Piecewise linear interpolation of noise in finite element approximations of parabolic SPDEs

Abstract.

Efficient simulation of stochastic partial differential equations (SPDE) on general domains requires noise discretization. This paper employs piecewise linear interpolation of noise in a fully discrete finite element approximation of a semilinear stochastic reaction-advection-diffusion equation on a convex polyhedral domain. The Gaussian noise is white in time, spatially correlated, and modeled as a standard cylindrical Wiener process on a reproducing kernel Hilbert space. This paper provides the first rigorous analysis of the resulting noise discretization error for a general spatial covariance kernel. The kernel is assumed to be defined on a larger regular domain, allowing for sampling by the circulant embedding method. The error bound under mild kernel assumptions requires non-trivial techniques like Hilbert–Schmidt bounds on products of finite element interpolants, entropy numbers of fractional Sobolev space embeddings and an error bound for interpolants in fractional Sobolev norms. Examples with kernels encountered in applications are illustrated in numerical simulations using the FEniCS finite element software. Key findings include: noise interpolation does not introduce additional errors for Matérn kernels in ; there exist kernels that yield dominant interpolation errors; and generating noise on a coarser mesh does not always compromise accuracy.

Key words and phrases:

stochastic partial differential equations, finite element method, Lagrange interpolation, cylindrical Wiener process, Q-Wiener process, noise discretization, circulant embedding2020 Mathematics Subject Classification:

60H15, 65M12, 65M60, 60G15, 60G60, 35K511. Introduction

Finite element approximation excels at handling complex geometries. We unlock its potential for stochastic partial differential equations (SPDEs) by interpolating the driving noise on a convex polyhedron and analyzing the induced error. This applies to stochastic advection-reaction-diffusion equations

for with initial value . The functions satisfy an ellipticity condition, and homogeneous Dirichlet or Neumann boundary conditions are considered. The nonlinearities are given by and for functions on , a vector field and Lipschitz functions on . The noise is Gaussian, white in time with spatial covariance kernel . These equations have numerous applications in fields like hydrodynamics, geophysics and chemistry and are treated as Itô stochastic differential equations in the Hilbert space of square integrable functions:

| (1) |

see [11]. Here is a standard cylindrical Wiener process on the reproducing kernel Hilbert space (RKHS) (equivalently a -Wiener process for the associated integral operator , see Remark 3.5) and generates an analytical semigroup.

We discretize (1) using a semi-implicit Euler method combined with piecewise linear finite elements for a triangle mesh on with maximal mesh size . Such approximations are well-studied [1, 12, 32, 35, 20, 2, 23, 10], but rigorous analyses of noise discretizations are rare. This refers to the approximation of

| (2) |

for each time and nodal basis function . Here and approximates with constant time step . Conditioned on , the vector (with the number of nodes in ) is Gaussian with

Recomputing the covariance matrix and sampling from it at each time by, e.g., Cholesky decompositions becomes costly. To remedy this, in (2) is discretized. In this paper we interpolate between meshes and derive a strong error bound:

| (3) |

for , rates , mesh sizes and some . Here is the standard SPDE approximation error and the noise discretization error.

Literature on noise discretization for parabolic SPDEs mainly focus on truncation of an eigenbasis of [2]. Explicit bases are only available for special kernels and domains , like cubes, which partly defeats the purpose of using finite elements. Numerical approximation of the basis is an alternative, analyzed in [20] for . The requirements on therein are hard to verify, but has to be piecewise analytic (a strong condition) for the cost of to be [20, Corollary 3.5]. In [21], a related approach of expanding the noise on wavelets is used, also for . Conditions are derived for which a severe truncation of the expansion does not affect the strong error in a semidiscretization. However, constructing the wavelet basis is challenging for general and needs strong assumptions on (see [21, Section 7.2, Theorem 7.1] but note that a Dirichlet condition on is missing).

In this paper, noise discretization is handled by first assuming to be positive semidefinite on another polyhedron , typically a cube. Given , we interpolate the noise onto another triangulation on , replacing in (2) with . Here and are the piecewise linear interpolants with respect to and , restricts functions on to and is an extension of with the same covariance. In terms of the basis functions for the nodes of ,

| (4) |

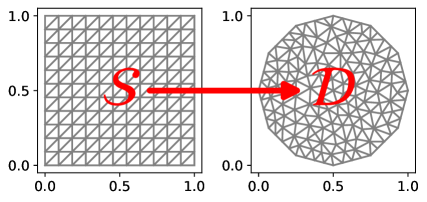

We thus only need to sample values from to approximate (2), avoiding integrals involving . This strategy is easily implemented in modern finite element software and, for stationary and uniform, fast and exact FFT-based algorithms can be used to sample from . This includes the circulant embedding method applied to a Matérn kernel, where the sampling cost of is [17]. Figure 1 illustrates this for a dodecagon inside a square , including a realization of computed with this method with parameters as in Example 5.6. For non-stationary , one can instead combine our results with truncation of an eigenexpansion of .

We derive (3) under mild conditions on , Assumption 3.4. To use the results of [23] for the SPDE approximation error bound, we construct as a standard cylindrical Wiener process on the RKHS and derive new Hilbert–Schmidt bounds on multiplication operators and finite element interpolant products. Non-trivial techniques are needed for the noise discretization error, like entropy numbers of Sobolev space embeddings and generalized error bounds for interpolants. The analysis shows that the noise discretization error is non-dominant for most kernels in , (including the Matérn class), but dominant for some factorizable kernels in and rough Matérn kernels in . Moreover, there are settings where , so that we may take , increasing computational savings with retained accuracy.

Interpolation of noise in finite element approximations of (1) with was considered in [7], but without analyzing how the strong error is affected. Lemma 6.1 in [23] contains the only such analysis we are aware of. The author considers modified interpolants and spatial semidiscretization only, for with Dirichlet boundary conditions and given by a sine expansion. Then the convergence of the strong error is unaffected, but the author notes that

it is only barely analyzed in the literature, how [the replacement of with ] affects the order of convergence. …We leave a rigorous justification in a more general situation as a subject to future research. [23, p. 139]

We give this justification in Section 4 and demonstrate it by numerical simulations in Section 5 for concrete example kernels. Sections 2-3 contain prerequisite material.

2. Notation and mathematical background

This paper employs generic constants . These vary between occurrences and are independent of discretization parameters. We write for to signify for such a constant .

2.1. Operator theory

For Banach spaces and (all over unless otherwise stated), we denote by the linear and bounded operators from to and set . We write if and .

For separable Hilbert spaces and , is the space of Hilbert–Schmidt operators. It is an operator ideal and a separable Hilbert space with inner product

where is an arbitrary orthonormal basis (ONB) of . For , the range is a Hilbert space with , where is the pseudoinverse and the orthogonal complement of the kernel of . The norm on is given by . Note that coincides with the orthogonal projection , whereas . We write for the subspace of positive semidefinite operators on and refer to [29, Appendix C] for more details on these concepts.

2.2. Reproducing kernel Hilbert spaces

Let be a positive semidefinite kernel on a non-empty connected subset , . The RKHS of on is the Hilbert space of functions on such that

-

(i)

for all and

-

(ii)

for all , (the reproducing property).

Each has a unique RKHS , but may have multiple equivalent norms for different kernels. A Hilbert space of functions on is an RKHS if and only if the evaluation functional , , is bounded for all [33, Theorem 10.2]. We write if need not be emphasized. If is positive semidefinite on , then the restriction of to a function on belongs to and with equal norms [6, Theorem 6]. Thus the pseudoinverse is an extension operator with .

For continuous and bounded , is separable [6, Corollary 4]. This yields

| (5) |

for any ONB with convergence in respectively . When and is of the form , it is called stationary. If it also is continuous, bounded and integrable, it has a positive and integrable Fourier transform (the spectral density) [33, Chapter 6]. We refer to [6, 33] for more details on RKHSs.

2.3. Fractional Sobolev spaces

Let , be a bounded Lipschitz domain. We let with inner product and norm . We let , denote the Sobolev space equipped with the norm

| (6) |

for non-integer , , where is the integer order Sobolev norm and the Euclidean norm on , see also [18, Definition 1.3.2.1]. The space is a Hilbert space. We write and when is not emphasized. The properties here and below, typically given for Sobolev spaces over , readily transfer to our setting in , cf. [22, Section 2.2].

For , is bounded by the Sobolev embedding theorem, making an RKHS [18, Theorem 1.4.4.1]. The stationary kernel of the Bessel potential space is given by the continuous and bounded function for , where is the modified Bessel function of the second kind [33, p. 133]. Since is Lipschitz, with equivalent norms, see [18, p. 25] and [33, Corollary 10.48]. The expressions (17) and (18) in [31, Section 2.7] yield for all ,

| (7) |

for some constant . When , the exponent is replaced by for arbitrary . When , it is replaced by .

2.4. Fractional powers of elliptic operators

From here on, we let be convex and define as the part in of the operator defined by for a Gelfand triple and bilinear form . We consider either Neumann-type homogeneous zero boundary conditions () or Dirichlet-type ( with the trace operator), with

The derivative is with respect to , fulfill and for some and all , . The function is non-negative a.e. on . Without loss of generality, let for some , a.e. on , in the Neumann case. Then is continuous, symmetric and coercive, and densely defined, closed and positive definite.

Since is compact, has a compact inverse, enabling fractional powers by spectral decomposition. We write for and let, for , be the completion of under . Since is convex, the functions of are the elements of that satisfy the boundary conditions of while

| (8) |

with norm equivalence [34, Theorems 16.9, 16.13]. Moreover, by complex interpolation [3, Theorem 3.2, Remark 3.3]. We refer to [23, Appendix B] and [34, Chapter 2] for more on this setting.

3. Parabolic SPDEs driven by cylindrical Wiener processes in RKHSs

Here, mild solutions to (1) and cylindrical Wiener processes in are introduced. We extend to , state our assumptions on and derive regularity in the setting of stochastic reaction-diffusion-advection equations.

3.1. Mild solutions of SPDEs

For , let be a filtered probability space under the usual conditions. The process on given by

| (9) |

is called mild if also , , where is the analytic semigroup generated by . The stochastic integral is of Itô type [11, Chapter 4] and a standard cylindrical Wiener process in . In [23], the existence of a unique solution (9) is derived with the regularity estimate This is shown in [23, Theorem 2.27] under the following assumption.

Assumption 3.1.

For some , , there is a such that:

-

(a)

The initial value is -measurable and .

-

(b)

The non-linear reaction-advection term satisfies

-

(i)

for all

-

(ii)

for all .

-

(i)

-

(c)

The non-linear multiplicative noise operator satisfies

-

(i)

for all and

-

(ii)

for all .

-

(i)

Assumption 3.1(a) depends on Sobolev regularity of and whether it satisfies the boundary conditions associated with . Assumption 3.1(b) is with

| (10) |

satisfied for regular , and functions on . The next proposition gives sufficient conditions on and for this to hold true.

Proposition 3.2.

3.2. Cylindrical Wiener processes in RKHSs

A family, indexed by , of linear maps from a Hilbert space to the space of real-valued random variables is called a cylindrical stochastic process in . Such a process is a (strongly) cylindrical Wiener process with covariance operator if is a Wiener process in for and for all . It is called standard if . For such in , another Hilbert space and the process defined by , , is a cylindrical Wiener process in with covariance . Here is the adjoint of . We have here followed the setting of [30] and [11, Section 4.1.2], identifying Hilbert spaces with their duals.

We now specify to be a standard cylindrical Wiener process in . With , one obtains by the reproducing property of a Gaussian random field with covariance . This yields that the interpolation (4), used for simulation of by sampling on , is well-defined. However, we also need to confirm that an extension of to a standard cylindrical Wiener process in exists, with .

Lemma 3.3.

If is positive semidefinite on there is a standard cylindrical Wiener process on such that .

Proof.

Recall that is a Hilbert subspace of . Let be a cylindrical Wiener process on , independent of , with covariance operator . Set . By independence, is an -valued Wiener process for all and for all , is given by

| (12) |

Since yields , and since ,

| (13) |

Note now that for and , as a result of

Since also we find that for . Combining this with the reproducing property, we find that for , , . By approximating with linear combinations of in (see [6, Theorem 3]), we then obtain

| (14) |

Combining (13) and (14) in (12) with the identity yields which shows that is a standard cylindrical Wiener process on . The fact that now follows from the identities and on . ∎

We now state our main assumption for on . Note that if satisfies this on , the corresponding assumption is also fulfilled for . The first part is used to verify Assumption 3.1(c), the second for the numerical analysis of Section 4.

Assumption 3.4.

The positive semidefinite kernel is bounded on and satisfies

-

(a)

for some and the Hölder-type regularity condition

-

(b)

and for some and the embedding property .

Remark 3.5.

Since is bounded, . The embedding is Hilbert–Schmidt, since continuity of yields an ONB of such that

see (5). Therefore, , viewed as cylindrical in , is under Assumption 3.4 induced by a so called -Wiener process with covariance [30, Theorem 8.1]. The relation to the original process is given by for . The operator is of integral type with kernel . We could equivalently work with instead of in (1), but the frequent use of the RKHS properties in Section 2.2 would make the notation and analysis cumbersome.

3.3. Non-linear multiplicative noise operator

We prove a result relating the Hölder-type regularity of in Assumption 3.4(a) to Assumption 3.1(c) on when in (11) satisfies, for some constant ,

| (15) |

In the special case where has a known expansion (Example 5.5 below), has Dirichlet boundary conditions and , it was derived in [19, Section 4]. We extend this setting to more general kernels, domains and boundary conditions.

Proposition 3.6.

Proof.

Note first that Assumption 3.4(a) along with the reproducing property of yields that all are bounded. Moreover, (15) ensures that for so that indeed takes values in for .

By Assumption 3.4(a), is separable with an ONB . By Tonelli’s theorem and the decomposition (5) for the bounded kernel , maps into since

Similarly, the claim (i) is obtained from the Lipschitz regularity of , as

can be bounded by for some . To prove (ii), we note that the definition of yields that is given by

The first of these terms, , was bounded above. For the second,

| (16) |

In the first integral, we use (5), (15) and Assumption 3.4(a) to see that

since . The second integral in (LABEL:eq:prop:G-reg:2) is bounded by

Since , the bound by on in Proposition 3.6 only applies in the Dirichlet case. It can be dropped if or if for all [34, Theorem 16.13]. Moreover, the result is sharp. Too see this, consider Neumann boundary conditions and for , so that in Assumption 3.4(a) by (7). If we let for , we have for . Proposition 3.6 shows that for whereas if , see, e.g., [22, Lemma 2.3].

4. Piecewise linear interpolation of noise in SPDE approximations

By Lemma 3.3 we write without loss of regularity the mild solution of (9) as

for and a standard cylindrical Wiener process on . We approximate by through the semi-implicit Euler scheme and piecewise linear finite elements. This was analyzed in [23], here we consider the additional noise discretization error coming from sampling pointwise on and interpolating onto .

4.1. Discretization setting

From here on, we let and be polyhedral, as is common for finite element methods to avoid dealing with curved boundaries [8]. Consider two triangulations on and with maximal mesh sizes , and let and be the spaces of piecewise linear functions on these. By and we denote the piecewise linear interpolants with respect to and . For a function on , is the unique function such that for all nodes of . In terms of the nodal basis functions ,

where is the number of nodes. We need two results on these interpolants. The first generalizes the results in [4] to , with a proof in Appendix A.

Proposition 4.1.

Let , be polyhedral with regular triangulation . Let , and . Assume also that is quasiuniform for and . Then, there is a such that

Lemma 4.2.

Let be polyhedral domains with triangulations and . Let be a bounded and continuous positive semidefinite kernel on . Let be given by for a.e. . Then

Proof.

Let us write and for the nodal bases on and . Then

Using (5), this can be written as

By stability of and in , . Moreover, are non-negative, sum to and for at most indices . Thus,

∎

We next set and denote by and the orthogonal projections under the topologies of and , respectively. Let be defined by for so that . Combining this equality with [23, (3.15)], we find such that

| (17) |

using also an interpolation argument. With this, we can introduce . For a time step , let be given by and . Set and let solve

| (18) |

for . Here . This is the same approximation as that of [23, Section 3.6], but with replaced by .

4.2. The main result

In this section, we derive an error bound on under noise interpolation. First, we need a regularity estimate for .

Lemma 4.3.

Proof.

By the Burkholder–Davis–Gundy (BDG) inequality [11, Theorem 4.36]:

| (20) |

For the last of these terms, we use (17), (19), Lemma 4.2 and (15) to bound it by

The first two terms of (20) are similarly bounded using (17), (19) and Assumption 3.1(a)-(b). A discrete Gronwall lemma, [23, Lemma A.4], completes the proof. ∎

In our main result, we show that noise interpolation results in an additional error , with a rate that depends on Assumption 3.4 as well as the dimension . We assume the triangulations and to be quasiuniform, but see Remark 4.5.

Theorem 4.4.

Proof of Theorem 4.4.

Note, that if , which can only occur in , the error is simply bounded by regularity of (9) and Lemma 4.3. Below, we let .

If we make the split for

the error is of the same form as the error without noise interpolation in [23, Theorem 3.14]. Since is convex, elliptic regularity yields for (see [15, p. 799]) so that [23, Assumption 3.3] is satisfied. Moreover, [23, Assumption 3.5] is satisfied by quasiuniformity, all assumptions of [23, Section 2.3] are satisfied by Assumption 3.1 (through Proposition 3.6) and is bounded by Lemma 4.3. Thus, it suffices to bound , since by [23, Theorem 3.14],

For the bound on , we use entropy numbers for operators on Banach spaces , see [28, Definition 12.1.2]. If we write and then a Hölder-type property holds for a further Banach space and operator :

| (21) |

This follows from Theorems 12.1.3-5 and 14.2.3 in [28]. By [14, Theorem 3.5] and an equivalence of Sobolev and Besov spaces (see [3, Section 2]), we have

| (22) |

for Lipschitz domains , , and .

For Hilbert spaces and , Theorems 11.3.4, 11.4.2, 12.3.1 and 15.5.5 in [28] yield that . Using also the BDG inequality,

This splits into by

The three terms are treated similarly. We only consider the most complex case,

We start by assuming , and derive three preliminary bounds.

First, commutativity of and , (21), (17) and (22) yield

| (23) | ||||

for a constant independent of , by choosing sufficiently close to . Second, by applying the Hölder inequality, a Sobolev embedding [3, Theorem 3.8] and the Lipschitz continuity (15) in the norm (6) for ,

for , with in and in , hence . Thus, by Lemma 4.3,

| (24) |

Third, if , Proposition 4.1 and yields for small

| (25) |

This is also obtained for by instead using .

We now use (21), (23), (24) and (25) to bound by

Without loss of generality, let . Then we can apply (22) if , which is true by assumption for sufficiently small . Moreover, if , which holds if we let . This completes the proof for . The case follows by similar arguments, except we need, for small , use the fact that when deriving (24) and replace (23) with a bound on with . ∎

5. Example kernels and numerical simulation

In this section we explore the implications of Theorem 4.4 for several common covariance kernels. We illustrate our discussion with numerical simulations in FEniCS.

5.1. Example kernels

We first examine for which , and Assumption 3.4 is satisfied for a given kernel .

Example 5.1 (Matérn kernel).

The stationary Matérn kernel is defined as

Here is the modified Bessel function of the second kind with smoothness parameter and is the Gamma function. It generalizes the kernel of Section 2.3 by scaling with . There, we had where now in terms of , with equivalent norms. This relies on being bounded from above and below by for some . It is the upper bound that yields . This does not change by scaling and , and neither does the Hölder property (7). Therefore Assumption 3.4 is satisfied with and for , for and for . The special case results in the exponential kernel , see [25, Example 7.17].

Example 5.2 (Gaussian kernel).

Example 5.3 (Polynomial kernels with compact support).

Let be a polynomial and let the stationary kernel be of the form

Not all yield positive semidefinite . We consider two admissible examples for which one can use Proposition 5.5 and Theorem 5.26 in [33] (to which we refer for more examples) to compute and then bound by a constant in a neighbourhood of . Without loss of generality we let .

The next example shows why we cannot always have in Assumption 3.4.

Example 5.4 (Factorizable kernels).

A kernel is called factorizable if it is a product , , of univariate kernels. Let be Matérn kernels, all with , so that is stationary. From equivalence of norms in and the equality

it follows that in Assumption 3.4(a). From [25, Example 7.12], is given by

Using this result in [33, Theorem 10.12], it can be seen that . If , this embedding does not satisfy Assumption 3.4(b) with since . However, we can find and such that . We let the factorizable exponential kernel in illustrate this. Here, so . By the reproducing property, we find that for ,

This implies that for all and by definition of . Combining these two embeddings, there is for all a such that and , satisfying Assumption 3.4(b). To see this, let and pick so small that . Then in terms of complex interpolation with and , so that if we let .

Example 5.5 (Kernel with known Mercer expansion).

Suppose there is an ONB of of uniformly bounded continuous functions, with, for some ,

Here , , is the space of -summable sequences. Let the kernel be given by for and define a Hilbert space by

for , under the notational convention . Since and for , must be the RKHS for on . We have

meaning that Assumption 3.4(a) holds for . As in Example 5.4, the reproducing property yields that and in Assumption 3.4(b).

5.2. Numerical simulations

We approximate the strong error (3) with , , a regular dodecagon centered at with radius and the unit square. We let with either Dirichlet or Neumann zero boundary conditions. We set and according to (11) and (10), picking different functions , and . We fix a small and let with (except in Example 5.8). When plotting the error versus , we see either the SPDE approximation error or the noise discretization error dominate, depending on whether or not. We write , , to denote for arbitrary .

We use a Monte Carlo method and a reference solution with . With sample size , the Monte Carlo errors are negligible, using the same samples of across all . The simulations are performed with the FEniCS software package (see [24]) on a laptop with an Intel® Core™ i7-10510U processor, with sampled by circulant embedding [17]. The code accompanies the arXiv version of the paper.

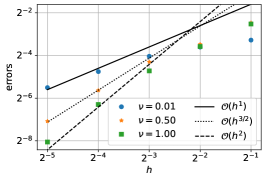

Example 5.6 (Non-dominance of noise discretization errors).

In the case that is a Matérn kernel as in Example 5.1, we have for , i.e., the noise discretization error does not dominate. This is true also for the Gaussian kernel of Example 5.2 and any . It is also true for the first polynomial kernel of Example 5.3 when (since then ) and the second for any (since then ).

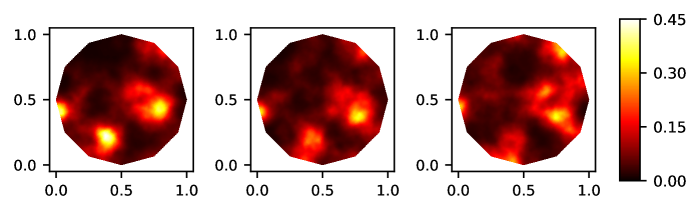

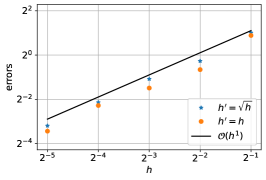

We illustrate this in the simulation setting outlined above with of Matérn type with parameters and . We let , pick Lipschitz functions , for , set and apply Neumann boundary conditions. The errors of Figure 2(a) are in line with the results of Theorem 4.4. See Figure 1(b) for a realization of with and .

Example 5.7 (Dominance of noise discretization errors).

In , the Matérn kernels yield and , with dominant noise discretization error if for Dirichlet and for Neumann conditions. Similar conclusions hold for the first polynomial kernel of Example 5.3. This was demonstrated in a linear setting in [5], with different rates owing to errors being measured pointwise in space. Numerical experiments (not included in [5]) suggest this applies in our setting as well.

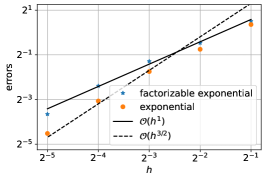

Factorizable kernels (Example 5.4) may exhibit dominant noise discretization errors even when . We illustrate this with a numerical simulation comparing the exponential and the factorizable exponential kernel, both with and . We set , for , for , equip with Dirichlet boundary conditions and otherwise follow the setting of Example 5.6. From Examples 5.1 and 5.4 we see that for both the exponential and the factorizable exponential kernel, whereas in the former case and in the latter. The results (Figure 2(b)) align with Theorem 4.4.

One can potentially mitigate these issues by computing using finer meshes on and than the mesh used in (18). Efficient sampling methods could still maintain competitiveness of the approximation schemes. However, as FEniCS does not appear to support this, we do not explore this further.

Example 5.8 (Dominance of SPDE approximation error and noise sampling on a coarse mesh).

In our last example, we consider a non-smooth initial condition, namely , . This function, while in , is not in due to its discontinuity (cf. [18, page 1]). With as the second polynomial kernel of Example 5.3, , , , , and Neumann boundary conditions for , we find and . Hence, the error stemming from the initial condition dominates the noise discretization error. We can therefore set and retain the same convergence rate as , which is seen in Figure 2(c). Thus, for rough initial conditions, the computational effort can be further decreased without any essential loss of accuracy. Similarly, if we had a smooth initial condition with Dirichlet boundary conditions for , we could set for analogous, albeit smaller, computational savings. This underscores the importance of noise discretization error analysis for efficient algorithm design.

References

- [1] E. J. Allen, S. J. Novosel, and Z. Zhang. Finite element and difference approximation of some linear stochastic partial differential equations. Stochastics Stochastics Rep., 64(1-2):117–142, 1998.

- [2] A. Barth and A. Lang. Simulation of stochastic partial differential equations using finite element methods. Stochastics, 84(2-3):217–231, 2012.

- [3] A. Behzadan and M. Holst. Multiplication in Sobolev spaces, revisited. Ark. Mat., 59(2):275–306, 2021.

- [4] F. Ben Belgacem and S. C. Brenner. Some nonstandard finite element estimates with applications to Poisson and Signorini problems. ETNA, Electron. Trans. Numer. Anal., 12:134–148, 2001.

- [5] F. E. Benth, G. Di Nunno, G. Lord, and A. Petersson. The heat modulated infinite dimensional heston model and its numerical approximation. Preprint at arXiv:2206.10166, June 2022.

- [6] A. Berlinet and C. Thomas-Agnan. Reproducing kernel Hilbert spaces in probability and statistics. Kluwer Academic Publishers, Boston, MA, 2004.

- [7] M. Boulakia, A. Genadot, and M. Thieullen. Simulation of SPDEs for excitable media using finite elements. J. Sci. Comput., 65(1):171–195, 2015.

- [8] S. C. Brenner and L. R. Scott. The mathematical theory of finite element methods, volume 15 of Texts in Applied Mathematics. Springer, New York, third edition, 2008.

- [9] P. j. Ciarlet. Analysis of the Scott-Zhang interpolation in the fractional order Sobolev spaces. J. Numer. Math., 21(3):173–180, 2013.

- [10] J. Cui and J. Hong. Strong and weak convergence rates of a spatial approximation for stochastic partial differential equation with one-sided Lipschitz coefficient. SIAM J. Numer. Anal., 57(4):1815–1841, 2019.

- [11] G. Da Prato and J. Zabczyk. Stochastic equations in infinite dimensions, volume 152 of Encyclopedia of mathematics and its applications. Cambridge University Press, Cambridge, second edition, 2014.

- [12] Q. Du and T. Zhang. Numerical approximation of some linear stochastic partial differential equations driven by special additive noises. SIAM J. Numer. Anal., 40(4):1421–1445, 2002.

- [13] T. Dupont and R. Scott. Polynomial approximation of functions in Sobolev spaces. Math. Comp., 34(150):441–463, 1980.

- [14] D. E. Edmunds and H. Triebel. Function spaces, entropy numbers, differential operators, volume 120 of Camb. Tracts Math. Cambridge: Cambridge Univ. Press, 1996.

- [15] H. Fujita and T. Suzuki. Evolution problems. Handbook of numerical analysis, II, pages 789 – 928. North-Holland, Amsterdam, 1991. Finite element methods. Part 1.

- [16] S. Geiger, G. Lord, and A. Tambue. Exponential time integrators for stochastic partial differential equations in 3d reservoir simulation. Comput. Geosci., 16(2):323–334, 2012.

- [17] I. G. Graham, F. Y. Kuo, D. Nuyens, R. Scheichl, and I. H. Sloan. Analysis of circulant embedding methods for sampling stationary random fields. SIAM J. Numer. Anal., 56(3):1871–1895, 2018.

- [18] P. Grisvard. Elliptic problems in nonsmooth domains, volume 24 of Monographs and studies in mathematics. Pitman (Advanced Publishing Program), Boston, MA, 1985.

- [19] A. Jentzen and M. Röckner. Regularity analysis for stochastic partial differential equations with nonlinear multiplicative trace class noise. Journal of Differential Equations, 252(1):114–136, 2012.

- [20] M. Kovács, S. Larsson, and F. Lindgren. Strong convergence of the finite element method with truncated noise for semilinear parabolic stochastic equations with additive noise. Numerical Algorithms, 53(2):309–320, Mar 2010.

- [21] M. Kovács, F. Lindgren, and S. Larsson. Spatial approximation of stochastic convolutions. J. Comput. Appl. Math., 235(12):3554–3570, 2011.

- [22] M. Kovács, A. Lang, and A. Petersson. Hilbert–Schmidt regularity of symmetric integral operators on bounded domains with applications to SPDE approximations. Stochastic Analysis and Applications, 2022. Published online.

- [23] R. Kruse. Strong and weak approximation of semilinear stochastic evolution equations, volume 2093 of Lecture notes in mathematics. Springer, Cham, 2014.

- [24] H. P. Langtangen and A. Logg. Solving PDEs in Python. The FEniCS tutorial I, volume 3 of Simula SpringerBriefs Comput. Cham: Springer Open, 2016.

- [25] G. J. Lord, C. E. Powell, and T. Shardlow. An introduction to computational stochastic PDEs. Cambridge Texts in Applied Mathematics. Cambridge University Press, 2014.

- [26] G. J. Lord and A. Tambue. A modified semi-implicit Euler-Maruyama scheme for finite element discretization of SPDEs with additive noise. Appl. Math. Comput., 332:105–122, 2018.

- [27] S. V. Lototsky and B. L. Rozovsky. Stochastic partial differential equations. Universitext. Springer, Cham, 2017.

- [28] A. Pietsch. Operator ideals. Licenced ed, volume 20. Elsevier (North-Holland), Amsterdam, 1980.

- [29] C. Prévôt and M. Röckner. A Concise Course on Stochastic Partial Differential Equations, volume 1905 of Lecture notes in mathematics. Springer, Berlin, 2007.

- [30] M. Riedle. Cylindrical Wiener processes. In Séminaire de Probabilités XLIII, Poitiers, France, Juin 2009., pages 191–214. Berlin: Springer, 2011.

- [31] M. L. Stein. Interpolation of spatial data. Springer Series in Statistics. Springer-Verlag, New York, 1999. Some theory for Kriging.

- [32] J. B. Walsh. Finite element methods for parabolic stochastic PDE’s. Potential Anal., 23(1):1–43, 2005.

- [33] H. Wendland. Scattered data approximation, volume 17 of Cambridge Monographs on Applied and Computational Mathematics. Cambridge University Press, Cambridge, 2005.

- [34] A. Yagi. Abstract parabolic evolution equations and their applications. Springer Monographs in Mathematics. Springer-Verlag, Berlin, 2010.

- [35] Y. Yan. Galerkin finite element methods for stochastic parabolic partial differential equations. SIAM J. Numer. Anal., 43(4):1363–1384, 2005.

Appendix A A fractional Sobolev norm error bound for piecewise linear finite element interpolants

Here we derive the bound of Proposition 4.1, generalizing the results of [4] to and . For the Scott–Zhang interpolant, [9] treats this case, but as far as we know Proposition 4.1 cannot be inferred from this.

Proof of Proposition 4.1.

In this proof, we use for general the notation

Here , , is the usual Sobolev seminorm and the -norm for .

Without loss of generality, let . We start with the cases and or . The claim for , then follows from real interpolation, see, e.g., [3, Theorem 3.1, Remark 3.3]. First note that for all , there is a such that for all ,

| (26) |

This is [4, Lemma 2.1] for , the proof is analogous for . We also need an estimate on the reference simplex with vertices , …. For , [18, Theorem 1.4.4.3] yields a such that

| (27) |

For each , there is an affine transformation . By regularity, there are , that only depend on (see [4, 8, 13]), such that

| (28) |

| (29) |

For quasiuniform , we also have corresponding lower bounds in terms of .

Writing , yields for , with

In the case that , . Let us write , and note that , cf. [13, page 461]. Combining this, (28), (29) and equivalence of norms in , it follows by a scaling argument that for

For , is instead bounded by . In case , we also use (27) with to similarly deduce the estimate

Let denote interpolation onto the set of linear polynomials on and note that . The Sobolev embedding (see [18, Theorem 1.4.4.1]) yields after using equivalence of norms in to see that

| (30) |

Similarly, . Since for and , this gives by real interpolation. These observations, the invariance of on and the Bramble–Hilbert Lemma [13, Theorem 6.1] imply that

This sum is bounded by after applying this estimate to the summand: