A Hawkes model with CARMA(p,q) intensity

Abstract

In this paper we introduce a new model, named CARMA(p,q)-Hawkes, as the Hawkes model with exponential kernel implies a strictly decreasing behaviour of the autocorrelation function while empirical evidences reject its monotonicity. The proposed model is a Hawkes process where the intensity follows a Continuous Time Autoregressive Moving Average (CARMA) process and specifically is able to reproduce more realistic dependence structures. We also study the conditions of stationarity and positivity for the intensity and the strong mixing property for the increments. Furthermore we compute the likelihood, present a simulation method and discuss an estimation approach based on the autocorrelation function.

keywords:

Point processes, Autocorrelation, CARMA , HawkesMSC:

[2022] 37A25, 47N30, 60G551 Introduction

Point processes are useful mathematical models that describe the dynamics of observed event times and have been studied and applied in several fields of study from queueing theory to forestry statistics. Among the family of point processes the Hawkes [1971a, b] process is widely the most established and widespread model in different areas, especially in quantitative finance, actuarial science and seismology (see Ogata 1988 and references therein for further details). Indeed the Hawkes process is particularly interesting since it is a self-exciting process, which means that each arrival excites the intensity such that the probability of the next arrival is increased for some period after the jump, and consequently it is well-suited to investigate, for instance, natural clustering effects and bank default in time. To show the versatility of the Hawkes process we mention a few other possible non-financial and non-insurance applications: a) social science area e.g., Mohler et al. [2011] for the modeling of urban crime and Boumezoued [2016] for the population dynamics; b) social media sector as done in Rizoiu et al. [2017]; and c) the modeling of disease spreading such as COVID-19 transmission as discussed in Chiang et al. [2022].

Recently the Hawkes process has gained a relevant role in financial modeling, in particular in the field of market microstructure. As a matter of fact it is used to model market activity, especially order arrivals in the limit order book [e.g., Bacry et al., 2013, Muni Toke and Yoshida, 2017, Clinet and Yoshida, 2017]. For a complete overview of applications of the Hawkes process in finance, we suggest the works of Bacry et al. [2015] and Hawkes [2018]. The Hawkes process has aroused its appeal among researchers and practitioners as well as in the insurance area. Indeed, as mentioned in Lesage et al. [2022], insurance companies are interested in point processes for the quantification of regulatory capital and in managing risks (e.g., computing ruin probabilities and measuring the effect of cyber-attacks as discussed respectively in Cheng and Seol 2020 and Bessy-Roland et al. 2021). Swishchuk et al. [2021] show that the use of a Hawkes process with exponential kernel for modeling insurance claim occurrences provides an improvement over the fit of a classical Poisson model. However, they are not able to fit different empirical autocorrelation functions as exhibited in Swishchuk et al. [2021, Figures 3 and 5, p. 112].

As stated in Errais et al. [2010], the Hawkes process with exponential kernel is Markovian and shows a good level of tractability that makes it useful for real applications in the presence of large data sets (e.g., high-frequency market data). The specification of the kernel restricts the shape of the time dependence structure of the number of jumps observed in intervals with same length. Indeed, as observed in Da Fonseca and Zaatour [2014], the autocorrelation in a Hawkes model is a decaying function of lags which is not flexible enough to represent the dependence structure observed in many data sets (e.g., wind speed data in which the exponential autocorrelation overshoots the empirical one for small lags and vice versa for large lags as documented in Benth and Rohde 2019; and, as shown in Hitaj et al. 2019, mortality rates where the empirical autocorrelation function of the shock term appears to be non-monotonic).

To overcome the aforementioned drawback, in this paper we introduce a new model named CARMA(p,q)-Hawkes process. The proposed model is a Hawkes process where the intensity follows a Continuous Time Autoregressive Moving Average (CARMA) process and it is able to provide several shapes of the autocorrelation function as it removes the monotonicity constraint detected in the standard Hawkes process. The greater flexibility relies on the CARMA(p,q) component of our model, especially in the choice of the autoregressive and moving average parameters. The CARMA process has been introduced in Doob [1944] and it is the continuous time version of the ARMA model. The advantage of the CARMA process, other than to design different shapes of autocorrelation functions, is to handle better irregular time series with respect to the ARMA process, especially for high-frequency market data, as discussed in Marquardt and Stelzer [2007] and Tómasson [2015]. As a matter of fact, the CARMA model has found many applications in the literature. Here, we list a few of these applications: a) Andresen et al. [2014] use a CARMA(p,q) model for short and forward interest rates, while b) Hitaj et al. [2019] employ such a model in order to capture the dynamics of the shock term in mortality modeling; c) Benth et al. [2014] consider a non-Gaussian CARMA process for the dynamics of spot and derivative prices in electricity markets; and d) Mercuri et al. [2021] provide formulas for the futures term structure and options written on futures in the framework of a CARMA(p,q) model driven by a time-changed Brownian motion. As remarked in Iacus and Mercuri [2015], CARMA models have manifold interests: they can be used to describe directly the dynamics of time series and to construct the variance process in continuous time models (see Brockwell et al. 2006 and Iacus et al. 2017, 2018 for further details). Our paper presents a different type of application as we use CARMA(p,q) models for the intensity of a point process.

In this paper, after reviewing the basic notions of the Hawkes and the CARMA processes, we introduce the CARMA(p,q)-Hawkes process and study the conditions of stationarity and positivity for the intensity, the autocorrelation function of the process and prove the strong mixing property of increments that leads us to the asymptotic distribution of the empirical autocorrelation function.

The remainder of the paper is organized as follows. Section 2 reviews the Hawkes process with exponential kernel while Section 3 presents the CARMA(p,q) model in the Lévy setting. Section 4 introduces the CARMA(p,q)-Hawkes process. Section 5 focuses on the autocorrelation function of the jumps in the proposed model and its asymptotic distribution, while Section 6 presents a simulation and an estimation exercise. Section 7 concludes the paper.

2 The Hawkes Process

Point processes are useful to describe the dynamics of observed event times, i.e., a collection of realizations , for with of the non-decreasing non-negative process called the time arrival process. The counting process , representing the number of events up to time , is obtained from the time arrival process as follows:

| (1) |

for with associated filtration that contains the information of the counting process up to time . An important quantity when dealing with a point process is the conditional intensity defined as:

It then follows that the counting process satisfies the following properties

The conditional intensity of a general self-exciting process has the following form:

| (2) |

with baseline intensity parameter and (excitation) kernel function that represents the contribution to the intensity at time that is made by an event occurred at a previous time . Following the general results about the Hawkes process in Brémaud and Massoulié [1996], the stationary condition reads:

| (3) |

The most used kernel is the exponential function and specifically with . The stationary condition in (3) implies while to prove the Markovianity of the couple it is enough to rewrite the intensity for any as

Observing that , thus

| (4) |

From (4) we have that the distribution of the intensity given the information at time depends only upon and on the increments of the counting process over the interval , which depend on the conditional intensity itself implying that the couple is itself Markovian. The intensity is the solution of the following differential equation:

Exploiting the Markovianity of the process , it is possible to get the infinitesimal generator (see Errais et al. 2010 and Da Fonseca and Zaatour 2014 for further details) associated to a function with continuous partial derivatives with respect to the first argument . Starting from the definition of the infinitesimal operator for a Markov process , that is:

Errais et al. [2010] compute the infinitesimal generator for the Hawkes process with exponential kernel that reads

| (5) |

For every function in the domain of the infinitesimal generator it is possible to build a martingale process with respect to the natural filtration in the following way:

that leads to the well-known Dynkin’s formula

The above formula for has been used in Da Fonseca and Zaatour [2014] to compute the moments and the autocovariance function of jump increments observed in intervals of length with lag .

Proposition 1.

Consider four time instants , , and , the following equalities for the Hawkes model are obtained (see Da Fonseca and Zaatour 2014 for further details).

-

1.

The long-run expected value of the number of jumps during an interval of length is

(6) -

2.

The long-run variance of the increments reads

-

3.

The long-run covariance of the number of arrivals for two non-overlapping intervals of length with lag is

(8) -

4.

The long-run autocorrelation function of the number of jumps over intervals of length separated by a time lag of reads

(9) and is always positive for (stationarity condition) and exponentially decaying with the lag .

From (8) and (9) it is clear that the Hawkes model with exponential kernel can reproduce only strictly decreasing autocorrelation functions for varying lag values . An interesting extension is given in Boswijk et al. [2018] where self-excitation is identified through the modeling of common jumps between the log price process and its own jump intensity.

3 Lévy CARMA(p,q) models

The formal definition of a Lévy CARMA(p,q) model with is based on the continuous version of the state-space representation of an autoregressive moving average ARMA(p,q) model. In particular we have that

| (10) |

where satisfies the following stochastic differential equation

| (11) |

and is a Lévy process. The matrix has the following form

| (12) |

and the vectors and are defined as follows

| (13) |

| (14) |

with . Given a starting value for , the solution of (11) is

where .

As reported in Brockwell et al. [2011, Section 2, p. 251], under the assumption that ensures the stationarity of (i.e., all eigenvalues of matrix are distinct with negative real part111The eigenvalues are sorted based on their real part in an increasing order.), the CARMA(p,q) model can be written as a summation of a finite number of continuous autoregressive models of order 1, which are also known as CAR(1) models. Specifically,

| (15) |

where and the polynomials and are defined as

Note that is the first derivative of the polynomial .

Remark 1.

The eigenvalues of matrix denoted by are the same as the zeros of the autoregressive polynomial . As observed in Tsai and Chan [2005], the assumption that the zeros of have negative real parts is a necessary condition for the stationarity of the CARMA(p,q) process .

Definition 1.

A stationary CARMA(p,q) process where is a second-order subordinator can be equivalently defined as:

where the function is the kernel of the CARMA(p,q) process. As is independent of , , the process is said to be a casual function of the subordinator , also known as casual CARMA(p,q) model.

In Brockwell and Marquardt [2005] it is shown that the function can be written as

| (16) |

The positivity conditions for the kernel and for the process itself, which is for instance required for modeling the volatility using CARMA(p,q) models, have been deeply investigated in Tsai and Chan [2005] and in Benth and Rohde [2019] for the case of positive subordinators.

4 CARMA(p,q)-Hawkes model

In this section, we introduce a point process where the intensity follows a CARMA(p,q) process that is a generalization of the Hawkes process with an exponential kernel.

4.1 CARMA(p,q)-Hawkes: stationarity and positivity conditions for the intensity

Definition 2.

A vector process of dimension is a CARMA(p,q)-Hawkes process if the conditional intensity of the counting process is a CARMA(p,q) process driven by and has the following form:

| (17) |

in which the baseline parameter is strictly positive and the vector is defined as in (14). The vector satisfies the linear stochastic differential equation

| (18) |

where the companion matrix and the vector have respectively the form in (12) and (13).

The dynamics of the state space process in (18) is described through a linear stochastic differential equation and it is a Markov process. Consequently, a CARMA(p,q)-Hawkes process is in turn a Markov process.

Remark 2.

The stochastic differential equation in (18) has an analytical solution given the initial condition, that is

| (19) |

The non-decreasing and non-negative trajectories of the counting process imply the positiveness of for non-negative kernel functions.

To investigate the stationary regime of a CARMA(p,q)-Hawkes model, it is necessary to determine the conditions required for a non-negative kernel, i.e., . In case of a CARMA(p,q) driven by a non-negative Lévy process the conditions of a non-negative kernel are presented in Tsai and Chan [2005, Theorem 1, p. 592]. In a similar fashion such conditions can be applied directly to our case due to the non-negative trajectories of the counting process . Indeed, as done in Brockwell et al. [2006, Theorem 5.2] for COGARCH(p,q) models, we rephrase their results for a generic CARMA(p,q)-Hawkes process when in the next proposition.

Proposition 2.

-

(a)

For a CARMA(p,q)-Hawkes process such that the real part of all eigenvalues of is negative, the kernel function is non-negative if and only if the ratio function is completely monotone222A function defined on is said to be completely monotone if and only it has derivatives of all orders and for . on .

-

(b)

A sufficient condition for the kernel function of a CAR(p)-Hawkes process to be non-negative is that all eigenvalues of are real and negative.

-

(c)

A sufficient condition for the kernel function of a CAR(p)-Hawkes process to be non-negative is that if is a partition of the set of all pairs of complex conjugate eigenvalues of (counted with multiplicity), then there exists an injective mapping such that real eigenvalue of satisfies .

-

(d)

For a non-negative kernel in a CAR(p)-Hawkes process, it is necessary to find a real eigenvalue such that where with .

-

(e)

Suppose all eigenvalues of are negative real numbers sorted as follows and that all the roots of are negative real numbers such that . If for , then the kernel of a CARMA(p,q)-Hawkes process is non-negative.

-

(f)

A necessary and sufficient condition for a non-negative in a CARMA(2,1)-Hawkes process is that and with .

We remark that the non-negativity requirement for the kernel implies a strictly positive intensity process as the baseline parameter is strictly positive.

Without loss of generality, we assume that matrix is diagonalizable which corresponds to the assumption that the eigenvalues of are distinct. The eigenvectors of are

used to define a matrix as

It follows that satisfies , a result used to prove the next proposition on the stationarity conditions for a CARMA(p,q)-Hawkes process.

Proposition 3.

Let us consider a non-negative kernel function and suppose . Then a CARMA(p,q)-Hawkes is a stationary process if all eigenvalues of are distinct with non-negative real part and .

Proof.

For a non-negative kernel function, the stationary condition in (3) for a CARMA(p,q)-Hawkes process becomes

| (20) |

where is the identity matrix with dimension . As is diagonalizable,

where . Thus the limit in (20) is

Recalling that all eigenvalues of have negative real part, we notice that tends to a zero matrix. The integral in (20) becomes

| (21) |

The stationarity condition in (3) implies . ∎

Assumption 1.

We shall assume for the remainder of the paper that: i) the kernel is a non-negative function and ; and ii) all eigenvalues of are distinct with negative real part and .

For practical applications, instead of checking ex-post signs of eigenvalues of matrix , it is possible to enforce ex-ante the negativity of the real part for eigenvalues using some transformations on the parameters space as done, for example, in Tómasson [2015]. As a CARMA(p,q)-Hawkes process is Markovian, we are able to calculate the infinitesimal operator as described in the following proposition.

Proposition 4.

Let be a function with continuous partial derivatives with respect to the first arguments. Under the same conditions in Assumption 1, the infinitesimal generator of function for a CARMA(p,q)-Hawkes process is:

| (22) | |||||

where is the -th row of the companion matrix and the intensity process is defined as in (17). Alternatively, the infinitesimal generator can be written as

| (23) |

where .

Proof.

Let us consider two cases. If , the vector becomes where means no jump (NJ) occurred in the interval and can be written in the following way

as the quantity is zero due to the absence of jumps in the interval . From

we have that

| (24) |

If then is computed as

Defining the jump time in the time interval we get

As , we observe that

| (25) |

Note that and consider the following quantity:

The infinitesimal generator is:

| (26) | |||||

To compute the limit (26) we use De l’Hôpital’s rule

| (27) | |||||

and substituting (27) in (26), we finally obtain the result in (23). ∎

The conditional expected value for can be computed applying the Dynkin’s formula:

| (28) |

that has a representation of the following form

| (29) |

with initial condition . We use the infinitesimal generator (23) and the result in (28) to obtain the following proposition for the computation of the first moment of the counting process . In the remainder of the paper, we use .

Proposition 5.

Let be a companion matrix where the last row has the following structure

| (30) |

Under Assumption 1 and supposing that all eigenvalues of are distinct with negative real part, for any , the conditional first moment of the counting process is

| (31) |

while the conditional expected value of the state process is

| (32) |

The quantities in (31) and (32) satisfy respectively the following ordinary differential equations:

| (33) |

and

| (34) |

with initial conditions333For , then and

. and . The long-run value for is obtained as follows

| (35) |

Moreover, the expected number of events that occurs in an interval with length , i.e., , given the information at time is

| (36) |

and the stationary behaviour of (36) is

| (37) |

Proof.

To determine the expected number of jumps in (31) we obtain first the infinitesimal generator of the function , that is where the conditional intensity is defined in (18). Applying the Dynkin’s formula in (29) we obtain the following ODE

| (38) |

Then, we compute that requires a system of infinitesimal generators. In particular, for , we have

and

Applying (29), we get

| (39) |

where is defined in (30). With the initial condition , the solution of the system in (39) is (32). Substituting (32) in (38) we obtain the following ODE for the expected number of jumps

whose solution is in (31) with initial condition . Using the result in (31) we observe by straightforward calculations that the expected number of jumps in an interval of length reads as in (36). Due to the negativity assumption for the real part of the eigenvalues of matrix , we obtain the asymptotic behaviour in (35) and (37) as where is a zero matrix (see (82)). ∎

Using the same arguments in Brockwell et al. [2006, proof of Proposition 4.1, p. 815] , all eigenvalues of matrix have negative real parts if for some positive integer the following inequality holds

| (40) |

where, in this context, denotes the natural matrix norm induced by the vector -norm. This result comes directly from an application of the Bauer-Fike Theorem (see Bauer and Fike 1960 for further details) since is obtained by perturbing matrix as .

A sufficient condition for (40) is

| (41) |

where is the Euclidean norm of , and are maximal and minimal singular values of . In particular, we observe that

| (42) |

and that , the condition number in 2-norm, can be written as

| (43) |

Moreover, denoting with the Frobenius norm of , we obtain . Applying the definition of the Frobenius norm we have

| (44) |

and combining (42), (43) and (44) we get

| (45) |

4.2 Simulation and Likelihood Estimation of the CARMA(p,q)-Hawkes

We propose a simulation method for the CARMA(p,q)-Hawkes model following the same idea presented in Ozaki [1979, Section 4, p. 148].

Suppose that , which correspond to time arrivals, are already observed. Then it is possible to simulate the next time arrival by generating a random number from a standard uniform distribution, i.e., , and by solving this equation with respect to :

| (46) |

The conditional intensity can be replaced by (17) and can be substituted by (19) obtaining so

| (47) |

Developing and rearranging the right-hand side of (47) we have

where the integral in the second equality is computed using the results in (76). Defining , we finally get

| (48) |

The quantity can be obtained recursively as follows

Note that a similar recursive expression has been obtained in Ozaki [1979] for a Hawkes process with exponential kernel.

As follows we present the likelihood of a CARMA(p,q)-Hawkes model. Consider that , then the likelihood of a CARMA(p,q)-Hawkes model is given by

| (49) |

Exploiting the fact that , then (49) can be written as

| (50) |

and recalling once again that can be expressed by (19) and rearranging the expression we have

| (51) |

Working on the inner integral, the likelihood becomes

| (52) |

while using the results in (76) we get

| (53) |

Developing the integral in (53) and recalling that , we finally obtain that the likelihood of a CARMA(p,q)-Hawkes model writes

| (54) |

5 Autocovariance and Autocorrelation of a CARMA(p,q)-Hawkes process

In this section we compute the stationary autocorrelation and autocovariance functions for the number of jumps in non-overlapping time intervals of length . To this aim we introduce some quantities that are useful to compute the asymptotic covariance of a CARMA(p,q)-Hawkes process.

The first quantity we introduce is the matrix defined as follows

| (55) |

where the square matrices , , have the following structure

with . Matrices for and are characterized by the entries with the form

while matrices for have form

Here an example of the matrix for a CARMA(3,2)-Hawkes model

The second quantity introduced is the matrix defined as:

| (56) |

where the generic -th row is the result of a row concatenation of vectors with dimensions , , , , , respectively. The first vectors have zero entries except the element in position that coincides with , the vector with dimension contains the elements and the remaining vectors have zero entries.

For example, in the case of a CARMA(3,2)-Hawkes model, the structure of matrix reads

The third quantity is the matrix in which the entry in the th row and in th column has the following structure

| (58) |

Let be a vector. Then we define the operator as a function that transforms the matrix into a vector containing the lower triangular part of the product . Specifically:

| (59) |

5.1 Conditions for existence of stationary autocovariance function

We rewrite the quantity using the operator defined in (59).

Lemma 1.

Proof.

Using the definition of matrix in (56), the identity in (60) is straightforward. To show the result in (61), we need first to compute the infinitesimal generator for each component of . From the definition in (59) we identify blocks where the dimension of each block decreases by one unit. More precisely, the th block has elements. Considering the first block (i.e., ) we have infinitesimal generators obtained applying the result in (22) of Proposition 4. For the first element in the first block, we have . While for the th element in the first block with we get and finally

For a generic th block, we get infinitesimal generators. In particular for we have . For we have and

The last block contains only one infinitesimal generator of the form

Using the Dynkin’s formula in (29) we obtain the following system of linear ODE’s:

| (62) |

where the vector is composed of zero entries except the last position where the element is one; and are defined in (55) and (58) respectively.

The first step is to solve the ODE defined in (62) whose solution has the following form

| (63) | |||||

We also observe that

| (64) | |||||

D contains the proofs of the following two propositions on the variance and covariance of the number of jumps that occur in two non-overlapping time intervals of the same length for a CARMA(p,q)-Hawkes model.

Proposition 6.

Proposition 7.

5.2 Strong mixing property for the increments of a CARMA(p,q)-Hawkes and asymptotic distribution of the autocorrelation function

The asymptotic distribution of the autocorrelation function of a CARMA(p,q)-Hawkes process can be easily obtained if we show that the increments of the process are strongly mixing.

Definition 3.

Let be a probability space and two sub algebras of . The strong-mixing coefficient is defined as:

| (70) |

Following Poinas et al. [2019], the quantity in (70) can be reformulated for a point process in the following way:

| (71) |

where denotes the algebra generated by the cylinder sets on the interval 444 Let be a counting process defined as a map from a probability space to a measurable space of locally finite counting measures on . Then the algebra is defined as: . Considering the sequence where is the number of jumps in the interval of length 1 and extremes , , the strong-mixing coefficient has the form

| (72) |

where is the algebra generated by the sequence . If (respectively ) as , the point process (respectively ) is said to be strongly-mixing.

Using Theorem 1 in Cheysson and Lang [2020], we obtain the following proposition.

Proposition 8.

A CARMA(p,q)-Hawkes process satisfying Assumption 1 is strongly mixing with exponential rate.

Proof.

We first prove the existence of a positive constant such that the kernel function satisfies the condition

| (73) |

We notice that Assumption 1 implies that

Choosing the condition in (73) is ensured and thus we can apply the result in Theorem 1 proved by Cheysson and Lang [2020], and the strong-mixing coefficient results to be where . ∎

As shown in Cheysson and Lang [2020], we have that and the result in Proposition 8 implies that the sequence is strongly mixing. This result is useful to determine the asymptotic distribution of the sample autocovariance and autocorrelation functions associated to the sequence . Following the result in Ibragimov and Linnik [1971], we obtain the following result for the asymptotic distribution of the sample mean, the sample variance and the sample autocovariance function.

Proposition 9.

Let be a stationary CARMA(p,q)-Hawkes process that satisfies the assumptions in Proposition 8. We assume the existence of a positive constant such that . Denoting with

as , we have:

| (74) |

where and

| (75) |

Proof.

The proof is quite standard and is an application of Theorem 18.5.3 in Ibragimov and Linnik [1971] and Cramér-Wold device. Denoting with

we apply Theorem 18.5.3 in Ibragimov and Linnik [1971] to the linear combination where is a generic real vector such that . Since the strong mixing property is preserved under linear transformations as well as the rate we have

that is

Applying Cramér-Wold device we obtain the asymptotic behavior in (74). ∎

Applying the Delta method, it is possible to use the result in Proposition 9 to obtain the asymptotic distribution of the autocorrelation function.

6 Application to simulated series

This section examines the time series of the counting process generated by the simulation of two different stochastic processes: the standard Hawkes process and the CARMA(3,1)-Hawkes process. We show the behaviour of the autocorrelation function and its confidence interval obtained applying the results of Subsection 5.2. Furthermore, we investigate the estimation of parameters by means of the Maximum Likelihood Estimation (MLE) method described in Subsection 4.2 and the Moment Matching Estimation (MME) method which we describe below.

Consider a sequence of empirical observations for the increments of a counting process , then the MME method is composed of two steps. The first step is to compute the least squares estimator:

where is a subset of such that the stationary condition is guaranteed, the kernel function is non-negative defined and higher order moments of a CARMA(p,q)-Hawkes process exist. For a fixed , is defined as:

in which denotes the lag order, represents a vector containing the empirical autocorrelations and is a vector of theoretical autocorrelations described in Section 5. The vector includes only the autoregressive () and moving average () parameters. Once obtained the autoregressive and moving average parameters, the parameter can be estimated, which corresponds to the second step, from Equation (37) using the empirical first moment of with .

Note that all chosen parameters for the Hawkes process and the CARMA(3,1)-Hawkes process ensure two conditions: the stationarity of the process (see Section 2) and the existence of the asymptotic autocorrelation function (see Section 5).

6.1 The Hawkes process

We simulate the Hawkes process with the following parameters: , and . For the sake of clarity, we recall that the Hawkes process can be seen also as a CAR(1)-Hawkes process as mentioned in the Remark 3.

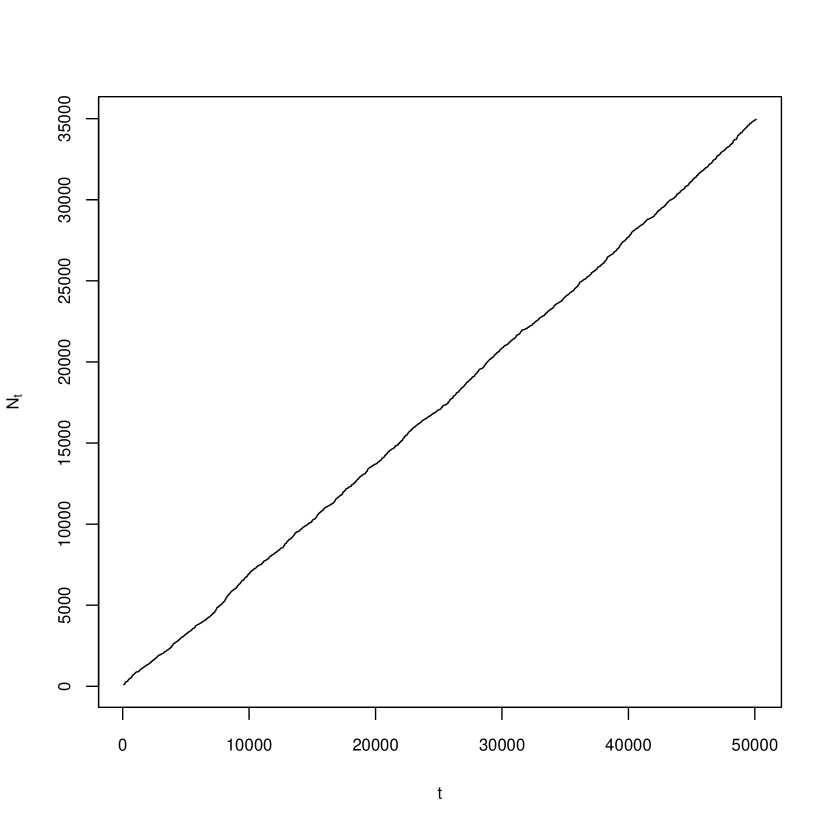

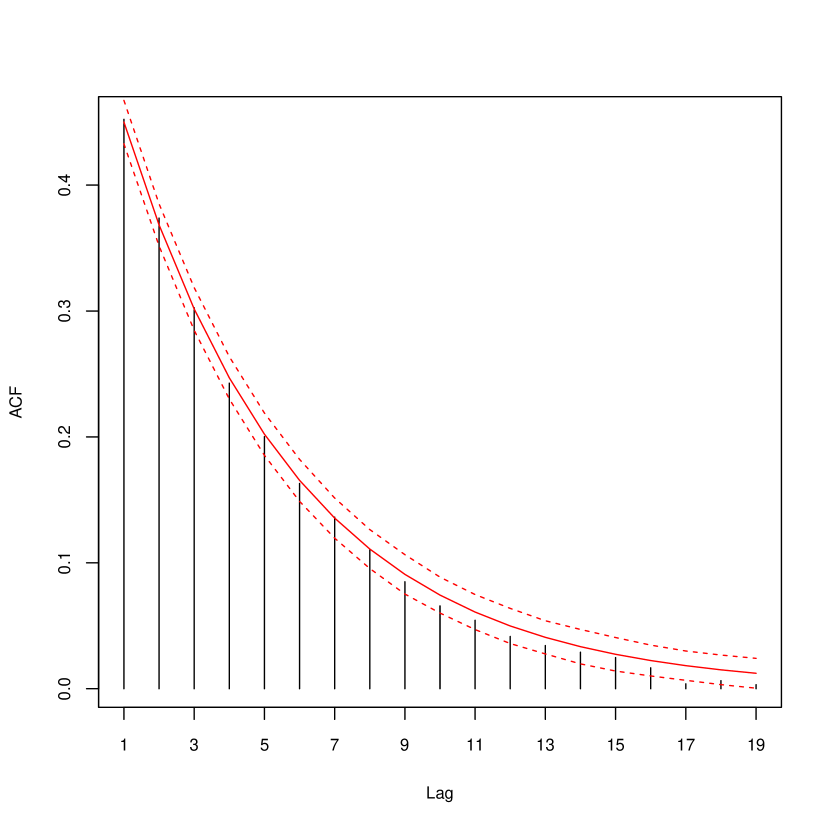

Figure 1(a) shows a simulated trajectory of the counting process , while Figure 1(b) exhibits the autocorrelation function at different lags. From Figure 1(b) we observe that all empirical autocorrelations belong to the 95% confidence interval and, as expected, the ACF depicts an exponential monotonic decay (decreasing) behaviour which is typical of the Hawkes processes.

Table 1 exhibits the MLE estimates for the parameters and the number of occurred events for different levels of final time , whereas Table 2 shows the estimated parameters using the MME method.

| 0.2101 | 0.7270 | 0.4883 | 3199 | 5000 |

| 0.2014 | 0.7389 | 0.5211 | 10240 | 15000 |

| 0.1987 | 0.7054 | 0.4997 | 17042 | 25000 |

| 0.2011 | 0.7028 | 0.5004 | 34914 | 50000 |

| 0.2440 | 0.7540 | 0.4877 | 5000 |

| 0.2121 | 0.7127 | 0.4954 | 15000 |

| 0.2044 | 0.7016 | 0.4951 | 25000 |

| 0.1992 | 0.7042 | 0.4990 | 50000 |

6.2 CARMA(3,1)-Hawkes process

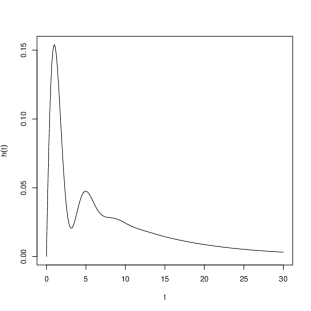

We simulate the counting process using a CARMA(3,1)-Hawkes model with the following parameters: , , , , and . This set of parameters ensures the stationary conditions since and the largest eigenvalue of is . We can easily verify the condition for the existence of in (37). Indeed, the real part of the largest eigenvalue of is negative . Moreover, it is possible to verify that all eigenvalues of have negative real part, thus the long-run autocorrelation function exists (the real part of the largest eigenvalue of is ). In order to analyze the nonnegativity of the kernel , Figure 2 presents the behaviour of with . From (16) the tail behaviour of is proportional to (i.e., as ).

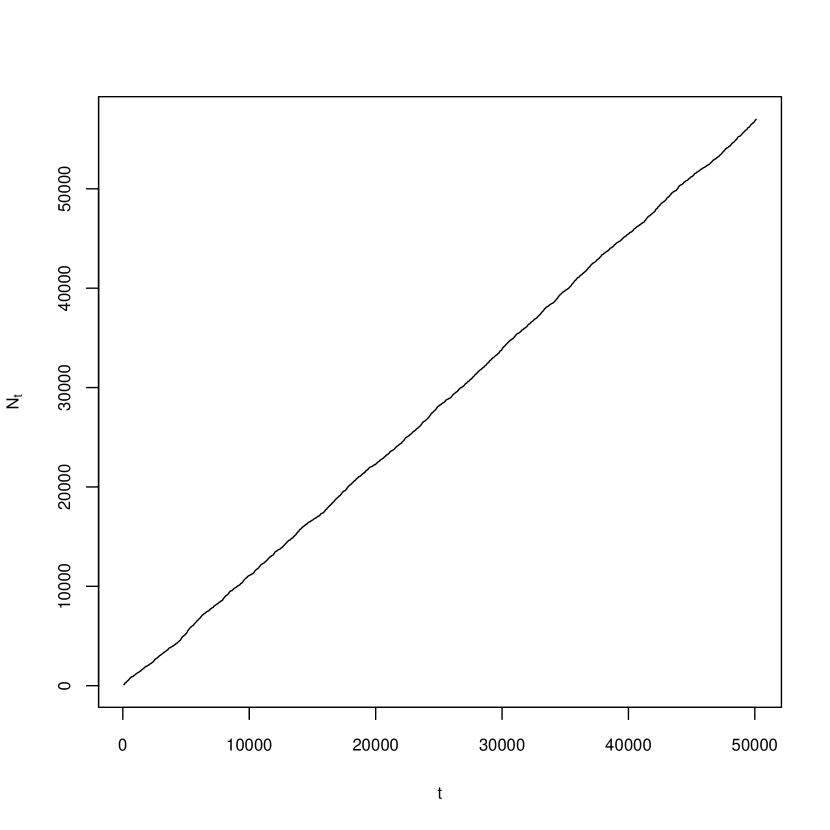

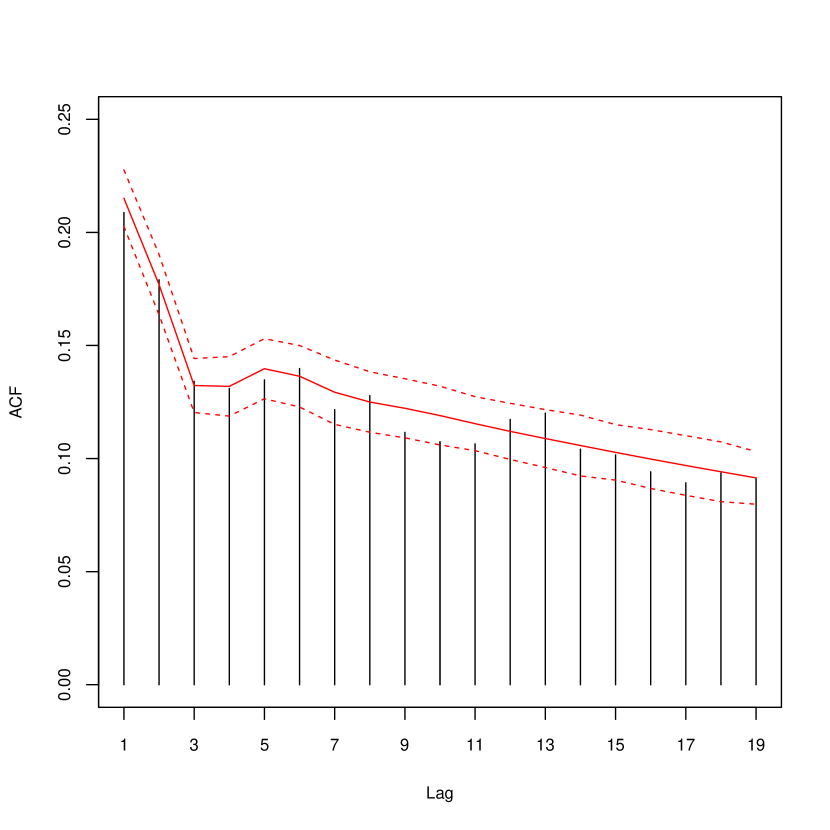

Figure 3(a) exhibits a simulated trajectory of the counting process , while Figure 3(b) displays the ACF at different lags. Figure 3(b) is a clear example of the fact that a CARMA(3,1)-Hawkes process can accommodate different shapes of autocorrelation structures rather than an exponential monotonic decay behaviour as it is the case of a standard Hawkes process.

Table 3 shows the estimated parameters obtained using the MLE method and the number of occurred events for different levels of final time , whereas Table 4 exhibits the estimated parameters using the MME method for different levels of final time .

| T | |||||||

|---|---|---|---|---|---|---|---|

| 0.3166 | 1.5372 | 2.8565 | 0.2869 | 0.2011 | 0.3345 | 5229 | 5000 |

| 0.3063 | 1.3521 | 2.6686 | 0.2758 | 0.1998 | 0.3023 | 16666 | 15000 |

| 0.3068 | 1.0811 | 2.4380 | 0.2480 | 0.1808 | 0.2508 | 28154 | 25000 |

| 0.2949 | 1.4177 | 2.6901 | 0.2550 | 0.1889 | 0.3138 | 56815 | 50000 |

| T | ||||||

|---|---|---|---|---|---|---|

| 0.2946 | 2.4941 | 2.9148 | 0.2228 | 0.1600 | 0.4954 | 4999 |

| 0.2788 | 2.8938 | 3.2043 | 0.2440 | 0.1827 | 0.6283 | 14999 |

| 0.2934 | 1.5754 | 2.8956 | 0.2634 | 0.1947 | 0.3592 | 24999 |

| 0.3104 | 1.2584 | 2.7107 | 0.2749 | 0.1998 | 0.2797 | 49999 |

7 Conclusion

In this paper we introduce a new Hawkes process where the intensity is a CARMA(p,q) model. We analyze the statistical properties of this process and obtain a closed-form expression for the autocorrelation function of the number of jumps observed in non-overlapping time intervals of same length. The model is a generalization of the standard Hawkes with exponential kernel but it is able to reproduce more complex dependence structures similar to those documented in several data sets.

Acknowledgments

This work was partly supported by JST CREST Grant Number JPMJCR14D7, Japan.

References

- Andresen et al. [2014] Andresen A, Benth FE, Koekebakker S, Zakamulin V. The CARMA interest rate model. International journal of theoretical and applied finance 2014;17(02):1450008.

- Bacry et al. [2013] Bacry E, Delattre S, Hoffmann M, Muzy JF. Modelling microstructure noise with mutually exciting point processes. Quantitative finance 2013;13(1):65–77.

- Bacry et al. [2015] Bacry E, Mastromatteo I, Muzy JF. Hawkes processes in finance. Market Microstructure and Liquidity 2015;1(01):1550005.

- Bauer and Fike [1960] Bauer FL, Fike CT. Norms and exclusion theorems. Numerische Mathematik 1960;2(1):137–41.

- Benth et al. [2014] Benth FE, Klüppelberg C, Müller G, Vos L. Futures pricing in electricity markets based on stable CARMA spot models. Energy Economics 2014;44:392–406.

- Benth and Rohde [2019] Benth FE, Rohde V. On non-negative modeling with CARMA processes. Journal of Mathematical Analysis and Applications 2019;476(1):196–214.

- Bessy-Roland et al. [2021] Bessy-Roland Y, Boumezoued A, Hillairet C. Multivariate hawkes process for cyber insurance. Annals of Actuarial Science 2021;15(1):14–39.

- Boswijk et al. [2018] Boswijk HP, Laeven RJ, Yang X. Testing for self-excitation in jumps. Journal of Econometrics 2018;203(2):256–66.

- Boumezoued [2016] Boumezoued A. Population viewpoint on Hawkes processes. Advances in Applied Probability 2016;48(2):463–80.

- Brémaud and Massoulié [1996] Brémaud P, Massoulié L. Stability of nonlinear Hawkes processes. The Annals of Probability 1996;:1563–88.

- Brockwell et al. [2006] Brockwell P, Chadraa E, Lindner A. Continuous-time GARCH processes. The Annals of Applied Probability 2006;16(2):790–826.

- Brockwell et al. [2011] Brockwell PJ, Davis RA, Yang Y. Estimation for non-negative lévy-driven CARMA processes. Journal of Business & Economic Statistics 2011;29(2):250–9.

- Brockwell and Marquardt [2005] Brockwell PJ, Marquardt T. Lévy-driven and fractionally integrated ARMA processes with continuous time parameter. Statistica Sinica 2005;:477–94.

- Carbonell et al. [2008] Carbonell F, Jimenez J, Pedroso L. Computing multiple integrals involving matrix exponentials. Journal of Computational and Applied Mathematics 2008;213(1):300–5.

- Cheng and Seol [2020] Cheng Z, Seol Y. Diffusion approximation of a risk model with non-stationary hawkes arrivals of claims. Methodology and Computing in Applied Probability 2020;22(2):555–71.

- Cheysson and Lang [2020] Cheysson F, Lang G. Strong mixing condition for Hawkes processes and application to Whittle estimation from count data. arXiv preprint arXiv:200304314 2020;.

- Chiang et al. [2022] Chiang WH, Liu X, Mohler G. Hawkes process modeling of COVID-19 with mobility leading indicators and spatial covariates. International journal of forecasting 2022;38(2):505–20.

- Clinet and Yoshida [2017] Clinet S, Yoshida N. Statistical inference for ergodic point processes and application to limit order book. Stochastic Processes and their Applications 2017;127(6):1800–39.

- Da Fonseca and Zaatour [2014] Da Fonseca J, Zaatour R. Hawkes process: Fast calibration, application to trade clustering, and diffusive limit. Journal of Futures Markets 2014;34(6):548–79.

- Doob [1944] Doob JL. The elementary Gaussian processes. The Annals of Mathematical Statistics 1944;15(3):229–82.

- Errais et al. [2010] Errais E, Giesecke K, Goldberg LR. Affine point processes and portfolio credit risk. SIAM Journal on Financial Mathematics 2010;1(1):642–65.

- Hawkes [1971a] Hawkes AG. Point spectra of some mutually exciting point processes. Journal of the Royal Statistical Society: Series B (Methodological) 1971a;33(3):438–43.

- Hawkes [1971b] Hawkes AG. Spectra of some self-exciting and mutually exciting point processes. Biometrika 1971b;58(1):83–90.

- Hawkes [2018] Hawkes AG. Hawkes processes and their applications to finance: a review. Quantitative Finance 2018;18(2):193–8.

- Hitaj et al. [2019] Hitaj A, Mercuri L, Rroji E. Lévy CARMA models for shocks in mortality. Decisions in Economics and Finance 2019;42(1):205–27.

- Iacus and Mercuri [2015] Iacus SM, Mercuri L. Implementation of Lévy CARMA model in YUIMA package. Computational Statistics 2015;30(4):1111–41.

- Iacus et al. [2017] Iacus SM, Mercuri L, Rroji E. COGARCH(p,q): Simulation and inference with the YUIMA package. Journal of Statistical Software 2017;80:1–49.

- Iacus et al. [2018] Iacus SM, Mercuri L, Rroji E. Discrete-time approximation of a COGARCH(p,q) model and its estimation. Journal of Time Series Analysis 2018;39(5):787–809.

- Ibragimov and Linnik [1971] Ibragimov I, Linnik YV. Independent and stationary sequences of random variables. Wolters, Noordhoff Pub 1971;.

- Lesage et al. [2022] Lesage L, Deaconu M, Lejay A, Meira JA, Nichil G, et al. Hawkes processes framework with a gamma density as excitation function: application to natural disasters for insurance. Methodology and Computing in Applied Probability 2022;:1–29.

- Marquardt and Stelzer [2007] Marquardt T, Stelzer R. Multivariate carma processes. Stochastic Processes and their Applications 2007;117(1):96–120.

- Mercuri et al. [2021] Mercuri L, Perchiazzo A, Rroji E. Finite mixture approximation of CARMA(p,q) models. SIAM Journal on Financial Mathematics 2021;12(4):1416–58.

- Mohler et al. [2011] Mohler GO, Short MB, Brantingham PJ, Schoenberg FP, Tita GE. Self-exciting point process modeling of crime. Journal of the American Statistical Association 2011;106(493):100–8.

- Muni Toke and Yoshida [2017] Muni Toke I, Yoshida N. Modelling intensities of order flows in a limit order book. Quantitative Finance 2017;17(5):683–701.

- Ogata [1988] Ogata Y. Statistical models for earthquake occurrences and residual analysis for point processes. Journal of the American Statistical association 1988;83(401):9–27.

- Ozaki [1979] Ozaki T. Maximum likelihood estimation of Hawkes self-exciting point processes. Annals of the Institute of Statistical Mathematics 1979;31(1):145–55.

- Poinas et al. [2019] Poinas A, Delyon B, Lavancier F. Mixing properties and central limit theorem for associated point processes. Bernoulli 2019;25(3):1724–54.

- Rizoiu et al. [2017] Rizoiu MA, Lee Y, Mishra S, Xie L. Hawkes processes for events in social media. In: Frontiers of multimedia research. 2017. p. 191–218.

- Swishchuk et al. [2021] Swishchuk A, Zagst R, Zeller G. Hawkes processes in insurance: Risk model, application to empirical data and optimal investment. Insurance: Mathematics and Economics 2021;101:107–24.

- Tómasson [2015] Tómasson H. Some computational aspects of Gaussian CARMA modelling. Statistics and Computing 2015;25(2):375–87.

- Tsai and Chan [2005] Tsai H, Chan K. A note on non-negative continuous time processes. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 2005;67(4):589–97.

- Van Loan [1978] Van Loan C. Computing integrals involving the matrix exponential. IEEE transactions on automatic control 1978;23(3):395–404.

Appendix A Integration of matrix exponentials

Let be a square matrix and . As the exponential of the matrix can be computed as

it is straightforward to show that

| (76) |

Appendix B Solution of a general Linear Ordinary differential Equation

To solve , we consider the transformation and observe that

from where we have that in terms of reads

| (77) |

Appendix C Computation of integrals with matrix exponentials

Some useful results for computing integrals that involve matrix exponentials are provided in Van Loan [1978] and Carbonell et al. [2008]. In particular, we recall the result that deals with the computation of the following two integrals:

| (78) |

| (79) |

where , , , and have dimension , , , and , respectively. We need to define a block triangular matrix as follows

| (80) |

The integrals (78) and (79) coincide with the elements and in the matrix exponential:

| (81) |

while , and .

Remark 5.

The eigenvalues of coincide with the eigenvalues of , and . If the real part of all eigenvalues of , and is negative, the following result holds

that implies

| (82) |

and

| (83) |

Appendix D Proofs of propositions on long-run covariance and variance of the number of jumps

We provide below the proof of Propositon 6 on the long-run covariance of the number of jumps in a CARMA(p,q)-Hawkes model.

Proof.

We first determine the covariance of number of jumps in two non-overlapping time intervals given the information at time . This quantity is formally defined as

| (84) | |||||

Using the iteration property of the conditional expected value, (84) becomes

Applying the result (36) in Proposition 5, we get

| (85) |

where

| (86) | |||||

In the rhs of (86), the last two terms are stationary due to the result in (37) and to the negativity of the real part for the eigenvalues of ; the third term converges to zero as while the fourth term has the following limit behaviour

| (87) |

For the first two terms in the rhs (86) consider the quantity:

| (88) |

as . In (88) the vector requires the calculation of infinitesimal generators. We then observe that for , the infinitesimal generator of the function is:

while for

that implies

| (89) |

from where we get

| (90) | |||||

The quantity is not stationary but it is useful as it appears in the rhs of the function introduced in (88) that can be rewritten as

| (91) | |||||

We analyze the long-run behaviour of each term in the rhs of (91). We first observe that

with

| (92) |

The formula for the conditional expected value of the state process in (32) allows us to rewrite the third term in the rhs of (91) as follows

| (93) | |||||

To compute the integral we use the result in (81) and exploiting its limit behaviour (82), the long-run behaviour of (93) becomes

| (94) |

The fourth term in the rhs of (91) can be written as

| (95) | |||||

Integrating by parts we get

Thus (95) becomes

Using the formula for the conditional expected value of the counting process in (31) we get

and its long-run behaviour is established considering , that is

| (96) |

The fifth term in the right-hand side of (91) can be rewritten as

that has the following long-run behaviour

| (97) |

Lemma 1 suggests that the last term in the rhs of (91) can be written as

The result in (76) implies that

To determine the asymptotic behaviour of this term, we analyze the long-run behaviour of the integral . Exploiting the result in C, we have

as all eigenvalues of and have negative real part. Using the Fubini-Tonelli’s Theorem the last integral becomes

Its long-run behaviour is obtained using the result in (83), that is

| (98) |

Finally, we have

| (99) |

From (92), (94), (96), (97) and (99) we obtain the limit behaviour for the quantity in (91)

| (100) | |||||

Using (100) we can determine the asymptotic behaviour of (86) and we get

| (101) | |||||

By straightforward calculations (101) becomes (66) and the covariance reads as in (65). ∎

Here we provide the proof of Proposition 7.

Proof.

For the asymptotic variance we need to compute the conditional variance of the number of jumps in an interval with length . First we observe that

We then compute the second moment of the increments

For it is useful to compute the infinitesimal operator for the function , that reads

Applying the Dynkin’s formula, we have

Therefore

| (102) | |||||

We study the asymptotic behaviour of the terms in (102). We denote with

We observe that the following integral is finite

from where we deduce that

| (103) |

We then concentrate on the quantity that through straightforward computations can be written as

Since we have a continuous integrand in a compact support

we have

| (104) |

Denoting with , we obtain

where is rewritten as

and using the same arguments as above, we get

The quantity can be rewritten as

while taking the limit as , we have

| (105) |

The quantity

| (106) | |||||

depends on the integral where from the substitutions and we get

| (107) |

Defining

and applying the result in C, the inner integral in (107) becomes

| (108) |

Thus the integral in (107) can be computed as follows

| (109) |

We notice that as and all eigenvalues of have negative real part, then

Similarly, we get the limit for the term as :

We define the following quantity

and observe that the first integral can be rewritten as

where both terms in the rhs tend to zero as thus

Similar arguments are used to determine the limit as for the quantity as follows

Combining all results, we get the stationary behaviour for the quantity that reads

| (110) | |||||

Furthermore

By straightforward calculations, we obtain the result in (67) for the asymptotic variance. ∎