remarkRemark \headersThe derivatives of Sinkhorn–Knopp convergeEdouard Pauwels and Samuel Vaiter

The derivatives of Sinkhorn–Knopp converge††thanks: Submitted .\fundingE. P. acknowledges the financial support of the AI Interdisciplinary Institute ANITI funding under the grant agreement ANR-19-PI3A-0004, Air Force Office of Scientific Research, Air Force Material Command, USAF, under grant numbers FA9550-19-1-7026, and ANR MaSDOL 19-CE23-0017-01. S. V. acknowledges the support ANR GraVa, grant ANR-18-CE40-0005.

Abstract

We show that the derivatives of the Sinkhorn–Knopp algorithm, or iterative proportional fitting procedure, converge towards the derivatives of the entropic regularization of the optimal transport problem with a locally uniform linear convergence rate.

keywords:

Optimal transport, Sinkhorn algorithm, Algorithmic differentiation65K10, 90B06, 40A30

1 Introduction

The optimal transport (OT) problem plays an increasing role in optimization and machine learning [26]. In particular, entropic regularization of OT has gained a lot of attraction by the existence of a simple and efficient algorithm introduced in [31], also known as matrix scaling or iterative proportional fitting procedure in the stochastic literature, see [28]. It is known that Sinkhorn–Knopp iterates converge linearly, with an explicit rate computable from the cost matrix, to the solution of entropic OT since the work of [16] introducing the use of the Hilbert metric.

1.1 Differentiation of the Sinkhorn–Knopp algorithm

Among the different properties of Sinkhorn–Knopp, a striking one is its differentiability with respect to the inputs. Differentiating the iterates of the Sinkhorn–Knopp algorithm is a common routine in machine learning. It was first used by [1] for ranking with linear objective function. They proposed to use backpropagation through Sinkhorn–Knopp iterates with respect to the cost matrix, without discussion of the convergence of the Jacobian. It was later used for different applications, such as computation of Wasserstein barycenters casted as an optimization problem [6], where backpropagation is performed with respect to the weight vector, for training generative models involving an OT loss as in [20, 17], definition of differentiable sorting procedures [13] or solving cluster assignments problems [8]. Popular libraries such as POT [15] or OTT [11] for computational optimal transport implement the backpropagation of Sinkhorn–Knopp. To mitigate the memory footprint required by backprogation, an alternative is to use implicit differentiation as discussed first by [24] for computing the derivatives of Sinkhorn divergences. This approach was later used in [12, 14]. To the best of our knowledge, even though some these works justify the correctness of using automatic differentiation for a given iterate, they do not consider the issue of the convergence of the derivatives computed by automatic differentiation.

1.2 Convergence of algorithmic differentiation

The issue of the convergence of the derivatives of an algorithm was considered in the automatic differentiation community. The linear convergence of derivatives was studied in [18, 19] for piggyback recursion and in [9, Theorem 2.3] for backpropagation. More recently, convergence of the derivatives of gradient descent [25, 23], the Heavy-ball [25] method or nonsmooth fixed point methods [5] were analyzed. All these analysis require explicitly, or implicitly, that the (generalized) Jacobians are strict contractions, i.e., Lipschitz continuous with a constant strictly lesser than 1. Unfortunately, the derivatives of Sinkhorn–Knopp do not enjoy this property.

1.3 Contribution

We prove (Theorem 3.3) that the derivatives of the iterates of Sinkhorn–Knopp algorithm converge towards the derivative of the entropic regularization of optimal transport, with an explicit expression of the derivative and with a locally uniform linear convergence rate, provided that all functions entering problem definition are twice continuously differentiable.

1.4 Organization

Our paper is organized as follows. Section 2 introduces the parameterized entropic regularized optimal transport problem with the Sinkhorn–Knopp algorithm and recalls linear convergence properties. In Section 3, we state our main result stating the convergence of the derivatives of Sinkhorn-Knopp towards the derivatives of the regularized optimal transport with a locally uniform linear convergence rate. Section 4 provides the proof of our result. Section 5 contains important intermediate results toward a linear rate for the convergence. Section 6 establishes miscellaneous lemmas that are used in the main proof.

1.5 Notations

The set of positive reals is denoted , of nonnegative reals and of nonzero reals . The simplex is the set of vectors of summing to 1

The identity matrix (of arbitrary size) is denoted by . For two vectors , the entry-wise (Hadamard) division is defined as , and the product is defined as , for all . The 1-vector is the vector only composed of 1’s. When the context is clear, and to lighten the notations, for should be understood as . Given a function , we extend its domain as by applying it entrywise, that is for , , for all . Given and a continuously differentiable function , we denote by its Jacobian matrix (or tensor) at , i.e.,

where is the canonical basis of . Given a differentiable function , we denote by the total derivative at , that is

where and are the partial derivatives of .

2 Entropic optimal transport and Sinkhorn–Knopp algorithm

2.1 Entropic regularization

We consider a parametric formulation of the entropic OT111We recover the standard formulation letting be constant functions.. The entropic regularization of optimal transport associated to the parameterized marginals and of level for the parameterized cost matrix reads for

| () |

where , is the set of admissible couplings (also called transportation polytope)

and is the entropic regularization of the coupling matrix defined as

where if , by continuous extension. Note that defined in () is -strongly convex, hence () has a unique minimizer222The (strict) positivity follows from assumptions and . Indeed, is feasible for (), with strictly positive entries, therefore Slater’s qualification condition holds for () and the required form follows from necessary and sufficient KKT conditions for the (attained) optimum, see for example [10, Lemma 2] . We will assume that all functions entering problem definition are twice continuously differentiable.

2.2 Sinkhorn–Knopp algorithm

The Sinkhorn–Knopp algorithm is built upon the fact [30, Theorem 1] that the unique solution of () has the form for all and

| (1) |

for positive numbers , , and . The goal is thus to find positive vectors and , such that

| (2) |

In its most elementary formulation, the Sinkhorn–Knopp algorithm, also called matrix scaling problem algorithm, has the following alternating updates,

| (3) |

starting from a couple , see [32] for a discussion on initializations strategies. Even though in practice it is not necessary to evaluate it at each iteration, one can use (1) to form a current guess at iteration as .

2.3 Reduced formulation of Sinkhorn–Knopp

We will analyse an equivalent version of (3) by considering a single iterate and performing the change of variable . Given an initilization , this results in rewriting (3) as the recursion in the “log-domain”

| () |

where

Note that this formulation is close to the dual formulation of () as explained in [26, Remark 4.22], but we will not need duality results along this paper.

We will work under the following standing assumption

Assumption \thetheorem (Data are continuously differentiable).

It is possible to get back to the scaling factors and from the reduced variable as

Using the relationship (1), the optimal coupling matrix can be approximated as

| (4) |

and we construct transport plan estimates associated to each iterate, for all ,

| (5) |

It is known that converges linearly [16] to the optimal transport plan for (). The next paragraph is dedicated to study the linear convergence of the reduced variable .

2.4 Linear convergence of the centered reduced iterates

It is known that converges to a limit , with a linear rate in the Hilbert metric [16], see also [26, Theorem 4.2], whereas we are concerned with the convergence of the reduced iterates in the “log-domain”. In order to study the convergence of , let us introduce the linear map which associates to its centered version:

| (6) |

To analyze the convergence rate of Sinkhorn-Knopp algorithm, it is standard to use the Hilbert projective metric [4] defined on as

where is the variation seminorm of defined as

| (7) |

The next lemma shows the (local) linear convergence in norm of the centered reduced variable .

Lemma 2.1 (Local linear convergence of ).

The centered reduced variable converges linearly, locally uniformly, to , i.e., there exists and continuous such that all and ,

Furthermore, is continuous on .

Proof 2.2.

We combine the linear convergence result on of [16] with Lemma 6.5, following the suggestion of [26, Remark 4.12].

We clarify below how to combine these arguments. We first show that the linear convergence of is such that for all there exists and such that for all

and the mapping and are continuous. Indeed, [16, Theorem 4] ensures that for all ,

where is the contraction ratio defined for as

Remark that and enjoy the relation

and . Using [26, Theorem 4.2], we deduce that

where

Since for all , and is continuous, we have that is continuous, and since is assumed to be continuous on , is also continuous. Thus, and depend continuously on the initial condition and problem data () which are all continuous functions of . Therefore the linear convergence is actually locally uniform in .

To conclude the proof, we need to remark that the Hilbert projective metric on corresponds to the variation seminorm after the change of variable so that for all and all ,

and Lemma 6.5 provides

which is the claimed result.

Regarding the continuity, let , for all and all , we have

We may choose such that the first two terms are as small as desired uniformly for in a neighborhood of . The last term is continuous in and evaluates to for so that reducing the neighborhood if necessary allows to choose it as small as desired, which proves continuity.

Note that Lemma 2.1 does not imply the linear convergence of . As we will see later in Lemma 4.6, this is not an issue to our objective – proving the convergence of the derivatives of () – because derivatives of the algorithm enjoy a directional invariance which makes them equal when evaluated at or .

3 Derivatives of Sinkhorn–Knopp algorithm and their convergence

3.1 Derivatives of the transport plan

Remark that for all , is an matrix. Hence, is a map from to and is a map from to . Thus, we identify its partial derivatives with third-order tensors:

| (8) |

Left multiplication by these derivatives is considered as follows, for arguments of compatible size: for any , and for any , for some , , both operations being compatible with the usual identification of vectors as single rows in . This multiplication is assumed to be compatible with the rules of differential calculus, for example, if is , then we have the identity, for any ,

| (9) |

The operation is also invariant with order of products, if , then

3.2 Spectral pseudo-inverse

In order to explicitly describe the derivative of , we will use the following notion of pseudo-inverse of a diagonalizable matrix.

Definition 3.1 (Spectral pseudo-inverse [29, 3]).

Given a diagonalizable matrix , let be a diagonalization, where is invertible and is diagonal. The spectral pseudo-inverse of is given by where denotes Moore-Penrose pseudo-inverse.

The Moore-Penrose pseudo-inverse of a diagonal matrix is given by if and 0 otherwise. The key property of the spectral pseudo-inverse is that it preserves the eigenspaces of , contrary to the more standard Moore–Penrose pseudo-inverse which preserve eigenspaces only in special cases such as symmetric matrices.

Lemma 3.2 (Eigenspaces presevation of spectral pseudo-inverse [29]).

Let a diagonalizable matrix. Then, and have the same kernel and the remaining eigenspaces are the same with inverse eigenvalues.

Note that this definition and result are defined even for non-diagonalizable matrices in [29] using its Jordan reduced form, but for the sake of our results, we only need this property for diagonalizable matrices.

3.3 Main result

Our contribution is the following.

Theorem 3.3 (The derivatives of Sinkhorn–Knopp converge).

Under Assumption 2.3, let the limit of Sinkhorn–Knopp iterations () initialized by for all .

Then, the optimal coupling matrix is continuously differentiable and its derivative is given by

where , are the components of the total derivative of at , i.e.,

(resp. ) is defined in () (resp. (4)), and partial derivatives of are described in Section 3.1. Here denotes the spectral pseudo-inverse of a diagonalizable matrix (Definition 3.1).

Furthermore, is continuously differentiable for all and the sequence of derivatives converges at a linear rate, locally uniformly in . In particular, for all ,

Remark 3.4 (Relation to previous works).

The differentiability of the Sinkhorn–Knopp iterations is an elementary and well-known fact, used for example in [1], the new contribution here being that the derivatives converge toward the derivative of entropic regularization (). Using an alternative formulation (in the context of implicit differentiation), [14] proves the differentiability of the entropic regularization of OT (first part of Theorem 3.3), and obtained an alternative expression of the derivative. They do not however prove the convergence of the derivatives, that is the main concern of our work and the expression for the derivative in Theorem 3.3 was not mentioned in previous literature, to our knowledge.

If was a strict contraction mapping, applying [18, Proposition 1] would be sufficient to conclude and obtain the same expression as in Theorem 3.3 with an inverse instead of the spectral pseudo-inverse. This is unfortunately not the case, and a more refined analysis is necessary to obtain the convergence. The main intuition behind this analysis is that Sinkhorn iterations are equivariant with respect to scaling of , and the optimal solution in (4) is invariant with respect to the same scaling. In terms of derivative, it produces a lack of invertibility of but the corresponding direction does not depend on , and precisely lies in the kernel of for all . This “alignment” allows to maintain an overall convergence of derivatives. Section 4 is dedicated to prove this intuition rigorously.

Remark 3.5 (Limitations of our result).

Despite the generality of Theorem 3.3, we would like to point out two limitations:

-

1.

We do not have any guarantees for the convergence of the derivatives of the iterates , . Said otherwise, we have guarantees for the derivatives of the optimal transport plan , not for the derivatives of the scaling factors , or the derivatives of the reduced variable .

-

2.

Inspecting the proof of Theorem 3.3, the linear convergence factor is a where is an upper bound on both the linear convergence factor of the iterates (Lemma 2.1) and the second largest eigenvalue of at the solution, call it . Classical discrete dynamical system arguments (see [26, Remark 4.5] on local linear convergence) suggest that the linear convergence factor of the iterates is asymptotically of order . Taking this into consideration, our proof suggest an asymptotic linear convergence factor of the order for the derivatives, a factor strictly greater than that of the sequence. This discrepancy is a consequence of Lemma 5.3 which we use for simplicity of the presentation which requires a non-asymptotic analysis to ensure uniformity in . However, removing uniformity, this could be improved to obtain pointwise an asymptotic linear convergence factor arbitrarily close to using Lemma 6.7 instead, combined with arguments outlined in [26, Remark 4.5].

Remark 3.6 (Application to automatic differentiation of Sinkhorn–Knopp).

Given and , forward automatic differentiation [33] allows to evaluate , e.g., Jacobian-Vector Products (JVP), just by implementing () in a dedicated framework. Similarly, given , the reverse mode of automatic differentiation [22], also called backpropagation, computes , e.g., a Vector-Jacobian Product (VJP). Using a similar argument as in [5], it is possible, thanks to Theorem 3.3, to prove the convergence of these quantities. Note that in practice, the object of interest is not necessarly by itself, but its composition by another function, e.g., to compute the primal Sinkhorn divergence, to compute the OT loss, a sum of similar terms when dealing with Wasserstein barycenters [2], or any function where is a continuously differentiable function. Applying our result (Theorem 3.3) and the chain rule leads to the same convergence of automatic differentiation for such quantities.

Remark 3.7 (Differentiation with respect , , or ).

Theorem 3.3 is presented with an abstract parameterization of the problem with variable . Choosing different values for allows to obtain derivatives of for as well as with respect to the original transport problem data: , , or . These are typically evaluated numerically by algorithmic differentiation, but one could get closed form expressions in simple cases. For example choosing , we have

Similarly, setting , we have

One could also compute derivatives with respect to the cost matrix or , but the corresponding expressions become more complicated, and the use of automatic differentiation alleviates this difficulty in practice.

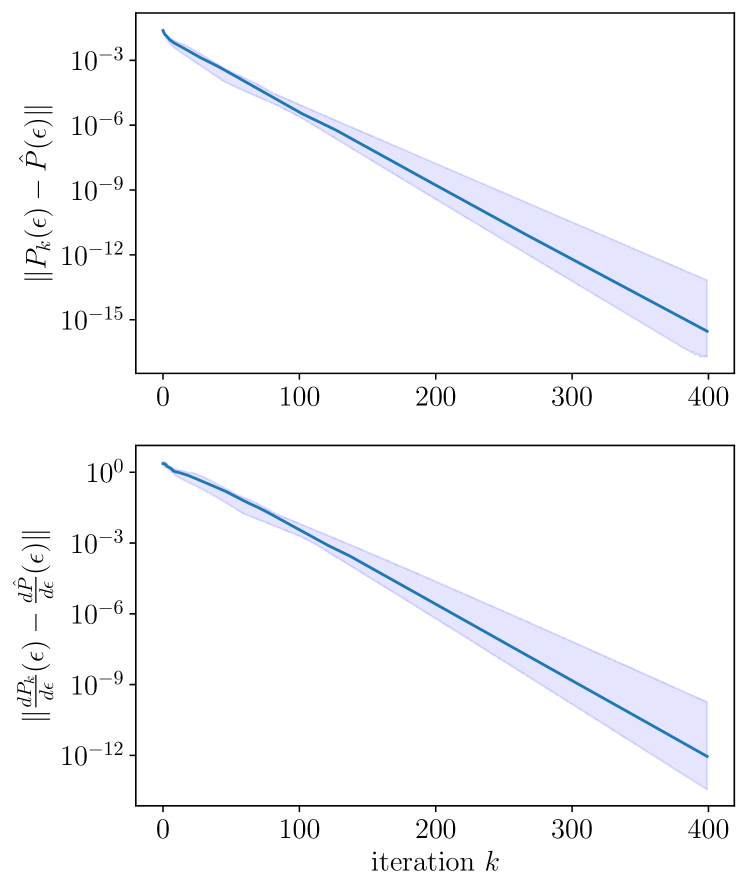

Remark 3.8 (Numerical illustration).

Figure 1 illustrates a simple example where is an Euclidean cost matrix between two point clouds in of size and . The starting point cloud follows a uniform law in the square and the target a uniform law on a circle inscribed in the square. The marginals are two uniform histograms and . Sinkhorn–Knopp algorithm () is automatically differentiated with the Python library jax [7] with respect to the parameter , and we record the median of 10 trials for . The blue filled area represents the first and last deciles. We run the algorithm for a high number of iterations and display both

Note we assume here that (resp. ) is close enough the optimal solution (resp. ) such that it is a good proxy. In particular, we ran () up to machine precision.

4 Proof of Theorem 3.3

Before diving into the proof, we are going to provide important spectral properties of the Jacobians of the algorithm and transport plan (Section 4.1), then introduce a proxy for the Jacobian of that is a contraction mapping in contrast of (Section 4.2) and finally rewrite (9) thanks to (Section 4.3).

4.1 Eigendecomposition of the transport plan and Jacobian

The following lemma provides important properties of the Jacobians of and as a function of . Here is fixed and we look at properties of the derivative with respect to , hence the dependency in does not appear.

Lemma 4.1 (Expression of the Jacobian of ).

Proof 4.2.

-

1.

We note that for all so that . This implies that .

-

2.

The first expression is a direct computation observing that if is an entry-wise function, then where is again applied entry-wise. Indeed, we have for , , which in turns gives . Then, we obtain the derivatives of the ratio

Similarly, since is a linear operator,

Finally, since , for a differentiable , we obtain that

The second expression uses the definition of in (4). Observe that

(10) and (using the fact that diagonal matrices commute)

(11) Observe now that,

(12)

Remark 4.3.

We have the following result on the eigenvalues and eigenvectors of .

Lemma 4.4 (Eigendecomposition of ).

For any , is diagonalisable on . is an eigenvalue with multiplicity and the other eigenvalue have modulus strictly smaller than . Furthermore, one has the following eigenvectors:

Proof 4.5.

Fix and let

The matrices and are diagonal with positive entries and is symmetric such that . Setting , we have, using the fact that diagonal matrix commute

and therefore is real symmetric, hence diagonalisable with real eigenvalues. As a consequence, being similar to it has the same property. It is an easy calculation to check that . Indeed, , and since for , we have that and then . Multiplicity of the eigenvalue as well as properties of the remaining eigenvalue is a consequence of Perron–Frobenius theorem [21, Theorem 8.2.8 and Theorem 8.3.4] applied to the stochastic matrix .

Let us prove the last identity. We have

from which we deduce

This concludes the proof.

4.2 Reduced partial Jacobian of

For any , we set

| (13) |

For any consider furthermore the block decomposition of the total derivative of , and set

| (14) |

We call the reduced partial Jacobian of . From Lemma 4.4, we have that is an eigenvector of and is an eigenvector of , both with eigenvalue , which has multiplicity , with . Therefore Lemma 6.1 ensures that the matrix is diagonalisable in the same basis as with the same eigenvalues, except eigenvalue which is set to , and therefore its spectral radius is strictly less than . Later in the proof, we will study a recursion involving (which is not a contraction), and we will use an equivalent recurrence involving (which is a contraction). By Assumption 2.3, the functions are continuously differentiable on .

The following lemma shows that and are invariant by the centering operation , and more generally by translation of .

Lemma 4.6 (Invariance by centering).

For all , , and , we have,

In particular, and where is the centering operator introduced in Lemma 2.1.

Proof 4.7.

We have for and ,

which implies for all , . Observe now that

Thus, and in turn, we get that .

To conclude, we have

following the fact that , and in particular .

4.3 Preliminary computation

We start with some computation and notations before providing the proof arguments. Setting for all , and , we have the piggyback recursion

| (15) |

We have for all and , using (9) for the total derivative of ,

| (16) |

For all and all , we have , we set

where is defined in (14) and is defined in (13). From Lemma 6.1, the matrix is diagonalisable in the same basis as with the same eigenvalues except eigenvalue which is set to and therefore its spectral radius is strictly less than .

From Lemma 4.1, we have for all and therefore

Plugging this in (16), we obtain

This allows to rewrite the iterations equivalently, with , for all and , using the product rule for partial derivatives of defined in Section 3.1,

| (17) |

We are now ready to prove our main result.

Proof 4.8 (Proof of Theorem 3.3).

Convergence of , and . For all , from Lemma 2.1, the centered iterates converge with a linear rate to which is locally uniform in . Furthermore, using Assumption 2.3, is twice continuously differentiable jointly in and and therefore and are continuously differrentiable, and hence locally Lipschitz on .

We remark that for all , using Lemma 4.6

so that, as , converges with a locally uniform linear rate to . Similarly converges with a locally uniform linear rate to and converges with a locally uniform linear rate to . Note that by Lemma 2.1, the map is continuous, so that , and are continuous functions of .

For any , is digaonalizable with spectral radius strictly less than , the recursion on should converge with a locally uniformly linear rate in . This assertion is a consequence of the following lemma which explicit the constants appearing in the linear rate for the matrix recursion.

Lemma 4.9 (Explicit rate for linear convergence).

Let and be diagonalisable on , with spectral radius smaller than and and an invertible matrix which rows are made of an eigenbasis of . Let . Let and be sequences of matrices such that there exists a constant such that for all ,

| (18) | ||||

| (19) |

Then, for the recursion

setting , there exists a continuous function such that for all ,

Convergence of . Let us explicit how Lemma 4.9 allows to prove convergence of . Start with a fixed , we first drop the dependency in for clarity. We have from Remark 4.3

Setting , we have that

which is symmetric. Therefore, there is an orthogonal matrix and diagonal matrix such that

and

Set , we have by submultiplicativity of

Similarly . From Lemma 6.1, diagonalizes both and .

Getting back the dependency in , we fix , and set for all

where is given in Lemma 2.1 and is the largest eigenvalue, in absolute value, of , which is smaller than and continuous with respect to . In particular, is continuous.

Fix a compact set which contains in its interior and a compact set which contains for all and (this exists thanks to Lemma 2.1). We set such that where is the constant in Lemma 2.1 and is a Lipschitz constant of and on (recall that they are continuously differentiable). Using Lemma 4.6, we have for all and ,

and

The largest eigenvalue of is at most so that Lemma 4.9 applies, and we have for all and all ,

where is continuous. All terms in the right hand side are continuous functions of and can be uniformly bounded on , so that at a locally uniform linear convergence rate.

Convergence of the derivatives of Sinkhorn–Knopp towards the derivatives of entropic regularization. From Lemma 4.9 the limit of is of the form

Recall that for any , and any , so that . Therefore expression (17) is equivalently rewritten as

We have shown locally uniform linear convergence of both and , by Assumption 2.3, equation (LABEL:eq:autodiffModifiedCentered) is continuously differentiable, hence it has a locally Lipschitz dependency in and , so that as uniformly linearly in a neighborhood of

| (21) |

Note that converges pointwise towards which is a solution to problem (). By local uniform convergence of derivatives and the fact that are continuously differentiable, thanks to Lemma 6.3, we have that is continuously differentiable and

Expression of the derivative. Finally, by construction of in (14) and thanks to Lemma 6.1, we have for all , that and have the same eigenspaces all eigenvalues being nonzero except the one generated by for which corresponds to eigenvalue for and for . Therefore, we have , where is the normalized eigenvector of associated to eigenvalue (see (13)). Recall that denotes the spectral pseudo-inverse for diagonalisable matrices (Definition 3.1). From Lemma 4.1, we have for all , therefore for all ,

We have therefore that

which concludes the proof.

5 Proof of Lemma 4.9

We start with two lemmas on real sequences. The first one is a quantitative version of [27, Lemma 9, Chapter 2].

Lemma 5.1 (Quantitative Gladyshev convergence).

Let and be positive summable sequences and be a positive squence such that for all

Then for all ,

Proof 5.2.

For all , set

Remark that using concavity of logarithm , so that is well defined. Remark also that for all .

The sequence is decreasing, indeed, we have for all ,

Therefore, for all ,

and the result follows.

The following lemma specify Lemma 5.1 when and are geometric sequences.

Lemma 5.3 (Application of Gladyshev’s convergence to geometric sequences).

Let , , and be a positive sequence such that for all ,

| (22) |

Then, is a geometric sequence: for all ,

Proof 5.4.

Lemma 5.5 (Reduced perturbated convergence).

Let and have operator norm smaller than and . Let and be a sequence of matrices such that there exists a constant such that for all ,

Then for the recursion

setting , we have

Proof 5.6.

Note that is invertible and it follows that the potential limit is , as it is a fixed point of the limiting recursion, . We rewrite the recursion as follows

Setting for all , , using the fact that is subordinate to , we have the recursion,

Note that . Since

we apply Lemma 5.3 with and use the fact that and .

Proof 5.7 (Proof of Lemma 4.9).

Note that is invertible and it follows that the potential limit is , which satisfy . Since is diagonalisable in the basis given by , there is a diagonal matrix such that . We rewrite equivalently the recursion as follows

and setting , and for all , this reduces to

When , we have , which has operator norm at most and . Set the fixed point of the limiting recursion for ,

Furthermore for all , we have the following bounds

| ( is submultiplicative) | ||||

| (by hypothesis (18)) | ||||

| ( is subordinate to ) | ||||

| (by hypothesis (19)) | ||||

We apply Lemma 5.5 with

which gives for all ,

which is the desired result

6 Additional lemmas

In the following, we prove some technical, but important, lemmas used in the main proof.

Lemma 6.1 (Reduced eigenspace).

Let be diagonalisable. Let be such that and such that , and assume that eigenvalue is simple, and that . Then and have the same eigenspaces with the same eigenvalues, except eigenvalue for which is set to for .

Proof 6.2.

of the form for an invertible and a diagonal matrix . Assume that the first diagonal entry of is . Columns of form an eigenbasis and we may impose that the first column is . Rows of form an eigenbasis of , set the vector corresponding to the first row. Since is a simple eigenvalue, the corresponding eigenspace has dimension and there exists such that . We have by assumption and because , this shows that and therefore is the first row of .

We have and therefore . Let be a different column of corresponding to an eigenvector of associated to eigenvalue , we have so that . This concludes the proof.

Lemma 6.3 (Uniform convergence leads to continuous differentiable limit).

Let be open and be a sequence of continuously differentiable functions from to converging pointwise to , such that converges pointwise, locally uniformly on . Then is continuously differentiable on and .

Proof 6.4.

Let the pointwise limit. By local uniform convergence, is continuous on . Fix any and any and set a closed interval such that for all and is in the interior of (such interval exists because is open). The sequence of univariate functions is continuously differentiable and satisfy for all and all

The derivatives converge uniformly on to which is continuous in . Therefore the function is continuously differentiable with derivative given by , by uniform convergence of derivatives. Since and were arbitrary, this implies that admits continuous partial derivatives and it is therefore continuously differentiable with gradient .

Proof 6.6.

Note that for and , . Set , we have so that

This implies the following

Now , so that which concludes the proof.

Lemma 6.7.

Let , and be a positive sequence such that for all ,

| (23) |

Then, for all , such that , we have

Proof 6.8.

Fix to be chosen latter. Dividing (23) on both sides by , we have for all ,

Setting for all ,

we apply Lemma 5.1 to obtain the result. As and are geometric sequences, we have and , so that for all ,

Since was arbitrary, the preceding holds for all and . Fix such that . Setting , since , we have

We have

and

Therefore, for all ,

proving our claim.

Acknowledgments

E.P. and S.V. would like to thank Jérôme Bolte for fruitful and inspiring discussions. S.V. thanks Jeremy Cohen and Titouan Vayer for raising the issue of the convergence of the derivatives of the Sinkhorn–Knopp iterates during a seminar in Lyon, France.

References

- [1] R. P. Adams and R. S. Zemel, Ranking via sinkhorn propagation, 2011, https://arxiv.org/abs/1106.1925.

- [2] M. Agueh and G. Carlier, Barycenters in the wasserstein space, SIAM Journal on Mathematical Analysis, 43 (2011), pp. 904–924.

- [3] A. Ben-Israel and T. N. Greville, Generalized inverses: theory and applications, vol. 15, Springer Science & Business Media, 2003.

- [4] G. Birkhoff, Extensions of jentzsch’s theorem, Transactions of the American Mathematical Society, 85 (1957), pp. 219–227.

- [5] J. Bolte, E. Pauwels, and S. Vaiter, Automatic differentiation of nonsmooth iterative algorithms, arXiv preprint arXiv:2206.00457, (2022).

- [6] N. Bonneel, G. Peyré, and M. Cuturi, Wasserstein barycentric coordinates: Histogram regression using optimal transport, ACM Transactions on Graphics, 35 (2016), https://doi.org/10.1145/2897824.2925918.

- [7] J. Bradbury, R. Frostig, P. Hawkins, M. J. Johnson, C. Leary, D. Maclaurin, G. Necula, A. Paszke, J. VanderPlas, S. Wanderman-Milne, and Q. Zhang, JAX: composable transformations of Python+NumPy programs, 2018, http://github.com/google/jax.

- [8] M. Caron, I. Misra, J. Mairal, P. Goyal, P. Bojanowski, and A. Joulin, Unsupervised learning of visual features by contrasting cluster assignments, in NeurIPS, vol. 33, 2020, pp. 9912–9924.

- [9] B. Christianson, Reverse accumulation and attractive fixed points, Optimization Methods and Software, 3 (1994), pp. 311–326.

- [10] M. Cuturi, Sinkhorn distances: Lightspeed computation of optimal transport, in NeurIPS, vol. 26, 2013.

- [11] M. Cuturi, L. Meng-Papaxanthos, Y. Tian, C. Bunne, G. Davis, and O. Teboul, Optimal transport tools (ott): A jax toolbox for all things wasserstein, arXiv preprint arXiv:2201.12324, (2022).

- [12] M. Cuturi, O. Teboul, J. Niles-Weed, and J.-P. Vert, Supervised quantile normalization for low-rank matrix approximation, in ICML, 2020.

- [13] M. Cuturi, O. Teboul, and J.-P. Vert, Differentiable ranking and sorting using optimal transport, in NeurIPS, vol. 32, 2019.

- [14] M. Eisenberger, A. Toker, L. Leal-Taixé, F. Bernard, and D. Cremers, A unified framework for implicit sinkhorn differentiation, in CVPR, 2022.

- [15] R. Flamary, N. Courty, A. Gramfort, M. Z. Alaya, A. Boisbunon, S. Chambon, L. Chapel, A. Corenflos, K. Fatras, N. Fournier, L. Gautheron, N. T. Gayraud, H. Janati, A. Rakotomamonjy, I. Redko, A. Rolet, A. Schutz, V. Seguy, D. J. Sutherland, R. Tavenard, A. Tong, and T. Vayer, Pot: Python optimal transport, Journal of Machine Learning Research, 22 (2021), pp. 1–8.

- [16] J. Franklin and J. Lorenz, On the scaling of multidimensional matrices, Linear Algebra and its Applications, 114-115 (1989), pp. 717–735, https://doi.org/https://doi.org/10.1016/0024-3795(89)90490-4.

- [17] A. Genevay, G. Peyré, and M. Cuturi, Learning generative models with sinkhorn divergences, in AISTAT, vol. 84, 2018, pp. 1608–1617.

- [18] J. C. Gilbert, Automatic differentiation and iterative processes, Optimization Methods and Software, 1 (1992), pp. 13–21, https://doi.org/10.1080/10556789208805503.

- [19] A. Griewank, C. Bischof, G. Corliss, A. Carle, and K. Williamson, Derivative convergence for iterative equation solvers, Optimization Methods and Software, 2 (1993), pp. 321–355, https://doi.org/10.1080/10556789308805549.

- [20] T. Hashimoto, D. Gifford, and T. Jaakkola, Learning population-level diffusions with generative rnns, in ICML, vol. 48, 2016, pp. 2417–2426.

- [21] R. A. Horn and C. R. Johnson, Matrix analysis, Cambridge University Press, Cambridge, second ed., 2013.

- [22] S. Linnainmaa, Taylor expansion of the accumulated rounding error, BIT Numerical Mathematics, 16 (1976), pp. 146–160.

- [23] J. Lorraine, P. Vicol, and D. Duvenaud, Optimizing millions of hyperparameters by implicit differentiation, in AISTAT, vol. 108, 2020, pp. 1540–1552.

- [24] G. Luise, A. Rudi, M. Pontil, and C. Ciliberto, Differential properties of sinkhorn approximation for learning with wasserstein distance, in NeurIPS, vol. 31, 2018.

- [25] S. Mehmood and P. Ochs, Automatic differentiation of some first-order methods in parametric optimization, in AISTAT, 2020, pp. 1584–1594.

- [26] G. Peyré and M. Cuturi, Computational optimal transport, Foundations and Trends in Machine Learning, 51 (2019), pp. 1–44, https://doi.org/10.1561/2200000073.

- [27] B. Polyak, Introduction to optimization, in Optimization Software, Publications Division, Citeseer, 1987.

- [28] L. Ruschendorf, Convergence of the Iterative Proportional Fitting Procedure, The Annals of Statistics, 23 (1995), pp. 1160 – 1174, https://doi.org/10.1214/aos/1176324703.

- [29] J. E. Scroggs and P. L. Odell, An alternate definition of a pseudoinverse of a matrix, SIAM Journal on Applied Mathematics, 14 (1966), pp. 796–810.

- [30] R. Sinkhorn, A Relationship Between Arbitrary Positive Matrices and Doubly Stochastic Matrices, The Annals of Mathematical Statistics, 35 (1964), pp. 876 – 879.

- [31] R. Sinkhorn, Diagonal equivalence to matrices with prescribed row and column sums, The American Mathematical Monthly, 74 (1967), pp. 402–405.

- [32] J. Thornton and M. Cuturi, Rethinking initialization of the sinkhorn algorithm, 2022, https://doi.org/10.48550/ARXIV.2206.07630.

- [33] R. E. Wengert, A simple automatic derivative evaluation program, Commun. ACM, 7 (1964), p. 463–464, https://doi.org/10.1145/355586.364791.