problem \BODY Input: Question:

Quantum Encoding and Analysis on Continuous Time Stochastic Process with Financial Applications

Abstract

Modeling stochastic phenomena in continuous time is an essential yet challenging problem. Analytic solutions are often unavailable, and numerical methods can be prohibitively time-consuming and computationally expensive. To address this issue, we propose an algorithmic framework tailored for quantum continuous time stochastic processes. This framework consists of two key procedures: data preparation and information extraction. The data preparation procedure is specifically designed to encode and compress information, resulting in a significant reduction in both space and time complexities. This reduction is exponential with respect to a crucial feature parameter of the stochastic process. Additionally, it can serve as a submodule for other quantum algorithms, mitigating the common data input bottleneck. The information extraction procedure is designed to decode and process compressed information with quadratic acceleration, extending the quantum-enhanced Monte Carlo method. The framework demonstrates versatility and flexibility, finding applications in statistics, physics, time series analysis and finance. Illustrative examples include option pricing in the Merton Jump Diffusion Model and ruin probability computing in the Collective Risk Model, showcasing the framework’s ability to capture extreme market events and incorporate history-dependent information. Overall, this quantum algorithmic framework provides a powerful tool for accurate analysis and enhanced understanding of stochastic phenomena.

1 INTRODUCTION

The continuous time stochastic process (CTSP) is a fundamental mathematical tool that encompasses various well-known stochastic processes, such as Poisson point process, compound Poisson process, Lévy process, continuous Markov process, and doubly stochastic Cox process. CTSP plays a crucial role in modeling stochastic phenomena occurring in continuous time variables, and its applications span multiple disciplines including finance, physics, statistics, and biology [1, 2, 3, 4, 5]. However, compared to its discrete counterpart, CTSP is considered more complex due to its continuous path. Analytic solutions or explicit formulas for the underlying stochastic differential equations and quantities are often unavailable for practical problems. Moreover, the application of numerical methods like Monte Carlo simulation can be computationally demanding, requiring unexpectedly large storage and computation resources. This is primarily due to the exponential growth of the sampling space as time slices become finer, and the intricate nature of the evolution dynamics within the process [6, 7]. These complexities make efficient and accurate analysis of CTSPs a challenging task in various fields of study.

The developments of quantum processors [8, 9, 10] and algorithms [11, 12, 13, 14, 15, 16, 17, 18, 19] have revealed that quantum computation has great potential beyond classical computers. Thus it would be one powerful tool to solve the above challenging problems. However, there are still two fundamental challenges to be overcome when implementing the storage and analysis of CTSP with a quantum computer.

The first challenge is the data-loading procedure of CTSP: As a common and primary bottleneck faced by quantum machine learning and many other algorithms[20], the state preparation problem has been studied and discussed in many works [21, 22, 23]. Quantum analog simulators are proposed to predict the future of a specified class of CTSP named renewal process with less past information, and an unbounded memory requirement reduction is made in [24, 25, 26]. The quantum advantage in simulating stochastic processes is further discussed in [27]. Nevertheless, those works have not totally solved the CTSP preparation problem. The information is not digital-encoded, so the analysis, such as quantum-enhanced Monte Carlo method is not easy to implement. Moreover, the type of CTSP is restricted to the renewal process. Furthermore, the storage of the entire path is absent, leading to crucial practical problems for financial engineering, quantitative trading, and many other path-dependent scenarios.

The second challenging problem is the information extraction of CTSP. Quantum-enhanced Monte Carlo method, which involves generating random paths and computing the expectation of desired values, has been shown to achieve quadratic quantum speedup in computing the final value of discrete sampling paths [28, 29, 30, 31, 32, 33]. Additionally, a weightless summation of discrete paths, targeting Asian-type option pricing, is proposed in the work by Stamatopoulos et al. [30]. However, the quantum-enhanced Monte Carlo method for CTSP, which involves computing the expectation of a weighted integral over the CTSP paths and extracting history-sensitive information (such as the first-hitting time problem), remains unresolved.

In this work, we establish a framework to solve the problems of state preparation and information extraction of quantum continuous time stochastic process (QCTSP). Two representations encoding general QCTSP are introduced. The corresponding state preparation method is developed to prepare the QCTSP with less qubit number requirement, higher flexibility, and more sensitivity to discontinuous jumps that are important to model extreme market events such as flash crash. An observation of the CTSP holding time is made, inducing further reductions in the circuit depth and the gate complexity of QCTSP. Specific quantum circuits are designed for most of the often-used CTSPs with exponential reduction of both qubit number and circuit depth on the key parameter of QCTSP named holding time (as summarized in table 2). As for the information extraction problem of QCTSP, the weightless integral and the arbitrary time-weighted integral of the QCTSP can be efficiently evaluated by computing the summation of directed areas. Furthermore, this method enables the quantum-enhanced Monte Carlo framework to extend to the continuous-time regime, admitting a quadratic quantum speed up. Moreover, by introducing a sequence of flag qubits, our method can extract the history-sensitive information that is essential and indispensable for quantitative finance, path-dependent option pricing, and actuarial science, to cite but a few examples.

Applications of computing the European type option price in the Merton Jump Diffusion Model and the ruin probability in the Collective Risk Model are given. The first application of evaluating a European-type option has been studied in previous work [29, 30, 31, 33], while our method takes the more practical situation of the discontinuous price movement into consideration, and the simulation result is consistent with the Merton formula. The second application of computing the ruin probability opens up new opportunities in the area of insurance as being the first time that quantum computing has been introduced into insurance mathematics up to known, illustrating the great potential power of QCTSP.

In addition to the theoretical importance and rich applicability of QCTSP mentioned above, our work also benefits from its low requirement of input data and circuit connectivity. It can be utilized as an input without quantum random access memory (qRAM) [34, 35, 36], partly mitigating the input problem that quantum machine learning and many other quantum algorithms are confronted with. Simultaneously, an indicator is given in this work to characterize not only the preparation procedure’s complexity but the circuit connectivity as well.

The structure of this article is as follows: Given the mathematical notations for readability and the formal problem statement, the main framework of QCTSP is sketched in Section 2. The main results of state preparation and information extraction are organized in Section 3 and Section 4, respectively. Followed by two applications of option pricing and insurance mathematics in Section 5, the discussion, together with an introduction of future work, is given in Section 6. The detailed construction of specific modified subcircuits and proofs can be found in the Appendix.

2 QUANTUM CONTINUOUS TIME STOCHASTIC PROCESS

The mathematical notation is given in the first subsection, followed by the formal definition of CTSP and the two representations of QCTSP. Then the core problems of state preparation and information extraction of QCTSP are stated. A brief framework of our QCTSP is described at the end of this section.

2.1 Preliminaries

| Notation | Nomenclature |

| The probability. | |

| The probability amplitude. | |

| Space of CTSP. | |

| Space of CTSP of deterministic pieces. | |

| Space of states of point. | |

| the size of the Space of states . | |

| The set of index . | |

| Time slices. | |

| The set of time . | |

| Number of Pieces. | |

| A CTSP. | |

| The piece’s value variable. | |

| A realization of , taking the index. | |

| The index vector denoting the state space indexes of the path. | |

| The piece’s increment. | |

| The piece’s holding time. | |

| A realization of in path. | |

| The holding time vector of one path realization. | |

| The piece’s cumulative time. | |

| The memory length of . |

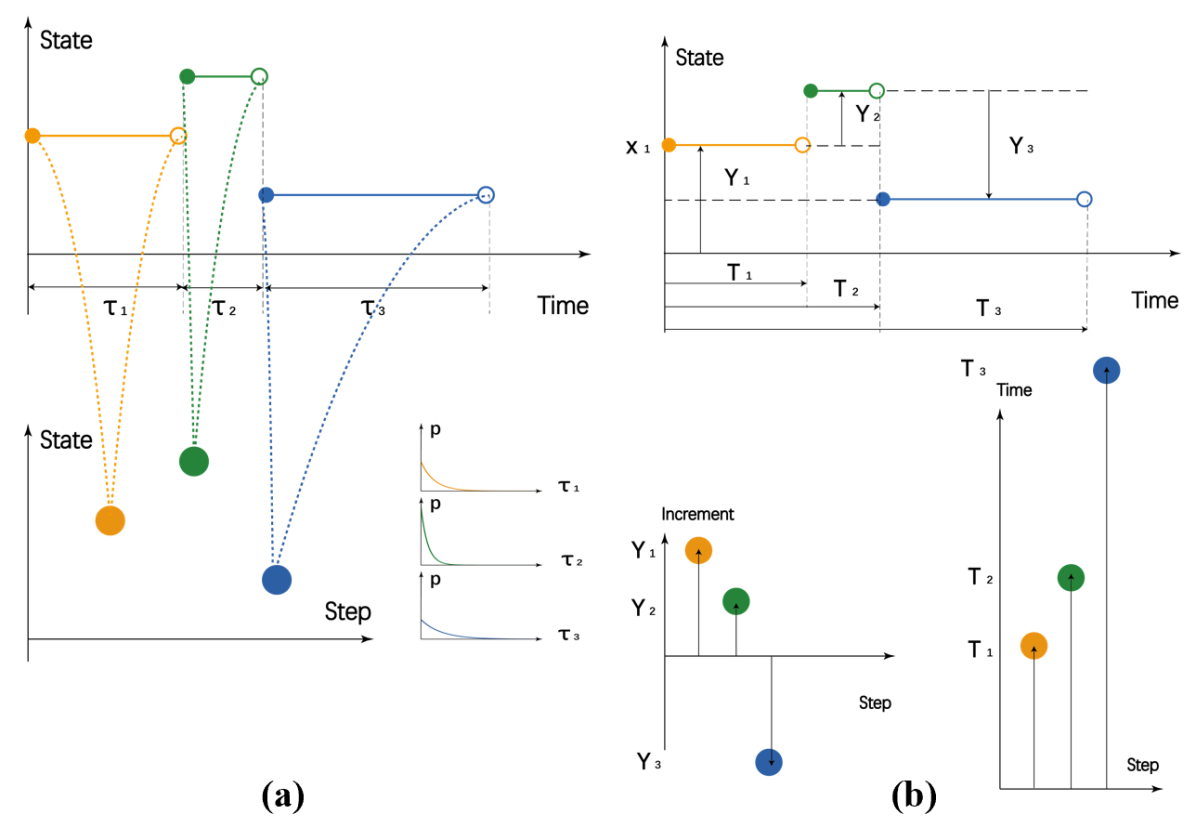

Intuitively, a continuous time stochastic process is a sequence of random variables indexed by a non-negative continuous parameter , such as the position of a particle or the price of a financial instrument. Wherein each random variable lies in the same space named the state space . In this article we consider the state space with a finite size , whereas the more generic continuous case can be solved via a discretization. For the current time , the random variable follows a distribution determined by the previous history , i.e., if an observation is made, the random variable falls into one specific state, as known as a realization, in the underlying space . In the generic case, the distribution also varies following the evolutionary dynamics of this CTSP. More formally, given the mathematical symbols in Table 1, a CTSP can be defined as

Definition 1.

(Continuous Time Stochastic Process) Given a discrete space , a continuous time stochastic process is a stochastic process defined on the continuous variable , where for each , the state is a stochastic variable whose possibility distribution is determined by .

For a given CTSP, the most significant distinction from the discrete case is the uncountable dimensional space of continuous sample paths denoted by . As the time slices become thinner, the sample space becomes a disaster for both theoretical analysis and simulation. Henceforth, the reduced space consists of those paths that can be divided into finite in-variate pieces is considered, where each in is a piece-wise determined random function for with .

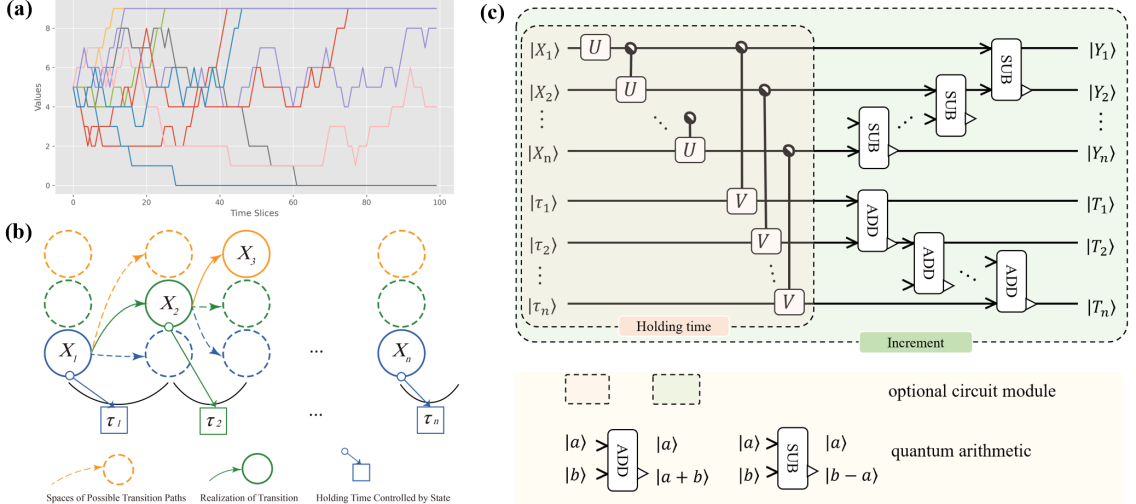

Thus the piece can be recorded as a pair of random variables , where is a discrete random variable that denotes the piece’s state, and is a strictly positive random variable that denotes lifetime length of the piece. In this way, the whole CTSP is encoded via a sequence of random variable pairs , which will be called the holding time representation hereafter (as illustrated in Figure 1 (a)). More precisely, we have:

Definition 2.

(Holding Time Representation of Quantum Continuous Time Stochastic Process ) Given a continuous time stochastic process , the holding time representation of quantum continuous time stochastic process is a sequence of stochastic pairs satisfying: (1) , (2) , and (3) .

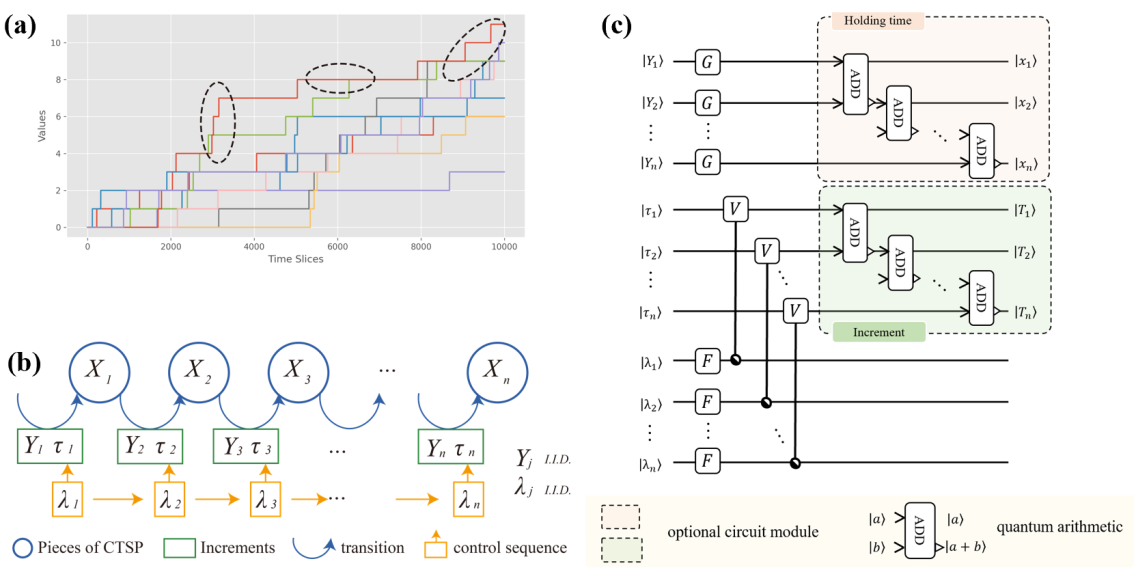

An alternative method named increment representation to encode a CTSP is to consider an equivalent sequence of random variable pairs where and are the increments of the CTSP (as illustrated in Figure 1 (b)):

Definition 3.

(Increment Representation of Quantum Continuous Time Stochastic Process ) Given a continuous time stochastic process , the increment representation of quantum continuous time stochastic process is a sequence of stochastic pairs satisfying: (1) , (2) , and (3) .

Instead of the uniform sampling method, these two encoding methods benefit from the reduction of qubit number (as shown in Figure 2), as well as the ability to capture randomly occurring discontinuous jumps (as circled in Figure 4 (a) and Figure 6 (a)). These two equivalent representations are proposed simultaneously to efficiently compute path-dependent and history-sensitive information, as stated later in Section 4.

2.2 Problem statement

In this paper, the QCTSP is assumed to be stored in three registers named the index register , the data register and the time register for the storage of the index sequence, the path sequence and the holding time sequence , respectively. Then the QCTSP state, defined as Definition 1 and encoded in either Definition 2 or Definition 3, lies in the Hilbert space . More specifically, it can be represented as a superposition of possible paths

| (1a) | |||

| where each path is stored in the state | |||

| (1b) | |||

| with possibility | |||

| (1c) | |||

| . | |||

Here the index vector satisfies

and means that the piece takes the value in the state space , and where is a realization of the sequence and means that the piece stays for time slices bounded by . According to Definition 1, for each time piece, the current pair is derived from the past pieces with the possibility satisfying

| (2a) | |||

| The corresponding possibility amplitude satisfies | |||

| (2b) | |||

as a direct result. Besides, the possibility amplitudes also satisfy

| (3) |

Given a CTSP as defined in Definition 1, our first goal is to derive the corresponding QCTSP Eq. (1a) encoded by Definition 2 and 3. More formally, the problem is defined as follows:

Supposed that a QCTSP has been prepared taking the form of Eq. (1), our second goal is to extract the information of interest, a quantity determined by the knowledge of the past path . This problem can be stated formally as:

Measurements can be implemented at the end of QCTSP-E circuit to extract the quantum information into a classical register. Despite this, it should be noticed that the information is stored in the quantum state before any measurements, and hence the QCTSP-E circuit can be utilized as a sub-module of another bigger circuit.

2.3 Framework

The problem of modeling and analyzing the paths of QCTSP via a quantum processor can be divided into two main steps: Encode and prepare the QCTSP, and then decode and analyze it.

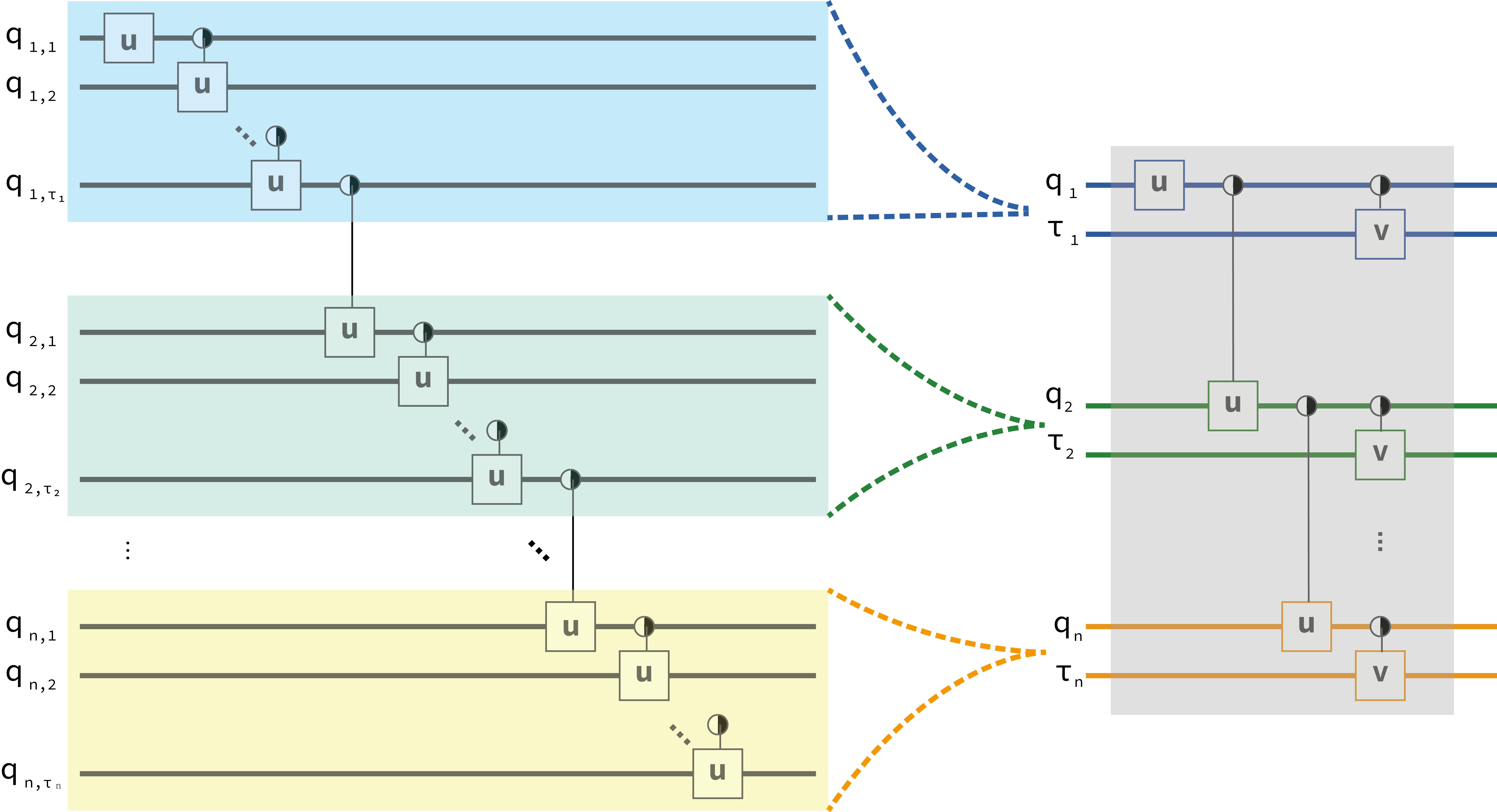

There are prominent challenges to overcome when we try to solve the QCTSP-P problem. Intuitively, the complexity of the QCTSP-P problem is determined by the number of pieces , the average holding time , and the intrinsic evolution complexity. The compressed encoding method appears to be natural and simple, and leads to reductions in the qubit number and the circuit depth (as illustrated in Figure 2). By introducing the indicator memory length to depict the evolutionary complexity of CTSP, we first study the simplest case of memory-less process. An interesting observation of the memory-less process holding time is made, and this induces a constant circuit depth. As the memory length increases, the underlying QCTSP turns to be more complicated (shown in Figure 3) while the property of the holding time still works: Specific types of QCTSP can be prepared efficiently (see Figure 4, Figure 5, and Figure 6), and the detailed construction and the corresponding proofs are given in section 3 and Appendix B, respectively. The qubit number is reduced from of the uniform sampling method to of the QCTSP method, making an exponential reduction on the parameter . And the circuit depth is optimized from of the uniform sampling method to of the QCTSP method, also making an exponential reduction of qubit number on the parameter . The results of state preparation are summarized in Table 2.

| QCTSP Type | Qubit Number | Circuit Depth | |||

| QCTSP (our work) | Uniform Sampling | QCTSP (our work) | Uniform Sampling | ||

| Poisson point process | 0 | ||||

| compound Poisson process | 0 | ||||

| Lévy process | 0 | ||||

| continuous Markov process | 1 | ||||

| -order Markov process | |||||

| Cox process | 0 | ||||

| general CTSP |

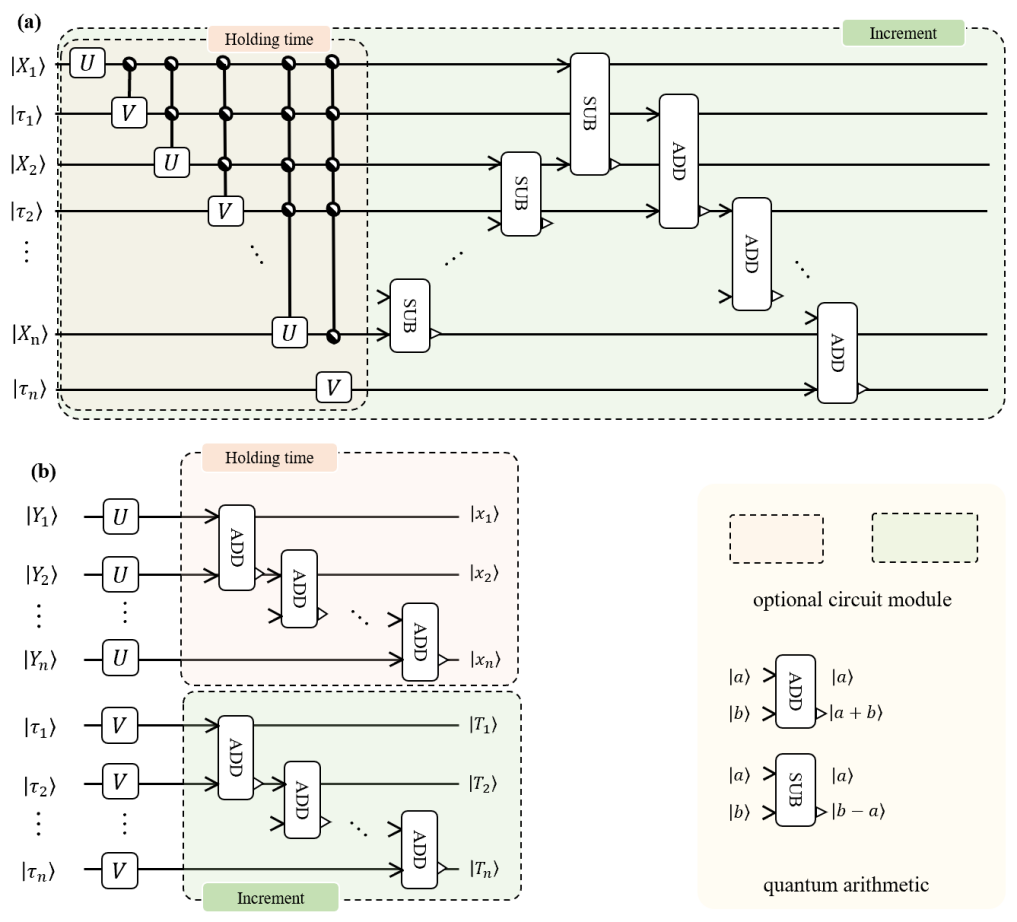

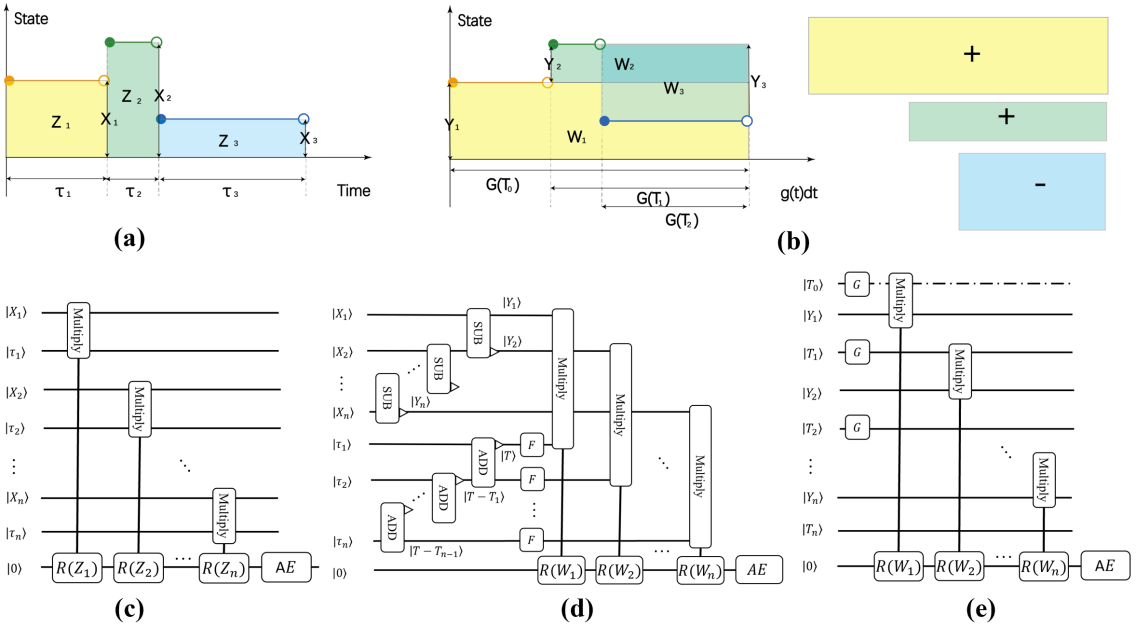

The even more challenging QCTSP-E problem is to efficiently decode and extract information from QCTSP so that the quantum speed-up on preparation will not be diminished. By a controlled rotation gate-based Riemann summation of rectangles (as illustrated in Figure 7 (a) and Figure 7 (c)), the weightless summation of a discrete path can be extended to the time integral of a continuous path. In addition, a parallel coordinate transformation can be implemented to achieve a path-dependent weighted integral (as illustrated in Figure 7 (b), Figure 7 (d) and Figure 7 (e)). Furthermore, benefited from our encoding and extracting method, the discontinuous jumps and transitions can be detected and modeled more precisely. And history-sensitive information such as first hitting time can be extracted easily as a consequence. Moreover, by introducing the amplitude estimation algorithm, the information extraction QCTSP also admits a further quadratic speed-up. The detailed construction and the corresponding proofs are given in section 4 and Appendix C.

3 STATE PREPARATION

To understand why the state preparation procedure of QCTSP is non-trivial, one should notice that the sequence of pairs can be entangled with each other for . Intuitively, the more the current state is influenced by past information, the more complicated gates and deeper circuits are needed. More precisely, the memory length of a given CTSP is defined as

| (4) |

which means that the conditional probability distribution of the current time is totally determined by the information in the latest time slices. Two extreme situations are compared in Figure 3: One is the worst case where the memory length is as long as the number of pieces. The other is the opposite case where the memory length , and is said to be memory-less in this case. For the first case of the longest memory length, the present pair registers should be entangled with all past time pairs of variables together (as illustrated in Figure 3 (a)), and this surely leads to a disaster of circuit depth and gate complexity. The second case, on the contrary, turns out to be quite simple, and we have the following result:

Theorem 1.

(Memory-less Process’ Holding Time) Supposing that is memory-less, then the holding time for any state follows an exponential distribution with determined by the current sate . Moreover, given an such that the cumulative density function(c.d.f) satisfies , can be prepared via a circuit consisting of qubits with constant circuit depth , and the gate complexity is . (see proof in Appendix B.1)

This simple result should not be surprising since, as discussed above, the memory-less condition leads to no-entanglement states and easier preparation. Following this thought, most of the often-used CTSPs have been systematically studied and efficiently prepared. The conclusion that the complexity of the state preparation of QCTSP tends to be higher as the memory length grows is further evidenced by those results summarized in table 2, leaving the detailed explanation and relevant applications given as follows.

3.1 Lévy process

The first and essential family of CTSPs is the Lévy process, which is one of the most well-known families of continuous-time stochastic processes, including the Poisson process and the Wiener process (also known as Brownian motion), with applications in various fields (For more details, refer to [37] and the references therein). Formally, is said to be a Lévy process if 1) the increments are independent for any , and 2) stationary which means that depends only on and hence is equal in distribution to (as illustrated in Figure 4 (a) and (b)).

Under these assumptions, a Lévy process for the most general case can be prepared efficiently, and we have the following result:

Theorem 2.

(Upper bound of general Lévy Process’ preparation) Suppose that is a Lévy process, is the length of step, is the length of sample path, and is the number of discretization intervals of the underlying distribution . Then the Lévy process can be prepared on qubits within circuit depth, and the gate complexity is thus . (see proof in Appendix B.2)

It should be mentioned that the preparation procedure’s complexity is mainly determined by two factors: the sampling times and the preparation complexity of the underlying distribution . In the most general case where compensated generalized Poisson process with countably many small jump discontinuities and Wiener process are taken into consideration, the sample space size is large and the preparation procedure of the underlying distribution may consume an enormous amount of classical computation resource. Hence it is requisite for one to study the more specific situations besides the upper bound given in Theorem 2, and some optimized preparation results are given below. The first example is the Poisson point process that plays an essential role in modeling the arrival of independent random events. More precisely, despite several equivalent definitions for different domains and applications, a CTSP is a Poisson point process on the positive half-line if the increment is a constant and the underlying distribution of each holding time between the events is an exponential distribution that can be efficiently prepared as shown in Theorem 1. As a direct consequence, one has:

Corollary 3.

(Poisson Point Process’ preparation) Supposing that is a Poisson process, is the length of step, is the length of sampling times, and is the truncation of the exponential distribution . Then the Poisson process can be prepared on qubits with control-rotation gates, and the circuit depth is . (see proof in Appendix B.3)

Another more flexible example is the compound Poisson process as a generalization, i.e., the jumps’ random arrival time follows a Poisson process and the size of the jumps is also random, following an underlying distribution . It should be noticed that each jump’s sampling space size of compound Poisson process is usually fixed in practical, apparently different from the general Lévy process discussed above. We then get the following result with some modification on the circuit(as illustrated in Figure 3 (b)):

Corollary 4.

(Compound Poisson Process’ preparation) Suppose that is a compound Poisson process with being the length of sample path, denoting the sampling space size of each point, and being the truncation of the exponential distribution , then the compound Poisson process can be prepared on qubits. The circuit depth is , and the gate complexity is . (see proof in Appendix B.3)

According to the Lévy-Itô decomposition, a general Lévy process can be decomposed into three components: a Brownian motion with drift , a compound Poisson process , and a compensated generalized Poisson process as follows:

| (5) |

where is the volatility of the Brownian motion, is the drift rate, is the compound Poisson process of jumps larger than 1 in absolute value, and is a pure jump process with countably (infinite) many small jump discontinuities. As contains infinitely many jumps as a zero-mean martingale, it is hard and unnecessary for preparation. One can prepare a general Lévy process without compensated parts as follows: Firstly, the sequence of exponential jumps and holding times are prepared via and operators, respectively. Secondly, the Brownian motions are derived by Grover’s state preparation method through operators controlled by holding time . Thirdly, an adder operator is introduced for the sum of pure jump and Brownian parts. It should be mentioned that the drift term has been omitted since any function on this linear term can be easily translated into a function and hence well-evaluated by Theorem 7 and Theorem 8. The circuit is shown in Figure 4 (c).

3.2 Continuous Markov process

The second and more complicated family of CTSPs is the continuous Markov process. In brief, a stochastic process is called a continuous Markov process if it satisfies the Markov condition: For all , , , where .

Intuitively speaking, given the present state , the future is independent of the past history , and the memory length of a continuous Markov process is (shown in Figure 5 (a) and (b)). A continuous Markov process can be efficiently prepared mainly for two reasons: the holding time only depends on the current state , while the state sequence is independent from . As a result, the continuous Markov process can be embedded into an independent discrete Markov chain depicting the transition probability, together with a sequence of controlled exponential distributions carrying the holding time information (as illustrated in Figure 5 (c)). More precisely, we have the following result:

Theorem 5.

(Continuous Markov Process’ Preparation)Supposing a stochastic process with discrete state space to be a continuous-time Markov chain. Then it can be prepared on qubits via a quantum circuit consisting of gates and circuit depth, where , is the minimum of , and is the truncation error bound for time. (see proof in Appendix B.4)

3.3 Cox process

As further evidence illustrating the flexibility and generalizability of our encoding method, the Cox process, a useful framework for modeling prices of financial instruments in financial mathematics [38], can be efficiently prepared. One of the most significant distinctions between the Cox process and those processes discussed above is that both the states and the evolutionary law vary randomly over time (as illustrated in Figure 6 (a) and (b)). As a direct consequence, the preparation procedure and the corresponding circuit should be dynamic and flexible to characterize this doubly stochastic property (shown in Figure 6 (c)). Precisely speaking, a Cox process is a generalization of the Poisson process where the intensity itself is also a stochastic variable of some distribution . The preparation procedure can be divided into two steps: First, the stochastic control sequence of is prepared by some operator for the underlying distribution . Then the holding time sequence is prepared by parallel controlled- operators for the underlying exponential distribution. The operators of different exponential distributions can be implemented by a sequence of controlled rotation gates of different rotation angles. The increments are assumed to be I.I.D. and can be prepared through some operators (common choice of distributions can be found in the appendix, see Figure 15(a) and Figure 15(c) for reference). In summary, we have the following result:

Theorem 6.

(Cox Process’ Preparation)Suppose that is a Cox process with a varying intensity variable , and follows an underlying statistical distribution that can be prepared on qubits with circuit depth . The increments follows an I.I.D. that can be prepared on qubits with circuit depth . Also it is supposed that the minimum value of is and the error bound is , then it can be efficiently prepared on qubits with circuit depth (holding time representation ) or (increment representation ). (see proof in Appendix B.5)

As the details of the QCTSP preparation procedure have been given above, the results are summarized in table 2. From a high-level view, the computation and storage resource of the preparation procedure is totally determined by the time length and the memory length of the underlying QCTSP . By our compressed encoding method and the corresponding preparation procedure, the number of copies of the state space is reduced from of the uniform sampling method to of the QCTSP method, leading an exponential reduction of qubit number on the parameter . By the encoding method and the observation on the holding time of the memory-less QCTSP, the circuit depths can be optimized from of the uniform sampling method to of the QCTSP method, also making an exponential reduction of qubit number on the parameter .

4 INFORMATION EXTRACTION

Besides the state preparation problem, another challenge of QCTSP is to decode the compressed process and rebuild the information of interest. To extract desired information from QCTSP, one needs to evaluate its continuous counterpart, i.e., the integral of random variable on time , instead of the discrete summation as studied in [33].

Weightless Integral.

More specifically, the expectation value of an integrable function of the random variable

| (6) |

can be efficiently evaluated via a framework developed as follows: First of all, the integral can be divided into vertical boxes (as shown in Figure 7 (a)) as a Riemann summation

Secondly, the area of each box is translated into multiplication of the holding time representation encoding variables and . Benefiting from the encoding method, this expression is quite simple (as illustrated in Figure 7 (c)). Thirdly, the expected value of the integrable function can be evaluated through a Fourier approximation as a function of order :

Each term and can be evaluated via rotation gates on the target qubit controlled by followed by a standard amplitude estimation algorithm. Leaving the detailed proof in the appendix, one has:

Theorem 7.

(Evaluating I(t))Suppose that a QCTSP is given via holding time representation with steps, qubits for each pair , and circuit depth. Also, one has that is the Fourier approximation of the desired integrable function of the random variable . Then given the error , the expectation value of can be efficiently evaluated within circuit depth and time complexity. (see proof in Appendix C.1)

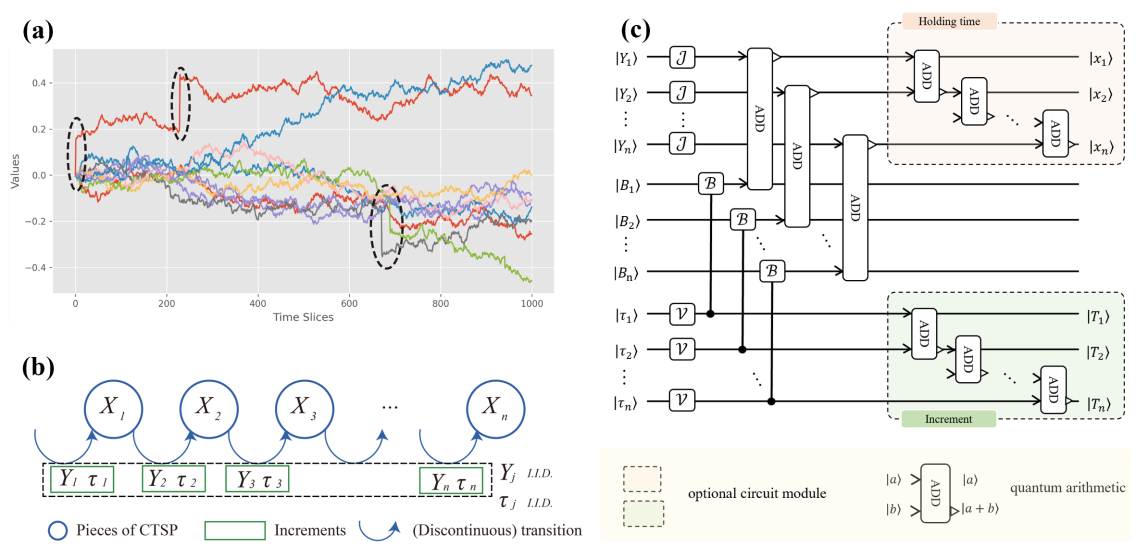

Weighted Integral.

Moreover, this framework applies to the more complicated and generalized situations where the time structure is considered and thus has no discrete correspondence. By introducing a time-dependent function , we can evaluate the expectation value of an integrable function of the random variable

| (7) |

Since the time structure is considered, the integral is divided into horizontal directed boxes(as shown in Figure 7 (b)):

Due to a trade-off on circuit depth and qubits number(see Figure 7 (d) and Figure 7 (e) for reference), this summation can be evaluated via either holding time representation or increment representation. A similar Fourier approximation and amplitude estimation are employed to compute

and hence the following result is given:

Theorem 8.

(Evaluating J(t))

i) Suppose a QCTSP of holding time representation given with steps, qubits for each pair , and circuit depth. is a function whose integral can be efficiently prepared with circuit depth. Also, one has that is the Fourier approximation of the desired integrable function of the random variable . Then given the error , the expectation value of can be efficiently evaluated within circuit depth and time complexity.

ii) Suppose a QCTSP of increment representation given with steps, qubits for each pair , and circuit depth. is a function whose integral can be efficiently prepared with circuit depth. Also, one has that is the Fourier approximation of the desired integrable function of the random variable . Then given the error , the expectation value of can be efficiently evaluated within circuit depth and time complexity. (see proof in Appendix C.2)

Therefore our algorithms would enable the quantum-enhanced Monte Carlo method to apply to path-dependent and continuous stochastic processes, including the time-weighted expectation and the exponential decay time-weighted expectation that are usually used in mathematical finance and quantitative trading.

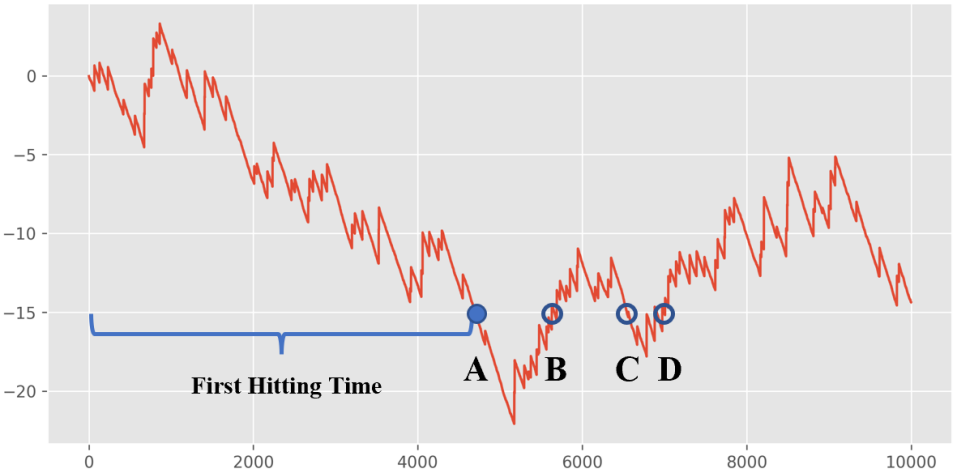

History-Sensitive Information.

Besides the global information defined on the whole path studied above, there is another category of history-sensitive problems that plays an essential role in statistics and finance, including the first-hitting time of Brownian motion, surviving time of ruin theory, and survival analysis, to name but a few. The most apparent difference of the first-hitting problem is that the path-dependent information needs to be extracted when knowing the whole history path. Thus it can not be derived directly by a quantum walk (as illustrated in Figure 8). Formally, a first-hitting problem can be regarded as evaluating the following

| (8) |

The basic idea to evaluate Eq. (8) is to consider flag qubits storing the comparison result of each piece in the sampling path. As a discontinuous jump representing extreme events or market hits always happens at the end of a piece, this method shall work much more precisely than the uniform sampling method. Formally speaking, supposing a given bound , to derive the first hitting time, a bound information register and a flag register is introduced with and qubits, respectively. For the piece of QCTSP, the remained value is derived through a controlled subtraction whose control qubit is and carry-out qubit is . And a CNOT gate is implemented to flip the qubit controlled by the qubit. Two classes are distinguished for each piece: Before the first hit, the remaining bound is , and the flag register is . This first class can be divided into two cases: If the hit does not happen at the piece, the state of the carry-out qubit after the subtraction remains , and then is flipped by the CNOT gate. Hence one has:

case 1 ( and ):

If the hit happens at the piece, the state of the carry-out qubit after the subtraction turns to be , and then is flipped by the CNOT gate. Hence one has:

case 2 ( and ):

For the second class where the current piece is after the first hit , the flag register is , and the subtraction and CNOT gates will not be implemented, and thus the result is:

case 3 ( for some ):

Leaving the theoretical analysis as future work, examples of option pricing and ruin theory will be given in the next section as proof of principle.

5 APPLICATION

In this section, two applications of QCTSP in different financial scenes are given to illustrate the wide range of applicability of QCTSP. In subsection 5.1, the first application is focused on the option pricing problem wherein the underlying stock price is no longer continuous Brownian motion and the original Black-Scholes formula fails. By simulation of QCTSP, option pricing is solved in a different way from previous works and is consistent with the more practical Merton Jump Diffusion formula. In subsection 5.2, the problem of computing the ruin probability under the Collective Risk Model is studied, introducing quantum computation into insurance mathematics.

5.1 Option pricing in Merton Jump Diffusion Model

Since first being introduced into the field of financial engineering, CTSP has been proven to be a powerful tool for financial derivatives pricing [39, 40]. Among those financial derivatives, the European call option is one basic instrument that gives someone the right to buy an underlying stock at a given strike price and maturity time . The famous Black-Scholes model is proposed to evaluate a European option [41], and the simulation for Black-Scholes type option pricing has been implemented on quantum computers [29, 30, 31, 33]. However, the assumption of a constant variance log-normal distribution in the original article [41] turns out to be less realistic as the empirical studies of discontinuous returns of stock are ignored. Hence the Merton Jump Diffusion Model was proposed to incorporate more realistic assumptions from Merton’s work [42].

In the Merton Jump Diffusion Model, the stock price is assumed to satisfy the following stochastic differential equation:

| (9) |

where is the current stock price, is the maturity time in years, is the annual risk-less interest rate, is the annual volatility, is the Weiner process, is the Poisson point process, and is the discontinuous jump follows a log-normally distribution. The last term on the right hand side represents the discontinuous price movements caused by such as acquisitions, mergers, corporate scandals, and fat-finger errors. Merton derives a closed form solution to Eq. (9) as an infinite summation of Black-Scholes formula conditional on the number of the jumps and the underlying distributions of each jump:

| (10) |

where is the mean of the jump size, is the volatility of the jump size, is the intensity of the underlying Poisson point process, and and are the corresponding interest rate and volatility, respectively. Despite being in line with empirical studies of market returns, the formula Eq. (10) takes the form of an infinite summation, and thus an alternative numerical method of Monte Carlo can be employed to compute the desired option price. Instead of a Brownian motion in the Black-Scholes model, one has to simulate, in the Merton Jump Diffusion Model, the more complicated case of a Lévy process where our method can be applied to make a quadratic speed-up against the classical Monte Carlo simulation. More precisely, for a European type call option given the underlying stock price , its price can be defined as:

| (11) |

where is the adjusted drift term on the purpose of risk neutral preferences, represents the Brownian motion term and follows a normal distribution , and represents the discontinuous jump and follows a normal distribution .

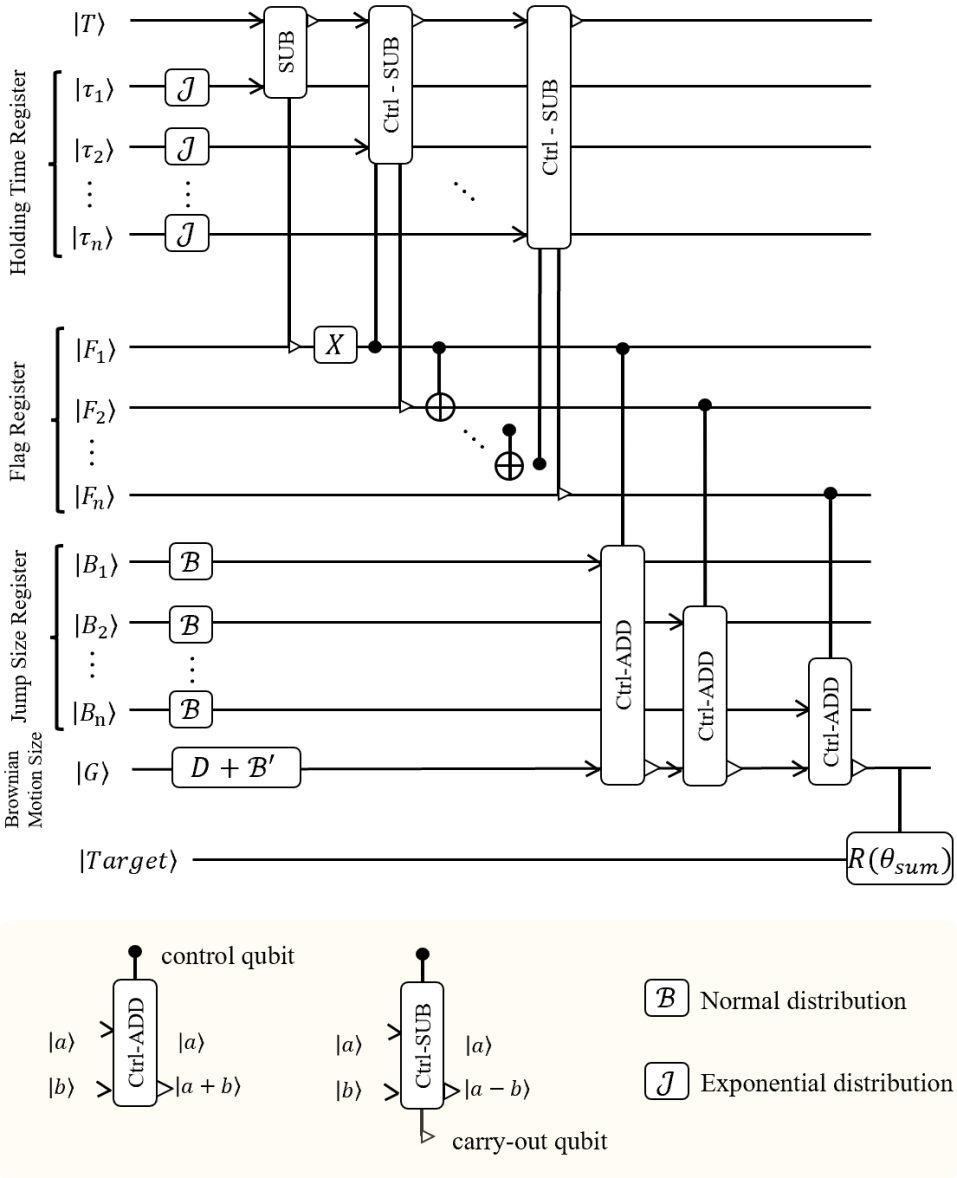

This Lévy process can be efficiently prepared as mentioned in subsection 3.1, and then the valuation procedure is implemented via the method given in section 4. More specifically, as illustrated in Figure 9, the quantum circuit consists of six quantum registers: the maturity time register , the holding time register , the flag register , the jump size register , the Brownian motion size register , and the target qubit . The holding time can be prepared via parallel exponential distribution subcircuits , and the jump size can be prepared via parallel normal distribution subcircuits . The drift term together with the geometric Brownian motion is prepared on via a normal distribution subcircuit . Subtractor and controlled-subtractors, together with X gate and CNOT gates, are implemented to justify the number of jumps that will be considered, and the result is output on the flag register . Adders controlled by the corresponding flag registers are employed to derive the final value of the stock price. A rotation gate is then implemented on the target qubit, controlled by the signed summation on register . Then the final value of the option price can be evaluated via measurement or an amplitude estimation.

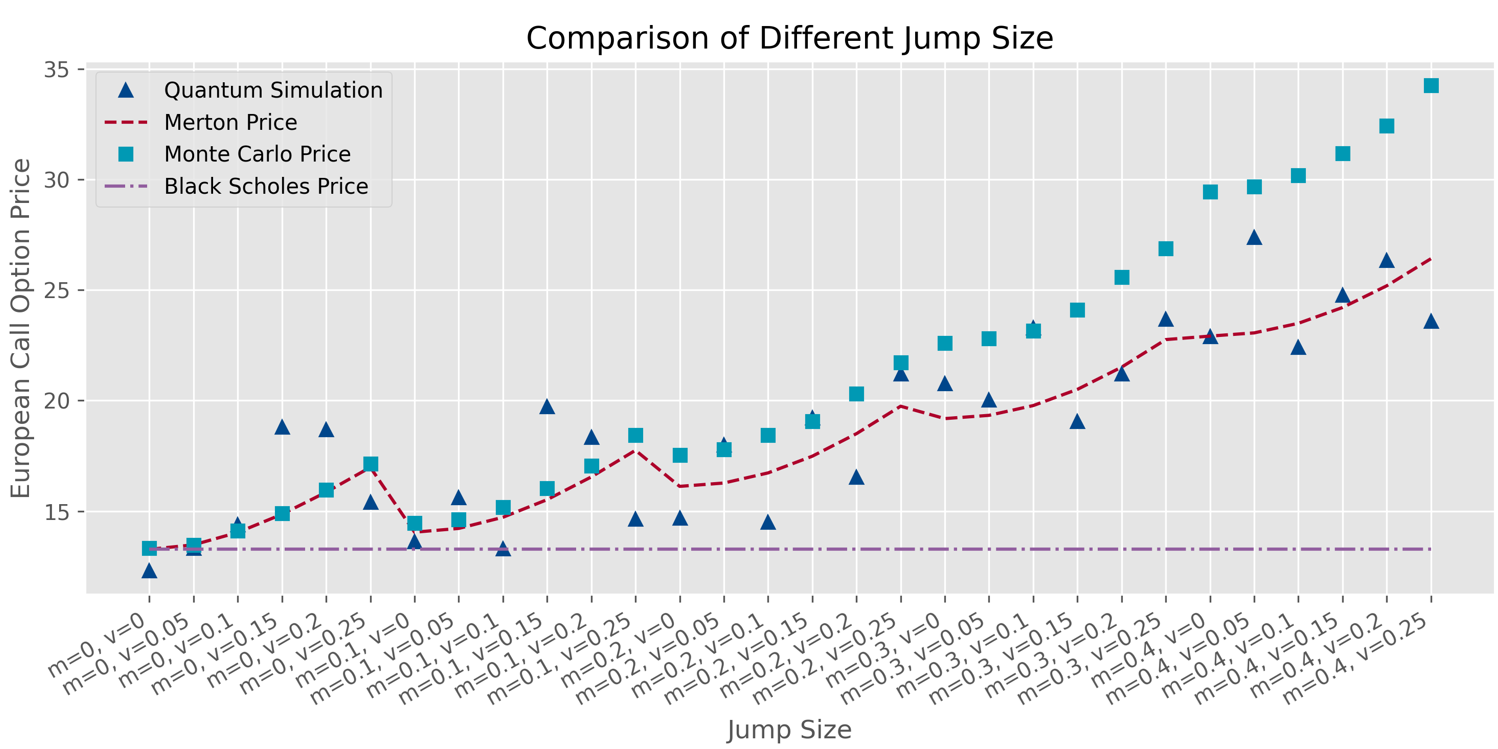

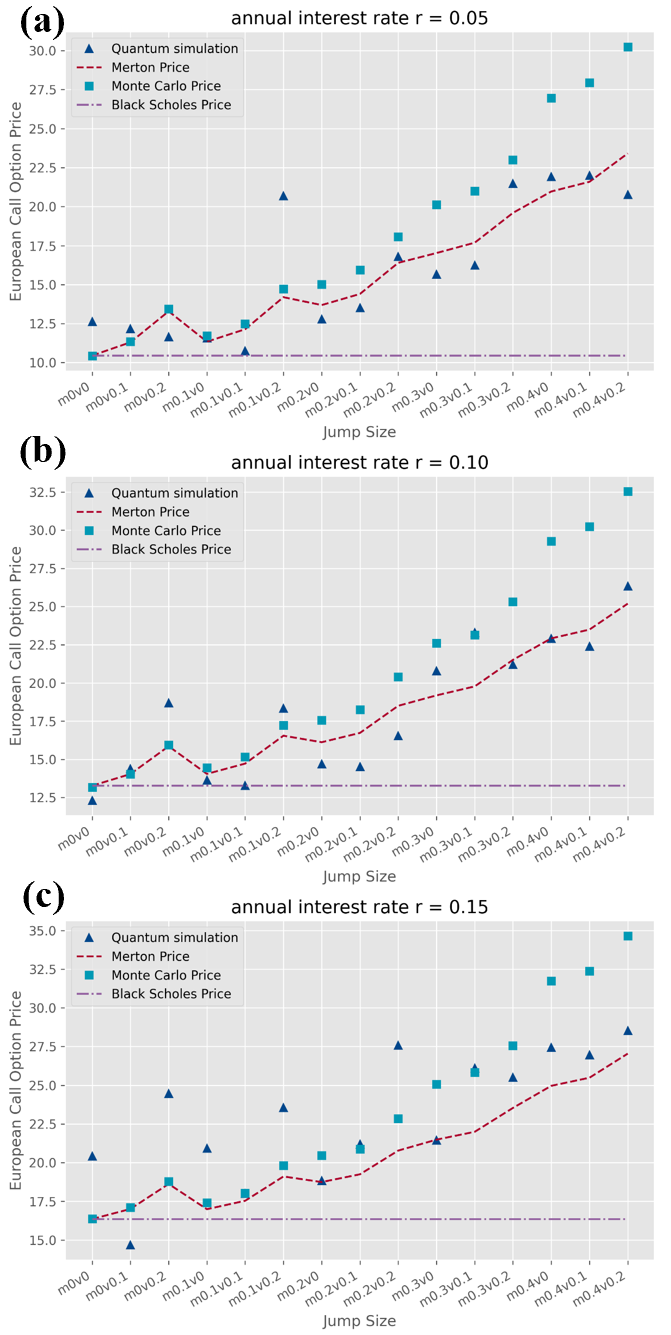

The corresponding quantum simulation result can be found in Figure 10 and Figure 11. In Figure 10, the underlying stock price is given with , , , , , and , and the range of and are and , respectively. Due to the restriction on the qubit number, the simulation is divided into two steps: groups of random rotation angles corresponding to the Brownian motion size. The jump sizes are generated by a classical random generator and then implemented on the target qubit. shots of QCTSP simulated paths are repeated for each group. As shown in Figure 10, the larger the jump size (characterized by and ) is, the farther the Merton Jump Diffusion value is away from the original Black-Scholes price as a consequence of the discontinuous jumps. Moreover, the QCTSP simulation result is consistent with the terms truncated Merton Jump Diffusion formula (Eq. (10)) as well as the classical Monte Carlo simulation, characterizing the property of Lévy discontinuous jump path well. The robustness of the QCTSP method is illustrated in Figure 11, where different annual interest rates are given in the three subfigures with varying jump sizes. The quantum simulation results are consistent with the Merton Formula for a wide range of different parameters.

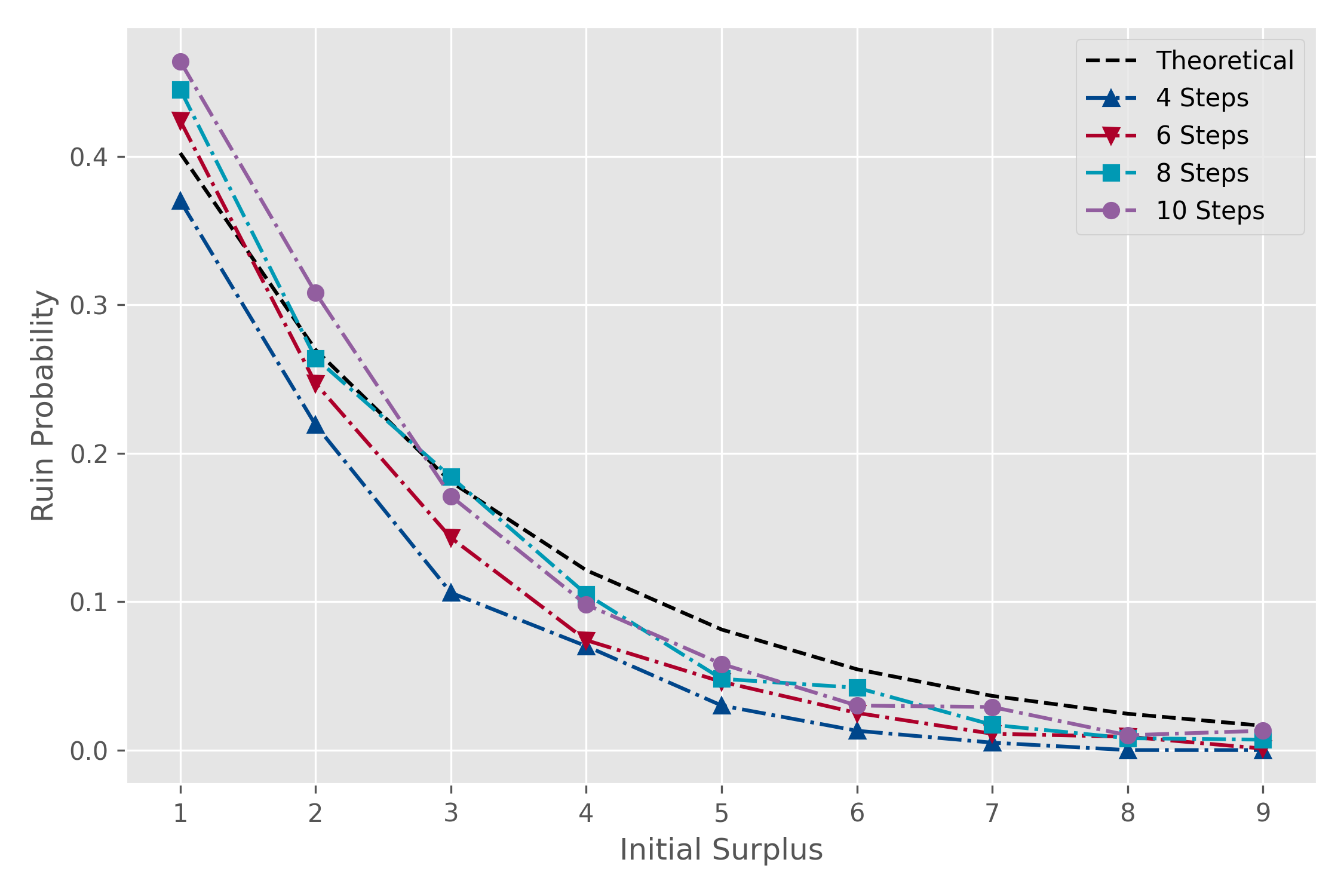

5.2 Ruin probability in Collective Risk Model

Since being a fundamental means to model the stochastic world, there is no surprise that the QCTSP framework developed in this work has great potential power applied to various fields, especially ruin theory. The ruin theory plays a central role in insurance mathematics, high-frequency trading’s market micro-structure theory, and option pricing [43, 44, 45, 46]. In ruin theory, the risk of an insurance company is assumed to be caused by random claims arriving at time , wherein the claim size and inter-claim time are both assumed to follow some independent and identically distributions. Hence the aggregate asset of the insurance company is a continuous time stochastic process

| (12) |

where the initial surplus is , and the premiums are received at a constant rate . In the Collective Risk Model, also known as the Cramér Lundberg model, the claim number process is assumed to be a Poisson process with intensity , and the underlying distribution of is an exponential distribution. In the Sparre Andersen model, can be extended to a renewal process with the arbitrary underlying distribution. Despite the detailed differences between them, both of the two stochastic processes in these models are Lévy processes with drift term , and hence can be prepared easily via our method.

| (13) |

To go one step further, one has a great variety of ruin-related quantities fall into the category of the expected discounted penalty function, also known as the time value of ruin. And those can be easily derived through a quantum-enhanced Monte Carlo modified by us. More precisely, following the notation of Gerber and Shiu [43], the time value of ruin is defined as

| (14) |

where denotes the time of ruin, and and are the surplus prior to ruin and the deficit at ruin, respectively. The expectation is taken over the probability distribution of the ruin samples, taking an interest discounting factor into consideration. The ultimate ruin probability is exactly a special case of Eq. (14) given and . Since ruin always happens after a claim,

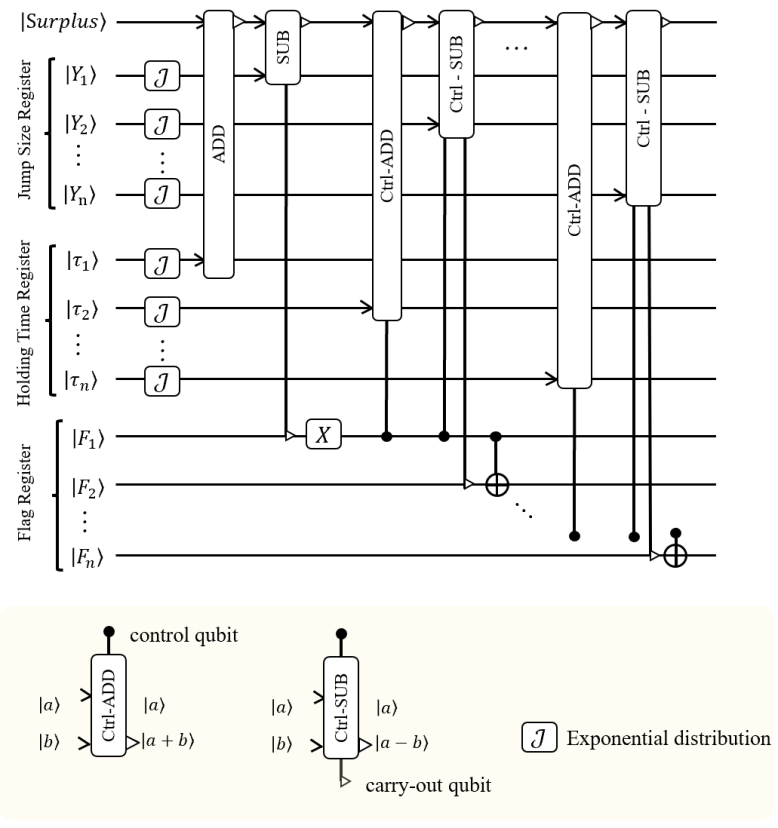

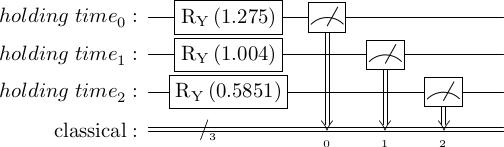

where the indicator function can be easily derived through a sequence of controlled adder and modified subtractor on the prepared states. The detailed construction of circuits and corresponding simulation result are given in Figure 12 and Figure 13.

6 DISCUSSION

In this study, we have focused on the efficient state preparation and quantum-enhanced analysis of continuous time stochastic processes (QCTSP). We have successfully established a robust procedure for QCTSP preparation, allowing the state to be sensitized to discontinuous jumps, which are crucial in modeling extreme market emergencies. Notably, we have achieved significant reductions in both qubit number and circuit depth, particularly concerning the key parameter of holding time.

Furthermore, we are excited to present our novel Monte Carlo simulation method tailored for QCTSP. This groundbreaking approach has led to a remarkable quadratic speed-up compared to the classical counterpart, the continuous time stochastic process (CTSP), making QCTSP a formidable tool in studying the continuous time stochastic world.

A significant contribution of our work lies in the development of techniques for extracting weighted integral and history-sensitive information. These methods are of paramount importance in various fields, such as quantitative trading, time series analysis, and actuarial mathematics. By eliminating the need for additional copies of random paths and relaxing the implied restriction of the independent and identically distributed (I.I.D.) condition, our techniques open new avenues for accurate analysis and computation.

In the context of practical applications, we have successfully demonstrated two scenarios: European option pricing under the Merton Jump Diffusion Model and the evaluation of ruin probability in the Collective Risk Model. These applications serve as compelling evidence of QCTSP’s potential and versatility in addressing real-world challenges.

There are four main reasons why QCTSP stands as a suitable candidate for practical applications in the noisy intermediate-scale quantum era:

Firstly, QCTSP does not impose input restrictions and can be implemented without assuming the need for a quantum oracle or quantum Random Access Memory (qRAM). This property enhances its versatility and applicability in various quantum algorithms, including quantum machine learning, thereby breaking through the input bottleneck often encountered in quantum computations.

Secondly, QCTSP allows for parallel preparation, thanks to a communicative equivalence class decomposition of the sample space. This decomposition results in a reduction in the number of required qubits, contributing to more efficient and resource-effective implementations.

Thirdly, our QCTSP preparation method imposes less requirements on the topological structure of the quantum processor. In many cases, the connectivity requirement, which concerns memory length, can be set at a low level. Consequently, most qubits only need to be entangled with their immediate neighbors, easing the burden of implementation and enhancing scalability.

Lastly, considering the fundamental and critical role that Continuous Time Stochastic Process (CTSP) plays in stochastic analysis, QCTSP holds immense potential for theoretical generalizability and applied flexibility. Its relevance in a wide range of stochastic processes further solidifies its status as a promising candidate for practical applications.

QCTSP exhibits remarkable advantages in terms of input flexibility, parallel preparation, compatibility with quantum algorithms, and potential for theoretical and applied advancements. These features position QCTSP as a promising tool for practical utilization in the emerging era of noisy intermediate-scale quantum computing.

While our work showcases the promising potential of QCTSP, it is essential to acknowledge certain limitations that warrant further investigation and exploration. We outline some of these limitations below:

Firstly, while QCTSP is believed to be hardware-efficient due to its low requirements on the topological structure, a more detailed and quantitative analysis is lacking in this article. We acknowledge this as an avenue for future research and plan to address it through experimental demonstrations.

Secondly, we have not explored the preparation of many other CTSPs with financial relevance, such as Hawkes processes, which may exhibit rich structures and evolutionary laws that could potentially lead to further quantum speed-up. These CTSPs warrant further investigation to understand their quantum computational implications.

Thirdly, while we have demonstrated the applications of QCTSP in European option pricing and ruin probability evaluation, many other relevant applications in fields such as high-frequency trading, actuarial science, and option pricing have not been explored in this work. We recognize the significance of studying these facets and plan to investigate them in future research while maintaining the thematic focus of this current work.

Furthermore, future research should focus on developing more techniques for the efficient extraction of path-dependent information. This aspect is crucial for enhancing the versatility and practicality of QCTSP in various financial analyses.

Additionally, there are intriguing topics related to the intrinsic relation of continuous quantum walk and finance, as discussed in [47, 48, 49]. While discrete and continuous quantum walk methods have shown promise as powerful tools for financial data state preparation and stochastic simulation in finance, we have not delved into this area in the current work. One of the challenges lies in finding suitable ways to store the history information of continuous quantum walks. We leave the exploration of this relationship as a promising avenue for future research.

In conclusion, while our work has made significant strides in the efficient state preparation and quantum-enhanced analysis of continuous time stochastic processes, there are various areas that warrant further investigation and study. We are committed to exploring these limitations and expanding the scope of our research in future endeavors.

ACKNOWLEDGEMENT

This work was supported by the National Natural Science Foundation of China (Grants No. 12034018), and Innovation Program for Quantum Science and Technology No. 2021ZD0302300.

References

- [1] Antonis Papapantoleon. “An introduction to lévy processes with applications in finance” (2008).

- [2] Ole E Barndorff-Nielsen, Thomas Mikosch, and Sidney I Resnick. “Lévy processes: theory and applications”. Springer Science & Business Media. (2001).

- [3] Thomas Milton Liggett. “Continuous time markov processes: an introduction”. Volume 113. American Mathematical Soc. (2010).

- [4] William J Anderson. “Continuous-time markov chains: An applications-oriented approach”. Springer Science & Business Media. (2012).

- [5] Angelos Dassios and Ji-Wook Jang. “Pricing of catastrophe reinsurance and derivatives using the cox process with shot noise intensity”. Finance and Stochastics 7, 73–95 (2003).

- [6] Sheldon M Ross, John J Kelly, Roger J Sullivan, William James Perry, Donald Mercer, Ruth M Davis, Thomas Dell Washburn, Earl V Sager, Joseph B Boyce, and Vincent L Bristow. “Stochastic processes”. Volume 2. Wiley New York. (1996).

- [7] Yuriy V Kozachenko, Oleksandr O Pogorilyak, Iryna V Rozora, and Antonina M Tegza. “Simulation of stochastic processes with given accuracy and reliability”. Elsevier. (2016).

- [8] Richard P Feynman. “Quantum mechanical computers”. Optics news 11, 11–20 (1985).

- [9] David P DiVincenzo. “The physical implementation of quantum computation”. Fortschritte der Physik: Progress of Physics 48, 771–783 (2000).

- [10] Frank Arute, Kunal Arya, Ryan Babbush, Dave Bacon, Joseph C Bardin, Rami Barends, Rupak Biswas, Sergio Boixo, Fernando GSL Brandao, David A Buell, et al. “Quantum supremacy using a programmable superconducting processor”. Nature 574, 505–510 (2019).

- [11] Roman Orus, Samuel Mugel, and Enrique Lizaso. “Quantum computing for finance: overview and prospects”. Reviews in Physics 4, 100028 (2019).

- [12] Daniel J Egger, Claudio Gambella, Jakub Marecek, Scott McFaddin, Martin Mevissen, Rudy Raymond, Andrea Simonetto, Stefan Woerner, and Elena Yndurain. “Quantum computing for finance: state of the art and future prospects”. IEEE Transactions on Quantum Engineering (2020).

- [13] Dylan Herman, Cody Googin, Xiaoyuan Liu, Alexey Galda, Ilya Safro, Yue Sun, Marco Pistoia, and Yuri Alexeev. “A survey of quantum computing for finance” (2022).

- [14] Sascha Wilkens and Joe Moorhouse. “Quantum computing for financial risk measurement”. Quantum Information Processing 22, 51 (2023).

- [15] Sam McArdle, Suguru Endo, Alan Aspuru-Guzik, Simon C Benjamin, and Xiao Yuan. “Quantum computational chemistry”. Reviews of Modern Physics 92, 015003 (2020).

- [16] Carlos Outeiral, Martin Strahm, Jiye Shi, Garrett M Morris, Simon C Benjamin, and Charlotte M Deane. “The prospects of quantum computing in computational molecular biology”. Wiley Interdisciplinary Reviews: Computational Molecular Science 11, e1481 (2021).

- [17] Prashant S Emani, Jonathan Warrell, Alan Anticevic, Stefan Bekiranov, Michael Gandal, Michael J McConnell, Guillermo Sapiro, Alán Aspuru-Guzik, Justin T Baker, Matteo Bastiani, et al. “Quantum computing at the frontiers of biological sciences”. Nature MethodsPages 1–9 (2021).

- [18] He Ma, Marco Govoni, and Giulia Galli. “Quantum simulations of materials on near-term quantum computers”. npj Computational Materials 6, 1–8 (2020).

- [19] Yudong Cao, Jhonathan Romero, and Alán Aspuru-Guzik. “Potential of quantum computing for drug discovery”. IBM Journal of Research and Development 62, 6–1 (2018).

- [20] Maria Schuld and Francesco Petruccione. “Supervised learning with quantum computers”. Volume 17. Springer. (2018).

- [21] Lov Grover and Terry Rudolph. “Creating superpositions that correspond to efficiently integrable probability distributions” (2002).

- [22] Almudena Carrera Vazquez and Stefan Woerner. “Efficient state preparation for quantum amplitude estimation”. Physical Review Applied 15, 034027 (2021).

- [23] Arthur G Rattew and Bálint Koczor. “Preparing arbitrary continuous functions in quantum registers with logarithmic complexity” (2022).

- [24] Thomas J Elliott and Mile Gu. “Superior memory efficiency of quantum devices for the simulation of continuous-time stochastic processes”. npj Quantum Information4 (2018).

- [25] Thomas J Elliott, Andrew JP Garner, and Mile Gu. “Memory-efficient tracking of complex temporal and symbolic dynamics with quantum simulators”. New Journal of Physics 21, 013021 (2019).

- [26] Thomas J Elliott. “Quantum coarse graining for extreme dimension reduction in modeling stochastic temporal dynamics”. PRX Quantum 2, 020342 (2021).

- [27] Kamil Korzekwa and Matteo Lostaglio. “Quantum advantage in simulating stochastic processes”. Physical Review X 11, 021019 (2021).

- [28] Ashley Montanaro. “Quantum speedup of monte carlo methods”. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 471, 20150301 (2015).

- [29] Patrick Rebentrost, Brajesh Gupt, and Thomas R Bromley. “Quantum computational finance: Monte carlo pricing of financial derivatives”. Physical Review A 98, 022321 (2018).

- [30] Nikitas Stamatopoulos, Daniel J Egger, Yue Sun, Christa Zoufal, Raban Iten, Ning Shen, and Stefan Woerner. “Option pricing using quantum computers”. Quantum 4, 291 (2020).

- [31] Ana Martin, Bruno Candelas, Ángel Rodríguez-Rozas, José D Martín-Guerrero, Xi Chen, Lucas Lamata, Román Orús, Enrique Solano, and Mikel Sanz. “Towards pricing financial derivatives with an ibm quantum computer” (2019).

- [32] Stefan Woerner and Daniel J Egger. “Quantum risk analysis”. npj Quantum Information 5, 1–8 (2019).

- [33] Carsten Blank, Daniel K Park, and Francesco Petruccione. “Quantum-enhanced analysis of discrete stochastic processes”. npj Quantum Information 7, 1–9 (2021).

- [34] Vittorio Giovannetti, Seth Lloyd, and Lorenzo Maccone. “Quantum random access memory”. Physical review letters 100, 160501 (2008).

- [35] Vittorio Giovannetti, Seth Lloyd, and Lorenzo Maccone. “Architectures for a quantum random access memory”. Physical Review A 78, 052310 (2008).

- [36] Fang-Yu Hong, Yang Xiang, Zhi-Yan Zhu, Li-Zhen Jiang, and Liang-Neng Wu. “Robust quantum random access memory”. Physical Review A 86, 010306 (2012).

- [37] David Applebaum. “Lévy processes-from probability to finance and quantum groups”. Notices of the AMS 51, 1336–1347 (2004). url: https://community.ams.org/journals/notices/200411/fea-applebaum.pdf.

- [38] David Lando. “On cox processes and credit risky securities”. Review of Derivatives research 2, 99–120 (1998).

- [39] Robert C Merton. “Applications of option-pricing theory: twenty-five years later”. The American Economic Review 88, 323–349 (1998). url: https://www.jstor.org/stable/116838.

- [40] Yue-Kuen Kwok. “Mathematical models of financial derivatives”. Springer Science & Business Media. (2008).

- [41] Fischer Black and Myron Scholes. “The pricing of options and corporate liabilities”. In World Scientific Reference on Contingent Claims Analysis in Corporate Finance: Volume 1: Foundations of CCA and Equity Valuation. Pages 3–21. World Scientific (2019).

- [42] Robert C Merton. “Option pricing when underlying stock returns are discontinuous”. Journal of financial economics 3, 125–144 (1976).

- [43] Hans U Gerber and Elias SW Shiu. “On the time value of ruin”. North American Actuarial Journal 2, 48–72 (1998).

- [44] Mark B Garman. “Market microstructure”. Journal of financial Economics 3, 257–275 (1976).

- [45] Ananth Madhavan. “Market microstructure: A survey”. Journal of financial markets 3, 205–258 (2000).

- [46] Hans U Gerber and Elias SW Shiu. “From ruin theory to pricing reset guarantees and perpetual put options”. Insurance: Mathematics and Economics 24, 3–14 (1999).

- [47] Olga Choustova. “Quantum-like viewpoint on the complexity and randomness of the financial market”. Coping with the Complexity of EconomicsPages 53–66 (2009).

- [48] Yutaka Shikano. “From discrete time quantum walk to continuous time quantum walk in limit distribution”. Journal of Computational and Theoretical Nanoscience 10, 1558–1570 (2013).

- [49] Yen-Jui Chang, Wei-Ting Wang, Hao-Yuan Chen, Shih-Wei Liao, and Ching-Ray Chang. “Preparing random state for quantum financing with quantum walks” (2023).

- [50] Steven A Cuccaro, Thomas G Draper, Samuel A Kutin, and David Petrie Moulton. “A new quantum ripple-carry addition circuit” (2004).

Appendix A Basic Circuits for Arithmetic and Distribution Preparation

Some basic arithmetic circuits and statistics distribution preparation circuits are given in this appendix.

A.1 Modified Quantum Subtractor

Although adder and subtractor circuits have been studied in many works(see [50] for reference), some modification is needed in our work as we wish to map to , i.e., store the result in the second register while leave the first register unchanged. The basic idea is as follows: since , X gates are introduced to calculate the complement of a as . Then a ripple-carry addition circuit is implemented to output the summation result on the first register . Finally, another sequence of X gates are put on the first register .

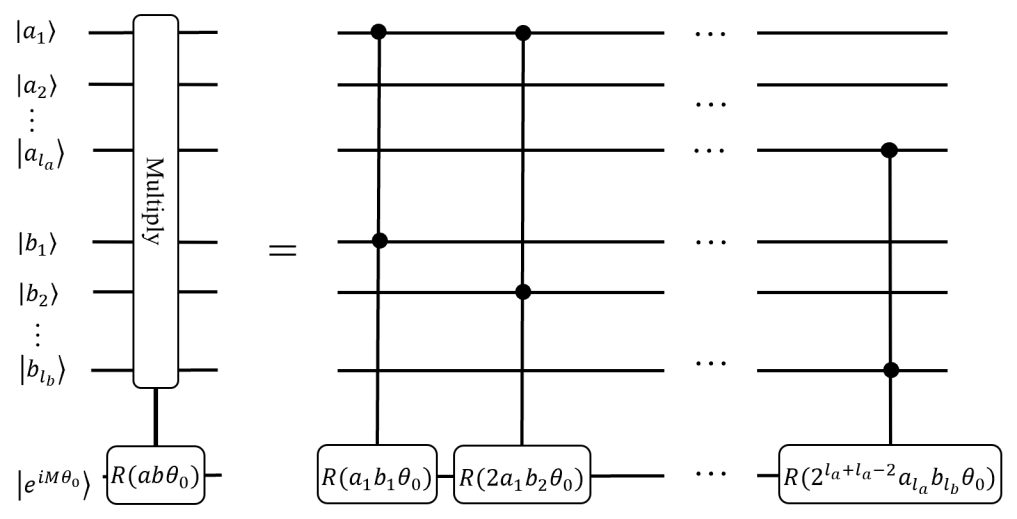

A.2 Quantum Multiplier for Amplitude Estimation and Quantum-Enhanced Monte Carlo

In this subsection, a quantum multiplier for quantum estimation, and hence quantum Monte Carlo is given as follows:

Lemma 9.

Suppose that and are -bit and -bit strings, respectively, and is an analog-encoded qubit, then the multiplication of and can be added to as , within controlled-rotation gates.

Proof.

The proof is directly: Given two bit strings and , their product can be computed as

Hence the term can be implemented by a rotation gate on the target qubit controlled by the and qubits of register and , where the rotation angle is determined by the index only. The final state is:

If and are signed integers, the rotation gates of two different directions should be controlled by the two sign qubits as well. The total number of controlled rotation gates is as claimed. ∎

A.3 State preparation for Statistical Distributions

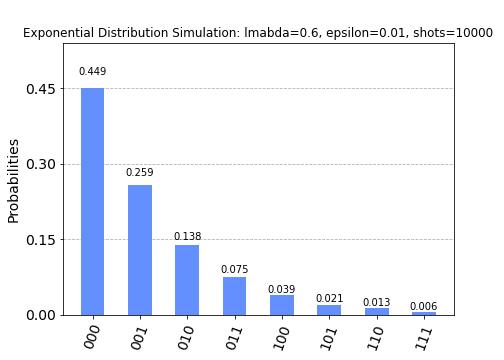

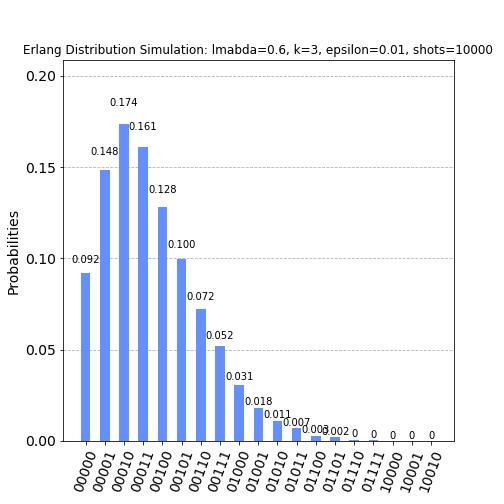

The exponential distribution is implemented by parallel rotation gates as illustrated in Figure 15(a). Detailed computation of rotation angles is given in Appendix B.1. The Erlang distribution is a summation of several exponential distributions and hence can be prepared via copies of exponential distribution preparation subcircuits together with a sequence of adder operators as shown in Figure 15(c). Corresponding simulation results are given in Figure 15(b) and 15(d), respectively.

Appendix B Proofs for QCTSP State Preparation Problem

B.1 Proof of Theorem 1

Proof.

By the definition of memory-less process, one has

and hence the c.d.f. satisfies:

Differentiating with respect to and setting leads to

Noticing that is a constant, the integrals of the two sides turn to be

where the constant is supposed to be exactly to satisfy . Thus the holding time follows an exponential distribution with determined by . As is given, without loss of generality, is supposed to be with so that

| (15) |

where

| (16) |

is a more strictly error bound which is easier to compute. On the truncated support set , simple computation shows that

| (17) |

Assuming that the preparation circuit consists of qubits initialized to be , the qubit is then aligned with the rotation gate with . A direct computation shows that

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (21) |

Here the binary number and the corresponding summation in Eq. (18) are both substituted by the decimal number varying from to in Eq. (19). Then Eq. (20) and Eq. (21) are derived by Eq. (16) and Eq. (17), respectively. Hence, with qubits and the same number of rotation gates, the desired truncated state is successfully prepared((as illustrated in Figure 15(a) and Figure 15(b))). ∎

B.2 Proof of Theorem 2

Proof.

Given a time interval , it can be uniformly divided into pieces with and , and the corresponding discrete random variables are denoted by . Then the increments and are independent and identically distributed random variables. The underlying distribution can be prepared by Grover’s method , where is the number of qubits of the approximation and is the probability amplitude that the random variable lies in the interval of with (see [21] for reference). The circuit depth of the preparation of is at most utilizing control-rotation gates. Then the increments sequence can be derived by repeating this procedure on parallel subcircuits: . The desired path variables are derived by a sequence of recursive add operators on these registers as (See Figure 4 (c)). Each add operator takes Toffoli gates and C-NOT gates. A simple computation shows that the circuit depth is and the gate complexity is at most gates. ∎

B.3 Proof of Corollary 3 and Corollary 4

Proof.

By definition of Poisson Point Process, the distinct increments are constant , and the varies exactly from to so that the adder subcircuit introduced in Theorem 2 can be omitted. As a consequent, each can be prepared parallel on at most qubits via rotation gates. And meanwhile the holding times are assumed to follow an exponential distribution , and can thus be prepared parallel, by Theorem1, on qubits via rotation gates with circuit depth . In summary, the qubit number, circuit depth and gate complexity are respectively , , and . As for the case of Compound Poisson Process, the only difference is the I.I.D. state space of jumps. Another qubits are introduced to record these jumps, and hence the qubits number turn to be . Instead of copies of Hadamard gates in Poisson point process, a sequence of adder operators are needed, asking for Toffoli gates and C-NOT gates. Thus the total gate complexity is , and the circuit depth is . ∎

B.4 Proof of Theorem 5

Proof.

Assuming that the pieces of the continuous Markov process are , and the transition time are , a direct computation shows that

| (22) |

This reveals that is totally determined by the previous state with the transition probabilities , and thus the embedded sequence is a discrete Markov chain as claimed above. By the Markov condition again, the holding time satisfies

| (23) |

Noticing that Eq. (23) is exactly the memory-less condition in Theorem1, and therefore follows an exponential distribution with the determined by the current state . As a consequence of the embedded discrete Markov chain and the exponential distribution holding time, a quantum continuous Markov process state can be prepared as follows: qubits are introduced for the storage of the discrete Markov chain, and another qubits are introduced for the holding time . The initial state is derived by control-rotation gates via Grover’s state preparation method. Following that, successive transition matrix operators, each of which consists of multi-controlled rotation gates, are applied to generate . The holding times can be prepared parallel, and each needs at most different exponential distribution with gates and circuit depth. In summary, the total number of gates is , and the circuit depth is . ∎

B.5 Proof of Theorem 6

Proof.

As shown in Figure 6, the preparation can be divided into two steps: Firstly, the stochastic process of intensity is prepared on parallel qubits, and the circuit depth is as given. Secondly, the holding time is prepared by a sequence of controlled- operators. Given a piece of Cox process and the corresponding fixed intensity , the holding time follows an exponential distribution as described in Theorem 1 so that it can be prepared within 1 circuit depth by rotation angles , where . As for varying digital-encoded , it can be divided into sequences of controlled-rotation gates with circuit depth. Hence the total circuit depth for preparing is . On the other hand, the preparation of increments can be implemented parallel with circuit depth. Thus the circuit depth of the preparation is . To derive or , adders are needed, with or , respectively. ∎

Appendix C Proofs for Information Extraction Problem

C.1 Proof of Theorem 7

Proof.

A direct computation shows that:

| (24) |

The expected value of Eq. (24) is evaluated as:

| (25) |

where can be derived via a quantum multiplication circuit introduced in Lemma 9 with complexity . The total circuit depth is (as shown in Figure 7 (c)). Noticing that the variables of in Eq. (25) can be evaluate through a standard procedure (one can see [28] for reference). To guarantee the theoretical closure, we shall sketch this procedure as follows. Suppose that the function can be truncated on an interval of length , then it can be extended to a function . The Fourier approximation of order for is denoted by , then Eq. (25) is evaluated as

| (26) |

Each term and in Eq. (26) can be evaluated via the standard amplitude estimation algorithm. Given the error bound , the circuit should be repeated times for each term. The total time complexity is hence ∎

C.2 Proof of Theorem 8

Proof.

A direct computation shows that:

where is a piece-wise integral on the interval with and , and is the increment. By exchanging the order of summation, one has that:

| (27) | ||||

| (28) |

where in Eq. (27) satisfies:

and in Eq. (28) satisfies:

Thus the expected value of Eq. (27) and Eq. (28) can be evaluated as

| (29) | ||||

| (30) | ||||

| (31) |

The state in Eq. (29) is a function of the variable , and hence can be computed via a operator on the qubit as illustrated in Figure 7 (d). And the directed area can be derived through a quantum multiplier introduced in Lemma 9 with complexity . In the same way the state in Eq. (30) is a function of the variable , and hence can be computed via a operator on the qubit. And the directed area can be derived with complexity (see Figure 7 (e) for reference). The total circuit depth is or . Noticing that the expression in Eq. (31) once again take the form of a summation, and thus can be solved through a standard procedure of amplitude estimation as mentioned above: The Fourier approximation of order for is denoted by , then Eq. (31) is evaluated as

| (32) |

Each term and in Eq. (32) can be evaluated via rotation operators on the target qubit controlled by together with a standard amplitude estimation subcircuit.(as shown in the box in Figure 7 (d) and Figure 7 (e). Given the error bound , the circuit should be repeated times for each term. The total time complexity is hence or for holding time and increment representation, respectively. ∎