BOME! Bilevel Optimization Made Easy:

A Simple First-Order Approach

Abstract

Bilevel optimization (BO) is useful for solving a variety of important machine learning problems including but not limited to hyperparameter optimization, meta-learning, continual learning, and reinforcement learning. Conventional BO methods need to differentiate through the low-level optimization process with implicit differentiation, which requires expensive calculations related to the Hessian matrix. There has been a recent quest for first-order methods for BO, but the methods proposed to date tend to be complicated and impractical for large-scale deep learning applications. In this work, we propose a simple first-order BO algorithm that depends only on first-order gradient information, requires no implicit differentiation, and is practical and efficient for large-scale non-convex functions in deep learning. We provide non-asymptotic convergence analysis of the proposed method to stationary points for non-convex objectives and present empirical results that show its superior practical performance.

1 Introduction

We consider the bilevel optimization (BO) problem:

| (1) |

where the goal is to minimize an outer objective whose variables include the solution of another minimization problem w.r.t an inner objective . The and are the inner and outer variables, respectively. We assume that and that attains a minimum for each .

BO is useful in a variety of machine learning tasks. A canonical example is hyperparameter optimization, in which case (resp. ) is the validation (resp. training) loss associated with a model parameter and a hyperparameter , and we want to find the optimal hyperparameter to minimize the validation loss when is determined by minimizing the training loss; see e.g., Pedregosa [42], Franceschi et al. [12]. Other applications include meta learning [12], continual learning [43], reinforcement learning [52], and adversarial learning [23]. See Liu et al. [32] for a recent survey.

BO is notoriously challenging due to its nested nature. Despite the large literature, most existing methods for BO are slow and unsatisfactory in various ways. For example, a major class of BO methods is based on direct gradient descent on the outer variable while viewing the optimal inner variable as a (uniquely defined) function of . The key difficulty is to calculate the derivative which may require expensive manipulation of the Hessian matrix of via the implicit differentiation theorem. Another approach is to replace the low level optimization with the stationary condition . This still requires Hessian information, and more importantly, is unsuitable for nonconvex since it allows to be any stationary point of , not necessarily a minimizer. To the best of our knowledge, the only existing fully first-order BO algorithms111By fully first-order, we mean methods that only require information of , so this excludes methods that apply auto-differentiation or conjugate gradient that need multiple steps of matrix-vector computation. are BSG-1 [15] and BVFSM with its variants [33, 34, 35]; but BSG-1 relies on a non-vanishing approximation that does not yield convergence to the correct solution in general, and BVFSM is sensitive to hyper-parameters on large-scale practical problems and lacks a complete non-asymptotic analysis for the practically implemented algorithm.

In this work, we seek a simple and fast fully first-order BO method that can be used with non-convex functions including those appear in deep learning applications. The idea is to reformulate (1) as a single-level constrained optimization problem using the so-called value-function-based approach [10, 7]. The constrained problem is then solved by stopping gradient on the single variable that contains the higher-order information and applying a simple first-order dynamic barrier gradient descent method based on a method of Gong et al. [16]. Our contributions are: 1) we introduce a novel and fast BO method by applying a modified dynamic barrier gradient descent on the value-function reformulation of BO; 2) Theoretically, we establish the non-asymptotic convergence of our method to local stationary points (as measured by a special KKT loss) for non-convex and . Importantly, to the best of our knowledge, this work is the first to establish non-asymptotic convergence rate for a fully first-order BO method. This result is also much beyond that of Gong et al. [16] and Ji et al. [22]. 3) Empirically, the proposed method achieves better or comparable performance while being more efficient than state-of-the-art BO methods on a variety of benchmarks.

2 Background

This section provides a brief background on traditional BO methods. Please see Bard [2], Dempe and Zemkoho [7], Dempe [6] for overviews, and Liu et al. [32] for a survey on recent ML applications.

Hypergradient Descent Assume that the minimum of is unique for all so that we can write as a function of ; this is known as the low-level singleton (LLS) assumption. The most straightforward approach to solving (1) is to conduct gradient descent on as a function of . Note that

The difficulty is to compute . From implicit function theorem, it satisfies a linear equation:

| (2) |

If is invertible, we can solve for and obtain a gradient update rule on :

where denotes iteration, and similarly for the other terms. This approach is sometimes known as the hypergradient descent. However, hypergradient descent is computationally expensive: Besides requiring evaluation of the inner optimum , the main computational bottleneck is to solve the linear equation in (2). Methods have been developed that approximate (2) using conjugate gradient [42, 44, 17], Neumann series [29, 37], and related variants [14]. Another popular approximation approach is to replace with , where denotes the -th iteration of gradient descent or other optimization steps on w.r.t. starting from certain initialization. The gradient can be calculated with auto-differentiation (AD) with either forward mode [11], backward mode [12, 11, 46, 28, 1] or their variants [31]. While these approaches claim to be first-order, they require many Hessian-vector or Jacobian-vector products at each iteration and are slow for large problems.

Other examples of approximation methods include a neural surrogate method which approximates and its gradient with neural networks [38] and Newton-Gaussian approximation of the Hessian matrix with covariance of gradient [15]. Both approaches introduce non-vanishing approximation error that is difficult to control. The neural surrogate method also suffers from high training cost for the neural network.

Stationary-Seeking Methods. An alternative method is to replace the argmin constraint in (1) with the stationarity condition yielding a constrained optimization:

| (3) |

Algorithms for nonlinear equality constrained optimization can then be applied [39]. The constraint in (3) guarantees only that is a stationary point of , so it is equivalent to (1) only when is convex w.r.t. . Otherwise, the solution of (3) can be a maximum or saddle point of . This makes it problematic for deep learning, where non-convex functions are pervasive.

3 Method

We consider a value function approach [see e.g., 41, 53, 33], which yields natural first-order algorithms for non-convex and requires no computation of Hessian matrices. It is based on the observation that (1) is equivalent to the following constrained optimization (even for non-convex ):

| (4) |

where is known as the value function. Compared with the hypergradient approach, this formulation does not require calculation of the implicit derivative : Although depends on , its derivative does not depend on , by Danskin’s theorem:

| (5) |

where the second term in (5) vanishes because we have by definition of the optimum . Therefore, provided that we can evaluate at each iteration, solving (4) yields an algorithm for BO that requires no Hessian computation. In this work, we make use of the dynamic barrier gradient descent algorithm of Gong et al. [16] to solve (4). This is an elementary first-order algorithm for solving constrained optimization, but it applies only to a special case of the bilevel problem and must be extended to handle the general case we consider here.

Dynamic Barrier Gradient Descent. The idea is to iterative update the parameter to reduce while controlling the decrease of the constraint , ensuring that decreases whenever . Specifically, denote as the step size, the update at each step is

| (6) |

| (7) |

Here , , and is a non-negative control barrier and should be strictly positive in the non-stationary points of : the lower bound on the inner product of and ensures that the update in (6) can only decrease (when step size is sufficiently small) until it reaches stationary. In addition, by enforcing to be close to in (7), we decrease the objective as much as possible so long as it does not conflict with descent of .

Two straightforward choices of that satisfies the condition above are and with . We find that both choices of work well empirically and use as the default (see Section 6.2).

Practical Approximation. The main bottleneck of the method above is to calculate the and which requires evaluation of . In practice, we approximate by , where is obtained by running steps of gradient descent of w.r.t. starting from . That is, we set and let

| (8) |

for some step size parameter . We obtain an estimate of at iteration by replacing with :

We substitute into (7) to obtain the update direction . The full procedure is summarized in Algorithm 1. Note that the is viewed as a constant when defining and hence no differentiation of is performed when calculating the gradient . This differs from truncated back-propagation methods [e.g., 46] which differentiate through as a function of . Alternatively, it can be viewed as a plug-in estimator. We know that

where denotes taking the derivative w.r.t. the first variable. Since is unknown, we estimate by plugging-in to approximate :

Each step of Algorithm 1 can be viewed as taking one step (starting from ) toward solving an approximate constrained optimization problem:

| (9) |

which can be viewed as a relaxation of the exact constrained optimization formulation (4), because is a subset of .

4 Analysis

We first elaborate the KKT condition of (4) (Section 4.1), then quantify the convergence of the method by how fast it meets the KKT condition. We consider both the case when satisfies the Polyak-Łojasiewicz (PL) inequality w.r.t. , hence having a unique global optimum (Section 4.2), and when have multiple local minimum (Section 4.3).

4.1 KKT Conditions

Consider a general constrained optimization of form s.t. . Under proper regularity conditions known as constraint quantifications [40], the first-order KKT condition gives a necessary condition for a feasible point with to be a local optimum of (4): There exists a Lagrangian multiplier , such that

| (10) | ||||

and satisfies the complementary slackness condition . A common regularity condition to ensure (10) is the constant rank constraint quantification (CRCQ) condition [20].

Definition 1.

A point is said to satisfy CRCQ with a function if the rank of the Jacobian matrix is constant in a neighborhood of .

Unfortunately, the KKT condition in (10) does not hold for the bilevel optimization in (4). The CRCQ condition does not typically hold for this problem. This is because the minimum of is zero, and hence if is feasible for (4), then must attain the minimum of , yielding and if is smooth; but we could not have uniformly in a neighborhood of (hence CRCQ fails) unless is a constant around . In addition, if KKT (10) holds, we would have which happens only in the rare case when is a stationary point of both .

Instead, one can establish a KKT condition of BO through the form in (3), because there is nothing special that prevents from satisfying CRCQ with (even though we just showed that it is difficult to have CRCQ with ). Assume and are continuously differentiable, and is a point satisfying and CRCQ with . Then by the typical first order KKT condition of (3), there exists a Lagrange multiplier such that

| (11) |

This condition can be viewed as the limit of a sequence of (10) in the following way: assume we relax the constraint in (4) to where is a sequence of positive numbers that converge to zero, then we can establish (10) for each and pass the limit to zero to yield (11).

Proposition 1.

This motivates us to use the following function as a measure of stationarity of the solution returned by the algorithm:

The hope is to have an algorithm that generates a sequence that satisfies as .

Intuitively, the first term in measures how much conflicts with (how much we can decrease without increasing ), as it is equal to the squared norm of the solution to the problem The second term in measures how much the constraint is satisfied.

4.2 Convergence with unimodal

We first present the convergence rate when assuming has unique minimizer and satisfies the Polyak-Łojasiewicz (PL) inequality for all , which guarantees a linear convergence rate of the gradient descent on the low level problem.

Assumption 1 (PL-inequality).

Given any , assume has a unique minimizer denoted as . Also assume there exists such that for any , .

The PL inequality gives a characterization on how a small gradient norm implies global optimality. It is implied from, but weaker than strongly convexity. The PL-inequality is more appealing than convexity because some modern over-parameterized deep neural networks have been shown to satisfy the PL-inequality along the trajectory of gradient descent. See, for example, Frei and Gu [13], Song et al. [48], Liu et al. [30] for more discussion.

Assumption 2 (Smoothness).

and are differentiable, and and are -Lipschitz w.r.t. the joint inputs for some .

Assumption 3 (Boundedness).

There exists a constant such that , , and are all upper bounded by for any .

Theorem 1.

Remark

Note that one of the dominant terms depends on the initial value . Therefore, we can obtain a better rate if we start from a with small (hence near the optimum of ). In particular, when , choosing gives rate. On the other hand, if we start from a better initialization such that , then choosing gives .

4.3 Convergence with multimodal

The PL-inequality eliminates the possibility of having stationary points that are not global optimum. To study cases in which has multiple local optima, we introduce the notion of attraction points following gradient descent.

Definition 2 (Attraction points).

Given any , we say that is the attraction point of with step size if the sequence generated by gradient descent starting from converges to .

Assume the step size where is the smoothness constant defined in Assumption 2, one can show the existence and uniqueness of attraction point of any using Proposition 1.1 of Traonmilin and Aujol [49]. Intuitively, the attraction of is where the gradient descent algorithm can not make improvement. In fact, when , one can show that is equivalent to the stationary condition .

The set of that have the same attraction point forms an attraction basin. Our analysis needs to assume the PL-inequality within the individual attraction basins.

Assumption 4 (Local PL-inequality within attraction basins).

Assume that for any , exists. Also assume that there exists such that for any .

We can also define local variants of and as follows:

Compared with Section 4.2, a key technical challenge is that and hence can be discontinuous w.r.t. when it is on the boundary of different attraction basins; is not well defined on these points. However, these boundary points are not stable stationary points, and it is possible to use arguments based on the stable manifold theorem to show that an algorithm with random initialization will almost surely not visit them [47, 27].

Theorem 2.

Unlike Theorem 1, the rate does not improve when is small because the attraction basin may change in different iterations, eliminating the benefit of starting from a good initialization. Choosing gives rate of .

5 Related Works

The value-function formulation (4) is a classical approach in bilevel optimization [41, 53, 7]. However, despite its attractive properties, it has been mostly used as a theoretical tool, and much less exploited for practical algorithms compared with the more widely known hypergradient approach (Section 2), especially for challenging nonconvex functions and such as those encountered in deep learning. One exception is Liu et al. [33], which proposes a BO method by solving the value-function formulation using an interior-point method combined with a smoothed approximation. This was improved later in a pessimistic trajectory truncation approach [35] and a sequential minimization approach [34] (BVFSM). Similar to our approach, these methods do not require computation of Hessians, thanks to the use of value function. However, as we observe in experiments (Section 6.2), BVFSM tends to be dominated by our method both in accuracy and speed, and is sensitive to some hyperparameters that are difficult to tune (such as the coefficients of the log-barrier function in interior point method). Theoretically, Liu et al. [33, 34, 35] provide only asymptotic analysis on the convergence of the smoothed and penalized surrogate loss to the target loss. They do not give an analysis for the algorithm that was actually implemented.

Our algorithm is build up on the dynamic control barrier method of Gong et al. [16], an elementary approach for constrained optimization. Gong et al. [16] also applied their approach to solve a lexicographical optimization of form s.t. , which is a bilevel optimization without an outer variable (known as simple bilevel optimization [8]). Our method is an extension of their method to general bilevel optimization. Such extension is not straightforward, especially when the lower level problem is non-convex, requiring introducing the stop-gradient operation in a mathematically correct way. We also provide non-asymptotic analysis for our method, that goes beyond the continuous time analysis in Gong et al. [16]. A key sophistication in the theoretical analysis is that we need to control the approximation error of with at each step, which requires an analysis significantly different from that of Gong et al. [16]. Indeed, non-asymptotic results have not yet been obtained for many BO algorithms. Even for the classic hypergradient-based approach (such results are established only recently in Ji et al. [22]). We believe that we are the first to establish a non-asymptotic rate for a purely first-order BO algorithm under general assumptions, e.g. the lower level problem can be both convex or non-convex.

Another recent body of theoretical works on BO focus on how to optimize when only stochastic approximation of the objectives is provided [14, 19, 22, 51, 18, 4, 25]; there are also recent works on the lower bounds and minimax optimal algorithms [21, 22]. These algorithms and analysis are based on hypergradient descent and hence require Hessian-vector products in implementation.

6 Experiment

We conduct experiments (1) to study the correctness, basic properties, and robustness to hyperparameters of BOME, and (2) to test its performance and computational efficiency on challenging ML applications, compared with state-of-the-art bilevel algorithms. In the following, we first list the baseline methods and how we set the hyperparameters. Then we introduce the experiment problems in Section 6.1, which includes 3 toy problems and 3 ML applications, and provide the experiment results. Finally we summarize observations and findings in Section 6.2.

Baselines A comprehensive set of state-of-the-art BO methods are chosen as baseline methods. This includes the fully first-order methods: BSG-1 [15] and BVFSM [34], ; a stationary-seeking method: Penalty [39], explicit/implicit methods: ITD [22], AID-CG (using conjugate gradient), AID-FP (using fixed point method) [17], reverse (using reverse auto-differentiation) [11] stocBiO [22], and VRBO [51].

Hyperparameters Unless otherwise specified, BOME strictly follows Algorithm 1 with , , and . The inner stepsize is set to be the same as outer stepsize . The stepsizes of all methods are set by a grid search from the set . All toy problems adopt vanilla gradient descent (GD) and applications on hyperparameter optimization adapts GD with a momentum of . Details are provided in Appendix A.

6.1 Experiment Problems and Results

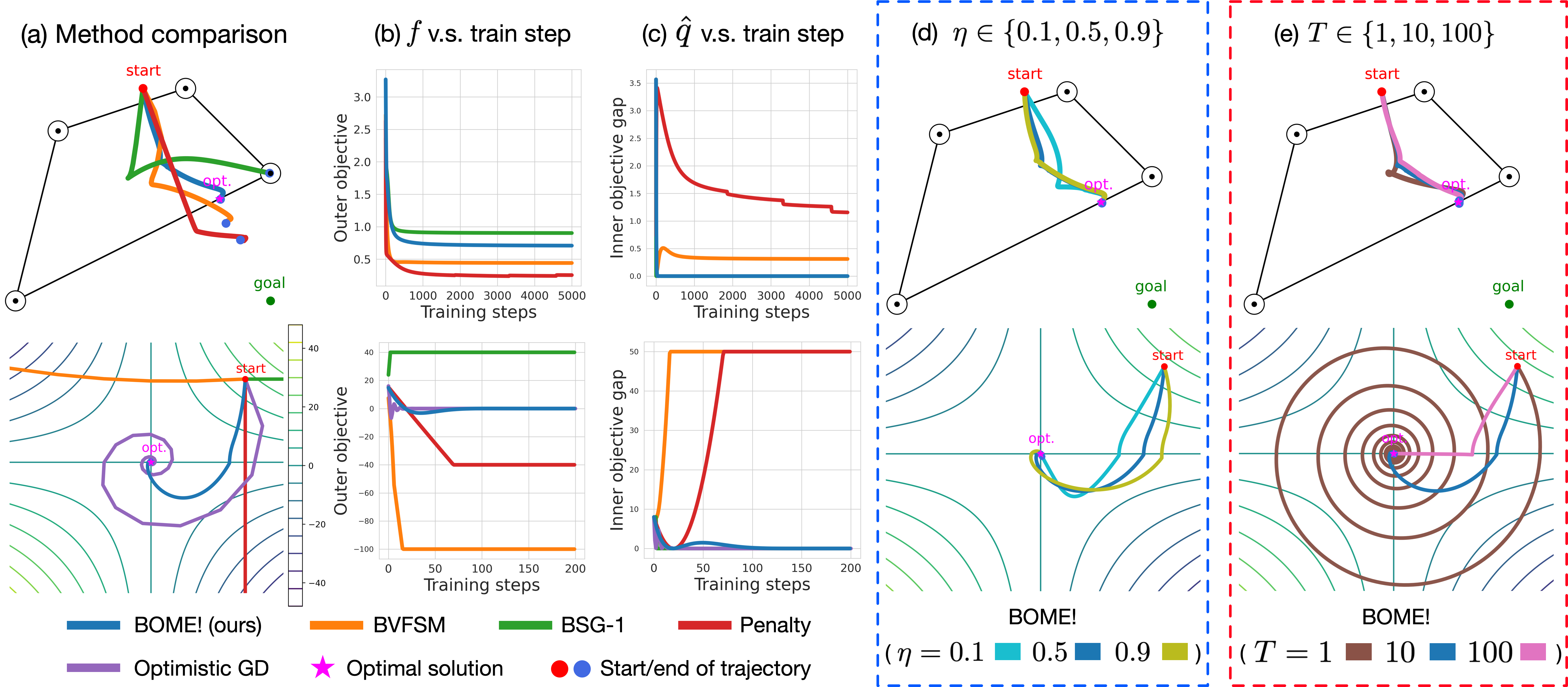

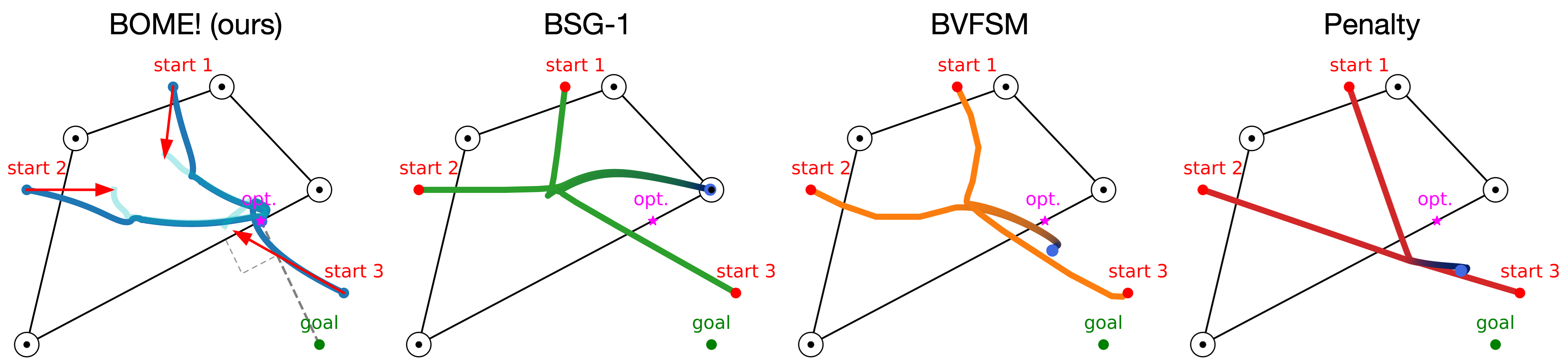

Toy Coreset Problem To validate the convergence property of BOME, we consider:

where is the softmax function, , and . The goal is to find the closest point to a target point within the convex hull of . See Fig. 1 (upper row) for the illustration and results.

Toy Mini-Max Game Mini-max game is a special and challenging case of BO where and contradicts with each other completely (e.g., ). We consider

| (12) |

The optimal solution is . Note that the naive gradient descent ascent algorithm diverges to infinity on this problem, and a standard alternative is to use optimistic gradient descent [5]. Figure 1 (lower row) shows that BOME works on this problem while other first-order BO methods fail.

Degenerate Low Level Problem Many existing BO algorithms require the low level singleton (LLS) assumption, which BOME does not require. To test this, we consider an example from Liu et al. [31]:

where and the solution is . See Fig. 4 in Appendix A.3 for the result.

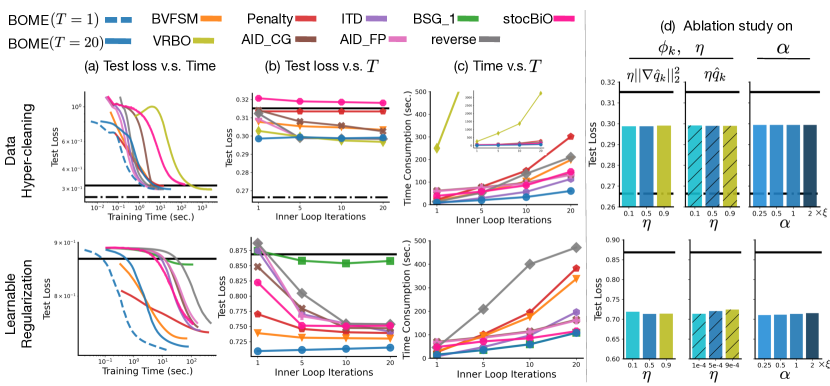

Data Hyper-cleaning We are given a noisy training set and a clean validation set . The goal is to optimally weight the training data points so that the model trained on the weighted training set yields good performance on the validation set:

where is the validation loss on , and is a weighted training loss: with and .

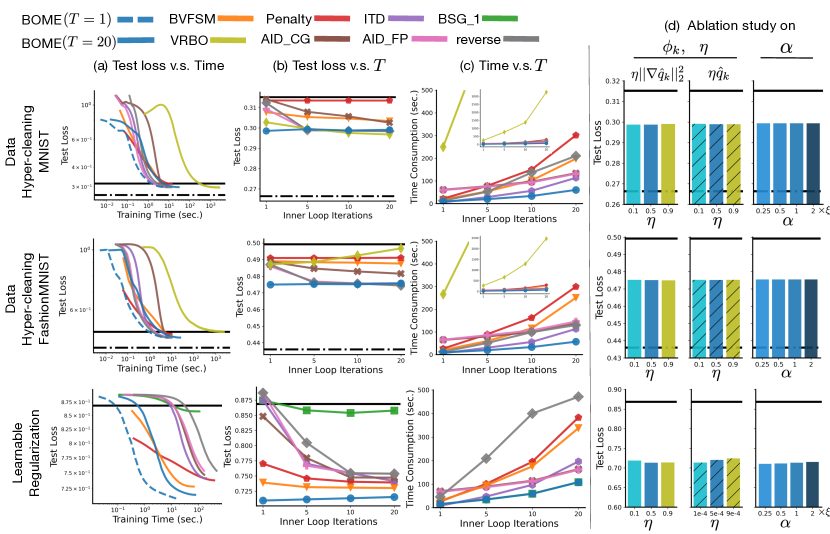

We set . For the dataset, we use MNIST [9] (FashionMNIST [50]). We corrupt 50% of the training points by assigning them randomly sampled labels. See Fig. 2 (upper panel) for the results. (Results for FashionMNIST are reported in Appendix A.4.)

Learnable Regularization We apply bilevel optimization to learn the optimal regularization coefficient on the twenty newsgroup dataset:222Dataset from https://scikit-learn.org/0.19/datasets/twenty_newsgroups.html.

where is a matrix depending on , e.g., . See Fig. 2 (lower panel) for results.

Continual Learning (CL) CL studies how to learn on a sequence of tasks in an online fashion without catastrophic forgetting of previously learned tasks. We follow the setting of contextual transformation network (CTN) from Pham et al. [43], which trains a deep neural network consisting of a quickly updated backbone network (parameterized by ) and a slowly updated controller network (parameterized by ). When training the -th task, we update by

where and are the training and validation loss available up to task . The goal is to update the controller such that the long term loss is minimized assuming is adapted to the available training loss when new tasks come. Assume the CL process terminates at time . Denote by the test accuracy of task after training on task . We measure the performance of CL by 1) the final mean accuracy on all seen tasks (), 2) how much the model forgets as measured by negative backward transfer , and 3) how fast the model learns on new tasks as measured by forward transfer . Note that .

We follow the setting of Pham et al. [43] closely, except replacing their bilevel optimizer (which is essentially ITD [22]) with BOME. See Appendix A.6 for experiment details. The results are shown in Table 1, where in addition to the bilevel algorithms, we also compare with a set of state-of-the-art CL algorithms, including MER [45], ER [3], and GEM [36]. Table 1 also includes an ‘Offline" basline – learning tasks simultaneously using a single model (which is the upper bound on performance).

| Method | PMNIST | Split CIFAR | ||||

|---|---|---|---|---|---|---|

| ACC | NBT | FT | ACC | NBT | FT | |

| Offline | - | - | - | - | ||

| MER | ||||||

| CTN (+ITD) | ||||||

| CTN (+BVFSM) | ||||||

| CTN (+BOME) | ||||||

6.2 Observations

BOME yields faster learning and better solutions at convergence Figure 1-4 show that BOME converges to the optimum of the corresponding bilevel problems and work well on the mini-max optimization and the degenerate low level problem; see also Fig.3 in Appendix A.1. In comparison, the other methods like BSG-1, BVFSM, and Penalty fail to converge to the true optimum even with a grid search over their hyperparameters. Moreover, in all three toy examples, BOME guarantees that , which is a proxy for the optimality of the inner problem, decreases to . From Fig. 2, it is observed that BOME achieves comparable or better performance than the state-of-the-art bilevel methods for hyperparameter optimization. Moreover, BOME exhibits better computational efficiency (Fig. 2), especially on the twenty newsgroup dataset where the dimension of is large. In Table 1, we find that directly plugging in BOME to the CL problem yields a substantial performance boost.

Robustness to parameter choices Besides the standard step size in typical optimizers, BOME only has three parameters: control coefficient , inner loop iteration , and inner step size . We use the default setting of , and across the experiments. From Fig. 1 (d,e) and Fig. 2 (b,d), BOME is robust to the choice of , and as varying them results in almost identical performance. Specifically, works well in many cases (see Figure 1 (e) and 2 (b)). The fact that BOME works well with a small empirically makes it computationally attractive in practice.

Choice of control barrier The control barrier is set as by default. Another option is to use . We test both options on the data hyper-cleaning and learnable regularization experiments in Fig. 2 (d), and observe no significant difference (we choose properly so that both choices of is on the same order). Hence we use as the default.

Comparison against BVFSM The most relevant baseline to BOME is BVFSM, which similarly adopts the value-function reformulation of the bilevel problems. However, BOME consistently outperform BVFSM in both converged results and computational efficiency, across all experiments. More importantly, BOME has fewer hyperparameters and is robust to them, while we found BVFSM is sensitive to hyperparameters. This makes BOME a better fit for large practical bilevel problems.

7 Conclusion and Future Work

BOME, a simple fully first-order bilevel method, is proposed in this work with non-asymptotic convergence guarantee. While the current theory requires the inner loop iterations to scale in a logarithmic order w.r.t to the outer loop iterations, we do not observe this empirically. A further study to understand the mechanism is an interesting future direction.

References

- Arbel and Mairal [2021] Michael Arbel and Julien Mairal. Amortized implicit differentiation for stochastic bilevel optimization. arXiv preprint arXiv:2111.14580, 2021.

- Bard [2013] Jonathan F Bard. Practical bilevel optimization: algorithms and applications, volume 30. Springer Science & Business Media, 2013.

- Chaudhry et al. [2019] Arslan Chaudhry, Marcus Rohrbach, Mohamed Elhoseiny, Thalaiyasingam Ajanthan, Puneet K Dokania, Philip HS Torr, and Marc’Aurelio Ranzato. On tiny episodic memories in continual learning. arXiv preprint arXiv:1902.10486, 2019.

- Chen et al. [2021] Tianyi Chen, Yuejiao Sun, and Wotao Yin. A single-timescale stochastic bilevel optimization method. arXiv preprint arXiv:2102.04671, 2021.

- Daskalakis et al. [2017] Constantinos Daskalakis, Andrew Ilyas, Vasilis Syrgkanis, and Haoyang Zeng. Training gans with optimism. arXiv preprint arXiv:1711.00141, 2017.

- Dempe [2002] Stephan Dempe. Foundations of bilevel programming. Springer Science & Business Media, 2002.

- Dempe and Zemkoho [2020] Stephan Dempe and Alain Zemkoho. Bilevel optimization. Springer, 2020.

- Dempe et al. [2021] Stephan Dempe, Nguyen Dinh, Joydeep Dutta, and Tanushree Pandit. Simple bilevel programming and extensions. Mathematical Programming, 188(1):227–253, 2021.

- Deng [2012] Li Deng. The mnist database of handwritten digit images for machine learning research. IEEE Signal Processing Magazine, 29(6):141–142, 2012.

- Dinh et al. [2010] Nguyen Dinh, B Mordukhovich, and Tran TA Nghia. Subdifferentials of value functions and optimality conditions for dc and bilevel infinite and semi-infinite programs. Mathematical Programming, 123(1):101–138, 2010.

- Franceschi et al. [2017] Luca Franceschi, Michele Donini, Paolo Frasconi, and Massimiliano Pontil. Forward and reverse gradient-based hyperparameter optimization. In International Conference on Machine Learning, pages 1165–1173. PMLR, 2017.

- Franceschi et al. [2018] Luca Franceschi, Paolo Frasconi, Saverio Salzo, Riccardo Grazzi, and Massimiliano Pontil. Bilevel programming for hyperparameter optimization and meta-learning. In International Conference on Machine Learning, pages 1568–1577. PMLR, 2018.

- Frei and Gu [2021] Spencer Frei and Quanquan Gu. Proxy convexity: A unified framework for the analysis of neural networks trained by gradient descent. Advances in Neural Information Processing Systems, 34, 2021.

- Ghadimi and Wang [2018] Saeed Ghadimi and Mengdi Wang. Approximation methods for bilevel programming. arXiv preprint arXiv:1802.02246, 2018.

- Giovannelli et al. [2021] Tommaso Giovannelli, Griffin Kent, and Luis Nunes Vicente. Bilevel stochastic methods for optimization and machine learning: Bilevel stochastic descent and darts. arXiv preprint arXiv:2110.00604, 2021.

- Gong et al. [2021] Chengyue Gong, Xingchao Liu, and Qiang Liu. Automatic and harmless regularization with constrained and lexicographic optimization: A dynamic barrier approach. Advances in Neural Information Processing Systems, 34, 2021.

- Grazzi et al. [2020] Riccardo Grazzi, Luca Franceschi, Massimiliano Pontil, and Saverio Salzo. On the iteration complexity of hypergradient computation. In International Conference on Machine Learning, pages 3748–3758. PMLR, 2020.

- Guo and Yang [2021] Zhishuai Guo and Tianbao Yang. Randomized stochastic variance-reduced methods for stochastic bilevel optimization. arXiv preprint arXiv:2105.02266, 2021.

- Hong et al. [2020] Mingyi Hong, Hoi-To Wai, Zhaoran Wang, and Zhuoran Yang. A two-timescale framework for bilevel optimization: Complexity analysis and application to actor-critic. arXiv preprint arXiv:2007.05170, 2020.

- Janin [1984] Robert Janin. Directional derivative of the marginal function in nonlinear programming. In Sensitivity, Stability and Parametric Analysis, pages 110–126. Springer, 1984.

- Ji and Liang [2021] Kaiyi Ji and Yingbin Liang. Lower bounds and accelerated algorithms for bilevel optimization. arXiv preprint arXiv:2102.03926, 2021.

- Ji et al. [2021] Kaiyi Ji, Junjie Yang, and Yingbin Liang. Bilevel optimization: Convergence analysis and enhanced design. In International Conference on Machine Learning, pages 4882–4892. PMLR, 2021.

- Jiang et al. [2021] Haoming Jiang, Zhehui Chen, Yuyang Shi, Bo Dai, and Tuo Zhao. Learning to defend by learning to attack. In International Conference on Artificial Intelligence and Statistics, pages 577–585. PMLR, 2021.

- Karimi et al. [2016] Hamed Karimi, Julie Nutini, and Mark Schmidt. Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 795–811. Springer, 2016.

- Khanduri et al. [2021] Prashant Khanduri, Siliang Zeng, Mingyi Hong, Hoi-To Wai, Zhaoran Wang, and Zhuoran Yang. A near-optimal algorithm for stochastic bilevel optimization via double-momentum. arXiv preprint arXiv:2102.07367, 2021.

- Kingma and Ba [2014] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- Lee et al. [2016] Jason D Lee, Max Simchowitz, Michael I Jordan, and Benjamin Recht. Gradient descent only converges to minimizers. In Conference on learning theory, pages 1246–1257. PMLR, 2016.

- Li et al. [2021] Junyi Li, Bin Gu, and Heng Huang. A fully single loop algorithm for bilevel optimization without hessian inverse. arXiv preprint arXiv:2112.04660, 2021.

- Liao et al. [2018] Renjie Liao, Yuwen Xiong, Ethan Fetaya, Lisa Zhang, KiJung Yoon, Xaq Pitkow, Raquel Urtasun, and Richard Zemel. Reviving and improving recurrent back-propagation. In International Conference on Machine Learning, pages 3082–3091. PMLR, 2018.

- Liu et al. [2022] Chaoyue Liu, Libin Zhu, and Mikhail Belkin. Loss landscapes and optimization in over-parameterized non-linear systems and neural networks. Applied and Computational Harmonic Analysis, 2022.

- Liu et al. [2020] Risheng Liu, Pan Mu, Xiaoming Yuan, Shangzhi Zeng, and Jin Zhang. A generic first-order algorithmic framework for bi-level programming beyond lower-level singleton. In International Conference on Machine Learning, pages 6305–6315. PMLR, 2020.

- Liu et al. [2021a] Risheng Liu, Jiaxin Gao, Jin Zhang, Deyu Meng, and Zhouchen Lin. Investigating bi-level optimization for learning and vision from a unified perspective: A survey and beyond. arXiv preprint arXiv:2101.11517, 2021a.

- Liu et al. [2021b] Risheng Liu, Xuan Liu, Xiaoming Yuan, Shangzhi Zeng, and Jin Zhang. A value-function-based interior-point method for non-convex bi-level optimization. arXiv preprint arXiv:2106.07991, 2021b.

- Liu et al. [2021c] Risheng Liu, Xuan Liu, Shangzhi Zeng, Jin Zhang, and Yixuan Zhang. Value-function-based sequential minimization for bi-level optimization. arXiv preprint arXiv:2110.04974, 2021c.

- Liu et al. [2021d] Risheng Liu, Yaohua Liu, Shangzhi Zeng, and Jin Zhang. Towards gradient-based bilevel optimization with non-convex followers and beyond. Advances in Neural Information Processing Systems, 34, 2021d.

- Lopez-Paz and Ranzato [2017] David Lopez-Paz and Marc’Aurelio Ranzato. Gradient episodic memory for continual learning. Advances in neural information processing systems, 30:6467–6476, 2017.

- Lorraine et al. [2020] Jonathan Lorraine, Paul Vicol, and David Duvenaud. Optimizing millions of hyperparameters by implicit differentiation. In International Conference on Artificial Intelligence and Statistics, pages 1540–1552. PMLR, 2020.

- MacKay et al. [2019] Matthew MacKay, Paul Vicol, Jon Lorraine, David Duvenaud, and Roger Grosse. Self-tuning networks: Bilevel optimization of hyperparameters using structured best-response functions. arXiv preprint arXiv:1903.03088, 2019.

- Mehra and Hamm [2021] Akshay Mehra and Jihun Hamm. Penalty method for inversion-free deep bilevel optimization. In Asian Conference on Machine Learning, pages 347–362. PMLR, 2021.

- Nocedal and Wright [2006] Jorge Nocedal and Stephen J. Wright. Numerical Optimization. Springer Science & Business Media, second edition, 2006.

- Outrata [1990] Jivrí V Outrata. On the numerical solution of a class of stackelberg problems. Zeitschrift für Operations Research, 34(4):255–277, 1990.

- Pedregosa [2016] Fabian Pedregosa. Hyperparameter optimization with approximate gradient. In International conference on machine learning, pages 737–746. PMLR, 2016.

- Pham et al. [2020] Quang Pham, Chenghao Liu, Doyen Sahoo, and HOI Steven. Contextual transformation networks for online continual learning. In International Conference on Learning Representations, 2020.

- Rajeswaran et al. [2019] Aravind Rajeswaran, Chelsea Finn, Sham Kakade, and Sergey Levine. Meta-learning with implicit gradients. 2019.

- Riemer et al. [2018] Matthew Riemer, Ignacio Cases, Robert Ajemian, Miao Liu, Irina Rish, Yuhai Tu, and Gerald Tesauro. Learning to learn without forgetting by maximizing transfer and minimizing interference. arXiv preprint arXiv:1810.11910, 2018.

- Shaban et al. [2019] Amirreza Shaban, Ching-An Cheng, Nathan Hatch, and Byron Boots. Truncated back-propagation for bilevel optimization. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 1723–1732. PMLR, 2019.

- Shub [2013] Michael Shub. Global stability of dynamical systems. Springer Science & Business Media, 2013.

- Song et al. [2021] Chaehwan Song, Ali Ramezani-Kebrya, Thomas Pethick, Armin Eftekhari, and Volkan Cevher. Subquadratic overparameterization for shallow neural networks. Advances in Neural Information Processing Systems, 34, 2021.

- Traonmilin and Aujol [2020] Yann Traonmilin and Jean-Francois Aujol. The basins of attraction of the global minimizers of the non-convex sparse spike estimation problem. Inverse Problems, 36(4):045003, 2020.

- Xiao et al. [2017] Han Xiao, Kashif Rasul, and Roland Vollgraf. Fashion-mnist: a novel image dataset for benchmarking machine learning algorithms. arXiv preprint arXiv:1708.07747, 2017.

- Yang et al. [2021] Junjie Yang, Kaiyi Ji, and Yingbin Liang. Provably faster algorithms for bilevel optimization. arXiv preprint arXiv:2106.04692, 2021.

- Yang et al. [2019] Zhuoran Yang, Yongxin Chen, Mingyi Hong, and Zhaoran Wang. Provably global convergence of actor-critic: A case for linear quadratic regulator with ergodic cost. 2019.

- Ye and Zhu [1995] JJ Ye and DL Zhu. Optimality conditions for bilevel programming problems. Optimization, 33(1):9–27, 1995.

Societal Impacts

This paper proposes a simple first order algorithm for bi-level optimization. Many specific instantiation of bi-level optimization such as adversarial learning and data attacking might be harmful to machine learning system in real world, as a general optimization algorithm for bi-level optimization, our method can be a tool in such process. We also develop a great amount of theoretical works and to our best knowledge, we do not observe any significant negative societal impact of our theoretical result.

Appendix A Experiment Details

We provide details about each experiment in this section. Regarding the implementation of baseline methods:

-

•

BVFSM’s implementation is adapted from https://github.com/vis-opt-group/BVFSM.

-

•

Penalty’s implementation is adapted from https://github.com/jihunhamm/bilevel-penalty.

-

•

VRBO’s implementation is adapted from https://github.com/JunjieYang97/MRVRBO.

-

•

AID-CG and AID-FP implementations are adapted from https://github.com/prolearner/hypertorch.

-

•

ITD implementation is adapted from https://github.com/JunjieYang97/stocBiO.

A.1 Toy Coreset Problem

The problem is:

where is the softmax function, , and . where is the softmax function. Here the outer objective pushes to towards while the inner objective ensures remains in the convex hull formed by 4 points in the 2D plane (e.g. ). We choose and the four points , , and . We set and . For all methods, we fix both the inner stepsize and the outer stepsize to be and set . For BVFSM and Penalty, we grid search the best hyperparameters from . For BOME, we choose and ablate over and . The visualization of the optimization trajectories over the 3 initial points are plotted in Fig. 3.

As shown, BOME successfully converges to the optimal solution regardless of the initial , while BSG-1, BVFSM and Penalty methods converge to non-optimal points. We emphasize that for BVFSM and Penalty, the convergence point depends on the choice of hyperparameters.

A.2 Toy Mini-max Game

The toy mini-max game we consider is:

| (13) |

For BOME and BSG-1, BVFSM, and Penalty methods, we again set both the inner stepsize and to be , as no significant difference is observed by varying the stepsizes. For all methods, we set the inner iteration . For BVFSM and Penalty, we grid search the best hyperparameters from .

A.3 Without LLS assumption

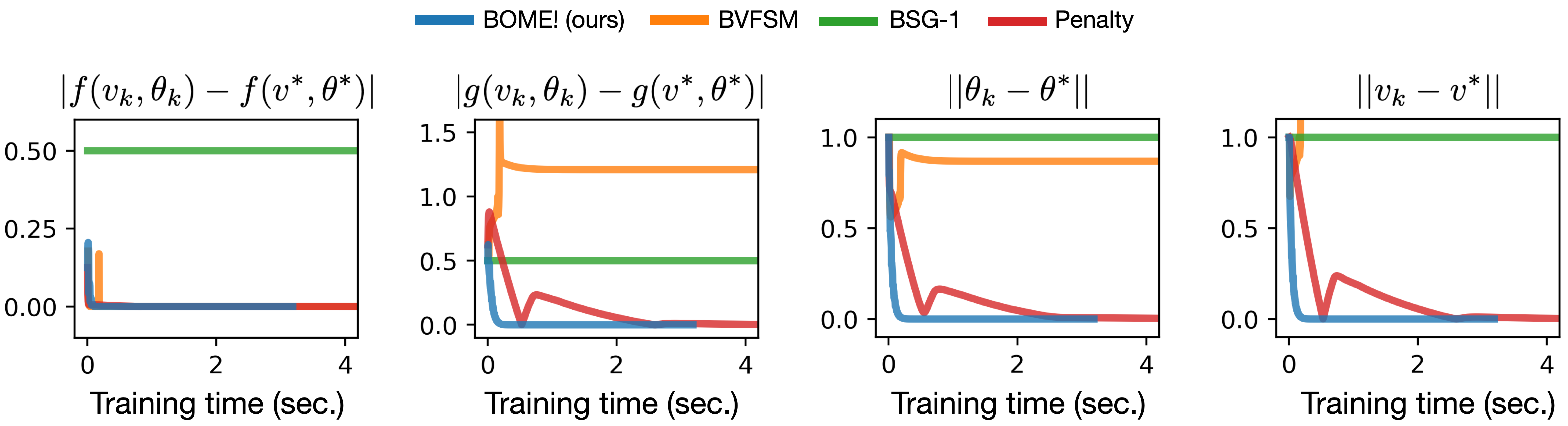

The toy example to validate whether BOME requires the low-level singleton assumption is borrowed from Liu et al. [31]:

where and the optimal solution is . Note that the inner objective has infinite many optimal solution since it is degenerated. We set both the inner and outer stepsizes to and for all methods. For BVFSM and Penalty, we grid search the best hyperparameters from . In Fig. 4, we provide the distance of to their corresponding optimal over training time in seconds. Note that BOME ensures that decreases to 0.

A.4 Data Hyper-cleaning

The bilevel problem for data hyper-cleaning is

where is the validation loss on , and is a weighted training loss: with and . The training data is of size and hence . The validation data is of size . The model is a linear model with weight and bias . Where and . For this problem, we set inner stepsize for both MNIST and FashionMNIST dataset for all methods as larger or smaller result in worse performance. As we observe ’s gradient norm is much smaller than ’s in practice, we conduct a grid search over from and also search whether to apply momentum for gradient descent, for all methods. The momentum is searched from . For BVFSM and Penalty methods, we also search for their best hyperparameters from . The model’s initial parameter is initialized from a pretrained model learned only on the corrupted data. We split the dataset into parts: train set, validation set 1, validation set 2, and the test set. For each method, the model is learned on the train set, and the hyperparameter is tuned using validation set 1. The best hyperparameter of any algorithm (e.g. stepsize, barrier coefficient, etc.) are then chosen based on the best validation performance on validation set 2. Then we report the final performance of the model on the test set. To conduct the ablation on for BOME, we search for , where is the best stepsize we found for BOME. Results on MNIST and FashionMNIST dataset are provided in Fig. 5. In the first column of Fig. 5, we compare BOME with ( and ) with baseline methods whose is chosen based on best performance on the validation set 2.

Remark: In Fig. 2 (top row), we do not include the performance of BSG-1 as we fail to find a set of hyperparameters for BSG-1 to make it work on these data hyper-cleaning problems. VRBO’s performance at convergence is tuned by hyparameter search. However, we observe that VRBO learns slowly in practice, as it requires multiple steps of Hessian vector products at each step. We notice that this is slightly inconsistent with the findings in the original paper [51]. We adapt the code from https://github.com/JunjieYang97/MRVRBO and find the original implementation is also slow. It is possible that a good set of hyperparameters can result in better performance.

A.5 Learnable regularization

The bilevel optimization formulation of the learnable rgularization problem is:

We use a linear model who’s parameter is a matrix (e.g. ). Hence . For this experiment, the inner stepsize of all methods are searched from . The outer stepsize is searched from . For BVFSM and Penalty methods, we also search for their best hyperparameters from . Similar to the experiment on Data Hyper-cleaning, we split the dataset into parts: train set, validation set 1, validation set 2, and the test set. The initial model parameter is initialized from a pretrained model without any regularization (e.g. ) to speed up the learning. To conduct the ablation on for BOME, we search for , where is the best stepsize we found for BOME. In the bottom left of Fig. 5, we compare BOME with ( and ) with baseline methods whose is chosen based on best performance on the validation set 2.

Remark: In Fig. 2 (bottom row), we do not include the performance of VRBO as we fail to find a set of hyperparameters for VRBO that works well on the learnable regularization experiment.

A.6 Continual Learning

Continual learning (CL) experiment follows closely to the setup in contextual transformation network (CTN) from Pham et al. [43], which trains a deep neural network consisting of a quickly updated backbone network (parameterized by ) a slowly updated controller network (parameterized by ). When training the -th task, the update on is solved from a bilevel optimization:

More specifically,

| (14) |

Here, and denote the semantic and episodic memory of task (e.g. they can be think of validation and training data) and is the training data of task . Hence, the inner objective learns a backbone that performs well on the training data which consists of the current task data as well as previous episodic memories . Then, the outer objective encourages good generalization on the held out validation data, which consists of the semantic memory . All hyperparameters of BOME are set to the same as those of CTN. We choose where , here is chosen from .

| Method | PMNIST | Split CIFAR | ||||

|---|---|---|---|---|---|---|

| ACC | NBT | FT | ACC | NBT | FT | |

| Offline | - | - | - | - | ||

| MER | ||||||

| GEM | ||||||

| ER-Ring | ||||||

| CTN (+ITD) | ||||||

| CTN (+BVFSM) | ||||||

| CTN (+Penalty) | ||||||

| CTN (+BOME) | ||||||

Appendix B Proof of the Result in Section 4.1

We proof Proposition 1 using Proposition 6.3 (presented below using our notation) in Gong et al. [16] by checking all the assumptions required by Proposition 6.3 in Gong et al. [16] are satisfied. Specifically, it remains to show that for any , , and is lower bounded (this is trivial as by its definition), which we prove below.

Firstly, simple calculation shows that for any ,

Here the last inequality is by . Secondly, note that as we assume is continuous, this implies that

As , we have . Using Proposition 6.3 in Gong et al. [16] gives the desired result.

Proposition B.1 (Proposition 6.3 in Gong et al. [16]).

Assume are continuously differentiable. Let be a sequence which satisfies and . Assume that is a limit point of as and satisfies CRCQ with , then there exists a vector-valued Lagrange multiplier (the same length as ) such that

Appendix C Proof of the Result in Section 4.2

We define and using Assumption 2 and 1, we are able to show that is -smooth (see Lemma 4 for details). For simplicity, we also assume that 1 throughout the proof. We use with some subscript to denote some general constant and refer reader to section E for their detailed value.

Note that defined in Section 3 changes in different iterations (as it depends on ) and so does . To avoid the confusion, we introduce several new notations. Firstly, given and , denotes the results of steps of gradient of w.r.t. starting from with step size (similar to the definition in (8)). Note that depends on , and . Our notation does not reflects this dependency on as we find it introduces no ambiguity while much simplifies the notation. Also note that when taking gradient on , the at iteration is treated as a constant and the gradient does not pass through it. To be clear, we define , where 0 denotes a zero vector with the same dimension as . Using this definition, at iteration . We also let be the solution of the dual problem of

| (15) |

That is

| (16) |

We might use for when it introduces no confusion. Also, denote and thus .

We start with several technical Lemmas showing some basic function properties.

C.1 Technical Lemmas

Lemma 1.

Under Assumption 1, for any , .

Lemma 5.

Lemma 6.

Under Assumption 3, for any , we have , where .

C.1.1 Lemmas

Now we give several main lemmas that are used to prove the result in Section 4.2.

Lemma 10.

Lemma 11.

C.2 Proof of Theorem 1

Using our definition of in (16), we have

Using Lemma 2, we know that when , we have and thus . In this case, . When , some algebra shows that

Notice that

Here the first inequality is by Lemma 2, the second inequality is by Lemma 1, the third inequality is by Lemma 5 and the last inequality is by Assumption 1 (using ). Similarly, under assumption that , ,

This implies that

We thus have

where the last inequality is by Lemma 6. Combining all the results and using by Lemma 8, we have

Using Lemma 12, we have

C.3 Proof of Lemmas

C.3.1 Proof of Lemma 9

When , by Lemma 4, we know that is -smoothness, we have

where the second and the last inequality is by Lemma 6 and the third inequality is ensured by the constraint in the local subproblem (.). And by Lemma 2, we have . Plug in the bound we have

Also notice that

where the third inequality is by Lemma 2, the equality is by and the last inequality is by Lemma 4.

C.3.2 Proof of Lemma 10

By Lemma 9, when , we have

Using those bounds, we know that

This implies that

Choosing such that where

we have

This implies that when and ,

Let . Also, when ,

Note that

This gives that in the case of ,

Define as the first iteration such that . This implies that, for any ,

When any , we show that . This can be proved by induction. At , if we have . Else if at , , . We thus have the conclusion that for any , . Combining the result, we have

where we denote

| (17) |

Let , we have the desired result.

C.3.3 Proof of Lemma 11

where is defined in (17). Also notice that

Here the first inequality is by triangle inequality, the second inequality is by Lemma 2, the third inequality is by Lemma 1, the forth inequality is by Lemma 5 and the fifth inequality is by Assumption 1. Taking summation over iteration and using Lemma 10, we have

where we define and .

C.4 Proof of Lemma 12

C.5 Proofs of Technical Lemmas

C.5.1 Proof of Lemma 1

Please see the proof of Theorem 2 in Karimi et al. [24].

C.5.2 Proof of Lemma 2

Since , we have . Thus

C.5.3 Proof of Lemma 3

C.5.4 Proof of Lemma 4

To prove the first property,

Also

C.5.5 Proof of Lemma 5

C.5.6 Proof of Lemma 6

Notice that . . When , . When ,

This concludes that .

C.5.7 Proof of Lemma 7

In the case that , . In the other case, . Thus in all cases,

C.5.8 Proof of Lemma 8

Notice that since , we have

Appendix D Proof of the Result in Section 4.3

We use with some subscript to denote some general constant and refer reader to section E for their detailed value.

For notation simplicity, given and , denotes the results of steps of gradient of w.r.t. starting from using step size (similar to the definition in (8)). And note that , where 0 denotes a zero vector with the same dimension as . We refer readers to the beginning of Appendix C for a discussion on the design of this extra notation and how it relates to the notation we used in Section 3. For simplicity, we omit the superscript in and simply use to denote in the proof.

We start with the following two Lemmas.

Lemma 13.

Under Assumption 4 and assume , for any , .

Proof.

It is easy to show that

We thus have . The result of the proof follows the proof of Theorem 2 in Karimi et al. [24]. ∎

Proof.

Now we proceed to give the proof of Theorem 2.

Note that

Note that

Notice that as ,

Also using Lemma 14, we have

This implies that

We thus have

where we define and Using the same argument in the proof of Lemma 10 and Lemma 11, we have

Here the second inequality is by Assumption 4. Choosing such that where

we have

Using Young’s inequality, given any ,

Choosing , we have

where we denote . This gives that

Using the same argument in the proof of Lemma 11,

We hence have

Similar to the proof of Lemma 12,

Using, we have

Also notice that by Assumption 4,

We hence have

Using the same argument as the proof of Theorem 1, when ,

This implies that

Appendix E List of absolute constants used in the proofs

Here we summarize the absolute constant used in the proofs.