Wilks’ theorems in the -model

Abstract

Likelihood ratio tests and the Wilks theorems have been pivotal in statistics but have rarely been explored in network models with an increasing dimension. We are concerned here with likelihood ratio tests in the -model for undirected graphs. For two growing dimensional null hypotheses including a specified null for and a homogenous null , we reveal high dimensional Wilks’ phenomena that the normalized log-likelihood ratio statistic, , converges in distribution to the standard normal distribution as goes to infinity. Here, is the log-likelihood function on the vector parameter , is its maximum likelihood estimator (MLE) under the full parameter space, and is the restricted MLE under the null parameter space. For the corresponding fixed dimensional null for and the homogenous null with a fixed , we establish Wilks type of results that converges in distribution to a Chi-square distribution with respective and degrees of freedom, as the total number of parameters, , goes to infinity. The Wilks type of results are further extended into a closely related Bradley–Terry model for paired comparisons, where we discover a different phenomenon that the log-likelihood ratio statistic under the fixed dimensional specified null asymptotically follows neither a Chi-square nor a rescaled Chi-square distribution. Simulation studies and an application to NBA data illustrate the theoretical results.

Key words: -model; Bradley–Terry model; Growing dimensional hypothesis; Likelihood ratio statistic; Wilks’ theorem.

The -model, a name coined by Chatterjee et al. (2011), is an exponential family distribution on an undirected graph with the degree sequence as the sufficient statistic. Specifically, the model assigns each node with its intrinsic degree parameter and postulates that random edges, for , occur independently with connection probabilities

| (2) |

where is the number of nodes in the graph. The -model can be viewed as the undirected version of an earlier -model [Holland and Leinhardt (1981)] and has been widely used to model degree heterogeneity in realistic networks [e.g., Park and Newman (2004); Blitzstein and Diaconis (2011); Chen et al. (2021)].

Since the number of parameters grows with the number of nodes and the sample is only one realized graph, asymptotic inference is nonstandard and turns out to be challenging [Goldenberg et al. (2010); Fienberg (2012)]. This stimulate great interests in exploring theoretical properties of the -model and some are known now, including consistency of the maximum likelihood estimator (MLE) [Chatterjee et al. (2011)], its central limit theorems [Yan and Xu (2013)] and conditions of the MLE existence [Rinaldo et al. (2013)]. Asymptotic theories are also established in generalized -models [e.g., Perry and Wolfe (2012); Hillar and Wibisono (2013); Yan et al. (2016); Graham (2017); Mukherjee et al. (2018); Chen et al. (2021)]. However, likelihood ratio tests have not yet been explored in these works and their theoretical properties are still unknown.

The likelihood ratio statistics play a very important role in parametric hypothesis testing problems. Under the large sample framework that the dimension of parameter space is fixed and the size of samples goes to infinity, one of the most celebrated results is the Wilks theorem [Wilks (1938)]. That says minus twice log-likelihood ratio statistic under the null converges in distribution to a Chi-square distribution with degrees of freedom independent of nuisance parameters, where is equal to the difference between the dimension of the full parameter space and the dimension of null parameter space. This appealing property was referred to as the Wilks phenomenon by Fan et al. (2001). Since the dimension of parameter space often increases with the size of samples, it is interesting to see whether the Wilks type of results continue to hold in high dimension settings. In this paper, we investigate Wilks’ theorems for both increasing and fixed dimensional parameter testing problems in the -model. Our contributions are as follows.

-

•

For two increasing dimensional null hypotheses for and , we show that the normalized log-likelihood ratio statistic, , converges in distribution to the standard normal distribution as , where is a known number. Here, is the log-likelihood function on the vector parameter , is its MLE under the full parameter space , and is the restricted MLE under the null parameter space. In other words, is approximately a Chi-square distribution with a large degree of freedom.

-

•

For a fixed , under the specified null , , and the homogenous null : , we show that converges in distribution to a Chi-square distribution with respective and degrees of freedoms, as the number of nodes goes to infinity. That says the high dimensional likelihood ratio statistics behave like classical ones as long as the difference between the dimension of the full space and the dimension of the null space is fixed.

-

•

The Wilks type of results are further extended into a closely related Bradley–Terry model for paired comparisons [Bradley and Terry (1952)], which assumes that subject is preferred to (or wins) subject with probability . However, when testing , with a fixed , a different phenomenon is discovered, in which in the Bradley–Terry model neither follows asymptotically a Chi-square nor a rescaled Chi-square distribution as in Sur et al. (2019).

To the best of our knowledge, this is the first time to explore Wilks’ theorems in both models with an increasing dimension. Our mathematical arguments depend on the asymptotic expansion of the log-likelihood function, up to the fourth order. Three innovated techniques are developed to analyze the expansion terms. The first is the central limit theorem for the sum of quadratic normalized degrees , where is the degree of node . The second is a small upper bound of a weighted cubic sum , which has an additional vanishing factor in contrast to the order of . The third is the consistency rate of the restricted MLE and the approximate inverse of the Fisher information matrix under the null space. In the case of fixed dimensional testing problems, we further establish the error bound between the MLE and the restricted MLE having an order of in terms of the maximum norm, and derive an upper bound of the absolute entry-wise maximum norm between two approximate inverses of the Fisher information matrices under the full space and the restricted null space. These technical results are collected in Lemmas 1, 2, 4, 5, 6, 10 and 12.

0.1 Related work

Hypothesis testing problems in random graph models have been studied from different perspectives, including detecting a planted clique in an Erdös–Rényi graph [Verzelen and Arias-Castro (2015)], goodness-of-fit tests in stochastic block models [Lei (2016); Hu et al. (2021)] or testing whether there are only one community or multiple communities [Jin et al. (2021)], testing between two inhomogeneous Erdös–Rényi graphs [Ghoshdastidar et al. (2020)]. However, the powerful likelihood ratio tests are not investigated in these works.

For an adjusted -model in which the connection probability in (2) has a rescaled factor with a known parameter , Mukherjee et al. (2018) considered a homogeneous null hypothesis with all being equal to against an alternative hypothesis with a subset of strictly greater than . Such hypotheses imply that the connection probability for any pair lies between and . Mukherjee et al. (2018) proposed three explicitly degree-based test statistics: , and a criticism test based on , and established their asymptotic properties under some conditions. Their problem settings are different from ours. First, their null hypothesis is that all parameters are equal to zero while ours cover a wide range of parameter testing problems including both fixed and increasing dimensions that are more practical relevant. Second, their test statistics do not involve the MLEs while ours are likelihood ratio tests that are most powerful in the simple null according to the well-known Neyman-Pearson lemma. Since likelihood ratio statistics depend on unknown MLEs, it needs to bridge the relationship between MLEs and observed random edge variables and turns out to be more challenging. It requires to develop a central limit theorem for the sum of weighted quadratic degrees and analyze various remainder terms in the expansion of as mentioned in the proofs of our theorems.

We note that the -model and the Bradley–Terry model can be recast into a logistic regression form. Under the “large , diverging ” framework in generalized linear models, Wang (2011) obtained a Wilks type of result for the Wald test under a simple null when . In our case, , not , where the dimension of parameter space is and the total number of observations is . In a different setting, by assuming that a sequence of independent and identical distributed samples from a regular exponential family, Portnoy (1988) showed a high dimensional Wilks type of result for the log-likelihood ratio statistic under the simple null. For logistic regression models with asymptotic regime , Sur et al. (2019) showed that the log-likelihood ratio statistic for testing a single parameter under the null , converges to a rescaled Chi-square with an inflated factor greater than one. In contrast, our results do not have such inflated factors and cover a wider class of hypothesis testing problems.

The rest of the paper is organized as follows. The Wilks type of theorems for the -model and the Bradley–Terry model are presented in Sections 1 and 2, respectively. Simulation studies and an application to NBA data are given in Section 3. Some further discussions are given in Section 4. Section 5 presents the proofs of Theorems 1 and 2. All other proofs including the proofs of Theorems 3 and 4 as well as those of supported lemmas and are relegated to the Supplemental Material.

1 Wilks’ theorems for the -model

We consider an undirected graph with nodes labelled as “”. Let be the adjacency matrix of , where denotes whether node is connected to node . That is, is equal to if there is an edge connecting nodes and ; otherwise, . Let be the degree of node and be the degree sequence of . The -model postulates that all , , are mutually independent Bernoulli random variables with edge probabilities given in (2).

The logarithm of the likelihood function under the -model in (2) can be written as

where . As we can see, the -model is an undirected exponential random graph model with the degree sequence as the exclusively natural sufficient statistic. Setting the derivatives with respect to to zero, we obtain the likelihood equations

| (3) |

where is the MLE of . The fixed point iterative algorithm in Chatterjee et al. (2011) can be used to solve .

With some ambiguity of notations, we use to denote the Hessian matrix of the negative log-likelihood function under both the -model and the Bradley–Terry model. In the case of the -model, the elements of () are

| (4) |

Note that is also the Fisher information matrix of and the covariance matrix of . We define two notations that play important roles on guaranteeing good properties of :

| (5) |

where and are equal to the minimum and maximum variances of over , and .

We first present Wilks’ theorems in parameter testing problems with an increasing dimension. We consider a specified null for with , where for are known numbers, and a homogeneous null . We assume that the random adjacency matrix is generated under the model with the parameter . When , the null , becomes the so-called simple null. Recall that denotes the restricted MLE of under the null parameter space.

Theorem 1.

-

(a)

Under the null , with , if , the log-likelihood ratio statistic is asymptotically normally distributed in the sense that

(6) where and .

-

(b)

Under the homogenous null , if , the normalized log-likelihood ratio statistic in (6) also converges in distribution to the standard normality.

The condition imposed on in Theorem 1 is used to control the increasing rate of . If all are different not too much, and the condition in Theorem 1 (a) becomes . Further, the condition in Theorem 1 (b) is stronger than that in Theorem 1 (a). This is partly due to that use a unified consistency rate in Lemma 7 that holds for any under the specified null. We note that consistency of the MLE in Chatterjee et al. (2011) is based on the condition that all parameters are bounded above by a constant while asymptotic normality of the MLE in Yan and Xu (2013) needs the condition: . In contrast, the condition here seems weaker. In addition, some intermediate results in Lemmas 1, 3, 4 and 7 are built under weaker conditions. For instance, the consistency rate of in Lemma 4 only requires .

The following corollary gives the smallest to guarantee Wilks’ type of results, which only requires far larger than a logarithm factor to the power of .

Corollary 1.

If is bounded by a constant and , the normalized log-likelihood ratio statistic in (6) converges in distribution to the standard normality under both specified and homogenous null hypotheses.

We describe briefly the idea for proving Theorem 1 here. We apply a fourth-order Taylor expansion to and at point , respectively. With the use of the maximum likelihood equations and the asymptotic representations of and (see (29) and (31)), the first-order and second-order expansion terms in the difference can be expressed as the difference between and ( under the homogenous null; see (41)) and several remainder terms, where is the bottom right block of , and is the last elements of . The left arguments are to show that the difference is approximately a Chi-square distribution with a large degree of freedom and various remainder terms tend to zero. The aforementioned technical results in Lemmas 3–9 are used to bound remainder terms.

By using a simple matrix in (79) to approximate , one can find that the main term includes a sum of a sequence of normalized degrees in a weighted quadratic form, i.e., , where . For single , is asymptotically a Chi-square distribution and for any pair is asymptotically independent. But for all , the terms in the sum are not independent.

Note that . By exploiting the independence of the triangular matrix of , the variance of can be calculated as

where and . Because the variance of is

where is the probability of node connecting node given in (2) and , we have

It follows that if , the limit of the ratio of the variance of to is . In view of the weak dependence of , this sum can be approximated by the Chi-square distribution with a large degree of freedom, as stated in the following lemma.

Lemma 1.

Under the -model, if , then is asymptotically normally distributed with mean and variance , where .

The above lemma shows that the normalized sum converges in distribution to the standard normality for arbitrary tending to infinity in the case of that is a constant. The proof of Lemma 1 is technical. The quadratic centered degree sequence is not independent and also not the commonly seen mixing sequences such as -mixing, -mixing and so on. As a result, classical central limit theorems for independent random variables or dependent random variables [e.g., Peligrad (1987); Withers (1987)] can not be applied. Further, it is not a natural martingale. Observe that and . This is analogous to the property of vanishing conditional expectations in one-sample -statistics [e.g., Hall (1984)] and the quadratic form [e.g., de Jong (1987)], where for a sequence of independent random variables and Martingale theory are used to derive the central limit theorem of the sum . Since there are three indices in the sum , the methods of constructing martingale in Hall (1984) and de Jong (1987) can not be used here. For the sake of obtaining its asymptotic distribution, we divide into two parts:

| (7) |

The first summation in the right-hand side of the above equation scaled by varnishes while the second summation can be represented as a sum of martingale differences with a delicate construction. Then we can use Martingale theory [e.g., Brown (1971)] to obtain its central limit theorem, whose details are given in the supplementary material.

Next, we present Wilks’ theorems for fixed dimensional parameter hypothesis testing problems. We consider the specified null for and the homogenous null , where is a fixed positive integer.

Theorem 2.

Assume that and is a fixed positive integer.

-

(a)

Under the null , the minus twice log-likelihood ratio statistic converges in distribution to a Chi-square distribution with degrees of freedom as goes to infinity.

-

(b)

Under the homogenous null , converges in distribution to a Chi-square distribution with degrees of freedom as goes to infinity.

Theorem 2 says that the log-likelihood ratio enjoys the classical Wilks theorem in the case that the difference between the full space and the null space of the tests is fixed. As mentioned before, the condition imposed on restricts the increasing rate of and is fully filled when is a constant. The proof of Theorem 2 needs additional technical steps, in contrast to the proof of Theorem 1. As mentioned before, it requires to bound in Lemmas 12 and 15 and to evaluate the maximum absolute entry-wise difference between two approximate inverse matrices in Lemmas 10 and 13. Further, it needs to carefully analyze the differences between remainder terms under the full space and the null space since we do not have a scaled vanishing factor as in Theorem 1.

2 Wilks’ theorems for the Bradley–Terry model

In the above section, we considered an undirected graph. Now we consider a weighted directed graph , where nodes denote subjects joining in paired comparisons and the element of the adjacency matrix denotes the number of times that one subject is preferred to another subject. Let be the number of comparisons between subjects and . For easy exposition, similar to Simons and Yao (1999), we assume for all , where is a fixed positive constant. Then, is the number of times that wins out of a total number of comparisons.

The Bradley–Terry model postulates that , , are mutually independent binomial random variables, i.e., , where

| (8) |

Here, measures the intrinsic strength of subject , and the win-loss probabilities for any two subjects only depend on the difference of their strength parameters. The bigger the strength parameter is, the higher the probability of subject having a win over other subjects is. Let be the total number of wins for subject .

Because the probability is invariable by adding a common constant to all strength parameters , , we need a restriction for the identifiability of model. Following Simons and Yao (1999), we set as a constraint. Notice that the number of free parameters here is , different from the -model with free parameters. The logarithm of the likelihood function under the Bradley–Terry model is

| (9) |

where and . To distinguish the log-likelihood function in the -model, we use a subscript in this section. As we can see, it is an exponential family distribution on the directed graph with the out-degree sequence as its natural sufficient statistic. Setting the derivatives with respect to to zero, we obtain the likelihood equations

| (10) |

where is the MLE of with . If the directed graph is strongly connected, then the MLE uniquely exists [Ford (1957)]. Note that is not involved in (10); indeed, given and , is determined.

Now, we present the Wilks type of theorems for the Bradley–Terry model. The corresponding definitions of and are as follows:

With some ambiguity, we use the same notations and as in the -model, where their expressions are based on .

Theorem 3.

Suppose .

-

(a)

Under the specified null , , the log-likelihood ratio statistic is asymptotically normally distributed in the sense that

(11) where and .

-

(b)

Under the homogenous null , the normalized log-likelihood ratio statistic in (11) also converges in distribution to the standard normality.

The principled strategy for proving Theorem 1 is extended to prove the above theorem. However, we emphasize some main differences, including different approximate inverses for the Fisher information matrices under the null space, different asymptotic representations of the MLE and restricted MLE and different methods for obtaining consistency rates. Roughly speaking, we use a diagonal matrix to approximate the Fisher information matrix in the -model while the approximate inverse is a diagonal matrix plus a commonly exceptive number in the Bradley–Terry model. Second, the main term in the asymptotic representation of is in the -model while it is under the specified null or in the homogenous null in the Bradley–Terry model, where . Third, the Newton method is used to obtain consistency rate in the -model while we use the common neighbors between any two of subjects as middleman, who have ratios being simultaneously close to and to establish the error bound of in the Bradley-Terry model as in Simons and Yao (1999).

Note that in order to guarantee the existence of the MLE with high probability, it is necessary to control the increasing rate of as discussed in Simons and Yao (1999). In the case that some ’s are very large while others are very small, corresponding to a large value of , the subjects with relatively poor merits will stand very little chance of beating those with relatively large merits. Whenever all subjects could be partitioned into two sets, in which the subjects in one set will win all games against those in the other set, the MLE will not exist [Ford (1957)].

Note that in the above discussion, we have assumed the ’s, are all equal to a constant . This is only for the purpose of simplifying notations. Theorem 3 can be readily extended to the general case, where ’s are not necessarily the same (but with a bound).

Next, we present Wilks’ theorem under the homogenous testing problem with a fixed dimension.

Theorem 4.

If , under the homogenous null with a fixed , the twice log-likelihood ratio statistic converges in distribution to a Chi-square distribution with degrees of freedom.

Different from Theorem 2 in the -model, the above theorem does not contain a Wilks type of result under the fixed dimensional specified null . Some explanations are as follows. With the use of to approximate the Fisher information matrix under the specified null and with similar arguments as in the proof of (19) and (33), we have

where , is the difference of the third-order expansion term of the log-likelihood function between the full space and the null space, and is the corresponding difference of the fourth-order expansion term. If , then asymptotically follows a Chi-square distribution. Even if , is not approximately a Chi-square distribution. This is because does not goes to zero whereas it vanishes in the -model. In the case of fixed , a key quantity to measure is . It has the order of in the -model whereas in the Bradley-Terry model the difference have the following representation:

under the specified null. The difference of two distributions of and is much larger than the order of . Under the homogenous null, the approximate inverse is , where the off-diagonal elements are the same as the approximate inverse for approximating in the full parameter space. This makes that does not contain the difference of the above two terms. It leads to that vanishes in the homogenous null while it does not vanish in the specified null. Therefore, the Wilks type of result does not hold in the fixed dimensional specified null in the Bradley–Terry model.

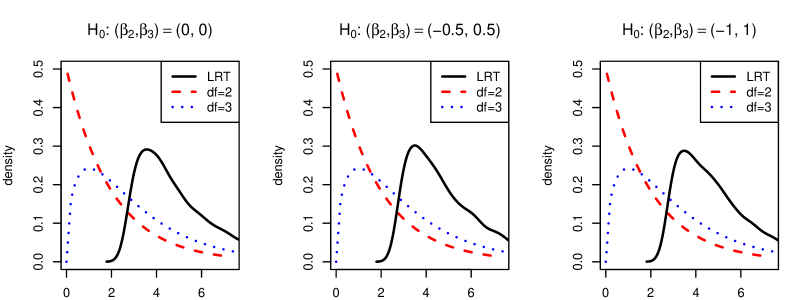

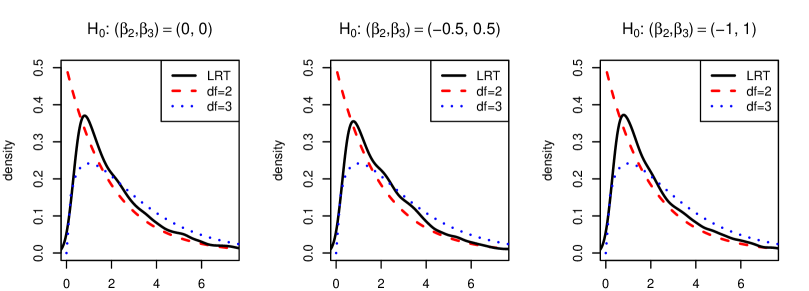

To give some intuition on the distribution of under the specified null, we draw its density curve against that of the Chi-square distribution. We consider several specified null with and other parameters are , where . The plots are shown in Figure 2(b), where the simulation is repeated times. As we can see, three findings are: (1) the distribution is far away from chi-square distributions with degree nor ; (2) even if , the density curve is very different from that of a Chi-square distribution; (3) the density curve depends crucially on and seems not sensitive to the choices of parameters.

3 Numerical Results

In this section, we illustrate the theoretical results via numerical studies.

3.1 Simulation studies

We carry out simulations to evaluate the performance of the log-likelihood ratio statistics for finite number of nodes. We considered the four null hypotheses: (1) : , ; (2) : , ; (3) : ; (4) : with a fixed , where is set to evaluate different asymptotic regimes. corresponds to the so-called simple null while aims to test whether a fixed number of parameters are equal to specified values. and aim to test whether a given set of parameters with increasing or fixed dimensions are equal. Under , and , we set the left parameters as: for . For homogenous null and , we set . Remark that in the Bradley–Terry model, is a reference parameter and is excluded in the above null. Four values for were chosen, i.e., , , and .

We evaluate the Type I errors and powers of the log-likelihood ratio statistics, and draw their QQ plots. For the increasing dimensional null hypotheses, we use the Chi-square approximation instead of the normal approximation due to that the former performs better than the latter in finite sample sizes. Two values for were considered: and . For the Bradley–Terry model, we assumed that each pair has one comparison, i.e., . Further, motivated by the schedules of the NBA regular season that is briefly described in next section, we considered additionally a relatively small size and let the number of paired comparisons equal to 3 for all . Each simulation was repeated times.

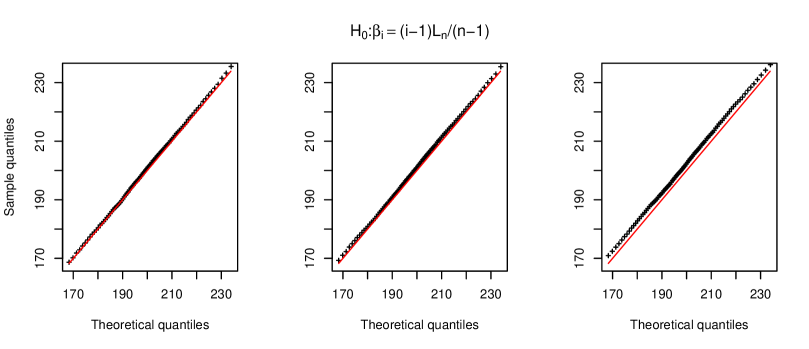

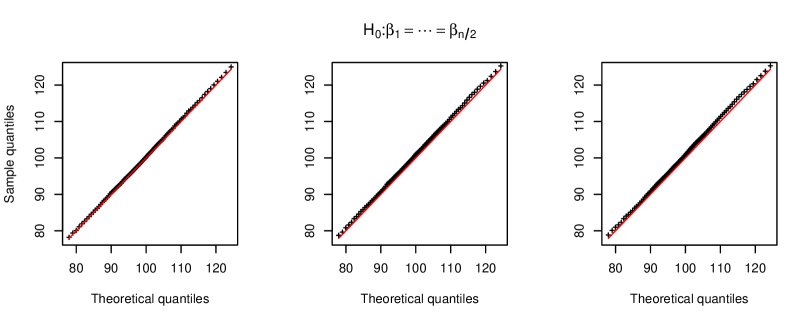

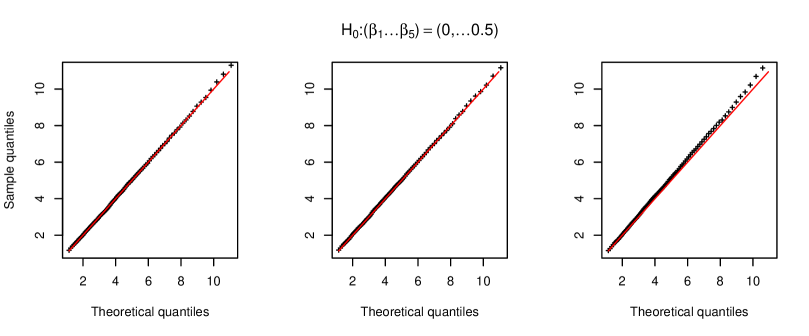

Due to the limited space, we only show plots of quantiles of Chi-square distributions vs sample quantiles in the case of under the -model and other QQ plots are similar. From figure 3(c), we can see that the sample quantiles agree well with theoretical quantiles when . On the other hand, when , there are a little derivation from the reference line under the null . When , the MLE failed to exist with a positive frequency (see Table 1).

| Type I errors under the -model | ||||||

|---|---|---|---|---|---|---|

| NULL | ||||||

| Type I errors under the Bradley–Terry model | ||||||

The simulated Type I errors are reported in Table 1. From this table, we can see that the MLE failed with positive frequencies in the -model when while the frequencies of MLE nonexistence in other cases is very small, less than . Most of simulated type I errors are close to the target nominal level and the difference between simulated values and nominal levels are relatively smaller when in contrast with those when .

Next, we investigate the powers of the log-likelihood ratio tests. We consider a homogenous hypothesis testing problem: : in the -model and in the Bradley-Terry model ( is the reference parameter). The true model was set to be , . The other parameters were set as for . In the Bradley–Terry model, each pair has only one comparison. The results are shown in Table 2. We can see that when , all simulated type I errors agree reasonably well with the nominal level . Further, when and are fixed, as increases, the power tends to increase and is close to when . Similar phenomenon can be observed when increases while and are fixed, or when increases while and are fixed. Further, we did additional simulations in the Bradley–Terry model under the situation that imitates the schedule of the NBA regular season. The number of nodes is and each pair of nodes has comparisons. Other parameters are the same as before. The results are shown in Table 3. From this table, we can see that the Type I errors are well controlled and powers are visibly high when . This shows that the asymptotic approximation is good even in the case is small, as long as the number of comparisons in each pair is over .

| Powers in the -model | ||||||

| Powers in the Bradley–Terry model | ||||||

3.2 An application to the NBA data

National Basketball Association (NBA) is one of the most successful men’s professional basketball league in the world. The current league organization divides its total thirty teams into two conferences: the western conference and the eastern conference. In the regular season, every team plays with every other team three or four times. It would be of interest to test whether some teams have the same merits. Here we use the recent 2020-21 NBA season data as an illustrative example.

The fitted merits in the Bradley–Terry model are presented in Table 4, in which Houston Rockets is the reference team. As we can see, the ranking based on the won-loss percentage and that based on the fitted merits are similar. As shown in the simulations, the asymptotic Chi-square distribution for the likelihood ratio statistic provides good approximation even when . We use the log-likelihood ratio statistic to test whether there are significant differences among top 3 teams and 6 teams in respective conferences.

Since the first three teams in the eastern conference–“Philadephia 76ers”, “Brooklyn Nets”, “Milwaukee Bucks” have similar won-loss percentages, we may want to test their equality. By using a Chi-square approximation, we get a value for the log-likelihood ratio with a p-value . For testing the equality of “Philadephia 76ers” and “Boston Celtics”, it yields a p-value , showing there exists significant difference between these two teams. For testing equality among top 4 teams in the western conference according the ranking of the won-loss percentage, we get a value for the log-likelihood ratio with a p-value , showing that the differences of the 4 teams do not exhibit statistical significance.

| Eastern Conference | Western Conference | |||||||

|---|---|---|---|---|---|---|---|---|

| Team | W-L | Team | W-L | |||||

| 1 | Philadephia | 49-23 | Utah J. | 52-20 | ||||

| 2 | Brooklyn N. | 48-24 | Phoenix S. | 51-21 | ||||

| 3 | Milwaukee B. | 46-26 | Denver N. | 47-25 | ||||

| 4 | New Y. K. | 41-31 | LA C. | 47-25 | ||||

| 5 | Miami H. | 40-32 | Los A. L. | 42-30 | ||||

| 6 | Atlanta H. | 41-31 | Portland T. B. | 42-30 | ||||

| 7 | Boston C. | 36-36 | Memphis G. | 38-34 | ||||

| 8 | Washinngton W. | 34-38 | Golden S. W. | 39-33 | ||||

| 9 | Indiana P. | 34-38 | Dallas M. | 42-30 | ||||

| 10 | Chicago B. | 31-41 | New O. P. | 31-41 | ||||

| 11 | Charlotte H. | 33-39 | San A. S. | 33-39 | ||||

| 12 | Toronto Raptors | 27-45 | Sacramento K. | 31-41 | ||||

| 13 | Orlando M. | 21-51 | Minnesota T. | 23-49 | ||||

| 14 | Cleveland C. | 22-50 | Oklahoma C. | 22-50 | ||||

| 15 | Detroit P. | 20-52 | Houston R. | 17-55 | ||||

4 Discussion

We have established the Wilks type of results for fixed and increasing dimensional parameter hypothesis testing problems under the -model and the Bradley–Terry model. It is worth noting that the conditions imposed on and may not be best possible. The simulation results indicate that there are still good asymptotic approximations when these conditions are violated. Note that the asymptotic behaviors of likelihood ratio statistics depend not only on (or ), but also on the configuration of all parameters. Moreover, both models assume a logistic distribution on observed edges . It would be of interest to investigate whether these conditions could be relaxed and whether the results continue to hold in some generalized models.

We only consider dense paired comparisons, in which all pairs have comparisons. However, this is not an unrealistic assumption for many situations. For example, the Major League Baseball schedule in the United States and Canada arranges that all teams play each other in a regular season. In some other applications, not all possible comparisons are available. For examples, some games might be cancelled due to bad weather. If only a small proportion of comparisons are not available, then it has little impact on the results developed in this paper. An interesting scenario is that paired comparisons are sparse, in which a large number of subjects do not have direct comparisons. The errors for the MLEs depend crucially on the sparse condition [Yan et al. (2012)]. This has impact on the remainder terms in the asymptotic expansion of the log-likelihood function. Extension to sparse paired comparisons seems not trivial. We will investigate this problem in future work.

5 Appendix

In this section, we present proofs for Theorems 1 and 2. The proofs of Theorems 3 and 4 are presented in the Supplementary Material A.

We introduce some notations. For a vector , denote by for a general norm on vectors with the special cases and for the - and -norm of respectively. For an matrix , let denote the matrix norm induced by the -norm on vectors in , i.e.,

and be a general matrix norm. denotes the maximum absolute entry-wise norm, i.e., . The notation or means there is a constant such that . means that and . means . The notation is a shorthand for .

We define a matrix class with two positive numbers and . We say an matrix belongs to the matrix class if

Define two diagonal matrices:

| (12) |

where is the bottom right block of for . Yan and Xu (2013) proposed to use the diagonal matrix to approximate .

Lemma 2.

For with and its bottom right block with , we have

| (13) |

The proof of Lemma 2 is an extension of that of Proposition 1 in Yan and Xu (2013) and presented in the Supplementary Material B. In Theorem 6.1 of Hillar et al. (2012), they obtained a tight upper bound of for symmetric diagonally dominant dimensional matrices satisfying :

where means is a nonnegative matrix, , denotes the identity matrix, and denotes the -dimensional column vector consisting of all ones. As applied here, we have that for with and its bottom right block with ,

| (14) |

It is noteworthy that the upper bounds in (80) and (83) are independent of . This property implies some remainder terms in the proofs of Theorems 1 are in regardless of .

We define a function and a notation for easy of exposition. A direct calculation gives that the derivative of up to the third order are

| (15) |

According to the definition of in (2), we have the following inequalities:

| (16) |

The above inequalities will be used in the proofs repeatedly. Recall that denotes the centered random variable of and define for all . Correspondingly, denote and .

5.1 Proofs for Theorem 1 (a)

To prove Theorem 1 (a), we need three lemmas below.

Lemma 3.

Recall that is the bottom right block of . Let , and . For any given , we have

where implies , and .

Lemma 4.

Under the null for any given , if

| (17) |

then with probability at least , the restricted MLE exists and satisfies

where means there is no any restriction on and implies . Further, if the restricted MLE exists, it must be unique.

From Lemma 4, we can see that the consistency rate for the restricted MLE in terms of the -norm is independent of while the condition depends on . The larger is, the weaker the condition is. When , the lemma gives the error bound for the MLE . When is a constant, this corresponds to the assumption in Chatterjee et al. (2011) and the -norm error bound of the MLE reduces to their error bound.

Lemma 5.

If (17) holds, then for an arbitrarily given ,

If is replaced with for , then the above upper bound still holds.

If we directly use the error bound for in (4) to bound the summation in the above lemma, it will produce the following bound:

If all s are positive constant, the term in the above right-hand side scaled by does not go to zero while Lemma 5 shows that it does go to zero. We explain briefly reasons here. The above process neglects the integrity for , which does have a much smaller error bound than that for . The proof of Lemma 5 uses the asymptotic representation of in (29), which leads to that the summarization is involved with a main term having the form of the weighted cubic sum . The variance of is in order of , although contains mixed items for . Lemma 5 plays an important role in (19) for proving .

We are now ready to prove the first part of Theorem 1.

Proof of Theorem 1 (a).

Under the null , the data generating parameter is equal to . For convenience, we suppress the superscript in when causing no confusion. The following calculations are based on the event that and simultaneously exist and satisfy

| (18) |

By Lemma 4, if .

Applying a fourth-order Taylor expansion to at point , it yields

where for some . Correspondingly, has the following expansion:

where is the version of with replaced by . Therefore,

| (19) |

Recall that

Therefore, can be written as

| (20) |

For the third-order expansion terms in , observe that if three distinct indices are distinct, then

| (21) |

and if there are at least three different values among the four indices , then

| (22) |

Therefore, and have the following expressions:

| (23) | |||||

| (24) | |||||

where lies between and .

It is sufficient to demonstrate: (1) converges in distribution to the standard normal distribution as ; (2) ; (3) . The second claim is a direct result of Lemma 5. Note that , . So has less terms than . In view of (67) and (39), if , then

| (25) | |||||

| (26) |

which shows the third claim. Therefore, the remainder of the proof is verify claim (1). This contains three steps. Step 1 is about explicit expressions of and . Step 2 is about the explicit expression of . Step 3 is about showing that the main term involved with asymptotically follows a normal distribution and the remainder terms goes to zero.

Step 1. We characterize the asymptotic representations of and . Recall that . To simplify notations, define . A second-order Taylor expansion gives that

where lies between and . Let

| (27) |

In view of (67) and (4), we have

| (28) |

Writing the above equations into the matrix form, we have

It yields that

| (29) |

| (30) |

Recall . Let and . Similar to (28) and (29), we have

| (31) |

where , and

| (32) |

In the above equation, lies between and for all .

Step 2. We derive the explicit expression of . Substituting (29) and (31) into the expressions of in (20) and respectively, it yields

By setting and , we have

| (33) |

Step 3. We show three claims: (i) ; (ii) and ; (iii) and . The first and second claims directly follows from Lemma 1 and Lemma 3, respectively. By (28) and (30), we have

If , then

| (34) |

In view of (83) and (32), with the same arguments as in the proof of the above inequality, we have

| (35) |

This demonstrates claim (iii). It completes the proof. ∎

5.2 Proofs for Theorem 1 (b)

Let and denote the Fisher information matrix of under the null , where

| (36) |

where is the lower right block of , , and

Note that is also the covariance matrix of . Similar to approximate by , we use to approximate . The approximation error is stated in the following lemma.

Lemma 6.

For any and , we have

| (37) |

As we can see, the order of the above approximation error is the same as that in (80) and is independent of . The proof of Lemma 6 is given in the Supplementary Material B. Similar to (83), by Theorem 6.1 of Hillar et al. (2012), we have the -norm bound of :

However, we use (120) to analyze here due to that the first diagonal element of is much smaller than other diagonal elements, up to a scaled factor , and the upper bound of neglects the difference between the first diagonal element and others.

Recall that denotes the restricted MLE of . Under the null , we have . Similar to the proof of Lemma 4, we have the following consistency result.

Lemma 7.

Under the null , if

then with probability at least , exists and satisfies

Further, if exists, it must be unique.

From the above lemma, we can see that the condition to guarantee consistency and the error bound depends on . Larger means a weaker condition and a smaller error bound. A rough condition in regardless of to guarantee consistency is that will be used in the proof of Theorem 1 (b). It implies an error bound that is generally larger than that in Lemma 4. Similar to Lemma 3, we have the following bound, which is independent of .

Lemma 8.

For any given , we have

The asymptotic representation of is given below.

Lemma 9.

Under the null , if , then for any given , we have

where with probability at least satisfy

uniformly, and satisfies

| (38) |

With some ambiguity of notations, we still use the notation here that is a little different from defined in (32) in Section 5.1. Specifically, the first element of can be viewed as the sum of , in (32). This difference leads to that the remainder term here is larger than that in (29).

Now, we are ready to prove Theorem 1 (b).

Proof of Theorem 1 (b).

Under the null , the data generating parameter is equal to . The following calculations are based on the event that and simultaneously exist and satisfy

| (39) |

Similar to the proof of Theorem 1 (a), it is sufficient to demonstrate: (i) converges in distribution to the standard normal distribution; (ii) ; (iii) . The fourth-order Taylor expansion for here is with regard to the vector because are the same under the null here. As we shall see, the expressions of and are a little different from and except from the difference and .

With the same arguments as in (25) and (26), we have claim (iii) under the condition . In Lemma 5, we show . For claim (ii), it is sufficient to show . Under the null , can be written as

With the use of the asymptotic representation of in Lemma 9, if

then we have

| (40) |

whose detailed calculations are given in the supplementary material.

Next, we show claim (i). Recall . The expression of is

| (41) |

where satisfies (38). In view of (120) and (38), setting yields

| (42) | |||||

This shows that if ,

Now, we evaluate the difference between and . By using and to approximate and respectively, we have

| (43) | |||||

| (44) |

Since , by the central limit theorem for the bounded case (Loéve (1977), page 289), converges in distribution to the standard normal distribution if . Therefore, as ,

By combining (5.1), (41), (34), (43) and (44), it yields

Therefore, claim (i) immediately follows from Lemma 1. This completes the proof. ∎

5.3 Proofs for Theorem 2 (a)

Let , and

| (45) |

where and are respective dimensional sub-matrices of and , and . Recall that denotes the Fisher information matrix of under the null and . It is worthy to mention that is a fixed constant in this section.

To prove Theorem 2 (a), we need the following three lemmas. The lemma below gives an upper bound of , whose magnitudes are . It is much smaller than that the error bounds of and themselves in (80) by a vanishing factor .

Lemma 10.

For a fixed constant , the error between and in terms of the maximum absolute entry-wise norm has the following bound:

| (46) |

The following lemma gives the upper bounds of three remainder terms in (48) that tend to zero.

Lemma 11.

Suppose is a fixed constant.

(a)If , then .

(b)If , then .

(c)If , then

The lemma below establishes the upper bound of .

Lemma 12.

Under the null , with a fixed , if , then with probability at least ,

The above error bound is in the magnitude of , up to a factor , which makes the remainder terms in (55) be asymptotically neglected. Note that this error bound is much smaller than those for and by a vanishing factor , whose magnitudes are .

Now, we are ready to prove Theorem 2 (a).

Proof of Theorem 2 (a).

The following calculations are based on the event that and simultaneously exist and satisfy

| (47) |

Similar to the proof of Theorem 1 (a), it is sufficient to demonstrate: (1) converges in distribution to the Chi-square distribution with degrees of freedom; (2) and are asymptotically neglected remainder terms, where is given in (33), and are given in (23) and (24), and are respective versions of and by replacing with . Claims (1) and (2) are shown in three steps in turns.

Step 1. We show . Using the matrix form in (62), in (33) can be written as

| (48) | |||||

It is sufficient to demonstrate: (i) converges in distribution to a Chi-square distribution with degrees of freedom; (ii) ; (iii) . Claim (ii) directly follows from Lemma 11. Because is independent over and is a fixed constant, the classical central limit theorem for the bounded case (Loéve (1977), p. 289) gives that the vector follows a -dimensional standard normal distribution. This verifies claim (i). Now, we show . Recall the definition of in (27). By setting and , we have

| (49) | |||||

| (50) |

where , , and and are given in (27) and (32), respectively. Since (see (28) and (32)), we have

The difference is bounded as follows:

| (51) | |||||

where the second inequality is due to (67) and the mean value theorem and the third inequality follows from (47). Therefore, if , then

| (52) |

| (53) | |||||

| (54) |

To evaluate the bound of , we divide it into three terms:

| (55) | |||||

The first term is bounded as follows. By (147) and (28), we have

| (56) | |||||

In view of (80) and (51), the upper bounds of and are derived as follows:

| (57) | |||||

and

| (58) |

By combining (49)–(58), it yields

| (59) |

This completes the proof of the first step.

Step 2. We bound . For a cubic term in , a direct scaling method gives that

The term in the above right hand does not tend to zero. Because is fixed, the approach for showing in the proof of Theorem 1 does not work yet. To prove that this term does go to zero, we did a careful analysis on the difference by using asymptotic representations of and . With the use of Lemmas 5 and 12, we have

| (60) |

whose detailed proofs are given in Section 4.4 in Supplementary Material A.

Step 3. We bound . With the same reason as in Step 2, we could not yet use the method of proving in the proof of Theorem 1. With the use of asymptotic representations of and and Lemma 12, we can show

| (61) |

whose detailed proofs are given in Section 4.5 in Supplementary Material A. This completes the proof. ∎

5.4 Proofs for Theorem 2 (b)

Recall that , , and is given in (120). is the Fisher information matrix of under the null . Remark that is a fixed constant in this section. Partition into four blocks

| (62) |

where is a scalar and the dimension of is . It should be noted is different from in the proof of Theorem 1 (a), where . With some ambiguity of notation, we use the same notation here. However, both share very similar properties.

To prove Theorem 2 (b), we need the following three lemmas, whose proofs are respectively similar to those of Lemmas 10, 11 and 12 and omitted.

Recall that is the bottom right block of . The lemma below gives an upper bound of , whose magnitudes are .

Lemma 13.

For a fixed constant , the error between and in terms of the maximum absolute entry-wise norm has the following bound:

| (63) |

It is remark that the absolute entry-wise error between and in the Bradley-Terry model is not in the order of that holds in the -model (i.e., (63)), but adding a special matrix whose order is (see (289) on page 20 in Supplementary Material B). The following lemma gives the upper bounds of three remainder terms in (64) that tend to zero, whose proof is similar to the proof of Lemma 11 and is omitted.

Lemma 14.

Suppose is a fixed constant.

(a)If , then .

(b)If , then .

(c)If , then

The lemma below establishes the upper bound of .

Lemma 15.

Under the null with a fixed , if , then with probability at least ,

The above error bound is in the magnitude of , up to a factor , which makes the remainder terms in (64) be asymptotically neglected. Note that this error bound is the same as that in Lemma 12.

Now, we are ready to prove Theorem 2 (b).

Proof of Theorem 2 (b).

Note that denotes the restricted MLE under the null space . The following calculations are based on the event that is defined in (39). By Lemmas 4 and 15, if .

Similar to the proof of Theorem 2 (a), it is sufficient to demonstrate: (1) converges in distribution to the Chi-square distribution with degrees of freedom; (2)

The proof of claim (2) is similar to those of (163) and (61) and omitted. We only present the proof of claim (1) here.

We show . Using the matrix form in (62), in (19) can be written as

| (64) | |||||

where is defined in (27) and is in (38). In view of Lemmas 11 and 14, it is sufficient to demonstrate: (i) converges in distribution to a Chi-square distribution with degrees of freedom; (ii) . Because is independent over and is a fixed constant, the classical central limit theorem for the bounded case (Loéve (1977), p. 289) gives that the vector follows a -dimensional standard normal distribution. Because under the null and , we have

Because , it follows that we have claim (i). Now, we show . By setting and , we have

where , , and and are given in (27) and (38), respectively. In view of (28) and (38), we have

With the same arguments as in the proof of (51), we have

Therefore, if , then

| (65) |

By (80), (28) and (120), we have

As in the proofs of (55)–(58), we have

Combining the above inequalities and (65), it yields

which shows claim (ii).

∎

Acknowledgment The views expressed are those of the authors and should not be construed to represent the positions of the Department of the Army or Department of Defense. Yan is partially supported by the National Natural Science Foundation of China (no. 12171188) and the Fundamental Research Funds for the Central Universities. Xu is partially supported by the General Research Fund of Hong Kong (17308820). Zhu is partially supported by the National Science Foundation (DMS 1407698 and DMS 1821243).

References

- Blitzstein and Diaconis (2011) Blitzstein, J. and Diaconis, P. (2011). A sequential importance sampling algorithm for generating random graphs with prescribed degrees. Internet Mathematics, 6(4):489–522.

- Boucheron et al. (2013) Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration Inequalities: A Nonasymptotic Theory of Independence. Oxford University Press.

- Bradley and Terry (1952) Bradley, R. A. and Terry, M. E. (1952). Rank analysis of incomplete block designs the method of paired comparisons. Biometrika, 39(3-4):324–345.

- Brown (1971) Brown, B. M. (1971). Martingale Central Limit Theorems. The Annals of Mathematical Statistics, 42(1):59–66.

- Chatterjee et al. (2011) Chatterjee, S., Diaconis, P., and Sly, A. (2011). Random graphs with a given degree sequence. The Annals of Applied Probability, pages 1400–1435.

- Chen et al. (2021) Chen, M., Kato, K., and Leng, C. (2021). Analysis of networks via the sparse -model. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83(5):887–910.

- de Jong (1987) de Jong, P. (1987). A central limit theorem for generalized quadratic forms. Probability Theory and Related Fields, 75(2):261–277.

- Fan et al. (2001) Fan, J., Zhang, C., and Zhang, J. (2001). Generalized Likelihood Ratio Statistics and Wilks Phenomenon. The Annals of Statistics, 29(1):153 – 193.

- Fienberg (2012) Fienberg, S. E. (2012). A brief history of statistical models for network analysis and open challenges. Journal of Computational and Graphical Statistics, 21(4):825–839.

- Ford (1957) Ford, L. R. (1957). Solution of a ranking problem from binary comparisons. The American Mathematical Monthly, 64(8):28–33.

- Ghoshdastidar et al. (2020) Ghoshdastidar, D., Gutzeit, M., Carpentier, A., and von Luxburg, U. (2020). Two-sample hypothesis testing for inhomogeneous random graphs. The Annals of Statistics, 48(4):2208 – 2229.

- Goldenberg et al. (2010) Goldenberg, A., Zheng, A. X., Fienberg, S. E., and Airoldi, E. M. (2010). A survey of statistical network models. Foundations and Trends in Machine Learning, 2(2):129–233.

- Gragg and Tapia (1974) Gragg, W. B. and Tapia, R. A. (1974). Optimal error bounds for the newton ckantorovich theorem. SIAM Journal on Numerical Analysis, 11(1):10–13.

- Graham (2017) Graham, B. S. (2017). An econometric model of network formation with degree heterogeneity. Econometrica, 85(4):1033–1063.

- Hall (1984) Hall, P. (1984). Central limit theorem for integrated square error of multivariate nonparametric density estimators. Journal of Multivariate Analysis, 14(1):1–16.

- Hillar and Wibisono (2013) Hillar, C. and Wibisono, A. (2013). Maximum entropy distributions on graphs. arXiv preprint arXiv:1301.3321.

- Hillar et al. (2012) Hillar, C. J., Lin, S., and Wibisono, A. (2012). Inverses of symmetric, diagonally dominant positive matrices and applications.

- Hoeffding (1963) Hoeffding, W. (1963). Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58(301):13–30.

- Holland and Leinhardt (1981) Holland, P. W. and Leinhardt, S. (1981). An exponential family of probability distributions for directed graphs. Journal of the American Statistical Association, 76(373):33–50.

- Hu et al. (2021) Hu, J., Zhang, J., Qin, H., Yan, T., and Zhu, J. (2021). Using maximum entry-wise deviation to test the goodness of fit for stochastic block models. Journal of the American Statistical Association, 116(535):1373–1382.

- Jin et al. (2021) Jin, J., Ke, Z. T., and Luo, S. (2021). Optimal adaptivity of signed-polygon statistics for network testing. The Annals of Statistics, 49(6):3408 – 3433.

- Kantorovich (1948) Kantorovich, L. V. (1948). Functional analysis and applied mathematics. Uspekhi Mat Nauk, pages 89–185.

- Kantorovich and Akilov (1964) Kantorovich, L. V. and Akilov, G. P. (1964). Functional Analysis in Normed Spaces. Oxford, Pergamon.

- Lei (2016) Lei, J. (2016). A goodness-of-fit test for stochastic block models. The Annals of Statistics, 44(1):401 – 424.

- Loéve (1977) Loéve, M. (1977). Probability theory I. 4th ed. Springer, New York.

- Mukherjee et al. (2018) Mukherjee, R., Mukherjee, S., and Sen, S. (2018). Detection thresholds for the -model on sparse graphs. Ann. Statist., 46(3):1288–1317.

- Park and Newman (2004) Park, J. and Newman, M. E. J. (2004). Statistical mechanics of networks. Physical Review E, 70(6):066117.

- Peligrad (1987) Peligrad, M. (1987). On the Central Limit Theorem for -Mixing Sequences of Random Variables. The Annals of Probability, 15(4):1387 – 1394.

- Perry and Wolfe (2012) Perry, P. O. and Wolfe, P. J. (2012). Null models for network data. Available at http://arxiv.org/abs/1201.5871.

- Portnoy (1988) Portnoy, S. (1988). Asymptotic behavior of likelihood methods for exponential families when the number of parameters tends to infinity. Ann. Statist., 16(1):356–366.

- Rinaldo et al. (2013) Rinaldo, A., Petrović, S., and Fienberg, S. E. (2013). Maximum lilkelihood estimation in the -model. Ann. Statist., 41(3):1085–1110.

- Simons and Yao (1999) Simons, G. and Yao, Y.-C. (1999). Asymptotics when the number of parameters tends to infinity in the bradley-terry model for paired comparisons. The Annals of Statistics, 27(3):1041–1060.

- Sur et al. (2019) Sur, P., Chen, Y., and Candès, E. J. (2019). The likelihood ratio test in high-dimensional logistic regression is asymptotically a rescaled chi-square. Probability Theory and Related Fields, 175(1):487–558.

- Verzelen and Arias-Castro (2015) Verzelen, N. and Arias-Castro, E. (2015). Community detection in sparse random networks. Annals of Applied Probability, 25(6):3465–3510.

- Wang (2011) Wang, L. (2011). GEE analysis of clustered binary data with diverging number of covariates. Ann. Statist., 39(1):389–417.

- Wilks (1938) Wilks, S. S. (1938). The Large-Sample Distribution of the Likelihood Ratio for Testing Composite Hypotheses. The Annals of Mathematical Statistics, 9(1):60 – 62.

- Withers (1987) Withers, C. (1987). Central limit theorems for dependent variables, ii. Probability theory and related fields, 76(1):1–13.

- Yan et al. (2016) Yan, T., Leng, C., and Zhu, J. (2016). Asymptotics in directed exponential random graph models with an increasing bi-degree sequence. The Annals of Statistics, (44):31–57.

- Yan and Xu (2013) Yan, T. and Xu, J. (2013). A central limit theorem in the -model for undirected random graphs with a diverging number of vertices. Biometrika, 100:519–524.

- Yan et al. (2012) Yan, T., Yang, Y., and Xu, J. (2012). Sparse paired comparisons in the bradley–terry model. Statistica Sinica, 22(3):1305–1318.

Supplementary material A for “Wilks’ theorems in the -model”222Supplementary Materials B and C are available by sending emails to Email: tingyanty@mail.ccnu.edu.cn

Ting Yan, Yuanzhang Li, Jinfeng Xu, Yaning Yang and Ji Zhu

Supplementary Material A contains the proofs of supported lemmas in the proofs of Theorems 1 and 2 as well as inequalities (39), (59) and (60) in the main text. This supplementary material is organized as follows. Section 6 gives the variances of the weighted quadratic sum , the weighted cubic sum and an upper bound of a mixed sum , which will be used in the proofs of supported lemmas repeatedly.

Section 7 contains the proofs of supported lemmas in the proof of Theorem 1 (a). This section is organized as follows. Sections 7.1 and 7.2 present the proofs of Lemmas 3 and 4. Section 7.3 gives an additional result about the upper bound for in terms of the -norm. Section 7.4 gives an asymptotically explicit expression for that will be used in the proof of Lemma 5. Section 7.5 presents the proof of Lemma 5. The proof of Lemma 2 about approximation error of using to approximate is present in Supplementary Material C. We defer the proof of Lemma 1 to Section 10 since it contains many long calculations.

Section 8 presents proofs of supported lemmas in the proof of Theorem 1 (b) This section is organized as follows. Sections 8.1, 8.2 and 8.3 present the proofs of Lemmas 7, 8 and 9, respectively. Section 8.4 presents the proof of (39) in the main text.

Section 9 presents proofs of supported Lemmas in the proof of Theorem 2 (a) as well as proof of (59) and (60) in the main text. This section is organized as follows. Sections 9.1, 9.2 and 9.3 present the proofs of Lemmas 10, 11 and 12, respectively. Sections 9.4 and 9.5 presents the proofs of orders of two remainder terms in (59) and in (60) in the main text, respectively.

Section 10 presents the proof of Lemma 1. Section 11 reproduces Bernstein’s inequality and a Martingale central limit theorem for easy readability.

All notation is as defined in the main text unless explicitly noted otherwise. Equation and lemma numbering continues in sequence with those established in the main text.

We first recall useful inequalities on the derivatives of , which will be used in the proofs repeatedly. Recall that

A direct calculation gives that the derivative of up to the third order are

| (66) |

Note that denotes the data generating parameter, under which the data are generated. Recall that

According to the definition of , we have

| (67) |

For a satisfying , we also have

| (68) |

These facts will be used in the proofs repeatedly. Recall that

is the centered random variable of and for all . Correspondingly, and .

6 Variances of weighted sums for and

This section presents the expressions of the variances of the weighted quadratic sum and the weighted cubic sum , as well as the upper bound of a mixed sum . They are stated in Lemmas 16, 17 and 18, respectively. Recall that for and for all , and

For a given sequence , the variance of the weighted quadratic sum is given below.

Lemma 16.

Let and . For a given sequence , we have

| (69) |

Proof.

The calculation of the variance of can be divided into two parts:

| (70) |

The first part can be calculated as follows:

Note that the random variables for are mutually independent. There are only two cases in terms of for which is not equal to zero: (Case A) ; (Case B) or . By respectively considering Case A and Case B, a direct calculation gives that

| (71) |

Now, we present the variance of the cubic weighted sum.

Lemma 17.

For a given sequence , the variance of has the following expression:

| (73) | |||

Proof.

Similar to the proof of Lemma 16, the calculation of the variance of can also be divided into two parts:

| (74) |

The first part can be expressed as

| (75) |

Note that the random variables for are mutually independent

and when .

The first part can be calculated as follows.

There are six cases to consider according to the number of distinct values of six indices: .

(Case A) All six indices, , are equal. In this case, the summation in (75) becomes

(Case B) All six indices, , have exactly two distinct values. By considering all possible pairs, e.g., , pairs where the covariance is not zero are those like for . In this case, the summation in (75) becomes

(Case C) All six indices, , have exactly three distinct values. By considering all possible pairs, e.g., , pairs where the covariance is not zero are those like for distinct . In this case, the summation in (75) becomes

(Case D) All six indices, , have exactly four, five, or six distinct values. In all these cases, and are equal zero because at least such one is independent of others. By combining the above cases, it yields,

| (76) |

Now, we present an upper bound of the variance of a mixed weighted sum.

Lemma 18.

For a fixed array , an upper bound of the variance of is below:

Proof.

Note that

For and , the calculation of the covariance between and can also be divided into eight cases: (Case 1) ; (Case 2) ; (Case 3) ; (Case 4) ; (Case 5) ; (Case 6) ; (Case 7) , ; (Case 8) , . By writing the covariance between and into the following form

and using the similar arguments as in the proof of Lemma 17, we have

| (78) |

Let

In view of that

by combining the above cases, it completes the proof. ∎

7 Proofs of supported lemmas in the proof of Theorem 1 (a)

We first reproduce some basic results here in the main text. Recall that an matrix belongs to the matrix class if

We use the diagonal matrix

| (79) |

to approximate . For , Yan and Xu (2013) proved

| (80) |

Further, for its bottom right block of and , we have

| (81) |

where

| (82) |

From (81), we can see that the error bound by using to approximate is independent of and depends only on , and n. Moreover, by Theorem 6.1 of Hillar et al. (2012), we have that for and its bottom right block ,

| (83) |

Recall that , where row column element of is

which is also the covariance matrix of .

This section is organized as follows. Sections 7.1 and 7.2 presents the proofs of Lemmas 3 and 4, respectively. Section 7.3 contains an additional result about an -norm error bound for . Section 7.4 presents an asymptotically explicit expression for that is used in the proof of Lemma 4. Section 7.5 presents the proof of Lemma 5.

7.1 Proof of Lemma 3

Proof of Lemma 3.

Recall that , , and . Note that when , and . The aim is to prove

| (84) |

We first have

| (85) |

which is due to that

Let . Next, we bound the variance of . Recall that . There are four cases for calculating the covariance

Case 1: . In view of (71), we have

| (86) |

Let and . By (67),

Note that the function with attains its maximum value at points or . It follows that

Thus, we have

Case 2: Three indices among the four indices are the same. Without loss of generality, we assume that and . Observe that

and, for distinct ,

It follows that

Therefore, by (67),

Similarly, we have the upper bounds in other cases.

Case 3. Two indices among the four are the same (e.g. or ):

Case 4: All four indices are different

Consequently, by (80), we have

It follows that from Chebyshev’s inequality and (85), we have

where is any positive sequence tending to infinity. This completes the proof. ∎

7.2 Proof of Lemma 4

Before beginning the proof of Lemma 4, we introduce one useful lemma. Let be a function vector on . We say that a Jacobian matrix with is Lipschitz continuous on a convex set if for any , there exists a constant such that for any vector the inequality

holds. We will use the Newton iterative sequence to establish the existence and consistency of the MLE. Gragg and Tapia (1974) gave the optimal error bound for the Newton method under the Kantovorich conditions [Kantorovich (1948)]. We only show partial results here that are enough for our applications.

Lemma 19 (Gragg and Tapia (1974)).

Let be an open convex set of and be Fréchet differentiable on with a Jacobian that is Lipschitz continuous on with Lipschitz coefficient . Assume that is such that exists,

and

Then: (1) The Newton iterations exist and for . (2) exists, and .

Proof of Lemma 4.

Under the null , are known and are unknown. Recall that denotes the restricted MLE under the null space, where , . For convenience, we will use and to denote the vectors and in this proof, respectively. Note that when .

Define a system of score functions based on likelihood equations:

| (87) |

and .

Let be a convex set containing . We will derive the error bound between and through obtaining the convergence rate of the Newton iterative sequence , where we choose the true parameter as the starting point . To this end, it is sufficient to demonstrate the Kantovorich conditions in Lemma 19, where we set . The Kantororich conditions require the Lipschitz continuous of and the upper bounds of . The proof proceeds three steps. Step 1 is about the Lipschitz continuous property of the Jacobian matrix . Step 2 is about the tail probability of . Step 3 is a combining step.

Step 1. We claim that the Jacobian matrix of on is Lipschitz continuous on with the Lipschitz coefficient . This is verified as follows. Let . The Jacobian matrix of can be calculated as follows. By finding the partial derivative of with respect to , for , we have

| (88) |

By the mean value theorem and (66), we have

For , this shows

It follows that

| (89) |

Let

It leads to that . Note that when and ,

Therefore, we have , for . Consequently, for vectors , we have

where is some real number.

Step 2. We give the tail probability of satisfying

| (90) |

This is verified as follows. Recall that , , are independent Bernoulli random variables and . By Hoeffding’s (1963) inequality, we have

By the union bound, we have

| (91) |

such that

Step 3. This step is one combining step. The following calculations are based on the event :

Recall that . By (83), we have . By the event , we have

Repeatedly utilizing (83), we have

In Step 1, we show that is Lipschitz continuous with Lipschitz coefficient . Note that for any , . Therefore, if , then

The above arguments verify the Kantovorich conditions. By Lemma 19, it yields that

| (92) |

Step 2 implies . This completes the proof. ∎

7.3 The upper bound of

We derive the upper bound for in terms of the -norm.

Lemma 20.

If , with probability at least , we have

Proof.

By (92), if , with probability at least , exists. Because minimizes , by the mean value theorem, we have

where

It follows from the Cauchy-Schwarz inequality that

This shows that

where denotes the smallest eigenvalue of . Because for any vector ,

we have

By (90), with probability at least , we have

Consequently,

∎

7.4 Asymptotic expression for

The following lemma gives an asymptotically explicit expression for that will be repeatedly used in the proof.

Lemma 21.

Suppose that with are known. If , then with probability at least , the following holds uniformly:

where

| (93) |

Proof of Lemma 21.

Since with are known, with some ambiguity of notations, here we use and to denote vectors and , respectively. By (92), if , then , where

The following calculations are based on the event .

Write . Let , and . By applying a second order Taylor expansion to , we have

| (94) |

where lies between and . We evaluate the last term in the above equation row by row. Its th row is

| (95) |

A directed calculation gives that

It follows that

By (68) and event , we have

| (96) |

Let and . Because , by (94), we have

| (97) |

Note that . By (96) and (83), we have

| (98) |

Now, we bound the error term , where . Note that

and

The summation of the above right hand can be viewed as the sum of independent random variables by noting that it is equal to

For any and for any , we have

It follows that

| (99) |

By Bernstein’s inequality in Lemma 24 and (99), with probability , for large , we have that

Therefore, with probability at least , the following holds:

It yields that

| (100) |

7.5 Proof of Lemma 5

In this section, we give the proof of Lemma 5.

Proof of Lemma 5.

The bounds of and in Lemma 5 are reproduced here:

| (101) | |||||

| (102) |

Note that are known and are unknown. Let be the event that

| (103) |

where

| (104) |

Let be the event

| (105) |

By Lemma 21 and (90), holds with probability at least . The following calculations are based on .

Let

| (106) |

In view of (67), we have

| (107) |

By substituting the expression of in (103) into , we get

| (108) |

We bound the four terms in the above right hand in an inverse order. The fourth term can be bounded as follows:

| (109) | |||||

In view of (104), (105) and (107), the upper bound of the third term is

| (110) | |||||

By Corollary 1 in the main text, we have that

In view of (104) and (107), the second term can be bounded as follows:

| (111) | |||||

Now, we bound the first term. By Lemma 17, we have that

Because

an upper bound of is

| (112) |

Because

we have

such that

| (113) |

In view of (112) and (113), we have

| (114) |

By combining the upper bounds of the above four terms in (109), (110), (111) and (114), it yields that

This leads to (101).

Now we bound the following terms in (102):

By substituting (103) into the above expression, we get

In view of (130), (107) and (104), we have the following bounds

| (115) | |||||

| (116) | |||||

| (117) |

The left argument is to bound the first term in (7.5). Because

by (107), we have

By Lemma 18, we have

Similar to (112), Chebyshev’s inequality gives that

| (118) |

By combining (7.5) and (115)–(118), we have

If

it yields (102). ∎

8 Proofs of supported lemmas in the proof of Theorem 1 (b)

This section is organized as follows. Sections 8.1, 8.2 and 8.3 present the proofs of Lemmas 7, 8 and 9, respectively. Section 8.4 presents the proof of (39) in the main text.

We reproduce some notations and some useful results in Section 6.2 here. Recall and denote the Fisher information matrix of under the null , where

| (119) |

where is the lower right block of , , and

We use to approximate and have the following approximation error

| (120) |

8.1 Proof of Lemma 7

In this section, we present the proof of Lemma 7. We introduce an error bound in the Newton method by Kantorovich and Akilov (1964) under the Kantorovich conditions [Kantorovich (1948)].

Lemma 22 (Theorem 6 in Kantorovich and Akilov (1964)).

Let be an open convex subset of and be Fréchet differntiable. Assume that, at some , is invertible and that

| (121) | |||

| (122) | |||

Then:

(1) The Newton iterates , are well-defined,

lie in and converge to a solution of .

(2) The solution is unique in , if

and in if .

(3) if and if .

Now, we are ready to prove Lemma 7.

Proof of Lemma 7.

Recall that denotes the restricted MLE under the null . In what follows, and denote respective vectors and with some ambiguity of notations. Define a system of score functions based on likelihood equations:

| (123) |

and , where .

Let be a neighbouring set containing . We will derive the error bound between and through obtaining the convergence rate of the Newton iterative sequence , where we choose the true parameter as the starting point . To this end, it is sufficient to demonstrate the Kantovorich conditions in Lemma 19, where we set . The proof proceeds three steps. Step 1 is about verifying condition (121). Step 2 is about verifying (122). Step 3 is a combining step.

Step 1. We claim that for any ,

| (124) |

This is verified as follows. Let and . The Jacobian matrix of can be calculated as follows. By finding the partial derivative of with respect to , we have

and

By the mean value theorem and (66), we have

This shows

It follows that

| (125) |

For any , define

By (125), we have

| (126) |

Consequently, for any vectors , we have

It follows that

This gives that

| (127) |

and, by (120),

| (128) |

Note that and . By combining (127) and (128), we have (124).

Step 2. We claim that with probability at least , we have

| (129) |

Recall that , , are independent Bernoulli random variables and . By Hoeffding’s (1963) inequality, we have

By the union bound, we have

| (130) |

such that

Note that

and the terms in the above summation are independent. Hoeffding’s (1963) inequality gives that

The above arguments imply that with probability at least ,

and, by (120),

8.2 Proof of Lemma 8

In this section, we present the proof of Lemma 8.

Proof of Lemma 8.

Recall that and . It is sufficient to demonstrate:

| (131) |

and

| (132) |

The claim of (131) is due to that

Let

where is the bottom right block of , is the matrix with all its elements being equal to , and is the matrix with all its row being equal to the vector , and is the transpose of . Therefore, we have

Because

with the same arguments as in the proof of Lemma 3, we have (132). This completes the proof. ∎

8.3 Proof of Lemma 9

In this section, we present the proof of Lemma 9.

Proof of Lemma 9.

Since and with under the null, with some ambiguity of notations, we still use and to denote vectors and , respectively. By Lemma 5, if , then , where

The following calculations are based on the event .

A second order Taylor expansion gives that

where lies between and , and, for any ,

It follows that

| (133) |

and, for ,

| (134) |

where

Writing (133) and (133) into a matrix form, we have

| (135) |

where . It is equivalent to

In view of that and the event , we have

| (136) |

and, for ,

| (137) |

By letting , in view of (35), (136) and (137), we have

| (138) | |||||

Now, we bound the error term . Note that

The summation of the above right hand can be viewed as the sum of independent random variables. Because , we have

It follows from Bernstein’s inequality in Lemma 24 and inequality (35), with probability , we have that

where . By the uniform bound, with probability at leas , we have

| (139) |

8.4 Proof of (39)

Let . The expression of can be written as

where

We shall in turn bound each term in the above summation. To simplify notations, let

In view of (67), we have

| (142) |

Because can be expressed as the sum of independent and bounded random variables,

and

by Bernstern’s inequality, with probability at least , we have

| (143) |

| (144) | |||||

Therefore, if , then

| (145) |

We now consider .

If , then

Finally, we bound . It can be written as

With similar arguments as in the proof of Lemma 5, we have

This gives that

If

then

which shows (39) in the main text.

9 Proofs of supported Lemmas in the proof of Theorem 2 (a)

This section presents the proofs of supported Lemmas in the proof of Theorem 2 (a) and two vanishing remainder terms. This section is organized as follows. Sections 9.1, 9.2 and 9.3 present the proofs of Lemmas 10, 11 and 12, respectively. Sections 9.4 and 9.5 presents the proofs of orders of two remainder terms in (59) and in (60) in the main text, respectively.

9.1 Proof of Lemma 10

This section presents the proof of Lemma 10.

Proof of Lemma 10.

Note that

where is the upper left sub-matrix of . Because

and

we have

where

With the similar arguments as in the proof of (80), we have

Note that is a fixed positive integer. A direct calculation gives that

and

This shows that

| (147) |

which has a much smaller error in contract to and whose magnitudes are . ∎

9.2 Proof of Lemma 11

In this section, we present the proof of Lemma 11.

Proof of Lemma 11.

Note that is a fixed constant, , and .

(b) We bound . Note that

It follows that

Now, we calculate

Note that

We evaluate according to four cases:

(Case A) , ;

(Case B) , ;

(Case C) , ;

(Case D) , .

Case A: the expression of is

Case B: the expression of is

Case C: the expression of is