Performance Bounds of Model Predictive Control for Unconstrained and Constrained Linear Quadratic Problems and Beyond

Abstract

We study unconstrained and constrained linear quadratic problems and investigate the suboptimality of the model predictive control (MPC) method applied to such problems. Considering MPC as an approximate scheme for solving the related fixed point equations, we derive performance bounds for the closed-loop system under MPC. Our analysis, as well as numerical examples, suggests new ways of choosing the terminal cost and terminal constraints, which are not related to the solution of the Riccati equation of the original problem. The resulting method can have a larger feasible region, and cause hardly any loss of performance in terms of the closed-loop cost over an infinite horizon.

keywords:

Model predictive control, optimal control theory.1 Introduction

Model predictive control (MPC) is a well-established scheme for constrained optimal control problems with continuous state and control spaces. In its most widely adopted form (Scokaert and Rawlings, 1998) a system model is used to predict its performance over some finite number of stages, and a terminal cost is added to account for the trajectory beyond this prediction horizon. Moreover, an additional constraint is imposed on the state at which the prediction ends. Suitably designed terminal cost and constraint lead to desirable properties (Mayne et al., 2000). A recent monograph (Bertsekas, 2022b) shows that this structure of MPC is quite similar to the algorithms applied in the high-profile successes in the field of reinforcement learning (Silver et al., 2017). It has also developed a conceptual framework centered around dynamic programming (DP), which is useful for analyzing the performance of MPC.

In this work, we apply the tools introduced in (Bertsekas, 2022b), and investigate the impact of the terminal cost on the performance of MPC measured by the closed-loop cost accumulated over infinite stages. Using unconstrained and constrained linear quadratic regulation (LQR) problems as a vehicle, we derive performance bounds of MPC applied to those problems compared against optimal control. The insights gained from our analysis suggest new designs of those terminal ingredients, which likely make MPC feasible for a larger set of states, while cause little to no degradation in its performance.

For the LQR problem, a performance bound of MPC is given (Bitmead et al., 1985). It relies on the monotonicity property, which holds well beyond the problem considered here, as discussed in (Bertsekas, 1975, 1977). A suboptimality analysis that is similar in purpose to our study is reported in (Grune and Rantzer, 2008). It relies in part on a relaxed form of DP introduced in (Rantzer, 2006). Our work makes different assumptions, and leads to new design choices of the terminal ingredients, and may be regarded as complementary to that of (Grune and Rantzer, 2008).

Unlike MPC where the performance bound analysis is relatively rare, bounds are pervasive in the study of Markovian decision problems (MDP), with some classical results presented in (Denardo, 1967). (Bertsekas, 2022b) takes an abstract approach that unifies the MDP and the problems addressed by MPC. It regards MPC as approximation in value space, where the approximation refers to the fact that terminal ingredients act together to approximate the real optimal cost. It also points out that the typical bounds in MDP may be too conservative to reflect the true performance, which we confirm by deriving better bounds for MPC.

Another concept that is related to our study is the investigation of regret in dynamical systems. Regret is a non-asymptotic performance metric for optimal control problems involving uncertainty. Given a controller, regret is measured by comparing its associated cost over a finite number of stages with that of a known policy with full or partial knowledge of the uncertainty. The regret of an MPC controller for unconstrained problems with process noise has been analyzed in (Yu et al., 2020), for cases where the terminal cost is related to the solution of the Riccati equation. Other related work includes (Muthirayan et al., 2021) and (Wabersich and Zeilinger, 2020). Although the major challenge addressed by these works comes from uncertainty or partial information, the results echo our conclusion that much of the credit for good performance goes to the MPC structure itself. This provides an alternative perspective for our work and may point to a direction of extensions of the results reported here.

In summary, this paper makes the following contributions:

-

(1)

We derive performance bounds for MPC applied to unconstrained and constrained LQR problems, as well as nonlinear systems;

-

(2)

We propose a new design for the terminal ingredients, which likely leads to a larger region where MPC is feasible;

-

(3)

We conduct numerical studies that verify our theoretical analysis.

2 Performance Bounds for the Linear Quadratic Problem

2.1 Preliminaries

We consider discrete-time optimal control problems with system dynamics

| (1) |

and -th stage cost defined

| (2) |

where prime denotes transposition, ,111If and are symmetric positive semidefinite matrices, then the notation () means that the matrix is positive (semi)definite. , stablizable, and detectable. The optimal feedback law [with respect to cost (2) accumulated over an infinite number of stages] is then given by

| (3) |

where is the unique positive definite solution fulfilling the algebraic equation

| (4) |

For this problem, we introduce the Bellman operator defined for some symmetric matrices as

| (5) |

The -fold composition of the operator is denoted by . In addition, given a policy , we define the -Bellman operator as

| (6) |

Similarly, the -fold composition of the operator is denoted by . A matrix will be called a stability matrix if all of its eigenvalues are less than one in absolute value. Let denote the space of real symmetric matrices. For the operators and , the following classical results hold.

Proposition 1

-

(a)

Let so that . Then we have that and .

-

(b)

The equation admits a unique positive definite solution . Moreover, as for so that .

-

(c)

Let be an by matrix such that is a stability matrix. Then the equation admits a unique positive definite solution . Moreover, as for so that .

2.2 Region of Decreasing

We will focus on a special set of symmetric matrices, which we call the region of decreasing. It is defined as

| (7) |

This set of matrices plays an important role in the design of model predictive control, which is a consequence of the definition. The following result can be proved by applying Theorems 10.4 and 10.6 from (Bitmead and Gevers, 1991).

Proposition 2

For all , for all ; moreover, .

Given a matrix and a positive integer , we are interested in solving the problem via the following scheme:

| (8) | ||||

for all . If the minimum is attained at , the scheme defines a policy by setting ; finite horizon LQR intuition shows that there exists a such that . If we apply the Bellman operator and -Bellman operator introduced in (5) and (6) respectively, the policy can be defined as

| (9) |

Under our assumption, for , the resulting closed-loop system is stable. This is proved in (Bitmead and Gevers, 1991, Theorem 10.19), and its generalization and connection to performance bound is given in (Bertsekas, 2022b, Section 3.3). Then there exists a unique positive semidefinite solution to the equation , which we denote as . In the rest of this section, we investigate the suboptimality of the scheme (8), which is measured through the difference between the infinite horizon cost obtained by the resulting policy (encoded through the matrix ) and the optimal infinite horizon cost (encoded through the matrix ).

To investigate the properties of , we introduce some additional notation. stands for the induced -norm of the matrix . Following (Bertsekas, 2022a, p. 382) we denote by a special weighted Euclidean norm such that for some . For those two norms, there exist some positive constants and such that

| (10) |

holds for all by matrices . An analytical formula for computing and is given in the Appendix A. Both norms have the submultiplicative property. In addition, we define positive integers and by , and , where is the horizon length in (8). Then by the submultiplicative property of the norm, we have that The norm also connects to positive semidefiniteness through the following lemma.

Lemma 3

Let and be symmetric matrices such that . Then .

Now we are ready to state our first result.

Proposition 4

For all and all integers ,

| (11) |

Moreover, if satisfies , then

| (12) |

We first show that

| (13) |

Since , we have and for all . Then

2.3 Performance Bound via Contraction

From the above results we can obtain a performance bound for by exploiting the contraction properties of the operators and .

Proposition 5

Let and defined as in (9). Then we have that

| (14) |

Denote as the matrix . By Prop. 4 with , we have

| (15) |

In addition, combining Prop. 4 with and the norm equivalence relation (10) yields

| (16) |

where the second inequality is due to contraction property of the operator .

We then proceed by showing that

| (17) |

We use the triangle inequality to write for every ,

Taking the limit as and in view of the convergence , we obtain the inequality (17).

For the value , by using the triangular inequality, and the definition of in (9), we have

| (18) |

where in the last step, we use the inequality (2.3). Combining the (2.3) to (17) gives

Applying on the left and on the right, we have

In view of the inequality (15), we get the desired result.

Remark 6

Our proof has followed closely the approach for establishing the classical error bound for the MDP, cf. (Bertsekas, 2022a, Prop.2.2,1). In particular, if and , then the bound established above can be obtained via applying Prop. 2.1.1(e) and Prop. 2.2.1 in (Bertsekas, 2022a, Prop.2.2,1), and the inequality (14) reduces to the known result in Prop. 2.2.1. This bound indicates that by selecting close to , the MPC policy obtained by solving (8) will perform close to the optimal policy in the infinite horizon.

2.4 Performance Bounds via Monotonicity and Newton Step Interpretation

Alternative bounds can be obtained based on monotonicity and the Newton step interpretation. We first derive the bound that relies solely on the monotonicity, and then provide an additional bound that is obtained by combining the two properties.

Proposition 7

Let and defined as in (9). Then we have that

| (19) |

Recall that the policy is defined as

Since , due to the monotonicity property, we have that . Therefore, applying on both sides and using the definition of , we have

Applying repeatedly on both sides and in view of its monotonicity property, we have Taking the limit as and we have On the other hand, we have , which implies that

where the second to last inequality is due to (11), and the last inequality is due to (12).

Remark 8

Note that by definition , and focusing on the last term of (14), we see that the bound in Prop. 7 is always tighter than the one in Prop. 5. This is consistent with what is noted in (Bertsekas, 2022b, Appendix A.3). Still, the result given in Prop. 5 resembles the classical performance bound in MDP, and holds true for where , while the bound in Prop. 7 only holds for .

Apart from the monotonicity properties of the operators and , the Newton step interpretation of computing can also be brought to bear for establishing another bound on the suboptimality of . For completeness, a slight generalization of the following lemma adopted from (Hewer, 1971, Theorem 2) and its proof are provided in the Appendix B.

Lemma 9

Let and defined as in (9). Then there exists such that

| (20) |

An explicit formula for is provided in Appendix B. Combining Lemma 9 and Prop. 4 leads to the following bound.

Proposition 10

Let and defined as in (9). Then there exists such that

| (21) |

Remark 11

The quadratic term in (21) manifests the nature of scheme (8) as a step of Newton’s method for solving (4). In addition, if , then the bound based on Newton step interpretation is tighter than the bound provided by Prop. 7. This is likely to happen if the value is large, which in turn makes the value small.

3 Performance Bound for Constrained Problems

Let us now consider problems involving both state and control constraints. For the same stationary dynamics (1) and stage cost (2), there are state constraint and control constraint . We assume that both and are compact and convex, and contain the origin in their interior.

The problem can be modeled as an optimal control problem involving stationary dynamics (1) and stage cost

| (22) |

where is an indicator function that maps to if , and otherwise. We consider stationary policies , which are functions mapping to .

The cost function of a policy , denoted by , maps to , and is defined at any initial state , as

| (23) |

subject to , . The optimal cost function is defined pointwise as

| (24) |

A stationary policy is called optimal if

It has the property that

| (25) |

if the minimum in (25) can be attained. For the problem considered here, it may be shown that there is a stationary optimal policy. A brief discussion regarding the existence of a stationary optimal policy is provided in Appendix C.

Similar to the scheme in (8), we may apply MPC of the following form to solve the problem

| (26) | ||||

where is a suitably designed matrix, and is a suitably designed set. If the minimum of (26) is attained at , then the scheme defines a suboptimal policy by setting . As in the unconstrained case, we would like to investigate the suboptimality of , depending on the choice of and , where suboptimality of the policy is measured by .

Due the presence of state constraint and control constraint , the analysis given in Section 2 does not apply as it is. Still, by suitably modifying the relevant definitions, a similar qualitative analysis remains valid. In particular, we denote by the set of all functions . A mapping that plays the key role in our development is the Bellman operator , defined pointwise as

| (27) |

This operator is well-posed in view of the nonnegativity (22) of the stage cost. In addition, we denote as the -fold composition of with itself, with the convention that . For every fixed policy , we also introduce the -operator , which is defined pointwise as

| (28) |

The operators and are generalizations of and . Their relations are extensively discussed in (Bertsekas, 2022b, Chapter 4).

Given a positive semidifnite matrix and a set , we can define a function associated with and as

| (29) |

Using the operator notations (27), (28), as well as the function defined in (29), the policy defined by the scheme (26) can be written succinctly as

| (30) |

which is a generalization of (9).

For the constrained problem, we can also define the region of decreasing, denoted as . It is given as a set of functions as

| (31) |

3.1 Performance Bounds via Monotonicity and Newton Step Interpretation

For the constrained problem, a result based on contraction, as in Section 2.3 may not be applicable. However, for suitably designed function , results that parallel Prop. 7 can be established. The proof of the result is deferred to Appendix D.

Proposition 13

Let and defined via (30). Then

| (32) |

for all with , . In addition, if such that for all , then

| (33) |

for all with , .

Remark 14

A close examination of the proof shows that the above bounds hold well beyond the constrained linear systems discussed here. If a stationary optimal policy exists, the performance bounds hold for the case where control constraints are state dependent, i.e., , or problems involving nonlinear, as well as hybrid systems. In fact, the tools applied here have been used to analyze MPC for hybrid systems in (Baoti et al., 2006).

3.2 New Designs for the Terminal Costs and Constraints

For the MPC scheme of the form (26), a common choice for has been given in (4), i.e., the optimal cost function for the unconstrained LQR problem. The rationale for such a choice is that the corresponding would be optimal when is near the origin, thus the performance of over all feasible should also be near optimal. However, in the presence of control constraints and if the matrix defined in (3) is large, the associated terminal constraint in (26) can be small, which means the subset of from where the scheme (26) is feasible (or equivalently, the support of ) is small.

On the other hand, our analysis suggests that a choice of that is near may not be necessary. In fact, one may prefer a much larger if its associated set can be larger. A plausible choice that may lead to larger is the solution of the equation

| (34) |

where . Such a matrix belongs to the region of decreasing, and it is likely that the corresponding is enlarged. This is confirmed in our numerical examples.

We note that a large terminal cost is also advocated in (Limón et al., 2006), where the terminal constraint is removed. Our study here has deployed different analytical tools and focuses on the classical form with both terminal cost and constraint. Still, it suggested that a terminal cost that corresponds to a smaller control would be preferred.

4 Numerical Studies

In this section, we provide numerical examples to demonstrate the differences between the bounds established in the preceding sections and the actual performance. It is observed that the actual performance is often much better than the bounds suggest, further corroborating our main point that it is not necessary to design the terminal cost close to optimal at the expense of reduced support of .

4.1 Numerical Study Results for LQR

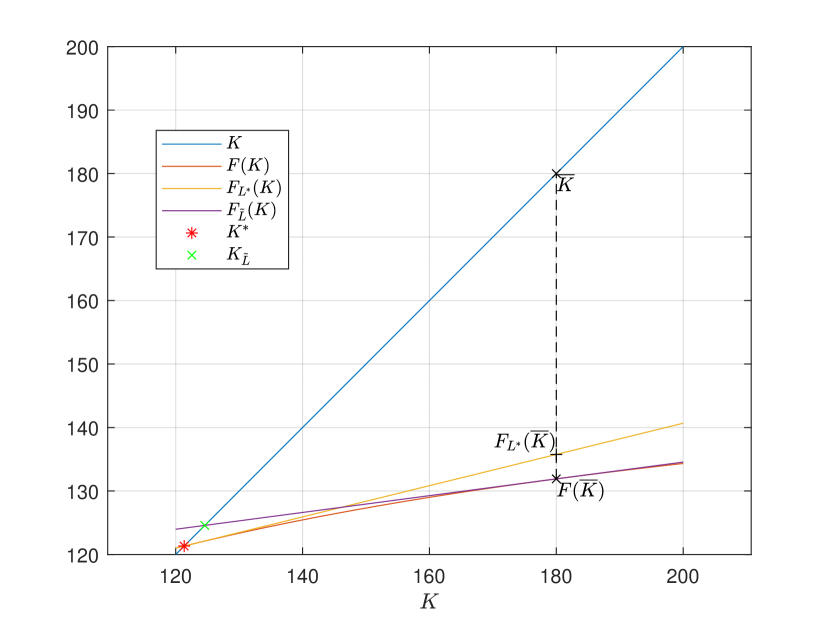

Example 15 (Bellman curve for a scalar example)

In this example, we consider a scalar system. The purpose is to illustrate the performance bound (19) based on monotonicity and the Newton step interpretation, as shown in Fig. 1. The system parameters are . We set so that . In this case, we have , the bounds (14), (19) and (21) are given as , and respectively. The interpretation of Newton’s step is evident by noting that is obtained by constructing a tangent line of at .

Example 16 (Conservativeness of bounds)

We consider a two dimensional double integrator and a four dimensional example from (Kapasouris et al., 1988). The problem data of those examples are listed in Appendix E. The matrices in (8) are computed by solving (34) with . Their magnitudes as well as their relations to the corresponding are listed in Table 1.

| Problem | ||

|---|---|---|

| 2-D | ||

| 4-D |

The actual optimality gap and various performance bounds for those two systems with different are listed in Table 2. It is clear that the actual performance is much better than what the performance bounds suggest. In addition, the bound (14) is always inferior than (19) and (21), which is consistent with our analysis.

4.2 Numerical Study Results for Constrained LQR

Here we investigate the performance of the scheme (26) when both state and control constraints are present. We introduce constraints to the two- and four-dimensional problems studied in Example 16. In particular, in Example 17, we demonstrate that with our choice of , the support of can be enlarged, while there is hardly any loss of optimality.

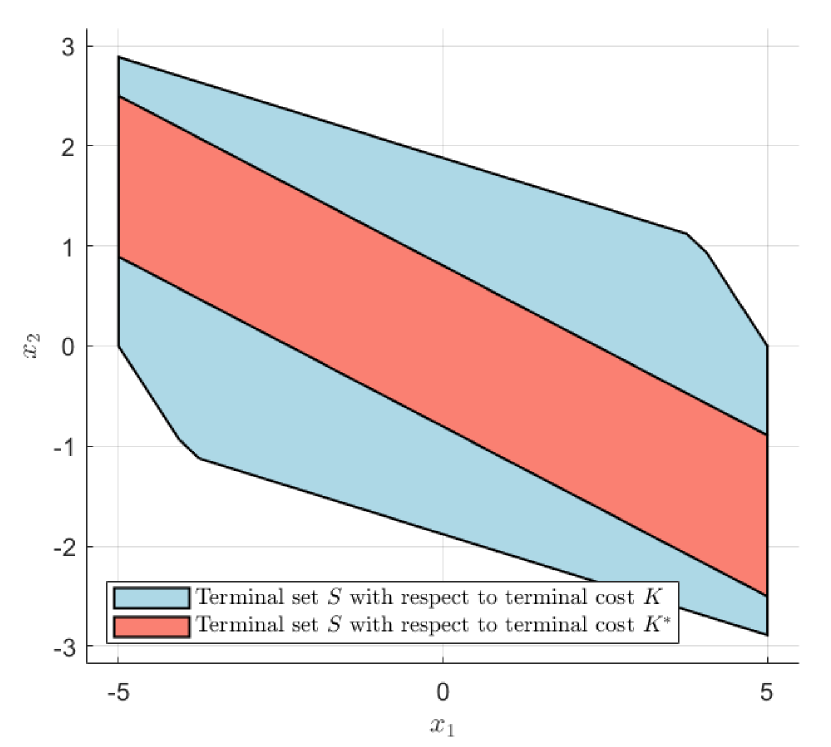

Example 17 (Enlarging the feasible region)

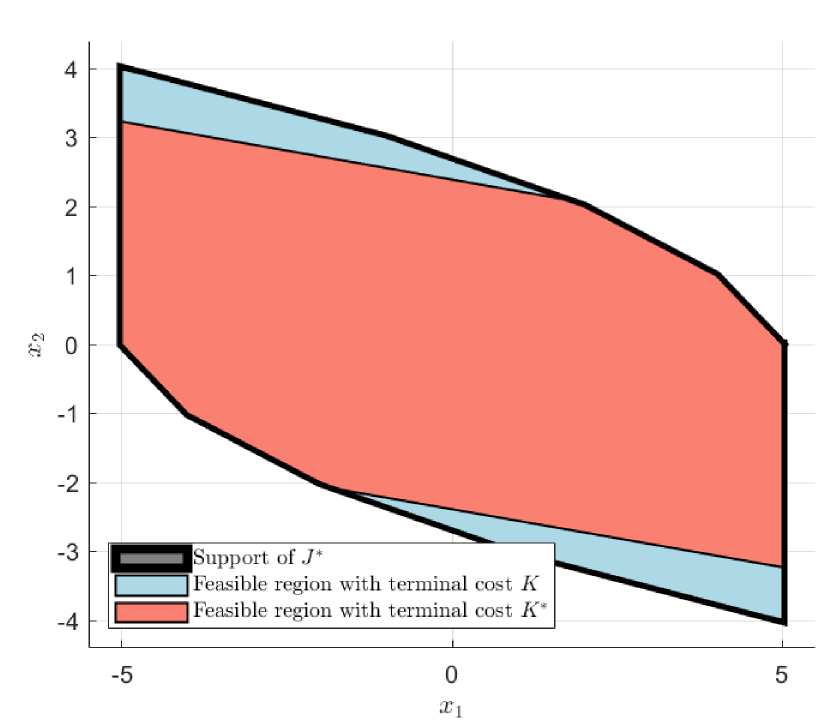

We consider the constrained version of the two-dimensional system investigated in Example 16. We use the same as in Example 16 and set . The sets designed according to and are shown in Fig. 2. The feasible regions of the MPC with those terminal constraints are illustrated in Fig. 3. For our choice of , the feasible region practically coincides with the support of .

If we vary the parameter in (34), the resulting would change as well. The following table shows the ratio of the respective terminal set volumes and for and with different values of in (34).

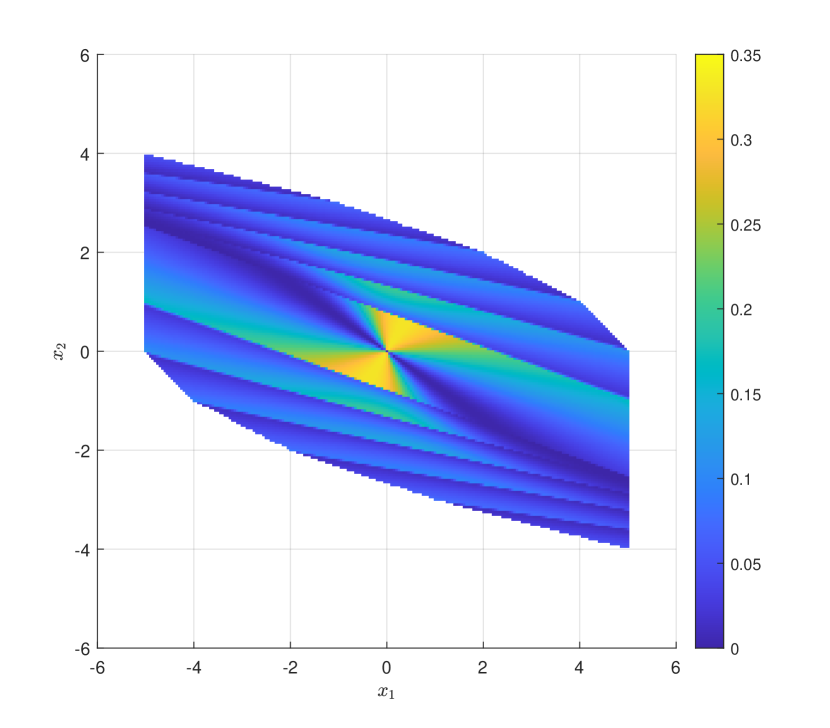

The suboptimality of the MPC scheme with our choice of (with ) and the optimal (approximated in the study by setting ) is given in Fig. 4. It can be seen that despite a that is much larger-than , the closed loop system hardly loses any performance.

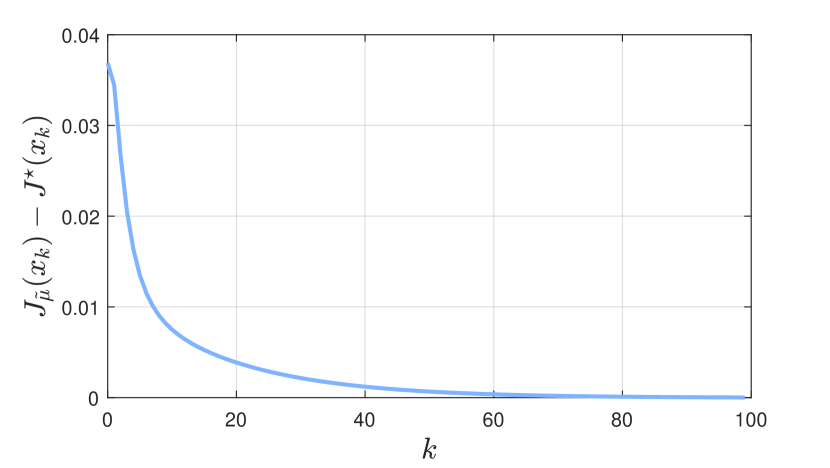

Example 18 (Performance loss)

Finally, we investigate the constrained version of the four dimensional system studied in Example 16. Using the terminal matrix applied there and setting , we show the optimality gap along a trajectory, which is driven by the policy , starting from . The result is shown in Fig. 5. To put the values in context, the optimal cost from is . Therefore, the performance is practically optimal.

5 Conclusion

We considered the performance of MPC applied to unconstrained and constrained LQR problems measured by the closed-loop cost accumulated over an infinite horizon. We derived performance bounds that connect the performance of MPC with its terminal cost as well as the true optimal policy of the problems. The derived bounds apply to problems beyond the scope of linear systems and suggest new design of terminal cost and constraint that is not related to the optimal cost of the problem. Numerical studies showed that the new design leads to larger region from which MPC is feasible, while cost little to none performance.

References

- Baoti et al. (2006) Baoti, M., Christophersen, F.J., and Morari, M. (2006). Constrained optimal control of hybrid systems with a linear performance index. IEEE Transactions on Automatic Control, 51(12), 1903–1919.

- Bertsekas (2022a) Bertsekas, D. (2022a). Abstract dynamic programming. Athena Scientific.

- Bertsekas (2022b) Bertsekas, D. (2022b). Lessons from AlphaZero for Optimal, Model Predictive, and Adaptive Control. Athena Scientific.

- Bertsekas and Shreve (1978) Bertsekas, D. and Shreve, S.E. (1978). Stochastic optimal control: the discrete-time case. Academic Press. Republished by Athena Scientific, Belmont, MA, 1996.

- Bertsekas (1975) Bertsekas, D.P. (1975). Monotone mappings in dynamic programming. In 1975 IEEE Conference on Decision and Control including the 14th Symposium on Adaptive Processes, 20–25. IEEE.

- Bertsekas (1977) Bertsekas, D.P. (1977). Monotone mappings with application in dynamic programming. SIAM Journal on Control and Optimization, 15(3), 438–464.

- Bitmead and Gevers (1991) Bitmead, R.R. and Gevers, M. (1991). Riccati difference and differential equations: Convergence, monotonicity and stability. In The Riccati Equation, 263–291. Springer.

- Bitmead et al. (1985) Bitmead, R.R., Gevers, M.R., Petersen, I.R., and Kaye, R.J. (1985). Monotonicity and stabilizability-properties of solutions of the riccati difference equation: Propositions, lemmas, theorems, fallacious conjectures and counterexamples. Systems & Control Letters, 5(5), 309–315.

- Denardo (1967) Denardo, E.V. (1967). Contraction mappings in the theory underlying dynamic programming. Siam Review, 9(2), 165–177.

- Grune and Rantzer (2008) Grune, L. and Rantzer, A. (2008). On the infinite horizon performance of receding horizon controllers. IEEE Transactions on Automatic Control, 53(9), 2100–2111.

- Hewer (1971) Hewer, G. (1971). An iterative technique for the computation of the steady state gains for the discrete optimal regulator. IEEE Transactions on Automatic Control, 16(4), 382–384.

- Horn and Johnson (2012) Horn, R.A. and Johnson, C.R. (2012). Matrix analysis. Cambridge university press.

- Kapasouris et al. (1988) Kapasouris, P., Athans, M., and Stein, G. (1988). Design of feedback control systems for stable plants with saturating actuators. Technical report, Massachusetts Institute of Technology, Laboratory for Information and ….

- Kvasnica et al. (2004) Kvasnica, M., Grieder, P., Baotić, M., and Morari, M. (2004). Multi-parametric toolbox (mpt). In International workshop on hybrid systems: Computation and control, 448–462. Springer.

- Limón et al. (2006) Limón, D., Alamo, T., Salas, F., and Camacho, E.F. (2006). On the stability of constrained mpc without terminal constraint. IEEE transactions on automatic control, 51(5), 832–836.

- Lopez et al. (2021) Lopez, V.G., Alsalti, M., and Müller, M.A. (2021). Efficient off-policy q-learning for data-based discrete-time lqr problems. arXiv preprint arXiv:2105.07761.

- Mayne et al. (2000) Mayne, D.Q., Rawlings, J.B., Rao, C.V., and Scokaert, P.O. (2000). Constrained model predictive control: Stability and optimality. Automatica, 36(6), 789–814.

- Muthirayan et al. (2021) Muthirayan, D., Yuan, J., Kalathil, D., and Khargonekar, P.P. (2021). Online learning for receding horizon control with provable regret guarantees. arXiv preprint arXiv:2111.15041.

- Rantzer (2006) Rantzer, A. (2006). Relaxed dynamic programming in switching systems. IEE Proceedings-Control Theory and Applications, 153(5), 567–574.

- Rawlings et al. (2017) Rawlings, J.B., Mayne, D.Q., and Diehl, M. (2017). Model predictive control: theory, computation, and design, volume 2. Nob Hill Publishing Madison, WI.

- Schäl (1975) Schäl, M. (1975). Conditions for optimality in dynamic programming and for the limit of n-stage optimal policies to be optimal. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 32(3), 179–196.

- Scokaert and Rawlings (1998) Scokaert, P.O. and Rawlings, J.B. (1998). Constrained linear quadratic regulation. IEEE Transactions on automatic control, 43(8), 1163–1169.

- Silver et al. (2017) Silver, D., Hubert, T., Schrittwieser, J., Antonoglou, I., Lai, M., Guez, A., Lanctot, M., Sifre, L., Kumaran, D., Graepel, T., et al. (2017). Mastering chess and shogi by self-play with a general reinforcement learning algorithm. arXiv preprint arXiv:1712.01815.

- Wabersich and Zeilinger (2020) Wabersich, K.P. and Zeilinger, M. (2020). Bayesian model predictive control: Efficient model exploration and regret bounds using posterior sampling. In Learning for Dynamics and Control, 455–464. PMLR.

- Yu et al. (2020) Yu, C., Shi, G., Chung, S.J., Yue, Y., and Wierman, A. (2020). The power of predictions in online control. Advances in Neural Information Processing Systems, 33, 1994–2004.

Appendix A Norm equivalence constants

We provide an analytical formula for the norm equivalence constants and in (10). The results are summarized in the following proposition. A related result is given as (Horn and Johnson, 2012, Theorem 5.6.7).

Proposition 19

Let be an by nonsingular matrix and the norm for a matrix is defined as

where . Then the norm equivalence condition (10) holds with

where and are largest and smallest eigenvalues of , respectively.

For note that

Also note that and

| (35) |

which gives a formula for .

Similarly, for , we have that

Moreover

as given in (35). In addition, we also have that

which completes the proof.

Appendix B Proof for quadratic convergence

We first list two useful lemmas. The first one can be found, among others, in (Lopez et al., 2021, Corollary 2), and the second is derived from (Hewer, 1971, Proof of Theorem 1 part 2)).

Lemma 20

Let be a stability matrix, then .

Lemma 21

Based on the above equality, we are ready to prove the quadratic convergence result.

Proposition 22

Given , there exists some , such that

where is defined by , and satisfies the equation .

Due to Lemma 21, we have that

The difference can be computed as

Using induced -norm for the matrix, we have

| (36) |

where as .

Now consider the term . By straightforward computation, we have that

Thus, we have that

| (37) |

where is given as

Appendix C Existence of a stationary optimal policy

We give a brief discussion on the existence of a stationary optimal policy for the constrained problems considered in Section 3. We provide the outline according to which one can establish the existence of a stationary optimal policy. Since such a result is peripheral to the main point of this work, the detailed discussion is omitted.

Let be the function that is identically zero. Define the sequence of functions by

For every fixed and , consider the sets

defined for . If there exists some such that is compact for all , then we can assert the existence of the stationary optimal policy. This condition is given in the form above in (Bertsekas, 1975). A related condition is derived independently in (Schäl, 1975).

Appendix D Proof of Prop. 13

We first introduce a useful result, which holds well-beyond the scope considered here (Bertsekas and Shreve, 1978, Prop. 5.2). It underlies the importance of the region of decreasing introduced in this work, and is closely related to the control Lyapunov function used in typical MPC analysis, see, e.g., (Rawlings et al., 2017, Definition B.39). The result stated below is adopted from (Bertsekas, 2022a, Prop. 4.3.4).

Lemma 23

Let and be some stationary policy. Then we have that

| (39) |

Moreover, if the inequality holds for all , then , .

Now we are ready to prove Prop. 13. {pf} Since , then . Therefore, we have

Since the policy is defined via (30), applying on both sides of the above inequality, we have that

where the equality is due to (30). By Lemma 23, we have as an upper bound of , i.e.,

Subtracting on both sides of the inequality leads to the left inequality of (32).

The right inequality in (32) follows from the definition of . In particular, for every , every stationary policy and every integer , we have that

The inequality follows by considering the optimal policy . In particular, we have that

| (40) |

where , . In view of (39) and the fact that for all , we have that

| (41) |

where , . Combining (40) and (41) together gives the desired result.

The inequalities in (33) are obtained by noting that .

Appendix E Problem data for numerical examples

For the two dimensional example in Example 16 and in Example 17 the system matrices are

and the cost matrices are taken to be and the identity matrix of dimension two for . In Example 17 the state and input constraints are and . For this example, the matrix is taken to be the solution of (34) with .

For the four dimensional example in Examples 16 and 18, the system matrices are taken to be the approximate time-invariant model studied in (Kapasouris et al., 1988). The continuous dynamics are discretized with a zero-order-hold and a sampling time of resulting in the following discrete time matrices

In Example 17 the state and input constraints are and . The matrix for this example has been taken to be the solution of (34) with .