Nonparametric Quantile Regression: Non-Crossing Constraints and Conformal Prediction

Abstract

We propose a nonparametric quantile regression method using deep neural networks with a rectified linear unit penalty function to avoid quantile crossing. This penalty function is computationally feasible for enforcing non-crossing constraints in multi-dimensional nonparametric quantile regression. We establish non-asymptotic upper bounds for the excess risk of the proposed nonparametric quantile regression function estimators. Our error bounds achieve optimal minimax rate of convergence for the Hölder class, and the prefactors of the error bounds depend polynomially on the dimension of the predictor, instead of exponentially. Based on the proposed non-crossing penalized deep quantile regression, we construct conformal prediction intervals that are fully adaptive to heterogeneity. The proposed prediction interval is shown to have good properties in terms of validity and accuracy under reasonable conditions. We also derive non-asymptotic upper bounds for the difference of the lengths between the proposed non-crossing conformal prediction interval and the theoretically oracle prediction interval. Numerical experiments including simulation studies and a real data example are conducted to demonstrate the effectiveness of the proposed method.

Keywords: Conformal inference; Non-crossing quantile curves; Deep neural networks; Nonparametric estimation; Prediction accuracy

1 Introduction

How to assess uncertainty in prediction is a fundamental problem in statistics. Conformal prediction is a general distribution-free methodology for constructing prediction intervals with a guaranteed coverage probability in finite samples (Papadopoulos et al.,, 2002; Vovk et al.,, 2005). We propose a method for nonparametric estimation of quantile regression functions with the constraint that two quantile functions for different quantile levels do not cross. We then use estimated non-crossing quantile regression functions for constructing conformal prediction intervals.

Since Vovk et al., (2005) formally introduced the basic framework of conformal prediction, there has been a number of important advancements on conformal prediction (Vovk,, 2012; Lei et al.,, 2013; Lei and Wasserman,, 2014; Lei et al.,, 2018). Lei and Wasserman, (2014) and Vovk, (2012) showed that the conditional validity for prediction interval with finite length is impossible without any regularity and consistency assumptions on the model and the estimator. Zeni et al., (2020) established that the marginal validity, a conventional coverage guarantee, can be achieved under the assumption that the observations are independent and identically distributed. Recently, several papers have studied the coverage probability, the prediction accuracy in terms of the length of prediction interval, and the computational complexities of conformal prediction using neural networks (Barber et al.,, 2021; Lei et al.,, 2018; Papadopoulos,, 2008).

Earlier works on conformal prediction were based on estimating a conditional mean function and constructing intervals of constant width, assuming homoscedastic errors. Recently, Romano et al., (2019) proposed a conformal prediction method based on quantile regression, called conformalized quantile regression. This method is adaptive to data heteroscedasticity and can have varying length across the input space. A similar construction of adaptive and distribution-free prediction intervals using deep neural networks have been considered by Kivaranovic et al., (2020). A comparison study of conformal prediction based on quantile regression with two choices of the conformity scores is given in Sesia and Candès, (2020).

Nonetheless, associated with the great flexibility of regression quantiles is the quantile-crossing phenomenon. The quantile crossing problem, due to separate estimation of regression quantile curves at individual quantile levels, has been observed in simple linear quantile regression, and can happen more frequently in multiple regression. Several papers have attempted to deal with the crossing problem. In linear quantile regression, Koenker, (1984) studied a parallel quantile plane approach to avoid the crossing problem. He, (1997) proposed a restricted regression quantile method that avoids quantile crossing while maintaining modeling flexibility. Neocleous and Portnoy, (2008) established the asymptotic guarantees that the probability of crossing will tend to zero for the linear interpolation of the Koenker-Bassett linear quantile regression estimator. These papers focused on the linear quantile regression setting. Bondell et al., (2010) proposed a constrained quantile regression to avoid the crossing problem, and considered nonparametric non-crossing quantile regression using smoothing splines with a one-dimensional predictor. However, this approach may not work well with a multi-dimensional predictor. Recently, interesting findings on simultaneous quantile regression that alleviates the crossing quantile problem were reported. Tagasovska and Lopez-Paz, (2019) proposed simultaneous quantile regression to estimate the quantiles by minimizing the pinball loss where the target quantile is randomly sampled in every training iteration. Brando et al., (2022) proposed an algorithm for predicting an arbitrary number of quantiles, which ensures the quantile monotonicity by imposing a restriction on the partial derivative of the quantile functions.

In this paper, we make the following methodological and theoretical contributions.

-

•

We propose a penalized deep quantile regression approach, in which a novel penalty function based on the rectified linear unit (ReLU) function is proposed to encourage the non-crossing of the estimated quantile regression curves.

-

•

Based on the estimated non-crossing quantile regression curves, we study a conformalized quantile regression approach to construct non-crossing conformal prediction intervals, which are fully adaptive to heteroscedasticity and have locally varying length.

-

•

We study the properties of the ReLU-penalized nonparametric quantile regression using deep feedforward neural networks. We derive non-asymptotic upper bounds for the excess risk of the non-crossing empirical risk minimizers. Our error bounds achieve optimal minimax rate of convergence, and the prefactor of the error bounds depends polynomially on the dimension of the predictor, instead of exponentially.

-

•

We establish theoretical guarantees of valid coverage of the proposed approach to constructing conformal prediction intervals. We also give a non-asymptotic upper bound of the difference between the non-crossing conformal prediction interval and the oracle prediction interval. Extensive numerical studies are conducted to support the theory.

2 Non-crossing nonparametric quantile regression

In this section, we describe the proposed method for nonparametric estimation of quantile curves with non-crossing constraints.

For any given , the conditional quantile function of given is defined by

| (1) |

where is a response, is a -dimensional vector of covariates, and is the conditional distribution function (c.d.f) of given . It holds that , where is the conditional probability measure of given . By definition (1), an inherent constraint of the conditional quantile curves is the monotonicity property: for any , it holds that

| (2) |

Therefore, estimated conditional quantile curves should also satisfy this property, otherwise, it would be difficult to interpret the estimated quantiles.

Quantile regression is based on the check loss function defined by

| (3) |

where is the indicator function. The target conditional quantile function is the minimizer of over all measurable function (Koenker,, 2005). In applications, only a finite random sample is available. The quantile regression estimator for a given is

| (4) |

where is a class of functions which may depend on the sample size .

For two quantile levels , we can obtain the estimated quantile curves and by using (4) separately for and . However, such estimated quantile curves may not satisfy the monotonicity constraint (2), that is, there may exist for which Below, we propose a penalized method to mitigate this problem.

2.1 Non-crossing quantile regression via ReLU penalty

In this subsection, we propose a penalized quantile regression framework to estimate quantile curves that can avoid the crossing problem. We first introduce a ReLU-based penalty function to enforce the non-crossing constraint in quantile regression. The ReLU penalty is defined as

This penalty function encourages when combined with the quantile loss function. At the population level, for , the expected penalized quantile loss function for is

| (5) |

where is a tuning parameter. Note that, with defined in (1), for . Moreover, as mentioned earlier, is the minimizer of the expected check loss over measurable function for respectively. The following lemma establishes the identifiability of the quantile functions through the loss function (5). This is the basis of the proposed method.

Lemma 2.1

Suppose is a random variable with c.d.f. . For a given , any element in is a minimizer of the expected check loss function . Moreover, the pair of true conditional quantile functions is the minimizer of the loss function (5), that is,

where is a class of measurable functions that contains the true conditional quantile functions.

Lemma 2.1 shows that the ReLU penalty does not introduce any bias at the population level. This is a special property of this penalty function, which differs from the usual penalty function such as the ridge penalty used in penalized regression.

When only a random sample is available, we use the empirical loss function

| (6) |

and define

| (7) |

where is a class of functions that approximate . In (6), a positive value of (i.e., the quantile curves cross at ) will be penalized with the penalty parameter . On the other hand, a negative value of (i.e., the quantile curves do not cross at ) will not incur any penalty. Therefore, with a sufficiently large penalty parameter , quantile crossing will be prevented.

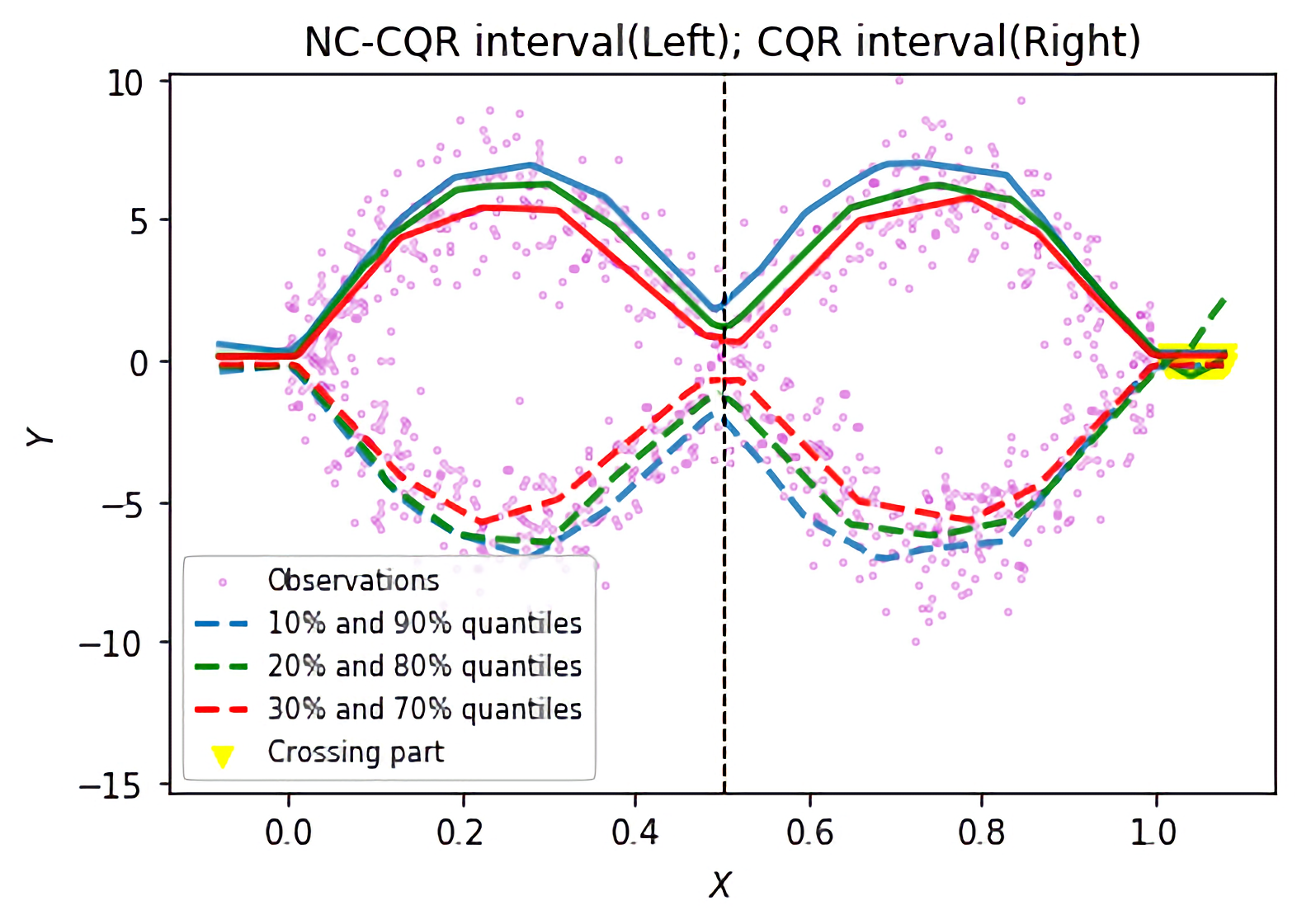

Throughout the paper, we choose the function class to be a function class of feedforward neural networks. We note that other approximation classes can also be used. However, an important advantage of neural network functions is that they are effective in approximating smooth functions in , see, for example, Jiao et al., (2021) and the references therein. A detailed description of neural network functions will be given in Section 2.2. Figure 1 previews non-crossing curve estimation via a toy example, which shows the comparison between the proposed method in (7) (with penalty) and the deep quantile estimation studied in Shen et al., (2021) (without penalty); see Section B.1.2 in Appendix for more details.

Remark 2.1

The rectified linear unit (ReLU) function is a piecewise-linear function. An important advantage of the ReLU penalty is that it is convex with respect to and , thus the loss function in (6) is also convex with respect to and .

Remark 2.2

The tuning parameter controls the amount of penalty on crossing quantile curves. As shown in Section 4, a bigger leads to a larger estimation bias. Therefore, there is a trade-off between the crossing and the accuracy of prediction intervals. Both can be achieved with proper choice of . In the appendix, we propose a cross-validation method to select .

Remark 2.3

Bondell et al., (2010) proposed a non-crossing nonparametric quantile regression using smoothing splines with non-crossing constraints. For two given quantile levels , they proposed to estimate the quantile curves and by minimizing the following constrained loss function

| (8) |

where denotes the derivative of a function , and is the total variation penalty to guarantee smoothness. Such a spline-based method works well in the one-dimensional setting, however, it is difficult to apply this approach to multi-dimensional problems.

2.2 ReLU Feedforward neural networks

For the estimation of conditional quantile functions, we choose the function class in (7) to be , a class of feedforward neural networks with parameter , depth , width , size , number of neurons and satisfying for some positive constant , where is the supreme norm of a function . Note that the network parameters may depend on the sample size , but this dependence is omitted for notational simplicity. Such a network has hidden layers and layers in total. We use a vector to describe the width of each layer; particularly in nonparametric regression problems, is the dimension of the input and is the dimension of the response. The width is defined as the maximum width of hidden layers, i.e., the size is defined as the total number of parameters in the network , i.e., the number of neurons is defined as the number of computational units in hidden layers, i.e., For an MLP , its size satisfies

From now on, we write as for short. Then, at the population level, the non-crossing nonparametric quantile estimation is to find a pair of measurable functions satisfying

| (9) |

3 Non-crossing quantile regression for conformal prediction

Now suppose we have a new observation . We are interested in predicting the corresponding unknown value of . Our goal is to construct a distribution-free prediction interval with a coverage probability satisfying

| (10) |

for any joint distribution and any sample size , where is often called a miscoverage rate. We refer to such a coverage stated in (10) as marginal coverage.

First, we define an oracle prediction band based on the conditional quantile functions. For a pre-specified miscoverage rate , we consider the lower and upper quantiles levels such as and . Then, a conditional prediction interval for given with a nominal miscoverage rate is

| (11) |

where and are the conditional quantile functions defined in (1) for quantile levels and respectively. Such a prediction interval with true quantile functions is ideal but cannot be constructed, only a corresponding empirical version can be estimated based on data in practice.

Next, we use the split conformal method Vovk et al., (2005) for constructing non-crossing conformal intervals. We split the observations into two disjoint sets: a training set and a calibration set . Non-crossing deep neural estimators of and based on the training set are given by

| (12) |

where

and is a tuning parameter. A key step is to compute the conformity score based on the calibration set Romano et al., (2019), which is defined as

| (13) |

Let . The conformity scores in quantify the errors incurred by the plug-in prediction interval evaluated on the calibration set , and can account for undercoverage and overcoverage.

Finally, for a new input data point and , the prediction interval for is defined as

| (14) |

where is the -th empirical quantile of , namely, the -th smallest value in , and denotes the smallest integer no less than . Here, is the cardinality of a set . The empirical quantile is a data-driven quantity, which conformalizes the plug-in prediction interval.

In contrast to the conformalized quantile regression procedure in Romano et al., (2019), our method produces conformal prediction intervals that avoid the quantile crossing problem. We refer to the proposed non-crossing conformalized quantile regression as NC-CQR, and the corresponding conformal interval (14) as NC-CQR interval.

Remark 3.1

The usual linear quantile regression (QR) model assumes that, for a given ,

| (15) |

where and are the intercept and slope parameters. Following Romano et al., (2019), a conformal interval based on linear quantile regression can be constructed. Specifically, by splitting the observations into two disjoint subsets: a training set and a calibration set , we can fit model (15) on the training set and obtain the estimators for and for a given , denoted by . Under model (15), the conformal interval with miscoverage rate is given by

| (16) |

where , with and , and is the -th smallest value among the conformity scores .

We summarize the implementation of NC-CQR interval construction in the following algorithm.

Algorithm Computation of non-crossing conformalized prediction intervals

Input: Observations and miscoverage level

Output:

4 Theoretical properties

In this section, we study the theoretical properties of the proposed NC-CQR method. We evaluate NC-CQR using the following two criteria:

-

1.

Validity: Under proper conditions, a conformal prediction interval satisfies that

(17) -

2.

Accuracy: If the validity requirement (17) is satisfied, a conformal prediction interval should be as narrow as possible.

The validity requirement (17) is evaluated based on the finite-sample marginal coverage in (10), which holds in the sense of averaging over all possible test values of . The accuracy of a prediction interval is usually measured by the discrepancy defined in (19) between the lengths of the prediction interval and the oracle one.

We assume that the target conditional quantile function defined in (1) is a -Hölder smooth function with as stated in condition (C3) below. Let , and , where denotes the largest integer strictly smaller than and denotes the set of non-negative integers. For a finite constant , the Hölder class of functions is defined as

| (18) |

where with and . We assume the following conditions.

-

(C1) The observations are i.i.d. copies of .

-

(C2) (i) The support of the predictor vector is a bounded compact set in , and without loss of generality we let (ii) Let be the probability measure of . The probability measure is absolutely continuous with respect to the Lebesgue measure.

-

(C3) For any fixed , the target conditional quantile function defined in (1) is a Hölder smooth function of order and a finite constant .

-

(C4) There exist constants and such that for any and any ,

for all up to a -negligible set, where is the conditional cumulative distribution function of given .

Condition (C1) is a basic assumption in conformal inference. The boundedness support assumption in Condition (C2) is made for technical convenience in the proof for deep neural estimation. Condition (C3) is a regular smoothness assumption on the target regression functions so that whose approximation result using deep neural networks can be obtained. Condition (C4) is imposed for self-calibration of the resulting neural estimator.

Theorem 4.1

Under Condition (C1), for a new i.i.d pair , the proposed NC-CQR interval satisfies

Theorem 4.1 shows that the proposed NC-CQR interval enjoys a rigorous coverage guarantee. The proof of this theorem is given in the Appendix.

We now quantify the accuracy of the prediction interval in terms of the difference between the NC-CQR interval and the oracle in (11) on the support of Let be the probability measure of defined in Condition (C2) and define for . The difference between the lengths of and is given by

| (19) |

By the triangle inequality, we have where

To bound and , we need to bound the error To this end, we first derive bounds for the the excess risk of defined as where is defined in (5). Without loss of generality, we assume that and , where denotes the smallest integer no less than and denotes the largest integer no greater than .

Theorem 4.2

Letting and , then the width, depth and size of the neural network satisfy

Suppose that Conditions (C1)-(C3) hold. If , the non-asymptotic error bound of the excess risk satisfies

where is a universal constant independent of and and .

The convergence rate of the excess risk is up to a logarithmic factor. The next theorem gives an upper bound for the accuracy of the proposed prediction interval defined in (19).

Theorem 4.3

(Non-asymptotic upper bound for prediction accuracy) Suppose that Conditions (C1)-(C4) hold. Let be a class of ReLU activated feedforward neural networks with width, depth specified as in Theorem 4.2 and let be the empirical risk minimizer over . Then, there exists a constant , for ,

where is a constant independent of and .

Theorem 4.3 gives an upper bound for the difference between the lengths of our proposed prediction interval and the oracle interval. With properly-selected neural network parameters, the oracle band can be consistently estimated by the NC-CQR band.

Finally, we consider the conformal interval based on linear quantile regression defined in (16).

Corollary 4.1

Suppose that at least one of and is a non-linear function on a subset of with non-zero measure. Then for any sample size , the accuracy of the conformal band defined in (16) is strictly worse than that of the oracle conformal band , i.e., there exists an such that

According to Corollary 4.1, a conformal interval based on the linear quantile regression will not reach the oracle accuracy in the presence of nonlinearity.

5 Numerical studies

5.1 Synthetic data

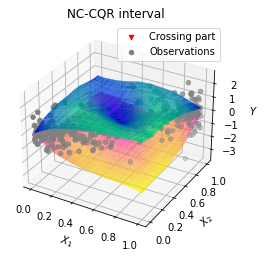

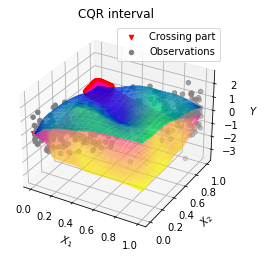

We first simulate a synthetic dataset with a -dimensional feature and a continuous response from the distributions defined in Section B.1.3. Our method is applied to independent observations from this distribution, using of them to train the deep quantile regression estimators and of them for calibration. The remaining data is for testing. We consider different dimensions to investigate how the dimensionality of the input affects the overall performance under multivariate input settings. The result is shown in Figure 2. In Figure 2(c), when dimension increases, NC-CQR method performs better than CQR in terms of smaller crossing rate. It shows that the NC-CQR method can mitigate the crossing problem in quantile regression. We also give a 3D visualization of the conformal intervals of our proposed NC-CQR estimation and that of the CQR method when in Figure 2. One can see from Figure 2(a) that the conformal interval by our proposed NC-CQR method does not have any crossing, while in Figure 2(b), the red region indicates that the lower bound is larger than the upper bound of the interval. More details of the results are given in Section B.1.3.

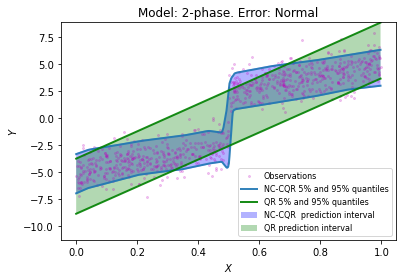

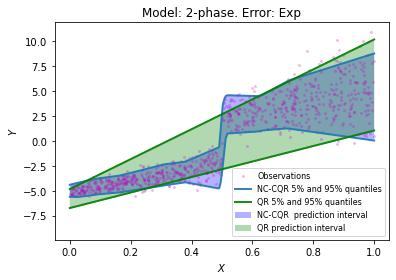

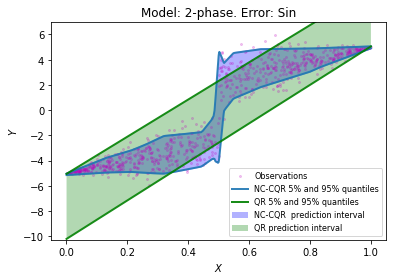

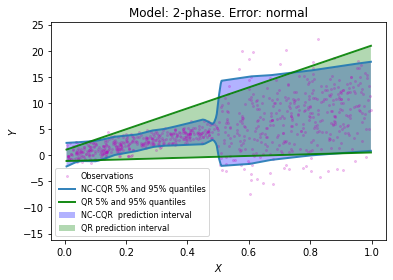

Our next synthetic example illustrates the adaptive property of the proposed NC-CQR prediction interval. We consider the following model with a discontinuous regression function:

| (20) |

A 90% NC-CQR interval is shown in color blue. The green lines represent a 90% conformal prediction intervals based on the standard linear quantile regression. As can be seen from the plots, the NC-CQR intervals automatically adapt to the shape of the regression function and the heteroscedasticity of the model error. Additional examples demonstrating the advantages of NC-CQR prediction intervals are given in the Appendix.

5.2 Real data examples

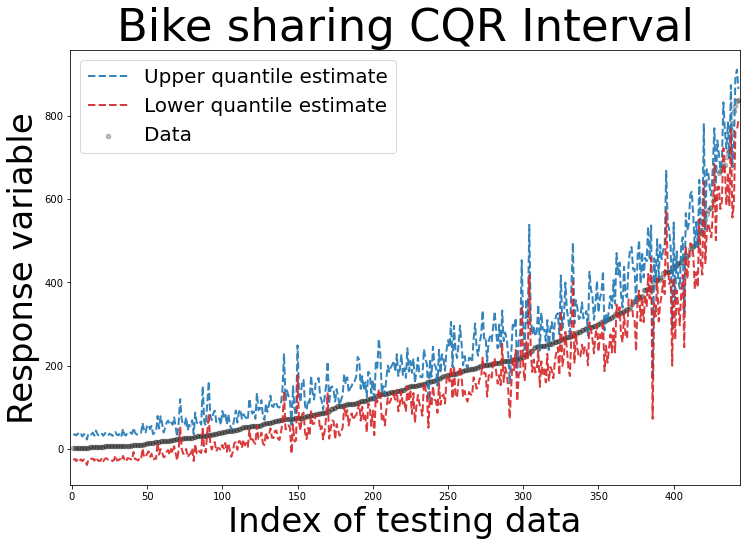

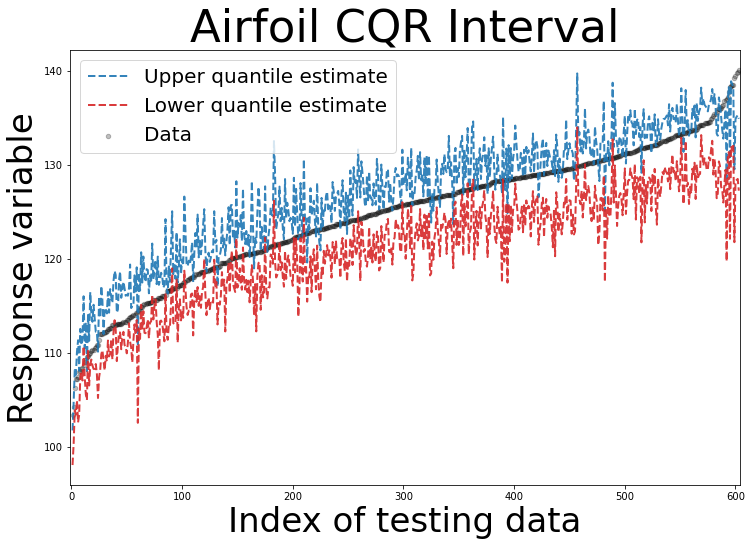

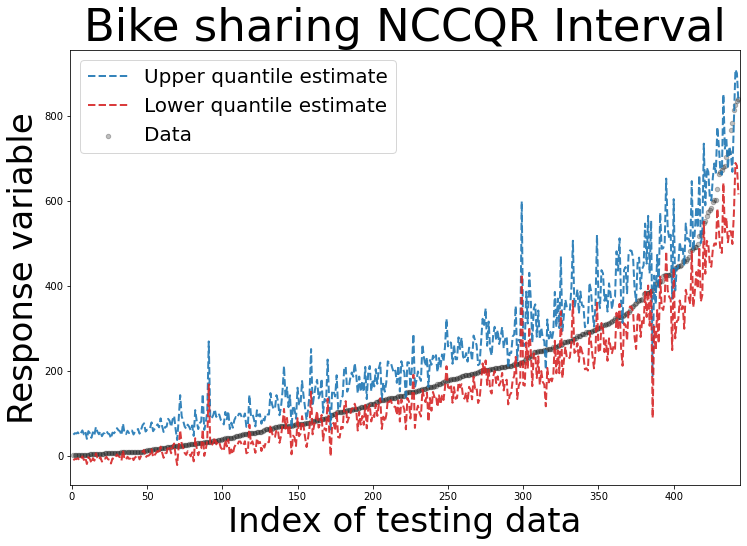

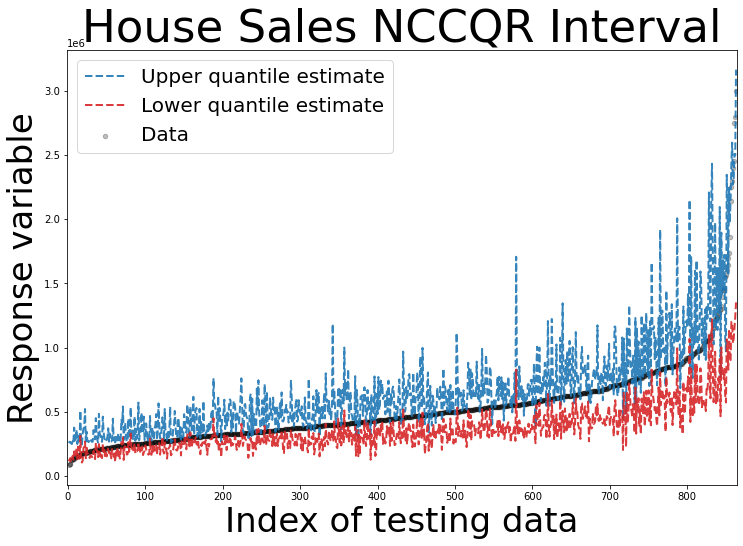

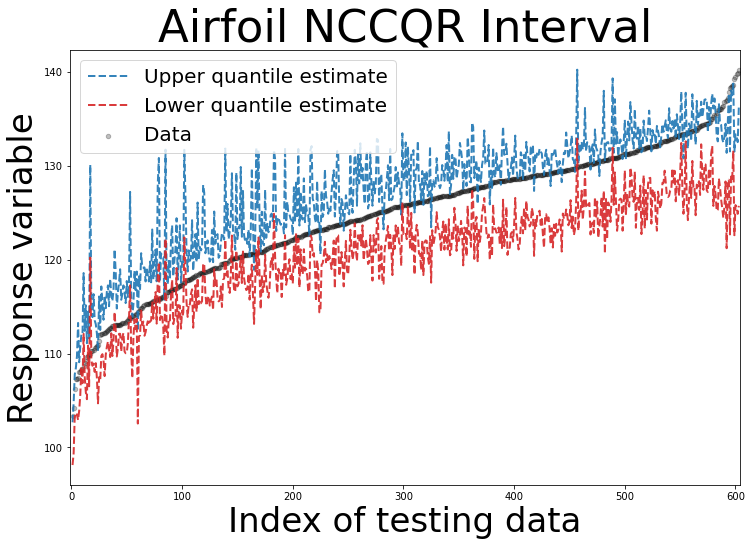

We compute the NC-CQR prediction intervals for the following datasets: bike sharing111https://archive.ics.uci.edu/ml/datasets/bike+sharing+dataset, house price222https://www.kaggle.com/datasets/harlfoxem/housesalesprediction and the air foil333https://archive.ics.uci.edu/ml/datasets/airfoil+self-noise data sets. To examine the performance of the ReLU penalty, we compare the NC-CQR with CQR. We compute the conformal prediction intervals based on these two methods using the same deep quantile regression estimator. Their performances are evaluated as in Section 5.1. We subsample of data for training, for calibration, and the remaining data is used for testing. All features are standardized to have 0 mean and unit variance. The nominal coverage rate is set to be . Figure S5 shows that the proposed NC-CQR method can mitigate the crossing problem encountered in the CQR estimation. Additional details of the result are given in Section B.2 in the Appendix.

6 Concluding remarks

We have proposed NC-CQR, a penalized deep quantile regression method which avoids the quantile crossing problem via a ReLU penalty. We have derived non-asymptotic upper bounds for the excess risk of the non-crossing empirical risk minimizers. Our error bounds achieve optimal minimax rate of convergence, the with the prefactor of the error bounds depending polynomially on the dimension of the predictor, instead of exponentially. The proposed ReLU penalty for monotonic constraints is applicable to problems with different loss functions. It is applicable to other nonparametric estimation method, including smoothing splines, kernel method and neural network. Therefore, the proposed ReLU penalty method may be of independent interest. Based on the estimated non-crossing conditional quantile curves, we construct conformal prediction intervals that are fully adaptive to heterogeneity. We have also provided conditions under which the proposed NC-CQR conformal prediction bands are valid with the correct coverage probability and achieve optimal accuracy in terms of the width of the prediction band.

A main limitation of the proposed method and the theoretical properties is that they rely on the i.i.d. assumption for the data. There are applications where observations are not independent (e.g., time series data) and there may be distribution shift. It would be interesting to extend the proposed method to deal with such non-i.i.d. settings and establish the corresponding theoretical properties.

Appendix A Appendix: Proofs

In this appendix, we prove the theoretical results stated in Section 4. First, we prove Lemma 2.1. For convenience, we restate this lemma below.

Lemma A.1

Suppose is a random variable with c.d.f. . For a given , any element in is a minimizer of the expected check loss function . Moreover, the pair of the true conditional quantile functions is the minimizer of the loss function (5), that is,

where is a class of measurable functions that contains the true conditional quantile functions.

Proof[of Lemma A.1] First, we write

Taking derivative w.r.t , we obtain

Since is a c.d.f., it is monotonic and thus any element of minimizes the expected loss . For functions , recall that the loss function (5) in the main context is

By the definition of in (1) in the main context, satisfies for . Then minimizes the expected loss for . Since the true quantile function satisfies the monotonicity requirement (2) in the main context, then . Therefore, is the minimizer of the loss function (5) in the main context.

Lemma A.2

Suppose that

| (S21) |

for some sequence and such that and when . Define

Then, under Conditions (C1)-(C4), for any independent of ,

Furthermore, if the calibration set is partitioned into

then for any constant , we have

Proof[of Lemma A.2] By Markov inequality, we have

When the calibration set is partitioned into

it follows from Hoeffding’s inequality that, for any ,

Letting , the proof of the second inequality in Lemma (A.2) is completed.

Proof[of Theorem 4.1] The proof of Theorem 4.1 is similar to that of Theorem 1 in Romano et al., (2019). Let be the conformity score

at the test point Recall that the prediction interval

By the construction of the prediction interval, if and only if , and particularly,

Since the data are i.i.d, so are the calibration variables for and . Therefore, by Lemma 2 on inflated empirical quantiles in Romano et al., (2019), we can conclude that

We now present a non-asymptotic upper bound for the excess risk.

Lemma A.3

(Non-asymptotic excess risk bound) Consider the -variate nonparametric regression model in (1) in the paper. For any given , Let be a class of feedforward neural networks with ReLU activation function with width and depth specified by

Assume that Conditions (C1)-(C3) hold with . For any given , let and denote the corresponding conditional quantile functions and let

be the empirical risk minimizer (ERM) over , then

| (S22) |

where is a universal constant independent of and , and

Lemma A.3 provides a general non-asymptotic upper bound for the excess risk. This bound clearly describes how the upper bounds of the excess risk depend on the neural network parameters. The first term of the bound (A.3) is the upper bound of the stochastic error and the second term is the upper bound of the approximation error. Notice that the stochastic error increases with , while the approximation error decreases with . Similar to Shen et al., (2021), we next discuss efficient designs of rectangle networks, i.e., networks with equal width for each hidden layer. It follows from the standard structure of multilayer perceptrons that the size of network . Thus, we can select the neural network width and depth given in terms of to balance the stochastic error and approximation error, so as to achieve the optimal convergence rate.

Proof[of Lemma A.3] The sample size of the training set is . Without loss of generality, we let the size of training data to be proportional to , i.e., there exists a constant such that . Let be a random sample from the distribution of and let be another random sample independent of . First, for any and , we denote

where

Note that for any , and

Then the excess risk of

and the expected excess risk

Define the “best in class” estimator by By the definition of empirical risk minimizer, we have

Then

where the first term is the expectation of a stochastic term and the second term is the approximation error.

Next, we give an upper bound for the stochastic term. Denote for any in . For a given sequence , let . For any , let be the covering number of under norm with radius . Define the uniform covering number as the maximum over all of the covering number , i.e.,

Let denote the uniform covering number with radius . We denote the center of the covering balls by . By the definition of the covering, there exist such that and for all . By the Lipschitz property of the check loss function , we have for

| (S23) |

and

Then we have

and

| (S24) |

Note that for any , . Let . For each and any , by applying the Bernstein inequality, we have

This leads to a tail probability bound of , that is

Thus, for any ,

Letting , we can obtain

| (S25) |

Now, we bound the covering number by the pseudo dimension of through its parameters. Denote by the pseudo dimension of , by Theorem in Anthony et al., (1999), for ,

where is the Euler’s number. Besides, based on Theorem 3 and 6 in Bartlett et al., (2019), there exist universal constants such that

Recall that for some constant , we set . Combining the inequalities (A), (S24) and (S25), we have

for some universal constant . For the second term on the right-hand side of the above inequality, it is sufficient to find the upper bound of the approximation error

By Theorem 3.3 in Jiao et al., (2021), an approximation result for Hölder smooth functions was obtained: given any , for the function class of ReLU multi-layer perceptrons with and depth , there exists an such that

for all , where , denotes the smallest integer no less than , and

with and an arbitrary number in . Note that the Lebesgue measure of is no more than which can be arbitrarily small since can be arbitrarily small. Since the probability measure of covariate is absolutely continuous to Lebesgue measure, we have

and

This leads to the non-asymptotic upper bound of excess risk and completes the proof of Lemma 4.2.

Proof[of Theorem 4.2] In order to achieve the optimal convergence rate, we should balance between the first term (stochastic error) and the second term (approximation error) of the right-hand side in (20) in the main context. It is obvious that when and get larger, the complexity of the neural network increases, and hence the upper bound of the stochastic error gets larger. In the meanwhile, the upper bound of the approximation error will become smaller and vice versa. Therefore we need a trade-off between the stochastic error and approximation error to achieve the optimal convergence rate. If we choose and , then

To get the optimal convergence rate, we balance the order of stochastic error to be the same as that of the approximation error with respect to the sample size , i.e., with respect to the sample size . By simple math, we get . Therefore, when we choose , and , we will obtain the optimal rate such that

where is a constant independent of and . The proof of Theorem 4.3 is completed.

Lemma A.4

(Self-calibration) Suppose that Conditions (C1)-(C4) hold. For any , denote . Let . Then, we have

where . Furthermore, for satisfying

for up to a -negligible set, we have

otherwise if , we have

Proof[of Lemma A.4] By equation (B.3) in Belloni et al., (2019), for any scalar , we have

Suppose that and satisfying for all . Let . Then given , taking conditional expectation on above equation with respect to , we have

Then by Condition (C4), we can obtain

Suppose that , similarly we have

Then,

The proof of Lemma 4.4 is completed.

Proof[of Theorem 4.3]

Since the sizes of the calibration set and the training set are proportional to , without loss of generality, we let . By Lemma 4.2 and Lemma 4.4, upper bounds for and can be obtained. Note that by Lemma 4.2 and Lemma 4.4, there exists constant such that for ,

and

where and are defined in Theorem 4.3 and is a constant independent of . By Markov inequality, Lemma 4.2 and Lemma 4.4, we can obtain that, for any ,

Let be a positive integer. We define , and . Then and are positive sequence such that and as . Therefore (S21) holds for the defined and and

| (S26) |

Next we bound . Recall that is defined as the -th empirical quantile of , where

Now we define for any Note that

Thus the population -th quantile of is , i.e., . By Lemma A.2, we have for , where and are defined in Lemma A.2. Denote and to be the empirical distributions of for and respectively. Then defined in (14) in the main context equals to .

For , is the largest number in . If for all , then the largest number in equals to . By the definition of and , elements in have larger quantity on average, therefore

Similarly, if for all , then the largest number in equals to . However, will obtain smaller quantity than , therefore

Combining these two inequalities and the Lemma A.2, we have

By Lemma (A.2), and . Thus we can obtain that

| (S27) |

We have already shown that . By Lemma 4.2, Lemma 4.2 and Theorem 4.3, there exists a constant such that for ,

where is a constant independent of and . The proof is completed.

Proof[of Corollary 4.4] The length of the prediction interval for linear quantile regression model is , where is the -th quantile of . The conformity score is larger than either or and it is a data-driven constant. Thus we assume that , where is a positive constant. The target term can be decomposed into

Since at least one of the and is nonlinear function, then there exists such that

This implies . We have completed the proof.

Appendix B Additional numerical experiments

In this section, we include additional numerical experiments to evaluate the performance of the proposed method. We also apply the proposed method to real datasets to illustrate its application.

We compare the performance of the proposed NC-CQR prediction interval with the conformal interval based on linear quantile regression (QR) in (16) in the main context and the conformalized quantile regression (CQR) in Romano et al., (2019).

B.1 Estimation and Evaluations

The training data are generated with size . First, the samples are randomly divided into two sets: the training set with samples and the calibration set with samples. We use to compute the empirical risk minimizer at the and quantiles, i.e.,

where is set to be a class of ReLU activated multilayer perceptrons with hidden layers and width in our simulations, is the dimension of the input predictor. Next, we calculate the conformity score according to

| (S28) |

Let be the -th smallest value among . Then for a given sample value , the NC-CQR conformal interval is constructed by

where and are the lower and upper bound of the conformal interval respectively. A test set of size is also generated, which are independent of and of the same distribution as the training set. The performance of the conformal intervals are evaluated on the test set via the following statistics.

-

1.

The average length of the interval, denoted by , is defined as

(S29) -

2.

The coverage rate is calculated by

(S30)

To show the effect of the non-crossing penalty, we also compute the crossing rate of the neural network output (CR-NN) and the crossing rate of the conformal interval (CR-CI) as follows:

| CR-NN | (S31) | |||

| CR-CI | (S32) |

In the simulation studies, we set in all settings.

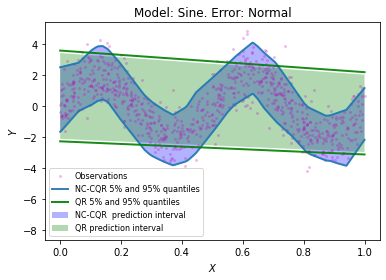

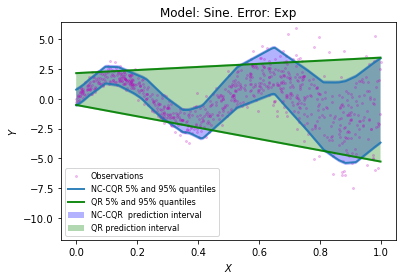

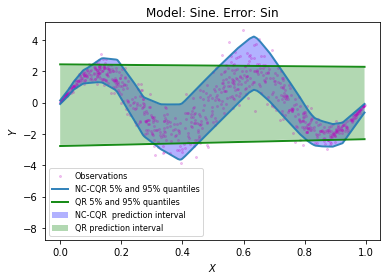

B.2 Data generation: univariate models

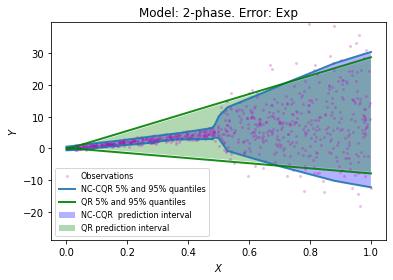

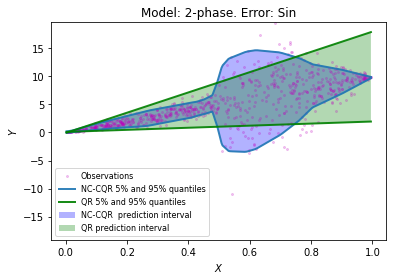

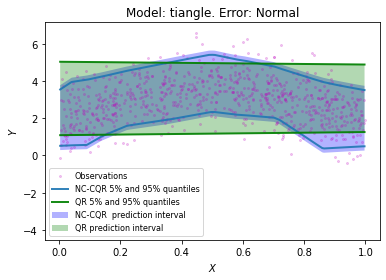

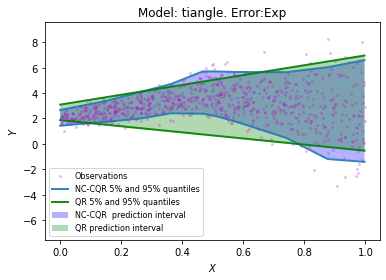

The training data is generated under different univariate models with size . In settings (1)-(5), the covariate follows Uniform distribution, and the response is generated by with different settings specified below.

-

Model 1. “Sine”: Sine function

(S33) -

Model 2. “2-phase”: Linear function

(S34) -

Model 3. “Triangle”: Triangular function

(S35) -

Model 4. “Discontinuous”: Discontinuous function

(S36)

For the above models, we try different error distributions:

-

•

follows the standard normal distribution, i.e., , denoted by Normal.

-

•

Conditional on , follows a normal distribution with mean 0 and variance increasing in , i.e., , denoted by Exp.

-

•

Conditional on , follows a normal distribution with mean 0 and variance depending on via a sine function, i.e., , denoted by Sin.

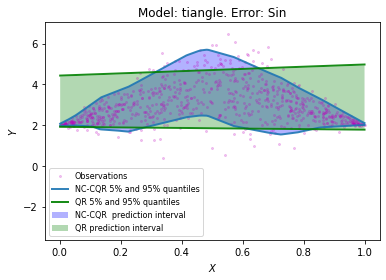

We construct conformal prediction intervals based on our proposed NC-CQR in (12) in the main context and the linear quantile regression (QR) method in (16) in the main context for univariate models 1-4 with , and . The prediction intervals based on NC-CQR and linear QR under different settings are displayed in Figure S5. In addition, we perform 50 replications by randomly splitting the training data times, and calculate the average statistics and their standard deviations. The comparison between NC-CQR and QR intervals under different univariate settings is given in Table S1, which shows that on average the NC-CQR interval can achieve valid coverage with shorter average length compared to the QR interval. It is worth noting that although the theoretical guarantees of the accuracy in Lemma 4.2 and Theorem 4.5 require that the target quantile function is a Hölder smooth function in Condition (C3), our NC-CQR method still works reasonably well in terms of valid coverage rate and accuracy under setting 4 with a discontinuous target quantile function.

| Error | ||||

|---|---|---|---|---|

| Setting | Method | Length | Coverage | |

| Sine | NC-CQR | 3.464(0.096) | 90.5%(0.016) | 0.085(0.092) |

| QR | 5.484(0.057) | 90.7%(0.010) | 0.068(0.066) | |

| 2-phase | NC-CQR | 9.854(0.276) | 90.0%(0.011) | 0.095(0.125) |

| QR | 10.870(0.256) | 89.8%(0.009) | 0.022(0.191) | |

| Triangle | NC-CQR | 3.411(0.091) | 90.3%(0.014) | 0.026(0.096) |

| QR | 3.836(0.087) | 89.9%(0.015) | 0.009(0.057) | |

| Discontinuous | NC-CQR | 3.521(0.081) | 90.8%(0.015) | 0.061(0.080) |

| QR | 5.234(0.112) | 89.6%(0.010) | 0.036(0.109) | |

| Error | ||||

| Setting | Method | Length | Coverage | |

| Sin | NC-CQR | 3.857(0.097) | 90.3%(0.016) | 0.054(0.064) |

| QR | 5.746(0.090) | 90.2%(0.013) | 0.001(0.087) | |

| 2-phase | NC-CQR | 14.739(0.550) | 90.6%(0.014) | 0.047(0.059) |

| QR | 16.543(0.482) | 90.3%(0.011) | 0.066(0.104) | |

| Triangle | NC-CQR | 3.807(0.107) | 90.0%(0.013) | 0.050(0.059) |

| QR | 4.407(0.094) | 89.9%(0.007) | 0.020(0.044) | |

| Discontinuous | NC-CQR | 3.851(0.066) | 90.4%(0.007) | 0.040(0.074) |

| QR | 5.627(0.103) | 90.2%(0.012) | 0.060(0.056) | |

| Error | ||||

| Setting | Method | Length | Coverage | |

| Sin | NC-CQR | 2.167(0.068) | 89.8%(0.014) | 0.034(0.041) |

| QR | 4.838(0.053) | 90.1%(0.012) | 0.032(0.057) | |

| 2-phase | NC-CQR | 6.566(0.208) | 90.2%(0.011) | 0.078(0.071) |

| QR | 7.967(0.442) | 90.1%(0.011) | 0.012(0.044) | |

| Triangle | NC-CQR | 2.149(0.039) | 89.6%(0.012) | 0.026(0.028) |

| QR | 2.853(0.070) | 89.2%(0.017) | 0.009(0.060) | |

| Discontinuous | NC-CQR | 2.211(0.040) | 90.1%(0.008) | 0.009(0.032) |

| QR | 4.758(0.075) | 90.7%(0.016) | 0.010(0.041) | |

In addition, we also simulated data under Model 5 to show the power of non-crossing penalty.

-

Model 5. Double sine function:

(S37) where and conditional on , follows a normal distribution with mean 0 and variance depending on via a sine function, i.e., .

Fig. 1 in the paper is generated from Model 5 with Sin error. It presents 6 distinct estimated quantiles by CQR method (right) and NC-CQR method (left) where there are crossing parts at the right-hand side and there is no crossing at the left-hand side.

B.3 Multivariate models

We consider a multivariate setting with heterogeneous error in the simulation studies.

-

Model 6. Single index model with heterogeneous error:

(S38) where follows Uniform with independent components, and the true value of the parameter vector is fixed to be a subvector of the first value of

We consider different dimensions with , to investigate how the dimensionality of the input affects the overall performance. We construct conformal intervals by our proposed NC-CQR and the CQR (Romano et al.,, 2019). Set , and . The conformal band is then constructed based on the estimated and quantiles respectively. The simulation results are reported in Table S2, which shows that the estimated quantile curves by our proposed NC-CQR have fewer crossing than the CQR method. While for conformal intervals, after making use of the conformity score in (S28), we observe that there is nearly no crossing in both CQR and NC-CQR, but CQR interval has a larger -th quantile of the conformity score and larger length than our proposed NC-CQR interval. We give a 3D visualization of the conformal intervals by our proposed NC-CQR and the CQR method with in Figure 2 in main context. Both NC-CQR and CQR intervals achieve coverage rate, and the crossing rate of the NC-CQR and CQR interval are and respectively. The average lengths of NC-CQR interval and CQR interval are and respectively, which shows that the NC-CQR interval is slightly shorter.

| Method | CR-NN | CR-CI | Coverage | Length | ||

|---|---|---|---|---|---|---|

| CQR | ||||||

| NC-CQR | ||||||

| CQR | ||||||

| NC-CQR | ||||||

| CQR | ||||||

| NC-CQR | ||||||

| CQR | ||||||

| NC-CQR | ||||||

| CQR | ||||||

| NC-CQR |

Notes: “CR-NN” denotes the crossing rate of neural network estimates defined in (S31); “CR-CI” denotes the crossing rate of the conformal interval defined in (S32); “Length” denotes the average length defined in (S29); is the -th empirical quantile of the conformity score defined in (S28). Each presented result is the average of experiments.

B.4 Real data analysis

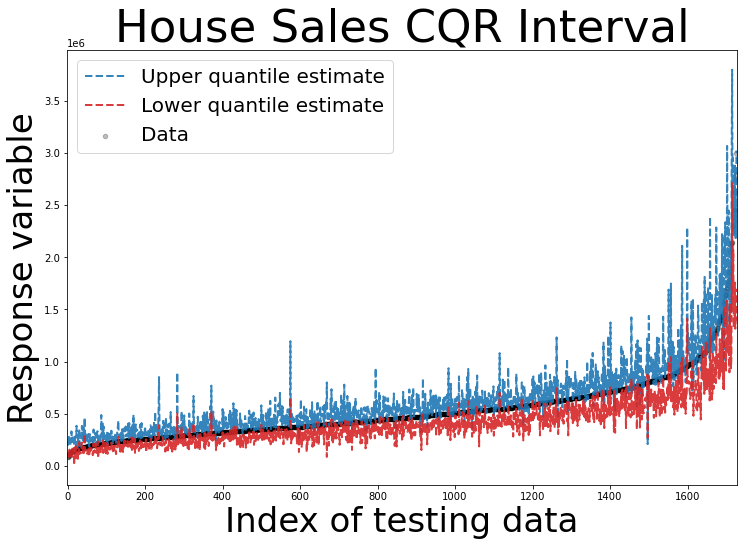

In this subsection, first, we apply the NC-CQR method to the housing sales data in King County, USA. The dataset contains sold houses data between May 2014 and May 2015. For each house sold, the data consists of attributes including housing price, the number of bedrooms, bathrooms, size, view, etc. The prediction target is the housing price. We exclude nominal variables including house id, date, and zip code, and intend to predict the housing price from the remaining attributes and construct an prediction interval corresponding to the observations. We also apply the proposed method to Bike sharing dataset with and the airfoil dataset with . The goal of the analysis on the Bike sharing dataset is to predict the interval of the total number of rental bikes number given the related attributes such as weather and season. The goal of the analysis on the airfoil dataset is to construct a prediction interval of the scaled sound pressure level given six attributes such as the angle of the attack. We let , and . The conformal band is constructed based on the estimated and quantiles respectively. We randomly select testing data from samples. And we evenly split the remaining samples into two subsets: a proper training set with samples and calibration set with samples.

According to Algorithm 1, we construct the conformal interval by (12) in the main context and the length and coverage rate are computed according to (S29) and (S30). Also, we compare the NC-CQR to CQR and QR described in subsection 4.1. We present the length in (S29) and the -th empirical quantile of the conformity score, denoted by , the coverage rate in (S30), CR-NN in (S31) and CR-CI in (S32) in Table S3. Table S3 shows that all three methods achieve valid coverage in the housing price prediction. In addition, NC-CQR avoids the crossing problem of lower and upper bounds in CQR. Besides, the average length of the prediction interval in NC-CQR is smaller than that of the QR method, which means that the NC-CQR is more accurate than QR.

| House sales | |||||

|---|---|---|---|---|---|

| Method | CR-NN | CR-CI | Coverage | Length | |

| NC-CQR | |||||

| CQR | |||||

| QR | |||||

| Bike sharing | |||||

| Method | CR-NN | CR-CI | Coverage | Length | |

| NC-CQR | |||||

| CQR | |||||

| QR | |||||

| Air foil | |||||

| Method | CR-NN | CR-CI | Coverage | Length | |

| NC-CQR | |||||

| CQR | |||||

| QR |

Notes: “CR-NN” denotes the crossing rate of neural network estimates defined in (S31); “CR-CI” denotes the crossing rate of the conformal interval defined in (S32); “Coverage” denotes the coverage rate defined in (S30); “Length” denotes the average length defined in (S29); is the -th empirical quantile of the conformity score defined in (S28; For house sales table, the scale of Length and is .

B.5 Tuning Parameter Selection

In the penalized loss function (6) in the paper, the tuning parameter determines the extent of penalization. The popular One Standard Error Rule (1se rule) is used with cross-validation (CV) to compare models with different numbers of parameters in order to select the most parsimonious model with low error.

The idea of -fold cross-validation is to split the data into roughly equal-sized parts: . For the -th part where , we train the model on data set and the conduct the evaluation on . Now consider in a set of candidate tuning parameter , we obtain the estimate on the training set . Then we calculate the summation of the average length and the number of crossing points (ALC) on the validation set defined as

| (S39) |

For each tuning parameter value , we compute the average error over all folds:

We then choose the value of the tuning parameter that minimizes the above-average error, By the proposed tuning parameter selection, we can choose the that can both avoid the crossing problem and achieve a narrow interval.

References

- Anthony et al., (1999) Anthony, M., Bartlett, P. L., Bartlett, P. L., et al. (1999). Neural network learning: Theoretical foundations, volume 9. cambridge university press Cambridge.

- Barber et al., (2021) Barber, F. R., Candes, E. J., Ramdas, A., and Tibshirani, R. J. (2021). The limits of distribution-free conditional predictive inference. Information and Inference: A Journal of the IMA, 10(2):455–482.

- Bartlett et al., (2019) Bartlett, P. L., Harvey, N., Liaw, C., and Mehrabian, A. (2019). Nearly-tight vc-dimension and pseudodimension bounds for piecewise linear neural networks. The Journal of Machine Learning Research, 20(1):2285–2301.

- Belloni et al., (2019) Belloni, A., Chernozhukov, V., and Kato, K. (2019). Valid post-selection inference in high-dimensional approximately sparse quantile regression models. Journal of the American Statistical Association, 114(526):749–758.

- Bondell et al., (2010) Bondell, H. D., Reich, B. J., and Wang, H. (2010). Noncrossing quantile regression curve estimation. Biometrika, 97(4):825–838.

- Brando et al., (2022) Brando, A., Center, B. S., Rodriguez-Serrano, J., Vitria, J., et al. (2022). Deep non-crossing quantiles through the partial derivative. In International Conference on Artificial Intelligence and Statistics, pages 7902–7914. PMLR.

- He, (1997) He, X. (1997). Quantile curves without crossing. The American Statistician, 51(2):186–192.

- Jiao et al., (2021) Jiao, Y., Shen, G., Lin, Y., and Huang, J. (2021). Deep nonparametric regression on approximately low-dimensional manifolds. arXiv 2104.06708.

- Kivaranovic et al., (2020) Kivaranovic, D., Johnson, K. D., and Leeb, H. (2020). Adaptive, distribution-free prediction intervals for deep networks. In International Conference on Artificial Intelligence and Statistics, pages 4346–4356. PMLR.

- Koenker, (1984) Koenker, R. (1984). A note on l-estimates for linear models. Statistics & probability letters, 2(6):323–325.

- Koenker, (2005) Koenker, R. (2005). Quantile Regression. Econometric Society Monographs. Cambridge University Press.

- Lei et al., (2018) Lei, J., G’Sell, M., Rinaldo, A., Tibshirani, R. J., and Wasserman, L. (2018). Distribution-free predictive inference for regression. Journal of the American Statistical Association, 113(523):1094–1111.

- Lei et al., (2013) Lei, J., Robins, J., and Wasserman, L. (2013). Distribution-free prediction sets. Journal of the American Statistical Association, 108(501):278–287.

- Lei and Wasserman, (2014) Lei, J. and Wasserman, L. (2014). Distribution-free prediction bands for non-parametric regression. Journal of the Royal Statistical Society: Series B: Statistical Methodology, pages 71–96.

- Neocleous and Portnoy, (2008) Neocleous, T. and Portnoy, S. (2008). On monotonicity of regression quantile functions. Statistics & probability letters, 78(10):1226–1229.

- Papadopoulos, (2008) Papadopoulos, H. (2008). Inductive conformal prediction: Theory and application to neural networks. INTECH Open Access Publisher Rijeka.

- Papadopoulos et al., (2002) Papadopoulos, H., Proedrou, K., Vovk, V., and Gammerman, A. (2002). Inductive confidence machines for regression. In European Conference on Machine Learning, pages 345–356. Springer.

- Romano et al., (2019) Romano, Y., Patterson, E., and Candes, E. (2019). Conformalized quantile regression. Advances in Neural Information Processing Systems, 32:3543–3553.

- Sesia and Candès, (2020) Sesia, M. and Candès, E. J. (2020). A comparison of some conformal quantile regression methods. Stat, 9(1):e261.

- Shen et al., (2021) Shen, G., Jiao, Y., Lin, Y., Horowitz, J. L., and Huang, J. (2021). Deep quantile regression: Mitigating the curse of dimensionality through composition. arXiv preprint arXiv:2107.04907.

- Tagasovska and Lopez-Paz, (2019) Tagasovska, N. and Lopez-Paz, D. (2019). Single-model uncertainties for deep learning. Advances in Neural Information Processing Systems, 32.

- Vovk, (2012) Vovk, V. (2012). Conditional validity of inductive conformal predictors. In Asian conference on machine learning, pages 475–490. PMLR.

- Vovk et al., (2005) Vovk, V., Gammerman, A., and Shafer, G. (2005). Algorithmic learning in a random world. Springer Science & Business Media.

- Zeni et al., (2020) Zeni, G., Fontana, M., and Vantini, S. (2020). Conformal prediction: a unified review of theory and new challenges. arXiv preprint arXiv:2005.07972.