Time series quantile regression using random forests

Abstract

We discuss an application of Generalized Random Forests (GRF) proposed by Athey et al. (2019) to quantile regression for time series data. We extracted the theoretical results of the GRF consistency for i.i.d. data to time series data. In particular, in the main theorem, based only on the general assumptions for time series data in Davis and Nielsen (2020) , and trees in Athey et al. (2019) , we show that the tsQRF (time series Quantile Regression Forests) estimator is consistent. Davis and Nielsen (2020) also discussed the estimation problem using Random Forests (RF) for time series data, but the construction procedure of the RF treated by the GRF is essentially different, and different ideas are used throughout the theoretical proof. In addition, a simulation and real data analysis were conducted. In the simulation, the accuracy of the conditional quantile estimation was evaluated under time series models. In the real data using the Nikkei Stock Average, our estimator is demonstrated to be more sensitive than the others in terms of volatility, thus preventing underestimation of risk.

1 Introduction

Quantile Regression (QR), proposed by Koenker and Bassett (1978) , is regression model that has been applied in various fields. QR analyzes the effects of covariates on outcomes by focusing on quantiles rather than means. Therefore, it can flexibly analyze the effect of covariates on the tail of the conditional distribution, which cannot be captured by regression on the mean. QR is used in a wide range of fields, including economics, medicine, and epidemiology, and is applicable not only to cross-sectional data, but also to panel data, for which the theory is well developed (Koenker , 2005) . In the analysis of time series data, many studies have focused on the dynamics of the mean of the series, and on that of the conditional distribution. Therefore, the estimation of conditional quantiles of time series data by QR can capture the local and quantile-specific dynamics of time series and is expected to improve the quality of analysis.

Research on QR for time series data is ongoing. Value-at-Risk (VaR) is one of the criteria used to measure the market risk of an asset in the field of risk management. Because VaR is defined as the quantile of the asset return at time , it is necessary to estimate the conditional quantile regression function to estimate VaR. There are two methods to estimate the quantile: parametric and nonparametric methods. For parametric QR, Koul and Saleh (1995) proposed a conditional quantile estimator for AR models, Koenker and Zhao (1996) proposed ARCH models, Taylor (1999) introduced a linear VaR model, and Chernozhukov and Umantsev (1996) introduced a quadratic VaR model. The CAViaR model proposed by Engle and Manganelli (2004) is a broader class of models in time series QR for VaR estimation. In CAViaR, the effect of past VaR on VaR at time is described as linear, and the effect of the observed time series on VaR at time is modeled linearly or nonlinearly by the researcher. Parametric QR has good properties in terms of interpretation and ease of implementation. However, parametric models have a serious bias if they are misspecified. To avoid this problem, Hall (1999) , Cai (2002) , Wu et al. (2007) and Cai and Wang (2008) proposed a nonparametric method for estimating the conditional distribution function using kernel smoothing. In particular, Cai (2002) showed that the Weighted Nadaraya-Watson (WNW) estimator proposed by Hall (1999) for time series satisfying the -mixing property has consistency and asymptotic normality. Furthermore, Cai and Wang (2008) proposed a Weighted Double-Krnel Local Linear (WDKLL) estimator, an extension of the WNW estimator, and showed its consistency and asymptotic normality. However, in a nonparametric quantile regression estimator using smoothing with kernel functions, the accuracy of the estimator highly depends on the choice of kernel function and bandwidth parameter.

Random forest is a representative algorithm in machine learning that has been successfully used in various applications since its proposal in Breiman (2001) In recent years, the asymptotic properties of the estimators obtained by random forests have been studied in terms of consistency (Biau et al. (2008) ; Denil et al. (2013) ; Scornet et al. (2015) , and asymptotic normality (Wager and Athey (2018) ). Consequently, random forests are now treated not only as a predictive model but also as a nonparametric statistical model.

Various extensions of random forests have also been proposed. A method for estimating conditional quantiles using random forests for i.i.d. data is quantile regression forests (Meinshausen (2006) ). Davis and Nielsen (2020) showed that random forest estimators are consistent with the problem of regression on the conditional mean of time series data with -mixing properties.

Among the recent extensions of random forests, the most notable is the Generalized Random Forests (GRF) by Athey et al. (2019) , which estimates a parameter defined as the solution to a local estimating equation. Athey et al. (2019) showed that the estimator obtained by the GRF had consistency and asymptotic normality under i.i.d. data observations. Thus, from a theoretical perspective, the GRF can be used to estimate parameter.

In this study, we devote quantile regression estimators to time series data using GRF. Thus, it is necessary to extend the existing studies to the following points: Davis and Nielsen’s results for time series data focus on estimating a regression model for the mean, which is applicable to quantile regression. However, this method assumes that the number of samples in each terminal node (leaf) is proportional to sample size. It is difficult to verify this assumption when considering applications. The subsample size included in the leaf should not depend on the sample size. In the GRF, the subsample size in the leaf can be fixed to resolve the above problem. The contribution of this study is to propose a time series Quantile Regression Forest (tsQRF) using the GRF framework for -mixing time series data. Furthermore, we extend the theoretical results of GRF consistency for i.i.d. data to time series data. In particular, in the main theorem, based only on the general assumptions for time series data in Davis and Nielsen (2020) and trees in Athey et al. (2019) , we showed that the tsQRF estimator is consistent. We also visualized the convergence of the tsGRF estimator through several simulation settings and compared its conditional quantile estimation accuracy with that of the WNW estimator. Furthermore, we fit the proposed method to the Nikkei Stock Average data and compared it with the WNW estimator to clarify the high sensitivity of tsQRF to time series volatility.

The remainder of this paper is organized as follows. Section 2 discusses the properties of the quantile regression estimator using the GRF. Therefore, we define the double-sample tree score and GRF score, and then show the consistency of our estimator. Section 3 discusses the asymptotic behavior of the estimator and compares its accuracy with that of the WNW estimator through simulations. Section 4 illustrates the result of applying the proposed method to Nikkei Stock Average data and compares the results with those obtained using the WNW estimator. Finally, Section 5 summarizes the discussion and presents future issues. Concrete proofs of the theoretical results presented in Section 2 are provided in the appendix.

2 Theoretical Results

Let be a sequence of i.i.d. random variables with and , and fix an integer . Given a measurable function , define a process

| (2.1) |

In this paper, we impose the followings.

Assumption 1.

-

(A-1)

The random variable admits a density which is positive almost everywhere on and, for some ,

Moreover, the cumulative distribution function of satisfies

for any .

-

(A-2)

The function in (2.1) is bounded and Lipschitz continuous.

Remark 1.

(A-1) and (A-2) include assumptions (A1) and (A2) of Davis and Nielsen (2020) , which implies that the process is strictly stationary and the -th order Markov chain strictly ensured geometrical ergodicity (c.f., An and Huang (1996) ,Theorem3.1) and exponentially -mixing (c.f., Doukhan (2012) ,p.89). Hence, let denote the -mixing coefficient. Then we have 444For two sequence and , we write if there exists a constant such that for all . under (A-1) and (A-2).

Remark 2.

On the other hand, we do not assume assumption (A-3) of Davis and Nielsen (2020) which is a condition for the minimum subsample size falling in each leaf. Instead, we introduce PNN (Potentical Nearest Neighber) -set in the splitting rule following Wager and Athey (2018) and Athey et.al. (2019) (see (A-5)).

Let and be compact subsets of the spaces taken value of and . Let 555The is a set of all uniformly bounded real functions on . be a set of function

In this paper, under some fixed , we interested in the estimation or prediction of conditional -quantile function defined as solution of the following locall estimationg equation:

| (2.2) |

Note that is a functional of , is a function of for any fixed , and . Throughout the paper, we use as the uniform norm over (i.e., ), and as the uniform norm over (i.e., ).

Remark 3.

As the empirical version of the in (2.2), we introduce the Generalized Random Forest (GRF) score , which will be defined below.

2.1 Double-sample tree score and Generalized Random Forest (GRF) score

Given a vector of initial data independent of , we suppose that observations from the model (2.1) are available and we group them in input-output pairs,

In this paper, we construct an conditonal quantile estimator based on the method of Athey et al. (2019). To do so that, we first intoduce a family of subsambles of by where is an index subset of defined below.

Definition 1.

(Double-sample) Let be subsample size and let an index set be with . A family of the index set denoted by is defined as follows:

where the elements of are different from each other. In addition, for any , subsamples and of are defined by and with , respectively.

In the double-smple tree defined below, achieves “honesty” by dividing its training subsamples into two halves and . Then, -sample is used to place the splits, while holding out the -sample to do within-leaf estimation falling in each leaf. In what follows, we define the splitting rule only by using -sample.

Definition 2.

(Splitting rule) Given -sample, we define a sequence of partitions by starting from and then, for each , construct from by replacing one set (parent node) by (childe node) and , where the split direction is randomly chosen 666In practice, the optimal direction is chosen from directions at each step of the division where for some ., and the split position is chosen to maximize a criterion .

In this paper, the criterion is the same as that of Athey et al. (2019) . Furthermore, we impose the following assumptions for the splitting rule.

Assumption 2.

-

(A-3)

(-Regular) Every split puts at least a fraction of the observations (of -sample) in the parent node into each child node, with .

-

(A-4)

(Random Split) At every split, the probability that the tree splits on the -th feature (i.e., ) is bounded from below by some , for all .

-

(A-5)

(PNN (Potential Nearest Neighbor) k-set) There are between and observations (of -sample) in each terminal node .

-

(A-6)

(Subsample Size) Subsample size scales for some with

Remark 4.

This assumption on is the same as (13) of Athey et al. (2019) , in which and as is satisfied.

Under this splitting rule, we denote a given partition of the feature space by , and the subspace (leaf) of rectangular type created by the partitioning by (). Then,

where , with () being the split direction for satisfying (A-4), independently, each other.

In addition, we introduce a map which transforms from the input vector to by

where is a cumulative distribution function defined by with

| (2.3) |

and . Based on the map , we define . Let be a partition of feature space in the same manner of with and replaced by and . Also, let be the leaf containing the test point transformed from the (original) test point into . Then, the moment bound of holds (see Lemma 1). Moreover, the same moment bound of also holds (see Corollary 1).

By and , the double-sample tree score is defined as follows.

Definition 3.

(Double-sample tree score) Under an observed data , a random vector , and any fixed , we fix a partition of the feature space by Definition 2. Then, for any and , the double-sample tree score is defined by

where is a leaf containing the test point ; ; and .

Gathering the double-sample tree scores, we introduce the GRF score.

Definition 4.

(Generalized Random Forest (GRF) score) Let be the double-sample tree score by Definition 3. Then, for any and , the GRF score is defined by

where

and

2.2 Time Series Quantile Regression estimator

Based on defined by Definition 4, we intoroduce a conditional quantile function estimator as follows.

Definition 5.

Under an observed data , the GRF score for any by Definition 4. Then, the conditional quantil function estimator is defined by

| (2.4) |

Here we impose the following assumption in order to guarantee the consistency of our estimator.

Assumption 3.

-

(A-7)

There exsists some constant , such that, for almost surely,

This assumption corersponds to the assumption 5 of Athey et al. (2019) . Then, we have our main result, that is, uniformly consistency of the conditionl quantile function estimator .

Theorem 1.

The proofs of the theorems, lemmas and corollary are given in Appendix A.

When is large, it is not realistic to generate all possible types of tree. In practice, under a sufficiently large , we randomly choose types of subset of defined by , and generate a double-sample tree score based on the subsample for each .

Definition 6.

(Generalized Random Forest (GRF) score) Define . For each subsamples determined by and , we generate the double-sample tree score by Definition 3. Then, for any and , the GRF score is defined by

where

and is a leaf containing the test point ; .

Based on defined by Definition 6, we introduce another conditional quantile function estimator as followns.

Definition 7.

Under an observed data , the GRF score for all by Definition 6. Then, the conditional quantile function estimator is defined by

| (2.5) |

If is sufficiently large, we have uniformaly consistency of as follows.

3 Simulation

In this section, we first check the asymptotic properties of tsQRF for several data generation settings. To illustrate the characteristics of our method, we compared tsQRF and WNW estimators (Cai, 2002) .

3.1 Data generation process

Four data generating models were used in this simulation. First, model (a) generates data using a bounded oscillating function, which was used by Davis and Nielsen (2020).

-

(a)

First order Markov chain model (Davis and Nielsen, 2020 , equation (4.1) )

This model satisfies the boundedness assumption (A-2) for function . However, such a bounded model is often not used in an actual time series data analysis. Therefore, we also generate data from models that do not satisfy (A-2), such as models (b), (c), and (d), and examine how our estimator converges to the true quantile function.

-

(b)

AR(2) model

-

(c)

Non-linear AR(2) model

-

(d)

AR(5) model

For each model, we consider two types of error distribution: the standard normal distribution (normal) and the standard Laplace distribution (Laplace) for . Both distributions satisfy (A-1). The difference between the two error distributions is the behavior of the tail of the distribution. In the simulation, we examined the effects of the tail behavior of error distributions. For each model, the true value of the conditional -quantile given is

where is the inverse of the distribution function of the error term.

In the simulation, length time series data were generated from each model. The first is used as training data for estimating the models, and the remaining is used as test data to evaluate the accuracy of the quantile prediction. We generated replicates of these time series data to compute the estimation/prediction error.

3.2 Evaluation of estimation accuracy for training data (consistency)

First, we illustrate the consistency of the conditional quantile estimated using the tsQRF. We estimated the , and quantiles for each scenario. We used the R package grf to estimate the target quantiles and set the parameters of the GRF as subsample size , number of trees , and the parameter for the ratio of splits (these are all default values from the grf package)

Theoretically, is used for ; however, in practice, when and are sufficiently large, becomes very large, and the computational cost becomes expensive. Therefore, instead of , we restrict the number of trees to ( elements of from are randomly chosen). If is as large as the sample size, the approximation error can be sufficiently small (Wager and Athey (2018)).

In this simulation, we computed the mean and standard deviation of the bias of the estimates and the mean squared error. Let be the training dataset for each replicate . We defined the difference between the true value of the quantiles and the estimated conditional quantiles at as . The average is defined as . The mean (MBias), standard deviation (SDBias), and mean squared error (MSE) of are defined as follows.

We performed the simulation for each data generating model (a) (d) with the length of time series and , and two types of error distribution (normal and Laplace). The MBias, SDBias and MSE for each simulation scenario are summarized in Tables 3.13.3.

| Model | 1% | 10% | 50% | 90% | 99% | ||

|---|---|---|---|---|---|---|---|

| (a) | Normal | 0.297 | 0.021 | 0.004 | -0.012 | -0.288 | |

| 0.297 | 0.018 | 0.000 | -0.017 | -0.294 | |||

| Laplace | 0.652 | -0.017 | -0.003 | 0.015 | -0.667 | ||

| 0.633 | -0.026 | 0.000 | 0.025 | -0.645 | |||

| (b) | Normal | -0.007 | -0.072 | -0.011 | 0.048 | -0.005 | |

| 0.078 | -0.014 | -0.000 | 0.014 | -0.074 | |||

| Laplace | 0.168 | -0.133 | -0.010 | 0.105 | -0.185 | ||

| 0.209 | -0.064 | -0.005 | 0.051 | -0.217 | |||

| (c) | Normal | 0.012 | -0.039 | -0.003 | 0.046 | 0.057 | |

| 0.077 | -0.007 | 0.001 | 0.009 | -0.064 | |||

| Laplace | 0.182 | -0.092 | -0.010 | 0.070 | -0.175 | ||

| 0.254 | -0.026 | -0.002 | 0.033 | -0.211 | |||

| (d) | Normal | -0.281 | -0.163 | 0.000 | 0.161 | 0.263 | |

| -0.170 | -0.108 | -0.002 | 0.107 | 0.168 | |||

| Laplace | -0.260 | -0.289 | 0.001 | 0.277 | 0.210 | ||

| -0.099 | -0.183 | -0.004 | 0.176 | 0.102 |

| Model | 1% | 10% | 50% | 90% | 99% | ||

|---|---|---|---|---|---|---|---|

| (a) | Normal | 0.068 | 0.046 | 0.037 | 0.054 | 0.081 | |

| 0.036 | 0.024 | 0.015 | 0.025 | 0.038 | |||

| Laplace | 0.218 | 0.093 | 0.037 | 0.086 | 0.201 | ||

| 0.088 | 0.042 | 0.016 | 0.042 | 0.096 | |||

| (b) | Normal | 0.084 | 0.045 | 0.031 | 0.048 | 0.083 | |

| 0.041 | 0.019 | 0.014 | 0.022 | 0.039 | |||

| Laplace | 0.222 | 0.089 | 0.039 | 0.081 | 0.260 | ||

| 0.112 | 0.038 | 0.016 | 0.042 | 0.102 | |||

| (c) | Normal | 0.093 | 0.047 | 0.038 | 0.054 | 0.085 | |

| 0.041 | 0.020 | 0.015 | 0.021 | 0.037 | |||

| Laplace | 0.254 | 0.093 | 0.035 | 0.086 | 0.240 | ||

| 0.101 | 0.040 | 0.017 | 0.040 | 0.111 | |||

| (d) | Normal | 0.109 | 0.054 | 0.034 | 0.048 | 0.105 | |

| 0.044 | 0.023 | 0.015 | 0.025 | 0.049 | |||

| Laplace | 0.280 | 0.099 | 0.035 | 0.088 | 0.244 | ||

| 0.117 | 0.036 | 0.016 | 0.040 | 0.112 |

| Mode | 1% | 10% | 50% | 90% | 99% | ||

|---|---|---|---|---|---|---|---|

| (a) | Normal | 0.316 | 0.118 | 0.062 | 0.117 | 0.304 | |

| 0.309 | 0.116 | 0.063 | 0.116 | 0.310 | |||

| Laplace | 1.941 | 0.394 | 0.057 | 0.386 | 1.872 | ||

| 1.865 | 0.393 | 0.056 | 0.397 | 1.875 | |||

| (b) | Normal | 0.182 | 0.091 | 0.055 | 0.090 | 0.189 | |

| 0.156 | 0.067 | 0.038 | 0.066 | 0.158 | |||

| Laplace | 1.211 | 0.287 | 0.085 | 0.273 | 1.195 | ||

| 1.137 | 0.225 | 0.047 | 0.223 | 1.175 | |||

| (c) | Normal | 0.368 | 0.150 | 0.054 | 0.130 | 0.492 | |

| 0.207 | 0.075 | 0.037 | 0.071 | 0.225 | |||

| Laplace | 1.360 | 0.313 | 0.064 | 0.285 | 1.318 | ||

| 1.163 | 0.221 | 0.036 | 0.219 | 1.181 | |||

| (d) | Normal | 0.335 | 0.189 | 0.145 | 0.188 | 0.321 | |

| 0.183 | 0.108 | 0.084 | 0.108 | 0.179 | |||

| Laplace | 1.155 | 0.471 | 0.299 | 0.469 | 1.058 | ||

| 0.794 | 0.281 | 0.161 | 0.279 | 0.791 |

We first discuss the case where follows a standard normal distribution. In model (a), there is no significant difference between and for MBias and MSE, but SDBias is much closer to zero when . In model (b), SDBias and MSE are much closer to zero when than . For MBias, is closer to zero for , but for relatively high (low) levels, such as , is closer to zero. Similarly in model (c), SDBias and MSE are much closer to zero when , and for MBias, is closer to zero for compared to . Because models (b) and (c) have the same lag order (i.e., dimension of covariate space), there is no significant difference in any of the indices, except for the relatively high (low) level. When the lag order is high, as in model (d), MBias is not significantly different, although is closer to zero at , and is closer to zero at all other levels. The accuracy of the estimation decreases slightly as the lag order increases, and in most of the other levels, the model takes values farther from zero than the other models.

Next, we discuss the case in which follows a standard Laplace distribution. In model (a), as in the case of the standard normal distribution, there is no significant difference between and for MBias and MSE, whereas for SDBias, the value approaches zero when . At relatively high (low) levels, such as and , the effect of increasing is smaller for the MBias and MSE than for the other models. In models (b) and (c), as in the case of the standard normal distribution, SDBias and MSE are much closer to zero when , and for MBias, is closer to zero for . For MBias, is closer to zero than . As in the case of the standard normal distribution, is closer to zero at most levels in model (d), and is farther from zero than the other models.

Comparing the case of with the standard normal distribution and the standard Laplace distribution, MBias, SDBias and MSE are farther from zero for the standard Laplace distribution which has a relatively heavy tail distribution. At , this phenomenon is remarkable. Although there are model-specific differences, for most levels, MBias, SDBias, and MSE tend to approach zero as increases, we may conclude that the quantile estimators by tsQRF are consistent with the simulations.

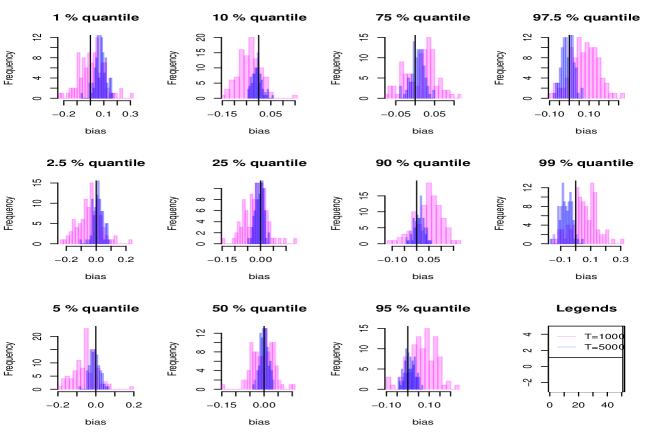

The consistency of the estimators is illustrated in Figure 3.1. The variance becomes small, and the bias approaches zero for compared with except for and . In addition, for , the bias tends to be positive, that is, the estimated value is larger than the true value, as and approaches , the estimated value tends to be smaller than the true value. From Table 3.1, this trend can also be observed in models (a) and (b). The opposite trend was observed for model (d). For the previously mentioned features at the 1% and 99% quantiles, the shape of the distribution of or the boundedness assumption of the function is considered to be affected.

3.3 Comparison of tsQRF and other quantile regression methods

Here, we compare the prediction accuracy when applying the kernel quantile regression of Cai (2002) and tsQRF proposed in this study.

Cai (2002) proposed a nonparametric method for estimating conditional quantiles by determing the inverse function of the Weighted Nadaraya-Watson (WNW) estimator of the conditional distribution function. For strongly stationary and -mixing , the WNW estimator of the conditional distribution function is defined as follows.

Here, is a nonnegative weighting function that, satisfies . In this study, we set using the R package np. To reduce the computational cost, we set the parameters of the np package as itmax=5000, tol=0.1, and ftol=0.1. In this simulation, we used training data and the accuracy of the estimators is compared using test data . The quantile levels to be compared were , and the prediction accuracy was evaluated using the same measures as in Section 3.2, but is replaced by except for . We denote these by , and , respectively.

Tables 3.4 and 3.5 show the , and of tsQRF and kernel QR (WNW) for data generation models (a) - (d), respectively.

| Models | 10% | 50% | 90% | 10% | 50% | 90% | ||

|---|---|---|---|---|---|---|---|---|

| (a) | Normal | WNW | -0.104 | 0.003 | 0.111 | 0.052 | 0.035 | 0.058 |

| tsQRF | 0.019 | 0.004 | -0.008 | 0.051 | 0.039 | 0.058 | ||

| Laplace | WNW | -0.107 | -0.001 | 0.112 | 0.098 | 0.042 | 0.086 | |

| tsQRF | -0.015 | -0.002 | 0.018 | 0.101 | 0.041 | 0.097 | ||

| (b) | Normal | WNW | -0.112 | -0.008 | 0.090 | 0.063 | 0.055 | 0.071 |

| tsQRF | -0.078 | -0.005 | 0.067 | 0.063 | 0.052 | 0.066 | ||

| Laplace | WNW | -0.127 | 0.008 | 0.131 | 0.133 | 0.091 | 0.113 | |

| tsQRF | -0.129 | 0.014 | 0.153 | 0.130 | 0.089 | 0.114 | ||

| (c) | Normal | WNW | -0.136 | -0.002 | 0.138 | 0.054 | 0.046 | 0.059 |

| tsQRF | -0.045 | -0.008 | 0.048 | 0.049 | 0.041 | 0.057 | ||

| Laplace | WNW | -0.173 | -0.015 | 0.130 | 0.099 | 0.044 | 0.088 | |

| tsQRF | -0.100 | -0.018 | 0.069 | 0.096 | 0.038 | 0.090 | ||

| (d) | Normal | WNW | -0.146 | 0.002 | 0.153 | 0.058 | 0.040 | 0.054 |

| tsQRF | -0.180 | 0.003 | 0.184 | 0.062 | 0.042 | 0.057 | ||

| Laplace | WNW | -0.187 | 0.004 | 0.190 | 0.106 | 0.048 | 0.087 | |

| tsQRF | -0.296 | 0.005 | 0.292 | 0.102 | 0.049 | 0.095 | ||

| Model | 10% | 50% | 90% | ||

|---|---|---|---|---|---|

| (a) | Normal | WNW | 0.059 | 0.030 | 0.059 |

| tsQRF | 0.119 | 0.062 | 0.117 | ||

| Laplace | WNW | 0.198 | 0.076 | 0.191 | |

| tsQRF | 0.400 | 0.057 | 0.397 | ||

| (b) | Normal | WNW | 0.078 | 0.054 | 0.077 |

| tsQRF | 0.109 | 0.075 | 0.109 | ||

| Laplace | WNW | 0.307 | 0.175 | 0.262 | |

| tsQRF | 0.348 | 0.162 | 0.352 | ||

| (c) | Normal | WNW | 0.181 | 0.085 | 0.161 |

| tsQRF | 0.161 | 0.063 | 0.135 | ||

| Laplace | WNW | 0.369 | 0.128 | 0.329 | |

| tsQRF | 0.310 | 0.078 | 0.273 | ||

| (d) | Normal | WNW | 0.151 | 0.110 | 0.153 |

| tsQRF | 0.201 | 0.160 | 0.203 | ||

| Laplace | WNW | 0.413 | 0.256 | 0.401 | |

| tsQRF | 0.490 | 0.350 | 0.491 |

We first discuss the case where follows a standard normal distribution. In models (a) and (b), there is no significant difference for , while is closer to zero for tsQRF, and is closer to zero for WNW. In model (c), tsQRF tends to be closer to zero for all indicators. Finally, the WNW was closer to zero for all indicators in model (d).

Next, we discuss the case in which follows a standard Laplace distribution. As in the case of the standard normal distribution, there is no significant difference in in model (a), and tends to be closer to zero for tsQRF, whereas and tend to be closer to zero for WNW. In model (b), is not significantly different, but and are closer to zero for WNW. In model (c), as in the case of the standard normal distribution, tsQRF was approximately zero for all indicators. Finally, model (d) shows that the WNW is approximately zero for all indicators.

4 Empirical Results

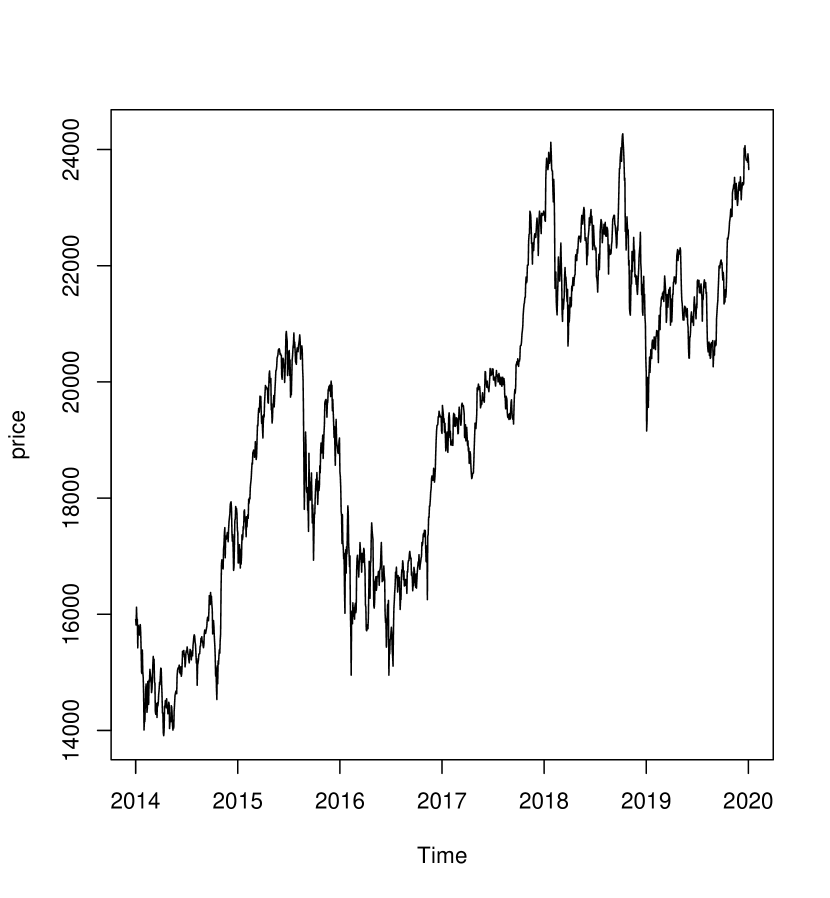

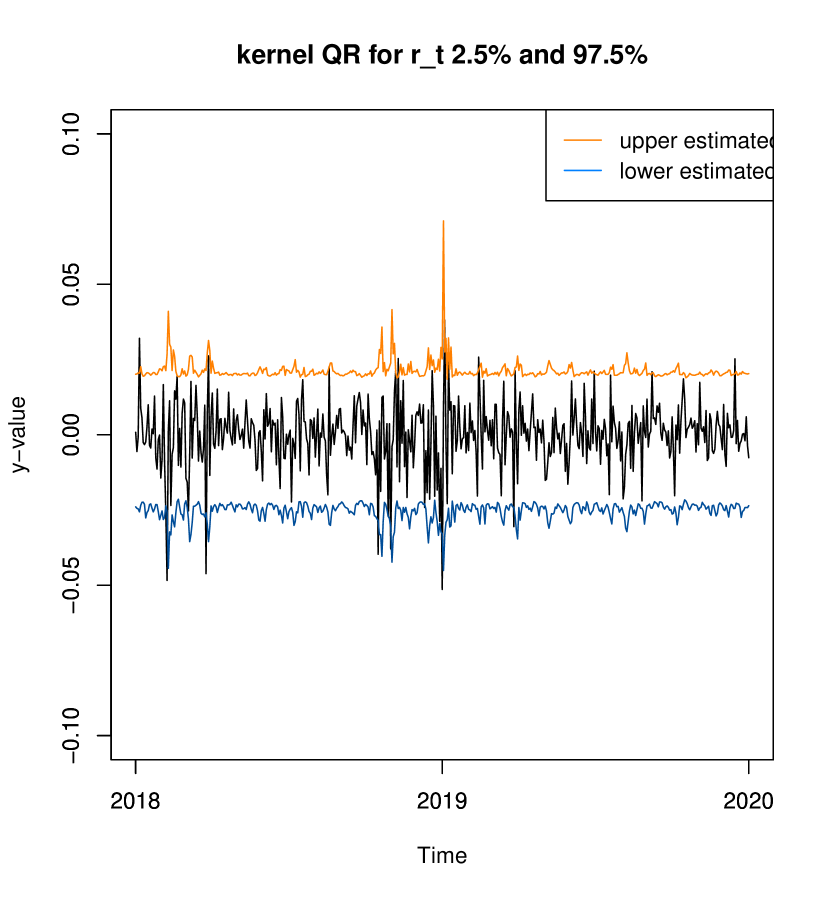

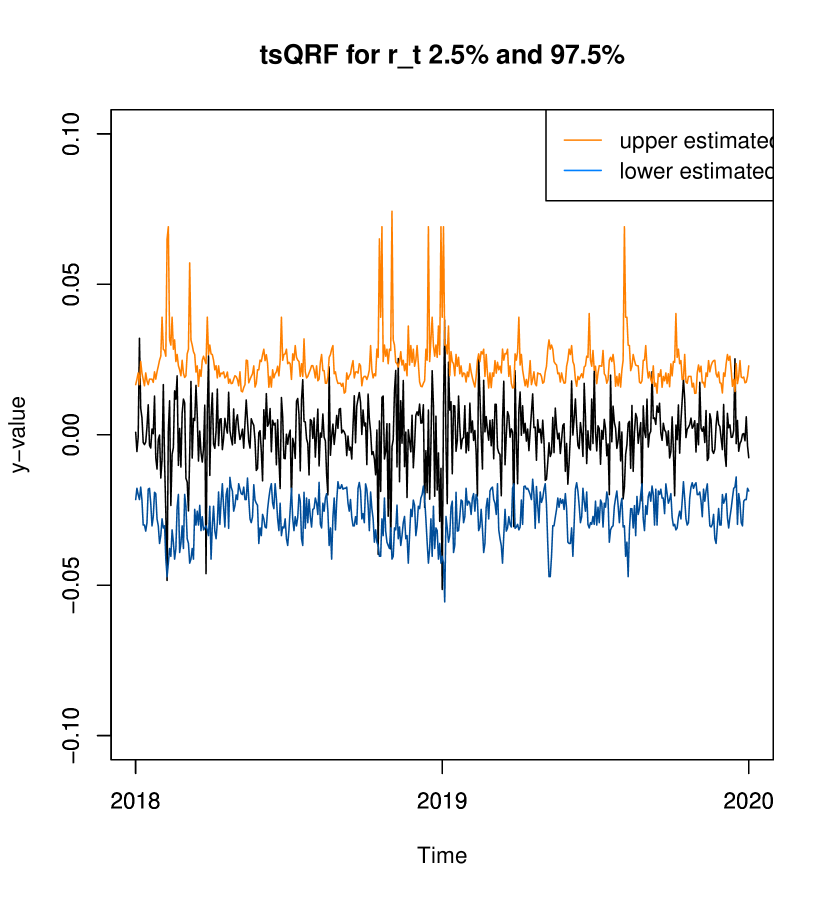

In this section, we analyze the closing prices of the Nikkei Stock Average from January 1, 2014 to December 31, 2019, using tsQRF and compare the results with the WNW estimator. The data contained missing values, such as weekends and holidays, so we removed these missing values from the data. The data also show a long-term increasing trend (Figure 4.3), and we transform the price at time to (Figure 4.3). In fact, the ADF test yields a p-value of , so the null hypothesis of “it is a unit root process” cannot be rejected. In this analysis, we used the first four years (length: 976) as training data and the remaining two years (length: 489) as test data.

Because the true conditional quantile values cannot be observed, the empirical coverage rate, which is defined as follows, is used to evaluate the accuracy of the quantile estimation and prediction:

We fit the kernel quantile regression (WNW) and tsQRF with the orders and and we set the parameters to the same values as those used in Section 3 for functions grf and np in R packages.

Tables 4.6 and 4.7 show the estimated empirical coverage rates for the WNW and tsQRF for the training and test data, respectively. The values and , which are closer to between the WNW and tsQRF, are shown in red.

From Table 4.6, tsQRF provides more conservative result compared to WNW for the training data, and there is no significant difference in the accuracy of and between and . Table 4.7 shows the prediction results for the test data, and tsQRF gives better estimated values for than WNW.

| Model | 2.5% | 10% | 50% | 90% | 97.5% | 2.5% | 10% | 50% | 90% | 97.5% | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| WNW | 0.027 | 0.102 | 0.501 | 0.891 | 0.969 | 0.024 | 0.097 | 0.496 | 0.894 | 0.974 | |

| tsQRF | 0.000 | 0.041 | 0.463 | 0.880 | 0.969 | 0.000 | 0.037 | 0.462 | 0.890 | 0.970 | |

| Model | 2.5% | 10% | 50% | 90% | 97.5% | 2.5% | 10% | 50% | 90% | 97.5% | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| WNW | 0.012 | 0.084 | 0.497 | 0.926 | 0.988 | 0.016 | 0.086 | 0.487 | 0.926 | 0.982 | |

| tsQRF | 0.022 | 0.108 | 0.493 | 0.922 | 0.984 | 0.018 | 0.086 | 0.497 | 0.924 | 0.988 | |

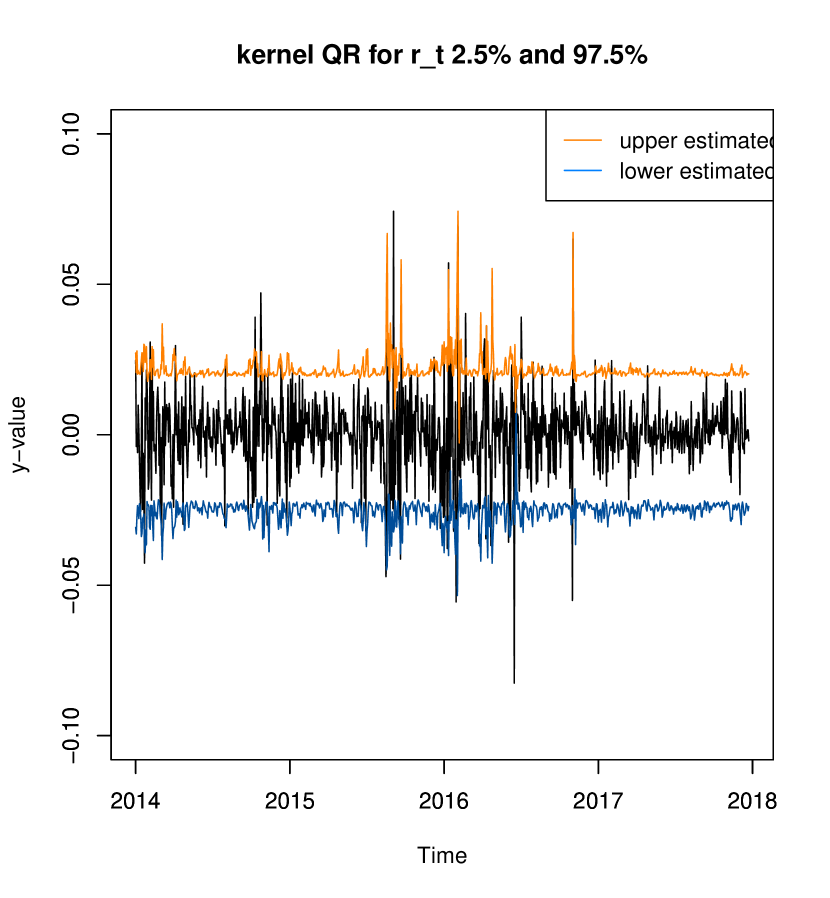

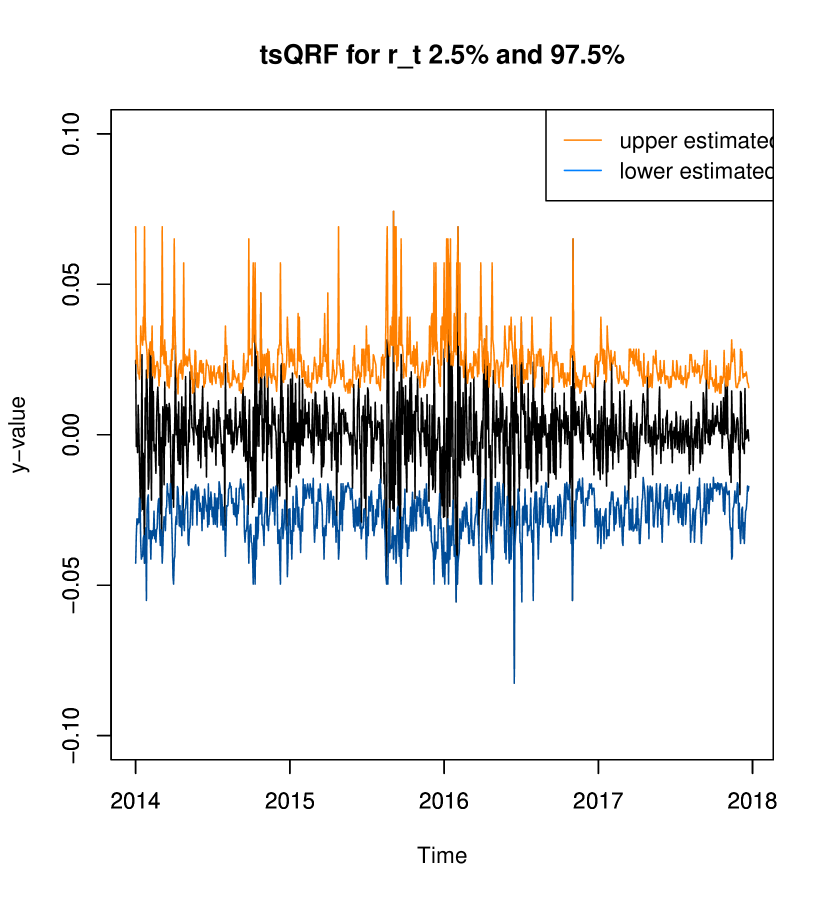

Figures 4.5 - 4.7 illustrate the variation in the estimated quantiles of at for each estimation method, with for the training and test data.

Figures 4.5 and 4.5 show that tsQRF is more sensitive to fluctuations than WNW. WNW does not capture the shocks of . The same trend is also observed for the test data in Figures 4.7 and 4.7.

Figures 4.5 and 4.7 show that the quantile function estimated by tsQRF captures the variation of . Even when there are large fluctuations in the time series, rarely exceeds the estimated 2.5% and 97.5% of points. Therefore, tsQRF is more sensitive to fluctuations in the time series than the WNW. For example, on September 9, 2015, concerns about the economy eased worldwide. Consequently, European and U.S. stocks rose the day before. The WNW could not capture the shock caused by this effect, whereas the tsQRF captured the effect properly. On June 24, 2016, supporters of leaving the European Union (EU) won the referendum in the United Kingdom. Consequently, there were concerns about the negative impact on the global economy, and the Nikkei Stock Average dropped sharply. Although tsQRF adequately captured these fluctuations, WNW did not.

Based on these results, especially for data with large volatility fluctuations, tsQRF can capture the change in time series data with high sensitivity and may contribute to preventing underestimation of the risk rather than WNW.

5 Summary and Future Work

We applied the Generalized Random Forests (GRF) proposed by Athey et al. (2019) to quantile regression for time series data. Although theoretical confirmation has not been considered for their use in a time series setting, we derived the uniform consistency of the estimated function under mild conditions. Davis and Nielsen (2020) also discussed the estimation problem using random forests (RF) for time series data, but the construction procedure of the RF treated by the GRF was essentially different, and different ideas were used throughout the theoretical proof. In addition, simulations and real data analyses were conducted. In the simulation, the accuracy of the conditional quantile estimation was evaluated under some time series models. In the real data using the Nikkei Stock Average, it was demonstrated that our estimator is more sensitive than the others in terms of volatility and can prevent the underestimation of risk.

However many challenges remain. If (A-2) is relaxed, the range of applicable models can be expanded, including the traditional AR model. The model is expected to be extended to handle not only NLAR as in (2.1), but also ARCH-type models. Furthermore, in this study, the order is fixed; however, in practice, it should be determined using an information criterion or other methods. This is related to the variable selection problems in the GRF. On the theoretical side, the discussion of asymptotic normality and asymptotic efficiency is the subject of future research. In particular, the efficiency involves the splitting procedure, and some methods, such as Neyman orthogonization, are expected to be effective.

Acknowledgments

This study was supported by JSPS KAKENHI Grant Number JP 21K11793. We would like to thank Editage (www.editage.com) for English language editing.

References

- [1] HZ An and FC Huang. The geometrical ergodicity of nonlinear autoregressive models. Statistica Sinica, pages 943–956, 1996.

- [2] Susan Athey, Julie Tibshirani, and Stefan Wager. Generalized random forests. The Annals of Statistics, 47(2):1148–1178, 2019.

- [3] Gérard Biau, Luc Devroye, and Gäbor Lugosi. Consistency of random forests and other averaging classifiers. Journal of Machine Learning Research, 9(9), 2008.

- [4] Leo Breiman. Random forests. Machine learning, 45(1):5–32, 2001.

- [5] Zongwu Cai. Regression quantiles for time series. Econometric theory, 18(1):169–192, 2002.

- [6] Zongwu Cai and Xian Wang. Nonparametric estimation of conditional var and expected shortfall. Journal of Econometrics, 147(1):120–130, 2008. Econometric modelling in finance and risk management: An overview.

- [7] Victor Chernozhukov and Len Umantsev. Conditional value-at-risk: Aspects of modeling and estimation. Empirical Economics, 26(1):271–292, 2001.

- [8] Richard A Davis and Mikkel S Nielsen. Modeling of time series using random forests: Theoretical developments. Electronic Journal of Statistics, 14(2):3644–3671, 2020.

- [9] Misha Denil, David Matheson, and Nando Freitas. Consistency of online random forests. In International conference on machine learning, pages 1256–1264. PMLR, 2013.

- [10] Paul Doukhan. Mixing: properties and examples, volume 85. Springer Science & Business Media, 2012.

- [11] Robert F Engle and Simone Manganelli. Caviar: Conditional autoregressive value at risk by regression quantiles. Journal of business & economic statistics, 22(4):367–381, 2004.

- [12] Peter Hall, Rodney CL Wolff, and Qiwei Yao. Methods for estimating a conditional distribution function. Journal of the American Statistical association, 94(445):154–163, 1999.

- [13] Roger Koenker. Quantile Regression. Econometric Society Monographs. Cambridge University Press, 2005.

- [14] Roger Koenker and Gilbert Bassett Jr. Regression quantiles. Econometrica: journal of the Econometric Society, pages 33–50, 1978.

- [15] Roger Koenker and Quanshui Zhao. Conditional quantile estimation and inference for arch models. Econometric Theory, 12(5):793–813, 1996.

- [16] Michael R Kosorok. Introduction to empirical processes and semiparametric inference. Springer, 2008.

- [17] Hira L Koul and AK Md E Saleh. Autoregression quantiles and related rank-scores processes. The Annals of Statistics, 23(2):670–689, 1995.

- [18] Nicolai Meinshausen and Greg Ridgeway. Quantile regression forests. Journal of Machine Learning Research, 7(6), 2006.

- [19] Erwan Scornet, Gérard Biau, and Jean-Philippe Vert. Consistency of random forests. The Annals of Statistics, 43(4):1716–1741, 2015.

- [20] James W Taylor. A quantile regression approach to estimating the distribution of multiperiod returns. The Journal of Derivatives, 7(1):64–78, 1999.

- [21] Stefan Wager and Susan Athey. Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523):1228–1242, 2018.

- [22] Wei Biao Wu, Keming Yu, and Gautam Mitra. Kernel Conditional Quantile Estimation for Stationary Processes with Application to Conditional Value-at-Risk. Journal of Financial Econometrics, 6(2):253–270, 12 2007.

Appendix A Proofs

Here, we present arguments leading up to our main result described in Section 2. To prove Theorem 1, we first derive an upper bound of the moment of . Each leaf can be expressed as based on a sequence with and . Denoting the diameter of by , we can write

Proof of Lemma 1

Let be the number of splits leading to any leaf , and let be the number of these splits along the -th coordinate. Then, from (A-3) and (A-5),

| (A.1) |

where with (see, (31) of Wager and Athey (2018)).

Let for any with . In what follows, we will show that there exists some sequence with such that

| (A.4) |

with probability one. Let be the depth of the tree splitted along the -th coordinate, let and be the rectangles before and after the -th splitting, respectively. Then, we can write

| (A.5) |

For each rectangle with , there exists with such that for , which implies that we have

where . In additon, from (5.45) and (5.46) of Davis and Nielsen (2020), we have

| (A.6) |

where . Since with probablity one, from (A.5), (A.6) and Glivenko-Cantelli theorem for ergodic process, it follows

which implies that there exits some sequence with satisfying (A.4). Therefore, from (A.3) and (A.4), we have

| (A.7) |

Let . Then, it follows

Since the above result does not depend on the test point , we obtain

From Lemma 1, the upper bound of the moment of for the original feature space can be derived. For any leaf , denoting the diameter of by , we define

Proof of Corollary 1

Since the map is one-to-one, from (A.7), there exists some such that

and since is a compact set, there exists some such that

for any , which implies that the proof is completed in the same as that of Lemma 1. ∎

Denoting the conditional expectation of given by , we define

and for two parameter define

Then, for the moments of , we can derive the followings.

Note that this result corresponds to Lemma 8 of Athey et al. (2019) in i.i.d. case. You can see that there exits a difference between i.i.d. case and dependent case.

Proof of Lemma 2

For simplicity, we drop the index in and so on. Denote

Then, we can write

Fix ; where is a partitioning based on ; and . If is satisfied for all , it follows from the -dependency of

| (A.8) |

Otherwise from (A-5), , and the stationarity of ,

| (A.9) |

where . Let () be a multiset of satisfying that there exists an such that and . Note that if there exist and with , and , the number of element in is two (see an example in Table A.8).

Then, we can interpret

where is the number of cases of all except for and is the number of cases of the divison for elements into and except for and . Therefore, from (A.8) and (A.9), we have

which is completed the proof of the first claim.

To prove the second claim, we denote the subsamples corresponds to for , and introduce

Let the conditional covariance of for given and by . Then, we can write

For each , from the continuously of and (A-5), there exists some such that

where . Hence, we have

| (A.10) |

Let be a multiset of satisfying that there exists an such that and . Then, we can interpret

where is the number of cases of all except for and is the number of cases of the divison for elements into and except for . Therefore, we have

| (A.15) | |||

| (A.24) | |||

| (A.25) |

On the other hand, as we state in Remark 1, is exponentially -mixing and is also exponentially -mixing. Therefore, denoting , we have with the mixing coefficient . Since

from (A-5) and the stationarity of , we have

| (A.26) |

The above evaluation does not depend on the condition and , and the dependency of and is negligible with high probability from the first claim, so that

which implies from (A.10)-(A.26), that there exists som such that

Although the above inequality is obtained under any fixed , the test point depends only on in the right hand side, and replacing this part by , the proof of the second claim is compleated. ∎

Proof of Lemma 3

From the triangle inequality,

it is sufficient to show ().

For , we consider the empirical process technique for U-statistics. Let any subsample for be an random element taking value on the sample space where and are the Borel sets on and , respectively. Define the empirical measure by where is a Dirac measure. Then, for any -mesurable function , we can write

We also define as a probabilty measure for any with Let be a parameter. We introduce an -mesurable function by

for any , and denote by the set of function . Moreover, for any signed meaure , we difine

then we can write

Under a fixed , for any , we construct an -bracket satisfying that the -norm is less than . Define

and for . For each , we also define

Since and are monotonically non-decreasing functions with respect to under any fixed and , it follows if . Let satisfying if and let , where and if . Then, for any , and any , there exists some , such that , and

which implies that is -bracket with respect to norm, and the bracketing number which is the minimum number of brackets of radius at most required to cover in terms of the norm, satisfies

| (A.27) |

For each , define . Define satisfying

for all . Then, we have

From Lemma 2 and the compactness of , we have , hence, is obtained. Moreover, by (A.27),

From Lemma 2, , as , which yields from the triangle inequality.

Proof of Theorem 1

Proof of Theorem 2

Suppose that for a fixed , and , is an multinomial random vector taking values on with probabilities and number of trials , and which is independent of the data and . Note that . Then, for any and , we can write

with

Let denote taking the expectation over . Then, we have

which implies that

By using this, under , we have , and from Lemma 3, . By the same argument of Theorem 1, we obtain as . ∎