The Russian Option with A Random Time Horizon

Abstract

This paper is intended to provide a unique valuation formula for the Russian option with a random time horizon; in particular, such option restricts its holder to make their stopping decision before the last exit time of the price of the underlying asset at its running maximum. By the theory of enlargement of filtrations associated with random times, this pricing problem can be transformed into an equivalent optimal stopping problem with a semi-continuous, time-dependent gain function whose partial derivative is singular at certain points. Despite these unpleasant features of the gain function, with our choice of the parameters, we establish the monotonicity of the free boundary and the regularity of the value function, which in turn lead us to the desired free-boundary problem. After this, the nonlinear integral equations that characterise the free boundary and the value function are derived. We also examine the solutions to these equations in details.

1 Introduction

Consider an ideal world with only one stock and one bond in the market which is free of friction (that is, the market involves no transaction costs and no restriction in selling short). We assume the stock and bond price processes, defined on a filtered probability space , are given by the SDEs

| (1.1) | |||

| (1.2) |

and is capturing the running maximum of the stock price process, i.e.

where is a standard Brownian motion process started at zero under measure , is the interest rate, is the volatility coefficient. This is a risk neutral model so that the discounted stock price is a martingale under measure ; in other words, is the risk neutral measure.

Then, there is this option entitles its holder to sell the stock at the highest price it has ever been traded during the time frame between its purchase time and its exercise time or the last time the stock price at its running maximum (whichever comes first); otherwise, it becomes worthless. How much are you willing to pay for this option?

When a contingent claim is valued, it is conventional to assume that there is no risk that the counter-party will default, that is, the counter party will always be able to make the promised payment. However, this assumption is far less defensible in the non-exchange-traded (or over-the-counter) market and the importance of considering default risk in over-counter markets is recognised by bank capital adequacy standards, see [6, Page 300] for a detailed introduction of default risk. According to [9, Pages 11 and 190], the contract given above can be viewed as the defaultable Russian contingent claims, with its default time modelled by the last exit time and by assuming that the default market is complete, such contract is hedgeable.

With the aid of the classic pricing theory, the question posed above can be formulated into a precise mathematical form (clearly, any rational agent will want to maximise the stopping reward):

| (1.3) |

with random time and the supremum taken over all the stopping times . The American option with payoff function is called Russian option, where we let and in the infinite and finite time formulation respectively; such option belongs to the class of put option with aftereffect and discounting, see [16, Page 626]. It is worth mentioning that there is no restriction to assume that (and ). The indicator function in (1.3) imposes, of course, some additional interpretation to the original Russian option pricing problem, for instance, the possibility of the option being withdrawn prematurely by the option writer, see [3]. The mathematical structure developed here is also potentially useful for study of insider trading, but this subject will not be dealt with directly.

Some useful references in this research area are [1, 2, 5]. In particular, the time-dependent reward problem was also studied in Du Toit, Peskir and Shiryaev [1, 2], Glover, Peskir and Samee [5].

The remainder of this paper is organised as follows:

In Section 2, we first look into question (1.3) as and introduce yet another Markov process to reduce the dimension of the problem, see [16] for similar treatment. Then, in Subsection 2.2, we examine the solution of the free-boundary problem and verify it as the smallest superharmonic function that dominates the gain function. Similar infinite-horizon problems have been studied in the work [3, 14] without reducing dimensions.

In Section 3, analogously, one can reduce the dimensions of the problem for . With our choice of parameters in problem (1.3), one can avoid the singularity of the partial derivative and the establishment of the continuous value function is within easy reach, which in turn implies the existence of the optimal stopping rule. After this, we turn our attention to analysing the structure of the continuation and stopping sets and Assumption 3.10 is made principally to guarantee the monotonicity of the boundary in Lemma 3.13. Subsection 3.4 covers the theoretical and numerical results concerning the price that the investor is willing to pay for this presuming contract.

2 Infinite-time Horizon

2.1 Reformulation and Basics

The main optimal stopping problem can be reformulated as follows by the measurability of stopping time and smoothing lemma:

| (2.4) |

First of all, we investigate the property of Azéma supermartingale associated with .

Proposition 2.1.

In our setting, the following formula holds for ,

where .

Proof.

Remark 2.2.

Therefore, (2.4) gets the form

| (2.5) |

With some additional effort, we can reduce the above two-dimensional problem (2.5) into a one-dimensional problem. To do so, we introduce the probability measure , which satisfies and the process .

It is a well-known fact that the strong solution of (1.1) is

| (2.6) |

for , where and are standard Brownian motions under measure and respectively.

Corollary 2.3.

The process is a (time-homogeneous) strong Markov process on the phase space with instantaneous reflection at the point , which satisfies the SDE

| (2.7) |

where and is the standard Brownian motion under measure . See [16, Page 770].

Proof.

(i) By exploiting Itô formula, we have

where we set and it only changes value as arrives at the boundary point , to stress this fact, we write ; after which, upon letting , SDE (2.7) follows.

(ii) Next in line is to show that is the instantaneous reflection point (i.e. the process spends zero time at -a.s.), that is,

for each . Via taking expectation under measure and using Fubini’s theorem,

where the last equality holds via the fact that the probability density function of exists, implying that is a continuous random variable, and that the probability of a continuous random variable equals a certain value is . The desired statement then follows from the simple fact that for non-negative random variables , if , then a.s.

(iii) The process has the property of being time-homogeneous, in the following sense:

where , . On the other hand, of course,

Since and

under measure , it follows by weak uniqueness of the solution of the SDEs that , that is, the process is time-homogeneous 222We write simply as hereafter whenever needed, so that when , is written as .. ∎

It then follows that increases on the set , with the infinitesimal generator

and if function and its limit exists, then .

Summarising our findings so far, we see that the problem (2.5), by using the process and change-of-measure, could be reduced to the following optimal stopping problem333For notational convenience, we simply write instead of hereafter.

| (2.8) |

2.2 The Free-boundary Problem

We are now ready to turn our attention to the free boundary problem but first for the sake of brevity, we define the gain function .

To begin with, we invoke the local time-space formula to obtain

where is the local time of at the level given by

after which, the important observation follows, that is, the further away gets from , the less likely the gain function will increase upon continuing, which suggests that there exists a point such that the stopping time

| (2.9) |

should be optimal in the problem (2.8), such fact will soon be confirmed.

It is then not far-fetched to ask whether or not the stopping time is finite.

Corollary 2.4.

The stopping time is finite.

Proof.

444We essentially follow the proof from [15, Page 116], the original proof is missing the minus sign.To prove for , it suffices to show that

To begin with, for ,

Then, let , and set event

Note that the events are independent and the crucial observation is that

Since , it follows that . An appeal to the second Borel-Cantelli lemma asserts that , and consequently that as desired. ∎

By reviewing [11, Page 40, Theorem 2.7], we know that the next task is to find the smallest superharmonic function that dominates and the unknown point by solving the corresponding free boundary problem:

| (2.10) | |||

| (2.11) | |||

| (2.12) | |||

| (2.13) | |||

| (2.14) | |||

| (2.15) |

We proceed to solve the free-boundary problem, after which, we prove that its solution coincides with the value function in (2.8) and is unique.

First, we apply the infinitesimal generator of to (2.10) and obtain the Cauchy-Euler equation as follows

| (2.16) |

from which, we know the solution gets form

| (2.17) |

By inserting (2.17) into (2.16), we obtain the following quadratic equation

| (2.18) |

whose roots are given by

where , . The general solution of (2.10) therefore equals

| (2.19) |

where and are arbitrary constants. An exploitation of conditions (2.11) and (2.13) on (2.19) gives us

so that

and by using (2.12), we then know that satisfies the following transcendental equation

| (2.20) |

Thus, we have arrived at the following theorem.

Theorem 2.5.

Proof.

(i) To prove the first part of Theorem 2.5 is to verify that . Notice that this is the same as showing that is the smallest superharmonic function dominating .

We begin by showing that for all . Let , so that from (2.12), we have

We then wish to show that the stationary point is the global minimum of in so that and thereby, proving that in this domain. For this, we take the second derivative of and obtain

where the strict inequality follows from the fact that , , and , indicating the convexity of function .

An appeal to the second derivative test tells us that as and for every , the stationary point is the global minimum point and thus demonstrating for all

Next we are ready to show that for all . From (2.21), it is fairly obvious that is on and , where

and therefore, we exploit the local time-space formula to obtain

| (2.22) |

where the first equality follows via the smooth-fit condition (2.12) and the second equality holds as satisfies the normal reflection condition (2.13).

Since in , we have

where we have used the fact that to conclude that the first term is negative, and for the second one. This, together with (2.10), shows that

| (2.23) |

everywhere on but . As , we thus have

| (2.24) |

where the first inequality follows from the first observation that , the second inequality holds via (2.22) and (2.23), and moreover, is a continuous local martingale.

Remember that a stopped martingale does not always remain a martingale, but for bounded stopping times, it always preserves its martingale property. Therefore, let be a bounded stopping time, for so that .

Then, taking the expectation under measure gives us

Now, let , so that . We invoke Fatou’s lemma to obtain

after which, we take the supremum over all stopping times of , together with (2.8), the desired assertion, that , suggests itself for all .

To finish off, we have to show that for all . Let for and be the finite stopping time defined in (2.9). Then, set in (2.22) so that

of which, taking the expectation under , upon using the same argument as before yields and letting ,

Furthermore, we conclude that, in the view of the fact that and (2.8),

for all , which, joining with the fact that , proving that the equality holds true. With being finite, [11, Theorem 2.7, Page 30] then provides us with the positive answer for being optimal.

(ii) It thus remains to show the second part of the Theorem 2.5, that is is unique, i.e. the equation (2.20) has only one root. Let

for . Then, upon using , we have

where the strict inequality holds via , and , which implies that the map is decreasing. To apply the intermediate value theorem, we need to further estimate the value of the endpoints:

where the first strict inequality follows by .

Let , then as , we have

| (2.25) |

With a little more effort, we could determine the sign of ,

from which, together with , we know that the first term of (2.25) heads towards more rapidly than the second term heading towards and thus, . Finally, we appeal to the intermediate value theorem, together with the fact that is decreasing, establishing the uniqueness of . ∎

3 Finite-time Horizon

3.1 Reformulation and Basics

In this section, we consider problem (1.3) in the finite time horizon and by the same arguments as that in Section 2, it can be reformulated as

| (3.26) |

Once again, some general facts of the Azéma supermartingale associated with random time to start the ball rolling. For notational convenience, we set555Not to confuse this with .

where and .

Proposition 3.1.

Let be the Azéma supermartingale of random time . Then

| (3.27) |

where is the process introduced in Corollary 2.3.

Proof.

Remark 3.2.

As the reader may have discovered, we have not yet defined properly if the process does not exceed level at all on , given that . However, it should now be clear that in such case, by Proposition 3.1, so that there is nothing to prove and thus the definition shall not concern us. Another more convenient way for this is to simply define the , see [8, Page 296], after which, the same result follows.

Proposition 3.3.

The function satisfies the PDE for .

| (3.29) |

Proof.

To prove (3.29), we first apply Itô’s formula and obtian

| (3.30) |

Then, recall the Doob-Meyer decomposition of the Azéma supermartingale, that is,

| (3.31) |

moreover, the measure is carried by the set .

The following result is simple yet useful, which we state for easy reference.

Corollary 3.4.

Both maps and are decreasing.

For the sake of brevity, we set the gain function

We are now in the position to reduce the original problem (3.26) to one-dimension by using the measure and generalise it by the strong Markov property of the process , that is

| (3.32) |

where is a stopping time of the diffusion process with under for given and fixed.

3.2 The Free-boundary Problem

In order to formulate and describe the free-boundary problem, it is convenient to introduce the following sets.

Definition 3.5.

The continuation set and the stopping set are defined respectively as

| (3.33) | |||

| (3.34) |

and we define the first entrance time of the stopping set , denoted as , as follows

| (3.35) |

Remark 3.6.

In the finite-time case, we have a.s, thus the condition is automatically satisfied for all .

Having defined stopping time , another natural challenge is to determine the optimality of . To do so, we begin by showing that the value function is continuous.

Lemma 3.7.

The value function is continuous on .

Proof.

We first show that (i) is continuous on for each given and fixed. Take any in , and let be a stopping time such that and that

and set , we see that

Noting that is decreasing (see Lemma A.2) and the time-homogeneous property of process , we then obtain

| (3.36) | ||||

| (3.37) |

where the last inequality follows from

| (3.38) |

Hence, by letting and , , the dominated convergence theorem (see (A.81) for the uniform integrability of ) yields

which finishes the first part of the proof.

We then show that (ii) is continuous for all . For this, we note that for all and ,

| (3.39) |

where the second inequality holds by

and the fourth inequality follows via the triangle inequality, the fifth inequality is immediate from (3.38) and the seventh one follows from

where the last term is the martingale under probability measure ; and the ninth inequality is due to the mean value theorem for so that implies a.s., while the last two steps are due to the fact that

and (2.6); in addition, note that function is bounded by for (see A.80) and the boundedness of the second term in the last inequality can be verified via the same fashion as in (A.81). By letting ,

after which statement (ii) follows. ∎

Lemma 3.8.

The stopping time is optimal.

Proof.

By Lemma 3.7 and [11, Corollary 2.9, Page 46], the stopping time defined as

is optimal (with the convention that the infimum of the empty set is infinite666We assume that if , ..) for the following problem

so that , where its corresponding stopping set is defined as . Furthermore, observe that

such that,

which implies that , and the desired claim follows. ∎

It will be shown in the next section that the continuation region and the stopping region could also be defined as

| (3.40) | |||

| (3.41) |

where is the unknown optimal stopping boundary, it then follows that can be rewritten as

We are now ready to formulate the following free-boundary problem.

3.3 The Continuation and Stopping Sets

Since the gain function is a continuous function whose derivative in is not continuous, we apply the local time-space formula on and obtain

| (3.48) |

where we set

| (3.49) |

and is a martingale.

By combining the above computation and using the fact that satisfying (3.29), we therefore have (3.49) rewritten as follows

Then, by taking the expectation under and applying the optional sampling theorem to get rid of the martingale part, we find that

| (3.50) |

We first investigate the map by a direct differentiation in , which yields

| (3.51) |

from which one sees that there exists a wide range of parameters for to be decreasing.

Remark 3.9.

The map being decreasing is rather crucial for showing the monotonicity of , the continuity of and the smooth-fit condition.

For the purpose of proving the properties mentioned in Remark 3.9, from now on, we assume:

Assumption 3.10.

Parameters and can be chosen so that the map is decreasing.

Lemma 3.11.

The continuation set is left-connected and non-increasing with respect to time .

Proof.

We shall show that for fixed and , implies .

We begin by recalling that

and for , it follows that

| (3.52) | |||

| (3.53) | |||

| (3.54) |

Let be the optimal stopping time for so that by (3.50) and (3.52)-(3.54),

where the first equality holds as , and are identically distributed and the last inequality holds by the fact that both and are decreasing on . Hence, we reach the following conclusion

| (3.55) |

indicating that if a point , then we have , which implies that , proving the initial claim. ∎

From (3.55), the following statement does not come to us as a surprise, that is the map is decreasing on .

Lemma 3.12.

The stopping set is right-connected and up-connected.

Proof.

The right-connectedness of the stopping set is another direct consequence of (3.55), since

that is, implies .

To justify its up-connectedness, we first take and such that . Then, by the right-connectedness of the exercise region, we have for any . If we now run the process from , we cannot hit the level to compensate the negative integrant in (3.50) before exercise as , which means that the local time term in (3.50) is 0 and the integrand is negative. Therefore, it’s optimal to exercise at and we have established the up-connectedness of the exercise region . ∎

Lemma 3.13.

The map is decreasing on .

Proposition 3.14.

All points for belongs to the continuation set .

Proof.

The proof follows, in fact, from the verbal statement, by exercising below , the option holder receive a null payoff, whereas waiting would have a positive probability of collecting a strictly positive payoff in the future.

A more detailed yet simple proof of this is that, from (3.50), we know that for , all integral terms on the right-hand side are nonnegative. ∎

We also recall the solution to the infinite time horizon optimal stopping problem, where the stopping time is optimal and is proved to be true, we therefore conclude that all points with for belong to the stopping set and that as is finite, so is .

By taking advantage of our findings so far, we can draw the conclusion that the continuation set and the stopping set indeed equal (3.40) and (3.41) respectively.

We close this section by constructing the continuity of the optimal stopping boundary .

Proposition 3.15.

The optimal stopping boundary is continuous on and .

Proof.

We first show that (i) is right-continuous. Let us fix and take a sequence as . Since is decreasing on , the right-limit exists. Remember that is closed so that its limit point is contained in , it then follows, together with (3.41), that . However, the fact that is decreasing suggests that and therefore, is right-continuous as claimed.

We then show that (ii) is left-continuous. Assume that, for contradiction, there exists such that . Then, fix a point .

| (3.56) |

for each where and . Knowing that the value function satisfies

and that

we have

Now recall that is decreasing and hence

| (3.57) |

in .

Using (3.56) and (3.57), we find that

and since is strictly negative in (as ), we set

so that

Via an integration by parts, we have

where the second equality follows from (3.43).

From Lemma 3.7 and the fact that the gain function is continuous on , we know that

and from (3.47), it follows that

Then, we observe that

where the third inequality holds via (A.81). Finally, let and an application of the dominated convergence theorem shows

where the first equality is due to the fact that , which is a contradiction, as belongs to the stopping set , indicating that such point cannot exist. Therefore, by combining statements (i) and (ii), we have established the continuity of on .

(iii) It remains to take care of the final piece of the claim, that is, .

According to Proposition 3.14, we must have . Assume that, such that a point exists on and let be an arbitrarily fixed point in the interval with . Rerunning the proof of (ii) with the above modifications, upon letting , we thus have arrived at the contradiction, that is

but the definition of the stopping set tells us that , which may allow us to conclude that . ∎

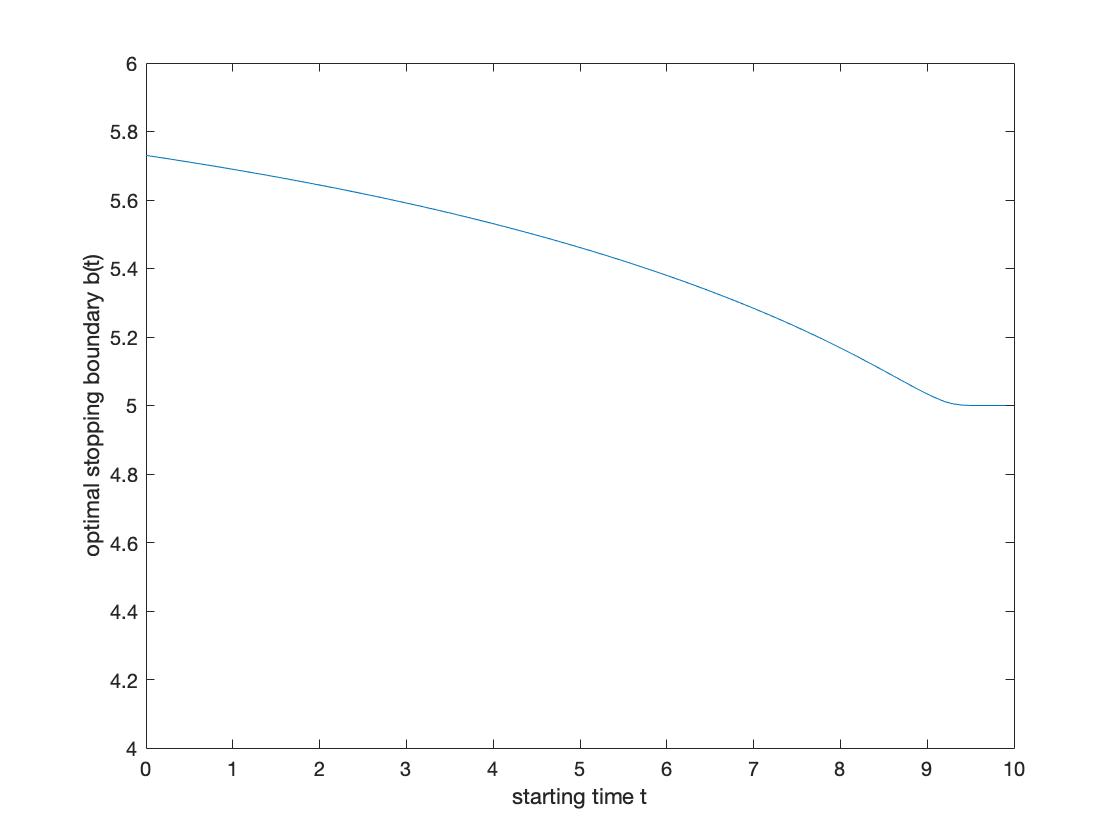

3.4 The Optimal Stopping Rule

Before we turn to presenting the main result, let us first complete the promise given in section 3.2, namely, to verify conditions (3.44)-(3.45) for the value function.

Lemma 3.16.

(Smooth-fit Condition) The value function is differentiable at the optimal stopping boundary and

whenever for .

Proof.

Let be given and fixed and set . Knowing that , let so that . Since

we have

| (3.58) |

and taking the limit as shows that

To prove the reverse inequality, let be the optimal stopping time for , so that

where the second inequality holds via the facts that ( because of the definition of the optimal stopping time) and that

and the third inequality follows from

and by mean value theory for , the last equality follows. Note that implies so that is bounded by .

Lemma 3.17.

The normal reflection condition holds, that is

Proof.

We begin by noticing that from (3.32) and the construction of the process

| (3.60) |

and that, in fact, there exists such that the map is increasing on in the sense that .

It then follows, from the view of (3.60), that is increasing on , meaning that for all , and moreover, since the value function is on the continuation set, we have is continuous on .

Assume that, for contradiction, there exists so that . Let be the optimal stopping time for and let for . Then, we apply Itô’s formula and the optional sampling theorem to obtain

Now in order to complete the proof, we need to further establish the martingale property of

| (3.61) |

Let us check the martingale property claimed in (3.61) for all :

where the first equality follows from the definitions of and the value function , the second and the fifth equalities are immediate from the strong Markov property of the process whereas the fourth equality holds by smoothing lemma as , and thereby, proving the martingale property.

With the aid of the above observation, we then obtain

which implies that

In particular, , which, together with the assumption that for all , tells us that

| (3.62) |

By the solution of (2.7), equation (3.62) and the optional sampling theorem, we see that

| (3.63) |

As for all , (3.63) implies that , which is not possible in the sense that the optimal stopping boundary and , proving the desired assertion. ∎

With a bit more effort, we can verify the following result to apply the local time-space formula freely later.

Corollary 3.18.

Let the function . Then

| (3.64) | |||

| (3.65) | |||

| (3.66) | |||

| (3.67) |

where .

Proof.

From [11, Page 409], we know that to verify (3.65) is to show that is locally bounded on for each compact set in . In , we have in the sense that satisfies . As in , , which is continuous on the compact set and hence, the range of is bounded as claimed.

Moving down the list, (3.67) follows from

where the first two terms on both regions are nonnegative and since the continuous function is in because of the -property of , the partial derivatives , and exist and are continuous, whereas as ,

whose continuity is immediate, so are the latter two terms in . ∎

Here is, finally, the result we have been waiting for.

Theorem 3.19.

Proof.

We follow, essentially, [11].

(i) We prove that the unknown optimal stopping boundary and value function indeed satisfy (3.68) and (3.69) respectively.

First of all, via an application of the local space-time formula on , we obtain

| (3.70) | ||||

| (3.71) | ||||

where is the local time process of on the curve given as follows

and the second equality holds by lemma 3.16 and lemma 3.17 and moreover,

is a martingale.

By setting , using that and taking the -expectation, we obtain by the optional sampling theorem

which is the desired result (3.69).

(ii) We now establish the uniqueness of the optimal stopping boundary .

First, assume that there exists a decreasing function , which solves (3.68) and satisfies for all and let

| (3.72) |

for . The following equalities then emerge by (3.72), the strong Markov property of and smoothing lemma:

which can be easily reshuffled into

| (3.73) |

Then, define the following function

and notice that since solves (3.68), it follows that and thus is continuous on .

Next in line, we reconstruct the continuation region and the stopping region by the means of

Since equals in the continuation set ,

With the verification being similar as Corollary 3.18, we manage to apply the local time-space formula to obtain

where is the martingale under measure .

Inspiring by (3.71), it seems only natural to investigate whether is differentiable at for each . And if we had known that

| (3.74) |

we would have directly obtained

and then consequently,

| (3.75) |

To derive (3.74), we consider the stopping time

and by setting in (3.73), we find that

where the second equality holds as and the third equality follows from (3.48) in the sense that for all , and the fifth equality holds by the definition of the stopping time , after which, (3.74) and (3.75) are fairly immediate.

By using (3.75) and considering the stopping time

and taking the expectation under , together with the optional sampling theorem, we have

and then recalling the value function in (3.32), we find that

| (3.76) |

for all .

With the above observation in mind, we are now ready to prove the first relation between and , that is, on .

Let for and consider the stopping time

By replacing in (3.71) and (3.75) with and taking the expectation under , we have

and from (3.76), we know that

that is

and since for all , it follows that , proving that for all .

In order to complete the proof, we must show that equals .

Assume that, for contradiction, there exists such that and pick a point .

Consider the stopping time

By replacing in (3.71) and (3.75) with and taking the expectation under , we have

Knowing that as , we find that

but in suggests otherwise, we have reach a contradiction and thereby establishing the uniqueness of .

The theorem is completely proved. ∎

4 Additional Remarks

Problem (3.32) can be further simplified as ,

| (4.77) |

Remark 4.1.

Lemma 4.2.

The value function is lower semi-continuous on .

Proof.

Since is continuous and bounded and the flow is continuous, it follows that the map is continuous (and thus, l.s.c). The value function, as the supremum of a lower semi-continuous function, is therefore lower semi-continuous. See [1, Page 6]. ∎

Corollary 4.3.

The stopping time is optimal.

Proof.

Remark 4.4.

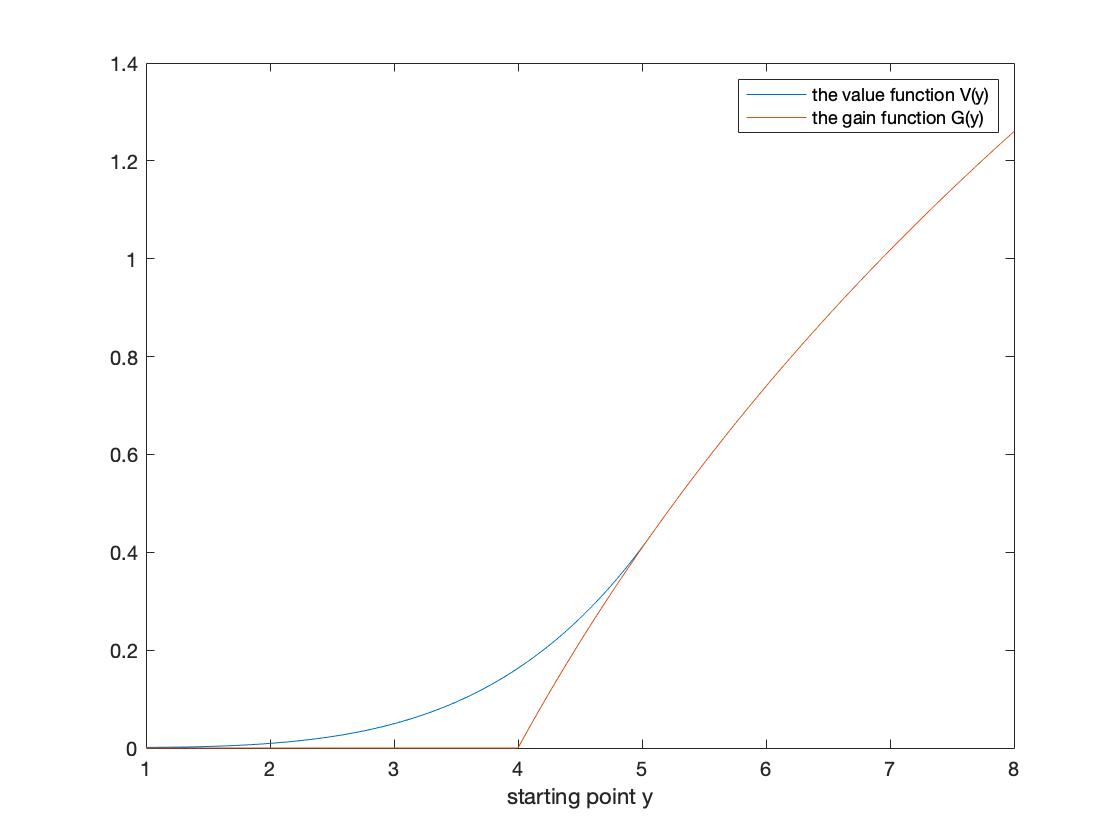

Figure 2 seemingly has a flat tail for , this is because the plot function in Matlab has automatically rounded the number to decimal places; but if vpa function is used to recover their values, we see that

Appendix A Computations Associated with Azéma Supermartingale

1. For notational convenience, we set:

2. The derivative of w.r.t time :

| (A.78) |

3. The derivative of w.r.t. space :

| (A.79) |

4. The derivative is bounded for and :

| (A.80) |

Note that for , but observe that as , which is decreasing much faster.

5. Useful Results for the Proof of Smooth-fit Condition

Lemma A.1 (For Chapter 4).

As , almost surely.

Proof.

By construction of and the definition of ,

Note that so that

Let and for notational convenience. As , (recalling that ),

where the inequality follows from the map being decreasing, and since is a lower function for standard Brownian motion under measure , so is , implying that , together with the fact that a.s, we know a.s. ∎

6. Property of the Value Function

Lemma A.2.

The map is decreasing.

Proof.

By the time-homogeneous property of process , for ,

and since the map is decreasing, we have is decreasing. Moreover, is decreasing so that the supremum is taken over a smaller set as increases and that by definition, is decreasing. ∎

7. The second derivative of w.r.t space :

8. The Uniform Integrability of

To apply the dominated convergence theorem, we observe that

| (A.81) |

where the first inequality holds as , and the last inequality follows from Young’s inequality and the random variable has the probability density function given as follows

We further estimate the following

We therefore, in a somewhat lengthy way, have proven that is dominated by a positive integrable random variable.

References

- [1] Du Toit, J., Peskir, G. and Shiryaev, A.N., 2008. Predicting the last zero of Brownian motion with drift. Stochastics: An International Journal of Probability and Stochastics Processes, 80(2-3), pp.229-245.

- [2] Du Toit, J. and Peskir, G., 2009. Selling a stock at the ultimate maximum. The Annals of Applied Probability, 19(3), pp.983-1014.

- [3] Gapeev, P.V. and Li, L., 2022. Optimal stopping problems for maxima and minima in models with asymmetric information. Stochastics, 94(4), pp.602-628.

- [4] Ghomrasni, R. and Peskir, G., 2004. Local time-space calculus and extensions of Itô’s formula. In High Dimensional Probability III (pp. 177-192). Birkhäuser, Basel.

- [5] Glover, K., Peskir, G. and Samee, F., 2011. The British Russian Option. Stochastics An International Journal of Probability and Stochastic Processes, 83(4-6), pp.315-332.

- [6] Hull, J. and White, A., 1995. The impact of default risk on the prices of options and other derivative securities. Journal of Banking and Finance, 19(2), pp.299-322.

- [7] Mansuy, R. and Yor, M., 2006. Random times and enlargements of filtrations in a Brownian setting (Vol. 1873). Berlin: Springer.

- [8] Meyer, P.A., Smythe, R.T. and Walsh, J.B., 1972, January. Birth and death of Markov processes. In Proceedings of the Sixth Berkeley Symposium on Mathematical Statistics and Probability (Vol. 3, pp. 295-305).

- [9] Elliott, R.J., Jeanblanc, M. and Yor, M., 2000. On models of default risk. Mathematical Finance, 10(2), pp.179-195.

- [10] Nikeghbali, A., 2006. An essay on the general theory of stochastic processes. Probability Surveys, 3, pp.345-412.

- [11] Peskir, G. and Shiryaev, A., 2006. Optimal stopping and free-boundary problems (pp. 123-142). Birkhäuser Basel.

- [12] Peskir, G., 2005. A change-of-variable formula with local time on curves. Journal of Theoretical Probability, 18(3), pp.499-535.

- [13] Peskir, G., 2007. A change-of-variable formula with local time on surfaces. In Séminaire de probabilités XL (pp. 70-96). Springer, Berlin, Heidelberg.

- [14] Shepp, L. and Shiryaev, A.N., 1993. The Russian option: reduced regret. The Annals of Applied Probability, 3(3), pp.631-640.

- [15] Shepp, L.A. and Shiryaev, A.N., 1995. A new look at pricing of the” Russian option “. Theory of Probability and Its Applications, 39(1), pp.103-119.

- [16] Shiryaev, A.N., 1999. Essentials of stochastic finance: facts, models, theory (Vol. 3). World scientific.