A note on quadratic constraints with indicator variables: Convex hull description and perspective relaxation

Abstract

In this paper, we study the mixed-integer nonlinear set given by a separable quadratic constraint on continuous variables, where each continuous variable is controlled by an additional indicator. This set occurs pervasively in optimization problems with uncertainty and in machine learning. We show that optimization over this set is NP-hard. Despite this negative result, we characterize the structure of the convex hull, and show that it can be formally studied using polyhedral theory. Moreover, we show that although perspective relaxation in the literature for this set fails to match the structure of its convex hull, it is guaranteed to be a close approximation.

1 Introduction

In this paper, given , we study set

where is a vector of s and “” denotes the Hadamard (entry-wise) product of vectors. Set is non-convex due to the binary constraints encoded by , as well as the complementarity constraints linking the continuous and binary variables. Observe that arbitrary separable quadratic constraints of the form can be modeled with as well through the change of variables . Note that since any satisfies , the complementarity constraints can be linearized as the big-M constraints

| (1) |

Our overall goal is to understand and characterize the convex hull of , denoted as . Throughout the paper, for simplicity, we use the following convention for division by : if , and () if and (or ).

1.1 Applications

Set arises pervasively in practice. We now discuss three settings where it plays a key role.

Sparse PCA

Set arises directly in sparse principal component analysis problems [11, 25, 12, 17], a fundamental problem in statistics which can be formulated as

| (2a) | ||||

| s.t. | (2b) | |||

where and is a parameter controlling the sparsity of the solution. Observe that the feasible region given by constraints (2b) corresponds exactly to with set . Thus, understanding is critical to designing better convex approximations of (2).

General convex quadratic constraints

Given , consider the system of inequalities

| (3) |

System (3) arises for example in mean-variance optimization problems [5], where the quadratic constraint is used to impose an upper bound on the risk (variance) of the solution. While system (3) involves a non-separable quadratic constraint, a study of set can be still used to construct strong convex relaxations. Indeed, if where , and diagonal, then we can reformulate system (3) by introducing additional variables as

| (4a) | |||

| (4b) | |||

where constraints (4a) correspond precisely to and constraints (4b) are convex and SOCP-representable. Therefore, convex relaxations for system (3) can be obtained by strengthening constraints (4a) using .

Robust optimization

Consider a robust optimization problem of the form

| (5) |

where vector are the decision variables, set is the (possibly non-convex) feasible region and set is an uncertainty set corresponding to the objective coefficients. Robust optimization (5) is a fundamental tool to tackle decision-making under uncertainty problems. Two popular choices for the uncertainty set , each with its own merits and disadvantages, are: the approach of Ben-Tal and Nemirovski [7], where is an ellipsoid; and the approach of Bertsimas and Sim [8], where only a small subset of the coefficients are allowed to change while satisfying box constraints.

Thus, a natural uncertainty set inspired by the aforementioned two approaches allows few coefficients to change and imposes ellipsoidal constraint on the changing coefficients, that is, set

| (6) |

where are the nominal values for the coefficients. The uncertainty set is appropriate for example when changes in coefficients are caused by rare events, and the change in the coefficients (when such changes occur) can be accurately modeled with a Gaussian distribution. Constraint could be replaced by other constraints to capture more sophisticated relationships on the support of the perturbed coefficients.

1.2 Perspective relaxation and outline

A closely related set to that is well understood in the literature is the mixed-integer epigraph of a separable quadratic function with indicators, that is, Its convex hull can be described via the perspective relaxation , see [10, 13, 2, 15] for the case and [6, 20, 21, 22, 23] for cases with more general constraints. Thus, a natural convex relaxation for set is also given by the perspective relaxation

| (7) |

However, it is unclear to what extent relaxation coincides with : Are they the same? Is “necessary” to describe ? Does the structure of even “matches” ? Is a strong relaxation? How can it be improved?

All these questions can be precisely answered for polyhedral sets: an inequality is necessary for a polyhedron if it is facet-defining; a relaxation matches the structure of a polyhedron if it is defined by a finite number of linear inequalities. However, since is in general non-polyhedral, it is unclear (to date) how to formally answer the aforementioned questions. Ideally, one would like to explicitly compute and “see” how well the set matches this structure. Unfortunately, as we show in §2, optimization over set is NP-hard even when . Thus, an explicit computation of is unlikely. This result immediately implies that , but does not provide insights into answering the remaining questions.

In this paper, we close this gap in the literature. In §3 we characterize the structure of , and in particular we show that convexification of reduces to the convexification of a family of polyhedral sets. Interestingly, this family of polyhedra is well-studied in the literature. In §4 we review how to obtain facet-defining inequalities, and we also show that corresponds to using a strong nonlinear relaxation of these polyhedral sets. In §5 we propose an approximate deterministic counterpart of the robust optimization problem (5) with discrete uncertainty (6), and in §6 we present computations with this proposed formulation.

2 NP-hardness

In this section we show that optimization of a linear function over set is NP-hard. This result indicates that a compact explicit computation of is unlikely to be possible.

Consider the optimization problem

| (8a) | ||||

| s.t. | (8b) | |||

| (8c) | ||||

| (8d) | ||||

Proposition 1.

Problem (8) is NP-hard even if .

Proof.

Consider problem (8) where vector is fixed, and let (assume ). Then, for this choice of , problem (8) reduces to

| (9a) | ||||

| s.t. | (9b) | |||

| (9c) | ||||

Since the Lagrangian dual of problem (9) has no duality gap (as Slater condition holds), an optimal objective value can be computed as

| () | ||||

| () |

Remark 1.

If but there is a constraint of the form , then (10) can be solved by sorting. Polynomial-time solvability of this case suggests that it may be possible to construct a convex relaxation that guarantees integrality of the solutions under these conditions. In other words, it may be possible to characterize the convex hull of the set

where is the cardinality of the support of . Indeed, set is permutation-invariant, and its convex hull is described in [16], or projection of the perspective relaxation (i.e., ). Note however that these relaxations are not ideal for , i.e., solutions of linear optimization problems over do not coincide with the solutions of optimization problems over if .∎

3 Structure of the convex hull

From Proposition 1, we know that an explicit characterization of is unlikely to be possible. In this section, we settle for a weaker structural result: in Theorem 1, we state an explicit description of that relies on the convex hulls of polyhedral sets. Naturally, describing these polyhedral sets is NP-hard as well; nonetheless, they are substantially easier to handle, thanks to the maturity of polyhedral theory.

We first define the polyhedral sets that are key to characterizing .

Definition 1.

Given , define sets as

Note that set is the convex hull of a union of a finite number of polytopes, one for each . Thus, is a polytope itself. We defer to §4 the discussion on constructing relaxations of set . As Proposition 2 below states, set is a relaxation of set .

Proposition 2 (Validity).

Set for all .

Proof.

It suffices to show that . Since and , we must have for all . Hence, we find that

where the first inequality is due to Hölder’s inequality, and the second one is because of . Hence, , concluding the proof. ∎

Moreover, we now show how to use to construct an equivalent convex formulation of the NP-hard problem (8). Note that in Proposition 3 below, we set .

Proposition 3 (Optimality).

Proof.

It suffices to show that problem (8) is equivalent to

| (12a) | ||||

| s.t. | (12b) | |||

In any feasible solution of (12), we find that

| (13) |

where the first inequality follows directly from the definition of the absolute value and the second inequality follows from constraints . Moreover, both inequalities (13) hold at equality in an optimal solution, since otherwise, it is always possible to increase/decrease for some index without violating feasibility while improving the objective value. Thus, projecting out variables , problem (12) reduces to (10), which, as shown in the proof of Proposition 1, is equivalent to (8). ∎

Propositions 2 and 3 together come with an alternative representation of which is expressed as intersections of sets for all .

Theorem 1.

The convex hull of can be described (with an infinite number of constraints, one for each ) as

| (14) |

Proof.

It is sufficient to show that the following two optimization problems

| (15) | |||

| (16) |

are in fact equivalent. First, due to Proposition 2, we find that (16) is a relaxation of (15). Second, the problem is a further relaxation of (16), as it is obtained by dropping all the constraints but one. Third, due to Proposition 3, this further relaxation is exact, and thus (16) is exact as well. This concludes the proof. ∎

The description (14) of can be highly nonlinear, since it involves an infinite number of constraints. However, the significance of Theorem 1 is that to understand it suffices to study the polyhedral set , which is arguably a simpler task due to advances in polyhedral theory, and since this set does not involve complementarity or other constraints linking the discrete and continuous variables. In §4 we discuss how to obtain strong relaxation of in general. However, an alternative approach to obtain valid inequalities is to restrict the values of , as the examples below show.

Example 1.

Let for some , where is the standard -th basis vector of . In this case,

Thus, we find that big-M constraints (1) are“ necessary” to describe . ∎

Example 2.

Suppose that , and let . In this case

In particular we find that the inequality , which was studied in [12] in the context of sparse PCA, is “necessary” to describe in this case. ∎

4 Convex relaxations

This section discusses how to describe or approximate . Interestingly, this family of polyhedra has already been studied in the literature. In §4.1 we review existing results on the facial structure of . In §4.2 we study the natural nonlinear relaxation of , show that this relaxation is guaranteed to be strong, and establish links between this relaxation and the perspective relaxation .

4.1 Short review of relaxations via linear inequalities

We assume in this section that . Given , the facial structure of polyhedron was first studied in [1], and the results were later refined in [19]. We now review these results.

Define , and define the set function as . Since function is submodular, the submodular inequalities of Nemhauser et al. [18] are valid for its hypograph. In particular, letting , the inequalities

| (17a) | |||||

| (17b) | |||||

are valid for . However, coefficients in (17a) and in (17b) are not tight. Thus, inequalities (17) are, in general, weak, and better inequalities can be obtained via lifting. Specifically, given , the base inequality

| (18) |

is facet-defining for . Inequality (18) can then be lifted into a facet-defining inequality for through maximal lifting. In this case, lifting is sequence independent and the resulting inequality can be obtained in closed form, see [19, Theorem 4]. Similarly, inequality (17b) can be improved through lifting, see [19, Theorem 5]. While the inequalities discussed here are facet-defining for the case , they may be weaker for the case with more general constraints. Nonetheless, we point out that strong valid inequalities have also been proposed for the case where is defined by a knapsack constraint, see [24].

4.2 Natural convex relaxation

Consider the natural nonlinear relaxation of , obtained by simply dropping the integrality constraints on variables :

While is hard to compute in general as it involves computing the convex hull of the feasible region , it can be obtained easily for example if , for some , or more generally if the constraints defining are totally unimodular. Moreover, the nonlinear constraint defining is SOCP-representable. Thus, this continuous relaxation can be used with many off-the-shelf solvers.

Optimization over relaxation has also been studied in the literature [3]. Specifically, consider the convex relaxation of the problem (11) given by

| (19a) | ||||

| s.t. | (19b) | |||

Proposition 4.

There exists an optimal solution of (19) where lies on an edge of . Moreover, if for all , then , where is the optimal objective value of problem (11) –equivalently, problem (8)–, and is the objective value of the feasible solution obtained by rounding to the best of the two extreme points of defining the edge where it lies.

In other words, Proposition 4 states that the solution of (19) is “close” to integral (e.g., if , then has at most one fractional coordinate), that its associated objective value is similar to the optimal objective value of the mixed-integer problem, and that rounding of this solution yields a constant factor approximation algorithm under mild conditions.

Proof of Proposition 4.

Now consider the relaxation of , as defined in (14), obtained by replacing polyhedra with their nonlinear relaxations :

| (21) |

Proposition 5 below states that the relaxation is in fact equivalent to the perspective relaxation.

Proposition 5.

Proof.

Note that the set can be described with constraint and the single nonlinear constraint

| (22) |

Since the function in (22) is positively homogeneous in , it follows that either the optimization problem in unbounded (and the constrained is violated), or the optimization problem is bounded (and the constraint is satisfied). Finally, a characterization on whether this problem is bounded or not can be found in [14, Proposition 2]: problem (22) is unbounded if and only if . Thus, concluding the proof.

∎

Remark 2.

5 Approximate robust counterpart

We now turn our attention to the robust optimization problem (5) with uncertainty set (6), discussed in §1.1. Instead of solving (5) directly, which is difficult due to the discrete uncertainty set, we propose to solve instead the perspective approximation

| (23) |

Since we relaxed the inner maximization problem, it follows that (23) is a conservative approximation of (5). Moreover, since does not appear in the objective of the inner maximization problem, the condition of Proposition 4 is satisfied: for any fixed the objective value of the inner maximization problem in (23) is at most times the corresponding objective value in (5). Thus, if for all , then solving (23) results in a -approximation algorithm for (5). We now derive a conic-quadratic formulation of problem (23).

Proposition 6.

Given , let be a permutation of such that , and let be the sum of the largest such values. Then problem (23) is equivalent to

Moreover, this problem can be reformulated as the SOCP

| (24a) | |||||

| s.t. | (24b) | ||||

| (24c) | |||||

| (24d) | |||||

Observe that since both and , (24b) are rotated cone constraints and thus (24) is indeed SOCP-representable (provided that is). The derivation of Proposition 6 is based on the following Fenchel duality result used in [4].

Lemma 1 (Fenchel dual).

For any and ,

Proof.

If , then both sides of the equality are . If and , then both sides are equal to . Otherwise, an optimal solution of the maximization problem is , and the corresponding objective value is . ∎

Proof of Proposition 6.

We find that

| ( Lemma 1 and Sion’s minimax theorem) | ||||

| () | ||||

| () |

The formulation above corresponds directly to the SOCP formulation (24). We now continue projecting out variables to recover the explicit form in the original space of variables:

| () | ||||

| () |

Finally, for any fixed , an optimal value of is given by -largest value of , i.e., , concluding the proof. ∎

6 Computations

According to the results of §4, the perspective is a simple relaxation that is guaranteed to be strong (Proposition 4). Thus, we suggest its use in practice. Note that if set appears directly in an optimization problem (e.g., the first two applications discussed in §1.1), the perspective is arguably already the state-of-the-art relaxation – thus we omit computations for those cases. However, we illustrate its application to the robust optimization problem (5) with uncertainty set (6). In particular, we consider a simple portfolio optimization problem with

6.1 Methods

We compare three conservative approximations of (5) – the first two are based on commonly used methods in the literature.

Budgeted uncertainty

Ellipsoidal uncertainty

Perspective approximation

The approach we propose, described in §5.

6.2 Results

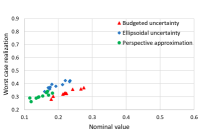

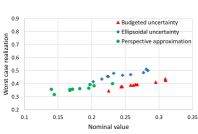

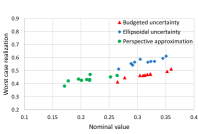

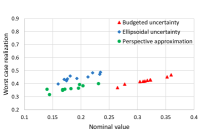

We set in our computations, and we set and in our computations. Each entry of and is drawn from an uniform distribution on the interval – under these conditions, since and , then for all and the perspective approximation is a 1.25 approximation algorithm for (5). All optimization problems are solved using CPLEX 12.8 with the default settings, in a laptop with Intel Core i7-8550U CPU and 16 GB RAM. Solution times for all methods are less than 0.1 seconds in all cases.

For each combination of parameters , we generate 10 instances and record for each method: the nominal objective value , where is the solution produced; and the worst-case realization given by

| (25) |

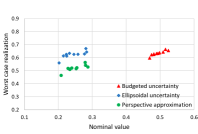

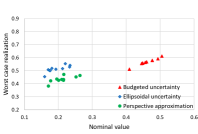

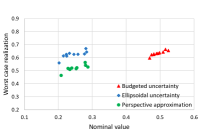

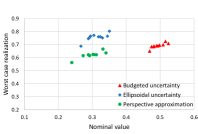

Note that computing the worst-case realization requires solving a mixed-integer optimization problem. However, since the perspective reformulation results in a strong relaxation and is not too large, problem (25) can be comfortably solved to optimality using CPLEX. Figure 1 presents the results, showing the nominal objective value and worst-case realization for each combination of parameters and each instance.

We observe that the budgeted uncertainty approach consistently has the worst nominal performance, although it tends to be better in terms of robustness than the ellipsoidal uncertainty. The perspective approximation results in the “best” worse-case realizations for all the combinations of parameters. It also results in the best solutions in terms of the nominal values, except for the case with and (where the ellipsoidal uncertainty has slightly better nominal performance). Thus, in our experiments, we can conclude that the perspective approximation is the best approach, delivering the most reliable solutions without affecting (and in most cases improving) the nominal performance.

7 Conclusion

We characterized the structure of the set , established links between the convexification of this set and convexification of polyhedral sets, and studied the strength of the perspective relaxation . On the one hand, we showed in this paper that the perspective reformulation is insufficient to describe , and that does not even match the structure of : using the perspective reformulation to approximate is akin to using a nonlinear relaxation to approximate a polyhedral set, see Proposition 5. On the other hand, we showed that while the perspective reformulation can be strengthened using polyhedral theory as discussed in §4.1, it is already quite strong. Our experiments on robust optimization with discrete uncertainty sets suggest that the perspective reformulation can be used as an accurate proxy, resulting in tractable approximations that outperform classical alternatives in the literature.

8 Acknowledgments

Andrés Gómez was supported in part by grant 2006762 from the National Science Foundation, and by grant FA9550-22-1-0369 from the Air Force Office of Scientific Research. Weijun Xie was supported in part by grants 2046426 and 2153607 from the National Science Foundation.

References

- Ahmed and Atamtürk [2011] Shabbir Ahmed and Alper Atamtürk. Maximizing a class of submodular utility functions. Mathematical Programming, 128(1-2):149–169, 2011.

- Aktürk et al. [2009] M Selim Aktürk, Alper Atamtürk, and Sinan Gürel. A strong conic quadratic reformulation for machine-job assignment with controllable processing times. Operations Research Letters, 37:187–191, 2009.

- Atamtürk and Gómez [2017] Alper Atamtürk and Andrés Gómez. Maximizing a class of utility functions over the vertices of a polytope. Operations Research, 65:433–445, 2017.

- Atamtürk and Gómez [2020] Alper Atamtürk and Andrés Gómez. Safe screening rules for L0-regression from perspective relaxations. In International Conference on Machine Learning, pages 421–430. PMLR, 2020.

- Atamtürk and Narayanan [2008] Alper Atamtürk and Vishnu Narayanan. Polymatroids and mean-risk minimization in discrete optimization. Operations Research Letters, 36(5):618–622, 2008.

- Bacci et al. [2019] Tiziano Bacci, Antonio Frangioni, Claudio Gentile, and Kostas Tavlaridis-Gyparakis. New MINLP formulations for the unit commitment problems with ramping constraints. Optimization, 2019.

- Ben-Tal and Nemirovski [2000] Aharon Ben-Tal and Arkadi Nemirovski. Robust solutions of linear programming problems contaminated with uncertain data. Mathematical Programming, 88(3):411–424, 2000.

- Bertsimas and Sim [2004] Dimitris Bertsimas and Melvyn Sim. The price of robustness. Operations Research, 52(1):35–53, 2004.

- Borrero and Lozano [2021] Juan S Borrero and Leonardo Lozano. Modeling defender-attacker problems as robust linear programs with mixed-integer uncertainty sets. INFORMS Journal on Computing, 33(4):1570–1589, 2021.

- Ceria and Soares [1999] Sebastián Ceria and João Soares. Convex programming for disjunctive convex optimization. Mathematical Programming, 86(3):595–614, 1999.

- d’Aspremont et al. [2008] Alexandre d’Aspremont, Francis Bach, and Laurent El Ghaoui. Optimal solutions for sparse principal component analysis. Journal of Machine Learning Research, 9(7), 2008.

- Dey et al. [2021] Santanu S Dey, Rahul Mazumder, and Guanyi Wang. Using -relaxation and integer programming to obtain dual bounds for sparse pca. Operations Research, 2021.

- Frangioni and Gentile [2006] Antonio Frangioni and Claudio Gentile. Perspective cuts for a class of convex 0–1 mixed integer programs. Mathematical Programming, 106(2):225–236, 2006.

- Gómez [2021] Andrés Gómez. Strong formulations for conic quadratic optimization with indicator variables. Mathematical Programming, 188(1):193–226, 2021.

- Günlük and Linderoth [2010] Oktay Günlük and Jeff Linderoth. Perspective reformulations of mixed integer nonlinear programs with indicator variables. Mathematical Programming, 124:183–205, 2010.

- Kim et al. [2021] Jinhak Kim, Mohit Tawarmalani, and Jean-Philippe P Richard. Convexification of permutation-invariant sets and an application to sparse principal component analysis. Mathematics of Operations Research, 2021.

- Li and Xie [2020] Yongchun Li and Weijun Xie. Exact and approximation algorithms for sparse PCA. arXiv preprint arXiv:2008.12438, 2020.

- Nemhauser et al. [1978] George L Nemhauser, Laurence A Wolsey, and Marshall L Fisher. An analysis of approximations for maximizing submodular set functions—I. Mathematical Programming, 14(1):265–294, 1978.

- Shi et al. [2022] Xueyu Shi, Oleg A Prokopyev, and Bo Zeng. Sequence independent lifting for a set of submodular maximization problems. Mathematical Programming, pages 1–46, 2022.

- Wei et al. [2020] Linchuan Wei, Andrés Gómez, and Simge Küçükyavuz. On the convexification of constrained quadratic optimization problems with indicator variables. In International Conference on Integer Programming and Combinatorial Optimization, pages 433–447. Springer, 2020.

- Wei et al. [2021] Linchuan Wei, Andrés Gómez, and Simge Küçükyavuz. Ideal formulations for constrained convex optimization problems with indicator variables. Mathematical Programming, 2021.

- Wei et al. [2022] Linchuan Wei, Alper Atamtürk, Andrés Gómez, and Simge Küçükyavuz. On the convex hull of convex quadratic optimization problems with indicators. arXiv preprint arXiv:2201.00387, 2022.

- Xie and Deng [2020] Weijun Xie and Xinwei Deng. Scalable algorithms for the sparse ridge regression. SIAM Journal on Optimization, 30(4):3359–3386, 2020.

- Yu and Ahmed [2017] Jiajin Yu and Shabbir Ahmed. Maximizing a class of submodular utility functions with constraints. Mathematical Programming, 162(1-2):145–164, 2017.

- Zou et al. [2006] Hui Zou, Trevor Hastie, and Robert Tibshirani. Sparse principal component analysis. Journal of Computational and Graphical Statistics, 15(2):265–286, 2006.