Measure-valued processes for energy markets

Abstract

We introduce a framework that allows to employ (non-negative) measure-valued processes for energy market modeling, in particular for electricity and gas futures. Interpreting the process’ spatial structure as time to maturity, we show how the Heath-Jarrow-Morton approach (see Heath et al. (1992)) can be translated to this framework, thus guaranteeing arbitrage free modeling in infinite dimensions. We derive an analog to the HJM-drift condition and then treat in a Markovian setting existence of non-negative measure-valued diffusions that satisfy this condition. To analyze mathematically convenient classes we build on Cuchiero et al. (2021) and consider measure-valued polynomial and affine diffusions, where we can precisely specify the diffusion part in terms of continuous functions satisfying certain admissibility conditions. For calibration purposes these functions can then be parameterized by neural networks yielding measure-valued analogs of neural SPDEs. By combining Fourier approaches or the moment formula with stochastic gradient descent methods, this then allows for tractable calibration procedures which we also test by way of example on market data. We also sketch how measure-valued processes can be applied in the context of renewable energy production modeling.

Keywords: HJM term structure modeling; energy markets; (neural) measure-valued processes,

polynomial and affine diffusions; Dawson-Watanabe type superprocesses

AMS MSC 2020: 91B72, 91B74, 60J68

1 Introduction

In this article we show how to employ non-negative measure-valued processes for energy market modeling, in particular for electricity and gas futures. Before describing in detail our approach we start by discussing some important features of these markets, following Benth et al. (2008).

The most liquidly traded products in electricity, gas, and also temperature markets are future contracts as well as options written on these. These future contracts deliver the underlying commodity over a certain period rather than at one fixed instance of time. By their nature, these contracts are often also called swaps, since they represent an exchange between fixed and variable commodity prices. We shall however employ the terms future or future contract throughout.

Our focus lies on these future markets as they exhibit higher liquidity than the spot energy markets. Indeed, even though it is possible to trade power and gas commodities on the spot market, one usually faces high storage and transaction costs, which in turn explains the lack of liquidity on the spot market. As a consequence it is potentially more difficult to recognize and model features or characteristic patterns of the spot price behavior. Nevertheless stochastic models for the spot prices are widely applied and also used to derive the dynamics of future prices based on no-arbitrage principles. Indeed, this is one of the two main approaches how to to set up tractable mathematical models for future contracts in power markets. The second approach consists in directly modeling the complete forward curve by applying a Heath-Jarrow-Morton (HJM) type approach (see Heath et al. (1992) and Benth and Krühner (2014) in the context of energy markets). We shall adapt this second approach and model directly an analog of the forward curve, however with non-negative measure-valued processes rather than function-valued ones. In the sequel, we shall omit “non-negative” and only use “measure” for “non-negative measure”.

There are many mathematical motivations to deal with this kind of processes. In general, measure-valued processes are often used for modeling dynamical systems for which the spatial structure plays a significant role. In the current setting, time to maturity takes the role of the spatial structure. This is similar to common forward curve modeling via stochastic partial differential equation (SPDE) as for instance in Benth and Krühner (2014) or Benth et al. (2021b). The potential advantage of using measure-valued processes instead of function-valued ones is that many spatial stochastic processes do not fall into the framework of SPDEs. In addition, it is often easier to establish existence of a measure-valued process rather than of an analogous SPDE, say in some Hilbert space, which would for instance correspond to its Lebesgue density, but which does not necessarily exist.

The decisive economic reason for using measure-valued processes in electricity and gas modeling however lies in the very nature of the future contracts, namely as products that deliver the underlying commodity always over a certain period instead of one fixed instance in time. To formulate this mathematically, denote the price of a future with delivery over the time interval at time by . Then, following Benth et al. (2008), can be written as a weighted integral of instantaneous forward prices with delivery at one fixed time , i.e.

| (1.1) |

where denotes some weight function. The crucial motivation for measure-valued process now comes from the fact that there is no trading with the instantaneous forwards for obvious reasons. Thus, rather than using in the expression of the future prices, we can also use a measure.

An additional motivation stems from the empirically well documented fact that energy spot prices can jump at predictable times, e.g. due to maintenance works in the power grid or political decisions which currently influence these markets substantially. In the context of such stochastic discontinuities we refer to the pioneering work Fontana et al. (2020) in the setup of multiple yield curves. To illustrate why these predictable jumps lead to measure-valued forward processes, consider the simple example where the spot price exhibits a jump at the deterministic time . In this case we can write for some jump-size which is supposed to be -measurable111Here, denotes some filtration supporting the spot price process and some finite time horizon. and some process that we suppose for simplicity to be continuous. As the instantaneous forward price is according to (Benth et al., 2008, equation (1.6)) given by

for each and , this implies that is discontinuous at . As forward curve modeling requires to take derivatives with respect to , the corresponding SPDE contains a differential operator and we thus have to deal with distributional derivatives, leading naturally to measure-valued processes that can be treated with the analysis presented in this paper. We also refer to Assefa and Harms (2022) where stochastic discontinuities are also used as one motivation for term structure models based on cylindrical measure-valued processes.

Due to these reasons one of the main goals of this article is to establish a Heath-Jarrow-Morton (HJM) approach for measure-valued processes. To this end we pass to the Musiela parametrization and thus consider time to maturity instead of time of maturity.

More precisely, fix a finite time horizon , consider a filtered probability space , and a measure-valued process supported on the compact interval . The measure will play the role of , meaning that if its Lebesgue density existed, it would correspond to instantaneous forward prices at time with time to maturity . Then future prices at time given by (1.1) become

Note that the integration domain does not include the left boundary point as we suppose a delivery over the left-open interval . Observe that the this choice permits to cumulatively add delivery periods, meaning that,

for each .

The next step is now to specify a suitable no-arbitrage condition. As long as the future contracts exist for potentially all delivery periods, it is natural to rely on no-arbitrage conditions for large financial markets allowing for a continuum of assets. In this respect the notion of no asymptotic free lunch with vanishing risk (NAFLVR), as introduced in Cuchiero et al. (2016b), qualifies as an appropriate and economically meaningful condition. Mathematically, in our setting, this is equivalent to the existence of an equivalent (local) martingale measure under which the (discounted) price processes of these contracts are (local) martingales. Modulo some technical conditions, this can then be translated to the following HJM-drift condition on the measure-valued process (see Theorem 3.1): if there exists an equivalent measure such that

is -martingale for all appropriate test functions , then NAFLVR holds. Here, the brackets mean . Note that this is a weak formulation to make sense out of

where denotes a measure-valued local martingale. Indeed, this would correspond to a (non-existing) strong formulation, well-known from function-valued forward curve modeling, see e.g. (Benth et al., 2021b, Section 2). Note that even though we here focus on energy markets, a similar framework can be used for term structure models in interest rate theory. The HJM-drift condition of course has to be adapted to guarantee that the bond prices are (local) martingales.

Clearly the HJM-drift condition restricts the choice of the measure-valued process since the drift part is completely determined, but we are free to specify the martingale part as long as we do not leave the state space of (non-negative) measures. To establish existence of measure-valued diffusion processes satisfying the drift condition, we rely on the martingale problem formulation of Ethier and Kurtz (2005) in locally compact and separable spaces which applies to our setting of measures on a compact set equipped with the weak--topology. Based on the positive maximum principle we then give sufficient conditions for the existence of such measure-valued diffusions (see Theorem 4.3). Additionally to these requirements we look for tractable specifications coming from the class of affine and polynomial processes as introduced in Cuchiero et al. (2021), where we can precisely specify the diffusion part due to sufficient and (partly) necessary conditions on its form. This setup then allows for tractable pricing procedures via the moment formula well-known from polynomial processes (see e.g. Cuchiero et al. (2012), Filipović and Larsson (2016)) and Fourier approaches. This holds in particular true for the affine class as we obtain explicit solutions for the Riccati PDEs. These pricing methods can then of course be used for calibration purposes. To this end we parameterize the function valued characteristics of polynomial models as neural networks to get neural measure-valued processes, an analog to neural SDEs and SPDEs. In Section 5.4 we exemplify such a calibration for the particular case of an affine measure-valued model which we calibrate to market call options written on certain future contracts whose prices are obtained from the EEX German Power data (see https://www.eex.com/en/market-data/power/options).

Apart from modeling energy futures via the described HJM approach, measure-valued processes also qualify for modeling quantities related to renewable energy production. In Section 6 we exemplify this briefly by considering wind energy markets.

Finally, let us remark that the setting of cylindrical measures considered in Assefa and Harms (2022) constitutes an interesting alternative approach to term structure modeling. In contrast to our framework there cylindrical measure-valued processes arising from SPDEs driven by some cylindrical Brownian motion are used to model the forwards. Note that being merely a cylindrical measure-valued process is a weaker requirement than being a measure-valued process. This weakening in turn allows to define SPDEs via cylindrical integrals, which would to be possible in the current measure-valued Markov process setup. One advantage of our approach is that we do not need Lipschitz conditions on the volatility function (imposed in Assefa and Harms (2022)), which is essential in order to accommodate affine and polynomial specifications. Another difference is that we consider concrete model specifications, in particular conditions that guarantee to stay in the state-space of non-negative measures, while the focus in Assefa and Harms (2022) lies rather on the abstract framework of cylindrical stochastic integration. Moreover, in the application to energy contracts, in Assefa and Harms (2022) the time of maturity parametrization (in contrast to the Musiela parametrization) is considered, which does not require to specify a HJM drift condition. Note that we could do this as well by specifying a measure-valued (local) martingale. The disadvantage of this approach is that – in order to keep the interpretation as forward process – the support of this measure-valued process should be and thus depends on the running time which is difficult to achieve. We therefore opted for the HJM approach with time to maturity where the support of the measure-valued process is constant over time.

The remainder of the paper is organized as follows: in Section 1.1 we introduce important notation used throughout the paper. Section 2 is dedicated to define the large financial market setting and the no-arbitrage condition NAFLVR. In Section 3 we establish the HJM approach for measure-valued processes and derive the corresponding drift condition, which then implies NAFLVR. In Section 4 we tackle existence of measure-valued diffusions satisfying the HJM-drift condition, while Section 5 is devoted to specify tractable examples of polynomial and affine type. In Section 5.3 we show how this can be exploited for pricing of options written on future contracts, while in Section 5.4 we present a calibration example based on a measure-valued neural affine process. Finally Section 6 sketches applications of measure-valued processes in wind energy markets.

1.1 Notation and basic definitions

Throughout this article, we denote by the compact interval for some finite time horizon and endow it with its Borel -algebra. Moreover, we shall use the following notation.

-

•

denotes the set of finite non-negative measures on , and the space of signed measures of the form with . We usually leave “non-negative” away and just say finite measures for . Both and are equipped with the topology of weak convergence, which turns into a Polish space. Recall that is locally compact since is compact (see, e.g. (Luther, 1970, Remark 1.2.3)). We denote its one-point compactification by and identify it with measures of infinite mass.

-

•

denotes the space of continuous real functions on equipped with the topology of uniform convergence. We denote by the supremum norm. Similary , , denote, respectively, the spaces of continuous, vanishing at infinity, and compactly supported real functions on .

-

•

For , denotes the restriction of -times continuously differentiable functions on , denoted by , to . Similary, is the restriction of smooth functions on , denoted by , to .

-

•

is the closed subspace of consisting of symmetric functions , i.e., for all , the permutation group of elements. For any we denote by the symmetric tensor product, given by

We emphasize that only symmetric tensor products are used in this paper.

-

•

Throughout the paper we let

be a dense linear subspace containing the constant function 1. We set . This generalizes to for .

Two key notions that we shall often use are the positive maximum principle, and the positive minimum principle for certain linear operators.

Definition 1.1.

Fix a Polish space and a subset . Moreover, let be a linear subspace of .

-

•

An operator with domain is said to satisfy the positive maximum principle on if

, , implies . -

•

An operator with domain is said to satisfy the positive minimum principle on if

Remark 1.2.

Note that the positive maximum principle implies the positive minimum principle. Indeed, let with and set (which is possible since is a linear space). Then the positive maximum principle yields .

Moreover, let be an operator with domain satisfying the positive minimum principle on and suppose that . Then for some map and some operator satisfying and the positive maximum principle on . and can be explicitly constructed by setting and .

These notions shall play an important role to establish existence of measure-valued diffusions. Indeed, the positive maximum principle (combined with conservativity) is essentially equivalent to the existence of an -valued solution to the martingale problem for , see (Ethier and Kurtz, 2005, Theorem 4.5.4). Here it is crucial that is locally compact. In our setting we shall apply this to which is locally compact.

The positive minimum principle will be used in the context of the HJM-drift condition. Note here that for generators of strongly continuous semigroups on the positive minimum principle is equivalent to generating a positive semigroup, if is compact, see (Arendt et al., 1986, Theorem B.II.1.6).

2 The large financial market and the no-arbitrage condition

Fix a finite time horizon and let be a filtered probability space, with an increasing and right-continuous filtration . We suppose that the basic traded instruments in our market consist of

-

•

a continuum of future contracts with delivery period over a time interval with , whose prices at time are denoted by , i.e.

are the traded energy products;

-

•

a bank account corresponding to a constant risk-free rate and chosen to be the numéraire.

Observe that due to the chosen risk-free rate the involved quantities are already discounted. As a next step we now introduce conditions guaranteeing absence of arbitrage. Due to the large financial market nature, we consider the no-arbitrage condition no asymptotic free lunch with vanishing risk (NAFLVR) introduced in Cuchiero et al. (2016b).222Observe that the current setup can be embedded in Example 2.2 in Cuchiero et al. (2016b) by considering an index set for the delivery periods from to . In words, (NAFLVR) requires that there is no sequence of terminal payoffs of so-called admissible generalized strategies that

-

•

converges almost surely to a non-negative random variable which is strictly positive with positive probability,

-

•

while their negative parts tend to 0 in .

The fundamental theorem of asset pricing in this context then asserts that NAFLVR is equivalent to the existence of a so-called equivalent separating measure ; see (Cuchiero et al., 2016b, Theorem 3.2). In the case where all are locally bounded processes, equivalent separating measures correspond to equivalent local martingale measures. As we shall deal with continuous processes, we therefore have the following assumption.

Assumption 2.1 (NAFLVR).

There exists an equivalent measure such that all elements in are local martingales.

3 A Heath-Jarrow-Morton approach for measure-valued processes

In this section we adapt the Heath-Jarrow-Morton (HJM) approach (see Heath et al. (1992)) to the current measure-valued setting which will in turn guarantee NAFLVR.

We start by briefly summarizing the classical HJM approach in a function-valued setup, usually in some Hilbert space, to model forward prices; see e.g. Benth and Krühner (2014). Recall that stands for the price at time of an instantaneous forward contract with delivery exactly at time with . Then, as outlined in the introduction, future prices are given by (1.1). Hence, to guarantee Assumption 2.1 it suffices to assume

with some (function-valued local) martingale under some equivalent measure . Supposing sufficient regularity of and passing to the Musiela parametrization via

the (local) martingale condition translates to the SPDE

| (3.1) |

where and hence is again a (function-valued local)-martingale.

Since the forwards cannot be traded and stochastic discontinuities in the spot prices give rise to measure-valued forward prices as explained in the introduction, the goal is now to replace the function-valued process by a measure-valued one supported on . This means to model future prices as

| (3.2) |

instead of (1.1). Recall that by our delivery convention just the right boundary point is included in the integration domain. We shall also suppose that .

As a first step let us introduce two functions sets. For functions of two variables we denote by the first argument and by the second one. We thus use and accordingly. The two sets are

| (3.3) | ||||

which correspond to -functions with vanishing -derivative at .

We are now ready to provide sufficient conditions on guaranteeing NAFLVR in sense of Assumption 2.1. The result is based on the measure-valued formulation of the HJM drift condition (3.1), given in (3.5). To see the analogy, observe that by integration by parts for each the martingale introduced in (3.1) satisfies

Theorem 3.1.

Proof.

We prove that are -martingales (instead of only local martingales). Note first that by the definition in (3.2)

for all . We now aim to apply Lemma A.1. Let be a bounded sequence of functions approximating pointwise such that for each . Define

Note that and

as and for all . This shows that . Moreover, for all . Therefore we have for all

and Lemma A.1 thus implies the martingale property of . By dominated convergence converges to and

which is integrable with respect to . Putting this together yields

whence the martingale property of under . ∎

Remark 3.2.

Remark 3.3.

In the setup considered so far the spot price did not play role. We here discuss how it can be deduced in the current framework. Fix some and denote the spot price by . Note that in accordance with (Benth et al., 2008, Chapter 4), would correspond to

Using the above weight function this yields

By the Lebesgue differentiation theorem this limit is well-defined if the measure given by is absolutely continuous with respect to the Lebesgue measure around . Since this is not necessarily satisfied, we can alternatively consider the following definition. As the spot price corresponds in reality to a delivery over one of the next hours, we can fix some and define via

Remark 3.4.

Observe that given a -valued martingale the -valued process obtained via

satisfies the HJM drift’s condition (3.5). This observation is interesting since it permits to conclude that

Since we can even get that

We explain now how (3.5) can be relaxed without compromising the results of Theorem 3.1. We also illustrate that these changes just affect the dynamics of the mass that puts in , which does not play a role for (3.2).

Remark 3.5.

Suppose now that (3.5) is replaced by

| (3.6) |

being a -local martingale on for all for some . The extra term regulates the amount of extra mass that can disappear () or appear () from the set . Observe indeed that if satisfies (3.5) then the -valued process

satisfies (3.6) for

Indeed, by the product formula we have

where the last equality follows since . As for , this implies

proving the claim.

Remark 3.6.

Note that it is in principle also possible to consider a discrete set of times to maturity, e.g. in the simplest case combined with a discrete time setup with . Then the measure-valued process becomes actually a discrete time stochastic process with values in and can be identified with the scalar product on , meaning that .

Set , assume that is a process in with non-negative components, , and

| (3.7) |

is a local martingale444Note that, as in the continuous case, with the requested integrability condition local martingality implies martingality. on for each . Then the (discounted) price of the future

is a martingale on for each .

This result can be shown following the proof of Theorem 3.1. In particular, let be the local martingale given by (3.7) and note that

for each . The summation by parts formula yields

and by reordering the terms and noting that is a local martingale on we get

Proceeding as in Lemma A.1 we can then show that for every the process

is a true martingale on . Since setting it holds

proceeding as in the proof of Theorem 3.1 we can conclude that is a martingale too.

4 Measure-valued diffusions satisfying the HJM condition

So far we implicitly assumed the existence of a non-negative measure-valued process satisfying the HJM-drift condition (3.5). To analyze when this non-negativity together with (3.5) holds true, we consider a Markovian setting where the process can be described by its (extended) generator. To this end we need to introduce spaces of functions on which these operators act. These are cylindrical functions and polynomials with certain regularity properties.

4.1 Cylindrical functions and polynomials

Recall that is a dense linear subspace containing the constant function 1. The set of cylindrical functions we consider are maps from to lying in

We shall denote the restriction of to by

Moreover, since elements in are not necessarily compactly supported we also define the following sets

| (4.1) |

These sets will serve as domain for the linear operators that we introduce subsequently.

Similarly to cylindrical functions, we also consider cylindrical polynomials. To this end denote by the set of polynomials on . We then call a map cylindrical polynomial if it lies in the set

Note that consists of all (finite) linear combinations of the constant polynomial and “rank-one” monomials with . Analogously to cylindrical functions we write for the restriction of to .

4.2 Directional derivatives

In order to be able to consider certain differential operators acting on functions with measure arguments, we need to introduce the notion of derivatives. We shall throughout apply directional derivatives. More precisely, a function is called differentiable at in direction for if

exists. We write for the map , and we use the notation

for iterated derivatives. We write for the corresponding map from to .

Remark 4.1.

Note for all functions in and , it holds . In particular, setting and we get

4.3 Diffusion-type operators and martingale problems

We shall consider here diffusion type operators that correspond to second-order differential operators, precisely introduced in the next definition. As domain we consider a generic set . Later on will be given by as defined in (4.1) but also by other sets which are more convenient in the polynomial setting (see Section 5).

Definition 4.2.

A linear operator is called diffusion-type operator if it admits a representation

| (4.2) |

for some operators and such that and are linear for all .

To such operators we can then associate measure-valued processes via the martingale problem.

Let be a linear operator acting on and being of form (4.2). A -valued process with continuous trajectories defined on some filtered probability space 555We here consider directly a risk neutral measure because we are interested when (3.5) is a martingale under . is called a -valued solution to the martingale problem for with initial condition if -a.s. and

| (4.3) |

defines a local martingale for every in the domain of . Uniqueness of solutions to the martingale problem is always understood in the sense of law. The martingale problem for is well–posed if for every initial condition there exists a unique -valued solution to the martingale problem for with initial condition .

4.4 Existence of measure-valued diffusions satisfying the HJM drift-condition

We are now concerned with proving existence of -valued-solution to such types of martingale problems. The following theorem provides sufficient conditions. For its formulation recall the space of as defined in (4.1) and the definition of given in (3.3).

Theorem 4.3.

Let be a linear operator of form (4.2) for some such that for all . Suppose that the drift part is given by

| (4.4) |

If the diffusion part satisfies the positive maximum principle on , i.e.

then there exists a -valued solution to the martingale problem for which satisfies the HJM-drift condition (3.5).

Proof.

We verify now that the conditions of Lemma B.1 are satisfied. First note that is a dense subset of which contains and

lies in for all . Moreover, note that

whence (B.1) is satisfied. Since satisfies the positive maximum principle by assumption, it remains to prove that does it as well. By (Cuchiero et al., 2021, Theorem 3.1) we know that for each such that

it holds for each with equality for . Since this in particular implies that has a maximum over in for each and thus for each and . Since we also know that its derivative vanishes in 0 and thus

what we needed to prove.

∎

Remark 4.4.

If condition (3.5) is replaced by (3.6) as outlined in Remark 3.5, then condition (4.4) translates to

| (4.5) |

Note however that is not continuous in general, since is not continuous. This could be recovered by restricting to maps vanishing in 0, but this new set is not dense in . To overcome the technical problems introduced by the lack of density we would need to slightly adapt all our technical results (in particular Lemma B.1) replacing with . For seek of exposition we will not deepen this direction any further.

Note that for the drift operator is the generator of the probability measure-valued process which describes the “law” of the deterministic spatial motion , absorbed at due the definition of . Adding to , which amounts to consider the operator given in (4.5), can be interpreted as adding a killing term to the spatial motion, meaning that the particles are killed at rate after being absorbed at . Indeed, in this case the generator of the spatial motion is given by

Remark 4.5.

Note that in order to apply Theorem 3.1, the solution to the martingale problem provided by Theorem 4.3 additionally needs to satisfy (3.4), namely

By the HJM-drift condition we know that is a local martingale. The BDG inequalities then yield

If is a true martingale, then we can also apply Doob’s -martingale inequality to get

Remark 4.6.

In the discrete time setup of Remark 3.6 choosing we can see that for each condition (3.7) yields

As a result the valued increments of can be described via

where denotes a martingale increment and is given by

The process corresponding to (3.8) for is similar only with instead of . In both cases the matrix corresponds to the generator matrix of the spatial motion. In the first case it describes (deterministic) downward jumps by being absorbed at , while in the second case the absorption at is followed by a killing with rate .

5 Tractable examples of affine and polynomial type

This section is dedicated to tractable examples of polynomial and affine type that satisfy the conditions of Theorem 4.3. For these specifications the moments as well as the Laplace transform (in the affine case) can be computed explicitly by solving a system of linear PDEs or Riccati PDEs respectively. Throughout we shall implicitly work under , but do not always indicate this in the expected values.

We start by providing the definition and a characterization result of polynomial operators given in Cuchiero et al. (2021). Their domain is always given by

| (5.1) |

instead of as in previous sections.

To define polynomial operators we need to introduce the notion of polynomials on . A polynomial of degree on is given by i.e.

for some coefficients with , where

The set of all polynomials is denoted by . Recall also the notion of cylindrical polynomials as introduced in Section 4.1. Note in particular that setting we get , showing that .

Definition 5.1.

A linear operator is called -polynomial if it maps to such that for every there is some whose degree is smaller or equal the degree of and .

The form of these operators in a diffusion setup can be characterized completely. For the proof of a corresponding statement see Theorem 4.6 in Cuchiero et al. (2021).

Theorem 5.2.

A linear operator is -polynomial and of diffusion-type if and only if admits a representation

| (5.2) | ||||

for some linear operators , , , , . These operators are uniquely determined by .

We now combine Theorem 4.3 with one of the main results of Cuchiero et al. (2021), which gives sufficient conditions for the existence of solutions to the martingale problem for polynomial operators. To state the result we first need the following definition.

Definition 5.3.

We say that a linear operator admits a -representation if

where

-

•

is a symmetric function such that for all ;

-

•

is a non-negative function such that for all ;

-

•

for all , , , the matrix

(5.3) where with entries ;

-

•

the map lies in for all .

Accordingly, sufficient conditions for the existence of the martingale problem such that additionally the HJM-condition (3.5) is satisfied can now be formulated as follows. Note that here the local martingale condition (4.3) holds for all with defined in (5.1).

Theorem 5.4.

Let and 666Note that enters in the definition of given by (5.1). be a linear operator of form (5.2), where

-

(i)

;

-

(ii)

;

-

(iii)

;

-

(iv)

is of the form

where with values in ;

-

(v)

admits a ()-representation.

Then is -polynomial and for every initial condition its martingale problem has a -valued solution that has continuous paths and satisfies the HJM-drift condition (3.5). Moreover, condition (3.4) holds.

The immediate consequence of this theorem and Theorem 3.1 is given in the following corollary.

Corollary 5.5.

Proof of Theorem 5.4.

The existence’s result follows by Theorem 5.9 in Cuchiero et al. (2021), of which we check now the conditions. Observe that for each , such that it holds

where the last property follows by definition of . This implies that , hence that satisfies the positive minimum principle on , and by Theorem 5.9 in Cuchiero et al. (2021) we can conclude that is -polynomial and for every initial condition its martingale problem has a -valued solution. Since for we have and , the HJM-drift condition (3.5) follows by the martingale problem.

As a next step, we are now interested in the so-called moment formula to get explicit expressions for the moments. Before stating it we need to associate to an -polynomial operator a family of so-called dual operators . These operators are linear operators mapping the coefficients vector of a polynomial of the form to the coefficients vector of . To introduce the dual operator, we now recall Definition 2.3 of Cuchiero and Svaluto-Ferro (2021).

Definition 5.6.

Fix and let be an -polynomial operator. The -th dual operator corresponding to is a linear operator such that satisfies

where . Whenever is a closable operator777We refer to (Ethier and Kurtz, 2005, Chapter 1) for the precise definition., we still denote its closure by and its domain by .

Remark 5.7.

If satisfies the conditions of Theorem 5.4, then the -th dual operator when applied to is of the form

| (5.4) |

Identifying with , we write here by a slight abuse of notation instead of . Note that applied to general is not for . Note also that .

Let satisfy the conditions of Theorem 5.4. Fix , and let be the closable -th dual operator corresponding to with domain . Before stating the moment formula in the current context, we extend the domain of to polynomials with coefficients in by setting

for all and . We here used that . As stated below, the moment formula corresponds to a solution of a system of linear PDEs. Note that in contrast to Cuchiero et al. (2021) we shall call these differential equations PDEs since the underlying space is here always . In the next definition we recall the precise solution concept.

Definition 5.8.

Let be given by (5.4). We call a function with values in a solution of the dimensional system of PDEs

if for every it holds

| (5.5) |

for all .

Remark 5.9.

Note that this solution concept reduces to a more classical one if we take with , and . Indeed, by polarization (5.5) can be transformed into

and thus reduces to a classical (except of the integral form) solution of a multivariate PDE.

Theorem 5.10 (Dual moment formula).

Let satisfy the conditions of Theorem 5.4. Fix , let be the -th dual operator corresponding to as of Remark 5.7, and assume that is closable with domain . Fix a coefficients vector and suppose that the following condition holds true.

-

•

There is a solution in the sense of Definition 5.8 of the dimensional system of linear ODEs on given by

(5.6)

Then, for any solution to the martingale problem for and all the representation

| (5.7) |

holds almost surely.

Remark 5.11.

Let us remark that the current setup can also be generalized to time-inhomogenous measure-valued polynomial processes which have been considered in finite dimensions in Agoitia Hurtado and Schmidt (2020) (see also Filipović (2005) for the affine case). This then allows in particular to incorporate seasonalities in a tractable manner.

Example 5.12.

Since and the corresponding system of PDEs reads

Choosing and , we see that the corresponding solution is given by . From the moment formula we can thus conclude that

where . Setting and , we obtain is supported on . This implies that for each such that and thus that is almost surely supported on , which is also in line with Remark 3.4.

Note, that since we only consider , does not play a role for this result. This in particular implies that this representations holds for any process satisfying the assumption of Theorem 3.1.

In the following sections we shall give important examples when the system of linear ODEs (5.6) has a solution in the sense of Definition 5.8. Recall that in this case the moment formula can be applied.

5.1 Black-Scholes type measure-valued HJM-models

We start by considering the case where the diffusion part corresponds to an analog of a multivariate Black-Scholes model.

Definition 5.13.

A Black-Scholes type measure-valued HJM-model is the solution to the martingale problem for some for some admitting the representation

for each , , where admits a ()-representation for some bounded and continuous on .

Observe that the operator corresponding to a Black-Scholes type measure-valued HJM-model satisfies the conditions of Theorem 5.4 for and as in the definition.

Proposition 5.14.

Let be a Black-Scholes type measure-valued HJM-model. Then the moment formula (5.7) holds true.

Proof.

Let be the -th dual operator corresponding to . Note that when applying it to with , we have

| (5.8) |

where we write here by a slight abuse of notation, similarly as in Remark 5.7, instead of .

Observe now that generates the strongly continuous contraction shift semigroup on given by

for each . Moreover, by the form of the closure of the operator is a bounded operator on . By (Ethier and Kurtz, 2005, Corollary 1.7.2), therefore generates a strongly continuous semigroup on which is additionally positive since (and also ) satisfies the positive minimum principle (see the end of Section 1.1). Denote now, for every , the strongly continuous positive semigroup corresponding to by which acts on . Then, by the definition of this semigroup

satisfies (5.6) for any initial value . Hence, the moment formula (5.7) holds true. ∎

Remark 5.15.

Observe that for each it holds

where and

for . Observe that is the generator of the -valued process that can be described as follows. Each component of can jump to the position of one of the other components. The stochastic intensity for a jump of the -th component to the position of the -th one is given by . Between two jumps each component of decreases linearly with slope -1. Since the derivative of each test function vanishes at 0 we can require the process to be absorbed in 0. This means that given two consecutive jump times it holds

Following a Feynman-Kac type of argument one can then show that the PDE

corresponding to is solved by

By the moment formula we can thus conclude that

for each .

Remark 5.16.

The choice in the -representation of can be seen as measure-valued analog of the quadratic variation structure of a multivariate Black-Scholes model. This was also the inspiration for the name of the whole model class introduced in Definition 5.13. Observe that the form of then simplifies to

| (5.9) |

Note that in this case the function has to be a positive semi-definite kernel to guarantee that (5.3) is satisfied. It can then be interpreted as the covariance structure between the maturities. To see this, we compute the carré du champ operator associated with , which is defined as the following symmetric bilinear map

This operator then yields a formula for the quadratic variation process of the martingale given by (4.3). Indeed, denote the quadratic variation process of by . Then, e.g. by adapting (Revuz and Yor, 1999, Proposition VIII.3.3) to the current setting we have

| (5.10) |

where denotes the solution to the martingale problem for as of (5.9). A straightforward calculation then yields for of the form with for some ,

Hence,

| (5.11) |

Comparing this with the classical form of a multivariate Black-Scholes model of dimension

where , is a -dimensional Brownian motion and where we deliberately do not specify the drift part, we see e.g. by Ito’s formula or (5.10) applied to the current situation that the quadratic variation of

is given by

This is exactly the same form as (5.11), which can be seen by setting , identifying with , inserting , noticing that takes the role of and replacing by .

5.2 Affine measure-valued HJM-models

Another tractable subclass of polynomial processes are affine type models, corresponding to Dawson-Watanabe-type superprocesses. There the focus will lie on the expression of the Laplace transform given in terms of one-dimensional non-linear PDEs of Riccati type. For this affine subclass it will turn out that . To introduce these models, we first recall the definition of affine type operators in sense of Definition 6.1 in Cuchiero et al. (2021). Such definition is inspired by the classical form of the infinitesimal generator of affine processes on finite dimensional state spaces, see, e.g., Kawazu and Watanabe (1971); Duffie et al. (2003); Cuchiero et al. (2011, 2016a). Again, recall that the set is given by

Definition 5.17.

We say that a linear operator is of affine type on if there exist maps and such that

for all and , where denotes all function in with values in .

The following theorem now gives the precise form of affine type operators such that the HJM-condition is satisfied (3.5). It also states the well-posedness of the associated martingale problem with unique solution and the exponential linear form of its Laplace transform which can be computed by solving a Riccati PDE. In its formulation we use the notation .

Theorem 5.18.

Let and be the linear operator of form (5.2) given by

| (5.12) |

for some taking values in . Then is of affine type, its martingale problem is well-posed and the -valued solution has continuous paths, satisfies the HJM-drift condition (3.5). Moreover, the market corresponding to satisfies NAFLVR in the sense of Assumption 2.1. Finally, the Riccati PDE

admits the -valued solution

and for all the conditional Laplace transform has almost surely the following representation

| (5.13) |

Proof.

A direct computation yields that is of affine type with and

for each . Existence of solutions to the martingale problem and all related assertions follow from Theorem 5.4 and the subsequent corollary. Uniqueness is a consequence of (Cuchiero et al., 2021, Corollary 6.9) by noticing that is the generator of a strongly continuous positive semigroup, namely the negative shift semigroup given by . Finally, a direct computation using that shows that is a -valued solution of the Riccati PDE. Since and we can conclude that it is also a solution in sense of Definition 6.4 in Cuchiero et al. (2021) and the form of the Laplace transform follows from Theorem 6.6 in same paper. ∎

Remark 5.19.

Notice that the operator defined in (5.12) is a variant of the Dawson-Watanabe superprocess (in the terminology of Etheridge (2000)888Note that in Li (2010) “Dawson-Watanabe superprocess” is used for a class of measure-valued branching processes which can also exhibit jumps.), also called super-Brownian motion, where the constant diffusion coefficient is replaced by a function and where the spatial motion is governed by the negative shift semigroup. It can thus be seen as measure-valued analog of one-dimensional Cox-Ingersoll-Ross processes.

5.3 Option pricing

We now investigate option pricing in the two model classes considered above. We focus on European-style options on future contracts with payoff function and exercise time . Classical examples are standard call and put options with strike price , for which the payoff function is defined by , respectively by . Computing the price of such an option at time then amounts to calculate

| (5.14) |

under some equivalent (local) martingale measure (compare e.g. Benth et al. (2008) or Benth et al. (2021b)). We here shall suppose that is given by

as in (3.2), with being either a Black-Scholes type or affine measure-valued HJM-model under .

5.3.1 Option pricing in Black-Scholes type measure-valued HJM-models

As shown in Proposition 5.14 all assumptions such that the moment formula holds true are satisfied if is a Black-Scholes type measure-valued HJM model. This can then be exploited to use polynomial techniques to compute (5.14). The simplest one is a variance reduction technique for Monte Carlo pricing. In this case one approximates the true payoff via a polynomial (e.g. in the uniform norm on some interval) and then computes an estimator for the price (here for ) via

for some constant . By choosing optimally namely as

the variance with respect to the usual Monte Carlo estimator corresponding to the case is reduced by the factor . Suppose now that for coefficients and hence

As in the proof of Theorem 3.1, let be a bounded sequence of functions approximating pointwise such that for each . Then since by (Cuchiero et al., 2021, Lemma 5.7) all moments are finite, we have by dominated convergence

As is a Black-Scholes type measure-valued HJM-model this expected value can then be computed by solving

where is given by (5.8) and

Alternatively to this variance reduction technique option pricing methods that build on orthogonal polynomial expansions as in Ackerer and Filipović (2020) can be applied.

5.3.2 Option pricing in affine measure-valued HJM-models

Let us now turn our attention to affine measure-valued HJM-models. In this case the Laplace transform is explicitly known once the associated Riccati-PDE is solved. Since this can be transferred to the Fourier-transform, Fourier option pricing methods (see e.g. Carr and Madan (1999)) that are often applied for standard finite dimensional affine processes also come into play in this measure-valued situation.

Suppose can be expressed by

| (5.15) |

for some integrable function and some constant . If, moreover

| (5.16) |

then (5.14) for can be expressed as

| (5.17) |

As above let us consider a bounded sequence of smooth functions approximating . Then (5.17) becomes

where the second equality follows due to (5.16) from dominated convergence and the third is a consequence of (5.13) extended to the Fourier-Laplace transform (see Remark 5.20 below). Here solves the Riccati PDE with initial condition Its value at time is thus given by

For this expression simplifies to

| (5.18) |

where is the primitive of .

Remark 5.20.

5.4 Calibration to market option prices

The above pricing methods clearly offer tractable calibration procedures, where the function-valued characteristics of the polynomial models can be calibrated to match the market option prices.

Indeed, the goal is to parametrize these functions as neural networks to get neural measure-valued processes, an analog to neural SDEs and SPDEs (see e.g. Gierjatowicz et al. (2020); Cuchiero et al. (2020); Salvi et al. (2021)). Note that we could of course also parametrize the map for , corresponding to the diffusion part in (4.2) via neural networks taking measures as inputs. We refer to Benth et al. (2021a); Acciaio et al. (2022); Cuchiero et al. (2022b) for neural networks with infinite dimensional inputs (and also outputs).

By considering the polynomial class the modeling simplifies to standard neural networks that parameterize the function-valued characteristics. While tractability is preserved, this leads to potentially highly parametric infinite dimensional stochastic models which have a great potential to capture multifarious features of energy markets. Parameter optimization can be performed efficiently due to stochastic gradient descent methods and tractable backpropagation schemes.

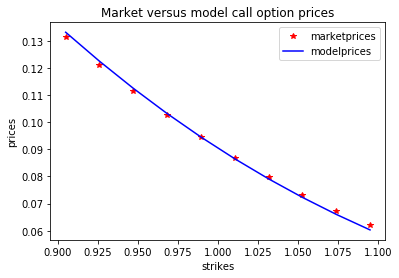

We shall now exemplify this by means of an affine measure-valued HJM model whose generator is given by (5.12) with being parameterized by a non-negative neural network. We here do not aim to perform a full calibration to all available option price data, but just show a proof of concept by calibrating the model to call option prices for one specific maturity and one delivery period (i.e. one slice of the volatility surface (or cube)).

We use EEX German Power data extracted from

| https://www.eex.com/en/market-data/power/options |

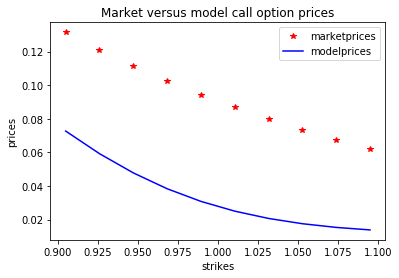

at March 22, 2022 and calibrate to call options with maturity April 26, 2022 and delivery period one month, starting on May 1, 2022. As our goal is to provide just a calibration example, we use a simple -criterion for minimizing the distance between the market call option prices and the respective model prices, i.e. we minimize

| (5.20) |

where denotes the market call option price with strike and the model call option price obtained via Fourier pricing as explained in Example 5.21 for

The day ahead forward price on March 22, 2022 is 236.49 and we normalize all prices by this quantity to start with . We then deal with 10 market strikes ranging from to and 71 daily values of the initial forward curve, encoded in , from March 22, 2022 to May 31, 2022. The corresponding and are thus approximately given by and . The integral with respect to in (5.19) is computed by discretization from to . The function is parameterized by a layer neural network with activation functions for the first layer and relu for the two outer layers.

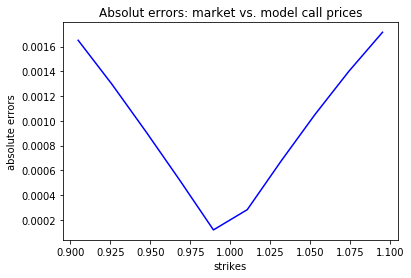

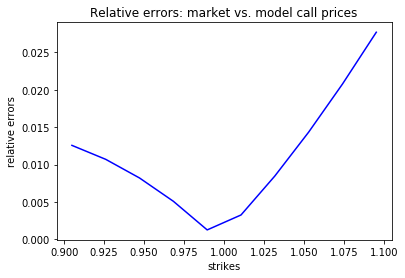

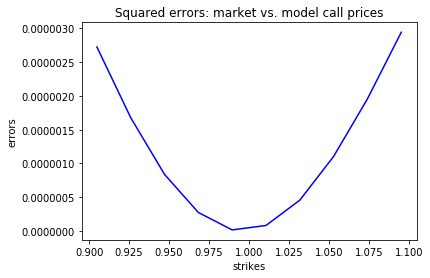

Computing then (5.20) yields the calibration results illustrated in Figure 1. Absolute, relative errors and also squared errors are shown in Figure 2. Note that the calibration is extremely accurate for the at the money options. The mean absolute error (over all strikes) is 0.00096, the mean relative error 0.011 and the mean squared error . When the parameters of the neural networks are appropriately initialized, then training is very fast (some seconds on a standard laptop), but the initialization is quite crucial in order to start in regimes where the model prices are not too far from the the market prices. In Figure 3, we show how the curves looked at the start of the training. The target curve can then be reached in around 150-300 gradient step iterations with a learning rate of 0.01.

As mentioned in Remark 5.11 the model can be easily extended by making the function-valued characteristics time-dependent, which then does not only allow to capture seasonality features but also to adapt the current calibration procedure to a slicewise calibration as conducted in Cuchiero et al. (2020); Gierjatowicz et al. (2020); Cuchiero et al. (2022a), leading to similarly accurate calibration results for all maturities.

6 Measure-valued processes for renewable energy production

In this section we give a brief outlook how measure-valued processes could be used to model renewable energy production. We outline this by means of the example of wind energy markets. We briefly introduce some characteristics of this market relying on Benth et al. (2018).

The production of wind energy has played an increasingly important role as a renewable energy source. This type of energy can be generated only in the presence of a suitable amount of wind: a minimum wind’s speed is required and too strong wind would cause damages. A direct law relating the maximal power production from a wind power plant to the wind speed is Betz’s law. If one introduces as the minimum wind speed which allows for production and as the maximum one, Betz’s law expresses the upper bound of wind power production in terms of the wind speed at time as

| (6.1) |

where is a positive constant describing the heat rate, being a real positive constant measuring the efficiency of the plant (see Benth et al. (2018) for further details). It can happen that the wind is too strong so that the company faces a surplus of production that must be sold in the market. This can in turn trigger a decrease of related electricity prices. Hence it becomes essential for an energy producer to hedge against these risks. In energy markets there exist weather derivatives that have been designed to cover such kinds of exposure. A particular class of contracts are so-called quanto options that simultaneously take into account the power production driven by the wind speed, as well as the electricity price. In order to price such contracts, one thus has to specify dynamics for both the electricity price and the wind speed. According to Benth et al. (2018), a typical payoff of a quanto option is the product of two put options written on the one hand on electricity futures and on the other hand on the future cumulative gap between the theoretical total maximum production and the actual wind power production . The price of such a quanto option can thus be written as

where is a future on electricity as in the previous sections, is the described payoff related to the wind power production given by

| (6.2) |

and are the respective strike values. Note that, when fixing and in (6.1), (6.2) describes the gap between the maximal wind power production and the actual one.

We now outline a possible method to exploit measure-valued processes for modeling wind energy markets. Suppose that for each time and each location the wind’s speed for the time period is known at time . Let be a measure-valued process on and interpret as the normalized distribution of the wind speed at the geographical location over 24 hours starting at time . For example, if at day the forecasts for the next 24 hours predict a constant wind of speed at location we set .

Assuming that the wind power production over 24 hours of a unit located in is a deterministic function of the wind speed and the location of the unit, then we can express the average wind’s power’s production at time by

According to Betz’s law this quantity is bounded by . Letting be the distribution of power plants’ units on the territory, (6.2) then becomes

One possibility would then be to model directly with a measure-valued model. By adding a further component to the underlying space one can then simultaneously model also the electricity futures via the measure-valued approach. Similar tractable methods as those studied in the previous sections can therefore be used to price quanto options.

Appendix A Auxiliary results

The following lemma is a key result for the proof of Theorem 3.1.

Lemma A.1.

Let be a -valued process such that and such that for all

| (A.1) |

is a local martingale on . Then for all

| (A.2) |

is a martingale on .

Proof.

We first prove the assertions for functions of the form with and . Denote by the process

which is a local martingale by (A.1). Then by the Itô’s product rule, we have

| (A.3) |

Note then that it holds

where denotes some constant and where the last inequality follows from the fact that and . Since the last expression is finite by assumption, we can conclude that is a true martingale. Since

the martingale condition for (A.2) in for follows from (A.3).

Next, note that the set of functions forms a point-separating algebra that vanishes nowhere, and which has additionally the property that for all and such that there exists some with . By an adaptation of Nachbin’s version of the Stone-Weierstrass theorem (see Nachbin (1949)) that it is dense in with respect to the -norm

Consider now a sequence converging in the -norm to . Observe that this in particular implies . Denote then by the true martingale

and by the corresponding right hand side without . By dominated convergence we know that for all almost surely and

which is an integrable random variable. By the dominated convergence theorem we thus get

and for each . This implies that and thus (A.2) is a true martingale showing the claim. ∎

Appendix B Existence for martingale problems

The next lemma is an adaptation of a well-known result from Ethier and Kurtz (2005) giving sufficient conditions for the existence of a solution to the martingale problem for a linear operator . Here, it is crucial that acts of -functions on a locally compact, separable, metrizable space, which is satisfied for since is a compact set. For the formulation of the lemma recall the set of functions defined in (4.1).

Lemma B.1.

Suppose that is of form (4.2) for some such that

| (B.1) |

for some constant . Assume furthermore that satisfies the positive maximum principle on . Then for every initial condition in , there exists a continuous -valued solution to the martingale problem for . Moreover, for

defines a local martingale.

Proof.

The proof is similar to the proof of (Cuchiero et al., 2021, Lemma B.2(i)), but we state it here for completeness. We shall verify the conditions of (Ethier and Kurtz, 2005, Theorem 4.5.4). As already mentioned, is a locally compact, separable and metrizable space. Moreover, by (Cuchiero et al., 2021, Lemma 2.6), we have that as defined in (4.1) is a dense subset of . Moreover, the positive maximum principle yields that for all such that . Since by assumption we may regard as an operator on . This means that all the assumptions of in (Ethier and Kurtz, 2005, Theorem 4.5.4) are satisfied. Recall from Section 1.1 that denotes the one-point compactification of and define according to the same theorem the linear operator on by

for all such that .

Then (Ethier and Kurtz, 2005, Theorem 4.5.4) yields that for every initial condition in , there exists a solution to the martingale problem for with càdlàg sample paths taking values in . Indeed, we obtain that (4.3) is a bounded local martingale (and thus a true martingale) for each where is replaced by . Moreover, by Proposition 2 in Bakry and Émery (1985) we also know that is continuous for each .

Fix now , define and set . We now aim to show that for all we have that , showing that . Fix and consider a map such that for . Set and . By continuity of , we already know that

for each . Observe then that and for each such that . This implies together with linearity of in its first argument that

which is a local martingale. Since it is also bounded due to to condition (B.1), we can conclude that it is a true martingale.

Fatou’s lemma then yields

By the Gronwall inequality we can thus conclude that

and hence that . This proves that every solution to the martingale problem takes values in and hence the assertion.

∎

References

- Acciaio et al. (2022) B. Acciaio, A. Kratsios, and G. Pammer. Metric hypertransformers are universal adapted maps. Preprint, arXiv:2201.13094, 2022.

- Ackerer and Filipović (2020) D. Ackerer and D. Filipović. Option pricing with orthogonal polynomial expansions. Mathematical Finance, 30(1):47–84, 2020.

- Agoitia Hurtado and Schmidt (2020) M. F. D. C. Agoitia Hurtado and T. Schmidt. Time-inhomogeneous polynomial processes. Stochastic Analysis and Applications, 38(3):527–564, 2020.

- Arendt et al. (1986) W. Arendt, A. Grabosch, G. Greiner, U. Moustakas, R. Nagel, U. Schlotterbeck, U. Groh, H. P. Lotz, and F. Neubrander. One-parameter semigroups of positive operators, volume 1184. Springer, 1986.

- Assefa and Harms (2022) J. Assefa and P. Harms. Cylindrical stochastic integration. Preprint, arXiv:2208.03939, 2022.

- Bakry and Émery (1985) D. Bakry and M. Émery. Diffusions hypercontractives. In Seminaire de probabilités XIX 1983/84, pages 177–206. Springer, 1985.

- Benth and Krühner (2014) F. E. Benth and P. Krühner. Representation of infinite-dimensional forward price models in commodity markets. Communications in Mathematics and Statistics, 2(1):47–106, 2014.

- Benth et al. (2008) F. E. Benth, J. S. Benth, and S. Koekebakker. Stochastic modelling of electricity and related markets, volume 11. World Scientific, 2008.

- Benth et al. (2018) F. E. Benth, L. Di Persio, and S. Lavagnini. Stochastic modeling of wind derivatives in energy markets. Risks, 6(2):56, 2018.

- Benth et al. (2021a) F. E. Benth, N. Detering, and L. Galimberti. Neural Networks in Fréchet spaces. Preprint, arXiv:2109.13512, 2021a.

- Benth et al. (2021b) F. E. Benth, N. Detering, and S. Lavagnini. Accuracy of deep learning in calibrating HJM forward curves. Digital Finance, pages 1–40, 2021b.

- Carr and Madan (1999) P. Carr and D. Madan. Option valuation using the fast Fourier transform. Journal of computational finance, 2(4):61–73, 1999.

- Cuchiero and Svaluto-Ferro (2021) C. Cuchiero and S. Svaluto-Ferro. Infinite-dimensional polynomial processes. Finance and Stochastics, 25(2):383–426, 2021.

- Cuchiero et al. (2011) C. Cuchiero, D. Filipović, E. Mayerhofer, and J. Teichmann. Affine processes on positive semidefinite matrices. The Annals of Applied Probability, 21(2):397–463, 2011.

- Cuchiero et al. (2012) C. Cuchiero, M. Keller-Ressel, and J. Teichmann. Polynomial processes and their applications to mathematical finance. Finance and Stochastics, 16(4):711–740, 2012.

- Cuchiero et al. (2016a) C. Cuchiero, M. Keller-Ressel, E. Mayerhofer, and J. Teichmann. Affine processes on symmetric cones. Journal of Theoretical Probability, 29(2):359–422, 2016a.

- Cuchiero et al. (2016b) C. Cuchiero, I. Klein, and J. Teichmann. A new perspective on the fundamental theorem of asset pricing for large financial markets. Theory of Probability & Its Applications, 60(4):561–579, 2016b.

- Cuchiero et al. (2020) C. Cuchiero, W. Khosrawi, and J. Teichmann. A generative adversarial network approach to calibration of local stochastic volatility models. Risks, 8(4):101, 2020.

- Cuchiero et al. (2021) C. Cuchiero, L. Di Persio, F. Guida, and S. Svaluto-Ferro. Measure-valued affine and polynomial diffusions. Preprint, arXiv:2112.15129, 2021.

- Cuchiero et al. (2022a) C. Cuchiero, G. Gazzani, and S. Svaluto-Ferro. Signature-based models: theory and calibration. Preprint, arXiv:2207.13136, 2022a.

- Cuchiero et al. (2022b) C. Cuchiero, P. Schmocker, and J. Teichmann. Universal approximation of path space functionals. Working paper, 2022b.

- Duffie et al. (2003) D. Duffie, D. Filipović, and W. Schachermayer. Affine processes and applications in finance. The Annals of Applied Probability, 13(3):984–1053, 2003.

- Etheridge (2000) A. Etheridge. An introduction to superprocesses, volume 20 of University Lecture Series. American Mathematical Soc., 2000.

- Ethier and Kurtz (2005) S. N. Ethier and T. G. Kurtz. Markov Processes: Characterization and Convergence. Wiley Series in Probability and Statistics. Wiley, 2 edition, 2005.

- Filipović (2005) D. Filipović. Time-inhomogeneous affine processes. Stochastic Processes and their Applications, 115(4):639–659, 2005.

- Filipović and Larsson (2016) D. Filipović and M. Larsson. Polynomial diffusions and applications in finance. Finance and Stochastics, 20(4):931–972, 2016.

- Fontana et al. (2020) C. Fontana, Z. Grbac, S. Gümbel, and T. Schmidt. Term structure modelling for multiple curves with stochastic discontinuities. Finance and Stochastics, 24(2):465–511, 2020.

- Gierjatowicz et al. (2020) P. Gierjatowicz, M. Sabate-Vidales, D. Siska, L. Szpruch, and Z. Zuric. Robust pricing and hedging via neural SDEs. Available at SSRN 3646241, 2020.

- Heath et al. (1992) D. Heath, R. Jarrow, and A. Morton. Bond pricing and the term structure of interest rates: A new methodology for contingent claims valuation. Econometrica: Journal of the Econometric Society, pages 77–105, 1992.

- Kawazu and Watanabe (1971) K. Kawazu and S. Watanabe. Branching processes with immigration and related limit theorems. Theory of Probability & Its Applications, 16(1):36–54, 1971.

- Keller-Ressel and Mayerhofer (2015) M. Keller-Ressel and E. Mayerhofer. Exponential moments of affine processes. The Annals of Applied Probability, 25(2):714–752, 2015.

- Li (2010) Z. Li. Measure-valued branching Markov processes. Springer Science & Business Media, 2010.

- Luther (1970) N. Luther. Locally Compact Spaces of Measures. Proceedings of the American Mathematical Society, 25:541–547, 1970.

- Nachbin (1949) L. Nachbin. Sur les algebres denses de fonctions différentiables sur une variété. Comptes rendus hebdomadaires des seances de l’academie des science, 228(20):1549–1551, 1949.

- Revuz and Yor (1999) D. Revuz and M. Yor. Representation of martingales. In Continuous Martingales and Brownian Motion, pages 179–220. Springer, 1999.

- Salvi et al. (2021) C. Salvi, M. Lemercier, and A. Gerasimovičs. Neural stochastic partial differential equations. Preprint, arXiv:2110.10249, 2021.