Strategic Asset Allocation with Illiquid Alternatives

Abstract

We address the problem of strategic asset allocation (SAA) with portfolios that include illiquid alternative asset classes. The main challenge in portfolio construction with illiquid asset classes is that we do not have direct control over our positions, as we do in liquid asset classes. Instead we can only make commitments; the position builds up over time as capital calls come in, and reduces over time as distributions occur, neither of which the investor has direct control over. The effect on positions of our commitments is subject to a delay, typically of a few years, and is also unknown or stochastic. A further challenge is the requirement that we can meet the capital calls, with very high probability, with our liquid assets.

We formulate the illiquid dynamics as a random linear system, and propose a convex optimization based model predictive control (MPC) policy for allocating liquid assets and making new illiquid commitments in each period. Despite the challenges of time delay and uncertainty, we show that this policy attains performance surprisingly close to a fictional setting where we pretend the illiquid asset classes are completely liquid, and we can arbitrarily and immediately adjust our positions. In this paper we focus on the growth problem, with no external liabilities or income, but the method is readily extended to handle this case.

1 Introduction

There is considerable investor interest across several financial contexts in constructing portfolios which mix liquid and illiquid assets, especially illiquid alternative investments. We wish to perform strategic asset allocation to asset classes that include illiquid alternative assets, as well as more liquid asset classes. Several challenges arise. First, we can only augment our illiquid positions by making capital commitments. Moreover, these commitments only indirectly affect our illiquid position through uncertain and delayed capital calls, that we have no direct control over. A further challenge is the solvency requirement: we should be able to fund the capital calls from our liquid positions with very high probability. A simple strategy to guarantee coverage of capital calls is to keep an amount equal to the uncalled capital commitments in cash. However this creates significant cash drag, since this cash could be invested in higher returning liquid assets. The method we describe in this paper addresses all of these issues.

2 Previous work

There is a rich history of studying portfolio construction. Our work helps extend the modern portfolio theory framework developed by Markowitz [Mar52] and Merton [Mer69], which focuses on liquid assets. We contribute to the further study of illiquidity and multi-period planning. While this work takes as an input a stochastic model which describes the risk and return of illiquid investments, calibrating such models is a nuanced and well studied problem. For a guide to the literature on the risks and returns of private equity investments, see Kortweg [Kor19].

Continuous time.

There is a breadth of work on modeling portfolio construction with illiquid assets. Many authors consider continuous time stochastic processes. Dimmock et al. study the endowment model, under which university endowments hold high allocations in illiquid alternative assets, via a continuous time dynamic choice model with deterministic-in-time discrete liquidity shocks every periods [DWY19]. They allow the investor to increase the position in the illiquid asset instantaneously, not modeling the delayed nature of capital calls. Ang et al. also study a continuous time problem, but model the timing of liquidity events of the illiquid asset as an independent Poisson process [APW13]. Optimal solutions are assumed to have almost surely non-negative liquid wealth, meaning that the investor must always be able to cover the effects of illiquidity. Another important line of inquiry studies the effects of illiquidity through the commitment risk of a fixed alternative’s commitment. Sorensen, Wang, and Yang [SWY14] study this problem by focusing on an investor who can modify their positions in stocks and bonds, taking an investment in an illiquid asset as given and held to maturity.

Discrete time.

The discrete time case is also well studied. Takahashi and Alexander first introduced what amounts to a deterministic linear system to model an illiquid asset’s calls, distributions, and asset value [TA02]. This model posits that calls are a time-varying fraction of uncalled commitments, and that distributions are a time-varying fraction of the illiquid asset value, and returns are constant. Our model is similar, but differs in two important ways. First, our model is time-invariant. Second our model incorporates randomness in these fractions as well as the returns. Giommetti and Sorensen use the Takahashi and Alexander model in a standard, discrete-time, infinite-horizon, partial-equilibrium portfolio model to determine optimal allocation to private equity [GS21]. Here the calls and distributions are deterministic fractions of the uncalled commitments and illiquid asset value, but the illiquid asset value grows with stochastic returns. Again, there is an almost sure constraint which insists that the investor’s liquid wealth is never exhausted, which means that the investor maintains a liquidity reserve of safe assets to cover calls.

Optimal allocation to illiquid assets.

Broadly, across the literature we have reviewed, the reported optimal allocations to illiquid assets are strikingly low compared to the de facto wants and need of institutional investors who are increasingly allocating larger and larger shares of their portfolios to illiquid alternatives. In their extensive survey of Illiquidity and investment decisions, Tédongap and Tafolong [TT18] report that recommended illiquid allocations range from the low single digits to around 20% on the upper end. This is strikingly lower than the target levels observed in practice. For example, the National Association of College and University Business Officers (NACUBO) provide data showing the allocation weights of illiquid alternatives in University endowments reaching 52% in 2010. Unlike other analyses, our method does not require investors be able to cover calls with probability one, and instead provides a tool for maintaining an optimized target asset allocation under uncertain calls, distributions, returns, and growth.

Hayes, Primbs, and Chiquoine propose a penalty cost approach to asset allocation whereby an additional term is added to the traditional mean-variance optimization (MVO) problem to compensate for the introduction of illiquidity [HPC15]. They solicit a user provided marginal cost curve which captures the return premium needed for an illiquid asset to be preferred over a theoretically equivalent liquid alternative. This leads to a formulation nearly identical to the standard MVO problem, with a liquidity-adjusted expected return (a function of the allocation). In their work the notion of liquidity is captured in a scalar between and .

Multi-period optimization.

Our policy is based on solving a multi-period optimization problem. Dantzig and Infanger [DI93] introduce a multi-stage stochastic linear programming approach to multi-period portfolio optimization. Mulvey, Pauling, and Madey survey the advantages of multi-period portfolio models, including the potential for variance reduction and increased return, as well as the ability to analyze the probability of achieving or missing goals [MPM03]. Boyd et al. [BBDK17] describe a general framework for multi-period convex optimization. This framework focuses on planning a sequence of trades over a set of periods trades given return forecasts, trading costs, and holding costs. Our framework also solves a multi-period convex optimization problem, but we do not make an approximation of the dynamics, which is more appropriate for the longer time horizons and thus more significant growth observed in strategic asset allocation.

Model predictive control.

Our method falls under the category of Model Predictive Control (MPC), which is both widely studied in academia and used in industry. For a survey of MPC, see for example the books Model Predictive Control [CA07] or García et al. [GPM89]. Herzog et al. [HKD+06] use an MPC approach for multi-period portfolio optimization, but only consider normally distributed returns and standard liquid assets. They do include a factor model of returns, as well as a conditional value at risk (CVaR) constraint which is different in interpretation but takes the same form as our insolvency constraint. The closest work we have identified to our own is the thesis of Lee, who uses a very similar multi-period optimization problem with linear illiquid dynamics [Lee]. We both use a quadratic risk, and use certainty equivalent planning to solve an open loop control problem. Lee’s problem is multi-period, but the objective is a function of only the final period wealth, whereas in our case we have stage costs, as well as constraints on the solvency of our portfolio. Additionally, in our stochastic model we use random call and distribution intensities.

Contributions.

The linear dynamics of the illiquid wealth motivate model predictive control (MPC) as a solution method. To the best of our knowledge, there do not exist multi-period optimization-based policies for constructing portfolios with both liquid and illiquid alternative assets. We believe our contributions include the following.

-

1.

Incorporating random intensities with the classic linear model of the illiquid asset’s calls and distributions.

-

2.

Formulating a multi-period optimization problem to perform strategic asset allocation with liquid and illiquid assets.

-

3.

Using homogeneous risk constraints to account for growth in the multi-period planning problem.

-

4.

Using liquidity/insolvency constraints to ensure calls are covered with high probability.

-

5.

Obtaining a performance bound for the problem by considering a stylized liquid world where the illiquid asset is completely liquid.

3 Stochastic dynamic model for an illiquid asset

In this section we describe our stochastic dynamic model of one illiquid asset. Our model is closely related to the linear system proposed by Takahashi and Alexander [TA02], with the addition of uncertainty in the capital calls and distributions. We demonstrate a straightforward extension of our model which would include the Takahashi model in §8. We consider a discrete-time setting, with period denoted by , which could represent months, quarters, years, or any other period. Our model involves the following quantities, all denominated in dollars.

-

•

is the illiquid wealth (or position in or NAV of the illiquid asset) at period .

-

•

is the total uncalled commitments at period .

-

•

is the capital call at period .

-

•

is the distribution at period .

-

•

is the amount newly committed to the illiquid asset at period .

The commitment is the only variable we can directly control or choose. All the others are affected indirectly by .

Dynamics.

Here we describe how the variables evolve over time. At period ,

-

•

we make a new capital commitment (which we can choose)

-

•

we receive capital call (which is not under our control)

-

•

we receive distribution (which is not under our control)

The uncalled commitment in period is

and the illiquid wealth in period is

where is a random total return on the illiquid asset.

Calls and distributions.

We model calls and distributions as random fractions of and . We model calls as

where is the random immediate commitment call intensity and is the random existing commitment call intensity. Similarly, we model distributions as

where is the random distribution intensity.

We assume the random variables are I.I.D., i.e., independent across time and identically distributed. (But for fixed period , the components , , , and need not be independent.) We do not know these random variables when we choose the current commitment . Formally, we assume that . The current commitment can depend on anything known at the beginning of period (including for example past values of returns and intensities), but the current period return and intensities are independent of the commitment.

3.1 Stochastic linear system model

The model above can be expressed as a linear dynamical system with random dynamics and input matrices. With state and the control or input , the dynamics are given by

where

| (1) |

With output , we have

where

| (2) |

We assume the initial state is known. We observe that , since the former depends on the initial state, , and for , and these are all independent of .

A careful reader might notice that these linear dynamics mean that the commitments and distributions asymptotically approach zero but never terminate. However, the fractions of calls and distributions relative to the initial amounts are minuscule after several periods, and are negligible in the presence of new commitments coming in each period. Additionally, Gupta and Van Nieuwerburgh [GN21] found in analyzing long-term private equity behavior that often funds have activity even fifteen years after inception, further justifying the persisting calls and distributions in the linear systems model.

3.2 Mean dynamics

Let denote the mean of the state, denote the mean of the input or control, and denote the mean of the output. We define the mean matrices

(which do not depend on ). We then have

| (3) |

which states that the mean state and output is described by the same linear dynamical system, with the random matrices replaced with their expectations. The mean dynamics is a time-invariant deterministic linear dynamical system.

3.3 Impulse and step responses

Our linear system model implies that the mapping from the sequence of commitments or inputs to the resulting outputs is linear but random. We review three standard concepts from linear dynamical systems.

Commitment impulse response.

We can consider the response of uncalled commitments, calls, illiquid wealth, and distributions to committing at period and for all , with zero initial state. This is referred to as the impulse response of the system. The impulse response is the stochastic process

From the mean dynamics (3), we know that the mean impulse response is given by

Commitment step response.

We can also consider the effect of committing , which is referred to as the step response of the system. The step response shows how a simple policy of constant commitment impacts our exposure over time in the illiquid asset, calls, distributions, and our level of uncalled commitment. The step response is the stochastic process

From the mean dynamics (3), we know that the mean step response is given by

| (4) |

Steady state response.

We define the unit steady-state mean response as . Assuming the spectral radius of is less than one, we take the limit of (4) as to obtain

We refer to the entries of

| (5) |

as the steady state gains from commitment to illiquid wealth, uncalled commitment, capital calls, and distribution. These numbers have a simple interpretation. For example, tells us what the asymptotic mean illiquid wealth is, if we repeatedly make a commitment of $1. It can be shown that , i.e., if we constantly commit $1, then asymptotically, and in mean, the capital calls will also be $1.

3.4 A particular return and intensity distribution

We suggest the following parametric joint distribution for . They are generated from a random 3-vector

| (6) |

From these we obtain

| (7) |

With this model, the return is log-normally distributed while the call and distribution intensities are logit-normally distributed. Dependency among the return and the intensities are modeled by the off-diagonal entries of .

3.5 Example

Here we describe a particular instance of the distribution described above, that we will use in various numerical examples in the sequel.

Example return and intensity distribution.

In this example we use the following parameters for the distribution of specified in (6):

| (8) |

This example is based on yearly periods. The mean return of the illiquid asset is derived from the BlackRock Capital Market Assumptions as of July 2021, which reports one private equity asset, Buyout, with a mean annual return of 15.8% [Bla21]. The call and distribution mean intensities are calibrated from private equity data for the eFront Buyout fund. The mean values of the intensities are we report the empirical means

(These are found by Monte Carlo simulation, since the mean of a logit-normal distribution doesn’t have an analytical expression.) The covariance matrix is calibrated from the same data.

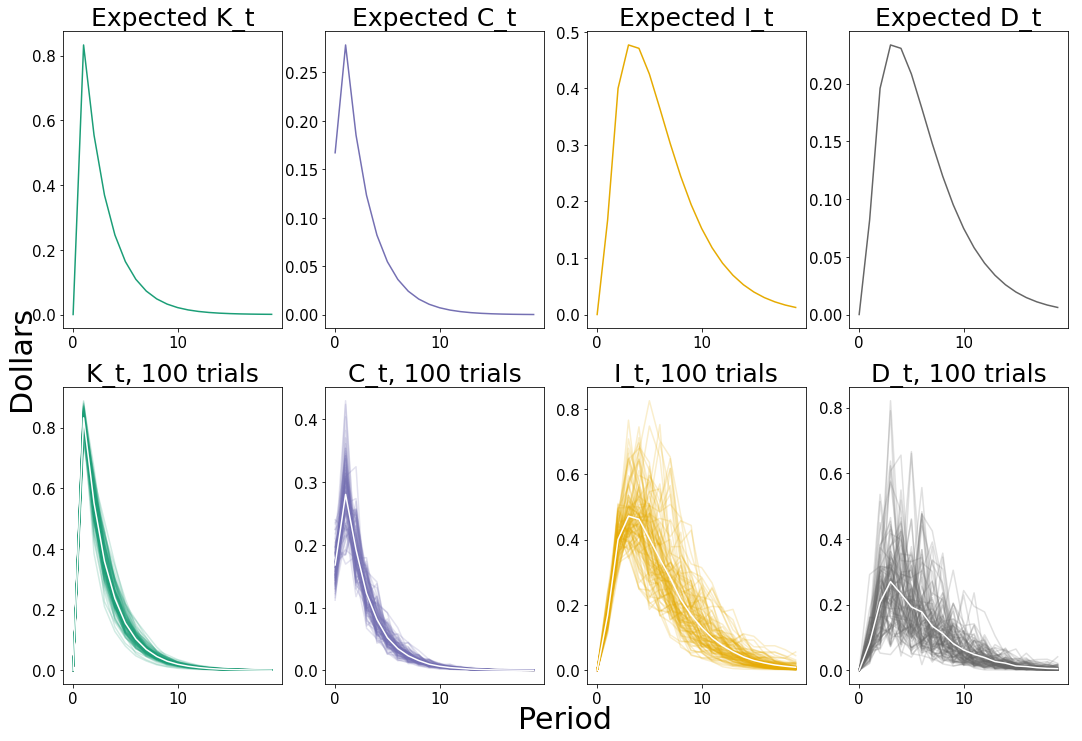

Commitment impulse response.

The impulse response from commitment to uncalled commitment, calls, illiquid wealth, and distributions is shown in figure 1. The top row shows the mean response, and the bottom shows 100 realizations, with the empirical mean shown as the white curve.

We see that the uncalled commitments peak in the next period at a level of about 0.8. The calls peak at the next period at .28. We can see that our initial commitment translates into an illiquid holding which, in expectation, peaks four periods later with a value of about .47. Similarly, the resulting distributions peak with the illiquid wealth four periods later, with a level of .24.

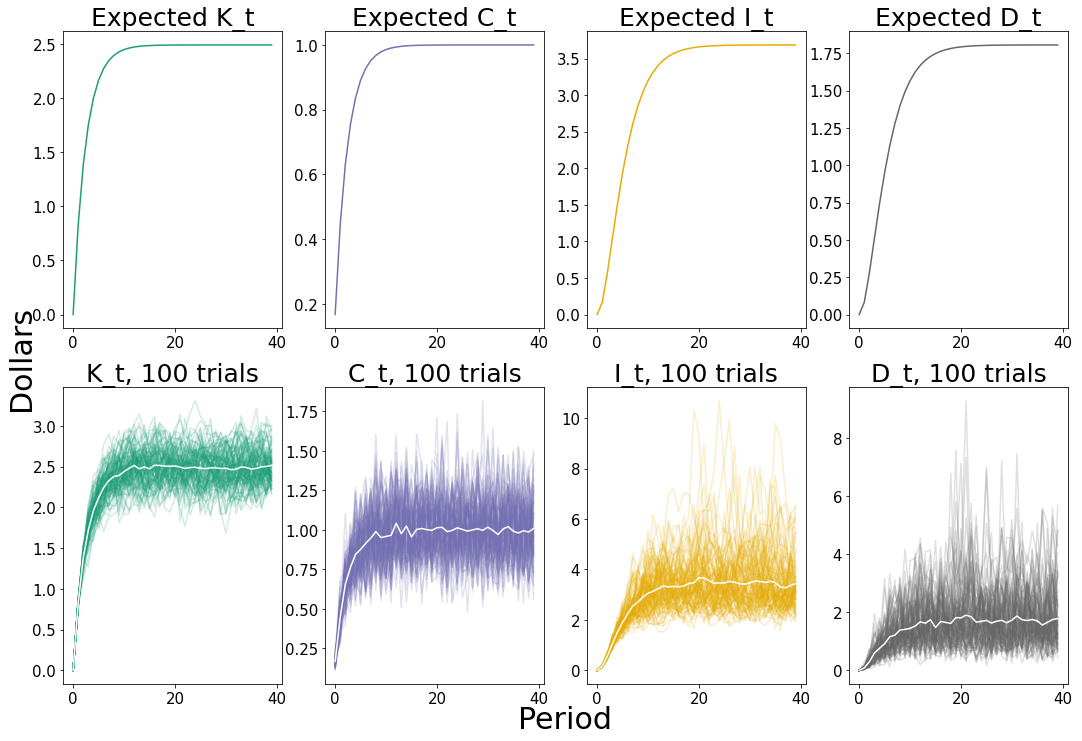

Commitment step response.

In figure 2, we see the step response to constant unit commitment of uncalled commitments, calls, illiquid wealth, and distributions. The top row shows the mean response, and the bottom shows 100 realizations. The mean step responses converge in around 8 periods to values near their asymptotic values.

Asymptotic expected response to constant commitment.

The steady-state gains are

For example, repeatedly committing $1 leads to an asymptotic mean illiquid wealth of $3.685.

3.6 Comparison with the Takahashi and Alexander model

Our stochastic model of an illiquid asset is closely related to that of Takahashi and Alexander [TA02], but it differs in to key ways. The most important difference is that our model is Markovian; the calls, distributions, and returns at time are conditionally independent of the all previous quantities, given the state at time . In comparison, Takahashi and Alexander’s model specifies time varying call and distribution intensity parameters. These time varying intensities mean that the final intensities can be set to 1, meaning calls and distributions can have deterministic end times, and the exposure will not geometrically decline. In §8 we describe how to modify our model to depend on arbitrarily many previous time periods. This means we can exactly capture the original Takahashi and Alexander model with this extension of our model. We emphasize that this generalization remains fully tractable from the portfolio optimization standpoint described in this paper. The second difference between our model and that of Takahashi and Alexander is that ours is a stochastic model, with random intensities, whereas theirs is deterministic.

4 Commitment optimization

Because the dynamics is linear, we can use convex optimization to choose a sequence of commitments to meet various goals in expectation. We consider a simple example here to illustrate.

We consider the task of starting with no illiquid exposure or uncalled commitments, i.e., , , and choosing a sequence of commitments, , . Our goal is to reach and maintain an illiquid wealth of , so we use as our primary objective the mean-square tracking error,

In addition, we want a smooth sequence of commitments, so we add a secondary objective term which is the mean square difference in commitments,

We also impose a maximum allowed per-period commitment, i.e., . (Of course we can add other constraints and objective terms; this example is meant only to illustrate the idea.)

We illustrate two methods. The first is simple open-loop planning, in which assume that state follows its mean trajectory, and we determine a fixed sequence of commitments, and then simply execute this plan. The second method is a closed-loop method, which adapts the commitments based on previously realized returns, capital calls, and distributions. This method is called model predictive control (MPC). We evaluate both policies under the mean dynamics and the stochastic dynamics.

4.1 Open loop commitment control

Planning.

We will find a plan of commitments based on the mean dynamics. This leads to the convex optimization problem

where is a hyperparameter that determines the weight of the smoothing penalty, and and are as defined in (2). The variables in this problem are and , with for . We use the notation , , to emphasize that these are quantities in our plan, and not the realized values. This is a simple convex optimization problem, a quadratic program (QP), and readily solved [BV04].

Example.

Solving this problem with our running example defined in (8) for

| (9) |

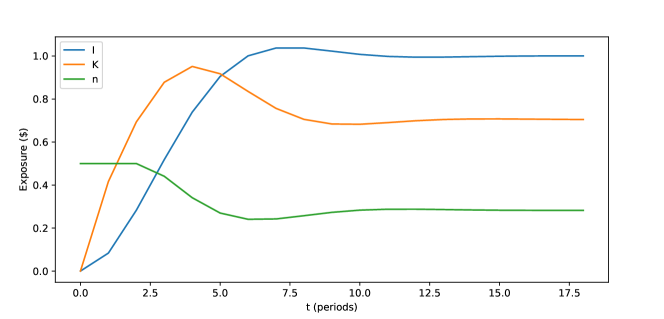

we find the optimal planned sequence of commitments and corresponding uncalled commitment and exposure shown in figure 3.

The mean-squared tracking error attained by our plan is 0.133. We can also calculate the tracking error from onwards to account for the large contribution to tracking error of the first four periods. Thus, a perhaps more meaningful metric is the delayed root-mean-square (RMS) tracking error,

(This is on the same scale as and is readily compared to it.) The plan attains a delayed RMS tracking error of 0.071.

The optimal commitment sequence makes sense. It hits the limit for the first two periods, in order to quickly bring up the illiquid wealth; then it backs off to a lower level by around period , and finally converges to an asymyptotic value near , which is the constant commitment value that would asymptotical give mean illiquid value .

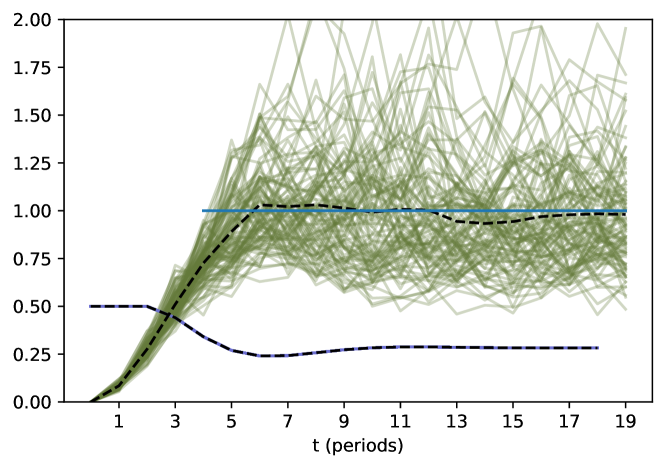

Results.

These results above are with the mean dynamics. We can also execute this sequence of planned commitments under random calls and distributions as specified by our stochastic model in §3.5. The results for 100 simulated realizations is shown in figure 4. The mean-squared tracking error, averaged across the realizations, is 0.199. The delayed root-mean-square tracking error, averaged across the realizations is 0.274.

4.2 Closed loop commitment control via MPC

We now perform model predictive control, which is a closed loop method, meaning can depend on , i.e., we can adapt our commitments to the current values of uncalled commitments and illiquid wealth.

Planning.

At every time , we plan commitments over the next periods , where is a planning horizon. We use to indicate that these are the quantities in the plan at time , from the plan made at time . These planned quantities are found by solving the optimization problem

with variables and , Note that when we plan at time , we include the constraint ; this closes the feedback loop by planning based on the current realized state.

Policy.

Our policy is simple to explain: at time , after planning as described above, we execute control

Note that the planned quantities , , , and , , are never executed by the MPC policy. They are only part of the plan.

Results.

We again execute our policy under random calls and distributions as specified by our stochastic model in §3.5. The results for 100 simulated trajectories a shown in figure 5. The average mean-squared error is 0.182. The average delayed root-mean-square tracking error is 0.244, an 11% reduction from the open loop policy.

5 Joint liquid and illiquid model

We now describe a model for an investment universe consisting of multiple illiquid alternative and liquid assets. First, we extend to a universe of illiquid assets.

Multiple illiquids.

We extend the same quantities as in §3 from scalars to vectors of dimension .

We have the exact same dynamics as before, duplicated for each illiquid asset. Each has its own states for exposure and uncalled commitment, and its own control for its new commitments. The illiquid calls, distributions, and returns are now part of a joint distribution. The illiquid dynamics extend in vectorized form to

with

We emphasize that while the return, call, and distribution dynamics here are separable across the illiquid assets, the underling random variables can be modeled jointly. We continue with our assumption that these random variables are independent across time.

Multiple liquids.

There are now a set of liquid assets available to us. The liquid assets are simple: we can buy and sell them at will at each period; they suffer none of the complex dynamics of the illiquid assets. We add one new state, , the (total) liquid wealth at period . In addition to new commitments for each illiquid asset, at each time we now control how we allocate our liquid wealth each period, as well as how much outside cash to inject into our liquid wealth. Thus we have the additional quantities, which we can control:

-

•

is the allocation in dollars invested in liquid assets at period

-

•

is the outside cash injected at period

At the beginning of period , we invest (or allocate) our liquid wealth in liquid assets. This corresponds to the constraint . We receive multiplicative liquid returns on liquid asset , yielding total return . We then pay out capital calls from and receive distributions to our liquid wealth, for all illiquid assets. This corresponds to a net increase in liquid wealth given by . Lastly, if at this stage our liquid wealth is negative, we are forced to add outside cash to at least bring our liquid wealth to zero. Compactly, the liquid dynamics are

with constraints

5.1 Stochastic linear system model

We can again represent these dynamics as a stochastic linear system. Let be the state vector. The control is . Extending the and matrices from §1, define

| (10) |

Then the random linear dynamics with multiple illiquids and liquids are

with constraints

The presence of the outside cash control implies that a feasible control exists for any feasible value of the states, since prevents the liquid wealth from ever being negative.

As in §3.2, we let denote the mean of the state, denote the mean of the input or control, define the mean system matrices as

and recover the same mean dynamics

| (11) |

5.2 Return and intensity distribution

6 Strategic asset allocation under the relaxed liquid model

In this section we introduce a highly simplified model, where all of the challenges of illiquid alternative assets are swept under the rug. This model is definitely not realistic, but we can use it to develop an unattainable benchmark for performance that can be obtained with the more accurate model.

6.1 Relaxed liquid model

As a thought experiment, we imagine the illiquid assets are completely liquid: we have arbitrary control of illiquid asset positions (immediate increase or decrease). This is a relaxation of the actual problem setting, where we must face stochastic and only indirectly controllable calls and distributions. The idea of a relaxed liquid model is not new; for example, Giommetti et al. [GS21] consider the target allocations resulting from treating illiquid assets as fully liquid for comparison, but do not evaluate stochastic control policies trying to achieve these allocations in an illiquid world. The relaxed liquid model is also implicitly behind various Captial Market Assumptions, where return ranges, and correlations, are given for both liquid and illiquid assets.

The relaxed liquid model is very simple. There is only one state, the total wealth . The quantities we have control over are the allocations to liquid and illiquid assets, denoted and . The wealth evolves according to the dynamics

where is defined in (12).

We use the standard trick of working with the weights of the allocations in each period, denoted , instead of . This is defined as , so . We recover the dollar allocations as .

6.2 Markowitz allocation and policy

A standard way to choose a portfolio allocation is to solve the one period risk-constrained Markowitz problem,

| (13) |

where is the maximum tolerable return standard deviation, and and are the expected return and return covariance, respectively. We denote the optimal allocation as . The natural policy associated with solving the Markowitz problem simply rebalances to : it sets for each period . This simple rebalancing is of course not possible under the accurate model that includes the challenges of alternative assets, but it is under the relaxed liquid model.

6.3 Example

Liquid performance.

Under the assumptions of §6.1, we solve the one period Markowitz problem with the mean and covariance of the joint distribution of liquid, illiquid asset returns. Using this relaxed Markowitz target, we simulate the fantasy performance achieved by being able to perfectly rebalance both liquids and illiquids to the Markowitz target each period, for multiple periods, using the policy described earlier in 6.2.

Risk-return trade-off.

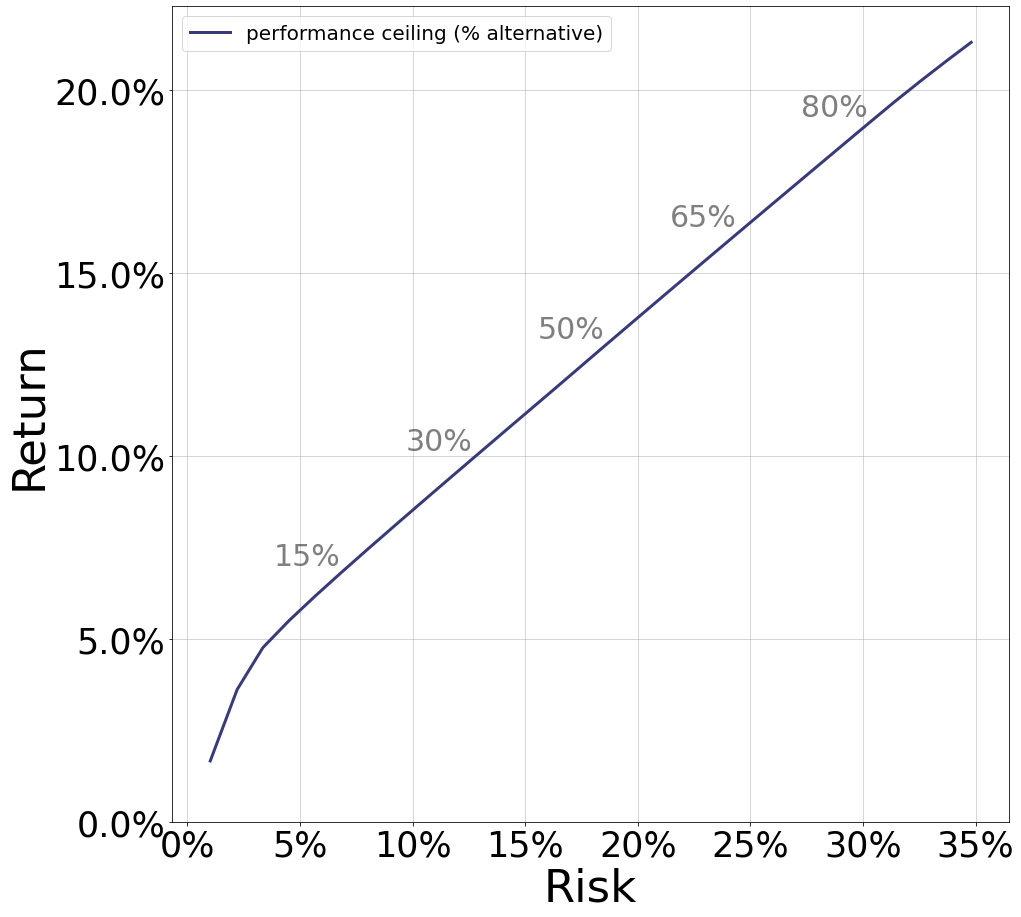

By solving the Markowitz problem with these parameters across a range of values for the risk tolerance (which give rise to corresponding Markowitz targets), we can create a risk-return trade-off plot, shown in figure 6. We should consider this trade-off curve as an unattainable performance benchmark, that we can only strive to attain when the challenges of illiquid alternatives are present.

7 Strategic asset allocation with full illiquid dynamics

In §6, we describe an approach to strategic asset allocation for portfolios including an imagined class of illiquid alternatives which are rendered completely liquid. In this section, we provide methods to perform strategic asset allocation with mixed liquid and illiquid alternative portfolios where we can only augment our illiquid position by making new commitments, and the effect of this action is random and delayed. First, we describe a method which over time establishes and then maintains a given target allocation under growth. Then, we describe a more sophisticated MPC method which jointly selects a target allocation based on a user’s risk tolerance, establishes the target, and maintains the target in growth.

7.1 Steady-state commitment policy

We first describe a simple policy, which seeks to track a target allocation . It allocates liquid assets proportionate to its desired liquid allocation, and makes new commitments of a target level of illiquid wealth scaled by the asymptotic expected private response to constant commitment. The input is a target allocation , current liquid wealth L and illiquid wealth I. First, the policy checks if is negative. If it is, it returns control

Otherwise, if the liquid wealth is positive, the policy proceeds as follows. First, the policy rebalances the liquid holdings proportionately to ,

where are the liquid and illiquid blocks of the allocation vector , respectively. Then, with as the 1 dollar private commitment step response defined in (5), and as the target illiquid level, , the policy commits

and returns control .

7.2 Model predictive control policy

We now describe a more sophisticated policy which plans ahead based on a model of the future, seeking to maximize wealth subject to various risk constraints. For a sequence of prospective actions, the policy forecasts future state variables using the mean dynamics described in (11). The policy then chooses a sequence of actions by optimizing an objective which depends on the planned actions and forecast states. Finally, the policy executes solely the first step of the planned sequence. The impact of that action is observed, and the resulting state is observed, and then this cycle repeats.

The policy selects a planned sequence of actions by trying to maximize the ultimate total liquid and illiquid wealth. However, it is also constrained by a user’s risk tolerance, which caps the allowable per period return volatility. Additionally, because capital calls are stochastic in nature, the policy seeks to guarantee that with high probability, all capital calls can be funded from the liquid wealth.

Modified Markowitz constraint.

Motivated by the standard one period risk-constrained Markowitz problem (13), we would like to include a risk constraint in our planning problem. However, the Markowitz problem has variables in weight space rather than wealth space. Other multi-period optimization problems based on the Markowitz problem, such as in [BBDK17], assume a timescale over which the wealth does not grow significantly over the planning horizon. In our case, since potential application contexts include endowments and insurers, we must handle substantial growth over the investment horizon. Thus, we consider an analogous risk constraint in wealth space rather than weight space,

is the liquid and illiquid exposure. Thus, we use the constraint

which is invariant in wealth. It is also convex, which means that problems with such constraints can be reliably solved.

Insolvency constraint.

An important challenge in performing strategic asset allocation with illiquid alternatives is ensuring that the probability of being unable to pay a capital call is extremely low. In our model, this corresponds to requiring

for a small probability of failure . We make several approximations to facilitate a convex constraint. First, we approximate as a multivariate normal random variable,

It is important to note that these parameters are the mean and covariance of the liquid returns, rather than the mean and covariance which parameterize the log normal liquid return distribution given by and in (12). Then we assume we receive the expected calls , which is a linear function of our controls. They are given by . Finally, we assume pessimistically there are no distributions or outside cash. With these approximations, we have

This probabilistic constraint holds if and only if

| (17) |

where is the standard normal cumulative distribution function. This constraint is convex provided , since then , and (17) is a second order cone constraint (see [BV04, §4.4.2]).

As mentioned above, the constraint (17) is pessimistic because it assumes no distribution. An alternative and less pessimistic formulation of the insolvency constraint would consider the distribution, the calls, and the liquid returns all under a joint normal approximation.

Smoothing penalty.

Among control sequences with similar objective values, we would like for new commitments to be fairly smooth across time. We can consider a natural commitment smoothing penalty

The time discount appears because in a growth context we expect to increase over time. Additionally, it helps account for the increased uncertainty of future planned steps.

MPC planning problem.

All objective terms and constraints outlined above are consolidated into one optimization problem. At time , we plan , , where is the planning horizon, by solving the optimization problem

| (18) |

where is a hyperparameter penalizing outside cash use. Recall that , , and are components of , and , , and are components of .

7.3 Example

In this example, we evaluate the performance of the two policies described in §7.1 and §7.2 using the risk return trade off. For the parameters defined in (12), we use the specific values of

| (19) | |||||

| (20) | |||||

| (21) |

with .

Illiquid dynamics.

Example policy specifications.

In this case study, we use the steady state commitment policy with parameters

and values of arising from solving the one period Markowitz problem defined in 6.2 for 30 evenly spaced values of between 0 and .3, with our specified return distribution parameters defined in (14–16).

For the MPC policy, we use the same values described above, but for numerical reasons use the standard trick of moving the risk limit to penalized form by subtracting

from each term of the objective defined in (18), penalizing excess risk. The parameter values are

with as defined in (11), with the distributions instantiated in (8) and (19–21).

Results.

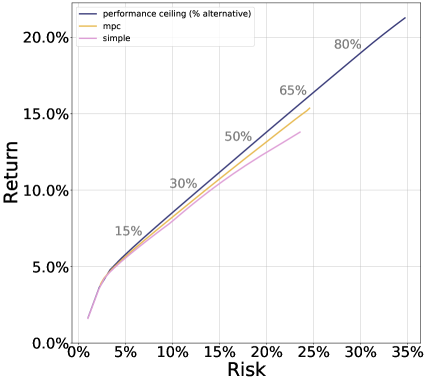

We see in figure 7 that both the MPC and heuristic policies are extremely close to the risk-return performance of the liquid relaxation, which is an unattainable benchmark. This is despite the challenging illiquid dynamics we face in the non-relaxed setting.

The performance stated here is averaged across 20 periods of simulation, for 200 simulated trajectories.

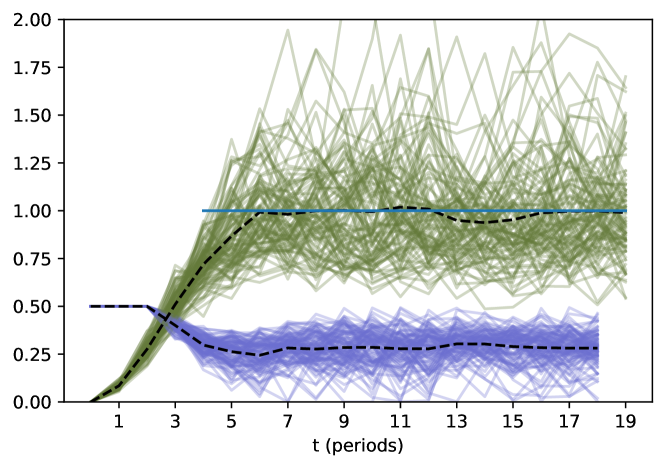

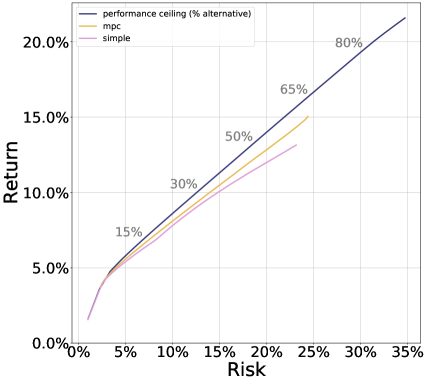

We can also examine the performance across a shorter time horizon. figure 8 shows the same risk-return tradeoff for 10 periods. Evidently, there is a larger gap between the MPC policy and the liquid performance ceiling, and also between the MPC and simple policies. This has a perfectly clear interpretation: because there is a roughly 4 period delay before peak illiquid exposure (see figure 1), the impact of the illiquid alternative asset’s high returns is delayed. Additionally, by planning ahead, the MPC policy achieves illiquid exposure faster than the simple policy.

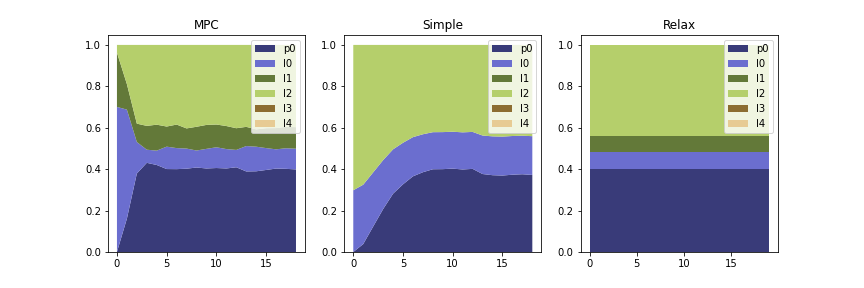

By looking at the average allocation across time for both policies shown in figure 9, we can further understand these differences. We can now see directly that the MPC policy is able to reach a stable allocation in fewer periods than the heuristic policy. If we include the proportional feedback control, the heuristic does reach the allocation faster, but still not as quickly as the MPC. Another difference is that the heuristic policy and MPC sweep out the same risk return trade-off profile, but may not choose the exact same portfolio steady state weights. Generally, the heuristic undershoots the illiquid target it is trying to reach.

8 Extensions

Liquidation.

We can easily extend the model to allow for liquidation of illiquid alternatives on the secondaries market. Per common practice (for example, see [GS21]), we assume that at time we can liquidate from which, after a haircut is available as liquid wealth . This changes the control by appending an to as defined in §5.1. Accordingly, the new control matrix is given by

with

where the block of zeros and the identity matrix are in dimension . There is also a new constraint enforcing , i.e.the maximum liquidation is the entire liquid exposure in a given asset.

Tracking fixed weights.

In this paper, a user specifies a risk tolerance parameter as in (13), which implicitly specifies the portfolio weights across the liquid and illiquid assets. However, an investor may have arrived with pre-selected target portfolio weights. Instead of seeking to track a target illiquid exposure, as in the problem posed in §4, we can instead seek to track target portfolio weights. A natural tracking constraint in planning is

where is the user-provided vector of target portfolio weights, and is a tracking variance hyperparameter. As with our risk constraint in (18), in practice a slack variable can be added to the above constraint to guarantee feasibility.

Liabilities.

We can incorporate external liabilities by modifying our liquid wealth update to

This encodes an external obligation of dollars in period . This could represent the liabilities of an insurer or a pension fund. MPC is able to handle these liabilities quite gracefully: at every time the planning problem takes in a forecast of the next liabilities , . The insolvency constraint (17) can be modified to include the liabilities as

Time varying forecasts.

In the current problem formulation, we plan based on the mean dynamics (11), which we treat as stationary at every time . The mean dynamics capture the expected returns, call intensities, and distribution intensities. It is immediate to replace these stationary forecasts with time varying ones: planning at time in (18) becomes

where and are the forecasted mean dynamics at time generated at time .

Illiquid dynamics with vintages.

A natural way to extend the Takahashi and Alexander illiquid asset model is to have time varying intensity parameters that depend on the age of the investment. This amounts to keeping track of vintages for each asset class, rather than aggregating all exposure to a given illiquid asset in one state, as this paper does. This extension is quite natural, and is readily implementable as an only slightly larger tractable convex optimization based planning problem. A given illiquid asset at time , rather than by two states and , will now require states,

where denotes the age of the investment and the maximum age tracked is . In words, at each time, we keep track of the exposure and uncalled commitments from commitments of age .

9 Conclusion

We have described a flexible stochastic linear system model of liquid and illiquid alternative assets, that takes into account the dynamics of the illiquid assets and the randomness of returns, calls, and distributions. This model allows us to develop an MPC policy that in each time period chooses a liquid wealth allocation, and also new commitments to make in each alternative asset.

We compare the results of this policy with a relaxed liquid model, where we assume that all illiquid assets are fully liquid. This relaxed liquid model is easy to understand, since the challenges of alternative assets have all been swept under the rug. For the relaxed liquid model, we can work out optimal investment policies. The performance with these policies can be thought of as an unattainable benchmark, that we know we cannot achieve or beat when all the challenges of alternative investments are present.

Suprisingly, the performance of the MPC policy under the real model, with all the challenges of alternative assets, is very close to the performance of the relaxed liquid model, under an optimal policy. Roughly speaking, there isn’t much room for improvement. This is a strong validation of the MPC policy.

Another interesting conclusion is that the relaxed liquid model is not as useless as one might imagine, since MPC can attain similar performance with all the challenges present. In a sense this validates reasoning based on the relaxed liquid model, where illiquid assets are treated as liquid assets. Roughly speaking, the asset manager can reason about the portfolio using the simple relaxed liquid model; feedback control with the MPC policy handles the challenges of illiquid alternative assets.

References

- [APW13] Andrew Ang, Dimitris Papanikolaou, and Mark Westerfield. Portfolio choice with illiquid assets. Working paper, National Bureau of Economic Research, 9 2013.

- [BBDK17] Stephen Boyd, Enzo Busseti, Steven Diamond, and Ronald Kahn. Multi-period trading via convex optimization. Foundations and Trends in Optimization, 3:1–76, 2017.

- [Bla21] BlackRock. Capital market assumptions, 7 2021.

- [BV04] Stephen Boyd and Lieven Vandenberghe. Convex Optimization. Cambridge University Press, 2004.

- [CA07] Eduardo Camacho and Carlos Alba. Model Predictive control. Springer, London, 2007.

- [DI93] George Dantzig and Gerd Infanger. Multi-stage stochastic linear programs for portfolio optimization. Annals of Operations Research, 45:59–76, 1993.

- [DWY19] Stephen Dimmock, Neng Wang, and Jinqiang Yang. The endowment model and modern portfolio theory. Working paper, National Bureau of Economic Research, 2 2019.

- [GN21] Arpit Gupta and Stijn Van Nieuwerburgh. Valuing private equity investments strip by strip. Working paper, National Bureau of Economic Research, 2021.

- [GPM89] Carlos García, David Prett, and Manfred Morari. Model predictive control: Theory and practice—a survey. Automatica, 25:335–338, 1989.

- [GS21] Nicola Giommetti and Morten Sorensen. Optimal allocation to private equity. Working paper, Tuck School of Business, 4 2021.

- [HKD+06] Florian Herzog, Simon Keel, Gabriel Dondi, Lorenz Schumann, and Hans Geering. Model predictive control for portfolio selection. In 2006 American Control Conference, 2006.

- [HPC15] Mark Hayes, James Primbs, and Ben Chiquoine. A penalty cost approach to strategic asset allocation with illiquid asset classes. The Journal of Portfolio Management, 41:33–41, 2015.

- [Kor19] Arthur Korteweg. Risk adjustment in private equity returns. Annual Review of Financial Economics, 11:131–152, 2019.

- [Lee] Joo Hyung Lee. Dynamic portfolio management with private equity funds.

- [Mar52] Harry Markowitz. Portfolio selection. The Journal of Finance, 7:77–91, 1952.

- [Mer69] Robert Merton. Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics, 51:247–257, 1969.

- [MPM03] John Mulvey, William Pauling, and Ronald Madey. Advantages of multiperiod portfolio models. The Journal of Porfolio Management, 29:34–45, 2003.

- [SWY14] Morten Sorensen, Neng Wang, and Jinqiang Yang. Valuing private equity. Review of Financial Studies, 27:1977–2021, 2014.

- [TA02] Dean Takahashi and Seth Alexander. Illiquid alternative asset fund modeling. The Journal of Portfolio Management, 28:90–100, 1 2002.

- [TT18] Roméo Tédongap and Ernest Trafolong. Illiquidity and investment decisions: A survey. Working paper, Essec Business School, 2018.