Biology-inspired geometric representation of probability and applications to completion and options’ pricing

Department of Mathematics

Bar Ilan University

Ramat-Gan, Israel

Abstract

Geometry constitutes a core set of intuitions present in all humans, regardless of their language or schooling [1]. Could brain’s built in machinery for processing geometric information take part in uncertainty representation? For decades already traders have been citing the price of uncertainty based FX optional contracts in terms of implied volatility, a dummy variable related to the standard deviation, instead of pricing with units of money. This work introduces a methodology for geometric representation of probability in terms of implied volatility and attempts to find ways to approximate certain probability distributions using intuitive geometric symmetry.

In particular, it is shown how any probability distribution supported on and having finite expectation may be represented with a planar curve whose geometric characteristics can be further analyzed. Log-normal distributions are represented with circles centered at the origin. Certain non-log-normal distributions with bell-shaped density profiles are represented by curves that can be closely approximated with circles whose centers are translated away from the origin. Only three points are needed to define a circle while it represents the candidate probability density approximating the distribution along the entire . Just three numbers: scaling and translations along the and axes map one circle to another. It is possible to introduce equivalence classes whose member distributions can be obtained by transitive actions of geometric transformations on any of corresponding representations.

Approximate completion of probability with non-circular shapes and cases when probability is supported outside of are considered too. Proposed completion of implied volatility is compared to the vanna-volga method.

1 Motivation

Geometric mechanisms constitute an essential part of conscious and subconscious cognitive processes of humans, e.g. [1, 2]. Geometric representation of uncertainty proposed here leads to a simple and intuitive procedure for approximation of several common families of probability distributions. Presumably, evolution causes biological systems to optimize the computational load of their performance; therefore, representation of uncertainty in human cognition may follow computational sub-optimality. Brain’s built in ability to process geometric information is utilized for visual, motor and other cognitive tasks; its involvement into processing uncertainty may be computationally beneficial to reduce recruitment of additional computational circuits. The above biological rationale is mainly conceptual and proposes perspectives for empirical and computational studies.

The proposed methodology relies on both:

-

1.

The way the uncertainty is priced by human professionals: options’ traders. Traders measure uncertainty with implied volatility that, roughly speaking, stands for the -scaled standard deviation of . Correct value of implied volatility being plugged into the Black-Scholes-Merton formula111Used for pricing future difference between the future asset price the value of . results in the market price of vanilla option with strike .

-

2.

Intuitive geometric concepts, for instance translation in plane.

Geometric visualization generally helps to get an intuitive understanding of different mathematical concepts and to find solutions to problems. For example, an effective teaching of fractions is based on “cutting a pie”222Henri Poincaré said [3]: ”If you want to teach fractions either you divide cakes, even in a virtual way or you bring an apple to the classroom. In all other cases students will continue adding numerators and adding denominators”., normal distribution with two variables can be identified with ellipse, integral of a scalar function is identified with area under a curve; geometric symmetries allow to solve or simplify certain differential equations [4, 5], and so on.

The proposed approach establishes geometric connection among different probability distributions. For example, translation and scaling connect among distributions represented with circles that in turn may presumably provide close approximation to distributions with bell-shaped density profiles. More than that, geometric representation and visualization of probability distributions would allow to employ geometric tools and geometric intuition into probabilistic reasoning.

2 Background

The “Background” section contains well known facts from financial mathematics and geometry. Books [6, 7, 8, 9] and numerous other works can serve as reference. The variables from financial mathematics employed in this work and their meaning are introduced in Table 1.

2.1 Risk-neutral probability density and vanilla options’ prices

Let be probability density of the random variable with expectation and be the corresponding cumulative density function. Let , be arbitrary real numbers and an arbitrary non-negative number. Denote

| (1) |

and

| (2) | |||

| (3) |

Consequently,

and

| (4) |

| Variable | Definition or meaning in financial mathematics |

|---|---|

| Spot: the currently traded value of an asset like exchange rate or a stock price | |

| Interest rate of the domestic currency: if the price of the traded asset is measured in USD, then USD interest for the period | |

| Interest rate of the foreign currency or dividend yield of the stock. Eg EUR interest for EUR/USD underlying | |

| call | Price of European vanilla call option (the right to buy an asset in future time for the predefined strike value K) |

| put | Price of European vanilla put option (the right to sell an asset in future time for the predefined strike value K) |

| Strike value of a financial derivative | |

| Time left to the moment when European option can be exercised (time to option’s expiry) | |

| Price of asset at future time | |

| Risk-neutral/implied probability density of future asset’s price . The word “implied” will sometimes be omitted further in text. Computations of volatility smiles in this work are related exclusively to implied probabilities. The term “implied” is used as values of and may be numerically implied from vanilla option prices known continuously over . | |

| Cummulative implied probability density of future asset’s price | |

| Implied volatility; for any given , when the value of is the same for any strike , then is log-normal and is equal to the standard deviation of annualized continuous returns of (standard deviation of ) | |

| ln(S0/ K) + (r - q + σ2/ 2 )TσT | |

| ln(S0/ K) + (r - q - σ2/ 2 )TσT = d_1(K) - σ(K) T | |

| 12 π ∫_-∞^x e^-y^2/2 dy | |

| N’(x) = 12 π e^-x^2/2 | |

| In case is log-normally distributed, | |

| In case is log-normally distributed, . Is used by option traders to represent strikes of cited options. For example, for and log-normally distributed , “25 delta put” stands for such strike that | |

| ATMF | At the money forward (strike) |

| At The Money risk neutral strike that zeros the delta of the portfolio : . For log-normally distributed , |

The values of call and put from formulae (2), (3) are usually represented in terms of a dummy variable called implied volatility by means of the Black-Scholes-Merton (BSM) formula:

| (5) |

| (6) |

where are chosen to make the right hand side be equal to the known left hand side; and are defined in Table 1. In other words, whenever the value of a or a is known, a unique makes equalities (5) and (6) hold for known , , , . The values of in formulae (5) and (6) are identical.

The ideal case when implied volatility is constant is equivalent to log-normality of the implied probability density of the future asset price ,

It it straightforward to show that

| (7) |

The vanna-volga approach can be used to interpolate and extrapolate implied volatility given its values at three strikes [10] in a parametric-free way.

2.2 Stereographic projection

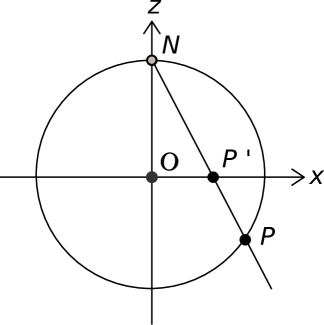

Stereographic projection is a one-to-one mapping of a 3D sphere without its north pole onto the plane . Figure 1 demonstrates how a slice of stereographic projection that belongs to the plane maps a unit circle without its north pole onto the axis.

The formulae for the stereographic projection and its inverse are well known. For the case of the slice in the plain the transformation is applied to a unit circle centered at the origin and the relationships between the coordinates of the circle and projections on the axis are as follows:

| (8) |

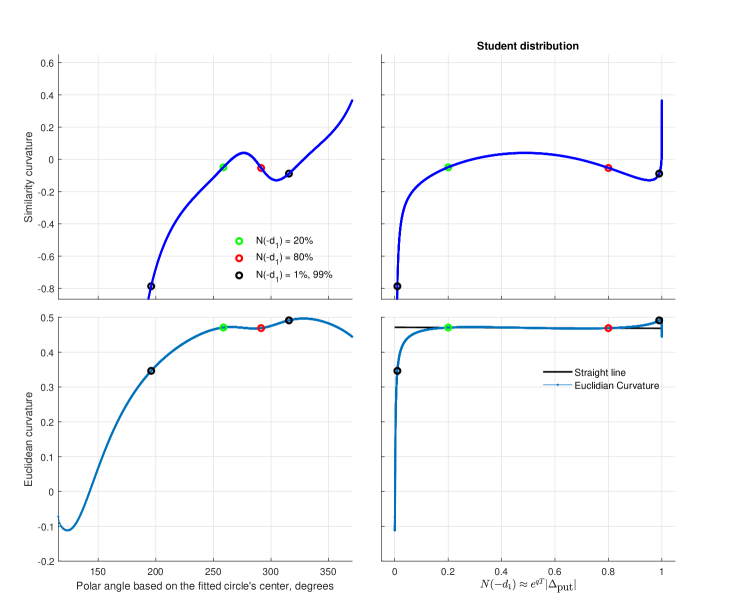

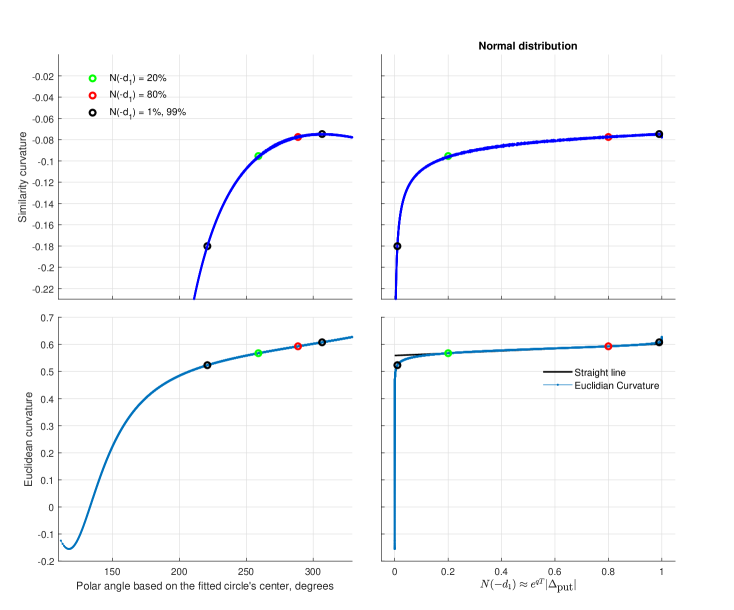

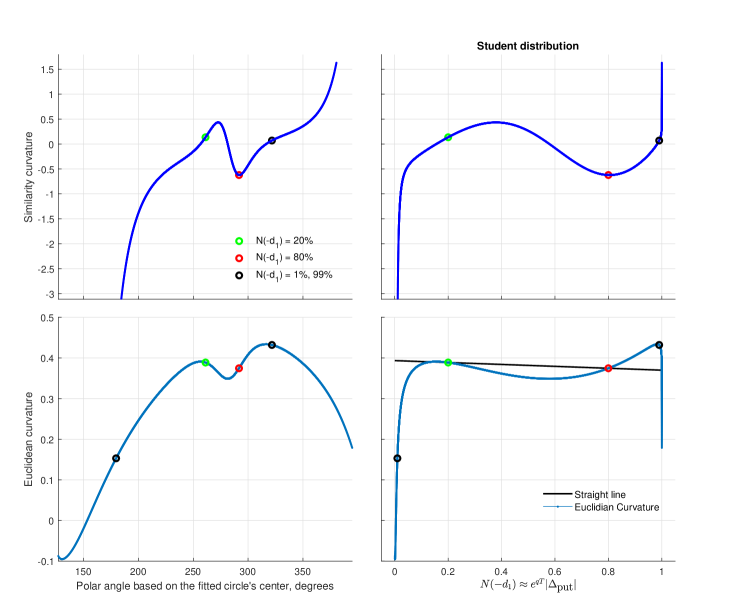

2.3 Euclidean and similarity curvatures

Circles have constant Euclidean curvature. Euclidean curvature of a curve is invariant under rotations and translations of a curve while similarity curvature is invariant under rotations, translations and uniform scaling. Closeness of Euclidean curvature of a curve to constancy characterizes curve’s “closeness” to being circular. Analysis of similarity curvature allows scale-invariant characterization of curves.

For an arbitrarily parameterized curve the formulae for the Euclidean and similarity curvatures respectively are as follows [8]:

2.4 Divergence between distributions

Kullback-Leibler divergence [11] (KL)

is used to estimate discrepancy between two distributions; for example, between the Gamma distribution and the distribution represented by a circle translated from the origin. In the current work integration is implemented numerically based on the trapezoid rule and computation is based on natural logarithm so that the divergence is measured in nats.

3 Methods

Given a market state and time to expiry, that is the values of , , , , a one-to-one correspondence can be established between the set of implied volatility profiles and the set of probability densities333Some implied volatility profiles correspond to densities that may take negative values. So density here means an integrable function with finite expectation and whose integral over is equal to 1. supported on and having finite expectation via the formulae (2), (4), and (5). Earlier work [12] provides explanation, derivations and examples that include popular distributions, like gamma and uniform. Here implied volatility profiles are used to establish geometric representations of corresponding probability distributions.

3.1 Representation of implied volatility smile by a curve in polar coordinate system

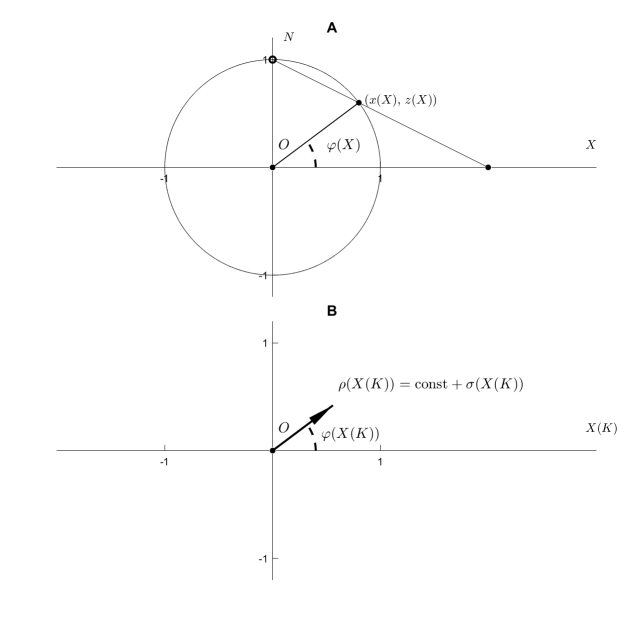

The proposed geometric representation of implied volatility employs the following steps:

-

1.

For a given strike compute the value . Here the constant controls how much of accumulated probability is supported for the strikes whose values fall within the unit circle () using the stretching/extension of by ; while is the only free parameter of the proposed methodology.

-

2.

Use equation (8) to compute the Cartesian coordinates of the unique point on the unit circle corresponding to .

-

3.

Compute the polar angle between the axis and the line connecting the origin to the point on the circle as demonstrated in Figure 2A.

- 4.

-

5.

Geometrically represent the implied volatility profile with the curve ; this curve also represents the probability distribution associated with .

In such a way the profile of implied volatility is mapped into a curve in the plane . For the presented construction, log-normal probability distribution whose implied volatility profile is constant is mapped into a curve with constant , in other words into a circle centered at the origin. For non log-normal distribution is not constant and so its geometric representation does not correspond to a circle centered at the origin.

The procedure for geometric representation of probability distribution was applied to several gamma distributions with bell-shaped density profiles and uniform distributions that do not have bell-shaped density profile, both supported on . Normal distribution and translated Student’s -distribution have bell-shaped probability density profile and can be picked in a way that the amount of the part supported outside of , that is , is as negligible as necessary by choosing sufficiently large positive expectation and sufficiently small standard deviation. Therefore, geometric representations of normal and translated Student’s distributions with small enough were also analyzed for the part supported on . Values of call options associated with probability densities of the considered distributions are needed to find corresponding to and vice versa. The formulae for call options are summarized in Table 2.

Market provides options’ prices for a small set of strikes and so the values of implied volatility are known at those points as well. Fitting curves to corresponding points in the representation space allows to implement continuous completion of implied volatility and to construct implied distribution.

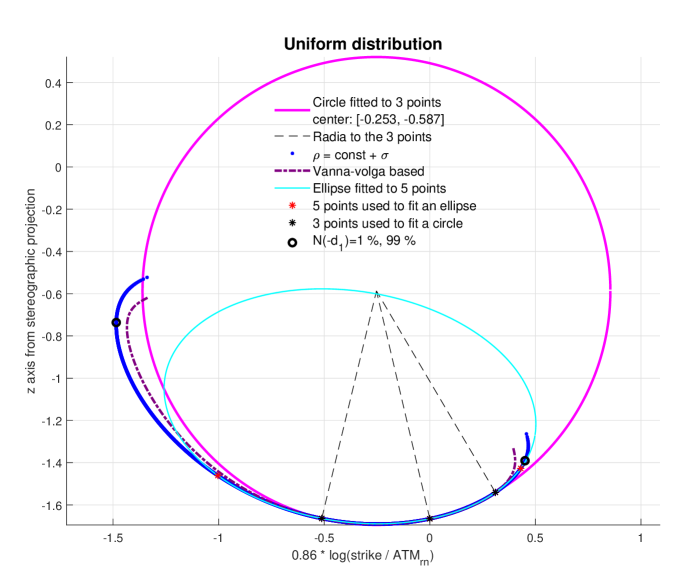

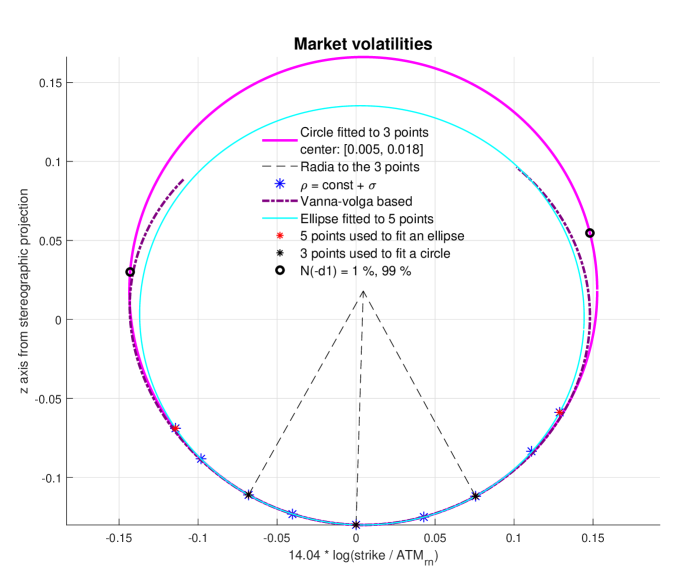

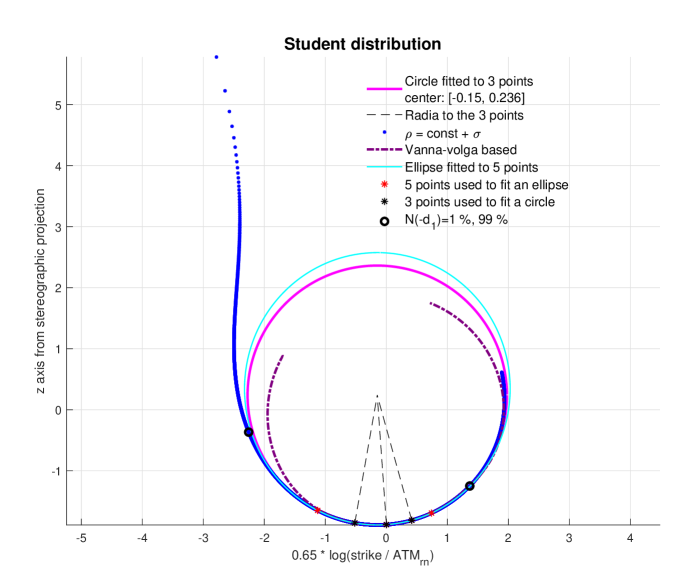

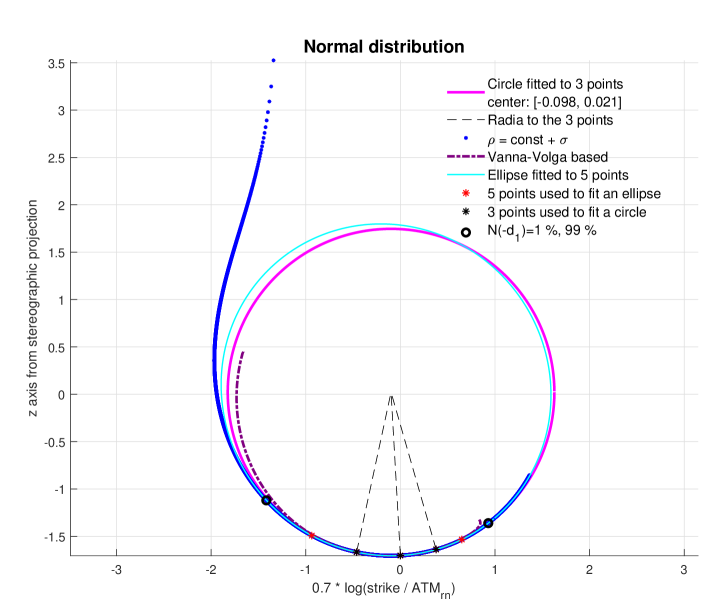

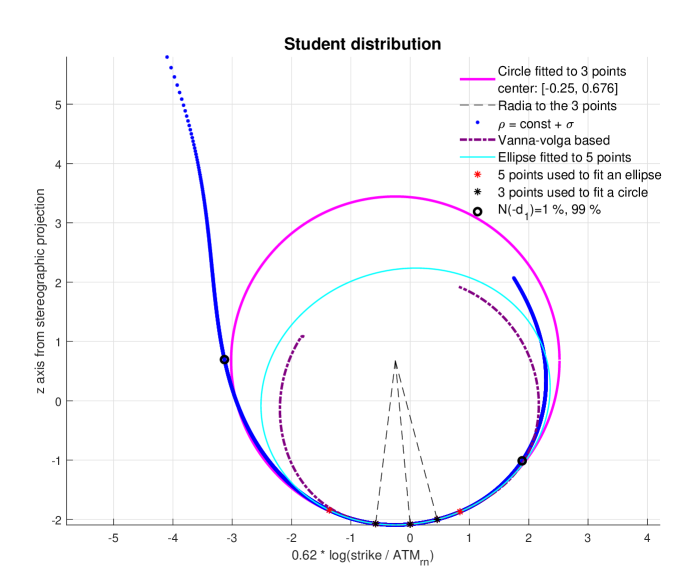

3.2 Fitting circle and ellipse to geometric representation

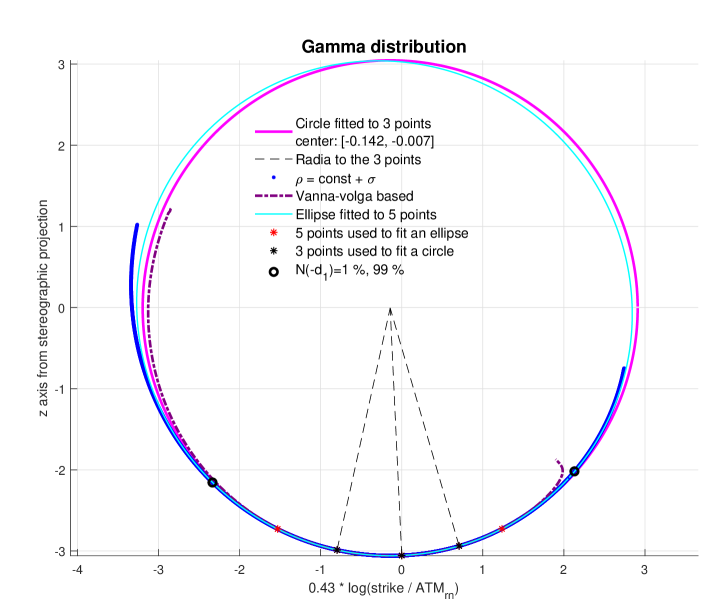

Once geometric representation of a continuous distribution or of the point-wise volatility smile is known, it can be fit with a circle. Three points are used to fit a circle:

-

1.

,

-

2.

,

-

3.

.

To fit an ellipse, the following 5 points can be used:

-

1.

,

-

2.

,

-

3.

,

-

4.

,

-

5.

.

In case of market smile, the values of and may correspond to without multiplication by .

4 Results

This section contains examples of applying the proposed methodology to probability distributions of different kinds and to a set of point-wise implied volatility data from the market. Two to three figures correspond to each considered distribution.

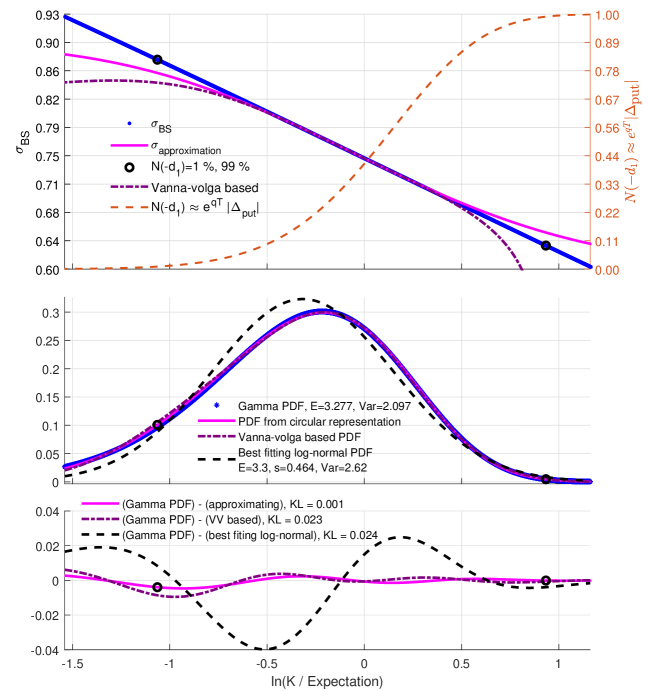

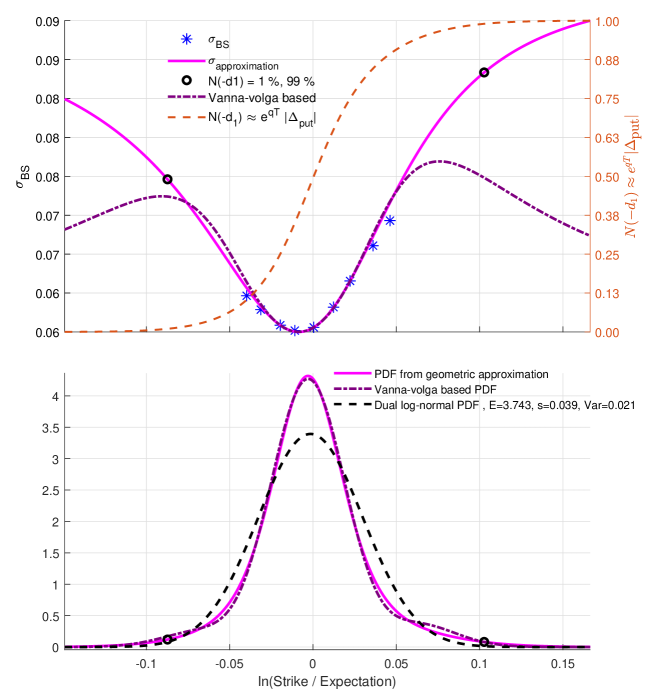

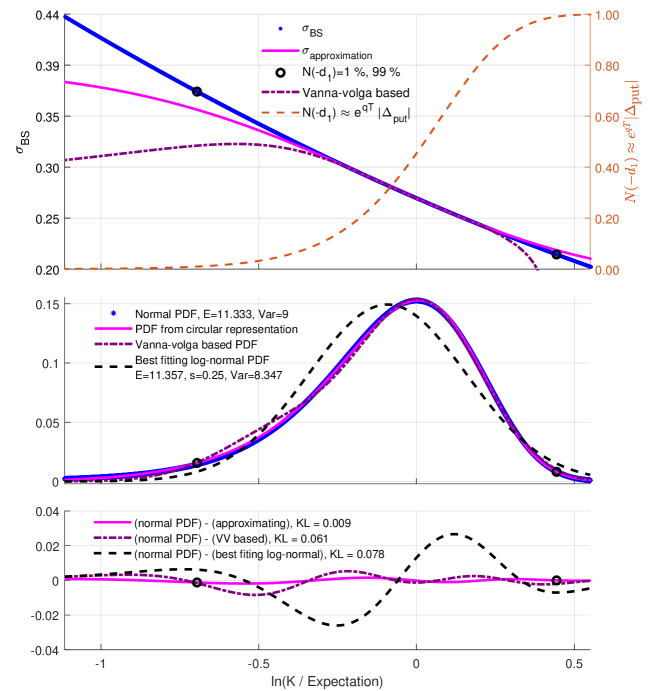

-

1.

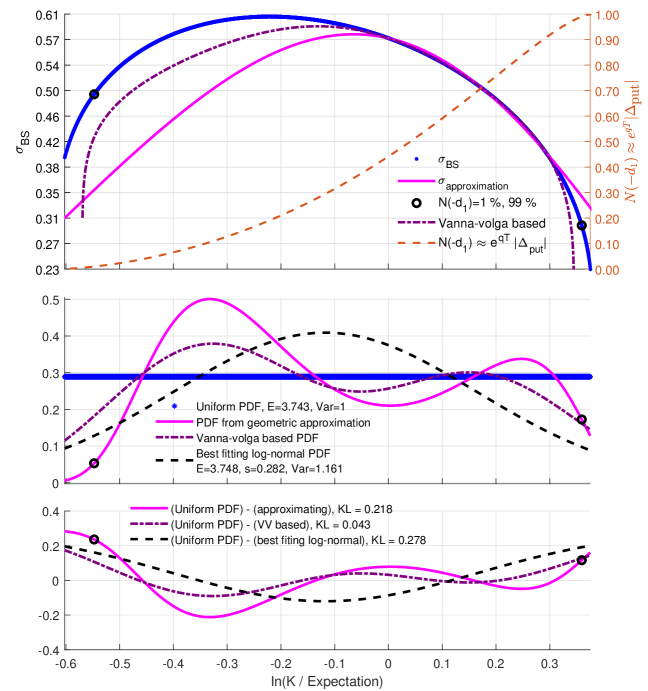

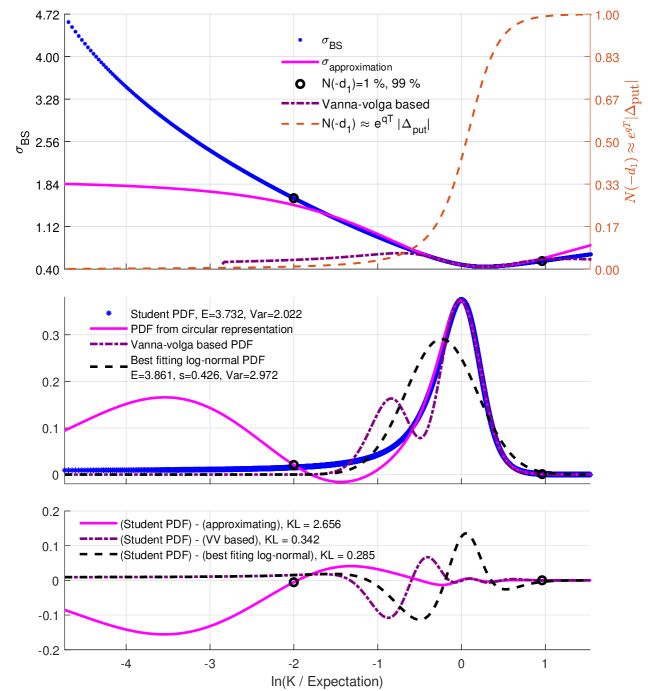

Geometric representation of the considered distribution, circle and ellipse fitted to this geometric representation and 3/5 points used to fit circle/ellipse. The figure also includes geometric representation of the distribution defined by the implied volatility obtained with vanna-volga method applied to the three points used to fit the circle.

-

2.

Volatility smiles corresponding to the objects from the previous item, their corresponding probability density functions and difference between density of the considered distribution and distributions corresponding to the fitted circle and to vanna-volga based implied volatility profile. Kullbak-Leibler divergence for pairs of distributions is provided as well.

-

3.

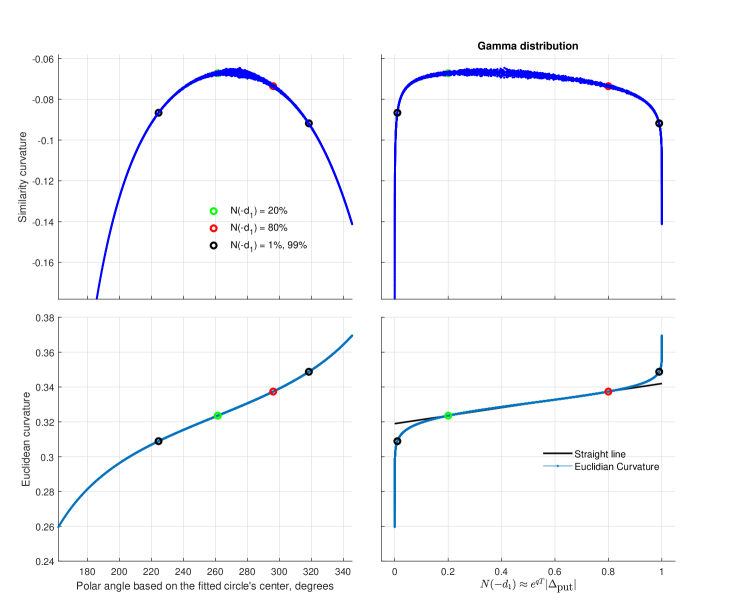

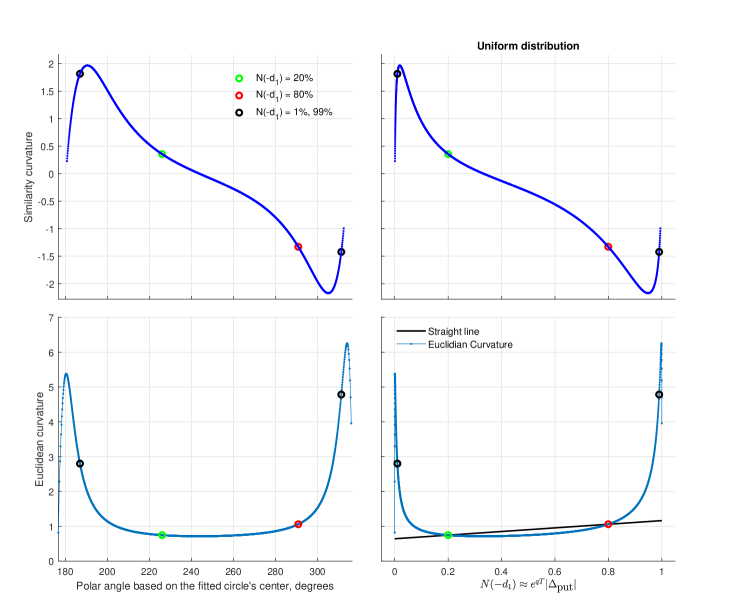

Similarity and Euclidian curvatures of the geometric representation as a function of the polar angle with resect to the center of the fitted circle and as a function of . Computation of curvature is not applicable to the sparse point-wise input from the market and therefore only two figures characterize example from the market.

4.1 Examples of distributions supported on

Gamma distributions and specifically chosen uniform distributions are supported on . While rich subset of gamma distributions consists of densities with bell-shaped profile, the profile of uniform distributions is non bell-shaped. Typically Gamma distributions with bell-shaped density profile are well approximated with distributions represented by fitted circles as demonstrated in Figures 3-5; however uniform distributions, as expected, cannot be well approximated with distributions represented by fitted circles as demonstrated in Figures 6-8.

The divergence between the Gamma and circle based approximating PDFs is much smaller than other divergences measured as can be seen in the legend to the below plot in Figure 4.

4.2 Geometric completion of implied volatility and partially observable probability, case of capital markets

The values of implied volatility are cited in the market for a limited set of strikes and expiries . Usually, such correspond to 3 points: (1) ATM and (2-3) call and put; sometimes additional values are provided at call/put, call/put, call/put. Known values of are interpolated/extrapolated for arbitrary values of in order to price options at arbitrary strikes.

Three volatility surfaces are considered here, one for each of the three currency pairs: EURUSD, USDJPY and USDILS444Market data courtesy of Bloomberg LP.. Volatility completion was implemented separately for each expiry based on circular representation and based on the vanna-volga approach; both methods used three volatility values, at (1) ATM and (2-3) call and put. The results of completion can be compared to the market values at call/put, call/put, call/put. As can be seen in Tables 3 - 8, the discrepancies between the modeled and “market” volatilities are smaller for completion based on circular representation than the one based on the vanna-volga method.

| Expiry | ATM | norm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | -0.0008 | -0.0004 | 0 | 0 | 0 | 0.0001 | 0 | -0.0002 | -0.0005 | 0.0011 | |

| 3W | -0.0007 | -0.0004 | 0 | 0 | 0 | 0.0001 | 0 | -0.0003 | -0.0007 | 0.0012 | |

| 1M | -0.0008 | -0.0005 | 0 | 0 | 0 | 0.0001 | 0 | -0.0004 | -0.0008 | 0.0013 | |

| 2M | -0.0011 | -0.0007 | 0 | 0 | 0 | 0.0001 | 0 | -0.0002 | -0.0005 | 0.0014 | |

| 3M | -0.0006 | -0.0005 | 0 | -0.0001 | 0 | 0.0001 | 0 | 0.0001 | 0.0001 | 0.0008 | |

| 4M | -0.0002 | -0.0003 | 0 | -0.0001 | 0 | 0.0001 | 0 | 0.0001 | 0.0001 | 0.0004 | |

| 6M | 0 | -0.0002 | 0 | -0.0001 | 0 | 0.0001 | 0 | 0.0004 | 0.0005 | 0.0007 | |

| 9M | 0.0003 | -0.0001 | 0 | -0.0002 | 0 | 0 | 0 | 0.0004 | 0.0005 | 0.0007 | |

| 1Y | 0.0003 | -0.0001 | 0 | -0.0001 | 0 | 0.0001 | 0 | 0.0007 | 0.0009 | 0.0012 | |

| 18M | 0.0007 | 0.0001 | 0 | -0.0002 | 0 | 0.0001 | 0 | 0.0005 | 0.0007 | 0.0011 | |

| 2Y | 0.0007 | 0.0002 | 0 | -0.0002 | 0 | 0.0001 | 0 | 0.0005 | 0.0005 | 0.0011 | |

| 3Y | 0.0009 | 0.0003 | 0 | -0.0001 | 0 | 0.0001 | 0 | 0.0003 | 0.0003 | 0.0010 | |

| 4Y | 0.0010 | 0.0004 | 0 | -0.0001 | 0 | 0 | 0 | 0.0003 | 0.0003 | 0.0012 | |

| 5Y | 0.0011 | 0.0005 | 0 | -0.0001 | 0 | 0 | 0 | 0.0003 | 0.0004 | 0.0013 | |

| norm | 0.0027 | 0.0014 | 0 | 0.0004 | 0 | 0.0003 | 0 | 0.0014 | 0.0020 | 0.0040 |

| Expiry | ATM | norm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | -0.0014 | -0.0008 | 0 | 0.0001 | 0 | 0.0001 | 0 | -0.0004 | -0.0010 | 0.0019 | |

| 3W | -0.0014 | -0.0008 | 0 | 0.0001 | 0 | 0 | 0 | -0.0004 | -0.0011 | 0.0020 | |

| 1M | -0.0015 | -0.0009 | 0 | 0.0001 | 0 | 0 | 0 | -0.0004 | -0.0011 | 0.0021 | |

| 2M | -0.0019 | -0.0012 | 0 | 0.0001 | 0 | 0.0001 | 0 | -0.0002 | -0.0007 | 0.0023 | |

| 3M | -0.0013 | -0.0011 | 0 | 0.0001 | 0 | 0 | 0 | 0.0003 | 0.0003 | 0.0017 | |

| 4M | -0.0008 | -0.0009 | 0 | 0.0001 | 0 | 0 | 0 | 0.0004 | 0.0003 | 0.0013 | |

| 6M | -0.0005 | -0.0008 | 0 | 0.0001 | 0 | 0 | 0 | 0.0007 | 0.0009 | 0.0014 | |

| 9M | 0 | -0.0007 | 0 | 0 | 0 | -0.0001 | 0 | 0.0008 | 0.0010 | 0.0015 | |

| 1Y | 0 | -0.0008 | 0 | 0.0001 | 0 | -0.0001 | 0 | 0.0012 | 0.0016 | 0.0022 | |

| 18M | -0.0001 | -0.0006 | 0 | 0 | 0 | 0 | 0 | 0.0008 | 0.0009 | 0.0013 | |

| 2Y | -0.0003 | -0.0007 | 0 | 0 | 0 | 0 | 0 | 0.0006 | 0.0004 | 0.0010 | |

| 3Y | -0.0007 | -0.0005 | 0 | 0 | 0 | 0 | 0 | 0 | -0.0006 | 0.0011 | |

| 4Y | -0.0006 | -0.0003 | 0 | 0 | 0 | 0 | 0 | -0.0002 | -0.0008 | 0.0011 | |

| 5Y | -0.0005 | -0.0002 | 0 | 0 | 0 | 0.0001 | 0 | -0.0002 | -0.0009 | 0.0010 | |

| norm | 0.0037 | 0.0029 | 0 | 0.0003 | 0 | 0.0002 | 0 | 0.0020 | 0.0034 | 0.0061 |

| Expiry | ATM | norm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | -0.0021 | -0.0014 | 0 | 0.0002 | 0 | 0.0003 | 0 | -0.0013 | -0.0024 | 0.0038 | |

| 3W | -0.0012 | -0.0009 | 0 | 0.0002 | 0 | 0.0003 | 0 | -0.0011 | -0.0021 | 0.0028 | |

| 1M | -0.0007 | -0.0005 | 0 | 0 | 0 | 0.0002 | 0 | -0.001 | -0.0019 | 0.0023 | |

| 2M | 0.0003 | -0.0001 | 0 | -0.0001 | 0 | 0.0001 | 0 | -0.0008 | -0.0016 | 0.0018 | |

| 3M | -0.0003 | -0.0004 | 0 | -0.0001 | 0 | 0.0001 | 0 | -0.0008 | -0.0016 | 0.0019 | |

| 4M | 0 | -0.0003 | 0 | -0.0001 | 0 | 0 | 0 | -0.0007 | -0.0015 | 0.0017 | |

| 6M | -0.0004 | -0.0005 | 0 | -0.0001 | 0 | 0 | 0 | -0.0008 | -0.0017 | 0.002 | |

| 9M | 0.0002 | -0.0002 | 0 | -0.0001 | 0 | -0.0001 | 0 | -0.0005 | -0.001 | 0.0012 | |

| 1Y | -0.0004 | -0.0005 | 0 | -0.0001 | 0 | -0.0001 | 0 | -0.0005 | -0.0011 | 0.0013 | |

| 18M | 0.0006 | 0 | 0 | -0.0001 | 0 | -0.0002 | 0 | 0.0001 | -0.0002 | 0.0006 | |

| 2Y | 0.0005 | 0 | 0 | -0.0002 | 0 | -0.0004 | 0 | 0.0004 | 0.0004 | 0.0009 | |

| 3Y | 0.0004 | -0.0001 | 0 | -0.0003 | 0 | -0.0005 | 0 | 0.0005 | 0.0005 | 0.001 | |

| 4Y | 0.0009 | 0.0002 | 0 | -0.0003 | 0 | -0.0007 | 0 | 0.0008 | 0.0009 | 0.0017 | |

| 5Y | 0.0013 | 0.0004 | 0 | -0.0004 | 0 | -0.0009 | 0 | 0.0009 | 0.0011 | 0.0022 | |

| norm | 0.0032 | 0.002 | 0 | 0.0007 | 0 | 0.0014 | 0 | 0.003 | 0.0053 | 0.0074 |

| Expiry | ATM | norm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | -0.0033 | -0.0021 | 0 | 0.0003 | 0 | 0.0002 | 0 | -0.0015 | -0.003 | 0.0052 | |

| 3W | -0.0027 | -0.0017 | 0 | 0.0003 | 0 | 0.0002 | 0 | -0.0012 | -0.0025 | 0.0043 | |

| 1M | -0.0024 | -0.0015 | 0 | 0.0002 | 0 | 0.0001 | 0 | -0.0011 | -0.0023 | 0.0038 | |

| 2M | -0.0014 | -0.0012 | 0 | 0.0002 | 0 | 0 | 0 | -0.0006 | -0.0016 | 0.0025 | |

| 3M | -0.0019 | -0.0015 | 0 | 0.0002 | 0 | -0.0001 | 0 | -0.0009 | -0.0021 | 0.0033 | |

| 4M | -0.0015 | -0.0014 | 0 | 0.0002 | 0 | -0.0001 | 0 | -0.0008 | -0.002 | 0.003 | |

| 6M | -0.0016 | -0.0016 | 0 | 0.0002 | 0 | -0.0001 | 0 | -0.0009 | -0.0024 | 0.0034 | |

| 9M | -0.0008 | -0.0013 | 0 | 0.0001 | 0 | -0.0002 | 0 | -0.0006 | -0.0019 | 0.0025 | |

| 1Y | -0.0006 | -0.0014 | 0 | 0.0002 | 0 | -0.0002 | 0 | -0.0008 | -0.0023 | 0.0029 | |

| 18M | 0.0005 | -0.0009 | 0 | 0.0001 | 0 | -0.0003 | 0 | -0.0004 | -0.0017 | 0.0021 | |

| 2Y | 0.0007 | -0.001 | 0 | 0 | 0 | -0.0004 | 0 | -0.0002 | -0.0013 | 0.0018 | |

| 3Y | 0.001 | -0.001 | 0 | 0 | 0 | -0.0005 | 0 | -0.0002 | -0.0013 | 0.002 | |

| 4Y | 0.0014 | -0.0008 | 0 | 0 | 0 | -0.0007 | 0 | 0 | -0.0009 | 0.002 | |

| 5Y | 0.0017 | -0.0008 | 0 | -0.0001 | 0 | -0.0009 | 0 | 0.0001 | -0.0006 | 0.0022 | |

| norm | 0.0065 | 0.0051 | 0 | 0.0007 | 0 | 0.0014 | 0 | 0.0029 | 0.0073 | 0.0115 |

| Expiry | 10put | 15put | 25put | 35put | ATM | 35call | 25call | 15call | 10call | norm | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | 0.0015 | 0.0008 | 0 | -0.0001 | 0 | -0.0001 | 0 | 0.0010 | 0.0021 | 0.0029 | |

| 3W | 0.0003 | 0.0002 | 0 | 0.0001 | 0 | 0 | 0 | 0.0005 | 0.0011 | 0.0013 | |

| 1M | -0.0004 | -0.0002 | 0 | 0.0002 | 0 | 0.0001 | 0 | 0 | 0.0002 | 0.0005 | |

| 2M | -0.0002 | -0.0001 | 0 | 0.0001 | 0 | 0 | 0 | 0.0001 | 0.0004 | 0.0005 | |

| 3M | -0.0003 | -0.0002 | 0 | 0.0001 | 0 | -0.0001 | 0 | -0.0001 | 0.0003 | 0.0005 | |

| 4M | -0.0004 | -0.0003 | 0 | 0.0001 | 0 | 0 | 0 | 0.0002 | 0.0007 | 0.0009 | |

| 6M | -0.0008 | -0.0005 | 0 | 0.0002 | 0 | 0 | 0 | -0.0004 | -0.0001 | 0.0010 | |

| 9M | -0.0011 | -0.0007 | 0 | 0.0003 | 0 | 0 | 0 | -0.0005 | -0.0004 | 0.0015 | |

| 1Y | -0.0017 | -0.0011 | 0 | 0.0003 | 0 | -0.0001 | 0 | -0.0008 | -0.0008 | 0.0023 | |

| 18M | -0.0004 | -0.0004 | 0 | 0.0003 | 0 | 0 | 0 | 0.0003 | 0.0015 | 0.0017 | |

| 2Y | -0.0002 | -0.0002 | 0 | 0.0004 | 0 | -0.0002 | 0 | -0.0002 | 0.0007 | 0.0009 | |

| 3Y | -0.0009 | -0.0006 | 0 | 0.0005 | 0 | -0.0002 | 0 | 0.0004 | 0.0019 | 0.0023 | |

| 4Y | -0.0012 | -0.0007 | 0 | 0.0006 | 0 | -0.0003 | 0 | 0.0008 | 0.0028 | 0.0033 | |

| 5Y | -0.0015 | -0.0009 | 0 | 0.0006 | 0 | -0.0003 | 0 | 0.0008 | 0.0026 | 0.0033 | |

| norm | 0.0034 | 0.0022 | 0 | 0.0013 | 0 | 0.0006 | 0 | 0.0020 | 0.0053 | 0.0071 |

| Expiry | 10put | 15put | 25put | 35put | ATM | 35call | 25call | 15call | 10call | norm | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W | -0.0004 | -0.0004 | 0 | 0.0001 | 0 | 0 | 0 | -0.0001 | -0.0001 | 0.0006 | |

| 3W | 0.0008 | 0.0002 | 0 | -0.0001 | 0 | -0.0001 | 0 | 0.0004 | 0.0008 | 0.0013 | |

| 1M | 0.0014 | 0.0006 | 0 | -0.0002 | 0 | -0.0002 | 0 | 0.0010 | 0.0018 | 0.0026 | |

| 2M | 0.0015 | 0.0006 | 0 | -0.0001 | 0 | -0.0001 | 0 | 0.0011 | 0.0018 | 0.0026 | |

| 3M | 0.0015 | 0.0006 | 0 | -0.0001 | 0 | -0.0001 | 0 | 0.0013 | 0.0021 | 0.0030 | |

| 4M | 0.0019 | 0.0008 | 0 | -0.0001 | 0 | -0.0002 | 0 | 0.0012 | 0.0018 | 0.0030 | |

| 6M | 0.0024 | 0.0011 | 0 | -0.0002 | 0 | -0.0002 | 0 | 0.0018 | 0.0026 | 0.0041 | |

| 9M | 0.0028 | 0.0013 | 0 | -0.0002 | 0 | -0.0003 | 0 | 0.0020 | 0.0030 | 0.0048 | |

| 1Y | 0.0035 | 0.0017 | 0 | -0.0003 | 0 | -0.0002 | 0 | 0.0022 | 0.0028 | 0.0053 | |

| 18M | 0.0024 | 0.0011 | 0 | -0.0003 | 0 | -0.0003 | 0 | 0.0013 | 0.0005 | 0.0030 | |

| 2Y | 0.0022 | 0.0009 | 0 | -0.0003 | 0 | -0.0002 | 0 | 0.0018 | 0.0010 | 0.0031 | |

| 3Y | 0.0028 | 0.0012 | 0 | -0.0004 | 0 | -0.0002 | 0 | 0.0011 | -0.0010 | 0.0034 | |

| 4Y | 0.0031 | 0.0013 | 0 | -0.0004 | 0 | -0.0002 | 0 | 0.0007 | -0.0023 | 0.0042 | |

| 5Y | 0.0035 | 0.0015 | 0 | -0.0005 | 0 | -0.0001 | 0 | 0.0006 | -0.0029 | 0.0049 | |

| norm | 0.0088 | 0.0039 | 0 | 0.0010 | 0 | 0.0007 | 0 | 0.0049 | 0.0074 | 0.0131 |

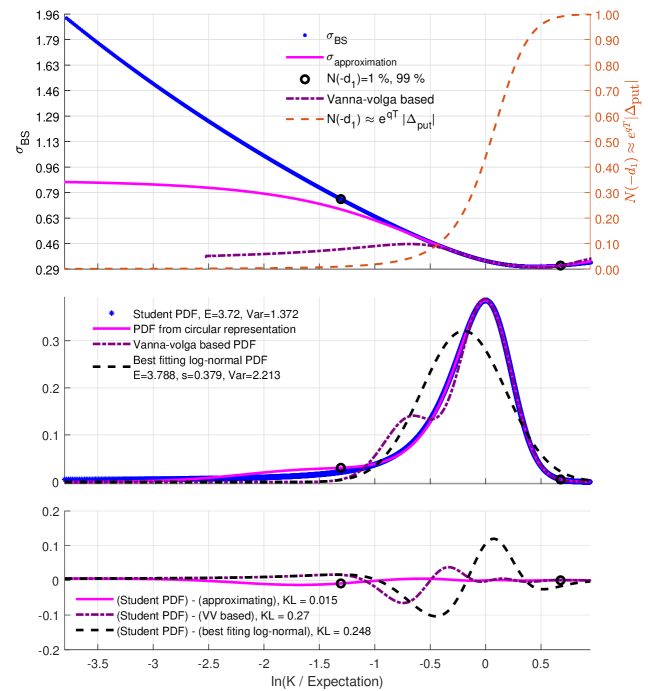

4.3 Distributions mostly supported on

Here examples of translated Student’s distribution and normal distributions, both with very small , are considered. The densities are rescaled so that and only the part supported on is further used for computing the KL divergence. As figures 12 and 15 demonstrate, the distributions reconstructed from circular representations fitted to three points provide a fair approximation to the original distributions.

4.4 Negative probability

Negative density values may arise by inverting shapes known in the representation space as demonstrated below. The KL divergence is not defined for negative distribution values. To be able to apply the formula for computing the KL divergence, negative values of were replaced with very small positive ones (e.g. of the order of ) and the density was rescaled to achieve , then the values of pseudo KL divergence were computed in such cases. An example of a circle that represents density obtaining negative values is demonstrated in Figure 17. The pseudo KL divergence between specific translated Student’s distribution and the density represented by the circle fitted to corresponding geometric representation is relatively large as can be seen in Figure 18. The considered Student’s distribution has non-negligible part supported outside as its standard deviation is not small enough versus the expectation. This causes the abnormality with negative density underlying the fitted circle in the representation space.

5 Discussion

A wide range of cognitive processes may utilize a rich machinery for geometric computations in the brain [14]. Does the brain incorporate its geometric intuition into its probabilistic reasoning? And if yes to what extent and how? On the practical side, FX options’ market makers provide pricing of uncertainty based on their experience and gut feeling, and measure uncertainty in terms of implied volatility. This work establishes a methodology of how to geometrically represent uncertainty measured with implied volatility in a way that allows to complete the knowledge about the represented probability distribution by extending the measurement of implied volatility to arbitrary strikes from only a small number of known values. The methodology also allows visualization of probability distributions based on intuitive geometric symmetries. For example, log-normal distributions are represented with circles centered at the origin and circles not centered at the origin seem to represent probability densities that closely approximate densities with bell-shaped profile.

The “Results” section presents examples of geometric representation for a number of distributions with both bell-shaped and non-bell-shaped probability density profiles. Geometric representations of probability densities with bell-shaped profile, fully or mostly supported on , were successfully approximated with circles; those circles, in turn, represent feasible probability distributions (reconstructed density is non-negative: ). Those reconstructed densities provide good approximation to the original distributions as measured with the Kullback-Leibler divergence. The above mentioned approximability based on circles in the representation domain is typical for the analyzed probabilities with bell-shaped density profiles. The circles-based approximability does not hold for probabilities whose density is non-bell-shaped, for example for uniform distributions. It may not hold for the densities whose cumulative probability (support outside of ) is non-negligible as demonstrated in Figure 18.

For all considered distributions with bell-shaped densities, their approximations with distributions arising from circular representations were noticeably superior to the approximations based on the vanna-volga method (Figures 4, 12, 15). The approximations of considered market volatility smiles were in general better for circular representations as well (Tables 3 - 8). So, the proposed method looks more precise for extending the volatility smile to entire continuum of strikes versus the vanna-volga approach, though circular approximation has one free parameter while the vanna-volga method is parameter-free. Ellipses have also been fit to the geometric representations based on five points that define a unique ellipse. For considered examples, in general, the fit with ellipses does not seem to be superior over the fit with circles while only three points are needed to pass a circle. Implied volatility contains information that, for bell-shaped densities at least, may allow completion based on just three values; what is not the case for point-wise probability values. While use of implied volatility and “delta” (see Table 1) in finance is convenient as it allows to apply a kind of uniform measure to strikes of options with different maturities, this technical convenience does not contradict the biological rationale introduced in the present work.

Geometric representation of probabilities allows to introduce geometric equivalence classes for distributions. In particular, circular representations are in the focus of the present work and they presumably either underlie densities with bell-shaped profile or approximate their representations. Real-world applications often deal with approximate data due to bid-ask spreads in finance and perception/action (measurement/implementation) imperfections in general. Therefore, mathematically defined class of geometric equivalence may be enriched with good enough approximations for many practical purposes and this should be accounted for. Specifically, biological systems may not need to distinguish small drifts in the represented probability distributions and so they may rely on equivalence classes that allow approximating geometric shapes in the representation space. So, accounting for small imperfections, circular geometric representations may actually cover representation of probability densities with bell-shaped profiles that are supported on ; this claim needs to get stronger support yet.

For probability densities supported outside of geometric representation can be based on the probabilities supported strictly on by applying one-to-one transformations, for example

| (9) |

Distributions defined by implied volatility like in formula (A.4) depend on market characteristics , , , from the Black-Scholes-Merton formula (5) and this “market-specificity” should be accounted for while inverting geometric representation into the corresponding probability distribution. Construction of geometric representation for a given probability distribution is “market-specific” in the same manner, so that the values of , , , should be introduced. Those “market” variables are not disconnected from the distribution as any implied distribution imposes constraint on them based on equation (1): and vice versa, the reconstructed probability distribution should satisfy the above constraint.

Furthermore, any non-negative integrable function defined on can be represented with a curve in polar coordinate system by transforming into a probability density 555Function should be rescaled with constant to achieve and transformation (9) or another relevant transformation should be applied if necessary to adjust the support. and further by representing the resulting probability distribution with the procedure introduced in this work.

Family of normal distributions is closed under convolution transformations while the set of log-normal distributions is not. So, in order to keep distributions represented with circles centered at the origin closed under the convolution, their argument should be log-transformed and the inverse transformation (9) should be applied to the result of the convolution. Consider the following open questions and problems related to the proposed concept of geometric representation of probability:

-

1.

What operations and for what classes of distributions preserve (or approximately preserve) geometric properties of the underlying geometric representations666That is are invariant., like circles being mapped to circles (or curves approximating circles well enough) and so on?

-

2.

How precisely do distributions represented with circles approximate arbitrary distributions with bell-shaped profile, what would be quantitative conditions on those shapes?

-

3.

What are possible equivalence classes for probability distributions, from the point of view of geometric representation, allowing also for small drifts, and how those classes can be used in applications and research?

-

4.

Finding methods for efficient completion of probabilities in general. Here completion of probabilities with bell-shaped densities was implemented based on circular representations.

Appendix A Probability density expressed through implied volatility

Here equations (4) and (5) are used to derive a differential expression based on for probability density . Equation 4 implies

| (A.1) |

Now differentiate the expression for from equation (5):

and apply (7) to get

| (A.2) |

Differentiation of (A.2) with respect to leads to the expression:

| (A.3) |

Now, formulae (A.1), (A.3) imply

| (A.4) |

Whenever an approximate geometric representation for probability is known (meaning that corresponding is known too) and has a functional form, for example a circle, a function can be used in equation (A.4) to obtain an approximate probability density function. If an approximate geometric representation has no known functional form but is available point-wise, equation (A.4) may still be useful in the form of finite difference for dense enough points. Approximate geometric representation may lead to negative values of probability density for some . Equation (A.4) implies condition on that is equivalent to non-negativity of probability density:

Denote differentiation with respect to with dot:

to get

References

- [1] S. Dehaene, V. Izard, P. Pica, and E. Spelke, “Core knowledge of geometry in an Amazonian indigene group,” Science, vol. 311, pp. 381–384, 2006.

- [2] P. Viviani and R. Schneider, “A developmental study of the relationship between geometry and kinematics in drawing movements,” Journal of Experimental Psychology: Human Perception and Performance, vol. 17, no. 1, pp. 198–218, 1991.

- [3] V. I. Arnol’d, Yesterday and long ago. Springer, Berlin, 2006.

- [4] P. J. Olver, Applications of Lie groups to differential equations. Springer-Verlag, 1993.

- [5] N. H. Ibragimov, Elementary Lie group analysis and ordinary differential equations. John Wiley & Sons, 2007.

- [6] J. C. Hull, Options, futures, and other derivatives.

- [7] E. G. Haug, The complete guide to option pricing formulas. New York: McGraw-Hill, 2007.

- [8] P. Shirokov and A. Shirokov, Affine differential geometry. Moscow: GIFML, 1959. German edition: Affine differentialgeometrie, Teubner, 1962. English translation of relevant parts of the book can be obtained from the author of the manuscript (FP) by request for non-commercial use in research and teaching.

-

[9]

J. Olsen, The geometry of Möbius transformations.

2010.

https://johno.dk/mathematics/moebius.pdf. - [10] A. Castagna and F. Mercurio, “The vanna-volga method for implied volatilities,” Risk, pp. 106 – 111, 2007.

- [11] T. M. Cover and J. A. Thomas, Elements of Information Theory. New York: Wiley, 1991.

-

[12]

F. Polyakov, “Representation of probability distributions with implied

volatility and biological rationale,” arXiv, 2021.

https://arxiv.org/abs/2110.03517. - [13] K. Iwasawa, “Analytic formula for the European normal Black Scholes formula,” 2001.

-

[14]

F. Polyakov, “Are cognitive processes encoded through sequences of geometric

transformations?,” Researchgate, 2019.

https://www.researchgate.net/publication/337032579_Are_cognitive_processes_encoded_through_sequences_of_geometric_transformations.