Do financial regulators act in the public’s interest? A Bayesian latent class estimation framework for assessing regulatory responses to banking crises

Abstract

When banks fail amidst financial crises, the public criticizes regulators for bailing out or liquidating specific banks, especially the ones that gain attention due to their size or dominance. A comprehensive assessment of regulators, however, requires examining all their decisions, and not just specific ones, against the regulator’s dual objective of preserving financial stability while discouraging moral hazard. In this article, we develop a Bayesian latent class estimation framework to assess regulators on these competing objectives and evaluate their decisions against resolution rules recommended by theoretical studies of bank behavior designed to contain moral hazard incentives. The proposed estimation framework addresses the unobserved heterogeneity underlying regulator’s decisions in resolving failed banks and provides a disciplined statistical approach for inferring if they acted in the public interest. Our results reveal that during the crises of 1980’s, the U.S. banking regulator’s resolution decisions were consistent with recommended decision rules, while the U.S. savings and loans (S&L) regulator, which ultimately faced insolvency in 1989 at a cost of $132 billion to the taxpayer, had deviated from such recommendations. Timely interventions based on this evaluation could have redressed the S&L regulator’s decision structure and prevented losses to taxpayers.

Keywords: Bank failures, Federal Deposit Insurance Corporation (FDIC), Federal Savings and Loans Insurance Corporation (FSLIC), Bayesian inference, collapsed Gibbs sampler, Latent class models.

1 Introduction

During financial crises when a large number of banks fail, actions of financial regulators receive substantial public scrutiny. The global financial crisis of 2008 is one such recent example that led to widespread bank failures, reviving debate over how financial regulators might preserve immediate financial stability while also safeguarding against future moral hazard. During a financial crisis, regulators determine and administer the bailout, sale or liquidation of failed banks. Regulators bail out banks when they place greater emphasis on preserving financial stability and liquidate institutions when they are more attentive to the curtailment of moral hazard incentives. Critical assessments of these actions are essential to ensuring regulators balance the competing concerns in a manner that serves the public interest. However, the public typically criticizes specific regulatory decisions instead of evaluating how closely their overall decision framework serves the public interest. Individuals disfavor bailouts because they represent transfers from taxpayers to shareholders222“The firms we rescued were usually not gracious about the terms of their rescues, while the overwhelming sentiment among the public was that they shouldn’t have been rescued at all.”(Bernanke et al., 2019). The public also criticizes bank liquidations because they are costly for depositors and loan customers (Isaac, 2010). How can the public and their elected representatives comprehensively assess the actions of regulators against their competing objectives of preserving financial stability and restraining moral hazard?

Theoretical studies of regulator and bank behavior develop decision rules that resolve the trade-off between the two objectives in a manner that maximizes the value of output generated by the banking sector, and thereby provide a benchmark for evaluating such agencies. Broadly, these studies recommend state-dependent decision rules that vary in response to economic and industry-wide conditions that accompanied bank failures (see for example Cordella and Yeyati (2003); Acharya and Yorulmazer (2008); DeYoung et al. (2013) and the references therein). For instance, theoretical models recommend that regulators adopt distinct decision rules for handling banks that failed in the midst of economic distress, and those that failed in normal economic conditions. However, data on bank resolutions do not contain details on the extent to which bank-specific and broader economic conditions were considered in each decision. Furthermore, even though distress in the economy and in the banking industry are observable through measures such as unemployment rate, and growth in output, it is not immediately clear (1) what threshold regulators may have used to distinguish between periods of distress and normalcy, and (2) what aspects of a failed bank’s overall health ultimately inform the regulator’s resolution decision.

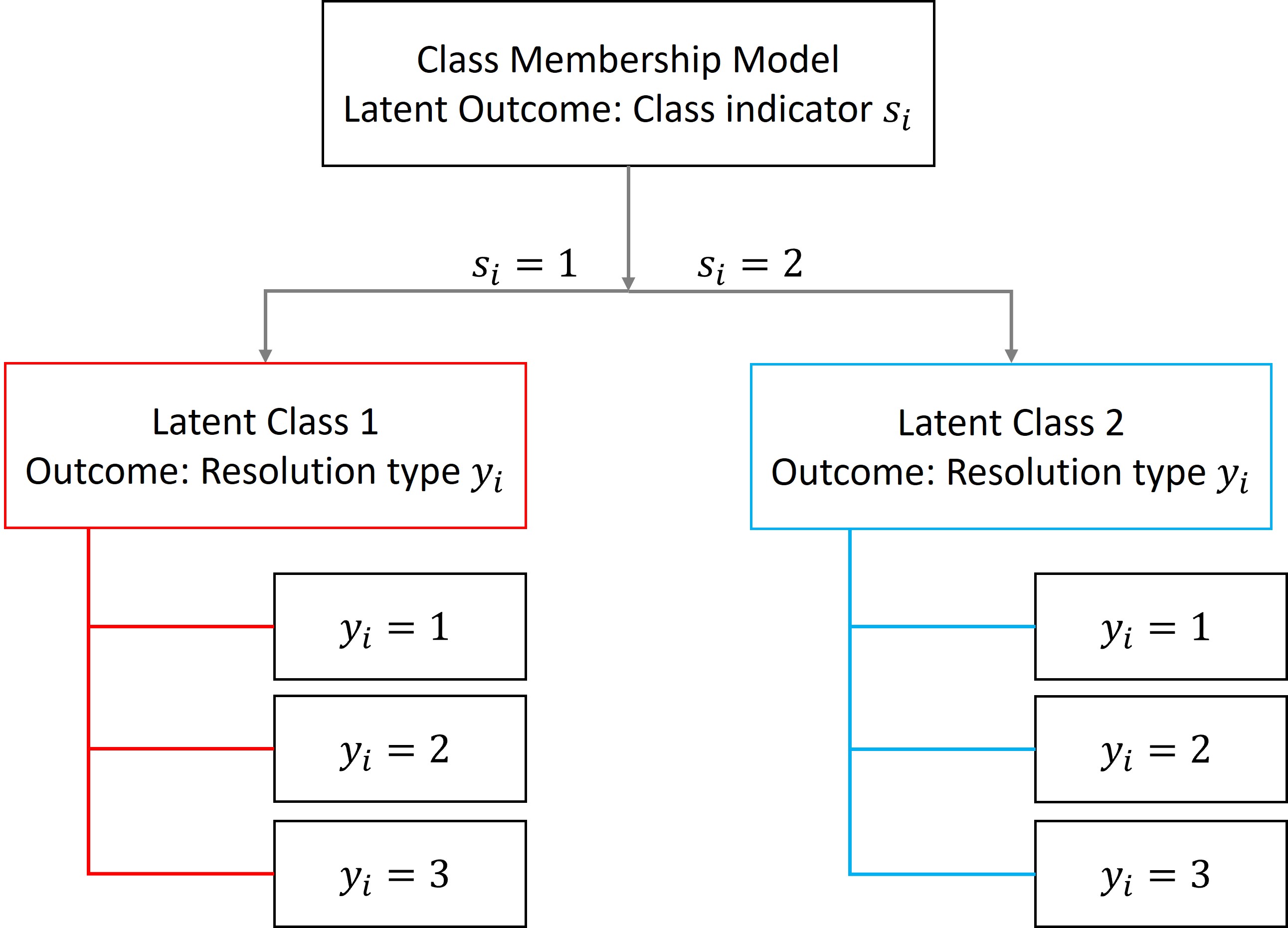

In this paper, we develop a Bayesian latent class estimation framework to compare regulators’ decisions against theoretical decision rules that foster financial stability while restraining moral hazard. Theoretical benchmarks recommend applying distinct decision rules that vary by economic and industry conditions, but the thresholds used by regulators to categorize banks into distinct decision rules are unobservable. For instance, when one bank failed in Kansas, and another in Kentucky in 1988 where unemployment rates were 5% and 8.5% respectively, it is not apparent whether regulators considered only one, both or neither banks to have failed amid high distress. The latent class model developed in this paper incorporates such uncertainty by assigning banks into distinct decision rules, or classes with probability, rather than certainty. The proposed model consists of a hierarchical structure (see figure 2) in which the first layer is a probabilistic class-membership model that assigns failed banks to classes that correspond to the two distinct states of nature, such as high or low underlying economic distress. Conditional on class membership, the second layer specifies the relationships between the resolution type, namely assistance, sale or liquidation of failed banks, and bank-specific covariates, such as size and asset quality. These relationships are homogeneous within and heterogeneous across the latent classes when the classes are statistically different from each other. Our approach serves as a classification algorithm that determines whether regulators assigned distinct decision rules to classes of banks that failed in disparate economic and industry conditions, and to systematically infer if they acted in the public interest.

1.1 Regulators of the U.S. banking sector, their resolution methods and the crises of 1980’s

In this article we assess regulators from two sub-sectors of the U.S. banking industry, commercial banks and Savings and Loans (S&L) institutions333“ A Savings and Loans institution is a financial institution that ordinarily possesses the same depository, credit, financial intermediary, and account transactional functions as a bank, but that is chiefly organized and primarily operates to promote savings and home mortgage lending rather than commercial lending. Also known as a savings bank, a savings association, a savings and loan association, or an S&L.”FDIC (1998), during their simultaneous crises of the 1980’s. The Federal Deposit Insurance Corporation (FDIC) serves as the regulatory authority for commercial banks while the Federal Savings and Loans Insurance Corporation (FSLIC) was the counterpart for S&L’s until its failure in 1989. The two regulators are comparable on account of the fundamental similarities across banks and S&L’s in that both institutions offer loans and deposits, undertake maturity transformation, monitor information and offer liquidity and payments services (Freixas and Rochet, 2008).

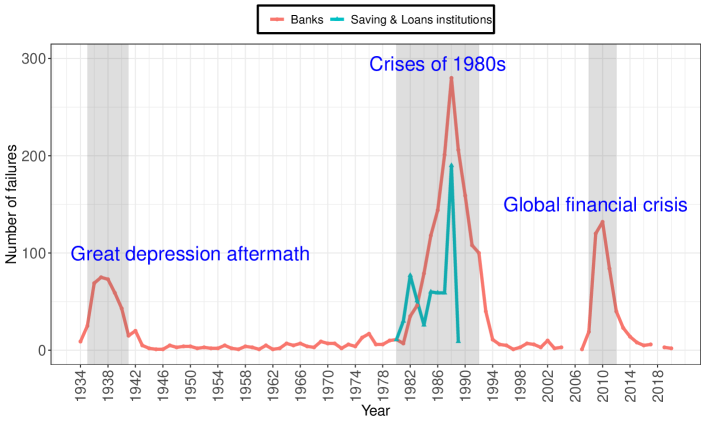

During the crises of 1980’s, these two related sectors of the U.S. banking industry, namely commercial banks and S&L’s, witnessed the highest number of failures since the Great Depression as depicted in Figure 1. Notably, the FDIC and FSLIC underwent contrasting trajectories following the crises. While the FDIC survived the crisis, albeit with depleted insurance funds, the FSLIC faced insolvency by the end of the crisis and was closed in 1989 at a cost of $132 billion to the taxpayer (FDIC, 1998).

When banks and S&Ls failed, the FDIC and FSLIC applied one of the following three resolution methods (Walter, 2004):

-

1.

Type I: Open Bank Assistance (OBA) - Under this resolution method, the regulator provides financial assistance to acquirers toward the purchase of a failing bank or grants direct assistance to the failing bank.

-

2.

Type II: Purchase and Assumption (P&A) - Resolutions under this category consist of acquiring a part of the assets and liabilities of a failed bank by a participating institution.

-

3.

Type III: Deposit Payout (PO) - Under this resolution category, the regulator liquidates the failed institution and pays out its insured depositors from the insurance fund.

Each of the three resolution methods described above involve a progressively more severe breakdown of relationships between the bank and its customers (Ashcraft, 2005). For instance while a Type I resolution method ensures continuity of banking relationships, a Type III resolution terminates all such relationships. We compare the decision rules employed by the FDIC and FSLIC in assigning of the three resolution methods to failed institutions during the crises of 1980’s in addition to assessing their decisions against recommended decision rules from theoretical studies. Our results expose specific weaknesses in the FSLIC’s decision structure and the FDIC’s relative strengths that are likely to have contributed to the former’s failure in 1989 and the latter’s continued survival.

The crises of the 1980’s are particularly suitable for comparing the resolution decisions of FDIC and FSLIC against theoretically recommended state-dependent decision rules for several reasons. First, the simultaneous crises in banking and S&L industries in the 1980’s provided a basis to compare the two regulators, and to identify the stronger of the two approaches to resolving failed institutions. Second, bank and S&L failures in this period occurred against the backdrop of shocks in specific sectors, namely, agriculture, real-estate and energy that resulted in regional crises (FDIC, 1998). For instance, the major sectoral crises that occurred during this period were the recessions following the collapse of energy prices in Texas, Louisiana and Oklahoma, the agricultural recession in Kansas, Iowa and Nebraska and the real-estate-led downturns in California, the Southwest and the Northeast (FDIC, 1997). Third, banks were subject to varying levels of branching restrictions and operated either within state borders or across states that had entered into reciprocal arrangements (Kroszner and Strahan, 1999). Specifically, this period predates the elimination of the interstate branching restrictions mandated by the 1994 Riegle-Neal Interstate Banking and Branching Efficiency Act (Medley, 2013). Thus, the combination of sectoral crises that were regionally contained and branching restrictions that limited the geographic scope of banking markets entailed that certain bank failures occurred amid economic and financial distress, and others, in relatively normal economic conditions. This provided an ideal setting for the two regulators towards implementing the theoretically recommended state-dependent decision rules for resolving failed banks during this crisis.

1.2 Recommended decision rules from theoretical studies and testable hypotheses

In this section we first discuss the decision rules that are recommended by the branches of theoretical literature for the resolution of failed banks under two state-dependent scenarios - economic distress and banking industry distress. Thereafter, we identify the specific testable hypotheses for each of these scenarios as wells as the hypothesis to infer the impact of political influence on regulators’ resolution decisions.

Economic distress and recommended decision rule for bank resolutions - Cordella and

Yeyati (2003) determined a resolution strategy, or a decision rule, in which the regulator provides bailouts to banks if their failure occurred under macroeconomic distress, when bank failures are less likely to have arisen due to their unsound portfolio decisions and more likely to have arisen due to exogenous factors. Correspondingly, in the event of bank failures under normal economic conditions, their theoretical model recommended liquidating such banks.

Hypothesis : The testable hypothesis is that the FDIC and FSLIC applied different decision rules for banks that failed in normal economic conditions and those that failed amid macroeconomic distress. Conditional on the presence of two distinct rules, the subsequent statistical inference centers on testing the hypothesis that the probability of receiving a Type I resolution was higher for banks that failed amid high economic distress relative to those that failed amid low distress.

Banking industry distress and recommended decision rule for bank resolutions - Acharya and

Yorulmazer (2007, 2008) propose resolution strategies for the “too-many-to-fail” problem or, equivalently, the simultaneous failure of many banks. Their recommended decision rule consisted of facilitating acquisitions of failed banks when such failures were small in number but providing bailouts and financial assistance when there were a large number of failures.444Acharya and

Yorulmazer (2007) note that it is optimal for regulators to commit to not assisting failed banks on an ex-ante basis. However, when a large number of banks fail, it becomes optimal to forgo that commitment and assist banks rather than liquidate them. This is the time-inconsistency between regulators’ ex-ante and ex-post decisions.

Hypothesis : The first testable hypothesis is that regulators applied distinct rules in the presence and absence of banking industry distress. Second, the decision rule employed in the presence of banking industry distress designated a higher proportion of resolutions as Type I compared to the rule applied in its absence.

Political influence on regulators’ decision rule for bank resolutions - Several empirical studies (Igan

et al., 2012; Duchin and

Sosyura, 2012) have revealed the evidence of political and lobbying influence on regulators’ decisions for bank resolutions. For instance, DeYoung

et al. (2013) find that when a regulator experiences political pressure to place greater emphasis on maintaining current liquidity, they will provide more bailouts than when the regulator prioritizes the prevention of future moral hazard.

Hypothesis : The primary hypothesis is that the presence of political influence induces a separate decision rule that is distinct from the rule applied in its absence. Subsequently, inferences center on whether the decision rule utilized under political influence resulted in a higher probability of receiving a Type I resolution relative to the rule applied in the absence of political influence.

1.3 Our contributions and connections to existing works

We consider the three hypotheses from Section 1.2 and test for the presence of state-dependent resolution strategies, either recommended by theory or arising from political interference, in the decision rules employed by the FDIC and FSLIC to resolve failed banks and S&Ls during the crises of 1980’s. Our findings reveal that regular assessments of financial regulators by lawmakers and the public can uncover gaps between observed and recommended resolution rules and provide guidelines for corrective actions. For instance, timely assessments of the FSLIC could have revealed that the agency had provided excessive assistance to institutions that failed amid relatively normal economic conditions and to institutions that received political support (Section 5). Interventions based on these assessments could have potentially prevented both, the failure of FSLIC in 1989 and the ensuing costs to the taxpayer. Conversely, the decision structure of the FDIC identified in this paper (Section 4) provides a road-map for newer resolution agencies that face widespread failures from systemic shocks. The ensuing discussion summarizes our main contributions.

-

1.

This paper contributes to the empirical literature examining bank resolution decisions in two ways. First, we statistically evaluate how regulators’ decisions align with recommended decision rules from alternative theoretical models, as well as the extent to which political economy factors interfere with those recommended decisions. Second, and to the best of our knowledge, this is the first article to compare between the decision rules of the FDIC and FSLIC during the simultaneous crises in the banking and S&L industries during the 1980’s.

-

2.

To evaluate the three hypotheses in Section 1.2, we develop a new methodology for assessing regulators in the form of a Bayesian latent class estimation framework for ordered outcomes. The proposed framework detects unobserved heterogeneity in regulators’ resolution decisions based on underlying economic and political conditions. For estimating this model and conducting inference, we design a novel collapsed Gibbs sampler algorithm that provides a technique for efficient sampling from the posterior distribution relative to standard approaches by reducing the autocorrelations across successive draws. Our method provides a statistical framework to compare parameters across the latent classes, and additionally allows for inferences on all estimated quantities of interest, including marginal effects and the probability of class membership.

-

3.

We consider hypothesis and evaluate whether the FDIC and FSLIC provided bailouts to banks or S&L’s that failed amid macroeconomic distress and withheld such assistance for failures in normal economic conditions. Our results reveal that the FSLIC deviated from and the FDIC adhered to this theoretically recommended rule. Specifically, banks that failed amid high economic distress received financial assistance, or bailouts from the FDIC with an average probability of 25% compared to 3% for banks that failed amid low distress. The FSLIC, on the contrary, assigned Type I assistance with probabilities 68% and 70% to the two groups of S&L institutions that did not statistically differ across measures of macroeconomic distress.

-

4.

We examine hypothesis on whether the two regulatory agencies experienced a too-many-to-fail problem and responded to it in the form of a greater reliance on bailouts and financial assistance to acquiring institutions. Our results show that the FDIC’s decision rules aligned with the theoretical rules as the agency provided Type I assistance with a probability of 27% for failures amid economic and banking industry distress and a statistically lower probability of 4% for failures amid low levels of such distress. The FSLIC assigned Type I assistance with probabilities of 76% and 70% among groups of institutions that did not statistically differ by industry and economic distress.

-

5.

We evaluate hypothesis and assess the extent to which political pressures influenced the resolution decisions of the two agencies. Whereas the previous two hypotheses examined the extent to which regulators followed recommended theoretical rules, this assessment examines potential institutional weaknesses. We find that political support for the banking industry played a limited role in the FDIC’s decisions, but a more salient role in the FSLIC’s decisions. Notably, the FSLIC assigned assistance to S&L’s that likely received a higher degree of political support and failed amid lower economic distress at a statistically higher probability of 92% relative to 59% for S&L’s that failed amid low political support and in a climate of higher economic distress.

A rich literature examined the financial costs incurred by the FDIC (Bennett and Unal, 2014; Balla et al., 2015) and the weaknesses of the FSLIC (Kane, 1989; Akerlof et al., 1993; Romer and Weingast, 1991; White, 1991). The empirical results in this paper align with the sources of weaknesses in the FSLIC’s decision structure discussed in previous literature. However, prior literature has not formally assessed both agencies against resolution rules recommended by theoretical models. Relatedly, the decision rules of the two agencies have not been compared with each other. Our paper addresses both these gaps in the literature.

Greene and Hensher (2010) developed a classical method to estimate latent class models with ordered outcomes by way of an Expectation-Maximization algorithm. Heckman and Singer (1984) proposed latent class models as a nonparametric alternative to random coefficients models in addressing unobserved heterogeneity without the problems of “over-parameterization” and excessive sensitivity to distributional assumptions associated with the latter method. Latent class models have since been developed for a range of outcomes including multinomial (Greene and Hensher, 2003; Burda et al., 2008), count (Wang et al., 1998; Wedel et al., 1993; Deb and Trivedi, 1997; Nagin and Land, 1993) and ordered (Greene et al., 2014) responses. These works apply latent class models to study heterogeneity in fields ranging across healthcare, marketing and transportation. Here we provide a new interpretation of latent class models as a tool to assess banking regulators and develop a framework for evaluating regulators in the event of future crises.

1.4 Organization

The rest of the article is organized as follows. In Section 2 we discuss the data used in this article. Section 3 presents the proposed Bayesian latent class estimation framework for evaluating the regulatory decision rules for resolving bank failures against recommended decision rules from theoretical studies. In Section 4 we discuss the results of our analysis pertaining to the FDIC’s resolution decisions while Section 5 is dedicated to analyzing the FSLIC’s resolution decisions. The article concludes with a discussion in Section 6. Additional technical details, numerical results and background information are relegated to the supplementary materials.

2 Data

We examine bank resolutions by the FDIC between 1984 and 1992 and S&L resolutions by the FSLIC from 1984 until the agency’s closure in 1989. The period between 1984 and 1992 is particularly suited to evaluate the decisions of the FDIC since the agency was subject to restrictions in applying Type I resolutions before 1982 and after 555Prior to 1982, the FDIC was restricted to providing assistance to a bank only when the institution’s continued existence was deemed to be essential to the community in which it operated. The Garn-St.Germain Depository Institutions Act of 1982 dropped this essentiality test. After 1993, new legislation prohibited the FDIC from using its funds to provide assistance to failing institutions, particularly if such assistance resulted in benefits to the troubled institution’s shareholders (Walter, 2004). Consequently, the FDIC was authorized to autonomously provide assistance under Type I resolutions during 1984-1992, the time period considered in this study.. The FSLIC, on the contrary, retained this authority from the start of the sample period until its closure in 1989.

The data used in this paper includes variables that can be broadly divided into seven categories that we describe below.

-

1.

Data on resolution methods - the data on resolution methods applied to failed banks and S&L’s are obtained from the Historical Statistics on Banking (HSoB) maintained by the FDIC. The sample consists of 1385 banks, of which there are 118, 1175 and 92 institutions resolved under resolution types I, II and III respectively. There are 389 S&L institutions in the sample of which 270, 104 and 15 institutions underwent resolution methods I, II and III respectively.

-

2.

Bank and S&L-level characteristics - failed banks from the HSoB are matched with call report data from the Federal Reserve Bank of Chicago to obtain information from the financial statements of each institution. We aggregate the call reports by certificate number, which the FDIC uniquely assigns to each head office of depository institutions, and use this identifier to merge the two datasets. To allow for the duration of 90 to 100 days (FDIC, 1998) between the FDIC receiving notification of an institution that is in danger of failing and determining the resolution method, call reports from two quarters prior to the date of failure are used in the study.

The failed S&L institutions in the sample are matched with Thrift Financial Reports as of six months prior to failure from the Research Information System (RIS) of the FDIC. The data on S&L institutions is less extensive than the corresponding bank-level data due to differences in the reporting requirements for banks and S&L’s. Specifically, data on Agricultural loans, Nonperforming loans and Core Deposits are not available for S&L institutions for the period under study.

-

3.

Insurer characteristic - we obtain the year-end data on outstanding balances on the deposit insurance fund of the FDIC from annual reports from the agency’s website666https://www.fdic.gov/about/financial-reports/reports/index.html. The balances on the FSLIC’s insurance fund are obtained from FDIC (1997)777The balances are reported in Table 4.1 of Chapter 4. These balances remain constant across banks and S&L’s, and vary by year. We use this information to calculate the amount of deposit insurance fund as a percentage of total deposit for both FDIC and FSLIC. This characteristic measures the extent of insurance funds available to the two agencies relative to the maximum value of their potential insurance payouts.

-

4.

State characteristics - our data hold several dimensions of information pertaining to the states in which the banks and S&L’s operated. Specifically, the data on quarterly housing starts at the state level have been obtained from IHS Global Insight, the data on annual unemployment at the state level were obtained from the Iowa Community Indicators Program of Iowa State University and the information on branching deregulation laws was collated using the table in Strahan et al. (2003).

-

5.

County characteristics - the data pertaining to county economic characteristics in which the banks and S&L’s operated have been collated from the Bureau of Economic Analysis. These characteristics consist of per capita growth in gross domestic product (GDP) and the share of employment in each sector, which measure the economic output of each county and the importance of each sector to the county’s economy respectively.

-

6.

County-level characteristics of bank distress -county-level statistics on the banking industry are obtained by aggregating bank-level data from the Research Information System (RIS) of the FDIC, which is available starting from 1984.

-

7.

State-level political economy characteristics - Congressional voting data were obtained from the website of GovTrack (https://www.govtrack.us) and converted into state-level percentages of representatives who voted in favor of each bill evaluated in this study. The description of these bills is available in Section A of the supplement.

Table 3 in Section A of the supplement provides a description of the variables available under each of these seven categories. Tables 4 and 5 in Section A provide summary statistics of the data across these seven categories for FDIC and FSLIC resolution decisions, respectively. In these tables, the Texas Ratio for a bank is defined as,

| (1) |

The Texas-Ratio is a measure of distress as it identifies institutions whose capital would be insufficient to absorb losses that could emanate from nonperforming assets.

3 Bayesian latent class estimation framework

In this section, we propose a Bayesian latent class estimation framework for ordinal outcomes to represent the decision rules of FDIC and FSLIC in resolving failed banks and to evaluate these decision rules against recommended rules from theoretical studies.

3.1 Ordering of resolution decisions

We model the primary outcome of interest, the resolution decision of the FDIC and FSLIC, as an ordered variable by specifying the three resolution methods of Section 1.1 as ordered categories. Previous studies have shown that these resolution methods resulted in progressively more severe effects on economic outcomes (Ashcraft, 2005) and on the level of liquidity (DeYoung et al., 2013). In particular, Ashcraft (2005) points out that each of the three resolution categories entail an increasingly severe breakdown of relationships between the bank and its customers. The provision of Type I assistance allows a bank to continue functioning in its present form. A Type II acquisition or purchase results in certain loan and deposit relationships continuing within the acquiring bank’s books. A Type III liquidation and deposit payout results in the termination of all banking relationships. The specification of resolution methods as an ordered outcome variable also allows for a decision structure in which the regulators order banks by their franchise value888A bank’s franchise value is the present discounted value of its future stream of profits and incorporates the value of its customer relationships and resulting informational advantages. and assign Type I resolutions to the most valuable and Type III resolutions to the least valuable banks. Such an ordering of banks and S&Ls by franchise value is consistent with a cost-minimization objective, which was relevant to both FDIC and FSLIC since they were required to preserve their insurance funds by controlling their costs of resolution (FDIC, 2007).

In the following discussion, bank refers to a representative bank or S&L without loss of generality. Let be the resolution method applied on bank where takes values and to denote resolution types I, II and III respectively.

3.2 Latent class model for ordinal outcomes

We use a latent class model to represent state-dependent rules in the two regulators’ decision structure. Figure 2 depicts the structure of the latent class model. The class indicator is introduced into the model to denote assignment of bank into one of the two classes. Within each latent class, the regulator applies a class-specific decision rule on the failed bank to assign it one of the three available resolution methods.

The distinguishing feature of the latent class model is that classes are determined with probability and not deterministically. This feature is relevant to the current problem since the true assignment of banks into distinct classes by regulators is not observable as the data record the final decision made by the regulators but not the rationale that motivated each decision. Specifically, is observed but is not. As a result, the probabilistic assignment of banks into classes addresses the researcher’s uncertainty on class assignments by the regulatory agencies.

Relatedly, the recommended decision rules from theoretical models described in Section 1.2 consisted of state-dependent rules, which entailed heterogeneity in relationships between the outcome and covariates across sub-groups of banks that failed in different states of nature. Moreover, each distinct decision rule recommended by theoretical studies represents a distinct latent class in our hierarchical model. Therefore, the latent class structure permits a direct comparison between theoretical decision rules and the observed decisions of the FDIC and FSLIC.

3.3 Random utility framework

The random utility representation of this model is based on the framework developed by Marschak (1974). We model the regulator’s problem of assigning bank to one of the two latent classes as a binary discrete choice problem with a latent outcome . To apply the random utility representation to this discrete choice problem, we introduce a continuous latent variable , which represents the difference in utilities or value to the regulator from assigning bank to latent class 2 relative to latent class 1. We express as,

| (2) |

where is a dimensional vector of covariates, are parameters and is the error term. Finally, the relationship between the discrete variable and the continuous variable is expressed via the following threshold crossing framework,

The covariates in Equation (2) are determined by the three hypotheses of interest described in Section 1.2. For instance, in testing hypothesis , the covariates consist of economic indicators pertaining to the state and the county in which bank operates, for hypothesis , they contain measures of the banking industry’s health in the county in which bank operates and for hypothesis , the covariates include the percentage of Congressional representatives in banks ’s state who voted for various bills that were favorable to the banking industry.

Within latent class , the regulator’s utility function determines the final resolution method applied on bank where,

| (3) |

Here is the utility that the regulator derives from preserving bank ’s franchise value as discussed in Section 3.1. The dimensional covariate vector consists of bank ’s characteristics that are representative of its financial health and importance, salient among which are its size, the quality of its assets and composition of risky asset classes. Note that in Equation (3), and represent the observable and unobservable components of utility respectively (Train, 2009) for . The relationship between the observed outcome and the latent utility is represented using the following threshold-crossing framework,

| (4) |

The regulator selects a resolution method that preserves more of the bank’s franchise value as crosses a progressively larger threshold. When is below the lowest threshold, , bank loses all its franchise value as the regulator’s utility level corresponds to liquidation under a Type III resolution.

3.4 Likelihood function

The likelihood contribution of bank receiving resolution type is the sum of the likelihood contribution based on each latent class weighted by the marginal probability of belonging to each of the two latent classes,

| (5) |

where is the probability of taking a particular value conditional on belonging to class and is the corresponding probability of bank belonging to class . With in Equation (2) distributed independently as , we obtain the following binary probit representation of the class membership model,

| (6) |

On specifying a distribution for the unobserved component in Equation (3), the probability of taking a particular value conditional on class from Equation (4) is,

| (7) |

In estimating the ordinal outcome model conditional on class membership , we use the identification scheme in which the cut-points and are restricted to 0 and the cut-points and are restricted to 1 (Jeliazkov and Rahman, 2012).This identification restriction eliminates the need for estimating cut-points and allows the scale parameter to be estimated as a free parameter in each latent class. As discussed in Jeliazkov and Rahman (2012) and Greene and Hensher (2010), identification restrictions are required in estimating ordinal models as neither the scale nor the location of the latent variable is identified in this category of models.

3.5 Augmented posterior

The augmented posterior for the parameters and latent variables in this model is obtained by augmenting the likelihood with the latent variables and using the method of Albert and Chib (1993). Denote

Using equations (2)-(7), the resulting expression for the augmented posterior is,

| (8) |

where , takes the value if and otherwise, is the density of a normal distribution with mean and standard deviation for and is the joint probability density function of the prior distribution of the parameters in . We assign a dimensional multivariate normal prior to that has mean and covariance , and an Inverse Gamma prior to with shape parameter and scale parameter . Finally, we assign a dimensional multivariate normal prior to with mean and covariance . Since the priors are independent, their joint density in Equation (8) can be represented as,

where is the density of an Inverse Gamma distribution with shape parameter and scale parameter .

3.6 MCMC algorithm

A standard approach to developing an MCMC algorithm results in a Gibbs sampler that draws from the full conditionals of all parameters as well as the two latent variables and . In this section we present a Collapsed Gibbs sampler (Liu, 1994) which provides an efficient technique for sampling from the posterior distribution relative to standard sampling approaches by reducing autocorrelations across successive draws. Specifically, in our algorithm, we do not have to draw from the conditionals of as we sample for the parameters of the class membership model, , independently of this latent variable. We first present the algorithm for our collapsed Gibbs sampler and then discuss the details underlying each step in the sampler.

Algorithm: Collapsed Gibbs Sampler

-

1.

Sample from the distribution for .

-

2.

Sample from for .

-

3.

Sample from where and .

-

4.

Sample from , where for .

-

5.

Sample from for .

For the following discussion, denote to be the matrix with the vector of -dimensional covariates from Equation (3) in its rows.

Sampling coefficients of the ordinal model - The coefficients of the ordinal model are sampled for the two latent classes, i.e., for from their respective conditional posterior distributions. We have , where

and . Here is the submatrix of that includes those rows of for which and is the number of observations in class which is updated in every MCMC iteration. Similarly, denotes the length subvector of that includes those elements of for which . In this sampling step, the computations involving are efficient as they only require working with matrices of reduced dimension , without having to preserve the full matrix .

Sampling the variance of the ordinal model -

The variances are sampled using the conditionals for , where and

. Here and are retained from the previous step.

Sampling coefficients of the class membership model -

The coefficients of the class membership model are sampled from , marginally of , by using a Metropolis Hastings (MH) step with a tailored proposal distribution. We use a dimensional distribution with location parameter , covariance matrix and degrees of freedom as the tailored proposal distribution where , is the inverse of the negative Hessian of evaluated at and

with

| (9) |

for . This MH step enhances the efficiency of the overall algorithm by circumventing the need for additional data augmentation through the latent variable from Equation (2).

The proposed draw from this proposal is accepted with probability,

where is the density of the tailored proposal distribution and the expression in the display above is proportional to the product of and the prior probability density of .

Sampling the class membership indicator -

The vector of class membership indicators identifies the latent class to which each observation belongs. These indicators are sampled from a Bernoulli distribution by introducing the binary variable , where for and,

The values and are retained from the previous step and are computed using Equation (9).

Sampling the latent variable -

The sampling of continuous latent variables is based on the data augmentation step from Albert and

Chib (1993), resulting in having a truncated normal distribution with mean , variance and truncated between for . The second subscript in is added to establish that the sampling scheme augments just the continuous outcomes associated with the class to which each observation belongs and does not require the augmentation based on the counterfactual latent class. This approach minimizes storage requirements and permits the sampling of the entire vector in one step.

In the Collapsed Gibbs sampler described above, the discrete latent variable is marginalized out of the conditional distribution for . This novel approach to marginalization results in a sharper decline in autocorrelations across successive lags of sample draws. Consequently, the draws from this algorithm are close to independently and identically distributed early in the chain. In Section B of the supplement we consider two simulation settings and demonstrate that the reduction in autocorrelations gained from our collapsed Gibbs sampler is substantial when compared to those from a full Gibbs sampler.

3.7 Estimation of model with values of the ordered outcome

The Bayesian latent class estimation framework developed in Sections 3.1 – 3.6 relies on the ordered outcome variable , the resolution method, taking three values. However, in several practical applications can take values. For instance, consumer ratings of products and credit ratings assigned to firms are ordered outcomes that typically span over five or more categories. In this section, we provide an extension of our latent class model that allows the ordered outcome variable to take values and develop a collapsed Gibbs sampler for posterior inference in that model.

The sampling algorithm is based on the identification scheme used in Section 3.4 where we set and for . In order to ensure that the ordering of the cut-points, namely , is preserved without having to resort to the introduction of computationally intensive constraints into the estimation procedure, the following transformation proposed in Chen and Dey (2000) is used,

We propose a collapsed Gibbs sampler algorithm that uses a MH step to sample and in one block along the lines of the examples provided in Chib and

Jeliazkov (2001). A multivariate normal prior is assigned to that has mean and covariance matrix .

Algorithm: Collapsed Gibbs Sampler for model with cut-points

-

1.

Sample and jointly from for .

-

2.

Sample from for .

-

3.

Sample from for where and .

-

4.

Sample from for and .

-

5.

Sample from for .

Steps (b)–(e) are identical to the algorithm described in Section 3.6. Step (a) of this algorithm is described below.

Sampling coefficients and cut-points of the ordinal model -

Sample by drawing from a tailored proposal distribution. We use a dimensional distribution with location , covariance matrix being the inverse of the negative hessian of the logarithm of the maximand evaluated at and degrees of freedom . Here,

for and

The proposed draw is accepted with probability

where is the density of the tailored proposal distribution.

4 Bank resolutions by the FDIC

This section provides an assessment of the FDIC’s resolution decisions over the period 1984-1992 by evaluating the agency’s decision rules against recommended rules from theoretical studies. We perform this assessment by interpreting the results from the latent class ordinal model developed in Section 3 to test the three hypotheses derived from theoretical studies as summarized in Section 1.2. In Section 4.1 we discuss the results for hypotheses while the results pertaining to hypotheses and are presented in sections G and H of the supplement. The prior distributions that we consider in this analysis are as follows: and for . The hyperparameters for are chosen to result in an uninformative prior with a mean of approximately 0.4 and prior standard deviation of 0.26. The collapsed Gibbs sampler algorithm of Section 3.6 is run for iterations and we use post-burn in samples for posterior inference.

4.1 Regional economic distress and FDIC’s decisions for bank resolutions

The period of this study, 1984-1992, presents a unique set of economic and banking conditions that facilitate the test for presence of the recommended resolution strategy from Cordella and Yeyati (2003) in the FDIC’s decisions. By virtue of the combination of regionally-contained sectoral crises and branching restrictions during this period (see discussion in Section 1.1), the FDIC simultaneously administered both, bank failures that occurred amid high and low economic distress. We find that the FDIC’s responses supported Hypothesis as the agency provided assistance to banks that failed amid economic distress with a higher probability than to banks that failed in low economic distress. Furthermore, our results reveal that within the class of high regional distress, the FDIC targeted assistance to banks with relatively healthy balance sheets that were more likely to recover and operate as going concerns and arranged for the sale or liquidation of the remaining banks.

4.1.1 Class-membership Model

The class membership model is represented in the first level of the decision structure in Figure 2. We perform a Bayesian model comparison, described in Section E of the supplement, to select the specification of the class-membership model that is most decisively supported by the data. The covariates in the resolution type model, the second level of the hierarchy in Figure 2, are constant across all the specifications considered and are discussed in Section 4.1.3.

Table 1 summarizes the covariate effects from the class membership model for four specifications that include indicators of state and county-level economic performance along with controls for institutional features underlying the resolution decision. The expression for the covariate effects are derived in Section D of the supplement. The values of log marginal likelihood reported in the last row of Table 1 point to specification (3) as the selected model as it has the highest posterior odds among the four candidate specifications. This selected specification highlights a statistically important role for state-level unemployment in assigning banks into two different classes. The other covariates that inform the assignment of banks to latent classes are county-level indicators of economic performance along with a control variable for the amount of insurance fund available per dollar of insured deposit in the banking system.

Among alternative specifications considered in Table 1, specifications (1) and (2) of the model entirely consist of state and county-level indicators of economic performance and controls for county-level shares of employment by sector. Note that specification (2) is a more parsimonious setting that is nested within specification (1). Specification (4) augments specification (2) with indicators for the charter status of failed banks since chartering agencies, namely, the OCC for federally chartered banks and state banking departments for state-chartered banks, retain the final authority to enforce closure. The reference group in this class membership model consists of nationally chartered banks that are supervised by the OCC.

In the following discussion, latent class 1 is labeled as the class of failures under “High Regional Distress (HRD)” and latent class 2, as “Low Regional Distress (LRD)”. In the model for class membership in Equation (6), the event of success in the binary probit model (where the latent binary indicator equals 1) is represented by a bank belonging to latent class 2. Therefore, the negative signs associated with unemployment in specification (3) and the positive signs for covariate effects of GDP growth rate and housing starts in Table 1 show that latent class 2 contains banks that failed during periods of low unemployment or periods of relatively low regional economic stress whereas banks that failed amid high regional distress belong to latent class 1. These findings support the first element of hypothesis by confirming that the FDIC distinguished across banks based on economic distress in applying its resolution decisions.

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| State-level characteristics | ||||

| Unemployment | -0.12 (0.06) | -0.11 (0.05) | -0.1 (0.04) | -0.15 (0.08) |

| Housing starts | 0.11 (0.05) | 0.09 (0.05) | 0.05 (0.05) | 0.1 (0.05) |

| County-level characteristics | ||||

| Per capita GDP growth | 0.04 (0.05) | 0.05 (0.05) | 0.04 (0.05) | 0.04 (0.05) |

| Farm, agri, mining | 0.11 (0.09) | 0.07 (0.05) | 0.06 (0.04) | 0.07 (0.05) |

| Manufacturing | 0.03 (0.05) | - | - | - |

| Construction | 0.02 (0.04) | - | - | - |

| Fin Serv Transport | 0 (0.07) | - | - | - |

| Government | 0.04 (0.05) | - | - | - |

| Insurer characteristics | ||||

| Dep. Ins. Fund/ Total Deposits | - | - | -0.05 (0.03) | - |

| Bank-level characteristics | ||||

| State charter Fed member | - | - | - | 0.03 (0.07) |

| State charter non-Fed member | - | - | - | -0.06 (0.05) |

| log Marginal Likelihood | -703.35 | -701.10 | -699.79 | -700.19 |

4.1.2 Heterogeneity in Decision Rules

The results from the second level of the decision structure in Figure 2 show that the average probability of the FDIC assigning a Type I resolution was statistically higher among HRD banks than among LRD banks. These findings confirm that the FDIC’s decisions fully aligned with hypothesis in that the agency was more likely to provide assistance to banks when their failure was accompanied by regional economic distress.

The average probability of each resolution type for the HRD and LRD failures is computed as follows.

| (10) |

where and correspond to the results for the class of HRD and LRD failures respectively and is the index for the post burn-in MCMC draws. The values are computed for each MCMC iteration using Equation (7).

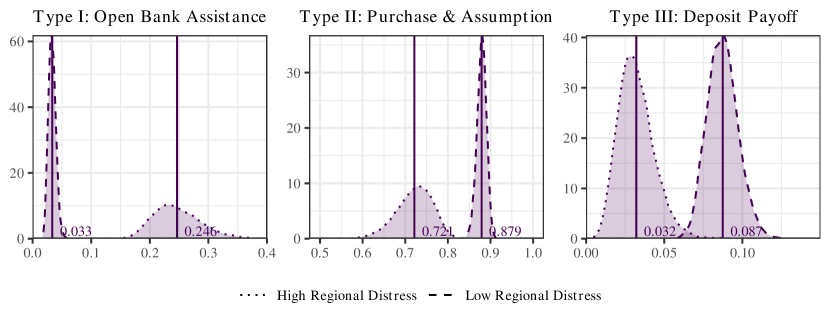

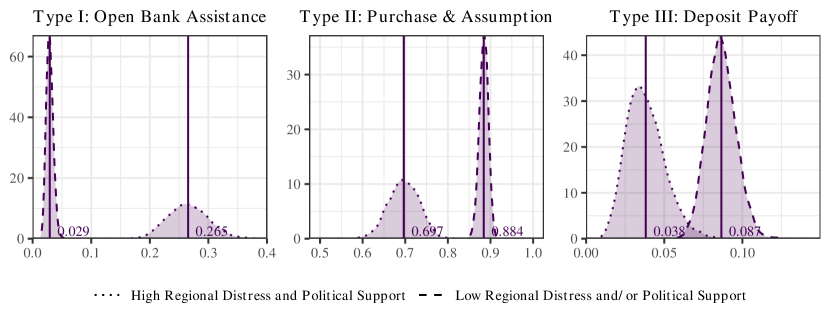

Figure 3 provides the density of the full posterior distribution of the average probability of receiving each resolution method across the two latent classes. The average probability of receiving a Type I resolution among HRD banks was 24.6% compared to 3.3% for LRD banks. The fully disjoint posterior densities of the average probability of receiving a Type I resolution for the HRD and LRD classes shows that the difference between their averages is statistically important. This observation continues to hold for Type II resolutions with statistically important differences in average resolution probabilities across HRD and LRD classes at 72.1% and 87.9% respectively. The theoretical recommendation from Cordella and Yeyati (2003) does not explicitly address the decision to facilitate partial or whole acquisitions of failed banks and the findings from this estimation exercise provide new insights into the differences in the probabilities of implementing the Type II resolution method under varying levels of economic distress. Finally, in a further confirmation of the predictions of the theoretical model, the average probability of being liquidated under a Type III resolution was 8.7% for LRD banks compared to 3.2% for HRD banks. This difference is also statistically important, as evidenced by the minimal overlap in posterior densities of the two classes.

4.1.3 Resolution Type

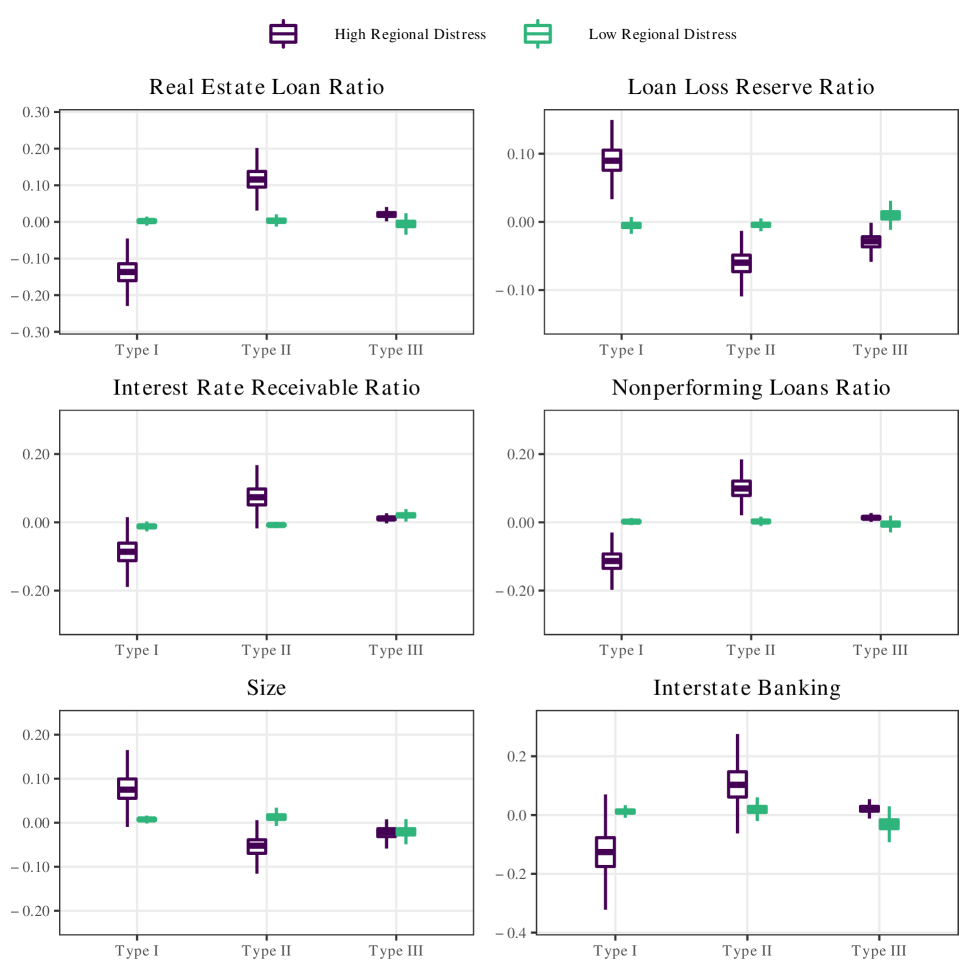

The next stage of the empirical analysis centers on the results from the ordinal probit models represented in Equation (7) and depicted in the second level of the decision structure in Figure 2. These models estimate separate relationships between the resolution method and bank-level financial indicators in the LRD and HRD classes. If the FDIC responded differently to LRD and HRD failures for the same change in bank financial characteristics, this would manifest in different magnitudes of covariates across the two classes and provide conclusive evidence of the presence of two different decision rules implemented by the FDIC. In this section, we report the six largest covariate effects from the selected ordered response model (specification 3 in Table 1) in Figure 4. The covariate effects of the remaining variables are provided in Section F of the supplement.

From Figure 4, the financial variables, Real Estate Loan Ratio and Nonperforming Loans Ratio, both exhibit qualitatively similar covariate effects. A unit standard deviation increase in Real Estate Ratio and Nonperforming Loans Ratio is associated with a reduced probability of obtaining assistance under a Type I resolution among HRD failures and an increased probability of such banks undergoing Type II and III resolutions. Since nonperforming loans provide a succinct measure of the quality of the failed bank’s assets and real estate loans represent a risky asset category, these results reveal that the FDIC provided assistance under Type I to banks that had relatively healthier balance sheets even among those banks that failed amid economic distress, which is consistent with the theoretical recommendations of Cordella and Yeyati (2003). The effects of these covariates on banks within the class of LRD failures, on the other hand, are not statistically important.

The Interest Receivable Ratio is seen to be important in the FDIC’s evaluation of bank health, with elevated levels of this ratio eliciting more stringent resolution methods from the FDIC. Balla et al. (2015) originally identified the Interest Receivable Ratio to be highly predictive of both bank failure and loss subsequent to failure in their study. Accordingly, an increase in Interest Receivable Ratio among HRD failures resulted in a reduction in the probability of Type I resolution and a corresponding increase in the probability of a Type II resolution, entailing partial or whole acquisitions of the failed institutions. Banks that belonged to the LRD class of failures experienced a more severe response in the form of an increased probability of a Type III resolution and hence, complete liquidation, along with a decreased probability of the other two resolution methods.

Larger banks were less likely to be liquidated under a Type III resolution across both latent classes. Among HRD failures, a standard deviation increase in log of assets was also associated with a decreased probability of a Type II resolution and a compensatory increase in the probability of assistance under Type I resolution. LRD failures experienced an increase in the probability of both, Type I and II resolutions concomitantly with a decrease in the probability of a Type III resolution. The increased probability of Type I resolutions associated with a larger bank reveals that the “too-big-to-fail” doctrine was present in the decisions of FDIC during the crisis of the 1980’s.

The estimation results provide new insights into the role of Loan Loss Reserve Ratio, an accounting variable that records the amount of funds set aside to meet expected losses. An increase in Loan Loss Reserves ratio was associated with a higher probability of receiving Type I resolution in the class of HRD failures. Contrarily, among LRD failures, an equivalent increase in this measure was associated with an increase in their probability of receiving a Type III resolution and being liquidated. A possible explanation for this disparity is that in the HRD class of banks, where failures are more likely to have occurred due to systemic factors, changes in loss reserve ratios can be attributed to the deterioration in asset quality resulting from market-wide fluctuations. However, among LRD failures, the FDIC is likely to have viewed the increase in this ratio as a signal of deterioration in asset quality arising from issues idiosyncratic to the failed bank.

Interstate is an indicator variable that identifies whether interstate banking was legal in the state in which a bank is located in the year of failure and is derived from summary tables in Strahan et al. (2003). Intuitively, interstate banking laws are likely to affect resolution outcomes as they determine the breadth of demand for assets of failed banks. For instance, the model in Acharya and Yorulmazer (2008) predicts that interstate banking, by expanding the set of available acquiring banks in the event of a failure, should be associated with an increase in the probability of a Type II resolution and an equivalent decline in the probability of a Type I resolution. In the bottom right panel of Figure 4, an increased probability of Type II resolutions is observed among both, HRD and LRD classes, even though the LRD class of failures also underwent a modest increase in the probability of Type I resolutions.

Overall, Figure 4 reveals that the magnitudes of the covariate effects from the selected model, specification (3), described in the preceding subsection, are larger for banks that belong to the latent class “High Regional Distress (HRD)” relative to banks in the class labeled “Low Regional Distress (LRD)”. This pronounced difference in the effects of each covariate on the FDIC’s decisions across the two classes confirms the presence of two distinct decision rules in the agency’s resolution procedure. The larger covariate effects for banks in the class of HRD failures indicate that within the group of banks that failed amid regional economic distress, the FDIC ordered banks based on their financial characteristics and provided Type I resolutions to relatively healthier banks and Type II and III resolutions to relatively weaker banks. The smaller covariate effects in the LRD class suggest that the FDIC evaluated banks that failed in low economic distress on a case-by-case basis rather than appraising their relative financial strength. This approach potentially included evaluating unobservable individual circumstances, which are captured by the error term in Equation (3). These results reveal a smaller role for observed financial statement information in determining resolution methods within the LRD class relative to the HRD class of banks and further support the hypothesis that banks in the former group are likely to have failed due to largely idiosyncratic factors.

5 Savings and loans resolution by FSLIC

The Federal Savings and Loans Insurance Corporation (FSLIC) insured S&L’s and served as a receiver for failed institutions, both of which were functions the FDIC performed within the banking industry. The FSLIC, however, was ultimately dissolved following unsustainable resolution losses that resulted in its insolvency in 1989. This section compares the decision rules of the FSLIC against theoretically recommended rules summarized in Section 1.2. To compare the FDIC with the FSLIC, we analyze the latter’s decisions through the same empirical lens and estimate the specifications described in Section 4 for FDIC decisions.

In Section 5.1 we discuss the results for hypotheses while the results pertaining to hypotheses and are presented in sections K and L of the supplement. The period under study covers the S&L failures that occurred over 1984-1989. The industry had also undergone an earlier wave of failures in the early 1980’s. Section I in the supplement provides an overview of the history of the crisis in the S&L industry and distinguishes between the two waves of S&L failures. In this analysis, we continue to use the same specifications as those described in Section 4 for the prior distributions, their hyperparameters and the number of post-burn in MCMC samples.

5.1 Regional economic distress and FSLIC’s decisions for S&L resolutions

We find that FSLIC’s designation of S&L institutions into classes based on regional economic distress is ambiguous and does not support Hypothesis . The FSLIC’s decisions deviated from the decision structure implied by Hypothesis in a notable way. The agency did not develop distinct decision rules to resolve failures that occurred amid high and low regional distress and is observed to have adopted a common decision rule for both groups of S&L’s. The implication of using a common decision rule is that institutions that failed due to weaknesses in their own risk management as well as due to economic factors are likely to have received assistance with similar probabilities. The theory underlying this hypothesis suggests that by not fully disentangling economic and idiosyncratic factors while providing assistance, the FSLIC potentially fostered moral hazard among S&L institutions.

5.1.1 Class-membership model

Table 2 summarizes the covariate effects from estimating the specifications reported in Section 4.1.

| (1†) | (2†) | (3†) | (4†) | |

| State-level characteristics | ||||

| Unemployment | -0.08 (0.06) | -0.71 (0.14) | -0.17 (0.48) | -0.72 (0.11) |

| Housing starts | -0.21 (0.1) | -0.01 (0.04) | -0.03 (0.09) | -0.02 (0.04) |

| County-level characteristics | ||||

| Per capita GDP growth | -0.13 (0.09) | 0.02 (0.06) | 0.00 (0.09) | 0.01 (0.05) |

| Farm, agri, mining | -0.09 (0.08) | 0.04 (0.04) | -0.01 (0.09) | 0.04 (0.03) |

| Manufacturing | 0 (0.07) | - | - | - |

| Construction | 0.09 (0.05) | - | - | - |

| Fin Serv Transport | -0.11 (0.12) | - | - | - |

| Government | -0.16 (0.1) | - | - | - |

| Insurer characteristics | ||||

| Dep. Ins. Fund/Total Dep. | - | - | 0.01 (0.08) | - |

| S&L-level characteristics | ||||

| State charter | - | - | - | -0.07 (0.15) |

| log Marginal Likelihood | -302.32 | -305.40 | -302.02 | -305.44 |

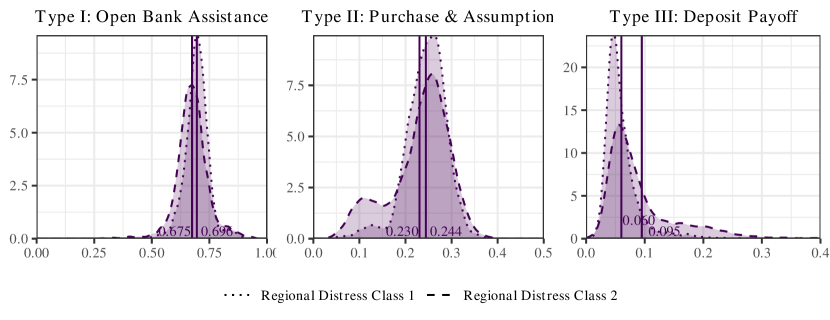

Specification (3†) is determined to be the model selected by the data by virtue of its marginal likelihood being the largest among candidate models. The covariate effects for unemployment, per capita income and housing starts in this specification are, however, not statistically important. Accordingly, the latent classes generated by this model cannot be distinguished as representing “high” or “low” regional distress and are labeled as “Regional Distress Class 1” and “Regional Distress Class 2”.

5.1.2 Heterogeneity in Decision Rules

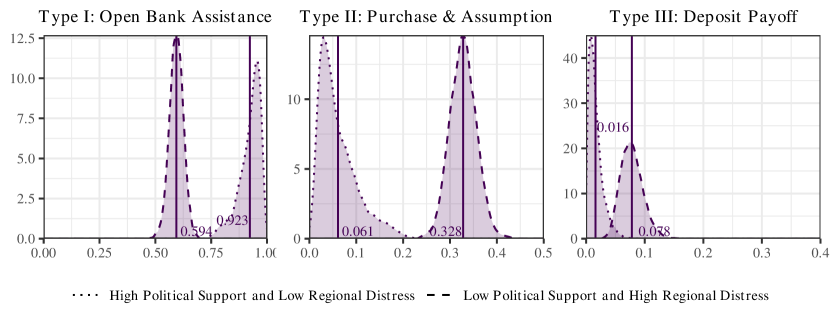

Figure 5 shows the posterior densities of the average probability of the FSLIC assigning each resolution method to S&L’s in the two latent classes. These distributions offer two main insights into the decisions of the FSLIC. First, on comparing with Figure 3, it is clear that the FSLIC relied more heavily on Type I resolutions relative to the FDIC. The average probabilities of the FSLIC assigning a Type I resolution were 67.5 % and 69.6% in class 1 and 2 compared with probabilities of 24.6 % and 3.3% of the FDIC assisting banks that failed in high and low regional distress respectively. Second, the FSLIC recognizably deviated from the recommended resolution strategy developed in Cordella and Yeyati (2003) since the posterior densities for the two classes overlap across all three resolution methods. Accordingly, the average probabilities of receiving a Type I resolution are not statistically different across the two classes. This finding signifies that the FSLIC did not distinguish between S&L institutions that failed amid high and low economic distress in assigning Type I assistance.

5.1.3 Resolution Type

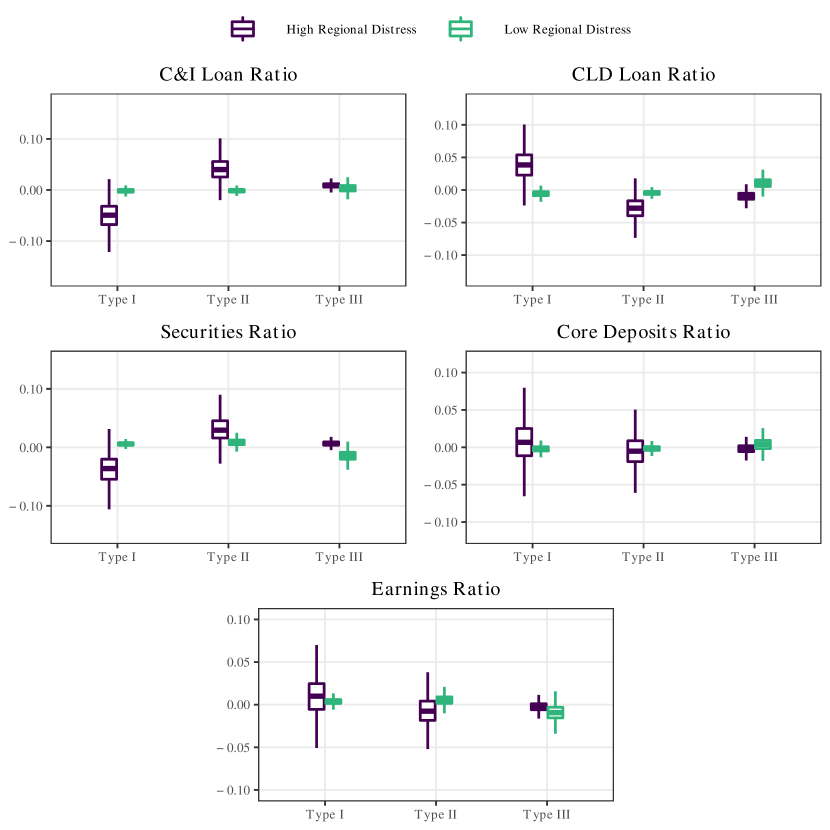

The box plots for covariate effects from specification (3†) in Figure 6 show that the FSLIC adopted a common decision rule in resolving institutions in the two classes. The covariate effects of S&L financial characteristics are homogeneous across the two latent classes. This contrasts with the covariate effects on the FDIC’s responses in Figure 4, which are statistically different across the classes of banks that failed amid high and low regional distress. In both latent classes in the FSLIC’s decision structure, a standard deviation increase in Real Estate Loan Ratio is seen to result in an average decline of around 7% in the probability of receiving a Type I resolution and a corresponding increase in the probability of receiving the other two resolution methods. Since real estate prices collapsed across several regions during this period, institutions with excess concentrations in real estate lending would have been exposed to heightened risks of defaults and losses. Thereby, the FSLIC likely considered such institutions to be incapable of being revived through assistance. Between the two latent classes, the FSLIC responded to Larger Loan Loss Reserve Ratios among institutions in “Regional Distress Class 2” by withholding assistance and instead facilitating their acquisition or liquidating them. This response is similar but more muted in “Regional Distress Class 1”. This suggests that the FSLIC viewed larger loss reserves as a signal of greater deterioration in the asset quality of the failed institution.

The FSLIC did not respond to changes in the Interest Rate Receivable Ratio, which has been shown to be correlated with the losses resulting from the failed institution to the resolution agency (Balla et al., 2015). The average change in the probability of assigning each resolution method is close to zero in response to a standard deviation increase in this measure. This finding suggests that the FSLIC did not distinguish across institutions that held larger or smaller shares of loans on which payments were past due, on which interest accrues and is thereby included in our measure of receivable interest. The FSLIC’s decisions with respect to bank size were similar to those of the FDIC. Larger institutions were more likely to be assisted by the agency and less likely to be sold or liquidated across both latent classes, thereby reflecting the “too-big-to-fail” doctrine in the agency’s decisions. The FSLIC assigned Type I assistance to a greater extent in states where interstate banking was permitted, but this effect was solely present in class 1. Average covariate effects were close to zero for all three resolution types in class 2. The variable “Interstate banking” pertains only to the deregulation within the banking industry as the S&L industry was not subject to such restrictions (Roster, 1985). Since S&L’s would have faced more intense competition from the banking industry in states where interstate banking was permitted, the FSLIC likely provided assistance with greater probability in such states as such competition would have adversely affected even those S&L’s that were healthy. The covariate effects of the remaining variables are provided in Section J of the supplement.

Overall, the FSLIC’s decision rules did not differ by the extent of regional distress that accompanied the failure of S&L’s. Moreover, the covariate effects in the ordinal models for the FSLIC’s decisions on resolution types were lower in magnitude relative to the equivalent values for the FDIC’s decisions. These findings suggest that the FSLIC did not adhere to the recommendation from theoretical studies of assigning S&L’s to distinct decision rules depending on whether the failure was likely related to broader economic factors or the institution’s idiosyncratic weaknesses. In addition, the FSLIC relied on S&L’s financial characteristics to a lesser extent than the FDIC in undertaking resolution decisions, thereby suggesting that the agency assigned resolution methods on a case-by-case basis rather than by adopting a consistent data-driven rule.

6 Discussion and contemporary relevance

During banking crises, financial regulators intervene to bail out certain failed institutions and liquidate others. Regulators are expected to meet the dual objectives of preserving financial stability and discouraging moral hazard in the process of reaching such decisions. However, they may deviate from socially optimal resolution decisions. Furthermore, as bailouts typically entail transfers from taxpayers to bank depositors and equity holders, these actions evoke public disapproval even when they are carried out in the public interest. The risk of regulatory transgressions creates a need for the public to regularly evaluate regulators’ actions. Additionally, in order to mitigate biases in assessments from unduly strong subjective beliefs against public assistance or liquidation, an objective framework of assessment is essential.

An important line of inquiry in assessing the appropriateness of resolution decisions consists of evaluating whether regulatory agencies applied two different decision rules for bank failures amid economic distress and under normal economic conditions. Since the true classification of banks into distinct decision protocols is unobservable, we have developed a Bayesian latent class estimation framework to detect unobserved heterogeneity in the resolution decisions of banks based on underlying economic conditions. This flexible estimation approach permits inferences on whether the decision rules across the latent classes are statistically different. Bayesian model comparison exercises predicated on posterior odds inform the selection of models that best explain the decision rules of regulatory agencies.

We utilize this modeling framework to assess the responses of the FDIC and the FSLIC to bank and S&L failures respectively during the crises of the 1980’s in the two industries. Our results show that the decision rules of the FSLIC, which subsequently faced insolvency at a significant cost to taxpayers, were inconsistent with the decision rules recommended by theoretical studies that address the trade-offs between financial stability and moral hazard. The FDIC, which survived the earlier crisis as well as the financial crisis of 2008, was found to have undertaken decisions that were consistent with those recommended rules. These findings consequently validate the applicability of this approach to assess regulators.

Were there structural differences between the FDIC and FSLIC that contributed to these distinct resolution strategies? First, diluted standards for closing S&L institutions implied that the financial position of S&L’s was more critical than that of banks at the time of failure. Second, deregulation and forbearance resulted in a deeper crisis in the S&L industry than in the banking industry (9% S&L failures relative to 2% bank failures). Following deregulation in the mid-1980’s, S&L’s that previously operated purely within the retail loan and deposit market were permitted entry into the commercial loan market. Despite their entry into a line of business that was historically serviced by banks, capital requirements were lower for S&L’s than they were for banks. This forbearance resulted in the rapid expansion of the S&L industry accompanied by augmented risk-taking, which ultimately led to widespread failures.

A regular assessment of resolution authorities by lawmakers and the public can uncover gaps between observed and recommended resolution rules and also point out the source of such gaps. Assessments of the FSLIC could have revealed the issues arising from deregulation of the S&L industry and prompted a review of the structure of the agency, preventing both, the failure of the agency and the ensuing costs to the taxpayer. The insights from this study can potentially guide the development of resolution strategies among newer resolution agencies such as the Single Resolution Board under the European Central Bank.

References

- Acharya and Yorulmazer (2007) Acharya, V. V. and T. Yorulmazer (2007). Too many to fail - an analysis of time-inconsistency in bank closure policies. Journal of financial intermediation 16(1), 1–31.

- Acharya and Yorulmazer (2008) Acharya, V. V. and T. Yorulmazer (2008). Cash-in-the-market pricing and optimal resolution of bank failures. The Review of Financial Studies 21(6), 2705–2742.

- Akerlof et al. (1993) Akerlof, G. A., P. M. Romer, R. E. Hall, and N. G. Mankiw (1993). Looting: The economic underworld of bankruptcy for profit. Brookings papers on economic activity 1993(2), 1–73.

- Albert and Chib (1993) Albert, J. H. and S. Chib (1993). Bayesian analysis of binary and polychotomous response data. Journal of the American statistical Association 88(422), 669–679.

- Ashcraft (2005) Ashcraft, A. B. (2005). Are banks really special? new evidence from the FDIC-induced failure of healthy banks. American Economic Review 95(5), 1712.

- Balla et al. (2015) Balla, E., E. S. Prescott, and J. R. Walter (2015). Did the financial reforms of the early 1990s fail? a comparison of bank failures and FDIC losses in the 1986-92 and 2007-13 periods.

- Becker (1983) Becker, G. S. (1983). A theory of competition among pressure groups for political influence. The Quarterly Journal of Economics 98(3), 371–400.

- Bennett and Unal (2014) Bennett, R. L. and H. Unal (2014). The effects of resolution methods and industry stress on the loss on assets from bank failures. Journal of Financial Stability 15, 18–31.

- Bernanke et al. (2019) Bernanke, B. S., T. F. Geithner, and H. M. Paulson (2019). Firefighting: The financial crisis and its lessons. Penguin Books.

- Burda et al. (2008) Burda, M., M. Harding, and J. Hausman (2008). A bayesian mixed logit–probit model for multinomial choice. Journal of econometrics 147(2), 232–246.

- Chen and Dey (2000) Chen, M.-H. and D. K. Dey (2000). Bayesian analysis for correlated ordinal data models. Generalized Linear Models: A Bayesian Perspective 5, 133–158.

- Chib (1995) Chib, S. (1995). Marginal likelihood from the gibbs output. Journal of the American Statistical Association 90(432), 1313–1321.

- Chib and Jeliazkov (2001) Chib, S. and I. Jeliazkov (2001). Marginal likelihood from the metropolis–hastings output. Journal of the American Statistical Association 96(453), 270–281.

- Cooke et al. (2015) Cooke, J., C. Koch, and A. Murphy (2015). Liquidity mismatch helps predict bank failure and distress.

- Cordella and Yeyati (2003) Cordella, T. and E. L. Yeyati (2003). Bank bailouts: moral hazard vs. value effect. Journal of Financial intermediation 12(4), 300–330.

- Deb and Trivedi (1997) Deb, P. and P. K. Trivedi (1997). Demand for medical care by the elderly: a finite mixture approach. Journal of applied Econometrics 12(3), 313–336.

- DeYoung et al. (2013) DeYoung, R., M. Kowalik, and J. Reidhill (2013). A theory of failed bank resolution: Technological change and political economics. Journal of Financial Stability 9(4), 612–627.

- Duchin and Sosyura (2012) Duchin, R. and D. Sosyura (2012). The politics of government investment. Journal of Financial Economics 106(1), 24–48.

- Economides et al. (1996) Economides, N., R. G. Hubbard, and D. Palia (1996). The political economy of branching restrictions and deposit insurance: A model of monopolistic competition among small and large banks. The Journal of Law and Economics 39(2), 667–704.

- FDIC (1997) FDIC (1997). History of the Eighties: Lessons for the Future. Federal Deposit Insurance Corporation.

- FDIC (1998) FDIC (1998). Managing the Crisis: The FDIC and RTC Experience. FDIC.

- FDIC (2007) FDIC (2007). Resolutions Handbook. FDIC.

- Freixas and Rochet (2008) Freixas, X. and J.-C. Rochet (2008). Microeconomics of banking. MIT press.

- Greene et al. (2014) Greene, W., M. N. Harris, B. Hollingsworth, and P. Maitra (2014). A latent class model for obesity. Economics Letters 123(1), 1–5.

- Greene and Hensher (2003) Greene, W. H. and D. A. Hensher (2003). A latent class model for discrete choice analysis: contrasts with mixed logit. Transportation Research Part B: Methodological 37(8), 681–698.

- Greene and Hensher (2010) Greene, W. H. and D. A. Hensher (2010). Modeling ordered choices: A primer. Cambridge University Press.

- Heckman and Singer (1984) Heckman, J. and B. Singer (1984). A method for minimizing the impact of distributional assumptions in econometric models for duration data. Econometrica: Journal of the Econometric Society, 271–320.

- Huber (1988) Huber, S. K. (1988). The competitive equality banking act of 1987: An analysis and critical commentary. Banking LJ 105, 284.

- Igan et al. (2012) Igan, D., P. Mishra, and T. Tressel (2012). A fistful of dollars: lobbying and the financial crisis. NBER Macroeconomics Annual 26(1), 195–230.

- Isaac (2010) Isaac, W. M. (2010). Senseless panic: how Washington failed America. John Wiley & Sons.

- Jeliazkov and Rahman (2012) Jeliazkov, I. and M. A. Rahman (2012). Binary and ordinal data analysis in economics: Modeling and estimation. Mathematical modelling with multidisciplinary applications, 123À150.

- Jeliazkov and Vossmeyer (2018) Jeliazkov, I. and A. Vossmeyer (2018). The impact of estimation uncertainty on covariate effects in nonlinear models. Statistical Papers 59(3), 1031–1042.

- Kane (1989) Kane, E. J. (1989). The high cost of incompletely funding the fslic shortage of explicit capital. Journal of Economic Perspectives 3(4), 31–47.

- Kaufman et al. (1981) Kaufman, G. et al. (1981). The depository institutions deregulation and monetary control act of 1980: What has congress wrought? Journal of the Midwest Finance Assocation, 20–35.

- Kroszner and Strahan (1999) Kroszner, R. S. and P. E. Strahan (1999). What drives deregulation? economics and politics of the relaxation of bank branching restrictions. The Quarterly Journal of Economics 114(4), 1437–1467.

- Liu (1994) Liu, J. S. (1994). The collapsed gibbs sampler in bayesian computations with applications to a gene regulation problem. Journal of the American Statistical Association 89(427), 958–966.

- Lowy (1991) Lowy, M. E. (1991). High rollers: Inside the savings and loan debacle. Greenwood Publishing Group.

- Marschak (1974) Marschak, J. (1974). Binary-choice constraints and random utility indicators (1960). In Economic Information, Decision, and Prediction, pp. 218–239. Springer.

- Mason (2004) Mason, D. L. (2004). From buildings and loans to bail-outs: a history of the American savings and loan industry, 1831–1995. Cambridge University Press.

- Medley (2013) Medley, B. (2013). Riegle-neal interstate banking and branching efficiency act of 1994. Federal Reserve History.

- Nagin and Land (1993) Nagin, D. S. and K. C. Land (1993). Age, criminal careers, and population heterogeneity: Specification and estimation of a nonparametric, mixed poisson model. Criminology 31(3), 327–362.

- Papastamoulis (2016) Papastamoulis, P. (2016). label.switching: An R package for dealing with the label switching problem in mcmc outputs. Journal of Statistical Software, Code Snippets 69(1), 1–24.

- Romer and Weingast (1991) Romer, T. and B. R. Weingast (1991). Political foundations of the thrift debacle. In Politics and Economics in the Eighties, pp. 175–214. University of Chicago Press.

- Roster (1985) Roster, M. (1985). The modern role of thrifts. Loy. LAL Rev. 18, 1099.

- Shleifer and Vishny (1992) Shleifer, A. and R. W. Vishny (1992). Liquidation values and debt capacity: A market equilibrium approach. The Journal of Finance 47(4), 1343–1366.

- Siems et al. (2012) Siems, T. F. et al. (2012). The so-called texas ratio. Financial Insights 1(3), 1–3.