Doubly Robust Estimation under Covariate-Induced Dependent Left Truncation

Abstract

In prevalent cohort studies with follow-up, the time-to-event outcome is subject to left truncation leading to selection bias. For estimation of the distribution of time-to-event, conventional methods adjusting for left truncation tend to rely on the (quasi-)independence assumption that the truncation time and the event time are “independent” on the observed region. This assumption is violated when there is dependence between the truncation time and the event time possibly induced by measured covariates. Inverse probability of truncation weighting leveraging covariate information can be used in this case, but it is sensitive to misspecification of the truncation model. In this work, we apply the semiparametric theory to find the efficient influence curve of an expected (arbitrarily transformed) survival time in the presence of covariate-induced dependent left truncation. We then use it to construct estimators that are shown to enjoy double-robustness properties. Our work represents the first attempt to construct doubly robust estimators in the presence of left truncation, which does not fall under the established framework of coarsened data where doubly robust approaches are developed. We provide technical conditions for the asymptotic properties that appear to not have been carefully examined in the literature for time-to-event data, and study the estimators via extensive simulation. We apply the estimators to two data sets from practice, with different right-censoring patterns.

Keywords: Conditional quasi-independence; Efficient influence curve; Machine learning; Rate doubly robust; Selection bias; Semiparametric theory.

1 Introduction

A time-to-event outcome in a prevalent cohort study is subject to left truncation because, starting from a well-defined time zero, such as the onset of a disease, often only subjects with time to events such as death greater than the enrollment times are included in the data set. Subjects with early or short event times therefore tend not to be captured in the data. For example, in prospective cohort pregnancy studies, women typically enroll after clinical recognition of their pregnancies, so women with early pregnancy losses tend not to be included in the data (Xu and Chambers, 2011; Ying et al., 2020). As another example, in aging studies, age is the time scale of interest, so the time origin is birth. However, in many such studies participants are recruited into the study at different ages, and participants with early event times tend not to be captured due to the study design.

In the presence of left truncation, subjects with longer event times are preferentially selected. In the estimation of the marginal distribution of the time to event, which is the focus of this paper, conventional methods typically rely on the random truncation assumption that the left truncation time and event time are independent in the full data, i.e. without truncation (Woodroofe, 1985; Wang et al., 1986; Wang, 1989, 1991; Gross, 1996; Gross and Lai, 1996; Shen, 2010). This can also be weakened to a quasi-independence assumption (Tsai, 1990). Such independence or quasi-independence assumptions may be violated in practice. For instance, in the retirement center example of Klein and Moeschberger (2003), the life lengths of the individuals in the retirement center are left truncated because individuals must survive long enough to enter the retirement center. However, individuals’ life lengths and entry times may be dependent because individuals who entered the retirement home earlier may have received better medical attention and therefore lived longer (Chaieb et al., 2006).

For dependent left truncation, copula models (Chaieb et al., 2006; Emura et al., 2011; Emura and Wang, 2012) and structural transformation models (Efron and Petrosian, 1994; Chiou et al., 2019) have been proposed to handle the dependence between the left truncation time and the event time under different assumptions. Copula models rely on strong modeling assumptions for the dependency, whilst structural transformation models specify a latent quasi-independent truncation time as a function of the observed dependent truncation time and the event time. There are also methods that incorporate the left truncation time as a covariate in the event time model (Mackenzie, 2012; Cheng and Wang, 2015) which, as pointed out in Vakulenko-Lagun et al. (2022), is biologically unjustified if the left truncation time is study-specific and not related to the event process. None of the above methods leverage covariate information if available; a more detailed discussion of the above approaches can be found in Vakulenko-Lagun et al. (2022).

When the dependence between the left truncation and the event times is captured by measured covariates in a regression setting, Cox (1972) model for example, can properly handle the left truncation via risk set adjustment (Andersen et al., 1993). For marginal survival probabilities, Vakulenko-Lagun et al. (2022) recently proposed two inverse probability weighted (IPW) estimators that account for the dependence induced by the covariates. IPW approaches (Rosenbaum and Rubin, 1983) are known to be not only sensitive to model specification but also inefficient. This motivated us to seek estimators that provide extra protection against model misspecification and are more efficient. To that end, we leverage semiparametric theory to find the efficient influence curve (EIC), which often suggests reasonable estimators in both the missing data and the causal inference literature (Tsiatis, 2006; Hernán and Robins, 2020). In our case, we show that the EIC leads to estimators that enjoy model double robustness and rate double robustness (Rotnitzky et al., 2021; Hou et al., 2021). The model doubly robust estimator is consistent and asymptotically normal (CAN) when one of the two parametric/semiparametric nuisance models is correctly specified, but not necessarily both. In addition, when both models are correctly specified, the estimator achieves the semiparametric efficiency bound. The rate doubly robust estimator is constructed from a cross-fitting procedure. It is CAN and achieves the semiparametric efficiency bound when both nuisance parameters are consistently estimated and the product error rate of the two nuisance estimators is faster than root-. This allows us to use flexible nonparametric or machine learning methods to estimate the nuisance parameters.

We remark that there has been a growing literature on doubly robust estimators to handle missing or coarsened data including right censoring for time-to-event data, as well as non-randomized treatment assignment in causal inference (Robins et al., 1995; Bang and Robins, 2005; Tsiatis, 2006; Tchetgen Tchetgen et al., 2010; Robins and Rotnitzky, 2005; Robins, 1997a, b, 1999; van der Laan and Robins, 2003, for examples). However, left truncation does not belong to the coarsened data framework. This is because for coarsened data, subjects in the observed data set are a random sample from the population of interest, while the data for each subject may be coarsened. For truncation problems, on the other hand, subjects in the observed data set are biasedly sampled. Therefore, the existing techniques for coarsened data (Heitjan and Rubin, 1991; Tsiatis, 2006) do not apply. To the best of our knowledge, our paper represents the first attempt to apply semiparametric theory in order to explore doubly robust estimation in the presence of left truncation, a common type of selection bias for time-to-event data.

The rest of the paper is organized as follows. We introduce notation in the next section and review preliminaries on left truncation that are not widely known. In Section 3, we show that the estimand can be identified from inverse probability of truncation weighting, derive the EIC and construct an estimating function that is doubly robust in the sense that it has expectation zero when either the time-to-event model or the truncation model is true. In Section 4 we construct a model doubly robust estimator and a rate doubly robust estimator, and carefully establish their asymptotic properties. We extend the estimators to two different right-censoring scenarios in Section 5. Extensive simulations are conducted in Section 6, and Section 7 contains applications to two data sets under the different right-censoring scenarios. Section 8 concludes with discussion.

2 Notation and Preliminaries

Let , , be random variables denoting the left truncation time, the event time of interest, and baseline covariates, respectively. Suppose that and both have absolutely continuous distributions. Let , and be the conditional cumulative distribution function (CDF) of given , given , and the CDF of in the full data, respectively; here by full data we mean if there were no left truncation. Let , , and be the corresponding full data densities or probability functions in the case of discrete .

Denote . In the presence of left truncation, we observe only if . The observed data distribution of is the conditional full data distribution of given . In this paper, we will denote as the probability operator of the full data, as the expectation with respect to the full data distribution, ‘pr’ as the probability operator of the observed data, i.e. , and as the expectation with respect to the observed data distribution. In addition, we will use and to denote the CDF and the density or probability function for the observed data; for example, , , and , etc.

In the following we characterize the distribution of including its associated martingale, which will be useful later. In particular, due to the asymmetry between and , it is often useful to consider the “reverse time” for the distribution of . In fact, without covariates the product-limit estimate of can be derived by moving backwards in time (Wang, 1991; Gross, 1996). Bickel et al. (1993) considered the “reverse time” counting processes, and here we extend them to the setting with covariates. For , let

| (1) |

with their natural history filtration on the reversed time scale:

| (2) |

Note that is a decreasing process (as increases) that starts at one and jumps to zero immediately after if , and is always zero if . Also decreases as increases.

Let be the reverse time hazard function of given for the full data; specifically,

| (3) |

It follows immediately that . In this way either or alone characterizes the full data distribution of given .

Define the compensator for , where

| (4) |

In the Supplementary Material we showed that

| (5) |

is a backwards martingale with respect to under the observed data law, if is the true CDF of given in the full data. A stochastic process is called a backwards martingale with respect to a set of decreasing -algebras if , is -measurable for all , and for all . If we reverse the time scale and define

| (6) | ||||

| (7) |

for some , then is a martingale with respect to the filtration .

In this paper we focus on estimating the expectation of a transformed event time in the full data:

| (8) |

where is a real-valued bounded function. Expression (8) includes commonly considered estimands for time-to-event data. For example, when for some fixed , is the survival probability; when , is the restricted mean survival time (RMST).

3 Identification, influence curve and Double Robustness

3.1 Identification via inverse probability weighting

We make the following conditional quasi-independence assumption.

Assumption 1 (Conditional quasi-independence).

The observed data density for satisfies

| (11) |

where .

Assumption 1 is a generalization of the quasi-independence assumption in Tsai (1990) to settings where the event time and the left truncation time are dependent via covariates. It is weaker than the conditional independence assumption that is independent of given in the full data, which was assumed in Vakulenko-Lagun et al. (2022), because Assumption 1 only constraints the distribution of on the observed region . In addition, it does not imply that is independent of given in observed data since , as shown in the Supplementary Material.

We also need the following positivity assumption, which ensures that there are enough observed data to identify the parameter of interest.

Assumption 2 (Positivity).

almost surely.

Under Assumptions 1 and 2, the estimand can be identified from the observed data distribution. This is shown by an inverse probability weighting type of argument below, where the inverse probability weights are constructed using the truncation distribution.

Lemma 1 (Identification).

Expression (12) suggests an inverse probability of truncation weighted estimator for from an observed sample :

| (13) |

where is an estimator of that will be discussed in more details later. When for a given , this estimator coincides with the ‘CW’ estimator proposed in Vakulenko-Lagun et al. (2022), when is estimated from a Cox proportional hazards model.

As mentioned in the Introduction, the IPW estimator (13) relies on the correct specification of the truncation model and is known to be inefficient. Augmented inverse probability weighted (AIPW) estimators are often developed in the literature to improve upon the IPW estimators; they have been shown to provide extra robustness and to be more efficient (Robins, 1997b; van der Laan and Robins, 2003; Tsiatis, 2006). In order to develop the improved estimators, we leverage the semiparametric theory below.

3.2 Efficient influence curve

Semiparametric theory has been developed and reviewed in the literature (Begun et al., 1983; Bickel et al., 1993; Tsiatis, 2006; Van der Vaart, 2000; Newey, 1994; Kosorok, 2008). In the following, we apply the semiparametric theory to first compute the efficient influence curve of , which in turn suggests estimators that have favorable properties such as double robustness.

Consider the Hilbert space of all one-dimensional mean-zero measurable functions of with finite second moments, equipped with the covariance inner product under the observed data distribution . We proceed as follows: we will first characterize the tangent space in ; we then introduce and find an influence curve ; the projection of the influence curve onto the tangent space gives the efficient influence curve (Tsiatis, 2006; Bickel et al., 1993).

Consider a regular (Bickel et al., 1993) parametric submodel indexed by a real-valued parameter for the observed data distribution of that satisfies Assumptions 1 and 2, and equals the true distribution of the observed data at . Its score function is

| (14) |

in the notation above as well as in the rest of the paper we suppress the dependence of on the parametric submodel. The closure of the linear span of the score functions of all such regular parametric submodels is the tangent space, denoted by .

Denote the space of all measurable functions of with mean zero and finite second moment under the law , and the space of all measurable functions of with mean zero and finite second moment under the law . The following Lemma is proved in the Supplementary Material.

Lemma 2 (Tangent space).

We now introduce the influence curve. The parameter of interest, , is pathwise differentiable with influence curve if, for any regular parametric submodel ,

| (19) |

Remark 1.

In the literature, there are two practically exchangeable terms: influence function (IF) and influence curve (IC). Here we follow the convention as reviewed in Kennedy (2017), to use IF for estimators, and use IC for parameters. Note that if is the IF for an arbitrary regular asymptotically linear (RAL) estimator (Tsiatis, 2006) of , then the IF for any RAL estimator of must lie in the space (Tsiatis, 2006; Bickel et al., 1993). RAL estimators and their IF’s will be used later in the paper. The IF of a RAL estimator suggests the asymptotic variance of the estimator.

For the remainder of this paper, we consider the semiparametric model under Assumptions 1 and 2, and assume that the true distribution also satisfies the following overlap assumption, which is stronger than Assumption 2. We borrow the word ‘overlap’ from the causal inference literature, which is also sometimes referred to as a strict positivity assumption.

Assumption 3 (Overlap).

There exist and constants such that a.s. and a.s. in the full data; a.s., and a.s..

Assumption 3 makes sure that the minimum support of is greater than the minimum support of , and that the maximum support of is greater than the maximum support of . This assumption is commonly made for left truncated data, see for example Cheng and Wang (2012). The existance of and is in line with most survival analysis approaches where a maximum follow-up time is assumed, so that the parameter space for a cumulative baseline hazard, for example, is bounded. It is also common for left truncated data, that any reasonable estimand, is conditional upon survival until a minimum truncation time when the data become available (Tsai et al., 1987).

Assumption 3 is simpler but stronger than Assumption 3’ below, which is in fact what is necessary. For the ease of exposition, we will continue with the Assumption 3. For data examples, however, we will verify Assumption 3’ which is more likely to be satisfied in practice. Denote the support of in the full data.

Assumption 3’ (overlap).

There exist constants and for each such that conditional on , a.s. and a.s. in the full data; and with probability one, or , and or .

Lemma 3.

It turns out that given in (20) lies in , and is therefore the efficient influence curve (EIF). We summarize this result formally below.

Proposition 1 (Efficient influence curve).

Remark 2.

Chao (1987) derived the influence function for the product-limit (PL) estimator of the survival function of under random left truncation, in the absence of covariates. Since the PL estimator is the nonparametric maximum likelihood estimator (NPMLE), which is known to be asymptotically efficient, the IF derived in Chao (1987) is the EIF. In the Supplementary Material we showed that when there are no covariates and , the EIC derived in this paper matches the (E)IF derived in Chao (1987).

3.3 Doubly robust estimating function

Leaving out the constant factor in (20), we have the following estimating function, assuming that and are known for the moment:

| (21) |

where is the backwards martingale related to that is defined in the preliminaries. The above can be viewed as the inverse probability of truncation weighted full data estimating function , plus an augmentation term. We note that the augmentation term can also be written as

| (22) |

The above resembles other augmented IPW (AIPW) estimating functions. For example, for the augmented inverse probability censoring weighted (AIPCW) estimating functions (Tsiatis, 2006), the augmentation term involves a weighted censoring time martingale integral, with the integrand of a full data conditional expectation. In comparison, (22) is a weighted truncation time (backwards) martingale integral, with the integrand also a full data conditional expectation, but with the additional multiplicative factor of the odds .

Denote the true values of , respectively. The following theorem shows that is a doubly robust estimating function.

Theorem 1 (Population Double robustness).

Theorem 1 helps us to construct doubly robust estimators next.

4 Estimation

4.1 Estimating equation

Let be a random sample of size from the observed data distribution, where . From (21) a natural estimating equation for would be , if and were known. In practice we would first estimate and , then solve for using

| (23) |

In particular, can be estimated from using existing regression methods that handle left truncation; and can be estimated similarly from on the reversed time scale, where is left truncated by , and is an upper bound of time. Since is linear in , we have a closed-form solution for (23):

| (24) |

We have immediately the following special cases in which we use degenerative constant (and likely wrong) estimates for or . The double robustness properties in the next subsection guarantees that they are CAN if conditions are met. More specifically, by setting , we obtain the IPW estimator in (13). On the other hand, by setting , we obtain a regression-based estimator:

| (25) |

The reason we call it regression-based is shown in the Appendix: estimates , while the inverse probability weight corrects for the selection bias caused by left truncation (Cheng and Wang, 2012; Ertefaie et al., 2014). Motivated by , we also consider another regression-based estimator:

| (26) |

where estimates .

For the rest of this section, we construct estimators with doubly robust properties from (23) under two scenarios. In Section 4.2, we consider the more classical case where both and are asymptotically linear. In Section 4.3, we consider nonparametric or machine learning methods and estimate using a cross-fitting procedure.

4.2 Model double robustness under asymptotic linearity

When parametric or semiparametric models like the Cox proportional hazards model are used to estimate and , the estimators and are root- consistent and asymptotically linear. In this case, the observed data are used to obtain and , and the same data are then used to solve equation (23). We denote the resulting estimator . We show that is model doubly robust, in that it is consistent and asymptotically normal when one of the models for and is correctly specified, but not necessarily both.

Let us first introduce some norms. For a random function with and , define and , where is the total variation of on the interval , and is the set of all possible partitions of . We assume the following.

Assumption 4 (Uniform Convergence).

There exist CDF’s and such that

| (27) |

Assumption 5 (Asymptotic Linearity).

For fixed , and are regular and asymptotically linear estimators for and with influence functions and , respectively. In addition, denote

| (28) | ||||

| (29) |

Suppose , , and either or .

In general, the rate conditions in terms of does not imply those under , and vice versa. As an example, if is the nonparametric maximum likelihood estimator (NPMLE) under the proportional hazards model, is usually of order , but even rate is not achievable for . In fact, we can show that for the simple case of estimating a smooth CDF by its empirical CDF, the of its error is . On the other hand, the rate conditions on the remainder terms in Assumption 5 are reasonable; in particular, we verify in the Supplementary Material that Assumption 5 is satisfied when the proportional hazards model is used to estimate and . The rate condition in terms of is needed to handle the involvement of time in both nuisance parameters and . To the best of our knowledge, the technical complication involved in the asymptotics of such doubly robust estimators have not been carefully studied in the previous literature. Using integration by parts, we can show that only one of the two conditions in Assumption 5 is needed.

In the following, we will use “” to indicate convergence in probability, and “” to indicate convergence in distribution. We have the following model double robustness property for .

Theorem 2 (Model double robustness).

Under Assumptions 1, 4, and regularity Assumption 8 in the Supplementary Material, assuming also that both (, ) and (, ) satisfy Assumption 3,

if either or , we have:

(i) ;

(ii) if in addition Assumptions 5 holds, then

.

Furthermore, when both and , achieves the semiparametric efficiency bound, and can be consistently estimated by , where

The proof of the theorem is given in the Supplementary Material, where the consistency proof utilizes concentration inequalities, and the asymptotic normality proof further utilizes asymptotic results of -Statistics.

Remark 3.

As mentioned earlier, since and are special cases of , they are CAN when and are uniformly consistent and asymptotically linear, respectively. In addition, when is uniformly consistent and asymptotically linear, and can be shown to be asymptotically equivalent under the slightly stronger assumption that is independent of given in the full data.

4.3 Rate double robustness with cross-fitting

In the contemporary data science era, analysts may wish to consider more flexible nonparametric or machine learning methods in order to estimate and . These estimators are known to converge slower than the root- rate, and are not asymptotically linear. To incorporate such methods, we utilize the cross-fitting procedure that are commonly considered in the literature (Hasminskii and Ibragimov, 1979; Bickel, 1982; Robins et al., 2008; Chernozhukov et al., 2018).

The cross-fitting procedure in Algorithm 1 introduces independence between the estimated nuisance parameters and the data used to estimate , thereby avoiding the asymptotic linearity assumption required in Section 4.2.

| (30) |

We again introduce some norms here, and show that enjoys a rate doubly robust property (Rotnitzky et al., 2021; Hou et al., 2021) as described below. Denote the data used to obtain and , Denote an copy of the data that is independent of, but from the same distribution, as . Let denote expectation taken with respect to conditional on the original data , and the expectation with respect to . Define

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) |

where and . We refer to as the out-of-sample cross integral product.

Assumption 6 (Uniform Consistency).

and .

Assumption 7 (Product rate condition).

.

In the above we assume that the model classes for estimating and are large enough so that and are uniformly consistent for the truth. The rate conditions in Assumptions 6 and 7 are extensions of common rate conditions assumed for the rate doubly robust estimators in the literature (Rotnitzky et al., 2021; Hou et al., 2021; Rava and Xu, 2023), again with particular attention to the handling of the fact that and are both functions of . Previous literature (Chernozhukov et al., 2018; Rotnitzky et al., 2021) typically imposes their product rate condition as a product of the error rates from estimating the two nuisance parameters, instead of an integral form as in Assumption 7 here. This is because at most one of their nuisance parameters involves time , which results in the ‘mixed bias property’ studied in Rotnitzky et al. (2021), and enables an easy application of the Cauchy-Schwartz inequality in the proofs. The time construct in both nuisance functions is inevitable in our study, and a more detailed discussion on this topic can be found in Ying (2023).

A technical note is that we have assumed conditions on the expectations of the estimation errors and the out-of-sample cross integral product. These are slightly stronger than the conditions where we would have only the inner expectation and assume that the rate is (Rotnitzky et al., 2021; Hou et al., 2021). But they are equivalent if we have regularity condition that the quantities are bounded almost surely. Our assumption here simplifies the proofs.

We have the following rate double robustness property for .

Theorem 3 (Rate double robustness).

The proof of the Theorem is given in the Supplementary Material.

Remark 4.

Neyman orthogonal scores (Neyman, 1959) have long been considered in the context of slower than root- estimation for nuisance parameters (Newey, 1994; Bickel et al., 1993). Under regularity conditions, it can be shown that all influence curves are Neyman orthogonal scores (Rava and Xu, 2023), so is the efficient influence curve and thus the estimating function in (21). In addition, it can be shown that all doubly robust estimating functions are Neyman orthogonal scores. With cross-fitting Neyman orthogonal scores can suggest root- consistent estimators when the nuisance parameters are estimated at faster than rate (Newey, 1994; Rotnitzky et al., 2021). However, as pointed out by Bilodeau (2022), Ogburn et al. (2022) and Tang (2022), the rate requirement can rule out a number of data adaptive machine learning methods. With the help of rate double robustness, alleviates the rate requirement; it allows one of and to converge arbitrarily slow, as long as the the product error rate is faster than root-. In practice few convergence rate results are known for nonparametric methods under left truncation, and in numerical studies later we will investigate empirically the performance of some of these methods.

5 Estimation under right censoring

5.1 Censoring before truncation

Now we extend the above estimators to handle right censoring in addition to left truncation. Denote the censoring time, and let be the possibly censored event time, and the event indicator. As discussed in Qian and Betensky (2014), there are two scenarios, depending on whether censoring can occur before truncation. In this subsection, we consider the first scenario where censoring can happen before left truncation, that is, . As an example, in the central nervous system (CNS) lymphoma data that will be analyzed in the applications later, the time to death is left truncated by the time to relapse, and censoring is due to loss to follow-up which can happen before a patient progresses to relapse.

In this first censoring scenario, subjects with are included in the data, and plays the role of in the case without the censoring. We observe for each subjects. Denote the conditional CDF of given in the full data, and . We assume that is independent of in the full data, and assume the positivity condition that a.s. for some .

Due to the above data generating mechanism, we construct an estimating function by first applying inverse probability of censoring weights to the full data estimating function , and then adjusting for left truncation. As such, an extended estimating function is

| (36) |

where , and . As we mentioned above, plays the role of in the case without right censoring, so it is not surprising that the nuisance parameters involved are and . Again we use subscript 0 to denote the true values of the parameters. We show in the Supplementary Material that is doubly robust in the sense that if or .

For estimation of we need to first estimate , and . In particular, can be estimated using , where is left truncated by . Since is left truncated by and right censored by , can be estimated from by the product-limit estimator (Wang, 1991; Qian and Betensky, 2014; Vakulenko-Lagun et al., 2022). And finally, similar to before, can be estimated from data on the reverse time scale. This way we can obtain a model doubly robust estimator and a rate doubly robust estimator, as well as extensions of the IPW and regression-based estimators, the expressions of which are all provided in the Supplementary Material. For the rate doubly robust estimator, is estimated using the same cross-fitting data as for estimating and .

Remark 5.

As discussed before the IPW estimator and the ‘CW’ estimator are the same when there is no censoring. In the Supplementary Material, the extended IPW estimator under censoring is however different from the extended ‘CW’ estimator in Vakulenko-Lagun et al. (2022) for this censoring scenario.

5.2 Censoring after truncation

The second censoring scenario is . This is the case for many studies where censoring is due to loss to follow-up after participants enter the study. The assumption implies that the left truncation time and the censoring are dependent (Vakulenko-Lagun et al., 2022), unless their supports do not overlap. Following the setup in Qian and Betensky (2014), we consider censoring on the residual time scale. In particular, denote the residual censoring time. Therefore, , , and . Denote . We assume that is independent of in the observed data, and the positivity condition that a.s. for some .

Under this scenario, subjects are included in the data set only if , and subsequently the subjects are possibly right censored. Therefore, we extend the estimating function (21) by first handling left truncation, then applying inverse probability of censoring weighting:

| (37) |

where is defined in the previous subsection. We show in the Supplementary Material that is doubly robust in the sense that if or .

As before, we estimate by first estimating , and . In particular, can be estimated using existing regression methods for left truncated and right censored data; can be estimated by the Kaplan-Meier estimator with the right censored data on the residual time scale, where is right censored by . For estimateion of after reversing the time scale, is only observed for uncensored subjects. We therefore apply inverse probability of censoring weighting following Vakulenko-Lagun et al. (2022), and restrict to the uncensored subjects and assign them case weights . This way we can obtain doubly robust estimators, as well as extensions of the IPW and regression-based estimators. The expressions of these estimators are provided in the Supplementary Material. For the rate doubly robust estimator, is estimated using the same cross-fitting data as for estimating and .

6 Simulation

In this section, we study the finite sample performance of the proposed estimators. We consider sample size for the observed data sets, and 500 data sets are simulated, which gives a margin of error of about for the coverage probability of nominal 95% confidence intervals. We focus on the setting without censoring here. Simulation results for the two censoring scenarios considered in Section 5 are shown in the Supplementary Material.

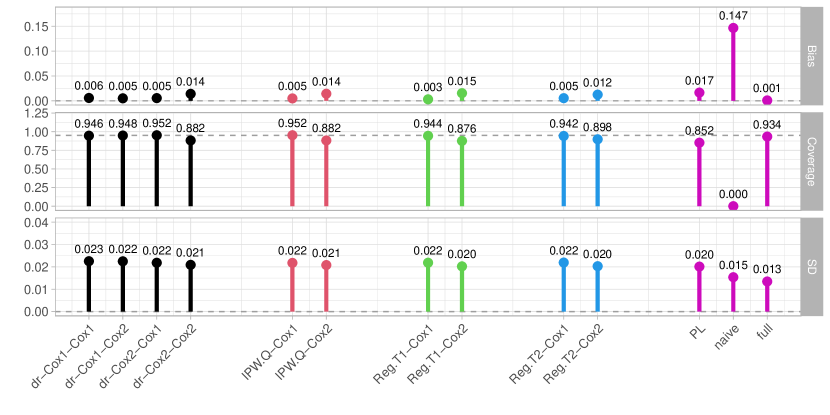

6.1 Under semiparametric models with asymptotic linearity

We study the finite sample performance of when semiparametric models are used to estimate and . In particular, we consider using the Cox (1972) proportional hazards model, under which Assumption 5 is satisfied as we mentioned in Section 4.2. We compare with the IPW estimator and the regression-based estimators. We also consider the naive estimator that is the simple average of the ’s from the observed data without accounting for left truncation, and the oracle full data estimator that is the average of the ’s from the full data.

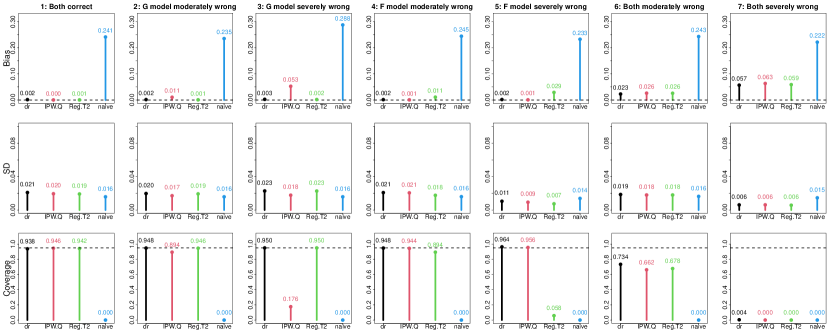

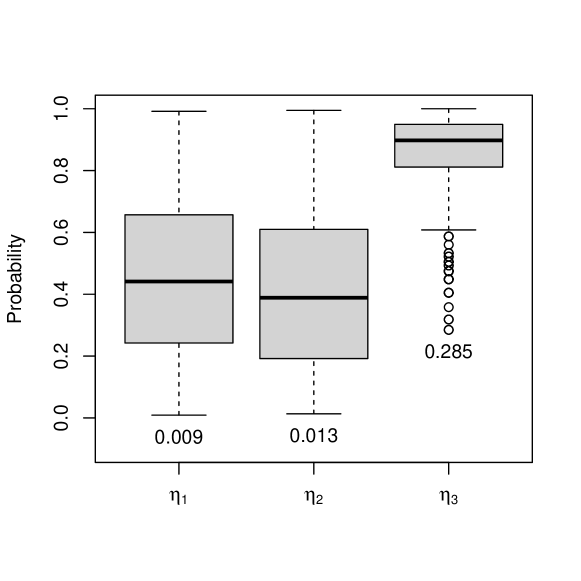

We generate the full data , where with and . Following that and are generated from seven different scenarios that are summarized in Table 1. The full details of the seven scenarios are described in the Supplementary Material. For the constants involved in the seven scenarios, we take , , and , resulting in about 55% truncation for Scenarios 1, 2, 4 and 6, 66% truncation for Scenario 3, 75% truncation for Scenario 5, and 85% truncation for Scenario 7, after excluding subjects with .

Our estimand is 0.2370 for Scenarios 1, 2 and 3, 0.2441 for Scenarios 4 and 6, and 0.0976 for Scenarios 5 and 7, each computed from a full data sample with sample size .

The nuisance parameters and are estimated using approaches described in Section 4. Specifically, we fit for , and fit for , both with risk set adjustment for left truncation. Obviously the proportional hazards model for is correctly specified for Scenarios 1, 2 and 3, moderately misspecified for Scenarios 4 and 6, and severely misspecified for Scenarios 5 and 7; the proportional hazards model for is correctly specified for Scenarios 1, 4 and 5, moderately misspecified for Scenarios 2 and 6, and severely misspecified for Scenarios 3 and 7.

We report the bias, %bias , empirical standard deviation (SD), average of the model-based standard errors (SE), average of the bootstrapped standard errors (boot SE), and the coverage probabilities (CP) of the nominal 95% confidence intervals constructed using the model-based SE and the boot SE, respectively. The model-based SE’s for is from the variance estimator in Theorem 2. The model-based SE for is from the sandwich variance estimator assuming that the weights are known. Bootstraps are carried out using resampling with replacement, with 100 bootstrap replicates, which are typically adequate for boostrapped variance estimates (Efron and Tibshirani, 1994, Page 52).

The simulation results are are shown in Figure 1 as well as Table 2, with full details in the table. As expected, the full data estimator has the smallest bias and close to perfect coverage in all scenarios. The estimator has in general small bias and attain close to nominal coverage rate with boot SE when at least one of the models for and is correctly specified. When both models are correctly specified, the average model-based SE is very close to the empirical SD and the coverage associated with the model-based SE is close to 95%. When only one model is correctly specified, the average model-based SE is smaller than SD and the corresponding coverage is lower. This is more apparently in Scenarios 3 and 5, where the model misspecifications are severe.

For the other estimators, we see that has a large bias and poor coverage when the model for is misspecified, especially for Scenarios 3 and 7 where the model misspecification is severe; and similarly, and have large bias and poor coverage when the model for is misspecified, especially for Scenarios 5 and 7 where the model misspecification is severe. For all scenarios, the naive estimator substantially overestimates the parameter of interest, which coincides with the direction of left truncation bias.

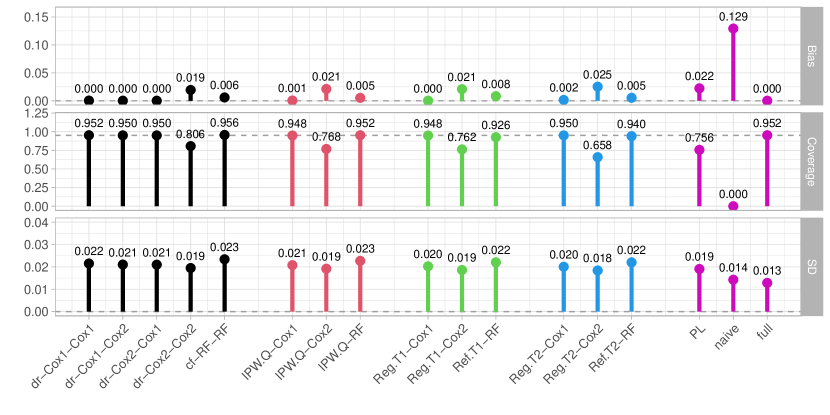

6.2 With machine learning methods

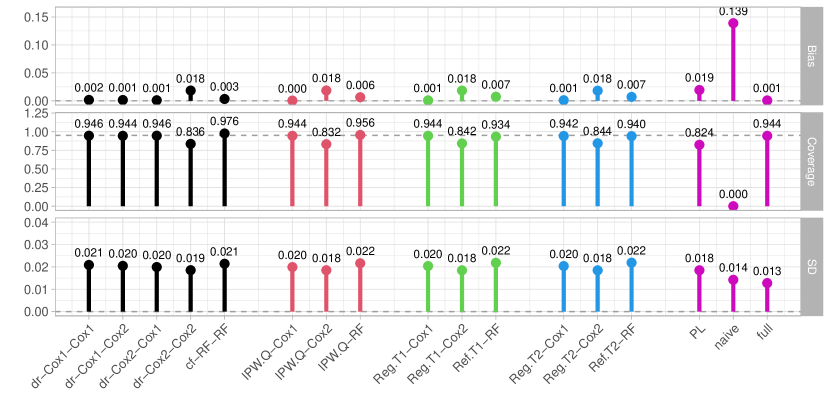

We study the finite sample performance of with machine learning methods to estimate and . In particular, we consider using the relative risk forest (‘RF’) for left truncated and right censored data (Yao et al., 2020). We compare it with that uses semiparametric models to estimate and , as well as the IPW and regression-based estimators that use semiparametric models or machine learning methods to estimate or , whichever is involved.

We generate the full data , where is generated in the same way as in Section 6.1. Following that and are generated from the following proportional hazards models, respectively:

where the baseline hazards if , and 0 otherwise; is the hazard function associated with the distribution. We take and , resulting in about 29.5% truncation after excluding subjects with .

Our estimand , computed from a simulated full data set with sample size . Again the nuisance parameters and are estimated using approaches described in Section 4, with when computing the reversed-time variables and . The models we consider are:

-

•

Cox1: ;

-

•

Cox2: ;

-

•

RF: LTRCforests::ltrcrrf with ntree = 100 and mtry = 2.

In particular, the relative risk forest (‘RF’) for left truncated and right censored data is implemented in the R package ‘LTRCforests’, and the estimates and from ‘RF’ are further bounded below by 0.05 to ensure the empirical overlap condition.

We consider the doubly robust estimators and (with ), denoted using the following convention; for instance, ‘dr-Cox1-Cox2’ corresponds to with estimated from model ‘Cox1’ and estimated from model ‘Cox2’. Obviously ‘Cox1’ is correctly specified for both and , while the ‘Cox2’ is misspecified for both and . We also consider the IPW estimator , and the regression-based estimators and , denoted using similar convention as above. In addition, we include the product-limit (PL) estimator (Wang, 1991) that assumes random left truncation, as well as the naive estimator and the oracle full data estimator described in Section 6.1.

As before, we report the bias, SD, average of the model-based SE, average of the boot SE, and the CP of the nominal 95% confidence intervals constructed using the model-based SE and the boot SE, respectively. The model-based SE for is from the variance estimator in Theorem 3. The model-based SE’s for and as well as the boot SE’s are computed in the same way as in Section 6.1.

The simulation results are summarized in Table 3, with additional visualization in Figure 4 of the Supplementary Material. As expected, the full data estimator has the smallest bias and close to perfect coverage of the CI’s. The estimator also has small biases and attain close to nominal coverage rates with boot SE, when at least one of the two models is correctly specified. When both models are correctly specified, the average model-based SE is very close to the empirical SD and the coverage associated with model-based SE is close to 95%. When only one model is correctly specified, the average model-based SE is smaller than SD and the corresponding coverage is lower. We also see that ‘cf-RF-RF’ has a small bias and good coverage rate associated with the model-based SE.

For the other estimators, we see that when the model for is misspecified, has a large bias and poor coverage; and similarly, when the model for is misspecified, and have large biases and poor coverages. In addition, the above three estimators have large biases when the nuisance parameter involved is estimated by ‘RF’, which is known to have slower than root- convergence. The product-limit estimator has a large bias, which is expected because it ignores the dependency between and . The naive estimator substantially overestimates the parameter of interest, which coincides with the direction of left truncation bias.

7 Applications

We apply the proposed estimators to analyze the data from a study on central nervous system (CNS) lymphoma and the data from Honolulu Asia Aging Study. The two data sets contain the two different censoring scenarios discussed earlier.

7.1 CNS Lymphoma Data

We analyze the data from a study on central nervous system (CNS) lymphoma (Wang et al., 2015), which is publicly available in the Supplementary Material of Vakulenko-Lagun et al. (2022). The data set initially contained 172 immunocompetent patients with primary CNS diffuse large B-cell lymphoma that achieved radiographic complete response (CR) to induction therapy. Within these patients, 98 progressed to relapse, 8 died without relapse, and 66 did not relapse by the end of the follow-up. The event time of interest is the overall survival time measured from the initiation of treatment at the time of diagnosis.

Following Vakulenko-Lagun et al. (2022), we restrict the data set to the 98 patients that progressed to relapse, where the overall survival time was left truncated by the time to relapse. Since patients could be lost to follow-up before progressing to relapse, the appropriate censoring model was the one described in Section 5.1. Among the 98 patients that progressed to relapse, 52 died during the follow-up. The patients who did not die by the end of follow-up were also right censored. Since it was possible that patients did not progress to relapse by the end of follow-up, the appropriate censoring model must allow censoring prior to left truncation, that is, the one described in Section 5.1.

As discussed in Vakulenko-Lagun et al. (2022), it is plausible that time to death and time to relapse are dependent, and treatment is strongly associated with both. We therefore follow Vakulenko-Lagun et al. (2022) and include the two binary treatment variables as covariates for the analysis: only MTX-based chemotherapy was used initially (yes/no), and initial radiation therapy was used (yes/no). We examine the overlap assumption for this data set in the Supplementary Material and show that it is satisfied empirically.

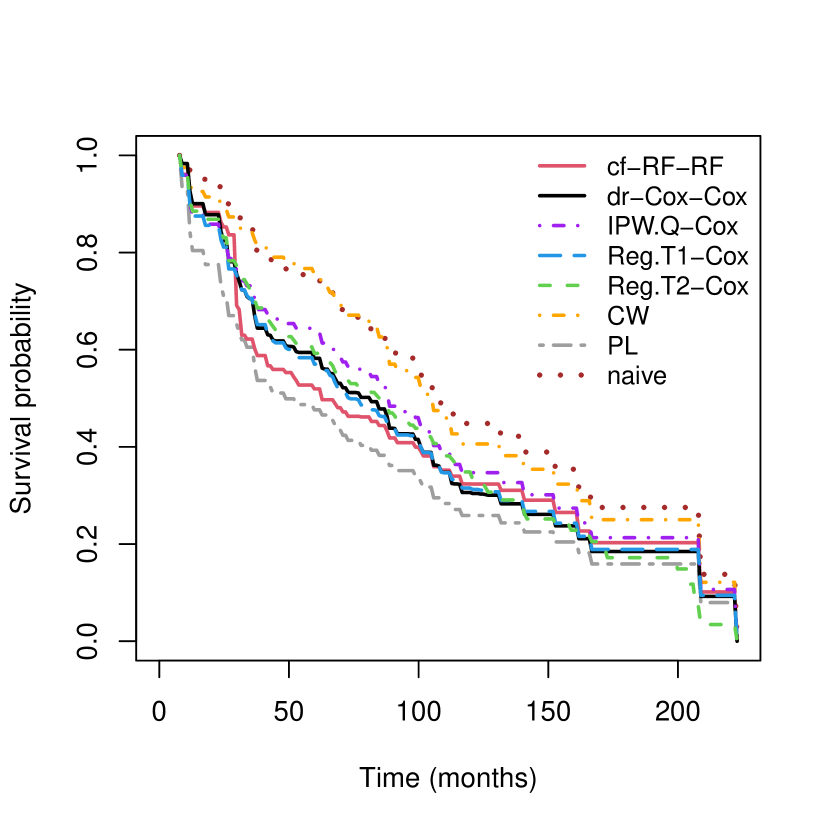

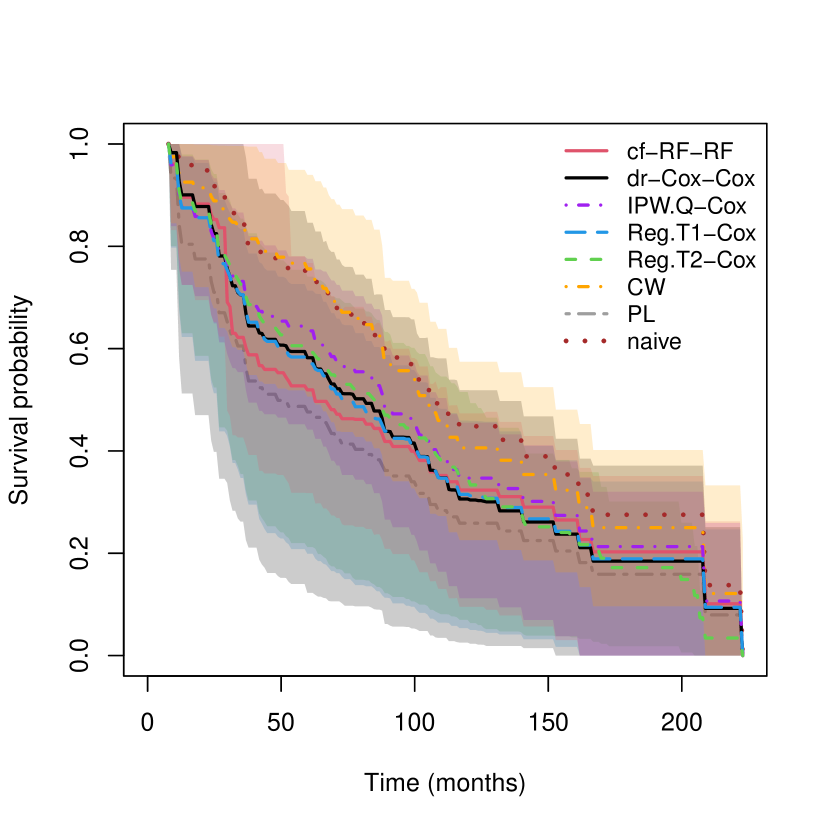

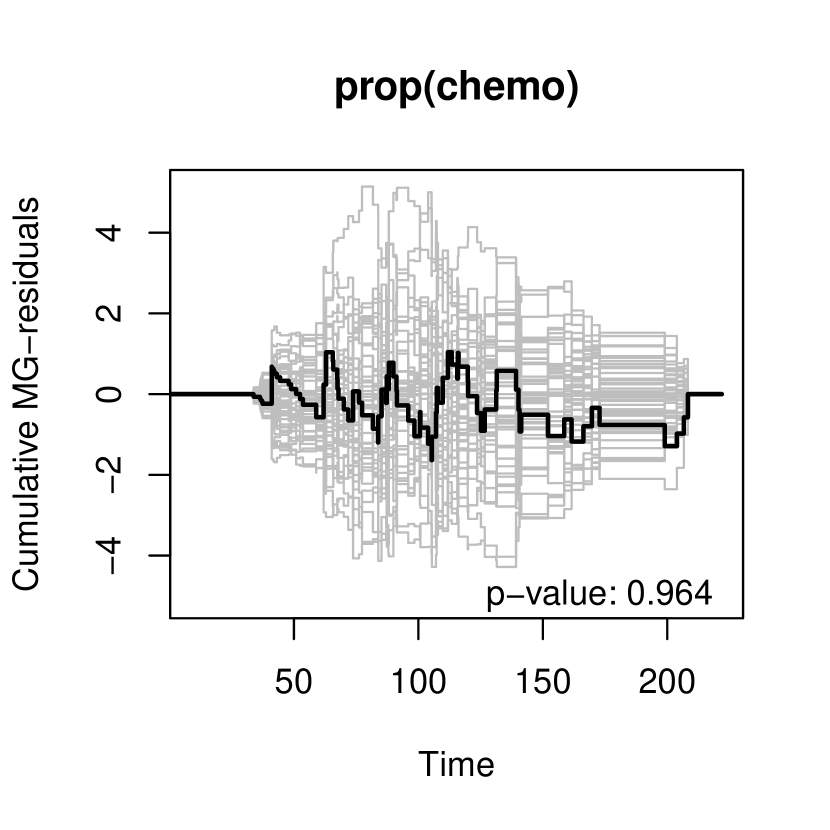

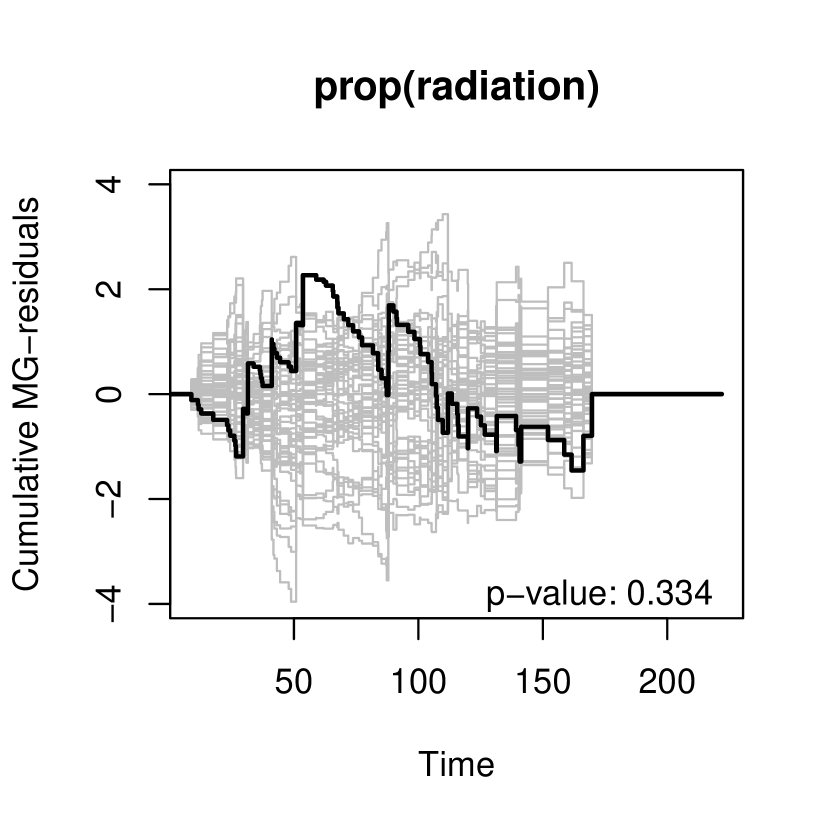

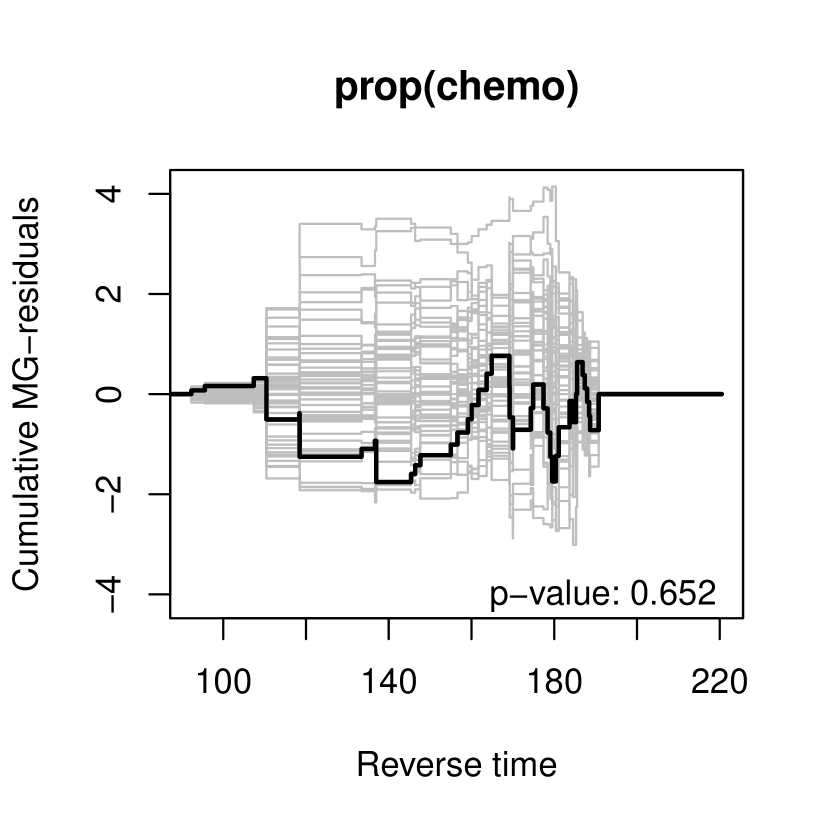

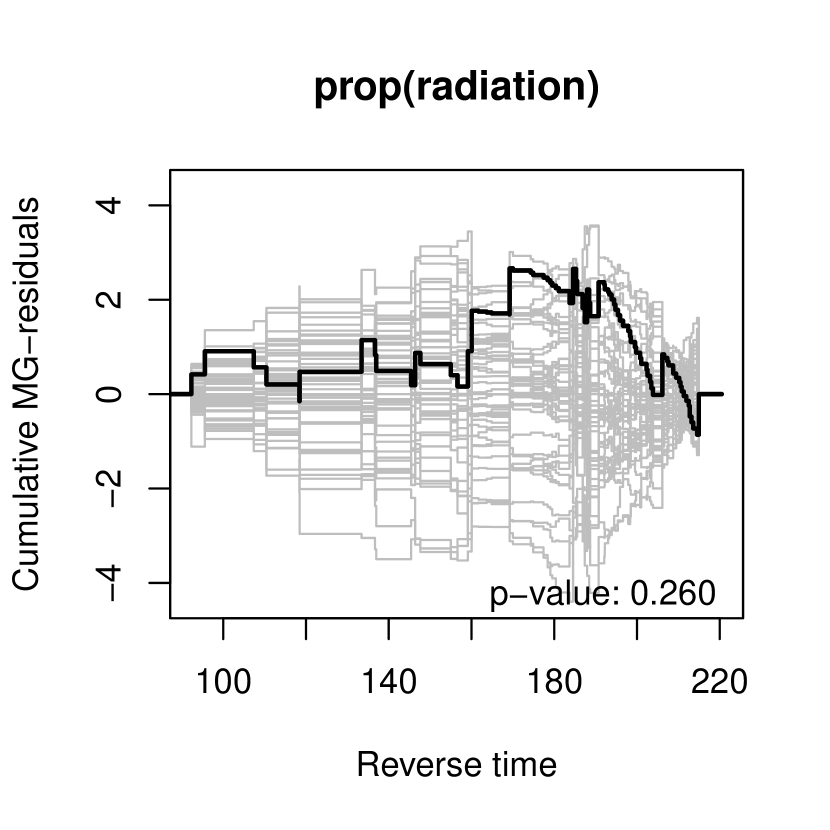

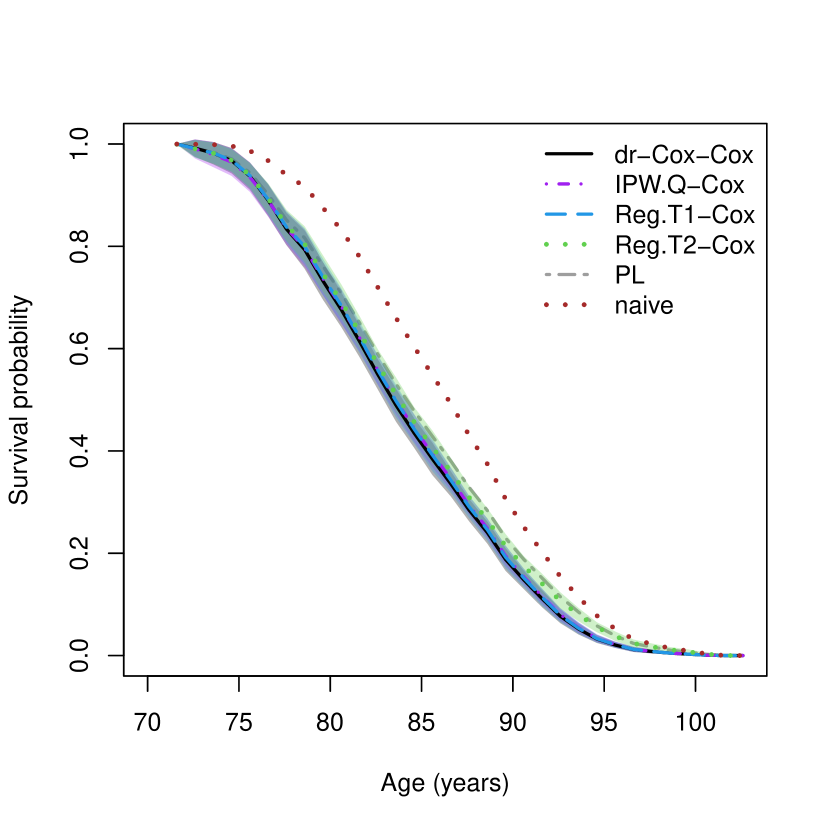

We consider estimating the overall survival curve for 8.8 months, the minimum event time in the data set. We consider the estimators , , and , with the nuisance parameters and estimated from the proportional hazards model. We also consider with 10-fold cross-fitting, and and estimated from the relative risk forest with mtry = 2 and ntree = 2000. The hyperparameter ntree is taken to be much larger than that in the simulation in order to obtain more stable estimates with the small sample size. As comparisons, we consider the PL estimator that assumes random left truncation, as well as the naive Kaplan-Meier estimator that ignores left truncation. In addition, we also compute the ‘CW’ estimator from Vakulenko-Lagun et al. (2022).

Figure 2 shows the estimated survival curves from different estimators. The corresponding 95% bootstrap confidence intervals are shown in the Supplementary Material. Due to the small sample size, in certain bootstrap runs and can be greater than one at early times up to about 50 months and we force them to be one in those cases. In addition, the estimates and their 95% confidence intervals at 36, 60, 120, and 180 months are also tabulated in the Supplementary Material.

From Figure 2, we see that the regression-based estimates and are very close to each other, suggesting that the Cox model might be a reasonable fit to . Test of proportionality in the Supplementary Material using cumulative martingale residuals (Lin et al., 1993) with risk set adjustment for left truncation detected no violations, although admittedly the test is probably under powered with such a small sample size. The PL estimate is visibly lower than the other estimates, consistent with the violation of random truncation assumption. The KM estimate is substantially larger than these other estimates, reflecting the known left truncation bias. The two IPW estimators, and the ‘CW’ estimator, are seen to be quite different for this data set.

7.2 HAAS data

We analyze the data collected between 1965 and 2012 from the Honolulu Heart Program (HHP, 1965-1990) and the subsequent Honolulu Asia Aging Study (HAAS, 1991-2012) (Gelber et al., 2012; Zhang and Xu, 2022). Age is the time scale of interest, and we are interested in the cognitive impairment-free survival, that is, the age to moderate cognitive impairment or death, whichever happened first. Only subjects that were alive and did not have cognitive impairment at the start of HAAS were included in the data set, therefore their ages for impairment-free survival were left truncated by their ages at the start of HAAS. Among the 2560 subjects in the data set, 463 (18.1%) were right censored due to loss to follow-up. Since loss to follow-up may only happen after subjects entered HAAS, this is censoring scenario 2 described in Section 5.2.

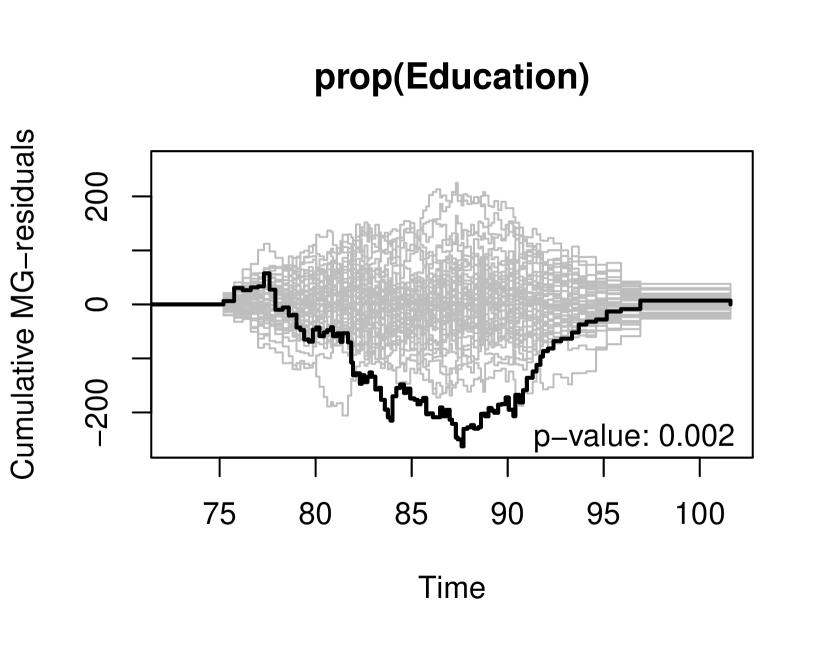

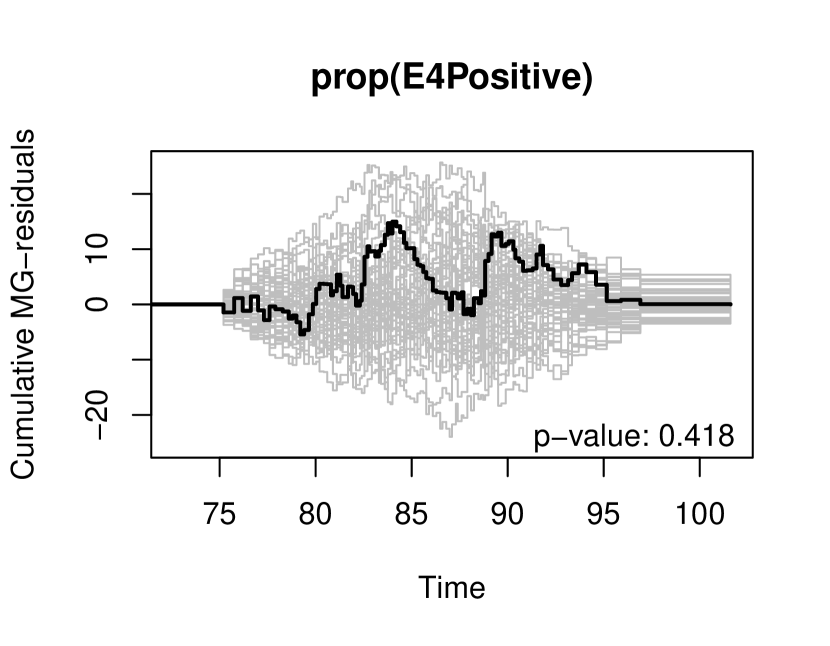

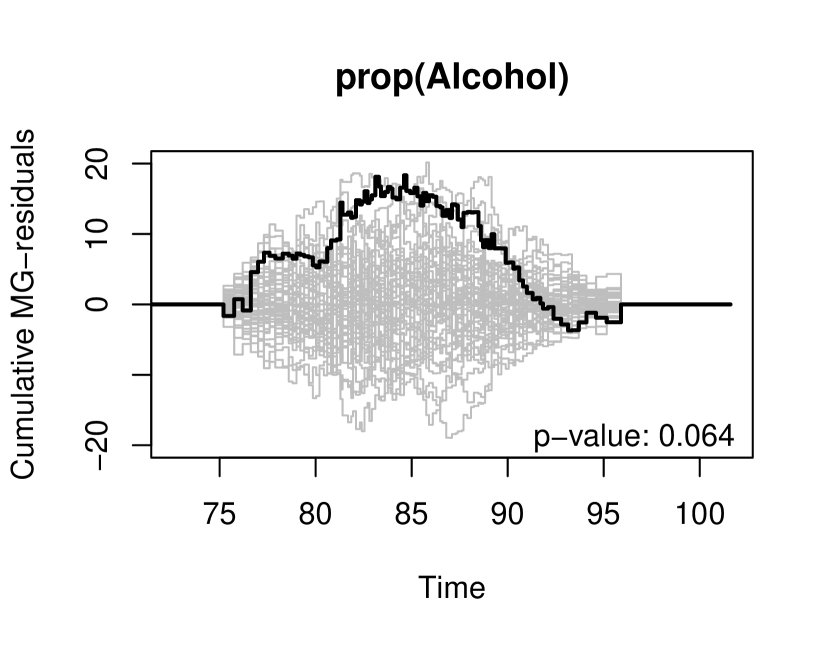

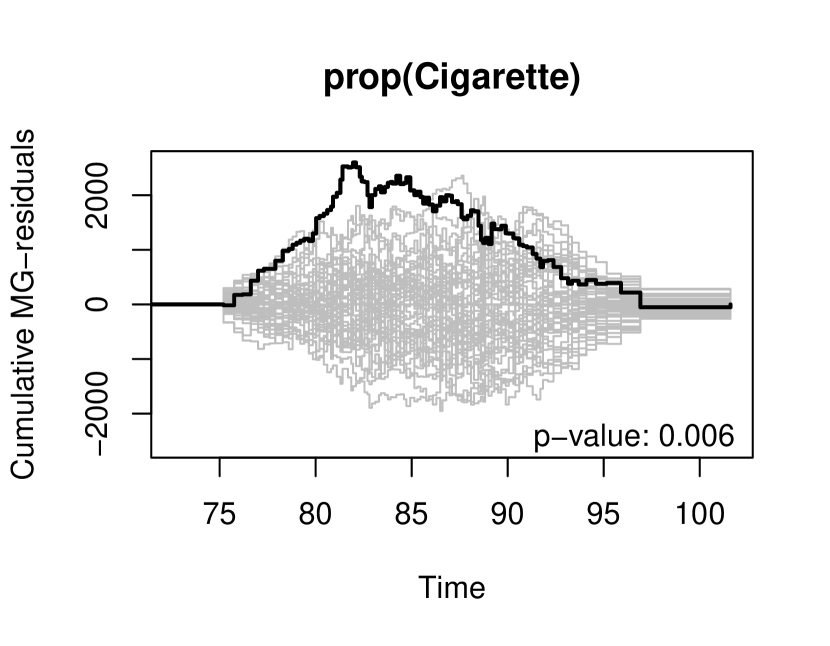

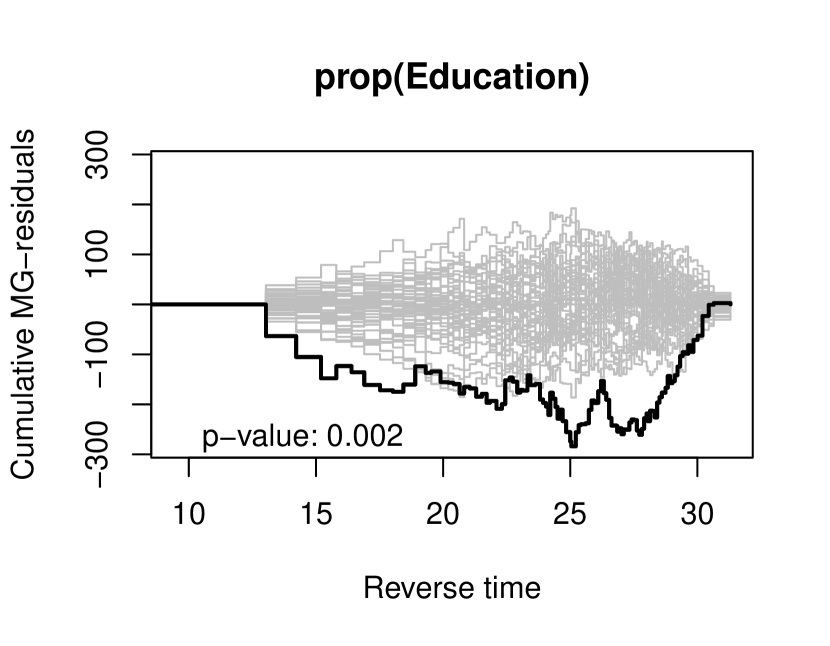

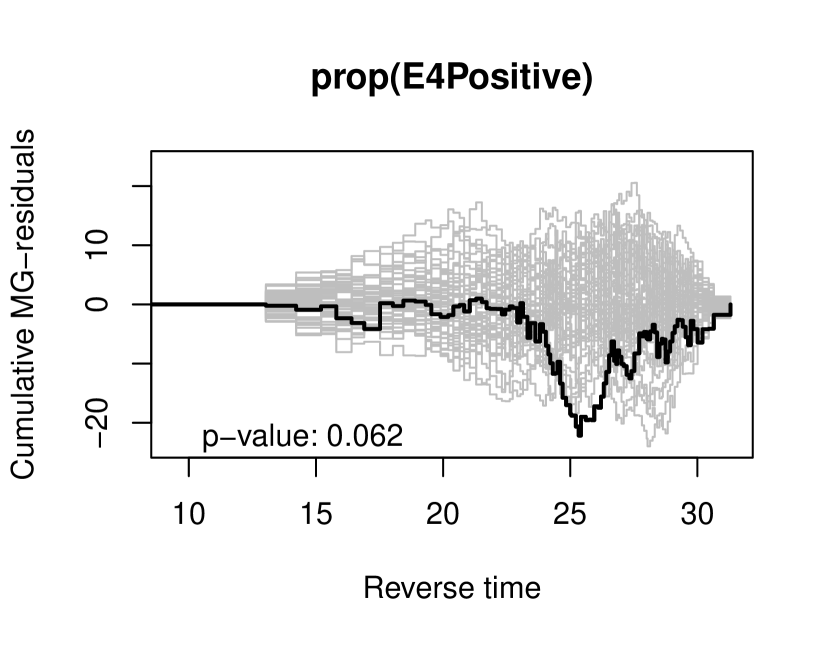

We detect dependency between age for impairment-free survival and age when entering HAAS using the conditional Kendall’s tau test (Tsai, 1990; Martin and Betensky, 2005), with tau = 0.0426 and -value of 0.0014. Therefore, we consider the risk factors collected during HHP that were thought to affect the outcomes including years of education, APOE (a ‘gene’ related to Alzheimer’s disease) positive (yes/no), mid-life alcohol consumption (heavy/not heavy), and mid-life cigarette consumption (packs per year). We examine the overlap assumption for this data set in the Supplementary Material and show that it is satisfied empirically.

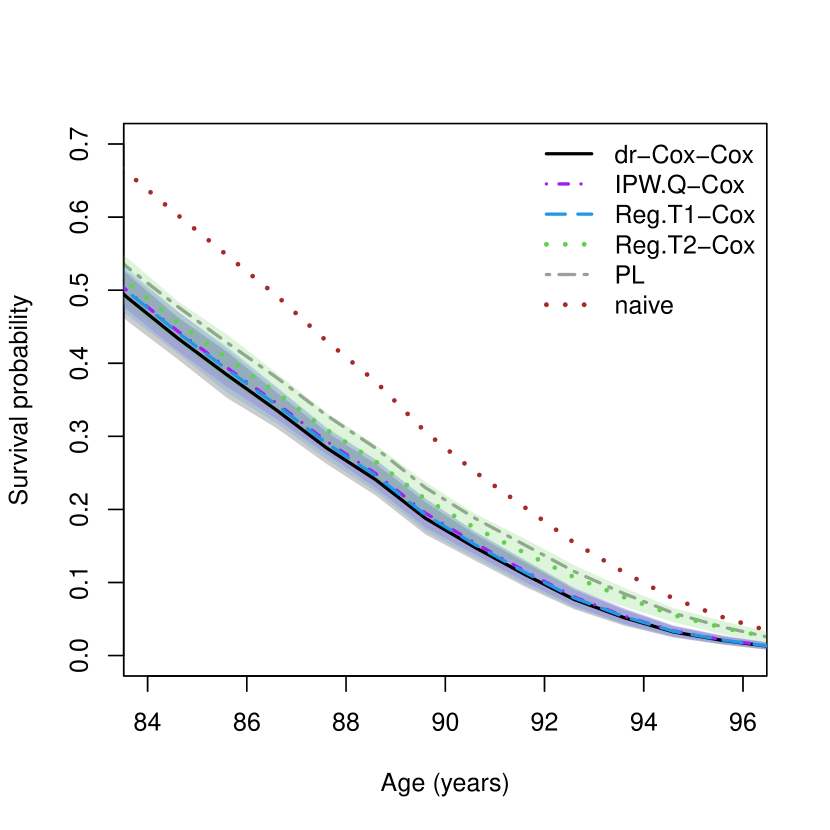

We focus on estimating the cognitive impairment-free survival for 72.6 years old, the minimum event time in the data set. We consider the estimators , , and , with the nuisance parameters and estimated from the proportional hazards model with the four covariates above. We do not implement because to the best of our knowledge, there is no existing R package of random forests for left truncated data that can incorporates case weights, which is needed in order to estimate as discussed in Section 5.2. As comparisons, we consider the PL estimator that assumes random left truncation, as well as the naive Kaplan-Meier estimator that ignores left truncation.

Figure 3 shows the estimated survival curves on the age interval 84 to 96 from different estimators and the corresponding 95% bootstrap confidence intervals. The entire survival curves are shown in the Supplementary Material. In addition, the estimates and their 95% confidence intervals at ages 80, 85, 90, and 95 years old are also tabulated in the Supplementary Material.

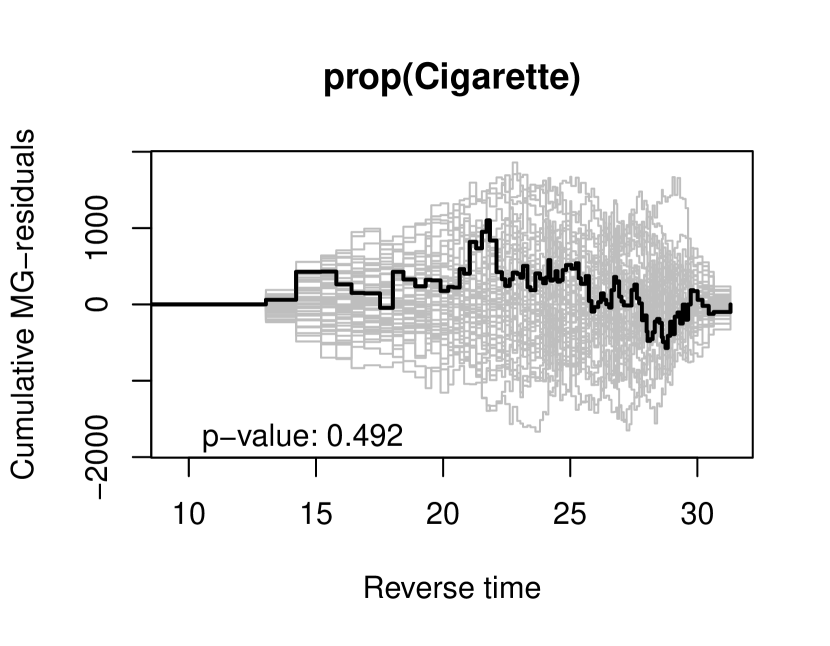

From Figure 3, we see that , and are close to each other. We also see that the is visibly larger than , especially for the later ages. Test using cumulative martingale residuals (see Supplementary Material) detected violation of proportional hazards assumption for education and cigarette consumption in the model for at significance level 0.05, and education in the model for . Model misspecification in this case appears to affect more than ; the difference between the two lies in the estimation of in the numerators, by for , and for . The latter seems to rely more on the correct model.

Finally the PL estimate is substantialy larger, most likely due to violation of the random truncation assumption. The KM estimate is obviously larger than all the other estimates, reflecting the known left truncation bias.

8 Discussion

It has been observed in the literature (van der Laan and Robins, 2003; Tsiatis, 2006; Dukes et al., 2019) that influence curves can yield doubly robust estimating functions. However, the derivation of influence curves and construction of the corresponding estimators can be non-trivial. In this paper, we have derived the EIC for the mean of an arbitrarily transformed survival time in the presence of covariate-induced dependent left truncation, and constructed model doubly robust and rate doubly robust estimators from an EIC-based doubly robust estimating function. The rate doubly robust estimator is constructed via cross-fitting, while the model doubly robust estimator does not require cross-fitting and is therefore more computationally efficient.

Rava and Xu (2023) and Luo and Xu (2022) have also considered constructing doubly robust estimators with one of the nuisance parameters estimated from a parametric or semiparametric model and the other from a nonparametric model. This situation is not covered in this paper. However, estimators constructed this way are not guaranteed to be root- consistent unless the the parametric or semiparametric model is correctly specified. As such, these estimators appear to have few advantages compared with the IPW or regression-based estimators.

The extension to right censoring assumes that the (residual) censoring variable is independent of the other variables, which may not be true in practice. A weaker assumption is that the censoring time and the left truncation and event times are independent conditional on measured baseline covariates. In the latter case inverse probability of censoring weighting may still be leveraged; the resulting estimator, however, relies on the correct specification of a censoring model given the covariates. It would be of interest to explore robust estimators that also have protection against censoring model misspecification, although this is beyond the scope of the current work.

Finally, the quasi-independence assumption requires the dependency between the left truncation time and the event time to be completely captured by measured baseline covariates, which may be unrealistic in practice. Alternative approaches include the “proximal identification framework” (Tchetgen Tchetgen et al., 2020), which leverages domain knowledge to avoid the “conditional independence” structure imposed by Assumption 1. This can be a promising approach and has been considered in a survival setting with right-censoring (Ying, 2022).

The code for the simulation and data analysis involved in this paper is available at

https://github.com/wangyuyao98/left_trunc_DR.

Acknowledgement

This research was partially supported by NIH/NIA grant R03 AG062432.

References

- Andersen et al. (1993) Andersen, P. K., O. Borgan, R. D. Gill, and N. Keiding (1993). Statistical Models Based on Counting Processes. New York, NY: Springer.

- Bang and Robins (2005) Bang, H. and J. M. Robins (2005). Doubly robust estimation in missing data and causal inference models. Biometrics 61(4), 962–973.

- Begun et al. (1983) Begun, J. M., W. Hall, W.-M. Huang, and J. A. Wellner (1983). Information and asymptotic efficiency in parametric-nonparametric models. Annals of Statistics 11(2), 432–452.

- Bickel (1982) Bickel, P. J. (1982). On adaptive estimation. Annals of Statistics 10(3), 647–671.

- Bickel et al. (1993) Bickel, P. J., C. A. Klaassen, Y. Ritov, and J. A. Wellner (1993). Efficient and Adaptive Estimation for Semiparametric Models, Volume 4. Baltimore, MD: Johns Hopkins University Press.

- Bilodeau (2022) Bilodeau, B. (2022). Blair Bilodeau’s contribution to the discussion of ‘Assumption-lean inference for generalised linear model parameters’ by Vansteelandt and Dukes. Journal of the Royal Statistical Society, Series B 84(3), 701–702.

- Chaieb et al. (2006) Chaieb, L. L., L.-P. Rivest, and B. Abdous (2006). Estimating survival under a dependent truncation. Biometrika 93(3), 655–669.

- Chao (1987) Chao, M.-T. (1987). Influence curves for randomly truncated data. Biometrika 74(2), 426–429.

- Cheng and Wang (2012) Cheng, Y.-J. and M.-C. Wang (2012). Estimating propensity scores and causal survival functions using prevalent survival data. Biometrics 68(3), 707–716.

- Cheng and Wang (2015) Cheng, Y.-J. and M.-C. Wang (2015). Causal estimation using semiparametric transformation models under prevalent sampling. Biometrics 71(2), 302–312.

- Chernozhukov et al. (2018) Chernozhukov, V., D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal 21(1), C1–C68.

- Chiou et al. (2019) Chiou, S. H., M. D. Austin, J. Qian, and R. A. Betensky (2019). Transformation model estimation of survival under dependent truncation and independent censoring. Statistical methods in medical research 28(12), 3785–3798.

- Cox (1972) Cox, D. R. (1972). Regression models and life-tables. Journal of the Royal Statistical Society, Series B 34(2), 187–202.

- Cox (1975) Cox, D. R. (1975). Partial likelihood. Biometrika 62(2), 269–276.

- Dukes et al. (2019) Dukes, O., T. Martinussen, E. J. Tchetgen Tchetgen, and S. Vansteelandt (2019). On doubly robust estimation of the hazard difference. Biometrics 75(1), 100–109.

- Durrett (2019) Durrett, R. (2019). Probability: Theory and Examples, Volume 49. New York, NY: Cambridge University Press.

- Efron and Petrosian (1994) Efron, B. and V. Petrosian (1994). Survival analysis of the gamma-ray burst data. Journal of the American Statistical Association 89(426), 452–462.

- Efron and Tibshirani (1994) Efron, B. and R. J. Tibshirani (1994). An Introduction to the Bootstrap. Boca Raton, FL: CRC Press.

- Emura and Wang (2012) Emura, T. and W. Wang (2012). Nonparametric maximum likelihood estimation for dependent truncation data based on copulas. Journal of Multivariate Analysis 110, 171–188.

- Emura et al. (2011) Emura, T., W. Wang, and H.-N. Hung (2011). Semi-parametric inference for copula models for truncated data. Statistica Sinica 21(1), 349–367.

- Ertefaie et al. (2014) Ertefaie, A., M. Asgharian, and D. Stephens (2014). Propensity score estimation in the presence of length-biased sampling: a non-parametric adjustment approach. Stat 3(1), 83–94.

- Fleming and Harrington (2011) Fleming, T. R. and D. P. Harrington (2011). Counting Processes and Survival Analysis. Hoboken, NJ: John Wiley & Sons.

- Gelber et al. (2012) Gelber, R., L. Launer, and L. White (2012). The Honolulu-Asia Aging Study: epidemiologic and neuropathologic research on cognitive impairment. Current Alzheimer Research 9(6), 664–672.

- Gross (1996) Gross, S. T. (1996). Weighted estimation in linear regression for truncated survival data. Scandinavian journal of statistics 23(2), 179–193.

- Gross and Lai (1996) Gross, S. T. and T. L. Lai (1996). Nonparametric estimation and regression analysis with left-truncated and right-censored data. Journal of the American Statistical Association 91(435), 1166–1180.

- Hasminskii and Ibragimov (1979) Hasminskii, R. Z. and I. A. Ibragimov (1979). On the nonparametric estimation of functionals. In Proceedings of the Second Prague Symposium on Asymptotic Statistics, pp. 41–51. Amsterdam: North-Holland.

- Heitjan and Rubin (1991) Heitjan, D. F. and D. B. Rubin (1991). Ignorability and coarse data. Annals of Statistics 19(4), 2244–2253.

- Hernán and Robins (2020) Hernán, M. A. and J. M. Robins (2020). Causal Inference: What If. Boca Raton: Chapman & Hall/CRC.

- Hou et al. (2021) Hou, J., J. Bradic, and R. Xu (2021). Treatment effect estimation under additive hazards models with high-dimensional confounding. Journal of the American Statistical Association, DOI: 10.1080/01621459.2021.1930546.

- Kennedy (2017) Kennedy, E. H. (2017). Semiparametric theory. arXiv preprint arXiv:1709.06418.

- Klein and Moeschberger (2003) Klein, J. P. and M. L. Moeschberger (2003). Survival Analysis: Techniques for Censored and Truncated Data, Volume 2. New York, NY: Springer.

- Kosorok (2008) Kosorok, M. R. (2008). Introduction to Empirical Processes and Semiparametric Inference. New York, NY: Springer.

- Lin et al. (1993) Lin, D. Y., L.-J. Wei, and Z. Ying (1993). Checking the Cox model with cumulative sums of martingale-based residuals. Biometrika 80(3), 557–572.

- Lopuhaä and Nane (2013) Lopuhaä, H. P. and G. F. Nane (2013). An asymptotic linear representation for the Breslow estimator. Communications in Statistics-Theory and Methods 42(7), 1314–1324.

- Luo and Xu (2022) Luo, J. and R. Xu (2022). Doubly robust inference for hazard ratio under informative censoring with machine learning. arXiv preprint arXiv:2206.02296.

- Mackenzie (2012) Mackenzie, T. (2012). Survival curve estimation with dependent left truncated data using Cox’s model. The International Journal of Biostatistics 8(1), 1–18.

- Martin and Betensky (2005) Martin, E. C. and R. A. Betensky (2005). Testing quasi-independence of failure and truncation times via conditional Kendall’s tau. Journal of the American Statistical Association 100(470), 484–492.

- Newey (1994) Newey, W. K. (1994). The asymptotic variance of semiparametric estimators. Econometrica: Journal of the Econometric Society 62(6), 1349–1382.

- Neyman (1959) Neyman, J. (1959). Optimal asymptotic tests of composite statistical hypotheses. In Probability and Statistics, U. Grenander (Ed.), pp. 416–444. New York, NY: Wiley.

- Ogburn et al. (2022) Ogburn, E. L., J. Cai, A. K. Kuchibhotla, R. A. Berk, and A. Buja (2022). Elizabeth L Ogburn, Junhui Cai, Arun K Kuchibhotla, Richard A Berk and Andreas Buja’s contribution to the discussion of ‘Assumption-lean inference for generalised linear model parameters’ by Vansteelandt and Dukes. Journal of the Royal Statistical Society, Series B 84(3), 715–716.

- Qian and Betensky (2014) Qian, J. and R. A. Betensky (2014). Assumptions regarding right censoring in the presence of left truncation. Statistics & probability letters 87, 12–17.

- Rava and Xu (2023) Rava, D. and R. Xu (2023). Doubly robust estimation of the hazard difference for competing risks data. Statistics in Medicine, DOI: 10.1002/sim.9644.

- Robins et al. (2008) Robins, J., L. Li, E. J. Tchetgen Tchetgen, and A. van der Vaart (2008). Higher order influence functions and minimax estimation of nonlinear functionals. In Probability and statistics: essays in honor of David A. Freedman, Volume 2, pp. 335–421. Beachwood, OH: Institute of Mathematical Statistics.

- Robins and Rotnitzky (2005) Robins, J. and A. Rotnitzky (2005). Inverse probability weighting in survival analysis. In Encyclopedia of Biostatistics, Volume 4, pp. 2619–2625. New York, NY: Wiley.

- Robins (1997a) Robins, J. M. (1997a). Causal inference from complex longitudinal data. In Latent variable modeling and applications to causality, pp. 69–117. New York, NY: Springer.

- Robins (1997b) Robins, J. M. (1997b). Marginal structural models. In 1997 Proceedings of the Section on Bayesian Statistical Science, pp. 1–10. Alexandria, VA: American Statistical Association.

- Robins (1999) Robins, J. M. (1999). Association, causation, and marginal structural models. Synthese 121, 151–179.

- Robins et al. (1995) Robins, J. M., A. Rotnitzky, and L. P. Zhao (1995). Analysis of semiparametric regression models for repeated outcomes in the presence of missing data. Journal of the American Statistical Association 90(429), 106–121.

- Rosenbaum and Rubin (1983) Rosenbaum, P. R. and D. B. Rubin (1983). The central role of the propensity score in observational studies for causal effects. Biometrika 70(1), 41–55.

- Rotnitzky et al. (2021) Rotnitzky, A., E. Smucler, and J. M. Robins (2021). Characterization of parameters with a mixed bias property. Biometrika 108(1), 231–238.

- Shen (2010) Shen, P.-s. (2010). Semiparametric estimation of survival function when data are subject to dependent censoring and left truncation. Statistics & Probability Letters 80(3-4), 161–168.

- Tang (2022) Tang, Y. (2022). Yanbo Tang’s contribution to the discussion of ‘Assumption-lean inference for generalised linear model parameters’ by Vansteelandt and Dukes. Journal of the Royal Statistical Society, Series B 84(3), 722–723.

- Tchetgen Tchetgen et al. (2010) Tchetgen Tchetgen, E. J., J. M. Robins, and A. Rotnitzky (2010). On doubly robust estimation in a semiparametric odds ratio model. Biometrika 97(1), 171–180.

- Tchetgen Tchetgen et al. (2020) Tchetgen Tchetgen, E. J., A. Ying, Y. Cui, X. Shi, and W. Miao (2020). An introduction to proximal causal learning. arXiv preprint arXiv:2009.10982.

- Tsai (1990) Tsai, W.-Y. (1990). Testing the assumption of independence of truncation time and failure time. Biometrika 77(1), 169–177.

- Tsai et al. (1987) Tsai, W.-Y., N. P. Jewell, and M.-C. Wang (1987). A note on the product-limit estimator under right censoring and left truncation. Biometrika 74(4), 883–886.

- Tsiatis (1981) Tsiatis, A. A. (1981). A large sample study of Cox’s regression model. Annals of Statistics 9(1), 93–108.

- Tsiatis (2006) Tsiatis, A. A. (2006). Semiparametric Theory and Missing Data. New York, NY: Springer.

- Vakulenko-Lagun et al. (2022) Vakulenko-Lagun, B., J. Qian, S. H. Chiou, N. Wang, and R. A. Betensky (2022). Nonparametric estimation of the survival distribution under covariate-induced dependent truncation. Biometrics 78(4), 1390–1401.

- van der Laan and Robins (2003) van der Laan, M. J. and J. M. Robins (2003). Unified Methods for Censored Longitudinal Data and Causality, Volume 5. New York, NY: Springer.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic Statistics, Volume 3. New York, NY: Cambridge University Press.

- Wang (1989) Wang, M.-C. (1989). A semiparametric model for randomly truncated data. Journal of the American Statistical Association 84(407), 742–748.

- Wang (1991) Wang, M.-C. (1991). Nonparametric estimation from cross-sectional survival data. Journal of the American Statistical Association 86(413), 130–143.

- Wang et al. (1986) Wang, M.-C., N. P. Jewell, and W.-Y. Tsai (1986). Asymptotic properties of the product limit estimate under random truncation. Annals of Statistics 14(4), 1597–1605.

- Wang et al. (2015) Wang, N., C. Gill, R. Betensky, and T. Batchelor (2015). Relapse patterns in primary CNS diffuse large B-cell lymphoma. Annual Meeting of the American Academy of Neurology, Washington D.C. 84(14 Supplement), P3.147.

- Woodroofe (1985) Woodroofe, M. (1985). Estimating a distribution function with truncated data. Annals of Statistics 13(1), 163–177.

- Xu and Chambers (2011) Xu, R. and C. Chambers (2011). A sample size calculation for spontaneous abortion in observational studies. Reproductive Toxicology 32, 490–493.

- Yao et al. (2020) Yao, W., H. Frydman, D. Larocque, and J. S. Simonoff (2020). Ensemble methods for survival data with time-varying covariates. arXiv preprint arXiv:2006.00567.

- Ying (2022) Ying, A. (2022). Proximal identification and estimation to handle dependent right censoring for survival analysis. arXiv preprint arXiv:2208.07014.

- Ying (2023) Ying, A. (2023). A cautionary note on doubly robust estimators involving continuous-time structure. arXiv preprint arXiv:2302.06739.

- Ying et al. (2020) Ying, A., R. Xu, C. D. Chambers, and K. L. Jones (2020). Causal effects of prenatal drug exposure on birth defects with missing by terathanasia. arXiv preprint arXiv:2004.08510.

- Zhang and Xu (2022) Zhang, Y. and R. Xu (2022). Marginal structural illness-death models for semi-competing risks data. arXiv preprint arXiv:2204.10426.

| Scenarios | Data-generating mechanism |

|---|---|

| 1. Both models correct | Cox: . |

| Cox: . | |

| 2. model moderately wrong | Cox: . |

| Cox: . | |

| 3. model severely wrong | Cox: . |

| mixture: Cox: , | |

| if . | |

| AFT: , | |

| if . | |

| 4. model moderately wrong | Cox: . |

| Cox: . | |

| 5. model severely wrong | mixture: AFT: , |

| if . | |

| Cox: , | |

| if . | |

| Cox: . | |

| 6. both models moderately wrong | Cox: |

| Cox: | |

| 7. both models severely wrong | mixture: AFT: , |

| if . | |

| Cox: , | |

| if . | |

| mixture: Cox: , | |

| if . | |

| AFT: , | |

| if . |

| Scenarios | Estimator | bias | %bias | SD | SE/boot SE | CP/boot CP |

|---|---|---|---|---|---|---|

| 1. | dr | -0.0015 | -0.6 | 0.021 | 0.020/0.020 | 0.946/0.938 |

| Both models | IPW.Q | -0.0004 | -0.2 | 0.020 | 0.015/0.019 | 0.864/0.946 |

| correct | Reg.T1 | -0.0004 | -0.2 | 0.019 | - /0.019 | - /0.942 |

| Reg.T2 | -0.0005 | -0.2 | 0.019 | - /0.019 | - /0.942 | |

| naive | 0.2414 | 101.9 | 0.016 | 0.016/0.016 | 0.000/0.000 | |

| full | -0.0005 | -0.2 | 0.009 | 0.009/0.009 | 0.954/0.946 | |

| 2. | dr | -0.0017 | -0.7 | 0.020 | 0.018/0.019 | 0.930/0.948 |

| model | IPW.Q | 0.0106 | 4.5 | 0.017 | 0.014/0.017 | 0.802/0.894 |

| moderately | Reg.T1 | -0.0007 | -0.3 | 0.019 | - /0.019 | - /0.944 |

| wrong | Reg.T2 | -0.0008 | -0.3 | 0.019 | - /0.019 | - /0.946 |

| naive | 0.2355 | 99.4 | 0.016 | 0.016/0.016 | 0.000/0.000 | |

| full | -0.0006 | -0.2 | 0.009 | 0.009/0.009 | 0.950/0.954 | |

| 3. | dr | -0.0027 | -1.1 | 0.023 | 0.018/0.024 | 0.896/0.950 |

| model | IPW.Q | 0.0528 | 22.3 | 0.018 | 0.015/0.018 | 0.064/0.176 |

| severely | Reg.T1 | -0.0019 | -0.8 | 0.023 | - /0.024 | - /0.948 |

| wrong | Reg.T2 | -0.0020 | -0.8 | 0.023 | - /0.024 | - /0.950 |

| naive | 0.2877 | 121.4 | 0.016 | 0.016/0.016 | 0.000/0.000 | |

| full | -0.0001 | -0.1 | 0.008 | 0.008/0.008 | 0.956/0.946 | |

| 4. | dr | -0.0015 | -0.6 | 0.021 | 0.019/0.020 | 0.930/0.948 |

| model | IPW.Q | -0.0007 | -0.3 | 0.021 | 0.016/0.020 | 0.872/0.944 |

| moderately | Reg.T1 | 0.0113 | 4.6 | 0.018 | - /0.017 | - /0.894 |

| wrong | Reg.T2 | 0.0110 | 4.5 | 0.018 | - /0.017 | - /0.894 |

| naive | 0.2446 | 100.2 | 0.016 | 0.016/0.016 | 0.000/0.000 | |

| full | -0.0006 | -0.2 | 0.009 | 0.009/0.009 | 0.948/0.944 | |

| 5. | dr | -0.0020 | -2.0 | 0.011 | 0.015/0.012 | 0.988/0.964 |

| model | IPW.Q | -0.0009 | -0.9 | 0.009 | 0.007/0.010 | 0.840/0.956 |

| severely | Reg.T1 | -0.0288 | -29.5 | 0.008 | - /0.008 | - /0.070 |

| wrong | Reg.T2 | -0.0293 | -30.0 | 0.007 | - /0.008 | - /0.058 |

| naive | 0.2329 | 238.7 | 0.014 | 0.015/0.015 | 0.000/0.000 | |

| full | -0.0001 | -0.1 | 0.005 | 0.005/0.005 | 0.956/0.956 | |

| 6. | dr | 0.0230 | 9.4 | 0.019 | 0.017/0.018 | 0.720/0.734 |

| Both models | IPW.Q | 0.0263 | 10.8 | 0.018 | 0.014/0.017 | 0.546/0.662 |

| moderately | Reg.T1 | 0.0262 | 10.7 | 0.018 | - /0.017 | - /0.672 |

| wrong | Reg.T2 | 0.0260 | 10.6 | 0.018 | - /0.017 | - /0.678 |

| naive | 0.2433 | 99.7 | 0.016 | 0.016/0.016 | 0.000/0.000 | |

| full | -0.0005 | -0.2 | 0.009 | 0.009/0.009 | 0.950/0.952 | |

| 7. | dr | -0.0570 | -58.4 | 0.006 | 0.006/0.007 | 0.000/0.004 |

| Both models | IPW.Q | -0.0635 | -65.0 | 0.006 | 0.003/0.006 | 0.000/0.000 |

| severely | Reg.T1 | -0.0589 | -60.4 | 0.006 | - /0.006 | - /0.000 |

| wrong | Reg.T2 | -0.0590 | -60.5 | 0.006 | - /0.006 | - /0.000 |

| naive | 0.2217 | 227.2 | 0.015 | 0.015/0.015 | 0.000/0.000 | |

| full | 0.0000 | 0.0 | 0.004 | 0.004/0.004 | 0.944/0.946 |

| Estimator | bias | SD | SE/boot SE | CP/boot CP |

| dr-Cox1-Cox1 | -0.0016 | 0.021 | 0.020/0.020 | 0.948/0.946 |

| dr-Cox1-Cox2 | -0.0014 | 0.020 | 0.019/0.020 | 0.930/0.944 |

| dr-Cox2-Cox1 | -0.0010 | 0.020 | 0.019/0.020 | 0.938/0.946 |

| dr-Cox2-Cox2 | 0.0184 | 0.019 | 0.018/0.019 | 0.838/0.836 |

| cf-RF-RF | 0.0032 | 0.021 | 0.023/0.025 | 0.966/0.976 |

| IPW.Q-Cox1 | -0.0004 | 0.020 | 0.018/0.020 | 0.924/0.944 |

| IPW.Q-Cox2 | 0.0184 | 0.018 | 0.017/0.019 | 0.814/0.832 |

| IPW.Q-RF | -0.0064 | 0.022 | 0.019/0.022 | 0.886/0.956 |

| Reg.T1-Cox1 | -0.0008 | 0.020 | - /0.020 | - /0.944 |

| Reg.T1-Cox2 | 0.0183 | 0.018 | - /0.019 | - /0.842 |

| Reg.T1-RF | -0.0073 | 0.022 | - /0.022 | - /0.934 |

| Reg.T2-Cox1 | -0.0010 | 0.020 | - /0.020 | - /0.942 |

| Reg.T2-Cox2 | 0.0181 | 0.018 | - /0.019 | - /0.844 |

| Reg.T2-RF | -0.0070 | 0.022 | - /0.022 | - /0.940 |

| PL | 0.0193 | 0.018 | - /0.018 | - /0.824 |

| naive | 0.1389 | 0.014 | 0.014/0.014 | 0.000/0.000 |

| full data | -0.0007 | 0.013 | 0.013/0.013 | 0.956/0.944 |

Appendix. Regression-based estimator

Estimator (25) can be seen as regression-based because . This way estimates the full data conditional expectation .

Supplementary Material

The Supplementary Material here contains the proofs, details of the estimators under right censoring, additional simulation results, and additional results for the analysis of the two data sets. In particular, this supplement contains the following materials:

-

1.

Preliminaries

-

2.

Martingale theory

-

3.

Identification of

-

4.

Derivation of the EIC

-

5.

Double robustness of the estimating function

-

6.

Asymptotics

-

7.

Estimation under right censoring

-

8.

Additional materials for simulations

-

9.

Applications

-

10.

Equivalence with the IF in Chao (1987)

Appendix A Preliminaries

We will use to denote the minimum of and , to denote the maximum of and , and ‘’ to denote less than or equal to up to a constant factor.

If we do not specify the limit for integrals, the integrals are taken on the support of the corresponding variables.

Here we define the quantities used in the Supplementary Material.

Let

| (38) |

Based on the joint density for in the observed data given in Assumption 1, we can derive the following marginal and conditional densities for observed data distribution in terms of and :

| (39) | ||||

| (40) | ||||

| (41) | ||||

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) |

In addition, denote

| (47) | ||||

| (48) | ||||

| (49) |

Appendix B Martingale theory

Recall that

| (50) | |||

| (51) |

where

| (52) | ||||

| (53) |

Lemma 4.

Proof.

In the following proof, we will first show that is -measurable and for all . Then we will show that for all if is the true CDF of given in the full data.

1) We first show that the at risk indicator is -measurable, where . For any , since

| (54) | ||||

| (55) | ||||

| (56) |

we have

| (57) |

so is -measurable, and is -measurable.

2) We now show that for any , . It suffices to show that is bounded. By (44),

| (58) | ||||

| (59) | ||||

| (60) | ||||

| (61) | ||||

| (62) | ||||

| (63) |

Therefore,

| (64) |

3) Suppose that is the true CDF of given in the full data. We will show that for any , , which implies that . Since the reversed time filtration

| (65) | ||||

| (66) |

by the definition of backwards martingale and properties of conditional expectations (Durrett, 2019), it suffices to show that for any non-negative measurable function on and any ,

| (67) | |||

| (68) |

For any such function ,

| (69) | ||||

| (70) | ||||

| (71) | ||||

| (72) | ||||

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |

On the other hand,

| (77) | ||||

| (78) | ||||

| (79) | ||||

| (80) | ||||

| (81) | ||||

| (82) | ||||

| (83) | ||||

| (84) | ||||

| (85) | ||||

| (86) | ||||

| (87) |

Therefore,

| (88) | ||||

| (89) |

so

| (90) | ||||

| (91) |

∎

The following proposition states the property of that is useful in the later proofs.

Proposition 2.

Proof.

Let for . By Assumption 3, a.s., so

| (93) | ||||

| (94) | ||||

| (95) |

where is defined in Section 2 of the main paper. Since is bounded on , is bounded on . Besides, as shown in Lemma 4, is a backwards martingale with respect to , so is a martingale with respect to the filtration (defined in Section 2 of the main paper). Therefore, is a martingale with respect to the filtration (Fleming and Harrington, 2011). Thus,

| (96) |

In addition, since for all , we have

| (97) |

∎

Appendix C Identification of

Proof of Lemma 1.

| (98) | ||||

| (99) | ||||

| (100) | ||||

| (101) |

As a special case with , we have . Therefore,

| (102) |

We now show that can be characterized by the reverse time hazard function . By definition,

| (103) |

Besides, . By solving the above differential equation, we get

| (104) |

Next, we will show that is identifiable from observed data distribution. Specifically, we will show that under Assumptions 1 and 2,

| (105) |

| (106) |

so

| (107) | ||||

| (108) | ||||

| (109) |

Therefore,

| (110) |

∎

Appendix D Derivation of the EIC

As previously defined, denotes a regular parametric submodel for observed data and the corresponding density. We use for instance, and to denote the density of and conditional density of given under . We have for example,

| (111) |

The following properties of the scores will be useful in the proofs. From the definition,

| (112) |

so we have

| (113) |

In addition, from the definition, we can show that , and , etc.

The quantities , and below appear during the computation to derive the influence curve. Let

| (114) | ||||

| (115) | ||||

| (116) |

We have immediately

| (117) |

Proof of Lemma 2.

(i) To prove that , we will first that and then show that . The proof follows the techniques used in Bickel et al. (1993) and Tsiatis (2006).

Recall that under Assumption 1, the joint density for in observed data is

| (118) | ||||

| (119) |

For any regular parametric submodel satisfing Assumption 1, the corresponding observed data density is

| (120) |

Denote

| (121) | ||||

| (122) | ||||

| (123) |

and denote

| (124) |

Then the score for observed data is

| (125) | ||||

| (126) | ||||

| (127) | ||||

| (128) | ||||

| (129) | ||||

| (130) | ||||

| (131) | ||||

| (132) | ||||

| (133) |

Since , we have

| (134) |

On the other hand, we will show that . Since bounded functions of and are dense in and , respectively, it suffices to show that for any bounded functions , , there exists a parametric submodel whose score is . For any bounded functions , , let

| (135) | ||||

| (136) | ||||

| (137) | ||||

| (138) |

Consider the parametric submodel

| (139) |

with

| (140) | ||||

| (141) | ||||

| (142) |

and is the parameter chosen sufficiently small to guarantee that , and are positive. Since

| (143) | ||||

| (144) | ||||

| (145) |

, , are density functions and, at they are (conditional) densities of of given , given , and , respectively. Therefore the class of functions given in (139) is a parametric submodel. Moreover, it can be verified that

| (146) |

Therefore,

| (147) |

Thus,

| (148) |

(ii) We now characterize . Since the Hilbert space is , by the definition of orthogonal complement,

| (149) |

We would like to find all functions such that for any and ,

| (150) |

Since and , it can be verified that (150) holds if and only if the following two conditions hold:

| (151) | |||

| (152) |

Therefore,

| (155) |

∎

Proof of Lemma 3.

To derive an influence curve, we consider a regular parametric submodel for the observed data . The proof contains much algebra related to the computation under .

Let denote the expectation taken with respect to the distribution , and the full data CDF of given under . Then

| (156) |

We want to find a function such that

| (157) |

and . Then will be an influence curve. We will first compute , and then try to write it in the form of the right hand side (RHS) of (157).

The derivative

| (158) | ||||

| (159) |

Because in the proof of Lemma 1 we have shown that and , therefore

| (160) |

We will compute the two derivatives in (160) next.

| (161) | ||||

| (162) | ||||

| (163) |

From (113) we have

| (164) |

so

| (165) | ||||

| (166) | ||||

| (167) |

As a special case with , we have

| (169) |

From (160), (LABEL:eq:lem2_2) and (LABEL:eq:lem2_3) we have

| (171) |

If we can write the second term of the RHS in (171) into for some function , then

satisfies (157).

We now focus on finding . To compute recall from (104), , so

| (172) | ||||

| (173) |

By (105), we have

In addition, using (113) we have

| (174) | ||||

| (175) | ||||

| (176) |

Therefore, from (173),

| (177) | ||||

| (178) |

So we have

| (179) |

where are stated as follows. We have

| (180) | ||||

| (181) | ||||

| (182) | ||||

| (183) |

Because , we have

| (184) | ||||

| (185) | ||||

| (186) | ||||

| (187) | ||||