The limit point in the Jante’s law process has an absolutely continuous distribution

Abstract

We study a stochastic model of consensus formation, introduced in 2015 by Grinfeld, Volkov and Wade, who called it a multidimensional randomized Keynesian beauty contest. The model was generalized by Kennerberg and Volkov, who called their generalization the Jante’s law process. We consider a version of the model where the space of possible opinions is a convex body in . individuals in a population each hold a (multidimensional) opinion in . Repeatedly, the individual whose opinion is furthest from the centre of mass of the current opinions chooses a new opinion, sampled uniformly at random from . Kennerberg and Volkov showed that the set of opinions that are not furthest from the centre of mass converges to a random limit point. We show that the distribution of the limit opinion is absolutely continuous, thus proving the conjecture made after Proposition 3.2 in Grinfeld et al.

Keywords: Jante’s law process, consensus formation, Keynesian beauty contest, rank-driven process, interacting particle system

Subject classification: 60J05, 60D05, secondary 60K35

1 Introduction

1.1 The multidimensional randomized Keynesian beauty contest

Let and be integers. Let denote Lebesgue measure on and let be a convex body, i.e. a closed convex subset of with non-empty interior. In particular, . For the moment, while describing the model studied in [2], we will also assume that is bounded so that , but later we will drop this assumption. We say that a random variable is uniform on , i.e. it is a random variable when its distribution is the probability measure . (This notion requires , of course.)

A discrete time Markov process , taking values in , called the multidimensional randomized Keynesian beauty contest was studied in [2]. In the sequel [4] a generalization of the process was studied which the authors called the Jante’s law process333The law of Jante is a literary caricature of the virtue in Scandinavian culture of not standing out from the crowd. It appeared in Aksel Sandemose’s satirical novel En flyktning krysser sitt spor, (A fugitive crosses his tracks), published in 1933. (see §1.4). In the present paper the process will take values in , so our setting is only a little more general than that of [2]; however, we prefer to retain the shorter name for the process.

If is either a finite sequence of points of , or a set of distinct points of , then we denote by its centre of mass, i.e.

We denote by the Euclidean distance between and in , and by

the open ball of radius centred at .

Let be a possibly random initial state. We will always assume that a.s. the points of are distinct. An informal description of each step of the Markov chain is that amongst points present at time , we choose the one that is furthest from the current centre of mass, and throw it out. After that, a new point arrives, distributed uniformly in , and replaces the thrown-out point, so that we have again points.

Formally, let be an i.i.d. sequence of random variables uniformly distributed on , denoted by , independent of the initial state . For each time in turn, let be the index of the furthest point of from , that is, is defined by

in case of a tie, choose uniformly at random among the tied indices444Any other way of breaking ties would also be acceptable since a.s. ties do not occur.. Define by

i.e., the point of that is furthest from the centre of mass of is removed and its place is taken by the new point . Note that although and depend continuously on the new point , they depend discontinuously on .

Let denote the core of the configuration , that is the set .

Definition 1.

We say that converges to some point if

It was shown in [2] that converges a.s. to a random limit point in the above sense; additionally, in the case , the distribution of has support . It was conjectured555The conjecture is stated immediately after [2, Proposition 3.2]. that the distribution of is, in fact, absolutely continuous with respect to the Lebesgue measure on ; see the appendix for the definition. The purpose of this paper is to prove this absolute continuity conjecture in the -dimensional setting described above.

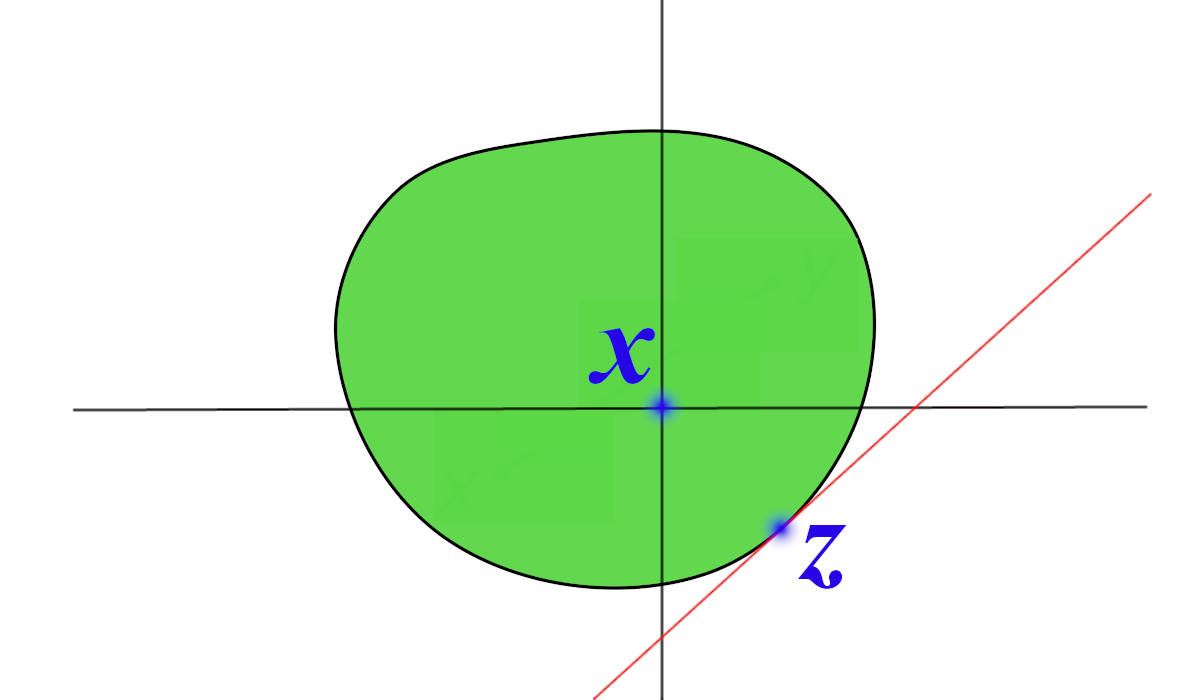

A.s. for every , is a sequence of distinct points, and it will be convenient to discard from the underlying probability space the null set where this fails. Hence, from now on, we work with a version of the process where for each the points of are surely distinct. In particular, the core process a.s. takes its values in the set of subsets of of cardinality . Assuming , we can ask what is the set of possible values of which would result in , that is, that we keep the newly sampled point in the core while throwing out one of the original points. The answer depends only on , and not on the point . The set of possible locations which could enter the core at time is denoted by

| (1) |

For later use, we extend the definition (1) to allow to be unbounded.

Observe that in the one-dimensional case is necessarily an interval ; and then is also a non-empty subinterval of . If the geometry of this set is a little more complicated, see e.g. Figure 1. Later, in Lemma 2, we will show that is in fact always the intersection of with a non-empty union of at most bounded open balls which only depend on . Moreover, always contains a nonempty open ball whose centre is . As a result, always has finite and positive Lebesgue measure, so it makes sense to sample a point uniformly from . In fact, conditional on and , the new point is uniformly distributed on .

1.2 Time-changed models

For convenience, we will work with a time-change of the process , namely the sequence defined by and for , , where is the increasing sequence of all times for which . The sequence is itself a Markov chain. It is an instance of a -valued Jante’s law process (defined below). When studying , there is no longer any reason to insist that be bounded, since we can describe the law of without making any reference to random variables. Instead, the definition involves sampling uniformly from sets of the form , which always have finite positive Lebesgue measure, regardless of whether is bounded. So in the following definition and for the rest of the paper we allow to be unbounded.

Definition 2 (-valued Jante’s law process ).

Let be any closed convex subset of with a non-empty interior. Let be any (possibly random) set of distinct points in . For each , sample a point uniformly from , conditionally independently of given , and set

| (2) |

where is the (a.s. unique) point which maximizes .

By definition, a -valued Jante’s law process is a Markov chain. When working with -valued Jante’s law processes, it is convenient to discard from our probability space the null set where for any either there is a tie in choosing , or . From the definition of , it is surely the case that , so .

By a slight modification of the proof in [2] we will show that even when is unbounded, the -valued Jante’s law process a.s. converges to a random limit point , in the sense that

Our strategy for proving that the limit point is an absolutely continuous random variable is to compare with another process, denoted by , which is just a -valued Jante’s law process with ; we call the Markov chain the scale-free core process. It eliminates the complicated effect of the boundary of and has the great advantage of being invariant in law with respect to scaling and translation.666An analogous modification of the original process was already used as a tool in [2, §3.4]. It will be useful to have notation for the points added and removed at each step of the scale-free core process :

Also let denote the a.s. limit of the process , in the sense of Definition 1.

1.3 Outline and results

In §2 we collect a number of basic results, including the fact that every -valued Jante process almost surely converges to a random limit (Proposition 1). We give a standalone proof because for the case where is unbounded, this is not a special case of the results of [2, 4], and because the required lemmas are needed again later in the paper.

In §3 we discuss a property of convex bodies called uniform geometry. This property is used later in the paper to avoid some geometric complications. Bounded convex sets have uniform geometry. We reduce the absolute continuity of the distribution of the limit point of a -valued Jante process to the case where is bounded.

Our first continuity result is for the scale-free core process:

Theorem 1.

For an arbitrary deterministic initial condition , where is any set of distinct points in , the distribution of is absolutely continuous.

Our proof of Theorem 1 is less straightforward than one might expect. The main difficulty is to show that a.s. all of the original points are eventually removed; we isolate this statement as Proposition 2 and prove it in §4 using a supermartingale argument, a trick using translational symmetry, and a compactness argument. Then in §5 we complete the proof of Theorem 1 by showing that the distribution of the limit is a mixture of absolutely continuous distributions. Each distribution in the mixture is seen to be absolutely continuous because it is a convolution with a uniform distribution over a set of positive Lebesgue measure.

In §6 we use another supermartingale argument and a coupling argument to deduce the absolute continuity of the distribution of the limit point for any -valued Jante’s law process.

Theorem 2.

Let be any convex body, and let be any set of distinct points of . Let be the limit point of the -valued Jante’s law process started at . Then the distribution of is absolutely continuous.

Of course this also shows that the distribution of the random limit of the original core process started at has an absolutely continuous distribution. Theorem 2 covers the original setting of [2] where , so it resolves the absolutely continuous distribution conjecture made in that paper. We remark that if is random, then the distribution of the limit point is still absolutely continuous since it is a mixture of such distributions. We also remark that because for any convex body .

In Appendix 3 we discuss the main obstacle to extending the Theorem 2 to a larger class of subsets . For example, if is a closed and bounded subset of whose boundary is a smooth compact hypersurface embedded in , then we can extend the definition of the -valued Jante process and check using the results of [4] that it converges almost surely to a random limit . But we do not have a proof that , which is certainly necessary for the absolute continuity of the distribution of . On the other hand, we show in Lemma 22 that if then the distribution of is absolutely continuous.

1.4 Related models

In the paper [4], the authors generalized the original model of [2] by allowing the common distribution of the new points to be an arbitrary absolutely continuous distribution on . They also allowed for more than one point to be replaced simultaneously. It was shown that if the distribution of has bounded support, together with some extra regularity assumptions, then a.s. a limit point exists. However, although the support of is certainly a subset of the support of , it may not be the whole of the support of . For example, if is uniform on and a.s. all coordinates of lie in , then for all , and after passing to the subsequence of times at which , we recover the original process with . In particular, in this case, the support of is . In case has unbounded support, [4] shows that a.s. either converges to a random limit point or , i.e. . However, no examples of distributions of are known to satisfy with positive probability. For an arbitrary common distribution of the random variables , and an arbitrary distribution of on , such that there is a positive probability that converges, one can ask whether the distribution of the limit conditional on its existence is absolutely continuous with respect to the distribution of the . We do not address this more general continuity problem in this paper, although it might be possible to extend our techniques to other cases where has an absolutely continuous distribution with a sufficiently well-behaved density.

In another paper [5], the authors studied asymptotic properties of a modified version of Jante’s law process. In this model, called the -contest, at each moment of time the point farthest from , where is the current centre of mass, is removed and replaced by an independent -distributed point; note that the case would correspond to the original Jante’s law process. Finally, in [6], a local version of the process was considered. In this version, vertices are placed on a circle, so that each vertex has exactly two neighbours. To each vertex assign a real number, called fitness. At each unit of time, the vertex whose fitness deviates most from the average of the fitnesses of its two immediate neighbours has its fitness replaced by a random value drawn independently according to some distribution . The authors showed that if has a uniform or a discrete uniform distribution, all fitnesses but at most one converge to the same limit. We would also like to mention that there is a related continuous-time model, called “Brownian bees”, which involves a fixed number of particles which perform independent Brownian motions, and branch from time to time simultaneously with the removal of the particle most distant from the origin, thus keeping the total number of particles constant; see e.g. [1] and [8]. It would be in the spirit of the current paper to identify extrema in the Brownian bees from the centre of mass of the swarm, rather than from the origin; and have exponential killing of the extreme bee with introducing a new bee at a random location.

2 Preliminaries

For any set we denote by the convex hull of , i.e. the smallest convex set containing . We denote by the boundary of and by the interior of . For any we denote by the -neighbourhood of , i.e. the set of points whose Euclidean distance to is less than .

Some basic facts about continuity of -valued random variables and continuity of Borel probability measures on are collected in the appendix. The main two facts that we will use are that any mixture of absolutely continuous random variables is absolutely continuous and that if an absolutely continuous random variable is conditioned on an event of positive probability then the conditioned random variable is absolutely continuous. We will see a simple argument that uses these two facts in the proof of Lemma 10 at the end of §3.

For any set of cardinality we let

and we define the following geometric functionals of :

| (5) |

We call the moment of inertia of . The functional serves as a Lyapunov function for the Jante’s law processes and . One can easily verify the following inequalities among the geometric functionals:

| (6) | ||||

Lemma 1.

Let be any set of distinct points in , and suppose . Then

| (7) | |||||

| (8) |

From (7) it follows that a point belongs to if and only if there exists such that . Moreover, if then any choice of which maximizes is also a choice which minimizes .

Proof.

Corollary 1 (Essentially Lemma 2.1 in [2]).

Let be a -valued Jante’s law process with (where may be ). Then for each .

Lemma 2.

Let , where . Then

| (9) |

Proof.

Lemma 3.

Let , where . Then

| (12) |

Proof.

Lemma 4.

Let , where and the are distinct. Then

| (15) |

Proof.

Let be a point of furthest from . Then lies on the line segment joining and , since . We have and . Therefore

Indeed, the boundary spheres of these two balls are tangent at the point . The result then follows from Lemma 2. ∎

Lemma 5.

Let , where and the are distinct. For each we have

Proof.

Lemma 6.

Let , where . Suppose for some , and . Let be a point of farthest from . Then

| (16) |

Proof.

Let be a point of farthest from , so that and

By the triangle inequality,

By Lemma 1 and equation (8) we have

The final strict inequality in (16) follows from the final inequality in (6).777In fact one could obtain , but the simpler lower bound given in (16) will suffice for the applications.

∎

The following estimate is well-known (see e.g. [7, Lemma 2.6]).

Lemma 7.

Let be a convex body. Let and . Then

Proof.

Since -dimensional Lebesgue measure is translation-invariant, we may assume w.l.o.g. that . Since is convex and contains , the dilation contains , so

Comparing volumes yields the desired inequality. ∎

Corollary 2 (Adapted from Lemma 2.3 and Lemma 2.5 in [2]).

Let be a -valued Jante’s law process, where is any convex subset of with non-empty interior. Let be the -algebra generated by . Then for every ,

| (17) |

Consequently,

| (18) |

Proof.

Suppose . Since is convex, . The new point in is distributed uniformly in , and by Lemmas 3 and 4 we have

Since , we have , so

where the second inequality follows from Lemma 7. When , we may take and in Lemma 6, so that inequality (16) becomes

| (19) |

The final consequence follows from the fact that (by Corollary 1) and the inequality for . ∎

Inequality (17) implies that a.s. converges exponentially fast.

Lemma 8 (essentially Lemma 2.5 in [2]).

Let . For any fixed choice of , there exists such that, a.s., for all sufficiently large .

Proof.

From the preliminary results established above it is now easy to recover the almost sure convergence result [2, Theorem 1.1] (for ) extended to the general setting of a -valued Jante’s law process ; we state it below as Proposition 1. For the case of a bounded convex body , this is in fact a special case of [4, Theorem 2]: the regularity assumption required by that theorem is satisfied by the uniform distribution on , as an immediate consequence of Lemma 7. In the case of unbounded the exponential decay of ensures that the process will not escape to infinity, a fact which was also implicitly used in [2, §3.4].

Proposition 1 (essentially Theorem 1.1 in [2]).

Let and . Let consist of distinct points in . Then there exists a random such that converges to a.s. in the sense of Definition 1.

It will be useful to know that if is small, then with high probability the -valued Jante’s law process never travels too far from .

Lemma 9.

Fix any and . Let and . Denote

Then

As a result,

as well.

Proof.

From Lemma 3 and (6), we have for every

Since for each , by applying the triangle inequality to the cases of the above displayed inequalities, we obtain

Now note that is the least natural number such that . As we showed in the proof of Lemma 8, , so with probability at least it holds for all that . Suppose that this event occurs. Applying the triangle inequality to the cases , we may bound the relevant increments by a geometric series. For every we have

For all the geometric series is bounded by . Applying the triangle inequality yet again and using gives the claimed bounds. ∎

3 Reduction to the case of uniform geometry

Following the terminology of [7, Ch. 3], a convex body is said to have uniform geometry when there exists some such that

| (20) |

(see [7, Ch. 3].) Since the volume depends continuously on , when is compact the infimum is achieved and is positive because is the closure of its interior. That is, every bounded convex body has uniform geometry. Examples of unbounded convex bodies with bounded geometry are itself, and any convex body which is the intersection of finitely many closed half-spaces. However, not every unbounded convex body has uniform geometry, see for example [7, Example 3.12].

Suppose is a convex body of uniform geometry, with and as in (20). Let denote the volume of the unit ball in , and define

| (21) |

Note that in the case we have , and in all other cases we have . For the case which was studied in [2], we have . By Lemma 7, using (20) and (21), for all and all we have

| (22) |

Recalling Lemma 3 and Lemma 4, for with we have

| (23) |

It follows from (22) and (23) that when ,

This means that conditional on , we may sample from the distribution of by rejection sampling with success probability bounded away from . That is, we repeatedly sample a point uniformly from until we obtain a sample that lies in , and for each trial the probability of success is at least . This property will be used several times. If did not have uniform geometry then the success probability for this rejection sampling procedure would not be bounded away from as ranges over all sets with sufficiently small . Fortunately, we may reduce Theorem 2 to the case where is bounded and therefore has uniform geometry, as follows.

Lemma 10.

Suppose the conclusion of Theorem 2 holds subject to the extra hypothesis that is bounded. Then it also holds without this hypothesis.

Proof.

Let be an unbounded convex body and consider the -valued Jante’s law process started at where is a set of distinct points of . For any , let . Define the random variable

Then (and the inf is a min) a.s., by Lemma 8 and Proposition 1. Let . Then by Corollary 1 and (6), we have for all . Suppose satisfies . Let be the -valued Jante’s law process started at , and define . We claim that and that the distribution of conditioned on is the same as the distribution of conditioned on . Indeed, and may be coupled by a maximal coupling, meaning that for each , on the event , conditional on we have with the largest possible probability. When and , this maximal coupling probability is . On the event that , this occurs for every . For then for every (since is convex), and therefore and so

It follows that for every

as required.

Let be the limit point of . By the hypothesis that Theorem 2 holds for bounded convex bodies, the distribution of conditioned on is absolutely continuous: it is an absolutely continuous distribution conditioned on an event of positive probability. Now the distribution of is a mixture of these conditioned distributions over the set of for which . Therefore the distribution of is indeed absolutely continuous (please see also Appendix 1). ∎

4 All original points are eventually removed, a. s.

In this section, we will study the -valued Jante’s law process . In particular, this is an instance of a -valued Jante’s law process where has uniform geometry. For some of the lemmas in this section, it takes very little extra work to make the proofs apply to subject to the uniform geometry assumption, and we will state them in that generality even though we will only apply them to the process . So for the whole of this section, we will assume that is a -valued Jante’s law process where is a convex body with uniform geometry and .

Let be the first time when all the original points of the configuration are removed, i.e.

| (24) |

with the usual convention that if there is no for which . We know from Proposition 1 that for every there exists a random such that for all we have , so if for some deterministic choice of it happened that then we would have , and the distribution of would not be absolutely continuous. Therefore Theorem 1 can only hold if it is true that a.s. It will be useful to prove this fact separately first.

Proposition 2.

a.s.

The rest of this section is devoted to the proof of Proposition 2.

In the case , i.e. , a.s. for each the set consists of two distinct points, which are equally likely to be removed at the next step. Thus in this simple case, is a geometric random variable, in particular a.s. finite.

The case is dealt with, so from now on we will assume that . Let be the volume of the unit ball in .

Let denote the -algebra generated by the process . Recall from Corollary 2 that

| (25) |

To complement this we need to bound the downward drift of the smallest inter-point distance .

Lemma 11.

Suppose that is a set of distinct points of such that . Then

Proof.

Next, for any set of distinct points in , define

Note that by (6), we have

Let be the space of subsets of of cardinality , with the obvious topology888 i.e. the topology which it inherits as a quotient of by the permutation action of the symmetric group , where is the subset consisting of sequences in which two or more terms coincide. Note that is not complete with respect to the Hausdorff metric.. For any , denote by the recentred and rescaled version of , defined by

| (26) |

We have , , and at the same time . For any , define

Then is invariant under translation and scaling, while is a compact subset of .

Our next goal is to show that for the -valued Jante’s law process , there is a constant such that a.s. the rescaled and recentred set visits the compact set infinitely often. The proof uses as a Lyapunov function.

Proposition 3.

There exist and , , such that on the event that and , we have

-

(a)

, and

-

(b)

.

Proof.

For part (a) we use inequality (25) and Lemma 11, along with (6) to compare and . This requires us to take .

For part (b), consider the ball “with holes” (see Figure 2)

where

and is the constant defined in (21), which depends on the geometry of .

Recall that . By Lemma 6 (with ), if , then

On the other hand, using Lemmas 3 and 4 with Lemma 7,

At the same time, the relative volume of the “holes” in is bounded. We have and , so we may use the hypothesis of uniform geometry to compare with . We find

Hence, . Next, on the event that ,

by (6). Let . Then

and thus

which equals provided . We see that both parts of the lemma hold when we take

∎

Let (where is the constant from Proposition 3). Since , and as , we get . Then define

Proposition 4.

The event occurs infinitely often a.s.

Proof.

First of all, by (6),

Indeed, by (6), we get that , while

For each let . By Proposition 3 we have that is a non-negative supermartingale for , for any fixed . From the supermartingale convergence theorem, it follows that a.s. converges as . Since on we have , where , , are from Proposition 3, we conclude that a.s. . As a result, returns to and hence also to infinitely often, a.s. ∎

For the remainder of this section, we focus on the process .

Lemma 12.

For every set of distinct points in , there exists a finite and a possible finite trajectory of the process , say , such that , , along the trajectory there are no ties, i.e. at each step there is a unique legal choice of point to remove, , and the added points are distinct and are not in .

Proof.

We will identify a trajectory meeting the conditions of the lemma through a combination of probabilistic and constructive reasoning. Note that the process , started at , a.s. obeys , implying that . Let be the least such that . Then a.s., and a.s. the points are distinct and not in . Therefore there exists some and a trajectory , with and for , such that , hence , and the points are distinct and not in . If then we are done. So from now on assume that .

The end of the construction falls into two cases, depending on whether is a furthest point in from the point

First, suppose we are in case 1, where is indeed a furthest point in from the point . If we had then we would also have and hence all points of would have to coincide, which was ruled out in the construction of . Therefore . Let , for some very small , chosen so that is not in . (This can fail only for finitely many values of .) Then is the unique furthest point of from its centre of mass, which is

To see this, note first that

while

Thus . Secondly, note that the ball contains the ball , and their boundary spheres meet only at the point . Hence for every . Hence the point is the unique point which may be removed, and we obtain . The trajectory is a permissible trajectory with no tiebreaks and no repeated points, and , as required.

Case 2 is the case where is not a furthest point in from the point . For the rest of the proof, we assume that we are in this case. We claim that if is sufficiently close to then from the trajectory we can obtain another permissible trajectory in which the arriving points are all perturbed by the vector . The perturbed trajectory is , where and for we have , where and is a point of furthest from . To say that the trajectory is permissible means that for each , so that . In fact, if is sufficiently close to then the corresponding points are removed at each step, by which we mean that , where either (if ), or (if ). To see this, note that each point or depends continuously on , as does . The (assumed) statement that is the unique point of furthest from is equivalent to a finite collection of strict inequalities: for each ,

It follows that when is sufficiently close to then for each ,

i.e. is the unique point of furthest from for each . In particular, the trajectory involves no tiebreaks when is sufficiently close to . By similar reasoning, since the trajectory involves no repeated points, the same is true of the trajectory when is sufficiently close to .

Having chosen a vector suitably close to , we now extend our two trajectories one further step, so that , i.e. is the translate of by the vector . To do this, we choose and . Then

| (27) |

Notice that in the translation which relates the two configurations, the roles of and the new point ( and respectively) are swapped. We may choose so that there is no tiebreak in either configuration when selecting the point furthest from the centre of mass. This is because the set of vectors which would cause such a tie is contained in a finite union of hypersurfaces of dimension less than , so we may choose as close as we like to but not in any of these hypersurfaces. From (27), we see that there are points and which are furthest from the centres of mass and respectively, and which are related by . Hence . Before proceeding, we must check that the trajectories and are permissible. This is where we use the assumption that we are in case 2, together with the continuity of all defined points as functions of . Let be a point of which is strictly further from than is from , and let . As , we have and , while , and . Therefore for close enough to we have

and

showing that both trajectories are indeed permissible.

Finally, by the same argument as in the first paragraph of this proof, there exists a possible trajectory such that , and having no tiebreaks, no repeated points, and no arriving points which were already in . There are now two possibilities: either , in which case we are done, or . In the latter case, consider the trajectory defined by for . It is also a permissible trajectory, being a translation of a permissible trajectory. Moreover, , and in particular , so that . Therefore is a trajectory satisfying the conclusion of the lemma, and we are done.

∎

Recall the following definition.

Definition 3.

Let and be two subsets of . The Hausdorff distance between them is defined as

Note that when and are both finite, then if and only if and have the same closure.

Lemma 13.

For every set , there is a finite , an , and a such that if has Hausdorff distance less than from then

Proof.

Let be any distinct points in , and let . Take a trajectory as provided by Lemma 12. Since at each step there is a unique choice of point such that maximizes the distance from , and there are only finitely many steps, there is an such that for all we have for any that

By making smaller if necessary, we may also assume that

Consider any perturbed trajectory where and for we have , and for each we have . Then one may prove by induction over that in the perturbed trajectory, the thrown out points correspond to the original points in the sense that for each , the index such that also satisfies . This is because the perturbation moves each point by a distance less than and also moves each centre of mass by a distance at most . It therefore alters corresponding distances by less than , and differences of distances by less than .

In particular, the points of are in one-to-one correspondence with points of so that corresponding pairs of points are at a distance less than . It follows that .

Finally, consider the random process started at . The probability that each new point , , lies in the ball is bounded away from , uniformly over all choices of that are -perturbations of . This is because the volumes of the sets are bounded above a priori in terms of , using the fact that

together with Lemma 3. When this occurs, we have . ∎

Lemma 14.

There exist and such that for every ,

Proof.

First, observe that since the process is time-homogeneous and invariant under translation and scaling, we have

where is defined by (26). So it suffices to prove that there exist and such that for all we have

This follows from Lemma 13, since for each point in the compact set , that statement specifies a neighbourhood of and constants , such that for all ,

Since is compact, there exists a covering of by some finite sequence of such neighbourhoods , and we may take

and

∎

We can now prove Proposition 2, which claims that a. s.

Proof of Proposition 2.

Starting from any configuration of distinct points in , the process a.s. eventually enters , by Proposition 4, say at stopping time . Let be the constant provided by Lemma 14. Inductively define for , by

For each , conditional on and , in time steps all the points of are removed, with probability at least , regardless of the configuration . Therefore with probability there exists a finite for which this event occurs. We then have , as required. ∎

5 Proof of Theorem 1

Without loss of generality, we assume that the initial state is deterministic. This is harmless since if for each deterministic choice of the limit exists a.s. and has an absolutely continuous distribution, then if instead is random, still exists a.s. and its distribution is a mixture of absolutely continuous distributions, which is necessarily absolutely continuous.

List the elements of in an arbitrary order as . Recalling that for , is the unique point of , we observe that for each we have

We discarded a null set to ensure that the points of the sequence are pairwise distinct. Thus for each , the unique point of is equal to for a unique index in the range . Moreover, the indices are pairwise distinct random variables since each point is removed at most once.

Lemma 15.

Fix any and any deterministic sequence of distinct indices such that for each we have and is the least positive integer such that . Let . Then the event that and is equivalent to the event that a certain finite collection of linear or quadratic inequalities are satisfied, which involve the coordinates of the random points , as well as the coordinates of the deterministic points .

Remark 1.

For example, take , , and w.l.o.g. , . Then on , , , we have and or and . See Figure 3.

These inequalities define a bounded semi-algebraic set999i.e., a set defined by a number of polynomial inequalities and equalities; in our case, a.s. these will be just inequalities. . (When , is a polytope, since the defining inequalities may be reduced to a collection of affine linear inequalities.) For some sequences , may be empty or have empty interior. Note that the boundary of is contained in a finite union of algebraic hypersurfaces where at least one of the defining inequalities becomes an equality. These hypersurfaces have trivial -dimensional Lebesgue measure. Thus has positive -dimensional Lebesgue measure if and only if it has a non-empty interior.

Let be the event that and . If then conditional on the sequence is distributed according to ; in particular it lies a.s. in the interior .

Define a -dimensional linear subspace of by

Consider the orthogonal projection of onto . We have

We conclude that if then for -a.e. , the set

has . Therefore we can sample a random variable by sampling first a random variable , then (conditional on ) sampling a random variable and setting .

Recall the definition of from (24) and let be the -algebra generated by the stopped process . Let be a random variable whose distribution conditional on is

such that is conditionally independent of given . That is to say, on the event , given , we let , independent of . Proposition 2, and the fact that ties a.s. do not occur, imply that a.s. holds for exactly one , so is well-defined. Since is the uniform distribution on a subset of of positive and finite -dimensional Lebesgue measure, the conditional distribution of on is a.s. absolutely continuous. This is a crucial property which we will use later.

We will now show that we can “perturb” the original path of new points by adding the same absolutely continuous random vector to each of them, without changing the distribution of the path. (Of course, this requires that the vector that we add is not independent of .) This implies that the distribution of the set is a mixture of distributions, each of which is the distribution of the translation by some absolutely continuous random vector of some set of distinct points. This is the key argument in showing that the limit point has an absolutely continuous distribution.

Define a new random sequence as follows.

Conditional on and on , the sequences and are identically distributed: both are random variables.

Let , then for let

For all we have

| (28) |

Moreover is a Markov chain with the same distribution as : by construction they have the same distribution up to the random time , and from time onwards, the transitions have the correct distribution by equation (28) together with the translation-invariance of the transition law of .

Therefore the sequence has the same distribution as the original sequence . Since a.s. converges to a limit , it also holds that a.s. converges; let be its limit. The distribution of coincides with the distribution of .

On the other hand, the distribution of is also the mixture of its conditional distributions on . But we have

and and are conditionally independent given . Thus the distribution of , conditionally on , is a distribution of a sum of two independent random variables, one of which (namely ) has an absolutely continuous distribution. It is well-known that such a sum is also an absolutely continuous random variable (see e.g. Theorem 2.1.16 in [3]). Therefore the unconditional distribution of is also absolutely continuous, being a mixture of absolutely continuous distributions. This completes the proof of Theorem 1.

6 Coupling and

In this section, we complete the proof of Theorem 2. By Lemma 10 it suffices to prove the absolute continuity of the limit point for a -valued Jante’s law process where is bounded. So we shall assume throughout this section that is bounded, and therefore has uniform geometry.

We will need an isoperimetric inequality for inner shells of convex bodies, for which we have been unable to find a reference. It concerns the following problem. Suppose you have a (possibly) hollow chocolate egg whose outer boundary is the boundary of a convex body. If all the chocolate is within distance of the outer boundary of the egg, what is the maximum quantity of chocolate that can possibly be contained within a ball of radius ? See Figure 4.

Lemma 16.

Let and let be a convex body in . For every , we have

| (29) |

where is the volume of the unit ball in , with the convention that .

Proof.

For the inequality holds with , since the set is a union of at most two intervals of length at most and therefore has length at most . Now assume that . Let . Consider any point . Then for some . Let be a supporting hyperplane through , meaning that . Then (as for any hyperplane through ) cuts at least one of the axis-parallel lines through at a point whose distance from is at most . It follows that there is a point of that lies between and on one of the axis-parallel lines through . The situation is illustrated in Fig. 5 below.

Thus is covered by the sets , where

where are the standard basis vectors of . Since , the orthogonal projection of onto a hyperplane orthogonal to has -dimensional Lebesgue measure at most . Each line parallel to that meets meets in at most two intervals, whose total length is at most . Hence for each . Summing over we get

∎

Lemma 16 will suffice for our purposes, but we remark that the sharp version of the inequality is as follows. (A proof is given in the appendix.)

Lemma 17.

Let and let be a convex body in . For every , we have

| (30) |

where is the volume of the unit ball in .

Let be a bounded convex body. For any set of distinct points of define

and for any set of distinct points of that is not entirely contained in , define

For a -valued Jante’s law process we define

Lemma 18.

There exists (depending on , , and ) such that for any set of distinct points of and any ,

and hence almost surely for infinitely many we have

Proof.

We may assume without loss of generality that has at most one point in . Indeed, a.s. all new points are not in , and a.s. as , so there exists an such that and therefore contains at most one point; now apply the lemma with . It follows from these assumptions that a.s. for every . Likewise we may assume that , where and are the constants used to specify the uniform geometry of , so that by Corollary 1 and inequality (6) we have for all .

We will use Lemma 16 to get an upper bound for the expectation of the positive part of the increment of .

| (31) |

Let

By (6) we have and by Lemma 3 we have . The numerator of the RHS of (31) may be rewritten as

where the first equality above uses Tonelli’s theorem, the next inequality uses Lemma 3, and the final inequality uses Lemma 16. On the other hand, by our assumption that , we have the uniform geometry bound

where is the constant from (21). Therefore the RHS of (31) is bounded above by

where is a constant depending on , and . Thus we have shown that

| (32) |

By almost the same argument,

Define

(note that ) and the stopping time

We aim to prove that is a supermartingale. Noting that and , inequality (17) in Corollary 2 implies

Combining this with (32), we find that on the event , we have

(Note that we used the fact that whenever when we went from the fifth to the sixth line.) We therefore have

| (33) |

Using the first part of Corollary 2, we find

so under the same condition that we also have

| (34) |

Inequality (33) shows that the random sequence is a supermartingale that is bounded below by , so it almost surely converges, but inequality (34) shows that it can only converge to a value less than or equal to . Therefore a.s., and indeed a.s. for infinitely many . ∎

Recall the definition of from before Lemma 18.

Lemma 19.

Let101010Think of small and large. and . Then there exist and (both depending on and ) such that for any ,

Proof.

Before we proceed with the formal proof, let us explain the idea behind it. The main ingredient is that there is a positive probability that for some number of consecutive steps the new point arrives very close to the centre of mass of the existing configuration, relative to its diameter. When this occurs, the moment of inertia decreases by a definite multiplicative factor at each step. As a result, after steps the square root of the moment of inertia will have decreased by at least a factor . At the same time, the convex hull of the configuration stays inside a bounding region that grows from step to step, by a geometrically decreasing sequence of increments. It can be arranged that the bounding region never gets closer to than , and hence .

We will combine ideas from the proofs of Corollary 2 and Lemma 9. Define

and

For each , define the event by

We have

so

We have because . Hence, using Lemmas 3, 4 and 7 (as in the proof of Corollary 2), we have

Therefore

Now suppose that and suppose that the event occurs. Our goal is to show that .

Using the condition together with , see (6), we obtain for each that

Then by inequality (19) from the proof of Corollary 2, we have

By induction we find that for ,

and in particular

| (35) |

For every , since ,

so

Since

where

it follows that

Moreover,

so

| (36) | |||||

Taking square roots of both sides of (35) and dividing by (36) we obtain

as required. ∎

Lemma 20.

Let . Then there exist and (both depending on , and ) such that for any set of points in such that , and any , we have

Proof.

The proof is very similar to the proof of Lemma 19. We take and then make the same choices of constants in terms of and as we did there:

Let be the unique point in . This time, the good sequence of events whose probability is at least is

Instead of applying Lemma 4, we apply Lemma 5 to see that

This requires us to check that , which follows from . It follows as before that on the event we have

It also follows as before that on the events and we have

Throughout the rest of the proof, we replace each set of the form by . Note that so that on the events we obtain

and it follows that

as before, and hence

| (37) |

On the other hand, if then

contrary to (37). We have shown that on the event , the event occurs with probability at least , and when it does, we have , as required. ∎

Corollary 3.

Suppose is a convex body in with uniform geometry and let be a -valued Jante’s law process. There exists (depending on and ) such that for any set of distinct points of , conditional on , a.s. there exists such that .

Proof.

Consider a -valued Jante’s law process started at . Define the stopping time

Note that if then . Let be as in Lemma 18, so that a.s. infinitely often . Note that if and then . So it suffices to show that a.s. .

We define a sequence of stopping times . Let

Since a.s., and a.s. all new points are in , we have a.s. . Let and be as provided by Lemma 20. Now inductively define for

Corollary 4.

Suppose is a convex body in with uniform geometry and let be a -valued Jante’s law process. Let be given. Then for any set of distinct points of , conditional on , a.s. there exists such that .

Proof.

We combine Lemma 19 with Corollary 3. Consider a -valued Jante’s law process started at . Now let and be as given by Lemma 19, applied to the specified in the statement of Corollary 4. Define a sequence of stopping times as follows. Set , and then inductively for

By Corollary 3, a.s. for all . By Lemma 19, for each ,

so

By letting and using the continuity of probability, as the RHS converges to zero, we arrive to the required conclusion. ∎

We can now give the proof of Theorem 2.

Proof.

In Lemma 9, we take . Define

On the event that , we have

and hence, using (6) to compare with ,

Now by Lemma 3,

Define an increasing sequence of stopping times as follows. Set and then inductively for

(If for some we have then for all we also have .) For each , on the event that , firstly a.s., by Corollary 4, and then . Hence a.s. there is a finite such that but .

We have shown that the distribution of is a mixture of distributions, each of which is (for some , , and ) the conditional distribution of given , and . Each such distribution is equal to the conditional distribution of for the -valued Jante’s law process started at , conditioned on the positive probability event that for all , . By Theorem 1, this distribution is absolutely continuous. Thus the distribution of is a mixture of absolutely continuous distributions and is therefore absolutely continuous. ∎

Acknowledgment

The research of S.V. is partially supported by the Swedish Science Foundation grant VR 2019-04173 and the Crafoord Foundation grant no. 20190667. S.V. would like to acknowledge the hospitality of the University of Bristol during his visits to Bristol. The research of E.C. is supported by the Heilbronn Institute for Mathematical Research. We would like to thank John Mackay for pointing us to the notion of uniform geometry in [7] and Rami Atar for pointing out the relevant Brownian bees model. Finally, we would like to thank the anonymous referee for many useful comments and recommendations, in particular the suggestion to explain what can be done in the non-convex case.

References

- [1] Addario-Berry, Louigi; Lin, Jessica; Tendron, Thomas. Barycentric Brownian bees, Ann. Appl. Probab. 32 (2022), no. 4, 2504–2539.

- [2] Grinfeld, Michael; Volkov, Stanislav; Wade, Andrew R. Convergence in a multidimensional randomized Keynesian beauty contest, Adv. in Appl. Probab. 47 (2015), no. 1, 57–82.

- [3] Durrett, Rick. Probability: theory and examples. Fifth edition. Cambridge University Press (2019).

- [4] Kennerberg, Philip; Volkov, Stanislav. Jante’s law process, Adv. in Appl. Probab. 50 (2018), no. 2, 414–439.

- [5] Kennerberg, Philip; Volkov, Stanislav. Convergence in the p-contest, Journal of Statistical Physics 178 (2020), 1096–1125.

- [6] Kennerberg, Philip; Volkov, Stanislav. A Local Barycentric Version of the Bak-Sneppen Model, Journal of Statistical Physics 182:42 (2021), 17 pp.

- [7] Leonardi, Gian Paolo; Ritoré, Manuel; Vernadakis, Efstratios. Isoperimetric Inequalities in Unbounded Convex Bodies. Memoirs of the American Math. Soc., no. 1354, Vol. 276 (2022).

- [8] Siboni, Maor; Sasorov, Pavel and Meerson, Baruch. Fluctuations of a swarm of Brownian bees, Phys. Rev. E 104 (2021), 7 pp.

Appendix 1: Absolute continuity of probability distributions

Here are the basic facts which we use about absolutely continuous -valued random variables.

-

1.

Definitions. Let be the Borel -algebra of Euclidean space . Let be a Borel-measurable random variable on a probability space , meaning that for every , . The distribution of is the unique Borel probability measure on such that for every we have . (It suffices to check that this holds for every open set , or for every closed set.) We call both and absolutely continuous when is absolutely continuous with respect to the Lebesgue measure . This means that for every Borel set ,

Equivalently, there exists an element of norm such that for every Borel set we have

This element is called the density of , or the density of . Every element of has a Borel-measurable representative, so we may assume that is Borel-measurable. The density of an absolutely continuous random variable is not necessarily representable by a continuous function, and if happens to be equipped with a topology which generates , the absolute continuity of as a random variable is unrelated to the continuity of as a function.

-

2.

Mixtures of absolutely continuous random variables are absolutely continuous. Suppose that is a Borel probability measure on and is a random absolutely continuous probability measure defined on whose density with respect to Lebesgue measure is distributed according to . Then for any Lebesgue measurable set we have (by Tonelli’s theorem)

so the mixture is an absolutely continuous probability measure with density . To see that the integral of this density with respect to is , take above. Even if a.s. has a density, it need not be true that has a continuous density.

-

3.

Conditioning on positive probability events. Let be a Borel probability measure on and an -valued random variable on with distribution . If is an event such that , then the conditional distribution of given is also absolutely continuous. Indeed, let . Then

so that implies , so that where is the Lebesgue measure.

Appendix 2: Proof of Lemma 17

Proof.

By replacing with , which does not alter the set whose volume is to be estimated, we may assume that is bounded.

Next, we reduce to the case where is a polyhedron. Let . We claim that there is a convex polyhedron (with finitely many facets) such that . To see this, let be any point in the interior of and let denote the radial projection about from onto the unit sphere that is centred on . For each point and each supporting hyperplane of at , the radial projection is a neighbourhood of in the sphere . Since is compact, some finite collection of such projections covers it. The corresponding finite collection of support hyperplanes defines a suitable polyhedron (by taking the intersection of the half-spaces that they bound which contain ).

For each , there exists a point such that , and a supporting hyperplane of such that passes through and if then is orthogonal to . Then the translate of by distance in the direction is a supporting hyperplane of and it follows that

Since , we have

It follows that

Hence if inequality (30) always holds for a bounded convex polyhedron with finitely many faces in place of , (and in place of ), then by taking the limit as , we obtain (30) for a general bounded convex body and hence also for any convex body .

Finally, we prove (30) in the case where is a bounded convex polyhedron which has finitely many faces. Suppose the facets of are . (A facet is a face of co-dimension one.) For each , let be the outward-pointing normal vector of , and let the facet be contained in the hyperplane , so that

Let be the cut-set of , which is the set of points in that are equidistant from at least two points in . Note that since is contained in the union of the finite set of hyperplanes which bisect the dihedral angles of pairs of hyperplanes . Also, . So to prove (30), if suffices to define a volume-preserving injection from to .

Partition the open set into finitely many pieces , where each piece consists of the points whose closest facet of is a given facet . is an open convex polyhedron contained in the -neighbourhood of the facet .

The map will translate each point of by a non-negative multiple of , where the multiple may vary from point to point. Specifically, for any , define

and

Then define

Note that if is also in then and , since both and are convex. Hence . Informally, the map slides each line segment of the form as far as possible in the direction (parallel to the line segment) such that it remains a subset of . Each of these line segments has length at most . It follows that every point in the image of is within distance of the boundary of . The restriction of to is a smooth volume-preserving map, since both and depend smoothly on , and in an appropriate coordinate system its Jacobian matrix is upper unitriangular.

Finally, we must check that is an injection. From the description in terms of sliding line segments, we see that the restriction of to each piece is an injection. Secondly, if , then the unique closest facet of to is . Therefore the images of distinct pieces under are disjoint and we are done.

∎

Appendix 3: Beyond convex bodies

For a bounded measurable set , we will explain below how some reasonable geometric assumptions on , which are more general than convexity, are sufficient to define the -valued Jante process (so that it is almost surely well-defined for all times) and to show that it converges almost surely to a random limit. However, it appears to be more difficult to show that the limit point has an absolutely continuous distribution, even in the nicest possible non-convex setting, where is a region bounded by a compact smooth hypersurface in . In this case, the boundary of is Lebesgue null, so to prove absolute continuity of the distribution of the limit point one must prove in particular that the limit point almost surely lies in the interior of . In Lemma 22 below, which applies to a reasonable class of non-convex bodies, we show that the only obstacle is proving that the limit point almost surely lies in the interior of .

First, the notion of -valued Jante process may be extended to any subset satisfying the following condition:

Condition A: is Lebesgue measurable and non-empty, and , where denotes Lebesgue measure on . (In particular this implies that .)

Condition holds for a non-empty Lebesgue measurable subset if and only if for every and we have . For example, condition holds whenever is is the closure of its interior.

Lemma 21.

Suppose satisfies condition A and is a set of distinct points of . Then the Lebesgue measure of is positive.

Proof.

Let be a point of such that , i.e. is a point of that is as far as possible from . Let () be another point of . Since lies in the closure of the ball , which is internally tangent to the ball at , but , we see that lies in the (open) ball and hence there is an such that

and hence by Lemma 2 we have . Condition A implies that has positive Lebesgue measure, so has positive Lebesgue measure, as required. ∎

Under condition , the -valued Jante process is well-defined starting at any set of distinct points of . Indeed, when is any set of distinct points in , it makes sense to sample a point uniformly from in order to define , because this set has positive but finite Lebesgue measure. Moreover, almost surely will also consist of distinct points.

To ensure that the -valued Jante process almost surely converges to a limit point, it is helpful to assume a stronger condition.

Definition 4.

Let be an -valued random variable. Any subset is called regular with parameters if for every and we have

is called regular if for every , there exists a such that the subset is regular (with any parameters).

This regularity condition is Assumption 2 in Kennerberg and Volkov [4]. Specializing to the case at hand, we introduce

Condition B: is a bounded measurable subset of such that and such that the random variable whose distribution is is regular.

We remark that condition B is closely related to the uniform geometry condition that we defined for the case of convex sets. Under conditions A and B, the -valued Jante process is a special case of the process studied by Kennerberg and Volkov, and [4, Theorem 2] implies that the -valued Jante process almost surely has a (random) limit in the closure of .

To make our coupling approach to generalize to a non-convex set , in addition to conditions A and B, we need two more conditions:

Condition C: is the closure of its interior.

Condition D: The limit point of the -valued Jante process almost surely lies in the interior of .

Unfortunately, we do not know whether in general conditions A, B and C imply condition D. In some special circumstances other than the convex case, it might be possible to prove a substitute for Lemma 16 and hence also a substitute for Corollary 4. For example, if is bounded by a compact smooth hypersurface, then conditions A, B and C hold, and one might also hope for a substitute for Lemma 16 to hold with uniform constants because the principal curvatures of the bounding hypersurface would be bounded.

Lemma 22.

Suppose satisfies conditions A, B, and C. Consider the -valued Jante process with initial state consisting of distinct points of . Then if condition D also holds, the distribution of is absolutely continuous.

Proof.

Assume conditions A, B, C, and D hold. Take a countable cover of the interior of by distinct open balls,

where each . Then define a random element of by letting where is minimal such that . By the assumptions, almost surely at least one such index exists.

For any and , let be the event that for all , . Let be the earliest time such that holds. (Note that is not a stopping time, but it is almost surely finite.) Then the distribution of is a mixture of the conditional distributions of conditioned on and , as ranges over the countable set

It therefore suffices to prove that each of these conditional distributions is absolutely continuous. So suppose that that and satisfy . The conditional distribution of given and is obtained from the conditional distribution of given only by further conditioning on the positive probability event that is not contained in any which precedes in the enumeration. So it suffices to prove that the conditional distribution of given is absolutely continuous.

The conditional distribution of given is a mixture of the distributions of given and , where the mixture is with respect to the distribution of conditioned on the positive probability event . So it suffices to prove the absolute continuity of the conditional distribution of given and , for every configuration such that .

Using a coupling argument, we will show that this distribution is absolutely continuous with respect to the distribution of the limit point of -valued Jante process started at , which is absolutely continuous by our Theorem 2. Since the Jante process is homogeneous, we may replace with without loss of generality in the rest of the proof.

Let be a -valued Jante process started in configuration , and let be a -valued Jante process started in configuration . Define the events

and

We claim that . Indeed, there is a coupling of and such that for all times up to and including the first time when , or for all if there is no such time. (After such a time, we may let and evolve independently.) Let be the limit point of , which exists almost surely. Let be the (defective) positive Borel measure defined by

(The equality here is a consequence of the coupling.) Since , we deduce that the conditional distribution of given is equal to the conditional distribution of given . (Indeed, both are obtained by normalizing .) Finally, note that is absolutely continuous with respect to the unconditional distribution of , with the Radon-Nikodym derivative at being . Finally, the unconditional distribution of is absolutely continuous, by Theorem 2.

Putting this all together we conclude that has an absolutely continuous distribution. ∎