Robust Causal Learning for the Estimation of Average Treatment Effects

Abstract

Many practical decision-making problems in economics and healthcare seek to estimate the average treatment effect (ATE) from observational data. The Double/Debiased Machine Learning (DML) is one of the prevalent methods to estimate ATE in the observational study. However, the DML estimators can suffer an error-compounding issue and even give an extreme estimate when the propensity scores are misspecified or very close to 0 or 1. Previous studies have overcome this issue through some empirical tricks such as propensity score trimming, yet none of the existing literature solves this problem from a theoretical standpoint. In this paper, we propose a Robust Causal Learning (RCL) method to offset the deficiencies of the DML estimators. Theoretically, the RCL estimators i) are as consistent and doubly robust as the DML estimators, and ii) can get rid of the error-compounding issue. Empirically, the comprehensive experiments show that i) the RCL estimators give more stable estimations of the causal parameters than the DML estimators, and ii) the RCL estimators outperform the traditional estimators and their variants when applying different machine learning models on both simulation and benchmark datasets.

Index Terms:

treatment effect estimation, causal inference, economics, healthcareI Introduction

Causal inference is ubiquitous for decision-making problems in various areas such as Healthcare [1, 2, 3] and Economics [4, 5, 6]. At the core of causal machine learning, estimating the average treatment effect (ATE) from observational data is challenging because some features (covariates) can influence both treatment and outcome in most practical circumstances. For example, factors such as regions and races (covariates) can affect both the vaccination (treatment) assignment and the post-vaccination infection rate (outcome). To obtain a clean ATE, one can conduct the Randomized Controlled Trials (RCTs). RCTs are regarded as the gold standard to evaluate ATE, whereas conducting RCTs is often expensive and time-consuming. As a result, more and more researchers tend to estimate ATE from observational data.

In the observational study, classical causal learning methods concerning ATE estimations mainly include regression adjustment methods and re-weighting methods (see more details in [7]). Regression adjustment methods require an estimated feature-outcome relation (aka the outcome model) and directly average the predicted potential outcomes over the whole population to estimate ATE, so the associated estimator is called the direct regression (DR) estimator. The conundrum of the DR estimator is that it overlooks the probabilistic impact of the covariates on the treatment assignment (i.e., the propensity score) and hence often results in biased estimations of ATE unless the outcome model is estimated accurately. Re-weighting methods mimic the principle of RCTs to make the re-weighted instances look like they receive alternative treatment. The Inverse Probability Weighting (IPW) is one of the prevalent re-weighting strategies. It involves the propensity scores rather than the outcome model. Nevertheless, the IPW estimator is sensitive to the estimation of propensity scores and even leads to high variance estimates. Such occasion often occurs when the estimated propensity scores are close to 0 or 1. This is called an error-compounding issue.

The Debiased Machine Learning (DML) method, which is exploited by [6] based on [8], offsets the shortcomings of classical causal learning methods. The DML method combines the two classical approaches to ensure that the corresponding estimator is accurate as long as either the outcome model or the propensity score, but not necessarily both, is correctly specified (see [9], [10], [11], [12], [13] and the references therein). This notable merit is well known as the “doubly robust” property. However, the DML estimator can still suffer the error-compounding issue since the inverse term of the propensity score is still present. Inevitably, propensity scores usually fail to be correctly specified in practice, especially when the distribution of the treated group is substantially different from that of the controlled group (see, for example, [14, 15, 16, 17, 18]). This observation motivates us to go beyond the DML estimator and construct estimators that are more robust to the misspecification of the estimated propensity scores.

In this paper, we propose a Robust Causal Learning (RCL) method to establish the RCL estimators of the ATE. The contributions are summarized as follows:

-

1.

Our RCL estimators robustly ease the error-compounding issue exhibited by the DML estimator since the propensity scores in the RCL estimators are no longer in an inverse form.

-

2.

The RCL estimators inherit the consistency and doubly robust property of the DML estimator.

-

3.

The RCL methodology to construct an ATE estimator can also be applied to establish other prevalent treatment effect estimators.

-

4.

Extensive experiments show that the proposed RCL method achieves superior performance than DR, IPW, DML, and their variants across various combinations of machine learning regressors and classifiers.

The rest of the paper is organized as follows. Section II introduces the problem setup and the background of orthogonal scores. Section III presents the main theoretical results, including the RCL score in Theorem 1 and the RCL estimator in Corollary 2. Section IV reports extensive experimental results on simulation datasets and benchmark datasets. Due to the space limit, we defer all proof details and the code for reproducing our experiments to the full paper version.

II Preliminaries

II-A The Problem Setup

In this paper, we consider the potential outcome framework [19, 20] to study ATE. Let be the covariates (aka confounders), and be the treatment variable which can take values from . We denote as the outcome variable (aka the response), and represents the potential outcome under the treatment . If the observed treatment is , then the factual outcome equals . We denote as observed realizations of the i.i.d. random variables . Given the true causal parameter , the target quantity ATE between treatment and treatment is defined as

| (1) |

Identifying the ATE under the potential outcome framework requires some fundamental assumptions to ensure that and are identifiable. Thus, we impose the following assumptions as stated in existing causal inference works.

Assumption 1 (Stable Unit Treatment Value Assumption (SUTVA)).

The potential outcomes for any individual do not vary regardless of the treatment status of other individuals.

Assumption 2 (Ignorability).

Given the covariates , the potential outcome is independent to the treatment assignment , i.e., .

Assumption 3 (Positivity).

Treatment assignment is not deterministic regardless of the values covariates take, i.e., and .

Assumption 4 (Consistency).

If an individual receives treatment , his factual outcome is equal to the potential outcome under treatment , i.e., if .

These assumptions guarantee that the ATE can be inferred if we specify the relation , which is equivalent to estimating for each in the generalized propensity score model setting111This model setting allows to be multi-valued. It can be reduced to the “iteractive model” in [6] once the treatment takes binary values. [21, 22] (2):

| (2) | ||||||||

Here, and are true nuisance parameters. and are the noise terms. is known as the generalized propensity score (GPS) with multi-valued treatment variables. Finally, the true causal parameter for can be computed by and the true ATE can be computed by .

II-B Non-Orthogonal Scores and Orthogonal Scores

We aim to estimate the true causal parameters given i.i.d. samples . According to [6], the standard procedure to obtain the estimated causal parameter is: 1) getting the estimated nuisance parameters , e.g., ; 2) constructing a score that satisfies the moment condition (Definition 1); 3) establishing the estimator of , which is solved from the moment condition (3).

Definition 1 (Moment Condition).

Let and be the true causal parameter with being a causal parameter that lies in the causal parameter set. Denoting the nuisance parameters as and the true nuisance parameters as , we say a score satisfies the moment condition if

| (3) |

The moment condition guarantees that the estimator derived from the score is unbiased if the nuisance parameters equal the true ones. Here, we give the scores which satisfy the moment condition of two classical causal learning methods (DR and IPW) introduced before.

Example 1 (The Score and Estimator for DR).

Let and . In the DR method, the score satisfying the moment condition and the associated estimator are

Example 2 (The Score and Estimator for IPW).

Let and . In the IPW method, the score satisfying the moment condition and the associated estimator are

Generally, the estimators established from the scores in Example 1 might be invalid unless and estimate and well. To obtain robust estimators, [6] suggest that we should construct scores which satisfy the Orthogonal Condition (Definition 2) apart from the moment condition.

Definition 2 (Orthogonal Condition).

Suppose that the nuisance parameters and the true nuisance parameters are -dimensional tuples, i.e., and . Given , we say a score satisfies the orthogonal condition if

| (4) |

can be any subset of . Throughout the paper, for some positive integer , we define as

| (5) |

and .

The orthogonal condition ensures that the established estimators can still be valid even though some nuisance parameters are misspecified (see [6, 10, 23] for more details). Below we demonstrate how to utilize to justify that the scores in Examples 1 and 2 violate the orthogonal condition. Suppose in (5) is .

The above calculations show that and do not satisfy the orthogonal condition. The scores are usually termed as the non-orthogonal scores. As a consequence, their associated estimators are not “doubly robust”. To obtain a doubly robust estimator, [6] propose the DML method to construct the DML score.

Example 3 (The Score and Estimator for DML).

Let and . In the DML method, the score that satisfies both the moment condition and orthogonal condition and the associated estimator are

We can prove that satisfies the orthogonal condition when in (5) (see [6] for detailed derivations) following similar calculation processes for DR and IPW. is therefore termed as the orthogonal score. The orthogonal condition assures that the DML estimator is doubly robust, i.e., the estimator is locally unbiased and consistent as long as either or is correctly specified. Despite the doubly robust property, the DML estimator still suffers an error-compounding issue once the encompassed inverse propensity score is slightly misspecified for some data points. In real applications, one seldom encounters a situation that propensity scores are correctly estimated for all individuals. This dilemma motivates us to construct scores such that 1) the scores are orthogonal scores, i.e., they satisfy the moment condition (Definition 1) and the orthogonal condition (Definition 2); 2) the estimators established from the scores can stabilize the estimation error due to the misspecifications on propensity scores.

In the upcoming section, we will introduce a novel method, the Robust Causal Learning (RCL) method, to overcome the difficulties encountered by DR, IPW, and DML methods.

III The Proposed Method

This section shows our main theoretical results. First, Section III-A demonstrates the RCL scores. Then Section III-B presents the detailed construction of the RCL estimators with an algorithm that describes how to obtain an estimate of from observational data using the proposed RCL method.

III-A Construction of The RCL Score

In this paper, we construct an orthogonal score, the RCL score, to derive an estimator of along the lines of orthogonal machine learning works (e.g., [23, 6]). The relevant result is stated in Theorem 1.

Theorem 1 (RCL score).

Suppose and are -dimensional tuples such that and . Let , be integers s.t. . Assume the local moments and . Under the assumptions on nuisance parameters and noise terms stated in [6] and [23], the RCL score that satisfies the moment condition and the orthogonal condition is

| (6) |

Given an integer and an integer , we have

| (7a) | ||||

| where and the coefficient is computed by descending order for : | ||||

| (7b) | ||||

From (7a), we can observe that , the nuisance parameter of the propensity score, is no longer in an inverse form for the RCL score. As a consequence, the established RCL estimators from (6) can avoid the error-compounding issue. Simultaneously, the RCL scores are orthogonal scores, so the RCL estimators are as doubly robust as the DML estimator.

III-B Establishment of the RCL estimators

In this part, we will go into detail about the establishment of the RCL estimators. To begin with, we can solve the estimator from (3) using the emprical version of the moment condition for the RCL score (6):

| (8a) | ||||

| (8b) | ||||

Equation (8a) is referred to as the DR estimator when the true nuisance parameter is replaced by the estimated one . Equation (8b) can then be divided into two parts:

| (9a) | ||||

| (9b) | ||||

where is the sample set in which the units are all treated with while is the sample set in which the units are not treated with . It is obvious that (8a) and (9a) can be directly calculated from observational data, whereas (9b) that contains the counterfactual outcomes is unavailable to compute in a direct manner. Instead of pursuing the unobservable counterfactuals, we realize that given ,

holds for . Thus, the sample mean of equals zero regardless the samples come from or . This observation allows us to replace the sample mean of the counterfactuals in (9b) with that of the factual ones. To be specific, we first define the set such that

| (10) |

Then, a replaced estimator of (9b) is obtained as follows:

-

1.

For the unit in the set , pick an element from and multiply it by . Repeat the process until we go through all the individuals in the set ;

-

2.

Compute ;

-

3.

Repeat above steps times to eliminate the randomness brought by the random picking procedure and return the substitute estimator .

Consequently, (9b) can be inferred indirectly from observational data. With (8a) and (9a), the RCL estimator of is finally established in Corollary 2.

Corollary 2 (RCL estimator).

Let , be the estimates of , be by replacing with in (10), and be the element that is randomly selected from the set in the of repeated selections. The RCL estimator is given by

| (11) | ||||

The proposed RCL estimator is a consistent estimator of if satisfy the assumptions stated in [23] and [6]. Due to the space limit, the proofs of Theorem 1 and the consistency of can be seen in the full paper version. We also outline the procedures of estimating from observational data using the proposed RCL method in Algorithm 1. Note that if the whole dataset is split into the training set and the test set, Step 2 will be only conducted on the training set, while Step 3 - Step 8 can be performed to obtain the estimates of on both the training set and the test set. The running complexity of our algorithm is at most .

IV Numerical Studies

In this section, we compare the performances of our RCL estimators with the DML estimator and the DR estimator through simulation and empirical experiments. In both experiments, we consider three types of regressors: Lasso, Random Forests (RF), and Multi-layer Perceptron (MLP); and three types of classifiers: Logistic Regression (LR), RF, and MLP. We combine the regression model A and the classification model B to estimate and respectively, and denote the combination as A+B, e.g., Lasso+LR. In the empirical experiments, we consider two additional state-of-the-art neural network models in causal inference: TARNet [24] and Dragonnet [25]. All the experiments are run on Dell 3640 with Intel(R) Xeon(R) W-1290P CPU at 3.70GHz, and a set of NVIDIA GeForce RTX 2080Ti GPU.

For all the experiments throughout the paper, we use the following two metrics to evaluate the performance:

| (12a) | |||

| (12b) |

Here, is the weighted relative error of the experiment such that with and being the true ATE and the estimated ATE between the treatment and the treatment of the experiment. is the number of treatments and is the number of experiments.

IV-A Numerical Studies on Simulation Datasets

We first introduce the data generating process (DGP) for the simulation experiments. Given the covariates which follow a standard multivariate Gaussian distribution, the treatment variable has the treatment space with the corresponding probability

| (13) |

where the values of coefficients are randomly picked from the uniform distribution . is the confounding ratio ranging from to , and the number of covariates in used to generate is and . For example, if and , then and . We generate the potential outcome for treatment indices as

| (14) |

where is a constant vector whose elements are randomly chosen from . We also set , , , , and . Next, we generate i.i.d. observations based on the DGP. Suppose the realized covariates of the individual are , then the actual treatment will be , where is determined by . Under the actual treatment , the observed factual outcome will correspondingly be .

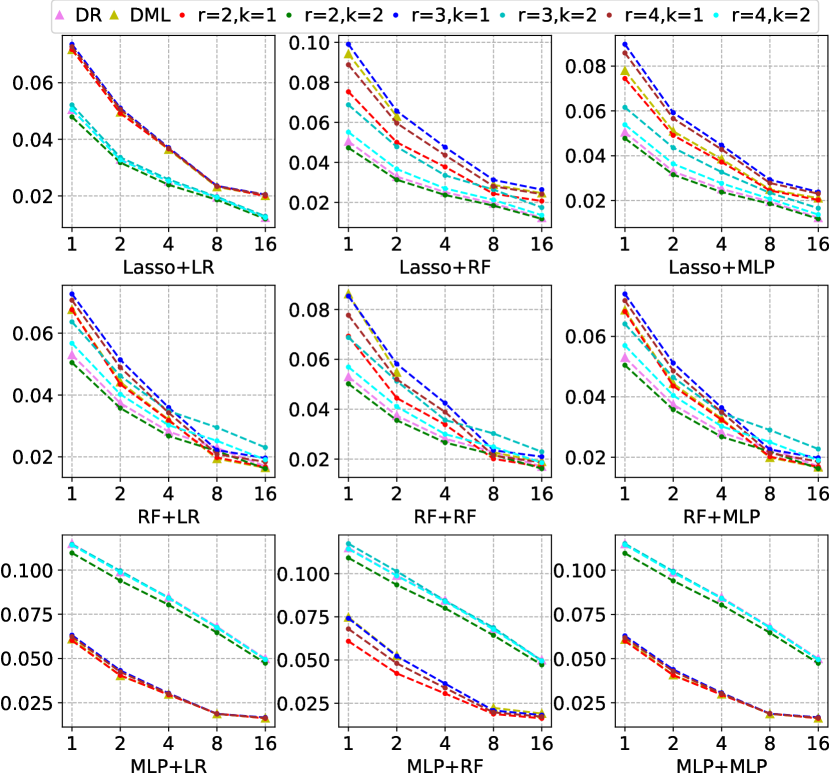

For the simulation experiments, we compute the DR, DML and our RCL estimators with different values of and (see Theorem 1), which is denoted by RCLr,k. We then use in (12a) with and to evaluate the performance of different estimators for each combination of the regressor and the classifier (denoted as regressor+classifier). We split every dataset by the ratio as training/validation/test sets.

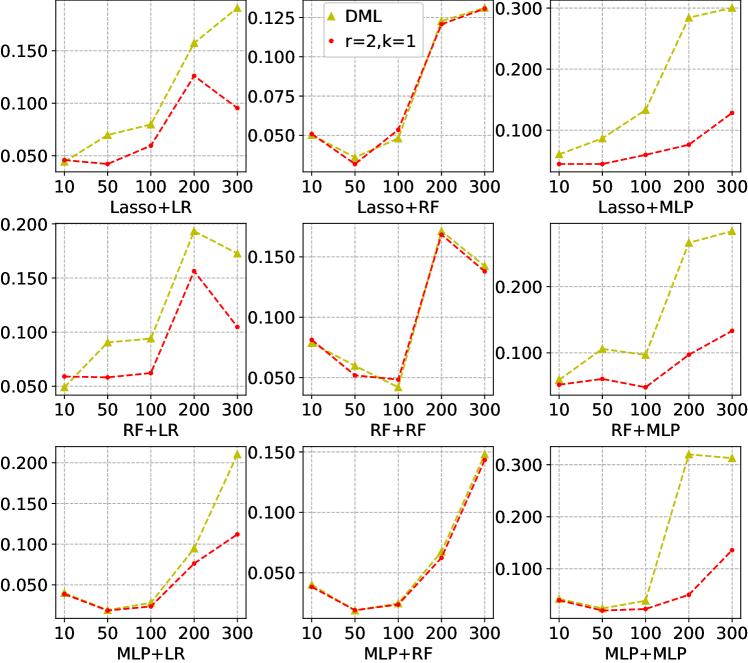

Consistency of RCL estimators

In this part, we set , , and let the number of observations vary in . We check the consistency of RCL estimators through simulations and report in Fig. 1. The result indicates that the error reduces when the sample size increases for our RCL estimators. Besides, we also find that when is fitted well (e.g., when the regressor is chosen as Lasso or RF), RCL2,2 performs better than DR, DML and other RCL estimators. On the other hand, when is not fitted well for some , e.g., when the regressor is chosen as MLP, the DML and the RCL estimator with can significantly correct the bias thanks to the doubly robust property. In this case, despite similar performances produced by RCL2,1 estimator and the DML estimator, RCL2,1 still has a smaller .

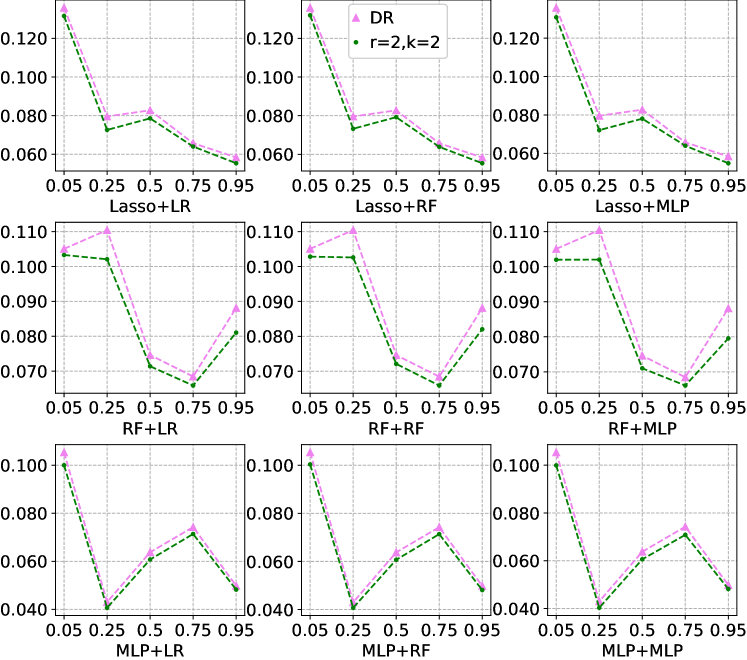

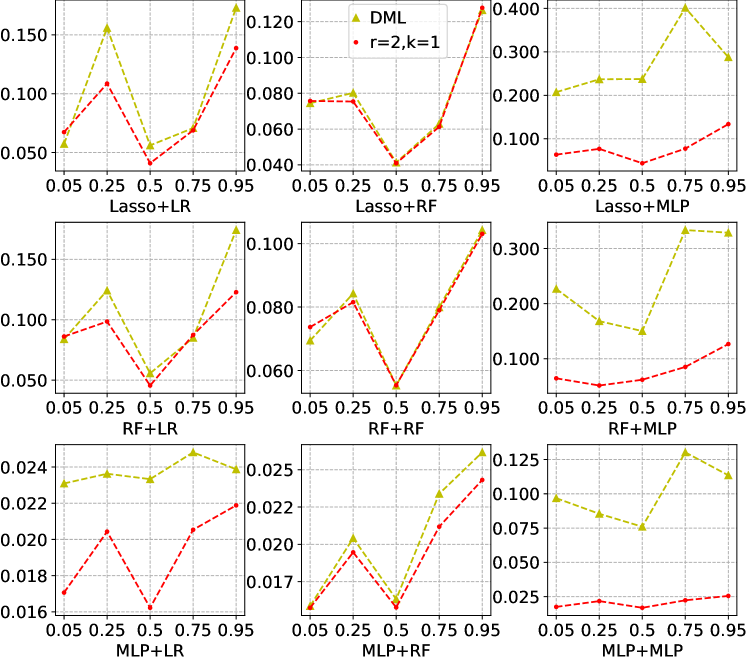

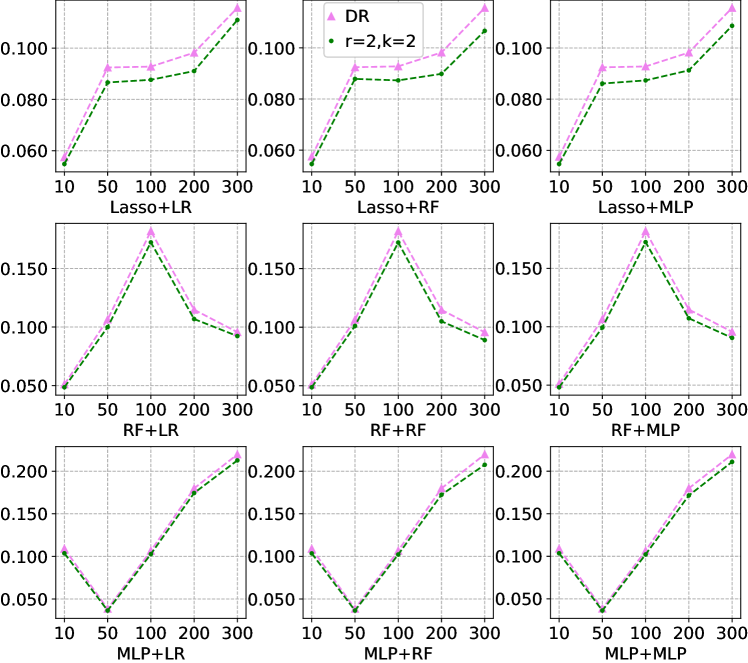

Varying and

In the following experiments, we mainly compare RCL2,2 with DR, and RCL2,1 with DML since the above simulation experiments indicate that RCL2,2 and DR perform similarly, and RCL2,1 has similar trends to DML. We set and plot produced by each model combination A+B versus i) different with in Fig. 2 and Fig. 3; ii) different with in Fig. 4 and Fig. 5. From all the four figures, we observe that the DML estimator is sensitive to the change of and , especially when the classifier is MLP. As analyzed before, if the estimation error of is non-negligible for some , the term of the DML estimator often gives extreme values especially when is small, leading to pronounced estimation errors of the ATE. Indeed, any ATE estimators that involve the inverse propensity score term might face this error-compounding issue. By contrast, our RCL estimators are less volatile to the variation of and regardless of the choice of classifiers. For example, in Fig. 5, we notice that when the classifier is MLP, the error of DML rises dramatically as increases, while RCL2,1 performs more steadily. In addition, our RCL2,2 estimator overall has a smaller than the DR estimator no matter how or varies.

IV-B Numerical Studies on Benchmark Datasets

| Model/Estimator | DR | RCL2,2 | IPW | AIPW | DML | DML-trim | RCL2,1 | ||

|---|---|---|---|---|---|---|---|---|---|

| LASSO+LR | -3.6% | -0.9% | |||||||

| LASSO+RF | -3.9% | -6.1% | |||||||

| LASSO+MLP | -3.1% | -47% | |||||||

| RF+LR | -4.8% | 0.0% | |||||||

| RF+RF | -3.8% | -1.2% | |||||||

| RF+MLP | -3.0% | -43% | |||||||

| MLP+LR | -1.7% | -26% | |||||||

| MLP+RF | -1.4% | -26% | |||||||

| MLP+MLP | -1.6% | -67% | |||||||

| TARNet | -1.7% | -6.8% | |||||||

| Dragonnet | -0.9% | -39% |

| Model/Estimator | DR | RCL2,2 | IPW | AIPW | DML | DML-trim | RCL2,1 | ||

|---|---|---|---|---|---|---|---|---|---|

| LASSO+LR | -3.2% | -0.3% | |||||||

| LASSO+RF | -4.0% | -6.8% | |||||||

| LASSO+MLP | -2.2% | -4.5% | |||||||

| RF+LR | -4.6% | -1.0% | |||||||

| RF+RF | -5.1% | -10% | |||||||

| RF+MLP | -3.7% | -5.5% | |||||||

| MLP+LR | -5.4% | -0.6% | |||||||

| MLP+RF | -6.3% | -10% | |||||||

| MLP+MLP | -4.6% | -5.5% | |||||||

| TARNet | -5.3% | -7.8% | |||||||

| Dragonnet | -5.2% | -0.6% |

Models

Similar to the simulation experiments, we choose Lasso, RF, and MLP as the regressors while LR, RF, and MLP as the classifiers. Additionally, two prevalent neural network models, TARNet and Dragonnet, are also considered for learning the nuisance parameters. According to [25], these two neural network structures can incorporate the estimations of both and using the representation learning technique.

Settings

We implement the above methods on two widely adopted benchmark datasets for causal inference, i.e., IHDP and Twins, and then compare RCL estimators with DR, IPW, DML, and their variants AIPW and DML-trim estimators. Mathematically, both the AIPW estimator and the DML-trim estimator are the same as the DML estimator. However, empirically, AIPW and DML-trim are less prone to suffer the extreme values. To be precise, AIPW decomposes the estimator into two parts that both contain the IPW term (see [26]), while DML-trim trims estimated propensity scores at the cutoff points of and (see [6]).

We take the RCL2,1 and RCL2,2 as the representatives of the general RCL estimators because for the real datasets with a relatively small sample size and a large dimension of features, the second-moment estimation of is more reliable compared to the higher-moment estimations. We use grid search to adjust the hyperparameters for those general machine learning models. For TARNet and Dragonnet, we use the same network structures (layers, units, regularization, batch size, learning rate, and stopping criterion) as suggested in [24] and [25].

IHDP

It is a widely used benchmark dataset for causal inference introduced by [27]. IHDP dataset is constructed based on the randomized controlled experiment conducted by Infant Health and Development Program. The collected 25-dimensional confounders from the 747 samples are associated with the properties of infants and their mothers, such as birth weight and mother’s age. Our aim is to study the treatment effect of the specialist visits (binary treatment) on the cognitive scores (continuous-valued outcome). By removing a subset of the treated group, the selection bias in the IHDP dataset occurs. There are 1000 IHDP datasets given in [27]. Each dataset is split by the ratio of as training/validation/test sets, which keeps consistent with [24].

Twins

Twins dataset is introduced by [28] and it collects twin births in the USA between 1989 and 1991. The treatment indicates the heavier twin while indicates the lighter twin; the outcome is a binary variable defined as the mortality in the first year; the covariates include 30 features relevant to the parents, the pregnancy and the birth. Similar to [29], we only select twins that have the same gender and both weigh less than 2kg. Finally, we have pairs of twins whose mortality rates are for lighter twin and for heavier twin. To simulate an observational dataset with selection bias, we selectively choose one of the two twins as the observed sample based on the covariates of individual: Bernoulli(Sigmoid()), where and . We repeat this process times, and each of the generated Twins datasets is split by the ratio of as training/validation/test sets, which keeps consistent with [29].

Analysis

In Table I and Table II, we report the performance of every model combination, measured by , for IHDP and Twins experiments, respectively. The smaller , the better. The metric () is used to evaluate the reduction ratio in of RCL2,2 relative to DR (RCL2,1 relative to the best estimator among IPW, AIPW, DML, and DML-trim). The negative () indicates that the RCL estimator has a smaller than the DR (IPW, AIPW, DML, and DML-trim) estimator.

Table I reports the experimental results on IHDP datasets. It illustrates that although the DR estimator produces reasonable estimates, the RCL2,2 estimator has a more minor than the DR estimator, with the error reduced relatively by . Simultaneously, RCL2,2 achieves the best performance among all the estimators across all the model combinations. We also notice that even though the AIPW and DML-trim avoid extreme values encountered by DML (e.g., when the classifier is chosen as RF, the inverse propensity score is estimated with an infinity value for some data points), the RCL2,1 estimator is still at most better than the best of IPW, DML, and DML-trim estimators. More importantly, when the variance of inverse propensity scores is large (e.g., when the classifier is MLP), the improvement of RCL2,1 to DML becomes more substantial.

Table II presents the experimental results on Twins datasets. It can be observed that the RCL2,2 estimator has a significantly smaller compared with other estimators for all model combinations, and it can reduce the estimation error relatively by compared with the DR method. Besides, the RCL2,1 estimator can reduce the estimation error by relative to the best of IPW, DML, and DML-trim estimators. It is also noticeable that when is well specified (e.g., the case on using Dragonnet in Table II), our RCL2,1 estimator still outperforms the DML estimator even though the error produced by the DML estimator is small enough.

IV-C Numerical Studies on Credit dataset

Causal inference benchmark datasets are typically generated by a parametric data generating process. Though the ground truth of treatment effects are accessable in this way, such semi-synthetic datasets fail to resemble the original real data sets.

In summary, DML is recognized as a better method than DR and IPW because when the DR (IPW) estimator has a notable bias due to the misspecification on (), the DML estimator can reduce the bias if () is well estimated. However, the advantages of DML are not easy to achieve in practice. First, the DML estimator, which incorporates the inverse propensity score term, may give a very large estimation or even infinite value of the ATE, reflecting that the DML estimator is volatile to the estimation of propensity scores. Second, if is approximated well enough, DML will not assuredly perform better than DR due to the high variance of the IPW term. By contrast, our RCL estimators are more practical since i) they can stabilize the error caused by the misspecification on propensity scores; ii) if is well approximated, the RCL2,2 estimator will outperform the DR estimator owing to the RCL scores are orthogonal scores; iii) if is not well approximated, but is correctly specified, the RCL estimator with performs better than the DML estimator with smaller estimation errors and slighter volatility to the estimated propensity scores.

V Conclusion

This paper constructs the RCL scores and establishes the RCL estimators for the ATE estimation. Theoretically, we prove that the RCL scores are orthogonal scores and the RCL estimators are consistent. Numerically, the comprehensive experiments have shown that our estimators outperform the commonly used estimators such as DR, IPW, AIPW, DML, and DML-trim estimators. In addition, the proposed RCL estimators have the same merit, i.e., the doubly robust property, as the DML estimator. However, unlike the DML estimator, the RCL estimators are more stable to the estimation error due to the misspecification on propensity scores than the DML estimator and its variants. In the future research, we will i) investigate the optimal values of in Theorem 1; and ii) provide interpretability for deep learning models in causal inference using the RCL method.

VI Acknowledgements

Qi WU acknowledges the support from the Hong Kong Research Grants Council [General Research Fund 14206117, 11219420, and 11200219], CityU SRG-Fd fund 7005300, and the support from the CityU-JD Digits Laboratory in Financial Technology and Engineering, HK Institute of Data Science. The work described in this paper was partially supported by the InnoHK initiative, The Government of the HKSAR, and the Laboratory for AI-Powered Financial Technologies.

Shumin MA acknowledges the support from the Guangdong Provincial Key Laboratory of Interdisciplinary Research and Application for Data Science, BNU-HKBU United International College under project code 2022B1212010006, the support from Guangdong Higher Education Upgrading Plan (2021-2025) of “Rushing to the Top, Making Up Shortcomings and Strengthening Special Features” with UIC research grant R0400001-22, and the UIC grant UICR0700019-22.

VII Appendices

VII-A proofs

We present the theoretical proofs of Theorems and Corollaries given in the paper.

Proof of Theorem 1.

Given the nuisance parameters and the true nuisance parameters , we find out the RCL score w.r.t. the nuisance parameters which can be used to construct the estimators of the causal parameter . We try an ansatz of such that

| (15) |

where

| (16) | ||||

Here, the coefficients depend on and only. Using the ansatz, we notice that satisfies the moment condition, i.e., . Indeed, we have

The second last equality comes from the fact that is a function of . The last equality comes from the fact that . Now, we aim to find out the coefficients of such that the score (15) satisfies the score. Indeed, we need to have for all and which are non-negative integers such that . Since when , we only need to solve the coefficients from

| (17a) | ||||

| (17b) | ||||

. However, (17a) always holds since

Consequently, we need to find out the coefficients , , , , from

| (17b) |

. From (17b), there are equations and we need to solve the unknowns from the equations. Generally, the unknowns could be solved uniquely.

To start with, we compute for . Note that

when and

when . Consequently, we need to solve for and simultaneously from

| (18a) | ||||

| and | ||||

| (18b) | ||||

From (18a), we have

| (18a*) | ||||

Since

we understand that

As such, (18a*) can be reduced as

Hence, we can solve for such that

It remains to find out from (18b). Indeed, we can simplify (18b) as

| (19) | ||||

. Now, we solve . We start with finding out , followed by iteratively. When , (19) becomes

Now, when , (19) becomes

Now, suppose are known and we want to find out what is. We have to solve it from

We can obtain from the above equation, which gives

The proof is completed. ∎

Proof of Corollary 2.

We have discussed the way to obtain the estimator in the main paper. ∎

To facilitate the upcoming studies, we first introduce some notations. Recall that is the potential outcome under the treatment . We use as the factual outcome if an individual receives , and as the counterfactual outcome if an individual receives alternative treatments. Hence, we have

Based on the introduced notations, we can define two residual differences and for the individual according to the sets and that the individual belongs to. Mathematically, if and if .

We give the statistical properties between and for . First, due to the SUTVA assumption for . Second. Regardless of the actual treatment the individual receives, the noises in terms of should be identical and independently distributed for different individuals. As a result, we should have

From the above assumptions, we have and .

We give the statistical properties between and . To be precise, we study and conditioning on . The properties are summarized in Proposition 3.

Proposition 3.

Given the covariates , the random variable and are independent and identically distributed, i.e., and .

Proof.

Using the SUTVA assumption, we have . In addition, we have

|

|

is due to the ignorability assumption. Similarly, we also have

|

|

∎

In the remaining sequel, we investigate the consistency of our RCL estimators based on the basics of orthogonal machine learning theory. To start with, we give the assumptions on the nuisance parameters. Only the assumptions that are helpful in studying the consistency of our RCL estimators are stated. Other assumptions that concentrate on the conditions of the scores, including orthogonality, identifiability, non-degeneracy, smoothness, and the regularity of moments can be found in [23] and references therein.

Assumption 5.

Given that the nuisance parameters and the true nuisance parameters are and , and , we have

-

1.

-

2.

.

For notational convenience, we rewrite our RCL estimator and denote it as . Indeed, we have

| (20) | ||||

Besides, we define two quantities and . They are

| (21) | ||||

| (22) |

We also define

|

|

Then (21) and (22) can be rewritten as

| (21) | ||||

| (22) |

for simplicity. In addition, we have to use two lemmas and two propositions to study the consistency of . We state them with the proofs.

Lemma 4.

Given two sequences of random variables and such that . If for some constant , then .

Proof.

Let and be the density functions of the random variables and respectively. Since , . Hence, . Consequently, implies . ∎

Lemma 5.

Given random variables , , , . If , , , then for any function .

Proof.

Define as the density function of , is the conditional density function of , is the conditional density function of , is the conditional density function of , is the conditional joint density function of , and is the conditional joint density function of . For a measurable set , we have

holds since , holds since , and holds since . ∎

Proposition 6.

Suppose and exist such that is finite for all . We have when .

Proof.

, we consider . Indeed, we have

Denoting as , we have

The last equality follows from

As a consequence, we have

when . As a result, we have . The proof is completed. ∎

Proposition 7.

Suppose that, conditioning on , are i.i.d. of and are i.i.d. of . We have

Proof.

Write

, we have

We simplify . Note that

|

|

The last equality in the above derivation follows from the fact that, conditioning on , are i.i.d. of for any . Indeed, we have for any and . Consequently, we have

|

|

In addition, we simplify the quantity . Note that . We therefore have

We justify the last equality. The last equality follows from the fact that, conditioning on , are i.i.d. of and are i.i.d. of for any . Indeed, under the given fact, we have

|

|

and

|

|

Consequently, we have

Thus, we have

| (23) | ||||

We notice that no matter we set followed by or vice versa, or we fix but let , we see that . ∎

Now, we are ready to investigate if the estimator is a consistent estimator of . Our goal is to show that . Before presenting the proof, we notice that when and satisfie Assumption 5. This is because that , , , , and .

Proof.

, we have

Since and , we have by Lemma 5. Moreover, we know that under the assumptions given in [23]. Together with the fact that , we have by Lemma 4. We turn to consider the quantity , and we aim to show that . Notice that

| (24) | ||||

Note that and do not incorporate any terms related to the estimated function . From Proposition 6 and Proposition 7, we conclude that (LABEL:eqt:consistent_proof_estimator_decompb) and (LABEL:eqt:consistent_proof_estimator_decompc) converge to in probability respectively. It remains to show the convergence of (LABEL:eqt:consistent_proof_estimator_decompa) and (LABEL:eqt:consistent_proof_estimator_decompd). Consider (LABEL:eqt:consistent_proof_estimator_decompd) first. Since

(LABEL:eqt:consistent_proof_estimator_decompd) is bounded above by

| (25) |

(25a) converges to in probability due to Proposition 6. We study the quantities (25b) and (25c).

(25b) can be further bounded. If is the size of , then we have

We see that (25b) can be further bounded by

| (26) |

We investigate if (26a), (26b), and (26c) converge to in probability. We consider (26a) first. Recall the assumptions that , and , we have by Lemma 5. Since , we have

Consider .

Note that it equals

|

|

Since and do not include the estimated nuisance parameters, is a constant. Moreover, note that when , we have

Now, we consider (26b). Indeed, we have

Here, the last inequality follows from the Hölders inequality, while the convergence holds according to Assumption 1.5 of [23]. Finally, we consider (26c). We can rewrite as

Now, we have

Using Assumption 1.5 of [23], we can conclude that . Next, we come to bound (25c). Since is the size of and

we see that (25c) can be further bounded by

| (27) |

Similarly, we can prove that (27a) and (27c) converge to in probability when using the arguments in proving that (26a) and (26c) converge to . As a result, the quantity (LABEL:eqt:consistent_proof_estimator_decompd) converges to in probability when .

Lastly, we turn to consider the quantity (LABEL:eqt:consistent_proof_estimator_decompa). In fact, we have

| (28a) | ||||

| (28b) | ||||

We can argue that (28a) converges to in probability as using similar arguments when we prove that (25b) converges to in probability. Simultaneously, we can argue (28b) converges to in probability as using similar arguments when we prove that (25c) converges to in probability. Consequently, we have converges to in probability.

The proof is completed. ∎

References

- [1] T. A. Glass, S. N. Goodman, M. A. Hernán, and J. M. Samet, “Causal inference in public health,” Annual review of public health, vol. 34, pp. 61–75, 2013.

- [2] J. Hill and Y.-S. Su, “Assessing lack of common support in causal inference using bayesian nonparametrics: Implications for evaluating the effect of breastfeeding on children’s cognitive outcomes,” The Annals of Applied Statistics, pp. 1386–1420, 2013.

- [3] A. M. Alaa and M. van der Schaar, “Bayesian inference of individualized treatment effects using multi-task gaussian processes,” in Advances in Neural Information Processing Systems, 2017, pp. 3424–3432.

- [4] A. Belloni, V. Chernozhukov, and C. Hansen, “Inference on treatment effects after selection among high-dimensional controls,” The Review of Economic Studies, vol. 81, no. 2, pp. 608–650, 2014.

- [5] M. H. Farrell, “Robust inference on average treatment effects with possibly more covariates than observations,” Journal of Econometrics, vol. 189, no. 1, pp. 1–23, 2015.

- [6] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins, “Double/debiased machine learning for treatment and structural parameters,” 2018.

- [7] L. Yao, Z. Chu, S. Li, Y. Li, J. Gao, and A. Zhang, “A survey on causal inference,” ACM Trans. Knowl. Discov. Data, vol. 15, no. 5, may 2021. [Online]. Available: https://doi.org/10.1145/3444944

- [8] J. Neyman, “C () tests and their use,” Sankhyā: The Indian Journal of Statistics, Series A, pp. 1–21, 1979.

- [9] J. M. Robins, L. Li, R. Mukherjee, E. T. Tchetgen, A. van der Vaart et al., “Minimax estimation of a functional on a structured high-dimensional model,” Annals of Statistics, vol. 45, no. 5, pp. 1951–1987, 2017.

- [10] J. Robins, L. Li, E. Tchetgen, A. van der Vaart et al., “Higher order influence functions and minimax estimation of nonlinear functionals,” in Probability and statistics: essays in honor of David A. Freedman. Institute of Mathematical Statistics, 2008, pp. 335–421.

- [11] R. Mukherjee, W. K. Newey, and J. M. Robins, “Semiparametric efficient empirical higher order influence function estimators,” arXiv preprint arXiv:1705.07577, 2017.

- [12] J. D. Kang and J. L. Schafer, “Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data,” Statistical science, pp. 523–539, 2007.

- [13] A. van der Vaart, “Higher order tangent spaces and influence functions,” Statistical Science, pp. 679–686, 2014.

- [14] F. Li, K. L. Morgan, and A. M. Zaslavsky, “Balancing covariates via propensity score weighting,” Journal of the American Statistical Association, vol. 113, no. 521, pp. 390–400, 2018.

- [15] M. Busso, J. DiNardo, and J. McCrary, “New evidence on the finite sample properties of propensity score reweighting and matching estimators,” Review of Economics and Statistics, vol. 96, no. 5, pp. 885–897, 2014.

- [16] M. C. Knaus, “Double machine learning based program evaluation under unconfoundedness,” Institute of Labor Economics (IZA), Tech. Rep., 2020.

- [17] P. C. Austin and E. A. Stuart, “Moving towards best practice when using inverse probability of treatment weighting (iptw) using the propensity score to estimate causal treatment effects in observational studies,” Statistics in medicine, vol. 34, no. 28, pp. 3661–3679, 2015.

- [18] M. Dudík, J. Langford, and L. Li, “Doubly robust policy evaluation and learning,” in Proceedings of the 28th International Conference on International Conference on Machine Learning, 2011, pp. 1097–1104.

- [19] D. B. Rubin, “Estimating causal effects of treatments in randomized and nonrandomized studies.” Journal of educational Psychology, vol. 66, no. 5, p. 688, 1974.

- [20] ——, “Causal inference using potential outcomes: Design, modeling, decisions,” Journal of the American Statistical Association, vol. 100, no. 469, pp. 322–331, 2005.

- [21] G. W. Imbens, “The role of the propensity score in estimating dose-response functions,” Biometrika, vol. 87, no. 3, pp. 706–710, 2000.

- [22] C. Tu, W. Y. Koh, and S. Jiao, “Using generalized doubly robust estimator to estimate average treatment effects of multiple treatments in observational studies,” Journal of Statistical Computation and Simulation, vol. 83, no. 8, pp. 1518–1526, 2013.

- [23] L. Mackey, V. Syrgkanis, and I. Zadik, “Orthogonal machine learning: Power and limitations,” in International Conference on Machine Learning. PMLR, 2018, pp. 3375–3383.

- [24] U. Shalit, F. D. Johansson, and D. Sontag, “Estimating individual treatment effect: generalization bounds and algorithms,” in Proceedings of the 34th International Conference on Machine Learning-Volume 70. JMLR. org, 2017, pp. 3076–3085.

- [25] C. Shi, D. Blei, and V. Veitch, “Adapting neural networks for the estimation of treatment effects,” in Advances in Neural Information Processing Systems, 2019, pp. 2503–2513.

- [26] A. Linden, S. D. Uysal, A. Ryan, and J. L. Adams, “Estimating causal effects for multivalued treatments: a comparison of approaches,” Statistics in Medicine, vol. 35, no. 4, pp. 534–552, 2016.

- [27] J. L. Hill, “Bayesian nonparametric modeling for causal inference,” Journal of Computational and Graphical Statistics, vol. 20, no. 1, pp. 217–240, 2011.

- [28] C. Louizos, U. Shalit, J. M. Mooij, D. Sontag, R. Zemel, and M. Welling, “Causal effect inference with deep latent-variable models,” in Advances in Neural Information Processing Systems, 2017, pp. 6446–6456.

- [29] J. Yoon, J. Jordon, and M. Van Der Schaar, “Ganite: Estimation of individualized treatment effects using generative adversarial nets,” in International Conference on Learning Representations, 2018.