Uncovering Regions of Maximum Dissimilarity

on Random Process Data

Abstract

The comparison of local characteristics of two random processes can shed light on periods of time or space at which the processes differ the most. This paper proposes a method that learns about regions with a certain volume, where the marginal attributes of two processes are less similar. The proposed methods are devised in full generality for the setting where the data of interest are themselves stochastic processes, and thus the proposed method can be used for pointing out the regions of maximum dissimilarity with a certain volume, in the contexts of functional data, time series, and point processes. The parameter functions underlying both stochastic processes of interest are modeled via a basis representation, and Bayesian inference is conducted via an integrated nested Laplace approximation. The numerical studies validate the proposed methods, and we showcase their application with case studies on criminology, finance, and medicine.

Keywords Functional Parameters, Multi-objective Optimization, Pairs of Random Processes, Kolmogorov metric, Set Function Optimization, Youden J Statistic

1 Introduction

Everyday millions of data patterns flow around the world at unprecedented speed, thus leading to an explosion on the demand for modeling stochastic process data—such as time series, point processes, and functional data; each of these types of data plays a key role in machine learning, as can be seen, for instance, from the recent papers of Berrendero et al. (2020), Faouzi and Janati (2020), and Xu et al. (2020). Hand in hand with this shock on demand arrived a pressing need for the development of data-intensive methods, techniques, and algorithms for learning and comparing random processes.

1.1 The Learning Problem of Interest

In this paper we deal with the following problem on the comparison of stochastic processes:

learning problem. For a pair of random processes, what is the region—with a given volume—where they statistically differ the most?

Specifically, the task of interest will entail tracking down regions with a certain volume, where the marginal attributes of two stochastic processes differ the most. Throughout, we will refer to this problem as that of uncovering regions of maximum discrimination (RMD) on random process data.

Let’s translate the learning problem into mathematical parlance. Since the target of interest consists of a set that fulfills an optimization criterion—i.e. a period of time or region over which a marginal feature of two stochastic processes differ the most—some of the main concepts in this paper can be framed as an optimization problem over a set function. The canonical problem in set function optimization is of the type,

| (1) |

where is a set function, is a set, and is the collection of feasible sets defining the constraint. Optimization problems over set functions—such as (1)—are commonplace in machine learning (e.g. Krause, 2010). For a recent review on the theory of discrete set function optimization see Wu et al. (2019). Most state of the art developments have been made on discrete or combinatorial set function optimization, especially on the class of submodular functions (e.g. Goldengorin, 2009). Our paper provides one of the first steps towards continuous set function optimization as here the aim will be to solve (1) when is a family of Borel subsets of a compact set .

As it will be seen in Section 2, the objective set function of interest in our case will be a measure of proximity between marginal features of the pair of stochastic processes of interest, whereas the collection of feasible sets introduces the constraint on the ‘size’ of the feasible regions—i.e. periods of time or space—over which the comparison is made.

1.2 Our Contributions

Our main contributions are:

- 1.

-

2.

In its most standard version, the proposed learning problem is shown to be equivalent to a continuous set function optimization on a monotone modular function, under a Lebesgue measure constraint. Hence, as a byproduct, the paper contributes to the literature on set function optimization which is mostly focused on a discrete and combinatorial framework, with a particular emphasis on monotone submodular functions (e.g. Nemhauser et al., 1978; Calinescu et al., 2011; Goldengorin, 2009; Buchbinder et al., 2017; Buchbinder and Feldman, 2018), under cardinality or matroid constraints. Little is known on continuous set function optimization, and thus the tools, concepts, and strategies devised herein can be of further interest elsewhere.

-

3.

Our approach is fully general in the sense that it applies to most random process data (including functional data, time series, and point processes). The functional parameters of the processes of interest (say mean functions, volatility functions, or intensity functions) are modelled by composing an inverse link function with a basis function representation, and Bayesian modeling is conducted via latent Gaussian models and inference is conducted via INLA (Integrated Nested Laplace Approximations) (Rue et al., 2009, 2017).

-

4.

An extension of the proposed method applies also to the context where the interest is on comparing more than one marginal feature via a multi-objective version of the set function optimization problem of interest.

-

5.

A variant of the proposed approach shows that a well-known performance measure known as Youden index and the Youden’s J statistic (e.g. Sokolova et al., 2006; Inácio de Carvalho et al., 2017) as well as the Kolmogorov metric (e.g., Gretton et al., 2012) can be regarded as particular cases of the framework developed herein.

1.3 Some Related Prior Work

While the learning problem introduced in Section 1.1 is new—and while there are novel contributions that will arise from our solution to it—there are some recent approaches in the context of functional data analysis (Ramsay and Silverman, 2002, 2006; Ferraty and Vieu, 2006; Horváth and Kokoszka, 2012) that are tangentially related to it, and that are briefly reviewed below.

Pini and Vantini (2016, 2017) propose an interval testing procedure for functional data that points out specific differences between functional populations. Also in the context of functional data, Berrendero et al. (2016) propose a discretization method consisting on learning to choose a finite collection of points in the domain of a set of functions in order to improve the performance of a functional data classifier. Martos and de Carvalho (2018) propose a Mann–Whitney type of statistic for functional data so to learn about the regions at which two processes differ the most on aspects related with symmetry. Finally, Dette and Kokot (2021) develop hypothesis tests for the equivalence of functional parameters in a two sample functional data setup.

Our approach differs from the ones mentioned above in a number of important ways. Perhaps the most important ones are that: i) here the goal is not to test hypothesis but rather to learn about regions with a given volume where two processes differ the most; ii) our approach applies to random processes in general whereas the methodologies reviewed above have mainly been designed with the context of functional data analysis in mind.

1.4 Outline of the Paper

The rest of the paper unfolds as follows. In Section 2 we introduce sets of maximum dissimilarity, present examples, and introduce the inference methods. In Section 3 we comment on extensions of the main concepts, methods, and ideas covered in Section 2. In Section 4 we report the main findings of a Monte Carlo numerical study on artificial data. In Section 5 we showcase the proposed methods on real data applications. Closing remarks are given in Section 6. Appendix A includes a selection of auxiliary facts, and the proofs of main results are included in Appendix B. Table 1 lists symbols and notation used throughout the article. We write instead of when typographically convenient.

| Symbol | Description |

|---|---|

| , | stochastic processes under comparison, that is, and |

| ground, or index, set over which processes and are defined | |

| , | functional parameters for and |

| data on proceses and | |

| sub-norm over | |

| set objective function | |

| set objective function evaluated at closed ball , that is, | |

| set objective functions in multi-objective context | |

| set of compact and convex subsets of the ground set | |

| volume functional, i.e., Lebesgue measure of in | |

| collection of feasible sets | |

| region of maximum or multi-maximum dissimilarity | |

| dissimilarity index for region of maximum dissimilarity | |

| ball of maximum or multi-maximum dissimilarity | |

| dissimilarity index for ball of maximum dissimilarity | |

| center and radius of ball of maximum dissimilarity | |

| set of all closed balls in | |

| Hausdorf distance between sets and | |

| minimum Euclidean distance between a point and set | |

| restriction of function to set | |

| boundary of set | |

| average integral symbol | |

| notation for defining correspondences (i.e. set-valued functions) |

2 Learning about Sets of Maximum Dissimilarity

2.1 Sets of Maximum Dissimilarity

A taster—some simple instances

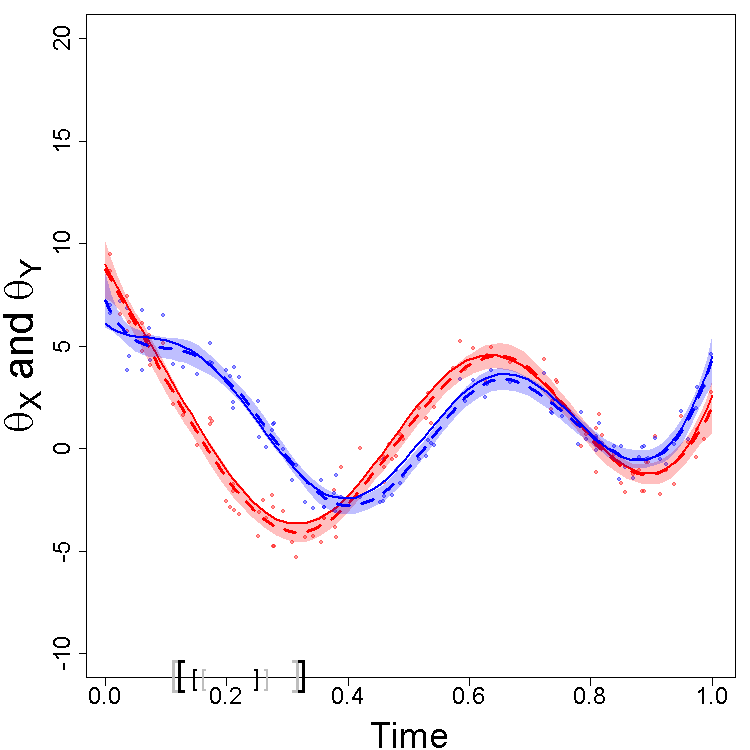

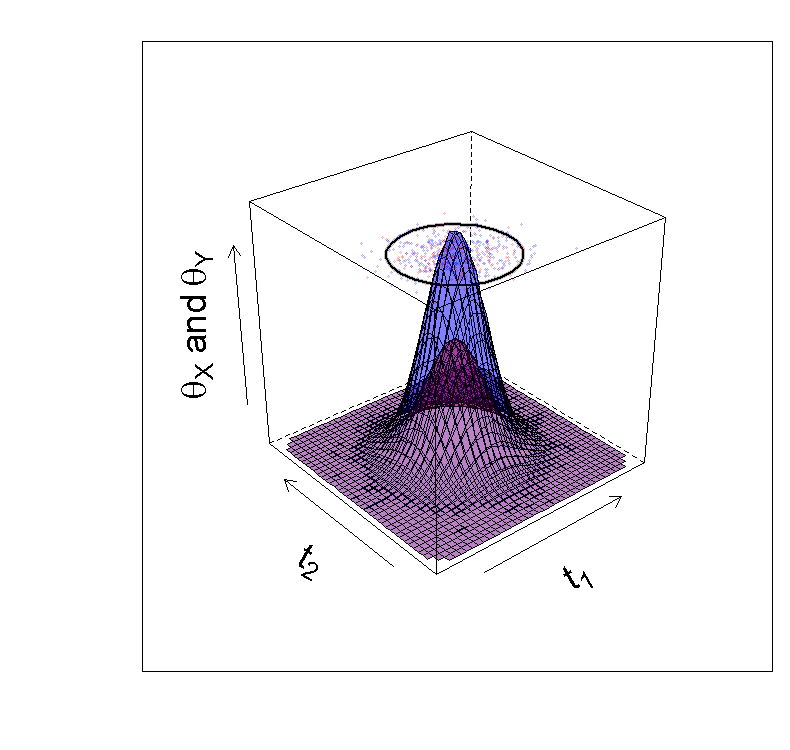

Prior to introducing sets of maximum dissimilarity in a formal fashion, we introduce some simple instances of the concept based on different parameter functions and . The respective sets of maximum dissimilarity and parameter functions for Examples 1–3 to be presented below are depicted in Fig. 1.

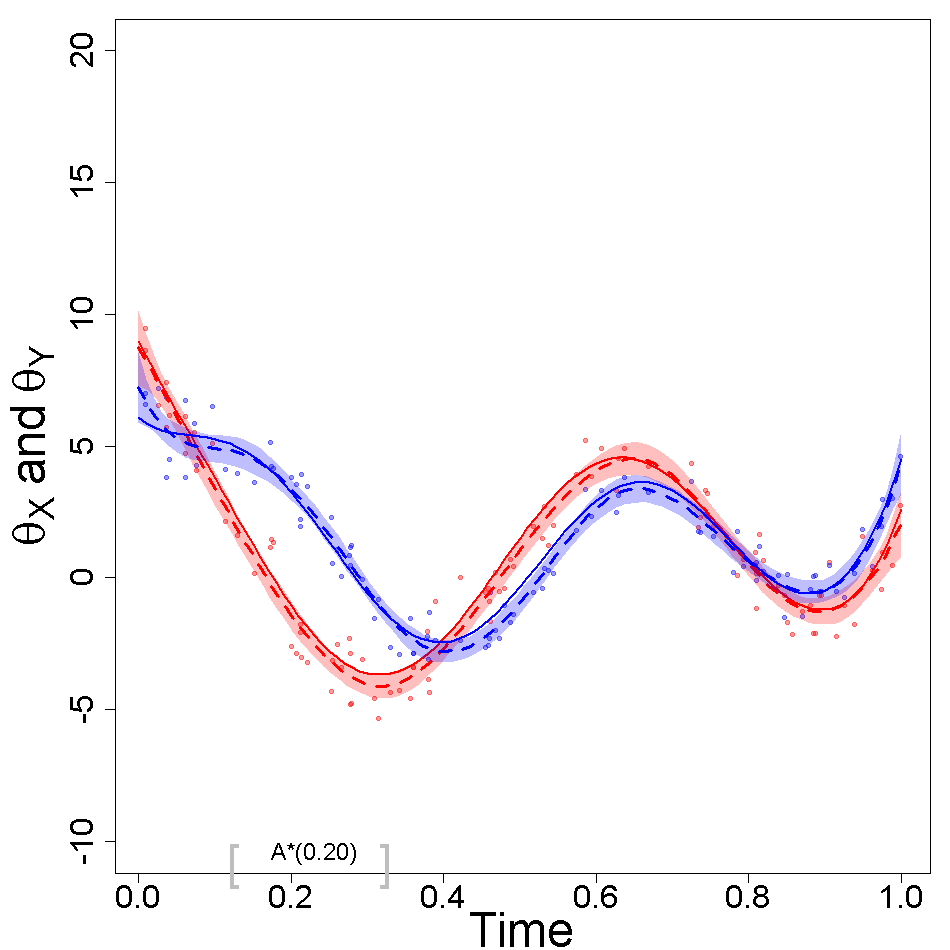

Example 1 (Mean Functions)

Let and be two stochastic processes defined on the unit interval, , with

| (2) |

where is a baseline curve, and and are zero mean Gaussian error functions. Fig. 1(a) shows the connected set of size where both mean functions differ the most in the sense.

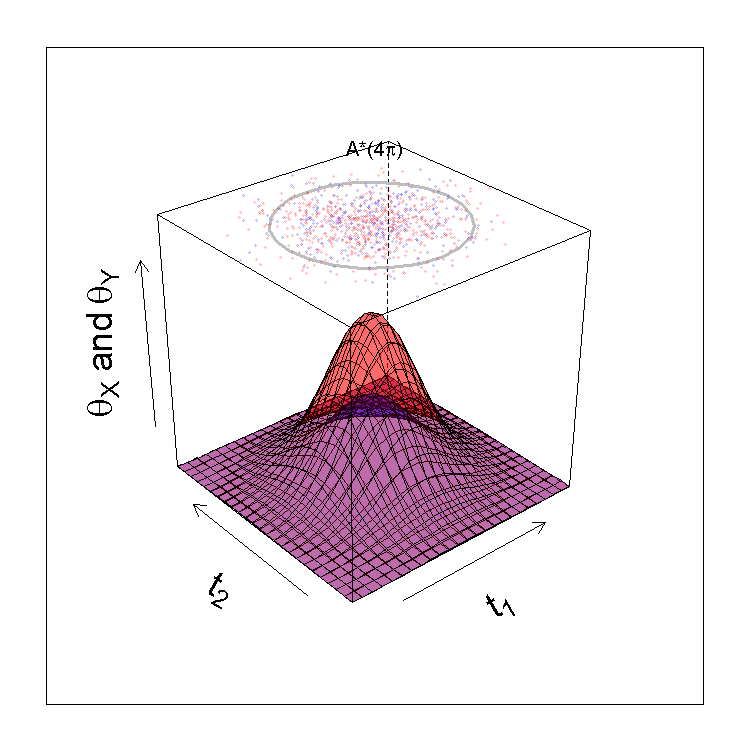

Example 2 (Intensity Functions)

Consider the intensity functions associated to two point processes

| (3) |

defined over the region with . Fig. 1(b) shows the true ball of maximum dissimilarity with area at which the two intensity functions differ the most in the sense in the case where and .

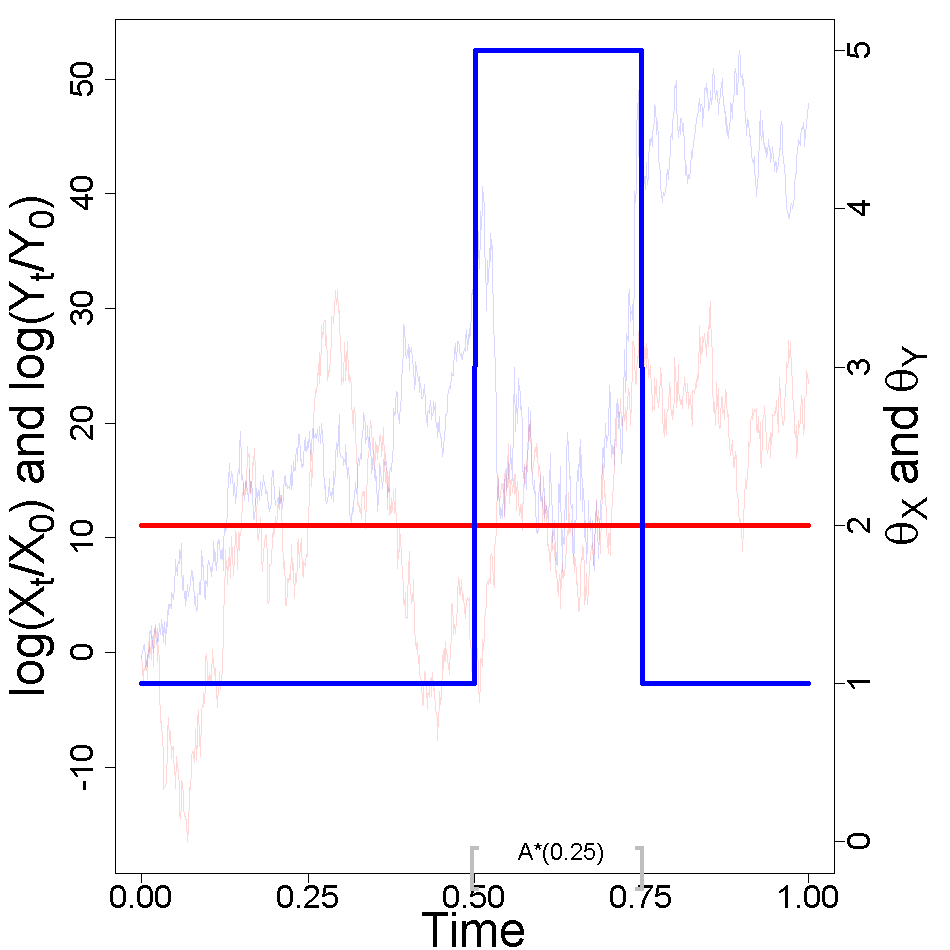

Example 3 (Volatility Functions)

Suppose and are the log returns of two stock markets, with , and that the goal is to search for the period of about a quarter (think of , so that ), where the volatility between both markets differed the most. Let

Fig. 1(c) depicts a simulated example of two artificial stock prices evolving during a period of 1 year (), along with the 3 month period over which the volatilities in both markets differed the most in the sense.

To allow for visualizations, in the examples above we focused on low-dimensional instances but the theory to be presented next holds in general for any compact ground set .

Preparations

We start by laying the groundwork and recalling background. Let and be functional parameters characterizing different marginal features of the processes and for . Throughout, we will assume that the ground set is compact and that and live in the Banach space , with , where is a measure over the Borel sets on ; we will refer to as the sub–norm over .

The learning problem from Section 1.1 boils down to searching for a set , with volume not greater than , over which the difference between and is highest. As it will be shown below, a solution to such optimization problem can be ensured to exist provided that we impose additional structure on the search domain, namely convexity and compactness. We equip the set of compact and convex subsets of the ground set , with the Hausdorff distance

Here, is the minimum Euclidean distance from the point to the set . Let be such that , where defines the maximum size of the regions of interest, and with denoting the Lebesgue measure of .

Regions of maximum dissimilarity

A compact and convex set is said to be a region of maximum dissimilarity, with volume bounded by , if it maximizes and if its volume does not exceed ; the formal definition is as follows.

Definition 1 ( Region of Maximum Dissimilarity)

Suppose and is compact. A region of maximum dissimilarity (RMD) is defined as a set that solves,

| (4) |

for a fixed . In addition, is said to be the dissimilarity index.

Some comments on Definition 1 are in order. Fig. 2 depicts the geometry underlying the set function optimization problem in (4). The optimization problem in (4) is a continuous set function optimization problem similar to (1), with

Clearly, is an increasing set function, that is if then . Also, is modular (or additive) in the sense that . While it is evident that exists for a few specific examples (say, almost everywhere, if is convex), the existence of in general is not straightforward and it is proved below in Theorem 1. RMDs and dissimilarity sets also have a number of attributes which we summarize over Theorem 1.

Theorem 1

Suppose and is compact. The quantities and obey the following properties:

-

1.

exists, for every .

-

2.

Suppose . Then, the RMDs of and are respectively and , where , , , and .

-

3.

is a distance over , for .

-

4.

is non-decreasing as a function of , for fixed .

Theorem 1 warrants some comments. The existence of RMDs (Claim 1) follows from the continuity of the volume functional and the Blaschke selection theorem (Appendix A); an RMD needs not however to be unique, as can be easily seen by considering the limiting case for which every compact and convex subset of with measure is an RMD. Claim 2 shows how RMDs are impacted by a group of linear transformations acting either on the functional parameter or over time; the assumptions and are only required for , as indeed holds more generally. It is proved in Claim 3 that defines a distance on the space of functional parameters in restricted to regions in , which implies that dissimilarity indices have a metric interpretation. Finally, Claim 4 notes that cannot decrease as increases.

Balls of maximum dissimilarity

Let be the family of all closed balls in , for , that is,

where ; to ease notation we drop the dependence of on . A more parsimonious option for modeling is to put more structure on the shape of RMDs, and this leads us to the following definition.

Definition 2 ( Ball of Maximum Dissimilarity)

Suppose and is compact. An ball of maximum dissimilarity (BMD) is defined as a set that solves,

| (5) |

for a fixed .

As in Definition 5 we refer to as the dissimilarity index for BMDs. Since the volume of an ball of radius in is

for all , where is the Gamma function, it follows that the volume constraint on BMDs, , can be rewritten as a function of the radius, that is

| (6) |

Given the similarities between the definitions of RMDs and BMDs it is not surprising that have identical properties (say, for , is a also distance and is non-decreasing). The line of attack for proving existence of BMDs is analogous to the one from Theorem 1 for RMDs but at this time Tikhonov’s theorem (Appendix A) implies compactness of the search domain. And interestingly the smoothness of is inherited by .

Theorem 2

Suppose and is compact. The quantities and obey the following properties:

-

1.

exists, for every .

-

2.

is continuous, and the “argmax” correspondence of center–radius, , defined as , is upper hemicontinuous for every , where .

A modicum on computing and numerical optimization

An important consequence of (6) is that the set function constrained optimization problem (5) that leads to BMDs, can actually be written as a standard continuous optimization problem over . Indeed, it follows from (6) that (5) is equivalent to computing

| (7) |

where . That is, the BMD is with maximizing (7), and hence in practice BMDs can be computed via derivative free optimization algorithms such as conjugate search, implicit filtering, pattern search, or Nelder–Mead (Nocedal and Wright, 2006, Ch. 9). When the center of the optimal BMD () is ‘sufficiently far’ from the boundary of , then the optimal radius () is in (6). That is, when the optimal radius is (as is a non-decreasing function of ) in which case the optimization problem in (7) resumes to searching for . This also implies that often in practice the marginal posterior of is essentially degenerated.

2.2 Learning from Data

Latent Gaussian model specification

To model BMDs in applications we consider a version of the latent Gaussian model specification in Rue et al. (2009) adapted to our setup; to ease notation, below we only refer to , and denote its functional parameter by , but all comments apply to as well. A latent Gaussian model is essentially a Bayesian generalized additive model that assigns Gaussian priors to parameters and a possibly non-Gaussian prior to its hyperparameters. Specifically, suppose that is in the exponential family, with its mean function coinciding with the functional parameter, and that

| (8) |

Here is a set of basis functions in , is a parameter, and is an inverse link function. Following Rue et al. we assign a multivariate Normal prior with a sparse precision matrix () to , which induces a Gaussian process prior on with a conditional independence property. Many functional parameters can be modeled in this way including those from Examples 1–3 and all numerical instances from Sections 4–5. The theoretical developments from Section 2.1 apply however more generally beyond the modeling assumptions made over this section.

Inla-based inference for balls of maximum dissimilarity

We now discuss how to conduct inference for balls of maximum dissimilarity. It is well-known that the latent Gaussian model described above can be fitted with an Integrated Nested Laplace Approximation (INLA) (Rue et al., 2009); the method is effective even when the dimension of the precision matrix is large, and is particularly tailored for the case where the number of hyperparameters, , is moderate (say, 6–12). INLA is a deterministic method for approximating the marginal posterior of each parameter that is based on the Laplace approximation; loosely speaking, the Laplace approximation is an approximation for integrals of the type for large , that approximates the integrand () with a Gaussian density centered at its mode and sets the covariance matrix as the inverse of the curvature (around the mode); see, for instance, Young and Smith (2005, Section 9.7). Below, we sketch some brief details on INLA; further details can be found elsewhere (Rue et al., 2009; Blangiardo and Cameletti, 2015; Rue et al., 2017; Wang et al., 2018; Krainski et al., 2018; Gómez-Rubio, 2020). The first step of INLA approximates the marginal posterior of via the Laplace approximation, that is,

| (9) |

where is the Gaussian approximation based on the mode—and the curvature around the mode—of the full conditional of , and where is the mode of this approximated full conditional for a given . Next, INLA approximates the marginal posterior of each component of . Let be the elements of , except . Similarly to (9) it follows that

| (10) |

which can be approximated using a Laplace approximation for ; faster approximations are also available from Rue et al. (2009). Finally, the marginal posterior density is obtained by numerically integrating out . Independent samples from the full posterior of can then be generated following Seppä et al. (2019, Section 2.5.2), which can then be used for estimating functionals of the parameters of interest.

Estimation and inference for balls of maximum dissimilarity can be conducted with an algorithm that combines the deterministic nature of INLA along with sampling, according to the steps below. Data from processes and are respectively denoted by and .

| (11) |

Algorithm 1 warrants some comments. Step 1 is deterministic, it follows by numerically integrating out the hyperparameters in (10), and to facilitate its implementation we recommend using the R-INLA package (Martins et al., 2013; Lindgren et al., 2015) from R (R Development Core Team, 2022), which is also equipped with routines that facilitate the implementation of Step 2 (e.g. inla.posterior.sample). Step 3 boils down to solving the optimization problem in (7) using the pair of posterior trajectories in (11). Except where mentioned otherwise, in all experiments reported below we draw times from the posterior distribution of BMDs using Algorithm 1.

3 Variants, Consequences, and Extensions

3.1 Multi-Objective RMDs

We now consider the context where the interest is on learning about regions over which a set of marginal features of two processes most differ. Let

be functional parameters characterizing marginal features of these processes. The learning problem consists of searching for a set , with volume , over which the overall difference between and is highest. Formally, the concept below entails the combination of two fields of optimization on whose interface little is known, namely: Multi-objective optimization (e.g. Pardalos et al., 2017) and set function optimization. In this section

| (12) |

denotes the set objective functions of interest, for .

Definition 3 (Region of Multi-Maximum Dissimilarity)

Suppose and is compact. The region of multi-maximum dissimilarity (RMMD) is defined as a set that solves,

| (13) |

for a fixed , where is defined as in (12). In addition, is said to be the multi-dissimilarity index.

Ideally, we would aim to simultaneously maximize all targets , for all . Yet, in practice targets may conflict each other, that is, if one is increased some other may be decreased; we illustrate this situation in Section 5.2. To give a more concrete meaning to Definition 3, an ordering concept over the collection of feasible sets is required, so to rank the corresponding objective function values. The following Pareto optimal concept induces that order, and it defines optimality via a compromise across all objective set functions, in the sense that improvements on one target cannot be made at the cost of deteriorating another target.

Definition 4 (Pareto Optimal Region of Multi-Maximum Dissimilarity)

Let be defined as in (12). The set is a Pareto optimal region of multi-maximum dissimilarity if there exists no other set such that , for all , and , for at least one .

In common with standard theory for multi-objective function, in our set function context the set of Pareto optimal RMMDs can be analytically obtained only in very specific cases, and thus we need to resort to scalarization (Pardalos et al., 2017, Ch. 2). The aim of scalarization is to reduce a multi-objective problem into a single-objective problem. Here, we define and characterize the following linear scalarization method for our set function context

| (14) |

, and we will refer to

| (15) |

as the solution to the set function linear scalarization problem with weight .

Theorem 3

Every solution to the linear scalarization problem is a Pareto optimal RMMD.

3.2 RMDs-Based on Averaging

This section shows that a simple modification of the notion of RMDs based on ‘averaging’ leads to links with other well-known concepts. To streamline the presentation of ideas we will focus in , and thus exceptionally over this section we will write to denote , and we will further set . Averaging is here understood in the usual sense of the well-known average integral symbol, , which is defined as

| (16) |

for an absolutely integrable and for and . For , the expression in (16) should be understood as the limit, , as . There are two motifs in this section:

- •

-

•

Moving beyond random processes: While the focus in the previous sections has been on modeling RMDs and BMDs for time and spatial processes, it would seem natural to employ these concepts beyond the context of stochastic processes. Thus, in this section will will be allowed to be general parameters, possibly unrelated with stochastic processes, such as distribution functions associated with random variables and .

We define the averaged or Hardy–Littlewood BMD as a ball, , that maximizes,

| (17) |

where are absolutely integrable and . As can be seen by comparing (17) with (7) the only difference between Hardy–Littlewood BMDs and standard BMDs in (7) is the use of the average integral symbol in (17) rather than the standard integral .111We will refer to these BMDs as “Hardy–Littlewood”, given that in (17) has links with the so-called Hardy–Littlewood maximal function (e.g. Tao, 2011, Section 1.6), where is absolutely integrable. The fact that exists follows by noticing that is continuous and that Tikhonov’s theorem (Appendix A) implies that the search domain, , is compact for every , as both and are themselves compact. In addition, the following proposition holds.

Proposition 1

Suppose are continuous and is compact. Then, for every it holds that , and as ,

The next example uses the lenses of Proposition 1 to show that a well-known performance measure known as Youden index (e.g. Sokolova et al., 2006; Inácio de Carvalho et al., 2017) has links with the averaged BMDs defined in (17).

Example 4 (Youden index and Kolmogorov metric)

If and are distribution functions supported on , and if we set , then maximization takes place over singletons and the Lebesgue differentiation theorem (Appendix A) yields that

Thus, when the set function optimization problem in (17), becomes a standard continuous optimization problem that can be written as

| (18) |

which is the well-known Youden index. Thus, the Youden index is an Hardy–Littlewood dissimilarity index, and the popular Youden’s J statistic (i.e. the maximizer of (18)) is a singleton averaged BMD, as in (17) with . Another consequence of (18) is that the limiting Hardy–Littlewood distance in (17) when is the well-known Kolmogorov metric (e.g., Gretton et al., 2012).

4 Numerical Study with Artificial Data

In this section we assess the performance of the proposed tools via a Monte Carlo study.

Artificial data generating processes and simulation settings

Examples 1–2 from Section 2.1 will form the basis of this numerical workout. Namely, we consider the following scenarios.

Scenario 1 (Mean Functions) BMDs between mean functions as in Example 1. Here, and are Gaussian processes with mean functions given in (2) and where the same Matérn covariance function is assumed for both processes. Specifically , where

for , where is the modified Bessel function (Abramowitz and Stegun, 1964, Section 9.6), and where , and are positive parameters, here set as . The simulated data are then a discretized version of simulated Gaussian processes evaluated over a grid on the unit interval,

with and ; the same comments apply to .

Scenario 2 (Intensity Functions) BMDs between intensity functions as in Example 2. Here, points drawn from non-homogeneous bivariate Poisson process with mean measures,

| (19) |

for . While the sample sizes in this scenario are random quantities, given by and , the mean number of simulated points over is , a simple yet accurate approximation that follows immediately from multiple Gaussian integrals. The simulated data are given by the following collection of points

with and , and where is analogously defined.

Modeling, prior specification, and posterior inference

Inferences for the BMDs were carried out by sampling and 500 times using Algorithm 1 for Scenarios 1 and 2, respectively. As can be seen from Algorithm 1, inferences for BMDs are constructed from the functional parameters, and thus we now comment on what versions of (8) have been used for fitting the latter. For Scenario 1 the identity link function was used in (8) along with B-spline basis, and the number of basis functions was selected using the DIC (Deviance Information Criterion; Spiegelhalter et al. 2002, 2014). The default uninformative priors of R-INLA have been used, which consist of diffuse priors for the ’s—i.e. and —and a long-tailed prior for the variance of the error term—i.e. a log gamma distribution, where the gamma distribution has mean and variance , with and ; see Wang et al. (2018, Section 5.2.1) for further details. For Scenario 2 we follow Simpson et al. (2016) and specify a log-Gaussian Cox process using (8) by setting a log link function, that links the intensity function with a Matérn random field using piecewise linear basis functions over a mesh, and where the ’s are Gaussian-distributed. For the parameters of the Matérn covariance function we use the PC prior approach of Fuglstad et al. (2019) setting and .

Before we move to the Monte Carlo study, we first illustrate the methods on a single run experiment for some instances of Scenarios 1 and 2.

Scenario 1

Scenario 2

One shot experiments

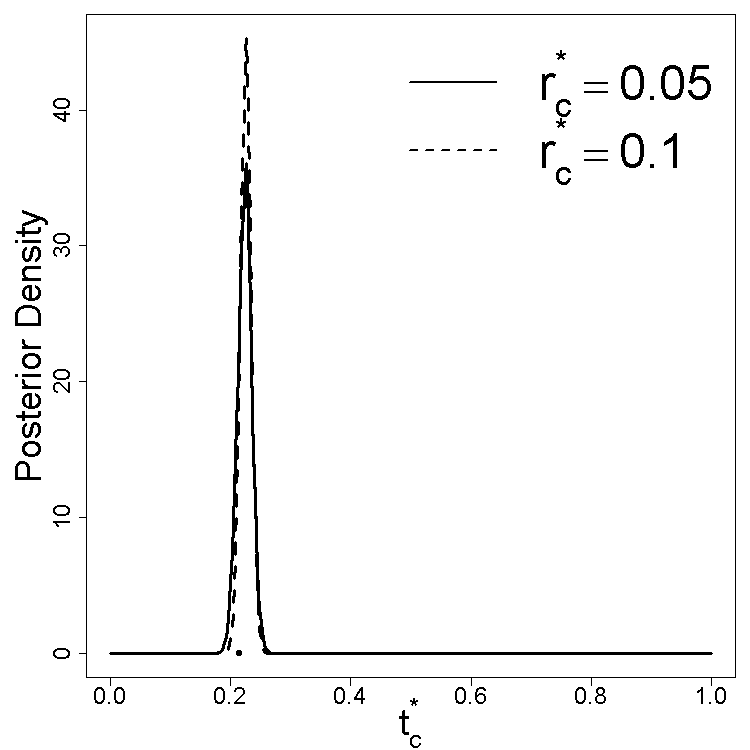

Let’s start with Scenario 1 and consider for illustration BMDs with length and . In Fig. 3(a) we show the fitted BMDs, along with the corresponding mean functions, on a one shot experiment with and . As can can be seen from Fig. 3(a), the fitted BMDs accurately recover the true and . In Fig. 3(b) we also display the marginal posterior density for the optimal center which quantifies the uncertainty surrounding the true. The marginal posterior for the radius is essentially degenerated, as predicted earlier in the comments surrounding (7), and hence not shown.

Let’s now move to Scenario 2 and consider for illustration a BMD with area . In Fig. 3(c) we depict the fitted BMD, on a one shot experiment with and , and display the fitted intensity functions. As it is evident from Fig. 3(c), the fitted BMD nicely uncovers the true, and indeed it completely overlaps it to the point that the true (depicted in gray) is barely visible.

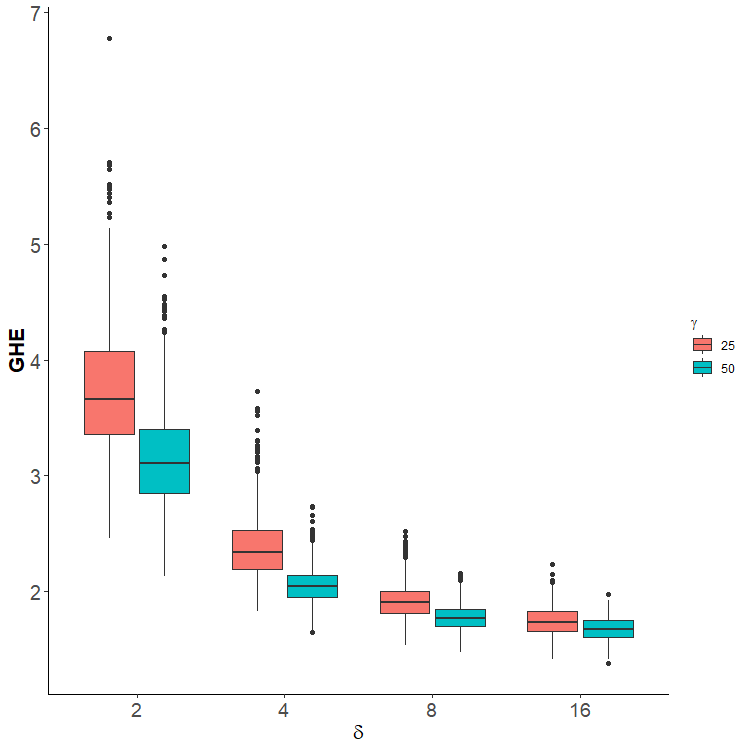

Monte carlo evidence

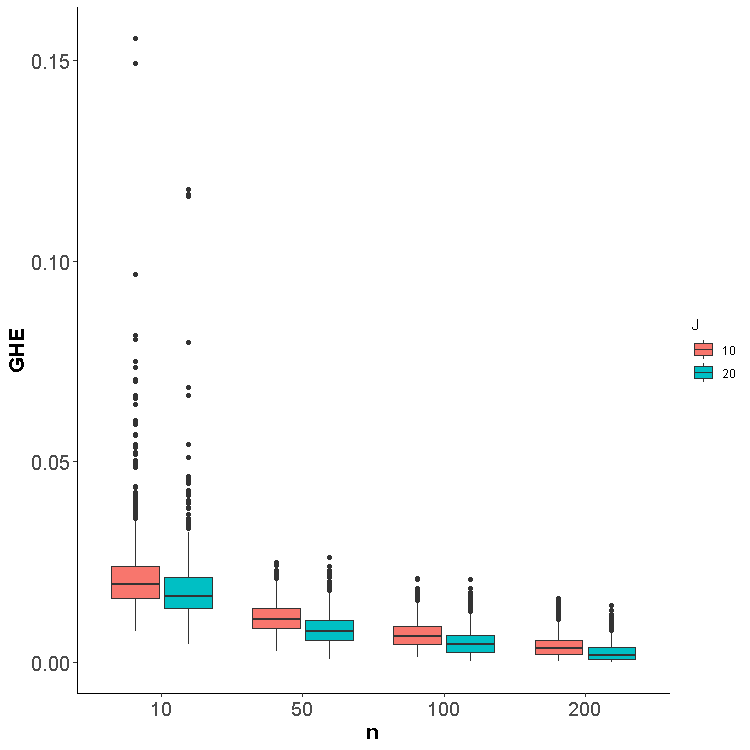

We now report the main findings of the Monte Carlo simulation study. We redo the previous one shot analyses times, considering different samples sizes, and relying on the GHE (Posterior Mean Global Hausdorff Error),

| (20) |

so to quantify how accurate on average are the estimated BMDs, , over .

| Scenario 1 Scenario 2 |

|

Some comments on the computation of (20) are in order. In Scenario 1 we use , while in Scenario 2 we use a numerical approximation of implemented using Borchers (2021). Finally, the GHE for each simulated dataset is computed as

where is the th posterior sampled BMD based on the th simulated sample, for and . As can be seen from Fig. 4, GHE tends to decrease as , and increases. Such behavior confirms the expected frequentist behavior of the methods, as and dictates the amount of simulated data for Scenario 1, and and does the same for Scenario 2. To put it differently, since larger values of these parameters imply larger sample sizes, the observed reduction in GHE as a function of the latter parameters suggests a sensible asymptotic performance of the proposed Bayesian inferences.

5 Empirical Section

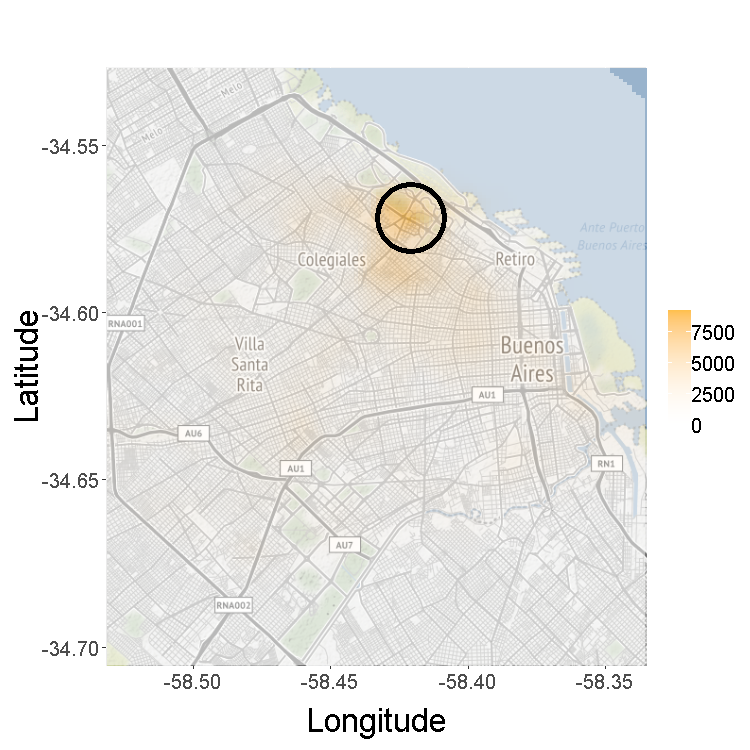

5.1 Thefts in Buenos Aires

Buenos Aires is the most dense metropolis in Argentina and its crime rates are significantly higher in comparison to the rest of the country. In this section we illustrate how the proposed method can reveal regions of the city where nonviolent crimes—such as burglary, pickpocketing or nonviolent thefts—have changed the most, comparing the years 2019 (pre COVID-19) and 2020 (when the COVID lockdown took place during several months). The data are publicly available online in the city hall web page, and consist of point process data on the latitude and longitude where thefts occurred during 2019 () and 2020 (). Here, the functional parameters of interest are the intensity functions

and its BMD will represent region of the city, of a given size, where the most noteworthy changes in thefts took place. The fitted BMDs were modeled according to (8) using again a log-Gaussian Cox process and a similar PC prior specification as in Section 4.

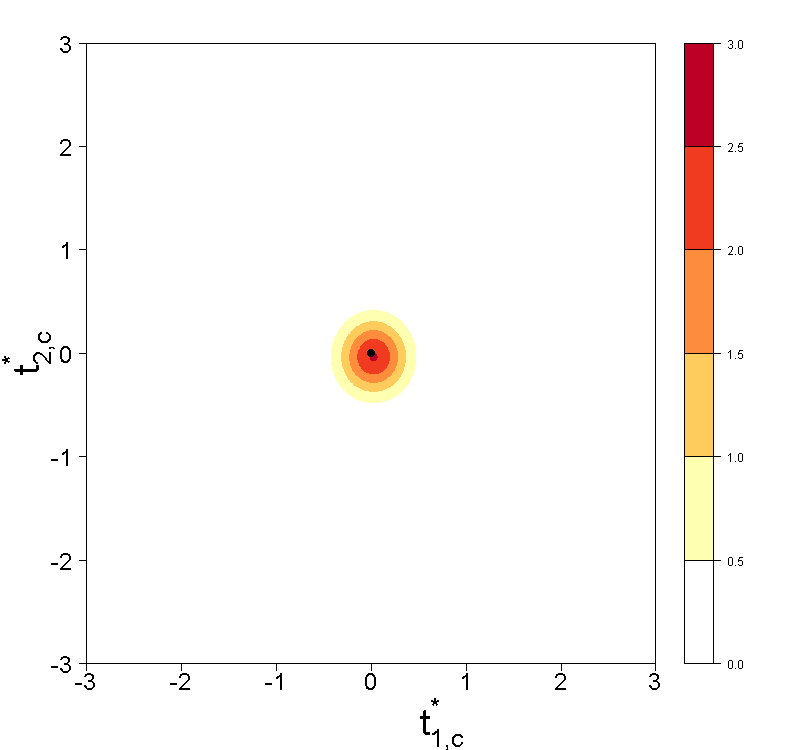

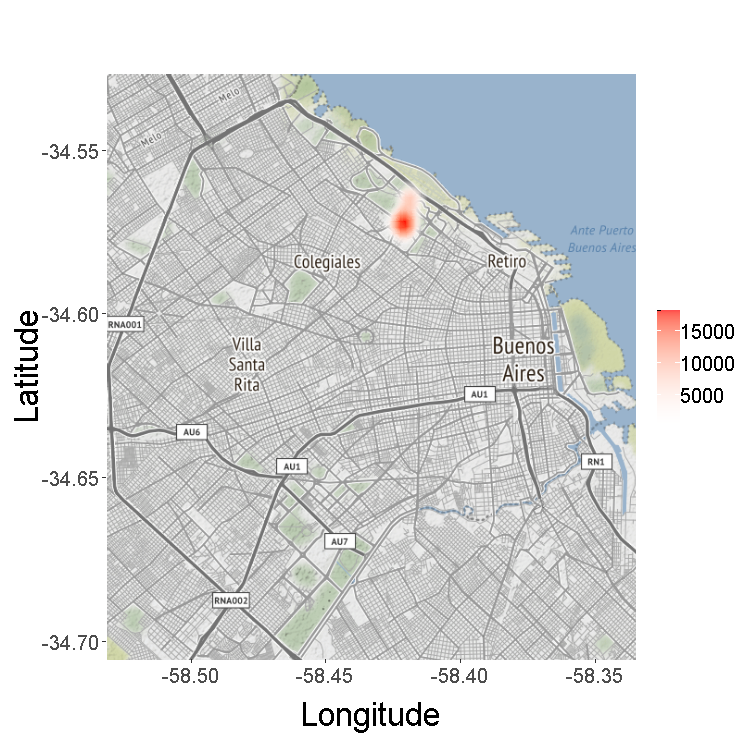

In Fig. 5(a) we depict the estimated BMD corresponding to an area of km2 along with an heat map of the differences in the estimated posterior intensity functions between consecutive years; the value of km2 was chosen for illustration as it corresponds to about twice the size of the largest neighborhood, which is Palermo. We also depict in Fig. 5(b) an heat map of the posterior density corresponding to the center of the BMD which shows that these are substantially concentrated, thus suggesting low uncertainty on the fitted BMD.

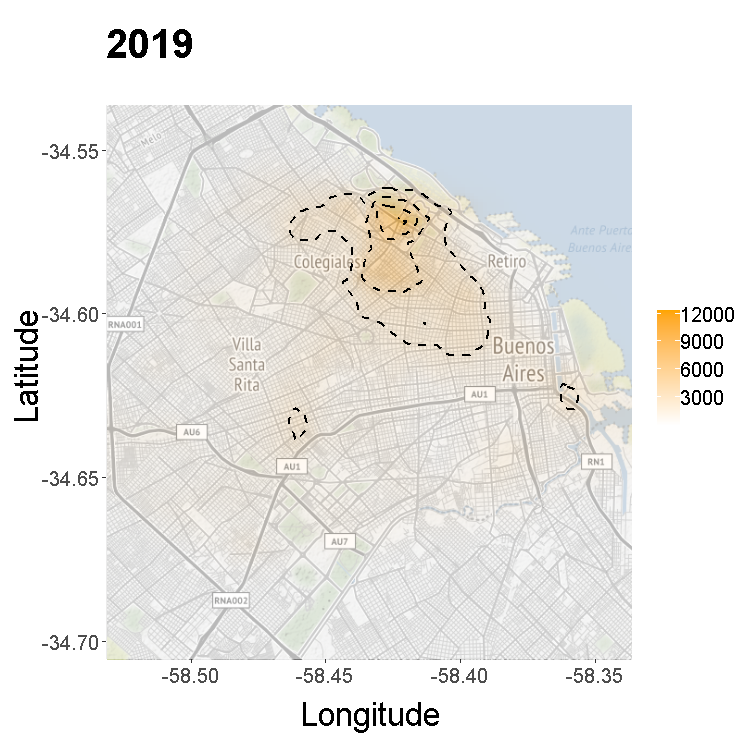

To clarify the applied meaning of such BMDs we provide some additional background on the social context surrounding the empirical analysis. In Fig. 5(c–d) we depict the fitted intensity functions corresponding to both years. As can be seen from Fig. 5, in 2019 and 2020 thefts were more likely to occur in APRV (Almagro, Palermo, Recoleta, and Villa Crespo) which are some of the neighborhoods where several commercial and touristic activities took place. Yet, important differences on the estimated intensity functions are perceived between both years. During the first half of year 2020, local authorities took strong social distancing measures such as the limitation to the access the public transportation system, restrictions on business and commerce during the day, limitations on gatherings and tourism activities, restriction to the capacity in bars and restaurants, among others. The difference on the estimated intensity functions between consecutive years evident from Fig. 5—and the implied reduction of thefts over 2020—is in line with the findings of Mohler et al. (2020) that report similar evidence on the effect of COVID-19 lockdown and social distance policies in nonviolent crime.

The BMD in Fig. 5(a) suggests that APRV (Almagro, Palermo, Recoleta, and Villa Crespo) are the neighborhoods where there was a most impactful effect of COVID-19 lockdown. To put it differently, while nonviolent crime has decreased during lockdown over the entire city, what the fitted BMD highlights is that such reduction was relatively much higher in the APRV neighborhoods.

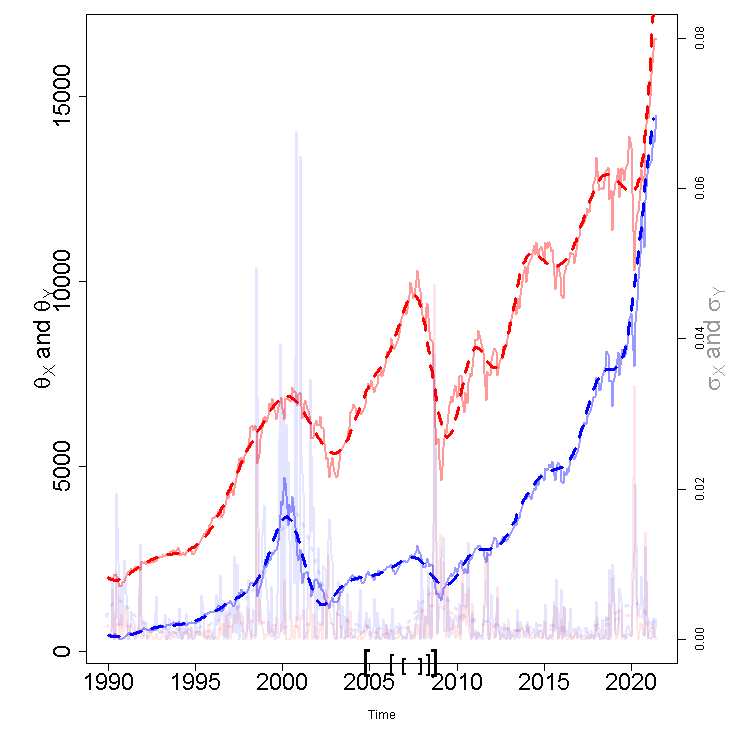

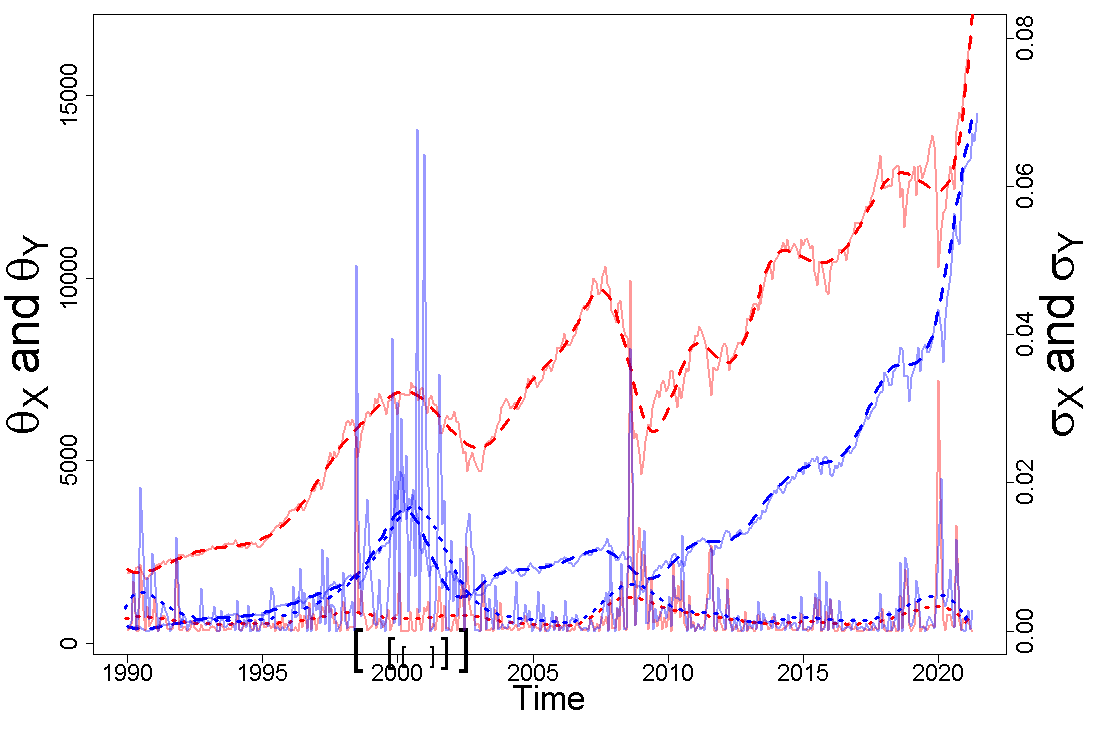

5.2 Volatility in Stock Markets

Our second illustration will shed light on the multi-objective approach from Section 3.1. Data were gathered from Yahoo Finance and consist of monthly values of the NYSE and NASDAQ composite indices from the New York Stock Exchange () and the NASDAQ Stock Exchange (), respectively. The data ranges from January 1990 to May 2021, thus covering a variety of episodes of financial turbulence such as the dotcom tech bubble that peaked around 2000, the subprime crisis that started around 2007, and the recent COVID–19 global pandemic. In the multi-objective RMD analysis to be conducted here, we will consider two functional parameters of interest: The mean values of the indices over time and the volatility of their log returns, that is,

These functional parameters were modeled according to (8) exactly as in Section 4, that is, using an identity link function and B-spline basis functions, choosing the number of basis functions using the DIC, and using the same uninformative prior.

We consider intervals of six months, one year, and two years (corresponding to , and 24) and we aim to evaluate on what periods of such length these two stock markets differed the most—in terms of both average returns as well as volatility. We thus seek for the interval of time that as in (15) maximizes the following scalarized set function optimization problem,

| (21) |

where is the scalarization parameter and

It follows from Theorem 3 that every solution to the linear scalarization problem (21) is a Pareto optimal BMMD (ball of multi-maximum dissimilarity), and hence Pareto optimal BMMDs obtained by linear scalarization have the nice feature of allowing one to put more emphasis on the mean values or on volatilities according to how we set . That is, by setting or , we only consider volatilities or mean values respectively and the analysis corresponds to a standard BMD, while for absolute values in differences between mean functions are more important than those in volatilities as increases. In terms of computing we adapt Algorithm 1 to the multi-objective context. That is, inference about the BMMDs is conducted by sampling times from the posteriors for means and volatilities—and rather than solving (7) as in Algorithm 1—we now solve the scalarized set function optimization problem in (21).

BMD for mean

BMD for volatility

Multi-objective BMD for mean–volatility

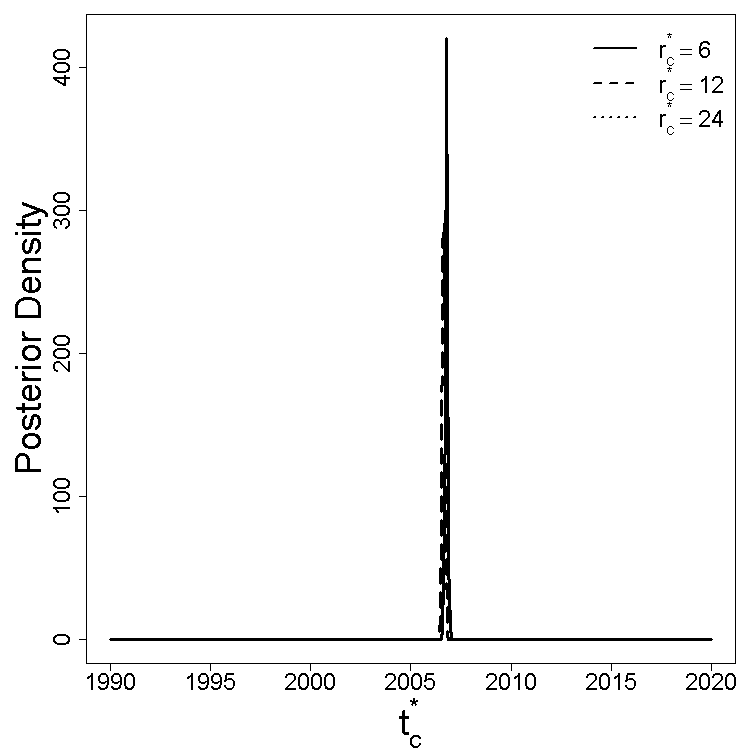

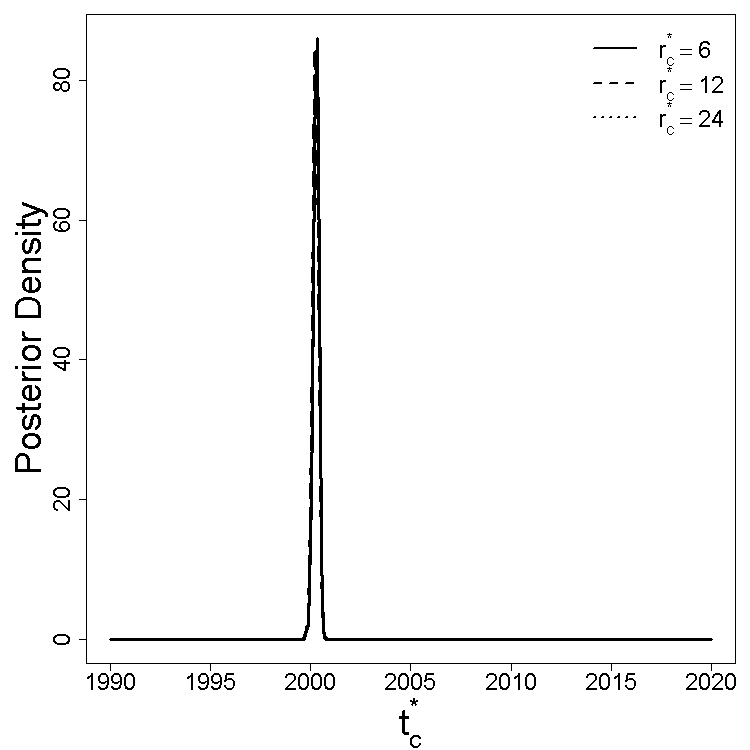

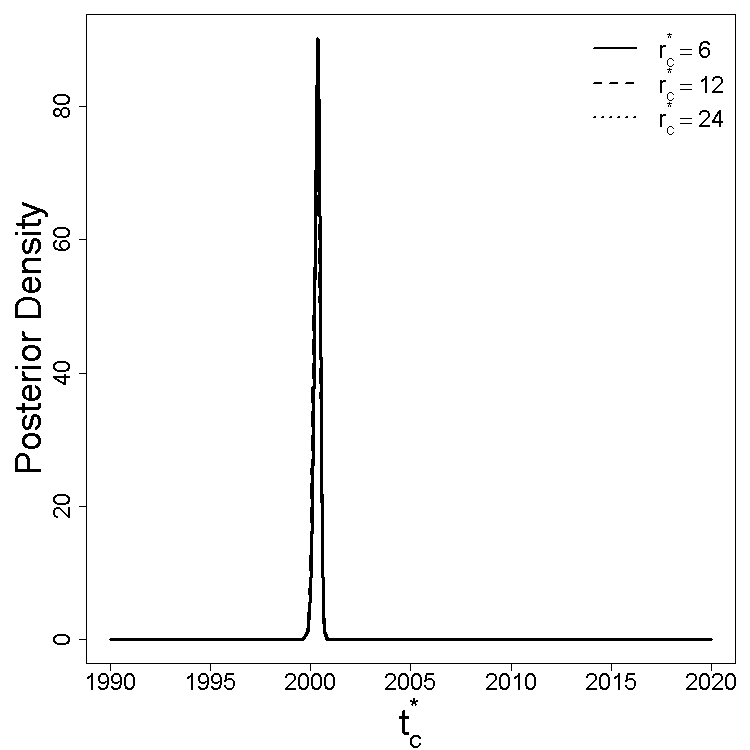

In Fig. 6 we compare the results of the single BMD analysis [panels (a) to (d)] versus the multi-objective analysis [panels (e) and (f)] considering a value of corresponding to a period of six months, one year, and two years. As can be seen from Fig. 6(a–b), the BMD associated with the mean () concentrates around the subprime crisis, indicating that July 2006 to July 2008 is the period over which mean levels of NYSE and NASDAQ differed the most. In Fig. 6(c–d), we see that the BMD associated with volatility () ranges from October 1999 to October 2001—which corresponds to the dotcom bubble burst. Finally, the multi-objective approach with is depicted in Fig. 6 (e–f) and it suggests that volatility has a greater control on the objective function in (21); that is, even when we set —that is, even when we set more emphasis on the differences in means rather than the differences in volatility—we still get a similar result as setting , as we end up recovering the period of the dotcom bubble burst as can be seen from Fig. 6(e–f).

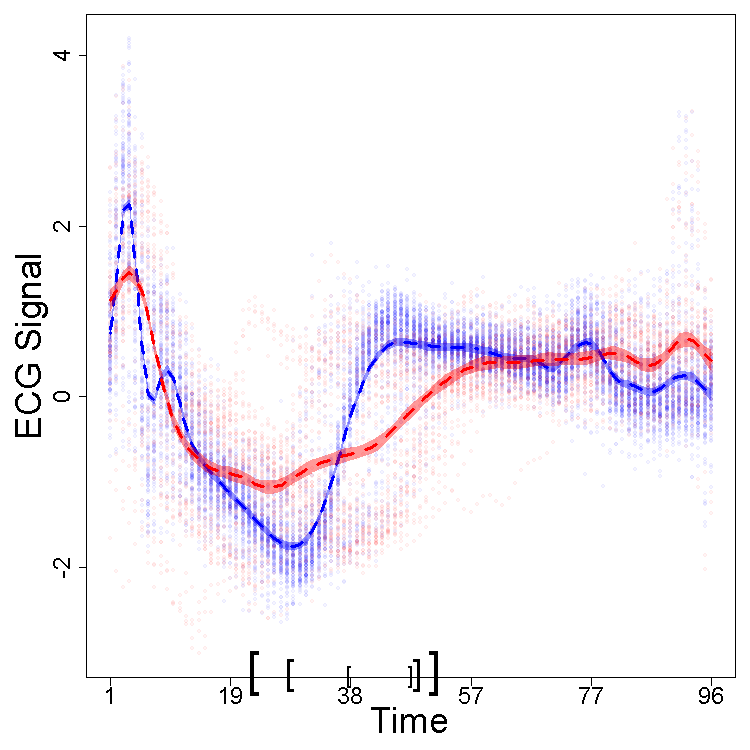

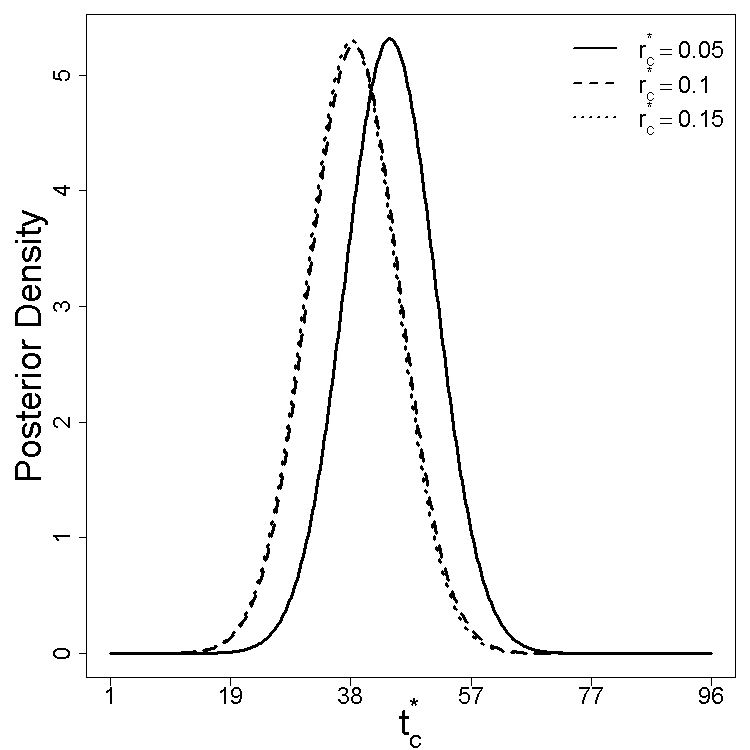

5.3 Electrocardiogram Data (ECG200)

For our final illustration we use the ECG200 dataset contributed by Olszewski (2001). The data is the result of monitoring electrical activity recorded during one heartbeat and it consists of 200 ECG signals sampled at 96 time instants, corresponding to 133 normal heartbeats () and 67 myocardial infarction signals (); the data are publicly available from the UCR Time Series Classification and Clustering website.

In this illustration, the functional parameters of interest are the mean functions of ECG signals for both classes (normal heartbeat , and myocardial infarction ) and one of the goals of the analysis is to track down periods, of a given length, over a cardiac cycle where the differences between the two classes is most pronounced. To model these functional parameters the Gaussian process prior specification in (8) was once more applied using an identity link, B-spline basis functions, the DIC to select the number of basis functions, and a Matérn covariance function with the PC prior of Fuglstad et al. (2019) setting and .

In Fig. 7(a), we plot the fitted posterior estimates for a sequence of BMDs (, , and ) using brackets in the time axis, along with the raw data, and the fitted mean functions with 95% credible bands. The obtained BMDs uncover periods of a given length where we observe largest differences between the estimated mean ECG functions. Informally, we may think of such BMDs as corresponding to intervals of about 10–30 deciseconds, since the 96 time instants cover about a cardiac cycle for all subjects and thus are not expected to last longer than 1 second. The fitted BMD centers are localized around the time instants 22–55. All in all, the analysis suggests that while normal heartbeats and myocardial infarction signals have similar ‘peaks’ at the beginning of the sample period (i.e. they have similar Q waves, in ECG signal analysis terminology), immediately in the period right after (i.e. over their ST segments) they greatly differ.

We close the analysis with two final remarks. First, in this illustration the fitted BMDs verify the chained inclusions , but this property does not hold in general—nor for the fitted BMDs, nor for the true ones; counterexamples can be constructed either numerically or analytically. Second, although BMDs are unrelated to classification, since the ECG200 dataset is a popular benchmark for new classifiers it may be sensible to ask whether the accuracy of some classifiers at discriminating outcome classes (diseased–nondiseased) can be improved by focusing on BMDs rather than treating the entire time horizon equally; we leave such open problem for future analysis.

6 Closing Remarks

Regions of maximum dissimilarity and their variants are here proposed as a tool for acquiring knowledge on the region with a given size where two stochastic processes differ the most. The proposed learning problem is shown to be equivalent to a continuous set function optimization on a monotone modular function, under a Lebesgue measure constraint. As a byproduct, the paper contributes to the literature on set function optimization which thus far is focused on a discrete and combinatorial framework, and which has been focused on monotone submodular functions (e.g. Nemhauser et al., 1978; Calinescu et al., 2011; Goldengorin, 2009; Buchbinder et al., 2017; Buchbinder and Feldman, 2018), typically under cardinality or matroid constraints.

The existence of the proposed regions of maximum dissimilarity is nontrivial but we prove their existence, and illustrate with artificial and real data that it only requires a moderate computational investment to learn them from data. The proposed methods are developed in full generality for the setting where the data of interest are themselves stochastic processes, and thus the proposed toolbox can be used for unveiling the regions of maximum dissimilarity with a given volume, for a variety of random process data. All modeling was framed within a latent Gaussian framework, with inference being conducted using the Integrated Nested Laplace Approximation; clearly, other computational approaches could have been employed as well, including, for example, variational inference (Blei et al., 2017).

A multi-objective version of the proposed framework is also devised so to learn about multi-objective RMDs, where several functional parameters are considered—each characterizing a specific feature of the processes being compared. In addition, another variant of the method to which we refer to as Hardy–Littlewood BMDs showcases that the current framework includes the Youden index and the Youden’s J statistic as well as the Kolmogorov metric as particular cases.

While the theoretical developments from Section 2.1 establish the existence of general compact and convex sets of maximum dissimilarity, BMDs turn out be a much convenient simplification for a variety of reasons. First, numerical optimization is much more challenging with general RMDs, whereas for BMDs it is relatively simple as can be seen from (7). Second, the inference for general RMDs would entail averaging posterior simulated RMDs—that is, averaging sets—whereas with BMDs we just need to compute posterior mean of the -dimensional centre-radius pair.

Acknowledgments. We thank, without implicating, Vanda Inácio de Carvalho for comments and feedback and Finn Lindgren for discussions on INLA. MdC was partially supported by FCT (Fundação para a Ciência e a Tecnologia, Portugal) through the projects PTDC/MAT-STA/28649/2017 and UID/MAT/00006/2019.

Appendix A Technical Details and Auxiliary Lemmata

In this section we state some auxiliary facts that will be used to prove the main results of this paper. Beyond the auxiliary lemmata to be stated below we use some basic facts from measure, topology, and convex analysis, such as, for example, Lebesgue differentiation theorem (e.g. Tao, 2011, Theorem 1.6.19), Tikhonov’s theorem (Waldmann, 2014, Theorem 5.3.1), and the well-known fact that the volume functional is continuous in the space of convex bodies (Schneider, 2014, Theorem 1.8.16), under the Hausdorff metric.

Recall that Tikhonov’s theorem implies that from the Cartesian product of two compact sets results a compact set. In addition, recall that Lebesgue differentiation theorem implies that if is an absolutely integrable function, then for almost every ,

where .

We now present the auxiliary lemmata. Blaschke selection theorem is a classical result on convex analysis; the version stated below can be found, for instance, in Benyamini (1998). In addition, we also recall below two key results on optimization of correspondences (i.e. set-valued functions), namely Berge’s maximum theorem and the product of correspondences theorem; the versions below can be found in Aliprantis and Border (2006, Theorems 17.31 and 17.28).

Lemma 1 (Blaschke selection theorem)

The set of all compact convex subsets of a fixed compact subset of is compact under the Hausdorff metric.

Lemma 2 (Berge’s maximum theorem)

Let be a continuous correspondence between topological spaces with nonempty compact values, and suppose that is continuous. Define the “value function” by

and the correspondence of maximizers by

Then:

-

1.

The value function is continuous.

-

2.

The “argmax” correspondence has nonempty compact values.

-

3.

If is Hausdorff, then the “argmax” correspondence is upper hemicontinuous.

Lemma 3 (Product of correspondences theorem)

The product of correspondences obeys the following properties:

-

1.

The product of a family of upper hemicontinuous correspondences with compact values is upper hemicontinuous with compact values.

-

2.

The product of a finite family of lower hemicontinuous correspondences is lower hemicontinuous.

Appendix B Proofs of Main Results

B.1 Proof of Theorem 1

Claim 1. We start by showing that

is compact, for every where is the family of compact and convex subsets of the ground set . Recall that by the Blaschke selection theorem (Lemma 1), is compact under the Hausdorff metric. Further, since the volume functional is continuous (Schneider, 2014, Theorem 1.8.16), and given that is the preimage of the closed set , it follows that is a closed subset of and hence it is compact.

Observe next that maximizing is equivalent to maximizing , for , and as we show next is upper semicontinuous under the Hausdorff metric, for every . Let in , for a fixed . It can be easily shown that (e.g. Schneider and Weil, 2008, Theorem 12.3.6)

| (22) |

Combining (22) with Fatou’s lemma yields that

thus showing that is upper semicontinuous under the Hausdorff metric, for every . The final step of the proof is tantamount to a standard argument used for proving Weierstrass theorem. Let . By definition, for every there exists a maximizing sequence such that . By compactness, we can assume that . Upper semicontinuity of implies that

and on the other hand we have since is the supremum. This proves that is the maximum of , subject to , and hence exists that solves (4).

Claim 2. First, observe that

from where it follows that a set that maximizes also maximizes ; that is, for all . Second, it follows from the change of variables formula that

where . Thus,

and hence, .

Claim 3. Note first that , for all . Also, it holds that if and only if in ; indeed, implies that , for every , which is only possible if in , as . Finally, the triangle inequality for and yields that

hence concluding the proof.

Claim 4. First, we note that an increase in represents augmenting the search domain as

This combined with the fact that the set objective function is non-decreasing ( implies ) yields that , for .

B.2 Proof of Theorem 2

Claim 1. As a consequence of Tikhonov’s theorem (Appendix A), the search domain is compact for every . Next, it is a routine exercise to prove that , is continuous for all as both and are compact. The final result then follows from Weierstrass theorem.

Claim 2. Let be fixed and set The proof uses Berge’s maximum theorem (Lemma 2) which, as can be seen from Appendix A, claims that a value function is continuous provided that both the objective function and the constraint correspondence are continuous. In our setup, the value function is

where , and the constraint correspondence is , defined by

| (23) |

Thus, we just have to prove that in (23) is continuous, given that the objective function is trivially continuous for all . Continuity of follows immediately from the product of correspondences theorem (Lemma 3), which yields that is continuous as both and are compacted-valued, and is a continuous function for every . Finally, upper semicontinuity of the argmax correspondence,

follows also from Berge’s maximum theorem as is Hausdorff.

B.3 Proof of Theorem 3

Suppose by contradiction that is the solution to the set function linear scalarization problem (15), for a fixed , but that was not a Pareto optimal RMMD; then, there would exist a Pareto improvement , with , so that , for all , and , for at least an . But then,

which is a contradiction as solves the set function linear scalarization problem.

B.4 Proof of Proposition 1

The proof of the first claim is straightforward. For every ,

The second claim follows directly from the Lebesgue differentiation theorem (Appendix A).

References

- Abramowitz and Stegun (1964) Milton Abramowitz and Irene A Stegun. Handbook of Mathematical Functions. Dover, New York, 1964.

- Aliprantis and Border (2006) CD Aliprantis and KC Border. Infinite Dimensional Analysis. Springer, New York, 2006.

- Benyamini (1998) Yoav Benyamini. Applications of the universal surjectivity of the cantor set. The American Mathematical Monthly, 105(9):832–839, 1998.

- Berrendero et al. (2016) José R Berrendero, Antonio Cuevas, and José L Torrecilla. Variable selection in functional data classification: A maxima-hunting proposal. Statistica Sinica, pages 619–638, 2016.

- Berrendero et al. (2020) José R Berrendero, Beatriz Bueno-Larraz, and Antonio Cuevas. On Mahalanobis distance in functional settings. Journal of Machine Learning Research, 21(9):1–33, 2020.

- Blangiardo and Cameletti (2015) Marta Blangiardo and Michela Cameletti. Spatial and Spatio-temporal Bayesian Models with R-INLA. Wiley, New York, 2015.

- Blei et al. (2017) David M Blei, Alp Kucukelbir, and Jon D McAuliffe. Variational inference: A review for statisticians. Journal of the American statistical Association, 112(518):859–877, 2017.

- Borchers (2021) Hans W. Borchers. pracma: Practical Numerical Math Functions, 2021. URL https://cran.r-project.org/web/packages/pracma/pracma.pdf. R package version 2.3.6.

- Buchbinder and Feldman (2018) Niv Buchbinder and Moran Feldman. Submodular functions maximization problems. In Handbook of Approximation Algorithms and Metaheuristics, 2nd ed, pages 753–788. Chapman and Hall/CRC, Boca Raton, FL, 2018.

- Buchbinder et al. (2017) Niv Buchbinder, Moran Feldman, and Roy Schwartz. Comparing apples and oranges: Query trade-off in submodular maximization. Mathematics of Operations Research, 42(2):308–329, 2017.

- Calinescu et al. (2011) Gruia Calinescu, Chandra Chekuri, Martin Pal, and Jan Vondrák. Maximizing a monotone submodular function subject to a matroid constraint. SIAM Journal on Computing, 40(6):1740–1766, 2011.

- Dette and Kokot (2021) Holger Dette and Kevin Kokot. Bio-equivalence tests in functional data by maximum deviation. Biometrika, 108(4):895–913, 2021. ISSN 0006-3444. doi: 10.1093/biomet/asaa096. URL https://doi.org/10.1093/biomet/asaa096.

- Faouzi and Janati (2020) Johann Faouzi and Hicham Janati. pyts: A python package for time series classification. Journal of Machine Learning Research, 21(46):1–6, 2020. URL http://jmlr.org/papers/v21/19-763.html.

- Ferraty and Vieu (2006) Frédéric Ferraty and Philippe Vieu. Nonparametric Functional Data Analysis: Theory and Practice. Springer, New York, 2006.

- Fuglstad et al. (2019) Geir-Arne Fuglstad, Daniel Simpson, Finn Lindgren, and Håvard Rue. Constructing priors that penalize the complexity of gaussian random fields. Journal of the American Statistical Association, 114(525):445–452, 2019.

- Goldengorin (2009) Boris Goldengorin. Maximization of submodular functions: Theory and enumeration algorithms. European Journal of Operational Research, 198(1):102–112, 2009.

- Gómez-Rubio (2020) Virgilio Gómez-Rubio. Bayesian Inference with INLA. Chapman and Hall/CRC, address=Boca Raton, FL, 2020.

- Gretton et al. (2012) Arthur Gretton, Karsten M Borgwardt, Malte J Rasch, Bernhard Schölkopf, and Alexander Smola. A kernel two-sample test. Journal of Machine Learning Research, 13(1):723–773, 2012.

- Horváth and Kokoszka (2012) Lajos Horváth and Piotr Kokoszka. Inference for Functional Data with Applications. Springer, New York, 2012.

- Inácio de Carvalho et al. (2017) V. Inácio de Carvalho, M. de Carvalho, and A. J. Branscum. Nonparametric Bayesian covariate-adjusted estimation of the Youden index. Biometrics, 73(4):1279–1288, 2017.

- Krainski et al. (2018) Elias Krainski, Virgilio Gómez-Rubio, Haakon Bakka, Amanda Lenzi, Daniela Castro-Camilo, Daniel Simpson, Finn Lindgren, and Håvard Rue. Advanced Spatial Modeling with Stochastic Partial Differential Equations using R and INLA. Chapman and Hall/CRC, Boca Raton, FL, 2018.

- Krause (2010) Andreas Krause. SFO: A toolbox for submodular function optimization. Journal of Machine Learning Research, 11(38):1141–1144, 2010. URL http://jmlr.org/papers/v11/krause10a.html.

- Lindgren et al. (2015) Finn Lindgren, Håvard Rue, et al. Bayesian spatial modelling with R-INLA. Journal of Statistical Software, 63(19):1–25, 2015.

- Martins et al. (2013) Thiago G Martins, Daniel Simpson, Finn Lindgren, and Håvard Rue. Bayesian computing with INLA: New features. Computational Statistics & Data Analysis, 67:68–83, 2013.

- Martos and de Carvalho (2018) G. Martos and M. de Carvalho. Discrimination surfaces with application to region-specific brain asymmetry analysis. Statistics in Medicine, 11(37):1859–1873, 2018.

- Mohler et al. (2020) George Mohler, Andrea L Bertozzi, Jeremy Carter, Martin B Short, Daniel Sledge, George E Tita, Craig D Uchida, and P Jeffrey Brantingham. Impact of social distancing during COVID-19 pandemic on crime in Los Angeles and Indianapolis. Journal of Criminal Justice, 68:101692, 2020.

- Nemhauser et al. (1978) George L Nemhauser, Laurence A Wolsey, and Marshall L Fisher. An analysis of approximations for maximizing submodular set functions—I. Mathematical Programming, 14(1):265–294, 1978.

- Nocedal and Wright (2006) Jorge Nocedal and Stephen Wright. Numerical Optimization. Springer, New York, 2006.

- Olszewski (2001) Robert T Olszewski. Generalized feature extraction for structural pattern recognition in time-series data. Technical report, Carnegie-Mellon University, School of Computer Science, 2001.

- Pardalos et al. (2017) Panos M Pardalos, Antanas Žilinskas, and Julius Žilinskas. Non-convex Multi-objective Optimization. Springer, New York, 2017.

- Pini and Vantini (2016) Alessia Pini and Simone Vantini. The interval testing procedure: A general framework for inference in functional data analysis. Biometrics, 72(3):835–845, 2016.

- Pini and Vantini (2017) Alessia Pini and Simone Vantini. Interval-wise testing for functional data. Journal of Nonparametric Statistics, 29(2):407–424, 2017.

- R Development Core Team (2022) R Development Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2022.

- Ramsay and Silverman (2006) James O. Ramsay and B. W. Silverman. Functional Data Analysis. Springer, New York, 2006.

- Ramsay and Silverman (2002) James O Ramsay and Bernard W Silverman. Applied Functional Data Analysis: Methods and Case Studies. Springer, New York, 2002.

- Rue et al. (2009) Håvard Rue, Sara Martino, and Nicolas Chopin. Approximate Bayesian inference for latent Gaussian models by using integrated nested Laplace approximations. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 71(2):319–392, 2009.

- Rue et al. (2017) Håvard Rue, Andrea Riebler, Sigrunn H Sørbye, Janine B Illian, Daniel P Simpson, and Finn K Lindgren. Bayesian computing with inla: A review. Annual Review of Statistics and Its Application, 4:395–421, 2017.

- Schneider (2014) Rolf Schneider. Convex Bodies: The Brunn–Minkowski Theory. Cambridge University Press, Cambridge, 2014.

- Schneider and Weil (2008) Rolf Schneider and Wolfgang Weil. Stochastic and Integral Geometry. Springer, New York, 2008.

- Seppä et al. (2019) Karri Seppä, Håvard Rue, Timo Hakulinen, Esa Läärä, Mikko J Sillanpää, and Janne Pitkäniemi. Estimating multilevel regional variation in excess mortality of cancer patients using integrated nested Laplace approximation. Statistics in Medicine, 38(5):778–791, 2019.

- Simpson et al. (2016) Daniel Simpson, Janine Baerbel Illian, Finn Lindgren, Sigrunn H Sørbye, and Havard Rue. Going off grid: Computationally efficient inference for log-Gaussian Cox processes. Biometrika, 103(1):49–70, 2016.

- Sokolova et al. (2006) Marina Sokolova, Nathalie Japkowicz, and Stan Szpakowicz. Beyond accuracy, F-score and ROC: A family of discriminant measures for performance evaluation. In Australasian Joint Conference on Artificial Intelligence, pages 1015–1021. Springer, 2006.

- Spiegelhalter et al. (2002) David J Spiegelhalter, Nicola G Best, Bradley P Carlin, and Angelika Van Der Linde. Bayesian measures of model complexity and fit. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 64(4):583–639, 2002.

- Spiegelhalter et al. (2014) David J Spiegelhalter, Nicola G Best, Bradley P Carlin, and Angelika Van der Linde. The deviance information criterion: 12 years on. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(3):485–493, 2014.

- Tao (2011) Terence Tao. An Introduction to Measure Theory. American Mathematical Society, Providence, RI, 2011.

- Waldmann (2014) Stefan Waldmann. Topology: An Introduction. Springer, New York, 2014.

- Wang et al. (2018) Xiaofeng Wang, Yuryan Yue, and Julian J Faraway. Bayesian regression modeling with INLA. Chapman and Hall/CRC, Boca Raton, FL, 2018.

- Wu et al. (2019) Wei-Li Wu, Zhao Zhang, and Ding-Zhu Du. Set function optimization. Journal of the Operations Research Society of China, 7(2):183–193, 2019.

- Xu et al. (2020) Ganggang Xu, Ming Wang, Jiangze Bian, Hui Huang, Timothy R. Burch, Sandro C. Andrade, Jingfei Zhang, and Yongtao Guan. Semi-parametric learning of structured temporal point processes. Journal of Machine Learning Research, 21(192):1–39, 2020.

- Young and Smith (2005) G. A Young and Richard L Smith. Essentials of Statistical Inference. Cambridge University Press, Cambridge, UK, 2005.