Mechanism Learning for Trading Networks

Abstract

We study the problem of designing mechanisms for trading networks that satisfy four desired properties: dominant-strategy incentive compatibility, efficiency, weak budget balance (WBB), and individual rationality (IR). Although there exist mechanisms that simultaneously satisfy these properties ex post for combinatorial auctions, we prove the impossibility that such mechanisms do not exist for a broad class of trading networks. We thus propose approaches for computing and learning the mechanisms that satisfy the four properties, in a Bayesian setting, where WBB and IR, respectively, are relaxed to ex ante and interim. For computational and sample efficiency, we introduce several techniques, including game theoretical analysis to reduce the input feature space. We empirically demonstrate that the proposed approaches successfully find the mechanisms with the four properties for those trading networks where the impossibility holds ex post.

1 Introduction

Trading networks, where firms trade via bi-lateral contracts, are becoming increasingly ubiquitous and essential to the world’s economy in vital areas such as transportation and supply chain. The purpose of such a trading network is both to benefit its participants and to contribute to the external markets. As such, a major goal of a trading network is efficiency in the sense of maximizing the value (social welfare) that the trading network creates (Hatfield et al., 2013).

The prior work on trading networks primarily investigates solution concepts such as stability and competitive equilibrium (Hatfield et al., 2013; Candogan, Epitropou, and Vohra, 2021), which can be shown to imply efficiency. To compute these solutions for a given trading network, however, one would require the full information about the value of each subset of trades to each firm (or the type of the firm), which is typically private information and needs to be truthfully revealed by the firms. As we will show, however, the firms typically have incentive to be untruthful.

Our goal in this work is to provide a mechanism for a given trading network such that the firms in the trading network have the incentive to be truthful, which in turn leads to efficiency. For this purpose, we follow the standard practice in mechanism design of introducing the payment to or from an Independent Party (IP) in the trading network and assume that there is a prior distribution over the types of the firms (i.e., we consider a Bayesian setting). More specifically, in this setting, we seek to compute (or learn) the mechanism that satisfies weak budget balance (WBB; which ensures non-negative utility of IP) and individual rationality (IR; which ensures non-negative utility of firms) in addition to efficiency and incentive compatibility (which promotes truthfulness). These four properties are standard in the literature of mechanism design (Parkes, 2001), and, for combinatorial auctions, the VCG mechanism with the Clarke pivot rule is known to satisfy all of the four properties ex post, i.e. surely for any types, (Nisan, 2007).

Notice, however, that trading networks are fundamentally more complex than combinatorial auctions. For example, a trade is a transfer of a good from a seller to a buyer, and the seller who has negative valuation on the trade is compensated by the payment from the buyer. We will show that, in this more complex settings, it is impossible to simultaneously satisfy all of the four properties ex post for a broad class of trading networks.

We thus relax the WBB and IR properties and seek to compute a mechanism that respectively satisfies these properties ex ante and interim (i.e., in expectation with respect to the prior distribution over the types) rather than ex post. To this end, we restrict ourselves to the class of Groves mechanisms to ensure incentive compatibility and efficiency and compute the pivot rule of a Groves mechanism via a linear program (LP) that encodes WBB and IR as constraints.

While this LP successfully computes a mechanism that simultaneously satisfies the four properties, it involves two fundamental challenges. First, the mechanism designer needs the exact knowledge of the prior distribution of types. Second, the linear program becomes intractable as the number of trades, players, or their types increases.

We thus further provide an approach of learning a mechanism from the sample of the prior distribution of types to mitigate the shortcomings of the computational approach. With the proposed learning approach, the mechanism designer only requires the access to the sample instead of the precise knowledge of the prior distribution. In addition, we propose several techniques to reduce the computational complexity in the proposed mechanism learning. In particular, we manually design special Groves mechanisms, which achieve some but not all of the four properties ex post, and demonstrate how the dimension of the feature vector of the types may be reduced based on the knowledge of those special Groves mechanisms.

Contributions

Our contributions are fourfold. First, we prove a fundamental theorem that holds for any mechanism for trading networks with payment to/from IP (Theorem 1), which shows that we may ignore the payment between firms without loss of generality. This greatly reduces the set of possible mechanisms that needs to be considered, thereby greatly simplifying the subsequent analysis and proposed algorithms. Second, we prove the impossibility of simultaneously satisfying the four properties ex post in trading networks (Theorem 2), which is analogous to the Myerson–Satterthwaite theorem (Myerson and Satterthwaite, 1983). Unlike the Myerson–Satterthwaite theorem, however, our theorem does not require the assumption that the prior distribution on types has absolutely continuous density. Third, we provide the approaches of automated mechanism design (Conitzer and Sandholm, 2002; Sandholm, 2003) for trading networks, by formulating an optimization problem and its learning variant whose solutions give the mechanisms that achieve the four properties, two in ex post and two in ex ante/ interim, and propose techniques to reduce the computational complexity in computing or learning the solution to these optimization problems (see Sections 5-6). These include the technique of reducing the dimensionality of the feature vector based on the manually designed special Groves mechanisms. Finally, we provide empirical support on the effectiveness of the proposed computational and learning approaches to mechanism design for trading networks (see Section 7).

Related Work

Trading networks and their efficiency have been extensively studied (Hatfield et al., 2013; Candogan, Epitropou, and Vohra, 2021; Ostrovsky, 2008; Hatfield and Kominers, 2012; Hatfield et al., 2015)), but no AMD approaches are known to simultaneously achieve the four properties in trading networks. In fact, there are few studies on incentive compatibility in trading networks with an exception of Schlegel (2022), who establishes incentive compatibility but only for those firms who are buyers (or sellers) in all trades.

From methodological perspectives, the prior work most related to ours is some of the AMD approaches for combinatorial auctions, where constrained optimization problems are formulated and approximated with the sample from the prior distribution of types. However, in Duetting et al. (2019); Rahme, Jelassi, and Weinberg (2021), DSIC is encoded as a constraint of the optimization problem and is not necessarily guaranteed due to the sample approximation unless the dataset covers the full support of the prior distribution, while we always ensure DSIC via the Groves mechanism. On the other hand, Manisha, Jawahar, and Gujar (2018); Tacchetti et al. (2022) learn the mechanism (specifically, the rule of redistributing payment from IP to players) that minimizes the expected revenue of IP, while ensuring the four properties via the VCG mechanism. In trading networks, however, we can guarantee only two properties via the Groves mechanism, and we encode the other two properties as constraints of our optimization problem.

Alon et al. (2021) also study an approach of computing (no learning) a mechanism for a principal-agent model as a solution to LP, while ensuring some of the properties via the VCG mechanism. Earlier work along this line of computing a mechanism within a restricted class of mechanisms includes Likhodedov and Sandholm (2004), who maximize expected revenue in combinatorial auctions. Sample approximation of this method is studied by Likhodedov and Sandholm (2005).

2 Trading networks

Following Hatfield et al. (2013), we model a trading network by a tuple , where is a set of players (or firms), is a set of bi-lateral trades, and , where each is the type (valuation) of player . That is, represents the (possibly negative) value of for the player with type . Without loss of generality, we assume that the value of no trade is zero for any player (i.e., ). Each trade is associated with a seller and a buyer in , and the buyer makes non-negative payment to the seller. Let be the payment associated with . We refer to a pair as a contract. A pair of and determines a set of contracts444 may need to specify the payment for to discuss some of the properties., .

One’s goal with a trading network is to determine a set of trades to be conducted together with the payment associated with each trade in a way that certain properties are satisfied. A particularly important metric is the total valuations associated with the trades to be conducted (i.e., ), since it is the value that the trading network produces to the external market(s). In particular, we say that the set of trades is efficient for a trading network if

| (1) |

The efficiency may also be represented in terms of the utilities of players. Specifically, when the set of contracts is conducted, the player gets the following (quasi-linear) utility555In the literature of trading networks (e.g., Hatfield et al. (2013)), a valuation function is often denoted by and a utility by , but we use the notations from mechanism design. Also, we reserve for the utility defined in Section 3 and use here.:

| (2) |

where is the subset of where is the seller, and is the one where is the buyer. Now, since we have

| (3) |

for any , the total payment from sellers equals the total payment to buyers:

| (4) |

which together with (2) implies

| (5) |

for any . Therefore, for any , (1) is equivalent to

| (6) |

The prior work has developed several algorithms for finding the set of contracts that achieve the properties that are stronger than efficiency (e.g., competitive equilibrium and stability) under certain conditions (e.g., full substitutability (Hatfield et al., 2019)). However, they all rely on the knowledge of the types .

In practice, however, the types are private information and need to be revealed by the players. Then, the players can have the incentive to be untruthful, which in turn leads to inefficiency, as the following example shows:

Example 1.

Consider a trading network with a single potential trade, , between two players, . With , the seller (S) incurs a production cost , and the buyer (B) gets a profit (retail price minus handling cost): i.e., and , where is the indicator function. Consider the payment, , that equally shares the net profit between S and B. Given the types (i.e., and ), we can achieve efficiency by letting if and otherwise. When , the utility of each player is . However, then each player has the incentive to untruthfully declare slightly higher cost to get slightly higher utility . If the declared cost is too high, the trade is not conducted. Since , untruthfulness indeed leads to inefficiency.

3 Introducing Payment to/from IP

We consider the trading networks where the types are private information of the respective players and study the mechanisms that promote truthfulness and hence lead to efficiency. To facilitate truthfulness, the mechanism may require each player to make (possibly negative) payment to an independent party (IP). A trading network with IP is denoted by , where denotes the set of all players and IP. Also, let be the space of types for each and let . Moreover, let be the set of trading networks with IP under . We will simply refer to or as a trading network.

We study the Bayesian setting where there exists a prior distribution over such that the players have types with probability . Throughout, we assume that the true type of each player is known by that player. We will, however, make varying assumptions on other knowledge about the types, which will be made explicit in each of the results in the following.

3.1 Direct Mechanisms

We study a direct mechanism, where players and IP act according to the following protocol:

-

1.

Each player declares a (possibly untruthful) type

-

2.

IP determines the set of contracts, , and (possibly negative) payment, , from each player to IP

Hence, the direct mechanism of a trading network is specified by an outcome rule , where is the allocation rule that maps declared types, , to a set of trades to be conducted; determines the rule of payment to IP, , for each ; is the payment rule that determines the payment associated with each trade, depending on the declared types. In the following, we refer to a direct mechanism simply as a mechanism.

When is declared by the players in the trading network , each player gets the following utility under the mechanism :

| (7) |

We denote the net-payment to IP (or utility of IP) by

| (8) |

3.2 Desirable Properties

We consider the four desirable properties of a mechanism that is standard in mechanism design (Parkes, 2001): Dominant Strategy Incentive Compatibility (DSIC), Efficiency, Weak Budget Balance (WBB), and Individual Rationality (IR). These properties are known to be simultaneously achievable in combinatorial auctions, but we will see that such positive results do not carry over to trading networks. We formally define each property in the following, but note that, under the Bayesian setting, we can discuss both ex post properties (which hold surely for any ) and ex ante or interim properties (which hold in expectation with respect to the prior distribution over ).

We will formally define each of these properties in the following (see Parkes (2001) for more details). Note that, under the Bayesian setting, we can discuss either ex post properties (which hold surely for any ) or ex ante/interim properties (which hold in expectation with respect to the prior distribution over ).

DSIC is an ex post property and ensures that the best strategy of each player is truthfully revealing its type regardless of the strategies of the other players. This gives a clear course of actions. Formally, we say that a mechanism for a trading network is DSIC if the profile of truthful strategies form a dominant-strategy equilibrium:

| (9) |

where is the strategy profile of players except . We will discuss the corresponding ex ante property of Bayesian Nash Incentive-Compatibility (BNIC) only in relation to the prior work, but BNIC only ensures that a truthful player can maximize its expected utility under the additional condition that other players are truthful.

Efficiency is also an ex post property and ensures that the trades are allocated in a way that they maximize total value. Following the definition without IP in (1), we say that a mechanism for is Efficient if

| (10) |

We will not discuss the corresponding ex ante property.

WBB ensures nonnegative utility of IP. We say that a mechanism for is ex post WBB if

| (11) |

and ex ante WBB if

| (12) |

where the expectation is with respect to the prior distribution of . That is, under the additional condition that the players are truthful (which is guaranteed with DSIC), the utility of IP is non-negative surely under ex post WBB and in expectation under ex ante WBB.

IR ensures that every player gets non-negative utility. IR can also be ex post or ex ante. However, when players know their own types, each player should require non-negative expected utility given its own type, and such a property is called interim IR. Formally, we say that a mechanism for is ex post IR if

| (13) |

for each and interim IR if

| (14) |

for each . That is, under the additional condition that the players are truthful (guaranteed with DSIC), a truthful player gets non-negative utility surely under ex post IR and in expectation under interim IR.

Note that ex post properties are more desirable than the corresponding ex ante properties. For example, maximizing expected utility may not be the objective of risk-sensitive players. Also, the optimality of the truthful strategy under BNIC relies on the truthfulness of the other players, which is not required under DSIC.

3.3 No Payment between Players

We claim that, as far as the utilities of the forms in (7)-(8) are concerned, we do not lose generality by ignoring the payment among players (i.e., ). Formally,

Lemma 1.

For any mechanism and a payment rule for a trading network , there exists a rule of payment to IP such that for any .

Proof.

The following theorem implies that we only need to consider the mechanisms without payment between players to achieve the four properties:

Theorem 1.

For any mechanism and a payment rule for , there exists a rule of payment to IP, such that each of DSIC, Efficiency, WBB (either ex ante or ex post), and IR (either ex ante or interim) is satisfied with iff it is satisfied with .

Proof.

By Lemma 1, for any pair of and , there exists such that utilities of the players and the IP under are the same as those under for any . Hence, it suffices to show that each of the properties depend only on the utilities of the players and the IP. For example, DSIC (9) depends only on the utilities; hence, if is DSIC, i.e.,

| (16) |

then, since for any , we must have

| (17) |

i.e., is DSIC. The converse also holds.

Since it is straightforward to see that ex post WBB (11), ex ante WBB (12), ex post IR (13), and interim IR (14) also depend only on the utilities of the players and the IP, it remains to show that Efficiency depends only on the utilities. Now, observe that (10) is equivalent to

| (18) |

which depends only on the utilities of the players and the IP, which establishes the theorem. ∎

Theorem 1 implies that we only need to consider mechanisms with no payment between players as long as the desirable properties are the ones that depend only on the utility. Namely, for any set of properties that depend on the utility, there exists a mechanism with no payment between players that achieves those properties if and only if there exists a mechanism (with an arbitrary payment rule) that achieves those properties. Hence, we will only consider designing a mechanism without payment between players and denote such a mechanism by . Intuitively, if there is a payment from a buyer to a seller, we can let the buyer pay to IP and let IP pay to the seller without changing the net-payment of the two players and IP.

4 Impossibility

Here, we show that no mechanism can achieve all of the four properties ex post for trading networks with a single potential trade except for trivial cases. Theorem 1 then implies that no mechanisms , with any payment rule , can simultaneously achieve the four properties except for trivial cases. Formally,

Definition 1.

We say that a trading network with a single trade between two players, , has non-trivial if it satisfies both of the following conditions: \romannum1) there exists such that , and \romannum2) for any , there exists such that , where .

In other words, is said to be trivial if at least one of the two conditions in Definition 1 are violated. When condition \romannum1) is violated, the trade should always be conducted (i.e., ) for Efficiency to hold, and all of the four properties are trivially satisfied with a constant payment rule666The simple example in (Othman and Sandholm, 2009), where impossibility is shown not to hold, violates condition \romannum1.. Specifically, consider a seller (S) and a buyer (B), and let be the minimum value of the trade for each . Since condition \romannum1) is violated, we have . Without loss of generality, let . Then, with the constant payment rule of and , it is straightforward to verify that the four conditions are satisfied.

When condition \romannum2) is violated, there exists a player who has the type that makes it impossible to make the social welfare, , positive no matter what types that the other player has. Such player should not participate in the trading network from the perspective of social welfare, even if all of the four properties may be achieved with some mechanisms.

For other non-trivial cases, no mechanisms achieve all of the four properties. Formally,

Theorem 2.

For any trading network with a single trade between two players having non-trivial , no mechanisms can achieve all of DSIC, Efficiency, ex post WBB, and ex post IR.

Proof.

Let be the two players. For each , let be the type that gives the lowest value on the trade, and let be the one giving the highest value. We say that player with has type for . We will show that we cannot simultaneously satisfy the conditions for the four properties associated with the players of those types (L and H).

We first consider the allocation rule , where are the types declared by (S, B). Efficiency (10) and the non-triviality of imply that we must have

| (21) |

Myerson and Satterthwaite (1983) show similar impossibility but assumes that the prior distribution over has absolutely continuous density, which does not hold e.g. for discrete (Othman and Sandholm, 2009). Our impossibility theorem does not require such an assumption, but ours is with DSIC and hence weaker in that respect than Myerson-Satterthwaite’s, which establishes impossibility with BNIC.

5 Computing Mechanisms

The impossibility suggested by Theorem 2 motivates us to study the mechanisms that achieve weaker properties of ex ante WBB and interim IR in addition to DSIC and Efficiency. These weaker properties are still meaningful in practice and are sufficient for risk-neutral players.

To guarantee DSIC and Efficiency, we rely on the Groves mechanism. For any trading network , a mechanism is called a Groves mechanism if it can be represented by the use of a pivot rule, where , as follows:

| (32) | ||||

| (33) |

for any . Here, the pivot rule determines the payment, in addition to the second term of the right-hand side of (33), in a way that it depends only on the types of other players (and not the type of player ). The Groves mechanism is guaranteed to satisfy Efficiency and DSIC, and we may arbitrarily choose to achieve other properties. We refer to as a Groves mechanism when it does not cause confusion.

With a Groves mechanism , the condition for ex ante WBB (12) is reduced to

| (34) | ||||

| (35) | ||||

| (36) |

and interim IR (14) is reduced to

| (37) | ||||

| (38) | ||||

| (39) |

There may or may not exist an that satisfies both ex ante WBB and interim IR. When it does not exist, one could seek to find the that minimizes the violation of these conditions. However, here we focus on studying whether such an exists and finding one if it does. Also, when there are multiple that satisfy both ex ante WBB and interim IR, we prefer the one with stronger budget balance (i.e., the total payment to IP should be as close to zero as possible).

Therefore, we proposed to find as the solution to the following optimization problem:

| (40) | ||||

| s.t. | (41) | |||

| (42) |

where is the expectation with respect to the prior distribution of types. The constraint (41) is on ex ante WBB and corresponds to (36). The constraint (42) is on interim IR and corresponds to (39). for a given trading network , the right-hand sides of (41)-(42) are constants that can be computed by the use of the allocation rule and the prior distribution of types When and are finite, the optimization problem (40)-(42) is a linear program (LP), where variables are for . When there are players, and each player has types, the LP has variables and constraints.

Example 2.

Consider the trading network in Example 1, but we now assume that each player has one of two types: the production cost of the seller of type is for , and the handling cost of the buyer of type is for . Let for . By Theorem 2, there is no mechanism that simultaneously achieves the four properties ex post when and for . Under the Groves mechanism, the amount of payment to IP from S of type and B of type is respectively given by

| (43) | ||||

| (44) |

where is the number of goods to be traded when the types of S and B are and respectively. Note that the pivot rule of each player depends on the type of the other player and can be determined by solving the optimization problem (40)-(42), which is reduced to the following for this example:

| (45) | ||||

| s.t. | (46) | |||

| (47) | ||||

| (48) |

where the expectation is with respect to the prior distribution of types. This is an LP with four variables and four constraints.

Although the solution to the optimization problem (40)-(42) indeed gives non-trivial Groves mechanisms that are of practical interest, it is intractable except for small trading networks. For example, \romannum1) there can be infinitely many types , which results in infinitely many variables in the optimization problem. Also, \romannum2) one may not know the exact prior distribution of types, which we need to compute the expectation in (40)-(42). In addition, \romannum3) it may be hard to compute the efficient allocation for a given .

6 Learning Mechanisms

Among the three challenges, \romannum1) and \romannum2) are fundamental, since one cannot even represent the optimization problem with infinitely many variables or without knowing the prior distribution. Here, we propose learning techniques to overcome these challenges. For the computational complexity of , efficient algorithms are known under some conditions on (Candogan, Epitropou, and Vohra, 2021; Iwata, Moriguchi, and Murota, 2005).

6.1 Learning Pivot Rules

We now assume that the mechanism designer (IP) has access to the sample of types from the prior distribution , rather than the exact knowledge on . The expectation in (40)-(42) can then be replaced with sample average, which solves Challenge \romannum2). IP may collect such by running a Groves mechanism that is not necessarily ex ante WBB (hence, IP needs investment). Since players act truthfully under the Groves mechanism, the collected should follow 777Assuming that players (or their types) are sampled independently each time.. One may then learn a better Groves mechanism (which less violates WBB) and collect additional data with the new mechanism for learning even better mechanisms (with the hope of eventually achieving ex ante WBB).

Recall that the variables in (40)-(42) correspond to the output values of the pivot rule, for and , which constitute the codomain of the functions . To deal with infinitely many variables that stem from the functions with infinite codomain, we approximate those functions with machine learning models, where with parameter for each .

Such approaches of machine learning have been successfully applied in the prior work of mechanism learning. Unfortunately, in our case, it is not sufficient to replace the expectation with sample average and with . In particular, the constraint (42) is problematic. Since the set is often small and can be empty for some , the sample average is unreliable or cannot be obtained with the empty set. A solution to this problem is to learn, for each , a regressor (e.g., Gaussian process regressor) that maps to for , where the training data is . Let be such a regressor trained with for .

We can now reduce (40)-(42) to the following constrained non-linear optimization and learn a locally optimal with the augmented Lagrangian method:

| (49) | ||||

| s.t. | (50) | |||

| (51) |

where is the set of the types of player that appear in . More precisely, we use a lower confidence bound for in (51) and an upper confidence bound for the right-hand side of (50). The learning problem (49)-(51) matches the optimization problem (40)-(42) in the limit of when the law of large numbers applies to the sample averages (e.g., has finite variance), the regressors are asymptotically consistent (i.e., ), the optimal is in the class of (i.e., realizable), the support of the prior distribution covers the whole , and is finite.

Although the use of alleviates Challenge \romannum1), the issue of computational complexity still remains. Namely, each takes types as its input, but each type is a function . A question is how to represent those functions. One may for example assume that the types are in a certain parametric family of functions (e.g., neural networks); then their parameters may be given as the input to (Faccio, Kirsch, and Schmidhuber, 2021).

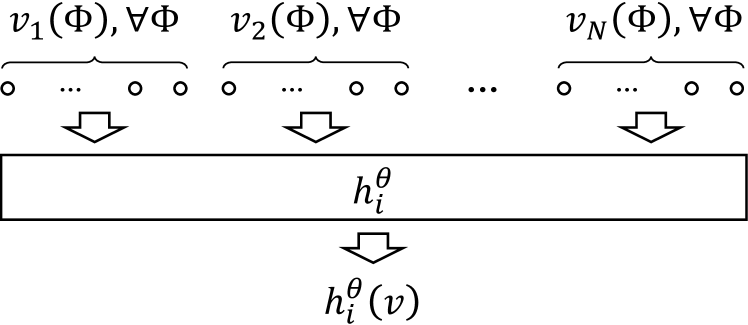

We take an alternative approach of representing a function with its output values (Harb et al., 2020). Observe that can be fully characterized by a -dimensional valuation-vector, , that represents the output values for all of the possible inputs. Each can then be seen as a function that maps vectors, each having dimensions, to a real number; namely, (see Figure 1(a)).

(a)

(b)

6.2 Variable Reduction

The valuation-vector has exponentially many dimensions and does not fully resolve Challenge \romannum1). We now show, based on game theoretic analysis, that some of the features of the valuation-vector are particularly important to achieve some of the desirable properties. A low dimensional valuation-vector can then be formed with these important features.

To this end, we have designed the following special Groves mechanisms:

| (52) | ||||

| (53) |

where is the set of trades where player is neither the seller nor the buyer. We will utilize these mechanisms, because it can be shown that is always ex post WBB, and is ex post IR when no players reduce the social welfare, where a player reducing the social welfare is defined as follows:

Definition 2.

In a trading network , a player with type is called a negative player if there exists such that

| (54) |

Formally,

Theorem 3.

Proof.

Since DSIC and Efficiency are guaranteed with the Groves mechanism, it suffices to prove ex ante WBB and interim IR, respectively. Under , the payment from to IP is

| (55) | ||||

| (56) | ||||

| (57) |

for any . We thus have for any , which implies ex post WBB (11). Also, when there are no negative players, the utility of player under is

| (58) | ||||

| (59) |

for any , which implies ex post IR (13). ∎

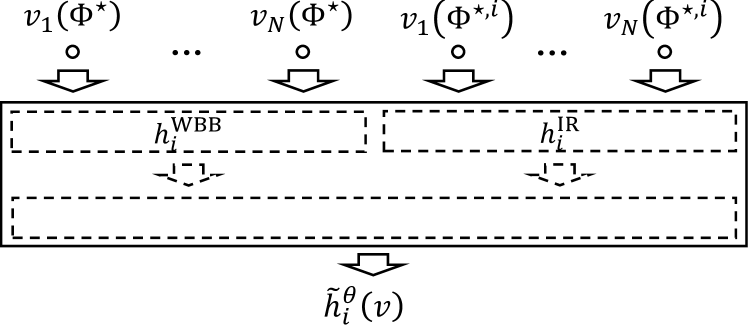

Since and , respectively, achieve ex post WBB and interim IR, one might expect that their combination may simultaneously achieve the weaker properties of ex ante WBB and interim IR. Observe that an arbitrary combination of two functions can be represented by a function that takes the input of the two functions. Since

we see that and are the input of and , respectively, and hence are the important features of the valuation-vector. We may thus seek to find the optimal function within the class of functions that take those important features as input (see Figure 1). We may also consider a larger class of functions by allowing additional (e.g., random) elements of the original valuation-vector as input, trading off the quality of approximation against computational complexity.

7 Experiments

We conduct our experiments with trading networks where it is impossible to achieve all of the four desirable properties ex post. Specifically, we generate non-trivial instances of trading networks uniformly at random in the setting of Example 2, which involves a single potential trade between a seller and a buyer888 To generate non-trivial instances, we first randomly generate 10,000 instances that are not necessarily non-trivial (for each player, pairs of numbers in [0,1] are generated uniformly at random and let those values be the cost of the two types; the prior probabilities of the types are also chosen uniformly at random). Out of those instances, 1,642 have non-trivial and used in the experiments. . By Theorem 2, there exist no mechanisms that satisfy all of the four desirable properties ex post for those non-trivial instances. We apply our proposed AMD approaches to these trading networks and study whether they can find the mechanisms that satisfy the four properties if WBB is ex ante and IR is interim.

7.1 Validating Computational Approach

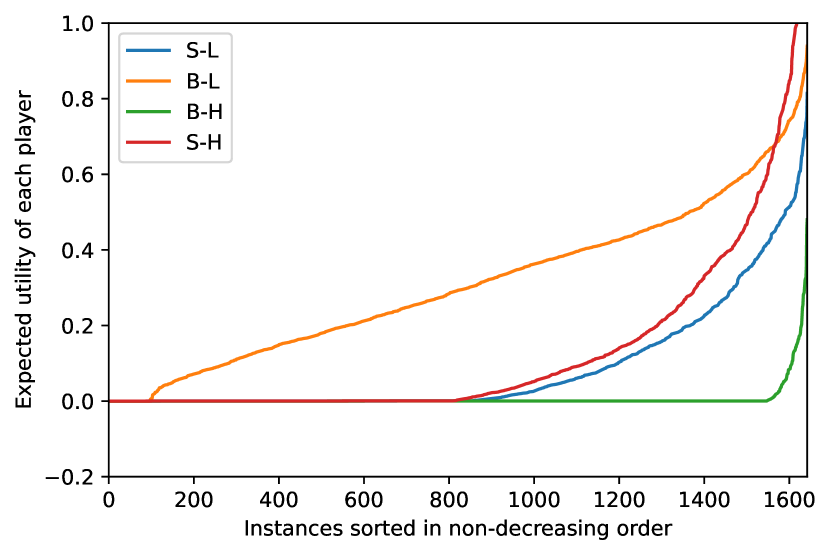

We first validate our computational approach by applying it to each of the randomly generated instances. Here, we solve the optimization problem in (40)-(42) via CPLEX 22.1.

(a) Budget balance

(b) Utility

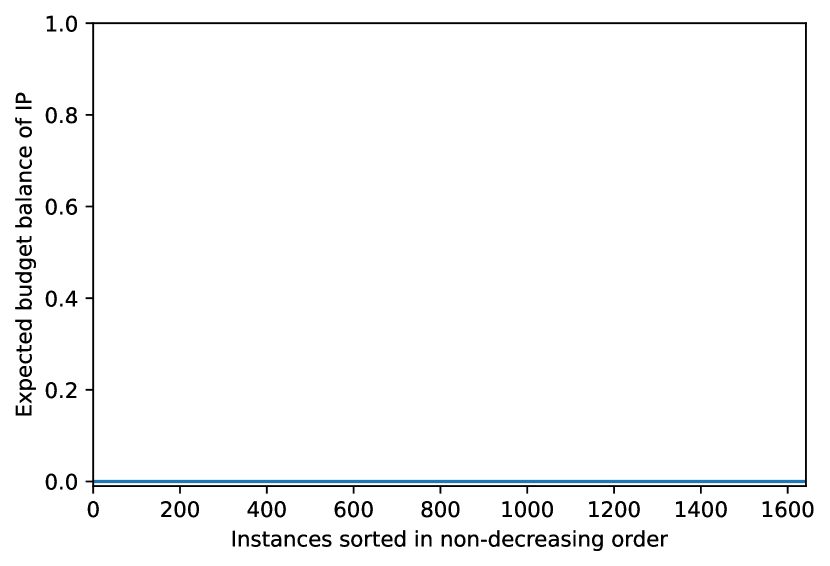

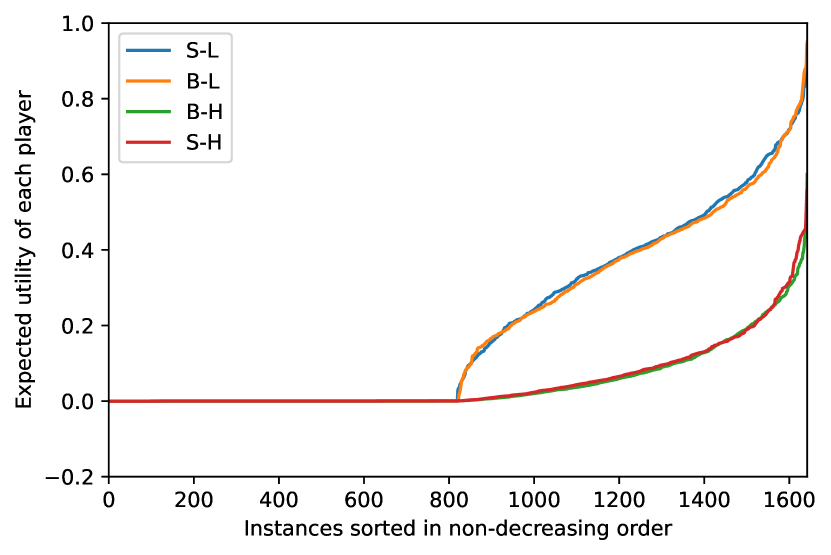

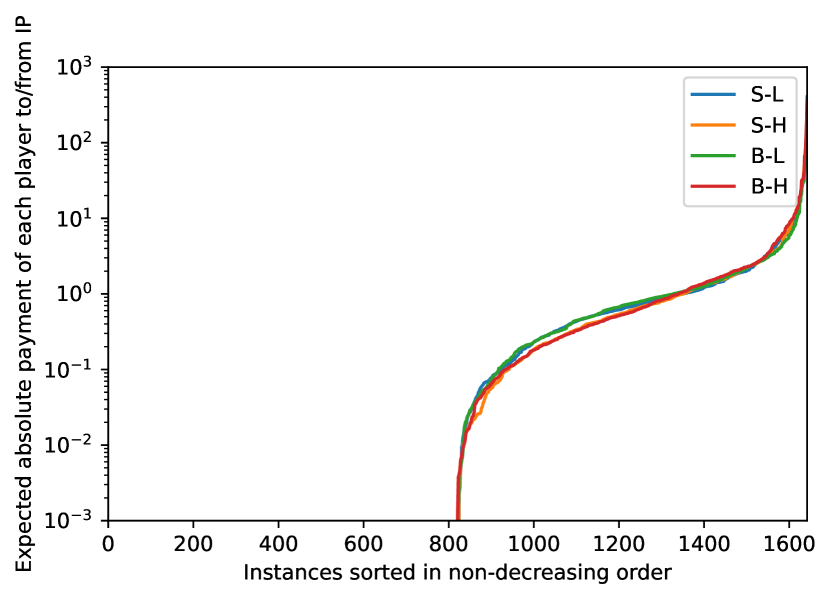

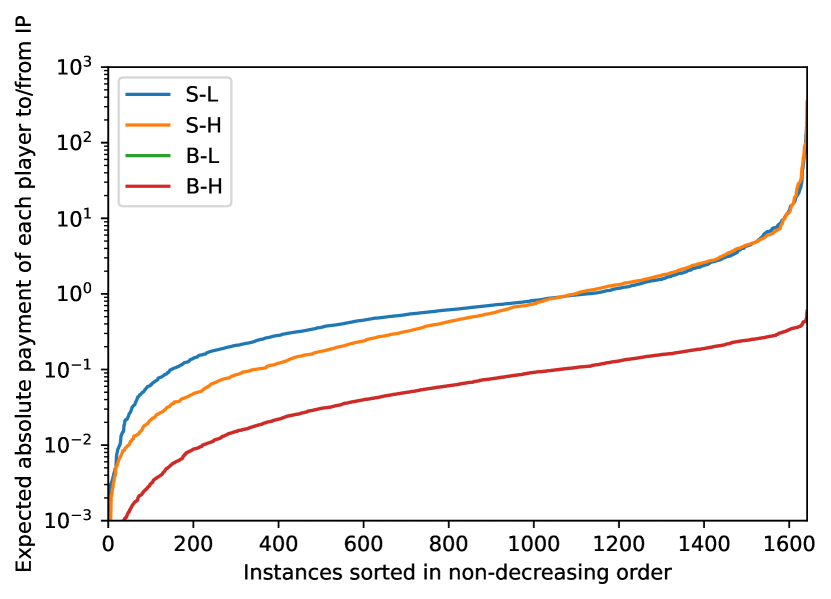

Figure 2 shows the expected budget balance (utility) of IP in (a) and the expected utility of each player in (b) for the 1,642 instances plotted in non-decreasing order. Observe that, for all instances, IP expects essentially zero budget balance, and every player (supplier or buyer of any type) expects non-negative utility. Therefore, the proposed approach finds the mechanism that achieves both of ex ante WBB999In fact, strong budge balance is achieved. and interim IR (in addition to DSIC and Efficiency) for every randomly generated instance where achieving the four properties ex post is impossible.

This however does not mean that one can always achieve ex ante WBB and interim IR. There indeed exist instances for which ex ante WBB or interim IR cannot be achieved. Empirically, however, such infeasible instances appear to have zero Lebesgue measure and are not generated in our random process. A caveat is that, when an instance is close to an infeasible instance, our approach tends to find the mechanism that requires a large amount of payment to or from IP. The amount of payment occasionally exceeds the cost of each player by more than 100 times, which is unlikely to be acceptable in practice even if the expected utility is non-negative. See the expected payment of each player to/from IP in Figure 3.

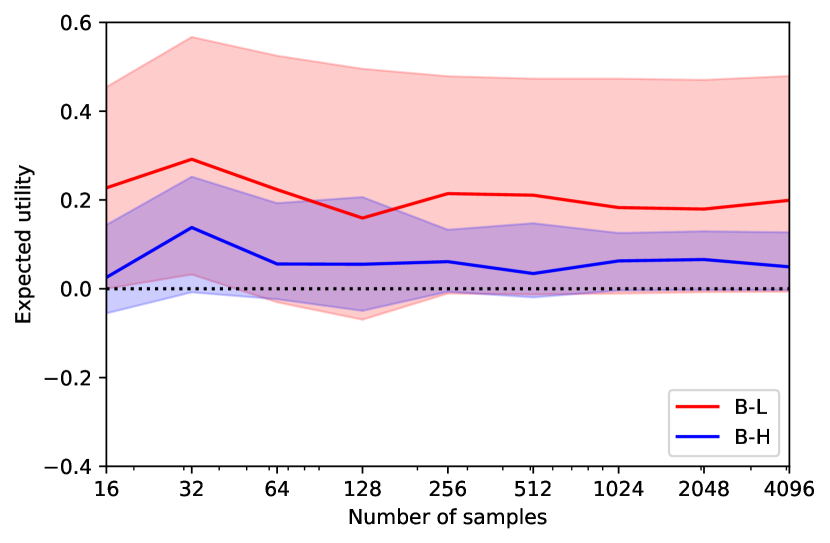

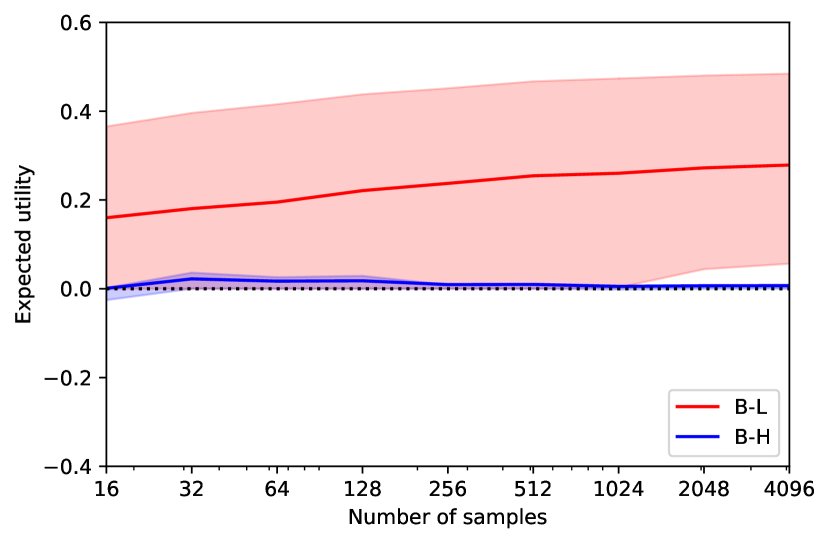

7.2 Validating Learning Approach

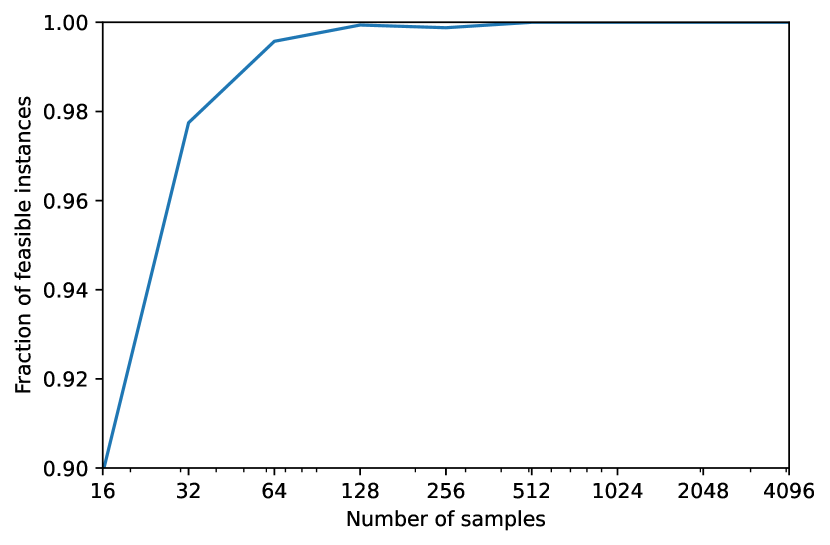

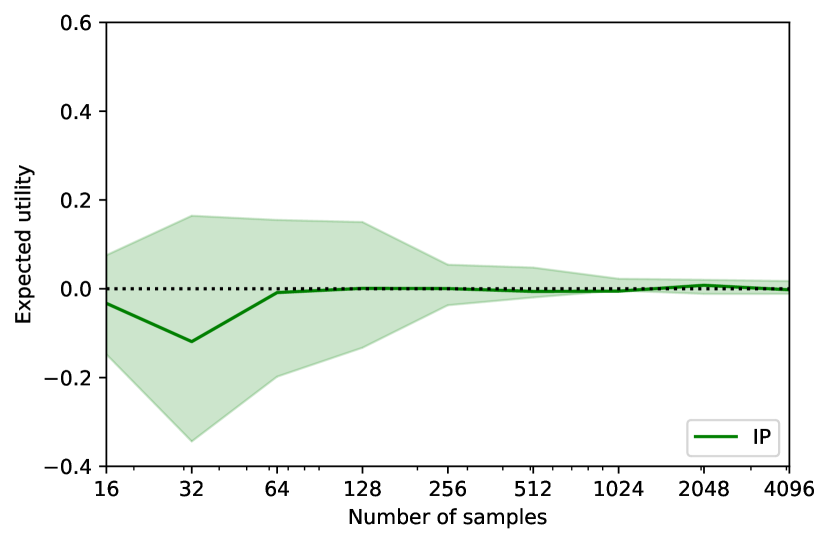

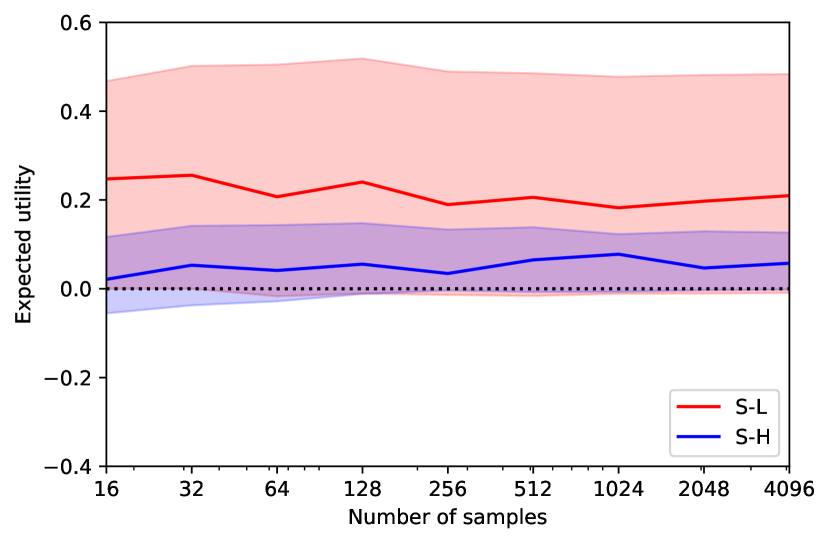

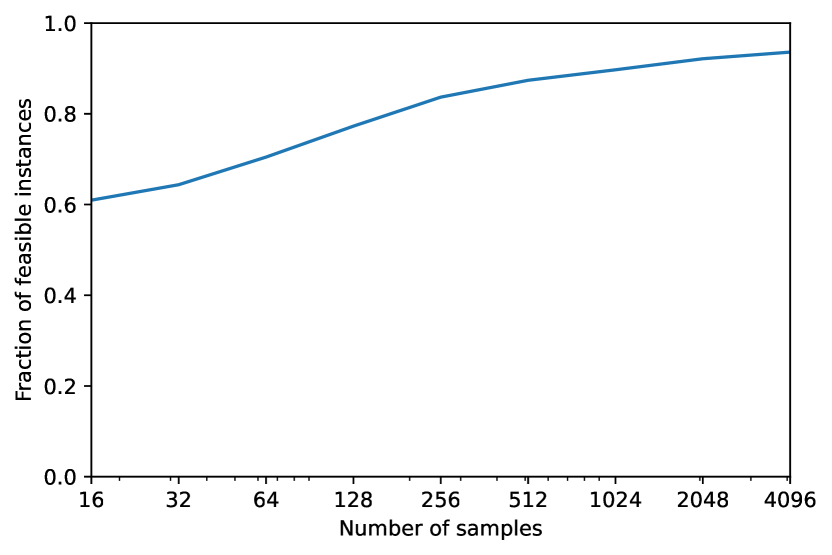

Next, we validate the effectiveness of our learning approach with a focus on the impact of sample approximation. Here, for each of the 1,642 instances, we take varying number of samples from the prior distribution of types to solve the learning problem (49)-(51). Here, we use the lower confidence bound of a Gaussian process regressor to evaluate the right-hand side of (51) and added the sample standard deviation to the right-hand side of (50) to form an upper confidence bound. We do not rely on functional approximation and seek to find an exact .

(a) Feasibility

(b) Budget balance

(c) Supplier utility

(d) Buyer utility

Figure 4 shows (a) the fraction of the instances for which the learning problem has feasible solutions as well as the expected utility of (b) IP, (c) the supplier, and (d) the buyer under the mechanisms learned with our approach. In (b)-(d), the solid lines show the average over the feasible instances, and the shared area represents the [15.9%, 84.1%]-quantile, which coincide with the confidence intervals set in (50)-(51).

We find that the learning problems do not necessarily have feasible solutions (while the corresponding optimization problems are all feasible), but with sufficient amount of data ( in this case), all of the learning problems become feasible. For those feasible learning problems, the proposed approach learns the mechanisms where the supplier and the buyer has strictly positive expected utility (achieving interim IR), and the IP has approximately zero expected utility (achieving ex ante WBB). Also, ex ante WBB and interim IR are achieved with high probability, but they are sometimes violated unlike the mechanisms computed with the exact knowledge of the prior distribution. As the sample size increases, however, ex ante WBB and interim IR get more frequently satisfied with the mechanisms found with learning.

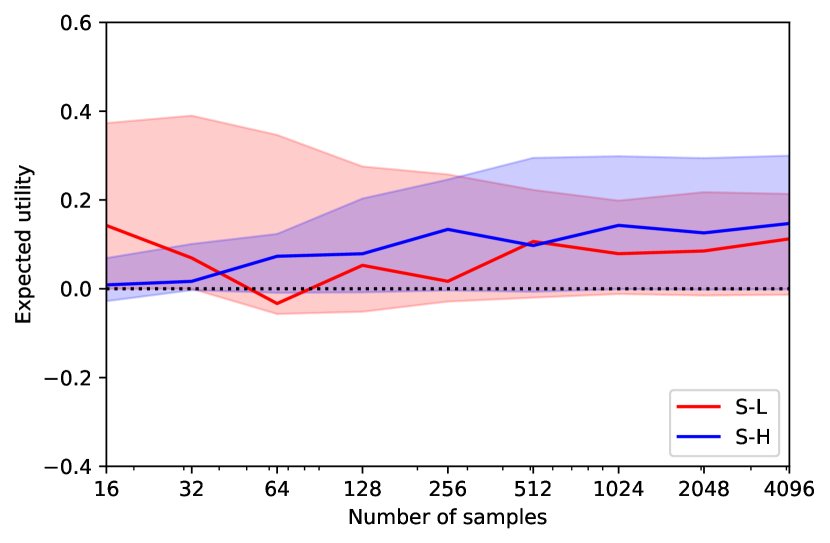

7.3 Validating Variable Reduction

Finally, we study the effectiveness of variable reduction by applying it to the settings of the previous experiments. Recall that the number of variables can be reduced from to . While this may not appear to reduce the number of variables when and , it reduces the essential number of variables even in this case. Specifically, for the trading network in Example 2, we have

| (60) |

so that both and are functions .

Figure 5 shows the performance of the mechanisms computed by the proposed approach with the technique of variable reduction. Compared to the corresponding results in Figure 2 and Figure 3 without variable reduction, we find different mechanisms depending on whether the variables are reduced or not, as is suggested by the different expected utilities of the players. However, the mechanisms computed with reduced variables still achieve ex ante WBB and interim IR for all of the randomly generated instances.

(a) Budget balance

(b) Utility

(c) Payment to/from IP

Figure 6 shows the performance of the mechanisms learned with variance reduction. Similar to the corresponding results without variable reduction (Figure 4), ex ante WBB and interim IR are achieved with high probability when the learning problems are feasible. Variable reduction, however, reduces the solution space, and the instances that are feasible without variable reduction can become infeasible. Nevertheless, the fraction of feasible instances increases with the sample size (and all of the instances become feasible with the exact prior distribution, as we have shown with the computational approach).

(a) Feasibility

(b) Budget balance

(c) Supplier utility

(d) Buyer utility

8 Conclusion

We have shown that, by computing or learning appropriate mechanisms, it can be made possible to achieve DSIC, Efficiency, ex ante WBB, and interim IR in trading networks where achieving these four properties ex post is impossible. Our AMD approach is greatly simplified with Theorem 1, which allows us to ignore the payment between players, and the Groves mechanisms, which allows us to focus on achieving WBB and IR.

This paper proposes the first AMD approach for trading networks and suggests interesting directions of future work. For example, while we learn mechanisms from previously collected (offline) data, the prior work has also investigated the approaches of learning mechanisms while collecting data in an online manner (Mohri and Medina, 2014; Chapman, Rogers, and Jennings, 2008; Balaguer et al., 2022b; Liu, Chen, and Qin, 2015) or by reinforcement learning (Tang, 2017; Rheingans-Yoo, 2020; Balaguer et al., 2022a; Zheng et al., 2021; Baumann, Graepel, and Shawe-Taylor, 2018; Koster et al., 2022; Brero et al., 2021b, a). Such online methods involves the additional challenge of the tradeoff between exploration and exploitation, and it is an interesting direction of future work to study such online methods for trading networks. (Morgenstern and Roughgarden, 2016; Cai and Daskalakis, 2017; Gonczarowski and Weinberg, 2018; Balcan et al., 2005) study sample complexity of learning mechanisms in combinatorial auctions, but such sample complexity for trading networks is unknown to date.

References

- Alon et al. (2021) Alon, T.; Lavi, R.; Shamash, E. S.; and Talgam-Cohen, I. 2021. Incomplete Information VCG Contracts for Common Agency. arXiv preprint arXiv:2105.14998.

- Balaguer et al. (2022a) Balaguer, J.; Koster, R.; Summerfield, C.; and Tacchetti, A. 2022a. The Good Shepherd: An Oracle Agent for Mechanism Design. In ICLR 2022 Workshop on Gamification and Multiagent Solutions.

- Balaguer et al. (2022b) Balaguer, J.; Koster, R.; Weinstein, A.; Campbell-Gillingham, L.; Summerfield, C.; Botvinick, M.; and Tacchetti, A. 2022b. HCMD-zero: Learning Value Aligned Mechanisms from Data. In ICLR 2022 Workshop on Gamification and Multiagent Solutions.

- Balcan et al. (2005) Balcan, M.-F.; Blum, A.; Hartline, J.; and Mansour, Y. 2005. Mechanism Design via Machine Learning. In Proceedings of the 46th Annual IEEE Symposium on Foundations of Computer Science (FOCS’05), 605–614.

- Baumann, Graepel, and Shawe-Taylor (2018) Baumann, T.; Graepel, T.; and Shawe-Taylor, J. 2018. Adaptive Mechanism Design: Learning to Promote Cooperation. CoRR, abs/1806.04067.

- Brero et al. (2021a) Brero, G.; Chakrabarti, D.; Eden, A.; Gerstgrasser, M.; Li, V.; and Parkes, D. C. 2021a. Learning Stackelberg Equilibria in Sequential Price Mechanisms. In Workshop for Reinforcement Learning Theory at ICML 2021.

- Brero et al. (2021b) Brero, G.; Eden, A.; Gerstgrasser, M.; Parkes, D.; and Rheingans-Yoo, D. 2021b. Reinforcement Learning of Sequential Price Mechanisms. In Proceedings of the 35th AAAI Conference on Artificial Intelligence, volume 35, 5219–5227.

- Cai and Daskalakis (2017) Cai, Y.; and Daskalakis, C. 2017. Learning Multi-Item Auctions with (or without) Samples. In Proceedings of the 58th Annual Symposium on Foundations of Computer Science (FOCS), 516–527.

- Candogan, Epitropou, and Vohra (2021) Candogan, O.; Epitropou, M.; and Vohra, R. V. 2021. Competitive Equilibrium and Trading Networks: A Network Flow Approach. Operations Research, 69(1): 114–147.

- Chapman, Rogers, and Jennings (2008) Chapman, A. C.; Rogers, A.; and Jennings, N. R. 2008. Learn While You Earn: Two Approaches to Learning Auction Parameters in Take-it-or-leave-it Auctions. In Proceedings of the 7th International Joint Conference on Autonomous Agents and Multiagent Aystems, volume 3, 1561–1564.

- Conitzer and Sandholm (2002) Conitzer, V.; and Sandholm, T. 2002. Complexity of Mechanism Design. In Proceedings of the 18th Conference on Uncertainty in Artificial Intelligence, 103–110.

- Duetting et al. (2019) Duetting, P.; Feng, Z.; Narasimhan, H.; Parkes, D.; and Ravindranath, S. S. 2019. Optimal Auctions through Deep Learning. In Chaudhuri, K.; and Salakhutdinov, R., eds., Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, 1706–1715. PMLR.

- Faccio, Kirsch, and Schmidhuber (2021) Faccio, F.; Kirsch, L.; and Schmidhuber, J. 2021. Parameter-Based Value Functions. In International Conference on Learning Representations.

- Gonczarowski and Weinberg (2018) Gonczarowski, Y. A.; and Weinberg, S. M. 2018. The Sample Complexity of Up-to-epsilon Multi-Dimensional Revenue Maximization. In Proceedings of the 59th Annual Symposium on Foundations of Computer Science (FOCS), 416–426.

- Harb et al. (2020) Harb, J.; Schaul, T.; Precup, D.; and Bacon, P. 2020. Policy Evaluation Networks. CoRR, abs/2002.11833.

- Hatfield and Kominers (2012) Hatfield, J. W.; and Kominers, S. D. 2012. Matching in Networks with Bilateral Contracts. American Economic Journal: Microeconomics, 4(1): 176–208.

- Hatfield et al. (2013) Hatfield, J. W.; Kominers, S. D.; Nichifor, A.; Ostrovsky, M.; and Westkamp, A. 2013. Stability and Competitive Equilibrium in Trading Networks. Journal of Political Economy, 121(5): 966–1005.

- Hatfield et al. (2015) Hatfield, J. W.; Kominers, S. D.; Nichifor, A.; Ostrovsky, M.; and Westkamp, A. 2015. Full Substitutability in Trading Networks. In Proceedings of the 16th ACM Conference on Economics and Computation, 39–40.

- Hatfield et al. (2019) Hatfield, J. W.; Kominers, S. D.; Nichifor, A.; Ostrovsky, M.; and Westkamp, A. 2019. Full Substitutability. Theoretical Economics, 14(4): 1535–1590.

- Iwata, Moriguchi, and Murota (2005) Iwata, S.; Moriguchi, S.; and Murota, K. 2005. A Capacity Scaling Algorithm for M-Convex Submodular Flow. Mathematical Programming, 103(1): 181–202.

- Koster et al. (2022) Koster, R.; Jan, B.; Tacchetti, A.; Weinstein, A.; Zhu, T.; Hauser, O.; Williams, D.; Campbell-Gillingham, L.; Thacker, P.; Botvinick, M.; and Summerfield, C. 2022. Human-centred Mechanism Design with Democratic AI. Nature Human Behaviour.

- Likhodedov and Sandholm (2004) Likhodedov, A.; and Sandholm, T. 2004. Methods for Boosting Revenue in Combinatorial Auctions. In Proceedings of the 19th National Conference on Artifical Intelligence, AAAI’04, 232–237. AAAI Press. ISBN 0262511835.

- Likhodedov and Sandholm (2005) Likhodedov, A.; and Sandholm, T. 2005. Approximating Revenue-Maximizing Combinatorial Auctions. In Proceedings of the 20th National Conference on Artifical Intelligence, 267–274.

- Liu, Chen, and Qin (2015) Liu, T.-Y.; Chen, W.; and Qin, T. 2015. Mechanism Learning with Mechanism Induced Data. In Proceedings of the 29th AAAI Conference on Artificial Intelligence, volume 29.

- Manisha, Jawahar, and Gujar (2018) Manisha, P.; Jawahar, C. V.; and Gujar, S. 2018. Learning Optimal Redistribution Mechanisms Through Neural Networks. In Proceedings of the 17th International Conference on Autonomous Agents and MultiAgent Systems, 345–353.

- Mohri and Medina (2014) Mohri, M.; and Medina, A. M. 2014. Learning Theory and Algorithms for Revenue Optimization in Second Price Auctions with Reserve. In Xing, E. P.; and Jebara, T., eds., Proceedings of the 31st International Conference on Machine Learning, volume 32 of Proceedings of Machine Learning Research, 262–270. Bejing, China: PMLR.

- Morgenstern and Roughgarden (2016) Morgenstern, J.; and Roughgarden, T. 2016. Learning Simple Auctions. In Feldman, V.; Rakhlin, A.; and Shamir, O., eds., 29th Annual Conference on Learning Theory, volume 49 of Proceedings of Machine Learning Research, 1298–1318. Columbia University, New York, New York, USA: PMLR.

- Myerson and Satterthwaite (1983) Myerson, R. B.; and Satterthwaite, M. A. 1983. Efficient Mechanisms for Bilateral Trading. Journal of Economic Theory, 29(2): 265–281.

- Nisan (2007) Nisan, N. 2007. Introduction to Mechanism Design (for Computer Scientists). In Algorithmic Game Theory, chapter 9, 209–241. Cambridge University Press.

- Ostrovsky (2008) Ostrovsky, M. 2008. Stability in Supply Chain Networks. American Economic Review, 98(3): 897–923.

- Othman and Sandholm (2009) Othman, A.; and Sandholm, T. 2009. How Pervasive is the Myerson-Satterthwaite Impossibility? In Proceedings of the 21st International Joint Conference on Artificial Intelligence, IJCAI’09, 233–238. San Francisco, CA, USA: Morgan Kaufmann Publishers Inc.

- Parkes (2001) Parkes, D. C. 2001. Iterative Combinatorial Auctions: Achieving Economic and Computational Efficiency. Ph.D. thesis, University of Pennsylvania.

- Rahme, Jelassi, and Weinberg (2021) Rahme, J.; Jelassi, S.; and Weinberg, S. M. 2021. Auction Learning as a Two-Player Game. In International Conference on Learning Representations.

- Rheingans-Yoo (2020) Rheingans-Yoo, D. 2020. Reinforcement Learning for Indirect Mechanism Design. Bachelor’s Thesis, Harvard College.

- Sandholm (2003) Sandholm, T. 2003. Automated Mechanism Design: A New Application Area for Search Algorithms. In Rossi, F., ed., Principles and Practice of Constraint Programming – CP 2003, 19–36. Berlin, Heidelberg: Springer Berlin Heidelberg. ISBN 978-3-540-45193-8.

- Schlegel (2022) Schlegel, J. C. 2022. The Structure of Equilibria in Trading Networks with Frictions. Theoretical Economics, 17(2): 801–839.

- Tacchetti et al. (2022) Tacchetti, A.; Strouse, D.; Garnelo, M.; Graepel, T.; and Bachrach, Y. 2022. Learning Truthful, Efficient, and Welfare Maximizing Auction Rules. In ICLR 2022 Workshop on Gamification and Multiagent Solutions.

- Tang (2017) Tang, P. 2017. Reinforcement Mechanism Design. In Proceedings of the 26th International Joint Conference on Artificial Intelligence (IJCAI-17), 5146–5150.

- Zheng et al. (2021) Zheng, S.; Trott, A.; Srinivasa, S.; Parkes, D. C.; and Socher, R. 2021. The AI Economist: Optimal Economic Policy Design via Two-level Deep Reinforcement Learning. CoRR, abs/2108.02755.

Appendix A When the payment rule is given by other means

Our approach may also be applied when is determined by other means. Namely, for any payment rule for , we may design a mechanism with no payment between players, and convert to via (15) to obtain the mechanism . See Algorithm 1.

Input: A trading network and a payment rule ; Desirable properties

Output: A mechanism that achieves the desirable properties

In particular, for an arbitrary payment rule , one may first find a Groves mechanism and transform it into a mechanism by following the procedure in Algorithm 1. Even though may not be a Groves mechanism in the sense of (32)-(33), DSIC and Efficiency of are guaranteed by the corresponding properties of according to Theorem 1.