for and are and , then we need to calculate kinds of combination of and . Therefore, to reduce the computational burden, we introduce a simplified yet efficient search strategy. In specific, we first identify a GIC-minimal choice of sparsity over a sequence of values with rank large enough, and then select an optimal rank with the minimum GIC value by fixed . The algorithm with the simplified search strategy is summarized in Algorithm 2, which is shown by Theorem 3 to recover the true tuning parameters.

Input: response matrix , predictor matrix , maximum number of rank

and row sparsity .

Output: .

3 Theoretical justification

In this section, we present the theoretical analysis for the estimators generated by Algorithm 1 and Algorithm 2. The proof of these results are provided in Appendix.

3.1 Technical conditions

First, we introduce some definitions that will be used later. For any output of Algorithm 2, denote the identified support set for rows as , where is the th row of . Denote the rank of as . Throughout this section, we search the solution in the following parameter space for the coefficient matrices

| (3.1) |

where and can be diverged with the sample size . We assume the following technical conditions for the theoretical analysis.

Condition 1.

With the given sparsity level , there is

with an arbitrary subset and .

Condition 2.

With the given sparsity levels , there is

with two arbitrary subsets , , and .

Condition 3.

Assume that the rows of are i.i.d from the normal distribution , and the operator norm of is bounded from the above.

Condition 4.

With the and , define the parameter as follows

and assume that .

Condition 1 is the restricted eigenvalue (RE), e.g. Zheng et al. (2019); Bickel et al. (2009), where the upper bound usually holds with the normalized data, and implies the value will slightly increase with the cardinality . The cardinality is small in practice thus the upper bound will be finite. As for the lower bound , it ensures the identifiability of the model. is equivalent to the matrix is inversible. Once is the true support set, we can directly implement the ordinary reduced rank estimation, which can be seen as the oracle estimation. Later, we will reveal that the numerical solution from the proposed algorithm is equal to the oracle estimation with a significant probability.

Condition 2 is a derivative of the upper bound in Condition 1. We define the notation for the algorithm analysis. In fact, there is . Compared with Condition 1, the difference is that describes the correlation among of different predictors. The larger results in a more challenging recovery for the coefficient, since the strong pseudo-correlation misleads the variable selection. A special case is , which means the columns of are mutually orthogonal. Under the case, there is a closed formulation for the optimization with nonconvex regularization that is easy to solve. In this paper, we concerns on the case .

Condition 3 is a regular condition to analyze the statistical convergence rate, where we use the Gaussian probability tail to bound the magnitude of noise. Compared with the previous work such as Bunea et al. (2012); She (2017), we allow the correlation among of the entries in the noise vector. This is more reasonable since the elements in the response vector are correlated with each other in practical applications.

We define a parameter in Condition 4 and impose that with . Huang et al. (2018) has shown that . Then with some appropriate and (e.g. and with ), we have . There is a similar parameter to in the univariate-response regression, where the only difference is the rank factor replaced by an absolute constant (Huang et al., 2018; Zhu et al., 2020). In a simple point of view, the will be smaller than 1 as long as the correlation among of the different covariates is small enough, in other words, is as small as enough. The difference between the univariate response and the multiple lies in the rank structure, where we need a smaller correlation with a higher rank. The parameter can be seen as a generalized version for the sparse reduced-rank regression.

Definition 1.

Define the signal strength of as follows

where is the th largest eigenvalue of , and is the projection matrix onto the space spanned by the columns of .

In Definition 1, the first term in measures the smallest signal strength of the true variables, which is a matrix version of the definition in Fan and Tang (2013) for the recovery of the support set . The second term in describes the signal strength on the singular value for the recovery of the true rank, and similar definitions have been proposed for the recovery of the rank in reduced-rank regression models, see Zheng et al. (2019); Bunea et al. (2011).

3.2 Main results

Now we are ready to present the main result. The first theorem guarantees the convergence of Algorithm 1, where the detail is as follows.

Theorem 1.

Theorem 1 shows that the solution from Algorithm 1 converges geometrically to the truth with . Moreover, with the large enough , we can obtain the statistical convergence rate, which is presented in the following corollary.

Corollary 1.

With the same conditions in Theorem 1 and , the below oracle inequalities

hold uniformly with the probability at least when the number of iterations satisfy

First, we emphasize that is the numerical output of the algorithm that is different from the current literature, where they concern on the statistical property of the global optimum of an optimization. However, the nonconvexity of the sparse reduced rank regression results in their numerical algorithms only attaining a local optimum. There exsits a gap between the computational method and the theoretical guarantee in the current literature. Recall the above corollary, the left of the inequality is the numerical error of the algorithm, and the right is the statistical convergence rate. Therefore, the corollary bridges the gap between the numerical computation and the theoretical analysis.

Second, compared with the minimax lower bound proposed by Ma et al. (2020); Ma and Sun (2014), the statistical convergence rate of has been nearly minimax optimal. Although there have been some methods attaining the optimal rate (She, 2017; Uematsu et al., 2019), their numerical results usually are some local optimums that leads to a gap between numerical solutions and their optimal convergence rate. As far as we know, the proposed algorithm in this paper is the first, where its numerical output enjoys the nearly minimax optimal rate.

Third, owing to the bridge of the above corollary, we can obtain the iteration complexity of the proposed algorithm, which is also a new result compared with the current methods. The corollary reveals that the proposed algorithm only needs a polynomial iteration complexity to attain the optimal estimation. Thereby, it enjoys a fast computation in high dimensions.

Last but not least, we establish the error bound with respect to the operator norm that is commonly used in the matrix perturbation. It enables us to obtain a tighter upper bound for the matrix decomposition than the Frobenius norm. This result also distinguishes our work from the current literature.

Theorem 1 and Corollary 1 are built on the output of Algorithm 1, say , where the algorithm depends on two hyper-parameters, and , which need be tuned. Once given with the ture and , we can obtain a very accurate estimation, together with the optimal convergence rate. Therefore, we propose a new information criterion for the tuning of and , and then it yields an oracle estimation stated in Theorem 3. We first introduce the property of the proposed GIC with regrad to the numerical solution in Algorithm 1. Note that actually is the reduced-rank estimator (Reinsel and Velu, 1998) restricted in the corresponding support set. Thus we consider an arbitrary reduced-rank estimator in Theorem 2. Let the oracle reduced-rank estimator be the baseline. The theorem reveals that the GIC arrives at the minimum only when with the large enough .

Theorem 2.

The above theorem implies we can obtain the oracle estimator by the proposed GIC asymptotically. In the recent literature, She (2017) also proposed a predictive information criterion (PIC) to tune the rank and the support set but there is fundamentally different from our GIC. In this paper, the proposed GIC aims to the consistency of the recovery for the rank and the true support set, however, PIC aims to obtain an accurate prediction error and it cannot ensure the consistency of the estimation for the rank and support set. Owing to the GIC, we can show that the numerical output of algorithm actually is the oracle estimation with a significant probability, which is presented in the next theorem.

Although Theorem 2 reveals that GIC can asymptotically recover the support set and rank, we still need to search parameters over the grid generated by and . To reduced the searching range, we develop Algorithm 2 to tune parameters along with the coordinate. That is, we first derive an optimal sparsity level under a given relatively large rank, say , and then tune the rank by GIC with the given . The following theorem provides the theoretical justification for this strategy.

Theorem 3.

Theorem 3 reveals an interesting result that the output of Algorithm 2 is exactly the oracle estimator with an overwhelming probability. Different from the existing literature, Theorem 3 guarantees the statistical property of the algorithmic solution. In the sparse reduced rank regression, the coordinate descending algorithm commonly used in the current literature (She, 2017; Ma and Sun, 2014; Mishra et al., 2017) converges to a local minimizer but there is no literature to discuss the relationship between the numerical solution and the oracle reduced rank regression. The oracle estimation is an important baseline since it is an ideal result for the variable selection and the dimension reduction. The result implies that the obtained estimation is unbiased with an overwhelming probability. The numerical results in Section 4 also show that the estimation error of MrBeSS is lower than those of other competing methods.

4 Numerical Studies

In this section, we investigate the finite-sample performance of MrBeSS on simulated data and compare it with other competing methods including the reduced rank regression via adaptive nuclear norm penalization (RRR-ada, Chen et al. (2013)), the rank constrained group lasso (RCGL, Bunea et al. (2012)), the sparse reduced rank regression using adaptive group lasso (SRRR, Chen and Huang (2012)), and the sequential factor extraction via co-sparse unit-rank estimation (SeCURE, Mishra et al. (2017)).

4.1 General setups

We first introduce some general notations and simulation settings, which will be used later. To generate the coefficient matrix, we first generate matrix , whose entries of matrix are i.i.d. from . Then, let the entries of matrix be i.i.d. from the uniform distribution on , and we can construct matrix as . We normalize the columns of and such that the norm of each column is unit-length, respectively. Moreover, we generate an diagonal matrix whose the th diagonal entry with . After that, we set the coefficient matrix as

where is the diagonal matrix. It is easy to see that the rank of is equal to .

We generate the predictor matrix from the normal distribution. In particular, the th row is independently sampled from with and . Similarly, the rows of the noise matrix are generated as i.i.d. samples of with and . We set to control the signal-to-noise ratio (SNR), defined as , where is the largest eigenvalue of . Moreover, in this paper, we consider two kinds of for the noise matrix: (1) the auto regression matrix (AR) satisfying ; (2) the strong correlation matrix (SC) satisfying if , otherwise, . With the given , and , the response matrix is . We set , and let be varied from 200 to 1000. For each setup, a total of 200 replications are conducted.

For any estimated coefficient matrix , we measure the estimation and prediction accuracy by , and , respectively. The variable selection performance is characterized by the false positive rate (FPR) and false negative rate (FNR) in recovering the sparsity patterns of the row support set of , where and with TP, FP, TN and FN being the numbers of true nonzeros, false nonzeros, true zeros, and false zeros of the rows of , respectively. In addition, we also report the estimated rank and the computational time (Time) in seconds.

To tune parameter(s), we search over a grid of sparsity and rank for all methods except RRR-ada, and a line search of rank for RRR-ada. We set the maximum rank as 10 when tuning parameters for all methods. Because there is no explicit information criteria for RCGL and SRRR under high dimensions, we tune the parameters by data validation for them. That is, we use samples to estimate coefficients and the other samples to measure the prediction with different combinations of sparsity and rank. Then we can determine the optimal pair of sparsity and rank with the minimum prediction error. As for RRR-ada and SeCURE, we follow the default criteria to tune the parameter, which can be found in Chen et al. (2013); Mishra et al. (2017) for more details. For a fair comparison, we present two versions of our proposal denoted by MrBeSS-V and MrBeSS. While in MrBeSS-V the optimal parameters are determined by data validation, MrBeSS tunes parameters based on GIC. All of the competing methods except SeCURE are implemented in the R package rrpack, and SeCURE are implemented in R package secure.

4.2 Simulation results

The simulation results are summarized in Table 1. It can be seen that all methods except RRR-ada and SeCURE have comparable performance in terms of estimation and prediction errors. This is due to RRR-ada doesn’t perform variable selection at all, and thus it leads to inaccurate estimation for the coefficient matrix in the sparse data setting. As for SeCURE, it imposes the sparsity on both rows and columns, and the performance is not well for the row-sparse setting. This can be seen from the high values in FNR and biased estimation in rank, which indicates it fails to recover the true nonzero rows nor the hidden structure in the coefficient matrix.

Among the methods suitable for row-sparse scenarios, both MrBeSS and MrBeSS-V have substantial better performance. In particular, MrBeSS-V yields the sparsest model with much lower values in FPR and comparable FNR values in comparison with SRRR and RCGL, the methods also using validation data to tune parameters. In other words, both SRRR and RCGL have the tendency of over-selecting irrelevant variables as indicated by the high FPR values, which is expected since a Lasso-type penalty is used to perform row selection. This shows the superiority of restricting the number of nonzero rows for variable selection in the reduced rank regression model. In addition, the computational time of MrBeSS-V is less than other two methods, and the gap is growing as increases.

From Table 1, we can tell that both MrBeSS and MrBeSS-V have comparable performance when is low. When is high, say , MrBeSS-V slightly outperform MrBeSS in terms of FNR, which might be due to the small sample size () compared with the dimension. Nevertheless, the computational time for MrBeSS is less than one tenth of those for MrBeSS-V, showing its feasibility in dealing with high-dimensional data.

Overall, the two MrBeSS approaches produce considerably sparser model with adequate estimation and prediction accuracy among all methods, and enjoy nice computational efficiency especially in high dimensions.

| Method | Er | Er | FPR (%) | FNR (%) | Time (s) | Estimated rank | |

|---|---|---|---|---|---|---|---|

| RRR-ada | 19.24 (2.21) | 1.99 (1.62) | 100 (0) | 0 (0) | 0.24 (0.03) | 2.87 (0.36) | |

| SRRR | 1.01 (0.5) | 1.16 (0.52) | 49.63 (5.79) | 0 (0) | 80.47 (5.11) | 3 (0) | |

| RCGL | 0.93 (0.42) | 1.2 (0.53) | 67.11 (5.41) | 0 (0) | 65.08 (3.96) | 3 (0) | |

| SeCURE | 23.84 (3.34) | 35.08 (7.37) | 0.64 (2.16) | 26.35 (15.95) | 0.38 (0.12) | 3.19 (0.84) | |

| MrBeSS-V | 0.81 (1.36) | 1.08 (1.43) | 2.38 (1.34) | 0.65 (2.85) | 58.45 (9.38) | 3.02 (0.16) | |

| MrBeSS | 1.24 (1.62) | 1.49 (1.53) | 0.67 (0.38) | 1.15 (3.35) | 2.54 (1.63) | 3.03 (0.59) | |

| RRR-ada | 13.95 (1.12) | 5 (7.9) | 98.5 (12.19) | 1.5 (12.19) | 1.28 (0.05) | 2.52 (0.73) | |

| SRRR | 0.42 (0.35) | 1.07 (0.55) | 23.56 (4.77) | 0.05 (0.71) | 227.35 (13.12) | 3.04 (0.5) | |

| RCGL | 0.47 (0.23) | 1.24 (0.62) | 40.18 (3.68) | 0 (0) | 177.45 (10.25) | 3 (0) | |

| SeCURE | 12.72 (1.74) | 38.6 (8.07) | 0.34 (1.49) | 32.25 (16.82) | 1.35 (0.47) | 3.02 (0.79) | |

| MrBeSS-V | 0.47 (0.84) | 1.2 (1.8) | 1.13 (0.68) | 1.05 (3.8) | 82.96 (13.25) | 3 (0.07) | |

| MrBeSS | 0.71 (0.88) | 1.65 (1.7) | 0.35 (0.22) | 1.5 (3.98) | 3.92 (1.96) | 2.94 (0.5) | |

| RRR-ada | 10.24 (0.63) | 5.92 (8.64) | 98 (14.04) | 2 (14.04) | 3.86 (0.11) | 2.46 (0.78) | |

| SRRR | 0.32 (0.46) | 1 (0.43) | 13.28 (2.91) | 0.35 (1.84) | 397.83 (23.23) | 3 (0) | |

| RCGL | 0.35 (0.18) | 1.29 (0.54) | 29.34 (2.05) | 0 (0) | 301.62 (17.8) | 3 (0) | |

| SeCURE | 8.52 (1.21) | 38.64 (7.81) | 0.08 (0.35) | 32.6 (17.43) | 3.28 (1.19) | 2.86 (0.53) | |

| MrBeSS-V | 0.36 (1.12) | 1.51 (4.67) | 0.86 (0.45) | 1.2 (6.99) | 97.36 (14.66) | 3 (0) | |

| MrBeSS | 0.52 (0.91) | 1.84 (2.73) | 0.22 (0.15) | 1.55 (5.85) | 4.88 (2.6) | 3.27 (1.15) | |

| RRR-ada | 8.1 (0.42) | 8.3 (12.33) | 96 (19.65) | 4 (19.65) | 8.89 (0.46) | 2.29 (0.91) | |

| SRRR | 0.24 (0.34) | 0.95 (0.44) | 8.21 (2.2) | 0.35 (1.84) | 587.2 (32.98) | 3 (0) | |

| RCGL | 0.28 (0.14) | 1.32 (0.61) | 22.96 (1.51) | 0 (0) | 442.25 (23.89) | 3 (0) | |

| SeCURE | 6.54 (0.82) | 39.1 (7.66) | 0.07 (0.32) | 35.2 (16.32) | 7.05 (2.82) | 2.75 (0.55) | |

| MrBeSS-V | 0.33 (0.94) | 1.81 (5.47) | 0.62 (0.33) | 1.75 (7.98) | 109.33 (17.75) | 3 (0) | |

| MrBeSS | 0.43 (1.05) | 1.98 (4.21) | 0.19 (0.16) | 2 (9.08) | 6.05 (3.45) | 3.22 (1.13) | |

| RRR-ada | 6.66 (0.38) | 11.62 (18.43) | 90 (30.08) | 10 (30.08) | 19.94 (5.82) | 2.15 (1.04) | |

| SRRR | 0.24 (0.39) | 0.98 (0.51) | 6.02 (3.04) | 0.7 (2.75) | 782.44 (41.02) | 3.04 (0.51) | |

| RCGL | 0.24 (0.11) | 1.33 (0.62) | 18.85 (1.16) | 0 (0) | 590.7 (32.43) | 3 (0.07) | |

| SeCURE | 5.26 (0.64) | 39.62 (8.47) | 0.06 (0.22) | 33.9 (17.15) | 14.73 (7.88) | 2.71 (0.51) | |

| MrBeSS-V | 0.25 (0.93) | 1.51 (4.72) | 0.53 (0.28) | 1.4 (8.68) | 120.43 (19.81) | 3 (0) | |

| MrBeSS | 0.37 (0.86) | 2.21 (5.62) | 0.14 (0.12) | 2.3 (9.23) | 6.34 (3.06) | 3.13 (0.95) | |

4.3 Tuning strategy in MrBeSS

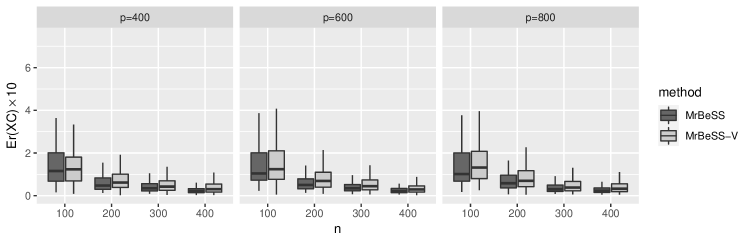

In this section, we show the effectiveness of using GIC to tune parameters by comparing two versions of our approach, i.e., MrBeSS and MrBeSS-V, under different setting of sample size . In particular, we adopt settings from Section 4.1 and vary the sample size from 100 to 400 with the step size 100. For space limit, we only present the results of and the noise with the SC covariance matrix, and the remaining results to be omitted since they are similar.

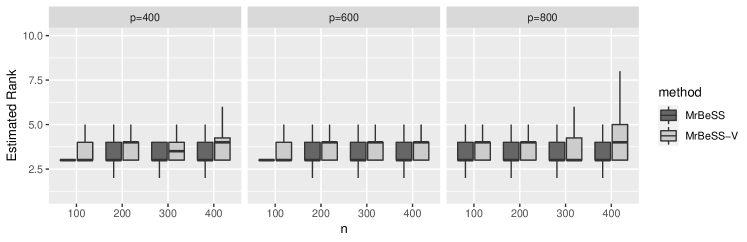

First the result of the rank estimation is presented in Figure 1.

From Figure 1, we can see that the proposed GIC is conservative for the rank estimation under the low sample size but it can estimate the rank accurately when increasing the sample size. The result coincides with the theory in Theorem 3 that the GIC can recover the rank asymptotically with the large enough .

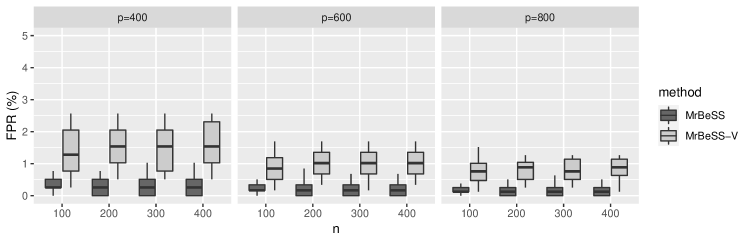

Next the variable selection performance is attached in Figure 2 that shows the GIC is outstanding in the variable selection. Even under the low sample size, GIC still recovery the support set accurately. Compared with the GIC, the method of data validation is conservative in the variable selection because it prefers to the solution that enjoys accurate prediction. This is a common issue for the data validation framework.

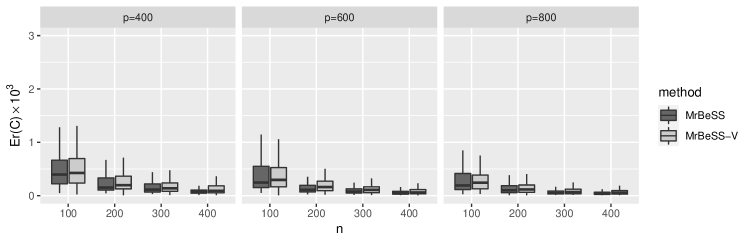

Finally, the performance of estimation and prediction is presented in Figure 3. With the increasing sample size , the accuracy of estimation and prediction is enhanced, which demonstrates the asymptotic consistency for both two versions of MrBeSS.

5 Real data

We consider a gene expression and microRNA (miRNA) dataset from The Cancer Genome Atlas (TCGA) consortium (Network et al., 2011). We are interested in identifying miRNAs that regulate the expression of ovarian cancer related genes. Instead of using the whole set of 11,864 genes, we focus on a subset of 12 genes that have shown to be significantly associated with the four cancer subtypes (Network et al., 2011). The final dataset consists of samples with genes and measurements of miRNAs, after excluding the miRNAs with standard deviations less than 0.5.

We apply MrBeSS, as well as other four competing methods including RRR-ada, RCGL, SRRR, and SeCURE to these data. As for the tuning parameter, we use the same implementation in the previous section. Table 2 reports the mean squared error , the estimated rank and the estimated row-sparsity. We find from Table 2 that while the classical method RRR-ada yields a null model, other methods result in a valid model with rank being non-zero. This suggests that RRR-ada might lose power in such high-dimensional data due to the horrible noise accumulation, which leads to RRR-ada mistakes the data all is noise. Both MrBeSS-V and SeCURE can achieve low prediction error, but the rank and the size of detected row support are much larger, which indicates a overfitting issue might occur in this specific data. This result is expect since MrBeSS-V is a validation method and would be conservative in the variable selection, see Figure 3. Since the number of free parameters is determined jointly by rank and row-sparsity in RRR, MrBeSS successfully selects a model with simple structure as well as acceptable prediction accuracy. Furthermore, the running time of our MrBeSS is the lower among all methods, showing its practical application feasibility in high-dimensional data.

| Method | Prediction Error | Time (s) | Estimated rank | Support set size |

|---|---|---|---|---|

| MrBeSS-V | 1.1 | 35.1 | 4 | 60 |

| MrBeSS | 1.55 | 0.51 | 1 | 10 |

| SRRR | 1.28 | 251.29 | 1 | 121 |

| RCGL | 1.23 | 236.37 | 1 | 235 |

| RRR-ada | 1.91 | 0.55 | 0 | 0 |

| SeCURE | 1.19 | 22.72 | 6 | 90 |

In order to compare prediction accuracy and stability of different variable selection methods, we randomly split the data into a training set with samples and a test set with samples. All model estimations are carried out using the training data, with the parameter tuning strategies same as the previous experiment. We use the test data to calibrate the predictive performance of each estimator , specifically, by its mean squared prediction error , where denotes the test data set. The random-splitting process is repeated 200 times with the results summarized in Table 3. Again, MrBeSS-V and SeCURE have the smallest prediction error, yet yield the most complicate model. Besides these two methods, our MrBeSS approach has superior performance compared to the other methods in terms of prediction error and support set size. The SRRR and RCGL has competitive values in terms of prediction error, but their products of support set size and rank are around 13 times and 18 times of those in MrBeSS. In addition, the results for MrBeSS are most robust with the smallest standard errors in almost all measurements. We conclude that in real applications, MrBeSS can produce models with high prediction accuracy and interpretability.

| Method | Prediction Error | Time (s) | Estimated rank | Support set size |

|---|---|---|---|---|

| MrBeSS-V | 1.47 (0.15) | 40.29 (0.94) | 4.76 (2.39) | 44.6 (12.86) |

| MrBeSS | 1.72 (0.16) | 0.59 (0.14) | 1.06 (0.25) | 10.61 (0.85) |

| SRRR | 1.81 (0.18) | 173.98 (16.21) | 1.02 (0.19) | 132.76 (27.3) |

| RCGL | 1.85 (0.21) | 210.44 (55.07) | 1.17 (0.49) | 178.62 (90.59) |

| RRR-ada | 1.91 (0.17) | 0.62 (0.03) | 0 (0) | 0 (0) |

| SeCURE | 1.51 (0.18) | 16.46 (8.47) | 3.72 (1.73) | 59.06 (20.84) |

6 Discussion

In this paper, we propose a new algorithm, called MrBeSS, for the estimation of the sparse reduced-rank regression, where the approach mainly has the following advantages: (1) the method considers the -norm constraint that avoids the bias in the estimation; (2) the algorithmic solution is nearly optimal with regrad to the statistical convergence rate; (3) the algorithm attains to the nearly optimal estimation with a polynomial number of iterations. Owing to the three advantages, MrBeSS enjoys not only nice sampling properties but also an accurate estimation and fast computation. Therefore, the performance of MrBeSS is better than other competitive methods.

There are some interesting problems for the future research. One extends the proposal to the case, where both rows and columns of coefficient matrix are sparse called the co-sparse structure (Mishra et al., 2017). Then we can implement the variable selection on responses and predictors simultaneously. Another one is to equip the primal-dual formulation with the unit-rank deflation, e.g. Zheng et al. (2019); Chen et al. (2022), that constructs the estimation for each rank-one component of the coefficient matrix. It can enhance the accuracy of estimation for each rank-one layer or singular vectors. Moreover, extending the algorithm to the multi-response generalized linear model is also important that has been widely used in recommender systems and reinforcement learning.

References

- Ahn et al. [2015] Mihye Ahn, Haipeng Shen, Weili Lin, and Hongtu Zhu. A sparse reduced rank framework for group analysis of functional neuroimaging data. Statistica Sinica, 25:295–312, 2015.

- Bickel et al. [2009] Peter J Bickel, Ya’acov Ritov, and Alexandre B Tsybakov. Simultaneous analysis of Lasso and Dantzig selector. The Annals of Statistics, 37(4):1705–1732, 2009.

- Bunea et al. [2011] Florentina Bunea, Yiyuan She, and Marten H Wegkamp. Optimal selection of reduced rank estimators of high-dimensional matrices. The Annals of Statistics, 39(2):1282–1309, 2011.

- Bunea et al. [2012] Florentina Bunea, Yiyuan She, and Marten H Wegkamp. Joint variable and rank selection for parsimonious estimation of high-dimensional matrices. The Annals of Statistics, 40(5):2359–2388, 2012.

- Chen et al. [2012] Kun Chen, Kung-Sik Chan, and Nils Chr Stenseth. Reduced rank stochastic regression with a sparse singular value decomposition. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 74(2):203–221, 2012.

- Chen et al. [2013] Kun Chen, Hongbo Dong, and Kung-Sik Chan. Reduced rank regression via adaptive nuclear norm penalization. Biometrika, 100(4):901–920, 2013.

- Chen et al. [2022] Kun Chen, Ruipeng Dong, Wanwan Xu, and Zemin Zheng. Fast Stagewise Sparse Factor Regression. Journal of Machine Learning Research, 23(271):1–45, 2022.

- Chen and Huang [2012] Lisha Chen and Jianhua Z Huang. Sparse reduced-rank regression for simultaneous dimension reduction and variable selection. Journal of the American Statistical Association, 107(500):1533–1545, 2012.

- Fan and Lv [2014] Yingying Fan and Jinchi Lv. Asymptotic properties for combined and concave regularization. Biometrika, 101(1):57–70, 2014.

- Fan and Tang [2013] Yingying Fan and Cheng Yong Tang. Tuning parameter selection in high dimensional penalized likelihood. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(3):531–552, 2013.

- Hastie et al. [2009] Trevor Hastie, Robert Tibshirani, Jerome H Friedman, and Jerome H Friedman. The elements of statistical learning: data mining, inference, and prediction, volume 2. Springer, 2009.

- He et al. [2018] Lifang He, Kun Chen, Wanwan Xu, Jiayu Zhou, and Fei Wang. Boosted sparse and low-rank tensor regression. Advances in Neural Information Processing Systems, 31, 2018.

- Huang et al. [2018] Jian Huang, Yuling Jiao, Yanyan Liu, and Xiliang Lu. A Constructive Approach to Penalized Regression. Journal of Machine Learning Research, 19(10):1–37, 2018.

- Lee et al. [2010] Mihee Lee, Haipeng Shen, Jianhua Z Huang, and James S Marron. Biclustering via sparse singular value decomposition. Biometrics, 66(4):1087–1095, 2010.

- Ma et al. [2020] Zhuang Ma, Zongming Ma, and Tingni Sun. Adaptive estimation in two-way sparse reduced-rank regression. Statistica Sinica, 30(4):2179–2201, 2020.

- Ma and Sun [2014] Zongming Ma and Tingni Sun. Adaptive sparse reduced-rank regression. arXiv preprint arXiv:1403.1922, 2014.

- Mishra et al. [2017] Aditya Mishra, Dipak K Dey, and Kun Chen. Sequential co-sparse factor regression. Journal of Computational and Graphical Statistics, 26(4):814–825, 2017.

- Network et al. [2011] Cancer Genome Atlas Research Network et al. Integrated genomic analyses of ovarian carcinoma. Nature, 474(7353):609, 2011.

- Qiu et al. [2022] Yixuan Qiu, Jing Lei, and Kathryn Roeder. Gradient-based Sparse Principal Component Analysis with Extensions to Online Learning. Biometrika, 2022.

- Reinsel and Velu [1998] Gregory C. Reinsel and Raja P. Velu. Reduced-Rank Regression Model, pages 15–55. Springer New York, 1998.

- She [2017] Yiyuan She. Selective factor extraction in high dimensions. Biometrika, 104(1):97–110, 2017.

- Uematsu and Tanaka [2019] Yoshimasa Uematsu and Shinya Tanaka. High-dimensional macroeconomic forecasting and variable selection via penalized regression. The Econometrics Journal, 22(1):34–56, 2019.

- Uematsu et al. [2019] Yoshimasa Uematsu, Yingying Fan, Kun Chen, Jinchi Lv, and Wei Lin. SOFAR: Large-Scale Association Network Learning. IEEE Transactions on Information Theory, 65(8):4924–4939, 2019.

- Zhang and Zhang [2012] Cun-Hui Zhang and Tong Zhang. A general theory of concave regularization for high-dimensional sparse estimation problems. Statistical Science, 27(4):576–593, 2012.

- Zhao et al. [2022] Peng Zhao, Yun Yang, and Qiao-Chu He. High-dimensional linear regression via implicit regularization. Biometrika, 2022.

- Zheng [2014] Wenming Zheng. Multi-view facial expression recognition based on group sparse reduced-rank regression. IEEE Transactions on Affective Computing, 5(1):71–85, 2014.

- Zheng et al. [2019] Zemin Zheng, Mohammad Taha Bahadori, Yan Liu, and Jinchi Lv. Scalable Interpretable Multi-Response Regression via SEED. Journal of Machine Learning Research, 20(107):1–34, 2019.

- Zhong and Huang [2022] Yan Zhong and Jianhua Z Huang. Biclustering via structured regularized matrix decomposition. Statistics and Computing, 32(3):1–15, 2022.

- Zhu et al. [2020] Junxian Zhu, Canhong Wen, Jin Zhu, Heping Zhang, and Xueqin Wang. A polynomial algorithm for best-subset selection problem. Proceedings of the National Academy of Sciences, 117(52):33117–33123, 2020.

Appendix A Proofs of main results

Before proving the main result, we introduce some notations required in the following proof. Let the row support set of in the iteration be

where is the th row of . We define the following index sets

| (A.1) |

with . Here is the true features selected in the th iteration, and is the missed features in the th iteration. Oppositely, is the false features selected in the step. is the unimportant features and not selected in the th iteration.

Similar to the above definition, there are corresponding sets from to

| (A.2) |

where is the missed trues features in , and are missed true features in . Oppositely, is the false features selected from . is the false features selected from . Moreover, we define the difference between the active set and the true support set as follows

which will be used in the following proofs. For convenience, we also define

| (A.3) |

with , which will be used later.

A.1 Proofs of Theorem 1

The proof of Theorem 1 relies on the complicated mathematical derivation, thus we divide complicated derivations into Lemmas 1–4. The key of proof is to suppress the loss due to the missed true features. Combining (B.6)–(B.8), we can get

| (A.4) |

where we use the fact because the each column of is normalized to . Then applying Lemma 6, we have . Thus utilizing Lemma 4 yields

| (A.5) |

where is a constant and the last inequality holds because of Lemma 3.

Moreover, following the definition of and similar simplifications in Lemma 2, we have

| (A.6) |

where , , and the last inequality holds due to Condition 2 and the triangle inequality.

Combining (A.7) and (A.4) yields

| (A.8) |

where we use the fact fact . Then applying the inequality (B.1) in Lemma 1, we can obtain

| (A.9) |

Note that there exists a large enough constant , which is subject to . Then after combining (A.8) and (A.9), some algebraic simplifications yields

where is a positive constant. Then define the as follows

which ensures that . Therefore, applying the inequality recursively and supposing , we have

where is a positive constant. Then by the inequality (B.2), there is

| (A.10) |

where and are some positive constants. Recall the definition of as follows

then applying Lemma 5, we have

| (A.11) |

holds with the probability at least . Finally, note that , and then combining (A.10) and (A.11) will conclude the proof.

A.2 Proofs of Theorem 2

Denote by the estimation of MrBeSS with the rank and row support set . Note that actually is the reduced rank estimator constrained in the support set and . For the sake of clarity, we first define the event as follows and then prove the result conditional on the event

with , and . Then there are two kinds of cases as follows.

1. Underfitted case: or . Define the signal strength parameter as follows

where is the th largest eigenvalue of . Therefore from Lemma 9, we have

with the underfitted case and some positive constant . Furthermore, combining Lemma 8 and the above inequality yields

| (A.12) |

under the event , where is the estimator of the oracle reduced rank regression with row support set and rank .

2. Overfitted case: and . Similar to the above argument, utilizing Lemma 8 and 9, we can obtain that

| (A.13) |

under the event .

Then recall the definition of the generalized information criterion (GIC) as follows

where denotes the number of the nonzero rows in and . Thus for any estimator with row support set and , there is

| (A.14) |

With the underfitted , combining (A.12) and (A.14) yields

| (A.15) |

Similarly, we compare the difference between and under the overfitted case. And then by the inequality (A.13), we have

| (A.16) |

Furthermore combining (A.14) and (A.16), we can get

Note that under the overfitted case, we have and . Therefore, it yields

| (A.17) |

under the overfitted case.

Assume that we tune the and in the parameter space as follows

with some . Thus with the underfitted , we have

by the inequality (A.15). Similar to the above and with the overfitted , there is

from the inequality (A.17).

If the following assumptions hold simultaneously

we can obtain that

where is the row support set of and . Specifically, we set then the above three assumptions can be concluded from

where we use the fact . Finally, applying Lemma 5 yields that holds with the probability at least , which finishes the proof.

A.3 Proofs of Theorem 3

In this section, we denote the output of MrBeSS by for the sake of clarity. With the given maximum rank , we first show that

leads to with high probability, where is the row support set of . Then under the given support set , we can recover the true rank by minimizing GIC with high probability. Similar to the proof of Theorem 2, we mainly prove the result conditional on the event , where is the maximum level of the search space. Moreover, denote the number of nonzero rows in by and for convenience.

With the given rank , the GIC defined in Theorem 2 is

with . Under the assumption and applying Case 1 and 2 in Lemma 9, we can obtain a similar result in the proof of Theorem 2, which is as follows. On the one hand, we have

with , and . On the other hand, there is

with and . By Lemma 8 and the above two inequalities, under the event , we can get

1) and .

2) and .

where the row support set of is but . Note that we search the solution with in the parameter space . By the similar argument in the proof of Theorem 2, we have

with . Thus under the same assumptions in Theorem 2 and conditional on the event , there is

constrained in .

Next we show that with the given , minimizing the GIC can recover the true rank of conditional on the event and with the large enough . Directly applying Cases 1 – 4 in Lemma 9 and by the similar argument in the proof of Theorem 2, we can obtain that

with the underfitted estimator . On the other hand, with the overfitted , there is

where is the oracle reduced rank estimator with and the support set . Thus under the same assumptions of Theorem 2 and conditional on , we can get

Finally applying Lemma 5, we have holds with the probability at least that concludes the proof.

Appendix B Auxiliary Lemmas

B.1 Lemma 1 and its proofs

Following the algorithm of MrBeSS, we have

after updating . For the sake of clarity, we denote by . Therefore, we have

Moreover, there is a fact . It yields

where , and we use the fact . Because the rows of restricted in are zeros, and . Recall the definition of , and they are also the top- right singular vectors of

where and are the th largest singular value and its corresponding left singular vector, respectively. Then there is

By the above equation, we can obtain

| (B.3) |

In addition, note that is the th largest singular value of

and . Then by the matrix perturbation theory, we have

| (B.4) |

where the last inequality is due to Condition 1. Similarly, recall the definition of , and there is

| (B.5) |

Thus combining (B.3)–(B.5), we will obtain

As for the upper bound of , we have

Finally, define , then it finishes the proof.

B.2 Lemma 2 and its proofs

Lemma 2.

By the definitions of and , we have and . On the one hand, the triangle inequality yields

On the other hand, note that . Applying the triangle inequality again, we have

B.3 Lemma 3 and its proofs

Lemma 3.

Following the algorithm of MrBeSS, we have

with .

Recall that and are the th rows of and . And there are

Because and are the missed features in the iterative algorithm. Thus by the algorithm and the definitions of , and , the elements of are no greater than the elements in . In addition, and are complementary from (2.9). Then there is

On the one hand, we can get

| (B.11) |

On the other hand, note that

which yields that . Then we have

| (B.12) |

Next we will show the upper bound of . For the sake of clarity, we denote that and . Then by some algebraic simplifications, we have

By Lemma 6, we can obtain

| (B.13) |

Combining (B.11)–(B.13) yields

Finally by the definition of and , and utilizing Lemma 6 again, we have . Thus there is

which finishes the proof.

B.4 Lemma 4 and its proofs

Lemma 4.

Recall the definition of and , we have

after some simplifications. Here we denote for convenience. Utilizing Lemma 6, we can get

| (B.14) |

Then we bound the second term in (B.14). Note that there is without loss of the generality. Moreover, we have . Thus there exists a linear transformer satisfying , since is a submatrix of the original. It ensures that

| (B.15) |

where is a positive constant, and we use the fact is bounded from above because the columns of are normalized.

Next we show the upper bound of . Utilizing the decomposition in Lemma 1 again, we have

Due to the orthogonality of and , there is

Then following the similar argument in Lemma 1, we can obtain

where we use Lemma 6 in the first inequality. Furthermore, under Conditions 1, 2 and , there is

| (B.16) |

Combining (B.15) and (B.16), we have the upper bound as follows

| (B.17) |

with a positive constant . Moreover, note that there is

| (B.18) |

Finally, combining (B.14), (B.17) and (B.18), we will get the result as follows

where is a positive constant. Then it concludes the proof.

B.5 Lemma 5 and its proofs

Lemma 5.

Note that the noise matrix can be rewritten as , where the entries of are i.i.d from . Moreover, there is . Thus together with Condition 3, the bounded , we only need to prove the upper of for an arbitrary .

Consider the two projection matrices and with an arbitrary and . Then we have

| (B.19) |

where the last inequality is due to Condition 1. Note that and thus we mainly prove the upper bound of , where

Directly applying Lemma 3 in She [2017], we can get

where and are the absolute constants. Let be that yields with the probability at least because of when . Together with (B.19) and Condition 3, we have

holds with the probability at least , which finishes the proof.

B.6 Lemma 6 and its proofs

Lemma 6.

Assume that and . Then for an arbitrary matrix there is

| (B.20) | |||

| (B.21) |

where .

On the one hand, note that thus we can get the last inequality in (B.20) immediately by the triangle inequality. Thus we mainly prove the first inequality in (B.20). For an arbitrary vector , there is

where we use the fact and . Denote that then we have

since and . It concludes the inequality (B.20).

On the other hand, by the definition of the operator norm, there is

where we use the fact and is the projection matrix onto the space spanned by the columns of . Thus we get the equation (B.21).

B.7 Lemma 7 and its proofs

Lemma 7.

We denote that for convenience then demonstrate the three inequalities as follows.

1. The upper bound of .

Note that and is the projection matrix onto the space . Thus we have

Applying Cauchy’s inequality to the above inequality, we can obtain

where is the nuclear norm of matrices. By the further simplification, there is

where we use Conditions 1 and 2 in the last inequality, and . Then we get that

with a positive constant .

2. The upper bound of .

Similar to the above argument, applying Conditions 1 and 2 yields

where the first inequality is due to the definition of the operator norm. And the last inequality is due to the rank of is no more than . Then we get

3. The upper bound of .

Recall that is the th eigenvalue of , and there is a decomposition as follows

Thus by Wely’s Theorem, we have

where we use the fact in the last inequality. By a further calculation, we can get

| (B.22) | ||||

Hereafter, we can use the similar argument as above. There are

| (B.23) | ||||

under Conditions 1 and 2. Combining (B.22) and (B.23), we can get

Thus it ensures that

which concludes the proof.

B.8 Lemma 8 and its proofs

Lemma 8.

Assume that Condition 1 holds then we have

where is the reduced rank estimator with oracle support set . That is

where the other rows excluding in are zero. Specially, the oracle reduced rank estimator with the support set and satisfies

By direct calculations, we have

| (B.24) |

On the one hand, utilizing the minimum of , we can obtain

| (B.25) |

where is the nuclear norm. Moreover, note that . Thus there is

| (B.26) |

In addition, utilizing Condition 1, we have

| (B.27) |

Combining these inequalities (B.25),(B.26) and (B.27), we can get

| (B.28) |

Furthermore, combining (B.28), (B.25) and (B.26), we have

| (B.29) |

with a positive constant .

B.9 Lemma 9 and its proofs

Lemma 9.

Denote by the reduced-rank estimation restricted in the row support set and rank , and define the event as follows

with , and . Assume that Conditions 1, 2 and the assumption hold. Then under the event , there are four cases as follows.

Case 1: and .

Case 2: and .

Case 3: and .

Case 4: and .

Here is the projection matrix onto the space , is the true rank of and the loss function . In addition, and are the th largest eigenvalue of and , respectively.

Recall the definition of the loss function . Moreover note that is the reduced-rank estimation restricted in row support set and rank thus we have

where the other rows in are zeros. Because is the reduced-rank estimator, directly applying Reinsel and Velu [1998, Theorem 2.2] yields that

where is the th largest eigenvalue of . For convenience, we denote that . It is the projection matrix onto the space . Moreover, note that there is

Therefore, we can obtain the difference between and as follows

| (B.31) |

In addition, we can rewrite as

| (B.32) |

because the maximum rank of is .

Then similar to the above argument and by some simplifications, we have

| (B.33) |

Combining (B.31), (B.32) and (B.33), we can obtain

| (B.34) | ||||

where we use the fact . Then we consider four cases as follows under the event

where has been defined in the above.

(1) Case 1: and . Directly applying the equation (B.34), we have

Then by Lemma 7, the above inequality can be bounded as follows

with a positive constant , where we use the fact with , and is the th eigenvalue of . Thus under event , there is

with some positive constant . Note that thus we can get

| (B.35) |

under the assumption , where is a positive constant.

(2) Case 2: and . Note that when . Thus directly applying (B.35), we have

| (B.36) |

with a positive constant .

(3) Case 3: and . Similar to the argument in Case 1, applying the equation (B.34) yields

Furthermore applying Lemma 7, we have

Then under the event , there is

Similar to Case 1, we have

| (B.37) |

under the assumption .

(4) Case 4: and . Utilizing again, there is

| (B.38) |

from the inequality (B.37). Moreover, note that and when . also is the th largest eigenvalue of . We rewrite the eigenvalue as for clarity. Therefore, the above four cases conclude the results.