Online Pricing Incentive to Sample Fresh Information

Abstract

Today mobile users such as drivers are invited by content providers (e.g., Tripadvisor) to sample fresh information of diverse paths to control the age of information (AoI). However, selfish drivers prefer to travel through the shortest path instead of the others with extra costs in time and gas. To motivate drivers to route and sample diverse paths, this paper is the first to propose online pricing for a provider to economically reward drivers for diverse routing and control the actual AoI dynamics over time and spatial path domains. This online pricing optimization problem should be solved without knowing drivers’ costs and even arrivals, and is intractable due to the curse of dimensionality in both time and space. If there is only one non-shortest path, we leverage the Markov decision process (MDP) techniques to analyze the problem. Accordingly, we design a linear-time algorithm for returning optimal online pricing, where a higher pricing reward is needed for a larger AoI. If there are a number of non-shortest paths, we prove that pricing one path at a time is optimal, yet it is not optimal to choose the path with the largest current AoI. Then we propose a new backward-clustered computation method and develop an approximation algorithm to alternate different paths to price over time. Perhaps surprisingly, our analysis of approximation ratio suggests that our algorithm’s performance approaches closer to optimum given more paths.

Index Terms:

Age of information, online multi-path pricing, polynomial-time algorithms, approximation errorI Introduction

Today content providers (e.g., Tripadvisor, Yelp and Google Maps) prefer not to deploy expensive dedicated sensor networks to cover the whole city or nation. Instead, they invite mobile users such as drivers to sample fresh information on diverse paths especially those infrequently visited in the past [1]. The sampled live information on the way include air quality data, shopping promotion and location, and traffic condition [1, 2, 3]. However, selfish drivers are not willing to travel through non-shortest paths to sample fresh information if there are no rewards to offset their extra costs in time and gas [4]. It is shown in [5] that the network performance degrades significantly due to drivers’ selfish routing behaviors. To leverage the power of the mobile crowd, it is critical for providers to properly offer monetary rewards to drivers to change their myopic routing decisions for sampling fresh information along diverse paths. Such incentive mechanisms should be designed in an online version to adapt to the actual variations of information freshness over paths and time.

Recent crowdsourcing works study optimal sensing policies by recruiting mobile vehicles to sense data (e.g., [6, 7, 8, 9]). For example, [6] takes advantage of the mobility of vehicles to provide location-based services in large scale areas. [7] defined spatial and temporal coverage as two metrics for crowdsourcing quality to design greedy and genetic approximation algorithm. [8] incentivizes a crow of vehicle drivers to sense and sample the desired target regions in one-shot. [9] allows allocated vehicles to follow their origin and destination routes while maximize the overall sensing benefit. However, all of these studies overlook the freshness of sampled data.

To model the information freshness, [10] proposes the concept of age-of-information (AoI) before a new information update is received. Following this, both time-average and peak AoI are developed to measure the average and maximum ages in the time domain, respectively [11, 12]. Numerous works have been analyzing AoI statistics and designing scheduling policies to minimize these two performance metrics [13, 14, 15, 16]. For example, by formulating the AoI state updating as a Markov decision process (MDP), [13] develops approximation algorithms to schedule information packets from multi-sources to end-users for minimizing the average AoI. [14] proposes online scheduling policies to minimize the AoI under different metrics in multi-flow, multi-server systems. [15] compares several scheduling policies to find that transmitting the packet with the largest current AoI is optimal. [17] studies link scheduling to optimize of min-max peak AoI in wireless networks. However, these works only consider the passive packet arrival process for transmission protocols design, and overlook the opportunity to design the sampling process.

To actively sample fresh data, several works study the path planning problem in UAV-assited IoT to minimize AoI [18, 19, 20]. [18] formulates an MDP to capture the dynamics of UAV locations and applies reinforcement learning to solve the problem. [19] jointly considers energy consumption and AoI evolution to study the data acquisition problem. However, these works only consider the fully controlled UAV to route but overlook vehicle users’ selfish behaviors to disobey. As today many mobile users are invited to sample information, it is important to leverage human-involved sampling or crowdsoucing to control AoI for content providers.

Only a few mobile crowdsourcing works have taken the economics effect of AoI into consideration for information update or reward maximization. [21] considers sampling costs for users to decide when to self-update local data, without considering any incentive design from the content providers. [22] studies how an information customer requests and pays for the fresh information to be updated by the source. [23] studies a two-stage game model for a fresh data market to maximize a platform’s profit, where the platform provides data with different AoI to dynamically arriving users. [24] jointly designs optimal upload strategy and incentivizes users to offload data in order to control the AoI. However, these works do not study how to motivate the power of the crowd for sampling fresh data to control AoI. The most related work to this paper is [25], which proposes an offline algorithm to provide sampling rewards to mobile users for controlling expected AoI. Yet this work cannot adapt to unexpected AoI change for dynamic incentive design, and it only looks at a single path instead of a road network for information sampling.

To our best knowledge, this paper is the first work to study how a content provider designs its optimal pricing to reward drivers online for diverse routing and fresh information sampling. To best adapt to the actual variations of AoI over paths and time, we formulate our online optimization problem as a stochastic dynamic program. However, we need to overcome the following technical challenges.

-

•

Incomplete information about drivers’ cost and arrival pattern: To control the actual AoI evolution in real time, our incentive pricing as compensation should be designed according to drivers’ actual arrivals and extra travel costs on non-shortest paths. Yet in practice, such information are private to drivers and unavailable for the content provider when deciding the online pricing. This makes it infeasible to apply online control methods such as Hamilton-Jacobi-Bellman equations and neural networks approximation here [26, 27].

-

•

Curse of dimensionality in both time and spatial path domains: The optimal online pricing should be time- and path-dependent, making the number of system states exponentially increase with the time horizon and path number in backward induction [28, 29, 30]. Some recent work finds special feature of system states (e.g., periodicity) to simplify the backward/forward induction yet cannot apply to our AoI problem (e.g., [31, 32]).

The existing AoI works design offline scheduling policies for multi-channel network by dynamic programming (e.g., [25, 33]). There are some recent work on online scheduling, yet they assume the system space to be countable and linearly increasing with number of channels and time (e.g., [14, 15, 34]). MDP techniques are widely used to model the dynamic pricing problem (e.g., [35, 36, 37]). [35] discretizes the state space into the set of finite intervals to greatly reduce its size, which is not applicable in our multi-path problem with possibly unbounded AoI. [36] proposes to aggregate similar states to reduce the computational times, but it cannot provide any rigorous performance analysis such as proving approximation error in the worst case. [37] applies heuristic methods to solve the MDP under completed cost information, which did not analyze the error bound or prove structural properties. Their algorithm design and performance analysis cannot apply to our online pricing problem to sample fresh information in a large-scale road network over time.

Our paper aims to overcome the above technical challenges for online pricing design, and our key novelty and main contributions in this paper are summarized as follows.

-

•

Novel online pricing to sample fresh information over time and space: To motivate the power of the mobile crowd, this paper is the first to propose online pricing incentive for a content provider to economically reward drivers to sample fresh information through diverse routing. We optimize pricing reward on human-involved sampling to affect the actual AoI dynamics over time and spatial paths, without knowing drivers’ hidden extra travel costs and even arrivals.

-

•

Linear complexity algorithm to solve online pricing for one non-shortest path: To minimize the state space of the our formulated MDP problem, we exploit the dynamics of AoI feature to jointly apply a fixed look-up table to greatly simplify the backward induction process. Then we design a linear-time algorithm for returning optimal online pricing. We prove structural properties of our unique pricing solution, and show that a higher pricing reward is needed for a larger AoI. We also show that our algorithm is applicable to infinite time horizon.

-

•

Approximation algorithm to solve online pricing for multiple non-shortest paths: We propose a new backward-clustered computation method to overcome the curse of dimensionality in the path number. We first prove that it is optimal to only price one path at a time, while it is not optimal to myopically choose the path with the largest current AoI. Based on the backward-clustered method, we develop a new approximation algorithm to alternate different paths to price over time. This algorithm has only polynomial-time complexity, and its complexity does not depend on the number of paths. Perhaps surprisingly, our analysis of approximation ratio suggests that this algorithm’s performance approaches closer to the optimum if more paths are involved to sample.

The rest of the paper is organized as follows. In Section II, we overview the system model to sample fresh information and introduce the problem formulation for online pricing. In Sections III and IV, we prove structural properties of our unique pricing solution, and then propose a linear-time algorithm to return optimal online pricing if there is only one non-shortest path. In Section V, we develop a new approximation algorithm to alternate different paths to price over time if there are a number of non-shortest paths, which has only polynomial-time complexity and does not depend on the path number. Finally, we conclude this paper in Section VI.

II System Model and Problem Formulation

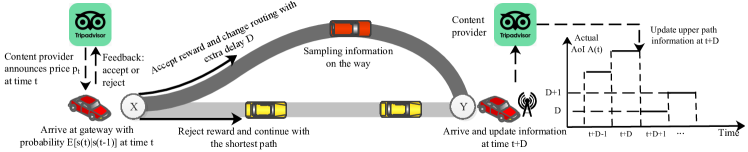

As illustrated in Fig. 1, a random flow of drivers sequentially arrive at the gateway X in the discrete time horizon of in total rounds. At any time slot , a driver (if any) needs to make routing decision from X to destination Y. Here, the road network includes the shortest path with normalized zero travel cost and another distant path with extra travel delay in the upper part of Fig. 1. For ease of exposition, we first focus on this case with only one non-shortest path, and then extend our analysis and pricing design to an arbitrary number of non-shortest paths later in Section V.

Selfish drivers hesitate to choose the non-shortest upper path to incur extra travel cost in time and gas, resulting in under-sampling of this path (e.g., to collect air quality data, shopping promotion and location, or traffic condition [1, 2, 3]). There are always enough drivers to cover the shortest path and we do not need to consider the AoI there. Our problem is how to motivate the randomly arriving drivers to sample the non-shortest path to control AoI there. At each time , the content provider observes the actual AoI of the non-shortest path (see Fig. 1), and compensates an arrived driver at the gateway with pricing reward to possibly change his routing to the upper path to return the sampled information of the whole path at time .

At each time slot , the content provider can predict the ongoing AoI evolution till , and its pricing decision needs to be adaptive to foreseeable AoI evolution in set

We can thus rewrite price at time as or simply . Note that the content provider will not decide any price after time , as a driver can no longer return the sampled information timely before the end time .

Next we first introduce the driver’s model and then present the online pricing problem formulation.

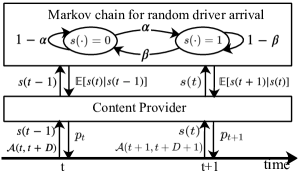

II-A Driver’s arrival and cost model for sampling

Following the traffic control literature (e.g., [4, 38]), we model drivers’ random arrivals at the gateway X over time as a Markov chain. As shown in Fig. 2, if a driver arrives at the beginning of time slot , we denote it as , and otherwise . Each time slot’s duration is set small enough such that there is at most one arrival at a time, and we practically model the correlation between arrivals across neighboring time slots. That is, if ,

Similarly, if , we update by replacing the two probabilities and above by and . At the beginning of time slot , the content provider only knows past arrival information in Fig. 2, and expects arrival probability during time slot by using the Markov chain, i.e.,

| (1) |

Besides the random arrival process, we consider the challenging incomplete information scenario that the content provider does not know each driver’s actual cost when deciding pricing before observing . A driver has extra cost to travel on the non-shortest path with delay , and different drivers have different cost sensitivities. Let be the normalized cost sensitivity of a driver, then we model its cost as , which is proportional to the delay with individual cost sensitivity . Thus, a driver with greater is more cost sensitive and less likely to accept the price offer to change route. Yet, the provider only knows that in a normalized range randomly follows cumulative distribution function (CDF) , which can be obtained by fitting different historical data’s frequencies into a histogram and converting it to CDF as [39]. The maximum travel cost is thus and the content provider will not decide any pricing reward beyond to over-pay any driver, and we expect

The cost sensitivity distribution in certain applications is considered to be truncated normal or logistic random distribution [39, 40], which are used for our simulations later. In this paper, we assume that the i.i.d. random distributions of drivers’ cost sensitivities satisfies the following assumption, which is the regular value distribution widely assumed in the mechanism design literature [41].

Assumption 1.

Assume that the following function

| (2) |

increases monotonically in , where and are the CDF and PDF of a driver’s random cost sensitivity.

According to [41], the second term of (2) is the complementary hazard rate and the monotonicity of tells the Myerson’s regularity. Assumption 1 is not strong and it is satisfied by multiple common distributions such as uniform, exponential and logistic distributions. Later in Section III we will relax Assumption 1 and extend our analysis and results to some other distributions (e.g., truncated normal distribution) in Corollary 1.

II-B Online Pricing Problem Formulation

Upon arrival at time with , a driver observes the current pricing reward . He decides to accept this offer or not, by checking if his utility

| (3) |

of travelling on the non-shortest path is positive or not. If and at time , the driver accepts the offer at the gateway X, and updates the whole path’s information after travel delay , helping reduce the AoI of this path to , as shown in the right part of Fig. 1. Otherwise, the next foreseen AoI at time increases from by one slot to . Thus, the dynamics of the actual AoI is given as

| (4) |

where is defined in (3), and the pricing reward is accepted in the former case with probability

| (5) |

with in (1) from the content provider’s point of view. The expectation of the final payment to the possibly arrived driver at time is thus , and the online pricing needs to well balance the next AoI evolution in (4) and the expected payment.

Finally, we are ready to formulate the provider’s online pricing problem in Fig. 2 by the Markov decision process (MDP) techniques with four components [28, 42] to best adapt to the actual AoI evolution and past arrival observation under the memoryless property.

-

•

States: We define the state of the MDP in slot by the tuple . Note that at initial time slot .

-

•

Actions: The action of the MDP in slot is the price . Note that the continuous action space size is infinite.

-

•

Transition probabilities: According to the conditional arrival probability in (1) and AoI dynamics in (4), there can be three possible states at the next time slot . The path will be sampled by an arrival driver with probability in (5). If there is no arrival at time , the state at will be with probability

(6) If there is an arrival at time but the driver does not accept the price, the state at will be instead with probability

(7) In summary, we can obtain the following state transitions of :

(8) which correspond to the three outcomes: arrival to sample, no current arrival, and arrival to not sample.

-

•

Cost: Let be the immediate cost of the MDP if action is taken in slot under state , which is defined as the summation of the actual AoI and expected economic payment:

(9)

Considering the discount factor under discrete time horizon, the objective of the MDP is to find the optimal pricing function at current time slot that minimizes the long-term total -discounted cost:

| (10) | ||||

which is a non-convex problem due to the non-convex AoI dynamics constraint. The current price to announce affects the dynamics of AoI since . Note that the current pricing decision can only affect the AoI after a time delay , thus like we also use the foreseen AoI in the cost objective function in (10) above.

II-C Characterization of Dynamic Program

For any time in the finite time horizon, problem (10) can be written as [28]:

| (11) |

where the cost-to-go is

according to the transition probabilities (8).

The optimal pricing satisfies the first-order necessary condition of (11) with respect to , i.e.,

| (12) |

where

| (13) |

To solve (12), we need the inputs of and . For each long-term cost function since time , it takes complexity to obtain its pricing solution to (12) using binary search with error [43].

Lacking the information about drivers’ hidden sampling costs and even arrivals, the transition probabilities are related with the pricing in (11). Therefore, it is infeasible to apply online control methods such as Hamilton-Jacobi-Bellman equations and neural networks approximation here [26, 27, 44].

| Notation | Definition |

|---|---|

| The extra travel delay of the single non-shortest path | |

| The time horizon | |

| The foreseen AoI with the travel delay at the beginning of time slot | |

| The pricing reward to compensate an arrived driver at time | |

| Driver’s arrival information of the last time slot | |

| The conditional probability of a driver’s arrival during time slot . | |

| The cost sensitivity of a driver | |

| The CDF of a driver’s random cost sensitivity | |

| The utility of a driver at time slot | |

| The state at time in the single path problem | |

| Q(t) | Transition probabilities at time slot in MDP |

| The immediate cost of the MDP | |

| The discount factor | |

| The -discounted long-term cost function at time | |

| The error of binary search | |

| The look-up table to store cost function for any | |

| The total number of non-shortest paths | |

| The travel delay of the -th non-shortest path | |

| The index of the path with the maximum net payoff at time slot | |

| The foreseen AoI set of all the non-shortest paths at the beginning of time slot | |

| The state at time in the multi-path problem |

As it is too late to price after for returning timely information before end-time , we obtain from (11) that

| (14) |

Based on the state transitions in (8) and equation (14), we find that the state space increases polynomially with time horizon in (11) for the single-path pricing problem. Thus, one can use backward induction to solve the problem (11) in polynomial time [28, 31], which may be not small for a large . Thus, we will further exploit the unique AoI feature and propose Algorithms 1 and 2 to reduce to linear complexity later in Section IV. On the other hand, we will show later in Section V that the state space increases exponentially in and path number , which forbids to apply traditional MDP methods [45].

III Proved Structural Properties of Optimal Online Pricing

Since the price is located in a compact interval , there always exists optimal pricing solutions to the problem (11). However, since drivers’ information about costs and random arrivals are incomplete, the monotonicity of cost function with respect to and the uniqueness of optimal pricing solution to (12) cannot be guaranteed [46] and [28]. In this section, at any time , we first examine the monotonic relationship of cost function and optimal pricing with respect to the foreseen AoI . Then we prove the uniqueness of optimal online solution to problem (11).

By observing (12), we find the optimal pricing solution is determined by the the cost functions without information update, with update, and the CDF . To examine the optimal pricing’s relationship with , we first need to examine the relationship between cost function in (11) and foreseen AoI [28].

Proposition 1.

The optimal cost function in (11) at any time increases monotonically with the foreseen AoI .

Proof.

Suppose that there are two states and with their actual AoI satisfying at any time slot . In the following, we apply both mathematical induction and backward induction to prove

| (15) |

which can tell the monotonicity of the optimal cost function.

We first prove the base case at the last time slot . According to (14), the two cost functions satisfy

which holds for (15).

Next, we assume the induction hypothesis that is true for a particular time slot . It follows to show that also holds. Denote and to be the optimal pricing to and , respectively. Consider another non-optimal pricing to :

| (16) |

whose corresponding non-optimal cost function must satisfy . Then we can derive the induction step:

which is larger than due to the facts that , and (16).

Intuitively, a larger foreseen AoI leads to larger long-term cost. Based on the monitonicity of the long-term cost function in Proposition 1, next we are ready to prove the uniqueness of optimal online pricing solution to problem (11) at any time .

Proposition 2.

Proof.

Let and define to be

where is defined in (2) and is in (13). According to (12), if there exists such that

at any time , its corresponding is the optimal pricing to (11).

To verify the existence of , we next check the two endpoints and . As and the two cost functions satisfy

by Proposition 1, we can obtain .

If , i.e., , there exists a solution of in . Under Assumption 1, is an increasing function, and thus increase with on , which means the solution is unique.

If instead, there is no solution in , but we can still uniquely set

to hurdle the large foreseen AoI. ∎

We can generalize our Proposition 2 to fit some other distributions such as truncated normal distribution.

Corollary 1.

If there exists a cutoff point , such that for and increases with , which holds for truncated normal distribution, then the optimal pricing solution to problem (11) exists and is unique.

Based on Propositions 1, 2 and the expression (12), we can also derive the monotonicity of optimal online pricing with respect to [28].

Corollary 2.

The unique optimal online pricing at any time increases monotonically with the foreseen AoI .

IV Linear-time algorithm for optimal online pricing

Recall that backward induction can be used to solve problem (11) in polynomial time. In this section, we exploit the dynamic feature of AoI to jointly use a fixed look-up table and backward induction to further reduce the increasing number of cost functions in the time domain. Furthermore, we show our designed algorithm is also applicable to infinite time horizon.

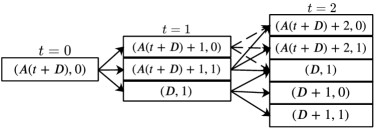

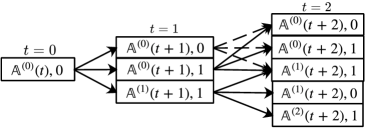

According to (12), at any time we first need to compute long-term cost functions and before solving optimal pricing . To obtain for example, as discussed at the end of Section II, we further need to apply iteration computation to derive another three cost functions , and at time . After careful examination of this branching network, we find out that a large number of cost functions repeatedly appear due to the linearly increasing feature of AoI over time. Take the transition of at time with as an illustrative example, which implies three decision slots . Fig. 3(a) shows the polynomial increase of state space for iterative computation from to . At time , with no driver arrival during last time slot (i.e., ) and with last arrival have the same branches to and at . As there are actually states at time , we can apply backward induction as [45] and [31] to derive the optimal online pricing at current time in polynomial time.

Moreover, as inspired by [47] and [48], we want to further simplify the state space by applying the look-up table approach. As shown in Fig. 3(a), we find the state appears at each time slot as it is possible to find the driver arrival to sample and update information at any time. Since the inputs and of these functions are constant, we do not need to wait till our observation of such constants to decide the pricing online. Instead, we propose to compute any before and store them in a fixed look-up table for any online use later. Then we no longer need to expand the state space from at any time . As illustrated in Fig. 3(b), by jointly applying the look-up table, we end up with only three cost functions to compute online at both and . Thus, we successfully reduce the number of cost functions to compute online from quadratic term to linear item at each time .

Thanks to the look-up table approach that successfully reduces the polynomially increasing number of cost functions to linear number, we are ready to propose Algorithm 1 to compute the look-up table and Algorithm 2 to optimally solve problem (11) for online pricing at any time .

In Algorithm 1, we apply backward induction to calculate cost functions from to :

- •

- •

- •

Note that here we use the state tuple in to distinguish from the state space elsewhere. After returning the fixed look-up table , we are ready to apply it to solve in Algorithm 2:

- •

- •

-

•

We finally obtain the optimal price during the last loop .

As the pricing action space is continuous, we equally discretize it into many points with as the gap. Here can also be viewed as the error of binary search to find the optimal online pricing according to (12).

Based on the above analysis, we propose the following theorem and further analyze the complexity of Algorithm 2.

Theorem 1.

Proof.

As mentioned above, the joint use of backward induction and look-up table reduces the number of cost function to for each time slot, and it takes complexity to obtain each price solution to the cost function by using binary search of (12). Thus, it takes complexity to obtain the optimal pricing for any particular time .

Note that as the look-up table is computed offline before , there is no need to take its complexity into consideration. Then we can say that Algorithm 2 costs linear-time to calculate the online optimal pricing at any time . ∎

Note that storing any other cost functions into a look-up table cannot help to reduce the complexity anymore, because the initial AoI at time is unknown and can be unbounded. Thus, the linear time complexity of Algorithm 2 is the minimum and cannot be further improved [28, 29].

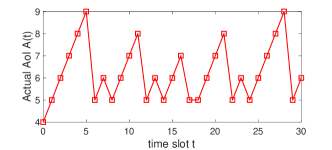

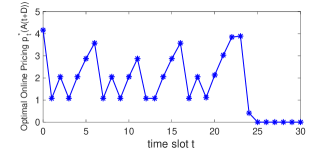

In the following experiment, we create a typical instance to run the online optimal pricing returned by Algorithm 2 and corresponding AoI , in Fig. 4. Here we set the travel delay for the non-shortest path in Fig. 1 with initial AoI , and the cost distribution of each driver to follow truncated normal distribution with mean and variance . Fig. 4 shows that the online pricing to announce follows a delayed pattern of the actual AoI observation over time. This is consistent with the monotonicity of the pricing with respect to delayed AoI by in Corollary 2. We also notice the online pricing converges to zero since , as any outdated update after cannot help.

Remark 1.

Actually, we can revise our algorithm to fit the infinite time horizon , by replacing the time window by a future finite window in Algorithm 1 and 2 for efficient computation (with constant complexity) at any time . We can first prove that the optimal cost functions are bounded under , and then prove that the performance error of this approximation algorithm (revised from Algorithm 2) exponentially reduces to zero as increases.

V Generalization of online pricing to Multi-Path Sampling Scenario

For ease of exposition, we only consider to sample one non-shortest path in Fig. 1 and propose a linear algorithm to solve the problem. In this section, we generalize to sample an arbitrary number of different non-shortest paths and introduce the generalized system model first. Different from the single-path problem, the state space here increases exponentially with time horizon and path number . To overcome the curse of dimensionality in the spatial path domain (i.e., the path number), we first prove that it is optimal to only price one path at a time, which is not necessarily the path with the largest current AoI. We then propose a new backward-clustered computation method across paths and design an approximation algorithm of polynomial complexity to alternate different paths to price over time.

V-A Model extension to sample multiple diverse paths

Upon arrival at the gateway X by following the Markov chain, a driver now faces an arbitrary number of non-shortest paths from X to destination point Y for routing. We consider diverse paths such that each path has a unique travel delay and a driver with personalized cost sensitivity incurs

to travel on this path to sample fresh information there. We aim to design online pricing to all the paths to help sample fresh information globally to control the maximum AoI. We summarize the actual AoI evolutions in all the paths in set

| (17) |

to tell the maximum foreseen AoI from time , depending on which path was sent by the last driver (if any) at time to sample. We next see how does update for all the paths.

At the beginning of time , the provider decides online pricing set

| (18) |

based on the foreseen AoI set . Given the online prices to different paths, a driver with cost sensitivity (if arrives at time ) finds path appealing as long as the price there can justify his travel cost, i.e., his utility of travelling path

| (19) |

is no less than 0, which depends on the pricing set and the driver’s private travel cost sensitivity . If he finds multiple paths appealing, he will optimally accept the path with maximum net payoff, i.e.,

| (20) |

If there is no driver arrival at time or this driver does not consider to sample any of the non-shortest paths, we set . Based on (20), we update all the paths’ next foreseen AoI as:

| (21) |

Based on the above model extension, we are ready to apply the MDP formulation as [28] and [42] again to formulate the provider’s online pricing problem below.

-

•

States: We define the state of the new MDP in slot by . Similarly, and at time .

-

•

Actions: The action of the MDP in slot is the price set defined in (18).

-

•

Transition probabilities: Compared to the state transitions (8) in single-path, the state space of now increases exponentially with , because every path has probability to be sampled at each time slot. Denote the probability that path is accepted by an arrived driver to sample (i.e., ) by . The state at time slot can change into

(22) where the dynamics of is defined in (21). There are totally outcomes: no current arrival, arrival to not sample, and arrival to sample path .

- •

Thus, we extent problem (10) by considering multiple paths: at the beginning of time slot ,

| (24) | ||||

Similar to (11), (24) can be rewritten as

| (25) |

where the cost-to-go is

according to transition probabilities (22). Note that drivers’ random choice model in among paths incurs totally cost functions to iteratively (25) much more difficult than (11).

Existing works (e.g.,[14, 15, 34]) also formulate dynamic program to design optimal scheduling policies for multi-channel network to minimize peak or average weighted AoI. However, the system space of actions only linearly increases in the path number and time horizon . However, in our problem (25), the system space increases exponentially. In the following, we first reduce multi-path pricing to single-path at a time and then propose our backward-clustered computation to design low-complexity algorithm.

V-B Reducing multi-path pricing to single-path at a time

Note that Propositions 1 and 2 can be extended for this multi-path model and ensure existence and uniqueness of the online pricing solution to problem (25). Here we need to overcome the curse of dimensionality in both the path number and time horizon . In this subsection, we prove that we can reduce the spatial searching dimensions greatly by reducing multi-path pricing to single-path pricing at each time .

Proposition 3.

To solve problem (25), it is optimal to only price path out of paths at each time , where

| (26) |

Proof.

We can first prove that updating path only is better at any time by comparing its cost function in (25) with any other single path’s cost function.

Denote the cost functions of pricing single path and single path by and , respectively, where and , such that the foreseen AoI of the two paths satisfy

Denote their corresponding optimal prices as and , respectively.

We consider another non-optimal policy

for path , then the corresponding non-optimal cost function satisfies

Note that , such that the non-optimal price will not exceed .

Then we can compare the two cost functions of updating single path and path

| (27) | ||||

where and are defined in (22). Here we can use the same backward and mathematical induction methods as the proof of Lemma 1 to obtain

and

Substituting the above two inequalities into (27), we can finally obtain

which means that updating the single path (26) is better than updating any other single path.

If there are multiple paths with appealing prices for a driver arrival at time (i.e., in the first case of (20)), he can only choose one to sample. Then the provider can simultaneously reduce the other non-target paths’ prices to zero and properly reduce the target path’s price to sample, while keeping the driver’s acceptance probability to sample the target path unchanged. This helps save the expected economic payment to the driver and reduce the cost function. Hence, we prove that only pricing path is optimal to solve (25). ∎

Proposition 3 shows that it is optimal to only price a single path at a time. Intuitively, if positive prices are given to more than one path, the driver will still choose only one to sample. Then the provider need to give higher price for the target path given the competitive prices from others, which incurs unnecessary cost.

Further, Proposition 3 tells that we should target at the path with the maximum foreseen AoI instead of largest current AoI . This result is different from [14] and [15], because the current pricing decision in our problem can only help reduce the AoI after a path-dependent time delay.

Thanks to Proposition 3, we only need to design the positive price for the target path in (26) instead of at each time . Then the cost function in (23) is simplified to:

| (28) |

Accordingly, (25) can also be simplified as

| (29) |

where the cost-to-go is

| (30) | ||||

by letting for all and in (22). Though the total number of cost functions has been greatly reduced from to in problem (29), it is still difficult to solve, and the direct application of backward induction approach in Section IV cannot help. Here we follow a random pattern to alternate and traverse the target path () to price over time, and we still need to adapt pricing online to a huge AoI evolution set with an exponentially increasing state space in .

V-C Backward-clustered computation for low-complexity approximation algorithm

In this subsection, we propose a new innovative simplification approach called backward-clustered computation method to solve problem (29). Different from the repeated long-term cost functions under the same sampled paths we analyzed in Fig. 3(a), the huge number of cost functions across paths are non-repeated themselves. To reduce the exponentially increasing state space, at current time , we cluster those states with the same number of future sampled paths from time to be one approximated state. By applying this approximation for clustered functions, we no longer count and compute all the long-term cost functions, and we do not need to consider any more.

More specifically, at current time , we propose to use and to approximate foreseen AoI evolution set and its cost function in (29), respectively, where the superscript means the number of the sampled paths from time is still at time . Note that the initial approximated AoI set equals . Then the three possible states at time in (22) can be approximated to and , respectively. Here only with superscript tells that one path is sampled from time to . Take the clustered approximation of in (29) with three decision slots ( under ) as an illustrative example, and Fig. 5 shows the approximated branching network from to as explained below.

-

•

At , there are only approximate AoI sets (i.e., and ) in Fig. 5, because there are at most two paths being sampled since , and we only have approximated states instead of .

-

•

At , our two approximated states with superscript (i.e., with last arrival and without last arrival) have the same branching structure to , and at . Thus, it suffices to cluster and by only expanding one of them to in Fig. 5.

Note that the original states and in (30) cannot branch to the same state at time , because the path is sampled during different time slots, i.e., and , respectively. In our approximation of backward-clustered computation, the actual AoI of a sampled path is mildly enlarged to the approximated AoI. Yet this error is always bounded by the elapsed time since current time and will not take effect until this path is priced to sampled again. By clustering the approximated cost functions with the same number of sampled paths from time to the whole branching network, we successfully reduce the number of long-term cost functions to compute from to around , which can be solved using backward induction.

Regarding the pricing solution, similar to (12), the approximation online pricing here satisfies the first-order condition of (29), yet the cost functions are replaced by their approximation and . Now we present Algorithm 3 to efficiently return the approximation online pricing to (29). We apply our backward-clustered computation to calculate approximation cost functions from to :

- •

- •

- •

Note that in step 9, we update the AoI of path to because this -th updated path can be sampled at any time from to , such that we take the average of all the possible AoI based on our linear model in (23).

As a counter-part of (29), we denote as the approximated cost function under our approximation pricing, and we next prove that it has bounded performance gap to the optimum in the following theorem.

Theorem 2.

At any time , our approximation Algorithm 3 takes only polynomial time complexity to return the approximation online pricing , and the complexity does not depend on the path number . As compared to the cost optimal objective in (29), Algorithm 3’s cost objective achieves the following approximation error in the worst case:

| (31) | ||||

and this error increases with but decreases with .

Proof.

As illustrated in Fig. 5, our approximation of the clustered computation reduces the number of cost functions from to only around for each time . It takes at most complexity to obtain the approximation pricing for each approximated cost function, by applying binary search of the first-order condition of (29) with error . Thus, it takes complexity to obtain the approximation pricing for any particular time .

Since the actual AoI set is enlarged to the approximated AoI set, the approximated cost function satisfies

Then we can use such relationship to compute the approximation error:

The second inequality above is obtained using the first-order conditions of the original and approximated cost functions with respect to their prices at time , and the third inequality is because the performance loss at any future time cannot exceed the elapsed time . The function above is an increasing function of to return the updating time cycle to sample path again. We can check the partial derivatives of the right-hand-side bound of (31) to show that it increases with but decreases with . ∎

The complexity of our Algorithm 3 does not depend on path number and can thus fit large-scale road networks. Actually, the approximation error on the right hand side of (31) is small most of the time. Perhaps surprisingly, it decreases with a larger path number . This is because individual paths become similar to each other in a larger path choice pool, and our backward-clustered computation in Algorithm 3 only counts the number of sampled paths (without checking which paths) for approximating cost functions.

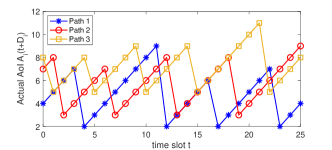

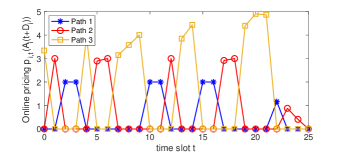

We create a typical instance but with paths in Fig. 6 to run the online approximation pricing and corresponding foreseen AoI set , returned by Algorithm 3. Here we set the travel delay set for the three paths, whose initial AoI , and the cost distributions of each driver to follow a truncated normal distribution with mean and variance .

Fig. 6(a) shows the evolution of the foreseen AoI of all the three paths, and the maximum AoI among all the paths are well controlled thanks to our online pricing solution in Fig. 6(b). We can also see that the platform will select the path with the maximum AoI to price, which is consistent with Proposition 3. In this case, the online pricing follows a -delayed pattern of the actual AoI over time.

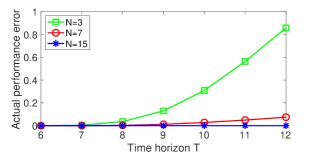

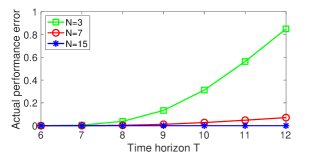

Finally, unlike (31)’s error for the worst-case, we run simulations to examine Algorithm 3’s actual performance loss as compared to the optimum, versus time horizon and path number in Fig. 7. Here we generally consider initial ’s online decision making, then the cost objective uses the approximation pricing returned by Algorithm 3. While the optimal cost function in (29) uses the optimal pricing returned by traditional iterative computation methods, whose complexity is high and only allows us to keep for simulation. In Fig. 7 with almost the same Fig. 7(a) and Fig. 7(b), we find that effect of to the performance error is limited, which shows our scalable Algorithm 3’s robustness to different cost distributions. The performance error is mild from the optimum under our algorithm. This result is also consistent with Theorem 2 to show the approximation error increase in time horizon and decrease in path number .

VI Conclusion

In this paper, we have proposed online pricing for a content provider to economically reward drivers for diverse routing and control the actual AoI dynamics over time and spatial path domains. This online pricing optimization problem should be solved without knowing drivers’ costs and even arrivals, and is intractable due to the curse of dimensionality in both time and space. If there is only one non-shortest path, we leverage the Markov decision process (MDP) techniques to analyze the problem. Accordingly, we design a linear-time algorithm for returning optimal online pricing, where a higher pricing reward is needed for a larger AoI. We also show that our algorithm is applicable to infinite time horizon. If there are a number of non-shortest paths, we prove that pricing one path at a time is optimal, yet it is not optimal to choose the path with the largest current AoI. Then we propose a new backward-clustered computation method and develop an approximation algorithm to alternate different paths to price over time. This algorithm has only polynomial-time complexity, and its complexity does not depend on the number of paths. Perhaps surprisingly, our analysis of approximation ratio suggests that our algorithm’s performance approaches closer to optimum if more paths are involved to sample.

We can consider some possible future works directions to extend this work. Recall that this paper focuses on the min-max foreseen AoI optimization in problem (25) if there are a number of non-shortest paths. We can extend to study the min-sum AoI optimization problem to minimize the total AoI across all the paths. Our backward-clustered computation method should still work and we should still choose to pricing one path at a time. Yet we may not choose the path with the largest foreseen AoI in Proposition 3. Moreover, we can also extend our analysis to deal with the random travel delay instead of deterministic delay in each path, where we need to further take expectation in the online optimization. The evaluation about the performance of our algorithms with real data is another point in our next step.

References

- [1] L. Wang, D. Zhang, Y. Wang, C. Chen, X. Han, and A. M’hamed, “Sparse mobile crowdsensing: challenges and opportunities,” IEEE Communications Magazine, vol. 54, no. 7, pp. 161–167, 2016.

- [2] D. Asghar, M. Zubair, and D. Ahmad, “A review of location technologies for wireless mobile location-based services,” Journal of American Science, vol. 10, no. 7, pp. 110–118, 2014.

- [3] R. Bhoraskar, N. Vankadhara, B. Raman, and P. Kulkarni, “Wolverine: Traffic and road condition estimation using smartphone sensors,” in the IEEE Fourth International Conference on Communication Systems and Networks, 2012.

- [4] Y. Li, C. Courcoubetis, and L. Duan, “Recommending paths: Follow or not follow?” in IEEE INFOCOM 2019-IEEE Conference on Computer Communications. IEEE, 2019, pp. 928–936.

- [5] D. R. Figueiredo, M. Garetto, and D. Towsley, “Exploiting mobility in ad-hoc wireless networks with incentives,” Relatório Técnico, pp. 4–66, 2004.

- [6] L. Xiao, T. Chen, C. Xie, H. Dai, and H. V. Poor, “Mobile crowdsensing games in vehicular networks,” IEEE Transactions on Vehicular Technology, vol. 67, no. 2, pp. 1535–1545, 2017.

- [7] Z. He, J. Cao, and X. Liu, “High quality participant recruitment in vehicle-based crowdsourcing using predictable mobility,” in 2015 IEEE Conference on Computer Communications (INFOCOM). IEEE, 2015, pp. 2542–2550.

- [8] S. Xu, X. Chen, X. Pi, C. Joe-Wong, P. Zhang, and H. Y. Noh, “iLOCuS: Incentivizing vehicle mobility to optimize sensing distribution in crowd sensing,” IEEE Transactions on Mobile Computing, vol. 19, no. 8, pp. 1831–1847, 2019.

- [9] Y. Lai, Y. Xu, D. Mai, Y. Fan, and F. Yang, “Optimized large-scale road sensing through crowdsourced vehicles,” IEEE Transactions on Intelligent Transportation Systems, vol. 23, no. 4, pp. 3878–3889, 2022.

- [10] S. Kaul, R. Yates, and M. Gruteser, “Real-time status: How often should one update?” in 2012 Proceedings IEEE INFOCOM. IEEE, 2012, pp. 2731–2735.

- [11] M. Costa, M. Codreanu, and A. Ephremides, “Age of information with packet management,” in 2014 IEEE International Symposium on Information Theory. IEEE, 2014, pp. 1583–1587.

- [12] A. Kosta, N. Pappas, and V. Angelakis, “Age of information: A new concept, metric, and tool,” Foundations and Trends in Networking, vol. 12, no. 3, pp. 162–259, 2017.

- [13] Y.-P. Hsu, E. Modiano, and L. Duan, “Scheduling algorithms for minimizing age of information in wireless broadcast networks with random arrivals,” IEEE Transactions on Mobile Computing, vol. 19, no. 12, pp. 2903–2915, 2019.

- [14] Y. Sun, E. Uysal-Biyikoglu, and S. Kompella, “Age-optimal updates of multiple information flows,” in IEEE INFOCOM 2018-IEEE Conference on Computer Communications Workshops (INFOCOM WKSHPS). IEEE, 2018, pp. 136–141.

- [15] I. Kadota, A. Sinha, E. Uysal-Biyikoglu, R. Singh, and E. Modiano, “Scheduling policies for minimizing age of information in broadcast wireless networks,” IEEE/ACM Transactions on Networking, vol. 26, no. 6, pp. 2637–2650, 2018.

- [16] C. Li, S. Li, Y. Chen, T. Hou, and W. Lou, “Minimizing age of information under general models for IoT data collection,” IEEE Transactions on Network Science and Engineering, 2019.

- [17] Q. He, D. Yuan, and A. Ephremides, “On optimal link scheduling with min-max peak age of information in wireless systems,” in IEEE International Conference on Communications, 2016.

- [18] C. Zhou, H. He, P. Yang, F. Lyu, W. Wu, N. Cheng, and X. Shen, “Deep RL-based trajectory planning for AoI minimization in UAV-assisted IoT,” in the IEEE 11th International Conference on Wireless Communications and Signal Processing (WCSP), 2019.

- [19] Z. Jia, X. Qin, Z. Wang, and B. Liu, “Age-based path planning and data acquisition in UAV-assisted IoT networks,” in IEEE International Conference on Communications Workshops, 2019.

- [20] W. Li, L. Wang, and A. Fei, “Minimizing packet expiration loss with path planning in UAV-assisted data sensing,” IEEE Wireless Communications Letters, vol. 8, no. 6, pp. 1520–1523, 2019.

- [21] E. Altman, R. El-Azouzi, D. S. Menasche, and Y. Xu, “Forever young: Aging control for hybrid networks,” in Proceedings of the Twentieth ACM International Symposium on Mobile Ad Hoc Networking and Computing, 2019, pp. 91–100.

- [22] M. Zhang, A. Arafa, J. Huang, and H. V. Poor, “Pricing fresh data,” IEEE Journal on Selected Areas in Communications, vol. 39, no. 5, pp. 1211–1225, 2021.

- [23] J. He, Q. Ma, M. Zhang, and J. Huang, “Optimal fresh data sampling and trading,” in the IEEE 19th International Symposium on Modeling and Optimization in Mobile, Ad hoc, and Wireless Networks (WiOpt), 2021.

- [24] N. Modina, R. El Azouzi, F. De Pellegrini, D. S. Menasche, and R. Figueiredo, “Joint traffic offloading and aging control in 5G IoT networks,” IEEE Transactions on Mobile Computing, 2022.

- [25] X. Wang and L. Duan, “Dynamic pricing for controlling age of information,” in 2019 IEEE International Symposium on Information Theory (ISIT), 2019, pp. 962–966.

- [26] A. Al-Tamimi, F. L. Lewis, and M. Abu-Khalaf, “Discrete-time nonlinear HJB solution using approximate dynamic programming: Convergence proof,” IEEE Transactions on Systems, Man, and Cybernetics, Part B (Cybernetics), vol. 38, no. 4, pp. 943–949, 2008.

- [27] T. Dierks and S. Jagannathan, “Optimal control of affine nonlinear continuous-time systems,” in Proceedings of the 2010 American Control Conference. IEEE, 2010, pp. 1568–1573.

- [28] M. L. Puterman, Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 2014.

- [29] M. L. Littman, T. L. Dean, and L. P. Kaelbling, “On the complexity of solving markov decision problems,” ArXiv preprint arXiv:1302.4971, 2013.

- [30] M. A. Alsheikh, D. T. Hoang, D. Niyato, H.-P. Tan, and S. Lin, “Markov decision processes with applications in wireless sensor networks: A survey,” IEEE Communications Surveys & Tutorials, vol. 17, no. 3, pp. 1239–1267, 2015.

- [31] D. Zhou, M. Sheng, J. Luo, R. Liu, J. Li, and Z. Han, “Collaborative data scheduling with joint forward and backward induction in small satellite networks,” IEEE Transactions on Communications, vol. 67, no. 5, pp. 3443–3456, 2019.

- [32] Z. Xiong, J. Zhao, D. Niyato, R. Deng, and J. Zhang, “Reward optimization for content providers with mobile data subsidization: A hierarchical game approach,” IEEE Transactions on Network Science and Engineering, vol. 7, no. 4, pp. 2363–2377, 2020.

- [33] Q. Liu, H. Zeng, and M. Chen, “Minimizing age-of-information with throughput requirements in multi-path network communication,” in Proceedings of the Twentieth ACM International Symposium on Mobile Ad Hoc Networking and Computing, 2019, pp. 41–50.

- [34] A. M. Bedewy, Y. Sun, S. Kompella, and N. B. Shroff, “Age-optimal sampling and transmission scheduling in multi-source systems,” in Proceedings of the Twentieth ACM International Symposium on Mobile Ad Hoc Networking and Computing, 2019, pp. 121–130.

- [35] C. Fang, H. Lu, Y. Hong, S. Liu, and J. Chang, “Dynamic pricing for electric vehicle extreme fast charging,” IEEE Transactions on Intelligent Transportation Systems, vol. 22, no. 1, pp. 531–541, 2020.

- [36] T. Rambha and S. D. Boyles, “Dynamic pricing in discrete time stochastic day-to-day route choice models,” Transportation Research Part B: Methodological, vol. 92, pp. 104–118, 2016.

- [37] A. A. Baktayan, I. A. Al-Baltah, and A. A. Abd Ghani, “Intelligent pricing model for task offloading in unmanned aerial vehicle mounted mobile edge computing for vehicular network,” Journal of Communications Software and Systems, vol. 18, no. 2, pp. 111–123, 2022.

- [38] G. Yu, J. Hu, C. Zhang, L. Zhuang, and J. Song, “Short-term traffic flow forecasting based on markov chain model,” in IEEE IV2003 Intelligent Vehicles Symposium. Proceedings (Cat. No. 03TH8683). IEEE, 2003, pp. 208–212.

- [39] E. Meijer and J. Rouwendal, “Measuring welfare effects in models with random coefficients,” Journal of Applied Econometrics, vol. 21, no. 2, pp. 227–244, 2006.

- [40] B.-D. Kim, R. C. Blattberg, and P. E. Rossi, “Modeling the distribution of price sensitivity and implications for optimal retail pricing,” in Perspectives On Promotion And Database Marketing: The Collected Works of Robert C Blattberg. World Scientific, 2010, pp. 283–295.

- [41] C. Ewerhart, “Regular type distributions in mechanism design and -concavity,” Economic Theory, vol. 53, no. 3, pp. 591–603, 2013.

- [42] Y.-P. Hsu, E. Modiano, and L. Duan, “Age of information: Design and analysis of optimal scheduling algorithms,” in 2017 IEEE International Symposium on Information Theory (ISIT). IEEE, 2017, pp. 561–565.

- [43] D. E. Knuth, “Optimum binary search trees,” Acta informatica, vol. 1, no. 1, pp. 14–25, 1971.

- [44] F. L. Lewis, D. Vrabie, and V. L. Syrmos, Optimal control. John Wiley & Sons, 2012.

- [45] R. Bellman, “Dynamic programming,” Science, vol. 153, no. 3731, pp. 34–37, 1966.

- [46] P. Kakumanu, “Continuously discounted markov decision model with countable state and action space,” The Annals of Mathematical Statistics, vol. 42, no. 3, pp. 919–926, 1971.

- [47] A. Bemporad, M. Morari, V. Dua, and E. N. Pistikopoulos, “The explicit linear quadratic regulator for constrained systems,” Automatica, vol. 38, no. 1, pp. 3–20, 2002.

- [48] Y. Wang and S. Boyd, “Fast model predictive control using online optimization,” IEEE Transactions on Control Systems Technology, vol. 18, no. 2, pp. 267–278, 2009.

![[Uncaptioned image]](/html/2209.08711/assets/Li.jpg) |

Hongbo Li received the B.S. degree in Electronics and Electric Engineering from Shanghai Jiao Tong University, Shanghai, China, in 2019. He is currently working toward the Ph.D. degree with the Pillar of Engineering Systems and Design, Singapore University of Technology and Design (SUTD). His research interests include network economics, game theory, and mechanism design. |

![[Uncaptioned image]](/html/2209.08711/assets/Duan.jpg) |

Lingjie Duan (S’09-M’12-SM’17) received the Ph.D. degree from The Chinese University of Hong Kong in 2012. He is an Associate Professor of Engineering Systems and Design with the Singapore University of Technology and Design (SUTD). In 2011, he was a Visiting Scholar at University of California at Berkeley, Berkeley,CA, USA. His research interests include network economics and game theory, cognitive and green networks, and energy harvesting wireless communications. He is an Editor of IEEE Transactions on Wireless Communications. He was an Editor of IEEE Communications Surveys and Tutorials. He also served as a Guest Editor of the IEEE Journal on Selected Areas in Communications Special Issue on Human-in-the-Loop Mobile Networks, as well as IEEE Wireless Communications Magazine. He received the SUTD Excellence in Research Award in 2016 and the 10th IEEE ComSoc Asia-Pacific Outstanding Young Researcher Award in 2015. |